Embed Size (px)

Citation preview

Economic and real estate overview 19 June 2019

Economic and real estate overview

Mike Straneva

Partner

US National Director of Transaction Real Estate

Ernst & Young LLP

How can we have so much uncertainty and the Goldilocks economy?

Mueller

Where are we in the cycle? Late

Source: Green Street Advisors

M-RevPAF Growth Slowing

(Expansion) Material rent growth

Rising/stable occupancy

New construction

M-RevPAF Growth Negative

(Oversupply/

Obsolescence) Rents failing

Occupancy failing

M-RevPAF Growth

Accelerating

(Recovery) Low/modest rent growth

Rising occupancy

Little new construction

M-RevPAF Growth Flat

(Bottoming) Rents and occupancy stabilizing

Little to no new construction

Community centers

Power centers

Low productivity malls

Neighborhood centers

High productivity malls

Office

Lodging

Self storage

Apartments

Student

Senior Housing

Man. Home

Industrial

Most property types will see

fundamentals progress on this chart in a

clockwise manner. That said, burgeoning

influences – like ecommerce in the case

of lower-quality retail – could actually

cause progression in a counter-clockwise

motion (i.e., deterioration in growth

without ever experiencing an expansion

on oversupply).

Today’s economy: the glass is half full

► REIT NAV very different by

sector

► Interest rates and inflation are

reaching historic norms

► Unprecedented selective

demand from domestic and

foreign investors

► Wave of private capital

► US experiencing accelerating

growth, outpacing others

► Full employment/increasing

participation

► Real estate priced to

perfection but appreciation

rates for the future may be

lower

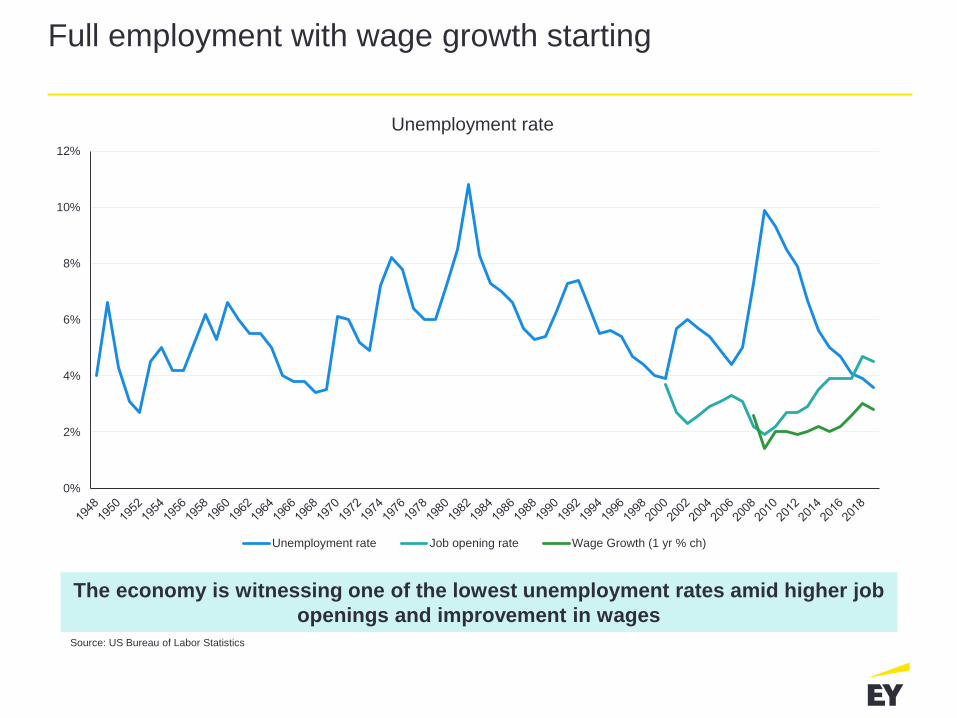

Full employment with wage growth starting

The economy is witnessing one of the lowest unemployment rates amid higher job

openings and improvement in wages Source: US Bureau of Labor Statistics

0%

2%

4%

6%

8%

10%

12%

Unemployment rate

Unemployment rate Job opening rate Wage Growth (1 yr % ch)

This is what full employment looks like – minorities and less educated starting to benefit

Source: US Bureau of Labor Statistics

0

2

4

6

8

10

12

14

16

18

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Ap

r-1

9

US Unemployment rate (%) by race

Total White Black Asian Latino

0

2

4

6

8

10

12

14

16

18

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Apr-

19

US Unemployment rate (%) by education level

Total No HS HS No College

Some Collegeor Assoc. Deg

College +

But the labor participation rate is historically low

Reasons for low participation

► Increase in global trade – especially China

► Automation

► Higher federal disability benefits

► Higher minimum wage

► More men in jail

Source: Bureau of labor Statistics, Market Watch

60

61

62

63

64

65

66

67

68

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Apr-19

Labor force participation rate (%)

The US yield curve inverted in Q1 2019: a harbinger of recession?

► Is an inverted yield curve a harbinger of recession?

► Third quarter growth is strong and is at Fed target.

