Embed Size (px)

Citation preview

Draft

Human Capital and Capital Formation in Agriculture of Bangladesh

Prof. S.M. Fakhrul Islam

Chapter 1

The Agriculture, Economy and Growth Scenarios

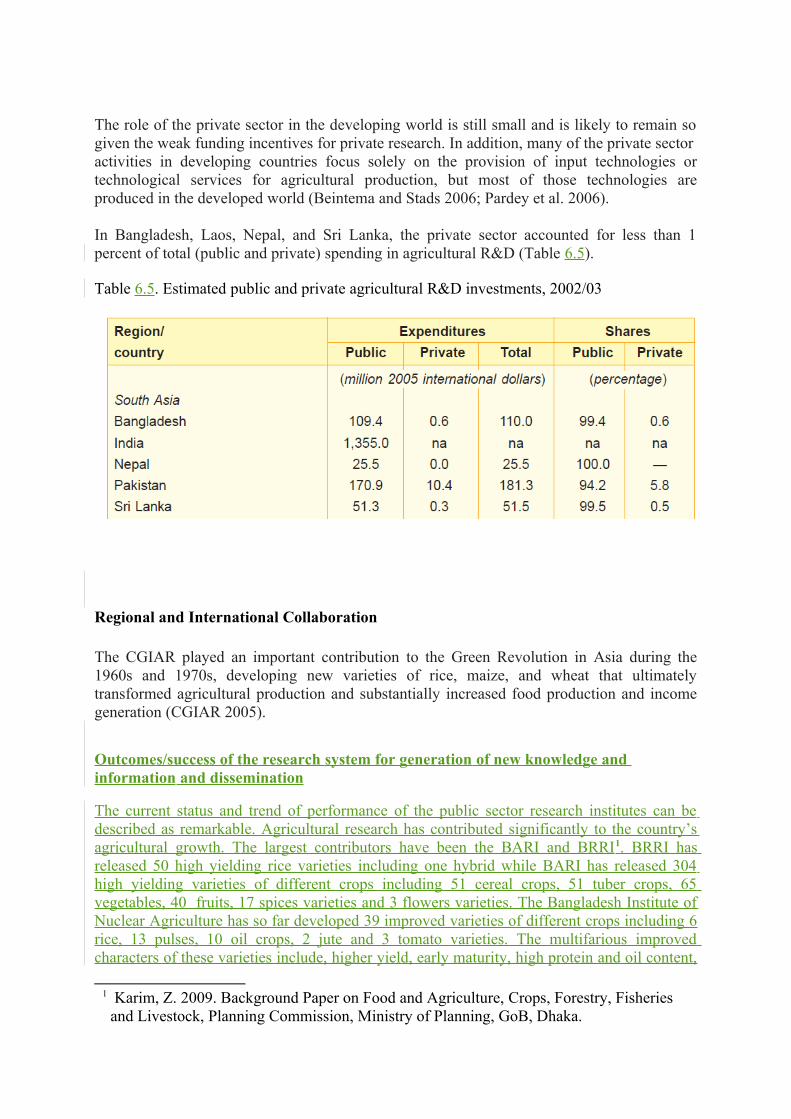

1. Current Situation of Agriculture and Food Security

Population, land use, farm structure and poverty

In 2010, the population of Bangladesh was about 165 million, inhabiting an area of just over 50,000 square miles—of which about 22.3 million acres (69 percent of total land area) are cultivated land. Competition for the use of land for agriculture, urbanization, homesteads, and infrastructure is intense; from 1983–84 through 1995–96, the cultivated area declined by 12 percent (BBS 1996). The average farm size fell from 2.26 to 1.69 acres; the cropping intensity averages 170 percent. Rice is the dominant crop, occupying about 73 percent of the cropped area.. Notwithstanding the country’s large and still-growing population, the rate of population growth has fallen over time, from an average of 2.3 percent annually between 1975 and 1985 to 1.65 percent between 2000 and 2010.

Food poverty, measured by counting the number of persons consuming less than 2,212 calories per day, is especially high in Bangladesh. Recent estimates, however, show that the average incidence of poverty might have declined slightly, to about 42 percent, between 1996 and 2009 (NMTPF 2009). The great majority of the poor live in rural areas and that more than half the rural population live below the poverty line, compared with about one-third of urban dwellers.

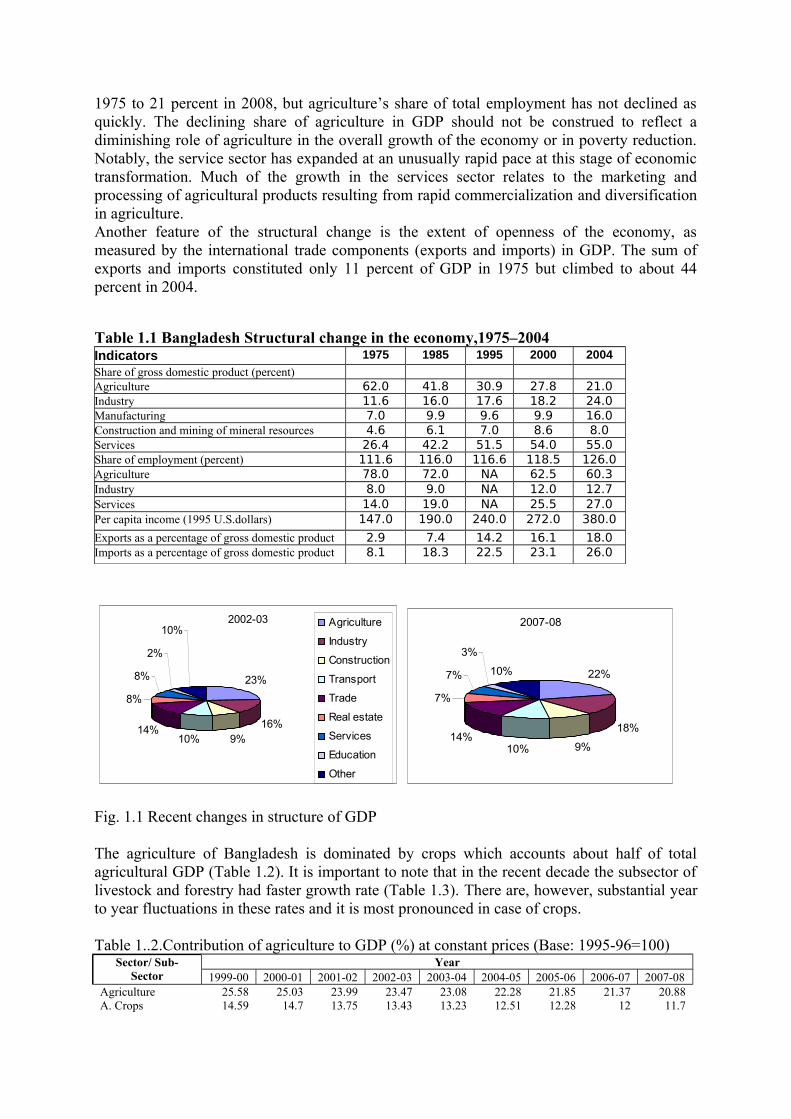

The economy and agriculture The GDP growth over the last five years consistently remained above 6 percent. Despite the losses caused by the two consecutive floods and the cyclone ‘Sidr’ in 2007 and also the adverse effects arising from unprecedented price hike of crude oil in international market and agricultural inputs. The growth of import-export trade, secular increasing trend in the flow of remittance and the favourable balance of the current account kept the external sector to some extent stable.During the recent decade overall GDP of Bangladesh has been shown a considerabley shown upward trend. But the growth in agriculture GDP slightly declined with an average of 3.4% during 1997 to 2008. Agriculture being the engine of growth of the economy, there is no other alternative but to develop agriculture sector for alleviation of poverty by attaining accelerated economic growth. Since provision of food security, improvement of the living standard and generation of employment opportunities of the huge population of the country are directly linked to the development of agriculture, there have been continued efforts by the Government for the overall development of this sector.Agriculture is the most important sector of Bangladesh economy due to its role in food security, employment and livelihood. Still more than 70% of the people in Bangladesh are directly or indirectly employed in this sector. The transformation of Bangladesh’s economy, measured by changes in the sectoral shares of gross domestic product (GDP), is shown in Table 1.1 and Fig. 1.1. This structural change clearly indicates a rapid movement away from an agriculture-dominated economy. Agriculture’s share of GDP declined from 62 percent in

1975 to 21 percent in 2008, but agriculture’s share of total employment has not declined as quickly. The declining share of agriculture in GDP should not be construed to reflect a diminishing role of agriculture in the overall growth of the economy or in poverty reduction. Notably, the service sector has expanded at an unusually rapid pace at this stage of economic transformation. Much of the growth in the services sector relates to the marketing and processing of agricultural products resulting from rapid commercialization and diversification in agriculture. Another feature of the structural change is the extent of openness of the economy, as measured by the international trade components (exports and imports) in GDP. The sum of exports and imports constituted only 11 percent of GDP in 1975 but climbed to about 44 percent in 2004.

Table 1.1 Bangladesh Structural change in the economy,1975–2004Indicators 1975 1985 1995 2000 2004Share of gross domestic product (percent)Agriculture 62.0 41.8 30.9 27.8 21.0Industry 11.6 16.0 17.6 18.2 24.0Manufacturing 7.0 9.9 9.6 9.9 16.0Construction and mining of mineral resources 4.6 6.1 7.0 8.6 8.0Services 26.4 42.2 51.5 54.0 55.0Share of employment (percent) 111.6 116.0 116.6 118.5 126.0Agriculture 78.0 72.0 NA 62.5 60.3Industry 8.0 9.0 NA 12.0 12.7Services 14.0 19.0 NA 25.5 27.0Per capita income (1995 U.S.dollars) 147.0 190.0 240.0 272.0 380.0

Exports as a percentage of gross domestic product 2.9 7.4 14.2 16.1 18.0Imports as a percentage of gross domestic product 8.1 18.3 22.5 23.1 26.0

2002-03

23%

16%9%10%

14%

8%

8%

2%

10%Agriculture

Industry

Construction

Transport

Trade

Real estate

Services

Education

Other

2007-08

22%

18%

9%10%14%

7%

7%

3%

10%

Fig. 1.1 Recent changes in structure of GDP

The agriculture of Bangladesh is dominated by crops which accounts about half of total agricultural GDP (Table 1.2). It is important to note that in the recent decade the subsector of livestock and forestry had faster growth rate (Table 1.3). There are, however, substantial year to year fluctuations in these rates and it is most pronounced in case of crops.

