Embed Size (px)

Citation preview

© 2013 Eaton. All rights reserved.

Eaton Investor Update September 2013

2 © 2013 Eaton. All rights reserved.

Forward-looking statements and non-GAAP financial information

The information provided today will include forward-looking statements relating to our goals and estimates for future years, including statements about expected sales, acquisition synergies, operating earnings per share, cash flow, segment margins, our worldwide markets, our anticipated effective income tax rate, the tax treatment of our dividends and others. These statements should be used with caution and are subject to various risks and uncertainties, many of which are outside the company’s control. The following factors could cause actual results to differ materially from those in the forward-looking statements: unanticipated changes in the markets for the company’s business segments; unanticipated downturns in business relationships with customers or their purchases from us; competitive pressures on sales and pricing; increases in the cost of material and other production costs, or unexpected costs that cannot be recouped in product pricing; the introduction of competing technologies; unexpected technical or marketing difficulties; unexpected claims, charges, litigation or dispute resolutions; the impact of acquisitions and divestitures; unanticipated difficulties integrating acquisitions or realizing expected synergies from the Cooper acquisition; new laws and governmental regulations; interest rate changes; changes in currency exchange rates; stock market fluctuations; and unanticipated deterioration of economic and financial conditions in the United States and around the world. We do not assume any obligation to update these forward-looking statements. This presentation includes certain non-GAAP measures as defined by SEC rules. A reconciliation of those measures to the most directly comparable GAAP equivalent is provided in the investor relations section of our website at www.eaton.com and is contained in your packet.

3 © 2013 Eaton. All rights reserved.

Eaton – A Power Management Company

• A balanced power management company • Cooper acquisition transforms the Electrical

Sector

• Creating consistent and profitable growth across our Industrial Sector

• Summary and guidance

4 © 2013 Eaton. All rights reserved.

Eaton is a global leader in power management

Uniquely positioned to provide safe, reliable, efficient and sustainable power management solutions for our global customers

Electrical Fluid Mechanical

Cities & Buildings

Industrial & Machinery

Information Technology

Energy & Utilities

Transportation Infrastructure

5 © 2013 Eaton. All rights reserved.

Our targeted mix shift has resulted in exposure to high-growth markets and powerful megatrends

60…Percentage increase in global demand for energy in buildings projected by 2050

600…Percentage increase in the global LED lighting market projected by 2020, a CAGR of ~25%

70…Percentage increase in food production by 2050 necessary to feed a global population of 9.1 billion people

150…Percentage increase in annual distances travelled by commercial aviation expected by 2030

25…Percentage increase in fuel economy necessary by model year 2018 to meet the first ever U.S. emissions standards for heavy-duty trucks

70…Percentage increase in liquid petroleum demand in Non-OECD nations expected by 2040

6 © 2013 Eaton. All rights reserved.

In 2012, we completed the transformational acquisition of Cooper Industries

Grows the global scale of our electrical business

Improves our breadth of products with virtually no overlap

Increases leverage to global megatrends: energy efficiency, utility grid upgrade, industrial safety

Brings our overall portfolio to $21.8 B in revenue, based on combined 2012 revenues

Combined company has 102,000 employees with sales in 175 countries

Founded 1833

2012 Sales $5.9 B

29,000 Employees

Manufacturing in 23 countries

Sales in over 100 countries

7 © 2013 Eaton. All rights reserved.

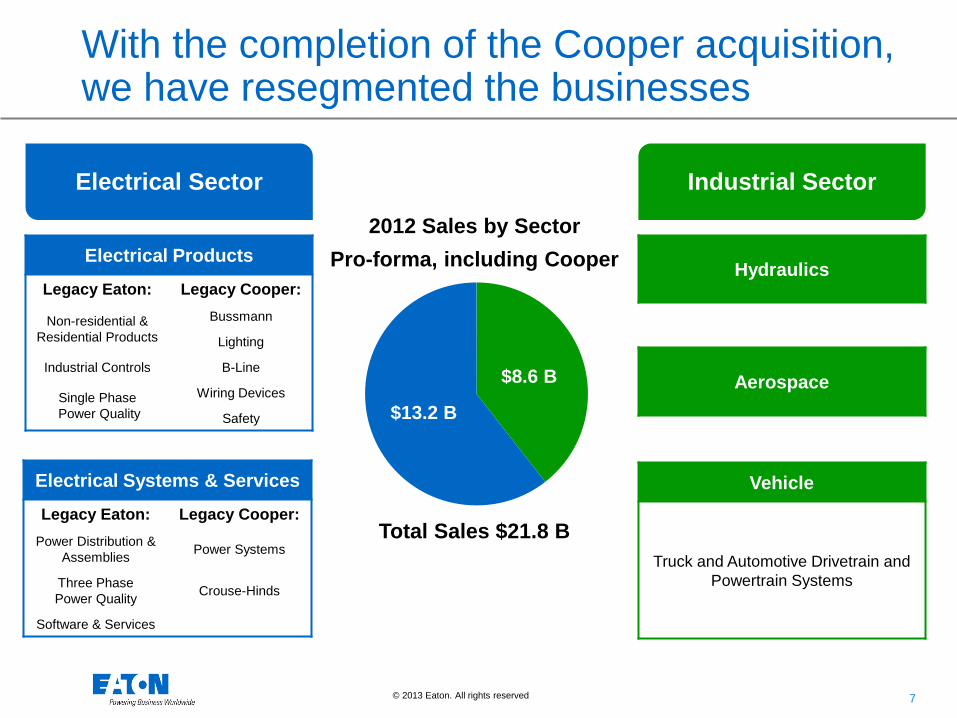

$8.6 B

$13.2 B

With the completion of the Cooper acquisition, we have resegmented the businesses

Industrial Sector Electrical Sector

2012 Sales by Sector Pro-forma, including Cooper Electrical Products

Legacy Eaton: Legacy Cooper:

Non-residential & Residential Products

Bussmann

Lighting

Industrial Controls B-Line

Single Phase Power Quality

Wiring Devices

Safety

Electrical Systems & Services

Legacy Eaton: Legacy Cooper: Power Distribution &

Assemblies Power Systems

Three Phase Power Quality Crouse-Hinds

Software & Services

Hydraulics

Aerospace

Total Sales $21.8 B

Vehicle

Truck and Automotive Drivetrain and Powertrain Systems

8 © 2013 Eaton. All rights reserved.

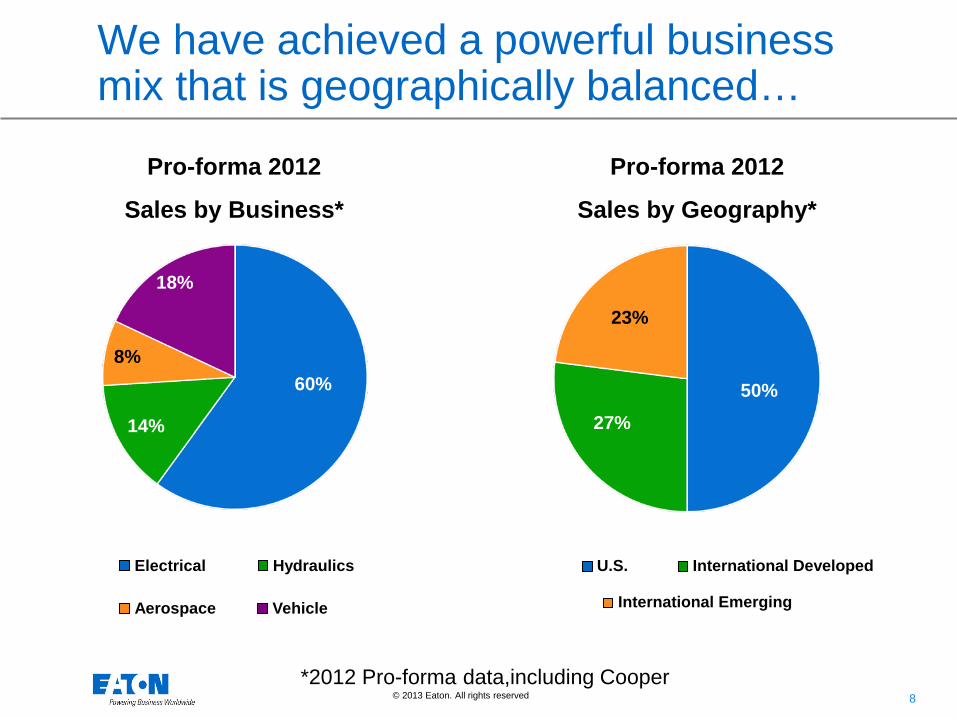

60%

14%

8%

18%

We have achieved a powerful business mix that is geographically balanced…

Pro-forma 2012

Sales by Business*

Electrical Hydraulics

Aerospace Vehicle

International Developed U.S.

