Embed Size (px)

Citation preview

April 2017

INSIDEFlying cars vs autonomous vehicles

The power of chatbots

Spotlight on Australia

Quarterly and monthly data reports

E-commerce boosts consumer

April 2017 I 2

Contents

Global Corporate Venturing

Address: 52-54 Southwark Street, London SE1 1UN

Published by Mawsonia Ltd™, all rights reserved, unauthorised copying and distribution prohibited. © 2017

Editor-in-chief: James Mawson Email: [email protected]

Features editor: Nicole Idar Lee Email: [email protected]

News editor: Rob Lavine Email: [email protected]

Reporter: Thierry Heles Email: [email protected]

Chief operating officer: Tim Lafferty Tel: +44 (0) 7792 137133 Email: [email protected]

Production editor: Keith Baldock

Website: www.globalcorporateventuring.com

3 Editorial: Customer choices – the key to innovation

5 News 11 Big deal: NBCUniversal invests $500m in a Snap 12 Big deal: MuleSoft musters $221m in IPO 13 Big deal: Flipkart files away $1bn 14 Big deal: iFlix inflates funding with $90m 14 Analysis: Venture and maturity go hand in hand

16 Interview: Corporate-startup collaboration goes to the Heart Tomasz Rudolf, the Heart

19 Sector focus: E-commerce expansion boosts consumer sector 26 Interview: John Haugen, 301 Inc 27 Interview: Ben Lee, CircleUp

30 New technologies: Flying cars versus autonomous vehicles 32 Interview: Thomas d’Halluin, Airbus Ventures 33 Viewpoint: Jon Lauckner, GM Ventures; Varun Jain, Qualcomm Ventures; Raj Singh, JetBlue Technology Ventures

35 Spotlight on UK innovation 35 Interview: Francesca Wuttke, Merck Global Health Innovation Fund 36 Interview: Paul Morris, UK Department for International Trade VC unit

38 Comment: The product launch fallacy of big consumer packaged goods Ryan Caldbeck, CircleUp

40 Comment: 2017 Startup Outlook Tracy Isacke, Silicon Valley Bank

41 Comment: Embracing innovation means thinking about the future Neal Hill, BDC Capital

42 Comment: Seeding Canada’s VC innovation ecosystem Whitney Rockley and Scott MacDonald, McRock Capital

44 Comment: CVCs back tech investment in the UK and Ireland Stuart McKnight, Ascendant Corporate Finance

46 Comment: Fintech chatbots: are they worth the hype? Jeff Allen, Mastercard

49 Gaule’s Question Time: Bill Taranto, Merck Global Health Innovation Fund

52 University Corner: Touchstone highlights the allure of immunotherapy

53 Government House: Airbnb booking takes CIC beyond infrastructure

54 Innovative region: Australia bolsters triple helix collaboration 57 University venturing in Australia 58 Profile: Reinventure pioneers fintech venturing model

60 Analysis: Last month’s venturing activity

64 Quarterly report

April 2017 I 3

EDITORIAL

www.globalcorporateventuring.com

Why do customers choose to buy one product or service rather than another? Clayton Christensen, the Harvard Business School professor who coined the phrase “disruptive innovation”, believes companies fail because they have neglected this critical question.

In his new book – Competing Against Luck – Christensen argues that in order to innovate effectively, companies must recognise that customers buy a particular product “to get a job done”. The key insight is that customers are not looking for a product – they have a job that needs to be seen to.

For example, if a fast-food restaurant wants to sell more milk shakes, the owner must first understand the nature of the job that has led customers to “hire” that brand of milk shake. Having studied the “job to be done” in the milk shake case, Christensen’s team discovered that customers hired the beverage to perform a specific task depending on the time of day. In the morning, the job was to provide a treat for customers during their morning commute. So to sell more milk shakes in the morning, the restaurant should offer a thicker, more viscous drink that takes longer to consume, to keep customers occupied during a long dull commute, Christensen’s team concluded.

Customer choices – the key to innovation

Nicole Idar Lee, features editor

Startupsector

Investors' sectorIT Financial Media Health Telecoms Services Industrial Consumer

ITHealthConsumerMediaServicesFinancialTransportIndustrialEnergyTelecomsTotal 149

113

10112021471124

1503

212510

433

122445

1771466

16412232

544

2071065

154

1924221092

285

2

22

6263

10

34814

41921488863

685

51739

16268542397597

125

71089

23375467627354

323

Corporate activity in startups

2015

2016

ITHealthConsumerServicesMediaFinancialTransportIndustrialEnergyTelecomsTotal 137

117

10117

1855

720

164732

14162016

81167

1642

193212

737

112744

1831288

112440311048

257

12

3

31

23710

3342168

279948541277

52976

17253056565636

240

553

68

33125

34534791

156

Transport Energy

381

2551

1

14

50222

2614

21

10

492

285

113

18

76131

493

4249

April 2017 I 4

EDITORIAL

www.globalcorporateventuring.com

Identifying the “job to be done” matters not just for milk shake providers, but for any corporate concerned with innova-tion. This month’s issue of GCV focuses on the consumer sector, which is getting to grips with major disruptions in the type of “jobs” customers want done. Investment professionals who spoke to GCV noted that for today’s consumers of packaged goods, the job to be done is more multi-faceted – “reflect my values as well as taste good and improve my health”, for instance.

Or as Ben Lee, managing director of funds at CircleUp, a US-based investment platform that connects early-stage consumer brands with investors, put it: “Even the act of selecting a household cleaner is now a form of self-expression.” (See interview). The failure to recognise the shift in jobs customers want done in the consumer sector might help to explain why incumbents in the consumer packaged goods sector are los-ing market share.

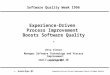

One way to import innovation could be by investing in emerging enterprises, and according to data from GCV Analytics, consumer CVCs appear to be among the laggards when compared with other sectors, such as services and industrials. The chart on the previous page shows the number of corporate-backed fundraising rounds in 2016 and 2015, separated by sector. Consumer CVCs were involved in the third-lowest number of rounds after energy and transport when compared with other sectors – 137 in 2016, down from 149 in 2015.

GCV contributing editor Tom Whitehouse’s feature on the flying cars versus autonomous ground vehicles debate offers another way of thinking about Christensen’s “jobs to be done” theory (see New technologies). We might be used to thinking of France-based Airbus as an aerospace company, but if we think in terms of the job to be done – “move me from point A to B quickly and efficiently” – it becomes clear why Thomas d’Halluin, CEO of the US office of Airbus Ventures, describes the ecosystem that Airbus’s CVC unit is operating in as “urban air mobility” (see interview). Whitehouse will be moderating a panel debating flying cars versus autonomous vehicles at the GCV Symposium in London on May 23.

In the meantime, join GCV at the Canadian Corporate Innovation Summit, to be held April 11-13 at the Fairmont Royal York in Downtown Toronto. This year’s summit will consider questions such as how cor-porations can identify relevant innovation strategies and incorporate them into their operations for greater agility and profitability. Use the code GCVBDC2017 when registering at www.ccisummit.ca to get a 20% GCV reader discount.

With this issue, my time as features editor of GCV magazine has come to a close. Thanks to the GCV team, our guest columnists and our loyal readers, without whom this magazine would not be possible. It has been a privilege and a pleasure serving as features editor, and I hope you will all enjoy this issue as much as I have.

For more insights on innovation, see GCV’s interview with Tomasz Rudolf, founder of the Heart, a Warsaw-based Euro-pean centre for corporate-startup collaboration, and our Spotlight on UK Innovation. u

Consumer CVCs appear to be among the laggards when compared with other sectors

The Coller Institute of Venture 2017 annual conference – Hong Kong

Tim Lafferty, chief operating officer of Mawsonia, the parent company of Global Corporate Venturing and sister titles Global University Venturing and Global Government Venturing, will be a keynote speaker at the Coller Institute of Venture 2017 (CIV2017) in Hong Kong on April 21.

