Embed Size (px)

Citation preview

Understanding the Impact of

EMV Migration in the U.S.

Sharon Pazlar

Director, Product Management

Output Solutions at Fiserv

February 21, 2013

E M V U . S . M i g r a t i o n

2 0 1 5

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Quick Facts

Year founded: 1984

Headquarters: Brookfield, Wisconsin

Locations: 158 worldwide

Employees: Approximately 20,000

Clients: Approximately 16,000

Revenue: $4.3 billion in 2011

Who We Are

Leading global provider of

information management and

electronic commerce systems

Who We Serve:

Banks, credit unions and

thrifts, billers, mortgage

lenders and leasing

companies, brokerage and

investment firms, healthcare

organizations, insurance

companies, utilities, retail,

govt. and more.

2

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Agenda

3

• What is EMV

• Understanding EMV

• Global View of EMV

• Why EMV Adoption in the U.S. Makes Sense

• Card Association’s Announcements/Roadmaps

• EMV Implementation Options

• EMV Challenges Facing the U.S.

• Determining Your Approach

• How to Get Started

• Fiserv Readiness and Timelines

E M V U . S . M i g r a t i o n

2 0 1 5

What is EMV?

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

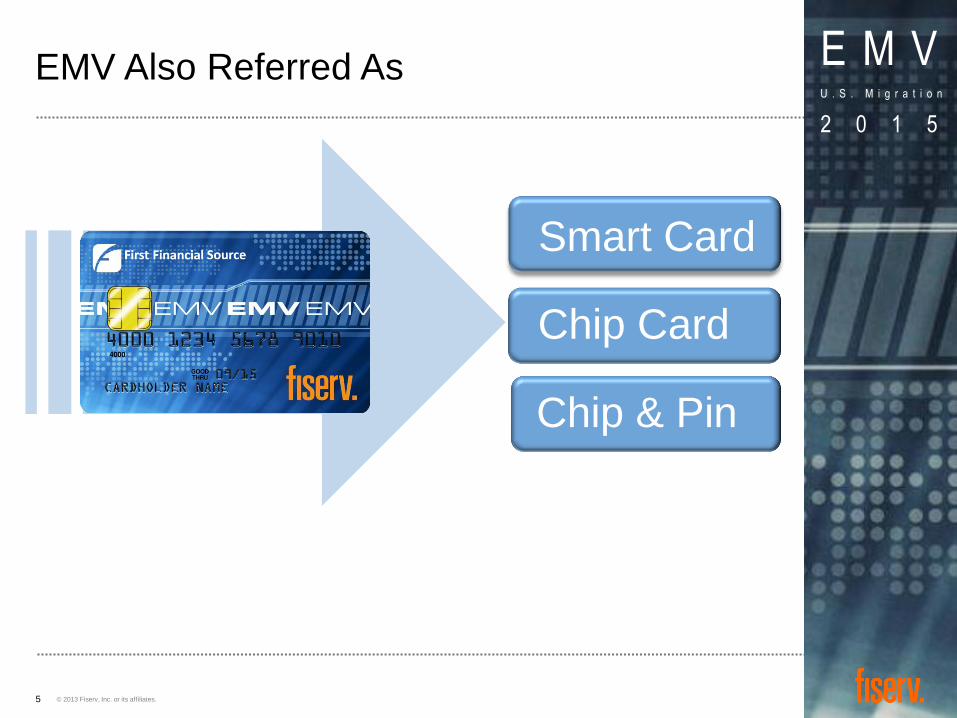

EMV Also Referred As

5

Chip & Pin

Smart Card

Chip Card

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

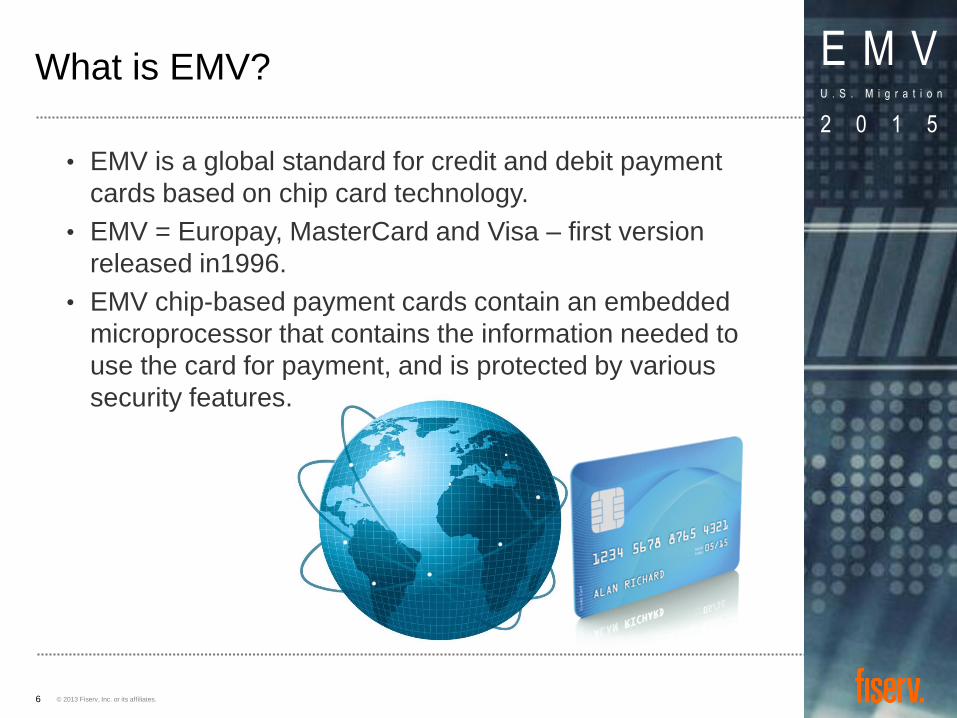

What is EMV?

6

• EMV is a global standard for credit and debit payment

cards based on chip card technology.

• EMV = Europay, MasterCard and Visa – first version

released in1996.

• EMV chip-based payment cards contain an embedded

microprocessor that contains the information needed to

use the card for payment, and is protected by various

security features.

E M V U . S . M i g r a t i o n

2 0 1 5

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

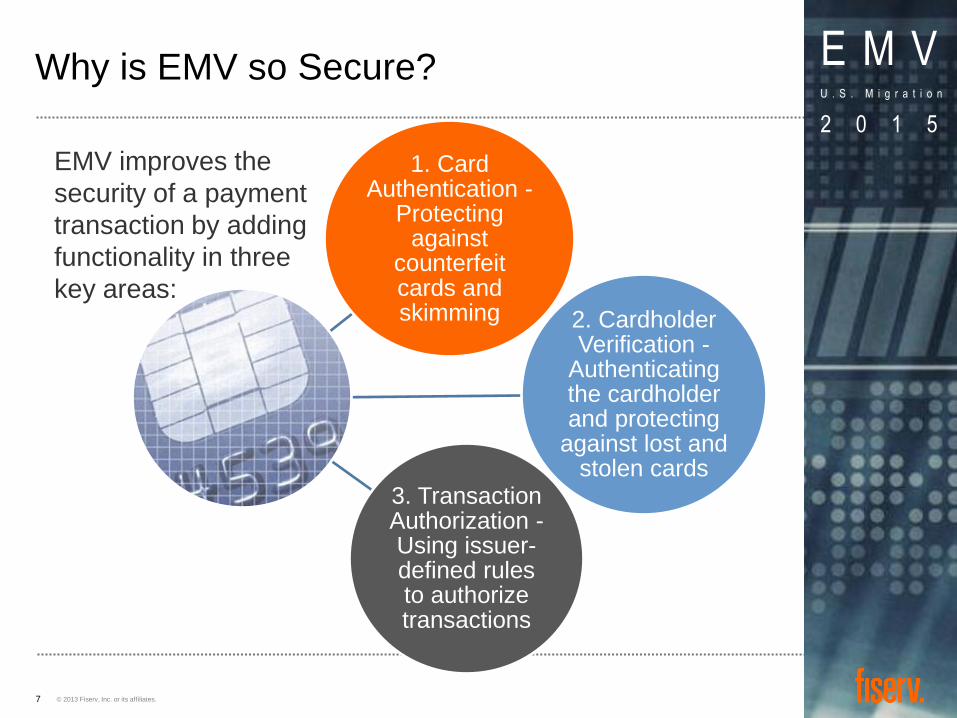

Why is EMV so Secure?

