Embed Size (px)

Citation preview

Economic Development

Incentive Program Audit

March 15, 2021

Report 202002

City Auditor:

Jed Johnson, CIA, CGAP

Major Contributor:

Patricia Meaux

Contents

Executive Summary ............................................................................................................................. 1

Authorization .......................................................................................................................................... 2

Objective(s) ............................................................................................................................................. 2

Scope and Methodology ..................................................................................................................... 2

Background ............................................................................................................................................. 3

Opportunities for Improvement ..................................................................................................... 6

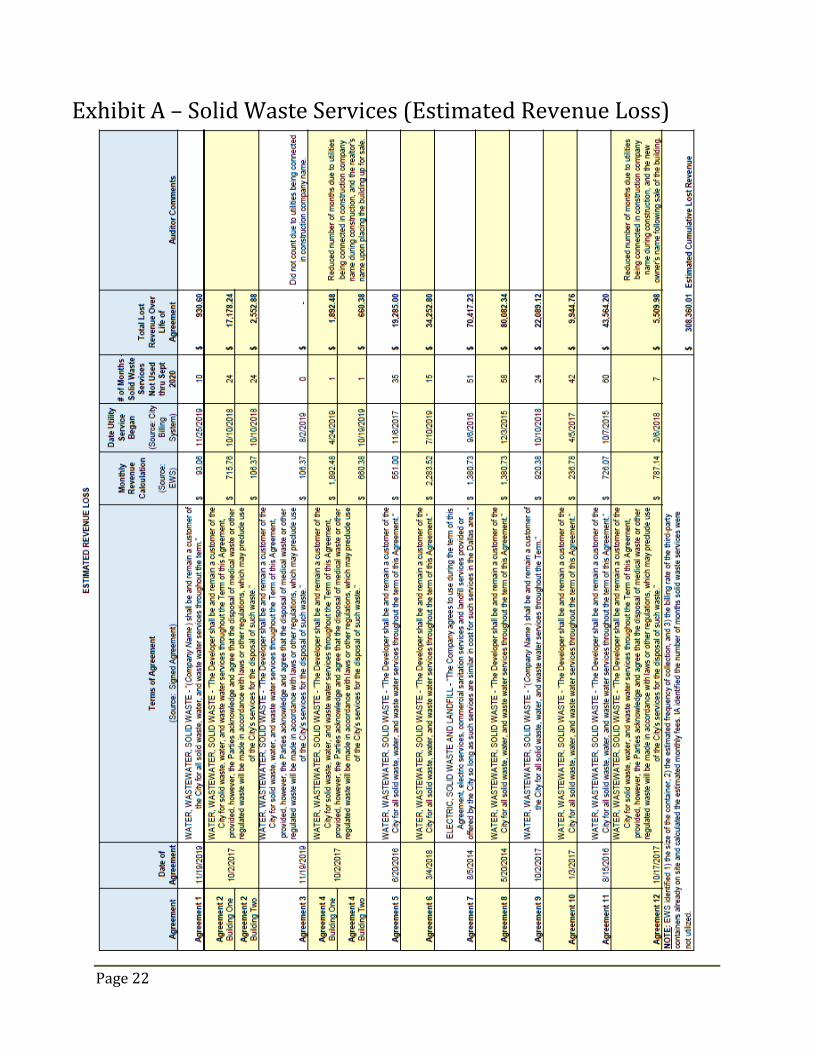

Exhibit A – Solid Waste Services (Estimated Revenue Loss) ............................................ 22

Exhibit B – Agreement C (Overpayment of Incentive) ........................................................ 23

Exhibit C – Agreement D (Incentive Paid Prior to Final Valuation) ............................... 24

Exhibit D – Sampling Methodology ............................................................................................. 25

Page 1

Executive Summary

The City of Garland provides economic development incentives to promote new development and redevelopment in Garland that aligns with the City’s Comprehensive Plan and Economic Development Strategy. Incentives are a tool used to attract new industries and to encourage retention and development through property tax exemptions or reductions, sales and use tax rebates, hotel occupancy tax rebates, and other Chapter 380 incentives.

Chapter 380 of the Local Government Code states: “The governing body of a municipality may establish and provide for the administration of one or more programs, including programs for making loans and grants of public money and providing personnel and services of the municipality, to promote state or local economic development and to stimulate business and commercial activity in the municipality.”

Incentives may be provided through, and managed by the Economic Development (ED) Department for commercial projects, as well as through the Planning and Engineering Departments for residential or mixed-use developments. On occasion, other departments have also initiated incentive agreements under Chapter 380 of the Local Government Code.

ED effectively brings target industries to Garland, as well as retaining businesses that have been present in Garland for many years. ED is experienced and creative when working with businesses that seek incentives, and performs impact analyses to identify prospective opportunities and estimate returns on investment. When incentives are provided, ED’s process is to perform an annual review to verify compliance of terms and conditions outlined in the agreement.

