Embed Size (px)

Citation preview

College of Education

School of Continuing and Distance Education 2014/2015 – 2016/2017

ECON 101

Introduction to Economics 1

Session 1 – Introduction I

Lecturer: Mrs. Hellen Seshie-Nasser, Department of Economics Contact Information: [email protected]

Session Overview

• This session introduces the student to Economics as a discipline; focusing on the nature and scope of economics, the economic way of thinking, the method of economics, and the principles that guide economic analysis.

Slide 2 Mrs. Hellen Seshie-Nasser, Dept of Economics, University of Ghana

Session Objectives

• At the end of the session, the student should be able to: – Define economics. – Describe the “economic way of thinking,” including definitions of

rational behaviour, marginal cost, marginal benefits and how these concepts may be used in decision making.

– Identify the three basic economic questions and describe how the market system answers each of these three basic questions.

– identify and explain the factors of production – State some important reasons for studying economics. – Explain how economists use the scientific method to formulate

economic principles. – Differentiate between microeconomics and macroeconomics. – Differentiate between positive and normative economics. – Explain and give examples of some hidden fallacies.

Mrs. Hellen Seshie-Nasser, Dept .of Economics, University of Ghana

Slide 3

Session Outline

The key topics to be covered in the session are as follows:

• Definition of Economics

• The Economic way of thinking

• The Scientific Method

• The Economist as a Policy Advisor

• Common Fallacies in Economics

• Principles of Economics

Slide 4 Mrs. Hellen Seshie-Nasser, Dept of Economics, University of Ghana

Reading List

• Lipsey R. G. and K. A. Chrystal. (2007). Economics. 11th Edition. Oxford University Press.

• Bade R. and M. Parkin. (2009). Foundations of Microeconomics. 4th Edition. Boston: Pearson Education Inc.,

• Begg. D. Fischer S. and R. Dornbusch. (2003). Economics. 7th Edition. McGraw-Hill

Slide 5 Mrs. Hellen Seshie-Nasser, Dept of Economics, University of Ghana

• Adam Smith (1776) – “The Wealth of Nations” defined Economics as, “An enquiry into the nature and causes of wealth of nations”

Some Definitions of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 6

• Alfred Marshal - Economics is the study of mankind in the ordinary business of life. It explains that part of individual and social action that is closely related to the attainment and with the use of material requisite of wellbeing.

Some Definitions of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 7

A.C. Pigou:

• Economics is the means of studying how total production could be increased so that the standard of living of the people might be improved.

Some Definitions of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 8

• Paul Samuelson (Nobel Laurette, 1970) “The study of how man and society end up choosing, with or without the use of money, to employ scarce, productive resources which have alternative uses to produce various commodities and distribute them for consumptions now or in the future among various people and groups in society.

Some Definitions of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 9

Man and society:- Economics broadly divided into two branches; microeconomics and macroeconomics

• Microeconomics focuses on the individual parts of the economy; how individuals, households and firms make decisions and how they interact in specific markets

• Macroeconomics looks at the economy as a whole. It involves economy-wide phenomena, including inflation, unemployment, and economic growth, interest rate, BOP. etc.

Key Emerging Issues: Samuelson’s Definition

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 10

• Choosing: Choice making is a direct result of a fundamental problem of scarcity. As a result of limited resources confronting unlimited wants, society is compelled to make choices among the alternative uses of the resources.

• With or without the use of money: Choices are made with or without the use of money. Example is a Barter system

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Key Emerging Issues - Samuelson’s Definition:

Slide 11

Key Emerging Issues - Samuelson’s Definition

• Choices are made to employ scarce productive resources. It means that resources (land, labour, capital and entrepreneur) are scarce

• Distribution: Production is incomplete if the commodities do not reach the final consumer

• Consumption could be undertaken in the present or in the future. It means that present consumption could be postponed to the future in order to maximize satisfaction

Slide 12 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

• “Economics is the study of how individuals and society in general allocate scarce resources among competing uses to maximize their satisfaction”

Working Definition

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana Slide 13

• Economics trains you to. . . a) Think in terms of alternatives.

b) Evaluate the cost of individual and social choices.

c) Examine and understand how certain events and issues are related.

• The economic way of thinking involves thinking analytically and objectively and makes use of scientific methods.

The Economic Way of thinking

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 14

• The Scientific Method: Observation, Theory, and More Observation.

The economic method:

• Uses abstract models to help explain how a complex real world operates.

• Develops theories, collects, and analyzes data to evaluate the theories.

The Methods of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 15

• What is a model?

