Embed Size (px)

Citation preview

‘ECONOMIC & FINANCIAL UPDATE’

FOR

BCK WEALTH MANAGEMENT LTD

Jim Power

May 22nd 2012

INTERNATIONAL BACKDROP Euro Zone debt crisis dominating global agenda Euro Zone economy under significant pressure,

Germany the most positive, but has its problems US economy has surprised positively in 2012, but

growth still below trend UK suffering from austerity Emerging world still doing well Interest rates to remain at historically low levels for

foreseeable future – ECB will probably cut further Debt the big evil issue in developed world Fiscal consolidation will dominate developed world

agenda, with implications for global growth

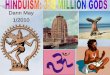

10-YEAR BOND SPREADS (19/5/12)COUNTRY SPREAD OVER GERMANY

Germany 1.42%

France +142 bps

Belgium +189 bps

Italy +437 bps

Spain +482 bps

Portugal +1,054 bps

Ireland +584 bps

Greece +2,713 bps

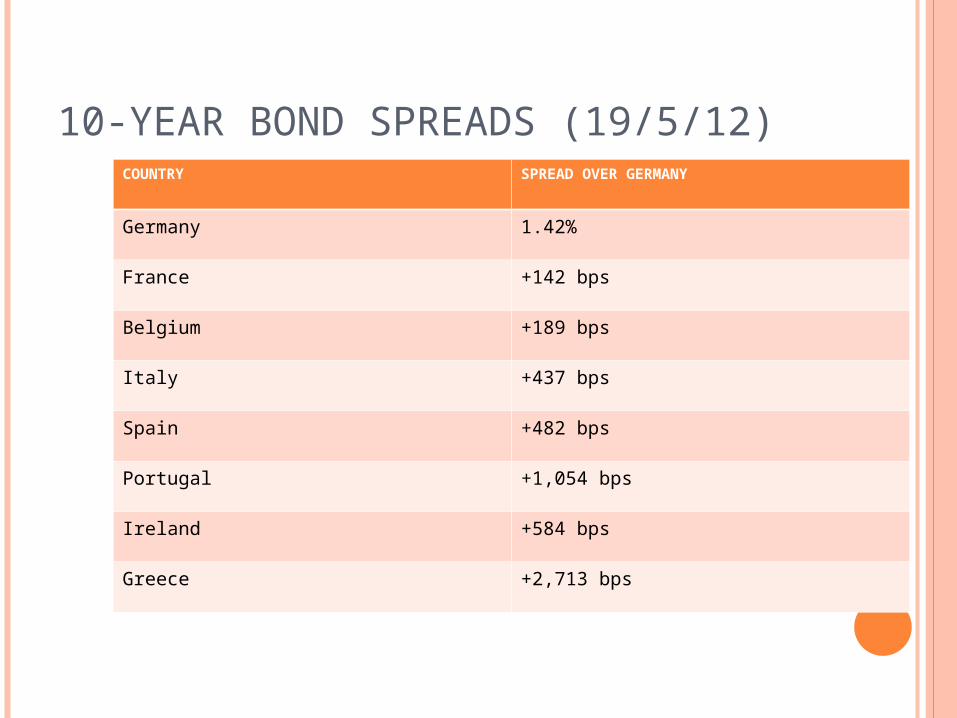

DEBT & UNEMPLOYMENT IN DEVELOPED WORLD 2012 – WHAT A MESS!

Source: OECD, Dec 2011

Gross Govt Fin Liabilities % GDP

Net Govt Fin Liabilities % GDP

Net Borrowing % GDP

Unemployment Rate (Latest)