Internal Audit (IA) identified the following areas of improvement during this audit.

The City lost revenue when certain entities did not utilize City solid waste services as specified in their agreements.

Entity A had their property tax abatement calculations for 2018 and 2019 performed three times, using three different methodologies resulting in receiving a refund, followed by an upcoming tax bill.

Entity B did not receive an abatement as outlined in their agreement for tax year 2017 and overpaid property taxes by $53,913.

Entity C was overpaid a rebate incentive in the amount of $49,177 due to the rebate being processed prior to the finalization of a pending property tax lawsuit. This entity was also provided a City fee waiver not to exceed a specific amount. However, the expected fees to be charged by the City were not calculated, and the amount waived was not accurately tracked. Because of this, it could not be verified that the total fees waived was within the specified limit in the agreement.

Entity D was paid their final incentive payment prior to finalization of their tax protest. Although ultimately there was no financial impact, the compliance verification process was not completed.

Page 2

There is no City Directive or policies that define roles, responsibilities, processes, compliance review, and periodic reporting.

IA would like to express our appreciation to ED management and other departments for their time, assistance, and cooperation during the course of the audit.

Authorization

This audit was conducted under the authority of Article IV, Section 8 of the Garland City Charter and in accordance with the Annual Audit Plan approved by the Garland City Council.

Objective(s)

Objective A: Determine if the City has established a standardized process to receive, evaluate, and approve requests for economic development incentives. Objective B: Determine if the City monitors and verifies compliance of economic development agreements prior to processing incentives.

Scope and Methodology

IA conducted this performance audit in accordance with Generally Accepted Government Auditing Standards. Those standards require that IA plans and performs the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for the findings and conclusions based on the audit objectives. IA believes that the evidence obtained provides a reasonable basis for the findings and conclusions based on the audit objectives.

The scope of this audit for Objective A mainly covered active incentive agreements initiated by ED from January 1, 2018 through May 31, 2020. The scope of this audit for Objective B covered 24 active incentive agreements being monitored by ED and eight additional agreements initiated by other City departments. Please note this may not be all agreements.

To adequately address the audit objectives and to describe the scope of the work on internal controls, IA performed the following:

Reviewed the ED website to gain an understanding of the department’s role in bringing development or redevelopment to the City of Garland.

Researched best practices for economic development to gain an understanding of economic development.

Reviewed applicable statutes and regulations regarding economic development. Reviewed all incentive agreements for terms and conditions. Conducted internal inquiries with Economic Development, Planning, Engineering,

Building Inspection, Finance, Tax Office, and the City Attorney’s Office. Reviewed City Council Agendas and Meeting Minutes.

Page 3

Reviewed the City document repository system to ensure all agreements have been sent to the City Secretary.

Obtained and reviewed supporting documentation provided by the Entities to perform compliance testing.

Ran reports and reviewed information from the City’s finance system to ensure compliance with contract terms and conditions.

Conducted inquiries with third parties such as DCAD and State Comptroller’s Office to obtain additional information regarding abatements.

Ran reports and reviewed information from the City’s utility billing system to determine compliance with utility usage clause.

Evaluated ED’s internal controls currently in place.

In addition, IA reviewed the management control (principles 10 & 12), information and communication (principles 13 and 14) and monitoring activities (principle 16) that are three components of the standards for an effective internal control system, as defined by the standards set forth by the Federal Government1.

Background

The purpose of economic development is to facilitate investment in Garland by providing development assistance and professional expertise to qualified applicants. Providing development assistance and/or incentives improves the economic growth of the City, creates more jobs, and facilitates an improved quality of life. This may involve recruiting specific industries to the region, or diversifying to grow additional industries. Economic development also encourages reinvestment in existing operations by facilitating expansion and growth. Attracting additional investment to Garland increases property and sales tax revenue, which helps fund community projects, local infrastructure, and an enhanced quality of life. (Source: ED)

Chapter 380, Section 380.001 of the Local Government Code states: “The governing body of a municipality may establish and provide for the administration of one or more programs, including programs for making loans and grants of public money and providing personnel and services of the municipality, to promote state or local economic development and to stimulate business and commercial activity in the municipality.”

ECONOMIC DEVELOPMENT DEPARTMENT (Commercial / Industrial Development)

Prior to 1995, City Administration managed Economic Development opportunities and incentives. From 1995 to 2015, the City of Garland contracted with the Garland Chamber of Commerce to manage Economic Development. The Economic Development Department was created in 2015 to champion commercial development efforts and provide oversight of associated development incentive agreements. ED was also tasked with tracking and monitoring the agreements that had been initiated by others in years prior to ED’s creation.