International Emerging

50% 27%

23%

Pro-forma 2012

Sales by Geography*

*2012 Pro-forma data,including Cooper

9 © 2013 Eaton. All rights reserved.

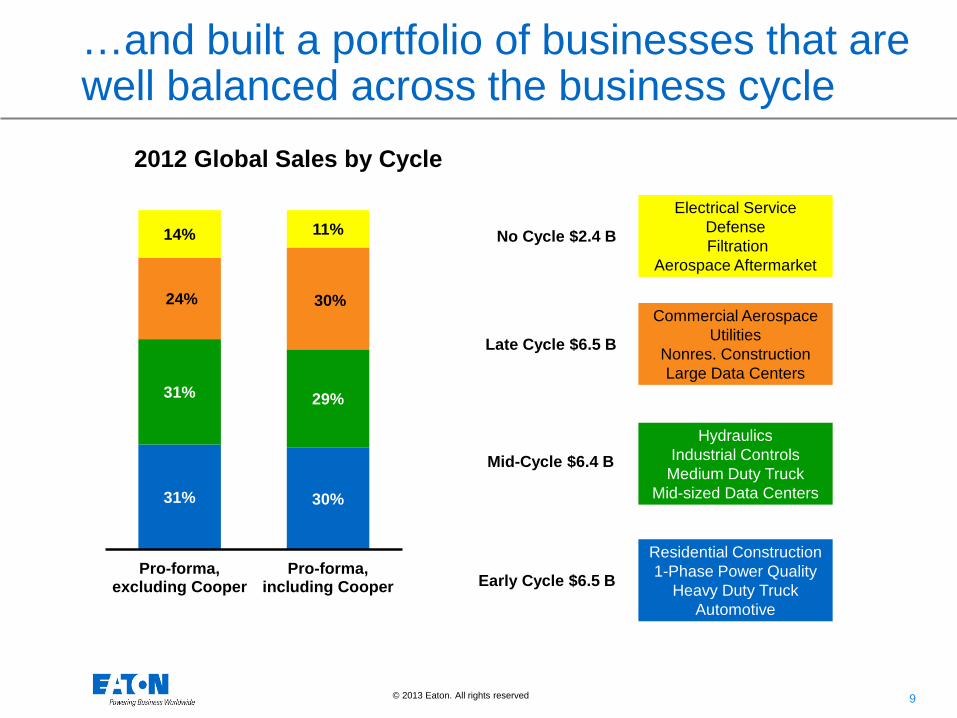

…and built a portfolio of businesses that are well balanced across the business cycle

Electrical Service Defense Filtration

Aerospace Aftermarket

Commercial Aerospace Utilities

Nonres. Construction Large Data Centers

Hydraulics Industrial Controls

Medium Duty Truck Mid-sized Data Centers

Residential Construction 1-Phase Power Quality

Heavy Duty Truck Automotive

Early Cycle $6.5 B

Mid-Cycle $6.4 B

Late Cycle $6.5 B

No Cycle $2.4 B

2012 Global Sales by Cycle

31% 30%

31% 29%

24% 30%

14% 11%

Pro-forma,excluding Cooper

Pro-forma,including Cooper

10 © 2013 Eaton. All rights reserved.

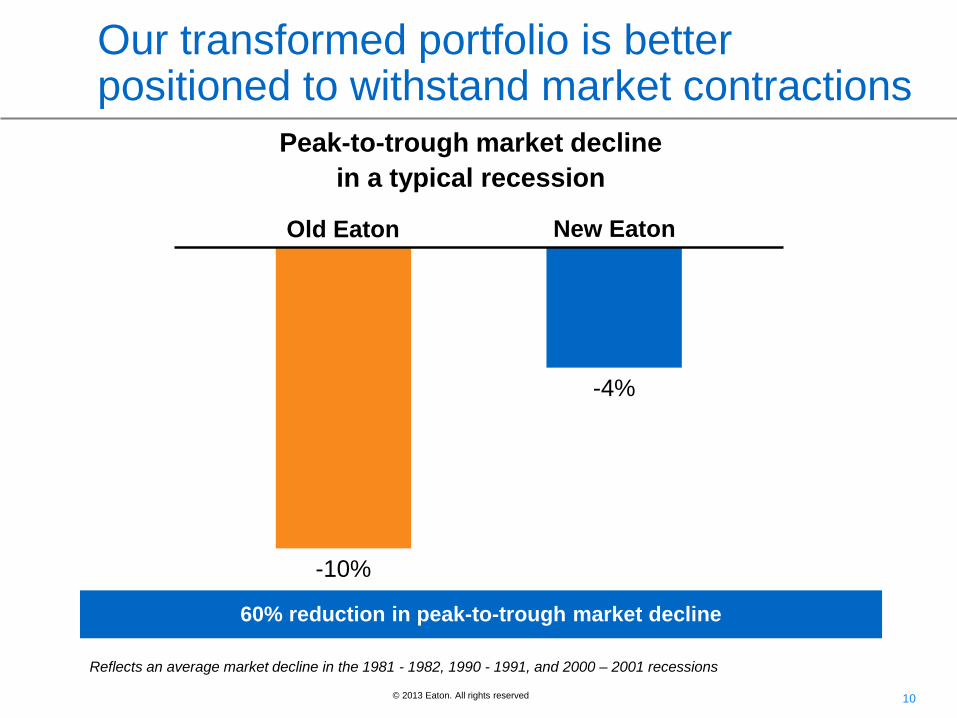

Our transformed portfolio is better positioned to withstand market contractions

60% reduction in peak-to-trough market decline

-10%

-4%

Old Eaton New Eaton

Peak-to-trough market decline in a typical recession

Reflects an average market decline in the 1981 - 1982, 1990 - 1991, and 2000 – 2001 recessions

11 © 2013 Eaton. All rights reserved.

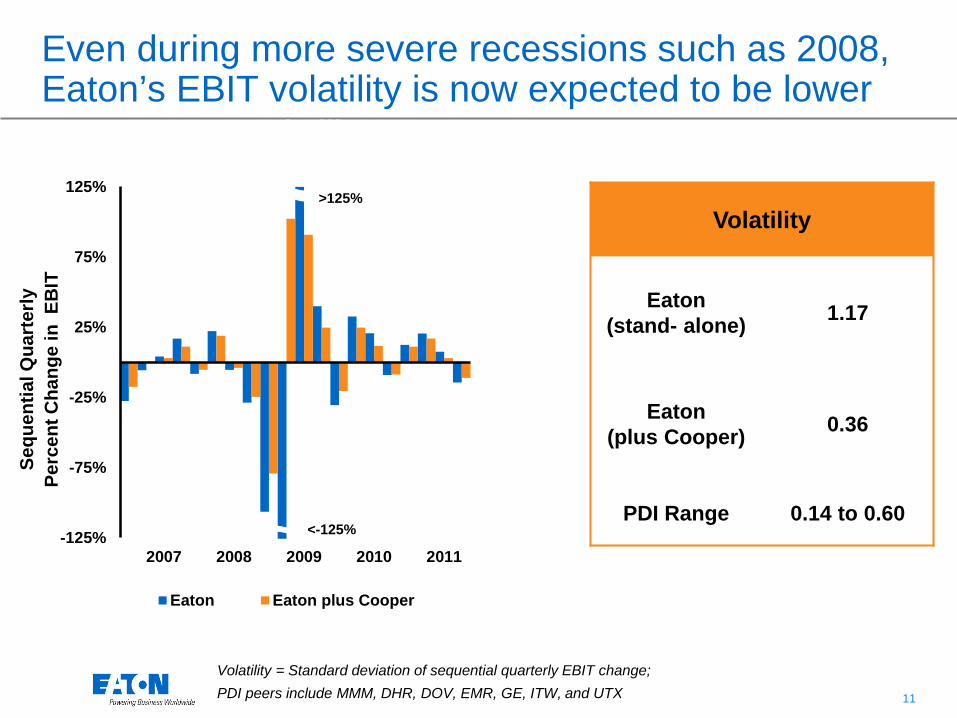

-125%

-75%

-25%

25%

75%

125%

2007 2008 2009 2010 2011

EBIT Volatility 2007 - 2011

Eaton Eaton plus Cooper

Even during more severe recessions such as 2008, Eaton’s EBIT volatility is now expected to be lower

Sequ

entia

l Qua

rter

ly

Perc

ent C

hang

e in

EB

IT

>125%

<-125%

Volatility

Eaton (stand- alone) 1.17

Eaton (plus Cooper) 0.36

PDI Range 0.14 to 0.60

Volatility = Standard deviation of sequential quarterly EBIT change; PDI peers include MMM, DHR, DOV, EMR, GE, ITW, and UTX

12 © 2013 Eaton. All rights reserved.

