Embed Size (px)

Citation preview

Vital SignsVital Signs

20212021Economic & Social Economic & Social

Indicators for Indicators for New HampshireNew Hampshire

2015-20192015-2019

State of New Hampshire Christopher T. Sununu, Governor

New Hampshire Employment Security

George N. Copadis, Commissioner

Economic and Labor Market Information Bureau

Brian J. Gottlob, Director

JUNE JUNE 20212021

State of New Hampshire Christopher T. Sununu, Governor

New Hampshire Employment Security

George N. Copadis, Commissioner

Economic and Labor Market Information Bureau

Brian J. Gottlob, Director

JUNE JUNE 20212021

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau | i

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 2020

TABLE OF CONTENTS

Introduction iii

Key Economic Indicators v

1. Population 1

2. Income & Wages 8

3. Labor Force & Unemployment 13

4. Employment by Industry 19

5. Occupational Trends 24

6. Private Enterprise 32

7. Transportation & Traffic 37

8. Energy 42

9. Production 47

10. Trade and Tourism 53

11. Construction & Housing 59

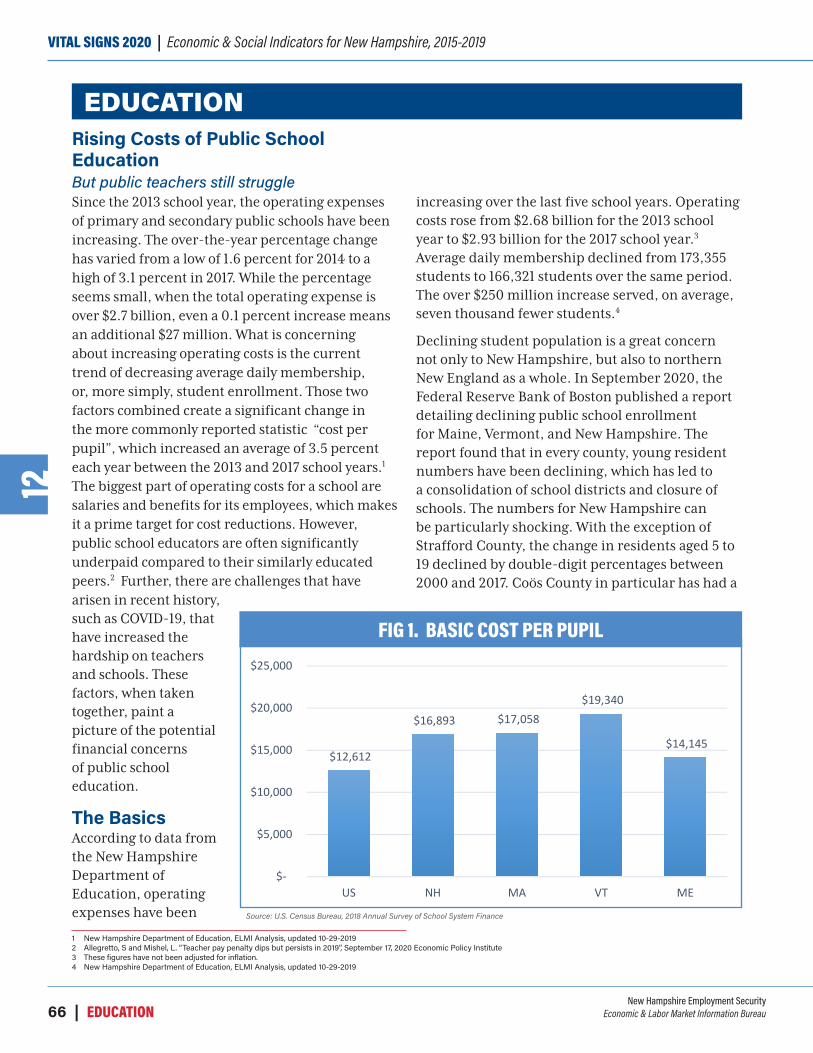

12. Education 66

13. Health 77

14. Crime & Crashes 84

15. Environment 89

Glossary and Index 95

TABLE OF CONTENTS

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau | iii

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 2020

This annual review of the economic and social conditions of New Hampshire highlights fifteen different indicators that describe the state’s economic, social, environmental, and cultural character. Each chapter of Vital Signs compiles five years of available data, analyzing emerging trends at the local, regional, and national levels where appropriate. Whenever possible, 2019 updates have been included in the summary analysis.

Attention should be paid to notations within the tables that describe data details such as sample size, time intervals, or rank order. Additionally, readers should note that throughout the text, proper titles of specific data elements (i.e. industry sectors such as retail trade and publication titles) are italicized to distinguish them from recurring ordinary usage. Readers are also encouraged to review the glossary and index on page 95 to become familiar with the different terminology used throughout the report.

The information presented in Vital Signs has been drawn from print and internet-based media reports, trade publications, academic journals, and the records of a wide variety of state and federal agencies and private organizations. Sources used in the text are identified with footnotes, and sources used in the tables are noted below each table. While all sources are believed to be reliable, no guarantee is made as to the correctness, sufficiency, or completeness of their information.

Some of the data tables are available by substate areas of New Hampshire. If you seek additional information, please contact the Economic and Labor Market Information Bureau at [email protected] or (603) 228-4124.

We are indebted to the numerous individuals who contributed special information or provided advice on evaluating reported data. The observations expressed in this report do not necessarily reflect those of New Hampshire Employment Security, and no official endorsement should be inferred.

INTRODUCTION

INTRODUCTION

Note on Coronavirus:The articles in this publication are primarily focused on the years 2015-2019. Although the coronavirus pandemic falls outside of this time frame, it has been difficult to ignore when discussing social and economic trends in New Hampshire. As a result, many chapters in this publication also address impacts of the coronavirus, and overall trends in 2020. Much of the data from 2020 is preliminary, and subject to revision once more complete data is available. Wherever possible, data in this publication has been updated to reflect the latest available numbers, including the 2020 benchmarking of Current Employment Statistics data. However, significant revisions to 2020 data are possible in the future.

The 2022 edition of Vital Signs will provide more data about economic trends throughout 2020 and the economic effects of the coronavirus pandemic.

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau | v

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 2020

CHANGE IN KEY ECONOMIC INDICATORS

2017-2018 2018-2019

CH

AP

TER

NET

CH

AN

GE

PER

CEN

T C

HA

NG

E

NET

CH

AN

GE

PER

CEN

T C

HA

NG

E

Population 4,700 0 3% 6,200 0 5% 1Income, per capita personal (not adjusted for inflation) $2,990 5 1% $2,451 4 0% 2

Wages, average weekly (private) $32 3 0% $39 3 5% 2Labor force 9,550 1 3% 8,880 1 2% 3Employment 10,510 1 4% 8,970 1 2% 3Unemployment -960 -4 5% -100 -0 5% 3Nonfarm jobs - total all industries 5,000 0 7% 6,500 1 0% 4Non-current loans and leases ($ millions) $4 9 65 4% -$4 0 -32 0% 6

Retail sales of electricity (million KWH) 259 2 4% -355 -3 2% 8

Gross domestic product by state (current dollars-millions) $3,564 4 4% $4,131 4 9% 9

Gross domestic product by state (chained 2012 dollars-millions) $1,714 2 3% $2,040 2 7% 9

Export sales to the world ($ millions) $158 3 1% $523 9 8% 9

Accomodations Rentals (Includes Motor Vehicle Rentals) ($ millions) $59 9 3% $17 2 4% 10

School enrollment, public and private (includes preschool)

-1,220 -0 6% -1,527 -0 8% 12

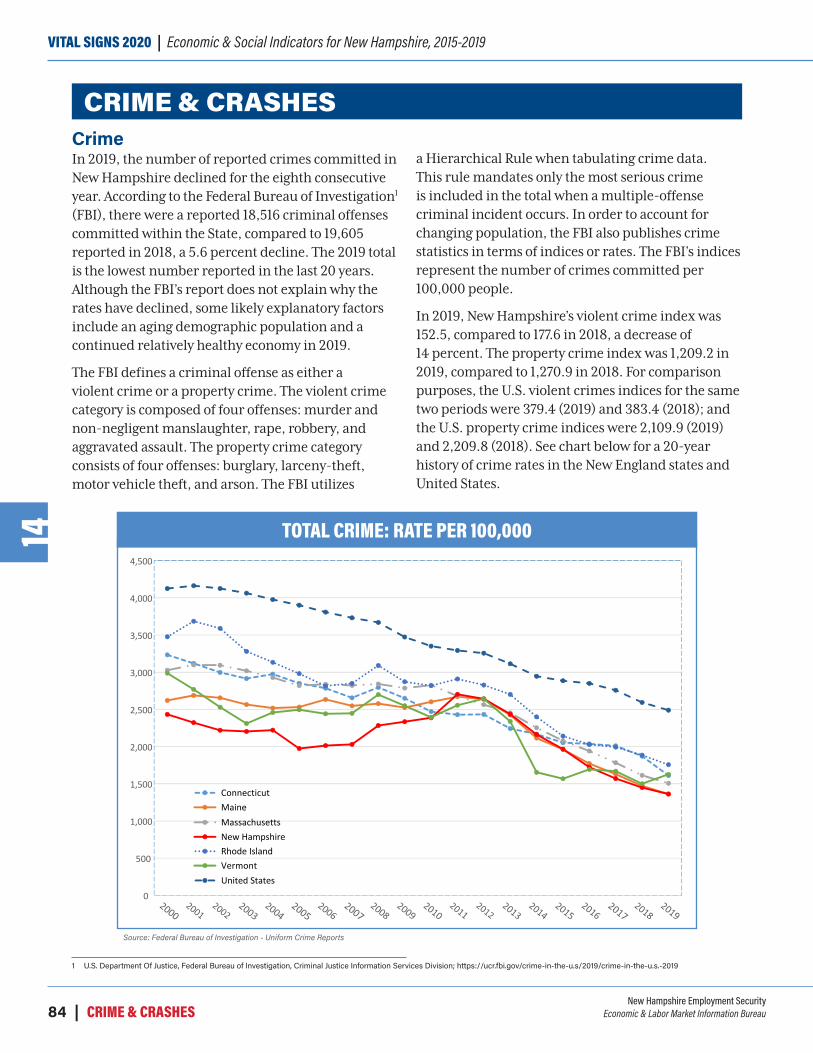

Violent crime index (Rate per 100,000 population) -18 1 -9 2% -25 1 -14 1% 14

Property crime index (Rate per 100,000 population) -103 4 -7 5% -61 7 -4 9% 14

Traffic crashes -2,507 -6 8% -582 -1 7% 14

KEY ECONOMIC INDICATORS

KEY ECONOMIC INDICATORS

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau POPULATION | 1

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20201

POPULATIONThe Impact of COVID-19 on the Workforce by Gender in New HampshireThe COVID-19 pandemic led to a sharp decline in female employment. Workers who lose employment during a recession often continue to have lower earnings long after the recession is over. This impact of a recession is particularly noticeable on women because of the gender wage gap and gender-based job prospects in the labor market.

New Hampshire is among 40 states that have a larger female population than male. The male to female ratio is 98:100. Table-1 shows the state’s total and gender-based population count.

The male-female employment distribution in the workforce presents the opposite scenario. Employment data from the Current Population Survey (CPS) shows that over the previous six years, employment has been higher for males than females. Figure 1 illustrates the inequality between male and female employment numbers during the last six years. This inequality has increased during the pandemic, which highlights the issue of lower labor force participation by women. This study focuses on a sector-based comparison of female and male employment, comparing aggregate data from 2015-2019 to year-to-date data from 2020, to illustrate the impact of coronavirus on the female workforce.