1 Internal control is the system of processes that an entity’s oversight body, management, and other personnel implement to provide reasonable assurance that the organization will achieve its operational, reporting, and compliance objectives. The five components are control environment, risk assessment, control activities, information and communication, and monitoring. See U.S. Government Accountability Office, “Standards for Internal Control in the Federal Government,” Washington, D.C., 2014, p. 9, available at http://www.gao.gov/products/GAO-14-704G.

Page 4

The City of Garland’s ED Department works with other departments to offer a variety of incentives, including:

Property Tax Abatements and Rebates City Fee Waivers and Rebates Grants Hotel Occupancy Rebates Sales Tax Rebates Electric Rate Incentives

Requesting a Development Incentive

A request for an incentive may be initiated by phone, email, or submission of an Application for Economic Development Incentive. This application must be submitted by the property owner/developer or their representative, and include property information and description. The requestor must also provide information as to the size of the building, valuation, number of employees, total payroll, and annual product sales subject to sales tax. When applicable, additional information is requested as it relates to project concept, zoning, platting, site plan submittal, and development cost.

Evaluation and Approval of Incentive Requests

ED created a point system for businesses that are applying for incentives. The point system is based on the projected number of new jobs created, amounts of annual payroll, valuation of facilities and business personal property, sales tax that may be generated, and Garland Power and Light electric usage. Requests for incentives must meet a minimum threshold in order to qualify for incentives. ED reviews all requests on a case-by-case basis since each business and each request is unique in nature. The City Council must approve all incentive agreements during a public meeting.

Review for Compliance

For most incentive agreements (exclusive of abatement incentives), the compliance review process begins in January of each year immediately following the subject performance tax year, when ED sends an email to each entity that has an active agreement with the City. The email contains a lengthy compliance form that requests information on the current status and/or performance of the project, the real property and personal property investment and valuation, job creation / retention, and building information. There are additional requirements, such as execution of a Certificate of Compliance, providing a copy of personal property rendering submitted to the county appraisal district, and a narrative highlighting the progress of the project. This form must be submitted it in its original form, rather than photocopies, scans or faxes.

Once the entity has provided the required supporting compliance documentation, ED’s process is to review the information and verify it with other City departments such as Building Inspection, and with external industry sources such as the Dallas Central Appraisal District, Texas Workforce Commission, and CoStar (commercial real estate information

Page 5

provider). In the event the entity has met eligibility requirements, it must submit an Incentive Payment Request form that includes an affidavit of having met all obligations, conditions, and terms of the agreement. If the entity did not meet compliance, it is notified in writing.

As described above, some projects require information from, and coordination with, the Planning and Engineering Departments.

PLANNING AND ENGINEERING (Residential and Mixed-Use Development)

The incentive agreements initiated by the Planning and Engineering Departments are for residential or multi-family projects, based on individual requests by developers. These agreements may provide for a waiver or rebate of City fees collected in accordance with the Garland Development Code.

While Planning and Engineering may provide a developmental impact analysis on the significance of the project to the infrastructure, they do not perform a financial impact analysis. Planning and Engineering take these requests, with the Developer, to City Council for approval.

On occasion, the opportunity for a mixed-use development is presented. These are a combination of residential and commercial projects and may be initiated by other departments.

Page 6

Opportunities for Improvement

During this audit, IA identified certain areas for improvement. The audit was not designed or intended to be a detailed study of every relevant system, procedure, and transaction. Accordingly, the Opportunities for Improvement section presented in this report may not be all-inclusive of areas where improvement might be needed.

#1 – CITY SOLID WASTE SERVICES (Obj. B)

CONDITION

(THE WAY IT IS)

1. ED monitors commercial/industrial incentive agreements for compliance. From a population of 24 active incentive agreements, IA identified 17 agreements that include usage of City utility services in the terms and conditions, such as electricity, water, wastewater, solid waste, and landfill. To evaluate compliance, IA reviewed active utility accounts and compared the primary account holder name with the name of the entity that executed the agreement. The purpose was to determine if that entity is still responsible for utilities at the location. IA noted 12 of the 17 are not using the City’s Solid Waste services. At IA’s request, the Environmental Waste Services Department (EWS) identified 1) the size of the container, 2) the estimated frequency of collection, and 3) the billing rate, of the third party containers currently used at the location, and calculated the estimated monthly fees the City would have received. IA then determined the date utilities were connected and calculated the number of months in which solid waste services were not provided by the City. IA did not include months in which utilities were in the name of a contractor, owner, or tenant. The estimated revenue loss is $308,000 (See Exhibit “A”). 2. When calculating potential loss of revenue, IA noted that most of the agreements contain the following language: “[Developer/owner/company name] shall be and remain a customer of the City…." Of the 12 agreements, 3 of them had utilities connected in another entity's name, such as a realtor, construction company, or new owner. The agreement is silent on this condition when the Developer has a Contractor onsite, sells the property, or leases it to a tenant, but is still receiving the incentive. 3. Additionally, during the review of the utility accounts, IA noted four entities had received an incentive (one abatement,

Page 7

two hotel occupancy tax rebates, and one sales tax rebate) during time periods in which their utility account was past due. 4. EWS is unaware of the Owner/Developer's agreement to use Solid Waste services.