7

EMV improves the

security of a payment

transaction by adding

functionality in three

key areas:

1. Card Authentication -

Protecting against

counterfeit cards and skimming 2. Cardholder

Verification - Authenticating the cardholder and protecting

against lost and stolen cards

3. Transaction Authorization - Using issuer-defined rules to authorize transactions

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

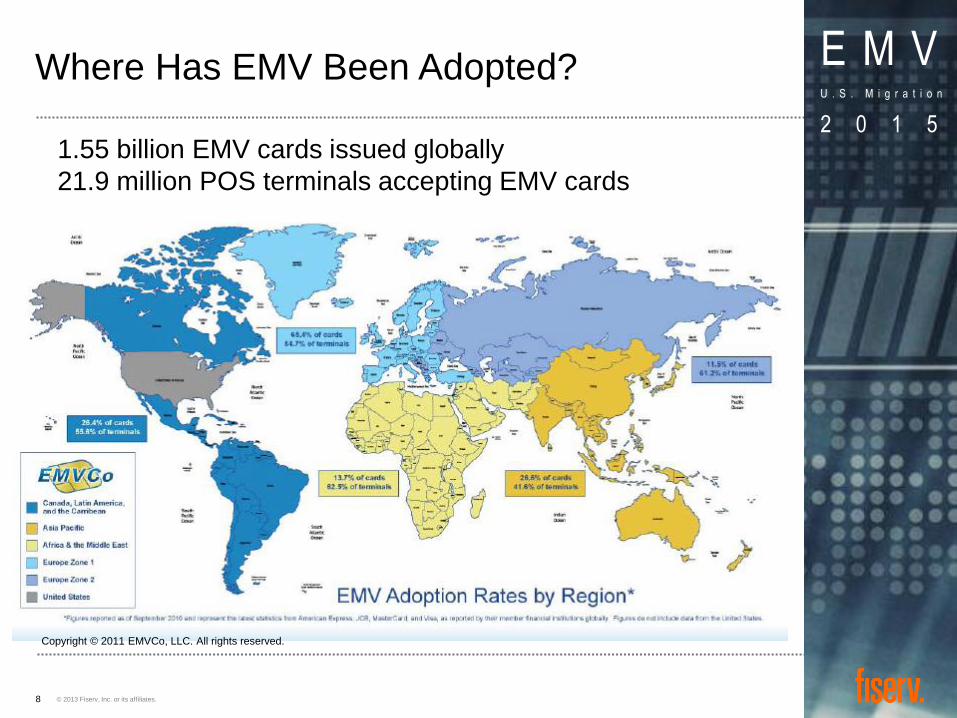

2 0 1 5 1.55 billion EMV cards issued globally

21.9 million POS terminals accepting EMV cards

Where Has EMV Been Adopted?

8

Copyright © 2011 EMVCo, LLC. All rights reserved.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

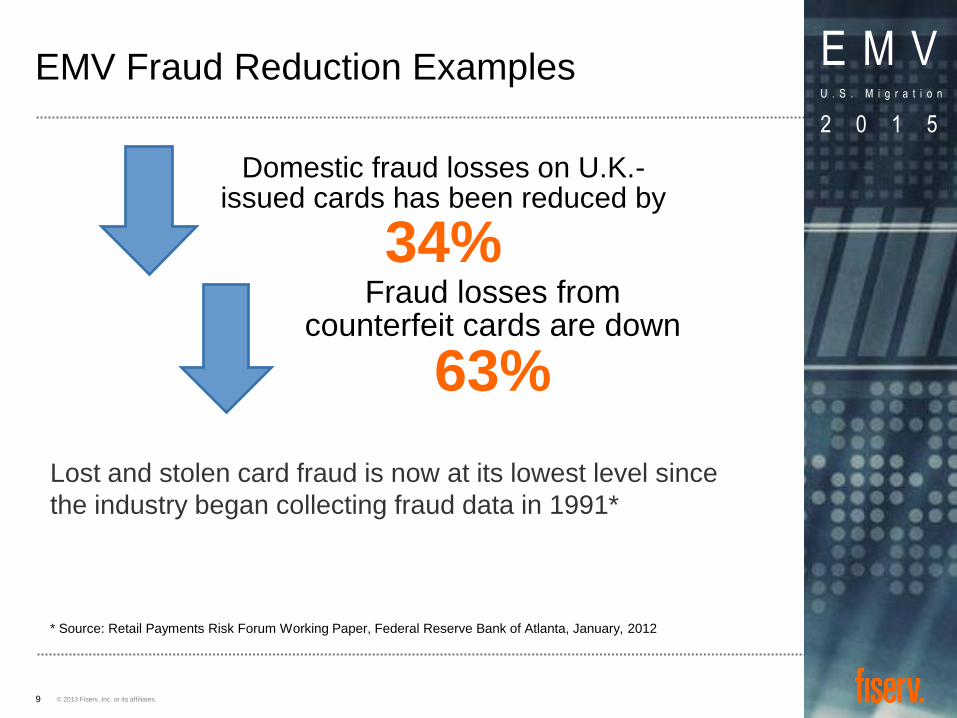

EMV Fraud Reduction Examples

9

Domestic fraud losses on U.K.-issued cards has been reduced by

34% Fraud losses from

counterfeit cards are down

63%

Lost and stolen card fraud is now at its lowest level since

the industry began collecting fraud data in 1991*

* Source: Retail Payments Risk Forum Working Paper, Federal Reserve Bank of Atlanta, January, 2012

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

U.S. Becomes an Easy Target Without EMV

10

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Fraud is Rising in U.S.

11

Discover Financial Services disclosed in its annual report

that its fraud losses in fiscal 2012 totaled $93 million —

70% higher than they were two years earlier, even

after adjusting for rising transaction volumes.

Capital One Financial reported a 20% increase in volume-adjusted fraud losses, between 2010 and 2011.

It has yet to release fraud data for 2012.

© 2013 Fiserv, Inc. or its affiliates.

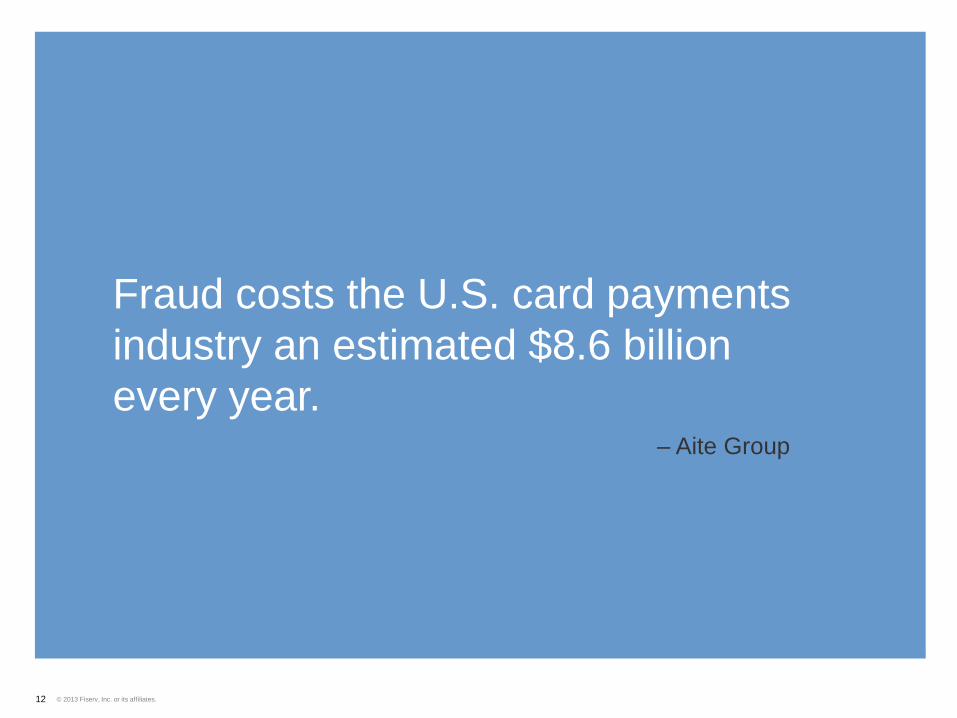

Fraud costs the U.S. card payments

industry an estimated $8.6 billion

every year. – Aite Group

12

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Lost Revenue

13

Incompatibility for International Travelers

Card issuers lost out on

nearly

$4 billion in

charge volume including

$78.7 million in interchange fees

because of problems

cardholders had with

their cards while

traveling internationally

Source: Aite Group, The Broken Promise of Anytime, Anywhere Card Payments, October 26, 2009

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

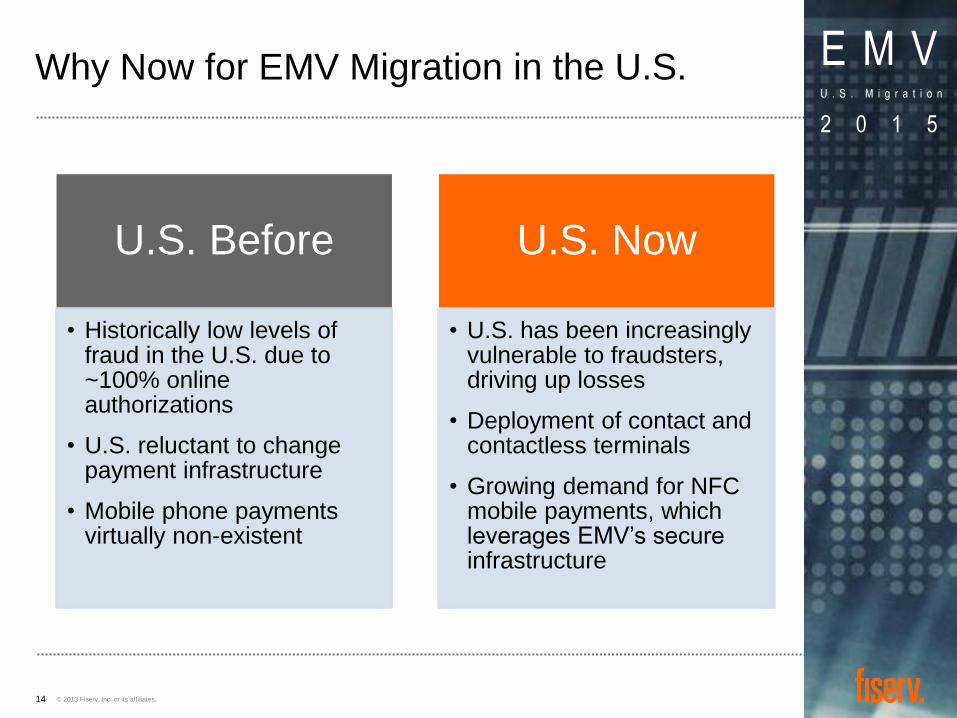

Why Now for EMV Migration in the U.S.

