Embed Size (px)

Citation preview

ModelModel with Exogenous Collateral

Equilibrium

Economia Financiera Avanzada

Jose Fajardo

EBAPE- Fundacao Getulio Vargas

Universidad del Pacıfico, Julio 5–21, 2011

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Default and Bankruptcy in GE Models

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Introduction

The possibility of default creates a need for the introductionof incentives (enforcement mechanisms) for agents to keeptheir promises.It is certainly not possible in practice to devise a strongenough mechanism that ensures that all promises will bekept in all circumstances.It is often the case that this is also not desirableeconomically.In fact, the main effect of such may be indistinguishable asimple restrictions on trade which prevent efficient risksharing.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Default and Bankruptcy in GE Models

Uncertain deliveries on contracts.Penalties: Shubik, M. and Wilson, C. (1977).“The optimalbankruptcy rule in a trading economy using fiat money”, Z.Nationalokon. 37, 337-354.Utility penalties: Dubey, Geanakoplos and Shubik (2005),“Default and Punishment in General Equilibrium”.Econometrica, 73(1), 1–38.Efficiency: Zame, W.R.,(1993), “Efficiency and the role ofdefault when security markets are incomplete”, AmericanEconomic Review 6, 167-196.Collateral seizure: Dubey, Geanakoplos and Zame (1995).“Default, collateral and derivatives”, Yale University, mimeo.Geanakoplos and Zame (2010). “Collateralized AssetMarkets”.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Fundamental Theorem of Asset Pricing with Defaultand Collateral

Fajardo (2005) and Orrillo (2005): Exogenous Collateral.Araujo, Fajardo and Pascoa (2005): EndogenousCollateral.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model Utility Penalties and Collateral

Agents are allowed to default and suffer utility penaltiesAgents need to put collateral when they short salesNo Tranching nor Pyramiding allowedAnonymous Market: Penalties and Collateral

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model Utility Penalties and Collateral

Exchange economy over two periods.Finite number of states s ∈ S = {1,2, ...,S}.H agentsJ assetsL durable goods.In the first period, there is a market where physicalcommodities and assets are traded against each other.In the second period asset returns are delivered.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model

Let θj ≥ 0 be the number of units of asset j the consumerbought.ϕj ≥ 0 be the number of units he sold..Every sale should be backed by a bundle of goods(collateral): Cj ∈ IRL

+ \ {0}.Asset j is defined by the promise of goods Rj ∈ IRL

+ \ {0} itmakes and the collateral backing it: (Rj ,Cj)

The collateral in this model is keep by the borrowers, in thisway they will have utility returns from the use of collateral,this is the case of the Collateralized Mortgage Obligationmarkets (CMO)

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model

ωh = (ωh0 , (ω

h)s∈S) ∈ IRL+ × IRSL

+ , initial endowments ofagent h, such that eh

s 6= 0, ∀s ∈ S⋃{0}.

p = (p0, (ps)s∈S) ∈ 4L−1 ×4SL−1 commodity price systemand π ∈ 4J−1 asset prices.(Rj ,Cj)j∈J are real assets.Y : S 7→ IRL

++ depreciation rates (durability ofgoods):Y (s)Cj is the depreciated bundle of goods. EachCjl in the collateral bundle Cj will produce a depreciatedgood Y l(s)Cjl in the second period.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model

Uh : IRL+ × IRSL

+ → IR is the utility function of agent h.x = (x0, (xs)s∈S) is the consumption plan, x0 and(x1, x2, .., xS) first and second period consumption.λh

sj ∈ IR+ utility penalty for each dollar of default by theborrower h on asset j in state s.dh

j : S 7→ IRL+ true return on asset j in state s. i.e. dh

j (s)bundle to be delivered by agent h on asset j in state s.(Depends on λ)Kj(s) expected bundle to be delivered by each unit of assetj in state s.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Model

Our economy is defined by

E = ((Uh, ωh)h∈H , (R j ,Cj , (λhj )h∈H)j∈J , (Y l )l∈L)

Budget set is given by:

p0(x0 − ωh0) + π(θ − ϕ) + p0

∑j∈J

Cjϕj ≤ 0, (1)

ps(xs−ωhs−Y (s)x0)−

∑j∈J

ϕjps[Y (s)Cj ]−∑j∈J

psKj (s)θj +∑j∈J

psdj (s) ≤ 0, ∀s ∈ S,

(2)

min{R jl (s),Y (s)Cjl} ≤ djl (s), ∀s ∈ S, j ∈ J, l ∈ L. (3)