US 103.6% 80.3% -9.3% 8.1%

Euro Area 97.9 62.8% -2.9% 10.9%

Germany 87.3% 51.6% -1.1% 6.8%

France 102.4% 66.2% -4.5% 10.0%

Italy 128.1% 100.6% -1.6% 9.8%

Japan 219.1% 134.8% -8.9% 4.5%

UK 97.2% 68.9% -8.7% 8.3%

Canada 92.8% 36.6% -4.1% 7.2%

Ireland 118.8% 72.5% -8.7% 14.3%

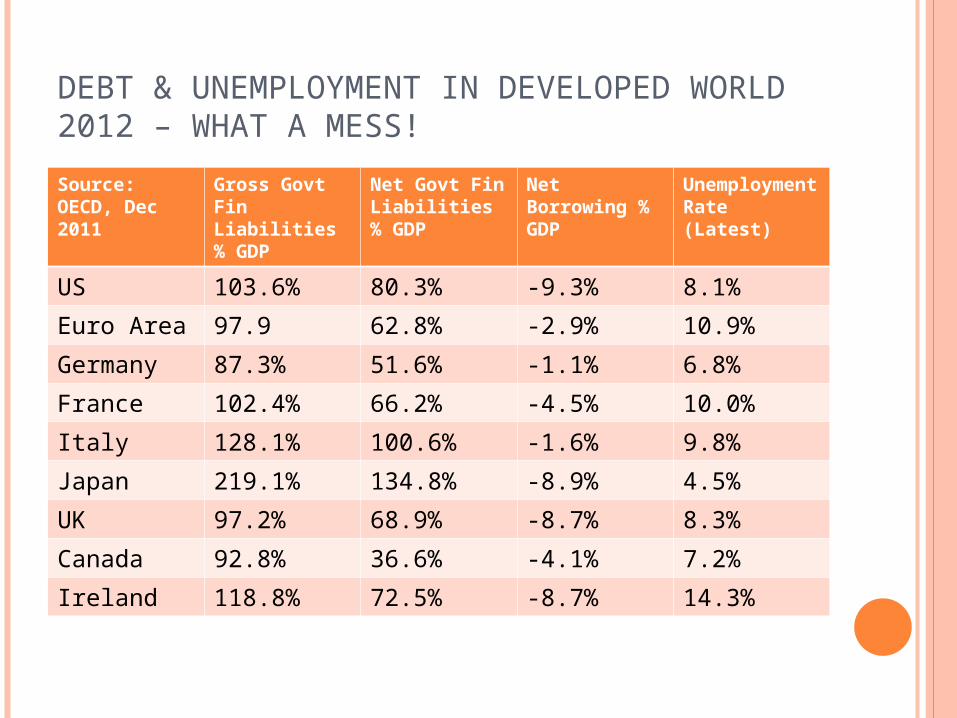

THE EURO ZONE CRISIS Perception that crisis had eased at beginning of year,

now back with a bang Strong and unorthodox approach to – very non-

Germanic Realisation that cost of keeping EMU together < cost

of it falling apart Can Greece possibly survive? If not, implications for

the rest very tricky Spain, Portugal, Ireland and Italy face serious

challenges Another LTRO/more bond purchasing/further interest

rate cuts etc etc – a lot more work to be done Fiscal Compact small step towards solution – impose

new rules on fiscal management

THE FISCAL COMPACT

Crisis has exposed deep flaws in EMU structure

Lack of banking oversight; fiscal federalism & super finance ministry; Political union; Euro Debt Agency; Fiscal Discipline; lack of focus on growth

Structural Deficit not to exceed 0.5% GDP; Debt not to exceed 60% GDP; strict EU oversight/European Court of Justice

Rules based approach to fiscal management or political fig leaf?

What choice for Ireland?

IF IRELAND VOTES NO Ireland cannot prevent ratification of Treaty – 12 of 17 Euro

Zone countries required No obvious upside from voting NO Risk premium on Irish debt would increase In event of not being able to return to markets, could not

access ESM-would depend on more expensive funding Will undermine confidence in Ireland Impact on FDI? Would require greater austerity – delivery of public services

would come under massive pressure Croke Park deal shredded? Hard choices would become even harder Potential relief on promissory notes would be undermined Could we remain part of the euro?

THE IRISH ECONOMY TODAY?

Export sector doing well – broadly based Domestic Demand still very weak In 2011 GDP +0.7% but GNP -2.5% Two ‘Pillar Banks’ allegedly starting to lend at modest rates – long

way to go to normal credit conditions Public finances stabilising-deficit gradually narrowing-tax take ahead

of target Competitiveness gradually improving Households saved €12.9 bln in 2011: Gross Savings Ratio 14.1% IDA created extra 13,000 jobs in 2011 – inflow FDI continuing in

2012 House prices still falling -49.3% Sept 2007-March 2012 Bond yields have fallen-markets have greater confidence in policy-

but they remain high International coverage much more positive – Ireland perceived to be

taking the pain and doing the right things

SO FAR IN 2012

Q1 Retail Sales Volume -1.3%; Value -0.9% Q1 Retail Sales Ex-Cars Volume -2.6%; Value -1.8% Q1 Manufacturing Output -3.3% ‘Modern’ -2.0% ‘Traditional’ -

