Embed Size (px)

Citation preview

Listed company

National Register of Corporate Taxpayers - (CNPJ)

No. 97.837.181/0001-47

NIRE -35300154410

Interim Financial Information on the Second Quarter of 2018

Duratex S.A.

DURATEX S.A. CNPJ. 97.837.181/0001-47 A Publicly Listed Company NIRE 35300154410

SUMMARIZED MINUTES OF THE MEETING OF THE BOARD OF OFFICERS HELD ON AUGUST 1st, 2018

DATE, TIME AND PLACE: on August 1st, 2018 at 8:30 a.m, at Avenida Paulista, 1938, 5th

floor, Room 505, in the city and state of São Paulo.

PRESIDING: Antonio Joaquim de Oliveira (Chairman) and Carlos Henrique Pinto Haddad

(Secretary).

QUORUM: the totality of the elected members.

RESOLUTIONS ADOPTED: following examination of the Company’s individual and

consolidated interim financial information for the quarter ended June 30, 2018, the Board of

Officers decided, unanimously and pursuant to the provisions in Sub-items V and VI, Article

25 of CVM Instruction 480/09, as amended, to declare that:

a) it has reviewed, discussed and agreed with the opinions expressed in the review report

issued by Ernst & Young Auditores Independentes S/S; and,

b) it has reviewed, discussed and agreed with the Company's individual and consolidated

interim financial information for the quarter ended June 30, 2018.

CONCLUSION: with the work of the meeting concluded, these minutes were drafted, read,

approved and signed by all. São Paulo (SP), August 1st, 2018. (aa) Antonio Joaquim de

Oliveira – Chief Executive Officer; Marcelo José Teixeira Izzo – Vice President of the Deca

Business Unit; Henrique Guaragna Marcondes – Vice President of the Wood Business Unit;

Bruno Basile Antonaccio, Carlos Henrique Pinto Haddad; José Ricardo Paraíso Ferraz,

Marcelo Koji Tahara, Marco Antonio Milleo, Maria Julieta Pinto Rodrigues Nogueira and

Nelson Ricardo Teixeira – Officers.

CARLOS HENRIQUE PINTO HADDAD

Investor Relations Officer

DURATEX S.A. CNPJ. 97.837.181/0001-47 A Publicly Traded Company NIRE 35300154410

OPINION OF THE FISCAL COUNCIL

The members of Fiscal Council of DURATEX S.A. have proceeded to examine the

Company’s individual and consolidated interim financial information for the quarter

ended June 30, 2018, which were reviewed by Ernst & Young Auditores

Independentes S/S (“E&Y”), as an independent auditor.

The Fiscal Councilors have verified the exactness of the elements examined and in

view of the unqualified review report issued by E&Y, understand that these

documents adequately reflect the equity situation, the financial position and the

activities of the Company in the period. São Paulo (SP), August 1st, 2018. (signed)

Flávio César Maia Luz – President; Carlos Eduardo de Mori Luporini and Guilherme

Tadeu Pereira Júnior – Councilors.

CARLOS HENRIQUE PINTO HADDAD Investor Relations Officer

(A free translation from Portuguese into English of Interim Financial Information prepared in Brazilian currency in accordance with accounting practices adopted in Brazil and International Financial Reporting Standards (IFRS), issued by International Accounting Standards Board – IASB) and consistently with the standards issued by the Brazilian Securities Commissions (CVM). Report on review of quarterly information To the Shareholders, Board of Directors and Officers of Duratex S.A. São Paulo - SP Introduction We reviewed the accompanying individual and consolidated interim financial information of Duratex S.A. and its subsidiaries (“the Company”), included in the Quarterly Information Form (ITR) for the quarter ended June 30, 2018, which comprise the balance sheet as of June 30, 2018, the related statement of profit or loss and comprehensive income for the three and six-month period then ended, and the statement of changes in equity and cash flows for the six month period then ended, including other explanatory information.

Management is responsible for the preparation of individual and consolidated interim financial

information in accordance with Accounting Pronouncement CPC 21 (R1) -– Demonstração

Intermediária (“CPC 21 (R1)”) and International Accounting Standard IAS 34 - Interim Financial

Reporting (“IAS 34”), issued by the International Accounting Standards Board (IASB), as well

as for the presentation of this information in a manner consistent with the standards issued by

the Brazilian Securities and Exchange Commission (CVM) applicable to the preparation of the

Quarterly Information Form (ITR). Our responsibility is to express a conclusion on this interim

financial information based on our review. Scope of review

We conducted our review in accordance with Brazilian and International Standards on Review

Engagements (NBC TR 2410 Revisão de Informações Intermediárias Executada pelo Auditor

da Entidade) and ISRE 2410 - Review of Interim Financial Information Performed by the

Independent Auditor of the Entity). A review of interim financial information consists of making

inquiries, primarily of persons responsible for financial and accounting matters, and applying

analytical and other review procedures. A review is substantially less in scope than an audit

conducted in accordance with Brazilian and International Standards on Auditing and

consequently does not enable us to obtain assurance that we would become aware of all

significant matters that might be identified in an audit. Accordingly, we do not express an audit

opinion.

Conclusion on the individual and consolidated interim financial information Based on our review, nothing has come to our attention that causes us to believe that the accompanying individual and consolidated interim financial information included in the quarterly

information referred to above is not prepared, in all material respects, in accordance with CPC

21 (R1) and IAS 34, applicable to the preparation of Quarterly Information Form (ITR),

consistently with the rules issued by the CVM. Other matters Statements of value added

We have also reviewed the individual and consolidated statements of value added for the six

month period ended June 30, 2018, prepared under the responsibility of the Company’s

management, the presentation of which in the interim financial information is required by rules

issued by the Brazilian Securities Commission (CVM) applicable to the preparation of Quarterly

Financial Information (ITR), and considered as supplementary information under IFRS -

International Financial Reporting Standards, which does not require the presentation of the

statement of value added. These statements have been subjected to the same review

procedures previously described and, based on our review, nothing has come to our attention that causes us to believe that they are not prepared, in all material respects, in accordance with

the overall individual and consolidated interim financial information.

São Paulo, August 01

st, 2018.

ERNST & YOUNG Auditores Independentes S.S. CRC-2SP034519/O-6 Drayton Teixeira de Melo Accountant CRC-1SP236947/O-3

1

Interim Financial Information Index on the second quarter of 2018 Management Report ................................................................................................................................................................. 02 Balance Sheet .......................................................................................................................................................................... 09 Statement of Income ................................................................................................................................................................ 10 Statement of Comprehensive Income ...................................................................................................................................... 11 Statement of Cash Flows …………………………...................................................................................................................... 12 Statement of Value Added ...................................................................................................................................................... 13 Statement of Changes in Stockholders’ Equity 2017 ............................................................................................................... 14 Statement of Changes in Stockholders’ Equity 2018 ............................................................................................................... 15 Note 1 – Operations ................................................................................................................................................................ 16 Note 2 – Basis of preparation and significant accounting practices…....................................................................................... 17 2.1 Accounting policies........................................................................................................................................................... 17 2.2 Consolidation of the interim financial information………..................................................................................................... 21 2.3 New accounting standards, amendments and interpretations.......................................................................................... 21 2.4 Presentation of segmented information............................................................................................................................ 21 Note 3 – Critical Accounting Judgments and Estimates............................................................................................................. 21 Note 4 – Financial Risk Management ....................................................................................................................................... 22 4.1 Financial Risk Factors ….................................................................................................................................................. 22 4.2 Capital Management ........................................................................................................................................................ 25 4.3 Fair Value Estimates ........................................................................................................................................................ 25 Note 5 – Cash and Cash Equivalents ….................................................................................................................................... 26 Note 6 –Securities………………….............................................................................................................................................. 26 Note 7 – Trade Accounts Receivable ........................................................................................................................................ 27 Note 8 – Inventories .................................................................................................................................................................. 28 Note 9 – Other Receivables ...................................................................................................................................................... 28 Note 10 – Recoverable Taxes and Contributions ..................................................................................................................... 28 Note 11 – Non-current assets available for sale........................................................................................................................ 29 Note 12 – Deferred Income Tax and Social Contribution …...................................................................................................... 29 Note 13 – Related Parties ......................................................................................................................................................... 31 Note 14 – Investments in Subsidiaries………………................................................................................................................... 33 Note 15 – Property, Plant and Equipment ................................................................................................................................. 35 Note 16 – Biological Assets (Forest Reserves) ......................................................................................................................... 36 Note 17 – Intangible Assets ...................................................................................................................................................... 38 Note 18 – Loans and Financing ............................................................................................................................................... 39 Note 19 – Accounts Payable ..................................................................................................................................................... 42 Note 20 –Taxes and contributions.............................................................................................................................................. 42 Note 21 – Contingencies............................................................................................................................................................ 43 Note 22 – Rural Leases …….................................................................................................................................................... 44 Note 23 – Stockholders’ Equity ................................................................................................................................................. 45 Note 24 – Insurance Coverage ................................................................................................................................................. 46 Note 25 – Net Sales Revenue ………........................................................................................................................................ 46 Note 26 – Expenses, by Nature ............................................................................................................................................... 47 Note 27 – Financial Income and Expenses ............................................................................................................................... 47 Note 28 – Other Operating Income (Expenses), Net ................................................................................................................ 48 Note 29 – Income Tax and Social Contribution …..................................................................................................................... 48 Note 30 – Stock Option Plan ..................................................................................................................................................... 48 Note 31 – Private Pension Plan ................................................................................................................................................ 49 Note 32 – Medical Assistance Plan “Post-Employment”………………………………………………………………………………. 50 Note 33 – Earnings Per Share .................................................................................................................................................. 50 Note 34 –Business Segments ................................................................................................................................................... 51 Note 35 – Subsequent events………………… .......................................................................................................................... 51