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Individual Optimization Problem

Each agent h ∈ H face the following problem:

max(x,θ,ϕ,d)∈Bh(p,π,K )

Uh(x0 + Cϕ, x−0)−∑

s

∑j

λhsj

(psR j (s)ϕj − psdj (s)

)+psvs

(4)where

Bh : 4L−1 ×4SL−1 ×4J−1 ×4SJ−1 7→ IRL(S+1)+ × IRJ

+ × IRJ+ × IRSJL

+

is defined by:

Bh(p, π,K ) := {(x , θ, ϕ,d) ∈ IRL(S+1)+ ×IRJ

+×IRJ+×IRSJL

+ : (1), (2) and (3) hold},

this budget set is convex and vs ∈ IRL+ \ {0} is an exogenous market

bundle used to measure disutility in real terms.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Matrix formNow lets use the following matrix form:

P · (x − ωh) ≤[−ΠA

]Ψ,

where P · (x − ωh) =(p0(x0 − ω0), . . . ,pS(xS − ωS)

),

x = (x0, x1 +∑

j dj (1), . . . , xS +∑

j dj (S)),ω = (ω0, ω1 + Y1x0, . . . , ωS + YSx0),Ψ = (θ, ϕ), Π = (π,p0C − π) and

A(D) =

p1K (1) p1Y (1)Cp2K (2) p2Y (2)C· ·· ·pSK (S) pSY (S)C

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Equilibrium

Definition

An equilibrium for E = ((Uh, ωh)h∈H , (Rj ,Cj , (λ

hj )h∈H )j∈J , (Y

l )l∈L) is a price vector (po, p, π) and an

allocation (xh, θh, ϕh, dh)h∈H such that:

1 Allocations (xh, θh, ϕh, dh) maximize utility functions subject to budget set B(po, p, π).

2 Markets clear: ∑H

(xho + Cϕh − ωh

o ) = 0,

∑H

(xhs − ω

hs − Ysxh

o − YsCϕh) = 0, s ∈ S,

∑H

(θh − ϕh) = 0,

3 ∑H

K hj (s)θh

j =∑

H

dhj (s)ϕ

hj in each state s and asset j.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

FTAP with Default and C = 0

Not possible to define arbitrage in micro terms.If agents maximize utilities, arbitrage free prices must exist

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Equilibrium and Efficiency with Default and C = 0

By imposing bounds on arbitrage free prices DGS (2005),prove existence of equilibrium.Moreover, they show numerically that it is possible tocreate a Pareto improvement by allowing agents to default.Drawback λ not observable.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

No Utility Penalties λ = 0

In this model Dj(s) := min{p(s)R j(s),p(s)Y (s)Cj} is the truereturn on asset j in state s.

Our economy is defined by

E = ((Uh, ωh)h∈H , (R j ,Cj)j∈J , (Y l)l∈L)

the budget constraints of each agent are:

p0(x − ωh0) + π(θ − ϕ) + p

∑j∈J

Cjϕj ≤ 0, (5)

p(s)(x(s)−ωh(s)−Y (s)x)−∑j∈J

ϕjp(s)[Y (s)Cj ]−∑j∈J

(θj−ϕj)Dj(s) ≤ 0, ∀s ∈ S.

(6)

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Individual Problem

In this setting each agent h ∈ H face the following problem:

max(x ,x−0,θ,ϕ)∈Bh(p,π)

Uh(x + Cϕ, x−0) (7)

where

Bh : 4L−1 ×4L−1 ×4J−1 7→ IRL+ × IRSL

+ × IRJ+ × IRJ

+

is defined by:

Bh(p, π) := {(x , θ, ϕ) ∈ IRL+×IRSL

+ ×IRJ+×IRJ

+ : (5) and (6) hold},

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Budget Set

P · (x − ωh) ≤[−ΠA(C)

]Ψ,

P · (x − ω) =(p0(x0 − ω0),p(1)(x1 − ω1 − Y1x0), ..,p(S)(xS − ωs − YSx0)),Ψ = (θ, ϕ),Π = (π,pC − π) and

A(C) =

D(1) p(1)Y1C − D(1)D(2) p(2)Y2C − D(2)· ·· ·D(S) p(S)YSC − D(S)

D(s) = (D1(s),D2(s), ..,DJ(s)) is the vector of true returns. πand π − p0C are the vectors of the buy price and the net saleprice, respect.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Arbitrage

Let us start by defining arbitrage opportunities in a nontrivialcontext where p0 >> 0 and p(s) >> 0,∀s.