Table 1..2.Contribution of agriculture to GDP (%) at constant prices (Base: 1995-96=100)Sector/ Sub-

SectorYear

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08Agriculture 25.58 25.03 23.99 23.47 23.08 22.28 21.85 21.37 20.88A. Crops 14.59 14.7 13.75 13.43 13.23 12.51 12.28 12 11.7

B. Livestock 3.02 2.95 2.96 2.93 2.91 2.95 2.92 2.88 2.79C. Forestry 1.88 1.87 1.88 1.86 1.83 1.82 1.79 1.76 1.75D. Fishing 6.09 5.51 5.4 5.25 5.11 5 4.86 4.73 4.64

Source: Statistical Yearbook of Bangladesh 2007

Table 1.3.Growth rate of agriculture and its sub-sectors at constant price (Base: 1995-96=100)Sector/ Sub-

SectorYear

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08GDP growth rate 5.94 5.27 4.42 5.26 6.27 5.96 6.63 6.43 6.21Agriculture 6.16 4.59 2.36 3.54 4.13 4.03 5.07 4.81 3.85A. Crops 8.10 6.18 -2.39 2.88 4.27 0.15 5.03 4.43 3.44B. Livestock 2.74 2.81 4.70 4.51 4.98 7.23 6.15 5.49 2.41C. Forestry 4.94 4.85 4.91 4.43 4.18 5.09 5.18 5.24 5.42D. Fishing 8.87 4.53 2.22 2.33 3.09 3.65 3.91 4.07 4.11

Source: Statistical Yearbook of Bangladesh 2007 & Statistical Pocket Book 2008

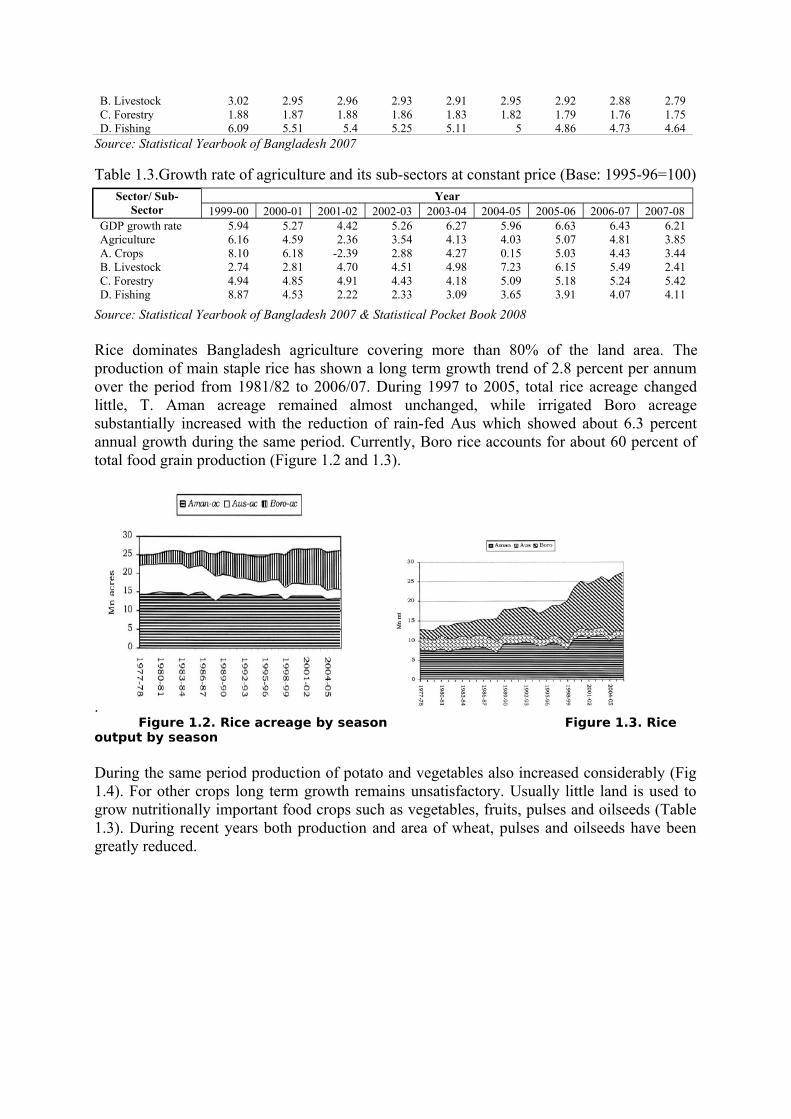

Rice dominates Bangladesh agriculture covering more than 80% of the land area. The production of main staple rice has shown a long term growth trend of 2.8 percent per annum over the period from 1981/82 to 2006/07. During 1997 to 2005, total rice acreage changed little, T. Aman acreage remained almost unchanged, while irrigated Boro acreage substantially increased with the reduction of rain-fed Aus which showed about 6.3 percent annual growth during the same period. Currently, Boro rice accounts for about 60 percent of total food grain production (Figure 1.2 and 1.3).

. Figure 1.2. Rice acreage by season Figure 1.3. Rice output by season

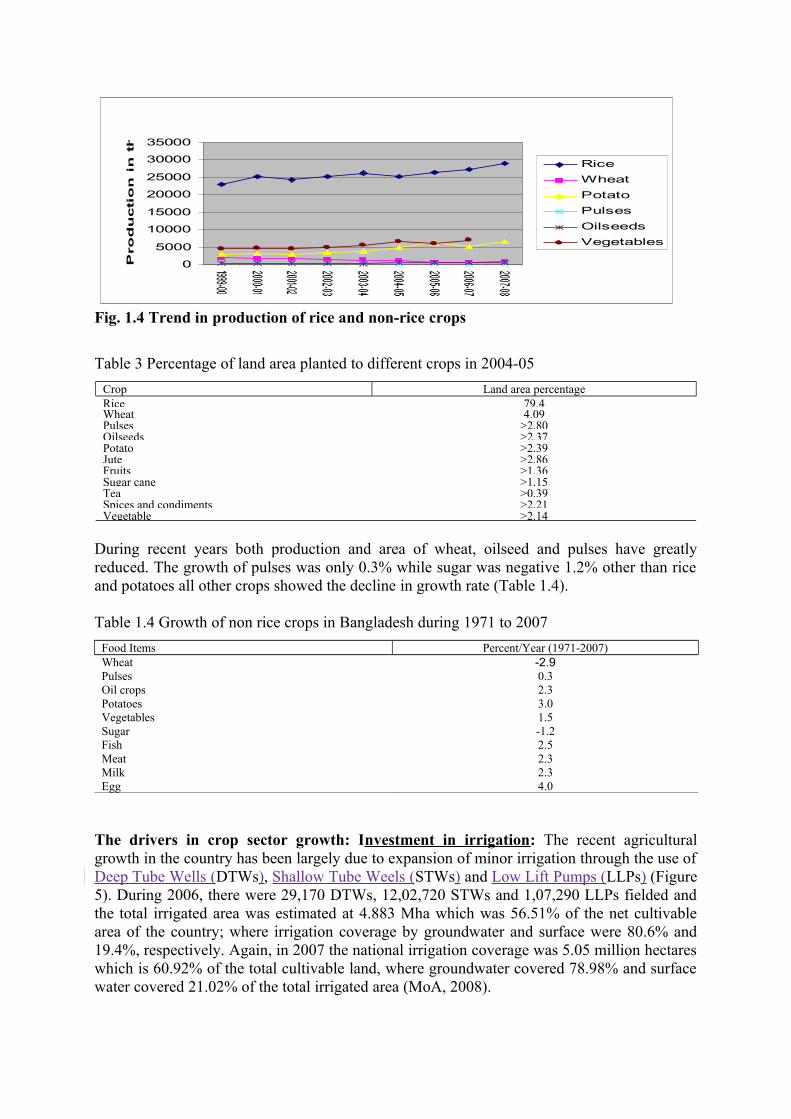

During the same period production of potato and vegetables also increased considerably (Fig 1.4). For other crops long term growth remains unsatisfactory. Usually little land is used to grow nutritionally important food crops such as vegetables, fruits, pulses and oilseeds (Table 1.3). During recent years both production and area of wheat, pulses and oilseeds have been greatly reduced.

0

5000

10000

15000

20000

25000

30000

35000P

ro

du

cti

on

in

th

ou

san

d M

t

Rice

Wheat

Potato

Pulses

Oilseeds

Vegetables

Fig. 1.4 Trend in production of rice and non-rice crops

Table 3 Percentage of land area planted to different crops in 2004-05

Crop Land area percentageRice 79.4Wheat 4.09Pulses >2.80Oilseeds >2.37Potato >2.39Jute >2.86Fruits >1.36Sugar cane >1.15Tea >0.39Spices and condiments >2.21Vegetable >2.14

During recent years both production and area of wheat, oilseed and pulses have greatly reduced. The growth of pulses was only 0.3% while sugar was negative 1.2% other than rice and potatoes all other crops showed the decline in growth rate (Table 1.4).

Table 1.4 Growth of non rice crops in Bangladesh during 1971 to 2007

Food Items Percent/Year (1971-2007)Wheat -2.9Pulses 0.3Oil crops 2.3Potatoes 3.0Vegetables 1.5Sugar -1.2Fish 2.5Meat 2.3Milk 2.3Egg 4.0

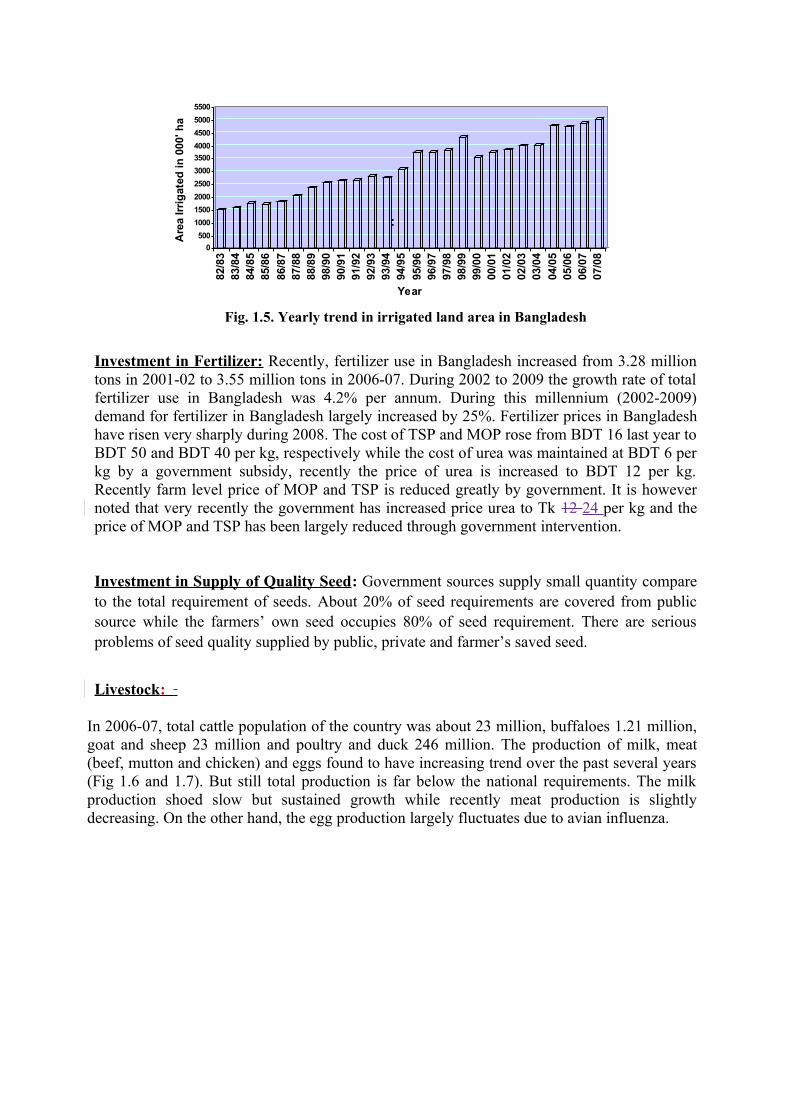

The drivers in crop sector growth: Investment in irrigation: The recent agricultural growth in the country has been largely due to expansion of minor irrigation through the use of Deep Tube Wells (DTWs), Shallow Tube Weels (STWs) and Low Lift Pumps (LLPs) (Figure 5). During 2006, there were 29,170 DTWs, 12,02,720 STWs and 1,07,290 LLPs fielded and the total irrigated area was estimated at 4.883 Mha which was 56.51% of the net cultivable area of the country; where irrigation coverage by groundwater and surface were 80.6% and 19.4%, respectively. Again, in 2007 the national irrigation coverage was 5.05 million hectares which is 60.92% of the total cultivable land, where groundwater covered 78.98% and surface water covered 21.02% of the total irrigated area (MoA, 2008).

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

Are

a Ir

rig

ated

in 0

00' h

a

82/8

383

/84

84/8

585

/86

86/8

787

/88

88/8

998

/90

90/9

191

/92

92/9

393

/94

94/9

5

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/0

202

/03

03/0

4

04/0

505

/06

06/0

707

/08

Year

Fig 1: Trend of Irrigation Growth in Bangladesh

:

Investment in Fertilizer: Recently, fertilizer use in Bangladesh increased from 3.28 million tons in 2001-02 to 3.55 million tons in 2006-07. During 2002 to 2009 the growth rate of total fertilizer use in Bangladesh was 4.2% per annum. During this millennium (2002-2009) demand for fertilizer in Bangladesh largely increased by 25%. Fertilizer prices in Bangladesh have risen very sharply during 2008. The cost of TSP and MOP rose from BDT 16 last year to BDT 50 and BDT 40 per kg, respectively while the cost of urea was maintained at BDT 6 per kg by a government subsidy, recently the price of urea is increased to BDT 12 per kg. Recently farm level price of MOP and TSP is reduced greatly by government. It is however noted that very recently the government has increased price urea to Tk 12 24 per kg and the price of MOP and TSP has been largely reduced through government intervention.