Employment Status Even though males make up a larger share of the total labor force, the unemployment rate for women was lower over the last five years (2015-2019). The average unemployment rate over the last five years for males age 20 and older was

3.76 percent and for females age 20 and older, the average rate was 2.84 percent. During the pandemic, the unemployment rate for females has been higher than the unemployment rate for

- 50,000

100,000 150,000 200,000 250,000 300,000 350,000 400,000 450,000

2015 2016 2017 2018 2019 2020

Figure-1 Employment by Gender

Male Female

FIG 1. EMPLOYMENT STATUS, MALE vs FEMALE

Source: U.S. Census Bureau, 2015 – 2019 American Community Survey 5-Year Estimate

1 U.S. Census Bureau, 2015 – 2019 American Community Survey 5-Year Estimate.

Table-2: Employed Persons by Sex, 2020 Month Total Male Female DifferenceJanuary 757,014 393,050 363,964 29,086

February 745,453 390,404 355,049 35,355

March 723,770 382,840 340,930 41,910

April 606,177 328,567 277,610 50,957

May 654,895 359,502 295,393 64,109

June 685,464 372,532 312,932 59,600

July 716,686 379,144 337,542 41,602

August 722,763 360,890 361,873 -983

September 715,822 375,270 340,552 34,718

October 725,672 376,425 349,247 27,178

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Figure 2. Employed Persons by Gender, Jan-Oct 2020

Total Employed Male Female

FIG 2. EMPLOYMENT PERSONS BY SEX, JAN - OCT 2020

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

Table-1: 2019-2020 Population by Gender1 Total population in New Hampshire 1,359,711Male Population 672,960

Female Population 686,751

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau2 | POPULATION

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20191

2 U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020.

males each month. This is a clear indicator that more women lost jobs during the pandemic than men. The average unemployment rate between January and October for males was 6.6 percent and for females it was 7.4 percent, which was 0.8 percentage points higher.2

Table 2 and Figure 2 show how employment for women decreased more than employment for men during 2020.

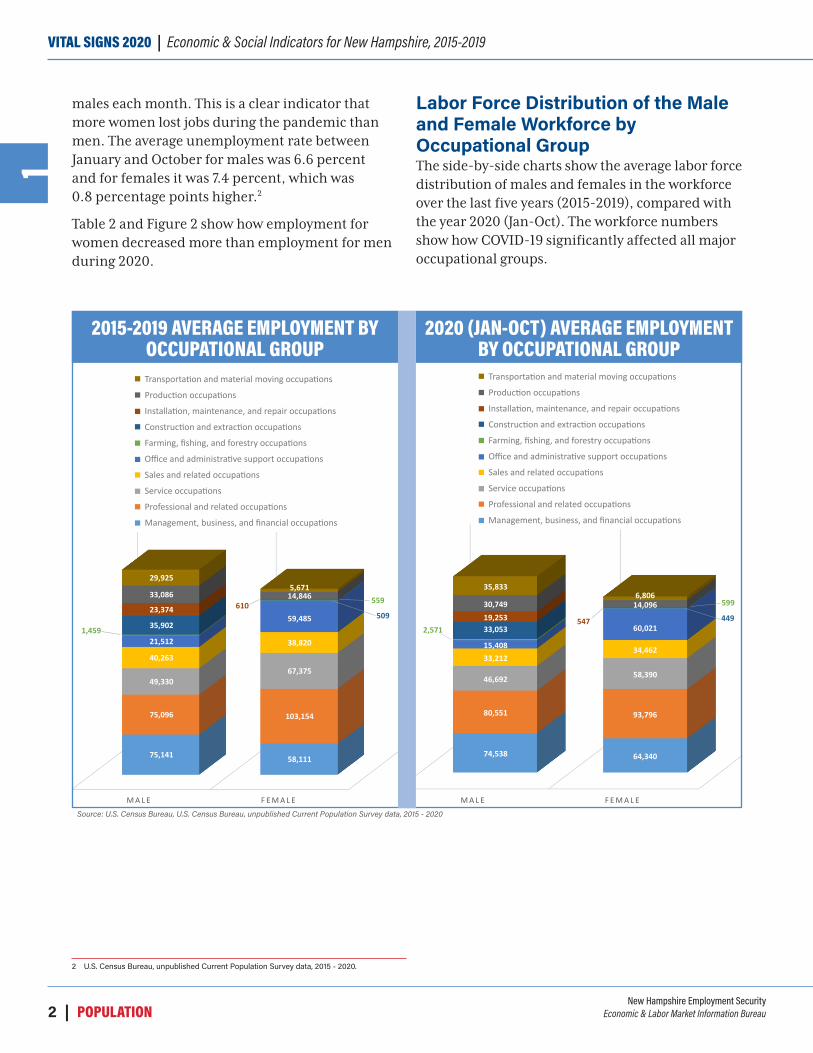

Labor Force Distribution of the Male and Female Workforce by Occupational GroupThe side-by-side charts show the average labor force distribution of males and females in the workforce over the last five years (2015-2019), compared with the year 2020 (Jan-Oct). The workforce numbers show how COVID-19 significantly affected all major occupational groups.

29,925 5,671

33,086 14,846

23,374 610 559

59,485 509

1,459 35,902

21,512 38,820

40,263 67,375

49,330

75,096 103,154

75,141 58,111

M A L E F E M A L E

2015-2019 AVERAGE EMPLOYMENT BY OCCUPATIONAL GROUP

Transporta�on and material moving occupa�ons

Produc�on occupa�ons

Installa�on, maintenance, and repair occupa�ons

Construc�on and extrac�on occupa�ons

Farming, fishing, and forestry occupa�ons

Office and administra�ve support occupa�ons

Sales and related occupa�ons

Service occupa�ons

Professional and related occupa�ons

Management, business, and financial occupa�ons

2020 (JAN-OCT) AVERAGE EMPLOYMENT BY OCCUPATIONAL GROUP

Transporta�on and material moving occupa�ons

Produc�on occupa�ons

Installa�on, maintenance, and repair occupa�ons

Construc�on and extrac�on occupa�ons

Farming, fishing, and forestry occupa�ons

Office and administra�ve support occupa�ons

Sales and related occupa�ons

Service occupa�ons

Professional and related occupa�ons

Management, business, and financial occupa�ons

35,833 6,806

30,749 14,096 599

19,253 547 449 2,571 33,053 60,021

15,408 34,462 33,212

46,692 58,390

80,551 93,796

74,538 64,340

M A L E F E M A L E

2015-2019 AVERAGE EMPLOYMENT BY OCCUPATIONAL GROUP

2020 (JAN-OCT) AVERAGE EMPLOYMENT BY OCCUPATIONAL GROUP

Source: U.S. Census Bureau, U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau POPULATION | 3

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20201

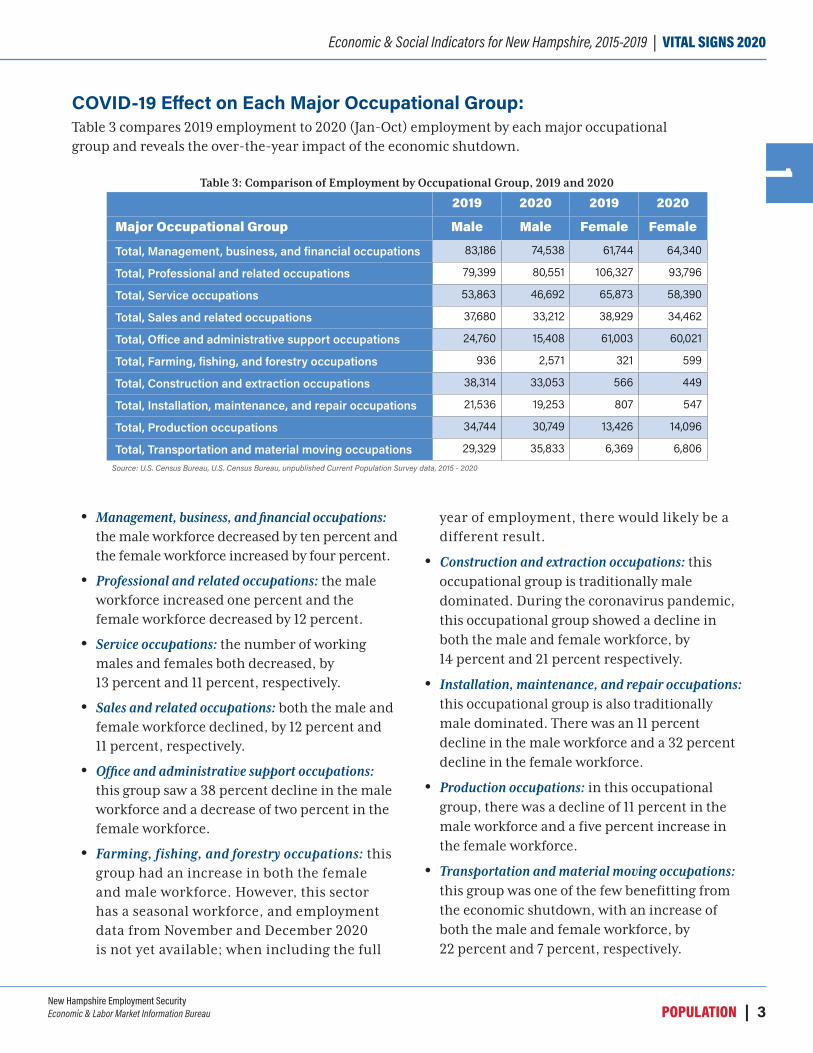

Table 3 compares 2019 employment to 2020 (Jan-Oct) employment by each major occupational group and reveals the over-the-year impact of the economic shutdown.

COVID-19 Effect on Each Major Occupational Group:

Management, business, and financial occupations: the male workforce decreased by ten percent and the female workforce increased by four percent.

Professional and related occupations: the male workforce increased one percent and the female workforce decreased by 12 percent.

Service occupations: the number of working males and females both decreased, by 13 percent and 11 percent, respectively.

Sales and related occupations: both the male and female workforce declined, by 12 percent and 11 percent, respectively.

Office and administrative support occupations: this group saw a 38 percent decline in the male workforce and a decrease of two percent in the female workforce.

Farming, fishing, and forestry occupations: this group had an increase in both the female and male workforce. However, this sector has a seasonal workforce, and employment data from November and December 2020 is not yet available; when including the full

year of employment, there would likely be a different result.

Construction and extraction occupations: this occupational group is traditionally male dominated. During the coronavirus pandemic, this occupational group showed a decline in both the male and female workforce, by 14 percent and 21 percent respectively.

Installation, maintenance, and repair occupations: this occupational group is also traditionally male dominated. There was an 11 percent decline in the male workforce and a 32 percent decline in the female workforce.

Production occupations: in this occupational group, there was a decline of 11 percent in the male workforce and a five percent increase in the female workforce.

Transportation and material moving occupations: this group was one of the few benefitting from the economic shutdown, with an increase of both the male and female workforce, by 22 percent and 7 percent, respectively.

Table 3: Comparison of Employment by Occupational Group, 2019 and 2020 2019 2020 2019 2020

Major Occupational Group Male Male Female Female

Total, Management, business, and financial occupations 83,186 74,538 61,744 64,340

Total, Professional and related occupations 79,399 80,551 106,327 93,796

Total, Service occupations 53,863 46,692 65,873 58,390

Total, Sales and related occupations 37,680 33,212 38,929 34,462

Total, Office and administrative support occupations 24,760 15,408 61,003 60,021

Total, Farming, fishing, and forestry occupations 936 2,571 321 599

Total, Construction and extraction occupations 38,314 33,053 566 449

Total, Installation, maintenance, and repair occupations 21,536 19,253 807 547

Total, Production occupations 34,744 30,749 13,426 14,096

Total, Transportation and material moving occupations 29,329 35,833 6,369 6,806Source: U.S. Census Bureau, U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau4 | POPULATION

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20191

The Effect of the Coronavirus Pandemic on Occupational Groups with a Larger Female WorkforceIn major occupational groups where the female workforce was larger than the male workforce, the pandemic caused a sharper decline for female employment when compared to males in the early phase of economic shutdown.

In service occupations, which includes the food service industry, hospitality, and tourism, females traditionally have held a higher share of employment than males (Figure 3). Figure 4 shows how sharply female employment declined in April, when the economic restrictions to slow the effect of the pandemic began.

Professional and related occupations include management, business and financial, healthcare

practitioners and technical occupations, and education and training occupations. These groups traditionally have more female workers than male (Figure 5). Figure 6 illustrates how the workforce in this group declined during the pandemic.

Sales and related occupations include occupations such as retail sales workers and cashiers, and had more female than male workers before the pandemic (Figure 7). Figure 8 shows that, similar to the service-related employment, female workers in these occupations struggled to stay on the job during the pandemic.