5.4% Jan-Feb Merchandise Exports +2.7% Live Register April -40,300 from July 2011 peak – role of

emigration? Jan-April 2012 Exchequer Deficit €7.1 bln (€9.9 bln in 2011) –

tax take ahead of target €370 million Credit remains very weak – SME sector a particular concern Housing activity continues to weaken Still a very challenging environment

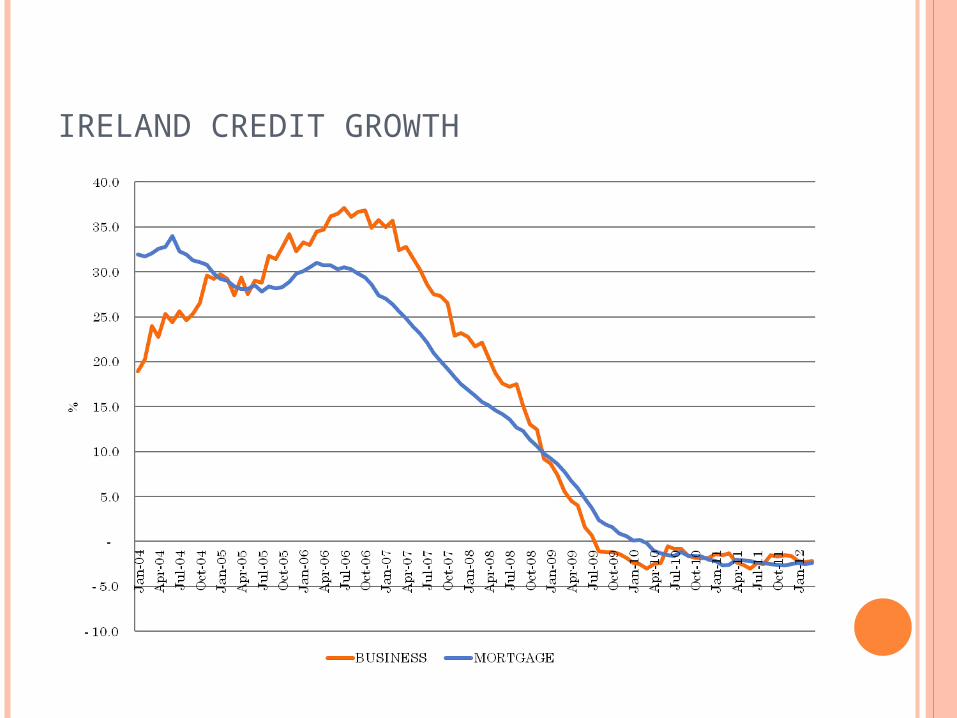

IRELAND CREDIT GROWTH

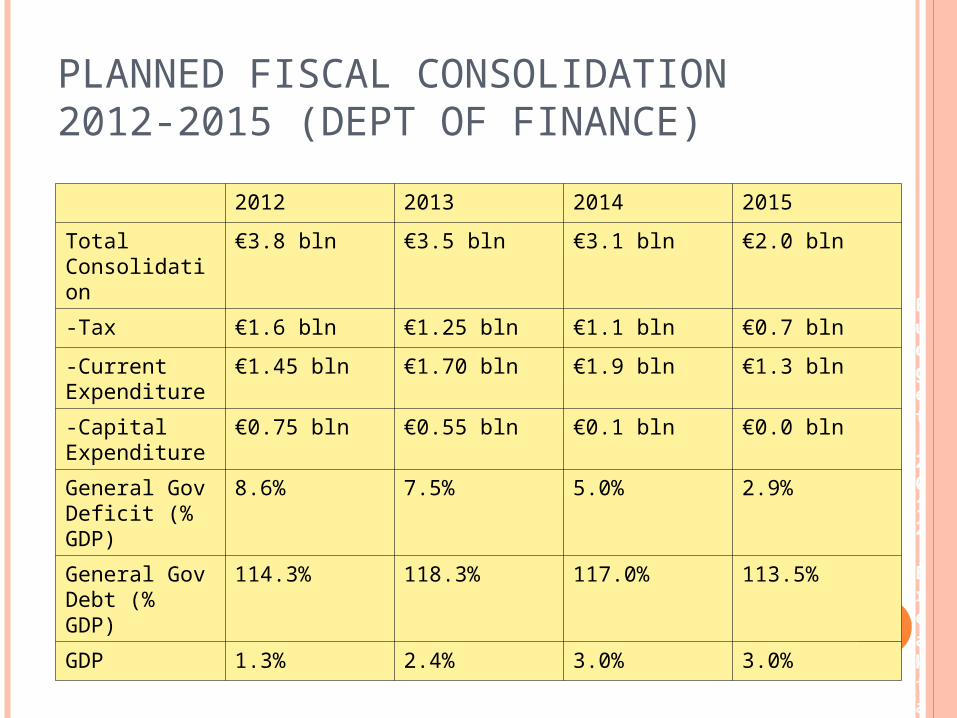

PLANNED FISCAL CONSOLIDATION 2012-2015 (DEPT OF FINANCE)