DefinitionWe say that there exists strong arbitrage opportunities if∃ Ψ ∈ IR2JL

+ such that

ΠΨ < 0 and A(C)Ψ ≥ 0

Definition

We say that Ψ ∈ IR2JL+ is an arbitrage opportunity if it is either a

strong arbitrage or is such ΠΨ = 0 and AΨ > 0. i.e.

ΠΨ ≤ 0 and A(C)Ψ ≥ 0

with at least one strictly inequality.Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

FTAP with Exogenous Collateral

Theorema) There is no strong arbitrage if and only if there exist

β ∈ IRS+ such the inequalities in (8) are satisfied.

b) There is no arbitrage if and only if there exist β ∈ IRS++ such

the inequalities in (8) are satisfied.S∑

s=1

βsDj(s) ≤ πj ≤ (p0 −S∑

s=1

βsp(s)Ys)C j +S∑

s=1

βsDj(s) (8)

Inequality (8) tell us that arbitrage free prices have a spreadthat takes in account the cost of collateral depreciation and thefact that promises can be not fully delivered, sinceDj(s) = p(s)R j(s)− (p(s)R j(s)− p(s)Y (s)C j)+.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof

Construct the following matrix:

A =

D(1) p(1)Y1C − D(1)D(2) p(2)Y2C − D(2)· ·· ·D(S) p(S)YSC − D(S)I 00 I

Where I is the J × J identity matrix and 0 is the J × J null matrix.We can observe that

∃y : Ay ≥ 0⇔ ∃y : Ay ≥ 0 and y ≥ 0.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof

Then absence of strong arbitrage is equivalent to /∃y ∈ IR2J

such that Ay ≥ 0 and Πy < 0. Now by the Farkas’ Lemma it isequivalent to ∃ β = (β1, .., βS+2J) ∈ IRS+2J

+ such that:

A′β = Π,

from here we obtain:

πj =S∑

s=1

βsDj(s)+βS+j and p0Cj−πj =S∑

s=1

βsp(s)YsCj−S∑

s=1

βsDj(s)+βS+J+j ,

(9)since β is positive we obtain the desired inequalities.

In analogous way we obtain (b) using another version ofFarkas’ Lemma (see Luenberger (1969), pag. 167).2

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Remarks

Another consequence of the above Theorem isp0C j − πj ≥ 0∀j ∈ J with strict inequality if C j 6= 0. Observethat pC j = πj creates also arbitrage opportunities sinceeven if p(s)YsC = Dj(s) for every s there would beunbounded utility gains from consumption of C jϕj bychoosing unbounded short sales of asset j .

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Second Part of FTAP

TheoremUnder the assumptions assumed on agents’s utility functions,UMP has a solution only if there are no whether arbitrage orstrong arbitrage on the financial markets. Conversely, if there isno arbitrage, then UMP has a solution.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof(i)⇒(ii) Let the vector (xh, θh, ϕh) be a solution to the optimization problem, then

po(xho − ωh

o) + πθh + (poC − π)ϕh = 0

andps(xh

s − ωhs − Ysxh

o ) ≤ Dsθh + (psYsC − Ds)ϕ

h, s ∈ S

Now, suppose π allows for strong arbitrage opportunities. Then there is an arbitrageportfolio (θ, ϕ) ∈ R2J

+ then, a new portfolio (θ = θh + θ, ϕ = ϕh + ϕ) such that

po(xo − ωho) + πθ + (π − poC)ϕ ≤ 0

andps(xs − ωh

s − Ysxo) ≤ Ds θ + (psYsC − Ds)ϕ, s ∈ S.