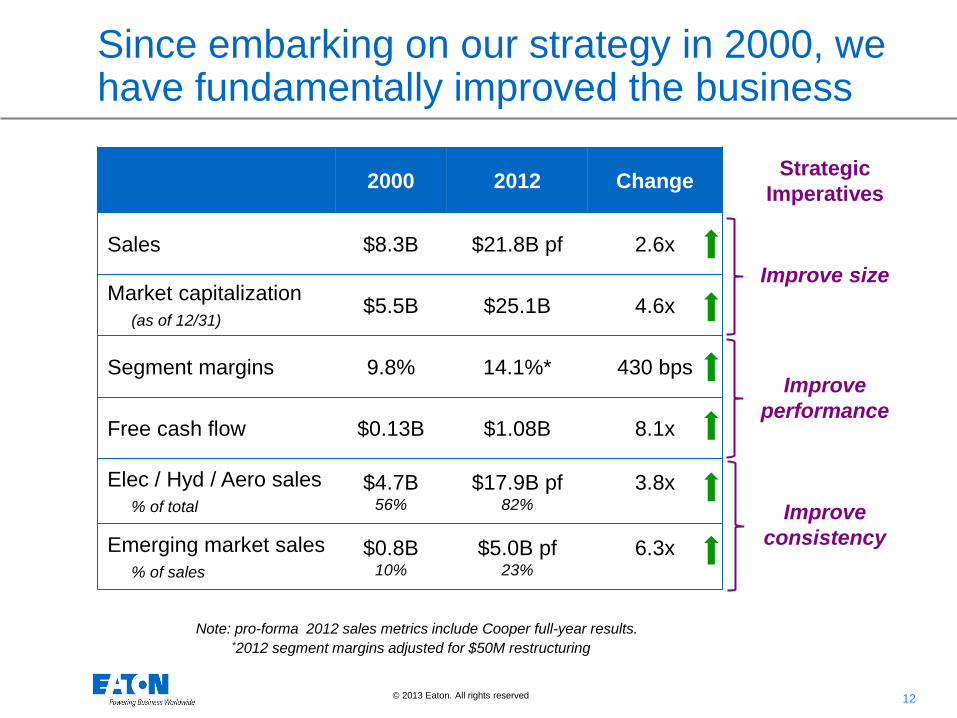

Since embarking on our strategy in 2000, we have fundamentally improved the business

2000 2012 Change Strategic Imperatives

Sales $8.3B $21.8B pf 2.6x Improve size

Market capitalization (as of 12/31)

$5.5B $25.1B 4.6x

Segment margins 9.8% 14.1%* 430 bps Improve

performance Free cash flow $0.13B $1.08B 8.1x

Elec / Hyd / Aero sales % of total

$4.7B 56%

$17.9B pf 82%

3.8x a Improve

consistency Emerging market sales % of sales

$0.8B 10%

$5.0B pf 23%

6.3x

Note: pro-forma 2012 sales metrics include Cooper full-year results. *2012 segment margins adjusted for $50M restructuring

13 © 2013 Eaton. All rights reserved.

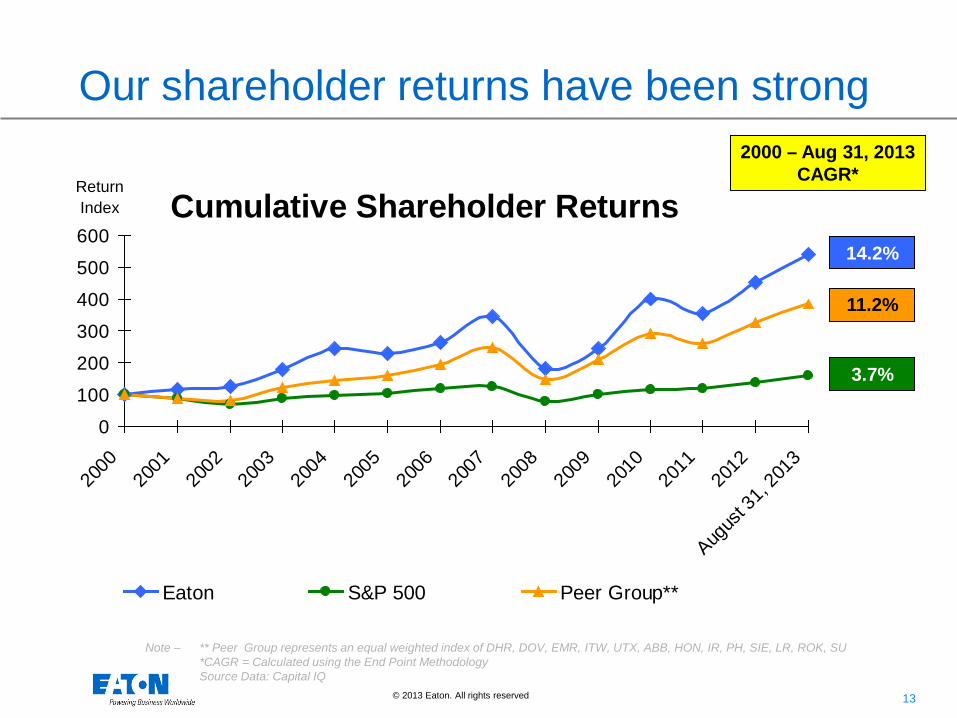

Cumulative Shareholder Returns

0

100

200

300

400

500

600

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Augus

t 31,

2013

Eaton S&P 500 Peer Group**

2000 – Aug 31, 2013 CAGR*

Return Index

14.2%

11.2%

3.7%

Note – ** Peer Group represents an equal weighted index of DHR, DOV, EMR, ITW, UTX, ABB, HON, IR, PH, SIE, LR, ROK, SU *CAGR = Calculated using the End Point Methodology Source Data: Capital IQ

Our shareholder returns have been strong

14 © 2013 Eaton. All rights reserved.

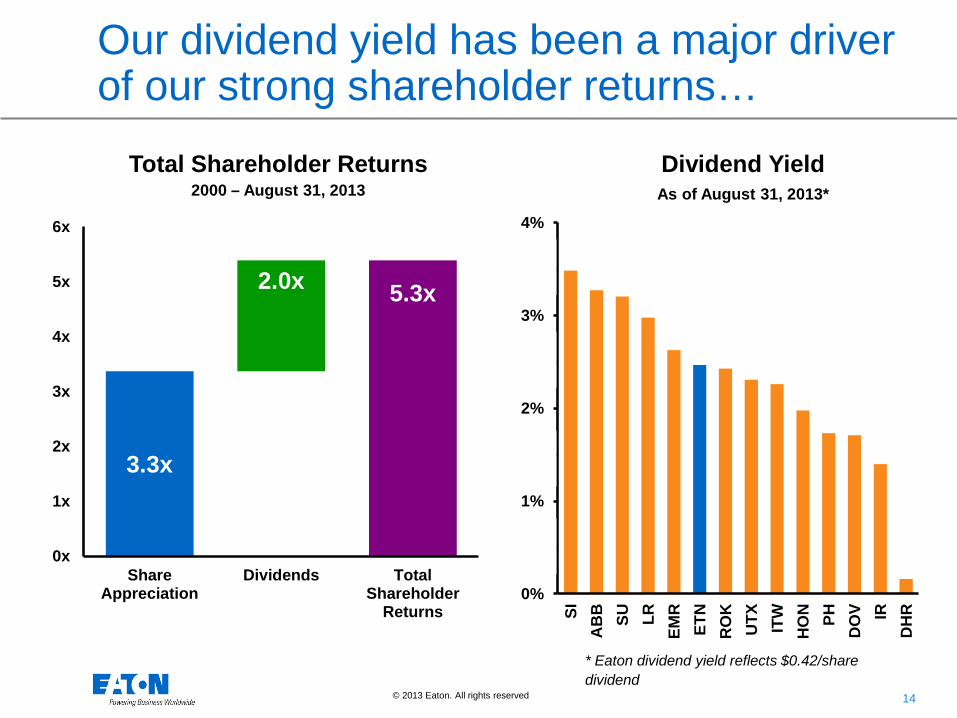

Our dividend yield has been a major driver of our strong shareholder returns…

Total Shareholder Returns 2000 – August 31, 2013

3.3x

5.3x 2.0x

0x

1x

2x

3x

4x

5x

6x

ShareAppreciation

Dividends TotalShareholder

Returns0%

1%

1%

2%

2%

3%

3%

4%

4%

SIA

BB SU LR

EMR

ETN

RO

KU

TX ITW

HO

N PHD

OV IR

DH

R

Dividend Yield As of August 31, 2013*

* Eaton dividend yield reflects $0.42/share dividend

15 © 2013 Eaton. All rights reserved.

