Embed Size (px)

Citation preview

MARCH 2013

EARLYBIRD VENTURE CAPITAL: MARKET OVERVIEW

EARLYBIRD I 1 I

VENTURE CAPITAL FIRMS IN GERMANY ARE INVESTING IN A THRIVING MARKET

German venture ecosystem has matured

§ Ecosystem is now systematically producing ’global category leaders',

enabling breading ground for several billion € exits

§ Although deal flow is better than ever, scarcity of venture capital

means valuations and capital efficiency ratios remain reasonable

§ Sharp increase of serial entrepreneurs and more experienced fund

managers form a sustainable basis for long term growth

§ Berlin is establishing itself as one of the key entrepreneurial hubs

globally

EARLYBIRD I 2 I JW_Pressebrunch_130314

GERMAN ECONOMY HAS A LEADERSHIP POSITION IN TERMS OF INNOVATION POWER… Global Innovation Index – Overall Rankings Index

5.28

4.99

4.84

4.82

4.81

4.73

4.73

4.69

4.65

4.64

US

Germany

Sweden

UK

Singapore

South Korea

Switzerland

Denmark

Japan

Netherlands

EARLYBIRD I 3 I

Source: INSEAD, The Global Innovations Rankings and Report 2008 - 2009

JW_Pressebrunch_130314

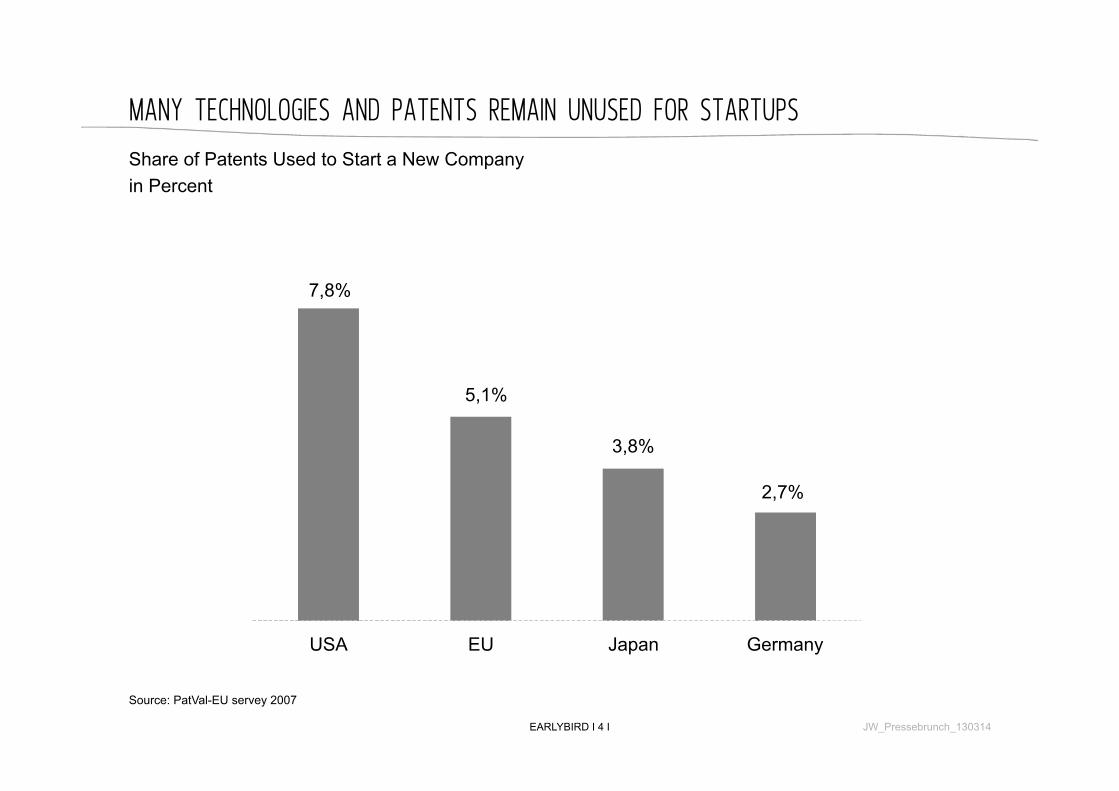

MANY TECHNOLOGIES AND PATENTS REMAIN UNUSED FOR STARTUPS

EARLYBIRD I 4 I

Share of Patents Used to Start a New Company in Percent

7,8%

5,1%

3,8%

2,7%

USA EU Japan Germany