As a result,uh(xh

o + Cϕ, xh−o) > uh(xh

o + Cϕh, xh−o)

since uh is strictly increasing with regard to first-period variables, and therefore a

contradiction of the individual optimality of (xh, θh, ϕh). For the case in which π allows

no arbitrage opportunity the argument is the same. 2

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof(ii)⇒ (i) It is sufficient to prove that the budget set at arbitrage-free prices is compact.As this is already closed, it remains to be shown that it is bounded. First, commodityprices are strictly positive, since Uh is strictly increasing. This implies that the set offeasible consumption plans x ∈ RL(S+1)

+ is bounded. In fact, from (4), it follows that

poxo +∑s∈S

βsDsθ +∑s∈S

βs[psYsC − Ds]ϕ ≤ poωho

andpoxo +

∑s∈S

βspsxs ≤∑s∈S

βsps(ωhs + Ysxo)

We now suppose that there is a feasible sequence (θn, ϕn) such that ||(θn, ϕn)|| → ∞. Thus, the sequence 1

||(θn,ϕn)|| (θn, ϕn) is bounded and therefore admits a convergent

subsequence whose limit, say (θ, ϕ), Budget feasibility implies that there exists abounded sequence xn ∈ RL(S+1)

+ such that

po(xno − ωh

o) + πθn + (poC − π)ϕn ≤ 0 (5)

ps(xns − ωh

s − Ysxno ) ≤ Dsθ

n + (psYsC − Ds)ϕn, s ∈ S (6)

Dividing both sides of the previous equalities by ||(θn, ϕh)||, and taking the limit as

n→∞, we obtainJose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof

πθ + (poC − π)ϕ ≤ 0

Dsθ + (psYsC − Ds)ϕ ≥ 0, ∀s ∈ S

with (θ, ϕ) belonging to the unitary sphere of R2J+ . Consider vectors β ∈ RS

++, of Item bof Theorem 1. Multiplying the last equality by βs then summing over s and finally using(4’) we have

πθ + (poC − π)ϕ = 0

Since both terms in the last equality are positive, each one is positive separately aswell. That is,

πθ = 0, (poC − π)ϕ = 0

From remarks of theorem 1 follows that both πj > 0, ∀j and poCj − πj > 0, ∀j. Thus

(θ, ϕ) = (0, 0) contradicting the fact of belonging to the unitary sphere of R2J . Thus,

the budget set is compact and therefore the consumer’s problem has a solution, since

the utility function is continuous. 2

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Equilibrium Existence

TheoremUnder the usual assumptions that utility functions arecontinuous , strongly monotonic and endowments are differentfrom zero. The absence of arbitrage implies the existence ofequilibrium, independent of the way that agents deliver.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Equilibrium Existence

TheoremUnder the usual assumptions that utility functions arecontinuous , strongly monotonic and endowments are differentfrom zero. The absence of arbitrage implies the existence ofequilibrium, independent of the way that agents deliver.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Proof

Basically, absence of arbitrage allow us to obtain endogenousbounds on short sales. As we can see from budget set:

p0x0 + πθ +∑j∈J

(p0Cj − πj)ϕj ≤ p0eh0,

From FTAP for each j ∈ J, p0Cj − πj > 0. Then,

ϕj ≤p0eh

0p0Cj − πj

.

As pointed out by Radner (1972), the failure of existence ofequilibrium is due to discontinuities in the budget set, that canbe avoided by putting bounds on short sales. 2.

Jose Fajardo Economia Financiera Avanzada

ModelModel with Exogenous Collateral

Equilibrium

Efficiency with Collateral

A. Araujo, F. Kubler and S. Schommer, 2011, “RegulatingCollateral Requirements when Markets are Incomplete”.forthcoming JET.Kilenthong, W. T. 2011. “Collateral Premia and RiskSharing under Limited Commitment”. Economic Theory,46, 475-501.Kilenthong, W. T. and R. M. Townsend (2011). “MarketBased, Segregated Exchanges with Default Risk”. WPFajardo, J. (2011). “Constrained Efficiency withEndogenous Collateral”. WP

Jose Fajardo Economia Financiera Avanzada

IntroductionThe model

Numerical examplesConclusion

General equilibrium with collateralScarcity and the efficiency of risk-sharingWelfare effects of regulation

Scarcity and the efficiency of risk-sharing

A key feature of the model is that scarcity and an unequaldistribution of collateralizable durable goods affectsrisk-sharing and welfare.

If the durable good is plentiful, the model is equivalent to astandard Arrow-Debreu model (and competitive equilibriumallocations are Pareto-optimal).