14

U.S. Before

• Historically low levels of fraud in the U.S. due to ~100% online authorizations

• U.S. reluctant to change payment infrastructure

• Mobile phone payments virtually non-existent

U.S. Now

• U.S. has been increasingly vulnerable to fraudsters, driving up losses

• Deployment of contact and contactless terminals

• Growing demand for NFC mobile payments, which leverages EMV’s secure infrastructure

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

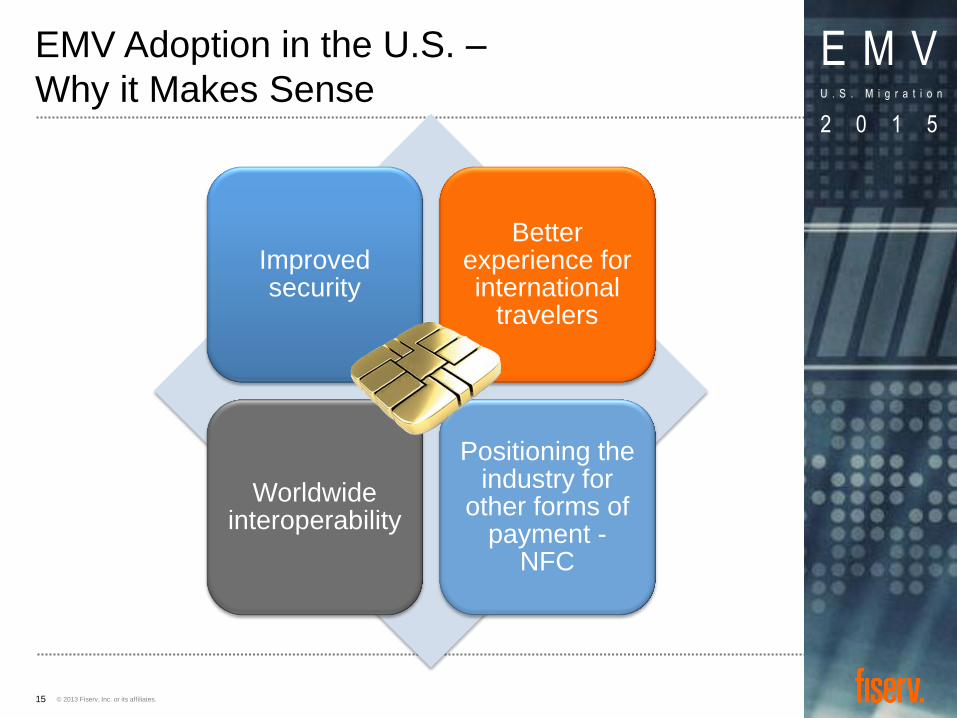

EMV Adoption in the U.S. –

Why it Makes Sense

15

Improved security

Better experience for international

travelers

Worldwide interoperability

Positioning the industry for

other forms of payment -

NFC

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

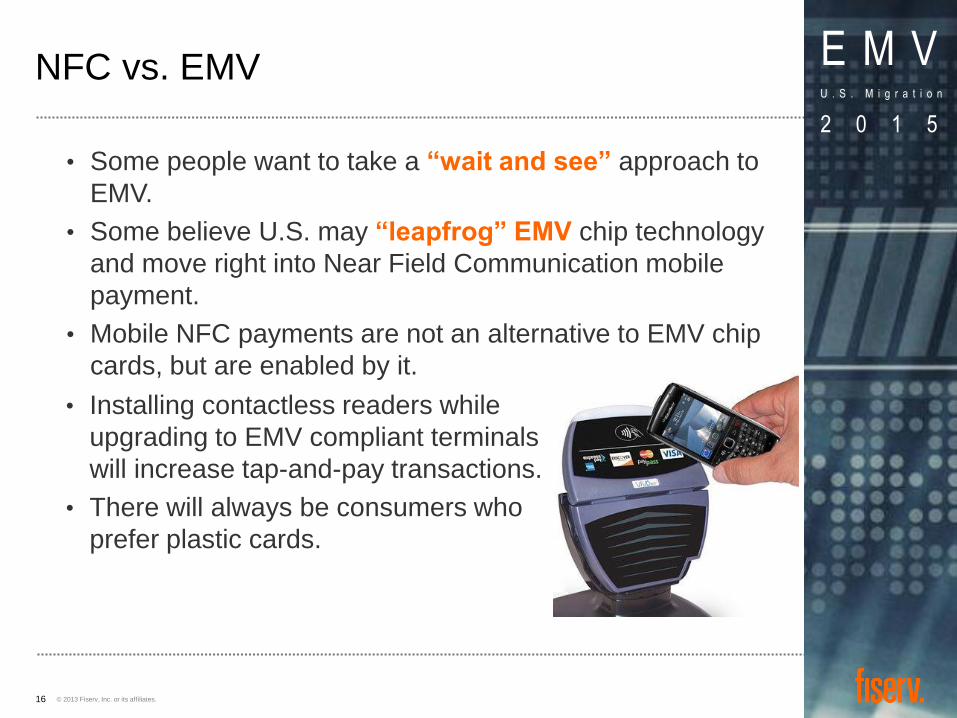

NFC vs. EMV

16

• Some people want to take a “wait and see” approach to

EMV.

• Some believe U.S. may “leapfrog” EMV chip technology

and move right into Near Field Communication mobile

payment.

• Mobile NFC payments are not an alternative to EMV chip

cards, but are enabled by it.

• Installing contactless readers while

upgrading to EMV compliant terminals

will increase tap-and-pay transactions.