2

MANAGEMENT REPORT 2Q2018 MARKET AND BUSINESS SCENARIO The set of macroeconomic indicators suggests that the economy continues to recover. Nonetheless, the expectations indicate that the pace of this recovery is more gradual than at the beginning of the year, signaling a slower recovery than previously expected. During the second quarter of 2018, we noticed a pick up in the domestic activity levels due to the growth in demand and unemployment rates following a downward trend at a moderate pace. The performance of the quarter was negatively impacted by the halt in the transportation sector, which occurred in May. Our operations faced supply and shipping issues, which hampered the performance of all business divisions. This effect was partially offset in June. According to ABRAMAT, the deflated sales of the building materials industry dropped by 0.4% in the first half of 2018. This data was impacted by the effects of the truck drivers' strike; thus, the association maintains a positive expectation regarding the evolution of this indicator in the rest of the year, sustaining the growth estimate of 1.5% in 2018. Employment level in the sector continues to show a decreasing trend, with a decline of 1.2% year to date. In the wood panels industry, IBÁ recorded a 2% growth in the local demand for wood panels during the first half of 2018. The demand for MDP grew 4% in volumes and the demand for MDF increased 1%. In the foreign market, exports grew 9% compared to the first half of 2017. MDP's volumes in exports increased 19%, while the MDF volumes grew 2%. Despite the revised estimates, projections still point to a growth in GDP during 2018. The growth in household consumption and investments, coupled with continued monetary policy and a reduction in the level of unemployment may have a positive impact on our operations throughout the year. STRATEGIC MANAGEMENT AND INVESTMENTS Consolidated investments in the quarter amounted to BRL 115.3 million, mainly directed towards the sustaining of our operations. This amount consists of BRL 68.0 million for manufacturing maintenance and projects and BRL 47.3 million invested in the formation of biological assets. In the first half of the year, the total amount invested was BRL 196.6 million. The internal agenda, supported by the solid Duratex Management System, remains a daily priority. The slower than expected resumption of the economy will demand even more efforts to save costs, gain productivity, and efficiently manage working capital and investments, with the clear objective of reaching a better return on our capital. In 2018, we are stepping forward in an important stage of the Journey of Cultural Transformation, strengthening a new way of approaching our business. In order to stimulate a more results-oriented organizational culture, we are investing in innovation and digital technology to sustain the growth of our operations. As a result of a deep review of our asset base, we have implemented movements that will be material to improving the returns in our business. Earlier this year, we announced the transaction with Eucatex for the sale of machinery and equipment dedicated to the production of hardboard, which remains under analysis by CADE for its effective conclusion. In addition, we have sold forest assets in the state of São Paulo to Suzano Papel e Celulose. This operation was completed at the beginning of July, with the exercise of the call option by Suzano. Finally, we dedicate part of our forests in the Triângulo Mineiro region to an association with the Austrian group Lenzing AG, through the constitution of a Joint Venture, to produce dissolving wood pulp. These initiatives ended a cycle of adjustments of surplus assets in the Wood Division, contributing to leverage the results without harmful effects in current operations.

3

Lastly, as a subsequent event, we announced in July 2018 an investment plan to expand production capacity in Ceramic Tiles. We have announced our debut in this industry through the acquisition of Ceusa in the second half of 2017 and this project shall increase market share and has the target of increasing margins and the return of this operation. It will be invested BRL 94 million in the years 2018 and 2019 to modernize the existing lines and build a new line, increasing production capacity by 83%. Therefore, the Ceramic Tiles operations will have annual production capacity of 11 million square meters after this project. We are positioning the Company in a strategic competitiveness level through financial deleveraging, management excellence, a renewed organizational culture and the definition of avenues for growth. CONSOLIDATED FINANCIAL RESULTS

(1) EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization): Measure of operational performance in accordance with CVM Instruction 527/12.

(2) EBITDA adjusted for non-cash events arising from variation in the fair value of biological assets and combination of businesses, in addition to extraordinary events.

(3) For better understanding, the net revenue of BRL 57,072 related to the sale of timber to Suzano Papel e Celulose was excluded from the calculation of Adjusted and Recurring EBITDA margin.

(4) Current liquidity: Current Assets Divided by Current Liabilities. Indicates the amount available in BRL to cover each BRL of short-term obligations.

(5) Net Indebtedness: Total Financial Debt (–) Cash balance. (6) Financial leverage calculated on the rolling EBITDA over the last 12 months, adjusted for events of a purely

accounting and non-cash nature. (7) ROE (Return on Equity): measure of performance obtained by taking the annualized Net Earnings over the

period, annualized, and dividing by Average Net Equity. (8) Net earnings per share is calculated by dividing the earnings attributable to the company’s shareholders by the

average weighted number of ordinary shares issued during the period, excluding the ordinary shares held by the Treasury.

ADDED VALUE Value Added in the quarter totaled BRL 621.9 million. Of this amount, BRL 176.2 million, equivalent to 28.3% of total Added Value, was allocated to the federal, state and municipal governments in the form of taxes and contributions.

In BRL '000 2Q18 2Q17 % 1Q18 % 1H18 1H17 %

Highlights

Volume shipped Deca (‘000 items) 6.821 6.252 9,1% 6.268 8,8% 13.089 13.058 0,2%

Volume shipped Ceramic tiles (m2) 1.237.116 - - 1.261.123 -1,9% 2.498.239 - 0,0%

Volume shipped Wood (m3) 613.601 526.572 16,5% 600.697 2,1% 1.214.298 1.112.558 9,1%

Consolidated Net Revenue 1.167.477 916.724 27,4% 1.005.982 16,1% 2.173.459 1.868.713 16,3%

Gross profit 309.858 245.306 26,3% 274.318 13,0% 584.176 477.398 22,4%

Gross margin 26,5% 26,8% 27,3% 26,9% 25,5%

EBITDA according to CVM No. 527/12 (1) 501.521 218.639 129,4% 224.889 123,0% 726.410 411.507 76,5%

EBITDA Mg CVM No. 527/12 43,0% 23,9% 22,4% 33,4% 22,0%

Adjustments for non-cash events (28.248) (40.542) -30,3% (42.761) -33,9% (71.009) (82.567) -14,0%

Non-recurring events (253.254) - - (253.254) (2.672) 9378,1%

Adjusted and Recurring EBITDA (2) 220.019 178.097 23,5% 182.128 20,8% 402.147 326.268 23,3%

Adjustred and Recurring EBITDA margin (3) 19,8% 19,4% 18,1% 19,0% 17,5%

Net income 166.584 24.767 572,6% 30.823 440,5% 197.407 17.253 1044,2%

Recurring net income 27.498 24.767 11,0% 30.823 -10,8% 58.321 15.489 276,5%

Recurring net margin 2,5% 2,7% 3,1% 2,8% 0,8%

INDICATORS

Current ratio(4) 2,86 2,30 24,4% 1,98 44,6% 2,86 2,30 24,4%

Net debt(5) 2.163.101 2.108.077 2,6% 2.216.066 -2,4% 2.163.101 2.108.077 2,6%

Net debt/EBITDA LTM(6) 2,59 2,89 -10,5% 2,79 -7,3% 2,59 2,89 -10,5%

Average Shareholder's equity 4.884.211 4.582.442 6,6% 4.743.865 3,0% 4.828.247 4.578.512 5,5%

ROE (7) 13,6% 2,2% 2,6% 8,2% 0,8%

Recurring ROE 2,3% 2,2% 2,6% 2,4% 0,7%

SHARES

Earnings per share (BRL) (8) 0,2415 0,0359 572,7% 0,0447 440,3% 0,2862 0,0250 1044,8%

Closing share price (BRL) 8,70 8,17 6,5% 11,85 -26,6% 8,70 8,17 6,5%

Net equity per share (BRL) 7,25 6,67 8,7% 6,92 4,7% 7,25 6,67 8,7%

Treasury Shares 2.410.659 2.485.759 -3,0% 2.478.659 -2,7% 2.410.659 2.485.759 -3,0%

Market Cap (BRL1.000) 5.997.552 5.631.571 6,5% 8.168.274 -26,6% 5.997.552 5.631.571 6,5%

4

OPERATIONS Wood

(1) EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization): Measure of operational performance

according to Instruction CVM527/12; (2) Non-recurring events: 2Q18: results from the sale of lands from Duratex Florestal (-) BRL 196.182; Results from

the sale of timber from Duratex Florestal in the transaction with Suzano Papel e Celulose (-) BRL 57.072; 1Q17: results from the sale of land from Duratex Florestal (-) BRL 2.672.

(3) For better understanding, the net revenue of BRL 57,072 related to the sale of timber to Suzano Papel e Celulose was excluded from the calculation of Adjusted and Recurring EBITDA margin.