CRITERIA

(THE WAY IT SHOULD BE)

Generally, the agreements state, "The [developer/owner/ company name] shall be and remain a customer of the City for all solid waste, water and waste water throughout the term of this agreement."

City Council Policies, Article II, Division 6, Section 7 states "It is the policy of the City Council that the City not do business with a person (including a business entity of any sort) who is delinquent on an account to the City. Examples of delinquent accounts include taxes, impact fees, special assessments, utility bills, and EMS fees. The City Manager shall cause the affected departments within the City (including Purchasing, Engineering, Planning, and GP&L) to be provided with sufficient information to enforce the provisions of this policy."

Government Accountability Office Standards for Internal Control states:

Principle 12.02: "Management documents in policies the internal control responsibilities of the organization."

Principle 12.05: "Management periodically reviews policies, procedures, and related control activities for continued relevance and effectiveness in achieving the entity’s objectives or addressing related risks."

Principle 13.04: "Management obtains relevant data from reliable internal and external sources in a timely manner based on the identified information requirements. Relevant data have a logical connection with, or bearing upon, the identified information requirements."

Principle 14.03: "Management communicates quality information down and across reporting lines to enable personnel to perform key roles in achieving objectives, addressing risks, and supporting the internal control system. In these communications, management assigns the internal control responsibilities for key roles."

CAUSE

(DIFFERENCE BETWEEN

According to City Management and the City Attorney’s Office, the intent of the utility usage clause language was not to mandate usage, but to encourage it.

Page 8

CONDITION & CRITERIA)

ED's annual compliance review has focused on incentive criteria without considering each of the terms and conditions specified in the agreement.

There are no comprehensive written Department policies and procedures with roles and responsibilities for compliance review.

There is limited communication between ED and other departments.

EFFECT

(SO WHAT?)

The City will incur revenue loss.

RECOMMENDATION Economic Development should: Coordinate efforts with EWS to encourage identified entities

to utilize city solid waste services. Consider re-wording or re-evaluating the city utility usage

language in future agreements. Clarify condition and incentive language in agreements to

include situations in which utilities are connected during construction, sale, or lease of property, when applicable.

Include City Council policy language regarding delinquent account holders in all agreements.

Verify compliance of all terms and conditions before approving payment of incentive. In the event an entity is delinquent, work with the City Attorney’s Office on a solution, such as delaying payment of the incentive until account is current.

Consider obtaining read-only access to the City utility account system to verify compliance.

Develop and implement written policies and procedures that outline roles and responsibilities of the compliance process and management review.

Provide a copy of the agreement to the appropriate departments, or communicate relevant details (if the agreement has confidential information) at the time of execution.

MANAGEMENT RESPONSE

Concur

ACTION PLAN ED negotiates development agreements with entity representatives who are generally not the individuals that contract solid waste services. There may be several factors that could impede these entities from using solid waste services provided by the city, such as an existing contract with another service provider, or a national contract. ED management will coordinate efforts with EWS management to encourage use of city services.

Page 9

ED will review and evaluate the city utility usage clause language in future agreements.

ED has modified the project checklist for each active agreement to include all required performance obligations.

All or most of the hotel occupancy tax rebates and/or sales tax rebates are made automatically by the Finance Department. ED will coordinate efforts with Finance, Tax and other departments to ensure payments are not made when accounts are delinquent.

ED will verify compliance of all terms and conditions during the Annual Compliance and Payment process.

Future agreements will include City Council policy language and state incentive payment will not be made until all delinquent payments are made current.

ED will notify appropriate City Departments: Water, Wastewater, EWS, GP&L, etc. when an applicable Agreement is executed.

ED will obtain read-only access to the City’s utility account system to better verify compliance.

IMPLEMENTATION DATE

6/30/2021

Page 10

#2 – ABATEMENTS (Obj. B)

CONDITION

(THE WAY IT IS)

Of the 24 active ED agreements, there are currently two that provide property tax abatement incentives to Garland entities. A tax abatement is a local agreement between a taxpayer and a taxing unit that exempts all or part of the increase in the value of the real property and/or tangible personal property taxation. Abatements must be applied for annually by the entity that has an incentive agreement with the City.

The Dallas Central Appraisal District (DCAD) is responsible for appraising property for the purpose of ad valorem property tax assessment. According to the DCAD website, “business personal property consists of movable items used in the course of business not permanently affixed to, or part of, the real estate. Examples are: a) furniture; b) machinery and equipment; c) computers; and d) vehicles.” Real property is defined as land, and improvements, such as buildings or structures, per the Texas Property Tax Code.