• There will always be consumers who

prefer plastic cards.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

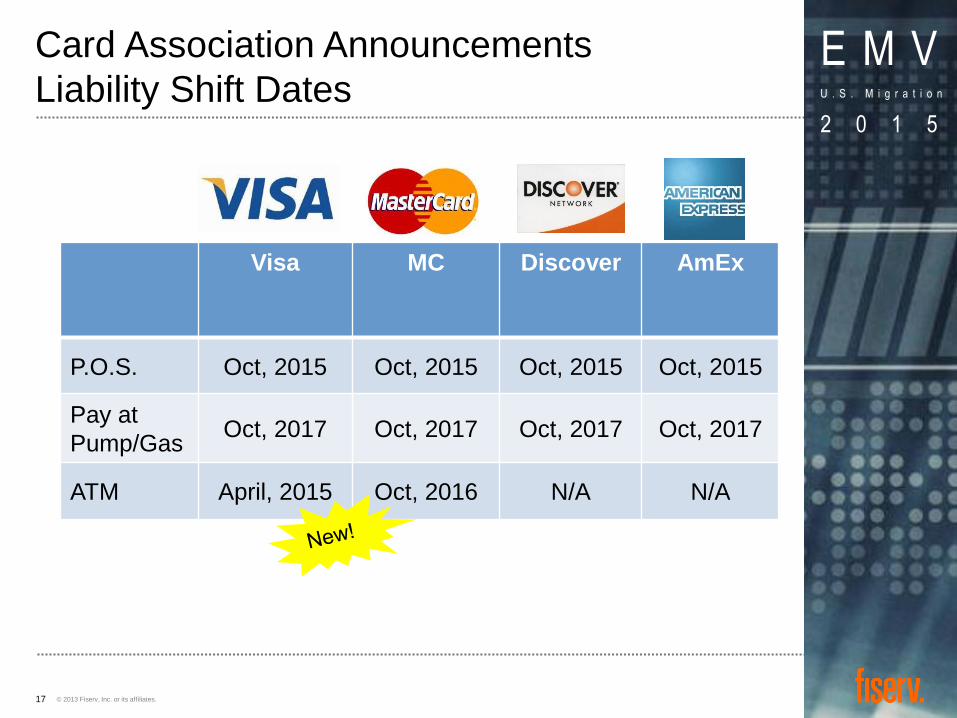

Card Association Announcements

Liability Shift Dates

17

Visa MC Discover AmEx

P.O.S. Oct, 2015 Oct, 2015 Oct, 2015 Oct, 2015

Pay at

Pump/Gas Oct, 2017 Oct, 2017 Oct, 2017 Oct, 2017

ATM April, 2015 Oct, 2016 N/A N/A

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

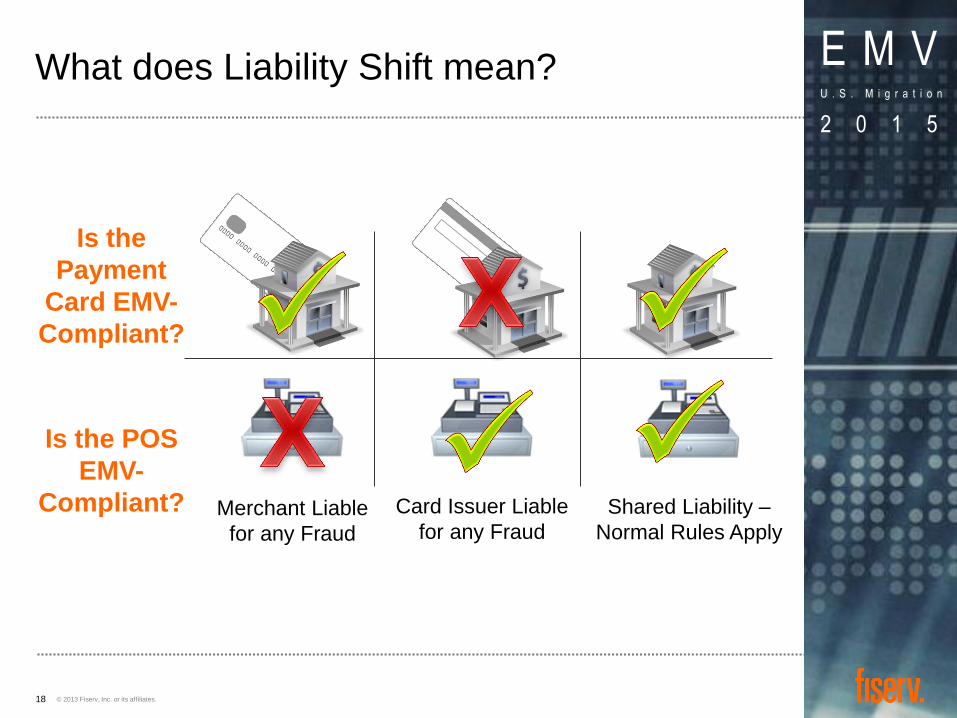

What does Liability Shift mean?

18

Is the

Payment

Card EMV-

Compliant?

