Embed Size (px)

Citation preview

Stability Investment Solutions Diligence

Institutional Sales Material. Not for Distribution to the Public. Federated Securities Corp., Distributor

Fund Not FDIC Insured May Lose Value No Bank Guarantee

Economic Assessment and Fixed-Income Outlook

Presented by:William E. Ehling, CFA

Vice PresidentFixed-Income Market Strategist

Client Portfolio ManagerFederated Investment Management Company

17-72025 (10/17)

Learning Objectives

By the end of the session you should be able to:

Have a greater understanding of the current fixed income environment.

Have a working knowledge of how the Fed, inflation, commodity prices and GDP influence fixed-income markets.

Have a global perspective on the opportunities and challenges in fixed-income going forward.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 2

3INSTITUTIONAL Sales Material. Not for Distribution to the Public.

Federated Taxable Fixed-Income Decision Tools

Bold text indicates change in positioning and/or rationale from previous month.

C u r r e n t P o s i t i o n i n g a s o f N o v e m b e r 9 , 2 0 1 7

C u r r e n t R a t i o n a l e

D U R A T I O NM A N A G E M E N T

Short relative to benchmark Geopolitical fears have abated, global purchasing managers’ indices and growth numbers have been good, rate normalization continues with Bank Of England tightening, and the promise of tax-reform twinkles on the horizon. Higher yields are likely through year end.

S E C T O RA L L O C A T I O N

Overweight Investment-Grade Corporates and High Yield, Emerging Markets/International

Neutral Treasuries and Commercial Mortgage-Backed Securities

Underweight Mortgage-Backed Securities and Agencies

The “’Carry Game” continues until risk assets correct or there are signs of recession. Seemingly low probability for both with the prospect of tax reform in Germany, France and the U.S.

Valuation issues in both sectors. Prefer allocations to credit.

There are valuation issues in the entire Mortgage-Backed Securities space. Rate increases should lead to an increase in volatility.

Y I E L D C U R V E A N A L Y S I S

Positioned for further flattening Historically the curve has flattened when the Fed tightens. We’ve re-entered our flattener. The Fed tightening in December and projected tightenings in 2018 should continue to flatten the curve absent an inflationary scare. Monitoring oil and wages diligently.

C U R R E N C YM A N A G E M E N T

Neutral the U.S. dollar but tactically short specific currency pairs

The U.S. Dollar bounced aggressively off technical support and the September lows rallying as much as 5-6% versus specific currency pairs. We’ve gone neutral but expect further depreciation of specific pairs like JPY and GBP.

S E C U R I T YS E L E C T I O N

Overweight select lower-quality credits, cyclical sectors and financials

The importance of broad diversification in credit portfolios can not be overstated, especially against a backdrop of Puerto Rico and Venezuela.

4INSTITUTIONAL Sales Material. Not for Distribution to the Public.

Federated Tax-Exempt Fixed-Income Decision Tools

*Neutral allocations are recommended for sectors and portions of sectors not listed above where valuation and risks seem balanced.Bold text indicates change in positioning and/or rationale from previous month.Positive, Neutral and Negative refer to recommended positioning relative to market/benchmark weightings.

C u r r e n t p o s i t i o n i n g a s o f N o v e m b e r 7 , 2 0 1 7

C u r r e n t R a t i o n a l e

D U R A T I O NM A N A G E M E N T

Short relative to benchmark U.S. growth outlook and Fed policy “normalization” should drive Treasury and muni yields moderately higher, restrained by low inflation. Tax proposals have prompted recent outperformance of munis on expected lower issuance, but stay tuned as no bill has been passed.

Y I E L D C U R V E Expect flatter municipal yield curve The prospect of lower muni issuance amid low inflation should lead to flattening for the long end of the municipal yield curve.

C R E D I T Q U A L I T Y

Negative on AAA-rated securities

Neutral on AA-rated securities

Positive on A-rated securities

Positive on BBB-rated securities and below-investment-grade securities

Lowest-yielding securities in an environment where carry (income) wins.

Mild income advantages over AAA and highly liquid.

Mid-grade bonds offer yield pick-up with modest incremental credit and valuation risk.