Source: DCAD

For both agreements, IA reviewed the incentive, terms, criteria, and current status.

Page 11

Entity A Term: 2015-2020

Incentive: Business Personal Property (BPP) Tax Abatement Not-To-Exceed Amount: $222,000

Required Criteria: Add $7.8M in BPP Value by 12/31/2016 Agreement Status: Active - Incentive is still available.

To determine the accuracy of the abatement provided, IA reviewed the contract language and inquired with ED staff about the method for calculating abatements. IA noted the methodology for calculating abatements is not defined in the agreement. o DCAD originally calculated the abatement for tax years

2018 and 2019 as shown in Method 1 below. o ED contacted DCAD in April 2020 and requested the

calculation be changed to the method shown in Method 2, which resulted in refunds to the entity in May and June of 2020, for tax years 2018 and 2019. The refunds totaled $13,506.25.

o ED contacted DCAD again in October 2020, requesting the calculation be changed to the method shown in Method 3, which will result in the entity receiving a tax bill in the amount of $13,145.32 for 2018 and 2019.

Abatement calculation using three different methodologies:

Page 12

IA interviewed DCAD about the proper methodology and was informed DCAD follows the method outlined in the agreement. Absent that language, DCAD stated they generally apply percentages (abatements) first, then flat dollar amounts (Freeport) second. IA also inquired with the City Attorney's office and State Comptroller's office who said there is no law or rule that provides a standard methodology.

Entity B Term: 2014-2024 Incentive: Business Personal Property (BPP) Tax Abatement Not-To-Exceed Amount: $369,915 Required Criteria: Add $3M in Real Property Value; Add $7M in BPP Value; Employ 80 Employees by 12/31/2015 Agreement Status: Active - Incentive is still available. This entity has received one abatement of property taxes

since entering into the agreement in 2014. The entity did not meet property valuation requirements in 2015 and 2016, and did not qualify for the abatement. In 2017, the entity applied for the abatement exemption timely, but the City denied the incentive. However, when IA performed calculations in the same manner described above in Method 3, and reviewed Texas Workforce Commission data, the entity met the requirements. Not receiving this abatement resulted in overpayment of $53,913 in property taxes by the Entity. IA believes the 2017 incentive was denied due to how ED evaluates abatements. During the compliance review process in 2017, ED staff considered the Entity's 2016 property valuation, instead of the value as of January 1, 2017. IA’s inquiry with DCAD confirmed that the value as of January 1 is what ED should consider. Once DCAD completes and certifies valuation, DCAD makes the final decision as to whether the entity receives the abatement. DCAD denied the application for 2018 because the entity submitted the application with the 2017 tax year filled in. An abatement cannot be granted for a prior tax year. The entity did not file an abatement application in 2019. The entity filed an abatement application in 2020, and has received the abatement.

Page 13

This agreement was approved and executed in September 2014, but written to take effect January 1, 2014. In accordance with Tax Code 312.207(a-b), an agreement must be approved before its effective date.

CRITERIA

(THE WAY IT SHOULD BE)

According to the Government Accountability Office Standards for Internal Control:

Principle 12.05: "Management periodically reviews policies, procedures, and related control activities for continued relevance and effectiveness in achieving the entity’s objectives or addressing related risks."

Principle 13.05 – “Management processes the obtained data into quality information that supports the internal control system. This involves processing data into information and then evaluating the processed information so that it is quality information…. Quality information is appropriate, current, complete, accurate, accessible, and provided on a timely basis.”

Entities A and B: The Assistant Manager of Property Records and Exemptions for DCAD stated: “Per the Texas Property Tax Code, all abatements must be

applied for annually. The application must be received between January 1 and April 30 for the current tax year. The Tax Code does not allow an owner to apply for a prior year for an abatement.”

Entity B, 2nd Bullet Only: Tax Code - Sec. 312.207. APPROVAL BY GOVERNING BODY.

(a) To be effective, an agreement made under this subchapter must be approved by the affirmative vote of a majority of the members of the governing body of the municipality or other taxing unit at a regularly scheduled meeting of the governing body. (b) On approval by the governing body, an agreement may be executed in the same manner as other contracts made by the municipality or other taxing unit.

CAUSE

(DIFFERENCE BETWEEN

CONDITION & CRITERIA)

Agreements do not contain tax abatement calculation methodology language and is subject to interpretation.

The tax abatement exemption and DCAD tax calendar phases are not fully followed.

Page 14

ED’s current compliance verification process is set up for previous year performance, which does not apply to abatement since abatements are for the current tax year.

Previous City staff that created the agreement in 2014 may not have considered or fully understood the Texas Property Tax Code.

EFFECT

(SO WHAT?)

The calculation methods are not consistently applied. The entity may receive a refund without being entitled to it or may receive a tax bill in error.

Calculation errors can damage relationships with business entities and other government agencies.