Source: PatVal-EU servey 2007

JW_Pressebrunch_130314

GERMAN VC ECO SYSTEM HAS COME OF AGE

EARLYBIRD I 5 I

§ Gaining critical mass

§ From copycats to true innovations

§ More repeat entrepreneurs

§ Better seed infrastructure

§ More interest from US VCs for late stage financing

§ Continously good investment environment driven by a still growing supply gap

§ Trade sale markets remain open - listings are challenging

Status European VC Eco System

JW_Pressebrunch_130314

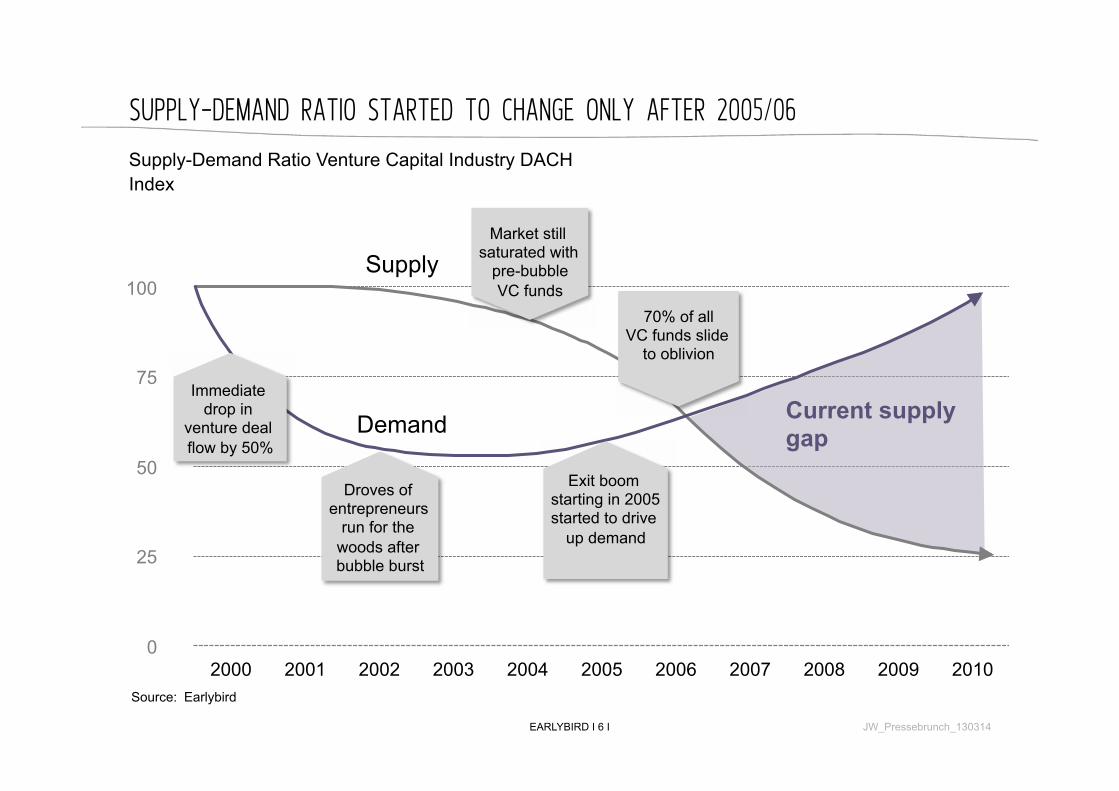

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

SUPPLY-DEMAND RATIO STARTED TO CHANGE ONLY AFTER 2005/06

EARLYBIRD I 6 I

Source: Earlybird

Supply-Demand Ratio Venture Capital Industry DACH Index

Current supply gap

Supply

Demand

Droves of entrepreneurs

run for the woods after bubble burst

Exit boom starting in 2005 started to drive

up demand

Market still saturated with

pre-bubble VC funds 100

75

50

25

0

Immediate drop in

venture deal flow by 50%

70% of all VC funds slide

to oblivion

JW_Pressebrunch_130314

-63%

THE NUMBER OF VCS HAS RIGHT-SIZED

1,600

711

1999 2011

* Active Funds = all VC funds, doing ≥ 4 investments per year Sub-set of so-called "Investment Grade Funds": US$ 100M; > 50% non-captive capital; raised successor fund with vintage year ≥ 2006 Source: NVCA; EVCA; Earlybird Estimates