Is the POS

EMV-

Compliant? Merchant Liable

for any Fraud

Card Issuer Liable

for any Fraud

Shared Liability –

Normal Rules Apply

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

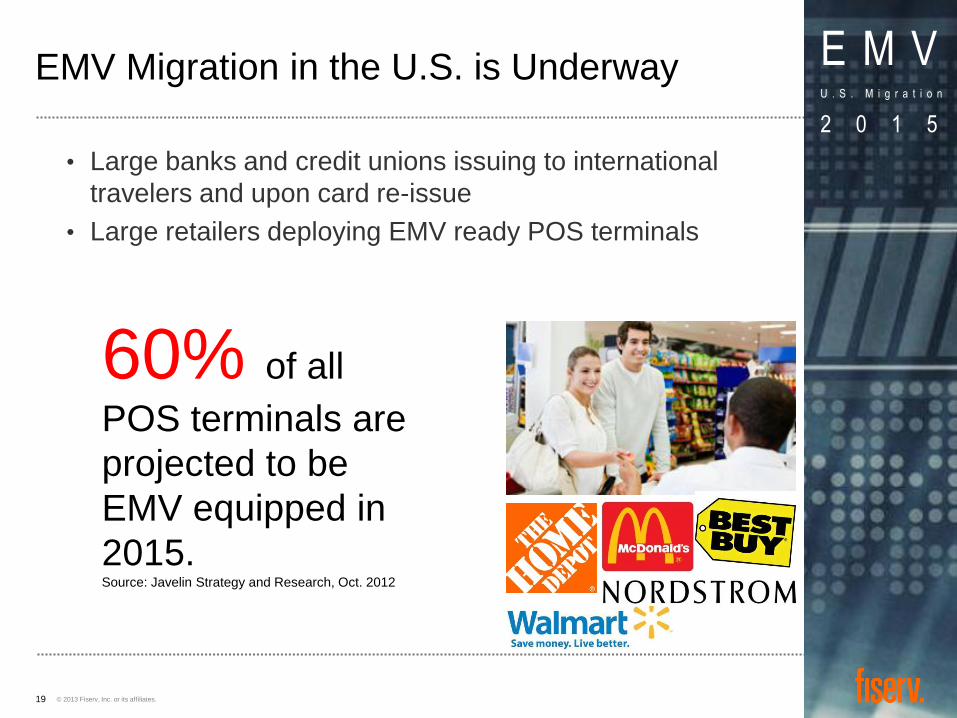

EMV Migration in the U.S. is Underway

19

• Large banks and credit unions issuing to international

travelers and upon card re-issue

• Large retailers deploying EMV ready POS terminals

60% of all

POS terminals are

projected to be

EMV equipped in

2015. Source: Javelin Strategy and Research, Oct. 2012

E M V U . S . M i g r a t i o n

2 0 1 5

EMV

Implementation

Options

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

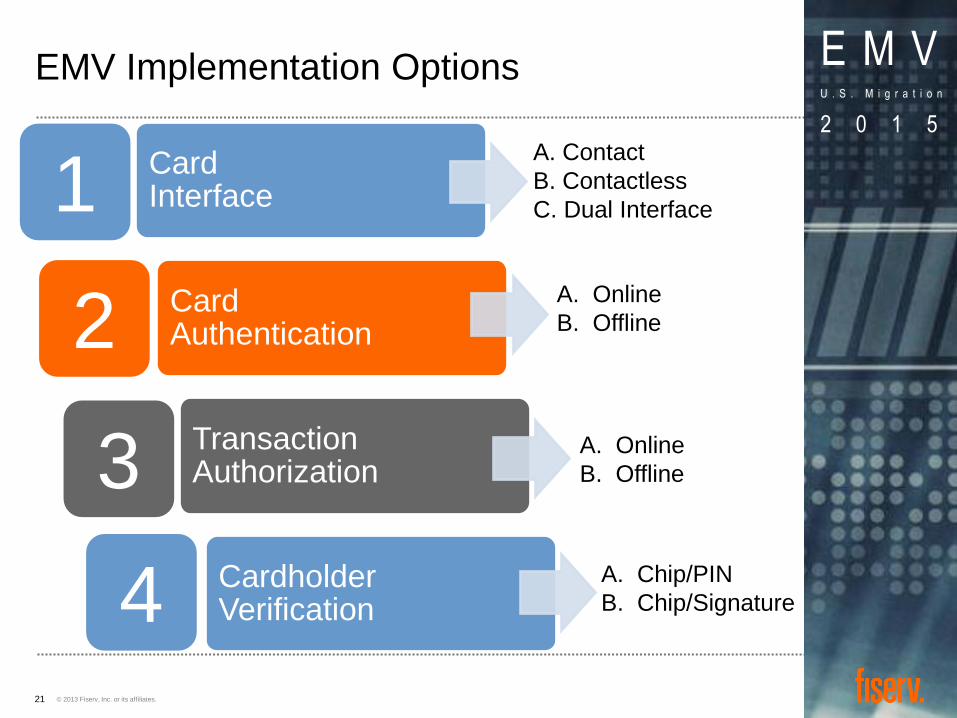

EMV Implementation Options

21

Card Interface

Card Authentication

Transaction Authorization

Cardholder Verification

1

2

3

4

A. Contact

B. Contactless

C. Dual Interface

A. Online

B. Offline

A. Online

B. Offline

A. Chip/PIN

B. Chip/Signature

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

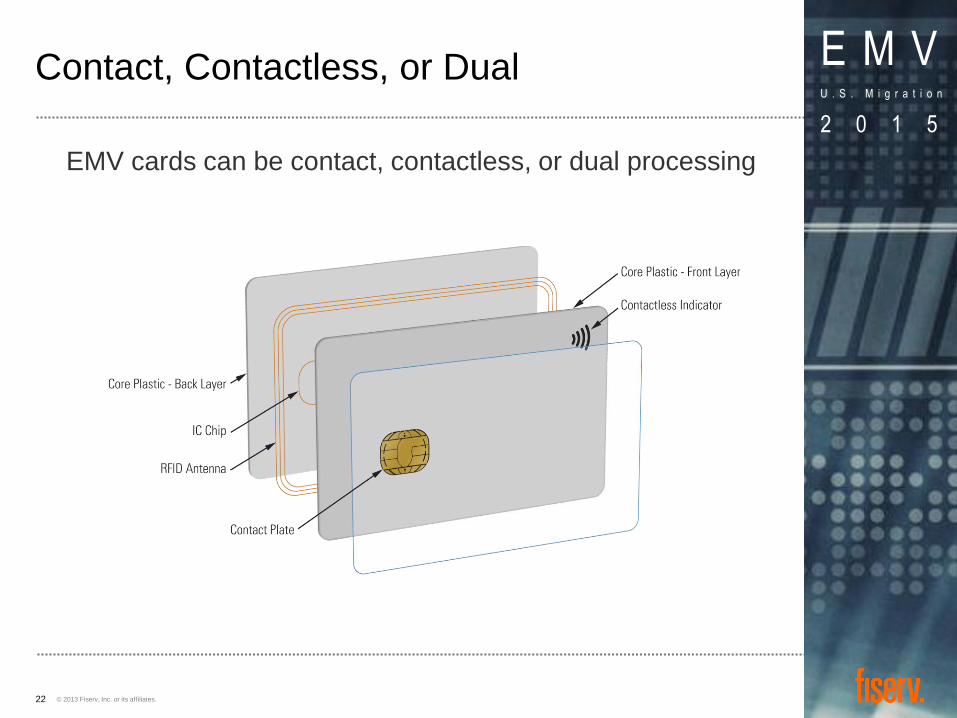

Contact, Contactless, or Dual

22

EMV cards can be contact, contactless, or dual processing

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

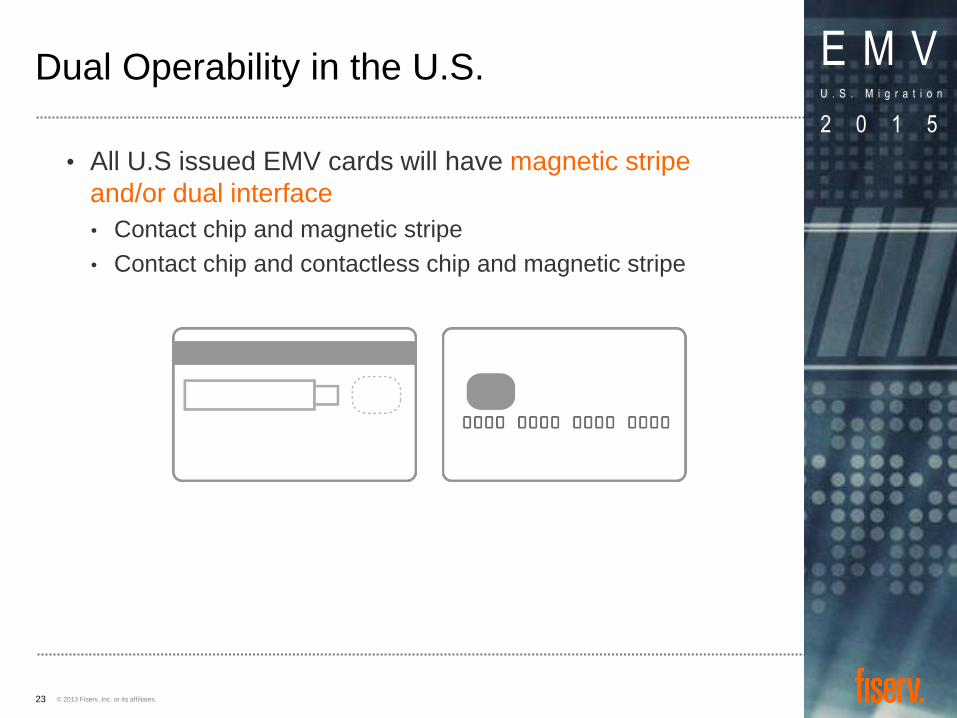

Dual Operability in the U.S.

23

• All U.S issued EMV cards will have magnetic stripe

and/or dual interface

• Contact chip and magnetic stripe

• Contact chip and contactless chip and magnetic stripe

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

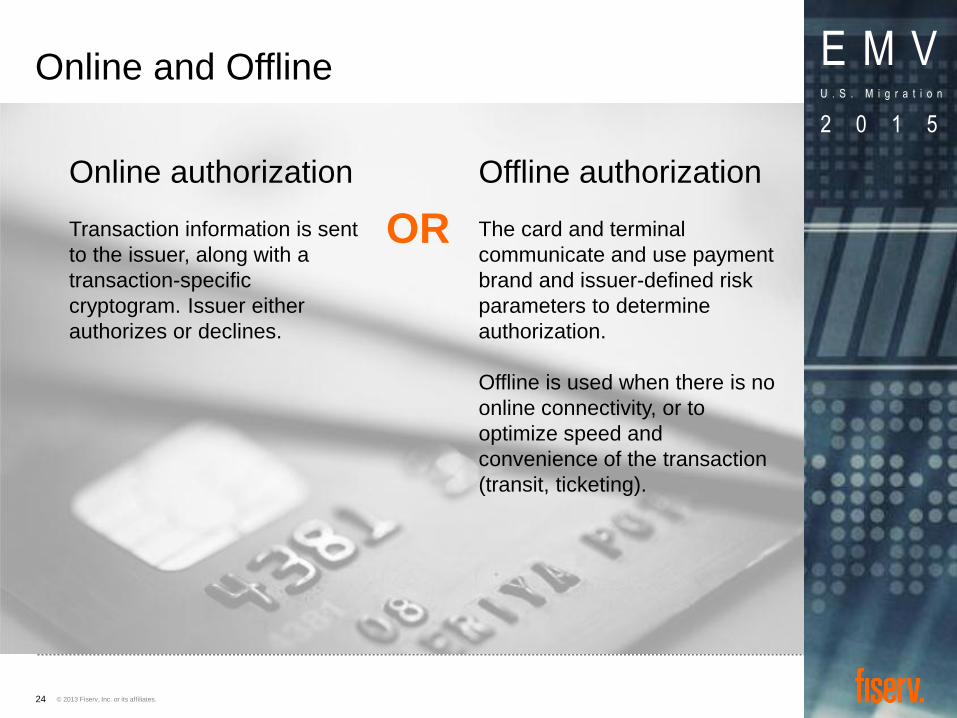

Online and Offline

24

Online authorization

Transaction information is sent

to the issuer, along with a

transaction-specific

cryptogram. Issuer either

authorizes or declines.

Offline authorization

The card and terminal

communicate and use payment

brand and issuer-defined risk

parameters to determine

authorization.

Offline is used when there is no

online connectivity, or to

optimize speed and

convenience of the transaction

(transit, ticketing).

OR

© 2013 Fiserv, Inc. or its affiliates.

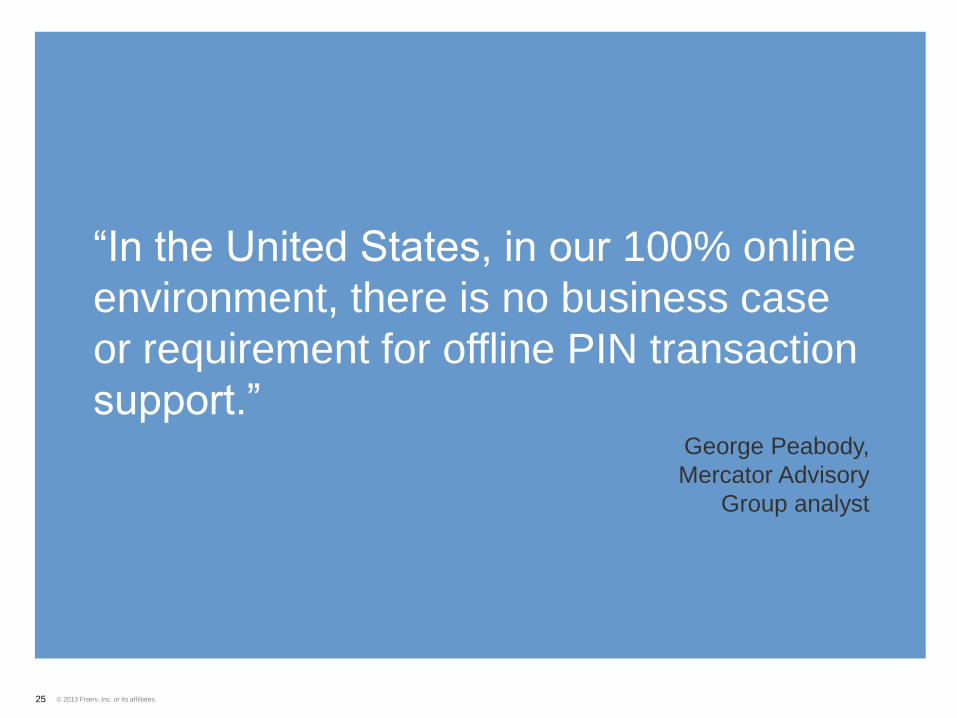

―In the United States, in our 100% online

environment, there is no business case

or requirement for offline PIN transaction

support.‖ George Peabody,

Mercator Advisory

Group analyst

25

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

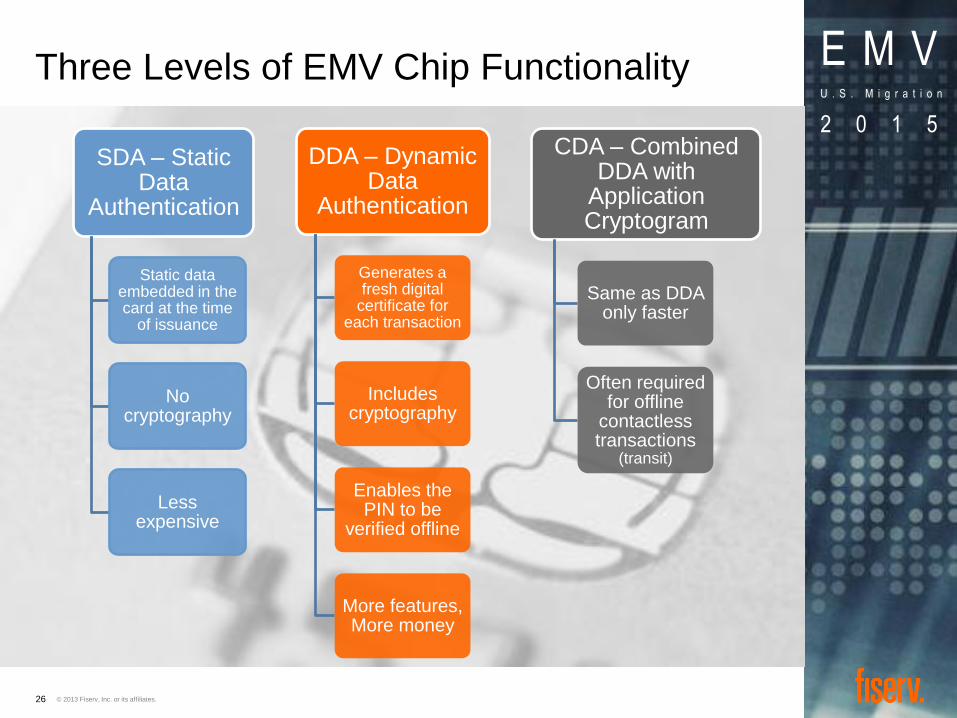

SDA – Static Data

Authentication

Static data embedded in the card at the time

of issuance

No cryptography

Less expensive

DDA – Dynamic Data

Authentication

Generates a fresh digital

certificate for each transaction

Includes cryptography

Enables the PIN to be

verified offline

More features, More money

CDA – Combined DDA with

Application Cryptogram

Same as DDA only faster

Often required for offline

contactless transactions

(transit)

Three Levels of EMV Chip Functionality

26

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

The Debate Over Signature vs. Chip & PIN

27

• Experts generally agree that Chip-and-PIN should be

the standard.

