Embed Size (px)

Citation preview

Dream > Believe > Pursue

Earning Revenues and Earning Revenues and Government SupportGovernment Support

Dream > Believe > Pursue

2

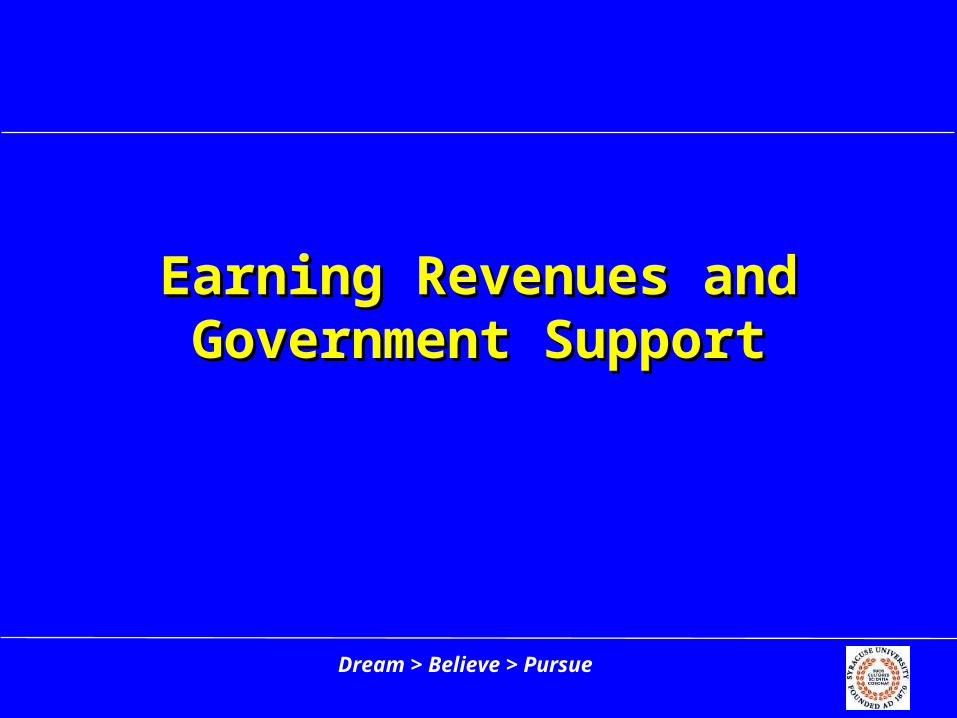

Nonprofit income sources, Nonprofit income sources, 20022002

Government funding, 33%

Private donations, 20%

Fee income, 47%

Dream > Believe > Pursue

3

OutlineOutline

• Earned income typesEarned income types• PricingPricing• Competition and Competition and

commercializationcommercialization• The government as customerThe government as customer• Government fundingGovernment funding