Strong carry advantages with limited supply; strong demand and favorable credit trends that should keep valuations around current fair-to-rich levels.

C R E D I T S E C T O RA L L O C A T I O N *

Neutral on state general obligation (GO) bonds

Negative on high- and mid-quality local GO bonds and neutral on low-quality local GO bonds

Positive on the following revenue sectors: industrial revenue; high- and mid-quality toll road; mid-and low-quality dedicated and incremental tax-backed; low-quality tobacco settlement revenue; lower-quality senior care; charter schools

Negative on the following revenue bond sectors: low-quality toll roads; low-quality hospital bonds; low-quality small colleges and universities

General state credit quality appears to have peaked and many are fair to rich; some face elevated pension and budgetary imbalances, depressing ratings, widening spreads and creating tactical opportunities.

Rising pension costs present downside risks for some high-quality local GOs; mid- and low-quality local GOs offer idiosyncratic opportunity at wider spreads.

Stable or improving credit fundamentals and fair or fair-to-rich valuations.

Low-quality toll road valuations are rich; lower-quality hospitals have somewhat high valuations amid credit challenges; falling enrollments present downside risks for many lower-quality small colleges.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 5

Fed’s Dual Mandate: At Full Employment, but Inflation May Be Stalling

3%

5%

7%

9%

11%

U.S. Unemployment Rate (Seasonally Adjusted)Dotted lines indicate start dates of Fed tightening cycles

Source: Bloomberg, U.S. Unemployment Rate, Total in Labor Force, Seasonally Adjusted, Period as of 9/30/17. Central Tendency excludes the three highest and three lowest economic projections of the Federal Reserve Board members and Federal Reserve Bank presidents for each variable in each year. U.S. Personal Consumption Expenditures Price Index Year over Year as of August 2017.Vertical lines mark the first tightening/first hikes in Fed tightening cycles.

-2%

-1%

0%

1%

2%

3%

4%

5%

Personal Consumption Expenditures Price Index YOY%Dotted lines indicate start dates of Fed tightening cycles

Personal Consumption Expenditures Price IndexCore PCE IndexFed Long-Run Inflation TargetSept ‘17 Longer run unemployment (Fed Proj., central tendency)

U.S. Unemployment Rate (U3)

Fed’s gradual normalization of policy will persist with unemployment below NAIRU, but the inflation shortfall, if not reversed, will slow the pace and lower the endpoint of tightening.

No matter who reaches the Fed Chair, a negative real fed funds rates is no longer necessary. Fed’s gradual balance sheet reduction—reducing the amount of reinvestment of maturing securities—began in October.

The Fed’s Terminal Funds Rate Has a Strong Pull on the US 10-Year Yield

6INSTITUTIONAL Sales Material. Not for Distribution to the Public.

Source: Bloomberg; U.S. Ten Year Yield and Federal Fund Target Rate as of 9/30/2017**Evercore ISI as of March 28, 2017

0

5

10

15

20

U.S. Ten Year Yield and Federal Funds Target Rate

Recession 10y Treasury Yield Fed Funds Target (upper bound)

4 yrs.

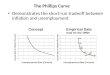

During the last 30 years, the 10-year Treasury yield tends to approach or equal the terminal rate as the Fed tightens. Fed policy makers expect that the terminal, or longer run, fed funds rate will likely be lower in this cycle relative to history. Fed will be very cautious not to over tighten given inflation disappointment, the flat Phillips Curve and historical tendency where

recessions tend to follow around 5 years after the start of Fed tightening cycles.**

First Hike This Cycle:December 2015

7 yrs.

4 yrs.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 7

Domestic vs. International Factors Driving U.S. Market Rates

International Factors• Modest global growth & low

inflation persist, with upside.• European election risk seems

to be receding but could return.

• BOJ & ECB negative rates and QE remain in effect.

• China appears to have stabilized but remains a risk.

• Oil prices seem to have stabilized around $50, but will OPEC cuts hold?

Domestic Growth & Policy• Moderate growth of 2% with

upside. • Trump plans may support

growth & inflation, but execution risk is high.

• Labor market and inflation improvements support Fed “normalization” at a faster rate.