• Merchants fear that fraud losses will be higher with

signature authentication - - majority of merchant

terminals will support both.

• Chip & PIN issuers will need to decide on online-only or

both offline and online capabilities.

• When traveling abroad cardholders may experience unattended offline transactions with PIN-only machines (European train ticket kiosks, toll roads, gas pumps).

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

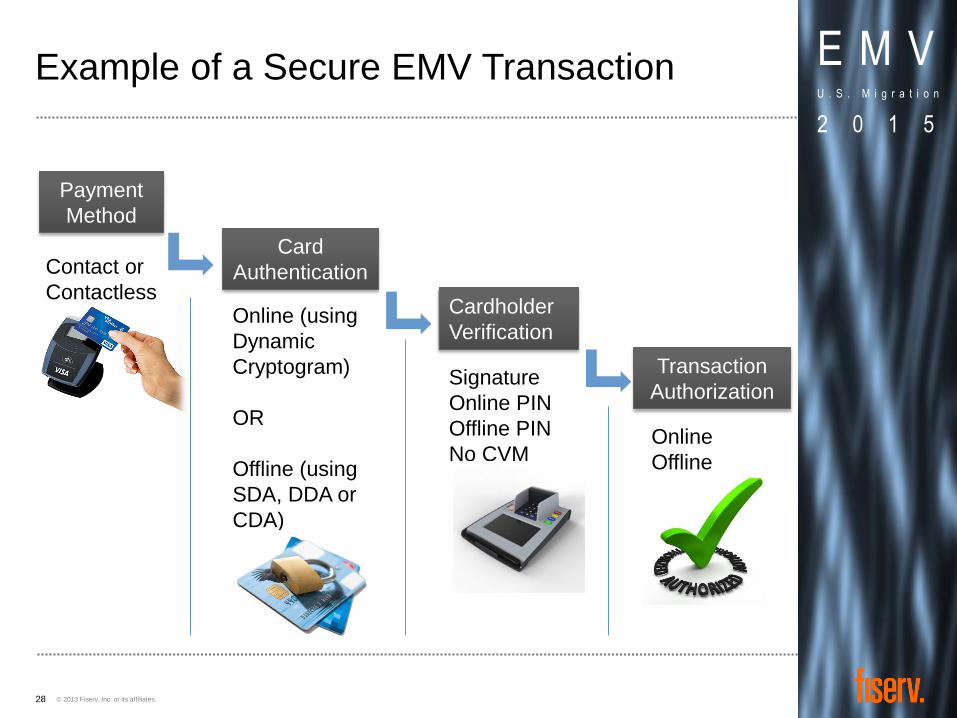

Example of a Secure EMV Transaction

28

E M V U . S . M i g r a t i o n

2 0 1 5

Contact or

Contactless

Payment

Method

Card

Authentication

Cardholder

Verification

Transaction

Authorization

Online (using

Dynamic

Cryptogram)

OR

Offline (using

SDA, DDA or

CDA)

Signature

Online PIN

Offline PIN

No CVM

Online

Offline

E M V U . S . M i g r a t i o n

2 0 1 5

EMV

Challenges

Facing the U.S.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

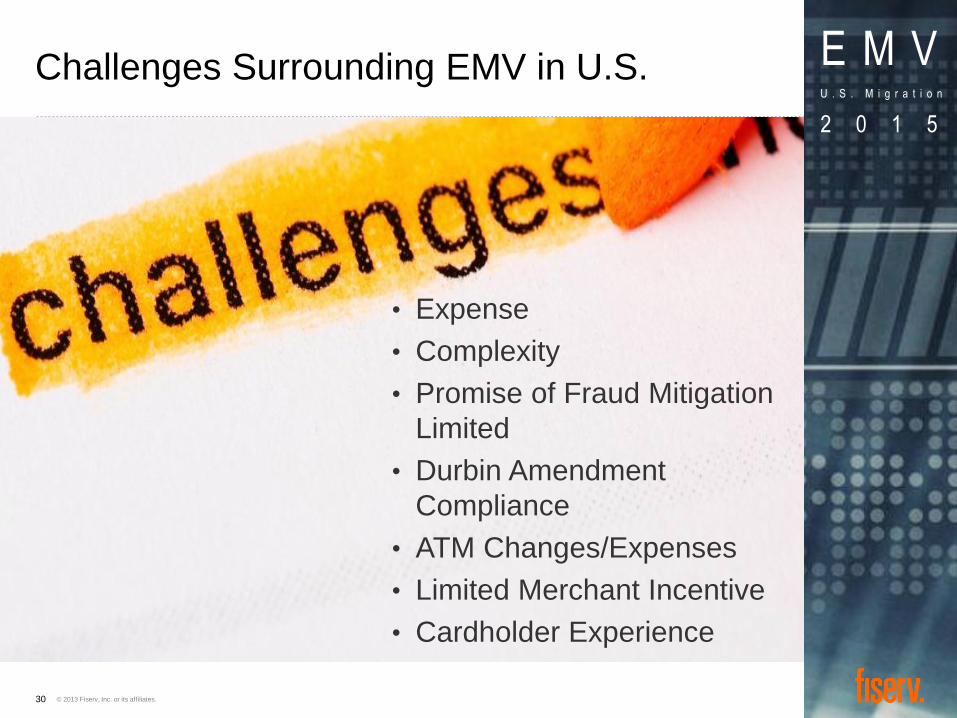

• Expense

• Complexity

• Promise of Fraud Mitigation

Limited

• Durbin Amendment

Compliance

• ATM Changes/Expenses

• Limited Merchant Incentive

• Cardholder Experience

Challenges Surrounding EMV in U.S.

30

© 2013 Fiserv, Inc. or its affiliates.

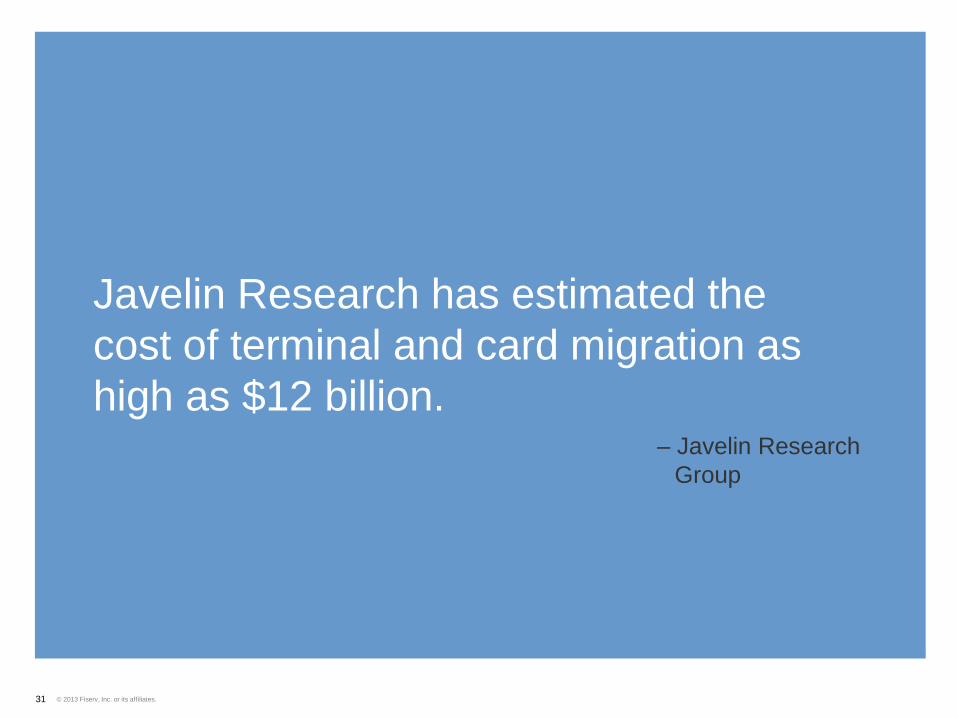

Javelin Research has estimated the

cost of terminal and card migration as

high as $12 billion. – Javelin Research

Group

31

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

EMV is Complex

32

• 1 billion payment cards in the U.S.