The event, organised by the Coller Institute, includes on its speaker list such luminaries as Lita Nelsen, former director of the MIT technology licensing office, Jeremy Coller, chief invest-ment officer of secondaries firm Coller Capital and a Mawsonia shareholder, and Prof Dong-min Chen, director of the science and technology office of Peking University.

The event brings together policymakers, venture capitalists, governments, universities and others to help universities evolve from being research institutions into their new role as cen-tres of venture and innovation. Delegates will also have the opportunity to visit innovation centres in Shenzen.

For more information, visit: https://civ.global/civ2017hk/

In addition, CIV2017 will have a panel at the Association of University Technology Managers (AUTM) Asia conference the following day: http://autmasia2017net.youdomain.hk/en/home/

Tim Lafferty

Lita Nelsen

Jeremy Coller

April 2017 I 5

www.globalcorporateventuring.com

NEWS

Maris to amass $100m for new fundBill Maris, formerly CEO of internet and technology group Alphabet’s GV corporate venturing subsidi-ary, is investing $100m in a new venture capital fund, Bloomberg has reported.

A co-founder of GV, originally known as Google Ventures, Maris played a prominent role in expand-ing its parent company’s focus to life sciences. He left the unit in August 2016, saying he wanted to spend more time with his family and explore new projects.

Reports later in the year indicated Maris had entered talks with prospective investors over a fund of between $350m and $500m. He secured the capital for a $230m healthcare-focused fund called Section 32, but then pulled the plug in December 2016, telling technology news site Recode that doing “exactly what I just did was not inspiring me”.

However, Maris changed his mind after finding financiers willing to contribute capital without requiring him to add other investing partners, or locate the fund outside San Diego, where he is based, according to a source. Maris will be the fund’s sole investment partner. It will retain the Section 32 name and concentrate on healthcare and biotechnology.

Siegel to Align for board positionSusan Siegel, CEO of industrial product and appliance manufacturer General Electric’s corporate venturing unit GE Ventures, has joined the board of US-based dental technology developer Align Technology.

Founded in 1997, Align produces a removable set of braces called Invisalign and a 3D digital scan-ning system for orthodontic or restorative dentistry dubbed iTero3D. Siegel, who ranked sixth on GCV’s 2016 Powerlist, also heads GE’s healthcare innovation initiative, Healthymagination.

Schöfer looks to make mark at MerckSebastian Schöfer has joined Merck Ventures, the corporate venturing arm of Germany-based phar-maceutical firm Merck Group, as a senior associate.

Schöfer moved from High-Tech Gründerfonds, the VC fund backed by a range of corporate limited partners. He had been an investment manager there since 2014 after stints at solar system provider Azuri Technologies and technology transfer fund Imperial Innovations.

Merck Ventures has offices in the Netherlands, the US and Israel, and had its fund size doubled from €150m to €300m ($320m) in June 2016.

Hubert Burda’s CVC arm heads for SingaporeBurda Principal Investments, the corporate venturing arm of Germany-based media group Hubert Burda, has opened an office in Singapore, according to Tech in Asia.

Albert Shyy, formerly a principal for Gree Ventures, the corporate venturing vehicle for mobile gam-ing company Gree, will head the office as part of a three-person team. He told Tech in Asia the unit was particularly interested in investing at series B stage.

Burda Principal Investments has already backed Southeast Asia-based startups Priceza, Medical Departures and Coc Coc, and is a limited partner in funds raised by local firms Golden Gate Ventures, Jungle Ventures and Kejora Ventures.

Xu bids farewell to SIG AsiaEric Xu has left SIG Asia Investment, the regional invest-ment arm of trading firm Susquehanna International Group, to join venture capital GGV Capital, China Money Network has reported.

Xu was a managing director at SIG Asia Investment, and has taken the same position at GGV Capital. At the VC firm, he will be in charge of investments in startups developing smartphone and internet technologies for the e-commerce, financial and entertainment sectors. He had

been with SIG since 2007, and had previously worked at Citic Capital and TDF Capital.

His appointments follows other recent additions to GGV Capital’s team, including Denise Peng, former chief operating officer of Chinese online travel company Qunar, and Semil Shah, founder of investment firm Hay-stack, who both joined as venture partners. Jason Costa, product manager at Pinterest, has also joined GGV as an entrepreneur-in-residence.

Bill Maris

Sue Siegel

Hubert Burda

Sebastian Schöfer

April 2017 I 6

www.globalcorporateventuring.com

NEWS

Park follows Echo Health Ventures callJohn Park has joined corporate venturing firm Echo Health Ventures as a managing director of the market development team. He was previously chief strategy officer at consumer-directed healthcare company Ale-geus, a position he had held since 2012.

Echo Health Ventures was created in November 2016 when health services provider Cambia Health merged with Mosaic Health Solutions, the corporate venturing unit of health insurance provider Blue Cross and Blue Shield of North Carolina.

The market development team will drive and create relationships between Echo Health Ventures’ portfolio and parent companies.

Rob Coppedge, chief executive of Echo Health Ven-tures, said: “John has demonstrated success across the health care industry, and understands what it takes to develop meaningful, high-value relationships. His addi-tion to the EHV team demonstrates our commitment to hands-on participation in the development of the next generation of great health care companies.”

Joyme and Kee Ever Bright bet $360m on gamingChina-based gaming e-commerce company Kee Ever Bright Technology is to form a strategic investment fund with Joyme Capital, a subsidiary of online gaming community operator Joyme Group.

The fund will initially be $140m but the companies intend eventually to increase it to $360m. It will focus on the gaming sector, in particular game development and distribution, eSports, and ancillary services and business models related to the creation and publishing of PC and mobile games.

In addition to capital, portfolio companies will benefit from Joyme’s resources, including online community Joyme Wiki and partnerships with e-commerce group Alibaba and online video streaming platform Youku Tudou, to help penetrate the Chinese market, seeking, according to Yang Chen, Joyme Group’s founder and CEO, “opportunities to acquire own-ership stakes in successful game developers” and “bringing western games to market in China”.

Nan Fung puts $300m into Pivotal fundUS-based venture capital firm Pivotal BioVenture Partners has closed its first fund at $300m, securing the capital from China-based property developer Nan Fung Group.

The fund, Pivotal BioVenture Partners Fund I, will make early-stage investments in biotechnology developers, and is focusing on those looking to advance technology to the clinical stage.

The firm was co-founded by managing partner Tracy Saxton, formerly an investment director at pharmaceutical com-pany Roche’s corporate venturing unit Roche Venture Fund, and a Global Corporate Venturing Rising Star 2016.

Karoly Nikolich, chairman and CEO of anti-ageing therapy developer Alkahest, is an adviser and venture partner for the firm. Vincent Cheung, managing director of Nan Fung, is also listed as managing partner on the firm’s website.

Saxton said: “Pivotal will invest in biotechnology companies with strong teams and differentiated science that can be mined to develop therapeutics to improve human health. There are many funds focused on derisked clinical assets rather than early-stage therapeutics. However, we plan to be an active investor in the early-stage arena and look forward to partnering with leading-edge science-based companies to achieve this goal.”

Saxton told Fierce Biotech the company is considering investments in infectious diseases, immunology, oncology, ophthalmology and orphan diseases, and is chiefly seeking deals where there is an unmet medical need.

Accion accepts $141m for fintech initiativeUS-based microfinance non-profit organisation Accion has launched a $141m financial technology and services invest-ment fund with contributions from limited partners including insurance groups Axa, MetLife and Prudential, and payment services firm Mastercard.

Accion Frontier Inclusion Fund will invest in startups developing technology that can help expand the range and qual-ity of financial services available to those currently underserved, a figure the organisation estimates is above 3 billion.

The fund will in particular look to invest in sub-Saharan Africa, Latin America and Asia, where it will prioritise India and Southeast Asia. Its first nine portfolio companies are Konfio, Creditas, Coins, NeoGrowth, Yoco, Invoinet, Eseye, IndiaMart and CreditMantri.