Dream > Believe > Pursue

4

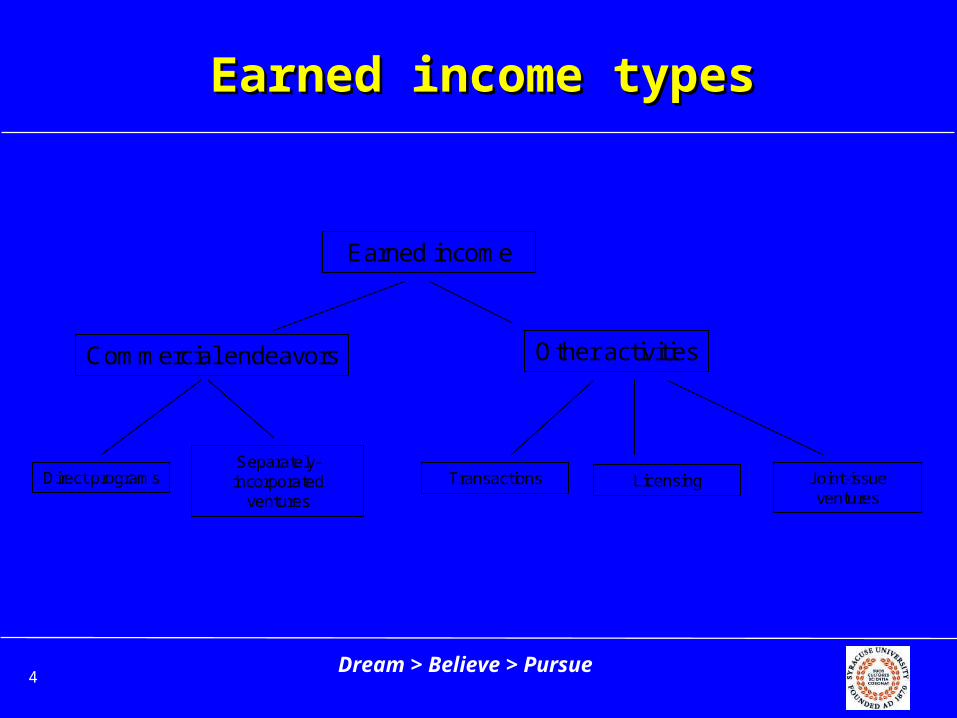

Earned income typesEarned income types

Commercial endeavors Other activities

Direct programs TransactionsSeparately-incorporated

ventures

Earned income

Licensing Joint-issue ventures

Dream > Believe > Pursue

5

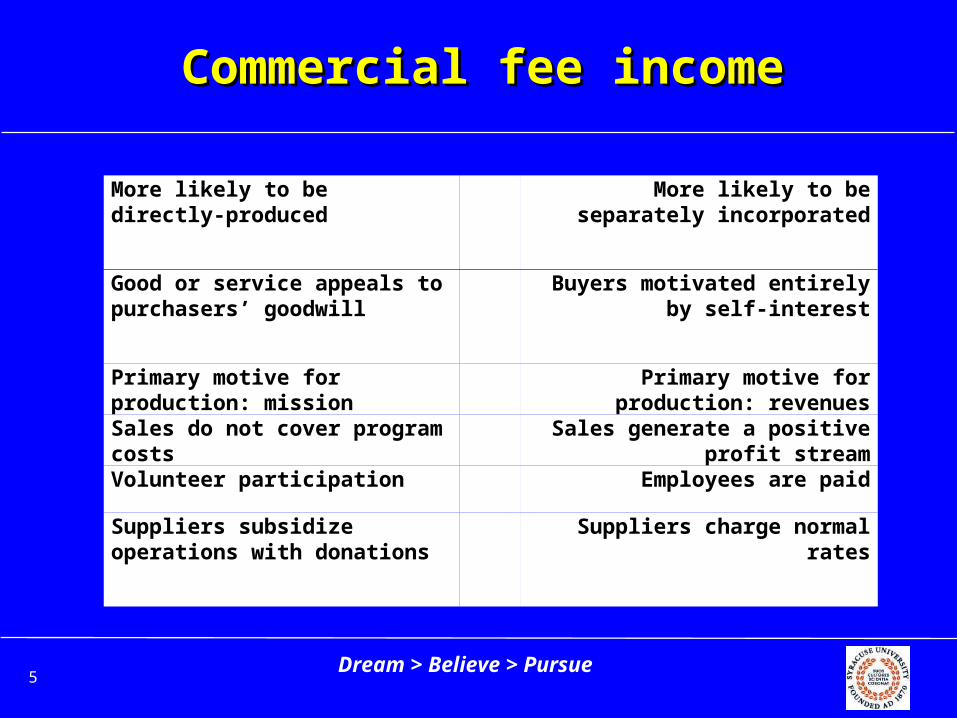

Commercial fee incomeCommercial fee income

More likely to be directly-produced

More likely to be separately incorporated

Good or service appeals to purchasers’ goodwill

Buyers motivated entirely by self-interest

Primary motive for production: mission

Primary motive for production: revenues

Sales do not cover program costs

Sales generate a positive profit stream

Volunteer participation Employees are paid

Suppliers subsidize operations with donations

Suppliers charge normal rates

Dream > Believe > Pursue

6

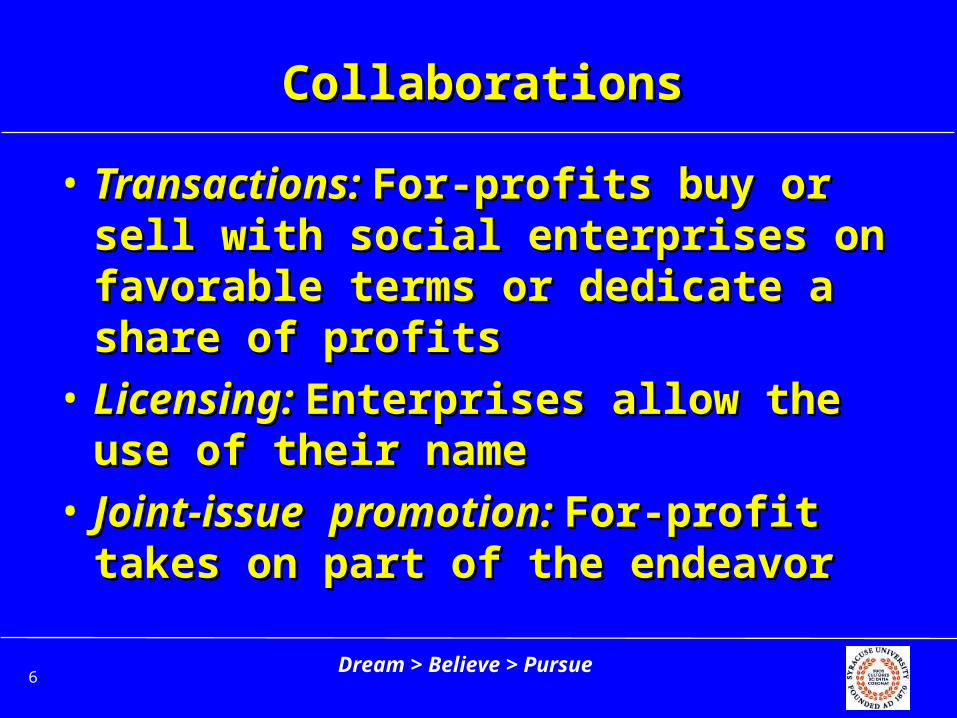

CollaborationsCollaborations

• Transactions: Transactions: For-profits buy or For-profits buy or sell with social enterprises on sell with social enterprises on favorable terms or dedicate a favorable terms or dedicate a share of profitsshare of profits

• Licensing: Licensing: Enterprises allow the Enterprises allow the use of their nameuse of their name

• Joint-issueJoint-issue promotion: promotion: For-profit For-profit takes on part of the endeavortakes on part of the endeavor

Dream > Believe > Pursue

7

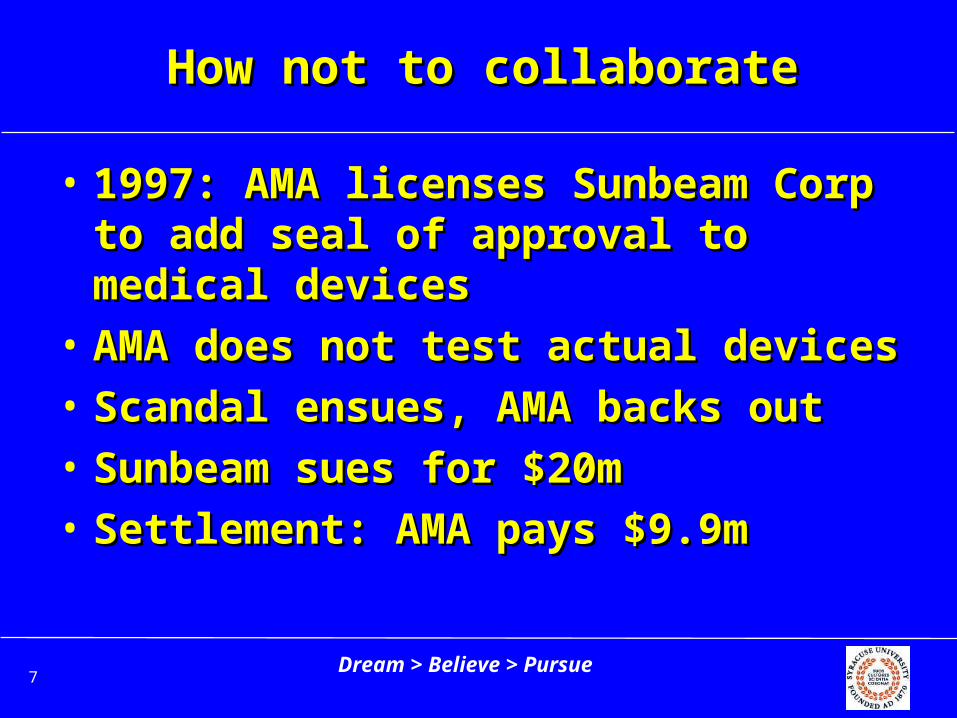

How not to collaborateHow not to collaborate

• 1997: AMA licenses Sunbeam 1997: AMA licenses Sunbeam Corp to add seal of approval to Corp to add seal of approval to medical devicesmedical devices

• AMA does not test actual devicesAMA does not test actual devices• Scandal ensues, AMA backs outScandal ensues, AMA backs out• Sunbeam sues for $20mSunbeam sues for $20m• Settlement: AMA pays $9.9mSettlement: AMA pays $9.9m