Thereof the Top 20 VCs in Europe

Number of VC Funds in Europe – 1999 vs. 2011*

EARLYBIRD I 7 I

UK

Germany

France

Other

JW_Pressebrunch_130314

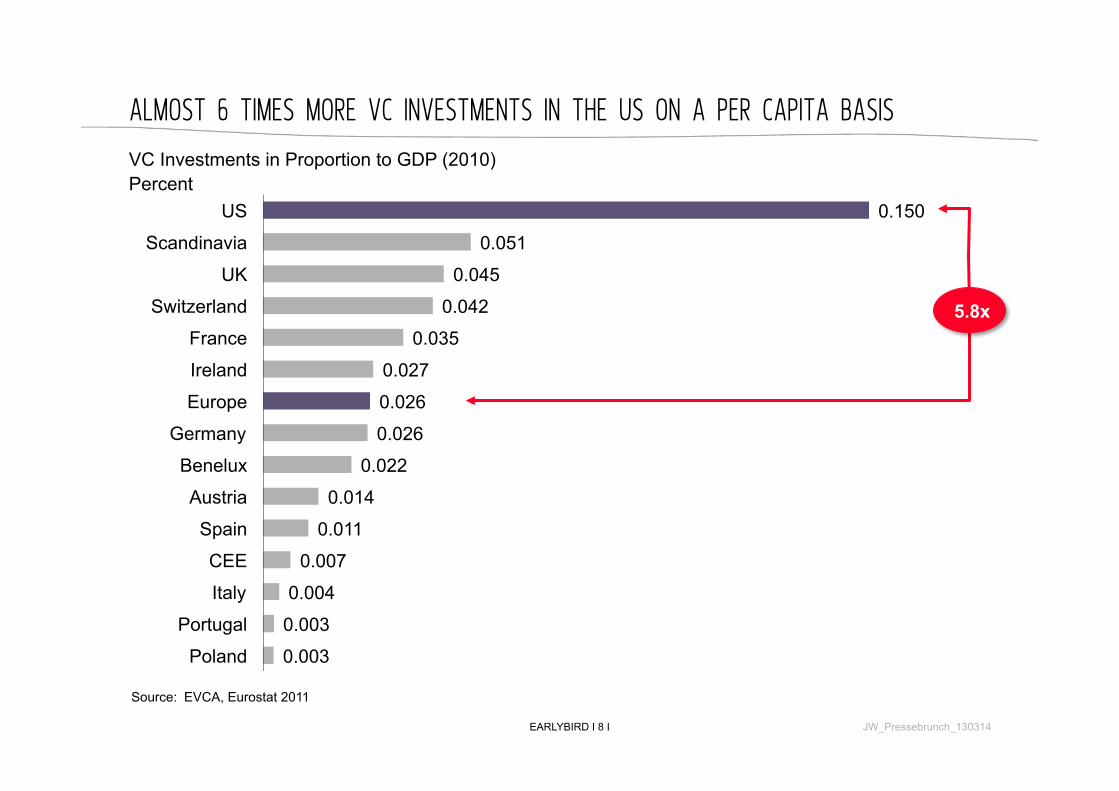

0.003

0.003

0.004

0.007

0.011

0.014

0.022

0.026

0.026

0.027

0.035

0.042

0.045

0.051

0.150

Poland

Portugal

Italy

CEE

Spain

Austria

Benelux

Germany

Europe

Ireland

France

Switzerland

UK

Scandinavia

US

VC Investments in Proportion to GDP (2010) Percent

Source: EVCA, Eurostat 2011

5.8x

ALMOST 6 TIMES MORE VC INVESTMENTS IN THE US ON A PER CAPITA BASIS

EARLYBIRD I 8 I JW_Pressebrunch_130314

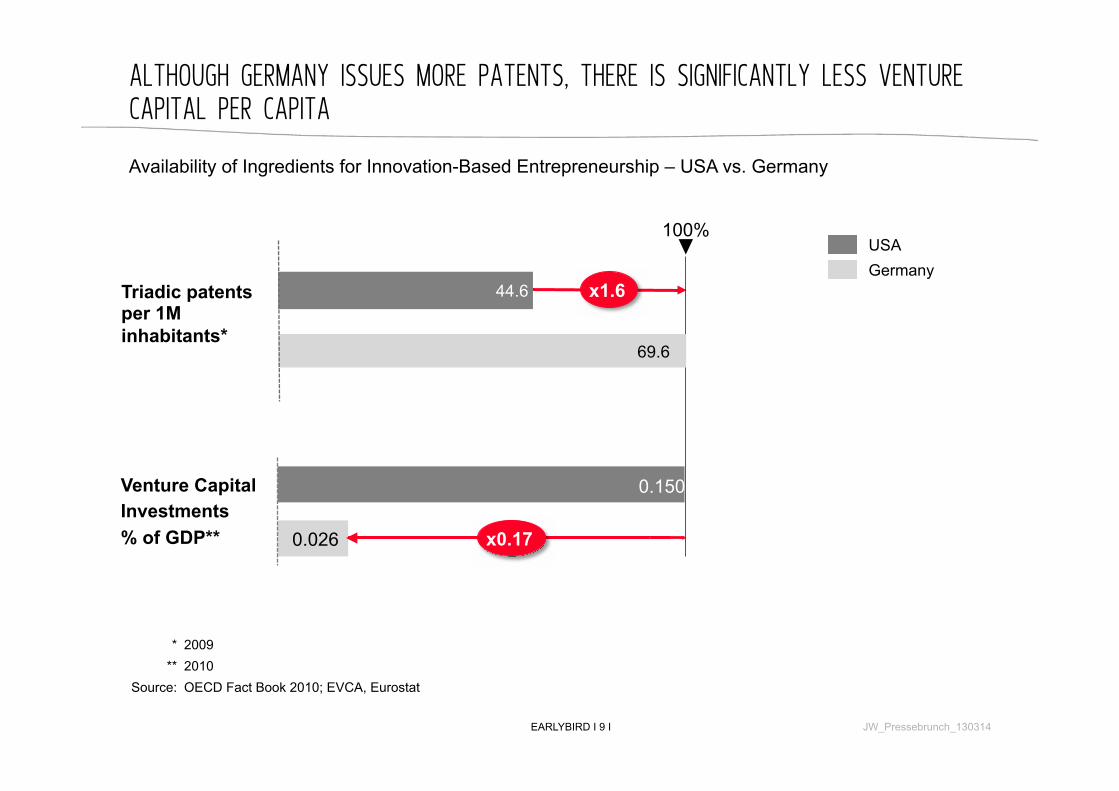

0.150

0.026

ALTHOUGH GERMANY ISSUES MORE PATENTS, THERE IS SIGNIFICANTLY LESS VENTURE CAPITAL PER CAPITA

* 2009 ** 2010

Source: OECD Fact Book 2010; EVCA, Eurostat

Availability of Ingredients for Innovation-Based Entrepreneurship – USA vs. Germany