Accion and the corporates were joined by financial services firm JPMorgan Chase, development bank FMO, World Bank subsidiary the International Finance Corporation, venture capital firm Quona Capital and investment firm PG Impact Investments. Other investors include family office Blue Haven Initiative, mutual fund Calvert Equity Portfolio, investment manager Triodos Investment Management’s Triodos Fair Share Fund and Triodos Microfinance Fund, and TIAA Invest-ments, an affiliate of investment manager Nuveen.

April 2017 I 7

www.globalcorporateventuring.com

NEWS

Panasonic to put $100m into corporate venturingJapan-based consumer electronics manufacturer Panasonic is putting $100m into a new California-based corporate venturing unit, Panasonic Ventures.

The unit will provide funding mainly for US-based startups, and is targeting unique business models, products and services that do not need to relate directly to the parent’s current focus. The $100m was described in a statement as an initial investment. The unit will be led by Masahiro Kinoshita, Panasonic’s head of business development and corporate planning.

The launch of Panasonic Ventures is part of a wide-ranging reorganisation within the company that will also involve the formation of a US-based sports and entertainment-focused sales division – Panasonic Media Entertainment. This will be one of six industry-specific divisions to be overseen by a new branch of the group – Panasonic Connected Solutions.

Panasonic has not been particularly active in the venture capital space but is an occasional investor, taking part in rounds for laundry-folding robot developer Seven Dreamers and waveguide optics technology company DigiLens in the past year. The corporate also launched a Japan-based accelerator in July 2016 in partnership with startup services provider Creww.

Aflac to assemble $100m corporate venturing fundUS-based insurance provider Aflac is to set up a $100m fund to make strategic venture capital investments, Atlanta Busi-ness Chronicle has reported. Aflac plans to develop the unit, Aflac Corporate Ventures, over the next three years and will target investments in developers of software or digital products that complement its core business and enhance the insurance value chain.

Nadeem Khan, senior vice-president of corporate development at Aflac, has been promoted to president of Aflac Corporate Ventures, with Bharat Rajaram as managing director. The unit will be run from offices in North Carolina and California and will be operated in conjunction with an as-yet undisclosed accelerator partner.

Paul Amos, Aflac’s president of global operations, said: “With a greater focus on the customer experience, we feel that it is vital that Aflac prioritises potential partners that will help us enhance services and shareholder value, while building our future growth engine.”

SAP supplies $35m to strategic fundGermany-based enterprise software provider SAP has launched SAP.iO, a $35m corporate venture capital fund that will invest in early-stage companies to expand the SAP ecosystem.

SAP previously directed its corporate venturing activities through SAP Ventures, the investment subsidiary it launched in 1996 and later spun out. The unit’s portfolio companies included LinkedIn and MuleSoft by the time it was spun out at the start of 2011. It rebranded as Sapphire Ventures in 2014, but retains SAP as its sole sponsor, and closed $1bn in financing for two funds in September 2016.

SAP.iO will invest strategically, backing startups that are using SAP data, technologies and application programming interfaces. The unit has been formed as part of the SAP.iO open innovation initiative and was launched alongside an incubator called SAP.iO Foundry, which will operate in San Francisco and in a Berlin centre to be managed by accelera-tor partner Techstars.

Ram Jambunathan is leading SAP.iO’s six-strong team as managing director. The first company to receive investment from the fund is Parable Sciences, a US-based creator of a big data analytics platform called Paradata.

Dymon Asia pulls in SCB to raise $20mFinancial services firm Siam Commercial Bank has com-mitted to the $20m first close of Dymon Asia Ventures, a VC fund formed by hedge fund Dymon Asia, TechCrunch has reported. The bank provided the capital through its fintech-focused corporate venturing vehicle, SCB Digital Ventures.

Dymon Asia Ventures plans to back between 15 and 20 fintech startups, with Southeast Asia of particular inter-est. Dymon Asia launched the fund to get more expo-sure to early-stage technology and to take advantage of potential in the space, partners Jinesh Patel and Chris-

tiaan Kaptein told TechCrunch.They said the fund would provide between $300,000

and $3m from seed stage to series B and had “significant reserves” for follow-on rounds. Dymon Asia Ventures has targeted a $50m close and intends to raise the full amount in the next year. It has already invested in five companies – blockchain asset management platform Otonomos, peer-to-peer lending startup Capital Match, foreign exchange technology developer 4XLabs, trad-ing platform Spark Systems and networking service WeConvene.

April 2017 I 8

www.globalcorporateventuring.com

NEWS

MFEC to establish $20m investment armThailand-based software company MFEC is to establish a corporate venturing division equipped with Bt700m ($20m) to invest in startups, local news provider Nation has reported.

MFEC will seek out opportunities in the education, media and entertainment sectors. It will also offer training and consultation to entrepreneurs, collaborating with the computer engineering department of Chulalongkorn University and the Industrial Liaison Program to set up a facility dubbed Data Café Thailand.

Additionally, the corporate will spin out a range of businesses beginning with Playtorium Solutions, a one-stop shop for software and crowd-testing services as well as IT staff recruitment.

Virginia Tech and Carilion launch $15m fundVirginia Polytechnic Institute and State University (Virginia Tech) and healthcare provider Carilion Clinic have raised a $15m VC fund for the local area in their third such collaboration, according to the Roanoke Times.

The VTC Innovation Fund is aiming to back seven to 10 startups around Blacksburg and Roanoke over the next four years. About 60% of the investments will be in the life sciences industry and most will be based in Virginia. If they are in another state, the companies must have some tie to the university or to Carilion. The fund will be managed by James Ramey and Scott Horner at Middleland Capital.

Virginia Tech and Carilion previously jointly formed the NewVa Capital Partners fund in 2004. The two also formed Valleys Ventures in 2013, but that fund reportedly went dormant after just two investments.

Intex enters venturing with Rooter investmentIndia-based consumer electronics producer Intex Technologies is investing between Rs1.5bn ($23m) and Rs2bn in a corporate venturing fund, Times of India has reported.

Intex manufactures smartphones, computer accessories, televisions and other home entertainment products. The decision to go into strategic investments comes weeks after competitor Micromax launched its own venturing unit.

Keshav Bansal, a director at Intex Technologies, told Times of India that the company was moving into corporate ven-turing to diversify its holdings into sectors such as sport, healthcare and the internet of things. Intex will target ticket sizes of between Rs100m and Rs150m and will look to take stakes of between 10% and 25%. Its first investment is in Rooter, an India-based creator of an app that allows sports fans to engage with each other during live events.

Phoenix rises with corporate-backed fundUS-based venture capital firm Phoenix Venture Partners has closed its second fund with limited partners that included pharmaceutical firm Pfizer, manufacturing con-glomerate 3M and glass and ceramics materials producer Corning.

Chemical producers Eastman Chemical, Solvay and Showa Denko, and manufacturing company WL Gore & Associates have also contributed to the fund, the size of

which has not been disclosed. Other LPs include undis-closed family offices and financial institutions.

Phoenix Venture Partners focuses on startups operat-ing in the advanced materials sector, working with its cor-porate network to identify strategic opportunities in their respective fields. John Chen, managing general partner of PVP, said the new fund had already made several new investments.

Stock exchange backs Digital-Plus PartnersStock exchange operator Deutsche Börse Group has contributed capital to Digital Growth Fund I, a growth-stage fund raised by Germany-based venture capital firm Digital-Plus Partners, Mondo Visione has reported.

The fund’s first tranche closed at about €132m ($139m), and it will invest in business-to-business software providers. It will provide between €20m and €30m for each company, which will be provided over several rounds.

Carsten Kengeter, CEO of Deutsche Börse, said: “Innovative and fast-growing companies are essential to our eco-nomic development. And so we support initiatives to ease their access to capital. Our investment in the fund launched by Digital-Plus Partners is the perfect supplement to our own direct investments in fintech firms via the DB1 Ventures platform.”

The fund’s limited partners also include optics and optoelectronics manufacturer Zeiss.

April 2017 I 9

www.globalcorporateventuring.com

NEWS

Henkel to heave funds into venturingGermany-based industrial and consumer product manufacturer Henkel has formed corporate venture capital subsidiary Henkel Ventures and plans to invest up to €150m ($163m) via the unit.