► The speed and extent to which rates rise will have a serious effect on commercial

real estate over the coming years – both on cap rates and for property valuations.

Source: US Treasury

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Apr-

17

Jul-1

7

Oct-

17

Jan-1

8

Apr-

18

Jul-1

8

Oct-

18

Jan-1

9

Apr-

19

10 Yr 5 Yr 2 Yr

The dollar rebound has coincided with Fed Fund rate increases

Pros:

► A strong dollar makes foreign goods more

affordable for consumers.

► For large multinationals a strong dollar means

greater ability to buy foreign companies.

► A strong dollar cools inflation and economic

growth, which may be overheating.

► A stronger dollar signals that investors believe

economic growth will accelerate in the longer

term.

Cons:

► American exports are more expensive abroad.

► Less domestic demand for US-produced

goods because of cheaper foreign goods.

► Reduced demand for American-made

products will place downward pressure on US

employment.

Source: The Wall Street Journal, US Federal Reserve

0

0.5

1

1.5

2

2.5

3

88

90

92

94

96

98

100

102

104

106

US dollar index vs Fed Funds Rate

US Dollar Index Fed Funds Rate

Source: The Wall Street Journal, US Federal Reserve Bank of St. Louis

Oil prices have recovered to near $60 per barrel

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

Jan-1

3A

pr-

13

Jul-1

3O

ct-

13

Jan-1

4A

pr-

14

Jul-1

4O

ct-

14

Jan-1

5A

pr-

15

Jul-1

5O

ct-

15

Jan-1

6A

pr-

16

Jul-1

6O

ct-

16

Jan-1

7A

pr-

17

Jul-1

7O

ct-

17

Jan-1

8A

pr-

18

Jul-1

8O

ct-

18

Jan-1

9A

pr-

19

WTI spot price ($ per barrel)

0%

1%

1%

2%

2%

3%

3%

0

100

200

300

400

500

600

700

800

900

1000

Jan-1

3A

pr-

13

Jul-1

3O

ct-

13

Jan-1

4A

pr-

14

Jul-1

4O

ct-

14

Jan-1

5A

pr-

15

Jul-1

5O

ct-

15

Jan-1

6A

pr-

16

Jul-1

6O

ct-

16

Jan-1

7A

pr-

17

Jul-1

7O

ct-

17

Jan-1

8A

pr-

18

Jul-1

8O

ct-

18

Jan-1

9A

pr-

19

Texas employment vs. rig count

Texas rig count (L)

Texas non-farm employment YOY % Ch (R)

Source: Bureau of Labor Statistics, Baker Hughes

0.1%

0.5%

1.1%

1.1%

1.2%

1.4%

1.4%

1.5%

1.7%

2.1%

2.2%

2.6%

5.0%

6.3%

7.0%

Italy

Japan

Canada

Germany

Brazil

France

Mexico

United Kingdom

Russia

South Korea

Australia

United States

Indonesia

China

India

2019 GDP Growth Forecast (%)

Revenge of the developed economies?

Source: Oxford Economics

Emerging markets Developed markets

Source: Oxford Economics

Real estate funds are sitting on a record amount of dry powder

Largest holders of dry powder

Rank Firm name

Dry powder

($USm)

1 Blackstone Group $ 31,938.85

2 Lone Star Funds $ 16,844.80

3 Brookfield Asset Management $ 15,435.83

4 Starwood Capital Group $ 7,396.31

5 The Goldman Sachs Group $ 6,517.43

6 GLP $ 6,061.12

7 Carlyle Group $ 5,176.04

8 Rockpoint Group $ 4,424.92

9 Cerberus Capital Management $ 4,322.16

10 LaSalle Investment Management $ 3,645.12

Source: Preqin

$-

$50

$100

$150

$200

$250

$300

$350

Dry powder: closed-end private real estate funds by geographic focus ($USb)

North America Europe Asia ROW

2018 volumes decreased, spreads continue to tighten

► 2019 volume through mid

May is on pace with 2018

volumes.

► Tight spreads in

issuances are causing

CMBS to be competitive

with banks.

► Market has adjusted to

risk retention rules and

interest rate volatility.

Source: Commercial RE Finance Council, Morgan Stanley, EY

$45

$82 $90

$95

$37

$47

$77

$24

2012 2013 2014 2015 2016 2017 2018 2019 (asof 19May)

US CMBS Issuance $USb

Source: Commercial RE Finance Council

Source: Commercial RE Finance Council, JP Morgan, EY

0

100

200

300

400

500

600

700

800

900

4/13/2012 4/13/2013 4/13/2014 4/13/2015 4/13/2016 4/13/2017 4/13/2018 4/13/2019

CMBS spreads over treasuries

10-year Treasurys Aaa/AAA Aa2/AA A2/A Baa3/BBB-

… but new rules for HVCRE loans may have reduced overbuilding

► The 2015 HVCRE rule effectively raised the capital reserve

requirement for qualifying acquisition, development and construction

loans from 8% of the value of the loans to 12% or a 150% risk

weighting.

► At the end of 2017, construction loans accounted for just 1.94% of the

industry’s total assets, down from nearly 5% a decade ago.