%%

The U.S. election outcome increased U.S. growth & inflation expectations based on tax cuts and less regulation, driving yields higher, but can DC deliver?

Non-U.S. sovereign yields have fallen from 2017 highs as central banks remain in stimulus mode and political risks linger, though global growth momentum seems to be improving.

%

%

Upward pressure on rates

Downward pressure on rates

%%

U.S. Broad Trade Weighted Dollar is up over 30% from 2011 low, but has weakened from its post-election peak.

$$

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 8

U.S. Treasuries: Highest Yielding of the G3 and Denominated in a Strong Currency

70

80

90

100

110

120

130

Strong U.S. Dollar

U.S. Dollar Index (DXY) Trade Weighted Dollar (Broad)

Source: Bloomberg, U.S. Dollar Index and Trade Weighted Dollar (Broad) as of 9/30/2017, G3 10-Year Note Yields as of 9/30/2017U.S. Dollar Index (DXY) indicates the general international value of the U.S. dollar (USD) by averaging the exchange rates between USD and major world currencies. Trade Weighted Dollar (Broad) was created by the Federal Reserve. The Broad index is a weighted average of the foreign exchange values of the U.S. dollar against the currencies of a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares and from U.S. and foreign import shares.

Dollar strength has weakened net exports, muted U.S. inflation and supported foreign investor returns in U.S. Treasuries. Treasuries look “cheap” to Japanese and German sovereign debt, though hedging costs erode the yield pick-up. Together, these forces continue to attract global capital to U.S. Treasuries and depress market yields.

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

G3 10-Year Note Yields

U.S. 10Y Germany 10Y Japan 10Y

Commodity Price Declines Have Depressed Inflation Expectations

Source: Bloomberg, all data as of 9/30/17WTI= Western Texas Intermediate Futures

Inflation indicators and expectations are highly sensitive to energy prices. Supply growth contributed to the oil price collapse, but demand weakness was also likely to blame. Broad-based commodities price weakness suggests weakening global demand is a risk factor for financial markets.

$100

$300

$500

$700

$900

$20

$60

$100

$140

$180

S&P

GSCI

Spo

t Ind

ex

Oil Futures & Broad-Based Commodity Indices

Core Commodity CRB Commodity Index (right axis)WTI 1st Crude Oil Futures

S&P GSCI Spot Index (right axis)

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 9

0%

1%

2%

3%

U.S. Inflation Breakevens From Treasury Securities

Fed 5-year Forward Breakeven Inflation RateU.S. 5 Year TIPS BreakevenU.S. 2 Year TIPS Breakevens

Commodities Bear Markets Have Often Been Deep and Protracted Events

Since 1800, there have been five previous BOOM/BUST cycles whose BUSTS have averaged 19.5 years in length. If history is a reliable guide, the current correction could linger for many years.

Copyright 2015 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.Past performance is no guarantee of future results.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 10

Good News!!! The bulk of commodity price declines happen in years one to six.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 11

Commodity price weakness has fueled doubts about global growth, yet supply considerations are perhaps more important.

Copyright 2015 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.Past performance is no guarantee of future results.

12INSTITUTIONAL Sales Material. Not for distribution to the public.

Sector Allocation Is a Powerful Tool Within Bonds

Source: Morningstar, as of 9/30/17This is for illustrative purposes and not indicative of any investment or representative of performance for any specific investment. The data presented herein represents securities and industry market data as of the dates specified. We at Federated have reviewed this data and consider it reliable, but we do not represent that it is accurate or complete. Indices are unmanaged and individuals cannot invest in them. Past performance does not guarantee future results. Diversification does not assure a profit nor protect against loss.