– An abstract representation of reality

• Economics relies heavily on modeling

– Economic theories must have a well-constructed model

• While most models are physical constructs

– Economists use words, diagrams, and mathematical statements

The Methods Cont’d.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 16

• Guiding principle of economic model building

– Should be as simple as possible to accomplish its purpose

• Level of detail that would be just right for one purpose will usually be too much or too little for another

• Even complex models are built around a simple framework

The Art of Building Economic Models

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 17

• Economists use models to simplify reality in order to improve our understanding of the world

• Two of the most basic economic models include:

– The Circular Flow Diagram

– The Production Possibilities Frontier

• The Circular-Flow Diagram

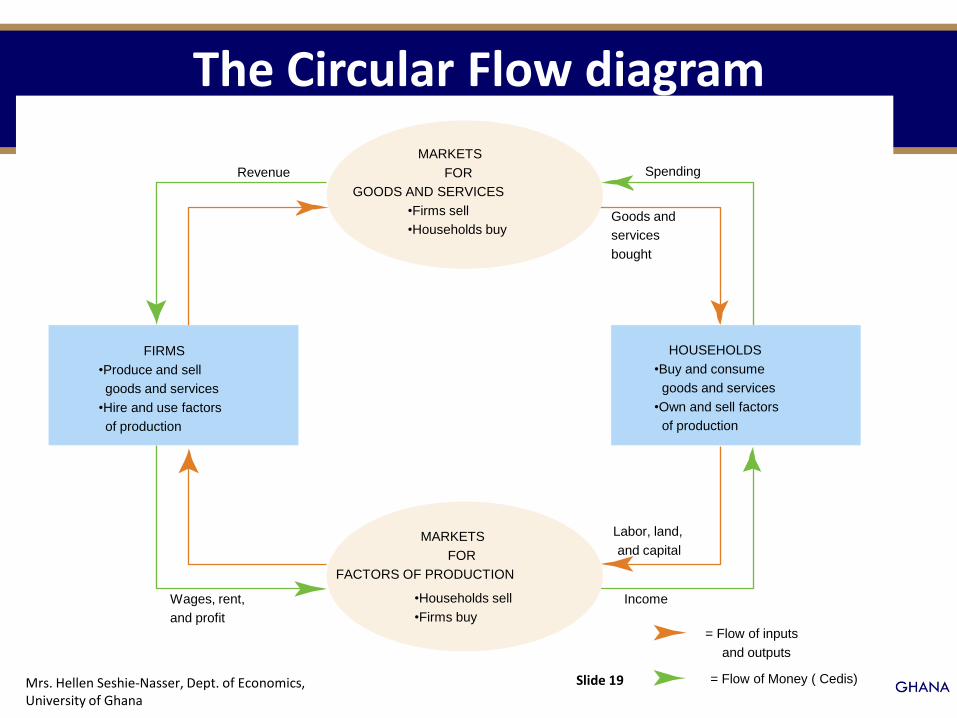

– The circular-flow diagram is a visual model of the economy that shows how money (Cedis) flows through markets between households and firms.

18

Economic Models

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

The Circular Flow diagram

Spending

Goods and

services

bought

Revenue

Labor, land,

and capital

Income

= Flow of inputs

and outputs

= Flow of Money ( Cedis)

Wages, rent,

and profit

FIRMS

•Produce and sell

goods and services

•Hire and use factors

of production

•Buy and consume

goods and services

•Own and sell factors

of production

HOUSEHOLDS

•Households sell

•Firms buy

MARKETS

FOR

FACTORS OF PRODUCTION

•Firms sell

•Households buy

MARKETS

FOR

GOODS AND SERVICES

Slide 19 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Explanation for the Circular Flow

• Firms – Produce and sell goods and services – Hire and use factors of production

• Households – Buy and consume goods and services – Own and sell factors of production

• Markets for Goods and Services – Firms sell – Households buy

• Markets for Factors of Production – Households sell – Firms buy

• Factors of Production – Inputs used to produce goods and services – Land, labour, capital and entrepreneurship

Slide 20 Mrs. Hellen Seshie-Nasser, Dept. of Economics,

University of Ghana

The PPF Model

The Production Possibilities Frontier (PPF) is a graph that shows the combinations of output that the economy can possibly produce given the available factors of production and the available production technology. Concepts illustrated by the Production Possibilities Frontier include;

Efficiency Trade-offs Opportunity Cost Economic Growth

Slide 21 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

• Economists make assumptions in order to make the world easier to understand.

• The art in scientific thinking is deciding which assumptions to make.

• Economists use different assumptions to answer different questions.