Dream > Believe > Pursue

8

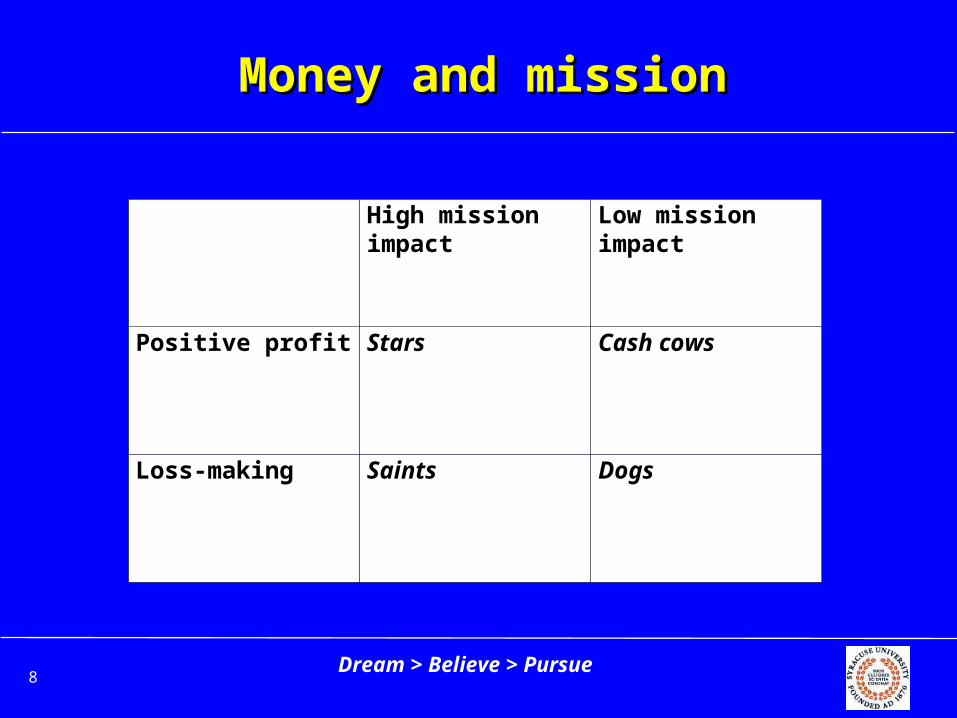

Money and missionMoney and mission

High mission impact

Low mission impact

Positive profit Stars Cash cows

Loss-making Saints Dogs

Dream > Believe > Pursue

9

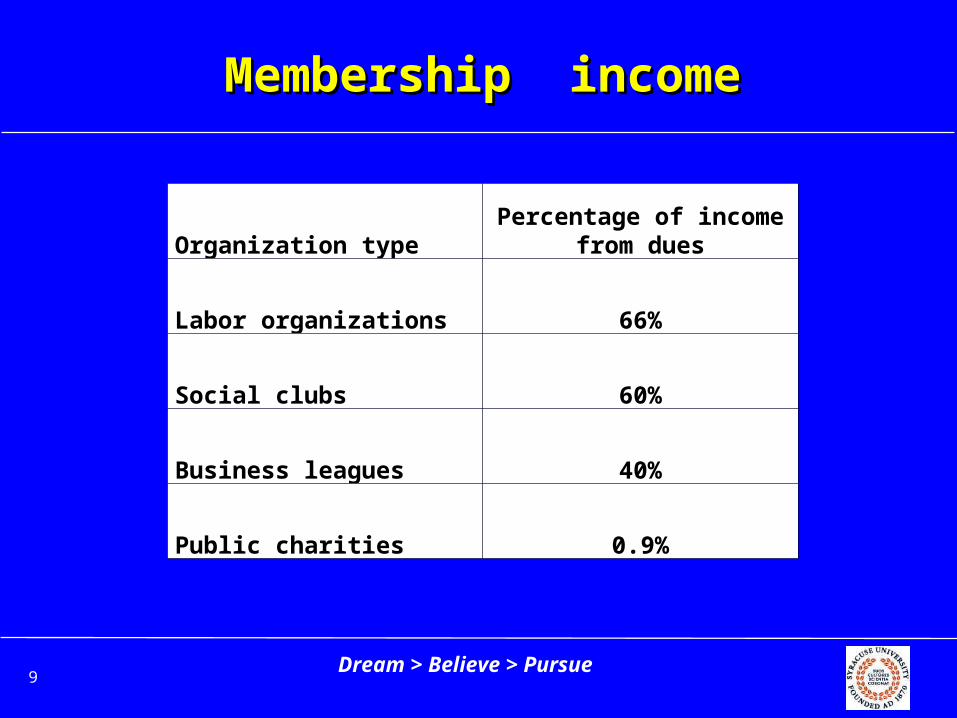

Membership incomeMembership income

Organization typePercentage of income

from dues

Labor organizations 66%

Social clubs 60%

Business leagues 40%

Public charities 0.9%

Dream > Believe > Pursue

10

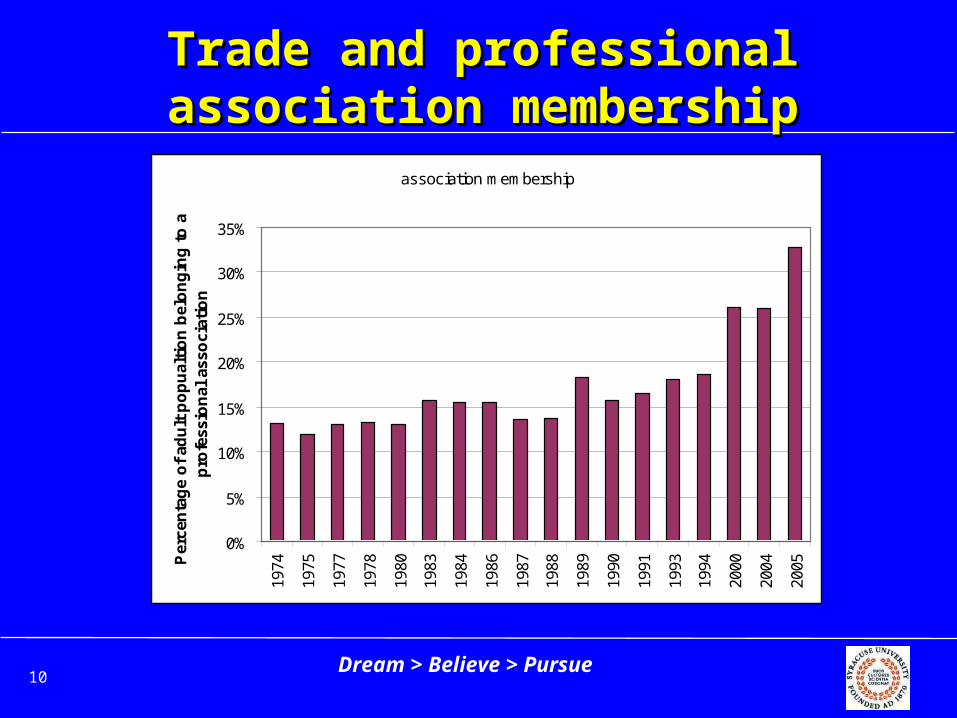

Trade and professional Trade and professional association membershipassociation membership