The second quarter of 2018 was positive for the Wood Division, continuing the process of recovery in the main markets, in spite of the negative effects of the truck drivers' strike. We noted a growth in volumes sold and the profitability of operations, following the gradual pace of recovery. Net revenue for the quarter was BRL 747.5 million, up 32.6% over the previous year. The growth in the volume sold of wood panels was a result of a better level of local demand in the period, with an increase in market share and an increase in exports. In addition, there were important forest sales in the quarter, which also contributed to this growth. In the first tranche of the operation with Suzano Papel e Celulose, accounted in this quarter, approximately BRL 60.0 million of timber was sold. Moreover, there was also a sale of timber to other customers around BRL 20.0 million above the average level in other quarters. In relation to the second quarter of last year, we had a higher concentration of lower value-added products goods in the composition of the product mix as a consequence of the market recovery in the furniture manufacturing chain. On the other hand, we noticed a better performance in the wood panel retail sector compared to the first quarter of that year, resulting in a slightly better mix than at the beginning of the year. In the Division's cost structure, we had a concentration of planned shutdowns to maintenance in the first half of this year. In addition, we noted an increase in the cost of the main commodities, both for price hikes and for the depreciation of the Brazilian Real. The adjusted and recurring EBITDA for the quarter was 163.3 million, with an EBITDA margin of 23.7%. It is worth mentioning that the recurring EBITDA and the respective margin disregard the sale of land and forests to Suzano Papel e Celulose. This result was also benefited by FX effect in the consolidation of Colombia's results, due to the appreciation of the Colombian Peso in relation to the Brazilian Real in the period.

HIGHTLIGHTS 2Q18 2Q17 % 1Q18 % 1H18 1H17 %

SHIPMENTS (IN M³)

STANDARD 357.601 294.887 21,3% 356.428 0,3% 714.029 608.343 17,4%

COATED 256.000 231.685 10,5% 244.269 4,8% 500.269 504.215 -0,8%

TOTAL 613.601 526.572 16,5% 600.697 2,1% 1.214.298 1.112.558 9,1%

FINANCIAL HIGHLIGHTS (BRL 1,000)

NET REVENUE 747.488 563.536 32,6% 628.103 19,0% 1.375.591 1.172.462 17,3%

DOMESTIC MARKET 535.494 417.654 28,2% 468.729 14,2% 1.004.223 888.575 13,0%

FOREIGN MARKET 211.994 145.882 45,3% 159.374 33,0% 371.368 283.887 30,8%

Net revenue per unit (BRL/m3 shipped) 1125,19 1070,20 5,1% 1045,62 7,6% 1085,83 1053,84 3,0%

cash cost per unit (BRL/m3 shipped) (679,82) (711,19) -4,4% (662,03) 2,7% (671,02) (710,95) -5,6%

Gross profit 189.769 129.925 46,1% 169.448 12,0% 359.217 255.805 40,4%

Gross margin 25,4% 23,1% - 27,0% - 26,1% 21,8% -

Selling expenses (93.811) (86.805) 8,1% (89.263) 5,1% (183.074) (175.001) 4,6%

General and administrative expenses (22.014) (18.403) 19,6% (18.026) 22,1% (40.040) (37.566) 6,6%

Operating profit before financial results 268.212 35.305 659,7% 57.751 364,4% 325.963 55.170 490,8%

Depreciation, amortization and depletion 113.075 77.291 46,3% 79.554 42,1% 192.629 159.196 21,0%

Depletion tranche of biological assets 64.134 27.385 134,2% 31.146 105,9% 95.280 61.463 55,0%

EBITDA according to CVM No. 527/12 (1) 445.421 139.981 218,2% 168.451 164,4% 613.872 275.829 122,6%

EBITDA margin according to CVM No. 527/12 59,6% 24,8% - 26,8% - 44,6% 23,5% -

Variation in fair value of biological assets (29.271) (38.582) -24,1% (42.579) -31,3% (71.850) (81.303) -11,6%

Employee benefits 419 (743) -156,4% 458 -8,5% 877 398 120,4%

Non Recurring events (2) (253.254) - - - - (253.254) (2.672) 9378,1%

Adjusted and Recurring EBITDA 163.315 100.656 62,3% 126.330 29,3% 289.645 192.252 50,7%

Adjusted and Recurring EBITDA margin (3) 23,7% 17,9% - 20,1% - 21,1% 16,4% -

5

We remain aiming attention at sustaining a commercial policy that focus on margins, without giving up our market share. Supported by the Duratex Management System and an efficient productivity management, we expect to continue the positive trend of profitability in the Wood Division. Deca

(1) EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization): Measure of operational performance

according to Instruction CVM527/12.

In spite of the still challenging scenario of the civil construction, the volumes shipped in the Deca showed a growth of approximately 9% in relation to the periods of comparison. Demand from new homes remained depressed; thus, the retail channel continued to be driver of demand for building materials in the period. In basic goods, we presented an increase of 14.2% compared to the same period of last year, in contrast to the 6.3% decrease compared to the previous quarter. Deca’s net revenue was BRL 374.3 million in the quarter, driven by the higher volume sold. This result represents a growth of 6.0% in relation to 2Q17 and 12.2% in relation to the first quarter of this year. The positive evolution of revenue signals the recovery compared to the negative scenario presented at the beginning of 2018. In relation to the same period last year, we noticed a deterioration of the mix of products sold in both Deca's three main businesses, with a concentration of sales of lower value-added goods. This change reflected a reduction of 2.9% in net revenue per unit. Compared to 1Q18, there was a greater increase in sales of electronic showers, stimulated by the seasonality of sales of this type of product. In addition, metals and ceramic sanitary ware showed a slight improvement in the mix of products sold compared to the previous quarter. Overall, costs continue to negatively pressure the results. The inflation of the raw materials in the Deca has been harmful to the profitability of the operations, with emphasis on the increase of the exchange rate and commodities costs. The initiatives within Duratex Management System partially offset this setback, but they were not sufficient to absorb all the worsening. We also noticed deterioration in industrial performance in the quarter, influenced mainly by the change of mix and instability in production. Adjusted and recurring EBITDA in the quarter was BRL 47.2 million, with an EBITDA margin of 12.6%. This performance was worse than the same period of last year, intensified by tax gains recorded at the time of around BRL 15.5 million. Compared to the first quarter of the year, there was an improvement of 3.3%.

HIGHLIGHTS 2Q18 2Q17 % 1Q18 % 1H18 1H17 %

SHIPMENTS (IN ‘000 ITEMS)

BASIC GOODS 1.851 1.621 14,2% 1.975 -6,3% 3.826 3.719 2,9%

FINISHING GOODS 4.970 4.631 7,3% 4.293 15,8% 9.263 9.339 -0,8%

TOTAL 6.821 6.252 9,1% 6.268 8,8% 13.089 13.058 0,2%

FINANCIAL HIGHLIGHTS (BRL1,000)

NET REVENUE 374.334 353.188 6,0% 333.534 12,2% 707.868 696.251 1,7%

DOMESTIC MARKET 351.696 338.835 3,8% 319.476 10,1% 671.172 671.016 0,0%

EXPORTS 22.638 14.353 57,7% 14.058 61,0% 36.696 25.235 45,4%

Net revenue per unit (BRL per item shipped) 54,88 56,49 -2,9% 53,21 3,1% 54,08 53,32 1,4%

Cash cost per unit (BRL per item shipped) (36,36) (34,12) 6,6% (35,50) 2,4% (35,95) (32,64) 10,1%

Gross profit 101.746 115.381 -11,8% 87.108 16,8% 188.854 221.593 -14,8%

Gross margin 27,2% 32,7% - 26,1% - 26,7% 31,8% -

Selling expenses (61.490) (66.199) -7,1% (53.913) 14,1% (115.403) (124.754) -7,5%

General and administrative expenses (18.722) (16.795) 11,5% (17.848) 4,9% (36.570) (32.368) 13,0%

Operating profit before financial results 17.591 50.789 -65,4% 17.864 -1,5% 35.455 80.731 -56,1%

Depreciation and amortization 28.980 27.869 4,0% 28.425 2,0% 57.405 54.947 4,5%

EBITDA according to CVM No. 527/12(1) 46.571 78.658 -40,8% 46.289 0,6% 92.860 135.678 -31,6%

EBITDA margin according to CVM No. 527/12 12,4% 22,3% - 13,9% - 13,1% 19,5% -

Employee benefits 604 (1.217) -149,6% (640) -194,4% (36) (1.662) -97,8%

Non-recurring events - - - - - - - -

Adjusted and Recurring EBITDA 47.175 77.441 -39,1% 45.649 3,3% 92.824 134.016 -30,7%

Adjusted and Recurring EBITDA margin 12,6% 21,9% - 13,7% - 13,1% 19,2% -

6

Despite the uncertainties regarding the resumption of the construction segment and, consequently, the demand for building materials, we are concentrating efforts to recover the margins and profitability of the operation for the rest of the year. We have structured a plan with a holistic approach to the reversal of this scenario, with emphasis on the implementation of a second price readjustment in the year, execution capacity at the point of sale, establishment of industrial initiatives aimed at improving the Division's operational performance and productivity gains, revaluation of fixed expenses and restructuring in the manufacturing areas at the end of the second quarter to make the hierarchy leaner and more agile. Ceramic Tiles

(1) EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization): Measure of operational performance

according to Instruction CVM527/12. Among the businesses that make up our portfolio of solutions, Ceusa was the largest affected by the transportation sector strike. Since the ceramic tiles operations are running with a high rate of capacity utilization, the stoppage directly affected the performance of the business. We recorded a slight reduction of volumes compared to 1Q18, down 1.9%, due entirely to the effects of the truck drivers’ strike. On the other hand, there was an improvement in the mix of products sold, partially offsetting the effects of volume reduction. Net revenue was BRL 45.7 million, an increase of 3.0% over the previous period. The worst dilution of fixed costs of the Ceramic Tiles Division had a direct impact on the performance of the quarter. Adjusted and recurring EBITDA was BRL 9.5 million, reflecting an EBITDA margin of 20.9%. This result was 6.1% lower than the one presented at the beginning of 2018. EBITDA totaled BRL 19.7 million in the six-month period, representing a margin of 21.9%, a benchmark in the ceramic tile industry.