Henkel has so far invested €25m in its venturing activities, supplying capital to barrier technology manufacturer Vit-riflex and coating material producer DropWise, as well as funds raised by VC firms Emerald Technology Ventures and Pangaea Ventures. In addition, the company’s laundry and home care division has invested in UK-based on-demand laundry and dry cleaning service ZipJet. However, the launch of Henkel Ventures will mean all the corporate’s venturing activities will be overseen by a single entity.

Robert Günther, the Henkel Ventures team member focusing on corporate development, said: “With Henkel Ventures, we are combining our corporate venture capital activities across our three business units – adhesive technologies, beauty care, and laundry and home care. We are partnering startups, helping them to develop their innovative ideas and technologies.”

Henkel Ventures will seek to invest at an early stage, preferably series A, and will provide portfolio companies with access to its brands and global network.

In addition to Günther, the unit’s team consists of Paolo Bavaj, focusing on adhesive technologies, Esther Kumpan-Bahrami, overseeing beauty care, and Thomas Schuffenhauer, specialising in laundry and home care deals.

Spectrum to add colour with venture capital unitUS-based healthcare system Spectrum Health is to commit up to $100m to a corporate venturing fund that will back healthcare startups, MiBiz has reported. Spectrum Health Ventures will invest in early-stage companies seeking to bring to market technology and services capable of improving the cost and effectiveness of medical treatment, according to Spectrum chief strategy officer Roger Jansen.

Five areas in particular are being considered – behavioural tools to improve health and wellbeing, personalised medicine and genomics, digital technology, population and health analytics, and artificial intelligence and cognitive computing software to help prevent disease.

The capital will be provided over a 10-year period, and Spectrum will look to participate in deals where it can co-invest with other health systems. The unit expects to make initial commitments of about $2m at series A or B stage, and to make follow-on investments in portfolio companies.

Spectrum Health Ventures is working with Avia, an innovation network that manages VC funds for health systems, and will seek to back two to four companies each year.

Symantec engineers CVC armUS-based cybersecurity company Symantec has launched corporate venturing subsidiary Symantec Ventures to target opportunities in the cybersecurity sector.

The unit will provide funding and help startups reduce expenses and accelerate their time to market. Symantec has not disclosed how much capital it is allocating. Startups will have access to Symantec’s next-generation technology assets, expertise in artificial intelligence, go-to-market resources and the corporate’s threat intelligence network.

The decision follows Symantec’s investment in US-based enterprise mobile threat platform Appthority, which closed a $17m series B round last July with the support of Symantec subsidiary Blue Coat Systems.

Greg Clark, chief executive of Symantec, said: “We are launching Symantec Ventures to catalyse innovation in the cybersecurity space. We can help startups by allowing them to build on our extensible Integrated cyberdefence plat-form. For example, a new algorithmic approach to anomaly detection can be built on top of our endpoint platform or run on top of our network and cloud security drive train.”

Walmart shops for startupsUS-based retail chain Walmart is set to launch an incuba-tor in Silicon Valley, Bloomberg has reported. The incuba-tor, Store No 8, will seek to partner startups, venture capi-tal investors and academics, and will back technologies such as drone delivery, personalised shopping, robotics, autonomous vehicles, virtual and augmented reality, and artificial intelligence.

Store No 8 will aim to help develop the technologies for use across Walmart. It takes its name from an early

Walmart store location where the retailer experimented with floor layouts.

The program was announced by Marc Lore, chief executive of the retailer’s e-commerce operations. He founded e-commerce company Jet, which was acquired by Walmart for $3.3bn last August.

Store No 8 will be led by principal Seth Beal, who was appointed Walmart’s senior vice-president of incubation and strategic partnerships in January 2017.

April 2017 I 10

www.globalcorporateventuring.com

NEWS

Cemex cements corporate venturing plansMexico-based building materials provider Cemex has launched corporate venturing vehicle Cemex Ventures to invest in innovative construction technology.

Cemex Ventures will be based in Spain and will act as an open innovation and venture capital unit, investing in tech-nologies in adjacent areas to its parent company’s core business and providing accelerator and incubator services for earlier-stage technology. The unit will be headed by Gonzalo Galindo, president of US east operations.

Specific targets for the fund include urban development, construction models and technologies, innovative project finance sourcing, and technology that improves the construction ecosystem by enhancing connectivity.

The unit has also announced it will launch a contest for startups and entrepreneurs developing technology in its investment areas. The Cemex Ventures Competition is accepting applications now.

Startup help arrives from Roc NationRoc Nation, the US-based entertainment services pro-vider founded by entertainer Shawn “Jay-Z” Carter, has launched Arrive, a platform to supply funding and assis-tance to startups.

Arrive will provide advice, brand services and business development help to early-stage companies. It also plans

to launch a corporate venturing fund to back portfolio companies as they grow. Venture capital firm Primary Venture Partners has been appointed venture adviser to the initiative, and institutional and operational support will come from GlassBridge Asset Management, part of hold-ing company GlassBridge Enterprises.

Innogy and OurCrowd forge investment strategyGermany-based energy utility Innogy has formed a partnership with crowdfunding platform OurCrowd to seek out investment targets in the latter’s home country of Israel.

The initiative will form part of Innogy’s open innovation strategy and involves OurCrowd looking for companies in areas such as smart and connected technology, urban solutions, disruptive digital technology, big data and automated technologies such as blockchain.

Peter Terium, Innogy’s CEO, said: “We are on a quest for innovation and are excited to be present in the vibrant and innovative ecosystem here in Israel. We have our own innovation team in Israel, connecting us with the startups and innovators in the country. OurCrowd is a natural partner for us. We are impressed by the depth of OurCrowd’s exposure and the quality of their portfolio.”

Verizon and R/GA to give startups studio timeVerizon Ventures, the corporate venturing subsidiary of telecoms company Verizon, has launched an accelerator scheme called Verizon Media Tech Venture Studio in partnership with advertising agency R/GA.

The initiative, described by the corporates as a venture studio, will work with early and growth-stage developers of disruptive digital media and entertainment technology. Applications opened last month and up to 10 companies will be admitted. Areas of interest will involve content creation, personalisation and distribution, virtual and augmented reality, artificial intelligence and image recognition, advertising and eSports.

The studio will be housed in New York and participants will be able to work with Verizon Ventures, Verizon’s digital media businesses and various teams from R/GA. They will also have access to the corporates’ investor network.

John Doherty, head of Verizon Ventures, said: “The Verizon Media Tech Ventures Studio with R/GA will connect us with emerging startups that are shaping the future of this business. Verizon and R/GA have created an advanced program for startups with unparallelled access to resources, technology and intellectual capital that will accelerate their growth.”

Stephen Plumlee, managing partner of R/GA’s corporate venturing fund, R/GA Ventures. added: “This program will be a game changer for the companies selected.”

Philips and EDBI push healthtech partnershipNetherlands-based electronics and healthcare technology manufacturer Royal Philips has boosted the digital health investment agreement it has in place with Singaporean state-owned venture capital fund EDBI.

Philips and EDBI launched the partnership early last year with a view to investing in connected health technology that could be beneficial in the Asian healthcare market. The first company to receive funding through the initiative is CXA Group, a Singapore-based employee benefits and wellness marketplace that closed a $25m series B round in February.

April 2017 I 11

www.globalcorporateventuring.com

NEWS

Banco do Brasil backs BR StartupsA subsidiary of financial services firm Banco do Brasil has provided an undisclosed amount of capital for BR Startups Fund, a Brazil-based initiative backed by several corporates, Baguete has reported.

BR Startups is managed by private equity and venture capital firm MSW Capital and was launched to invest in early-stage insurance technology and services providers. The holding company in question, BB Seguridade, oversees a range of funds for Banco do Brasil. The fund’s limited partners include Microsoft Participações, the Brazilian investment subsidiary of Microsoft, agribusiness Monsanto, mobile chipmaker Qualcomm, financial services firm Banco Votorantim, conglomerate Grupo Algar and the Rio de Janeiro State Development Agency, AgeRio.