Irregularities may not be identified timely.

RECOMMENDATION Economic Development should: Define incentive calculation methodology in the agreement. Develop policies and procedures to include calculation

methodology and tax abatement application. Have a secondary verification of compliance and accuracy of

calculation, to ensure entity receives incentive, when eligible.

Coordinate with the City Attorney's office and DCAD on how to resolve current conditions, and properly process the incentive for Entity B.

MANAGEMENT RESPONSE

Concur

ACTION PLAN Agreement A:

ED agrees that abatement methodologies should have been included and clearly articulated in any applicable agreement. ED has drafted a letter explaining the account changes, and will be sent with a tax bill from the Tax Department. ED also intends to notify the entity.

Agreement B: Once ED was notified by the audit department of the error, ED contacted the entity and requested further documentation. ED has also discussed this issue with DCAD and is ready to make the correction, and the entity will receive $53,913 within 30 days after the value is adjusted. Additionally, the Entity has applied for and received an abatement in 2020. Going Forward: Future Agreements will include a written explanation of the

incentive calculation methodology. ED will confirm that incentives have been applied accurately

twice: once during the yearly compliance process, and again

Page 15

once the abatement has been applied. This will be monitored via checklist.

ED staff will explain the abatement process to any new contact when the Entity submits a Notification Change Form.

IMPLEMENTATION DATE

6/30/2021

Page 16

#3 –COMPLIANCE MONITORING (Obj. B)

CONDITION

(THE WAY IT IS)

From a population of 24 active agreements being monitored by the ED Department, IA reviewed 12 agreements’ incentives, terms, criteria, and current status for compliance verification. (See Exhibit “D” for Sampling Methodology.) Entity C - Multiple Incentives

Term: 2015-2025

Incentive #1: Rebate of percentage of Real Property and BPP taxes paid. Incentive #2: Waiver of City Fees

Not-To-Exceed Amount: $550,000

Required Criteria: Achieve $13.6M in Real Property valuation and $1.6M in BPP valuation initially, with annual incremental increases. Agreement Status: Active - Incentives are still available. The entity filed a valuation protest for tax year 2017, which

was unsuccessful. Then the entity filed a lawsuit in September 2017. The entity did not notify ED of the protest or the lawsuit. In August 2018, while the lawsuit was still pending, the entity applied for the incentive rebate with the City, for the tax year 2017. ED processed the payment request application without verifying the status of the tax lawsuit. As a result, the entity was overpaid $49,177 in incentives. The lawsuit was not finalized until April 2019 (See Exhibit “B”).

As of October 2020, per the agreement, the City has waived all City fees. However, the expected fees to be charged by the City were not calculated, and the amount waived was not accurately tracked. Because of this, it could not be verified that the total fees waived was within the specified limit in the agreement. This project remains active, which could result in additional development fees being waived through 2027.

Entity D - City Fees Rebate

Term: 2017 until full and complete performance of all obligations and conditions have been met. Incentive: Rebate of City Fees

Not-To-Exceed Amount: $479,000

Required Criteria: Achieve $30M in Real Property and BPP valuations; design and construct building to achieve LEED certification. Agreement Status: Inactive - Incentive has been fully paid.

Page 17

The entity applied for LEED certification 3 years ago. However, according to the certifying organization's website (www.usgbc.org), Building #1 received 15 points, Building #2 received 16 points and Building 3 received 16 points, out of a possible 40 points, and the buildings have not yet been certified.

• The entity filed a 2019 tax valuation protest and notified ED on April 29, 2019. The protest was unsuccessful and the entity filed a lawsuit on September 28, 2019. The entity applied for the incentive rebate on December 10, 2019, while the lawsuit was still pending. ED performed compliance testing on January 30, 2020 without verifying whether the lawsuit was still pending, and processed the payment request application. The lawsuit concluded on March 5, 2020. (See Exhibit “C”).

Entity E - BPP Tax Rebate

Term: 2016-2026

Incentive: Rebate of percentage of BPP taxes paid

Not-To-Exceed Amount: N/A

Required Criteria: Achieve $3M in BPP valuation; employ 25 full-time employees, 8 of which must be paid $43,000 in annual wages. Agreement Status: Active - Incentive is still available. The entity provided documentation that revealed only one

employee met the annual wage requirement. The department deemed the entity to be in compliance and processed the incentive payments for 2017 and 2018, totaling $65,517.

Entity F - BPP Tax Rebate and Electric Incentive

Term: 2018 - 2025

Incentive #1: Rebate of percentage of BPP taxes paid Incentive #2: Credit of percentage of electric demand for first 3 years of contract Not-To-Exceed Amount: N/A

Required Criteria: Achieve $5.85M BPP valuation, employ 20 full-time employees, with a payroll greater than $800,000. Agreement Status: Active - Incentive is still available. Per DCAD records, the entity sold its business in 2018 and

tax rolls were changed effective May 21, 2018. The entity did not provide a Notification Change form to ED. IA noted the name had also been changed in the Texas Workforce

Page 18

Commission records and verified the name change in a Google search. A review of ED's compliance verification process revealed they had processed two incentive payments to the originally named entity without noticing the name change was reflected in compliance documentation provided by the entity, during their annual compliance verification process.