• 15 million POS devices

• EMV requires new security hardware and software in the

POS terminals

• Multiple configurations on chip cards

• Script and testing for

each card program

• Extensive testing needed

to avoid interoperability

failures and in-the-field

card failures.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Fraud Mitigation Limited

33

EMV cards only afford protection in a card-present

environment. Card-not-present uses is where fraud

predominately occurs.

Risk tools and PCI standards have dramatically reduced fraud

for U.S. issuers

2 times

Card-Not-Present

Fraud Losses

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

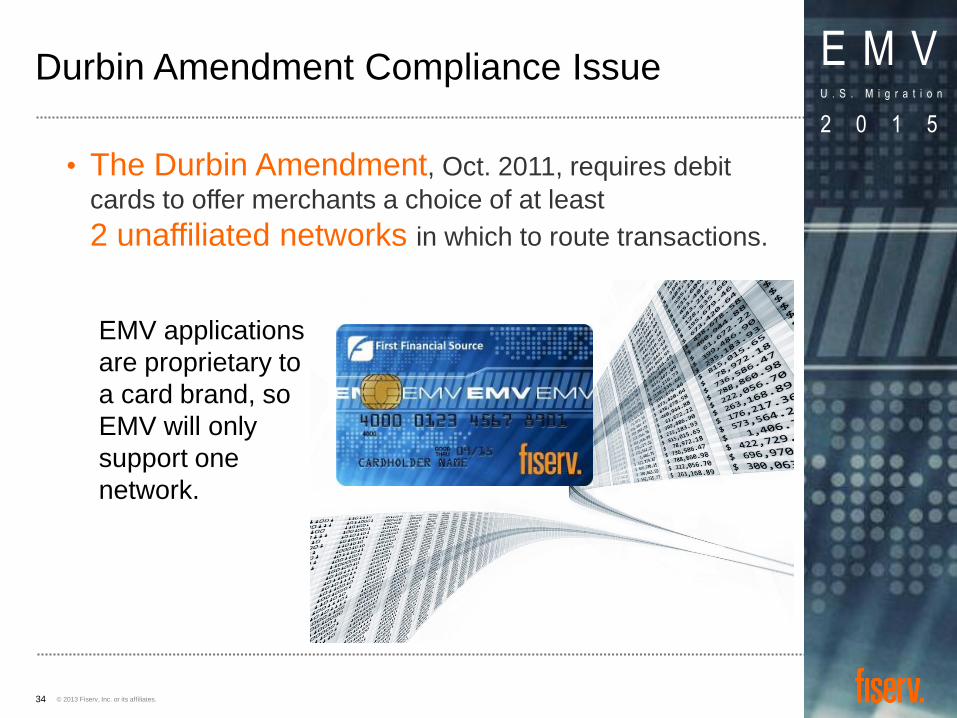

Durbin Amendment Compliance Issue

34

• The Durbin Amendment, Oct. 2011, requires debit

cards to offer merchants a choice of at least

2 unaffiliated networks in which to route transactions.

EMV applications

are proprietary to

a card brand, so

EMV will only

support one

network.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Possible Solution to Durbin Amendment

Compliance Issue

35

• EMV Migration Forum representing 18 networks is working

on a solution for a common application that would allow

merchants to have a choice in routing.

• The proposed common application ID would process the

transaction against a table of bank ID numbers to

determine which network the issuer belongs to and which

one the merchant prefers.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

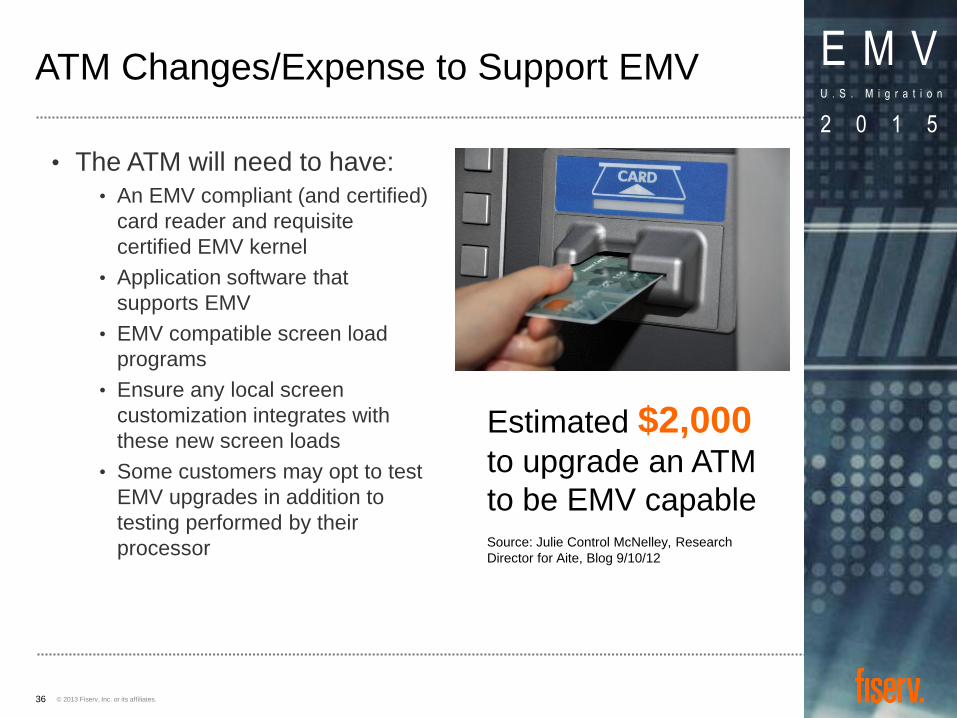

ATM Changes/Expense to Support EMV

36

• The ATM will need to have:

• An EMV compliant (and certified)

card reader and requisite

certified EMV kernel

• Application software that

supports EMV

• EMV compatible screen load

programs

• Ensure any local screen

customization integrates with

these new screen loads

• Some customers may opt to test

EMV upgrades in addition to

testing performed by their

processor

Estimated $2,000 to upgrade an ATM

to be EMV capable

Source: Julie Control McNelley, Research

Director for Aite, Blog 9/10/12

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Limited Merchant Incentive

37

• No TIP (Technology Innovation Program) for U.S.

• Merchant disagreement:

• Some retailers embracing EMV

• Others are questioning why U.S. retailers are being asked to

upgrade to an older technology that has existed for more

than a decade in Europe, instead of preparing for a more

secure, modern approach to protecting payments.

―We want

something better!‖

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Cardholder Experience

38

• Need to educate consumers on changes with new card.

• Chip card must be inserted in reader and left in for the

duration of the transaction.

• MC and Visa credit cards will most likely be signature

preferred at the POS.

• MC and Visa debit cards

will most likely be PIN

preferred at the POS.

• All ATM transactions

require PIN.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Overcoming These Challenges

39

• Adopting chip card technology in the U.S. seems

inevitable and will hold significant benefits for card

issuers.

• We will undoubtedly overcome many of these challenges

and forge ahead with EMV migration.

• 2013 will be the year of education and planning.

• 2014 may see sizeable deployment in the U.S.

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

Polling Question

40

What stage is your organization at in its EMV Migration

planning?

A. None - Haven’t started yet

B. Discovery – Learning and gathering information

C. Early Stage – Contacted processor and have begun

preliminary strategy development

D. Implementation – Active implementation. Have

issued EMV cards or are soon to be issuing

E. Don’t Know

E M V U . S . M i g r a t i o n

2 0 1 5

41

Determining

Your Approach

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

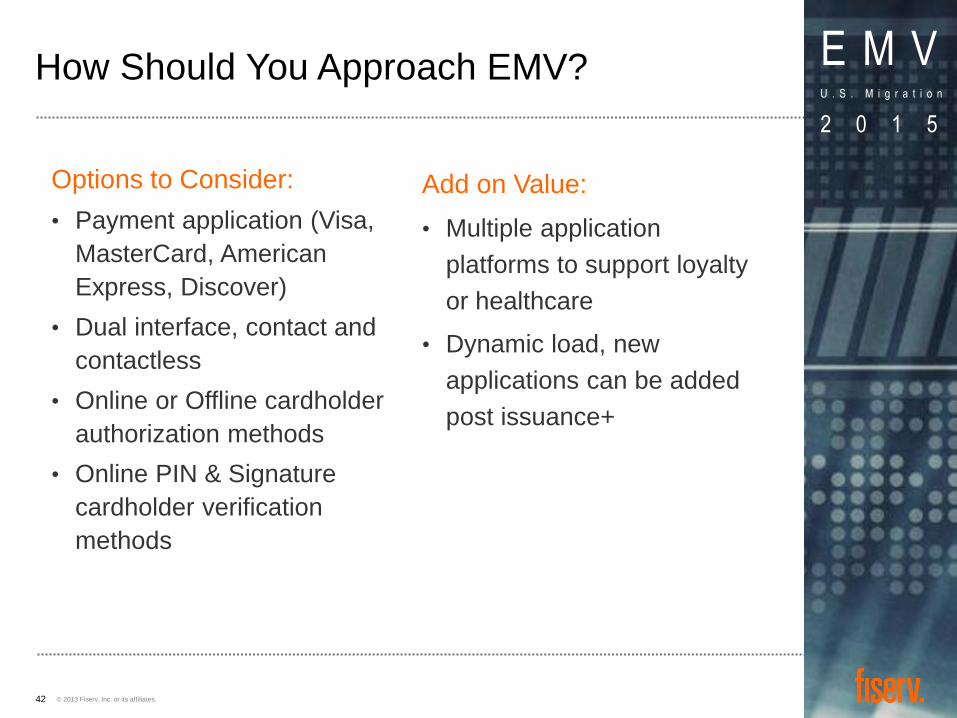

How Should You Approach EMV?

