Embed Size (px)

Citation preview

Driving Sales and Margin in a New Era of Chain Retailing A Preview of KSA’s Retail Leadership Report on Localization

BY CHRISTINA BIENIEK

In This Report Preview

The preliminary results of KSA’s study of nearly 300 retail leaders at more than 100 companies reveal:

> The standardized store approach

that has fueled the phenomenal

growth of many U.S. retail chains

today prevents them from

respond ing to profound local

differences in consumer tastes.

> Rapid advancements in information

technology and supply chains now

enable retailers to substantially

tailor their offerings and customer

experiences to boost sales, margins

and customer loyalty—while still

maintaining economies of scale.

> To win at localization, retailers must

master five key success factors.

In January 2010, KSA will pub lish the complete results of our in-depth industry research on localization.

About the Study

In 2009, KSA conducted extensive quantitative and qualitative primary research on the localization strategies of large U.S. retailers. The quantitative research comprised two online surveys. The first was a 22-question survey taken by 143 executives at retailers in six sectors (department; discount, mass, warehouse club; big box; drug; grocery and specialty stores), 93% of which had annual revenues of at least $1 billion. The second was a survey of 145 store and district managers at retailers in the same six sectors. The qualitative research was based on eight in-depth case studies based on on-site interviews with major retailers from the grocery, drug, big box and specialty sectors. We also conducted voluminous secondary research to gather what retailers have disclosed publicly about their localization initiatives. We analyzed that data, tapping into our consulting expertise from helping several major retailers localize their stores in recent years.

The study was designed to shed light on four core issues:

> Why are retailers localizing?

> What are they localizing, and

how are they doing it?

> What success have they had

with localization?

> What are the key factors to

maximizing the benefits of

localization?

Driving Sales and Margin in a New Era of Chain Retailing

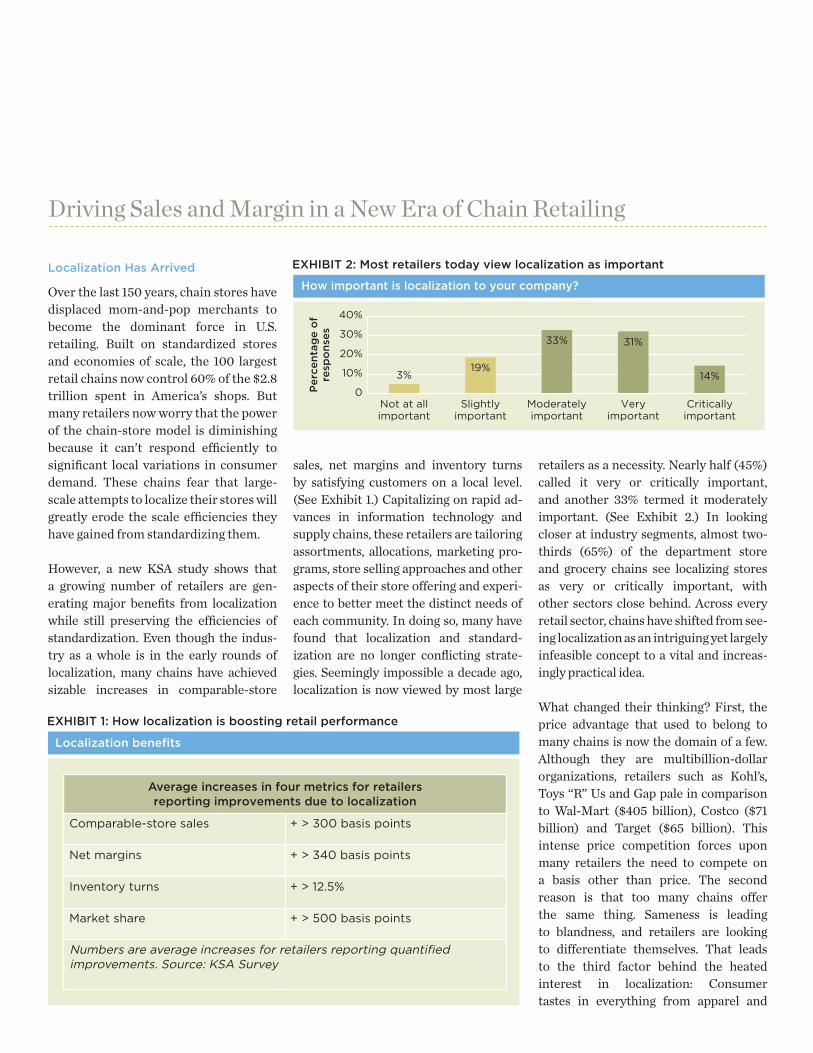

Localization Has Arrived

Over the last 150 years, chain stores have displaced mom-and-pop merchants to become the dominant force in U.S. retailing. Built on standardized stores and economies of scale, the 100 largest retail chains now control 60% of the $2.8 trillion spent in America’s shops. But many retailers now worry that the power of the chain-store model is diminishing because it can’t respond efficiently to significant local variations in consumer demand. These chains fear that large-scale attempts to localize their stores will greatly erode the scale efficiencies they have gained from standardizing them.

However, a new KSA study shows that a growing number of retailers are gen-erating major benefits from localization while still preserving the efficiencies of standardization. Even though the indus-try as a whole is in the early rounds of localization, many chains have achieved sizable increases in comparable-store

sales, net margins and inventory turns by satisfying customers on a local level. (See Exhibit 1.) Capitalizing on rapid ad-vances in information technology and supply chains, these retailers are tailoring assortments, allocations, marketing pro-grams, store selling approaches and other aspects of their store offering and experi-ence to better meet the distinct needs of each community. In doing so, many have found that localization and standard-ization are no longer conflicting strate-gies. Seemingly impossible a decade ago, localization is now viewed by most large

retailers as a necessity. Nearly half (45%) called it very or critically important, and another 33% termed it moderately important. (See Exhibit 2.) In looking closer at industry segments, almost two-thirds (65%) of the department store and grocery chains see localizing stores as very or critically important, with other sectors close behind. Across every retail sector, chains have shifted from see-ing localization as an intriguing yet largely infeasible concept to a vital and increas-ingly practical idea.