Office and administrative support was another occupational group where women were employed at higher levels than the men prior to the COVID-19 pandemic (Figure 19). Figure 10 shows that this group follows a similar trend of sharply declining female employment observed in previous occupational groups.

- 20,000 40,000 60,000 80,000

100,000 120,000 140,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Figure 4. Service Occupation Employment, Jan-Oct, 2020

Total Male Female

FIG 4. SERVICE OCCUPATIONS JAN-OCT, 2020

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

2015 2016 2018 2019 2020

Figure 3. Service Occupation Employment, 2015-2020

Male Female

2017

FIG 3. SERVICE OCCUPATIONS (2015-2020)

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020 -

50,000

100,000

150,000

200,000

250,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Figure 6: Professional and Related Occupation Employment, Jan-Oct, 2020

Total Male Female

FIG 6. PROFESSIONAL AND RELATED OCCUPATIONS, JAN-OCT 2020

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

-

20,000

40,000

60,000

80,000

100,000

120,000

2015 2016 2017 2018 2019 2020

Figure 5: Professional and Related Occupation Employment, 2015-2020

Male Female

FIG 5. PROFESSIONAL AND RELATED OCCUPATIONS (2015-2020)

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau POPULATION | 5

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20201

3 Alon et al., “This Time It’s Different: The Role of Women’s Employment in a Pandemic Recession,” National Bureau of Economic Research. https://www.nber.org/papers/w27660. 4 Alon, et al., “Impact of the Covid-19 Crisis on Women’s Employment,”Econofact. https://econofact.org/impact-of-the-covid-19-crisis-on-womens-employment.5 Sarah Mattson Dustin, J.D., “The Status of Women in New Hampshire”, New Hampshire Women’s Foundation. https://nhwomensfoundation.org/wp-content/uploads/2018/10/Final-

SoW-2018-PDF-for-Website.pdf.6 U.S. Bureau of Labor Statistics, “Supplemental data measuring the effects of the coronavirus (COVID-19) pandemic on the labor market.” https://www.bls.gov/cps/effects-of-the-

coronavirus-covid-19-pandemic.htm.

1. Childcare: The closure of schools and day care facilities has had the greatest impact on childcare needs, which typically has a larger impact on women’s ability to work. The increase in childcare responsibilities affected the female workforce more than the male workforce, as there are more single or stay-at-home mothers than single or stay-at-home fathers.3 More specifically, school and day care closings resulted in an increase in the amount of time spent on childcare for parents with young children.4

2. Unequal pay: Based on a study by the New Hampshire Women’s Foundation, published in 2018, women who work full time

earn 79¢ for every $1 that men earn. The wage gap can be bigger or smaller based on marital status, race, and ethnicity. Unequal pay is another reason which made women more likely to leave the labor force during the pandemic.5

3. Type of employment: The U.S. Bureau of Labor Statistics reported that workers who were usually employed part-time were more likely to be laid off or furloughed during the pandemic than full-time workers.6 More than 60 percent of part-time jobs in New Hampshire were filled by female workers, meaning women would be disproportionately impacted by declines in part-time employment. In addition, some industries that tend to employ more women,

-

20,000

40,000

60,000

80,000

100,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Figure 8: Sales and Related Occupation Employment, Jan-Oct, 2020

Total Male Female

FIG 8. SALES AND RELATED OCCUPATIONS, JAN-OCT, 2020

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

Figure 7. Sales and Related Occupa�on Employment, 2015-2020

50,000

40,000

30,000

20,000

10,000

-2015 2016 2017

Male

2018 2019 2020

Female

FIG 7. SALES AND RELATED OCCUPATIONS (2015-2020)

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

-

20,000

40,000

60,000

80,000

100,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Figure 10: Office and Administrative Support Occupation Employment, Jan-Oct, 2020

Total Male Female

FIG 10. OFFICE AND ADMIN SUPPORT OCCUPATIONS, JAN-OCT, 2020

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

Figure 9. Office and Administra�ve Support Occupa�on Employment, 2015 - 2020

70,000

60,000

50,000

40,000

30,000

20,000

10,000

-2015 2016 2017

Male

2018 2019 2020

Female

FIG 9. OFFICE AND ADMIN SUPPORT OCCUPATIONS (2015-2020)

Source: U.S. Census Bureau, unpublished Current Population Survey data, 2015 - 2020

Reasons for women to leave the labor force during the COVID-19 pandemic:

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau6 | POPULATION

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20191

such as accommodation and food services, which had a 57 percent female workforce in 2019, were severely affected by the pandemic. Social distancing and other measures to slow the spread of the coronavirus have forced businesses in these sectors to shut down or reduce capacity, which had a greater impact on female employment.7

4. Utilization of Unemployment Insurance benefits: Unemployment insurance benefit changes enacted early in the pandemic allowed self-employed and gig workers to have access to benefits, and allowed people who were not actively looking for work due to pandemic-related reasons to remain eligible for benefits as well. This allowed women who left the workforce during the pandemic to take care of their children to receive unemployment benefits, even if they were not actively looking for work.

The reasons listed above beget the question: what measures can business leaders, stakeholders, employers, and policymakers consider to minimize a similar crisis in the future during another recession or pandemic?

Women with younger children are more likely to look for jobs with flexible work hours. Limited availability of affordable childcare can lead more women to work multiple jobs, or longer hours. During the pandemic, the lack

7 New Hampshire Employment Security, New Hampshire 2018 Workforce Analysis - In Review. https://www.nhes.nh.gov/elmi/products/documents/workforce-analysis-2018.pdf8 Madgavkar et al. “Covid-19 and gender inequality: Countering the regressive effect.” https://www.mckinsey.com/featured-insights/future-of-work/covid-19-and-gender-equality-countering-

the-regressive-effects.9 Ibid.

of childcare during led more women to quit their jobs. Policies that are family-friendly, or flexible programs to support female workers who experience an increased childcare burden during a pandemic, would increase female labor force participation.8 Employers could offer daycare support either in the workplace or other benefits for employees with children, such as subsidized childcare expenses, flexible hours, or paid family leave. This could ensure working mothers are able to work without worrying about childcare considerations.

During the coronavirus pandemic, working virtually with the help of digital technologies grew exponentially. Many jobs transitioned to allow workers to work from home. Many businesses have migrated to online platforms. Training in digital technologies for female workers could lead to a larger percentage of the female workforce being able to work remotely. Training and access to digital devices and software could create more opportunities for jobs for women in the future as well. Employers play key roles in creating infrastructure and support for such digital technologies.9

A change in the societal mindset to more equal sharing of childcare responsibilities between mothers and fathers would lead to more women participating in the workforce.

– Nusrat Jahan

RESIDENT POPULATION 2015 2016 2017 2018 2019Population, July 1st 1,336,350 1,342,307 1,348,787 1,353,465 1,359,711Annual percent change 0.2% 0.4% 0.5% 0.3% 0.5%United States rank of annual percent change (including District of Columbia) 39 27 21 23 21

Population by GenderPopulation, Males 661,455 664,650 667,781 670,773 673,793Population, Females 674,895 677,657 681,006 682,692 685,918

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau POPULATION | 7

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20201

RESIDENT POPULATION (continued...) 2015 2016 2017 2018 2019Distribution by AgeUnder 5 years 4.8% 4.8% 4.8% 4.7% 4.7%5 to 17 years 15.0% 14.8% 14.5% 14.3% 14.1%18 to 24 years 9.7% 9.6% 9.5% 9.3% 9.1%25 to 44 years 23.5% 23.5% 23.7% 23.9% 24.2%45 to 64 years 30.6% 30.4% 30.1% 29.7% 29.2%65 years and over 16.4% 16.9% 17.5% 18.0% 18.7%

Median AgeUnited States 37.8 37.9 38.0 38.2 38.4New Hampshire 42.7 42.8 42.9 43.0 43.1Connecticut 40.8 40.9 40.9 41.0 41.1Maine 44.4 44.6 44.8 44.9 45.0Massachusetts 39.3 39.4 39.4 39.4 39.6Rhode Island 39.9 39.9 40.0 40.0 40.1Vermont 42.7 42.8 42.8 42.9 43.0

Components of Population Change (annual)Natural increase rate (per 1,000 population) 0.3 0.4 -0.1 -0.3 -0.1Net migration rate (per 1,000 population) 2.1 4.1 4.9 3.8 4.7

Source: Population Division, U.S. Census Bureau, ELMI Analysis. Last Update 7/22/2020

VITAL STATISTICS 2015 2016 2017 2018 2019Marriages 9,234 9,319 9,445 9,405 9,030Marriage rate (per 1,000 population) 6.9 6.9 7.0 6.9 6.6

Divorces 4,481 4,607 4,262 4,217 4,180Divorce rate (per 1,000 population) 3.4 3.4 3.2 3.1 3.1

Live births 12,495 12,350 12,064 11,977 11,826Birth rate (per 1,000 population) 9.4 9.2 8.9 8.8 8.7

Births to teenage mothers (less than 20 years old) 475 409 370 346 285

Percent of total live births 3.8% 3.3% 3.1% 2.9% 2.4%Non-marital births (percent of live births) 34.6% 34.5% 33.3% 33.5% 32.6%

Resident deaths 11,987 12,182 12,480 12,779 12,740Crude death rate (per 1,000 population) 9.0 9.1 9.3 9.4 9.4Infant death rate (per 1,000 live births) 4.2 3.6 4.2 3.6 3.2

Source: Division of New Hampshire Vital Records Administration, ELMI Analysis. Last Update 7/22/2020

Prepared by: New Hampshire Employment Security, Economic and Labor Market Information Bureau

www.nhes.nh.gov/elmi | (603) 228-4124

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau8 | INCOME & WAGES

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20192

Per Capita Personal IncomePer capita personal income rose in New Hampshire by 4.0 percent in 2019 over the previous year. This was the smallest increase since 2014, although, adjusted for inflation, it was still an increase of 2.4 percent. New Hampshire ranked 8th among all states in per capita personal income for the third year in a row.1

On a county level, per capita personal income was highest in Rockingham County, $76,902, and lowest in Coös County, $44,399. Commuting pattern data from the U.S. Census Bureau shows that in 2018, more than one quarter of employed Rockingham County residents commuted to Massachusetts for work, and were able to take advantage of the higher wages paid there.2 Per capita personal income in Massachusetts was $74,187 in 2019, second highest in the U.S. Roughly half of Rockingham County residents who worked in Massachusetts were employed in Middlesex and Suffolk counties, which had per capita income even higher than the Massachusetts average, at $87,192 and $83,490, respectively.

Income DistributionIncome is not distributed evenly for all residents. The Gini index measures income equality on a scale from 0 to 1, with a 0 indicating perfect equality, where there is equal distribution of income. A Gini index of 1 indicates perfect inequality, where one household has all the income.3

New Hampshire’s Gini coefficient was 0.4384 in 2019, the 4th lowest of any state in the U.S. It had a lower Gini coefficient, and less income inequality, than

1 Income includes earnings from employment, as well as other sources of income, including interest and dividends, social security, child support, and money from rental income.2 U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages, 2018. https://www.bls.gov/cew/data.htm3 U.S. Census Bureau, Household Income: 2018. https://www.census.gov/content/dam/Census/library/publications/2019/acs/acsbr18-01.pdf.4 Retired workers still earn incomes, as income includes non-employment related income such as social security, and interest and dividends from investments.

INCOME & WAGES

GINI INDEX, 2010 – 2019

0.38

0.4

0.42

0.44

0.46

0.48

0.5

0.52

2019201820172016201520142013201220112010

Gini Index, 2010 - 2019

NH U.S. CT ME MA RI VT

Source: U.S. Census Bureau, American Community Survey 5-Year Estimates

any other state in New England. In both the U.S. and in New Hampshire, Gini coefficients have increased slightly since 2010. New Hampshire’s Gini coefficient was 0.4210 in 2010, while the U.S. Gini coefficient increased from 0.4670 in 2010 to 0.4823 in 2019.

In New Hampshire, the increase is at partially attributable to demographic shifts. Older and younger individuals tend to have lower incomes, as one group begins their careers, and the other retires and leaves the workforce.4 Recent demographic changes in New Hampshire have increased the size of these two groups. New Hampshire’s population is aging, and the share of the population that is retirement age is increasing. In addition, migration in recent years has led to a net increase in residents in their 20s and 30s.