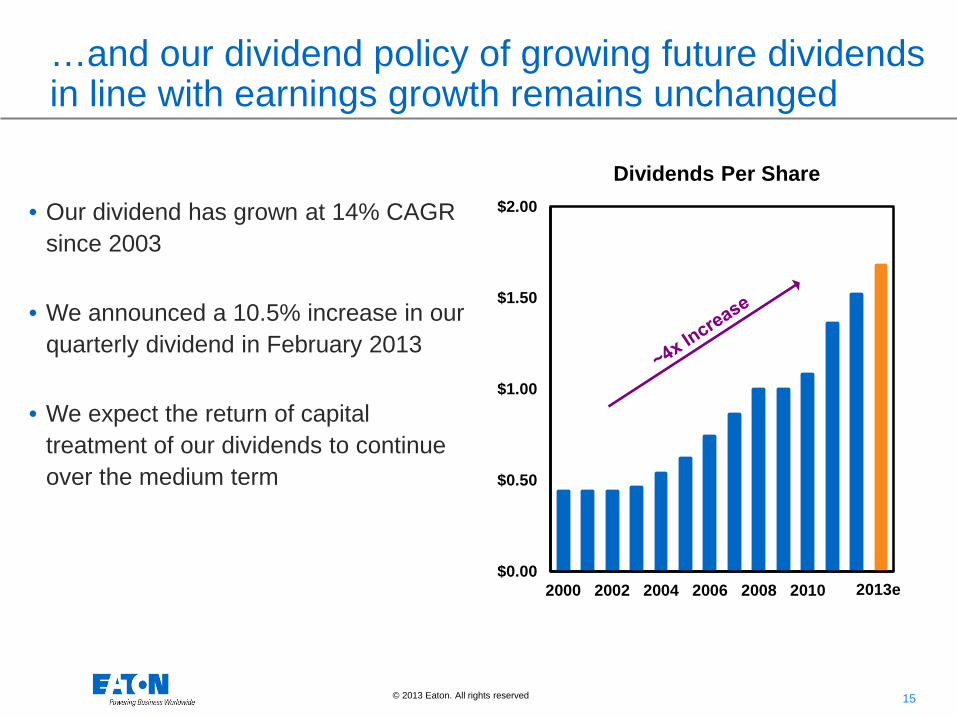

…and our dividend policy of growing future dividends in line with earnings growth remains unchanged

$0.00

$0.50

$1.00

$1.50

$2.00

2000 2002 2004 2006 2008 2010 2012

Dividends Per Share

2013e

• Our dividend has grown at 14% CAGR since 2003

• We announced a 10.5% increase in our quarterly dividend in February 2013

• We expect the return of capital treatment of our dividends to continue over the medium term

16 © 2013 Eaton. All rights reserved.

Eaton – A Power Management Company

• A balanced power management company • Cooper acquisition transforms the Electrical

Sector

• Creating consistent and profitable growth across our Industrial Sector

• Summary and guidance

17 © 2013 Eaton. All rights reserved.

The acquisition of Cooper is transformational for our business

• Largest acquisition in Eaton’s 102-year history

• Broad set of complementary electrical products and solutions • Significant synergies with little overlap

• Expansion across the entire power system • Upstream into power solutions encompassing primary and

secondary distribution, grid automation and smart grid • Downstream into lighting, lighting controls and wiring devices

* Cooper 2012 results on a stand-alone basis

18 © 2013 Eaton. All rights reserved.

Cooper has a wide range of complementary electrical businesses

Power Systems

• Distribution grid protection & automation

Crouse-Hinds • Global leader in

electrical solutions for harsh & hazardous environments

Safety

• Leading European provider of emergency lighting, notification & video security

Lighting

• Broad lighting packages for indoor & outdoor use

Bussmann

• Global leader in circuit protection

B-Line • Global provider of

structural systems & wire management solutions

Wiring Devices • Electrical devices for

commercial & residential power distribution

19 © 2013 Eaton. All rights reserved.

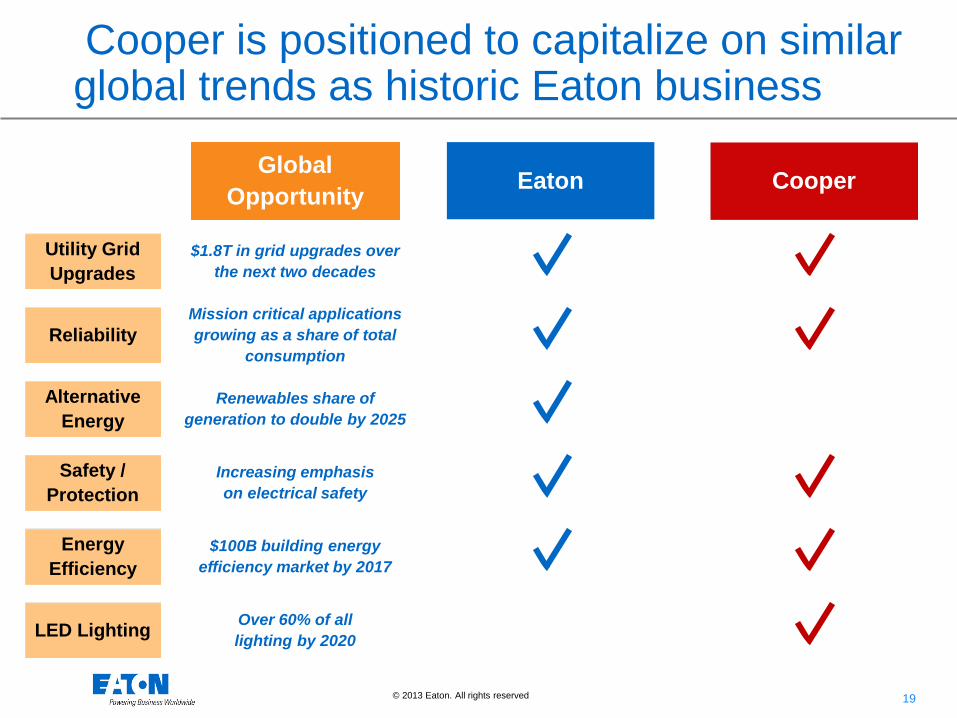

Cooper is positioned to capitalize on similar global trends as historic Eaton business

Utility Grid Upgrades

LED Lighting

Alternative Energy

Safety / Protection

Energy Efficiency

$1.8T in grid upgrades over the next two decades

Over 60% of all lighting by 2020

Renewables share of generation to double by 2025

Increasing emphasis on electrical safety

$100B building energy efficiency market by 2017

Cooper

Reliability Mission critical applications growing as a share of total

consumption

Global Opportunity Eaton

20 © 2013 Eaton. All rights reserved.

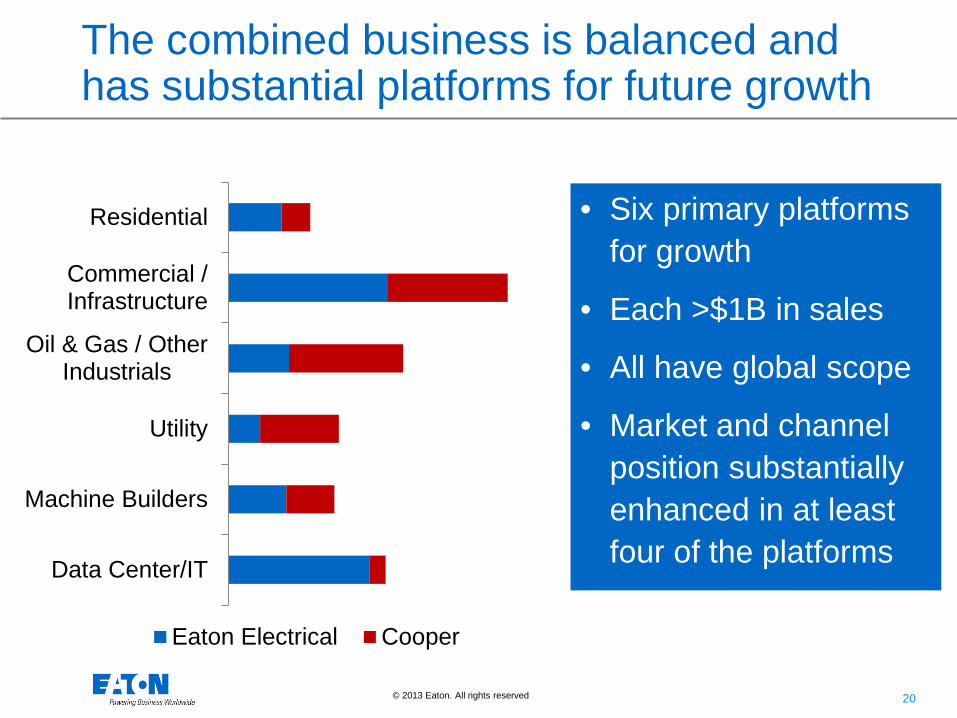

The combined business is balanced and has substantial platforms for future growth

Data Center/IT

Machine Builders

Utility

Oil & Gas / OtherIndustrials

Commercial /Infrastructure

Residential

Eaton Electrical Cooper

• Six primary platforms for growth

• Each >$1B in sales

• All have global scope

• Market and channel position substantially enhanced in at least four of the platforms

21 © 2013 Eaton. All rights reserved.