association membership

0%

5%

10%

15%

20%

25%

30%

35%

1974

1975

1977

1978

1980

1983

1984

1986

1987

1988

1989

1990

1991

1993

1994

2000

2004

2005P

erce

nta

ge

of

adu

lt p

op

ual

tio

n b

elo

ng

ing

to

a

pro

fess

ion

al a

sso

ciat

ion

Dream > Believe > Pursue

Source: 2004 Maxwell School Poll of Civil Society

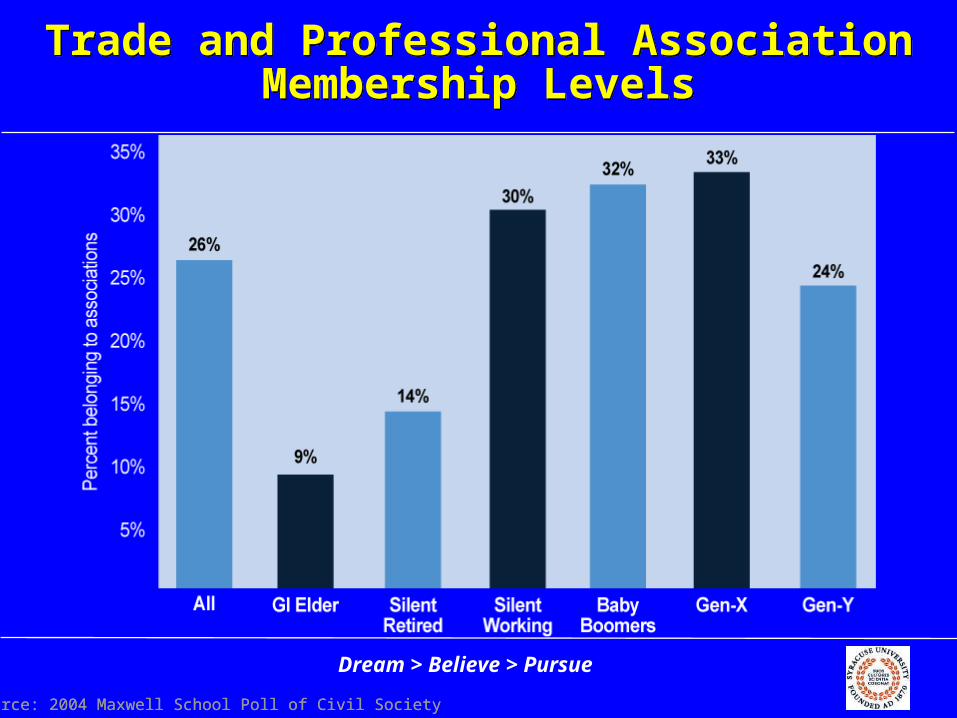

Trade and Professional Association Membership Levels

Trade and Professional Association Membership Levels

Source: 2004 Maxwell School Poll of Civil Society

Dream > Believe > Pursue

12

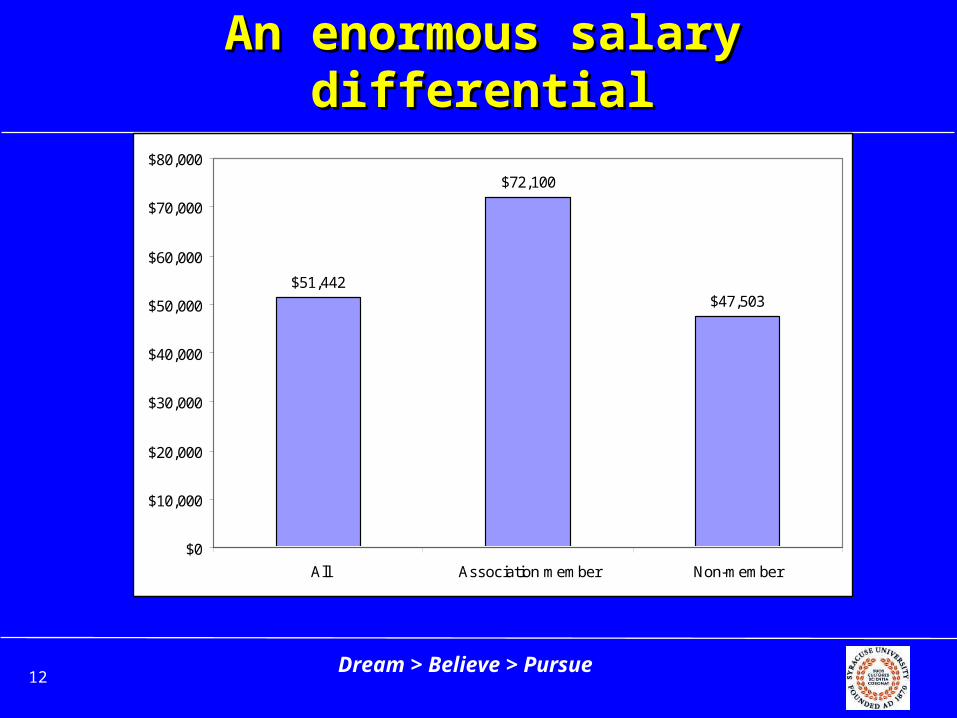

An enormous salary An enormous salary differentialdifferential

$51,442

$72,100

$47,503

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

All Association member Non-member

Dream > Believe > Pursue

13

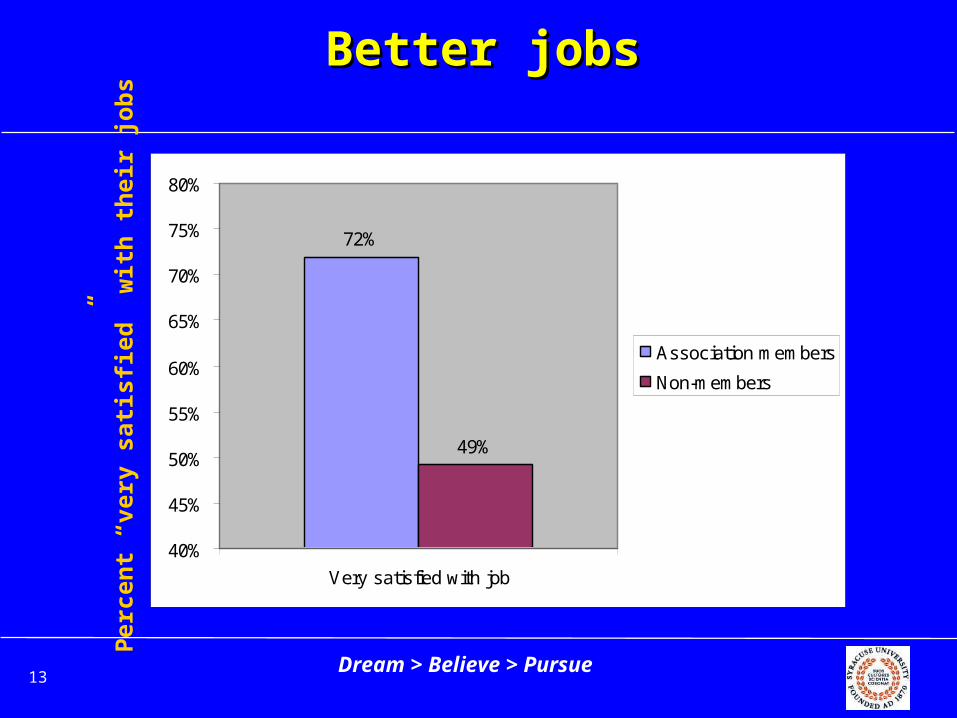

Better jobsBetter jobsP

erce

nt “

very

sat

isfi

ed”

wit

h th

eir

job

s

72%

49%

40%

45%

50%

55%

60%

65%

70%

75%

80%

Very satisfied with job

Association members

Non-members

Dream > Believe > Pursue

14

The story hereThe story here

Associations are where the Associations are where the winners meetwinners meet

Through association involvement, Through association involvement, upwardly-mobile professionalsupwardly-mobile professionals

• Identify themselvesIdentify themselves• Learn from one anotherLearn from one another

• Form communities of winnersForm communities of winners

Dream > Believe > Pursue

15

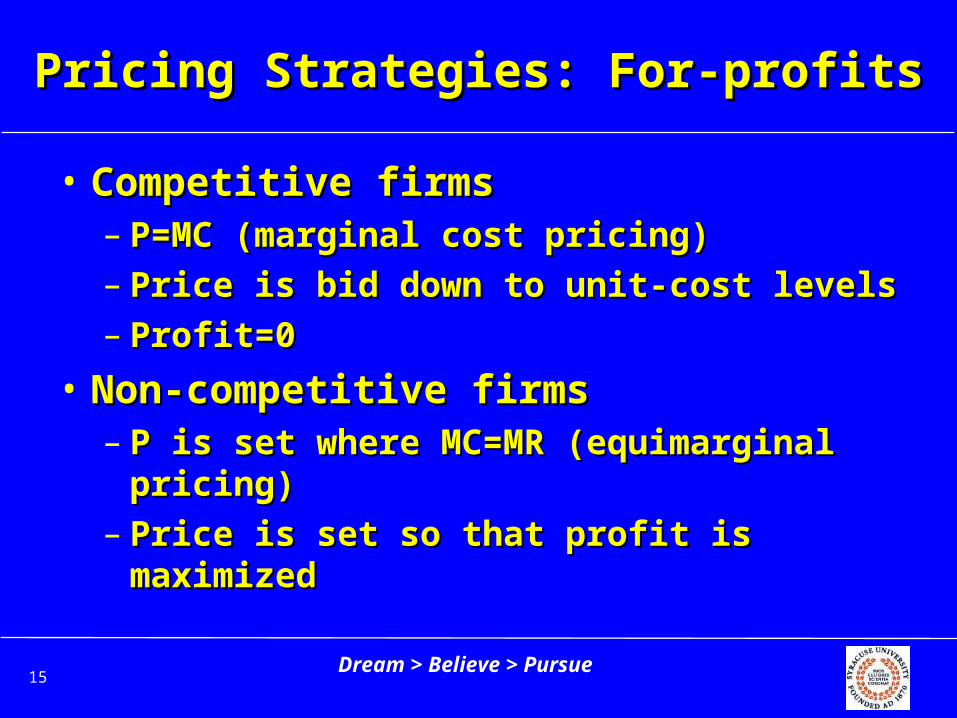

Pricing Strategies: For-profitsPricing Strategies: For-profits

• Competitive firmsCompetitive firms– P=MC (marginal cost pricing)P=MC (marginal cost pricing)– Price is bid down to unit-cost levelsPrice is bid down to unit-cost levels– Profit=0Profit=0

• Non-competitive firmsNon-competitive firms– P is set where MC=MR (equimarginal P is set where MC=MR (equimarginal

pricing)pricing)– Price is set so that profit is Price is set so that profit is

maximizedmaximized

Dream > Believe > Pursue

16

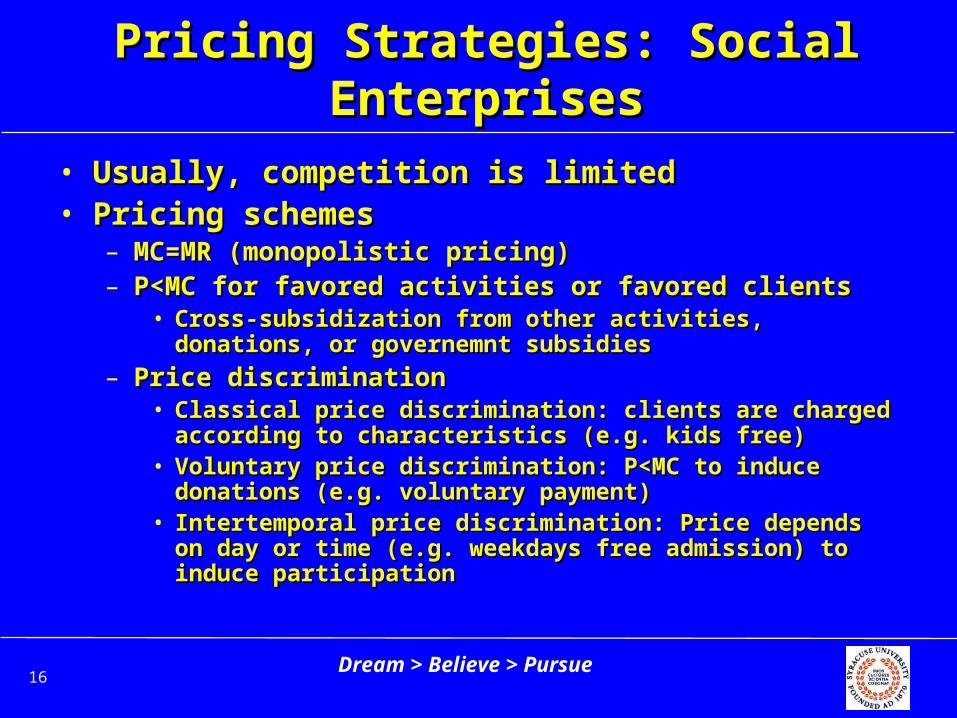

Pricing Strategies: Social Pricing Strategies: Social EnterprisesEnterprises

• Usually, competition is limitedUsually, competition is limited• Pricing schemesPricing schemes