Google launches machine learning startup contestInternet technology provider Google has launched a contest for machine learning technology startups. The winner will be eligible for up to $1m in venture funding. The Machine Learning Startup Competition is open to startups implement-ing machine learning in their products, and which have raised less than $5m in funding. VC firms Data Collective and Emergence Capital could each invest up to $500,000 in the winner of the contest. Google Cloud is running the scheme and will supply up to $1m in Google cloud platform credits for the winner as well as technical support.

Comcast NBCUniversal to give startups a LiftMass media group Comcast NBCUniversal has launched US-based startup assistance initiative Lift Labs for Entrepreneurs.Lift – leveraging innovation for tomorrow – will encompass a startup accelerator, entrepreneurs’ resource centre and a series of advice programs intended to help media, entertainment and connectivity technology startups bring their prod-ucts to market. The accelerator will be run by Techstars out of the Comcast Technology Centre, which is scheduled to open in Philadelphia in early 2018. A second branch of Lift is set to begin in Atlanta later the same year, with an accelera-tor partner yet to be announced.

PayPal’s Singapore incubator graduates threeUS-based online payment platform operator PayPal has graduated the first three startups from Start Tank, its Sin-gapore-based Technology Centre incubator, Tech in Asia has reported.

The startups in question are digital insurance tech-nology provider Axinan, blockchain network developer

TenX and InvoiceInterchange, in which external investors help businesses with financing for late invoices.

PayPal launched Start Tank last May. It does not pro-vide funding but does supply coaching and mentoring, and will put startups in touch with its venture capital connections.

IDG Ventures and Axilor look to new FrontierIDG Ventures India, a venture capital affiliate of media and events firm International Data Group, has formed a partner-ship with accelerator and seed fund Axilor Ventures to invest in disruptive startups.

The Frontier Tech Innovators initiative seeks to make investments in advanced technologies such as artificial intel-ligence, robotics, blockchain, drones, autonomous driving systems, and augmented and virtual reality. The scheme accepts about 20 startups at seed or pre-series A stage, with the partners particularly interested in those under three years old, according to the Economic Times.

Big deal: NBCUniversal invests $500m in a Snap

James Mawson, editor-in-chief, and Thierry Heles, editor, Global Government Venturing

When US-based visual media platform Snap’s long-awaited initial public offering took place last month the company priced 200 million shares, or about 6% of its stock, at $17 each, resulting in a $3.4bn windfall.

The flotation valued Snap – creator of the Snapchat messaging app, which has about 160 million daily users, and developer of hardware such as augmented glasses – at $24bn, a jaw-dropping 60 times its revenue. Its aftermarket

Big deal: NBCUniversal invests $500m in a Snap

April 2017 I 12

www.globalcorporateventuring.com

NEWS

performance lifted the share price above $24, meaning investors were trading the stock at nearly 100-times revenue.

While it is not unusual for a company to go public before making a profit, it is nevertheless noteworthy that Snap’s losses have been increasing – they were up 38% last year – and the company has been fairly vague about how it intends to make a profit in future. Adding to that struggle is the reality that Facebook is trying to steal Snap’s thunder by copying a range of features into its own suite of apps, which include WhatsApp, Instagram and Messenger.

Also noteworthy is that investors buying the new shares will not have voting rights, while co-founders Evan Spiegel and Bobby Murphy are reinforcing their hold over the company through their voting shares, a move taken from Facebook co-founder Mark Zuckerberg’s playbook.

Amid that enthusiasm, however, media operator NBCUniversal, a subsidiary of mass media group Comcast, paid $500m for a stake of about 2.1% in Snap via the IPO. NBCUniversal has previously bought stakes in private companies, investing $400m in online media company BuzzFeed and $200m in news site Vox.

However, NBCUniversal’s investment in Snap is a bet both on its potential financial returns – perhaps with an eye on the subsequent success of Facebook since its own flotation – and an indication that it wants to build a closer partnership with the hardware maker and communications service.

In a memo to staff, NBCUniversal CEO Steve Burke described the investment as another step in a “growing partnership” with Snap, news provider Recode reported. The companies worked together on the Rio Olympics, and NBCUniversal media properties the Voice, SNL and E! News: The Rundown have launched series on Snapchat.

While it has been increasingly common for corporations to try to build strategic relations with entrepreneurs in the pri-vate market – GCV Analytics tracked investment rounds of more than $83bn by nearly 1,000 corporate venturers last year – and there is a long history of larger corporations taking minority stakes in one another, there have been relatively few private corporate investments in public equities at the IPO stage.

More common has been mutual funds and other fund managers trying to invest in startups in order to understand the disruption that might impact their public holdings, and to ease greater access to hot prospects at their IPOs.

In its annual letter to investors, mutual fund manager T Rowe Price’s $17bn New Horizons fund for the first time provided more transparency about its $1.2bn of investments in 63 private companies, including Twitter and GrubHub since 2009, noting annualised weighted returns of 34.8%.

The fund had previously provided only a list of individual investments, the purchase price and current valuation. It has 28 investments valued at a total of $836m in its portfolio, including a $79m stake in GrubHub.

While the letter admitted that “any early-stage growth investment – especially a private investment – carries a high level of risk”, it argues that the strategy helped the fund understand industries under disruption and was a valuable contributor to returns, Henry Ellenbogen, the fund’s manager, told the Financial Times.

Fund rating agency Morningstar, which acquired corporate venturing portfolio company PitchBook last autumn, counted 194 US mutual funds that have invested in 133 private companies, with their overall holdings valued at $11.5bn. Fidelity is the biggest investor in unlisted companies according to the study, followed by T Rowe Price and Hartford. u

Big deal: MuleSoft musters $221m in IPO

Rob Lavine, news editor

Salesforce Ventures, the corporate venturing arm of the enterprise software provider, has achieved another exit in a $221m initial public offering by US-based integration software producer MuleSoft.

The company issued 13 million shares on the New York Stock Exchange at $17 each, above the $12 to $14 target range it set earlier last month, allowing backers that included networking technology supplier Cisco and enterprise software producer ServiceNow to exit.

Founded in 2006, MuleSoft has built a software integration platform that helps businesses integrate their various appli-cations into a single network. It has more than 1,000 customers, more than 30 of which each provide over $1m in sales of subscriptions and services each year, spread across 60 countries. According to its IPO prospectus, MuleSoft made a $49.6m full-year loss in 2016 from revenue of approximately $188m, having made a $65.4m loss the year before from $110m in revenue.

The offering followed $259m in funding, including a $128m series G round in 2015 that valued the company at $1.5bn and was led by Salesforce Ventures. Other backers were ServiceNow, Cisco Investments, Sapphire Ventures, Adage Capital Management, Brookside Capital, Sands Capital Ventures, New Enterprise Associates (NEA), Lightspeed Venture Partners, Meritech Capital Partners, Bay Partners, Hummer Winblad Venture Partners and Morgenthaler Ventures.

Salesforce Ventures first invested in MuleSoft as part of a $37m series E round in 2013, subsequently returning for a

Big deal: MuleSoft musters $221m in IPO

April 2017 I 13

www.globalcorporateventuring.com

NEWS

$50m round the following year that valued MuleSoft at $800m and which included Cisco, Sapphire Ventures, NEA, Lightspeed, Meritech Capital, Hummer Winblad, Morgenthaler and Bay Partners.

None of the corporates are major investors – the company’s largest shareholder is Lightspeed Venture Partners, which saw its stake diluted from 17% to 15.3% in the offering. Other notable shareholders are Hummer Winblad (with a 14.1% post-IPO stake), NEA (12.7%), Morgenthaler (6.7%), Sapphire (6%) and Bay Partners (5.6%). MuleSoft’s stock opened at $24.25 on March 17 and held steady to close at $24.75, an increase of around 44% from the offering price.

The offering is Salesforce Ventures’ second exit of the year, after Amazon Web Services’ acquisition of meeting tool developer Do in March. But the offering could be the first of many, as the success of MuleSoft and the kickstarting of the IPO market looks likely to encourage several more enterprise software companies looking to list.