What changed their thinking? First, the price advantage that used to belong to many chains is now the domain of a few. Although they are multibillion-dollar organizations, retailers such as Kohl’s, Toys “R” Us and Gap pale in comparison to Wal-Mart ($405 billion), Costco ($71 billion) and Target ($65 billion). This intense price competition forces upon many retailers the need to compete on a basis other than price. The second reason is that too many chains offer the same thing. Sameness is leading to blandness, and retailers are looking to differentiate themselves. That leads to the third factor behind the heated interest in localization: Consumer tastes in everything from apparel and

Average increases in four metrics for retailersreporting improvements due to localization

Comparable-store sales

Net margins

Inventory turns

Market share

Numbers are average increases for retailers reporting quantified improvements. Source: KSA Survey

+ > 300 basis points

+ > 340 basis points

+ > 12.5%

+ > 500 basis points

Localization benefits

EXHIBIT 1: How localization is boosting retail performance

Pe

rce

nta

ge

of

resp

on

ses

0

10%

20%

30%

40%

Not at allimportant

3%

Slightlyimportant

19%

Moderatelyimportant

33%

Veryimportant

31%

Criticallyimportant

14%

How important is localization to your company?

EXHIBIT 2: Most retailers today view localization as important

appliances to toothpaste and sport-ing goods can vary significantly—from region to region and even neighborhood to neighborhood. The shift in consumer attitudes demands that these differences be met with more tailored offerings and services. The cookie-cutter store model glosses over those differences. Retailers no longer can ignore this, given that consumers can shop the entire world from their homes for products that fit their pre-cise needs. And more and more, they want their local stores to answer their distinct needs because they still spend 92% of their shopping dollars in stores.

All this explains why retailers have taken a significant interest in localization. Yet it all would be wishful thinking without this decade’s rapid advances in infor-mation technology and supply chains. For the first time, retailers can buy off-the-shelf software for processing and analyzing enormous volumes of transac-tional data and for localizing assortments, allocations and markdowns. Flexible supply chains are the other game- changer. A distribution network built on shipping the same assortments, in- store displays and marketing materi-als to every store can’t handle much variation by region or store. But over the last 10 years, many retailers have made their distribution and trans-portation networks far more sophist- icated. For example, some supply chains can flow goods based on real-time, store-level demand. Others can split import purchases at the port of entry so that products fashionable in some locales aren’t shipped at the same time to others that lag in fashion trends. In the face of such forces, a number of

large retailers have begun to turn their operations upside down to cater to sig-nificant local differences in consumer tastes. However, localization requires a much deeper understanding of local markets than the typical retailer possesses. Those who gain such insights and act efficiently on them can significantly boost sales, margins and customer loyalty.

Our research tells us that the ability to localize the right things the right way—without destroying the efficiencies of standardization—is becoming integral to retail success. We believe that over the next decade, it will greatly determine which retailers gain or lose market share.

The Early Stages of Localization

The impact of localization is just beginning. The reason: Most retailers haven’t actually localized most of what they could localize. While 83% of U.S. retailers have localized some aspect of the store offering and customer

experience, most are not far down the path. On all 11 “levers” of localization (e.g., assortments, inventory planning and markdowns), less than a third had completed their localization initiative. (See Exhibit 3.)