CRITERIA

(THE WAY IT SHOULD BE)

Section 6, Page 14 of Agreement for Entity C states:

“Developer agrees that by submitting to the City a request for

the payment of an Incremental Tax Rebate Payment under Sec.

3.6 of this Agreement, the Developer has (i) fully and finally

agreed to the DCAD assessed tax values…; Developer shall

promptly notify the City in writing if Developer receives any

form of refund, repayment, or rebate of taxes that have been the

basis of an Incremental Tax Rebate Payment under this

agreement and shall fully disclose to the City the basis of such

refund, repayment or rebate. The Parties shall then recalculate

the affected Incremental Tax Rebate Payment and Developer

shall promptly reimburse the City for any overpayment of the

Incremental Tax Rebate Payment resulting from the refund,

repayment or rebate.”

“Notwithstanding any other provision of this agreement to the

contrary, no Incremental Tax Rebate Payment shall become due

for any tax year in which or for which Developer is protesting

the appraised value or contesting an ad valorem tax due until the

protest is final. Developer shall promptly notify the City in

writing of any ad valorem tax protest relating the Property or

any of Developer’s tangible personal property located for tax

situs purposes on the Property.”

Section 6, Pages 6-7 of Agreement for Entity D states:

“(A) Developer agrees that by submitting to the City a request

for the final payment of the Incentive under this Agreement, the

Developer has (i) fully and finally agreed to the DCAD assessed

tax values and the City’s tax rate and procedures on which the

assessed value of the Property is or will be based without protest

or challenge” … (B) Notwithstanding any other provision of this

agreement to the contrary, the final incentive payment shall not

become due in any tax year in which or for which Developer is

protesting the appraised value or contesting an ad valorem tax

due until the protest is final. Developer shall promptly notify the

City in writing of any ad valorem tax protest relating to the

Property or any of Developer’s tangible personal property

located for tax situs purposes on the Property.”

Page 19

According to the Government Accountability Office Standards for Internal Control:

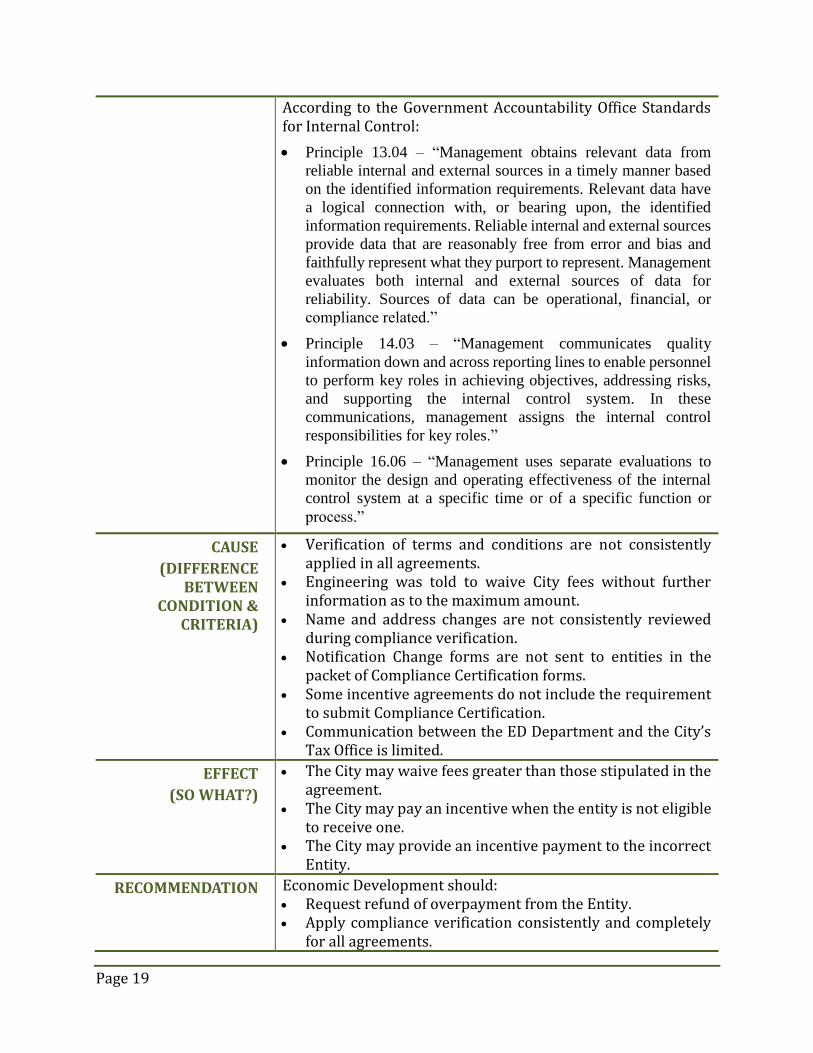

Principle 13.04 – “Management obtains relevant data from

reliable internal and external sources in a timely manner based

on the identified information requirements. Relevant data have

a logical connection with, or bearing upon, the identified

information requirements. Reliable internal and external sources

provide data that are reasonably free from error and bias and

faithfully represent what they purport to represent. Management

evaluates both internal and external sources of data for

reliability. Sources of data can be operational, financial, or

compliance related.”

Principle 14.03 – “Management communicates quality

information down and across reporting lines to enable personnel

to perform key roles in achieving objectives, addressing risks,

and supporting the internal control system. In these

communications, management assigns the internal control

responsibilities for key roles.”

Principle 16.06 – “Management uses separate evaluations to

monitor the design and operating effectiveness of the internal

control system at a specific time or of a specific function or

process.”

CAUSE

(DIFFERENCE BETWEEN

CONDITION & CRITERIA)

Verification of terms and conditions are not consistently applied in all agreements.

Engineering was told to waive City fees without further information as to the maximum amount.

Name and address changes are not consistently reviewed during compliance verification.

Notification Change forms are not sent to entities in the packet of Compliance Certification forms.

Some incentive agreements do not include the requirement to submit Compliance Certification.

Communication between the ED Department and the City’s Tax Office is limited.

EFFECT

(SO WHAT?)

The City may waive fees greater than those stipulated in the agreement.

The City may pay an incentive when the entity is not eligible to receive one.

The City may provide an incentive payment to the incorrect Entity.

RECOMMENDATION Economic Development should: Request refund of overpayment from the Entity. Apply compliance verification consistently and completely

for all agreements.

Page 20

Develop and implement written policies and procedures that outline roles and responsibilities of the compliance process and management review.

Include the Notification Change form in the Compliance Certification packet to Entities.

Work with the City Tax Assessor to obtain copies of Notice of Protest and other correspondence DCAD sends to the Tax Office.

Consider obtaining read-only access to the Customer Relations Management software to verify City fee payments.

Engineering, Planning, and Other Departments should: Prepare a calculation of expected fees for each Project that

includes a waiver of City fees in order to track the incentive granted.

MANAGEMENT RESPONSE

ED Response: Concur

Engineering Response: Concur

Planning Response: Concur

ACTION PLAN ED Response: • ED has communicated with Entity C regarding the

overpayment of the incentive rebate, and the entity has already sent a refund of $49,177 to the City.

ED has refined the compliance checklist to include verifying active tax law suits on the DCAD website and with the City Tax Department.

• ED will include a Notification Change Form with the Compliance Certification packet with instructions to fill out if either the legal name, ownership, address or primary contact for the Entity has changed.

• ED will routinely check all prior year’s certified values against prior year’s compliance as part of the current year compliance process to see if any adjustments have occurred for prior years’ value since the last compliance period.

ED will continue to track reduced fees and communicate with other departments about the limits of any waivers.

Engineering Response:

Engineering was not originally provided adequate information on this project and did not calculate potential fees at the time the project was initiated. However, Engineering did provide a calculation of fees upon the auditor’s request, and it is anticipated that there will be no further engineering fees associated with this project, and will not surpass the not-to-exceed amount. In the future,

Page 21

engineering will perform a detailed fee calculation when fee waivers are provided.

Planning Response:

The Planning Department will prepare a calculation of expected fees for each project that includes a waiver of city fees in order to track the incentive granted.

IMPLEMENTATION DATE

ED: 6/30/2021

Engineering: 12/4/2020

Planning: 12/4/2020

Page 22

Exhibit A – Solid Waste Services (Estimated Revenue Loss)

Page 23

Exhibit B – Agreement C (Overpayment of Incentive)

Page 24

Exhibit C – Agreement D (Incentive Paid Prior to Final Valuation)

Page 25

Exhibit D – Sampling Methodology

IA obtained a list of active incentive agreements from the ED Department. There are several types of incentives executed by this Department, including rebates, waivers, and abatements. The total population of active agreements for ED was 24, and IA judgmentally selected 12 to review and test for compliance. The total population of active agreements for other departments was eight, and IA judgmentally selected five to review and test. This design was chosen based on discussions with the departments as to the variety of incentives provided and uniqueness of each. The agreements may outline job/employment compliance, or construction date compliance, or tax valuation compliance, that may be conditions in order to receive an incentive. Incentives may be percentages or exact dollars, and may be rebates, waivers, or abatements. The results cannot be projected to the entire population due to the unique nature of each entity and agreement.