2012 2013 2014 2015

Total Consolidation

€3.8 bln €3.5 bln €3.1 bln €2.0 bln

-Tax €1.6 bln €1.25 bln €1.1 bln €0.7 bln

-Current Expenditure

€1.45 bln €1.70 bln €1.9 bln €1.3 bln

-Capital Expenditure

€0.75 bln €0.55 bln €0.1 bln €0.0 bln

General Gov Deficit (% GDP)

8.6% 7.5% 5.0% 2.9%

General Gov Debt (% GDP)

114.3% 118.3% 117.0% 113.5%

GDP 1.3% 2.4% 3.0% 3.0%

Budget 2012 Breakfast Briefing

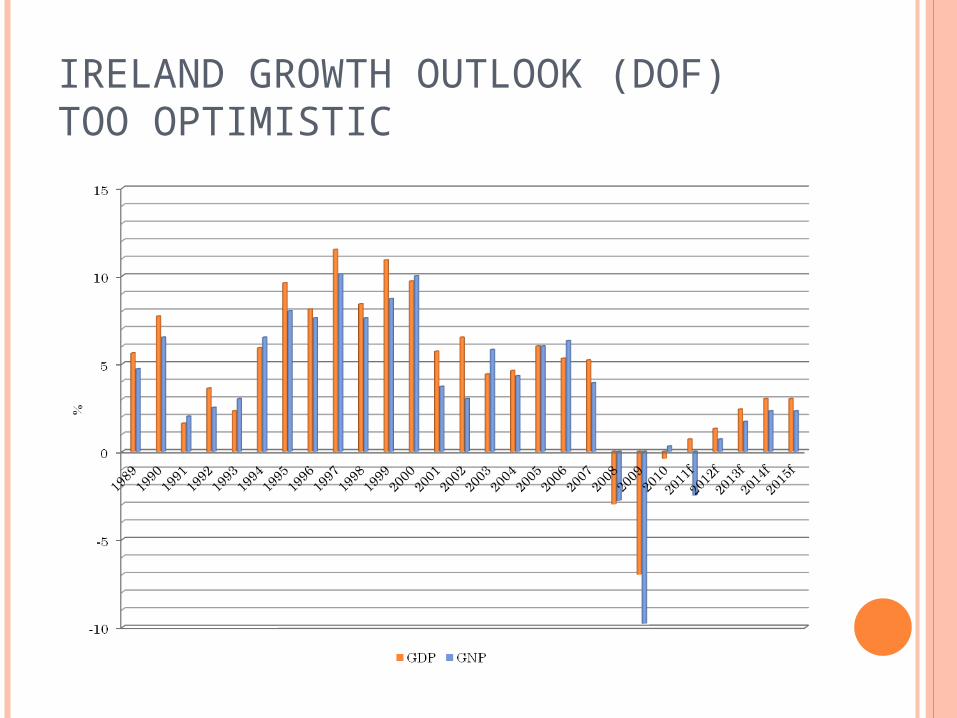

IRELAND GROWTH OUTLOOK (DOF) TOO OPTIMISTIC

THE CHALLENGES AHEAD

Restoring sustainable public finances Improve competitiveness Market the country aggressively Sort personal debt overhang Rebuild sustainable economic model – identify

and nurture sectors that will represent the future

Continue to negotiate debt relief Create functioning banking system Create confidence Recovery in domestic demand the imperative and

the challenge

Any Questions?

![Pseudo-BCK algebras as partial algebras · 2 Pseudo-BCK semilattices In this paper, we examine a certain class of pseudo-BCK algebras [23]. As the ad-junct “pseudo” suggests,](https://img.pdfslide.us/doc/110x75/5fc171594abab747344e561d/pseudo-bck-algebras-as-partial-2-pseudo-bck-semilattices-in-this-paper-we-examine.jpg)