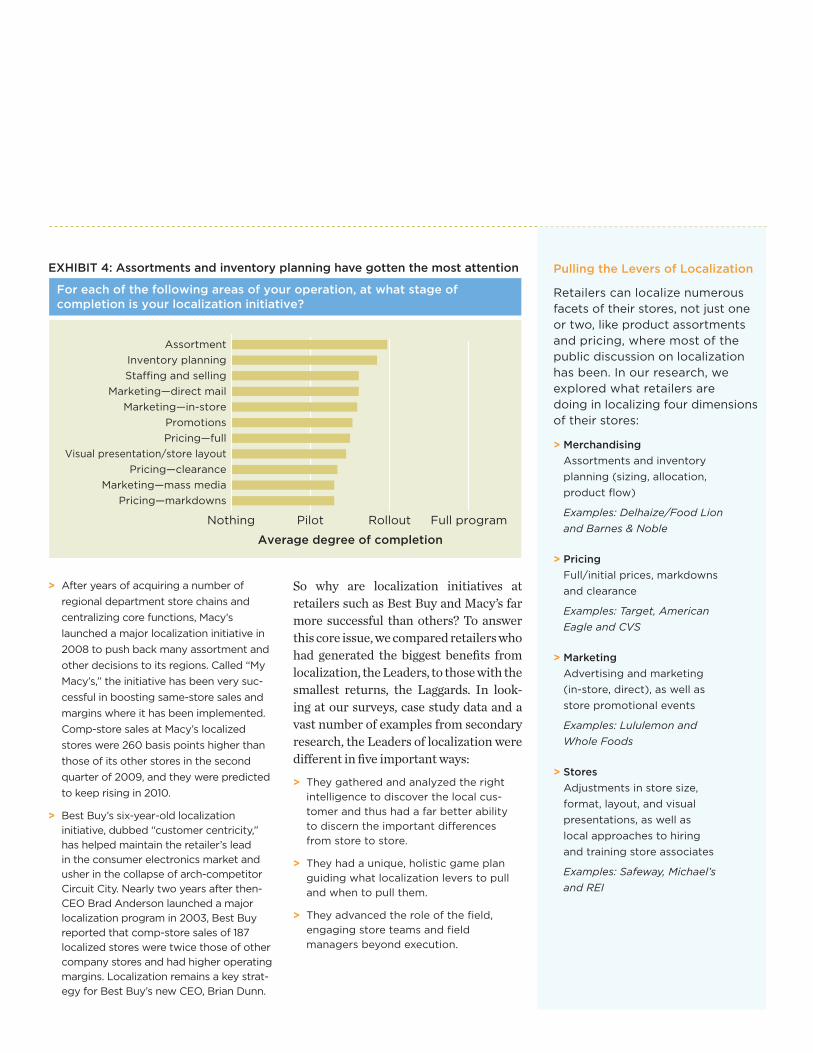

On five of those levers, the majority had done nothing or were just piloting ini-tiatives: visual presentation/store lay-outs, mass-media marketing programs, clearance pricing, markdowns and full pricing. Many retailers see localization as being solely about tailoring category mixes. Indeed, the survey group was farther ahead in localizing assortments and inventory plans than in other aspects of the offering and experience. (See Exhibit 4 and “Pulling the Levers of Localization.”)

But other retailers have taken a broader approach to localization, pulling most or all of the levers. For these merchants, localization has become a core strategy:

Even though the industry as a whole is in the early rounds of localization, many chains have achieved sizable increases in comparable-store sales, net margins and inventory turns through localization.

Visual presentation/store layout

Staffing and selling

Marketing—in-store

Marketing—mass media

Pricing—markdowns

Marketing—direct mail

Promotions

Pricing—full

Pricing—clearance

Assortment

Inventory planning

20%

25%

25%

19%

21%

26%

19%

21%

18%

29%

28%

0% 20% 60% 80%40% 100%

Percentage of retailers with full localization programs in place (by lever)

EXHIBIT 3: Most retailers have not fully localized their stores

So why are localization initiatives at retailers such as Best Buy and Macy’s far more successful than others? To answer this core issue, we compared retailers who had generated the biggest benefits from localization, the Leaders, to those with the smallest returns, the Laggards. In look-ing at our surveys, case study data and a vast number of examples from secondary research, the Leaders of localization were different in five important ways:

> They gathered and analyzed the right

intelligence to discover the local cus-

tomer and thus had a far better ability

to discern the important differences

from store to store.

> They had a unique, holistic game plan

guiding what localization levers to pull

and when to pull them.

> They advanced the role of the field,

engaging store teams and field

managers beyond execution.

Pulling the Levers of Localization

Retailers can localize numerous facets of their stores, not just one or two, like product assortments and pricing, where most of the public discussion on localization has been. In our research, we explored what retailers are doing in localizing four dimensions of their stores:

> Merchandising

Assortments and inventory

planning (sizing, allocation,

product flow)

Examples: Delhaize/Food Lion

and Barnes & Noble

> Pricing

Full/initial prices, markdowns

and clearance

Examples: Target, American

Eagle and CVS

> Marketing

Advertising and marketing

(in-store, direct), as well as

store promotional events

Examples: Lululemon and

Whole Foods

> Stores

Adjustments in store size,

format, layout, and visual

presentations, as well as

local approaches to hiring

and training store associates

Examples: Safeway, Michael’s

and REI

Average degree of completion

Visual presentation/store layout

Marketing—direct mail

Marketing—in-store

Pricing—clearance

Promotions

Staffing and selling

Marketing—mass media

Pricing—full

Pricing—markdowns

Assortment

Inventory planning

Nothing Pilot Rollout Full program

For each of the following areas of your operation, at what stage ofcompletion is your localization initiative?

EXHIBIT 4: Assortments and inventory planning have gotten the most attention

> After years of acquiring a number of

regional department store chains and

centralizing core functions, Macy’s

launched a major localization initiative in

2008 to push back many assortment and

other decisions to its regions. Called “My

Macy’s,” the initiative has been very suc-

cessful in boosting same-store sales and

margins where it has been implemented.

Comp-store sales at Macy’s localized

stores were 260 basis points higher than

those of its other stores in the second

quarter of 2009, and they were predicted

to keep rising in 2010.

> Best Buy’s six-year-old localization

initiative, dubbed “customer centricity,”

has helped maintain the retailer’s lead

in the consumer electronics market and

usher in the collapse of arch-competitor

Circuit City. Nearly two years after then-

CEO Brad Anderson launched a major

localization program in 2003, Best Buy

reported that comp-store sales of 187

localized stores were twice those of other

company stores and had higher operating

margins. Localization remains a key strat-

egy for Best Buy’s new CEO, Brian Dunn.

In the rest of this article, we examine each of these key success factors.

Discovering the Local Customer

Determining what to localize and how to do it begins with an intimate under-standing of customers. A retailer needs to know more than who its customers are, what they buy and when. It must also understand customer behaviors and attitudes to determine why they shop and why they do or don’t buy.