42

Options to Consider:

• Payment application (Visa,

MasterCard, American

Express, Discover)

• Dual interface, contact and

contactless

• Online or Offline cardholder

authorization methods

• Online PIN & Signature

cardholder verification

methods

Add on Value:

• Multiple application

platforms to support loyalty

or healthcare

• Dynamic load, new

applications can be added

post issuance+

E M V U . S . M i g r a t i o n

2 0 1 5

Fiserv

Readiness and

Timelines

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

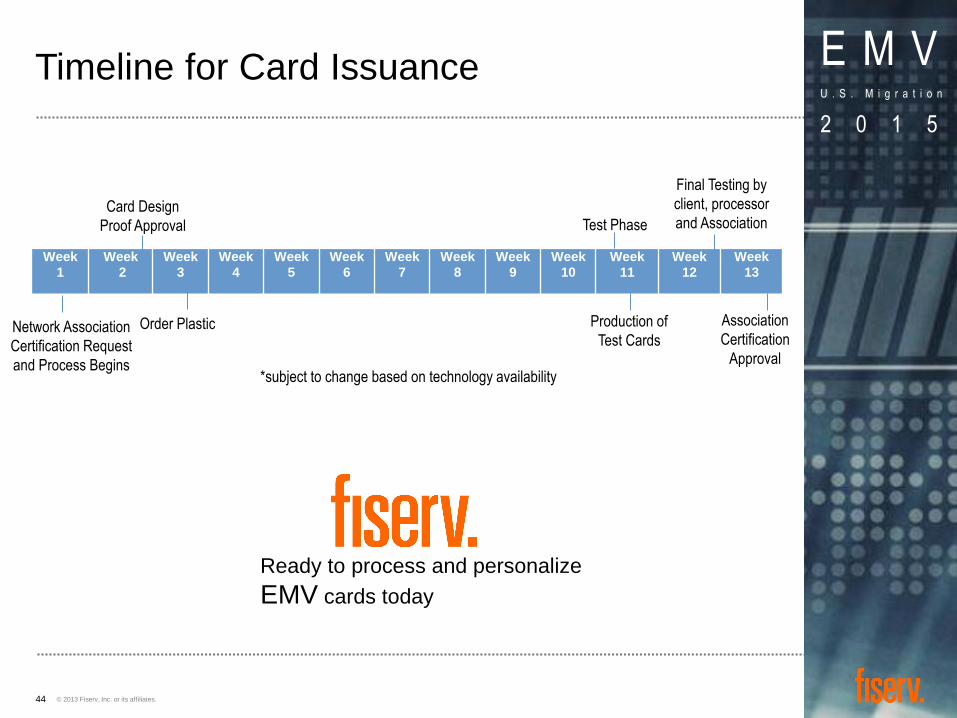

Timeline for Card Issuance

44

Week

1 Week

2 Week

3 Week

4 Week

5 Week

6 Week

7 Week

8 Week

9 Week

10 Week

11 Week

12 Week

13

Card Design

Proof Approval

Network Association

Certification Request

and Process Begins

Order Plastic

*subject to change based on technology availability

Association

Certification

Approval

Final Testing by

client, processor

and Association

Test Phase

Production of

Test Cards

Ready to process and personalize

EMV cards today

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

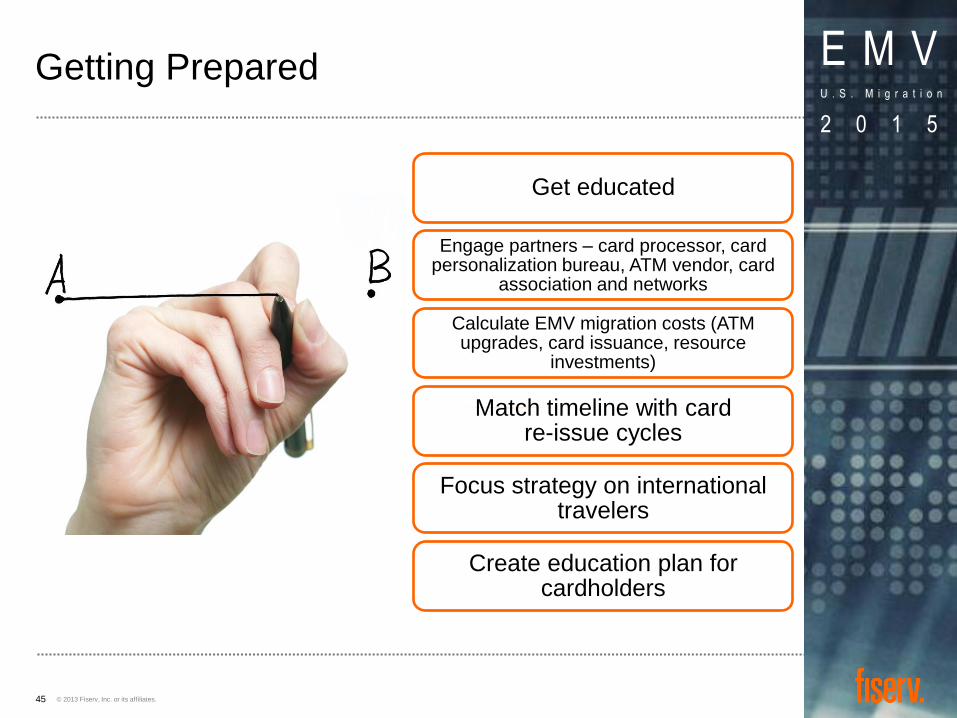

Getting Prepared

45

Get educated

Engage partners – card processor, card personalization bureau, ATM vendor, card

association and networks

Calculate EMV migration costs (ATM upgrades, card issuance, resource

investments)

Match timeline with card re-issue cycles

Focus strategy on international travelers

Create education plan for cardholders

E M V U . S . M i g r a t i o n

2 0 1 5

Questions

Sharon Pazlar

Director, Product Management

Fiserv Output Solutions

651-846-3618

© 2013 Fiserv, Inc. or its affiliates.

E M V U . S . M i g r a t i o n

2 0 1 5

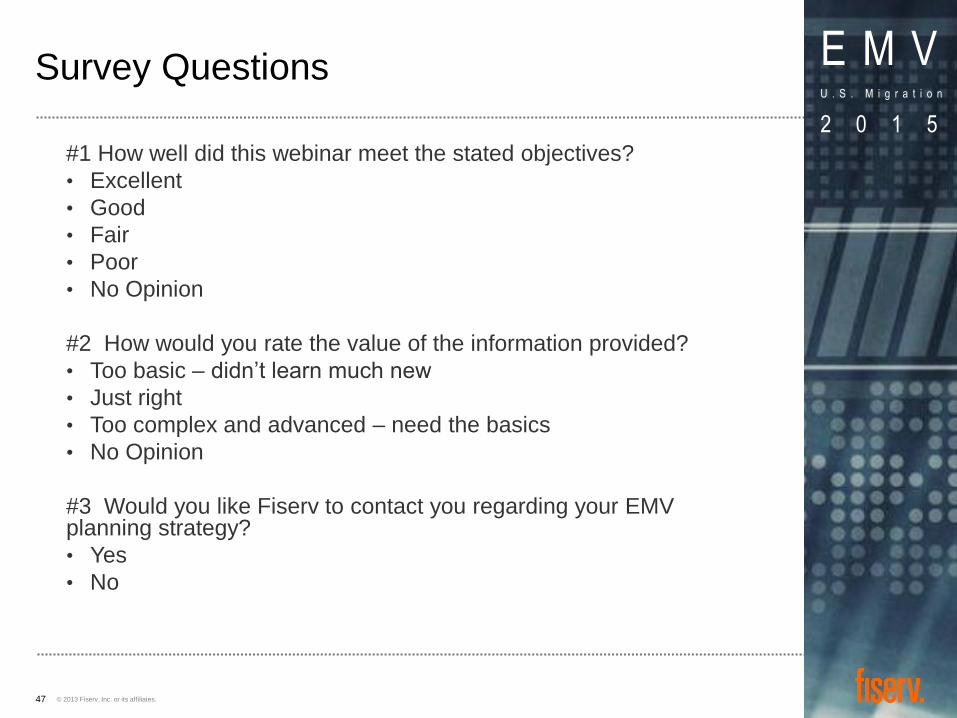

Survey Questions

47

#1 How well did this webinar meet the stated objectives?

• Excellent

• Good

• Fair

• Poor

• No Opinion

#2 How would you rate the value of the information provided?

• Too basic – didn’t learn much new

• Just right

• Too complex and advanced – need the basics

• No Opinion

#3 Would you like Fiserv to contact you regarding your EMV planning strategy?

• Yes

• No