Median EarningsAmong New Hampshire residents who were employed full-time, year-round in 2019 (this accounted for roughly 65 percent of all individuals

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau INCOME & WAGES | 9

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20202

- 20,000 40,000 60,000 80,000 100,000 120,000

$14,999 or less(including loss)

$15,000 to $24,999

$25,000 to $34,999

$35,000 to $49,999

$50,000 to $64,999

$65,000 to $74,999

$75,000 to $99,999

$100,000 or more

2019 Earnings for Full-Time, Year-Round Workers in New Hampshire

2019 EARNINGS FOR FULL-TIME, YEAR-ROUND WORKERS IN NEW HAMPSHIRE

Source: U.S. Census Bureau, American Community Survey, 2019 1-Year Estimate

5 The U.S. Department of Labor does not have a standard definition of “full-time” employment. Typically this determination is made by employers. 6 Average weekly wages is not an earnings measure, but is the quarterly total of compensation paid, including bonuses, stock options, severance pay, profit distributions, the cash value of

meals and lodging, tips and other gratuities, divided by average quarterly employment, then divided by 13 weeks.

age 16 or older who had earnings in 2019), median annual earnings were $55,283. The largest cohort of full-time year-round New Hampshire workers, 20 percent, earned between $35,000 and $49,999 annually, followed by 19 percent who earned more than $100,000.

An estimated 15,500 workers, three percent of full-time, year-round workers, earned less than $15,000. Since an individual working 40 hours per week at federal minimum wage would earn $15,080 annually, workers earning less than $15,000 may earn less than minimum wage, although some may work fewer than 40 hours per week.5 Workers in this earnings category include self-employed individuals with an earnings loss over the previous 12 months. In addition, there are a few groups of workers, including some tipped employees, some workers with disabilities, and some agricultural workers, to whom the federal minimum wage doesn’t apply.

Average Weekly Wages By IndustryThe average weekly wage in New Hampshire was $1,145 in 2019, a 3.5 percent increase over the previous year.6 Average weekly wages have grown by more than three percent in each of the last four years. Average weekly wages vary significantly by industry. The finance and insurance industry had the highest average wages in 2019, with $2,134 per week, nearly double the overall average. The industry with the lowest average wage was accommodation and food services, where the average was $435 per week.

The coronavirus pandemic caused thousands of New Hampshire residents to lose their jobs, either temporarily or permanently. Many other workers had their salaries or hours reduced. The change in

average weekly wages over the first two quarters of 2020 shows how wages in different industries were impacted by the pandemic.

For total private employment, seasonal factors typically cause average weekly wages to be lower in the second and third quarters, and higher in the first and fourth. In 2020, average weekly wages fell from $1,223 in Q1 to $1,215 in Q2, a decline of 0.6 percent. This was a smaller decline than in 2018 and 2019, when the average weekly wage fell an average of eight percent from Q1 to Q2.

The smaller decline in total wages in 2020, relative to previous years, is likely the result of layoffs caused by the pandemic, rather than wages increasing year-over-year for workers. Job losses were more likely to impact newly hired workers, who are typically laid off before more experienced staff, and who earn less than their more experienced colleagues.

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau10 | INCOME & WAGES

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20192

7 State of New Hampshire, Office of the Governor, Emergency Order #31, https://www.nhes.nh.gov/services/employers/documents/emergency-order31-ltcs-program.pdf.

In addition, employment in several industries with low average wages – particularly accommodation and food services and arts, entertainment and recreation – decreased more than New Hampshire employment overall. Wages in accommodation and food services increased seven percent from the first quarter of 2020 to the second quarter, while wages in arts, entertainment and recreation increased nearly 30 percent. At the same time, employment in these industries decreased by 46 and 39 percent, respectively. With low-wage workers disproportionately impacted by layoffs, these workers made up a smaller share of overall employment, resulting in an increase in overall average wages.

Layoffs were not the only cause of increased wages. In April 2020, the governor’s Emergency Order #31 established a stipend of up to $300 per week for front-line workers employed at Medicaid-eligible long-term care providers.7 Average weekly wages

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2018Q1

2018Q2

2018Q3

2018Q4

2019Q1

2019Q2

2019Q3

2019Q4

2020Q1

2020Q2

Average Weekly Wage by Industry

Total Private

Manufacturing

Retail Trade

Transportation and Warehousing

Information

Finance and Insurance

Professional and Technical Services

Educational Services

Health Care and Social Assistance

Arts, Entertainment, and Recreation

Accommodation and Food Services

AVERAGE WEEKLY WAGE BY INDUSTRY

Source: New Hampshire Employment Security, Quarterly Census of Employment and Wages

for workers in the nursing and residential care facilities industry increased from $750 per week in 2020 Q1 to $889 per week in Q2, an increase of 18 percent.

Other businesses, including several large retailers, temporarily increased wages for workers who remained at work during early months of the pandemic. Average wages for workers at food and beverage stores, who typically see average weekly wages decrease during the second quarter, saw average weekly wages increase 1.5 percent in 2020 Q2.

In other industries, wages were largely unchanged during the early months of the pandemic. Average weekly wages in finance and insurance, information, and professional and technical services, three of the highest paying industries, appear to follow existing trends, trending upwards with some seasonal variation.

– Greg David

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau INCOME & WAGES | 11

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20202

TOTAL PERSONAL INCOME 2015 2016 2017 2018 2019New Hampshire ($ millions) $73,212.4 $75,816.7 $78,822.1 $83,142.6 $86,858.7Components:Net Earningsa 67.5% 67.5% 67.7% 67.2% 67.2%Dividends, interest, rent 17.8% 17.5% 17.4% 17.9% 17.6%Transfer payments 14.7% 15.0% 14.9% 14.9% 15.3%

a Earnings (wages and salaries, other income, and proprietors’ income) by place of work, less personal social insurance by place of work, adjusted for place of residence.

Per Capita Personal IncomeNew Hampshire $54,788 $56,482 $58,439 $61,429 $63,880United States rank (excluding D.C.) 9 7 8 8 8Annual percent change 4.0% 3.1% 3.5% 5.1% 4.0%Percent change after adjusting for inflation using CPI 5.2% 4.0% 3.7% 4.3% 2.4%

Per Capita Disposable IncomeNew Hampshire $48,987 $50,333 $52,026 $54,991 $57,295United States rank (excluding D.C.) 8 7 7 7 8Annual percent change 3.4% 2.7% 3.4% 5.7% 4.2%Percent change after adjusting for inflation using CPI 4.6% 3.6% 3.7% 5.0% 2.3%

Source: Bureau of Economic Analysis; ELMI Analysis. Last Update 9/23/2020

MEDIAN HOUSEHOLD INCOME (in current dollars) 2015 2016 2017 2018 2019

New Hampshire $75,675 $76,260 $75,630 $81,346 $86,900Connecticut $72,889 $75,923 $74,304 $72,812 $87,291Maine $50,756 $50,856 $53,316 $58,663 $66,546Massachusetts $67,861 $72,266 $76,243 $86,345 $87,707Rhode Island $55,701 $61,528 $65,401 $62,266 $70,151Vermont $59,494 $60,837 $63,682 $70,066 $74,305Source: CPS Annual Social and Economic Supplement. Last Update 9/28/2020

AVERAGE WEEKLY EARNINGS OF ALL EMPLOYEES, IN DOLLARS 2015 2016 2017 2018 2019

Earnings of Production Workers in Manufacturing $821.18 $866.07 $914.57 $937.01 $955.40Average Weekly Earnings of All Employees $836.64 $869.34 $891.57 $888.11 $901.80

Source: US DOL, Bureau of Labor Statistics - Current Employment Statistics. Last update 7/22/2020

U.S. PRICE INDICES 2015 2016 2017 2018 2019CONSUMER PRICE INDEX, All Urban Consumers, Year End (Not-seasonally Adjusted)Annual Average (U.S., 1982-1984 = 100) 237.017 240.007 245.120 251.107 255.657Over-the-Year Change in Annual Average 0.1% 1.3% 2.1% 2.4% 1.8%

Northeast Urban Region CPI-U, Year End (Not-seasonally Adjusted)Annual Average (U.S., 1982-1984 = 100) 252.185 254.850 259.538 265.139 269.392Over-the-Year Change in Annual Average -0.1% 1.1% 1.8% 2.2% 1.6%

Source: US DOL, Bureau of Labor Statistics - Consumer Price Index; ELMI Analysis. Last update 7/22/2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau12 | INCOME & WAGES

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20192

WAGES 2015 2016 2017 2018 2019TOTAL WAGES, workers covered by unemployment compensation (millions)Private and public employers $33,466 $34,675 $36,032 $37,409 $39,038Annual percent change 4.4% 3.6% 3.9% 3.8% 4.4%

AVERAGE WEEKLY WAGE in employment covered by unemployment compensationAll Private industries (annual average) $1,011 $1,043 $1,074 $1,106 $1,145Annual percent change 1.4% 3.2% 3.0% 3.0% 3.5%

Agriculture, Forestry, Fishing, and Hunting $681 $678 $697 $698 $733Mining $1,113 $1,125 $1,214 $1,215 $1,278Utilities $1,983 $1,981 $2,140 $2,245 $2,126Construction $1,101 $1,132 $1,183 $1,205 $1,248Manufacturing $1,286 $1,313 $1,355 $1,379 $1,404Wholesale Trade $1,742 $1,729 $1,762 $1,805 $1,870Retail Trade $591 $596 $608 $631 $653Transportation and Warehousing $811 $819 $846 $889 $926Information $1,591 $1,641 $1,695 $1,800 $1,870Finance and Insurance $1,830 $1,941 $1,943 $2,032 $2,134Real Estate and Rental and Leasing $978 $1,002 $1,023 $1,059 $1,143Professional and Technical Services $1,674 $1,707 $1,807 $1,881 $1,940Management of Companies and Enterprises $2,049 $1,993 $2,103 $1,966 $2,046Administrative and Waste Services $869 $888 $914 $955 $995Educational Services $1,029 $1,040 $1,041 $1,075 $1,119Health Care and Social Assistance $1,000 $1,022 $1,052 $1,085 $1,123Arts, Entertainment, and Recreation $417 $413 $426 $443 $453Accommodation and Food Services $373 $387 $401 $418 $435Other Services, except Public Admin $680 $691 $705 $729 $755

Total Government $937 $946 $968 $994 $1,014Data are not adjusted for inflation.

Source: New Hampshire Employment Security; ELMI Analysis. Last Update 9/23/2020

Prepared by: New Hampshire Employment Security, Economic and Labor Market Information Bureau

www nhes nh gov/elmi | (603) 228-4124

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau LABOR FORCE & UNEMPLOYMENT | 13

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20203

Understanding Labor Force Statistics during the first nine months of the Coronavirus PandemicPrior to the coronavirus pandemic, New Hampshire’s labor force statistics had been steady for more than four years. The unemployment rate was 2.9 percent in January 2016, reached a low of 2.5 percent in September 2018 and was 2.6 percent in February 2020. During that time, both the labor force and the number of employed residents increased almost every month. Although statewide action to contain the coronavirus began in the third week of March 2020, labor force statistics were not significantly affected until April. New Hampshire’s seasonally adjusted unemployment rate reached a historic high of 16.0 percent in April, the eighth highest rate in the country. The unemployment rate rapidly declined thereafter to 3.8 percent in December.

The calculation of state labor force statistics during 2020 was a challenge for the Bureau of

LABOR FORCE & UNEMPLOYMENT

Labor Statistics. The magnitude of employment disruptions caused by the coronavirus pandemic, which resulted in more volatile month-to-month estimates of the seasonally adjusted series than in prior years, necessitated modifications to the seasonal adjustment process.1 However, the underlying trends indicated progress over the course of the year. As of December 2020, three-quarters of the lost employment had been recovered and approximately half of those residents who exited the labor force were participating once again.