► The Economic Growth, Regulatory Relief and Consumer Protection

Act of 2017 reduces the burden on smaller lenders from some of the

toughest requirements of the Dodd-Frank Act, such as the Volcker

Rule.

► It clarifies the widely criticized High Volatility Commercial Real Estate

(HVCRE) rule, which was first introduced as part of Basel III

regulations.

US economy: the glass is half empty

► Will Goldilocks economy end?

► Stocks are trading at 30.1x earnings,

which is above long-term historic

multiples 17.2x

► Is there a bubble in tech?

► Effect of tax policy still uncertain

► Emerging market growth moderate

► Real wage/income inequality

► Interest rate increases could

destabilize stock and real estate

pricing

► Geopolitical instability and war

► Student debt crisis

► 2020 Election

Frothy market multiples need increased earnings

Source: SNL Financial Source: ThomsonOne

30.1

17.2

0

5

10

15

20

25

30

35

40

45

50

1/1

/18

72

1/1

/18

78

1/1

/18

84

1/1

/18

90

1/1

/18

96

Jan

-02

Jan

-08

Jan

-14

Jan

-20

Jan

-26

Jan

-32

Jan

-38

Jan

-44

Jan

-50

Jan

-56

Jan

-62

Jan

-68

Jan

-74

Jan

-80

Jan

-86

Jan

-92

Jan

-98

Jan

-04

Jan

-10

Jan

-16

Jan

-19

Shiller PE Ratio

PE Ratio Long term average

-10

0

10

20

30

40

50

60

70

Broad market indices – price change (%)

DJIA S&P 500 NASDAQ

Advantages of globalization overshadowed by negative consequences …

10 years after crisis –

repercussions are still

present in many countries

Labor market threats –

outsourcing and modern

tech

Volatility of stock markets,

oil prices and currencies $ Migration issues in Europe

and the US

Fragile security – cyber

crime and terrorism

Increase of wealth inequality

despite global growth

China the Seller

Source: US Treasury, Real Capital Analytics

RE deal value

2017 – decline of 64% y-o-y

2018 – increase of 7% y-o-y

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$0

$5

$10

$15

$20

$25

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 1Q

China investment in the US real estate and treasuries

RE deal value - $Usb 12 mo avg treasuries holdings - $USt (RHS)

Trade war is escalating …

The US trade war with China continues.

Source: Oxford Economics

Jan-18 Apr-18 Jul-18 Oct-18 Jan-19 Apr-19

Trump imposes tariffs on washing

machines and solar panels

Trump orders tariffs on steel and

aluminum imports

Trump plans for 25% tariffs on $50b of Chinese imports

China plans retaliatory tariffs on $50b of US imports

US sets date for 25% tariffs on $34b of Chinese imports. China responds

Trump threatens tariffs on $267b more of Chinese imports

US implements 10% tariffs on $200bn of Chinese imports. China responds.

US and China agree on a 90 day halt to new

tariffs

Trump extends the 1 March deadline,

leaving tariffs on $200b of Chinese goods at

10%

Trump tweets that he intends to raise tariffs on $200b of Chinese

goods to 25%

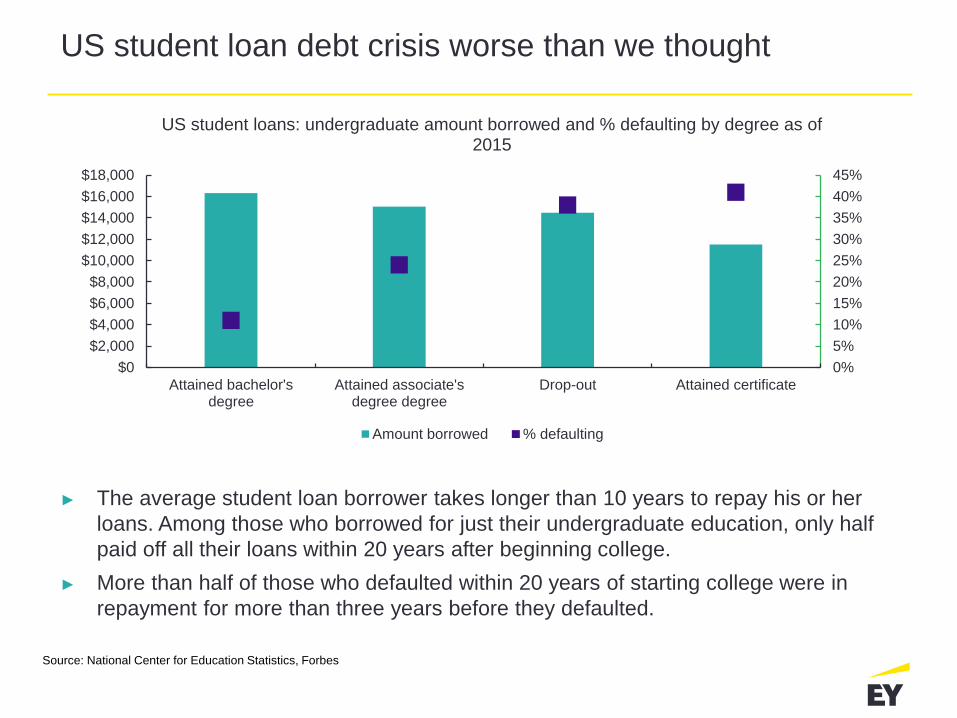

US student loan debt crisis worse than we thought

► The average student loan borrower takes longer than 10 years to repay his or her

loans. Among those who borrowed for just their undergraduate education, only half

paid off all their loans within 20 years after beginning college.