EARLYBIRD I 9 I

Triadic patents per 1M inhabitants*

Venture Capital Investments % of GDP**

USA Germany

100%

x0.17

44.6

69.6

x1.6

JW_Pressebrunch_130314

DEAL MULTIPLES START TO SHOW THE IMPACT OF THE EXCELLENT INVESTMENT ENVIRONMENT

6.7

3.4 3.5 4.3

4.8 4.5 3.9

11.4

6 6.4

5

6.5

11.4

5.6

6.6

11.4

2004 2005 2006 2007 2008 2009 2010 2011*

US EU

EARLYBIRD I 10 I

Ø 7.4

Ø 5.3

Average Multiple Value Created

* First half year Source: Dow Jones VentureSource, DFJ Esprit

JW_Pressebrunch_130314

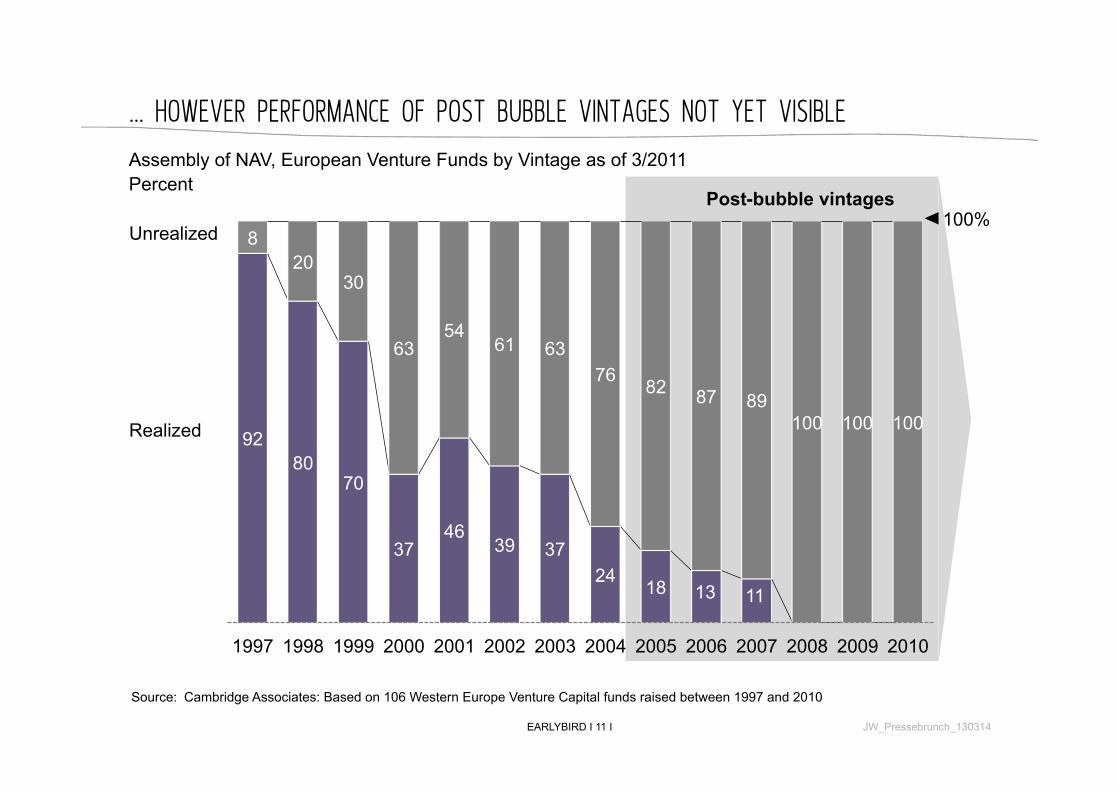

… HOWEVER PERFORMANCE OF POST BUBBLE VINTAGES NOT YET VISIBLE

EARLYBIRD I 11 I

Source: Cambridge Associates: Based on 106 Western Europe Venture Capital funds raised between 1997 and 2010

Assembly of NAV, European Venture Funds by Vintage as of 3/2011 Percent

92 80

70

37 46

39 37 24 18

8 20

30

63 54

61 63 76 82 87 89

100 100 100

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Unrealized

Realized

100% Post-bubble vintages

13 11

JW_Pressebrunch_130314

2000 2005 2011

1,500,000

500,000

50,000

SIMULTANEOUSLY IT HAS BECOME DRAMATICALLY CHEAPER TO START AN INTERNET COMPANY…

JW_Pressebrunch_130314 EARLYBIRD I 12 I

Required Capital to start a consumer internet company In € M

Open source

Cloud

…WHILE A SURGE IN SMART SEED / ENABLING STAGE FUNDS COVER THE SEED STAGE OF THE MARKET

§ Successful entrepreneurs are re-cycling their wealth & know-how within the ecosystem, e.g. − Atlantic (Christophe Maire) − Passion (Stefan Glänzer) − HackFWD (Lars Hinrichs) − TEV (Lukasz Gadowski) − ...

§ Various players (VCs, corporates,

angels) working together to create seedfunds or new VC funds, e.g. − unternehmertum, Seedcamp …