The Role of Assumptions

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 22

• Types of assumptions in an economic model

– Simplifying assumptions • Way of making a model simpler without affecting any of its

important conclusions

– Critical assumptions • Affect conclusions of a model in important ways

• If critical assumptions are wrong model will be wrong

• All economic models have one or more critical assumptions

Assumptions and Conclusions

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 23

The economy is complex • Economists make sense of all this activity in two steps

– First, the decision makers in the economy are divided into three broad groups: • Households • Business • Government agencies

– In Microeconomic models • Individual households • Firms • Government agencies

– In Macroeconomic models • Household sector • Business sector • Government sector • Foreign sector

• The next step in understanding the economy is to make two critical assumptions about decision makers

Two Fundamental Assumptions

Slide 24 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

• Every economic decision maker tries to make the best out of any situation – Typically, making the best out of a situation means maximizing

some quantity

– While economists often have spirited disagreements about what is being maximized, there is virtually unanimous agreement that any economic model should begin with the assumption that someone is maximizing something

– The first fundamental assumption seems to imply that we are all engaged in a relentless, conscious pursuit of narrow goals • An implication contradicted by much of human behavior

• In truth, we only rarely make decisions with conscious, hard calculations

• Why, then, do economists assume that people make decisions consciously, when, in reality, they often don’t?

First Fundamental Assumption

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 25

– This is an important question • Economists answer it this way;

– The ultimate purpose of building an economic model is to understand and predict behavior

» The behavior of households, firms, government, and the overall economy

– As long as people behave as if they are maximizing something, then we can build a good model by assuming that they are

– One last thought about the assumption that people maximize

something • It does not imply that people are selfish or that economists think they are

– Economics also recognizes that people often care about their

friends, their neighbors, and the broader society in which whey live

First Fundamental Assumption

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 26

• Every economic decision maker faces constraints – Society’s overall scarcity of resources constrains each of us

individually in much the same way as the overall scarcity of space in a crowded elevator limits each rider’s freedom of movement

– Together, the two fundamental assumptions help define the

approach economists take in answering questions about the world • Economists always begin with the same three questions:

– Who are the individual decision makers? – What are they maximizing? – What constraints do they face?

• This approach is used so heavily by economists that it is one of the basic principles of economics.

Second Fundamental Assumption

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 27

• When economists are trying to explain the world, they are scientists.

• When economists are trying to change the world, they are policy advisors.

The Economist as a Policy Advisor

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 28

• Study of how the economy works, e.g. descriptive analysis

• Positive statements are statements about how the economy works, whether they are true or not. Statements about “what is, was or will be”.

• Accuracy of positive statements can be tested by looking at the facts—and just the facts.

Examples:

Ghana was the fastest growing economy in 2011 with GDP growth rate of 14%.

If government wants to reduce unemployment, ….. is an effective way of doing so.

Positive Economics/Statements

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 29

• Study of what should be. It is also referred to as prescriptive analysis

– It is used to make value judgments, identify problems, and prescribe solutions

– Statements that suggest what we should do about economic facts, are normative statements

• Based on values

Normative statements are statements about how the world should be. Statements about “what ought to be”.

– Normative statements cannot be proved or disproved by the facts alone

Normative Economics/Statements

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 30

These types of statements depend on value judgement about what is good and bad.

• They are informed by philosophical, cultural and religious positions

• E.g. Work hard to reduce the high incidence of unemployment in the country.

Positive or Normative?

Slide 31 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

– An increase in the minimum wage will cause a decrease in employment among the least-skilled.

– Higher government budget deficits will cause interest rates to increase.

– The income gains from a higher minimum wage are worth more than any slight reductions in employment.

– State governments should be allowed to collect from tobacco companies the costs of treating smoking-related illnesses among the poor.

Positive or Normative?

?

?

? Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 32

• Fallacies are errors made in the course of making an argument. Three possible fallacies are usually committed in economic arguments, namely;

• Fallacy of composition: If something that is true for an individual economically is assumed to be true for the whole economy.

• E.g. Employment to economics graduates does not mean employment to all graduates.

Fallacies of Composition and Division

Slide 33 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

• Fallacy of division: If something valid for the whole is assumed to be valid for the individual parts. For example, increased employment in an economy does not mean no individual is unemployed. A fall in inflation does not mean prices of all goods have experienced a fall in the rate of rise.

• Post-hoc fallacy: This fallacy occurs if an argument is made that because one-event follows the other there is a cause-and-effect relationship between the two events. E.g. anytime a budget is read, prices of goods rise. The act of reading a budget may have nothing to do with prices. There may or may not be increase in taxes in the budget.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 34

• In some cases, the disagreement may be positive in nature because

– Our knowledge of the economy is imperfect

– Certain facts are in dispute

• In most cases, the disagreement is normative in nature because

– While the facts may not be in dispute

• Differing values of economists lead them to dissimilar conclusions about what should be done

Why Economists Disagree

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 35

Ten Basic Principles of Economics

Principles of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana Slide 36

1. “There is no such thing as a free lunch”

– To get one thing, we usually have to give up

another thing. Making decisions require

trading off one goal against another.