► More than half of those who defaulted within 20 years of starting college were in

repayment for more than three years before they defaulted. Source: National Center for Education Statistics, Forbes

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Attained bachelor'sdegree

Attained associate'sdegree degree

Drop-out Attained certificate

US student loans: undergraduate amount borrowed and % defaulting by degree as of 2015

Amount borrowed % defaulting

Source: National Center for Education Statistics, Forbes

Are higher interest rates and affordability affecting existing home sales?

Source: National Association of Realtors

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Ja

n-1

3

Apr-

13

Ju

l-1

3

Oct-

13

Ja

n-1

4

Apr-

14

Ju

l-1

4

Oct-

14

Ja

n-1

5

Apr-

15

Ju

l-1

5

Oct-

15

Ja

n-1

6

Apr-

16

Ju

l-1

6

Oct-

16

Ja

n-1

7

Apr-

17

Ju

l-1

7

Oct-

17

Ja

n-1

8

Apr-

18

Ju

l-1

8

Oct-

18

Ja

n-1

9

Apr-

19

Annualized existing single family home sales (seasonally adjusted in millions)

Lack of inventory in some markets has negatively affected home sales

► Due to

relatively

limited

housing

supply, home

prices are on

the rise.

► US inventory

has inched up

to 5.9 months

in April 2019

from low of 4.0

in January

2013.

Source: US Federal Reserve, Redfin

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Jan

-12

Ap

r-12

Jul-

12

Oct-

12

Jan

-13

Ap

r-13

Jul-

13

Oct-

13

Jan

-14

Ap

r-14

Jul-

14

Oct-

14

Jan

-15

Ap

r-15

Jul-

15

Oct-

15

Jan

-16

Ap

r-16

Jul-

16

Oct-

16

Jan

-17

Ap

r-17

Jul-

17

Oct-

17

Jan

-18

Ap

r-18

Jul-

18

Oct-

18

Jan

-19

Ap

r-19

US single family housing supply (in months)

US LA Phoenix SF

Price growth has slowed, but housing still isn’t cheap

Source: S&P Dow Jones Indices LLC.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Ja

n-0

8A

pr-

08

Ju

l-0

8O

ct-

08

Ja

n-0

9A

pr-

09

Ju

l-0

9O

ct-

09

Jan-1

0A

pr-

10

Ju

l-1

0O

ct-

10

Ja

n-1

1A

pr-

11

Ju

l-1

1O

ct-

11

Ja

n-1

2A

pr-

12

Ju

l-1

2O

ct-

12

Ja

n-1

3A

pr-

13

Ju

l-1

3O

ct-

13

Ja

n-1

4A

pr-

14

Jul-14

Oct-

14

Ja

n-1

5A

pr-

15

Ju

l-1

5O

ct-

15

Ja

n-1

6A

pr-

16

Ju

l-1

6O

ct-

16

Ja

n-1

7A

pr-

17

Ju

l-1

7O

ct-

17

Ja

n-1

8A

pr-

18

Ju

l-1

8O

ct-

18

Ja

n-1

9

Case Shiller Home Price Indices YOY % change

10 City Composite Intex 20 City Composite Index

Will baby boomers define real estate market dynamics?

32 million Total homes owned

by BBs

Key facts

Constitutes 40% of total homes

in the country

US$13.4

trillion in value (includes

14 million homes of

silent generation)

Scenario 1

Baby boomers stick to their old

homes

► Housing shortage, triggering price

increases

► Demand for home improvement

products and services

► Demand for new technology in terms

of media, flex rooms-libraries

Scenario 2

Baby boomers sell their homes

and move to smaller homes or

relocate to other cities

► High inventory creating oversupply

► Millennials’ low appetite for homes may

impact prices negatively in some

markets

► Trigger-health issues and death

► As per Fannie Mae, 10.5m owners will

sell during 2016 to 2026. 13.1m owners

will sell during 2026 to 2036

Source: CBS News.com, Washington Post .

Real estate priced to perfection … or beyond

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

40

50

60

70

80

90

100

110

120

130

140

Jan-0

7

Ma

y-0

7

Sep-0

7

Jan-0

8

Ma

y-0

8

Sep-0

8

Jan-0

9

Ma

y-0

9

Sep-0

9

Jan-1

0

Ma

y-1

0

Sep-1

0

Jan-1

1

Ma

y-1

1

Sep-1

1

Jan-1

2

Ma

y-1

2

Sep-1

2

Jan-1

3

Ma

y-1

3

Sep-1

3

Jan-1

4

Ma

y-1

4

Sep-1

4

Jan-1

5

Ma

y-1

5

Sep-1

5

Jan-1

6

Ma

y-1

6

Sep-1

6

Jan-1

7

Ma

y-1

7

Sep-1

7

Jan-1

8

Ma

y-1

8

Sep-1

8

Jan-1

9

Green Street Advisors Commercial Property Price Index vs Premium/Discount to NAV Jan 07- Apr 19

GSA CPPI (L)

GSA Premium/Discount to NAV (R)

Green Street Advisors Commercial Property Price Index is indexed to 100 in August 2007.