§ Structured organizations / accele-

rator programs emerging, e.g. − Startup Bootcamp …

EARLYBIRD I 13 I

Source: EVCA & Earlybird

JW_Pressebrunch_130314

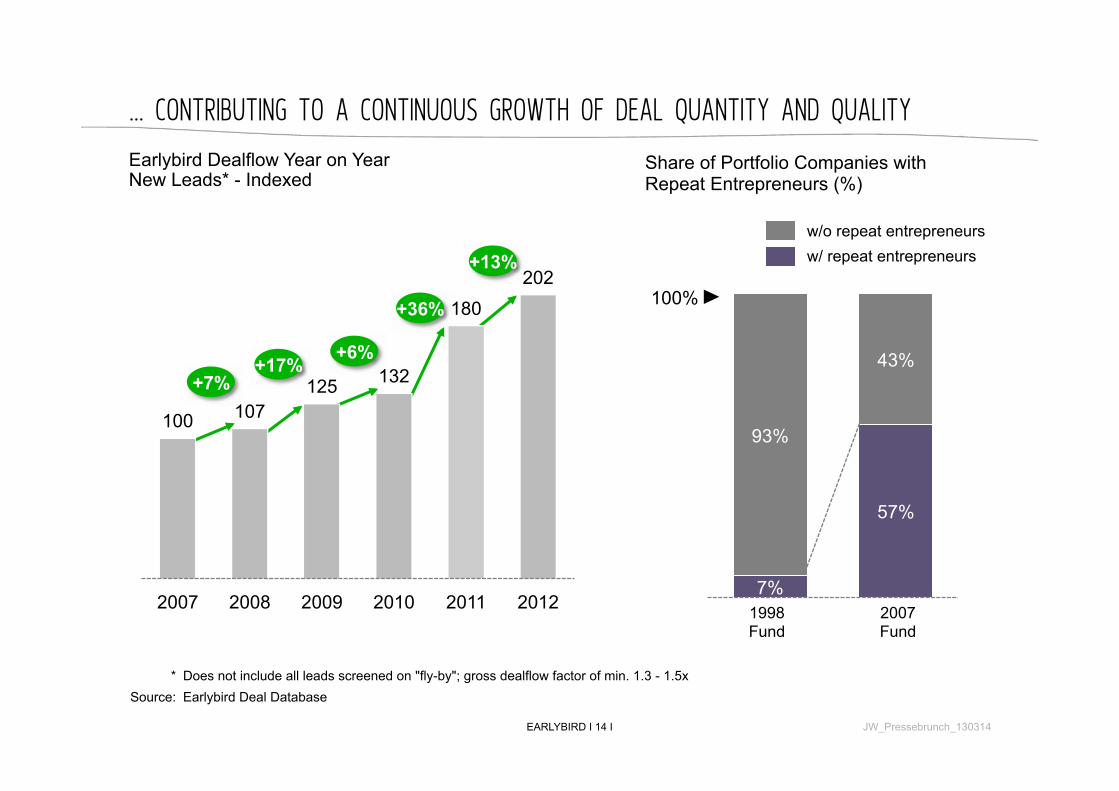

… CONTRIBUTING TO A CONTINUOUS GROWTH OF DEAL QUANTITY AND QUALITY

EARLYBIRD I 14 I

* Does not include all leads screened on "fly-by"; gross dealflow factor of min. 1.3 - 1.5x Source: Earlybird Deal Database

Earlybird Dealflow Year on Year New Leads* - Indexed

Share of Portfolio Companies with Repeat Entrepreneurs (%)

7%

57%

93%

43%

100%

w/o repeat entrepreneurs w/ repeat entrepreneurs

1998 Fund

2007 Fund

100 107 125 132

180 202

2007 2008 2009 2010 2011 2012

+7% +6%

+36%

+17%

JW_Pressebrunch_130314

+13%

21 (78%) 10

(59%)

2 (10%)

5 (18%)

6 (35%)

16 (76%)

1 (4%) 1 (6%) 3 (14%)

EARLYBIRD PORTFOLIO EVIDENCE: LATER ENTRIES AT LOWER VALUATIONS …

EARLYBIRD I 15 I

Stage Median Pre-Money Valuation – Initial Round in €M

No. of Investment per Earlybird Fund

5.3

9.8

3.8

1998 Fund

2000

Fund 2007 Fund

2007 Fund

2000 Fund

1998 Fund

Mid-stage

Early stage

Seed

Per December 2011

JW_Pressebrunch_130314

… LEADING TO MORE REVENUES AND FEWER WRITE OFFS

EARLYBIRD I 16 I

19%

32%

13% 0 0

5

10

14

0

4

8

9

11

1

2 2 2

5

Yr1 Yr2 Yr3 Yr4 Yr5

1998 Fund

2000 Fund

2007 Fund

No. of Write-Offs (Cumulative) Years 1-5 of Fund Lifetime

Revenue Traction per Fund Generation (Year 1-5)* in €M

* Aggregate shareholding weighted revenue contribution of portfolio companies Source: Earlybird Analysis