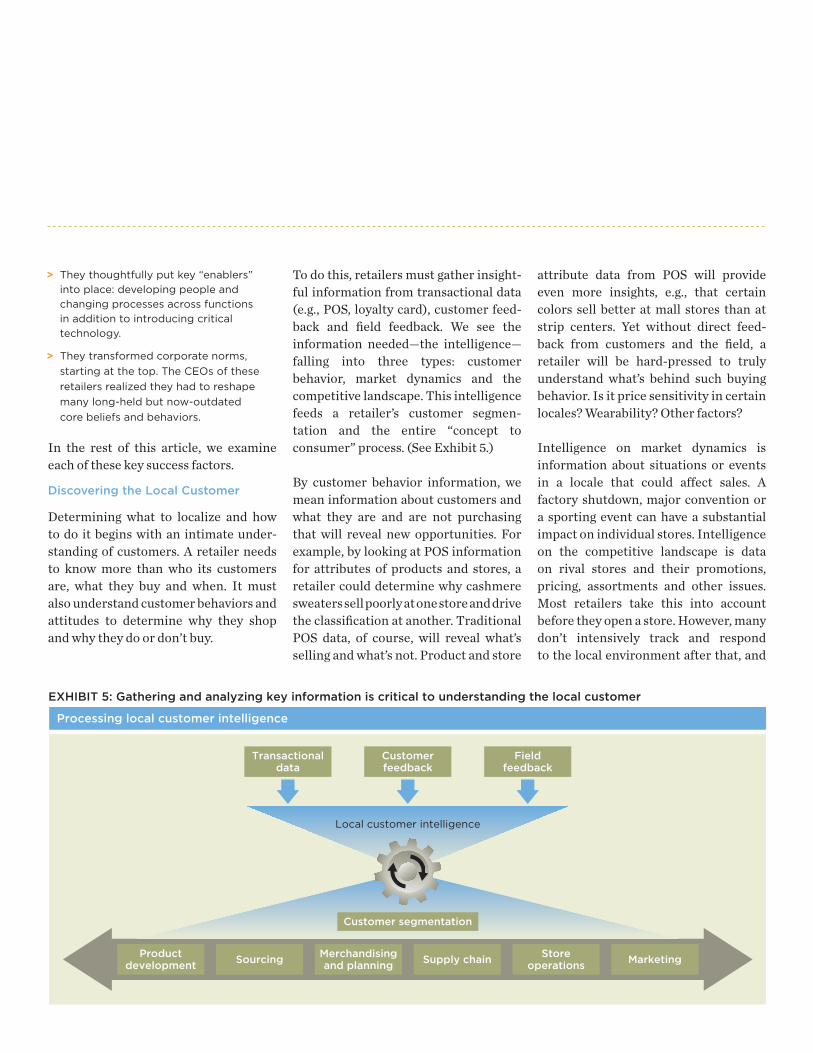

To do this, retailers must gather insight-ful information from transactional data (e.g., POS, loyalty card), customer feed-back and field feedback. We see the information needed—the intelligence—falling into three types: customer behavior, market dynamics and the competitive landscape. This intelligence feeds a retailer’s customer segmen- tation and the entire “concept to consumer” process. (See Exhibit 5.)

By customer behavior information, we mean information about customers and what they are and are not purchasing that will reveal new opportunities. For example, by looking at POS information for attributes of products and stores, a retailer could determine why cashmere sweaters sell poorly at one store and drive the classification at another. Traditional POS data, of course, will reveal what’s selling and what’s not. Product and store

attribute data from POS will provide even more insights, e.g., that certain colors sell better at mall stores than at strip centers. Yet without direct feed-back from customers and the field, a retailer will be hard-pressed to truly understand what’s behind such buying behavior. Is it price sensitivity in certain locales? Wearability? Other factors?

Intelligence on market dynamics is information about situations or events in a locale that could affect sales. A factory shutdown, major convention or a sporting event can have a substantial impact on individual stores. Intelligence on the competitive landscape is data on rival stores and their promotions, pricing, assortments and other issues. Most retailers take this into account before they open a store. However, many don’t intensively track and respond to the local environment after that, and

Processing local customer intelligence

EXHIBIT 5: Gathering and analyzing key information is critical to understanding the local customer

Transactionaldata

Productdevelopment

SourcingMerchandisingand planning

Storeoperations

Supply chain Marketing

Customerfeedback

Local customer intelligence

Fieldfeedback

Customer segmentation

> They thoughtfully put key “enablers”

into place: developing people and

changing processes across functions

in addition to introducing critical

technology.

> They transformed corporate norms,

starting at the top. The CEOs of these

retailers realized they had to reshape

many long-held but now-outdated

core beliefs and behaviors.

not doing so can have a major impact on a store’s results.