Investment in Supply of Quality Seed: Government sources supply small quantity compare to the total requirement of seeds. About 20% of seed requirements are covered from public source while the farmers’ own seed occupies 80% of seed requirement. There are serious problems of seed quality supplied by public, private and farmer’s saved seed.

Livestock :

In 2006-07, total cattle population of the country was about 23 million, buffaloes 1.21 million, goat and sheep 23 million and poultry and duck 246 million. The production of milk, meat (beef, mutton and chicken) and eggs found to have increasing trend over the past several years (Fig 1.6 and 1.7). But still total production is far below the national requirements. The milk production shoed slow but sustained growth while recently meat production is slightly decreasing. On the other hand, the egg production largely fluctuates due to avian influenza.

Fig. 1.5. Yearly trend in irrigated land area in Bangladesh

0

5

10

15

20

25

30

200

2-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007

-08

Pro

du

cti

on

(L

ac t

on

)

Milk

Meat

420004400046000480005000052000540005600058000

2002-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007-0

8

Eg

g p

rod

ucti

on

(L

ac N

um

ber)

Fig. 1.6 Trend in production of milk and meat in Bangladesh Fig. 1.7 Trend in egg production in Bangladesh

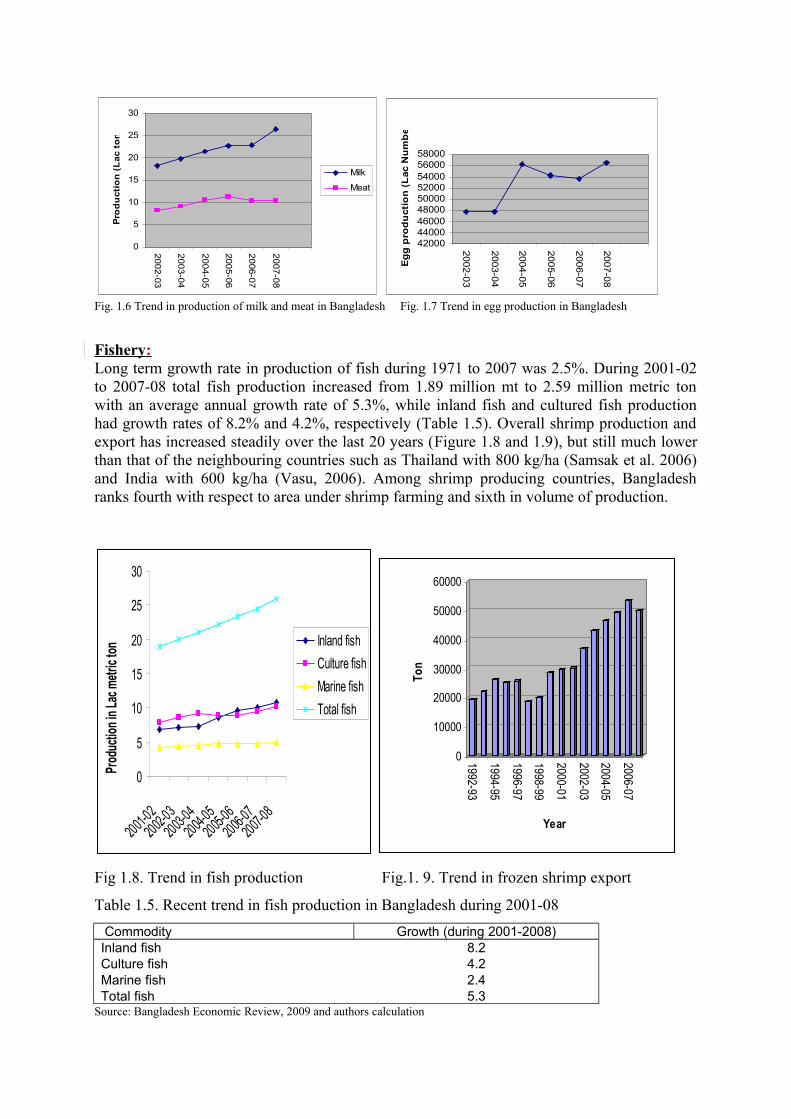

Fishery : Long term growth rate in production of fish during 1971 to 2007 was 2.5%. During 2001-02 to 2007-08 total fish production increased from 1.89 million mt to 2.59 million metric ton with an average annual growth rate of 5.3%, while inland fish and cultured fish production had growth rates of 8.2% and 4.2%, respectively (Table 1.5). Overall shrimp production and export has increased steadily over the last 20 years (Figure 1.8 and 1.9), but still much lower than that of the neighbouring countries such as Thailand with 800 kg/ha (Samsak et al. 2006) and India with 600 kg/ha (Vasu, 2006). Among shrimp producing countries, Bangladesh ranks fourth with respect to area under shrimp farming and sixth in volume of production.

0

5

10

15

20

25

30

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

Prod

uctio

n in

Lac

met

ric to

n Inland fish

Culture fish

Marine fish

Total fish

0

10000

20000

30000

40000

50000

60000

Ton

1992-93

1994-95

1996-97

1998-99

2000-01

2002-03

2004-05

2006-07

Year

Fig 1.8. Trend in fish production Fig.1. 9. Trend in frozen shrimp export

Table 1.5. Recent trend in fish production in Bangladesh during 2001-08

Commodity Growth (during 2001-2008)Inland fish 8.2Culture fish 4.2Marine fish 2.4Total fish 5.3

Source: Bangladesh Economic Review, 2009 and authors calculation

Current food security situation

About 40% of Bangladesh’s total population are calorie poor, consuming less than 2122 kcal per capita per day, while one-fifth of population are hard core poor who consume less than 1805 kcal per capita per day (BBS, 2007). Food security worsens with inter-year shortfall in food grain production caused by climatic variations and natural disaster such as floods, tidal surge and insect and pest attacks. Variations in food intake also exist between regions of the country, between adults and children and between men and women at the household level.

Household Income and Expenditure Survey 2000 shows that malnutrition is widespread among the poorest 14 percent of the rural population, who consume only about 1600 Kcal per capita per day. Another 10 percent consume between 1600 and 1800 Kcal (BBS, 2000). Bangladesh Demographic and Health Survey (2004) shows that 43 percent of children under 5 are stunted and the prevalence of stunting increases from 10 percent of children below 6 months to 51 percent of children from 48-59 months of age. The survey also shows that mothers suffer from calorie deficiency and pregnant women suffer from anaemia.

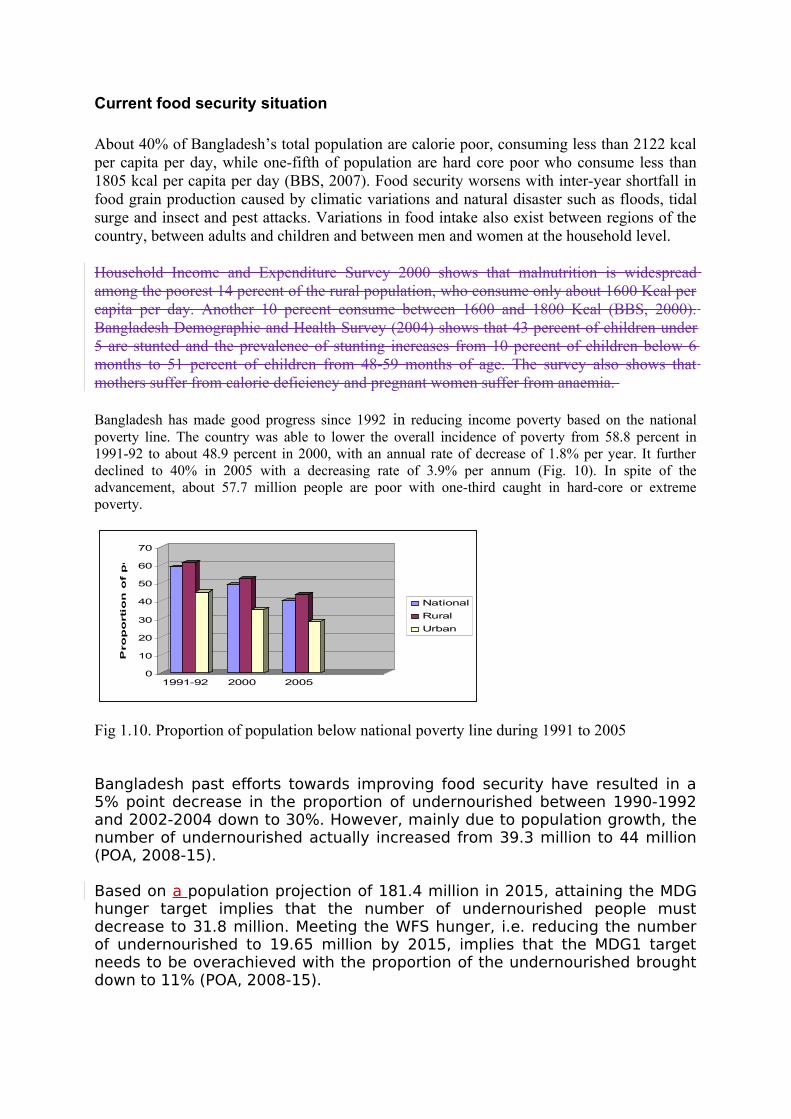

Bangladesh has made good progress since 1992 in reducing income poverty based on the national poverty line. The country was able to lower the overall incidence of poverty from 58.8 percent in 1991-92 to about 48.9 percent in 2000, with an annual rate of decrease of 1.8% per year. It further declined to 40% in 2005 with a decreasing rate of 3.9% per annum (Fig. 10). In spite of the advancement, about 57.7 million people are poor with one-third caught in hard-core or extreme poverty.

0

10

20

30

40

50

60

70

Pro

po

rti

on

of

po

pu

lati

on

1991-92 2000 2005

National

Rural

Urban

Fig 1.10. Proportion of population below national poverty line during 1991 to 2005

Bangladesh past efforts towards improving food security have resulted in a 5% point decrease in the proportion of undernourished between 1990-1992 and 2002-2004 down to 30%. However, mainly due to population growth, the number of undernourished actually increased from 39.3 million to 44 million (POA, 2008-15).

Based on a population projection of 181.4 million in 2015, attaining the MDG hunger target implies that the number of undernourished people must decrease to 31.8 million. Meeting the WFS hunger, i.e. reducing the number of undernourished to 19.65 million by 2015, implies that the MDG1 target needs to be overachieved with the proportion of the undernourished brought down to 11% (POA, 2008-15).