If, on the other hand, the collateralizable durable good isscarce, most assets are not traded in equilibrium and marketsappear to be incomplete.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

General equilibrium with collateralScarcity and the efficiency of risk-sharingWelfare effects of regulation

Can regulation improve welfare?

In the presence of scarcity, a most interesting question iswhether welfare improvements might be achieved throughgovernment regulation.

It is a quantitative question who in the economy gains andwho loses through a regulation of collateral-requirements.

We provide a series of examples, some of them illustrative andsome realistically calibrated, in order to address this question.

The numerical examples illustrate that regulation of marginrequirements generally does not lead to Pareto-improvements.However often a majority of agents would favor a regulationsince it is welfare improving for them.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

General equilibrium with collateralScarcity and the efficiency of risk-sharingWelfare effects of regulation

Subprime regulation

In our model, we can interpret the assets with lowcollateral-requirement as a ‘subprime loan’. In particularthey carry higher interest rates, and tend to be bought byagents who lack collateralizable durable goods in the present.

Should one banish subprime loans?

We find out that restricting trade in the subprime assets tendsto hurt all agents.

This was a robust feature in our numerical investigations ofthe model.

On the other hand, in some cases, both rich and poor agentsgain if only subprime loans can be traded (and markets forprime loans are shut down). However, the middle-class loses ifonly subprime loans can be traded and it is therefore notPareto-improving.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

EconomyUtility maximization problemSome theoretical observations

Economy

We consider a pure exchange economy over two periods t = 0, 1.

s ∈ S = {1, . . . , S} : set of states in period 1;S∗ = S + 1 : set of all states;l ∈ L = {1, 2} : set of commodities or goods;Ys = (0, 1) for each state s : consumption-durability technology;h ∈ H = {1, . . . H} : set of agents;eh ∈ RS∗L

+ : initial endowment of agent h;uh : RS∗L

+ → R : utility function of agent h;j ∈ J = {1, . . . , J} : set of assets;Aj ∈ RSL

+ : promise per unit of asset j of each good l ∈ L in eachstate s ∈ S. We assume that Aj = (1, 0)T in period 1.Cj ∈ RL

+ : borrower collateral requirement.

We will assume that: S = J

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 1: Plentiful collateralizable goods can lead to theArrow-Debreu allocation

Two states in period 1 S∗ = {0, 1, 2};Two agents, H = {1, 2} with utility function of the form:

uh =0.2 log(x1(0)) + 0.8 log(x2(0))

+12

2∑s=1

(0.2 log(x1(s)) + 0.8 log(x2(s)))

Suppose that durable goods is plentiful and endowments are:

e1(0) = (4, 2), e1(1) = (4, 0), e1(2) = (4, 0);e2(0) = (2, 2), e2(1) = (6, 0), e2(2) = (2, 0).

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 1: Plentiful collateralizable goods can lead to theArrow-Debreu allocation

The set {Cj , j ∈ J CC} = {p1(s)/p2(s), s ∈ S} consists ofthe two assets with collateral requirements C1 = 0.1 andC2 = 0.16667.

With two states, these two assets are sufficient to completethe markets.

The crucial point of this example is that each agent has somuch collateralizable goods that collateral constraints are notbinding and agents can trade to the complete marketsallocation.

Agent 1’ portfolio z1j = θ1

j − φ1j is given by z1

1 = 5.2 and

z12 = −4.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 1: Unequal distribution of collateralizable goodsaffects risk-sharing

Now, we assume that endowments are:

e1(0) = (4, 4), e1(1) = (4, 0), e1(2) = (4, 0);e2(0) = (2, 0), e2(1) = (6, 0), e2(2) = (2, 0).

Agent 1’s portfolio is now z11 = 2.667 and z1

2 = 0 and secondperiod risk is not shared at all.

We report welfare numbers in terms of wealth equivalencecompared to the Arrow-Debreu allocation. We computeWRh = exp(uhGEICC−uhAD

2 ).

The welfare rates in this example are:

(WR1,WR2) = (0.9998, 0.9567).