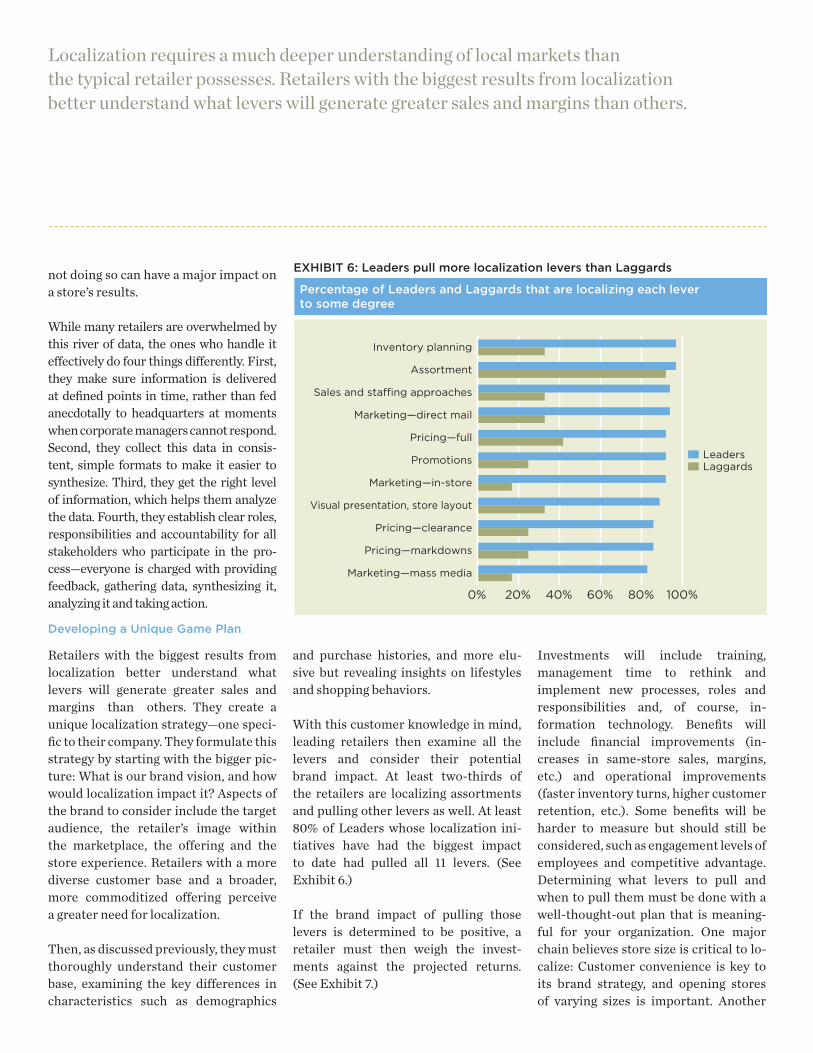

While many retailers are overwhelmed by this river of data, the ones who handle it effectively do four things differently. First, they make sure information is delivered at defined points in time, rather than fed anecdotally to headquarters at moments when corporate managers cannot respond. Second, they collect this data in consis-tent, simple formats to make it easier to synthesize. Third, they get the right level of information, which helps them analyze the data. Fourth, they establish clear roles, responsibilities and accountability for all stakeholders who participate in the pro-cess—everyone is charged with providing feedback, gathering data, synthesizing it, analyzing it and taking action.

Developing a Unique Game Plan

Retailers with the biggest results from localization better understand what levers will generate greater sales and margins than others. They create a unique localization strategy—one speci- fic to their company. They formulate this strategy by starting with the bigger pic-ture: What is our brand vision, and how would localization impact it? Aspects of the brand to consider include the target audience, the retailer’s image within the marketplace, the offering and the store experience. Retailers with a more diverse customer base and a broader, more commoditized offering perceive a greater need for localization.

Then, as discussed previously, they must thoroughly understand their customer base, examining the key differences in characteristics such as demographics

and purchase histories, and more elu-sive but revealing insights on lifestyles and shopping behaviors.

With this customer knowledge in mind, leading retailers then examine all the levers and consider their potential brand impact. At least two-thirds of the retailers are localizing assortments and pulling other levers as well. At least 80% of Leaders whose localization ini-tiatives have had the biggest impact to date had pulled all 11 levers. (See Exhibit 6.)

If the brand impact of pulling those levers is determined to be positive, a retailer must then weigh the invest-ments against the projected returns. (See Exhibit 7.)

Investments will include training, management time to rethink and implement new processes, roles and responsibilities and, of course, in-formation technology. Benefits will include financial improvements (in-creases in same-store sales, margins, etc.) and operational improvements (faster inventory turns, higher customer retention, etc.). Some benefits will be harder to measure but should still be considered, such as engagement levels of employees and competitive advantage. Determining what levers to pull and when to pull them must be done with a well-thought-out plan that is meaning-ful for your organization. One major chain believes store size is critical to lo-calize: Customer convenience is key to its brand strategy, and opening stores of varying sizes is important. Another

Localization requires a much deeper understanding of local markets than the typical retailer possesses. Retailers with the biggest results from localization better understand what levers will generate greater sales and margins than others.

Percentage of Leaders and Laggards that are localizing each leverto some degree

EXHIBIT 6: Leaders pull more localization levers than Laggards

Visual presentation, store layout

Marketing—direct mail

Pricing—full

Pricing—clearance

Promotions

Sales and staffing approaches

Pricing—markdowns

Marketing—in-store

Marketing—mass media

Inventory planning

LeadersLaggards

Assortment

0% 20% 60% 80%40% 100%

retailer believes that localizing visual displays at the front of the store is cru-cial to enticing local shoppers. A large chain sees localized pricing as neces-sary to battle against discounters such as Wal-Mart. A major grocer believes tai-lored marketing is a critical differentia-tor in generating traffic.