But there are stark contrasts in REIT share values across property types

Revenge of the Denominator: Since 2012, the link between sector risk and broader

market trends has broken down. Instead, REITs have become hypersensitive to interest

rates. Sectors that have long lease lives have been the riskiest, even as the most

economically sensitive sector – lodging – has been a safe haven.

Source: Green Street Advisors

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Premium/discount to NAV by property type

Apartment Industrial Mall Office Health Care

RE outperforming broad markets

Source: NAREIT

13.50%

10.35%

18.70%

15.48%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Performance: Real Estate vs. Broader Markets Annual % Change

S&P 500 Dow Jones FTSE/NAREIT All REIT NASDAQ

What’s next?

Average current and target allocations to real estate by investor type

Source: Preqin

9.8%

8.2% 7.8%

7.0%

5.9%

6.7%

10.4% 10.4%

12.4%

8.7%

7.8%

8.9%

Public PensionFund

Private SectorPension Fund

SovereignWealth Fund

EndowmentPlan

Foundation InsuranceCompany

Institutional investors’ mean current and target allocations to real estate by investor type

Current Allocation Target Allocation

“Haves” “Rising Markets” “Obsolete”

► Redevelopment

opportunities in the top

15 markets

► 90%+ leased with

limited roll over next

three years

► Assets with good

“current yield”

► Trophy assets

► “Core” investments

► A & B+ quality assets

► Strong development

sites

► Strong value-add play

opportunities

► Infill projects that need

development

► Strong economic drivers

or growth potential

► Diverse business base

► B+ & C quality assets

► Secondary markets

► Attractive risk-adjusted

returns

► Price and yield

advantages

► Development in all

product categories

► Significant rollover or

lease up over next two

years

► Mixed use development

► Tertiary markets

► Certain types of

buildings are becoming

functionally obsolete

► Poor quality assets with

no foreseeable

turnaround

► Shallow tenant pool

► B malls

► Large suburban office

campuses

► Under 25’ ceiling height

industrial

► Big box retail

► Apparel retail

Source: Eastdil Secured; REIS; CBRE;CCIM

Is there more risk in core assets than rising assets?

Property sector fundamentals: office

Top markets by rent increases: office

1Q 19 vacancy rate

1Q 19 vacancy rate

change y-o-y (bps)

1Q 19 rent

change y-o-y

Tampa-St. Petersburg 17.1% 20 3.8%

Raleigh-Durham 14.8% -20 3.7%

Austin 13.2% 40 3.6%

Orange County 16.3% 80 3.6%

Portland 13.2% 50 3.5%

Seattle 10.2% -40 3.2%

Nashville 13.6% 40 3.2%

San Jose 17.7% 20 2.9%

Denver 16.8% -70 2.9%

Colorado Springs 20.6% 50 2.9%

US 16.6% 10 2.2%

Source: Reis

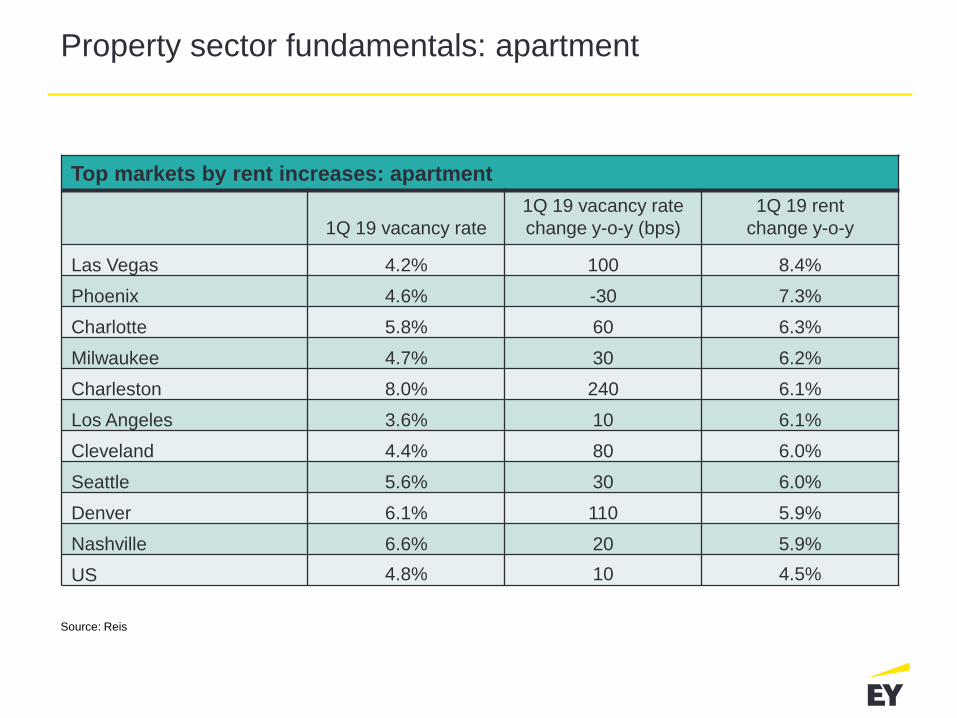

Property sector fundamentals: apartment

Top markets by rent increases: apartment

1Q 19 vacancy rate

1Q 19 vacancy rate

change y-o-y (bps)