HIGHLIGHTS 2Q18 1Q18 % 1H18

SHIPMENTS (IN M²)

FINISHING GOODS 1.237.116 1.261.123 -1,9% 2.498.239

TOTAL 1.237.116 1.261.123 -1,9% 2.498.239

FINANCIAL HIGHLIGHTS (BRL1,000)

NET REVENUE 45.655 44.345 3,0% 90.000

DOMESTIC MARKET 41.480 40.693 1,9% 82.173

EXPORTS 4.175 3.652 14,3% 7.827

Net revenue per unit (BRL per m² shipped) 36,90 35,16 5,0% 36,03

Cash cost per unit (BRL per m² shipped) (20,88) (19,95) 4,6% (20,41)

Gross profit 18.343 17.762 3,3% 36.105

Gross margin 40,2% 40,1% - 40,1%

Selling expenses (8.478) (7.377) 14,9% (15.855)

General and administrative expenses (1.817) (1.554) 16,9% (3.371)

Operating profit before financial results 8.002 8.698 -8,0% 16.700

Depreciation and amortization 1.527 1.451 5,2% 2.978

EBITDA according to CVM No. 527/12(1) 9.529 10.149 -6,1% 19.678

EBITDA margin according to CVM No. 527/12 20,9% 22,9% - 21,9%

Employee benefits - - -

Non-recurring events - - - -

Adjusted and Recurring EBITDA 9.529 10.149 -6,1% 19.678

Adjusted and Recurring EBITDA margin 20,9% 22,9% 21,9%

7

We expect a slight improvement over the result presented in this quarter for the rest of the year, including the total recovery of volumes not shipped at the strike. In the Ceramic Tiles Division, we remain focused on integrating our businesses and constantly improving the mix of products sold. CAPITAL MARKETS AND CORPORATE GOVERNANCE In the end of the second quarter of 2018, the market cap was equivalent to BRL 5,997.6 million as a result of a final share price of BRL 8.70. During this period, there were 309,251 trades with our shares in the spot market of B3. It represented a trading volume of BRL 1,246.9 million or an average daily trading volume of BRL 19.8 million. Our shares are listed on the Novo Mercado, a segment of B3 that brings together companies with the highest corporate governance standards. We also have a differentiated dividend distribution policy, with a payout ratio equivalent to 30% of adjusted net income. Lastly, we adhered to the Abrasca Code of Self-Regulation and Good Practices of Publicly-held Companies. SOCIAL AND ENVIRONMENTAL RESPONSABILITY The headcount showed a slight increase compared to the previous quarter, ending the period with 11,450 employees. In the comparison of the quarters, we presented a reduction in the workforce in spite of the incorporation of Ceusa employees, acquired in October 2017.

In April, we launched the project "Proteger e Sorrir em Rede" in partnership with Childhood Brasil, which aims to contribute to the reduction of sexual violence against children and adolescents in Brazil. As a first step in the initiative, stakeholders were gathered around the Deca Louças unit in João Pessoa, Paraíba, to develop a methodology to help companies in the region identify and curb cases of sexual violence against children and adolescents. In the next steps of this work, Duratex will host, in the third quarter of 2018, a workshop to map the activities already carried out by the local communities for the protection of children and adolescents, regarding the care, prevention and diagnosis of situations of violence against this public. Duratex launched in June a pilot project, through the brand Hydra, in which it encourages its consumers to return used electric showers for proper disposal. It was an unprecedented initiative in this industry and foreseen in the Sustainability Strategy 2025. The initiative covers the metropolitan region of São Paulo, in addition to the city of Sorocaba, and was developed in partnership with the network of building materials stores Leroy Merlin and the company Sinctronics, which operates systems for the collection and reuse of electronic components. INDEPENDENT AUDITORS – CVM INSTRUCTION Nº 381 Procedures adopted by the Company and its subsidiaries The Company's and its subsidiaries' policy of contracting services not related to external auditing with our independent auditors is based on internationally accepted principles that preserve the independence of these auditors and consist of: (a) the auditor should not audit their own work (b) the auditor should not perform managerial duties on his client and (c) the auditor should not promote the interests of his client.

(BRL'000) 2Q18 2Q17 % 1Q18 % 1H18 1H17 %

Employees (quantity) 11.450 11.510 -0,5% 11.437 0,1% 11.450 11.510 -0,5%

Remuneration 112.885 106.925 5,6% 109.882 2,7% 222.767 209.657 6,3%

Obligatory legal charges 60.411 58.504 3,3% 52.542 15,0% 112.953 108.423 4,2%

Differentiated benefits 28.741 26.333 9,1% 26.644 7,9% 55.385 51.953 6,6%

8

In the period from January to June 2018, the independent auditors Ernst & Young Auditores Independentes S.S. provided the following services not related to external auditing:

Review of accounting and tax accounting records - ECF, date of hiring on May 16, 2018, for the total amount of BRL 0.105 million.

The amount represents 5.2% of the total audit fees for the 2018 financial statements. Explanation from the Independent Auditors - Ernst & Young Auditores Independentes S.S. The professional services described above do not affect the independence or the objectivity in conducting the external audit examinations provided to the Company and its subsidiaries. The policy of providing the Company and its subsidiaries in services not related to external auditing is based on the principles that preserve the independence of the Independent Auditor and all the services are in compliance with this policy. ACKNOWLEDGEMENTS We are grateful for all the support received from shareholders, the dedication and commitment of our employees, the partnerships we have with our suppliers and the confidence placed on us by our clients and consumers.

The Management

ASSETS LIABILITIES AND STOCKHOLDERS' EQUITY

06/30/2018 12/31/2017 06/30/2018 12/31/2017 06/30/2018 12/31/2017 06/30/2018 12/31/2017

CURRENT ASSETS Note 1,980,419 2,022,042 3,313,163 3,023,458 CURRENT LIABILITIES Note 885,532 1,219,308 1,159,729 1,551,576

Cash and cash equivalents 5 287,296 402,698 826,516 1,074,364 Loans and financing 18 373,870 696,882 447,545 764,824

Securities 6 - 57,292 - - Suppliers 272,987 216,040 358,737 296,372

Trade accounts receivable 7 713,488 765,188 971,535 932,917 Related parties suppliers 13 24,079 22,958 - -

Related parties accounts receivable 7 97,240 53,307 40,949 35,146 Personnel 99,488 95,538 125,227 119,037

Inventories 8 696,747 614,843 876,314 760,093 Accounts payable 19 85,202 92,311 155,051 163,704

Other receivables 9 30,733 25,915 185,224 63,529 Related parties accounts payable 13 2,050 2,050 2,640 2,640

Recoverable taxes and contributions 10 104,152 87,955 162,565 138,878 Taxes and contributions 20 27,583 32,390 70,097 143,726

Other credits 13,473 9,336 18,313 13,023 Dividends and interest on capital 273 61,139 432 61,273

Non current assets available for sale 11 37,290 5,508 231,747 5,508

NON-CURRENT ASSETS 5,928,680 5,753,996 6,174,728 6,442,116 NON-CURRENT LIABILITIES 2,027,862 1,841,365 3,331,152 3,197,679

Restricted deposits 49,952 48,183 53,982 51,343 Loans and financing 18 1,721,370 1,541,038 2,542,072 2,410,000

Other receivables 9 69,017 53,544 111,742 106,493 Contingencies 21 84,010 82,641 114,697 114,432

Pension plan credits 31 95,207 96,093 104,899 105,740 Deferred income tax and social contribution 12 166,365 162,331 481,815 483,338

Recoverable taxes and contributions 10 9,300 10,999 11,547 13,215 Accounts payable 19 50,993 49,206 185,968 181,989

Deferred income tax and social contribution 12 246,547 230,089 319,737 313,146 Related parties 13 5,124 6,149 6,600 7,920

Investments in subsidiaries and associates 14 2,653,704 2,397,310 5,588 6,260

Other investments 921 921 3,446 1,638

Property, plant and equipment 15 2,329,982 2,435,529 3,346,080 3,490,141 STOCKHOLDERS' EQUITY 23 4,995,705 4,715,365 4,997,010 4,716,319

Biological assets 16 - - 1,559,202 1,698,855 Capital 1,970,189 1,970,189 1,970,189 1,970,189

Intangible assets 17 474,050 481,328 658,505 655,285 Costs on issue of shares (7,823) (7,823) (7,823) (7,823)