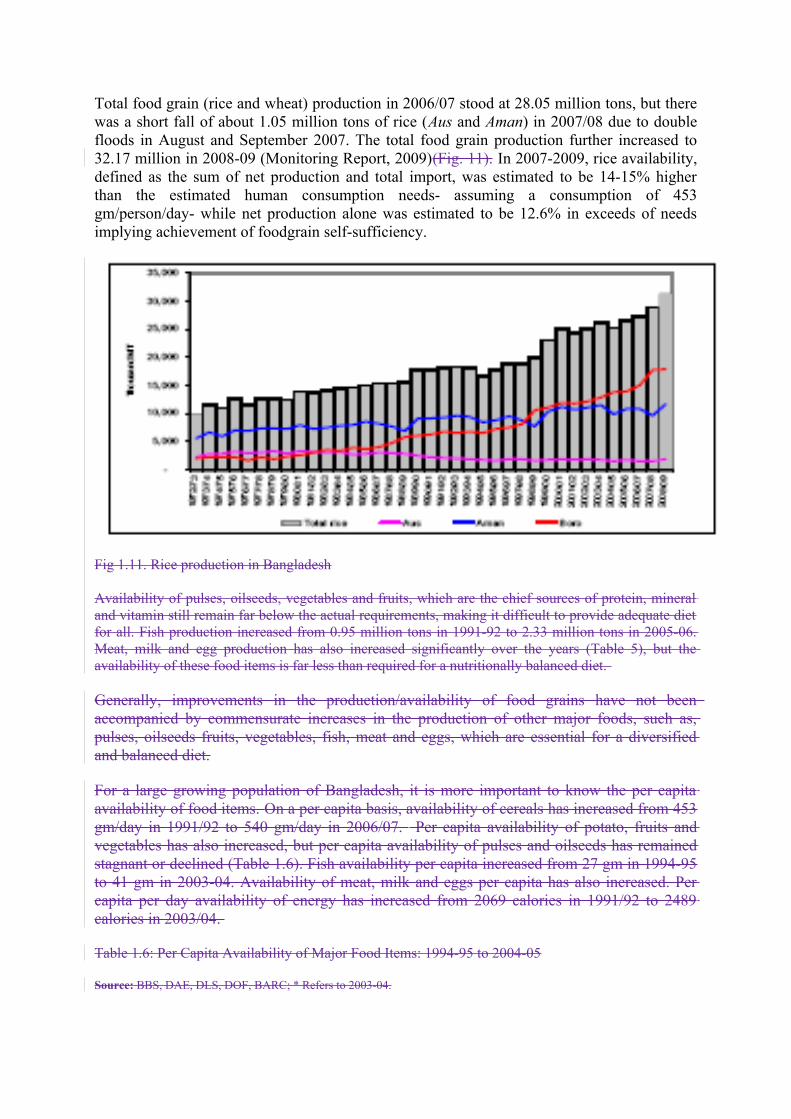

Total food grain (rice and wheat) production in 2006/07 stood at 28.05 million tons, but there was a short fall of about 1.05 million tons of rice (Aus and Aman) in 2007/08 due to double floods in August and September 2007. The total food grain production further increased to 32.17 million in 2008-09 (Monitoring Report, 2009)(Fig. 11). In 2007-2009, rice availability, defined as the sum of net production and total import, was estimated to be 14-15% higher than the estimated human consumption needs- assuming a consumption of 453 gm/person/day- while net production alone was estimated to be 12.6% in exceeds of needs implying achievement of foodgrain self-sufficiency.

Fig 1.11. Rice production in Bangladesh

Availability of pulses, oilseeds, vegetables and fruits, which are the chief sources of protein, mineral and vitamin still remain far below the actual requirements, making it difficult to provide adequate diet for all. Fish production increased from 0.95 million tons in 1991-92 to 2.33 million tons in 2005-06. Meat, milk and egg production has also increased significantly over the years (Table 5), but the availability of these food items is far less than required for a nutritionally balanced diet.

Generally, improvements in the production/availability of food grains have not been accompanied by commensurate increases in the production of other major foods, such as, pulses, oilseeds fruits, vegetables, fish, meat and eggs, which are essential for a diversified and balanced diet.

For a large growing population of Bangladesh, it is more important to know the per capita availability of food items. On a per capita basis, availability of cereals has increased from 453 gm/day in 1991/92 to 540 gm/day in 2006/07. Per capita availability of potato, fruits and vegetables has also increased, but per capita availability of pulses and oilseeds has remained stagnant or declined (Table 1.6). Fish availability per capita increased from 27 gm in 1994-95 to 41 gm in 2003-04. Availability of meat, milk and eggs per capita has also increased. Per capita per day availability of energy has increased from 2069 calories in 1991/92 to 2489 calories in 2003/04.

Table 1.6: Per Capita Availability of Major Food Items: 1994-95 to 2004-05

Source: BBS, DAE, DLS, DOF, BARC; * Refers to 2003-04.

The average Bangladeshi diet contains very high intake of cereals (74.4% of total dietary energy of 2240 kcal) with too little contents of non-cereal food items and thus an average diet is not only deficient in energy but also imbalanced and deficient in vitamins and minerals. Gaps between requirement and production of other important food crops and livestock products are wide. According to MOA estimate, deficit of pulses and oilseeds are 1.12 million tons and 2.26 million tons respectively (2004-05). Similarly, shortage of vegetables and fruits is estimated at 2.24 million tons and 2.70 million tons respectively. The national deficit of milk and meat is 10.54 million tons and 5.12 million tons respectively, and of eggs is 9253 million (DLS, 2007). The national requirement of fish is estimated at 3.0 million tons, showing a deficit of 0.67 million tons (DOF, 2007).

There is wide gap between projected cereal production and requirements for 2010-25. The implications of this projected consumption and requirements for acceleration and sustenance of cereal and non-cereal food production is that it is necessary to change in land use pattern for crop diversification, and improvement in food processing and food consumption habit. To determine the required food demand, production, import, export and caloric supply levels required in 2025 Zero Hungry level Investment assessment Project (IAP), FAO utilized the data points developed for the 2006 FAO analysis for “World Agriculture: Towards 2030/2050”. It used a IAP 2025 Zero Hunger framework. The resulting production estimates for Bangladesh are summarized in the table below (Table 2): The table indicates that Investment projections must support production increases ranging from 1.2 to 2.5 times for the most important crops and commodities in the country, with wheat and meat presenting the largest increases. It should be noted, however, that due to Bangladesh Government efforts to diversify food consumption, the required 2025ZH production of Vegetables is likely to be higher than suggested above. Additionally, recent trends are indicating that an increase in Maiz planting, which has a comparative advantage over wheat, may reduce the total contribution of wheat in 2025ZH production.

This increase of production under the 2025ZH scenario will also require considerable increase in current yields. Taking the case of rice as the major crop, rainfed yields will need to rise from the current 2.8 tonnes/ha to 3.2 tonnes/ha. While irrigated yields would move from 4.8 tonnes /ha to 6.0 tonnes /ha.

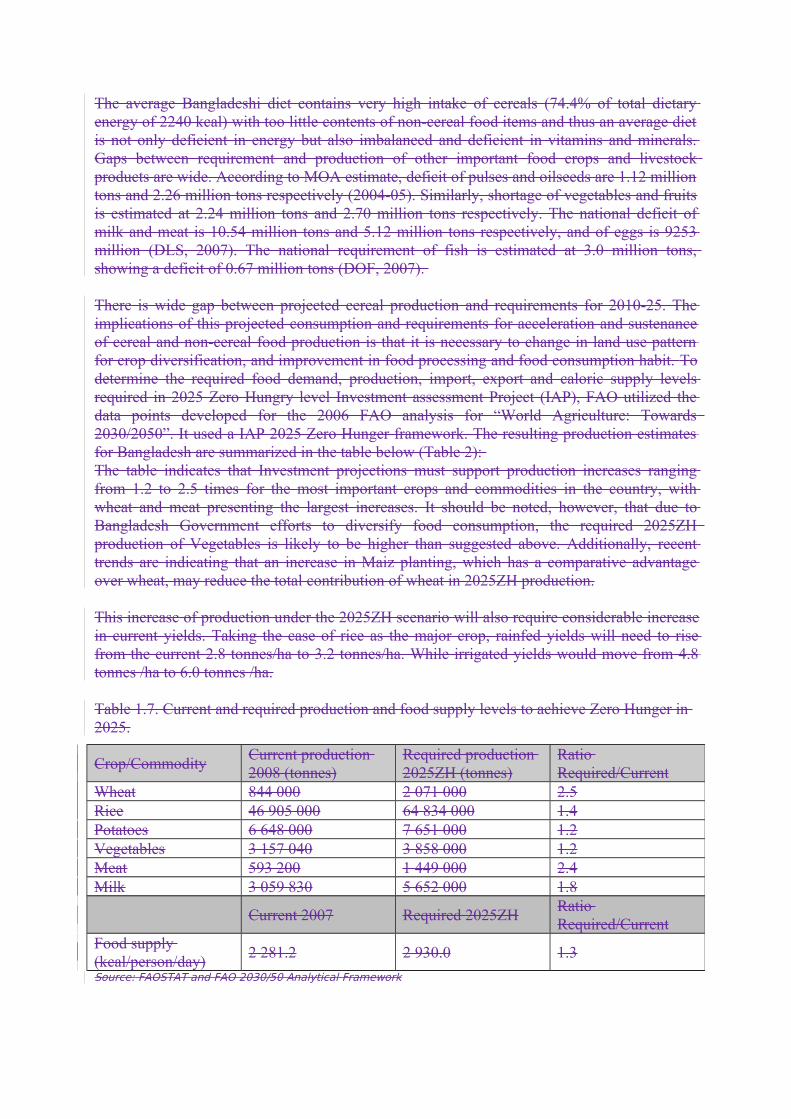

Table 1.7. Current and required production and food supply levels to achieve Zero Hunger in 2025.

Source: FAOSTAT and FAO 2030/50 Analytical Framework

Crop/CommodityCurrent production 2008 (tonnes)

Required production 2025ZH (tonnes)

Ratio Required/Current

Wheat 844 000 2 071 000 2.5Rice 46 905 000 64 834 000 1.4Potatoes 6 648 000 7 651 000 1.2Vegetables 3 157 040 3 858 000 1.2Meat 593 200 1 449 000 2.4Milk 3 059 830 5 652 000 1.8

Current 2007 Required 2025ZHRatio Required/Current

Food supply (kcal/person/day)

2 281.2 2 930.0 1.3

2. Growth Experiences in Bangladesh

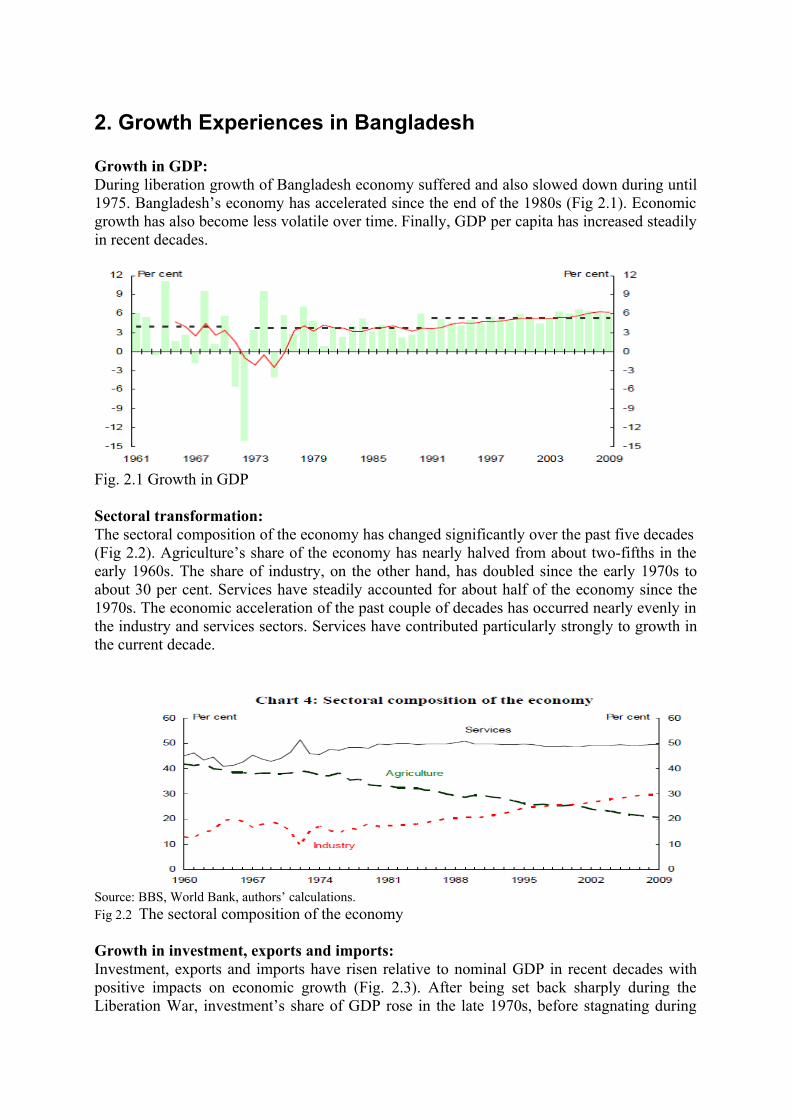

Growth in GDP:During liberation growth of Bangladesh economy suffered and also slowed down during until 1975. Bangladesh’s economy has accelerated since the end of the 1980s (Fig 2.1). Economic growth has also become less volatile over time. Finally, GDP per capita has increased steadily in recent decades.