KEYGlobal - JPM GBI Global Ex U.S. TR USD Corporate High Yield – Bloomberg Barclays U.S. HY 2% Issuer Cap TR USDU.S. Investment Grade – Bloomberg Barclays U.S. Agg Bond TR USD U.S. Government – Bloomberg Barclays U.S. Government TR USDU.S. Credit – Bloomberg Barclays U.S. Credit TR USD Emerging Markets - JPM EMBI Plus TR USD10 Year Treasury - Bellwether 10Y TR USD Municipals – Bloomberg Barclays Muni TR USD

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD 2017

4.93 26.78 39.30 13.02 18.28 25.97 15.66 10.40 22.09 28.83 12.04 11.86 10.76 11.30 12.39 58.76 14.94 10.70 18.04 7.44 9.05 3.30 17.13 8.64

-0.96 22.25 11.47 12.85 9.85 2.39 13.24 8.44 14.24 28.78 11.77 3.51 10.49 8.66 11.40 25.95 11.83 9.20 15.78 -2.01 7.53 1.82 9.62 8.22

-2.92 21.12 5.27 10.23 8.69 -0.82 11.68 7.23 11.50 18.63 11.14 2.76 6.84 6.97 5.24 16.04 8.47 9.02 9.37 -2.02 6.15 0.86 5.63 7.00

-3.38 19.06 4.43 9.65 8.57 -1.96 11.63 5.46 10.52 7.70 5.24 2.65 4.84 6.45 -2.47 12.91 6.78 8.35 6.78 -2.55 5.97 0.55 2.65 5.08

-3.93 18.47 3.63 9.59 6.48 -2.06 9.39 5.13 10.26 5.31 4.48 2.43 4.33 5.11 -3.08 5.93 6.54 7.84 4.21 -2.60 4.92 -0.77 1.86 4.66

-5.17 18.34 3.28 9.19 1.87 -2.23 -2.47 -0.79 9.60 4.10 4.34 1.96 4.26 3.36 -9.70 3.94 5.52 5.91 2.02 -5.08 2.46 -4.43 1.05 3.14

-18.93 17.45 2.77 -3.77 -14.35 -6.17 -5.79 -3.59 -0.24 2.36 3.48 -9.24 3.48 2.27 -25.88 -2.20 2.38 4.96 0.84 -8.31 -2.53 -4.84 0.25 2.25

Comparison to U.S. Treasury 10-Year Bellwether

-7.85 23.76 0.10 11.26 12.87 -8.43 14.45 4.04 14.56 1.27 4.90 2.07 1.34 9.72 20.07 -9.76 8.01 17.18 4.13 -7.81 10.74 0.91 -0.16 2.40

13INSTITUTIONAL Sales Material. Not for Distribution to the Public.

Credit Spreads Narrowed on Falling Volatility and Improving Fundamentals

Source: Bloomberg. The Merrill Lynch Option Volatility Estimate (MOVE) Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options which are weighted on the 2-, 5-,10- and 30-year contracts. Data as of 9/27/2017.*J.P. Morgan Domestic High Yield Index

0

25

50

75

100

125

0

100

200

300

400

500

600

700

800

900

Volat

ility L

evel

(BP)

Spre

ads (

BP)

JPM US High Yield* Index Spread to Worst Bloomberg Barclays U.S. Agg Corp. Avg. Spread to WorstMOVE Index-Implied volatility on Treasury Securities (right axis)

Fixed income volatility has declined to multi-year lows, reflecting the decline in inflation risk and the related caution among central banks.

Low interest rate volatility, expanding corporate profits and ongoing moderate growth expectations have supported tightening corporate spreads.

A Lackluster Economic Recovery

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 14

Deleveraging after the financial crisis, aging demographics, low investment, low productivity and fiscal policy actions & constraints have combined to limit the pace of the recent economic expansion.

Source: U.S. Department of Commerce, Bureau of Economic Analysis; www.bea.gov/national. Information through 2Q17

*In chained 2009 dollars; chained dollars is a method of adjusting real dollar amounts for inflation over time, so as to allow comparison of figures from different years. Chained-weighted indexes were introduced in 1996 to improve the accuracy of the U.S. estimates of the growth in real gross domestic product (GDP) and prices. These indexes use up-to date weights in order to provide a more accurate picture of the economy, to better capture changes in spending patterns and in prices, and to eliminate the bias present in fixed-weighted indexes.

1960 Recession

1981 Recession1990 Recession1980 Recession

1969 Recession1973 Recession

0%

10%

20%

30%

40%

50%

60%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32

U.S.