Our expanded capabilities position us to provide solutions across a broad range of end markets

Legacy Eaton

Legacy Cooper

Power Distribution & Circuit Protection

Backup Power

Protection

Control & Automation

Structural Solutions &

Wiring Devices

Engineering Services

Solutions for Harsh & Hazardous

Environments

Lighting & Security

Power Distribution & Circuit Protection

Data Centers

22 © 2013 Eaton. All rights reserved.

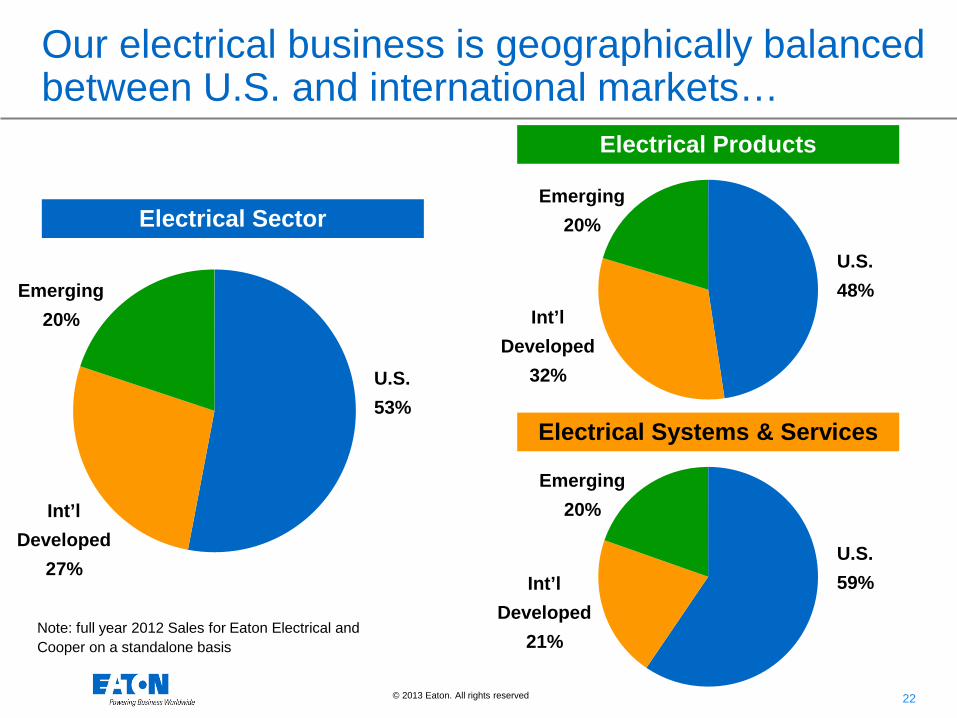

Our electrical business is geographically balanced between U.S. and international markets…

Emerging 20%

Emerging 20%

Int’l Developed

32%

Int’l Developed

21%

U.S. 48%

U.S. 59%

Emerging 20%

Int’l Developed

27%

U.S. 53%

Electrical Sector

Note: full year 2012 Sales for Eaton Electrical and Cooper on a standalone basis

Electrical Products

Electrical Systems & Services

23 © 2013 Eaton. All rights reserved.

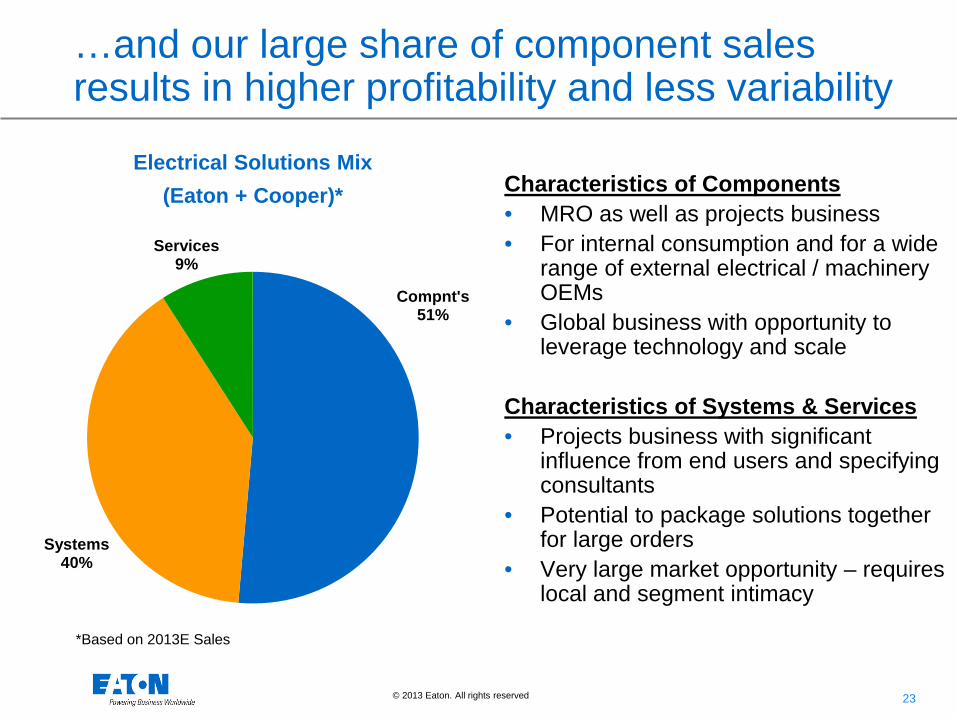

…and our large share of component sales results in higher profitability and less variability

Electrical Solutions Mix (Eaton + Cooper)*

Compnt's 51%

Systems 40%

Services 9%

Characteristics of Components • MRO as well as projects business • For internal consumption and for a wide

range of external electrical / machinery OEMs

• Global business with opportunity to leverage technology and scale

Characteristics of Systems & Services • Projects business with significant

influence from end users and specifying consultants

• Potential to package solutions together for large orders

• Very large market opportunity – requires local and segment intimacy

*Based on 2013E Sales

24 © 2013 Eaton. All rights reserved.

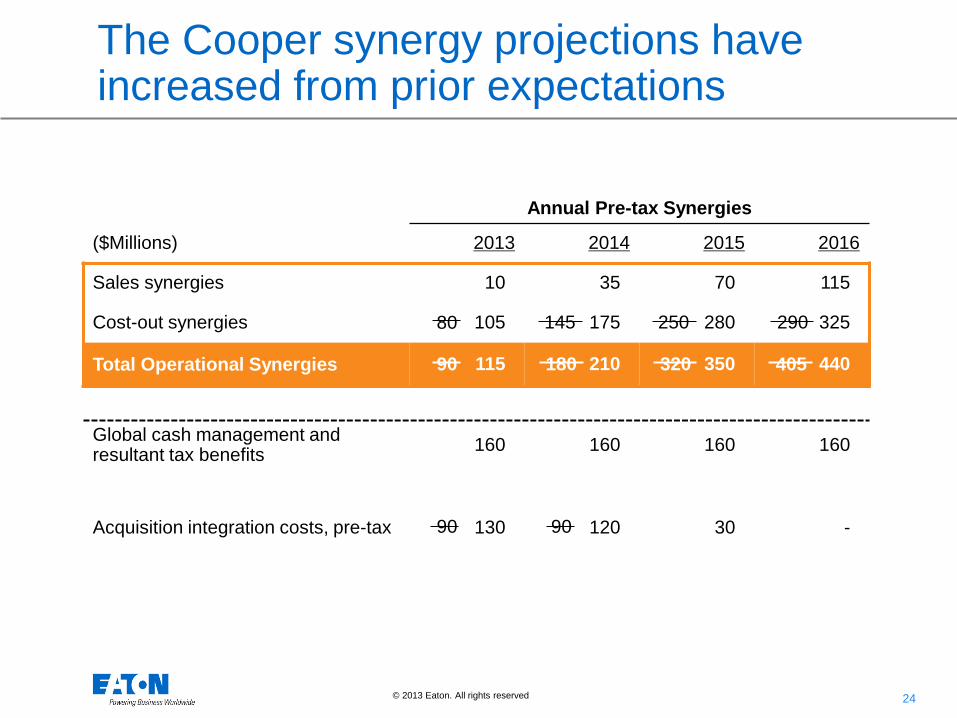

250

Annual Pre-tax Synergies

($Millions) 2013 2014 2015 2016

Sales synergies 10 35 70 115

Cost-out synergies 105 175 280 325

Total Operational Synergies 115 210 350 440

Global cash management and resultant tax benefits 160 160 160 160

Acquisition integration costs, pre-tax 130 120 30 -

80

90 180 405 320

90 90

290 145 250

The Cooper synergy projections have increased from prior expectations

25 © 2013 Eaton. All rights reserved.