Fig. 2.1 Growth in GDP

Sectoral transformation:The sectoral composition of the economy has changed significantly over the past five decades(Fig 2.2). Agriculture’s share of the economy has nearly halved from about two-fifths in the early 1960s. The share of industry, on the other hand, has doubled since the early 1970s to about 30 per cent. Services have steadily accounted for about half of the economy since the 1970s. The economic acceleration of the past couple of decades has occurred nearly evenly in the industry and services sectors. Services have contributed particularly strongly to growth in the current decade.

Source: BBS, World Bank, authors’ calculations.Fig 2.2 The sectoral composition of the economy

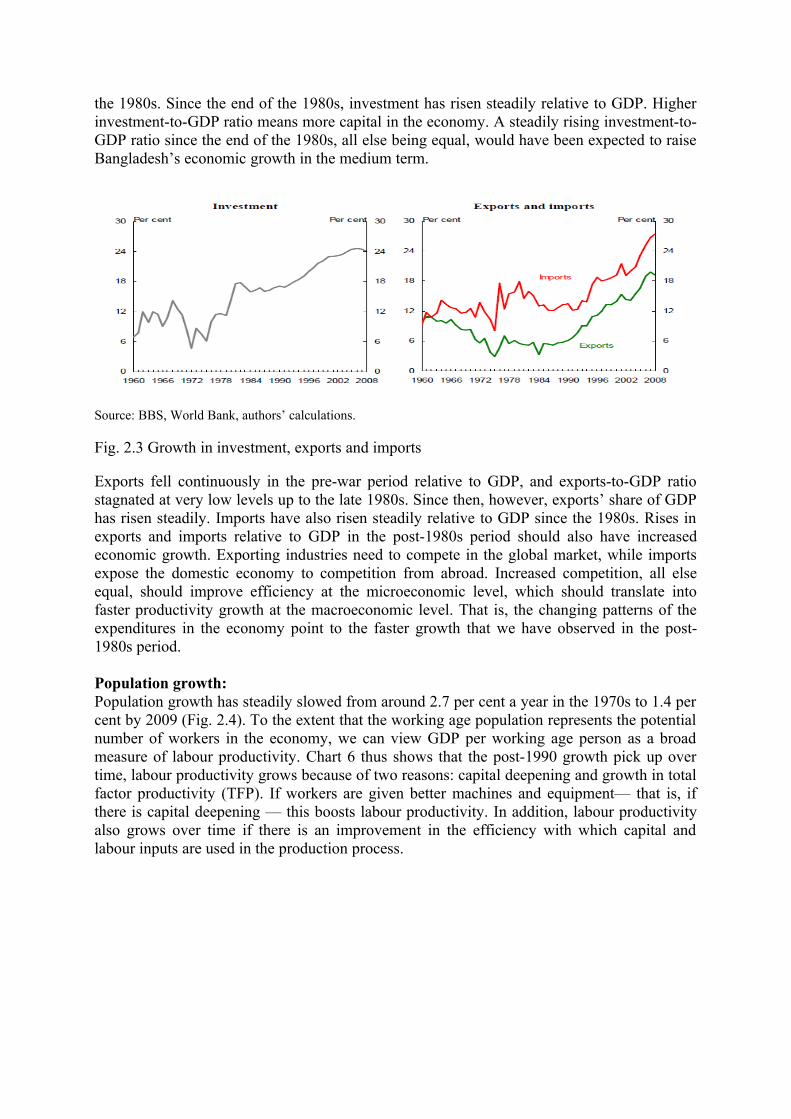

Growth in investment, exports and imports:Investment, exports and imports have risen relative to nominal GDP in recent decades with positive impacts on economic growth (Fig. 2.3). After being set back sharply during the Liberation War, investment’s share of GDP rose in the late 1970s, before stagnating during

the 1980s. Since the end of the 1980s, investment has risen steadily relative to GDP. Higher investment-to-GDP ratio means more capital in the economy. A steadily rising investment-to-GDP ratio since the end of the 1980s, all else being equal, would have been expected to raise Bangladesh’s economic growth in the medium term.

Source: BBS, World Bank, authors’ calculations.

Fig. 2.3 Growth in investment, exports and imports

Exports fell continuously in the pre-war period relative to GDP, and exports-to-GDP ratio stagnated at very low levels up to the late 1980s. Since then, however, exports’ share of GDP has risen steadily. Imports have also risen steadily relative to GDP since the 1980s. Rises in exports and imports relative to GDP in the post-1980s period should also have increased economic growth. Exporting industries need to compete in the global market, while imports expose the domestic economy to competition from abroad. Increased competition, all else equal, should improve efficiency at the microeconomic level, which should translate into faster productivity growth at the macroeconomic level. That is, the changing patterns of the expenditures in the economy point to the faster growth that we have observed in the post-1980s period.

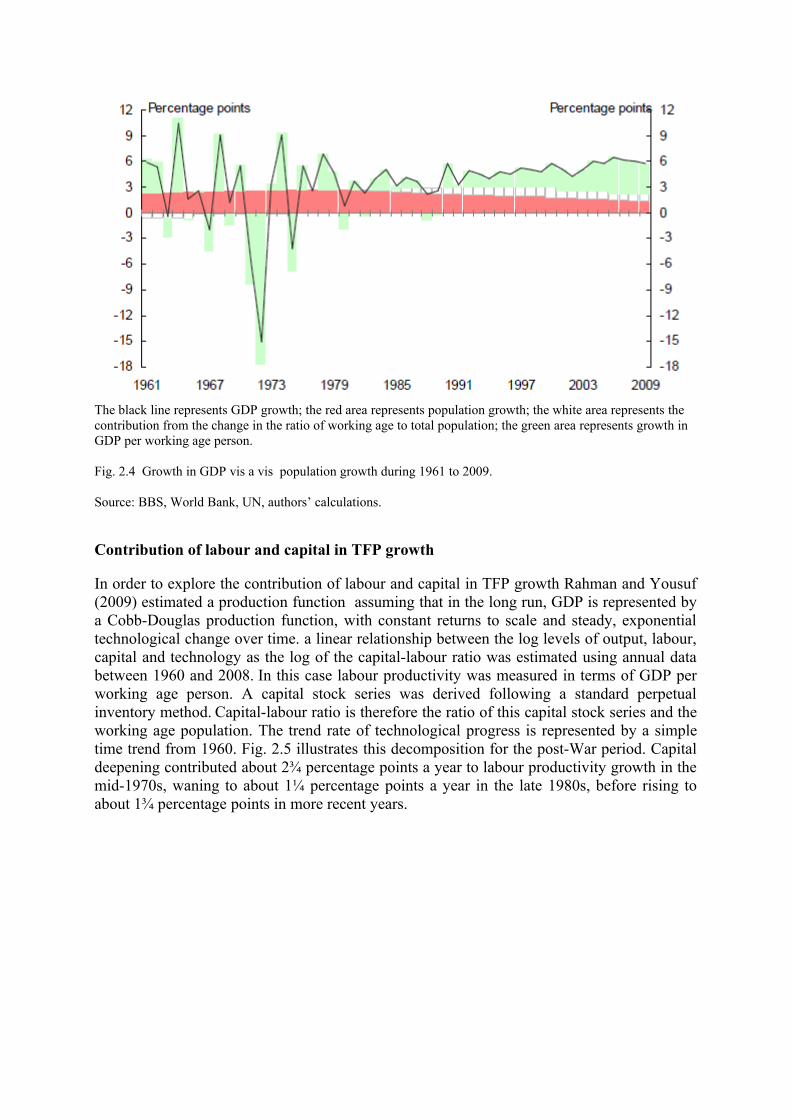

Population growth:Population growth has steadily slowed from around 2.7 per cent a year in the 1970s to 1.4 per cent by 2009 (Fig. 2.4). To the extent that the working age population represents the potential number of workers in the economy, we can view GDP per working age person as a broad measure of labour productivity. Chart 6 thus shows that the post-1990 growth pick up over time, labour productivity grows because of two reasons: capital deepening and growth in total factor productivity (TFP). If workers are given better machines and equipment— that is, if there is capital deepening — this boosts labour productivity. In addition, labour productivity also grows over time if there is an improvement in the efficiency with which capital and labour inputs are used in the production process.

The black line represents GDP growth; the red area represents population growth; the white area represents thecontribution from the change in the ratio of working age to total population; the green area represents growth inGDP per working age person.

Fig. 2.4 Growth in GDP vis a vis population growth during 1961 to 2009.

Source: BBS, World Bank, UN, authors’ calculations.

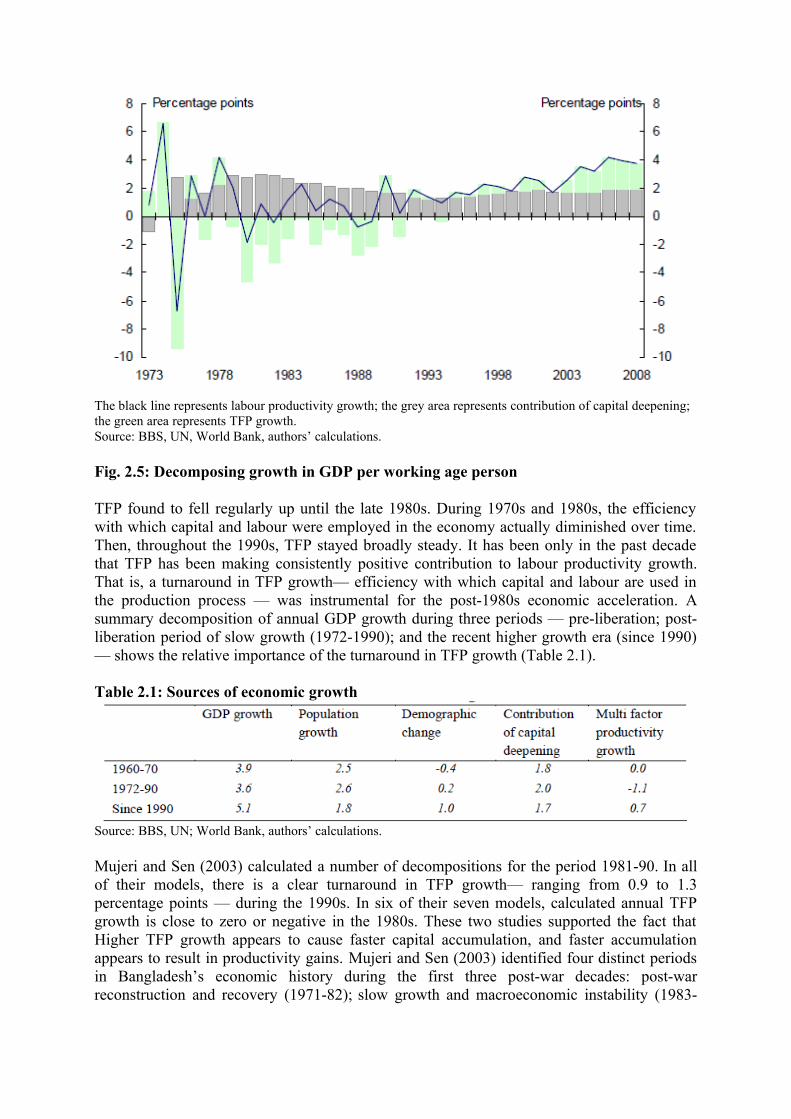

Contribution of labour and capital in TFP growth

In order to explore the contribution of labour and capital in TFP growth Rahman and Yousuf (2009) estimated a production function assuming that in the long run, GDP is represented by a Cobb-Douglas production function, with constant returns to scale and steady, exponential technological change over time. a linear relationship between the log levels of output, labour, capital and technology as the log of the capital-labour ratio was estimated using annual data between 1960 and 2008. In this case labour productivity was measured in terms of GDP per working age person. A capital stock series was derived following a standard perpetual inventory method. Capital-labour ratio is therefore the ratio of this capital stock series and the working age population. The trend rate of technological progress is represented by a simple time trend from 1960. Fig. 2.5 illustrates this decomposition for the post-War period. Capital deepening contributed about 2¾ percentage points a year to labour productivity growth in the mid-1970s, waning to about 1¼ percentage points a year in the late 1980s, before rising to about 1¾ percentage points in more recent years.