GDP

cum

ulat

ive g

rowt

h in

billi

ons*

Number of Quarters Since the Trough of the Last Recession

2007 Recession

2001 Recession

Global Concern: Growth of Debt Has Exceeded Growth of GDP

0%

50%

100%

150%

200%

250%

300%

350%

400%

1929 1946 1963 1980 1997 2014

Government GSE/Agency Financial ABS Household Corporate

U.S. Debt to GDP

Source: Deutsche Bank, AG, Frankfurt am Main, 2013, U.S. Debt to GDP as of 12/31/2014

Global debt includes government, financial, corporate, and household debt.

The high debt burden in the U.S. seems to be a restraint on accelerating growth.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 15

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 16

100%

200%

300%

400%

500%

600%

700%

1990 1994 1998 2002 2006 2010 2014

Japan UK France Spain Portugal Italy Greece U.S. Germany

Total Debt to GDP,A Global Perspective

The high debt burden across the developed world will continue to restrain global growth

Source: Deutsche Bank, AG, Frankfurt am Main, 2013, Total Debt to GDP as of 12/31/2014Global debt includes government, financial, corporate, and household debt.

Excessive indebtedness is a global phenomenon.

11.612.012.412.813.213.614.014.414.815.215.616.016.416.817.217.618.018.418.819.219.620.020.420.821.221.622.022.422.823.223.624.024.424.8

60.060.661.261.862.463.063.664.264.865.466.066.667.267.868.469.069.670.270.871.472.072.6

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Recessions

Age Group: 25-54

Age Group: 16-24

Age Group: 55+

Demographic Forces are Driving the Economy and Asset Allocation

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 17

A sell off in fixed-income will be viewed as a buying opportunity to a large portion of the American population.

More than 10,000 “Baby Boomers” turn 65 every day and will continue to do so for the next 19 years.*

Monthly Data 1/31/1948 – 9/30/2017Shaded areas represent National Bureau of Economic Research recessions.Based on source: Ned Davis Research Group, Macro Insights, September 27, 2013.. * Reuters, Sept.2013.**Source: U.S. Census Bureau, 2014 National Projections

Labor Force by Age Group (as a % of Labor Force)

Record

Age G

roup

25-5

4 (%

)

Age G

roup

s 16-

24 an

d 55

+ (%

)

Percent of Population >65 years

old:**

2014 15%2020 17%2030 21%2040 22%2050 22%2060 24%

Labor Force Growth and GDP – Trend Shows Continued Slow Growth

Source: Evercore ISI, China Research, July 12, 2017

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 18

The Power of the Millennials

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 19

Copyright 2017 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.Past performance is no guarantee of future results.

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 20

Yesterday, the Supercomputer Today’s Handheld

Technological Change: is more perfect information undercutting pricing power?

Source reference: http://www.phonearena.com/news/A-modern-smartphone-or-a-vintage-supercomputer-which-is-more-powerful_id57149#LlSzY53wTmeITdy4.99

"Today, your cell phone has more computer power than all of NASA back in 1969, when it placed two astronauts on the moon.“

-- Dr. Michio Kaku

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 21

Karl MarxKarl MarxAdam SmithAdam Smith

Post-WW II: An ideological war between Capitalism and Communism

“The ideas of economists and political philosophers, both when they are right and when

they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influence, are

usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air,

are distilling their frenzy from some academic scribbler of a few years back. I am sure that the power of vested interests is vastly exaggerated

compared with the gradual encroachment of ideas.”-- John Maynard Keynes

Capitalism has won!

“The ideas of economists and political philosophers, both when they are right and when

they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influence, are

usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air,

are distilling their frenzy from some academic scribbler of a few years back. I am sure that the power of vested interests is vastly exaggerated

compared with the gradual encroachment of ideas.”-- John Maynard Keynes

Capitalism has won!

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 22

The Long-Term Context for the 10-Year Treasury Yield

As of 9/30/17Source: Bloomberg, US Generic Govt 10 Year YieldThe US Generic Govt 10 Year Yield rates are comprised of Generic United States on-the-run government bill/note/bond indices.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

10 Y

ear T

reas

ury Y

ield

(%)

1964Gulf of Tonkin

Resolution

Intermediate/long-term Treasury yields are likely to climb amid some acceleration in U.S. growth & inflation. Factors that fueled bond rally since the 1980s—demographics, technology, globalization & policy—are not fully reversing. With U.S. potential GDP growth likely to remain near 2%, and if the Fed delivers on its 2% long-term inflation target,

the 10-yr. yield should remain low relative to history, but somewhat higher than today in years to come.