– MC=MR (monopolistic pricing)MC=MR (monopolistic pricing)– P<MC for favored activities or favored clientsP<MC for favored activities or favored clients

• Cross-subsidization from other activities, donations, Cross-subsidization from other activities, donations, or governemnt subsidiesor governemnt subsidies

– Price discriminationPrice discrimination• Classical price discrimination: clients are charged Classical price discrimination: clients are charged

according to characteristics (e.g. kids free)according to characteristics (e.g. kids free)• Voluntary price discrimination: P<MC to induce Voluntary price discrimination: P<MC to induce

donations (e.g. voluntary payment)donations (e.g. voluntary payment)• Intertemporal price discrimination: Price depends on Intertemporal price discrimination: Price depends on

day or time (e.g. weekdays free admission) to induce day or time (e.g. weekdays free admission) to induce participationparticipation

Dream > Believe > Pursue

17

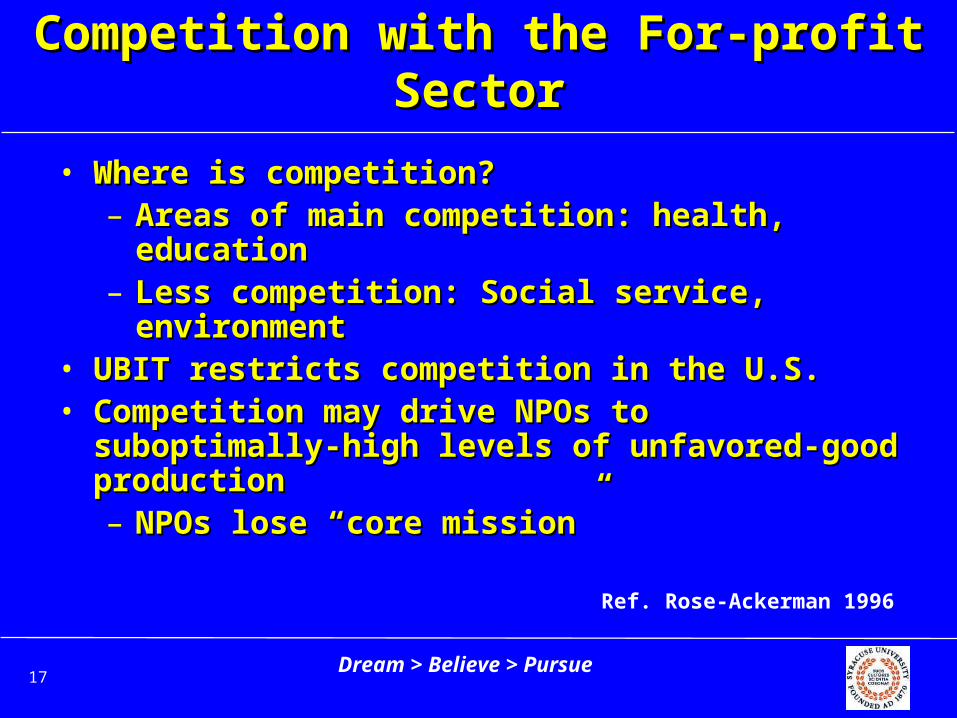

Competition with the For-profit Competition with the For-profit SectorSector

• Where is competition?Where is competition?– Areas of main competition: health, Areas of main competition: health,

educationeducation– Less competition: Social service, Less competition: Social service,

environmentenvironment• UBIT restricts competition in the U.S.UBIT restricts competition in the U.S.• Competition may drive NPOs to Competition may drive NPOs to

suboptimally-high levels of unfavored-good suboptimally-high levels of unfavored-good productionproduction– NPOs lose “core mission”NPOs lose “core mission”

Ref. Rose-Ackerman 1996

Dream > Believe > Pursue

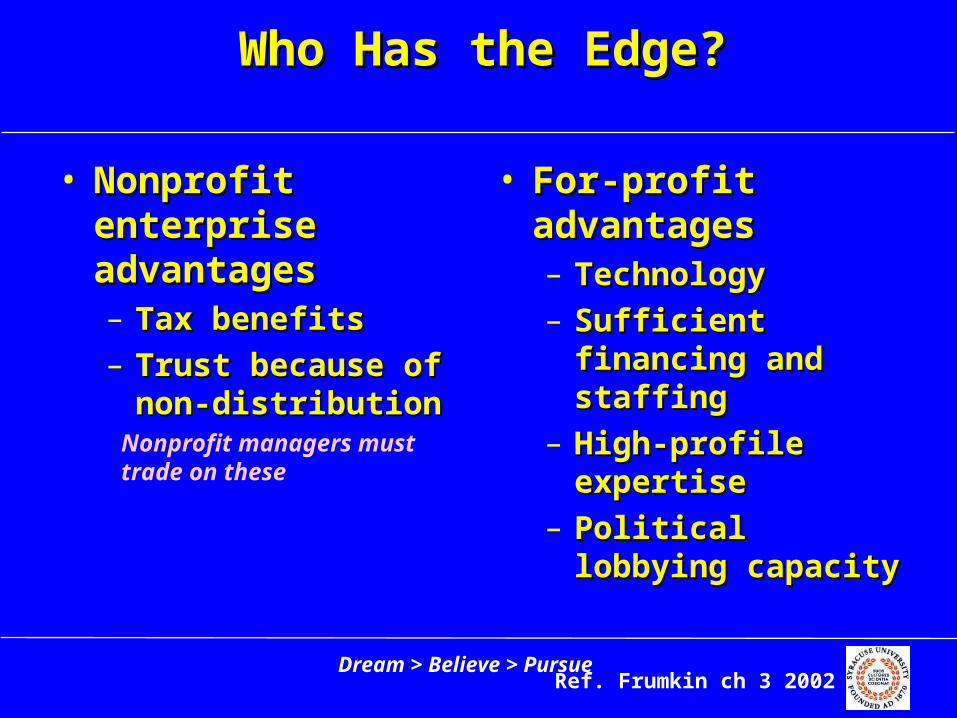

Who Has the Edge?Who Has the Edge?

• Nonprofit Nonprofit enterprise enterprise advantagesadvantages– Tax benefitsTax benefits– Trust because of Trust because of

non-distributionnon-distribution

• For-profit For-profit advantagesadvantages– TechnologyTechnology– Sufficient Sufficient

financing and financing and staffingstaffing

– High-profile High-profile expertiseexpertise

– Political lobbying Political lobbying capacitycapacity

Nonprofit managers must trade on these

Ref. Frumkin ch 3 2002

Dream > Believe > Pursue

19

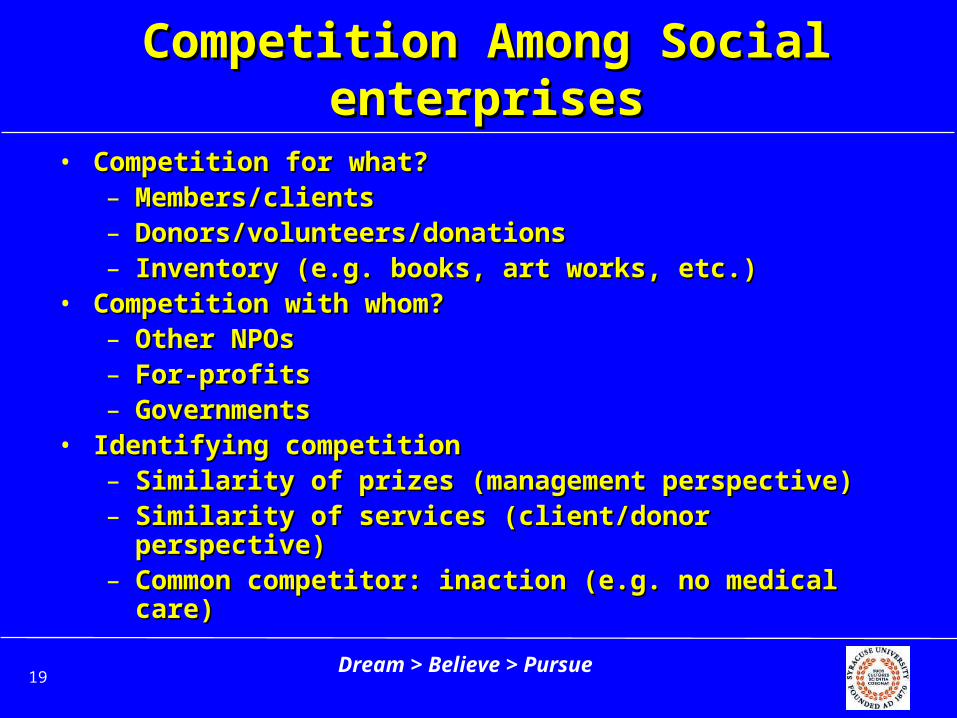

Competition Among Social Competition Among Social enterprisesenterprises

• Competition for what?Competition for what?– Members/clientsMembers/clients– Donors/volunteers/donationsDonors/volunteers/donations– Inventory (e.g. books, art works, etc.)Inventory (e.g. books, art works, etc.)