Corporate Cost Reduction • Corporate

functions • Back office

support • Data centers

Plant & Distribution • 133 small /

medium plants • 64 distribution

centers • $3.8B in fixed

costs • High % of

fixed overhead in small / medium plants

Application of EBS Tools • ELSS • EQS • 6% average

improvement in our manufacturing costs on large Electrical acquisitions

Supply Chain Economies of Scale • $4.8B direct

spend • $2.3B indirect

spend • $0.5B logistics • 4% average

supply chain savings on large Electrical acquisitions

Leveraging Eaton’s Infrastructure • Technology

centers in Pune, Shenzhen, Prague

• Global shared service centers

$325M in mature year cost-out savings

Operating synergies will be derived from five main areas…

EBS

26 © 2013 Eaton. All rights reserved.

Larger Package to Common Customers • Oil & Gas • Data Centers • Mining • Utility

Boost Channel Sales • Strengthen regional presence

• Stronger niche presence

Service Business • Build on strong Global infrastructure

• Use Lighting to extend Energy Services

Deal Enables Geographic Expansion • China • Mexico • Middle East • Africa • Russia

$565M in incremental mature year sales

…and sales synergies will come from four key areas

27 © 2013 Eaton. All rights reserved.

Eaton – A Power Management Company

• A balanced power management company • Cooper acquisition transforms the Electrical

Sector

• Creating consistent and profitable growth across our Industrial Sector

• Summary and guidance

28 © 2013 Eaton. All rights reserved.

Hydraulic, fuel, pneumatic, and electrical products that deliver safe and efficient solutions for aircraft

Hydraulic motion and control products that efficiently solve the world’s most demanding needs for power

Transmissions and engine air management products that efficiently transfer power and improve fuel economy, emissions and safety

Our Industrial businesses offer compelling power management solutions…

Aerospace 2012 Sales $1.7B

Hydraulics 2012 Sales $3.0B

Vehicle 2012 Sales $3.9B

29 © 2013 Eaton. All rights reserved.

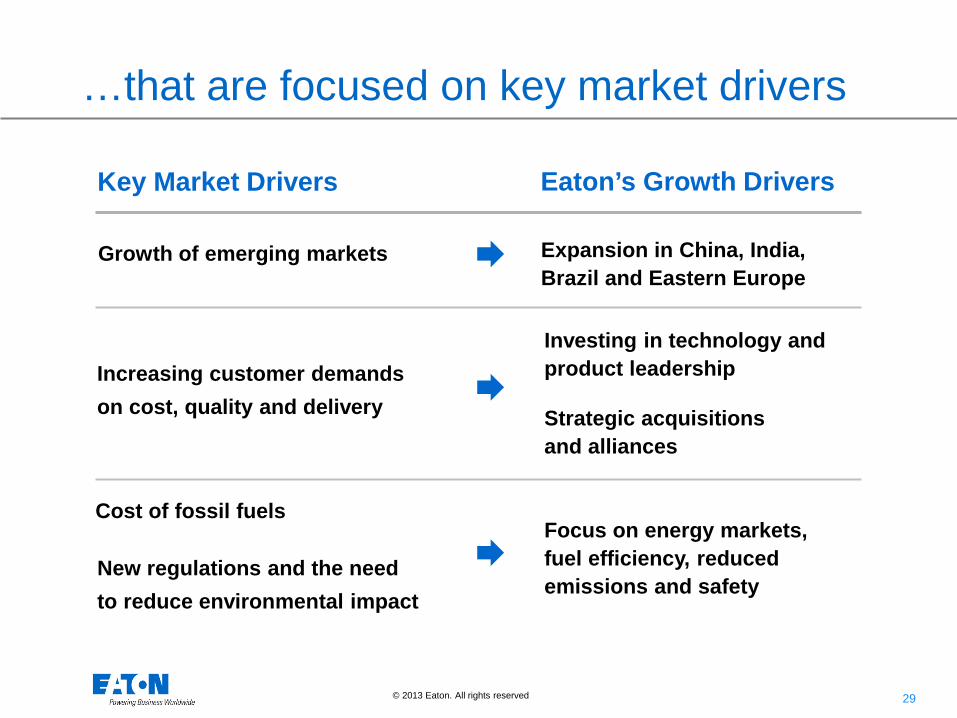

…that are focused on key market drivers

Key Market Drivers Eaton’s Growth Drivers

Growth of emerging markets

Increasing customer demands on cost, quality and delivery

New regulations and the need to reduce environmental impact

Expansion in China, India, Brazil and Eastern Europe

Investing in technology and product leadership

Strategic acquisitions and alliances

Focus on energy markets, fuel efficiency, reduced emissions and safety

Cost of fossil fuels

30 © 2013 Eaton. All rights reserved.

Our Hydraulics business serves large and diverse end markets

Expected 2013 operating margin of 13.5%

• 70% Mobile 30% Stationary

• 50% Direct 50% Distribution

2012 sales of $3.0B

Business Mix Market Mix

• Better profitability across the business cycle

• Well positioned in key growth markets

• Investment in product innovation

• Emerging markets • Acquisitions and alliances

Key Business Drivers

Construction

Agriculture

Oil & Gas / Energy Commercial

Vehicles

Manufacturing

Material Handling

Processing

Other

Recreation

31 © 2013 Eaton. All rights reserved.

Our two Hydraulics acquisitions in 2012 are a platform for growth in emerging markets

• HQ in S. Korea, 2011 sales $189M

• Expands our portfolio of components for global construction equipment

• Strengthens our ability to serve local OEMs with best cost manufacturing

• HQ in Turkey, 2011 sales $335M

• Expands our rubber, PVC, and thermoplastic industrial hose portfolio

• Enhances market access to Eastern Europe, Asia, and Africa

Acquisition Rationale:

Delivering for Customers:

Eaton has won the main control valves business from Hyundai Heavy Industries for their next generation 5-ton and 8-ton class excavators

Eaton has significantly expanded sales in Turkey, Middle East, Baltics, and CIS countries

New customers added in 10 countries where Eaton Hydraulics had no prior sales

32 © 2013 Eaton. All rights reserved.

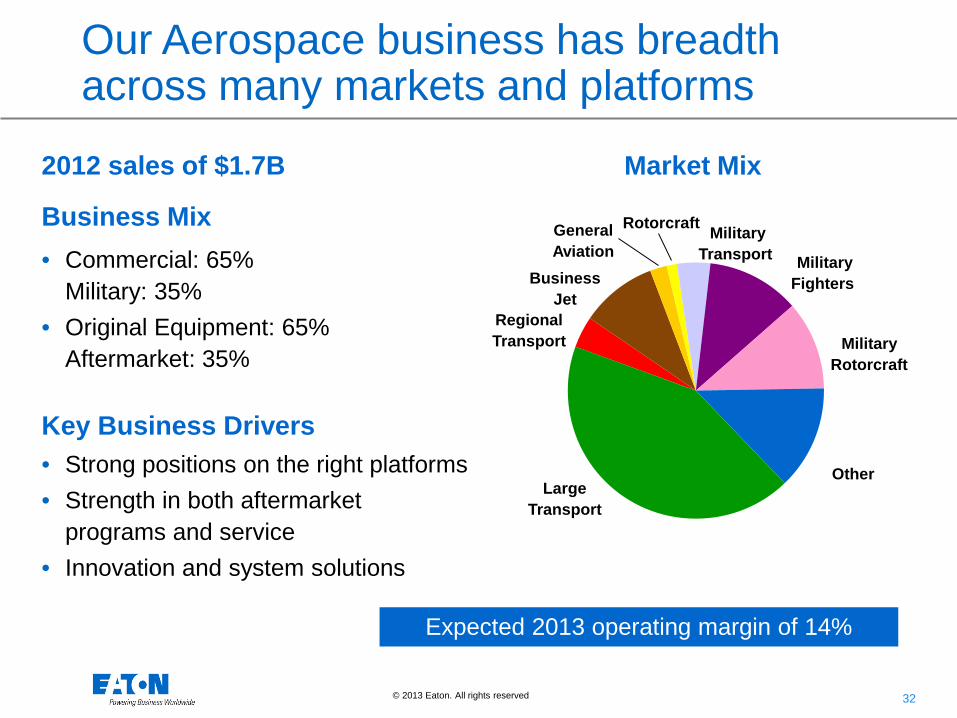

Rotorcraft

Military Fighters

General Aviation

Military Transport

Other

Military Rotorcraft

Expected 2013 operating margin of 14%

• Commercial: 65% Military: 35%

• Original Equipment: 65% Aftermarket: 35%

2012 sales of $1.7B

Business Mix

• Strong positions on the right platforms • Strength in both aftermarket

programs and service • Innovation and system solutions

Key Business Drivers

Market Mix

Large Transport

Regional Transport

Business Jet

Our Aerospace business has breadth across many markets and platforms

33 © 2013 Eaton. All rights reserved.