Capital reserves 346,564 345,300 346,564 345,300

Capital transactions with partners (18,731) (18,731) (18,731) (18,731)

Revaluation reserves 55,085 57,344 55,085 57,344

Revenue reserves 2,172,263 1,980,082 2,172,263 1,980,082

Treasury shares (27,087) (27,851) (27,087) (27,851)

Carrying value adjustments 505,245 416,855 505,245 416,855

Equity attributable to equity holders

of the parent company 4,995,705 4,715,365 4,995,705 4,715,365

Noncontrolling interests - - 1,305 954

TOTAL ASSETS 7,909,099 7,776,038 9,487,891 9,465,574 TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY 7,909,099 7,776,038 9,487,891 9,465,574

(A free translation of the original in Portuguese)

Duratex S.A. - Listed companyNational Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

BALANCE SHEET

PARENT COMPANY CONSOLIDATED PARENT COMPANY CONSOLIDATED

(In thousands of Reais)

9

Note 06/30/2018 06/30/2017 06/30/2018 06/30/2017

NET SALES REVENUE 25 1,660,256 1,551,097 2,173,459 1,868,713

Variations in the fair value of biological assets 16 - - 71,850 81,303

Cost of products sold (1,319,049) (1,284,893) (1,661,133) (1,472,618)

GROSS PROFIT 341,207 266,204 584,176 477,398

Selling expenses (248,810) (244,027) (314,332) (299,755)

General and administrative expenses (54,315) (51,861) (79,981) (69,934)

Management fees (7,658) (7,293) (8,252) (7,683)

Other operating income (expenses), net 28 (8,796) 31,181 196,507 35,875

Equity in the results of investees 229,509 83,603 - -

OPERATING PROFIT BEFOREFINANCIAL RESULT AND TAXES 251,137 77,807 378,118 135,901

Financial income 27 39,142 36,566 58,039 86,268

Financial expenses 27 (107,675) (128,542) (149,858) (208,186)

PROFIT (LOSS) BEFORE INCOME TAX ANDSOCIAL CONTRIBUTION 182,604 (14,169) 286,299 13,983

Income tax and social contribution - current 29 (1,142) - (114,883) (24,687)

Income tax and social contribution - deferred 29 15,857 31,370 25,991 27,957

NET INCOME FOR THE PERIOD 197,319 17,201 197,407 17,253

Net income attributable to:

Owners of the company 197,319 17,201 197,319 17,201

Noncontrolling interests - - 88 52

Net income per share (R$):

Basic: 33 0.2862 0.0250 0.2862 0.0250

Diluted: 33 0.2827 0.0246 0.2827 0.0246

Duratex S.A. - Listed companyNational Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

STATEMENT OF INCOME

PARENT COMPANY

(A free translation of the original in Portuguese)

CONSOLIDATED

10

(A free translation of the original in Portuguese)

Periods ended June 30

(In thousands of Reais)

06/30/2018 06/30/2017 06/30/2018 06/30/2017

NET INCOME FOR THE PERIOD 197,319 17,201 197,407 17,253

Other components of comprehensive income

Items that will not be reclassified for net income

Equity of investees on comprehensive of subsidiaries (162) - (162) (311)

Adjustments from CPC 47 and 48 transition (4,833) - (4,833) -

Equity of investees reflex on transition adjustments CPC 47 and 48 (2,048) - (2,048) -

Items that will be reclassified for net income

Accumulated conversion adjustments 88,390 7,971 88,722 7,998

COMPREHENSIVE INCOME FOR THE PERIOD, NET OF TAX 278,666 25,172 279,086 24,940

Attributable to:

Owners of the company 278,666 25,172 278,666 25,172

Noncontrolling interests - - 420 (232)

Duratex S.A. - Listed companyNational Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

STATEMENT OF COMPREHENSIVE INCOME

PARENT COMPANY CONSOLIDATED

11

(A free translation of the original in Portuguese)

06/30/2018 06/30/2017 06/30/2018 06/30/2017

OPERATING ACTIVITIES:

182,604 (14,169) 286,299 13,983

ADJUSTMENTS:

Depreciation, amortization and depletion 153,876 149,535 348,292 275,606

Variations in the fair value of biological assets - - (71,850) (81,303)

Interest, foreign exchange and monetary variations, net 77,519 122,849 113,790 192,145

Equity in the results of investees (229,509) (83,603) - -

Allowance for doubtful accounts 2,431 8,119 4,214 7,974

Provisions, disposal of assets 11,375 33,614 83,910 31,938

(Increase)/Decrease in Assets

Trade accounts receivable (1,249) (2,177) (47,764) (56,104)

Inventories (79,227) (69,065) (99,864) (78,587)

Other assets (41,455) (81,418) (290,378) (53,254)

Increase (Decrease) in Liabilities

Suppliers 58,068 60,019 54,590 75,108

Personnel liabilities 3,950 20,828 5,708 26,908

Accounts payable (6,838) (2,840) (21,407) (6,423)

Taxes and contributions (349) (7,238) (75,641) (54,642)

Other liabilities (3,804) (8,975) (7,373) (17,160)

Cash provided by operations 127,392 125,479 282,526 276,189

Income tax and social contribution paid (5,600) (4,257) (116,065) (11,638)

Interests paid (45,367) (72,525) (77,099) (126,894)

CASH PROVIDED BY OPERATING ACTIVITIES 76,425 48,697 89,362 137,657

INVESTMENT ACTIVITIES:

Securities 57,925 - - -

Investments in fixed assets (62,430) (73,016) (96,377) (94,750)

Investments in intangible assets (9,707) (3,742) (9,801) (3,768)

Investments in biological assets - - (90,412) (98,269)

Receipt by sale of property, plant and equipment - - 126,515 -

Dividends received from subsidiaries 199,999 250,000 - -

Advance for future capital increase in subsidiaries (144,762) (9,410) - -

CASH USED IN INVESTMENT ACTIVITIES 41,025 163,832 (70,075) (196,787) - - - -

FINANCING ACTIVITIES:

Financing 385,000 15,069 389,850 16,083

Amortization of financing (557,843) (308,383) (605,029) (332,174)

Interest on capital and dividends (60,773) (6,046) (60,773) (6,084)

Tresury shares 764 - 764 -

NET CASH FLOW FROM FINANCING ACTIVITIES (232,852) (299,360) (275,188) (322,175)

Exchange variations on cash and cash equivalents - - 8,053 470

INCREASE (DECREASE) IN CASH FOR THE PERIOD (115,402) (86,831) (247,848) (380,835)

OPENING BALANCE 402,698 361,923 1,074,364 1,416,360

FINAL BALANCE 287,296 275,092 826,516 1,035,525

Duratex S.A. - Listed company

National Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

STATEMENT OF CASH FLOWS

PARENT COMPANY CONSOLIDATED

PROFIT (LOSS) BEFORE INCOME TAX AND SOCIAL

CONTRIBUTION

12

(In thousands of Reais)

06/30/2018 06/30/2017 06/30/2018 06/30/2017

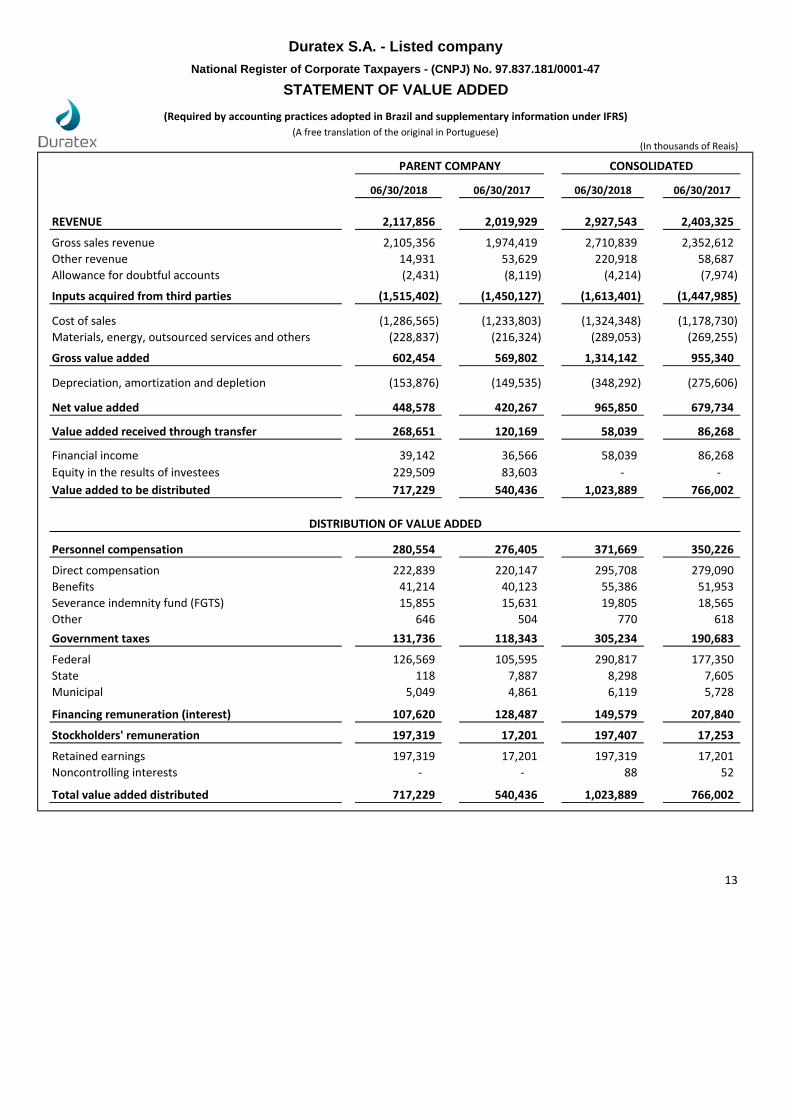

REVENUE 2,117,856 2,019,929 2,927,543 2,403,325

Gross sales revenue 2,105,356 1,974,419 2,710,839 2,352,612

Other revenue 14,931 53,629 220,918 58,687

Allowance for doubtful accounts (2,431) (8,119) (4,214) (7,974)