• Competition with whom?Competition with whom?– Other NPOsOther NPOs– For-profitsFor-profits– GovernmentsGovernments

• Identifying competitionIdentifying competition– Similarity of prizes (management perspective)Similarity of prizes (management perspective)– Similarity of services (client/donor perspective)Similarity of services (client/donor perspective)– Common competitor: inaction (e.g. no medical Common competitor: inaction (e.g. no medical

care)care)

Dream > Believe > Pursue

20

Social Enterprise Social Enterprise CommercializationCommercialization

• ReasonsReasons– Increasing competition with for-profitsIncreasing competition with for-profits– Increasing competition with other social venturesIncreasing competition with other social ventures– Growing reliance on donations and earned incomeGrowing reliance on donations and earned income– Corporate partnershipsCorporate partnerships– Demand for accountabilityDemand for accountability– Nonprofit culture becoming more “corporate”Nonprofit culture becoming more “corporate”

• RisksRisks– Loss of core missionLoss of core mission– Decreased attention to need, more on bottom lineDecreased attention to need, more on bottom line

Ref. Salamon & Young 2002

Dream > Believe > Pursue

21

Privatization: A Common Privatization: A Common Opportunity to Earn RevenuesOpportunity to Earn Revenues

•The practice of delegating public The practice of delegating public duties and responsibilities to private duties and responsibilities to private organizations (nonprofit and for-organizations (nonprofit and for-profit)profit)

•A frequent revenue-generating A frequent revenue-generating opportunity for social entrepreneursopportunity for social entrepreneurs

•Governments are often the customer Governments are often the customer for an enterprise’s servicesfor an enterprise’s services

Dream > Believe > Pursue

22

Why Privatization?Why Privatization?

• Reduced costsReduced costs• Specialized expertiseSpecialized expertise• Increased qualityIncreased quality• Smaller government Smaller government

and less bureaucracyand less bureaucracy• Market based Market based

incentives resulting incentives resulting in efficienciesin efficiencies

• Competition vs Monopoly

• Greater reliance on free enterprise - market based principles (assumes competition)

• Greater use of voluntarism

• Politics

Dream > Believe > Pursue

23

Dangers to Social enterprises from Dangers to Social enterprises from Partnerships with GovernmentPartnerships with Government

• Loss of nonprofit autonomyLoss of nonprofit autonomy• VendorismVendorism• BureaucratizationBureaucratization

Source: Frumkin ch 3 2002

Dream > Believe > Pursue

24

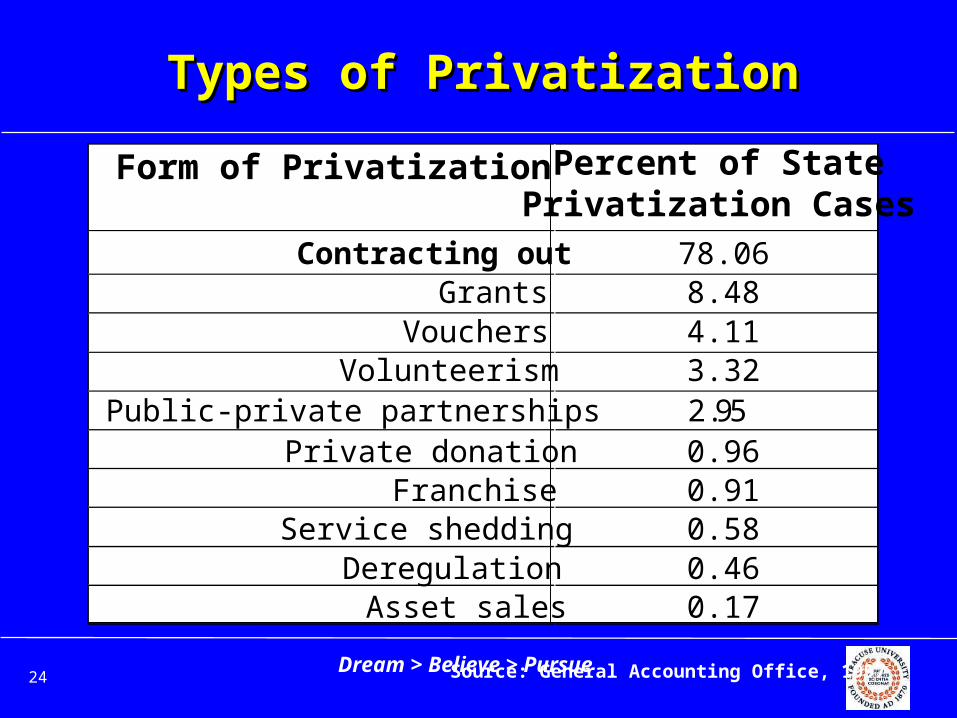

Types of PrivatizationTypes of Privatization

Source: General Accounting Office, 1997

Form of Privatization Percent of StatePrivatization Cases

2.95

78.06 8.48 4.11 3.32

0.96 0.91 0.58 0.46

Public-private partnerships

Contracting outGrants

VouchersVolunteerism

Private donationFranchise

Service sheddingDeregulation

Asset sales 0.17

Dream > Believe > Pursue

25

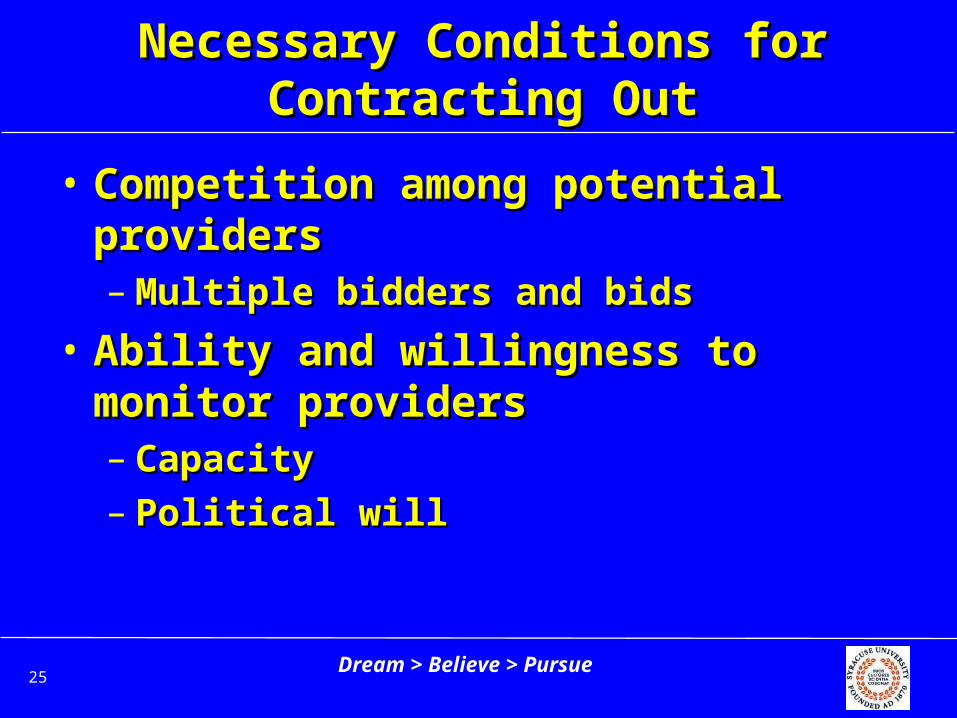

Necessary Conditions for Necessary Conditions for Contracting OutContracting Out

• Competition among potential Competition among potential providersproviders– Multiple bidders and bidsMultiple bidders and bids

• Ability and willingness to Ability and willingness to monitor providersmonitor providers– CapacityCapacity– Political willPolitical will

Dream > Believe > Pursue

26

Privatization in Competitive Privatization in Competitive IndustriesIndustries

• More competitionMore competition– GarbageGarbage– Snow removalSnow removal– TowingTowing– Data processingData processing