MuleSoft formed part of a substantial stable of unicorns – venture capital-backed companies valued at more than $1bn – built up by Salesforce Ventures, including SurveyMonkey, InsideSales, Apttus, Anaplan, MongoDB, Evernote and the largest of them all, Dropbox, the data storage provider valued at more than $10bn in its last round.

SurveyMonkey CEO Zander Lurie has said the company is looking beyond 2017 to go public, but Anaplan has said it is preparing a flotation and InsideSales and Apttus have been touted as likely IPOs this year. Dropbox reportedly met advisers last August to discuss plans for an offering, but has so far been quiet on the subject.

Still, the relative success of messaging platform Snap’s IPO – the largest for a VC-backed company in two and a half years – combined with MuleSoft’s bump will inevitably lead to more offerings, particularly as investors may want to get in before a market downturn. This could well be the year in which Salesforce Ventures cashes in and starts racking up some big exits. u

Big deal: Flipkart files away $1bn

Rob Lavine, news editor

Last month India-based e-commerce company Flipkart raised $1bn from several corporates, but at a lower valuation for the business, suggesting investors may have to sacrifice returns to ensure portfolio companies continue to grow.

The round included software producer Microsoft, online marketplace eBay and internet group Tencent, and followed a reported $38.8m investment by media firm Bennett, Coleman & Co in December 2016.

Flipkart operates a diversified online marketplace that lists more than 80 million items spanning some 80 categories, including books, clothing, jewellery, appliances and electronics.

The $1bn investment boosted the company’s overall funding to about $4.1bn since it was founded in 2007, its previous backers including media and e-commerce group Naspers, IDG Ventures India, an affiliate of media company Inter-national Data Group, and several institutional investors. However, the cash was raised at a valuation of about $10bn, sources told Bloomberg, a steep drop from the $15.5bn valuation at which Flipkart closed its last round in 2015. In that round, Flipkart received $700m from backers including Tiger Global Management and Steadview Capital.

The lower valuation can be attributed partly to the stiff competition in India’s e-commerce sector, which has made profit-ability difficult for all its players, not least after the entry of US-based competitor Amazon into the market.

Flipkart was reportedly losing ground until Tiger Global managing director Kalyan Krishnamurthy, previously chief finan-cial officer, rejoined the company last May to take charge of sales. He took on the CEO role in January and after a suc-cessful holiday season Flipkart is generally regarded as being on an upswing.

However, India’s startup space is going through a tough time following a boom in 2015. Hundreds of India-based startups reportedly closed down last year, while high-profile names such as Ola and Flipkart rival Snapdeal had their valuations written down and others, like Housing.com, were acquired for less than they had raised in VC funding.

Despite the lowering of its valuation, Flipkart has big plans that include raising a further $1bn in the coming months. Perhaps the most interesting part of the deal is the rumour suggesting eBay will provide $500m of the capital as part of a deal in which its Indian subsidiary will merge with Flipkart.

The funding was expected to be earmarked for promotions and coupons as part of a market war, but the proposed deal suggests that the long-term strategy for Flipkart, which has purchased fellow e-commerce companies Jabong and Myntra in the past three years, will involve at least some element of strategic investment.

Acquisitions that can increase its market share may be necessary to head off not only Flipkart’s present rivals but also a relatively new player, Paytm E-Commerce. One of two companies to emerge from One97 Communications – the other being financial services platform Paytm – Paytm E-Commerce is backed by the deep pockets of e-commerce giant Alibaba and its financial services affiliate Ant Financial, and is likely to pursue a similar strategy to the one that made Alibaba so successful in China.

Big deal: Flipkart files away $1bn

April 2017 I 14

www.globalcorporateventuring.com

Both Flipkart and Paytm E-Commerce are said to be in talks with Snapdeal over an acquisition, and that may be where a significant portion of Flipkart’s new funding goes. Either way it looks as if the online marketplace sector is ripe for con-solidation, and is still a viable attraction for corporate venturing funds. u

Big deal: iFlix inflates funding with $90m

Rob Lavine, news editor

Malaysia-based online video streaming service iFlix has raised more than $90m in a round backed by media com-panies Liberty Global and Sky, indicating that geographic opposition to global market leader Netflix is emerging in

several markets.

Evolution Media Capital (EMC), the investment firm co-founded by talent agency Creative Artists Agency and private equity firm TPG, also invested in the round along with domestic internet company Catcha Group, telecoms firm Zain and an unnamed investment management firm.

The company has begun talks with possible investors over an increase to the round, which values it at more than $500m post-money, co-founder Patrick Y-Kin Grove told Forbes. The capital, which boosted iFlix’s overall funding to $175m, fol-lows a $45m investment by Sky in March 2016 at a $450m valuation, and $30m from Catcha, EMC and telecoms group Philippine Long Distance Telephone (PLDT) 11 months earlier. Grove said its backers included entertainment producer MGM, broadcaster Emtek and venture capital firm Jungle Ventures.

Founded in 2015 by Catcha and EMC, iFlix runs an on-demand film and television streaming service. It has licensed con-tent from Walt Disney, Warner Bros, Fox, MGM, Paramount Pictures and Starz as well as local producers, and has built up a base of about 5 million users. The company began its service in Malaysia and the Philippines and operates in 10 Asian countries, having expanded across Southeast Asia before launching in Pakistan, Vietnam and Burma this year. The new capital will support a move into the Middle East and Africa.

The push will be backed by a joint venture with Kuwait-based Zain, which will offer iFlix to its 47 million customers across the Middle East and North Africa on top of its own service. That approach mirrors existing deals iFlix has struck with PLDT and several other telecoms networks across the Philippines, Malaysia, the Maldives and Indonesia.

Although Netflix is present in the region, iFlix is using local connections to forge ahead, not only utilising the help of local strategic partners, but also striking promotional deals with national celebrities, negotiating censorship rules with indi-vidual governments and offering its service at a fraction of the price of Netflix in a bid to cut into markets that are awash with piracy. “We are like McDonald’s and they are like a Michelin two-star restaurant,” Grove told Bloomberg, describing the companies’ relative positions in the market. “We both sell food, but we are not competitors.”

The progress of iFlix can perhaps be compared to that of ride-hailing company Uber’s regional rivals – though Netflix has a stronger global market position than Uber – but as it grows its challenge will be to see off not only its larger rival but also homegrown players offering a localised service. Hooq, which has raised some $95m from its founding partners, telecoms group SingTel, media conglomerate Warner Bros and electronics firm Sony’s AXN Investment unit, is already competing with iFlix in the Philippines, Thailand and Indonesia, and also operating in India.

The purported expansion will put iFlix up against the likes of Icflix in the Middle East and potentially iRokoTV in Africa, and at that point it will have to see whether the model that has served it well over the past 18 months still works when it is stretching its resources over a wider swathe of countries. It may well look to harness not only its telecoms partners but also the knowledge of Sky and Liberty Global, both of which have ample experience in paid television services. u

Analysis: Venture and maturity go hand in hand

James Mawson, editor-in-chief

Venture capital is risk management, and the finest exponents of the practice are still in Silicon Valley, California. Plenty of things with entrepreneurial companies can, and often do, go wrong, but being aware of what these issues are

hopefully allows for more sensible pricing and funding of these companies.

David Mes, managing partner at secondaries firm Arc Venture Partners, said he would question his process only if a portfolio company failed from a risk he had not considered. At a GCV drinks reception co-hosted by healthcare com-pany Johnson & Johnson and held at its innovation centre in Menlo Park, Silicon Valley, Mes talked about one of his angel portfolio companies, virtual reality technology developer Skylights, which has contracts to provide its headsets for airplanes, and the challenges it was taking on to improve passenger experience. The list was lengthy, but the founder’s user and business experience and successes so far gave Mes hope of a substantial win over the next few years.

NEWS

Big deal: iFlix inflates funding with $90m

Analysis: Venture and maturity go hand in hand

April 2017 I 15

www.globalcorporateventuring.com

NEWS

It is classic venture capital by an experienced investor in an underappreciated area. Mark Suster, managing partner at VC firm Upfront Ventures, in his outlook for the technology startup world and venture capital overall – WTF Happened to Winter? – said: “A large number of VCs believed that virtual and augmented reality and blockchain, while interesting, would take a few more years to mature.”