Unemployment rate estimates throughout the country were subjected to significant scrutiny and criticism throughout 2020. The rates were often expected to be much higher based on the magnitude of unemployment benefit claims, and fell rapidly in contrast to continuing

1 U.S. Bureau of Labor Statistics. 2020. Frequently asked questions: The impact of the coronavirus (COVID-19) pandemic on the Employment Situation for April 2020. May 8. Accessed January 8, 2021. https://www.bls.gov/covid19/employment-situation-covid19-faq-april-2020.htm.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Employment Status of New Hampshire Residents 2019-2020

Employed Unemployed Not In Labor Force

EMPLOYMENT STATUS OF NEW HAMPSHIRE RESIDENTS, 2019-2020

Source: New Hampshire Employment Security, Local Area Unemployment Statistics

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau14 | LABOR FORCE & UNEMPLOYMENT

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20193

2 U.S. Bureau of Labor Statistics. 2020. How the Government Measures Unemployment. Accessed January 8, 2021. https://www.bls.gov/cps/cps_htgm.htm.3 U.S. Bureau of Labor Statistics. 2020. Frequently asked questions: The impact of the coronavirus (COVID-19) pandemic on the Employment Situation for April 2020. May 8. Accessed January

8, 2021. https://www.bls.gov/covid19/employment-situation-covid19-faq-april-2020.htm.4 116th Congress. 2020. “H.R.748 - CARES Act.” CONGRESS.GOV. March 27. Accessed January 15, 2021. https://www.congress.gov/bill/116th-congress/house-bill/748.

unemployment claims, which decreased much more slowly. Unemployment claims and the unemployment rate measure two related but different populations. The criteria for measuring the unemployment rate is firmly established, while the criteria for unemployment claims is subject to legislative changes. The expansion of unemployment benefit eligibility and payment amounts to provide a stronger safety net for job losers during the coronavirus pandemic increased the divergence between the two populations.

The Bureau of Labor Statistics classifies people as unemployed if they did not have a job, were available for work and had actively searched for work in the prior four weeks. Workers who expected a recall from a temporary layoff are an exception, as they were not required to perform a job search during their short-term layoff. In addition to the number of people who had lost jobs, the unemployed also include people who had quit their jobs to look for other work and those individuals who looked for a job upon entering or re-entering the labor force.2 The key point is that, with the exception of temporary layoffs, an active job search is required to be classified as unemployed. Individuals who were neither employed nor unemployed were classified as not in the labor force, regardless of their receipt of unemployment benefits.

April 2020 labor force estimates indicated that there were approximately 133,000 fewer New Hampshire residents employed and 97,500 more unemployed than in February. The difference of approximately 35,500 represented the number individuals who exited the labor force, and were classified as neither employed nor unemployed. The shift from employment to unemployment was directly or indirectly influenced by a number of factors including health concerns, coronavirus mitigating actions taken by employers and government officials, temporary changes to the supply and demand for goods and services, the expanded availability of unemployment benefits

and increases to weekly benefit payments, and other factors. Expanded unemployment benefits provided workers and employers with the opportunity to reduce the risk of exposure to the coronavirus while maintaining an income stream for workers’ living expenses. Many of the residents who were no longer in the labor force expected a long-term or permanent separation from their previous employment or self-employment and were not looking for work. Health concerns, reduced job opportunities, mandatory closures and stay-at-home orders due to the coronavirus pandemic were the driving force behind this exodus.3

Self-EmploymentThe treatment of self-employed individuals regarding unemployment benefit compensation compared to labor force statistics also differs. The official unemployment rate includes self-employed individuals as employed. Individuals who ceased self-employment and searched for work were classified as unemployed labor force entrants. In most cases, these individuals were not eligible for unemployment benefits. Prior to the coronavirus pandemic, monthly unemployment estimates exceeded claims due to the inclusion of the unemployed who were not eligible for unemployment benefits due to a variety of reasons.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act extended unemployment benefits to self-employed individuals who were unable to conduct business due to the coronavirus pandemic.4 This extension of benefits to those not typically eligible changed the relationship between unemployment claim levels and official unemployment estimates. Unemployment claim levels during the pandemic not only included former self-employed individuals who became unemployed due to pandemic-related reasons, but also those who exited the labor force and those who continued to operate their businesses at a reduced capacity. The official unemployment rate classifies

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau LABOR FORCE & UNEMPLOYMENT | 15

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20203

5 U.S. Bureau of Labor Statistics. 2020. The Employment Situation – April 2020. USDL-20-0815, May 8.

individuals who continued to perform tasks for their businesses as employed regardless of whether the businesses were profitable or operating at reduced capacity.

Labor Force MisclassificationThe Bureau of Labor Statistics (BLS) caused significant discussion of an “error” in the national unemployment rate with the publication of a technical note entitled “Coronavirus (COVID-19) Impact on March 2020 Establishment and Household Survey Data” in the April 3, 2020 release of The Employment Situation - March 2020. This was related to a subcategory of the employed, which includes those who were not at work during the week for which Current Population Survey data were collected. This subcategory is further parsed into the various reasons for absence from work, including vacation or personal days, own illness or injury, child care problems, family or personal obligations, maternity or paternity leave, labor dispute, weather affected job, school or training, civic or military duty and “other.” The BLS detected a large increase in the number of individuals

included in the “other” category. A worst-case scenario calculation was performed in which all of those in this category above a typical March estimate were assumed to be unemployed rather than employed. This assumption was based on the possibility that survey respondents misunderstood the questions, and did not respond appropriately. The BLS estimated that the U.S. unemployment rate would have been nearly one percentage point higher in March. A subsequent calculation for the April estimate determined that the unemployment rate would have been almost five percentage points higher based on this assumption.5

Although this was frequently referred to as an “error” in the BLS estimates, it simply represented a worst-case scenario if all other possible explanations were invalid. It is reasonable to assume that this “other” category may have also included misclassified individuals who were on vacation but couldn’t travel due to the coronavirus, misclassified individuals who had exited the labor force on a temporary leave without pay, and misclassified individuals who were working

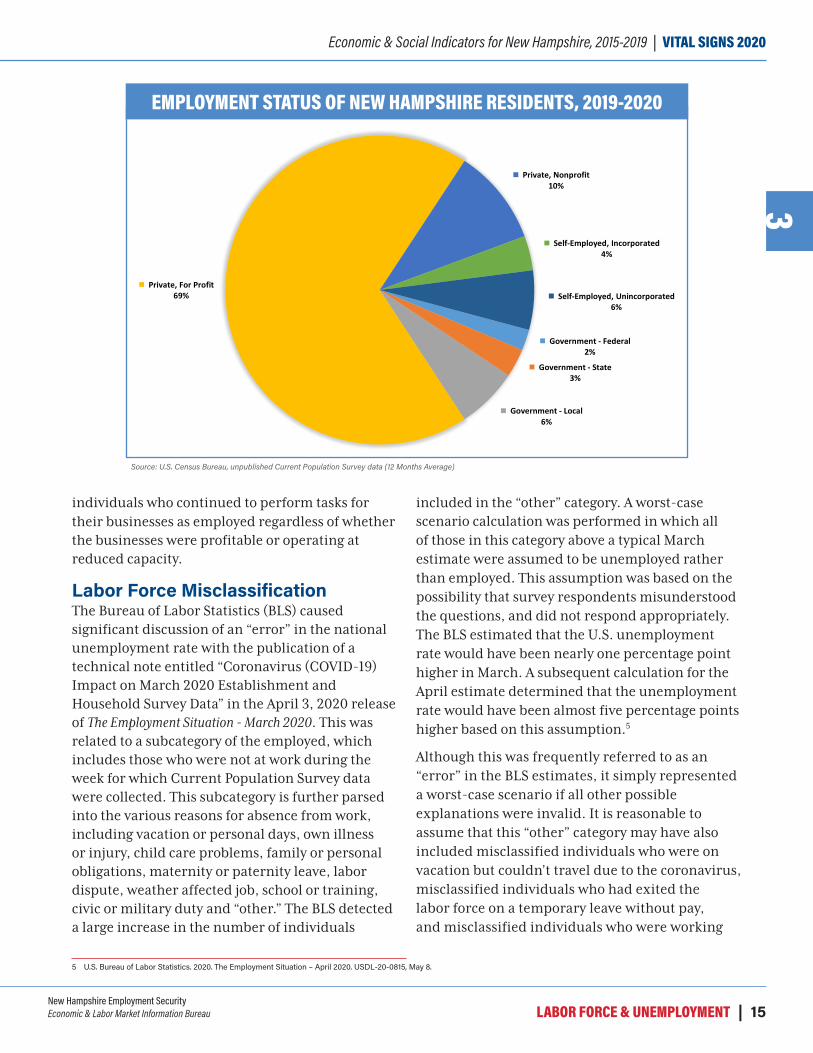

Government - Federal2%

Government - State3%

Government - Local6%

Private, For Profit69%

Private, Nonprofit10%

Self-Employed, Incorporated4%

Self-Employed, Unincorporated6%

NEW HAMPSHIRE LABOR FORCE IN 2020 BY CLASS OF WORKER

EMPLOYMENT STATUS OF NEW HAMPSHIRE RESIDENTS, 2019-2020

Source: U.S. Census Bureau, unpublished Current Population Survey data (12 Months Average)

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau16 | LABOR FORCE & UNEMPLOYMENT

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20193

from home. Such misunderstandings and misclassifications would have been possible in every month of the survey; however the uncertainty caused by the coronavirus pandemic increased the probability that these response errors may have occurred.

State level data for this analysis are not readily available and are not statistically reliable. Furthermore, since official state labor force statistics are not derived directly from Current Population Survey data, any misclassification estimate produced would not be comparable to monthly state labor force statistics.

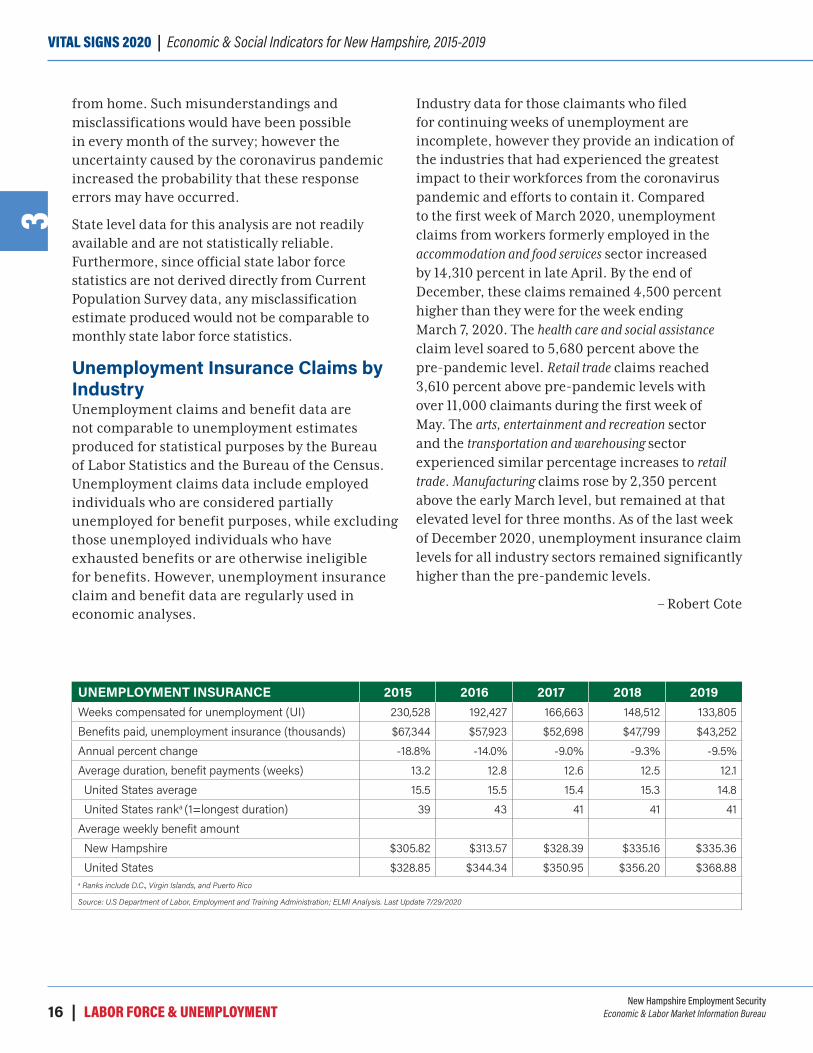

Unemployment Insurance Claims by IndustryUnemployment claims and benefit data are not comparable to unemployment estimates produced for statistical purposes by the Bureau of Labor Statistics and the Bureau of the Census. Unemployment claims data include employed individuals who are considered partially unemployed for benefit purposes, while excluding those unemployed individuals who have exhausted benefits or are otherwise ineligible for benefits. However, unemployment insurance claim and benefit data are regularly used in economic analyses.