• Less competition– Foster care– Domestic

violence– Chemical

dependency

Dream > Believe > Pursue

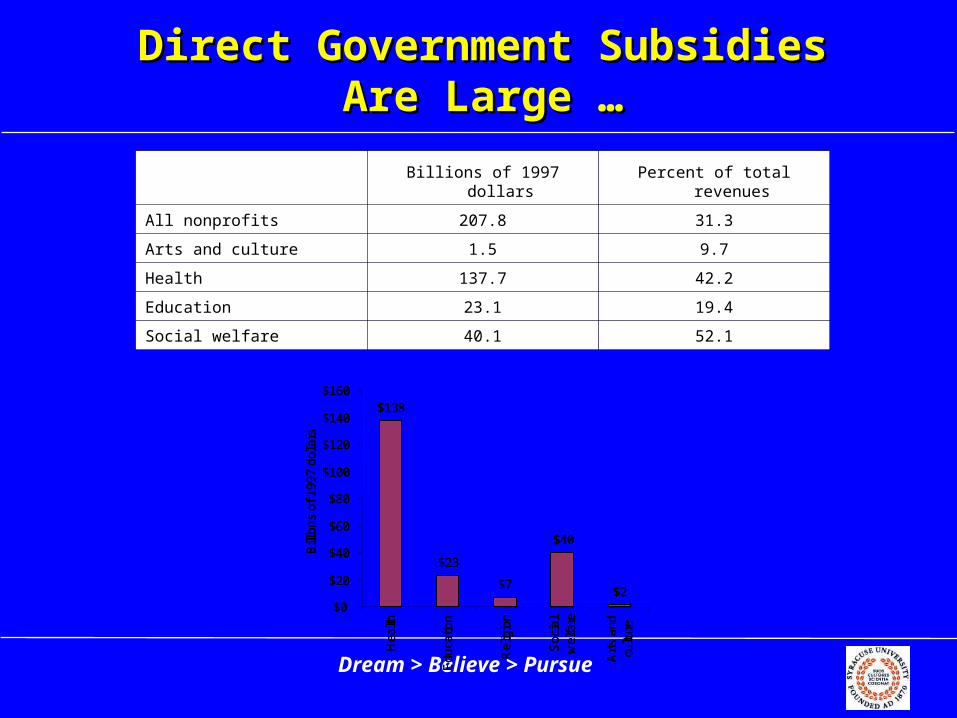

Direct Government Subsidies Direct Government Subsidies Are Large …Are Large …

Billions of 1997 dollars Percent of total revenues

All nonprofits 207.8 31.3

Arts and culture 1.5 9.7

Health 137.7 42.2

Education 23.1 19.4

Social welfare 40.1 52.1

$138

$23

$7

$40

$2$0

$20

$40

$60

$80

$100

$120

$140

$160H

ealth

Edu

catio

n

Re

ligio

n

So

cia

lw

elfa

re

Art

s a

ndcu

lture

Bill

ion

s of

199

7 d

olla

rs

$138

$23

$7

$40

$2$0

$20

$40

$60

$80

$100

$120

$140

$160H

ealth

Edu

catio

n

Re

ligio

n

So

cia

lw

elfa

re

Art

s a

ndcu

lture

Bill

ion

s of

199

7 d

olla

rs

Dream > Believe > Pursue

28

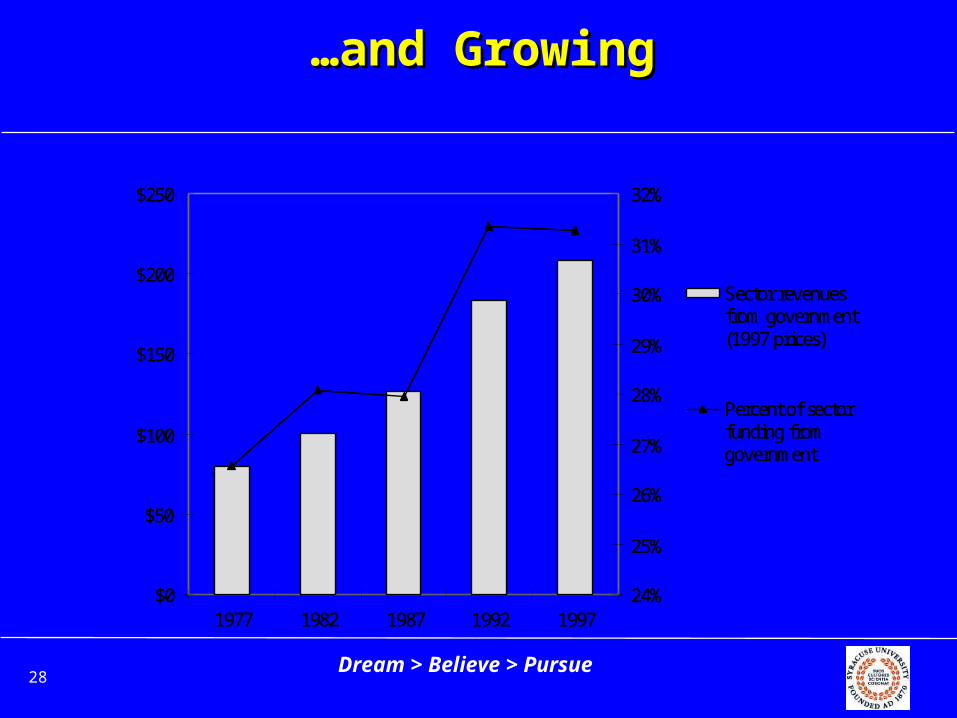

……and Growingand Growing

$0

$50

$100

$150

$200

$250

1977 1982 1987 1992 199724%

25%

26%

27%

28%

29%

30%

31%

32%

Sector revenues from government (1997 prices)

Percent of sector funding from government

$0

$50

$100

$150

$200

$250

1977 1982 1987 1992 199724%

25%

26%

27%

28%

29%

30%

31%

32%

Sector revenues from government (1997 prices)

Percent of sector funding from government

Dream > Believe > Pursue

29

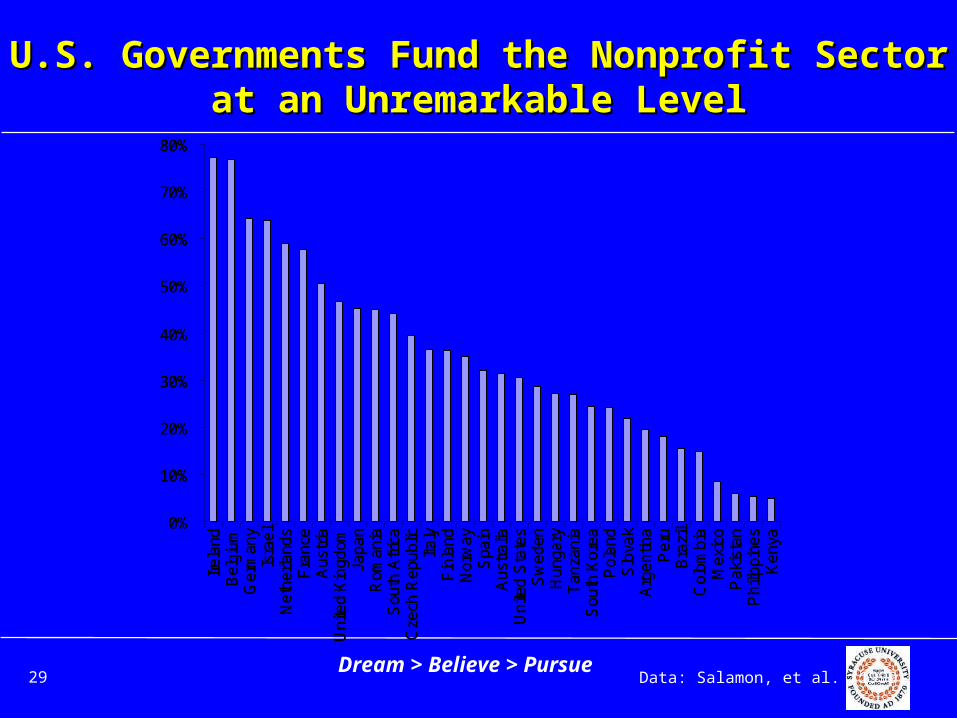

U.S. Governments Fund the Nonprofit Sector U.S. Governments Fund the Nonprofit Sector at an Unremarkable Levelat an Unremarkable Level