The black line represents labour productivity growth; the grey area represents contribution of capital deepening;the green area represents TFP growth.Source: BBS, UN, World Bank, authors’ calculations.

Fig. 2.5: Decomposing growth in GDP per working age person

TFP found to fell regularly up until the late 1980s. During 1970s and 1980s, the efficiency with which capital and labour were employed in the economy actually diminished over time. Then, throughout the 1990s, TFP stayed broadly steady. It has been only in the past decade that TFP has been making consistently positive contribution to labour productivity growth. That is, a turnaround in TFP growth— efficiency with which capital and labour are used in the production process — was instrumental for the post-1980s economic acceleration. A summary decomposition of annual GDP growth during three periods — pre-liberation; post-liberation period of slow growth (1972-1990); and the recent higher growth era (since 1990) — shows the relative importance of the turnaround in TFP growth (Table 2.1).

Table 2.1: Sources of economic growth

Source: BBS, UN; World Bank, authors’ calculations.

Mujeri and Sen (2003) calculated a number of decompositions for the period 1981-90. In all of their models, there is a clear turnaround in TFP growth— ranging from 0.9 to 1.3 percentage points — during the 1990s. In six of their seven models, calculated annual TFP growth is close to zero or negative in the 1980s. These two studies supported the fact that Higher TFP growth appears to cause faster capital accumulation, and faster accumulation appears to result in productivity gains. Mujeri and Sen (2003) identified four distinct periods in Bangladesh’s economic history during the first three post-war decades: post-war reconstruction and recovery (1971-82); slow growth and macroeconomic instability (1983-

89); crisis-driven reforms (1990-93); and stronger economic growth and social development (1994-2000).

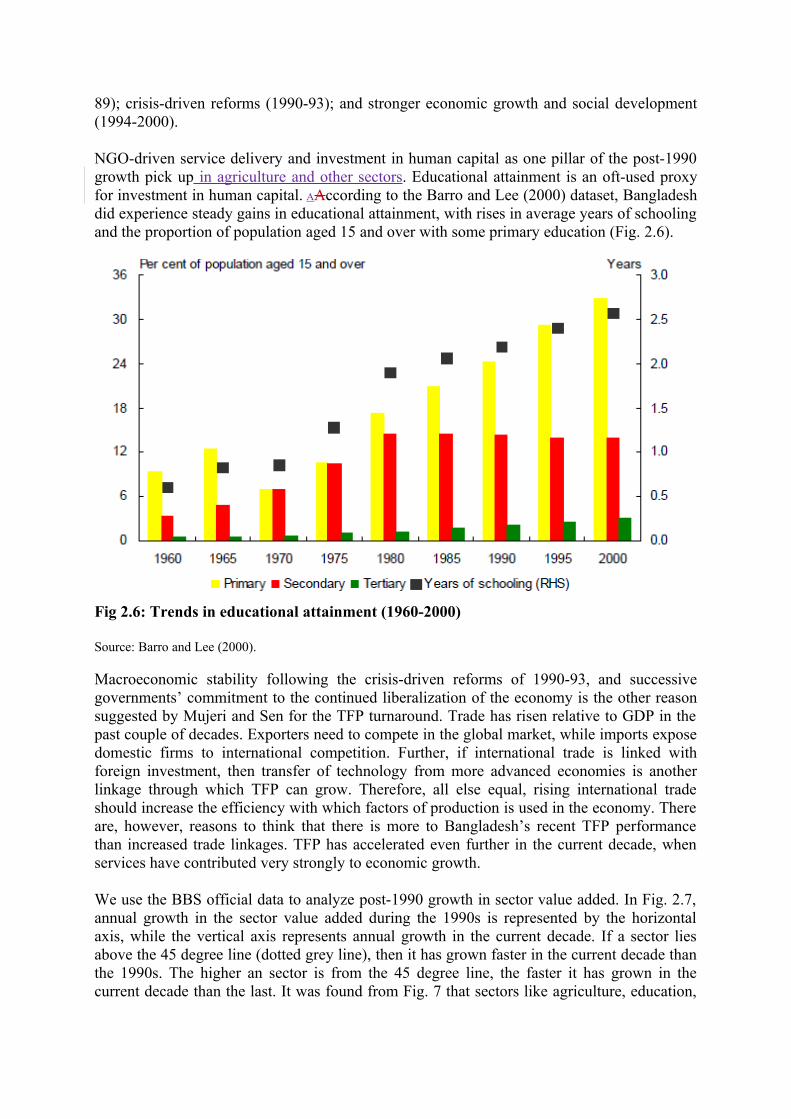

NGO-driven service delivery and investment in human capital as one pillar of the post-1990 growth pick up in agriculture and other sectors. Educational attainment is an oft-used proxy for investment in human capital. AAccording to the Barro and Lee (2000) dataset, Bangladesh did experience steady gains in educational attainment, with rises in average years of schooling and the proportion of population aged 15 and over with some primary education (Fig. 2.6).

Fig 2.6: Trends in educational attainment (1960-2000)

Source: Barro and Lee (2000).

Macroeconomic stability following the crisis-driven reforms of 1990-93, and successive governments’ commitment to the continued liberalization of the economy is the other reason suggested by Mujeri and Sen for the TFP turnaround. Trade has risen relative to GDP in the past couple of decades. Exporters need to compete in the global market, while imports expose domestic firms to international competition. Further, if international trade is linked with foreign investment, then transfer of technology from more advanced economies is another linkage through which TFP can grow. Therefore, all else equal, rising international trade should increase the efficiency with which factors of production is used in the economy. There are, however, reasons to think that there is more to Bangladesh’s recent TFP performance than increased trade linkages. TFP has accelerated even further in the current decade, when services have contributed very strongly to economic growth.

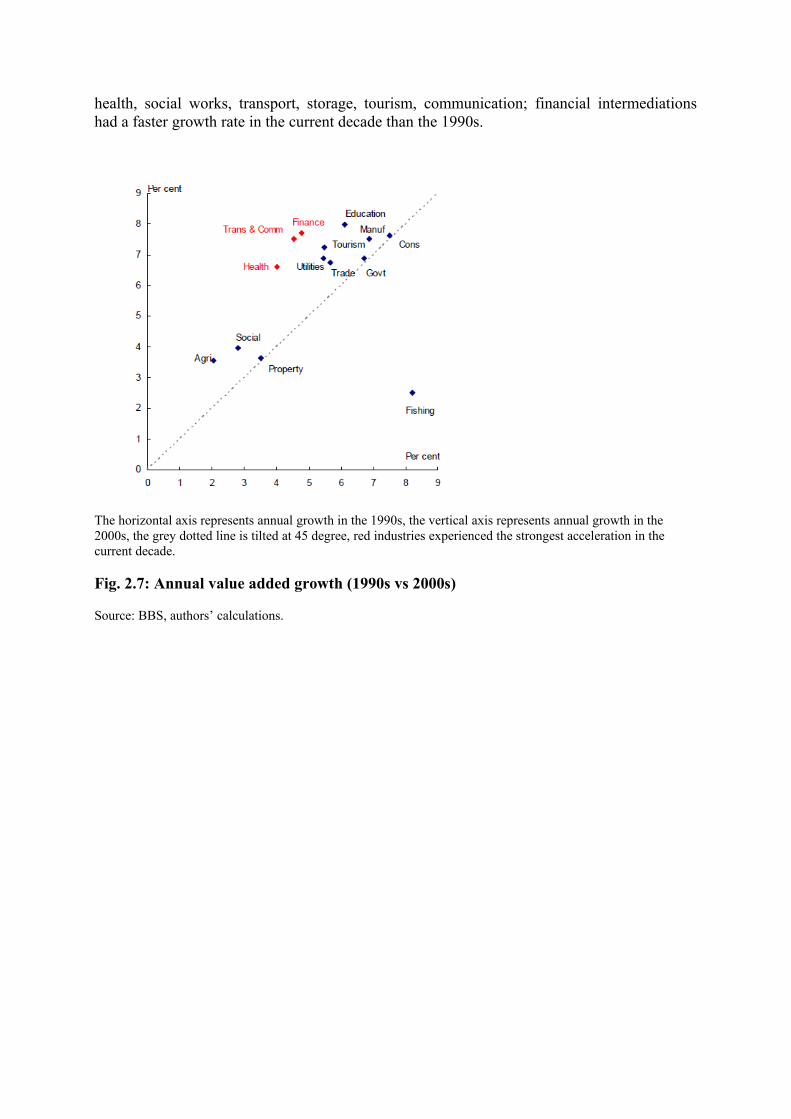

We use the BBS official data to analyze post-1990 growth in sector value added. In Fig. 2.7, annual growth in the sector value added during the 1990s is represented by the horizontal axis, while the vertical axis represents annual growth in the current decade. If a sector lies above the 45 degree line (dotted grey line), then it has grown faster in the current decade than the 1990s. The higher an sector is from the 45 degree line, the faster it has grown in the current decade than the last. It was found from Fig. 7 that sectors like agriculture, education,

health, social works, transport, storage, tourism, communication; financial intermediations had a faster growth rate in the current decade than the 1990s.

The horizontal axis represents annual growth in the 1990s, the vertical axis represents annual growth in the2000s, the grey dotted line is tilted at 45 degree, red industries experienced the strongest acceleration in thecurrent decade.

Fig. 2.7: Annual value added growth (1990s vs 2000s)

Source: BBS, authors’ calculations.

Chapter 3

Public policies promoting the formation of human capital in the rural sector

Government Policy and Interventions

Education receives the highest allocation of resources in the Bangladeshi social sector. Primary education has been a priority in Bangladeshi politics since independence in 1971: basic measures to implement universal primary education were taken from the outset. The Bangladesh government has a success story in that its education programs dramatically improved in the 1990s, especially during the latter half of the decade. The 90s saw a rekindled dedication for interventions off primary education, and as a consequence the Bangladeshi primary education system experienced significant enhancement during this period. A large part of this renewed commitment was a direct result of the 1990 World Conference on Education for All (WCEFA), which encouraged all participating nations to expand their vision to meet goals in the education sector, especially the goal of making primary education universal. Following this conference, donors in Bangladesh invested in the education sector much more heavily and NGOs increased their involvement in assisting the Bangladeshi government in meeting its primary education goals.

The Government of Bangladesh itself took many initiatives in the years following the WCEFA, including: the 1993 Compulsory Primary Education Act, which made the five-year primary education program free in all government schools and declared education for girls in rural areas free through grade eight; the establishment of the ministry for Primary and Mass Education in 1992, which set as its objective the universalization of primary education as well as the elimination of the gender- and poverty-gaps; demand-side interventions such as the Female Stipend program, the Food for Education (FFE) program; and most recently the Primary Education Development Program (PEDP II), a six-year program beginning in the year 2000 which aims to increase access, quality and efficiency across the board in the primary education sector. These measures have resulted in impressive gains in the achievement of Bangladesh’s primary education goals. Nationwide enrollment rates have sharply increased both in rural and urban areas, dropout rates have gone down, significant progress has been made in raising equality of access between different geographic and socioeconomic groups both in rural and rural areas, and the gender gap has literally been removed at the primary level. Girls have actually overtaken boys in rates of enrollment, completion, and attendance in primary schools (Kabeer et al, 292).

The Government’s Food-for-Work Program and the stipend scheme for girls up to grade 8 are some of the important factors behind the rise in enrollment of girls at the primary level in rural areas. To achieve a 100 percent literacy rate by the year 2005, the Government has also started a massive total literacy movement. Various program and policy measures have been undertaken to increase enrollment and arrest dropout rates, especially for girls. Adult education for rural women has also been

emphasized. There is also provision for increasing teachers’ training of women for both the primary and secondary levels. Non-formal education programs run by Bangladeshi NGOs such as the Bangladesh Rural Advancement Committee have been internationally acclaimed. Some large NGOs run thousands of schools providing education to children in rural areas who are not able to avail of Government-sponsored education. The Government has recognized this contribution of NGOs and there is significant collaboration between them. There is a special emphasis on girls’ education as education and the eradication of illiteracy are considered to be the first steps toward the empowerment of women.