Inputs acquired from third parties (1,515,402) (1,450,127) (1,613,401) (1,447,985)

Cost of sales (1,286,565) (1,233,803) (1,324,348) (1,178,730)

Materials, energy, outsourced services and others (228,837) (216,324) (289,053) (269,255)

Gross value added 602,454 569,802 1,314,142 955,340

Depreciation, amortization and depletion (153,876) (149,535) (348,292) (275,606)

Net value added 448,578 420,267 965,850 679,734

Value added received through transfer 268,651 120,169 58,039 86,268

Financial income 39,142 36,566 58,039 86,268

Equity in the results of investees 229,509 83,603 - -

Value added to be distributed 717,229 540,436 1,023,889 766,002

Personnel compensation 280,554 276,405 371,669 350,226

Direct compensation 222,839 220,147 295,708 279,090

Benefits 41,214 40,123 55,386 51,953

Severance indemnity fund (FGTS) 15,855 15,631 19,805 18,565

Other 646 504 770 618

Government taxes 131,736 118,343 305,234 190,683

Federal 126,569 105,595 290,817 177,350

State 118 7,887 8,298 7,605

Municipal 5,049 4,861 6,119 5,728

Financing remuneration (interest) 107,620 128,487 149,579 207,840

Stockholders' remuneration 197,319 17,201 197,407 17,253

Retained earnings 197,319 17,201 197,319 17,201

Noncontrolling interests - - 88 52 - - - -

Total value added distributed 717,229 540,436 1,023,889 766,002

13

DISTRIBUTION OF VALUE ADDED

Duratex S.A. - Listed company

National Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

STATEMENT OF VALUE ADDED

(Required by accounting practices adopted in Brazil and supplementary information under IFRS)

PARENT COMPANY CONSOLIDATED

(A free translation of the original in Portuguese)

(In thousands of Reais) (A free translation of the original in Portuguese)

BALANCES AS AT DECEMBER 31, 2016 1,970,189 (7,823) 342,212 (18,731) 60,903 1,852,527 398,161 (27,931) - 4,569,507 1,145 4,570,652

COMPREHENSIVE INCOME FOR THE YEAR

Net Income for the year - - - - - - - - 184,875 184,875 140 185,015

Accumulated conversion adjustments - - - - - - 19,999 - - 19,999 206 20,205

Actuarial net gain (loss) - - - - - - (1,305) - - (1,305) - (1,305)

TOTAL COMPREHENSIVE INCOME FOR THE YEAR - - - - - - 18,694 - 184,875 203,569 346 203,915

Noncontrolling interest acquisition - - - - - - - - - - (246) (246)

Ceusa acquisition - non controlling interest - - - - - - - - - - (291) (291)

Share options granted - - 3,088 - - - - - - 3,088 - 3,088

Realization of revaluation reserve - - - - (3,559) - - - 3,559 - - -

Sale of treasury shares - - - - - - - 80 (39) 41 - 41

Interests on capital - - - - - - - - (60,840) (60,840) - (60,840)

APPROPRIATION OF NET INCOME FOR THE YEAR - - - - - - - - - - - -

Allocated to the legal reserve - - - - - 9,244 - - (9,244) - - -

Appropriation of tax incentives article 195-A Law 6.404/76 - - - - - 26,786 - - (26,786) - - -

Appropriation to reserves - - - - - 91,525 - - (91,525) - - -

BALANCES AS AT DECEMBER 31, 2017 1,970,189 (7,823) 345,300 (18,731) 57,344 1,980,082 416,855 (27,851) - 4,715,365 954 4,716,319

14

Total

Stockholders'

equity

Duratex S.A - Listed company

STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITYNational Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

Note CapitalCosts on issue

of sharesCapital reserves

Revaluation

reserves

Capital

transactions

with partners

Revenue

reserves

Carrying value

adjustments

Treasury

shares

Retained

earningsTotal

Noncontrolling

interests

(In thousands of Reais) (A free translation of the original in Portuguese)

BALANCES AS AT DECEMBER 31, 2017 1,970,189 (7,823) 345,300 (18,731) 57,344 1,980,082 416,855 (27,851) - 4,715,365 954 4,716,319

COMPREHENSIVE INCOME FOR THE PERIOD

Net Income for the period - - - - - - - - 197,319 197,319 88 197,407

Accumulated conversion adjustments - - - - - - 88,390 - - 88,390 332 88,722

Equity of investees reflex - - - - - - - - (162) (162) - (162)

Transition adjustments CPC 47 and 48 - - - - - - - - (4,833) (4,833) - (4,833)

Equity of investees reflex on CPC 47 and 48 - - - - - - - - (2,048) (2,048) - (2,048)

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD - - - - - - 88,390 - 190,276 278,666 420 279,086

Noncontrolling interest acquisition - - - - - - - - - - (69) (69)

Share options granted - - 1,264 - - - - - - 1,264 - 1,264

Sale of treasury shares - - - - - - - 764 (354) 410 - 410

Realization of revaluation reserve - - - - (2,259) - - - 2,259 - - -

APPROPRIATION OF NET INCOME FOR THE PERIOD

Allocated to the legal reserve - - - - - 9,866 - - (9,866) - - -

Appropriation to reserves - - - - - 182,315 - - (182,315) - - -

BALANCES AS AT JUNE 30, 2018 1,970,189 (7,823) 346,564 (18,731) 55,085 2,172,263 505,245 (27,087) - 4,995,705 1,305 4,997,010

15

Total

Stockholders'

equity

Duratex S.A - Listed company

STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITYNational Register of Corporate Taxpayers - (CNPJ) No. 97.837.181/0001-47

Note CapitalCosts on issue

of sharesCapital reserves

Revaluation

reserves

Capital

transactions

with partners

Revenue

reserves

Carrying value

adjustments

Treasury

shares

Retained

earningsTotal

Noncontrolling

interests

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

16

NOTES TO THE INTERIM FINANCIAL INFORMATION AS AT JUNE 30, 2018

(All amounts in thousands of Brazilian Reais, unless otherwise indicated)