Industry data for those claimants who filed for continuing weeks of unemployment are incomplete, however they provide an indication of the industries that had experienced the greatest impact to their workforces from the coronavirus pandemic and efforts to contain it. Compared to the first week of March 2020, unemployment claims from workers formerly employed in the accommodation and food services sector increased by 14,310 percent in late April. By the end of December, these claims remained 4,500 percent higher than they were for the week ending March 7, 2020. The health care and social assistance claim level soared to 5,680 percent above the pre-pandemic level. Retail trade claims reached 3,610 percent above pre-pandemic levels with over 11,000 claimants during the first week of May. The arts, entertainment and recreation sector and the transportation and warehousing sector experienced similar percentage increases to retail trade. Manufacturing claims rose by 2,350 percent above the early March level, but remained at that elevated level for three months. As of the last week of December 2020, unemployment insurance claim levels for all industry sectors remained significantly higher than the pre-pandemic levels.

– Robert Cote

UNEMPLOYMENT INSURANCE 2015 2016 2017 2018 2019Weeks compensated for unemployment (UI) 230,528 192,427 166,663 148,512 133,805Benefits paid, unemployment insurance (thousands) $67,344 $57,923 $52,698 $47,799 $43,252Annual percent change -18.8% -14.0% -9.0% -9.3% -9.5%Average duration, benefit payments (weeks) 13.2 12.8 12.6 12.5 12.1United States average 15.5 15.5 15.4 15.3 14.8United States ranka (1=longest duration) 39 43 41 41 41

Average weekly benefit amountNew Hampshire $305.82 $313.57 $328.39 $335.16 $335.36United States $328.85 $344.34 $350.95 $356.20 $368.88

a Ranks include D.C., Virgin Islands, and Puerto Rico

Source: U.S Department of Labor, Employment and Training Administration; ELMI Analysis. Last Update 7/29/2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau LABOR FORCE & UNEMPLOYMENT | 17

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20203

610%

40%

440%

500%

2,350%

1,290%

3,610%

3,370%

1,330%

520%

2,080%

1,070%

1,800%

1,110%

5,040%

5,680%

3,560%

14,310%

6,570%

1,920%

0% 2,000% 4,000% 6,000% 8,000% 10,000% 12,000% 14,000% 16,000%

Agriculture, Forestry, Fishing and Hunting

Mining, Quarrying, and Oil and Gas Extraction

Utilities

Construction

Manufacturing

Wholesale Trade

Retail Trade

Transportation and Warehousing

Information

Finance and Insurance

Real Estate and Rental and Leasing

Professional and Technical Services

Management of Companies and Enterprises

Administrative and Waste Services

Educational Services

Health Care and Social Assistance

Arts, Entertainment, and Recreation

Accommodation and Food Services

Other Services, Except Public Administration

Public Administration

Peak percentage increase in New Hampshire continued claims filed compared to pre-pandemic levels by industry sector

PEAK PERCENTAGE INCREASE IN NEW HAMPSHIRE CONTINUED CLAIMS FILED COMPARED TO PRE-PANDEMIC LEVELS BY INDUSTRY SECTOR

Source: New Hampshire Employment Security, Unemployment Insurance Claim data

ALTERNATIVE MEASURES OF LABOR UNDERUTILIZATION 2015 2016 2017 2018 2019

U-1: persons unemployed 15 weeks or longer, as a percent of the civilian labor forceNew Hampshire 1.3% 1.0% 0.9% 0.9% 0.8%United States 2.3% 2.0% 1.7% 1.4% 1.3%

U-2: job losers and persons who completed temporary jobs, as a percent of the civilian labor forceNew Hampshire 1.9% 1.5% 1.5% 1.2% 1.1%United States 2.6% 2.3% 2.1% 1.8% 1.7%

U-3: total unemployed, as a percent of the civilian labor force (this is the definition used for the official unemployment rate)New Hampshire 3.4% 2.8% 2.8% 2.6% 2.6%United States 5.3% 4.9% 4.4% 3.9% 3.7%

U-4: total unemployed plus discouraged workers, as a percent of the civilian labor force plus discouraged workersNew Hampshire 3.7% 3.0% 2.9% 2.7% 2.7%United States 5.7% 5.2% 4.6% 4.1% 3.9%

U-5: total unemployed, plus discouraged workers, plus all other marginally attached workers, as a percent of the civilian labor force plus all marginally attached workers

New Hampshire 4.2% 3.6% 3.5% 3.0% 3.1%United States 6.4% 5.9% 5.3% 4.8% 4.5%

U-6: total unemployed, plus all marginally attached workers, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all marginally attached workers

New Hampshire 8.0% 6.4% 6.2% 5.6% 5.2%United States 10.4% 9.6% 8.5% 7.7% 7.2%

Source: Bureau of Labor Statistics, Current Population Survey; ELMI Analysis. Last Update 7/29/2020

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau18 | LABOR FORCE & UNEMPLOYMENT

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20193

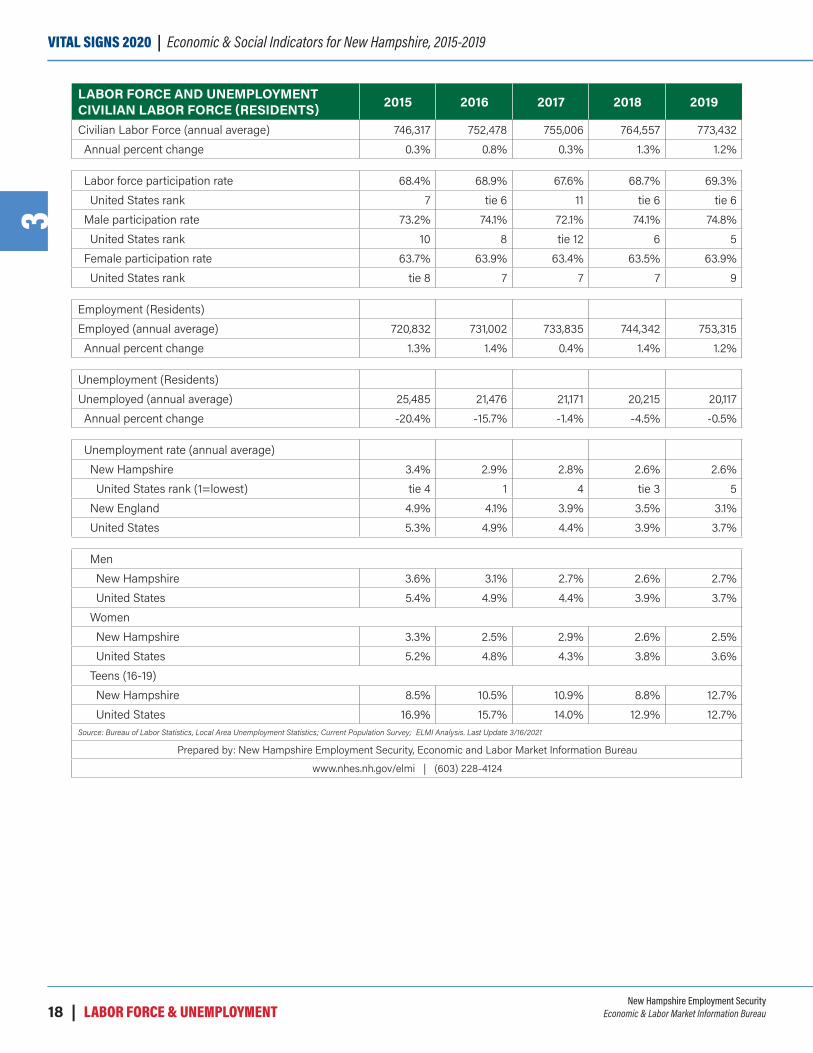

LABOR FORCE AND UNEMPLOYMENT CIVILIAN LABOR FORCE (RESIDENTS) 2015 2016 2017 2018 2019

Civilian Labor Force (annual average) 746,317 752,478 755,006 764,557 773,432Annual percent change 0.3% 0.8% 0.3% 1.3% 1.2%

Labor force participation rate 68.4% 68.9% 67.6% 68.7% 69.3%United States rank 7 tie 6 11 tie 6 tie 6

Male participation rate 73.2% 74.1% 72.1% 74.1% 74.8%United States rank 10 8 tie 12 6 5

Female participation rate 63.7% 63.9% 63.4% 63.5% 63.9%United States rank tie 8 7 7 7 9

Employment (Residents)Employed (annual average) 720,832 731,002 733,835 744,342 753,315Annual percent change 1.3% 1.4% 0.4% 1.4% 1.2%

Unemployment (Residents)Unemployed (annual average) 25,485 21,476 21,171 20,215 20,117Annual percent change -20.4% -15.7% -1.4% -4.5% -0.5%

Unemployment rate (annual average)New Hampshire 3.4% 2.9% 2.8% 2.6% 2.6%United States rank (1=lowest) tie 4 1 4 tie 3 5

New England 4.9% 4.1% 3.9% 3.5% 3.1%United States 5.3% 4.9% 4.4% 3.9% 3.7%

MenNew Hampshire 3.6% 3.1% 2.7% 2.6% 2.7%United States 5.4% 4.9% 4.4% 3.9% 3.7%

WomenNew Hampshire 3.3% 2.5% 2.9% 2.6% 2.5%United States 5.2% 4.8% 4.3% 3.8% 3.6%

Teens (16-19)New Hampshire 8.5% 10.5% 10.9% 8.8% 12.7%United States 16.9% 15.7% 14.0% 12.9% 12.7%

Source: Bureau of Labor Statistics, Local Area Unemployment Statistics; Current Population Survey; ELMI Analysis. Last Update 3/16/2021

Prepared by: New Hampshire Employment Security, Economic and Labor Market Information Bureau

www.nhes.nh.gov/elmi | (603) 228-4124

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau EMPLOYMENT BY INDUSTRY | 19

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20204

1 Data from the Current Employment Statistics (CES) program measure employment by place of work. CES data estimate the number of workers who are employed in New Hampshire, regardless of where they reside, and do not include the self-employed, unpaid family members, or agricultural workers.

2 On an over-the-month basis, changes to employment reflect both changes in economic conditions and seasonal patterns of employment growth and decline. All industries experience seasonal changes to some degree, although these patterns tend to be more obvious in leisure and hospitality; trade, transportation, and utilities and construction. Employment estimates can be seasonally adjusted, to eliminate the part of the over-the-month change attributable to normal seasonal variation and make it possible to observe cyclical and other nonseasonal movements from month to month. For data that has not been seasonally adjusted, the most appropriate method of comparison is to compare the estimates for the same month in different years; this will minimize the effect of seasonal employment patterns on observed changes.

EMPLOYMENT BY INDUSTRYEmployment Growth, 2015 to 2019Average annual nonfarm employment in New Hampshire grew 1.0 percent from 2018 to 2019, slightly faster than the 0.7 percent growth during the previous year.1 Between 2015 and 2019, employment in New Hampshire grew by 4.7 percent, an increase of 30,400 jobs. Employment in the construction sector grew 15.3 percent between 2015 and 2019, faster than any other sector. Construction employment increased by 3,700 jobs. Transportation, warehousing, and utilities and private educational services employment also experienced double-digit growth between 2015 and 2019, growing by 11.7 percent and 12.3 percent, respectively. Transportation, warehousing, and utilities added 1,800 jobs during the period, while educational services added 3,400 jobs.

Employment declined in two sectors between 2015 and 2019. Retail trade employment decreased by 900 jobs, a decrease of 0.9 percent, while information lost 100 jobs, a decrease of 0.8 percent.