Bangladesh’s achievements in education over the last two decades have been impressive, especially when seen against the backdrop of the performance of other countries in the region. Major successes include (a) rapid expansion of primary education – the gross primary enrolment increased from 72 per cent in 1990 to 91 per cent in 2000 (b) a narrowing of disparity between rural and urban primary enrolment and (c) the closing of the gender gap, including the very poor. Moreover, enrolment in secondary education expanded at an annual rate of 10 per cent during the 1993-99 period. Gender and urban rural parity in Bangladesh are comparable to that in Sri Lanka. Roughly 9 out of every 10 children eventually enroll in primary school, and Bangladesh has achieved levels of primary and secondary gross enrolment similar to those in countries with higher per capita income, such as Vietnam, Thailand and Indonesia (BIDS 2001; GoB 2003; World Bank 2002; World Bank 2003).

What explains this success in accumulating favourable social conditions for pro-poor growth at a relatively low level of income? One important factor of political commitment to social development has been reflected in the policy consistency that cut across the regime types since the Independence. Successive governments emphasized the need for reducing population growth, the importance of investing in primary and girl’s education, the role of primary health care in the forms of child and maternal immunization, and universal coverage of safe drinking water. Perhaps the agony of governing a state in the context of highest population density in the world and least amount of natural resources sustained this commitment to basic population, health and education—a concern widely shared in popular imagination in Bangladesh, igniting actions and adoption behaviour conducive to technological change.

Policy reforms affecting formation of human capital

For analytical purposes, the development of human capital and growth-history of Bangladesh may conveniently be divided into four distinct phases using the policy-based periodization. The first period, covering the period until 1981/82, may be termed as the period of ‘reconstruction and recovery amidst political turbulence’ during which the country achieved the pre-independence level of per capita GNP as well as other macroeconomic ratios relative to GDP, such as gross savings and investment. The subsequent period of the 1980s (until 1988/89) was the period of ‘slow economic growth with growing macroeconomic instability’. The slow growth of the

period, however, became increasingly unsustainable and the ensuing macroeconomic crisis led to the compulsion for undertaking a range of stabilization measures. Although the reform measures in Bangladesh signalled a qualitatively new phase of development. This transitional period, covering 1989/90 to 1992/93, may be considered as the period of ‘crisis-driven economic reforms and formation of favourable initial condition state’ both in terms of improved economic fundamentals and attaining a ‘threshold level’ of human and other forms of capital. With the necessary conditions for graduating into a higher level of economic growth in place, the subsequent period since 1993/94 exhibited much improved performance both in terms of economic growth and the pace of social development. Accordingly, the period may be characterized as the period of ‘higher economic growth and faster social development’. The better performance of the last period may be viewed as the outcome of the interactions between the improved ‘initial condition state’ and the policy and institutional changes during the 1990s toward more market-responsive and democratic policy regimes. The 1990s witnessed a more facilitating macroeconomic environment and achieved higher economic growth.

The period of the 1990s, which may be termed as an era of higher economic growth and faster social development, provides a potentially instructive story of development with a key message: higher human and social development outcomes can be achieved even at relatively low levels of per capita income. Several features of the period are noteworthy: (i) favourable macroeconomic fundamentals; (ii) continued emphasis on the private sector as the engine of economic growth; (iii) liberalization and outward orientation; (iv) emphasis on agriculture and rural development; (v) reduced income poverty and child malnutrition; (vi) impressive success in human development; (vii) strong emphasis on NGOs in social and economic development; (viii) enhanced disaster management capacity; (ix) continued political confrontation and uncertainties; and (x) continued deterioration of governance, especially law and order situation. In short, building on favourable conditions and pursuing more prudent policies, the period achieved higher economic growth accompanied by faster improvement in social indicators.

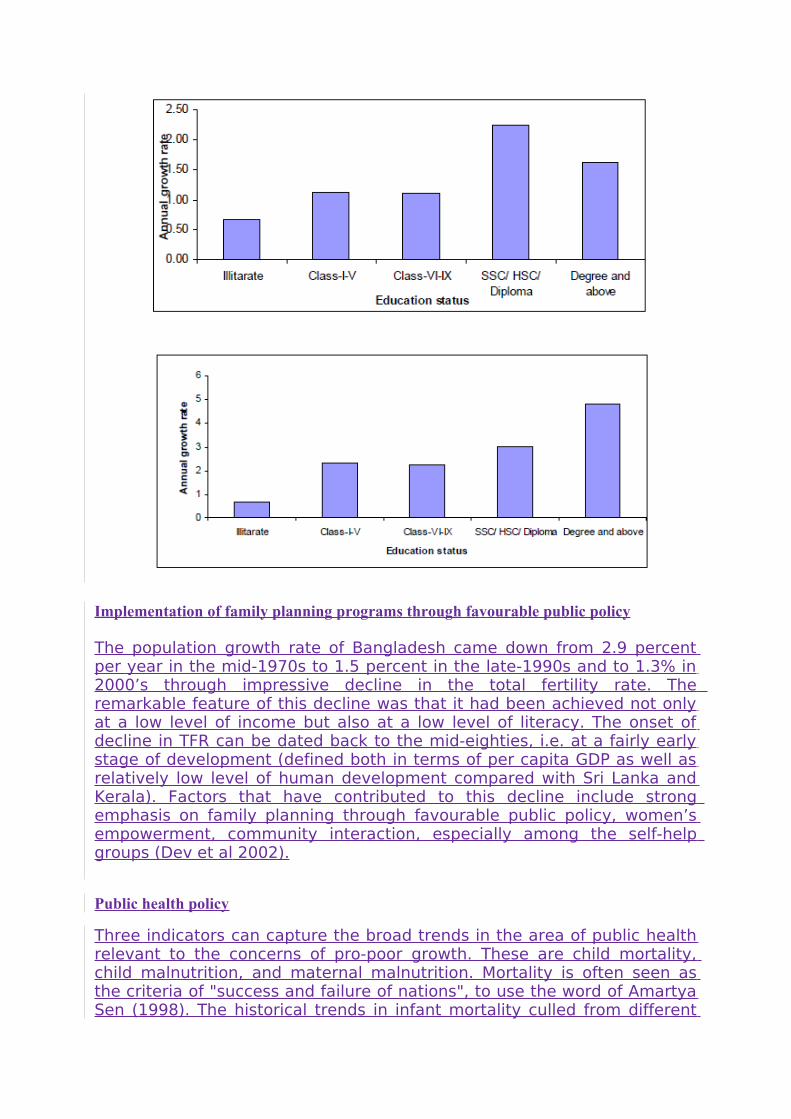

Chart #: Comparative Growth Rate by Education of Household Head, Rural: 1991/92-2000

Implementation of family planning programs through favourable public policy

The population growth rate of Bangladesh came down from 2.9 percent per year in the mid-1970s to 1.5 percent in the late-1990s and to 1.3% in 2000’s through impressive decline in the total fertility rate. The remarkable feature of this decline was that it had been achieved not only at a low level of income but also at a low level of literacy. The onset of decline in TFR can be dated back to the mid-eighties, i.e. at a fairly early stage of development (defined both in terms of per capita GDP as well as relatively low level of human development compared with Sri Lanka and Kerala). Factors that have contributed to this decline include strong emphasis on family planning through favourable public policy, women’s empowerment, community interaction, especially among the self-help groups (Dev et al 2002).

Public health policy

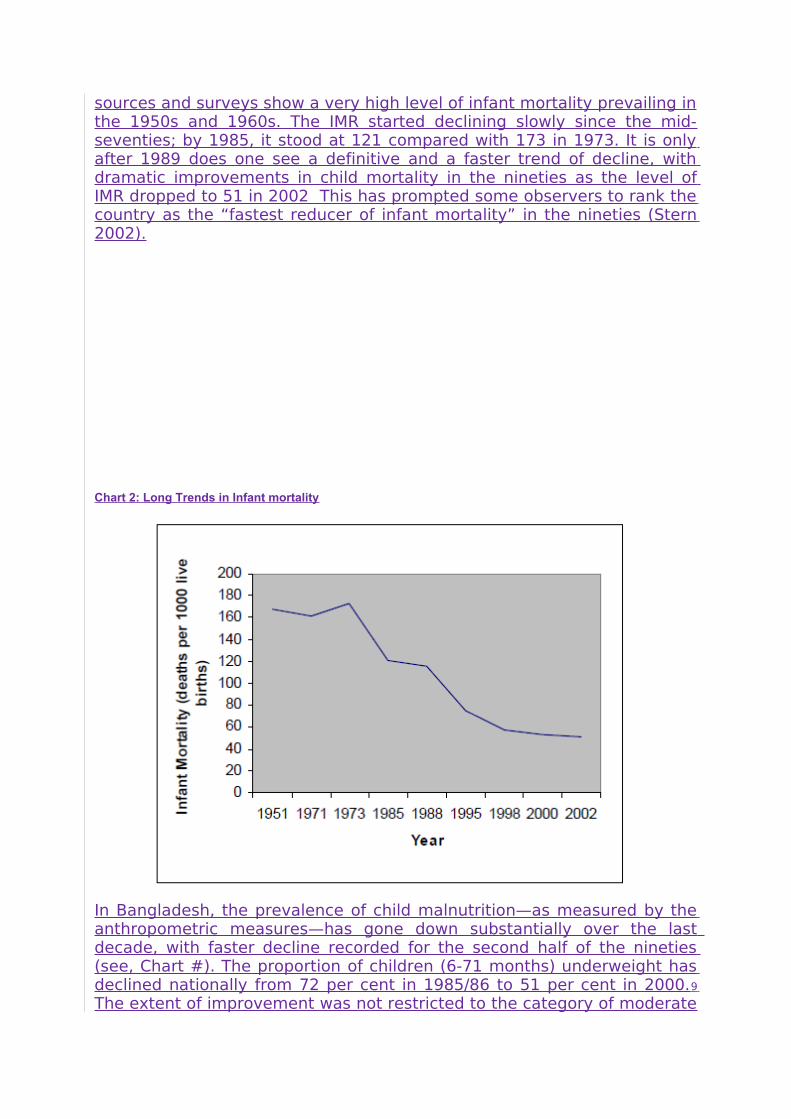

Three indicators can capture the broad trends in the area of public health relevant to the concerns of pro-poor growth. These are child mortality, child malnutrition, and maternal malnutrition. Mortality is often seen as the criteria of "success and failure of nations", to use the word of Amartya Sen (1998). The historical trends in infant mortality culled from different

sources and surveys show a very high level of infant mortality prevailing in the 1950s and 1960s. The IMR started declining slowly since the mid-seventies; by 1985, it stood at 121 compared with 173 in 1973. It is only after 1989 does one see a definitive and a faster trend of decline, with dramatic improvements in child mortality in the nineties as the level of IMR dropped to 51 in 2002 This has prompted some observers to rank the country as the “fastest reducer of infant mortality” in the nineties (Stern 2002).