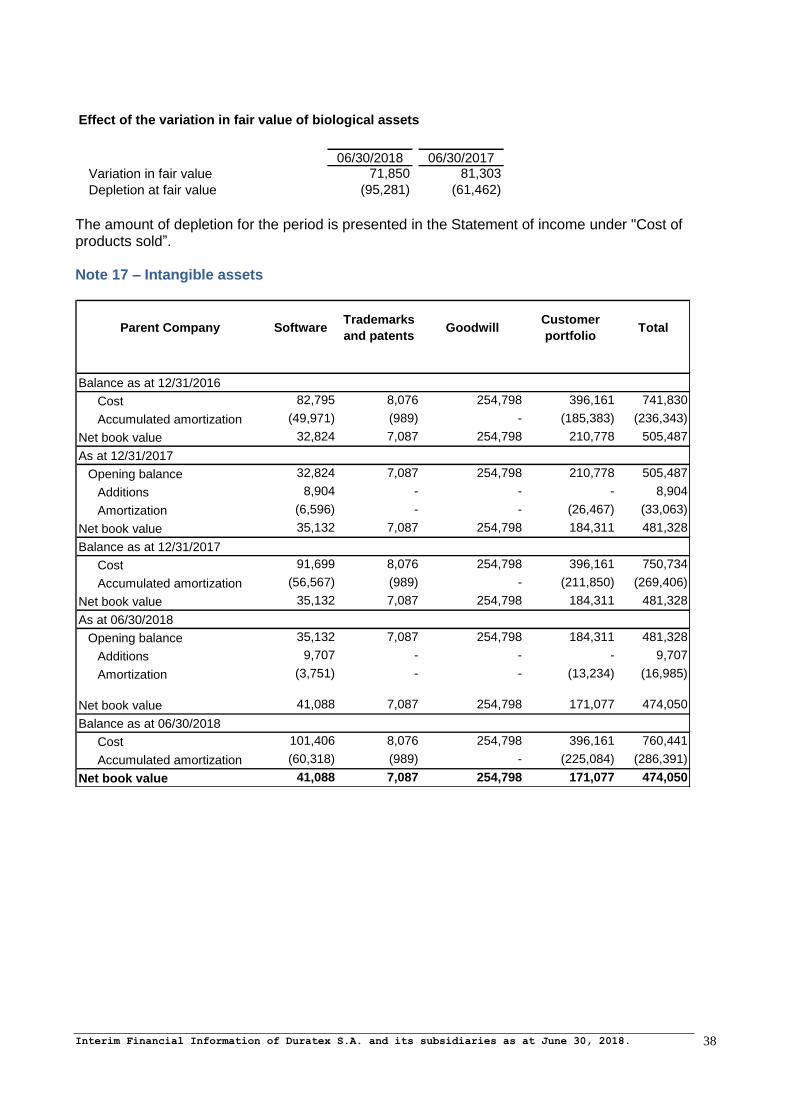

Note 1 – Operations a) General information Duratex S.A. (“the Company”) is a publicly-traded corporation headquartered in the city of São Paulo, SP, Brazil. Its controlling stockholders are Itaúsa - Investimentos Itaú S.A., which has significant operations in the financial and industrial sectors, and Companhia Ligna de Investimentos, which operates principally in the retail market and distribution of civil construction and woodworking materials, and in property construction and rental. The main activities of Duratex and its subsidiaries (collectively “Group”) comprise the manufacture of wood panels (Wood Division), and ceramics, sanitary metals and showers (Deca Division) and Ceramic Tiles Division. Duratex presently has seventeen industrial plants in Brazil and three industrial plants in Colombia, through of its subsidiary Duratex S.A. (current name of Tablemac S.A.), maintaining branches in the main Brazilian cities and commercial subsidiaries in the United States, Belgium and Peru. The Wood Division operates five industrial plants in the country and three in Colombia, responsible for the production of hardboard, medium density particle (MDP) panels, medium and high density fiberboard (MDF and HDF) panels, laminate flooring of Durafloor trademark and semi-finished components for furnitures. The Deca Division operates with ten industrial plants in the country, responsible for the production of sanitary ceramic, metal products, showers and ceramic tiles under the trademarks Deca, Hydra, Belize, Elizabeth and Hydra Corona. The Ceramic Tiles Division operates with two industrial plants in the country, responsible by production of ceramic tiles, with the brand Ceusa. b) Celebration’s agreement with Austrian group LENZING On June 21, 2018, the Company celebrated with LENZING AG, Austrian group world leader in the cellulosic fiber production, an agreement to establish a joint venture for production and commercialization of dissolving wood pulp (type viscose). Duratex will participate with 49% and Lenzing with 51% from the New Company. The results of the New Company will be recognized in the Duratex’s results by equity in the results of investees. Besides establishing the joint venture’s governance, the Agreement also assures the sale of the totality of dissolving wood pulp production to Lenzing, in the standard market condition will be strategically located in the state of Minas Gerais, within the Triângulo Mineiro region, close to São Paulo. The annual capacity of this project might be 450,000 tons of dissolving wood pulp and the initial estimated investment will be approximately USD 1.0 billion. The investment by Duratex in the New Company’s capital will be 43 thousand hectares of eucalyptus forests that it holds in the region, in addition to cash disbursements. The New Company will have its’ own capital structure, and it will fund part of the investment in order to optimize its cost of capital. The Agreement will not affect Duratex’s capacity to supply its wood panel business, nor does it affect the costs of its operations of own timber, at the same time it will optimize its forest assets which are currently idle, thus improving the returns of its recurring operations and will diversify the Company’s risk exposure as it broadens the Company’s range of activities to include the dissolving wood pulp market, which has lower exposure to Brazilian domestic activity. The final decision relating to the implementation of the project will occur in the 2nd semester 2019 and the beginning of the production is planned to 2022. There are no accounting impacts relating to this transaction on 2nd quarter 2018.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

17

c) Approval of Interim financial information The issuance of interim financial information of Duratex S.A. and its subsidiaries (Parent company and Consolidated) was approved by the Board of Directors on August 01, 2018. Note 2 – Basis of preparation and significant accounting practices The interim financial information has been prepared in accordance with technical pronouncement nº 21 R1 - Interim Reporting, issued by the Brazilian Accounting Pronouncements Committee (CPC) as well as in accordance with International Accounting Standard (IAS) nº 34 – “Interim Financial Reporting”, issued by the International Accounting Standards Board (IASB) and presented consistently with the standards issued by Brazilian Securities Commission (CVM), applicable to interim financial information. As described in Circular Letter CVM/SNC/SEP n° 03/2011, the Company has opted to present the explanatory notes in these interim financial information in a summarized manner when the information is the same as that presented in the annual financial statements. Thus this interim financial information should be read in conjunction with the annual financial statements ended December 31, 2017, which were disclosed on February 05, 2018. The non-financial data included in this interim financial information, such as planted area and number of units, and others, have not been subject of audit or revision by our independent auditors. 2.1 - Accounting policies 2.1.1. Main changes in the accounting policies

In exception to described below, the accounting policies applied in these interim financial information are the same as applied in the consolidated financial statements from the Group in the year ended on December 31, 2017. The Group adopted initially the CPC 47/ IFRS 15 – Revenues from contracts with customers (vide a) and the CPC 48/ IFRS 9 – Financial Instruments (vide b) from January 1, 2018. The effect of the initial application of these standards is attributed mainly: - Adequacy in the recognition of sales deduction by bonuses given to the customers by

attainment of purchases volumes of products;

- Increase in the losses by impairment recognized as financial assets.

Effect on transition

on January 1, 2018 47/IFRS 15 48/IFRS 9 Total

Asset

Accounts receivable from customers - (5,001) (5,001)

Non-current assets

Deferred income tax and social contribution 1,844 1,700 3,544

Current liability

Accounts payable / provisions 5,424 - 5,424

Stockholders' equity

Retained earnings (3,580) (3,301) (6,881)

New CPCs

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

18

a) CPC 47/ IFRS 15 Revenues from contracts with customers The CPC 47/ IFRS 15 establish a model of five steps for record of revenues from contracts of customers. The revenue is recognized by an amount that reflects the counterpart that the entity expects to have rights in return of transfer of goods or services for a customer. This standard replaces CPC 30/ IAS 18 – Revenues, the CPC 17/ IAS 11 Construction contracts and related interpretations. The Group adopted CPC 47/ IFRS 15 using cumulative method with effect of adoption of the standard recognized in the initial application date on January 1, 2018. Consequently, the information presented for 2017 was not resubmitted and, of this form, was presented in accordance to early reported in according with CPC 30/ IAS 18 and related interpretations. Sales of goods For contracts with clients in that generally expects that sale of products being the only obligation of execution, the adoption of CPC 47 didn’t impact the revenue and results from the Group, once the revenue is recognized in the moment that the control of the good is transferred for the customer in the delivery of the goods. After analysis of contracts with customers, we verified the necessity of adjustments in the recognition of deductions from sales by bonuses given to the customers by attainment of purchases volume of products. The following table resumes the impact, net of taxes, of CPC 47/ IFRS 15 transition on retained earnings on January, 1 2018.

Asset

Deferred income tax and

social contribution 1,844

Liability

Accounts payable 5,424

Stockholders' equity

Retained earnings (3,580) The following tables resume the impact from adoption of CPC 47/ IFRS 15 in the interim balance sheet consolidated on June 30, 2018, interim statement of income and statement of comprehensive income consolidated.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

19

Impact in the Interim Balance Sheet Consolidated

01/01/2018 06/30/2018

Asset Transition Posterior

Current asset 3,313,163 3,313,163

Deferred income tax and social contribution 319,737 (1,844) (109) 317,784

Other non current assets 5,854,991 - - 5,854,991

Non-current asset 6,174,728 (1,844) (109) 6,172,775

Total asset 9,487,891 (1,844) (109) 9,485,938

Liability

Accounts payable / provisions 155,051 (5,424) (322) 149,305

Other current liability 1,004,678 - - 1,004,678

Current liability 1,159,729 (5,424) (322) 1,153,983

Non-current liability 3,331,152 3,331,152

Stockholders' equity

Others accounts of stockholders' equity 4,807,652 - - 4,807,652

Retained earnings 189,358 3,580 213 193,151

Stockholders' equity 4,997,010 3,580 213 5,000,803

Total liability and stockholders'equity 9,487,891 (1,844) (109) 9,485,938

As Presented

Adjustments

No effect of CPC

47 / IFRS 15

Impact in the Interim Statement of Income and Statement of Comprehensive income Consolidated for the period of six months ended on June 30, 2018

As No effect of

Presented CPC 47 / IFRS 15

Net sales revenue 2,173,459 10,313 2,183,772

Variations in the fair value of biological assets 71,850 - 71,850

Cost of products sold (1,661,133) - (1,661,133)

Gross profit 584,176 10,313 594,489

Operacional expenses (206,058) - (206,058)

Operating profit before financial 378,118 10,313 388,431

Financial result (91,819) - (91,819)

Income before taxes 286,299 10,313 296,612

Income tax and social contribution (88,892) (3,506) (92,398)

Net income for period 197,407 6,807 204,214

Comprehensive income total 279,086 6,807 285,893

Adjustments

b) CPC 48/ IFRS 9 Financial Instruments The CPC 48/ IFRS 9 establish requirements for recognize and to measure financial assets and liabilities and some purchase contracts or sale of non-finance items. This standard replaces the CPC 38/ IAS 39 Financial Instruments: Recognition and measurement. The follow table resumes the impact, net of taxes, of transition for CPC 48/ IFRS 9 on retained earnings on January 1, 2018.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

20

Asset

Accounts receivable from customers (5,001)

Deferred income tax and social

contribution 1,700

Stockholders' equity

Retained earnings (3,301) Classification and measurement of Financial Assets and Liabilities The CPC 48/ IFRS 9 hold in largely part the requirements existents in the CPC 38/ IAS 39 for classification and measurement of financial liabilities. However, eliminates the olds categories of CPC 38/ IAS 39 for financial assets: held until the maturity, loans and receivables and available for sale. The adoption of CPC 48/ IFRS 9 do not have significant effect in the accounting policies from the Group related to financial liabilities and financial instruments derivatives. The impact of CPC 48/ IFRS 9 in the classification and measurement of financial assets are described below. Impairment The adoption effect of CPC 48/ IFRS 9 on book values of financial assets refers to trade accounts receivable of customers and other receivables that were classified in the category of loans and receivables in accordance to CPC 38/IFRS 39 and are currently classified to the amortized cost. An increase of R$ 5,001 in the provision for impairment of these receivables were recognized in the initial balance of retained earnings on January 1, 2018 in the transition for CPC 48/ IFRS 9. Accounting of Hedge Once CPC 48/ IFRS 9 not changed the general principles of how an entity record effectives hedges, the application of requirements do not have impact in the financial statements from the Group. The follow table and the notes below explain the original categories of measurement in the CPC 48/ IAS 39 and new categories of measurement of CPC 48/ IFRS9 for each class of financial assets from the Group on January 1, 2018.