95

100

105

110

115

120

100

= 20

15 E

mpl

oym

ent L

evel

Industry Growth Index, 2015 - 2019

Total Non-Farm ConstructionTransportation, Warehousing, and Utilities Educational ServicesRetail Trade Information

INDUSTRY GROWTH INDEX, 2015 – 2019

Source: New Hampshire Employment Security, Current Employment Statistics

Seasonally Adjusted Nonfarm Employment, 20202 After increasing every year since 2011, preliminary nonfarm employment estimates for New Hampshire fell in 2020, as a result of the coronavirus pandemic and efforts to contain it. Employment decreased from 687,200 in January 2020 to 572,600 in April, for a loss of 114,600 jobs. Through December, a total of 66,700 jobs have been recovered.

Eight private industry supersectors also experienced their lowest level of employment in April. Construction employment decreased by 2,900 from January to April, but by December had recovered 2,400 jobs compared to the level in April. Private education and health services lost 800 jobs between August and December, but had still recovered 10,400 of the jobs lost in April. The leisure and hospitality supersector was hit hardest by the pandemic, with 39,200 jobs lost by April. By December, the supersector had recovered 25,000

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau20 | EMPLOYMENT BY INDUSTRY

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20194

jobs. Trade, transportation, and utilities hit a low of 119,100 employed in April, a loss of 20,900 from January. Since May, this supersector recovered 17,600 jobs, primarily in retail trade. Manufacturing employment fell by 6,300 jobs by April, and by December had gained 1,900 of those jobs back. Professional and business services lost 9,700 positions by June. By December, employment in this supersector had increased by 5,100 jobs, but remained 4,300 below the January level. Financial activities suffered a loss of only 700 positions as of April, and had regained 400 of those jobs by December. Other services lost about one-third of its employment as of April, with 9,400 jobs lost. By December, this supersector had recovered 5,700 jobs.

Two supersectors experienced their lowest level of employment after April, as secondary effects of the coronavirus impacted these industries in subsequent months. Employment in the information sector fell to 11,400 jobs in June, 1,000 jobs lower than it had been in January. Employment in information remained at that level for most of the second half of 2020. Government employment decreased 7,600 jobs from January to April, before recovering 4,600 jobs over the next four months.

However, the sector dropped 7,700 jobs between September and December, a total decline of 10,700 since January. The majority of the employment decline was concentrated in state government, which declined by 5,700 jobs.

Not Seasonally Adjusted Nonfarm Employment, 2020Estimates for December 2020 show that total nonfarm employment decreased by 50,800 jobs since December 2019. Employment losses were experienced in all but one supersector over-the-year, professional and business services, which had 600 more positions than in December 2019. Leisure and hospitality experienced the largest decrease, with 15,800 fewer jobs than in December 2019. Trade, transportation, and utilities employment decreased by 4,400, while manufacturing shed 4,600 jobs.

Private education and health services lost 12,300 positions over-the-year, while information employment declined by 1,000. Construction employment decreased by 200 from December 2019 to December 2020, and government employment decreased by 9,300.

- Robert Cote and Greg David

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

Over-the-Year Change in Employment by Industry

Professional and Business Svcs, 0.7%Financial Activi�es, -0.3%Construction, -0.7%Trade, Transporta�on, and Utili�e,s -3.1%Manufacturing , -6.5%Total Nonfarm, -7.3%Information, -8.1%Educa�on and Health Svcs, -9.5%Government, -9.9%Leisure and Hospitality, -22.6%

OVER-THE-YEAR CHANGE IN EMPLOYMENT BY INDUSTRY

Source: New Hampshire Employment Security, Current Employment Statistics

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau EMPLOYMENT BY INDUSTRY | 21

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20204

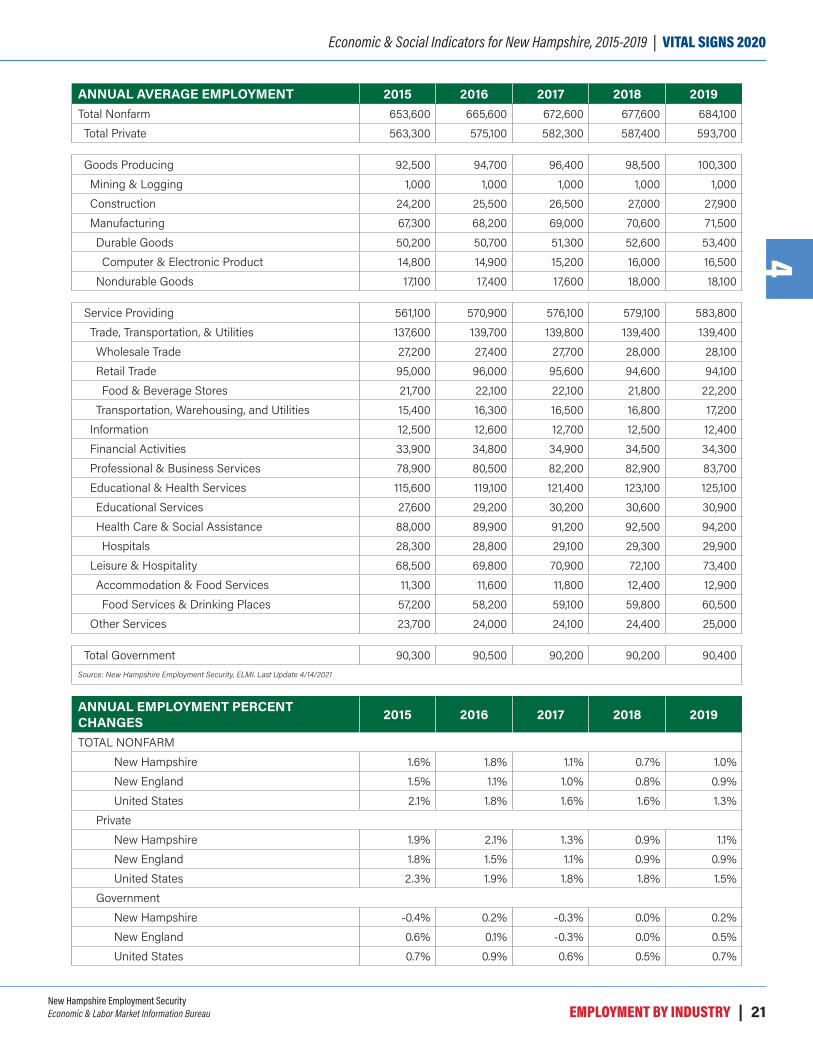

ANNUAL AVERAGE EMPLOYMENT 2015 2016 2017 2018 2019Total Nonfarm 653,600 665,600 672,600 677,600 684,100Total Private 563,300 575,100 582,300 587,400 593,700

Goods Producing 92,500 94,700 96,400 98,500 100,300Mining & Logging 1,000 1,000 1,000 1,000 1,000Construction 24,200 25,500 26,500 27,000 27,900Manufacturing 67,300 68,200 69,000 70,600 71,500Durable Goods 50,200 50,700 51,300 52,600 53,400Computer & Electronic Product 14,800 14,900 15,200 16,000 16,500

Nondurable Goods 17,100 17,400 17,600 18,000 18,100

Service Providing 561,100 570,900 576,100 579,100 583,800Trade, Transportation, & Utilities 137,600 139,700 139,800 139,400 139,400Wholesale Trade 27,200 27,400 27,700 28,000 28,100Retail Trade 95,000 96,000 95,600 94,600 94,100Food & Beverage Stores 21,700 22,100 22,100 21,800 22,200

Transportation, Warehousing, and Utilities 15,400 16,300 16,500 16,800 17,200Information 12,500 12,600 12,700 12,500 12,400Financial Activities 33,900 34,800 34,900 34,500 34,300Professional & Business Services 78,900 80,500 82,200 82,900 83,700Educational & Health Services 115,600 119,100 121,400 123,100 125,100Educational Services 27,600 29,200 30,200 30,600 30,900Health Care & Social Assistance 88,000 89,900 91,200 92,500 94,200Hospitals 28,300 28,800 29,100 29,300 29,900

Leisure & Hospitality 68,500 69,800 70,900 72,100 73,400Accommodation & Food Services 11,300 11,600 11,800 12,400 12,900Food Services & Drinking Places 57,200 58,200 59,100 59,800 60,500

Other Services 23,700 24,000 24,100 24,400 25,000

Total Government 90,300 90,500 90,200 90,200 90,400Source: New Hampshire Employment Security, ELMI. Last Update 4/14/2021

ANNUAL EMPLOYMENT PERCENT CHANGES 2015 2016 2017 2018 2019

TOTAL NONFARMNew Hampshire 1.6% 1.8% 1.1% 0.7% 1.0%New England 1.5% 1.1% 1.0% 0.8% 0.9%United States 2.1% 1.8% 1.6% 1.6% 1.3%

PrivateNew Hampshire 1.9% 2.1% 1.3% 0.9% 1.1%New England 1.8% 1.5% 1.1% 0.9% 0.9%United States 2.3% 1.9% 1.8% 1.8% 1.5%

GovernmentNew Hampshire -0.4% 0.2% -0.3% 0.0% 0.2%New England 0.6% 0.1% -0.3% 0.0% 0.5%United States 0.7% 0.9% 0.6% 0.5% 0.7%

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau22 | EMPLOYMENT BY INDUSTRY

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20194

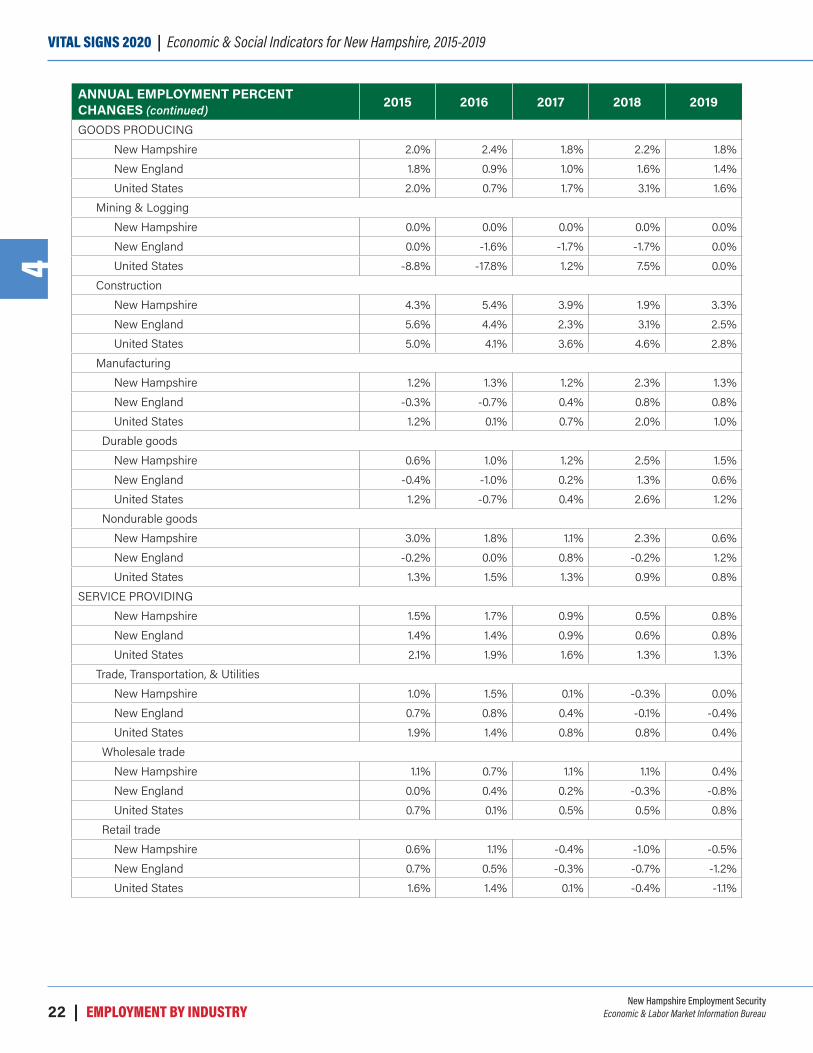

ANNUAL EMPLOYMENT PERCENT CHANGES (continued)

2015 2016 2017 2018 2019

GOODS PRODUCINGNew Hampshire 2.0% 2.4% 1.8% 2.2% 1.8%New England 1.8% 0.9% 1.0% 1.6% 1.4%United States 2.0% 0.7% 1.7% 3.1% 1.6%