0.3 2.8

7.1 6.7 9.1

3.4 3.1

7.6

13.4

19.7

3.7

10.5

13.9

25

63.6

Yr1 Yr2 Yr3 Yr4 Yr5

JW_Pressebrunch_130314

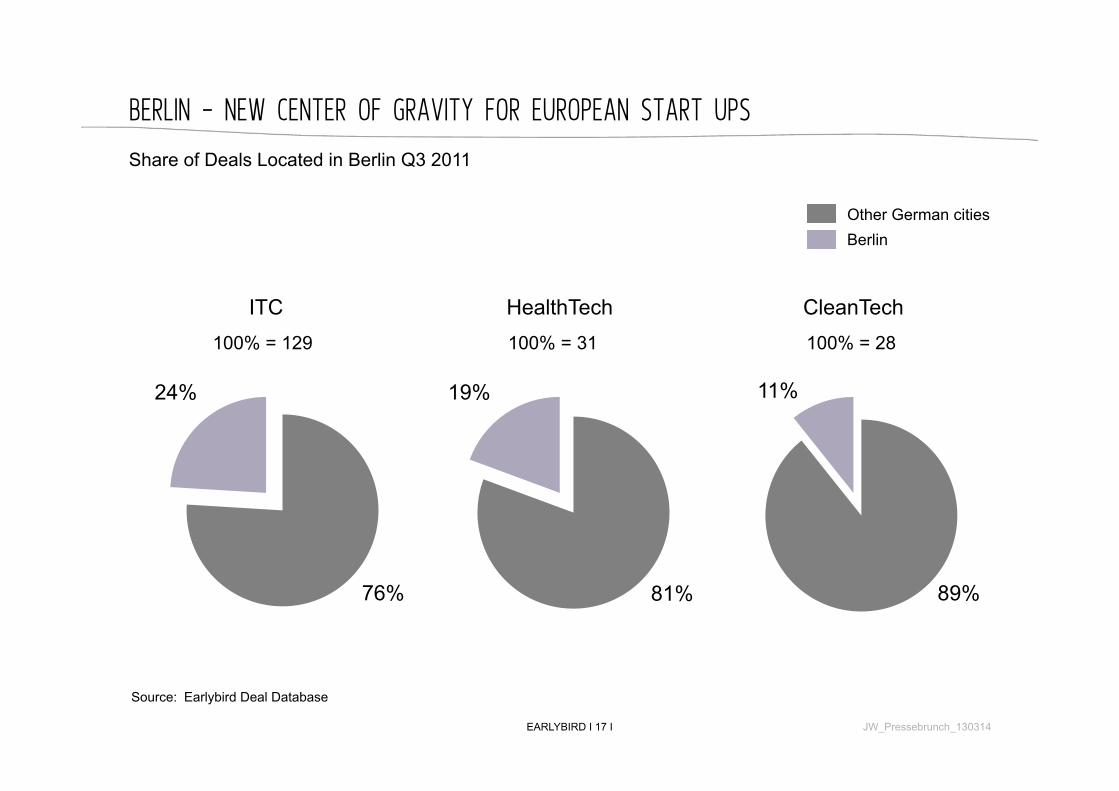

BERLIN - NEW CENTER OF GRAVITY FOR EUROPEAN START UPS

ITC HealthTech CleanTech

EARLYBIRD I 17 I

Other German cities Berlin

Share of Deals Located in Berlin Q3 2011

Source: Earlybird Deal Database

100% = 129 100% = 31 100% = 28

24% 19% 11%

76% 81% 89%

JW_Pressebrunch_130314

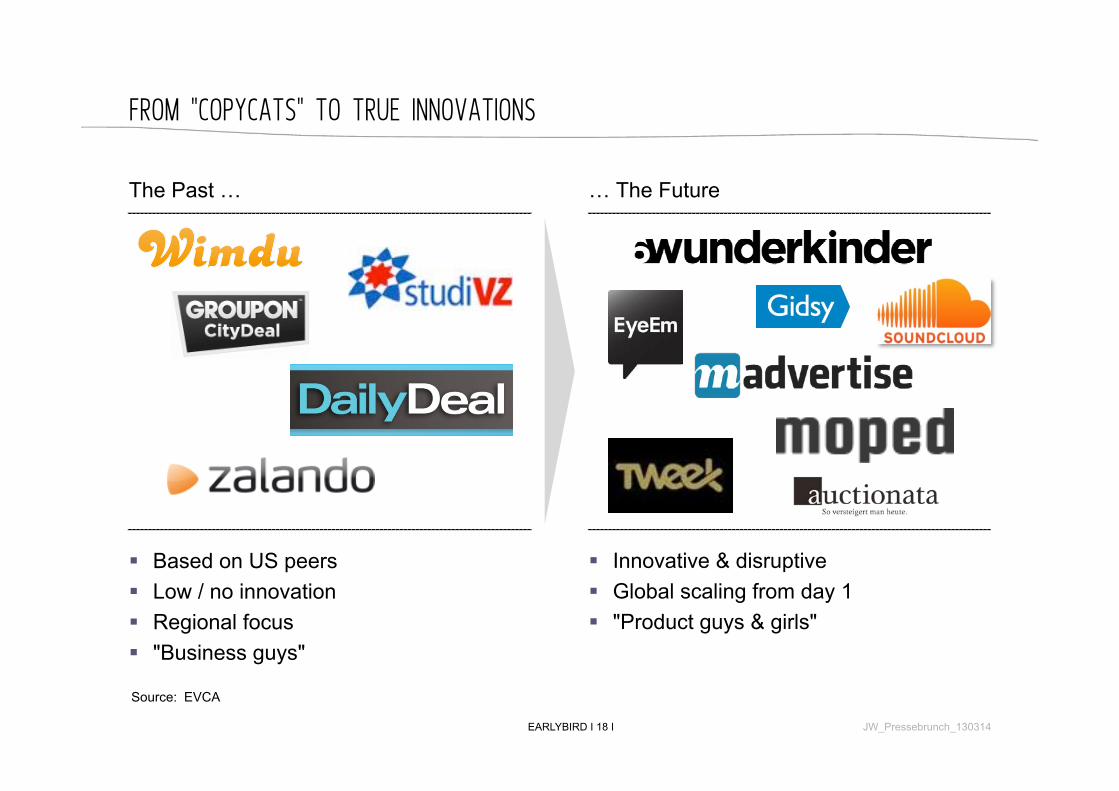

FROM "COPYCATS" TO TRUE INNOVATIONS

EARLYBIRD I 18 I

Source: EVCA

§ Based on US peers § Low / no innovation § Regional focus § "Business guys"

The Past … … The Future

§ Innovative & disruptive § Global scaling from day 1 § "Product guys & girls"

JW_Pressebrunch_130314

BERLIN BECOMING ONE OF THE KEY ENTREPRENEURIAL HUBS GLOBALLY

§ #2 number of new start-ups p.a. globally behind the Valley

§ 1,300 Internet start-ups founded since 2008 (500 in 2012)