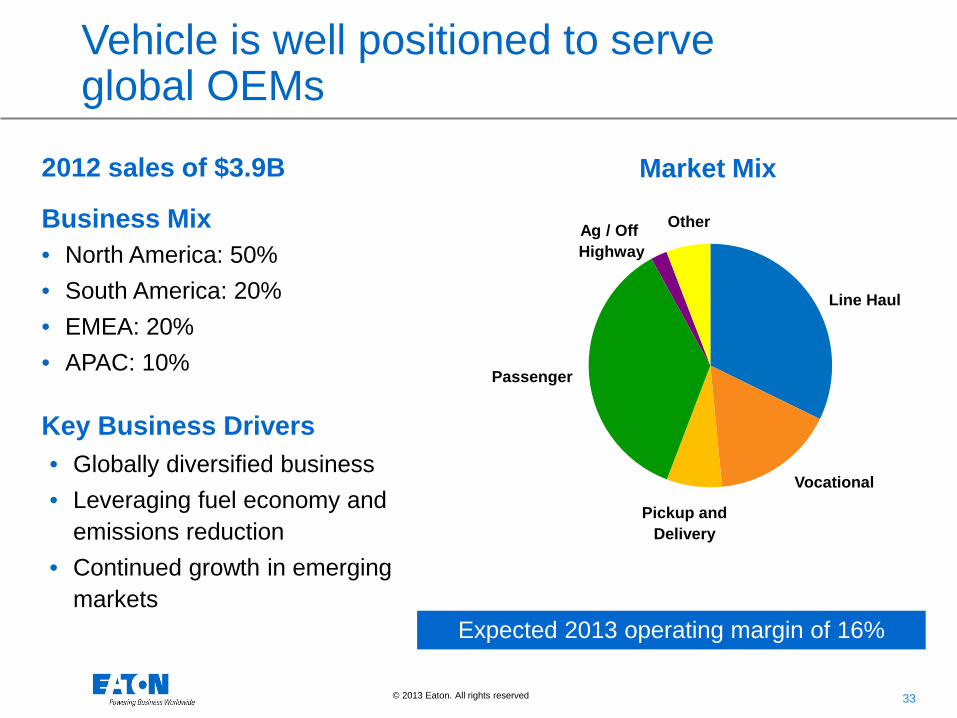

Pickup and Delivery

Expected 2013 operating margin of 16%

• North America: 50% • South America: 20% • EMEA: 20% • APAC: 10%

2012 sales of $3.9B

Business Mix

Market Mix

• Globally diversified business • Leveraging fuel economy and

emissions reduction • Continued growth in emerging

markets

Key Business Drivers

Line Haul

Vocational

Passenger

Ag / Off Highway

Other

Vehicle is well positioned to serve global OEMs

34 © 2013 Eaton. All rights reserved.

Eaton – A Power Management Company

• A balanced power management company • Cooper acquisition transforms the Electrical

Sector

• Creating consistent and profitable growth across our Industrial Sector

• Summary and guidance

35 © 2013 Eaton. All rights reserved.

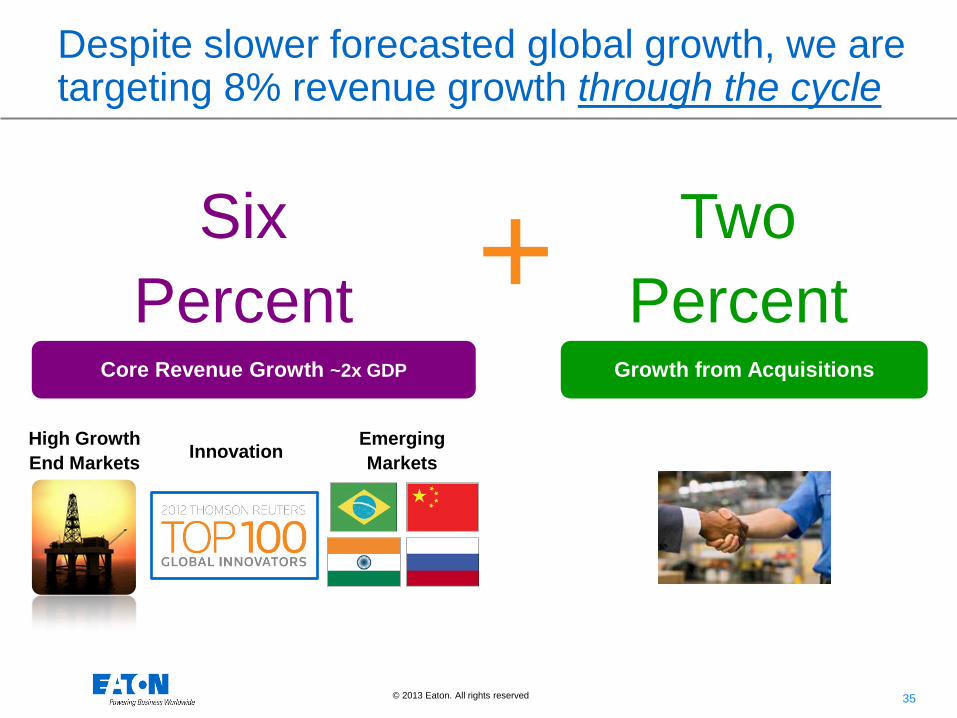

Despite slower forecasted global growth, we are targeting 8% revenue growth through the cycle

Six Percent

Core Revenue Growth ~2x GDP

High Growth End Markets Innovation

Emerging Markets

+ Two Percent

Growth from Acquisitions

36 © 2013 Eaton. All rights reserved.

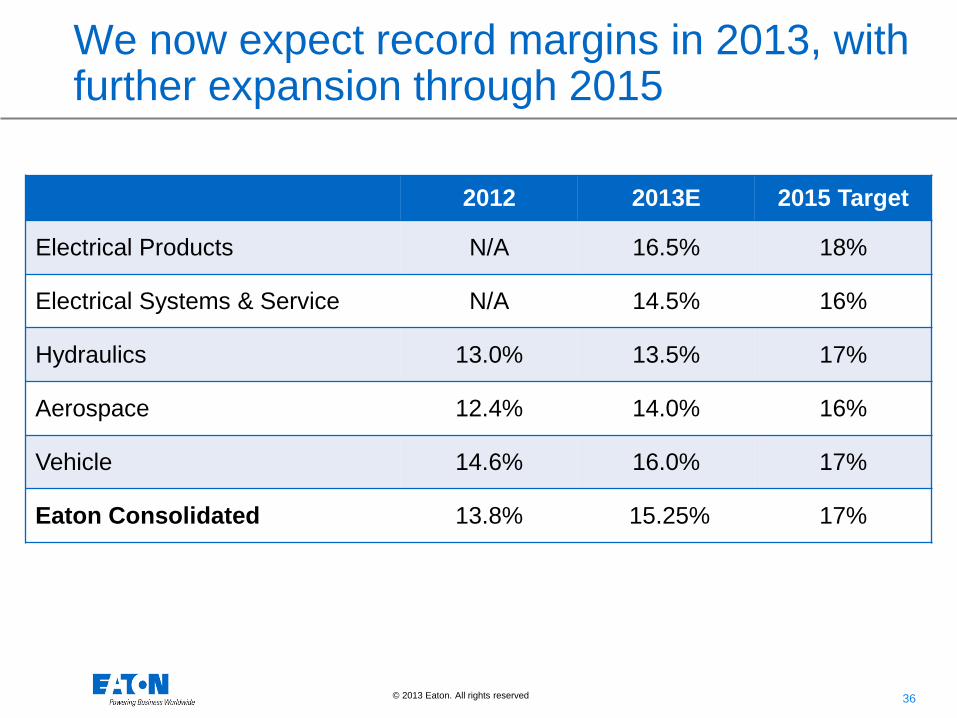

We now expect record margins in 2013, with further expansion through 2015

2012 2013E 2015 Target

Electrical Products N/A 16.5% 18%

Electrical Systems & Service N/A 14.5% 16%

Hydraulics 13.0% 13.5% 17%

Aerospace 12.4% 14.0% 16%

Vehicle 14.6% 16.0% 17%

Eaton Consolidated 13.8% 15.25% 17%

37 © 2013 Eaton. All rights reserved.