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ire

land

Be

lgiu

mG

erm

any

Isra

el

Ne

the

rland

sF

ran

ceA

ust

riaU

nite

d K

ingd

omJa

pan

Rom

ania

Sou

th A

fric

aC

zech

Re

pub

licIt

aly

Fin

land

No

rwa

yS

pain

Au

stra

liaU

nite

d S

tate

sS

we

den

Hun

gary

Tan

zan

iaS

outh

Ko

rea

Po

land

Slo

vak

Arg

en

tina

Pe

ruB

razi

lC

olo

mb

iaM

exi

coP

aki

stan

Ph

ilipp

ine

sK

enya

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ire

land

Be

lgiu

mG

erm

any

Isra

el

Ne

the

rland

sF

ran

ceA

ust

riaU

nite

d K

ingd

omJa

pan

Rom

ania

Sou

th A

fric

aC

zech

Re

pub

licIt

aly

Fin

land

No

rwa

yS

pain

Au

stra

liaU

nite

d S

tate

sS

we

den

Hun

gary

Tan

zan

iaS

outh

Ko

rea

Po

land

Slo

vak

Arg

en

tina

Pe

ruB

razi

lC

olo

mb

iaM

exi

coP

aki

stan

Ph

ilipp

ine

sK

enya

Data: Salamon, et al. (1999)

Dream > Believe > Pursue

30

Indirect Subsidies and TaxesIndirect Subsidies and Taxes

• Taxes foregone on deductible Taxes foregone on deductible contributionscontributions

• UBITUBIT• Property taxesProperty taxes• Tax creditsTax credits

Dream > Believe > Pursue

31

Income Tax Revenues Income Tax Revenues ForegoneForegone

• t=individual’s marginal tax ratet=individual’s marginal tax rate• m=gross incomem=gross income• D=tax-deductible donationsD=tax-deductible donations• t(m-D)=taxes paidt(m-D)=taxes paid• tD=indirect government subsidytD=indirect government subsidy• 2002 estimate: $37.2b2002 estimate: $37.2b

Dream > Believe > Pursue

32

Corporate Tax Exemption and Corporate Tax Exemption and the UBITthe UBIT

• As a general rule, organizations have As a general rule, organizations have incentives to invest in activities incentives to invest in activities where their earnings are tax exempt where their earnings are tax exempt but other organizations must pay taxbut other organizations must pay tax

• Nonprofits to a significant degree can Nonprofits to a significant degree can shift costs from exempt to non-shift costs from exempt to non-exempt activitiesexempt activities

• → → UBIT payments to government are UBIT payments to government are very lowvery low

Dream > Believe > Pursue

33

The Property Tax The Property Tax ExemptionExemption

• Could be thought of as a subsidy Could be thought of as a subsidy by the state, or as a reflection of by the state, or as a reflection of the “sovereignty” of nonprofitsthe “sovereignty” of nonprofits

• Total US value of exemption Total US value of exemption around $6 billion (mostly in around $6 billion (mostly in hospitals and education)hospitals and education)

• Increased use of PILOTS: Increased use of PILOTS: strategic move for nonprofits strategic move for nonprofits

Dream > Believe > Pursue

34

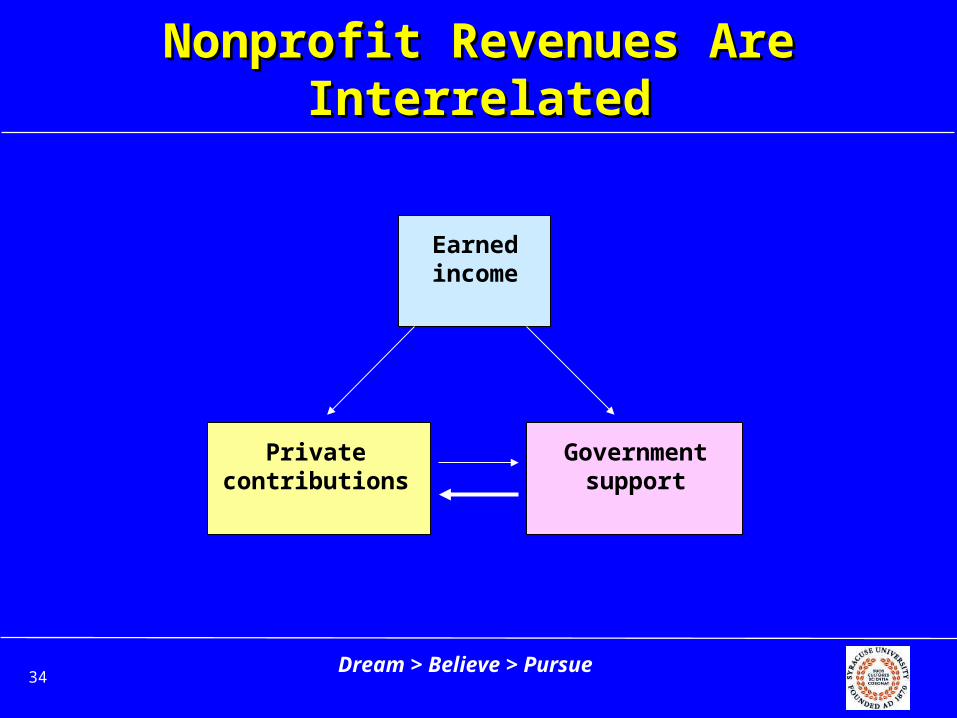

Nonprofit Revenues Are Nonprofit Revenues Are InterrelatedInterrelated

Earnedincome

Governmentsupport

Privatecontributions

Dream > Believe > Pursue

35

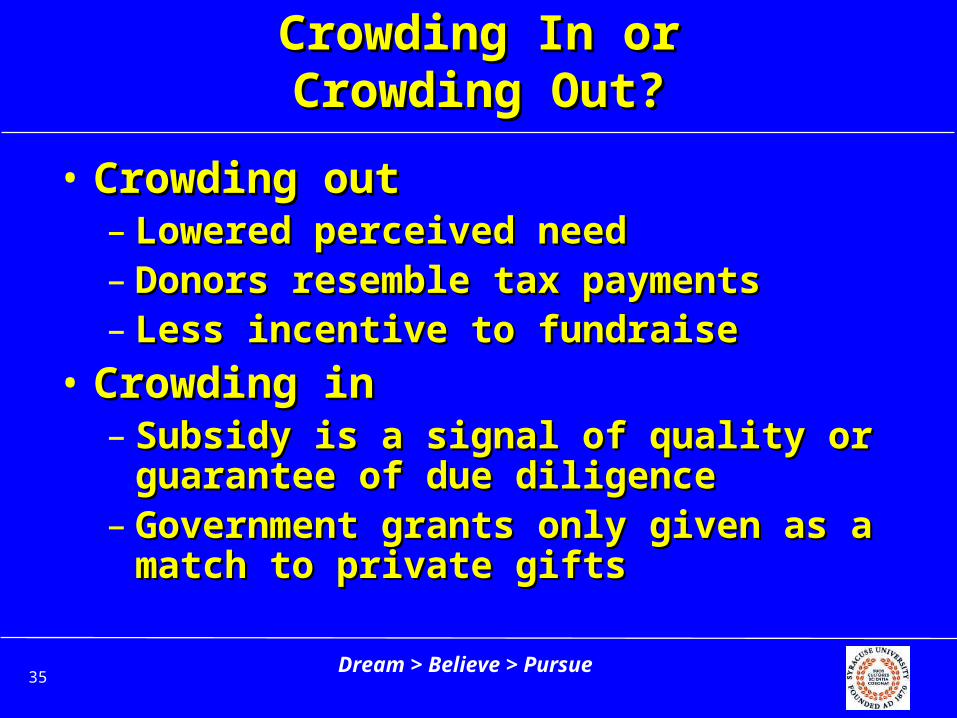

Crowding In orCrowding In orCrowding Out?Crowding Out?

• Crowding outCrowding out– Lowered perceived needLowered perceived need– Donors resemble tax paymentsDonors resemble tax payments– Less incentive to fundraiseLess incentive to fundraise

• Crowding inCrowding in– Subsidy is a signal of quality or Subsidy is a signal of quality or

guarantee of due diligenceguarantee of due diligence– Government grants only given as a Government grants only given as a

match to private giftsmatch to private gifts

![Did Jesus Teach Different Commandments? - COGMessenger€¦ · righteousness, [pursue] godliness, [pursue] faith, [pursue] love, [pursue] patience, [pursue] meekness. Fight the good](https://img.pdfslide.us/doc/110x75/6013f9fd8bd492289f768781/did-jesus-teach-different-commandments-cogmessenger-righteousness-pursue-godliness.jpg)