1971The microprocessor,

foundation oftoday’s computer

is introduced

1971Nixon suspends

$/Gold Convertibility

1973Arab OilEmbargo

1975Vietnam War

is Over

1979Deng Xiaoping

Acting Chairman ofChina’s Communist

Party

Paul VolckerNamed

Chairman ofFederal Reserve

1984Apple introduces

Macintosh PC with a graphical

user interface

1989Berlin Wall is torn down

1994NAFTA –

North AmericanFree Trade Agreement

goes into effect

1995World TradeOrganization

Founded2001

September 11TerroristsAttacks

2008Bankruptcyof LehmanBrothers

2013Bernankesuggests

tapering QE

2014Declining Oil Prices

2016U.S. Election

2016Brexit Vote

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 23

The Role of Bonds in Diversified Portfolio

S&P 500 inception is 1972, Ibbotson SBBI US Large Stock TR USD is used to represent S&P 500 returns. Past performance is no guarantee of future results.This chart is for illustrative purposes only and is not representative of performance for any specific investment. Diversification does not assure a profit nor protect against loss. Published by Ibbotson Associates, IA SBBI US IT Govt Index is an index of treasury and agency securities with 3-10 years in maturity.Source: Morningstar Direct, calendar year returns 1963 – 2016.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Annu

al Re

turn

Portfolio 1: S&P 500 Porfolio 2: 60% S&P 500, 40% IA SBBI US IT Govt

Standard Deviationof Annualized

Return

Annualized Return

S&P 500 14.71 10.13%

60% S&P 500, 40% IA SBBI US IT Govt 9.21 9.10%

Result: Significant risk reduction with modest return reduction

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 24

Bad Year in Bonds Versus a Bad Day in Stocks

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

1994 2013 1999 2015 1978 1979 2005 2016 1980 1987

Annu

al Re

turn

10 Worst Years of theBloomberg Barclays U.S. Aggregate Bond Index

Source: Morningstar Direct, Period analyzed: 01/01/1976-12/31/2016

Past performance is no guarantee of future results. This chart is for illustrative purposes only and is not representative of performance for any specific investment.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

1-Da

y Ret

urn

10 Worst Days of theS&P 500 Index

Many of the WORST years for diversified bonds are positive, reflecting the role of income and lower price risk of bonds.

Although these dates are outliers, they illustrate the nature of equity risk at the extremes.

Stocks

Bonds

Other

Asset Allocation is the Key…. Not Asset Abandonment

ASSET ALLOCATION ATPORTFOLIO LEVEL

DECISIONS WITHINFIXED-INCOME ALLOCATION

• Short, Intermediate, or Long Products• Active management of interest rate risk based on macroeconomic and policy environment

Interest Rate Risk/Duration

• Government, Mortgages, Corporates, High Yield, Emerging Markets, Municipal

• Assessment of relative value opportunities amid changing economic and market conditions

Sector

• Opportunities arise from diverging global growth and policy shifts

• Currency can be a powerful tool to drive global-based returns

Domestic vs. International

• Federated supports asset allocation decisions via risk-based, asset-class models

• Models reflect macro economic/investment committee’s active calls• Current macro allocation is overweight equity

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 25

INSTITUTIONAL Sales Material. Not for Distribution to the Public. 26

Selected Fund Profiles as of September 30, 2017

Total Return Bond Fund Bond Fund Strategic Income Fund Floating Rate Strategic Income Fund

Institutional High Yield Bond Fund

Portfolio Total Assets $7.5 billion $1.2 billion $740.7 million $966.2 million $6.8 billion

Description Pursues total return Pursues current income consistent with preservation of capital

Pursues a high level of current income

Pursues total return consistent with current income and low interest rate volatility

Pursues a high level of current income

Investment Strategy

Invests in a broad, strategic mix of bond sectors: primarily U.S. government and investment-grade corporate, high-yield allocation limited to 25%, typically under 15%.