1Q 19 rent

change y-o-y

Las Vegas 4.2% 100 8.4%

Phoenix 4.6% -30 7.3%

Charlotte 5.8% 60 6.3%

Milwaukee 4.7% 30 6.2%

Charleston 8.0% 240 6.1%

Los Angeles 3.6% 10 6.1%

Cleveland 4.4% 80 6.0%

Seattle 5.6% 30 6.0%

Denver 6.1% 110 5.9%

Nashville 6.6% 20 5.9%

US 4.8% 10 4.5%

Source: Reis

Property sector fundamentals: retail

Top markets by rent increases: retail

1Q 19 vacancy rate

1Q 19 vacancy rate

change y-o-y (bps)

1Q 19 rent

change y-o-y

Tacoma 14.0% -100 4.2%

Raleigh-Durham 7.4% -40 3.8%

San Francisco 3.5% 30 3.7%

San Jose 5.5% 30 3.6%

Austin 7.3% 130 3.4%

Orlando 9.6% -100 3.3%

Houston 11.8% 40 2.9%

Columbia 11.5% 120 2.5%

Greensboro/Winston-Salem 10.1% 10 2.4%

Miami 5.9% 10 2.4%

United States 10.2% 20 1.6%

Source: Reis

Although retail continues to grow steadily, not everyone is winning …

Retail is driven by e-commerce and generational change

Source: Euromonitor

Internet retail as % of total

3

1

8

5 4 4

3

0

7

14 13

9 8

7 6

3

11

22

18

15

12 11

8 7

World China UK US Germany Japan Australia India

2010 2015 2020

Retail is changing and getting more complicated

► Alibaba.com

► Asos

► Amazon

► Ocado

► Flipkart

Internet

pure players

► Aldi

► Dollar General

► Dollar Tree

► F21 Red

► Lidl

► Primark

► TJ Maxx

Discount and

off-price

retailers

► Gillette

► Nespresso

► Nike

► P&G

► Unilever

Manufacturers

reaching

directly

to consumers

Disruption is accelerating

Source: Press clippings

Amazon

First online sale

Amazon

One-Click

purchasing

Alibaba Amazon

Prime

1995 1997 1999 2000 2003 2005 2007 2009 2011 2013 2015 2017 2019

Amazon

Prime Air Amazon

Same Day

delivery

Trunk delivery

Prime Day

Dash Button

Brick & Mortar

book store

Asos

Ocado

Zalando AliPay

Amazon Fresh Lidl to open 150

stores the US

Singles Day

Bonobos

Dollar Shave Club

The Honest Co.

P&G e-store

Circuit City

KB Toys

Mammouth

Pay N Save

Entrance

Exit

Amazon

Kiva

Tower

Records

Stern’s

WebVan

Pets.com

Great Mills

Boo.com

Levitz

Friedman’s

Sunflower Market

Franks

Nursery

Walden Books

Virgin

megastores

HMV

Blockbuster

David Morgan

Hancock Fabrics

Sports Authority

BHS

Amazon Go

Crazy Eddie

Schlecker

Comet JJB

Sports

FAO Schwarz

Bottom Dollar Foods

Deb Shop

A&P

Fresh & Easy

Radioshack

Macintosh Retail Group

Sears

Nine West

Mattress Firm

David’s Bridal

Brookstone

Rockport

Claires

Payless

Toys R Us

Diesel

Gymboree

► Use of digital to increase basket size

► Growing proportion of mobile-based digital orders

► Growth of “online” as primary shopping channel

1:1 customer

relationships

Store as theatre

Home not shelf

Solution and product

Blurring physical

and digital

Going forward retail revolution offers business opportunities for the ones able to adapt keep

Themes Trends Leaders

► Innovation among retailers to win customers

► Increasing own brand penetration

► Greater interaction between retailers and

CP companies

► Shift in fulfillment

► Growth of independent shipping services to

homes

► Shifting towards experiential

selling/complimentary services

► Pop-up stores positioning their activity around

holiday/events

► Trend toward a “segment of one”

► Growth of 3D printing

► Differentiation in offerings to high-value/

loyal customers

► Carrefour

► Walmart

► Amazon

► Trader’s Joe

► Nespresso

► Instacart

► Ikea

► Burberry

► Lidl ski pop-up

► Stitch Fix

► Shoes of Prey

► Nordstrom

Property sector fundamentals: industrial

Top markets by rent increases: industrial

1Q 19 vacancy rate

1Q 19 vacancy rate

change y-o-y (bps)