§ Surge in US VC syndication, late stage US VC investments more than tripled in the last 2 years

§ Fuelled by dozens of seed funds, angel networks & accelerators

Top start-ups in Berlin Example: US VCs

syndicating in Berlin

EARLYBIRD I 19 I JW_Pressebrunch_130314

GERMANY AND EUROPE ARE NOW SYSTEMATICALLY CREATING GLOBAL CATEGORY LEADERS, GENERATING A BROAD BASE FOR OUTSIZED EXITS DOWN THE ROAD

JW_Pressebrunch_130314 EARLYBIRD I 20 I

CONSUMER INTERNET THE WORLD'S GAMING HUB ENTERPRISE PROCESS EFFICIENCY

PAYMENT COMMUNICATION PRODUCTIVITY E-COMMERCE

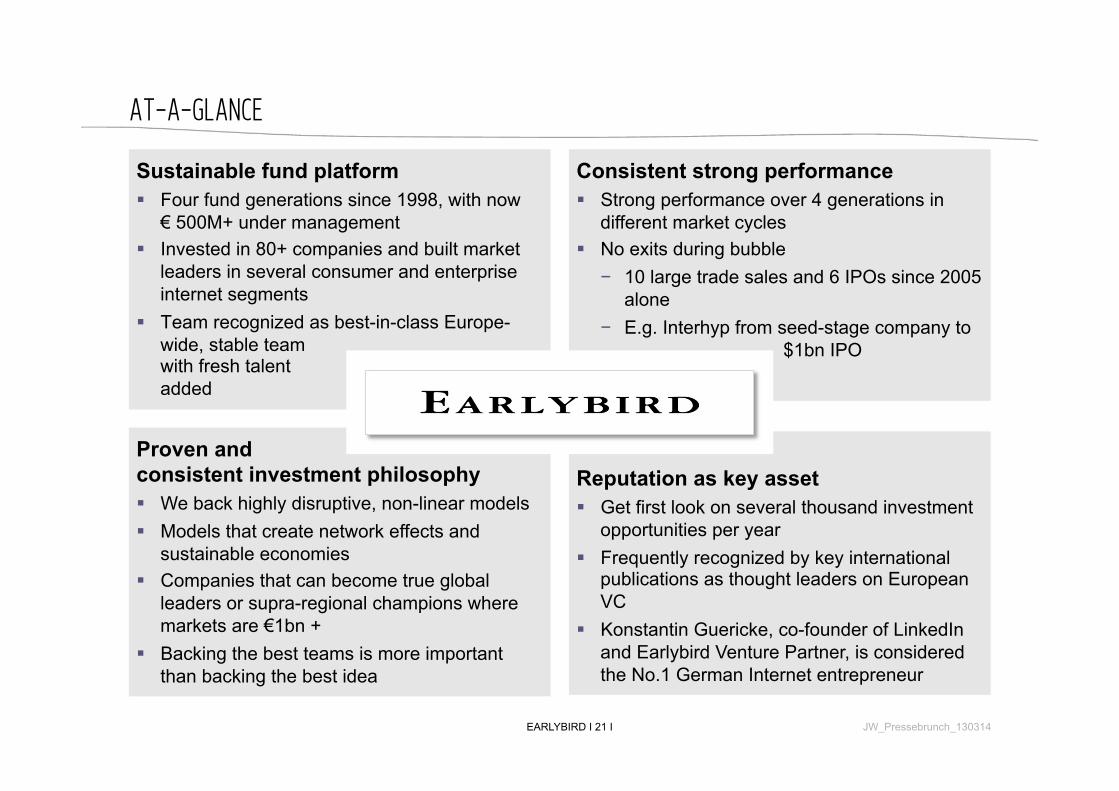

AT-A-GLANCE

Sustainable fund platform § Four fund generations since 1998, with now € 500M+ under management

§ Invested in 80+ companies and built market leaders in several consumer and enterprise internet segments

§ Team recognized as best-in-class Europe- wide, stable team with fresh talent added

EARLYBIRD I 21 I

Consistent strong performance § Strong performance over 4 generations in

different market cycles § No exits during bubble − 10 large trade sales and 6 IPOs since 2005

alone − E.g. Interhyp from seed-stage company to

$1bn IPO −

Proven and consistent investment philosophy § We back highly disruptive, non-linear models § Models that create network effects and

sustainable economies § Companies that can become true global

leaders or supra-regional champions where markets are €1bn +

§ Backing the best teams is more important than backing the best idea

Reputation as key asset § Get first look on several thousand investment

opportunities per year § Frequently recognized by key international

publications as thought leaders on European VC

§ Konstantin Guericke, co-founder of LinkedIn and Earlybird Venture Partner, is considered the No.1 German Internet entrepreneur

JW_Pressebrunch_130314

THE EARLYBIRD TEAM

Hendrik Brandis Munich Partner

Christian Nagel Berlin Partner

Jason Whitmire Berlin Partner

Ciarán O'Leary Berlin Partner

Maximilian Claussen Berlin Principal

EARLYBIRD I 22 I

§ 18 years VC/PE investment experience

§ Entrepreneur prior to co-founding Earlybird

§ Engineering & Economics, McKinsey & Co.