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 2: With scarce collateralizable goods only fewassets are traded

Four states in period 1 S∗ = {0, 1, . . . , 4}.Two agents, H = {1, 2}, each with identical utility,

uh(x) = log(x1(0)) + log(x2(0)) +14

4∑s=1

(log(x1(s)) + log(x2(s)))

We consider a variety of profiles of endowments, differing bydistribution of durable (collateralizable) good in the first period:

e1(0) = (4, η), e1(1) = e1(2) = (1, 0), e1(3) = e1(4) = (2, 0);e2(0) = (1, (1− η)), e2(1) = e2(3) = (1, 0), e2(2) = e2(4) = (2, 0.2).

We consider η ≥ 1/2Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Since we assume identical homothetic utility, spot-prices donot depend on η (distribution of durable good in the firstperiod).

The set {Cj , j ∈ J CC} = {p1(s)/p2(s), s ∈ S} consists ofthe four assets with collateral requirements C1 = 0.5,C2 = 0.4, C3 = 0.333 and C4 = 0.3.

The assets’ payment in the states is defined bymin{p1(s),p2(s)Cj}

p1(s) follows in Table below:

Table: Assets’ payment in the states

Assets state 1 state 2 state 3 state 4

j=1 1 1 1 1j=2 0.8 1 1 1j=3 0.667 0.833 1 1j=4 0.6 0.75 0.9 1

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 2: Only few assets are traded

Table: Portfolio agent 1 for different values η (agent 1’s durable good inthe first period)

η asset 1 asset 2 asset 3 asset 40.95 0 0 0 0.510.85 0 0.15 0 0.620.81 0 0.68 0 00.8 0 0.70 -0.01 00.5 -0.48 1.08 -0.81 0

The only asset traded is the one with the lowest margin requirement.

Asset 2 is traded for risk-sharing in the second period.

Agent 2 has sufficient collateral to sell only asset 2.

Buying asset 3 is a way for the borrower to insure.

Both agents have sufficient collateral to establish short positions.Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 2: How large are the welfare losses?

Table: Welfare rate for distribution of durable good: agent 1 and 2

η Lender (agent 1) Borrower (agent 2)0.95 0.988 0.9330.9 0.989 0.969

0.85 0.991 0.9780.8 0.992 0.982

0.75 0.992 0.9890.5 0.993 0.996

Agent 2 would gain more than 7 percent if he could commit to payback all promises and trade in all assets without holding anycollateral.

Between η = 0.8 and η = 0.5 the welfare losses remain more or lessconstant for agent 1, while there are still substantial improvementsfor agent 2.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 2: Exogenously selecting margin requirements canmake both agents better off?

In this example all agents have identical homothetic utility.

According to the identical homothetic utility Theorem isimpossible to make both agents better off, by exogenouslyselecting margin requirements.

This obviously does not imply, however, that all possiblemargin-requirements are Pareto-ranked.

First we assume η = 0.95, i.e,

e12(0) = 0.95, e22(0) = 0.05

In this case, it seems likely that GEIC equilibrium allocationsare in fact Pareto-ranked.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Figure: Welfare Rate for regulated collateral (η = 0.95)

The highest utility for both agents is with low collateral (redpoint), this is true for all η ≥ 0.88.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

For the case η = 0.85, i.e., e12(0) = 0.85, e22(0) = 0.15 the GEICequilibria are not Pareto-ranked.

Now low collateral is good only lender (red point), this is true forall 0.82 ≤ η ≤ 0.87.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 3: Three agents with heterogeneous utility

The three agents’ endowments are given by:

e1(0) = (4, η), e1(1) = (1, 0), e1(2) = (4, 0), e1(3) = (2, 0);e2(0) = (1, γ), e2(1) = (1, 0), e2(2) = (2, 0), e2(3) = (4, 0);

e3(0) = (2, 1− η − γ), e3(1) = (2, 0.2), e3(2) = (2, 0), e3(3) = (2, 0.2).