2. The cost of something is what you give up to get it

– Decision requires comparing costs (opportunity cost) and benefits of alternatives. E.g. Microsoft CEO, Bill Gates gave up college to start his own Software company.

Principles of Economics

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 37

3. Rational people think at the marginal

– Marginal changes are small, incremental changes to an existing plan of action. People make decisions by comparing costs and benefits at the margin.

4. People respond to incentives

– Marginal changes in costs or benefits motivate people to respond. The decision to choose one alternative over the other occurs when the alternative’s marginal benefits exceed its marginal costs.

Principles Cont’d.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 38

5. Trade can make everyone better off – People gain from their ability to trade with

one another. Competition results in gains from trading

– Trade allows people to specialize in what they do best.

6. Markets are usually a good way to organize economic activity

– Households decide what they want

to buy. Firms decide who to hire and

what to produce

– Prices get decision makers to reach

outcomes that tend to maximize the

welfare of society as a whole.

Principles Cont’d.

Slide 39 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

7. Government can sometimes improve market

outcomes

– Market failure occurs when the market fails to allocate

resources efficiently.

– Government can intervene to promote efficiency and equity when the market fails or break down.

– Market failure may be caused by an externality or market power.

Principles Cont’d.

Slide 40 Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

8. The standard of living depends on a country’s production

• Standard of living may be measured in different ways:

• By comparing personal incomes

• By comparing the total market value of a nation’s production

• Most of the variations in living standards of countries are explained by differences in countries’ productivities.

Principles Cont’d.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 41

9. Prices rise when the government prints too much money.

• Inflation is an increase in the overall level of prices in the economy.

• Growth of money is one of the causes of inflation.

• The value of money falls when the government creates large quantities of money.

Principles Cont’d.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 42

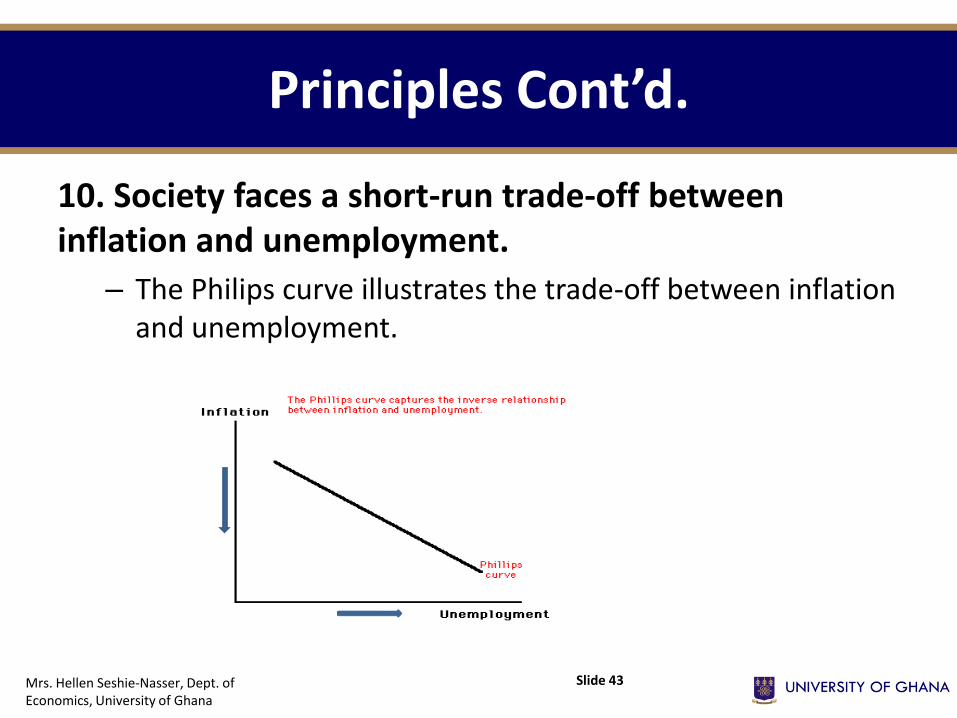

10. Society faces a short-run trade-off between inflation and unemployment.

– The Philips curve illustrates the trade-off between inflation and unemployment.

Principles Cont’d.

Mrs. Hellen Seshie-Nasser, Dept. of Economics, University of Ghana

Slide 43