Invests primarily in investment-grade corporate bonds; may also invest up to 35% in high-yield, lower-rated bonds

Invests in a strategic mix of bond sectors: U.S. high yield, U.S. high quality (government and corporate) and international (emerging and developed)

Invests primarily in a strategic mix of floating rate fixed-income investments, which pay interest at rates that increase or decrease with changes in the market rates

Invests in below-investment-grade securities, providing exposure to the higher-yielding, lower-rated, corporate bond market

Benchmark Bloomberg Barclays U.S. Aggregate Bond Index

75% Bloomberg Barclays U.S. Credit Bond Index/25% Bloomberg Barclays U.S. High Yield 2% Issuer Capped Index

35% Bloomberg Barclays Mortgage-Backed Securities Index/40% Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index/25% Bloomberg Barclays Emerging Markets USD Aggregate Index

55% Credit Suisse Leveraged Loan Index/15% One-Month Libor/30% BofA Merrill Lynch 1-Year U.S. Treasury Note Index

Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index

Morningstar® Category Intermediate-Term Bond Corporate Bond Multisector Bond Bank Loan High Yield Bond

Duration +/- 20% of index +/- 20% of index +/- 20% of index Negative two (-2) years to positive three (+3) years +/- 20% of index

Share ClassesA: TLRAX R: FTRKXB: TLRBX R6: FTRLXC: TLRCX SS: FTRFXIS: FTRBX

A: FDBAX F: ISHIXB: FDBBX IS: FDBIXC: FDBCX R6: FDBLX

A: STIAX F: STFSXB: SINBX IS: STISXC: SINCX R6: STILX

A: FRSAXC: FRICXIS: FFRSXR6: FFRLX

IS: FIHBXR6: FIHLX

Portfolio Manager(s)

Donald EllenbergerTodd Abraham, CFAMark Durbiano, CFAIhab SalibB. Anthony Delserone, Jr., CFAChristopher McGinley

Brian RuffnerMark Durbiano, CFAB. Anthony Delserone Jr., CFAChristopher McGinley

Mark Durbiano, CFADonald EllenbergerTodd Abraham, CFAIhab SalibChristopher McGinleyB. Anthony Delserone, Jr., CFA

Mark Durbiano, CFASteven WagnerB. Anthony Delserone Jr., CFATodd Abraham, CFAChristopher McGinley

Mark Durbiano, CFA

Portfolio composition is subject to change. Duration is a measure of a security’s price sensitivity to changes in interest rates. Securities with longer durations are more sensitive to changes in interest rates than securities of shorter durations.

Disclosures

INSTITUTIONAL Sales Material. Not for Distribution to the Public.

Bond prices are sensitive to changes in interest rates, and a rise in interest rates can cause a decline in their prices.

High-yield, lower-rated securities generally entail greater market, credit/default and liquidity risks and may be more volatile than investment grade securities.

There is no guarantee that the funds will achieve their investment objectives. Mutual funds are subject to risks and fluctuate in value.Investors should carefully consider the fund’s investment objectives, risks, charges and expenses before investing. To obtain a summary prospectus or prospectus containing this and other information, contact us or visit FederatedInvestors.com. Please carefully read the summary prospectus or prospectus before investing.

27

These materials are intended for use by sophisticated parties as described in Section (c)(1) of the Department of Labor’s Fiduciary Rule, 81Fed. Reg. 68, at 20999 (April 8, 2016). Federated is not undertaking to provide impartial investment advice, or to give advice in a fiduciarycapacity for purposes of the Employee Retirement Income Security Act of 1974, as amended or section 4975 of the Internal Revenue Code of1986, as amended or otherwise in connection with the sale or distribution of our products and services to in-scope clients such as ERISAplans and IRAs (“Transaction”). While Federated has a financial interest in a Transaction because Federated earns revenue from the sale ofour products and services, Federated does not receive a fee or other compensation directly from you or your in-scope clients for theprovision of investment advice (as opposed to other services) in connection with any Transaction.

28INSTITUTIONAL SALES MATERIAL. Not for Distribution to the Public.

Federated is a registered trademark of Federated Investors, Inc.