We assume that there are S=3 states in the second period;We assume that agents have heterogeneous utility

uh(x) =αh log(x1(0)) + (1− αh) log(x2(0))

+13

3∑s=1

(αh log(x1(s)) + (1− αh) log(x2(s)))

withα1 = 0.7, α2 = 0.77, α3 = 0.625.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 3: Regulating collateral-requirement

Since preferences are heterogeneous, identical homotheticutility Theorem no longer applies;

To investigate this question, we search for GEIRC equilibriathat could be Pareto better;

We examine the case η = 0.8, γ = 0.1, i.e.,

e12(0) = 0.80, e22(0) = 0.10, e32(0) = 0.10

While it is still impossible to Pareto-improve on the GEICCallocation, both agents 2 and 3 can obtain relatively largegains through a regulation.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Figure: Welfare rate for regulated collateral(e12(0) = 0.80, e22(0) = 0.10, e32(0) = 0.10)

0.977

0.978

0.979

0.98

0.981

0.982

0.983

0.984

0.985

0.986

0.962 0.964 0.966 0.968 0.97 0.972 0.974

agen

t 3

agent 2

GEICC

GEIRC1

GEIRC2

GEIRC3

Agents 2 and 3 can obtain gains through a regulation (GEIRC1).Low collateral is good for lender (red point - GEIRC2).

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 4: Calibration to match real world data

We want to investigate the role of sub-prime loans forrisk-sharing as well as who in the economy gains and wholoses through regulation;

We assume that there are 4 types of agents whoseendowments we calibrated to match the income and wealthdistribution in US data;

We interpret endowments in the non-durable as income whileendowments in the durable good are interpreted as wealth;

The estimates on wealth and income distribution in the US for1995 and 2004 follow Di, Z.X. (2007). “Growing Wealth,Inequality, and Housing in the United States.” HarvardUniversity’s Joint Center for Housing Studies W07-1.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

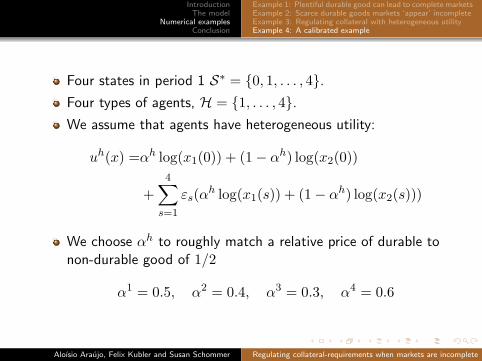

Four states in period 1 S∗ = {0, 1, . . . , 4}.Four types of agents, H = {1, . . . , 4}.We assume that agents have heterogeneous utility:

uh(x) =αh log(x1(0)) + (1− αh) log(x2(0))

+4∑

s=1

εs(αh log(x1(s)) + (1− αh) log(x2(s)))

We choose αh to roughly match a relative price of durable tonon-durable good of 1/2

α1 = 0.5, α2 = 0.4, α3 = 0.3, α4 = 0.6

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

The four agents’ endowments are given by:

e1(0) = (0.61, 0.84), e1(1) = e1(3) = (0.63, 0), e1(2) = e1(4) = (0.21, 0);

e2(0) = (0.22, 0.12), e2(1) = e2(3) = (0.21, 0), e2(2) = e2(4) = (0.63, 0);

e3(0) = (0.12, 0.04), e3(1) = e3(2) = (0.11, 0), e3(3) = e3(4) = (0.05, 0);

e4(0) = (0.05, 0.00), e3(1) = e3(2) = (0.05, 0), e3(3) = e3(4) = (0.11, 0).

Probabilities are given by:

εs = (0.60, 0.18, 0.18, 0.04).

Since preferences are heterogeneous, we search for GEIRCequilibria that could be Pareto better.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

In the GEICC equilibria two assets are traded.GEIRC1 corresponds to the equilibrium where there is fulldefault for all traded assets.GEIRC2 corresponds to the equilibrium with default occurringonly for asset 4 in the states 1 and 3 (i. e. in this economythe sub-prime loans are not available).GEIRC3 corresponds to the equilibrium where all agents totrade in an asset that never defaults.

Table: Portfolios Agents 1, 2, 3 and 4

GEIC Agent 1 Agent 2 Agent 3 Agent 4CC (0,0.37,-0.16,0) (0,-0.24,0.11,0) (0,-0.11,0.05,0) (0,-0.02,0,0)

RC1 (0,0.43,-0.09,0) (0,-0.21,0,0) (0,-0.19,0.09,0) (0,-0.03,0,0)RC2 (0,-0.16,0,0.34) (0,0.11,0,-0.23) (0,0.05,0,-0.10) (0,0,0,-0.01)RC3 (0.11,0.06,0,0) (-0.11,0,0,0) (0,-0.05,0,0) (0,-0.01,0,0)

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

0.9615

0.962

0.9625

0.963

0.9635

0.964

0.9645

0.965

0.9655

0.99718 0.9972 0.99722 0.99724 0.99726 0.99728 0.9973 0.99732

agen

t 2

agent 1

GEICC

GEIRC1

GEIRC2

GEIRC3

In the GEICC equilibria twoassets are traded. The richagent 1 lends in thesub-prime asset (0.37 units)and borrows (0.16 units) inthe safe asset. Agents 2-4borrow exclusively sub-prime,while agents 2 and 3 (themiddle-class) actually savessome money in the safebond.