New Original value New value

Classification Classification according with effect of

CPC 38/IAS 39 CPC 48/IFRS 9 CPC 38 / IAS 39 CPC 48 / IFRS 9

Financial assets

800,786 800,786

988,429 983,428

Accounts receivable

and other receivables

Loans and

receivables

Loans and

receivables

Amortized cost

Amortized cost

Cash and cash

equivalents

2.1.2 Going concern The Management evaluated the Company and its subsidiaries capacity to continue in normally operating and is convinced that has resources to give continually in its business in the future. Additionally, the Management doesn’t have knowledge of any material uncertainty that can generate significate doubts about its capacity to continue operating. So, these interim financial information were prepared based on the presupposed of continuity.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

21

2.2 - Consolidation of the interim financial information The interim financial information includes the companies: Duratex S.A. and its direct subsidiaries: Duratex Florestal Ltda., Hydra Corona Sistemas de Aquecimento de Água Ltda., Cerâmica Urussanga S.A. (Ceusa), Estrela do Sul Participações Ltda., Duratex Empreendimentos Ltda., Bale Comércio de Produtos para Construção S.A., Pescara Administração e Participações S.A., Trento Administração e Participações S.A., Duratex Europe N.V., Duratex Andina S.A.C. and its indirect subsidiaries: Duratex North America Inc., Duratex Belgium N.V., Duratex S.A. (current name of Tablemac S.A.), Tablemac MDF S.A.S and Forestal Rio Grande S.A.S.. 2.2.1 – Transactions with and participation in non-controlling entities For acquisitions of non-controlling ownership interests, the difference between any consideration paid and the acquired portion of the controlling stockholder's net assets are recorded in stockholders’ equity (on capital transactions with partners), as along with the gains or losses on sales to non-controlling stockholders. 2.3 – New accounting standards, amendments and interpretations IFRS 16 - Leases, which replaces IAS 17, unifying the accounting treatment of operating and finance leases for the similar model to financial leasing with impact on fixed asset and financial liability. This standard will effective on January 1st, 2019 and the Group is evaluating the content and the possible impacts of the adoption of this pronouncement. As at disclosure date of this interim financial information, these works do not have concluded, impossible the disclosure of any possible effect that can come from application of these new normative. There are no other standards and interpretations issued and not yet adopted that, in Management's opinion, can have a significant impact on the results or stockholders’ equity disclosed by the Group. 2.4 – Presentation of segmented information Segmented information is presented consistently with the main operating decision maker. The main operating decision maker, responsible for allocating funds and evaluating the performance of operating segments, is the Company's Board of Directors, which is in charge of the Group's strategic decision making, with the support of the Supervisory Board. Note 3 – Critical accounting judgments and estimates During the preparation of the interim financial information, accounting judgments, estimates and assumptions are utilized to record the amounts of certain assets, liabilities and other transactions. The definition of estimates and accounting judgments adopted by Management were based on the information available on the date, based on experience of past events and forecasts of future events. The interim financial information includes several estimates, such as: useful lives of property plant and equipment items, the realization of deferred tax credits, the allowance for doubtful accounts, inventory losses, the evaluation of the fair value of biological assets, and provision for contingencies and impairment testing of goodwill, pension plan and health benefits, and others. The following are the main estimates and assumptions that entail a substantial risk with probability to causes adjustments in the book values of assets and liabilities:

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

22

a) Risk of variations in the fair value of biological assets The Group used several estimates to evaluate its forestry reserves in accordance with the methodology established by CPC 29/IAS 41 – “Biological asset and agriculture product”. These estimates were based on market references, and are subject to changes which could impact the interim financial statements. Specifically, a 5% reduction in standing wood prices would result in a reduction in the fair value of biological assets in order to R$ 55.9 million, net of tax effects. If the discount rate used were increased by 0.5%, this would result in a reduction in the fair value of biological assets of about R$ 10.0 million, net of tax effects. b) Estimated impairment of goodwill The Company and its subsidiaries test the goodwill on annual basis or if there is an indication any time that the goodwill may be impaired. The balance could be impacted by changes in the economic or market scenario. c) Pension plan and health benefits The current value of assets/ liabilities related to pension plans and health depends on a number of factors that are determined using actuarial calculations. These calculations involve a series of assumptions, including the discount rate and current market conditions. Any changes in these assumptions will affect the corresponding book values. d) Provision for contingencies The Group constitute provision for tax, labor, civil and social security contingencies, based on valuation of probability of loss that are made by legal advisors from the Company, the amounts are updated and believe that the constituted provisions as at closing date are sufficient for cover eventual losses with lawsuits and administrative in progress. e) Fair value of financial instruments When the fair value from financial assets and liabilities presented in the balance sheet cannot be obtained of market assets, are determined utilizing valuation techniques, including cash flow discounted method. The data for these methods is based in those practiced in the market, when it possible, however, when this does not viable, a determined level of judgement is required for establishes the fair value. The judgment includes considerations on used data, for example, risk of liquidity, risk of credit and volatility. Changes in the assumptions on these factors could affect the fair value presented of the financial instruments. Note 4 – Financial risk management 4.1 Financial risk factors The Group are exposed to market risk in relation to fluctuations of interest, exchange rates and credit. So, the risk manage follows the policies approved by Board of Directors, including monitoring by Audit and Management of Risk Committee. The Company and its subsidiaries have procedures to manage these situations and can use hedging instruments to reduce the impact of the risks. These procedures include monitoring the level of exposure to each market risk, in addition to establish limits for the respective decision-making. All hedging transactions entered into by the Group are intended to protect its debts and investments. The Group does not utilize any leveraged financial derivatives.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

23

Market risk (I) Exchange rate risk: Exchange rate risk corresponds to a reduction in the value of the Group's assets or an increase in its liabilities due to changes in exchange rates. The Company and its subsidiaries have indebtedness policy that establishes the maximum amount in foreign currency to which it is exposed to exchange rate variations. In line with the risk management procedures, the objective is to minimize the foreign exchange exposure of the Company and its subsidiaries, hedging mechanisms are maintained, in order to mitigate, in large part, the foreign exchange exposure. (II) Derivatives: In terms of derivative instruments, there are no verifications, monthly settlements or margin calls are made, and the contracts are settled upon maturity and recorded at fair value, considering the market conditions for terms and interest rates. The outstanding contracts as at June 30, 2018 were as follow: a) US$ vs. Interbank deposit certificate (CDI) swap agreements The Company has two agreements of this nature, whose aggregate notional amount is US$ 100,000,000, and varying maturities up to August 16, 2019, with an asset (purchase) position in US Dollars and a liability (sale) position in CDI. The Company made these agreements in order to change its debts denominated in US Dollars into debts indexed to the CDI. b) Fixed rate vs. Interbank deposit certificate (CDI) swap agreements The Company has two agreements with aggregate amount of R$ 385,000, being the last maturity date on June 17, 2020 with asset position at fixed rate and liability position at a percentage variation from CDI. The Company contracted these operations with the purpose of change the debts with fixed interests rates in debts indexed to CDI. c) Non Deliverable Forward (NDF) agreement

The Company has one agreement of this nature, whose contracted amount totalizes US$ 34,700,000 maturing through July 31, 2018 and position sold in US Dollars.

The Company contracted this agreement in order to reset the foreign exchange exposure on the contracted date (June 28, 2018). In this transaction the contracted is settled at their respective maturity, considering the difference between the exchange rate to term (NDF) and exchange rate in the end of the period (Ptax). d) Calculation of the fair value of positions The fair value of the financial instruments was calculated utilizing the estimated present value of both liability and asset positions, where the difference between the two represents the market value of the Swap.

Interim Financial Information of Duratex S.A. and its subsidiaries as at June 30, 2018.

24

Amount Amount

06/30/2018 12/31/2017 06/30/2018 12/31/2017 receivable/ payable/

received paid

I. Swap contracts

Asset position

Foreign currency (USD) 354,985 584,333 391,263 607,911 30,434 -

Fixed rate 385,000 20,000 379,115 20,236 - (8,969)

Liability position

CDI (739,985) (604,333) (748,913) (611,764) - -