§ 17 years VC/PE investment experience

§ Prior to co-founding EB: entrepreneur, Project Manager at EADS

§ Aerospace Engineering, McKinsey & Co

§ 16 years tech industry expe-rience, 3 years VC investment experience

§ Sr. Advisor Intel, GM Mobile WindRiver, MD FSMLabs, GM SW at Infineon

§ MBA, BA/MA

§ 8 years VC/PE § Experience at

several start-ups prior to joining EB

§ Previously The Carlyle Group

§ Degree in Economics (HHL / Technical University of Singapore)

§ 5 years VC/PE investment experience

§ Advised several start-ups

§ The MediaLab, LEK Consulting

§ Degree in Economics (ESB Reutlingen, ICADE)

§ LinkedIn co-founder & CMO

§ Serial entrepreneur, German citizen based in Silicon Valley

§ Exec. Roles at Jaxtr (CEO), Presenter.com

§ B.S., M.S. Eng. Stanford

Konstantin Guericke Palo Alto Venture Partner

§ Highly complementary background and skill sets § Helped build market leaders in all cycles § Exited 50+ companies § Co-founded 10+ companies § Over 50 years of experience in venture investing

JW_Pressebrunch_130314

Wolfgang Seibold Munich Partner

§ 12 years VC experience

§ Focus on clean tech

§ Prior: Alctatel/ SEL; BCG

§ Dipl. Physicist; INSEAD MBA

EARLYBIRD BRAND BUILDING

2013: Selected by European Entrepreneurs

as the No.1 VC in Germany

2013: Nominated by Global VCs/Investors as one of the top VCs /

Teams in Europe

2012: Most quoted European VC in the Global Financial

Press

JW_Pressebrunch_130314 EARLYBIRD I 23 I

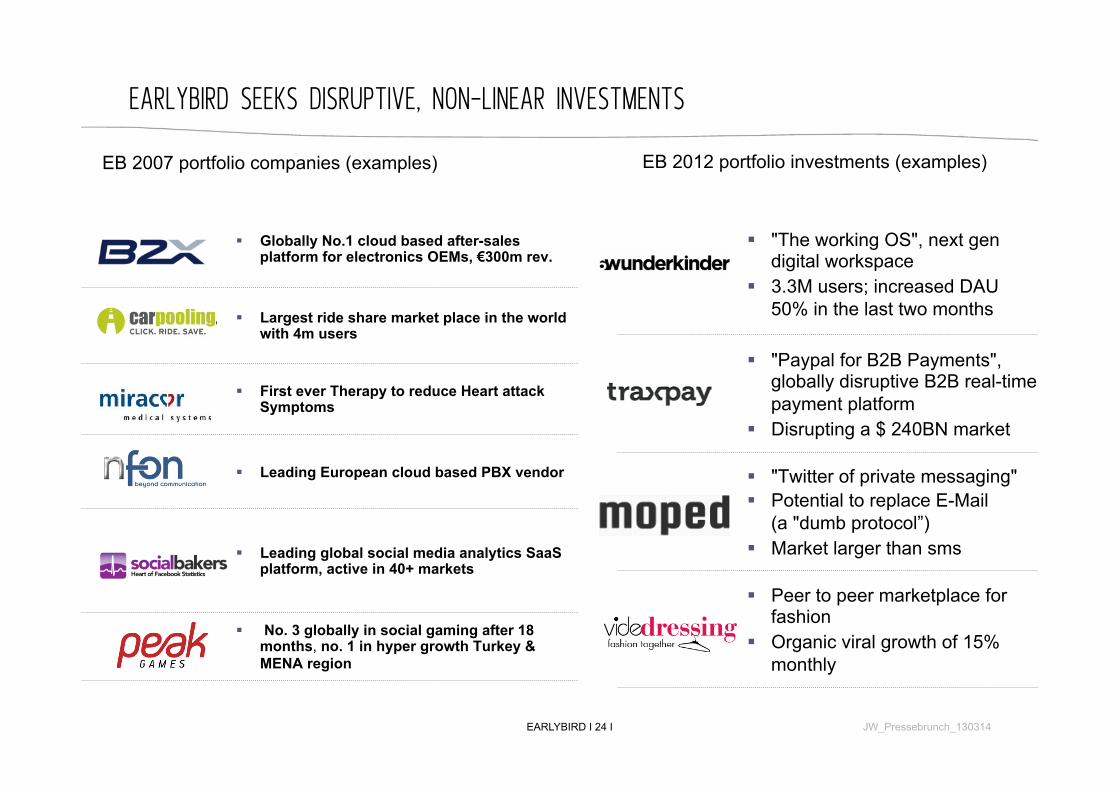

§ Globally No.1 cloud based after-sales platform for electronics OEMs, €300m rev.

§ Largest ride share market place in the world with 4m users

§ First ever Therapy to reduce Heart attack Symptoms

§ Leading European cloud based PBX vendor

§ Leading global social media analytics SaaS platform, active in 40+ markets

§ No. 3 globally in social gaming after 18 months, no. 1 in hyper growth Turkey & MENA region

EARLYBIRD SEEKS DISRUPTIVE, NON-LINEAR INVESTMENTS

EARLYBIRD I 24 I

EB 2007 portfolio companies (examples) EB 2012 portfolio investments (examples)

§ "The working OS", next gen digital workspace

§ 3.3M users; increased DAU 50% in the last two months

§ "Paypal for B2B Payments", globally disruptive B2B real-time payment platform

§ Disrupting a $ 240BN market

§ "Twitter of private messaging" § Potential to replace E-Mail

(a "dumb protocol”) § Market larger than sms

§ Peer to peer marketplace for fashion

§ Organic viral growth of 15% monthly

JW_Pressebrunch_130314

www.earlybird.com

THANK YOU FOR YOUR ATTENTION!