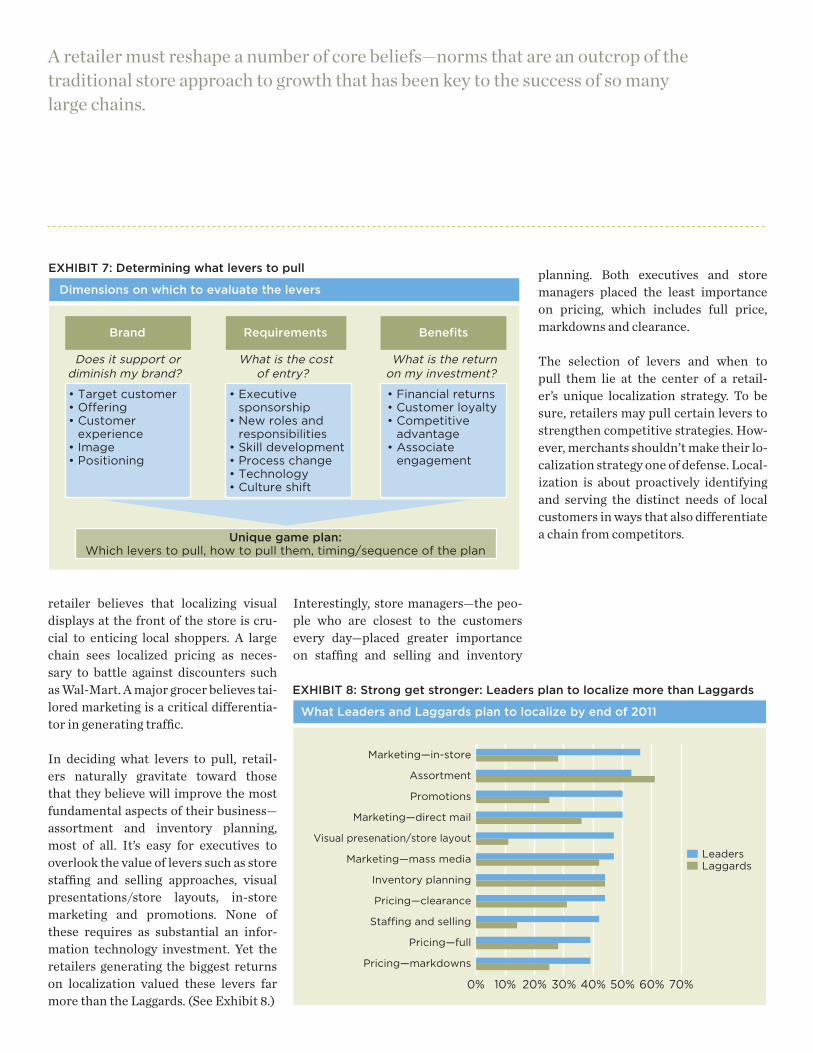

In deciding what levers to pull, retail-ers naturally gravitate toward those that they believe will improve the most fundamental aspects of their business— assortment and inventory planning, most of all. It’s easy for executives to overlook the value of levers such as store staffing and selling approaches, visual presentations/store layouts, in-store marketing and promotions. None of these requires as substantial an infor-mation technology investment. Yet the retailers generating the biggest returns on localization valued these levers far more than the Laggards. (See Exhibit 8.)

Interestingly, store managers—the peo-ple who are closest to the customers every day—placed greater importance on staffing and selling and inventory

planning. Both executives and store managers placed the least importance on pricing, which includes full price, markdowns and clearance.

The selection of levers and when to pull them lie at the center of a retail-er’s unique localization strategy. To be sure, retailers may pull certain levers to strengthen competitive strategies. How-ever, merchants shouldn’t make their lo-calization strategy one of defense. Local-ization is about proactively identifying and serving the distinct needs of local customers in ways that also differentiate a chain from competitors.

A retailer must reshape a number of core beliefs—norms that are an outcrop of the traditional store approach to growth that has been key to the success of so many large chains.

Dimensions on which to evaluate the levers

EXHIBIT 7: Determining what levers to pull

Brand

Does it support ordiminish my brand?

• Target customer• Offering• Customer

experience• Image• Positioning

Requirements

Unique game plan:Which levers to pull, how to pull them, timing/sequence of the plan

What is the costof entry?

• Executive sponsorship

• New roles and responsibilities

• Skill development • Process change• Technology • Culture shift

Benefits

What is the returnon my investment?

• Financial returns• Customer loyalty• Competitive

advantage• Associate

engagement

What Leaders and Laggards plan to localize by end of 2011

EXHIBIT 8: Strong get stronger: Leaders plan to localize more than Laggards

Pricing—clearance

Marketing—direct mail

Visual presenation/store layout

Staffing and selling

Marketing—mass media

Promotions

Pricing—full

Inventory planning

Pricing—markdowns

Marketing—in-store

Assortment

0% 30%20%10% 50% 60%40% 70%

LeadersLaggards

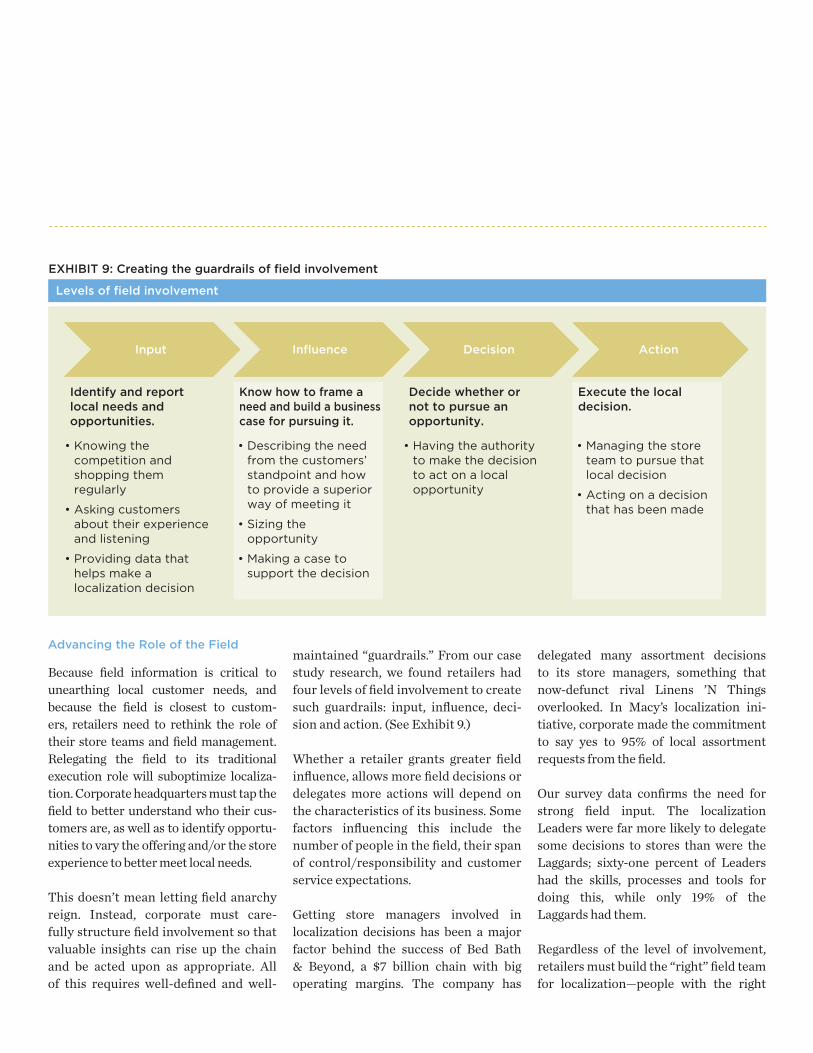

Advancing the Role of the Field

Because field information is critical to unearthing local customer needs, and because the field is closest to custom-ers, retailers need to rethink the role of their store teams and field management. Relegating the field to its traditional execution role will suboptimize localiza-tion. Corporate headquarters must tap the field to better understand who their cus-tomers are, as well as to identify opportu-nities to vary the offering and/or the store experience to better meet local needs.