1Q 19 rent

change y-o-y

Sacramento 6.4% -70 4.2%

Portland 4.8% -140 3.7%

Orlando 7.6% 90 3.7%

Fort Worth 7.4% -160 3.6%

Dallas 10.0% -20 3.6%

Phoenix 6.8% -160 3.6%

Denver 5.1% -60 3.5%

Chicago 7.5% -50 3.5%

San

Bernardino/Riverside 4.8% -110 3.5%

Orange County 1.9% 30 3.3%

US 6.8% -30 2.9%

Source: Reis

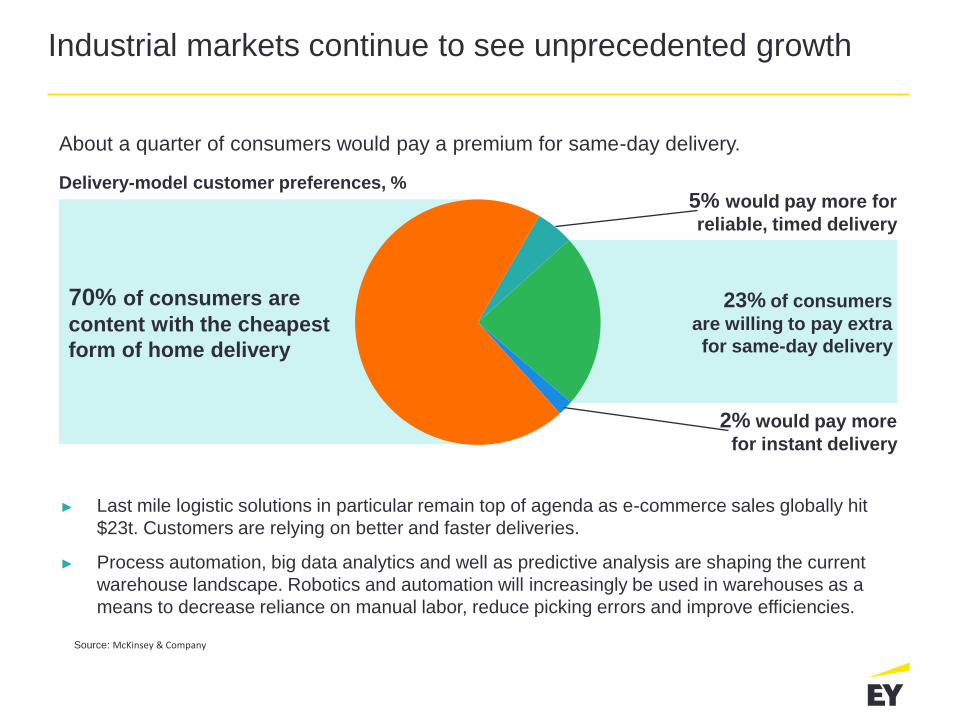

Industrial markets continue to see unprecedented growth

► Last mile logistic solutions in particular remain top of agenda as e-commerce sales globally hit

$23t. Customers are relying on better and faster deliveries.

► Process automation, big data analytics and well as predictive analysis are shaping the current

warehouse landscape. Robotics and automation will increasingly be used in warehouses as a

means to decrease reliance on manual labor, reduce picking errors and improve efficiencies.

About a quarter of consumers would pay a premium for same-day delivery.

Delivery-model customer preferences, %

23% of consumers

are willing to pay extra

for same-day delivery

70% of consumers are

content with the cheapest

form of home delivery

5% would pay more for

reliable, timed delivery

2% would pay more

for instant delivery

Source: McKinsey & Company

Hotels at a glance

Source: Green Street Advisors, Company Reports

1Q, 22%

2Q, 27% 3Q, 26%

4Q, 24%

Revenue seasonality

1.8%

1.1%

1.8%

4.3%

-1.0%

4.3%

1.3%

1.9%

H MAR HLT SHO HST PEB RLJ

1Q 19 YOY RevPAR Growth

C-Corps REITs Average

New lease accounting rules may impact corporate real estate strategy

► In February 2016, The Financial Accounting Standards Board issued final

guidance that will require lessees to put most leases on their balance sheets

but recognize expenses on their income statements in a manner similar to

today’s accounting.

► The new standard should be a catalyst for organizations to revisit their

corporate real estate strategy.

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 (31May)

Single tenant, owner occupied trransactions ($M)

Will WeWork’s IPO change real estate?

► Only four IPOs in 2018 – three are non-traditional.

► Only the traditional REIT is trading below issue price.

Source: SNL Financial

75

100

125

150

175

200

225

1 71

31

92

53

13

74

34

95

56

16

77

37

98

59

19

71

03

109

115

121

127

133

139

145

151

157

163

169

175

181

187

193

199

205

211

217

223

229

235

241

247

253

259

265

271

277

283

289

295

301

307

313

319

325

331

337

343

349

Number of trading days since IPO

2018-19 US REIT IPO Performance

Inustrial Logistics Properties (trad.) Americold (non-trad.)

Vici Properties (non-trad.) Essential Properties Realty Trust (non-trad.)

Nontraditional REITs have grown rapidly

► New frontier of nontraditional REITs is in small cell and fiber optic REITs.

► Recent conversions and spin-offs include Windstream (telco), MGM Resorts (gaming/lodging),

Gaming and Leisure Properties (gaming and lodging), Iron Mountain (document storage) and

CBS Outdoor (billboards), Four Corners Property Trust (restaurants)

► Hudson’s Bay entered into a JV partnership with Simon Properties that involved a sale-

leaseback.