Perhaps that is why angels, such as Mes, are getting involved in virtual and augmented reality – a classic stage of devel-opment for them to get in before an area of technology becomes mainstream.

But what is more interesting in the Skylights example is the other participants in its development. There appears to be an increasing willingness from large businesses to use startup services such as Skylights’ even if the technology is nascent. The pressure is on incumbents to compete, and speed and innovation are coming from their partnerships with entre-preneurs rather than internal developments. In turn, these contracts increase the chances of success for the startup.

Mes described Skylights’ two contracts with major airlines, with two more in the offing, while major media companies, such as 20th Century Fox, have struck content deals with it. Skylights, therefore, seems able with relatively modest funding to cover a full stack of hardware development, content distribution and sales. If it gains traction, any later-stage rounds are likely to be bigger and more expensive, which is great for entrepreneurial shareholders and early investors.

Entrepreneurs in some areas are able to cover the full stack at lower costs, but corporations can develop these ideas and take them into the business. It would be little surprise Skylights’ partners try to take a stake in the startup.

This, in turn, is helping to underpin a potentially seismic change in the venture market. Traditionally, ven-ture capital has been procyclical – one where more is invested in faster-growing economies and less in recessions – and dictated by VCs’ sentiment. If venture becomes more mature and steady throughout an economic cycle, because investors are looking beyond pure financial returns, then trying to time an economic cycle becomes less of a risk factor for entrepreneurs.

There is no greater sign of the shift in this direction than the relative stability of the past 12 to 18 months in global activity. A year or more ago, there was pessimism in the US that valuations had gone too far and funding would fall only in a new venture winter – hence the title of Suster’s analysis – but so far the decline has been muted and short-lived.

While this may be due to the resilience of the US and the world economy over the past year, it also points to the healthy interest in venture from other investor types beyond typical VC firms. GCV Analytics tracked corporations involved in rounds worth an aggregate $83bn last year, compared with the $134bn collected in nearly 10,000 venture capital-backed deals that data provider Preqin reported in 2016.

As data provider Go4Venture noted in its recent report: “Although VCs did cut investment, did take a more cautious approach to the burn rate of their portfolio companies, and did see a decline in valu-ations, overall the innovation financing market has been lifted by money from outside the classic VC realm.”

Looking at these investors and their likely reaction to any recession has become increasingly important given that an economic downturn is increasingly likely. After all, the US is eight years into its recovery from the global financial crisis, and China is preparing for slower growth and looking for systemic risks.

A straw poll of corporate venturers at a Global Corporate Venturing Leadership Society roundtable discussion before the drinks reception found about half feared the rapid growth in their communities over the past five years could decline if the economy slowed down substantially or went into recession. Their worries were that if the momen-tum swung towards cost-cutting rather than seeking growth then CVC would be one of the areas targeted, especially if portfolio company valuations fell, or if strategic insights or a new product built off venture were yet to be realised. The other half of the vox pop were more confident. The fear of missing out is a powerful driver for corporate, government and sovereign investors, either directly or as limited partners in VC funds.

So far, therefore, the risks are outweighed by the opportunity, with CEOs bluntly tasking their CVC units with finding “the next big thing”. Whether this will be virtual and augmented reality, artificial intelligence and machine learning – favoured by most VCs in Suster’s survey – or a host of other sectors, including healthcare, according to noted consultancy Cam-bridge Associates, remains to be seen.

But being around to see the results will be important.

The GCV-J&J roundtable hosted an interesting discussion on what leadership in the industry would look like in five years’ time and how to provide a means for sustainability through financial and strategic returns. These insights, shared under Chatham House rules, will form a separate article and complement the qualitative interviews of about 40 CVCs as an Insights Project carried out by consultancy Bell Mason Group and also to be published by GCV.

Combining data with insights and managing its risks makes more sense of the venture world than relying on one or the other. u

“Overall the innovation financing market has been lifted by money from outside the classic VC realm”

April 2017 I 16

www.globalcorporateventuring.com

INTERVIEW

You set up the Heart after noticing that corporates were taking far too long to create new ventures internally. Why is this, and how does the Heart solve this problem?

As Clayton Christensen, author of Innovator’s Dilemma, has noted, successful big organisations can do everything right and still lose market leadership. They are great at scaling proven business models, yet find it hard to experiment with new products and ventures. When an entrepreneur comes up with an idea for a disruptive innovation, it is more likely to be implemented outside corporate boundaries than within them.

It is natural that internal decision-making processes and organisational politics often slow down new business creation. After all, would you blame a leader managing a huge business line for focusing his attention on the core business that brings him hundreds of millions, and not some crazy ideas that have not been validated? It is so much easier to explore new oceans when you lose sight of the well-known shore. I believe the startup ecosystem is a perfect lab for discovering technologies, products and businesses of tomorrow. Smart corporate leaders recognise that, and want to leverage that potential as a source of innovation. The Heart is a European centre for such corporate-startup collaboration.

You began helping corporates innovate 12 years ago, when you co-founded Innovatika to run corporate accelera-tors. How has corporate innovation evolved since then?

I have been reflecting on that journey a lot recently. We have helped organisations build different “innovation muscles” – from design thinking to new business model generation. But the ones that are growing in importance, and are often underdeveloped in large organisations, are the ones connected with open innovation.

Even the greatest team of developers at Nokia could not compete with the ecosystem of independent innovators creat-ing apps for Google or Apple. In the digital world, organisations need to get ready for co-creating value with startups. They need to admit limitations of internal innovation units and buy, partner or invest in the best external solutions.

What lessons can you share with executives wishing to prepare their businesses to innovate?

We sometimes hear complaints from startups about corporations that just want to look around, see the solutions, but

Corporate-startup collaboration goes to the HeartTomasz Rudolf, founder and CEO of the Heart, a Warsaw-based European centre for corporate-startup collaboration, spoke to features editor Nicole Idar Lee about helping corporates develop “innovation muscles” and central Europe’s growing role as a digital sandbox for testing innovative ideas

The Warsaw Spire, home of the Heart

April 2017 I 17

www.globalcorporateventuring.com

INTERVIEW

lack the resources or decision-making power to actually implement anything. Often, this is a result of so called “innova-tion theatre” – launching corporate startup programs just for public relations value, without the commitment to open the organisation for true collaboration.

Such initiatives are not sustainable and often get killed when people start asking for results. The best open innovation initiatives that I have seen are deeply connected with the corporate’s business strategy, have well-thought processes and top-management commitment.

A great example is Unilever Foundry, a pragmatic approach that led to more than 100 commercial pilots in the first 18 months of the program, with 48% of them ending in longer-term collaboration. Part of that success was preparing the organisation properly – securing a $50,000 budget for each pilot, building a central unit and website to screen and select partners, or leveraging external scouts to find high-quality partners across the world.

Tell us about the tech-entrepreneur dynamic in central and eastern Europe.

We work across Europe, but the fact that we are headquartered in Poland is actually helpful. Many of our corporate clients treat the region as a digital sandbox. In the building where we have our hub – the tallest skyscraper in Warsaw – you can find digital R&D and the regional offices of companies like Samsung, Goldman Sachs, JLL and Mastercard.

Central Europe is not only a valuable spot for shared service centres, but increasingly a development and testing ground for innovations that later get scaled internationally. The startup ecosystem here is also developing fast, mostly thanks to the great talent pool – some statistics show the Central and Eastern Europe region has more engineering graduates than the US, and the quality of their work is perceived to be impressive.

EU and government support is also giving a boost to the ecosystem – many new programs inspired by Israel’s Yozma initiative [a government-led effort launched in 1993 to promote venture investment] are now under way. All of that puts us at the heart of digital transformation in Europe.

The Heart offers three types of service – a corporate club, sector-focused programs, and a scouting service to identify suitable business partners. How many members does the corporate club have, and what role does it play?