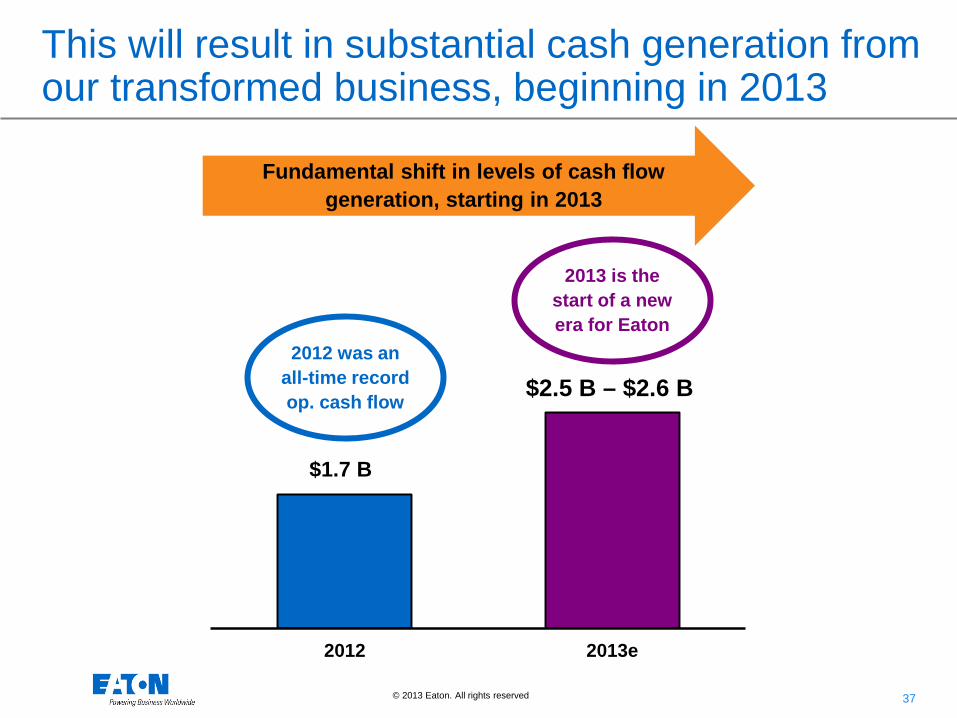

This will result in substantial cash generation from our transformed business, beginning in 2013

2012 2013e

$1.7 B

$2.5 B – $2.6 B

Fundamental shift in levels of cash flow generation, starting in 2013

2012 was an all-time record op. cash flow

2013 is the start of a new era for Eaton

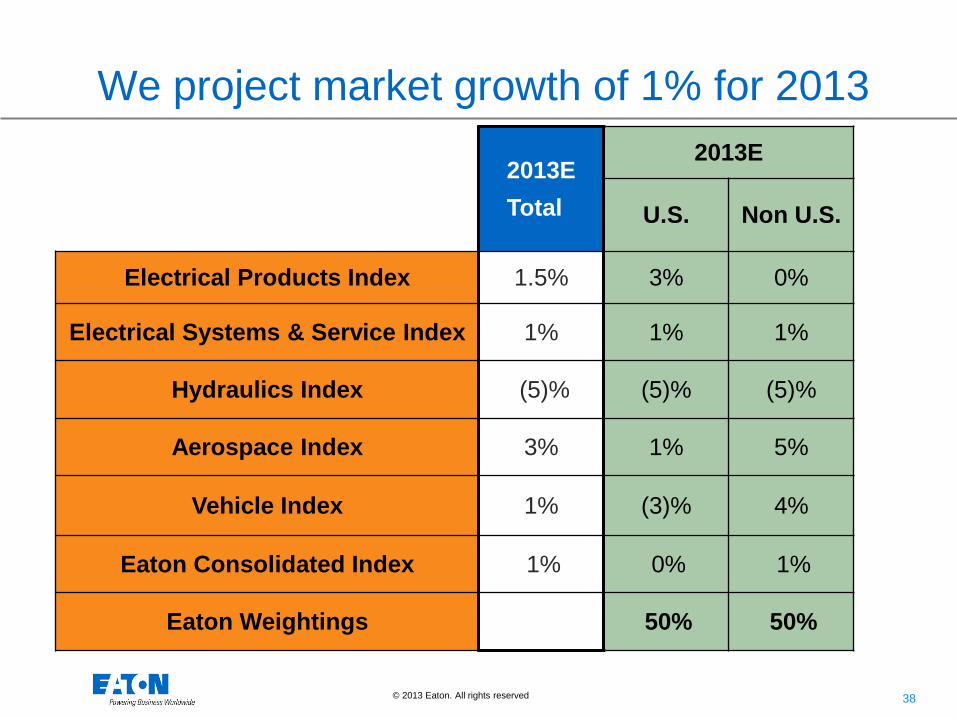

38 © 2013 Eaton. All rights reserved.

We project market growth of 1% for 2013

2013E Total

2013E

U.S. Non U.S.

Electrical Products Index 1.5% 3% 0%

Electrical Systems & Service Index 1% 1% 1%

Hydraulics Index (5)% (5)% (5)%

Aerospace Index 3% 1% 5%

Vehicle Index 1% (3)% 4%

Eaton Consolidated Index 1% 0% 1%

Eaton Weightings 50% 50%

39 © 2013 Eaton. All rights reserved.

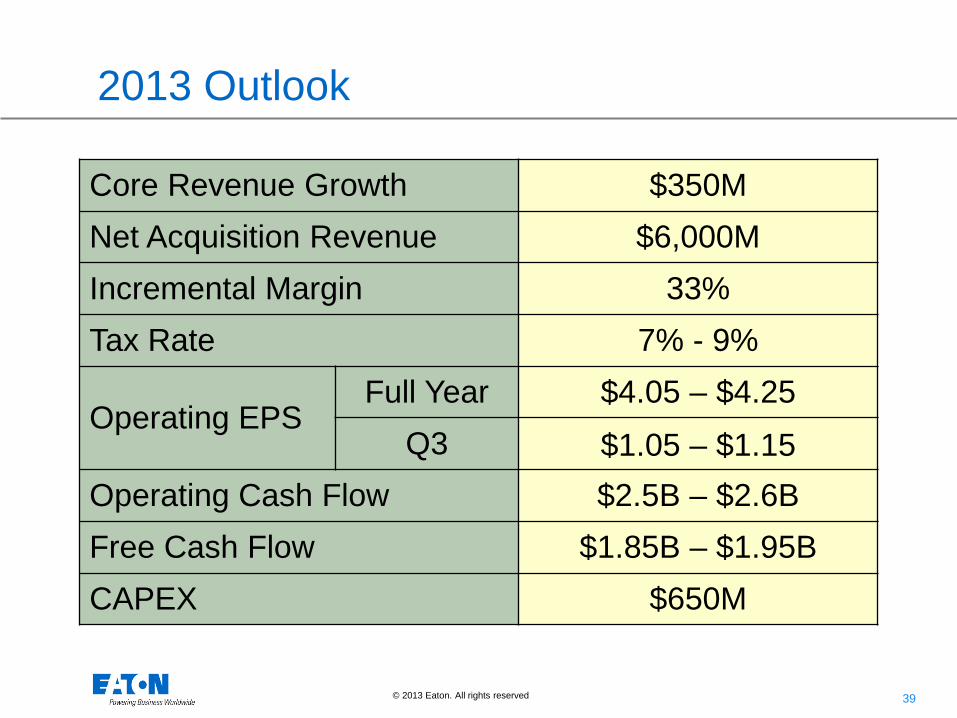

2013 Outlook

Core Revenue Growth $350M Net Acquisition Revenue $6,000M Incremental Margin 33% Tax Rate 7% - 9%

Operating EPS Full Year $4.05 – $4.25

Q3 $1.05 – $1.15 Operating Cash Flow $2.5B – $2.6B Free Cash Flow $1.85B – $1.95B CAPEX $650M

40 © 2013 Eaton. All rights reserved.

2013 – the start of a new era for Eaton

• We have the balance across our businesses to drive strong earnings growth throughout the economic cycle

• The transformed company will be higher growth, higher margin • We expect revenue growth through the cycle of 8% • We have raised our 2015 segment margin goal to 17%

• Post the Cooper acquisition, Eaton’s earnings volatility is near the midpoint of

performance for peer diversified industrials

• The Eaton Business System powers our integrated operating model, and will drive the integration of Cooper

• Strong EPS accretion from year one; exceeding original estimates

• Our dividend provides a yield in the top half of our peers, and for U.S. shareholders the majority is expected to be treated as a return of capital over the medium term

• Performance in 2013 is more dependent on execution than on global growth

41 © 2013 Eaton. All rights reserved.