Mining & LoggingNew Hampshire 0.0% 0.0% 0.0% 0.0% 0.0%New England 0.0% -1.6% -1.7% -1.7% 0.0%United States -8.8% -17.8% 1.2% 7.5% 0.0%

ConstructionNew Hampshire 4.3% 5.4% 3.9% 1.9% 3.3%New England 5.6% 4.4% 2.3% 3.1% 2.5%United States 5.0% 4.1% 3.6% 4.6% 2.8%

ManufacturingNew Hampshire 1.2% 1.3% 1.2% 2.3% 1.3%New England -0.3% -0.7% 0.4% 0.8% 0.8%United States 1.2% 0.1% 0.7% 2.0% 1.0%

Durable goodsNew Hampshire 0.6% 1.0% 1.2% 2.5% 1.5%New England -0.4% -1.0% 0.2% 1.3% 0.6%United States 1.2% -0.7% 0.4% 2.6% 1.2%

Nondurable goodsNew Hampshire 3.0% 1.8% 1.1% 2.3% 0.6%New England -0.2% 0.0% 0.8% -0.2% 1.2%United States 1.3% 1.5% 1.3% 0.9% 0.8%

SERVICE PROVIDINGNew Hampshire 1.5% 1.7% 0.9% 0.5% 0.8%New England 1.4% 1.4% 0.9% 0.6% 0.8%United States 2.1% 1.9% 1.6% 1.3% 1.3%

Trade, Transportation, & UtilitiesNew Hampshire 1.0% 1.5% 0.1% -0.3% 0.0%New England 0.7% 0.8% 0.4% -0.1% -0.4%United States 1.9% 1.4% 0.8% 0.8% 0.4%

Wholesale tradeNew Hampshire 1.1% 0.7% 1.1% 1.1% 0.4%New England 0.0% 0.4% 0.2% -0.3% -0.8%United States 0.7% 0.1% 0.5% 0.5% 0.8%

Retail tradeNew Hampshire 0.6% 1.1% -0.4% -1.0% -0.5%New England 0.7% 0.5% -0.3% -0.7% -1.2%United States 1.6% 1.4% 0.1% -0.4% -1.1%

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau EMPLOYMENT BY INDUSTRY | 23

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20204

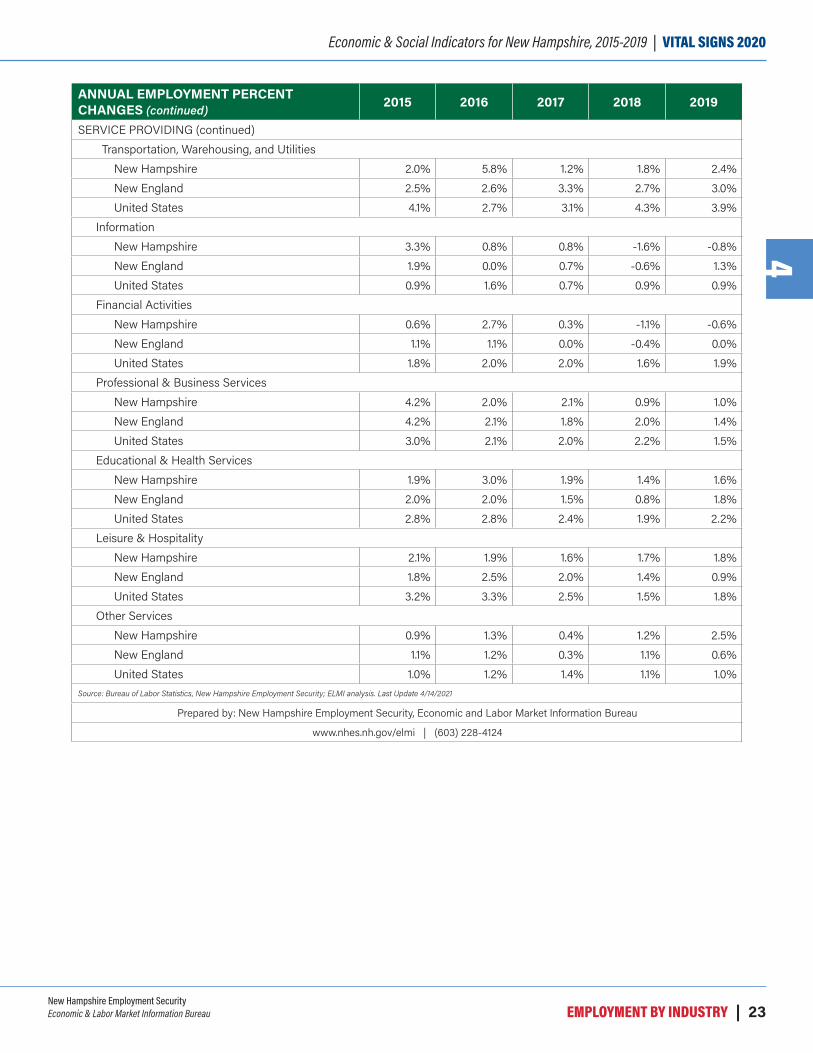

ANNUAL EMPLOYMENT PERCENT CHANGES (continued)

2015 2016 2017 2018 2019

SERVICE PROVIDING (continued)Transportation, Warehousing, and Utilities

New Hampshire 2.0% 5.8% 1.2% 1.8% 2.4%New England 2.5% 2.6% 3.3% 2.7% 3.0%United States 4.1% 2.7% 3.1% 4.3% 3.9%

InformationNew Hampshire 3.3% 0.8% 0.8% -1.6% -0.8%New England 1.9% 0.0% 0.7% -0.6% 1.3%United States 0.9% 1.6% 0.7% 0.9% 0.9%

Financial ActivitiesNew Hampshire 0.6% 2.7% 0.3% -1.1% -0.6%New England 1.1% 1.1% 0.0% -0.4% 0.0%United States 1.8% 2.0% 2.0% 1.6% 1.9%

Professional & Business ServicesNew Hampshire 4.2% 2.0% 2.1% 0.9% 1.0%New England 4.2% 2.1% 1.8% 2.0% 1.4%United States 3.0% 2.1% 2.0% 2.2% 1.5%

Educational & Health ServicesNew Hampshire 1.9% 3.0% 1.9% 1.4% 1.6%New England 2.0% 2.0% 1.5% 0.8% 1.8%United States 2.8% 2.8% 2.4% 1.9% 2.2%

Leisure & HospitalityNew Hampshire 2.1% 1.9% 1.6% 1.7% 1.8%New England 1.8% 2.5% 2.0% 1.4% 0.9%United States 3.2% 3.3% 2.5% 1.5% 1.8%

Other ServicesNew Hampshire 0.9% 1.3% 0.4% 1.2% 2.5%New England 1.1% 1.2% 0.3% 1.1% 0.6%United States 1.0% 1.2% 1.4% 1.1% 1.0%

Source: Bureau of Labor Statistics, New Hampshire Employment Security; ELMI analysis. Last Update 4/14/2021

Prepared by: New Hampshire Employment Security, Economic and Labor Market Information Bureau

www.nhes.nh.gov/elmi | (603) 228-4124

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau24 | OCCUPATIONAL TRENDS

VITAL SIGNS 2020 | Economic & Social Indicators for New Hampshire, 2015-20195

OCCUPATIONAL TRENDS

1 New Hampshire long-term projections designate four categories of potential job outlook based on projected growth and openings, with “Very Favorable” assigned to occupations with the best prospects.

2 U.S. Bureau of Labor Statistics, “Nursing Assistants and Orderlies,” https://www.bls.gov/ooh/healthcare/nursing-assistants.htm#tab-6

Growing Occupations in the 2018 to 2028 ProjectionsOverall, employment in New Hampshire was projected to grow by 5.3 percent from 2018 to 2028, adding more than 37,250 jobs. By itself, that number may be impressive, but is not very useful for many users of projections reports and related products.

Career counselors and students, job seekers and job changers, education and training specialists, and policy specialists are more interested in the details of which occupations are growing and are expected to have the best career prospects in the next ten years. It is also useful to examine the “why” of growth and what causes an increase in demand for particular occupations. Examples of factors causing occupational growth include an aging population, which is a driver in the growth of healthcare and related occupations; change in the relative employment of an occupation, such as the employment of more physician assistants as a lower-cost alternative to physicians; and changes in technology, such as cloud-based applications, which require new expertise.

In looking ahead, it is also useful to look back at the labor force of ten years ago. Some occupations that had few workers in 2008 have experienced significant growth, increasing more than two or threefold. “Trending occupations” are identified as those with an increase of more than 100 percent from 2008 to 2018 and having better-than-average growth for 2018 to 2028.

Another type of occupation to consider is occupations that did not exist in the 2008 occupational classification system. The federal government maintains a Standard Occupational Coding (SOC) system to classify workers for statistical purposes and disseminating data. Detailed occupations are grouped by job duties, skills, and education requirements. The 2018 version of the SOC includes several new occupations, with significant revisions to information technology and healthcare occupations.

Some newly classified occupations have strong potential for employment increases between 2018 and 2028.1 Some of these emerging occupations were classified as part of another occupational code in prior SOC classifications, but are now broken out into a separate SOC code. This action recognizes the changing scope of occupational duties caused by technology, business practices, or changes in demand and consumer behavior.

Trends in Healthcare OccupationsEmployment of nursing assistants is projected to grow by nearly eight percent in New Hampshire between 2018 and 2028, matching the national trend, adding 650 jobs. More nursing assistants will be needed to care for an aging baby-boom population in long-term care facilities, hospitals, and in the homes of care recipients, which is driven by the shift to home and community-based long-term care. Additionally, there will be a need to replace workers that leave the occupation by retiring, returning to school, caring for family, or changing careers. In fact, most of the openings will be for that reason due to the relatively low pay – an average of $16.67 per hour in 2020 – and burnout found in this occupation.2 Entering this occupation requires completion of a state-approved education program and licensure by the New Hampshire Board of Nursing.

Classified in the same SOC code as registered nurses prior to 2010, three occupations were broken out into separate codes as of the 2010 SOC revision: nurse anesthetists, nurse practitioners, and nurse midwives. These occupations are all Advanced Practice Registered Nurses (ARPN), who must attain a registered nurse license, complete a Master’s degree, and meet advanced educational and clinical practice requirements. Licensure from the New Hampshire Board of Nursing is also required, including maintaining a New Hampshire registered nurse license.

New Hampshire Employment SecurityEconomic & Labor Market Information Bureau OCCUPATIONAL TRENDS | 25

Economic & Social Indicators for New Hampshire, 2015-2019 | VITAL SIGNS 20205

3 O*Net Online Summary Report, https://www.onetonline.org/link/summary/29-1171.004 O*Net Online Summary Report, https://www.onetonline.org/link/summary/29-1151.005 O*Net Online Summary Report, https://www.onetonline.org/link/summary/29-1161.00

Nurse practitioners work independently or as part of the healthcare team in hospitals, clinics, and doctor’s offices and may provide primary and specialty healthcare.3 Nurse anesthetists assist anesthesiologists, other physicians or dentists, and may administer anesthesia and oversee patient recovery from anesthesia.4 Nurse midwives specialize in childbirth, diagnosing and coordinating all aspects of the birthing process, either independently or as part of a healthcare team.5 Nurse practitioners are projected to grow by 30 percent over ten years, much faster than the statewide average, driven by their expanded role in primary healthcare. Overall, more than 100 annual openings are projected for 2018 to 2028 for nurse practitioners. Nurse anesthetists, projected to grow by 17 percent, are expected to have 16 job openings annually. Demand for nurse midwives is not

as strong, and although the occupation is expected to grow by 19 percent, only four job openings are projected annually.

Opioid abuse remains a problem in New Hampshire, creating demand for substance abuse, behavioral disorder, and mental health counselors that is much higher than average, with growth of more than 27 percent from 2018 to 2018 projected. Total employment in this occupation is projected to increase by more than 510 jobs through 2028. Demand is expected to continue as states and communities provide treatment and counseling as alternatives to jail time for drug offenders. Treatment programs have been found to be cost-effective and can reduce repeat offenses.6 Workers in this occupation are employed in ambulatory health care services, such as clinics and community health

459

408

2670

769

36

498

377

45

150

681

3965