This doesn’t mean letting field anarchy reign. Instead, corporate must care-fully structure field involvement so that valuable insights can rise up the chain and be acted upon as appropriate. All of this requires well-defined and well-

maintained “guardrails.” From our case study research, we found retailers had four levels of field involvement to create such guardrails: input, influence, deci-sion and action. (See Exhibit 9.)

Whether a retailer grants greater field influence, allows more field decisions or delegates more actions will depend on the characteristics of its business. Some factors influencing this include the number of people in the field, their span of control/responsibility and customer service expectations.

Getting store managers involved in localization decisions has been a major factor behind the success of Bed Bath & Beyond, a $7 billion chain with big operating margins. The company has

delegated many assortment decisions to its store managers, something that now-defunct rival Linens ’N Things overlooked. In Macy’s localization ini-tiative, corporate made the commitment to say yes to 95% of local assortment requests from the field.

Our survey data confirms the need for strong field input. The localization Leaders were far more likely to delegate some decisions to stores than were the Laggards; sixty-one percent of Leaders had the skills, processes and tools for doing this, while only 19% of the Laggards had them.

Regardless of the level of involvement, retailers must build the “right” field team for localization—people with the right

Levels of field involvement

EXHIBIT 9: Creating the guardrails of field involvement

Input Influence Decision Action

• Knowing the competition and shopping them regularly

• Asking customers about their experience and listening

• Providing data that helps make a localization decision

Identify and report local needs and opportunities.

• Describing the need from the customers’ standpoint and how to provide a superior way of meeting it

• Sizing the opportunity

• Making a case to support the decision

Know how to frame a need and build a business case for pursuing it.

• Having the authority to make the decision to act on a local opportunity

Decide whether or not to pursue an opportunity.

• Managing the store team to pursue that local decision

• Acting on a decision that has been made

Execute the local decision.

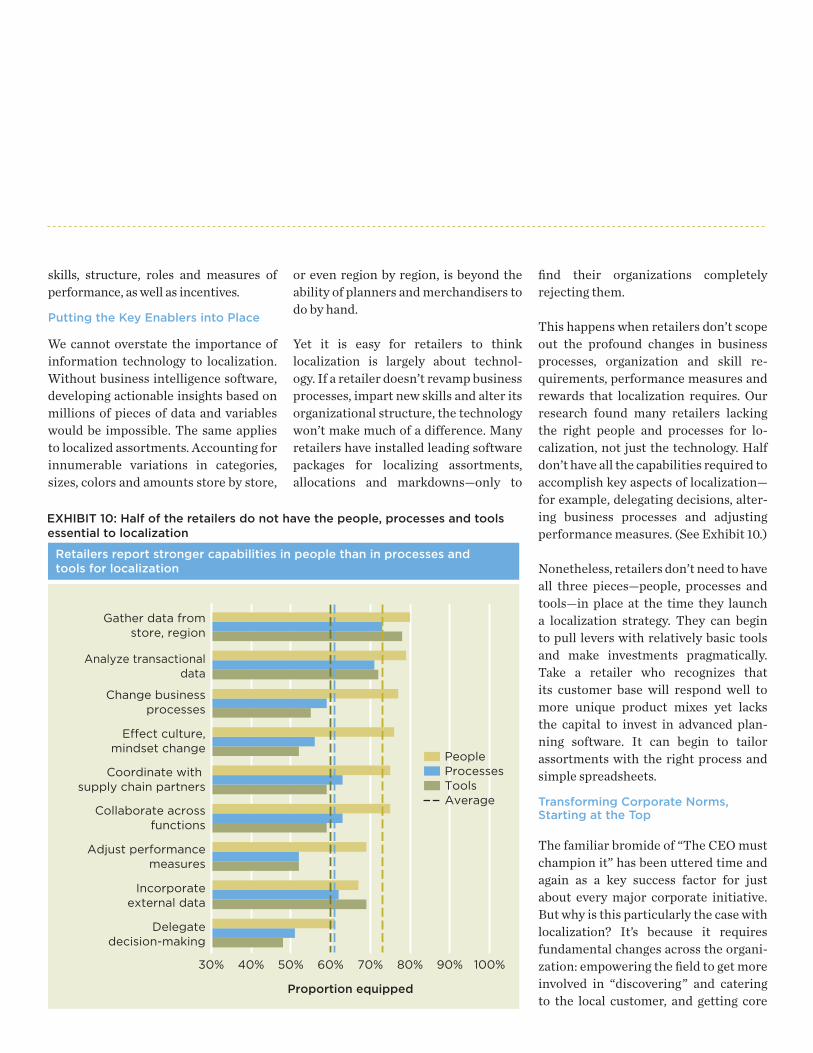

skills, structure, roles and measures of performance, as well as incentives.

Putting the Key Enablers into Place

We cannot overstate the importance of information technology to localization. Without business intelligence software, developing actionable insights based on millions of pieces of data and variables would be impossible. The same applies to localized assortments. Accounting for innumerable variations in categories, sizes, colors and amounts store by store,

or even region by region, is beyond the ability of planners and merchandisers to do by hand.

Yet it is easy for retailers to think localization is largely about technol-ogy. If a retailer doesn’t revamp business processes, impart new skills and alter its organizational structure, the technology won’t make much of a difference. Many retailers have installed leading software packages for localizing assortments, allocations and markdowns—only to

find their organizations completely rejecting them.