► As part of the deal, the Bob Evans restaurant chain entered a similar sale-leaseback deal with

non-traded REIT Broadstone Net Lease. Source: SNL Financial

$-

$100

$200

$300

$400

$500

$600

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Market Cap (US$b) Golf Course

Land

Energy Infrastructure

Prison

Student Housing

Specialty

Advertising

Casino

Single Family

Manufactured Home

Timber

Self-Storage

Data Center

Health Care

Communications

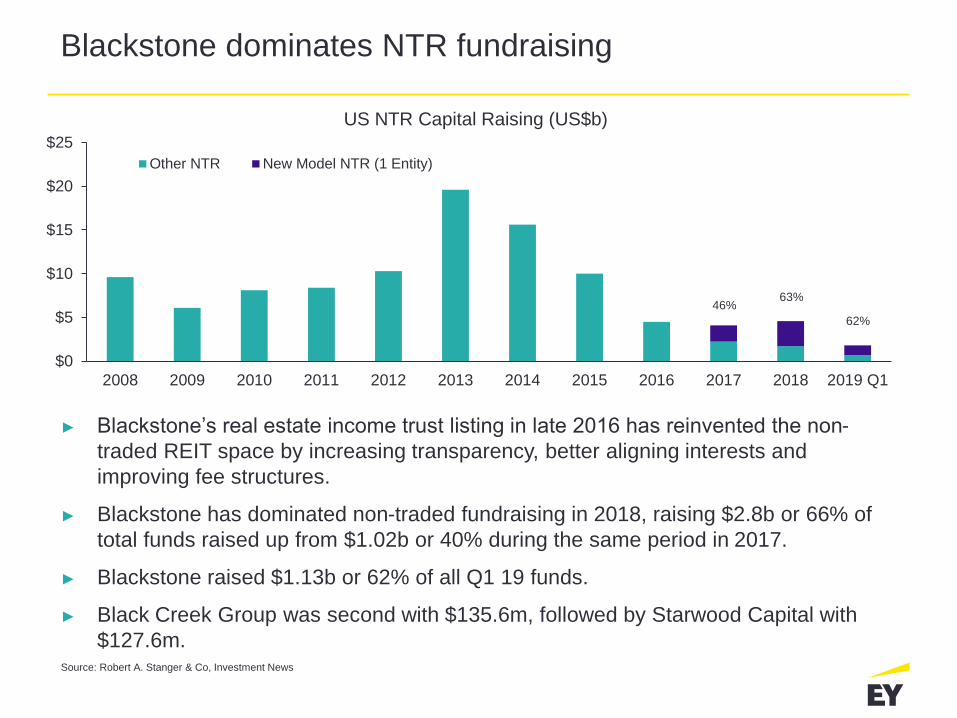

Blackstone dominates NTR fundraising

► Blackstone’s real estate income trust listing in late 2016 has reinvented the non-

traded REIT space by increasing transparency, better aligning interests and

improving fee structures.

► Blackstone has dominated non-traded fundraising in 2018, raising $2.8b or 66% of

total funds raised up from $1.02b or 40% during the same period in 2017.

► Blackstone raised $1.13b or 62% of all Q1 19 funds.

► Black Creek Group was second with $135.6m, followed by Starwood Capital with

$127.6m.

Source: Robert A. Stanger & Co, Investment News

46% 63%

62%

$0

$5

$10

$15

$20

$25

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Q1

US NTR Capital Raising (US$b)

Other NTR New Model NTR (1 Entity)

The road ahead – real estate is priced to perfection

► Will this Goldilocks economy end?

► Be prepared for inflation, and how do we measure inflation?

► Has the inverted yield curve foretold an upcoming recession? How

much will gas prices negatively impact the economy?

► Multifamily will continue to grow.

► Single family housing has limited new supply leading to lower sales

leading to a good environment for homebuilders.

► RE looks like a safe position compared to S&P and NASDAQ.

► Technology companies look overpriced.

Questions

Disclaimer

• EY refers to the global organization, and may refer to one or more, of the member firms of

Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-

serving member firm of Ernst & Young Global Limited operating in the U.S.

• This presentation is © 2019 Ernst & Young LLP. All rights reserved. No part of this document may be

reproduced, transmitted or otherwise distributed in any form or by any means, electronic or

mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any

information storage and retrieval system, without written permission from Ernst & Young LLP. Any

reproduction, transmission or distribution of this form or any of the material herein is prohibited and is

in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in

connection with use of this presentation or its contents by any third party.

• Views expressed in this presentation are those of the speakers and do not necessarily represent the

views of Ernst & Young LLP.

• This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does

not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s

facts and circumstances.

• These slides are for educational purposes only and are not intended, and should not be relied upon,

as accounting advice.

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities.

EY refers to the global organization, and may refer to one

or more, of the member firms of Ernst & Young Global Limited,

each of which is a separate legal entity. Ernst & Young

Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our

organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2019 Ernst & Young LLP.

All Rights Reserved.

Score: 04426-181US

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

ey.com