GEIRC1 corresponds to the equilibrium where there is fulldefault for all traded assets. The rich agent 1 benefits fromlending more units in the subprime asset (0.43 units), due tohigher interest rate, in relation to GEICC equilibrium.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

0.9855

0.986

0.9865

0.987

0.9875

0.988

0.9885

0.9615 0.962 0.9625 0.963 0.9635 0.964 0.9645 0.965 0.9655

agen

t 3

agent 2

GEICC

GEIRC1

GEIRC2

GEIRC3

0.946

0.9462

0.9464

0.9466

0.9468

0.947

0.9472

0.9474

0.99718 0.9972 0.99722 0.99724 0.99726 0.99728 0.9973 0.99732

agen

t 4

agent 1

GEICC

GEIRC1

GEIRC2

GEIRC3

Agents 2 and 3 cannot be made better off through anyregulation (GEICC point).

Agents 1 and 4 gain simultaneously if only subprimeborrowing is allowed (GEIRC1 point).

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 4: Robustness analysis

In order to verify if the previous specification are robust weconsider more specifications for preferences.

In Yao, R. and Zhang, H.H. (2005). “OptimalConsumption and Portfolio Choices with Risky Housing andBorrowing Constraints”. The Review of Financial Studiespreferences over housing and other goods are represented bythe Cobb-Douglas function.

They estimate the housing preference (1− αh) as 0.2 for USin 2001 based on the average proportion of household housingexpenditure according to the Bureau of Labor Statistics (BLS)of the US Department of Labor.

Here we estimate the durable good preference (1− αh) foreach type of agent, based on the proportions of housing,furniture and vehicle purchases according to the BLS for 2004.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Example 1: Plentiful durable good can lead to complete marketsExample 2: Scarce durable goods markets ‘appear’ incompleteExample 3: Regulating collateral with heterogeneous utilityExample 4: A calibrated example

Example 4: Robustness analysis

In this case the preference are:

α1 = 0.74, α2 = 0.73, α3 = 0.72, α4 = 0.71

As in the above example, both agents 1 and 4 can be madebetter off when trade is restricted to be in the sub-prime asset.

The following values for α also give this result:

α1 = 0.7, α2 = 0.6, α3 = 0.5, α4 = 0.4

α1 = 0.4, α2 = 0.3, α3 = 0.5, α4 = 0.7

α1 = 0.5, α2 = 0.4, α3 = 0.3, α4 = 0.2

indicating that what seems to be the most robust case is acase as in the above example.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete

IntroductionThe model

Numerical examplesConclusion

Conclusion

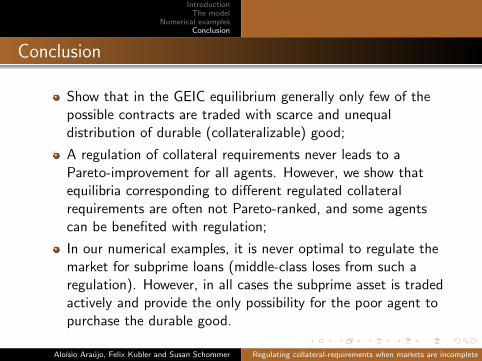

Show that in the GEIC equilibrium generally only few of thepossible contracts are traded with scarce and unequaldistribution of durable (collateralizable) good;

A regulation of collateral requirements never leads to aPareto-improvement for all agents. However, we show thatequilibria corresponding to different regulated collateralrequirements are often not Pareto-ranked, and some agentscan be benefited with regulation;

In our numerical examples, it is never optimal to regulate themarket for subprime loans (middle-class loses from such aregulation). However, in all cases the subprime asset is tradedactively and provide the only possibility for the poor agent topurchase the durable good.

Aloısio Araujo, Felix Kubler and Susan Schommer Regulating collateral-requirements when markets are incomplete