This happens when retailers don’t scope out the profound changes in business processes, organization and skill re-quirements, performance measures and rewards that localization requires. Our research found many retailers lacking the right people and processes for lo-calization, not just the technology. Half don’t have all the capabilities required to accomplish key aspects of localization—for example, delegating decisions, alter-ing business processes and adjusting performance measures. (See Exhibit 10.)

Nonetheless, retailers don’t need to have all three pieces—people, processes and tools—in place at the time they launch a localization strategy. They can begin to pull levers with relatively basic tools and make investments pragmatically. Take a retailer who recognizes that its customer base will respond well to more unique product mixes yet lacks the capital to invest in advanced plan-ning software. It can begin to tailor assortments with the right process and simple spreadsheets.

Transforming Corporate Norms, Starting at the Top

The familiar bromide of “The CEO must champion it” has been uttered time and again as a key success factor for just about every major corporate initiative. But why is this particularly the case with localization? It’s because it requires fundamental changes across the organi-zation: empowering the field to get more involved in “discovering” and catering to the local customer, and getting core

Retailers report stronger capabilities in people than in processes andtools for localization

EXHIBIT 10: Half of the retailers do not have the people, processes and tools essential to localization

Proportion equipped

Adjust performancemeasures

Collaborate acrossfunctions

Change businessprocesses

Coordinate with supply chain partners

Effect culture,mindset change

Gather data fromstore, region

Delegatedecision-making

Analyze transactionaldata

Incorporateexternal data

30% 50%40% 70% 80% 90%60% 100%

PeopleProcessesToolsAverage

functions to work collaboratively in the pursuit of local customer needs, not just the mass market. Both demand that a retailer reshape a number of core beliefs—norms that are an outcrop of the tradition-al store approach to growth that has been key to the success of so many large chains.

The first set of norms that must change is how corporate views the field. Corporate must no longer look at field personnel as good only at executing strategy, not help-ing to define it. If it does, it won’t welcome or use field observations that point to local customer opportunities. As Bed Bath & Beyond Co-Chairman Warren Eisenberg once put it, “This culture, which takes ad-vantage of the knowledge, independence and customer focus of our associates, has always been the foundation of our long-term performance.”

Well-established beliefs and behaviors of functional team silos will also undermine localization. Merchandising, sourcing, store operations, marketing and other functions could initially view localization as creating new demands on them, rather than as something with corporate-wide benefit. For example, localization could mean that a retailer uses fewer pre-packs or increases the number of custom pre-packs. At face value, sourc-ing and supply chain managers will see this as detrimental to them because it may raise production and distribution costs. Distribution center managers rewarded on throughput may also see it as a threat to their performance. New styles, new colors and more sizes going to different stores will mean they must spend more time fill-ing each order and getting it right. How-

ever, the corporate-wide benefit is signifi-cant—increased sales and margins.

It’s up to the CEO to ensure that functional heads recognize the benefits of localiza-tion, not just its burdens. The CEO must align roles and responsibilities for localiza-tion, as well as revamp performance mea-sures and rewards.

The New Era of Localization

Some 150 years after mom-and-pop stores began to be displaced by re-gional chains, U.S. retail chains are entering a whole new phase—the era of localization. Growth strategies of the past, based on standardized stores and processes, will no longer suffice. While the one-size-fits-all store model has led to the rise of many giant retailers, they must now adjust their finely honed ma-chines to address the distinct needs of local markets without eroding their economies of scale.

Moreover, retailers need to view localization not as a one-time effort to pull one or two levers, but rather as an ongoing initiative that may require pull-ing nearly every lever over time to gener-ate the greatest benefits. Just like mer-chants who have made the Internet a formidable sales channel and tool for brick and mortar sales, localization will require both a long-term roadmap and short-term initiatives. Pilot projects must allow a retailer to test its plans on a sub-set of stores and work out all the kinks before full rollout. Retailers should design those initiatives to generate real benefits so that they can fund the next phase. These quick wins will also defuse

those who are skeptical about the value of localization.

Localization is here to stay. Retailers who wait to see how it plays out will risk driv-ing customers away and into the stores of regional, independent and chain retail-ers who respond well to the idiosyncratic needs of local communities. They will be forced even more to compete on price be-cause their offering and store experience aren’t distinctive enough. However, retail-ers who move quickly to meet different customer needs that are applicable across clusters of stores or in individual stores will build a profound competitive advantage that will drive sales and margin benefits.

Is Your Chain Sufficiently Localized?

How can retail executives assess the localization opportunity for their organization? Answers to these questions will be revealing.

> Are you gaining or losing market

share to your competitors?

> Do you have a clear under-

standing of why customers shop

your stores on a local level?

> Do you have significant

variations in sales by category

across your store base?

> Do you incorporate field

and customer feedback into

corporate processes?

> Do you have a plan for the

levers you are pulling now,

and over the next few years?

Retailers need to view localization not as a one-time effort to pull one or two levers, but rather as an ongoing initiative that may require pulling nearly every lever over time to generate the greatest benefits.

© 2009 Kurt Salmon Associates.

www.kurtsalmon.com

About the AuthorsChristina Bieniek, a partner based in KSA’s Atlanta office, is a retail industry expert, former retail executive and leads Kurt Salmon Associates’ ongoing research on localization. Clementine Martin, a manager based in KSA’s New York office, also contributed to this article. For more information, please contact us at [email protected].

Kurt Salmon AssociatesKurt Salmon Associates is the leading global management consulting firm specializing in the retail and consumer products industries. We leverage our unparalleled industry expertise to help business leaders make strategic, operational and technology decisions that achieve tangible and meaningful results.

ContactKurt Salmon Associates650 Fifth AvenueNew York, New York 10019212.319.9450