Since we started, more than 40 corporations have joined our community. The goal of the club was to help companies just starting to work with startups by giving access to regular knowledge-sharing roundtables. We regularly bring in international practitioners from around the world to inspire and share the learnings. It is great to see how our members develop their innovation initiatives, but also initiate joint projects with other corporations. It is a truly open community.

We also organise regular corporate demo days, bringing the best European scale-ups to inspire and work with corporate executives. Having such a diverse group is inspiring, as the industry boundaries are blurring and trends impact everyone.

Your sector-focused programs target fintech, omnichannel and healthtech. Why did you select these areas?

Besides doing individual scouting projects for our corporate clients, we decided to bring together companies interested in similar areas. Such innovation alliances allow us to identify the top three common themes for the cluster each year and match them with the best ready-to-scale startups in that space.

Fintech was a natural choice, as we work with many of the leading banks in that space, and topics like cybersecurity, PSD2 [the EU’s revised Payment Services Directive], big data or blockchain interest everyone. The omnichannel program is even more diverse, connecting companies that are transforming their retail operations and looking for innovations in areas like customer intelligence and marketing and sales automation of future point of sale.

A smart city program is also in the pipeline. Tell us more about it?

This will be the first of our global programs, and we are currently confirming the focus areas with our first partners. We are definitely looking at areas like smart offices and buildings or construction. Digital transformation will definitely affect those capital-intensive industries, and potentially drive both efficiency and new value-added services.

Together with our investor, international developer Ghelamco, we also want to create sand-boxes for testing such solutions. One of these will definitely be the Hub – a new real estate project in the heart of Warsaw that will become the regional centre for corporate digital R&Ds, startups and ecosystem partners.

How did payment services company Mastercard come to be a founding partner of the Heart?

We were lucky to have Mastercard as one of the first clients in our corporate club. Last year, they were moving their offices to Ghelamco’s Warsaw Spire building, and we were able to get

“The startup ecosystem here is also developing fast, mostly thanks to the great talent pool”

Tomasz Rudolf

April 2017 I 18

www.globalcorporateventuring.com

INTERVIEW

their support for joining forces on creating our centre as a European hub for corporate-startup collaboration. Two months later, we could already announce the opening of our space with Mastercard’s CEO, Ajay Banga.

It is a very synergistic relationship – Mastercard is very active in working with startups through the Start Path program. Together, we can offer both corporations and startups unique collaboration opportunities.

You recently launched a scale-up club and an investors club. What is the role of each, and what do you hope they will achieve this year?

Although the focus on corporate needs is part of our DNA, we act as a single point of contact for the whole tech ecosystem in the region. Working with accelerators and venture capital funds across Europe and Israel has always been important for us, as they support us in scouting and selecting the best startups for specific corporate needs.

Recently, we decided to use our growing corporate network to help investors introduce their ready-to-scale portfolio companies to enterprise clients and partners. The scale-ups can use our executive briefings to present their solutions to our corporate network and use scheduled one-to-one meetings with interested executives to move to enterprise deals faster.

In June, the Heart Warsaw will host GCV Academy, Global Corpo-rate Venturing’s training division, which helps organisations boost their open innovation and venturing capabilities. Tell us more about this collaboration.

As a hub, we like to work with global partners that bring in leading know-how and capabilities in their field. We have been attending the GCV Symposium in London for many years now, and had no doubt that we should bring the academy to Warsaw one day. Many of our clients are in the process of setting up corporate venturing activities and it is great that we can connect them with other practitioners and thought leaders in the space. u

The GCV Academy will be running one of its accredited two-day programs at the Heart in Poland on June 13-14. Speakers will include Marcin Hejka, vice-president and managing director of Intel Capital in Poland; Paul Morris, investment director of the UK Department for International Trade’s venture capital unit, who previously set up and ran the CVC operation of Dow Chemical Europe; Andrew Gaule, leader of GCV Academy, and other leading experts. See the details and register at www.gcvacademy.com.

See the accreditation of GCV Academy by the leaders of global CVC units such as GE, Merck, IBM, Swisscom, REV and Ten-cent at: https://www.linkedin.com/pulse/from-zero-cvc-heroes-andrew-gaule

For more on the Heart, visit: www.theheart.tech

April 2017 I 19

www.globalcorporateventuring.com

SECTOR FOCUS

Our definition of the consumer sector encompasses food

and beverages, hygiene and beauty products, apparel and other clothing accessories, e-commerce platforms, con-sumer electronics and other physical consumer goods.

GCV reported 124 rounds involving corporate investors from the consumer sector between March 2016 and Feb-ruary 2017 – 52 took place in the US, 27 in China and seven in the UK and six in Germany.

Most of these 124 commit-ments went to emerging enterprises in the consumer sector (50), IT (18), services (17) and financial (12).

On a calendar year-on-year basis, total capital raised in corporate-backed investment rounds rose significantly, from $17.61bn in 2015 to $21.59bn last year, a 23% increase. The deal count on the other hand went down, declining by 8% from 149 rounds in 2015 to 137 last year.

The 10 largest investments by corporate venturers from the consumer sector cover a range of businesses, spanning transport, tel-ecoms, fashion and apparel companies, and e-commerce platforms.

Investment professionals from consumer companies told GCV they were observing two key trends – the rise of e-commerce plat-forms and the growing importance of brands that resonated with today’s buyers, who were looking for high-quality products offering “unique consumer experiences”.

Natalie Hwang, managing director at Simon Ventures, the corporate venturing arm of US-based real estate company Simon Property, specialises in evaluating next-generation commerce and retail technologies. She said the rise of e-commerce reflected the evolution of the consumer sector in the digital age.

“There are good reasons why commerce [initially] evolved to a model where consumers go to stores rather than have

E-commerce expansion boosts consumer sectorConsumer-focused corporate venturers committed a record $21.59bn over 137 rounds in 2016, primarily in consumer businesses, with e-commerce platforms dominating

Kaloyan Andonov, reporter, GCV Analytics

27

52

3

3

7

6

6

2

2

2

1

1

1

11

1

1

1

Global view of past year’s deals

ConsumerFinancialHealth

IndustrialITMedia

ServicesTelecomsTransport

Total: 124

50

18 1712

9 7 6 41

Consumer IT Services Financial Transport Industrial Media Health Telecoms

Investments by consumer venturers by sector 2016

2011 2012 2013 2014 2015 2016 2017 to date

$5,426m

$21,589m

$2,524m

$1,812m

$1,111m $359m

$17,612m

4453 52

88

149137

16

ConsumerEnergyFinancial

HealthIndustrialIT

MediaServicesTelecoms

TransportUtilities

Deals by consumer sector investors 2011-17

Number of dealsTotal value

April 2017 I 20

www.globalcorporateventuring.com

SECTOR FOCUS

merchants go to the consumer,” Hwang said. “E-commerce reverses the product selection par-adigm by bringing com-merce to the consumer, making product selection and ordering much more efficient, but with product delivery remaining the weak link in online trans-actions, particularly with last-mile logistics.”

Hwang forecast a future in which e-commerce continued to dominate a wide variety of consumer products, while tra-ditional retail largely revolved around brand differentiation. “Commodity retailing and price-sensitive categories involv-ing goods that are inexpensive to ship will increasingly continue to transact online, with in-store retailing going to highly branded retailers who excel at crafting unique consumer experiences that Will inspire, engage and compel their audiences.”

John Haugen, vice-president and general manager of 301 Inc, the corporate venturing arm of US-based consumer foods manufacturer General Mills, also stressed the role of brand differentiation. “We seek to invest in emerging food startups with a compelling product and strong brand that can be expandable,” he said (see interview).

Ben Lee, managing director of funds at CircleUp, a US-based investment platform connecting early-stage consumer brands and investors, attributes the critical role of branding to a fundamental shift in consumer attitudes. “Today people want to feel connected to what they are buying and consuming. They do not want the makeup their parents wore, and do not want to feed their dogs the brands they grew up with.”

The challenge for large corporations was that consumers were losing interest in mass-market products that have remained unchanged for decades, Lee noted. “Better-quality authentic emerging products are surfacing left and right, and they have entered the mainstream,” he said (see interview).