Chart 2: Long Trends in Infant mortality

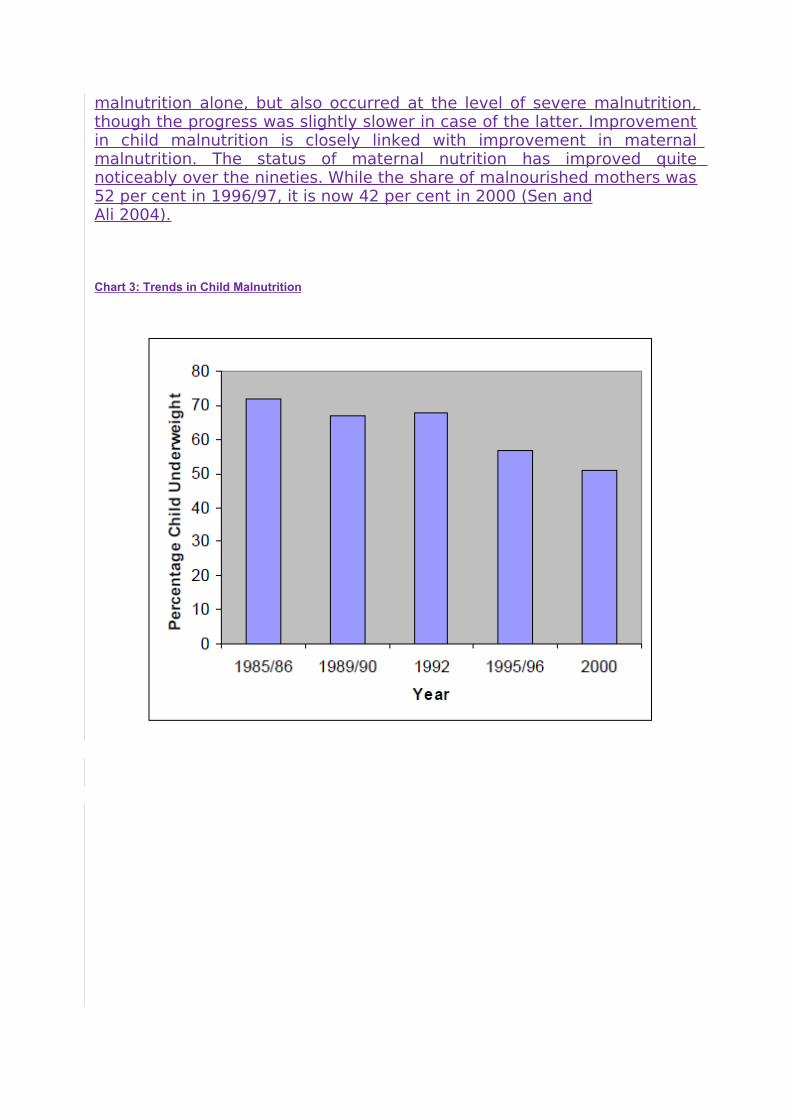

In Bangladesh, the prevalence of child malnutrition—as measured by the anthropometric measures—has gone down substantially over the last decade, with faster decline recorded for the second half of the nineties (see, Chart #). The proportion of children (6-71 months) underweight has declined nationally from 72 per cent in 1985/86 to 51 per cent in 2000.9

The extent of improvement was not restricted to the category of moderate

malnutrition alone, but also occurred at the level of severe malnutrition, though the progress was slightly slower in case of the latter. Improvement in child malnutrition is closely linked with improvement in maternal malnutrition. The status of maternal nutrition has improved quite noticeably over the nineties. While the share of malnourished mothers was 52 per cent in 1996/97, it is now 42 per cent in 2000 (Sen andAli 2004).

Chart 3: Trends in Child Malnutrition

Chapter 4

Training programs provided by additional sectors for improving farmers´ abilities and skills

1. KATALYST’s intervention

KATALYST, which started in 2002, is supported by DFID, SDC and SIDA. It is implemented by Swisscontact and GTZ International Services and partners with the Ministry of Commerce. KATALYST is currently promoting more than 25 sectors and markets comprised of services such as accounting, marketing and quality management services; manufacturing sectors such as plastics, furniture, private health care and agro-tools & machineries to agricultural sectors like pond fishery, vegetables, maize and poultry. It also works with business associations to improve the enabling environment for businesses. The project has nationwide activities but has a special focus on areas in and around Dhaka, Faridpur, Rajshahi, Rangpur, Bogra and Jessore.

This section describes KATALYST’s experience with one intervention in the vegetable sector in Rangpur. The project undertakes other activities in the sector – notably in relation to soil testing and packaging. However, KATALYST’s work in stimulating training of agricultural input retailers and the flow of knowledge and information within the distribution system is especially interesting and has wider implications for other development organizations.

The performance of Bangladesh’s important vegetable sector is undermined by very low productivity. Early evidence from this 2-year pilot project in Rangpur suggests that improving knowledge and information services embedded within the supply chain offers one means of addressing this problem. Focusing on training retailers of agricultural inputs, the results from the project - instigated by KATALYST in collaboration with Syngenta, an input supplier - hold the promise of improvements in the competitiveness and poverty reducing benefits of the sector.

The analysis of main sources of information to the poor vegetable farmers

Rangpur, located in the north of Bangladesh, is predominately rural, one of the country’s poorest regions. Within Rangpur, the vegetable sector represents a logical focus for KATALYST for different reasons. First, the vegetable sector is important in terms of size. Vegetables are estimated to contribute 3.68% to the economy nationally and more than this in Rangpur. Out of Rangpur’s 1.6m rural households 60% are estimated to be engaged in vegetable cultivation and a further 50,000 people are estimated to be employed downstream in the industry in trading, distribution and packing. Second, it is growing. A number of factors have combined to generate per annum volume growth of 5-6% in Bangladesh, faster than agriculture as a whole.

For women in particular, vegetables is an important sector. While women are rarely involved in buying inputs (such as seeds and fertilizers), homestead production is undertaken primarily by them and there has been a recent marked increase in female employment in vegetable

cultivation. Anecdotally, women’s wage rates in vegetables are closer to men’s than in other spheres of employment.

A weak productivity performance is a problem for the Rangpur and Bangladesh economies as a whole. Although regional trade in vegetables is currently limited, it is growing. If productivity is not addressed, Bangladesh – as in other sectors – will have to rely on low labour costs to be competitive. More generally, the potential for wider economic growth from efficient food production cannot be realized without productivity growth. But for the poor in particular, low productivity is a barrier to their development. As consumers, it ensures that prices are relatively high; as producers, it prevents them from getting the most from their own resources and as labourers it is likely to mean less opportunity to increase earnings. Other problems, of course, do impinge on the sector. For example, although there appear to be few major regulatory constraints, there is a general absence of formal standards relating to seeds and other inputs. The structure of different value chains linking farmers to the ultimate consumer market limits farmers’ access to appropriate information and concentrates power in key traders and other intermediaries.

The general problem of low productivity is related with low levels of knowledge and information among farmers about good vegetable farming practices. There is broad consensus in the sector that farming practices – especially in this still new activity for many farmers - are deficient with regard to, for example, use of inputs (where dosage rates are commonly incorrect), planting techniques, and recognition and treatment of problems. For KATALYST, therefore, it was vital to address the knowledge and information issue at the heart of the productivity malaise.

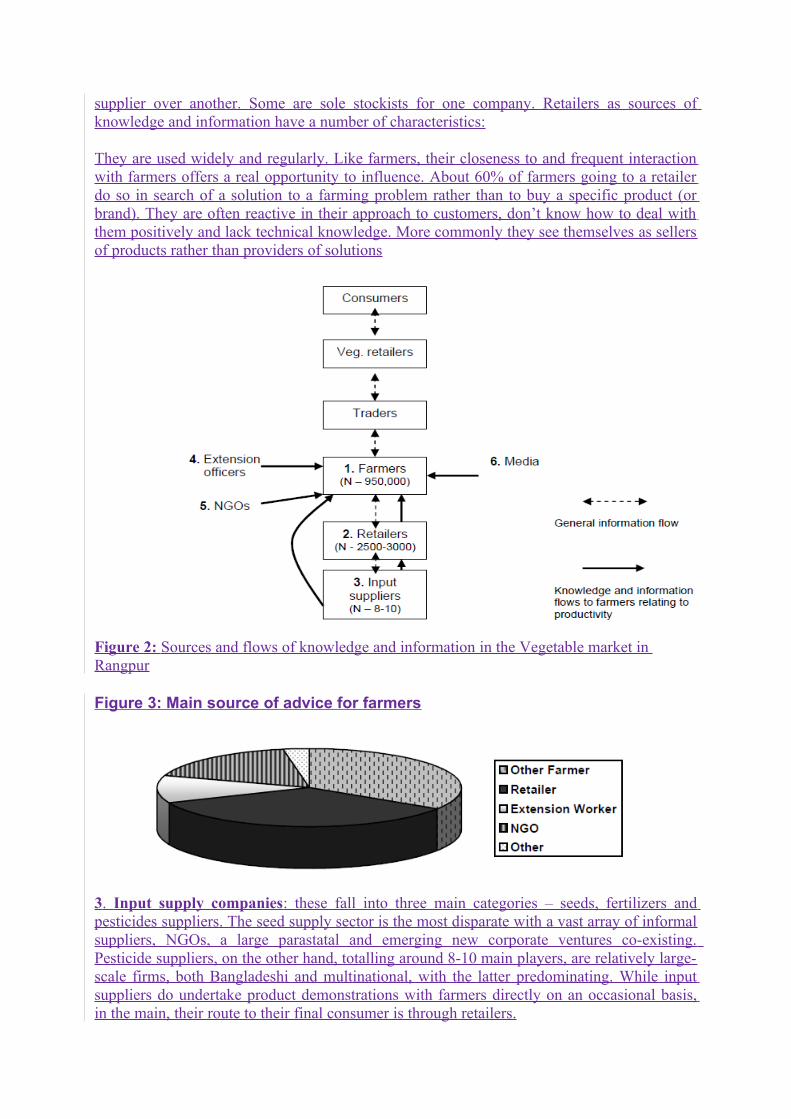

Recognition of the importance of knowledge and information in enhancing productivity prompted another question for KATALYST: why wasn’t the wider market system providing a solution to weak knowledge and information? Why were existing knowledge and information services not addressing the wider productivity problem in the vegetable sector? KATALYST’s intervention had to be shaped by answers to these questions – by an understanding of the underlying systemic constraints impinging on the supply and demand for information. It therefore had to understand the existing picture – including which sources of information were commonly being used by farmers, their perceptions of these and the wider experience of development agencies in engaging with farmers. From a combination of consumer research surveys, interviews and document analysis a number of potential sources of information related to productivity were evident (Figure 2).

1. Farmers: farmers like to go to other farmers for information. Over one-third say that this is their preferred source and certainly within every farming community, respected “lead” farmers exist who are available, local and perceived to be practical. Advice offered here is in the context of wider social relationships and structures. However, progressive and influential farmers still need to be able to access new information (on new approaches, products etc), raising the question of where this can be sourced?

2. Retailers: along with farmers, the main and most regularly used source of information is retailers. Retailers are, typically, independent owner-managed small businesses, located in simple shop premises in rural villages and towns. Typically, they sell a combination of fertilizers, pesticides and seeds and information is offered as a service embedded within these commercial transactions as a means of adding value to customer relationships. They are likely to stock the products of a number of input suppliers, although sometimes favouring one

supplier over another. Some are sole stockists for one company. Retailers as sources of knowledge and information have a number of characteristics:

They are used widely and regularly. Like farmers, their closeness to and frequent interaction with farmers offers a real opportunity to influence. About 60% of farmers going to a retailer do so in search of a solution to a farming problem rather than to buy a specific product (or brand). They are often reactive in their approach to customers, don’t know how to deal with them positively and lack technical knowledge. More commonly they see themselves as sellers of products rather than providers of solutions

Figure 2: Sources and flows of knowledge and information in the Vegetable market in Rangpur

Figure 3: Main source of advice for farmers

3. Input supply companies: these fall into three main categories – seeds, fertilizers and pesticides suppliers. The seed supply sector is the most disparate with a vast array of informal suppliers, NGOs, a large parastatal and emerging new corporate ventures co-existing. Pesticide suppliers, on the other hand, totalling around 8-10 main players, are relatively large-scale firms, both Bangladeshi and multinational, with the latter predominating. While input suppliers do undertake product demonstrations with farmers directly on an occasional basis, in the main, their route to their final consumer is through retailers.

4. Government extension officers: the role of the Department of Agricultural Extension (DAE) is to advise farmers directly and to organise fairs to bring different actors together. In Rangpur there are believed to be around 200-300 block supervisors (ie officers with responsibility for a particular “block” of land). Although most farmers are aware of the government extension service and respect block supervisors’ technical knowledge, few are regular users of their services. The main beneficiaries tend to be larger farmers.

5. NGOs: like many parts of Bangladesh, there is an extensive NGO presence in rural Rangpur. They work with groups of low income “beneficiaries/clients” and provide a range of advisory and more tangible (seeds) support. Their coverage is limited and they depend upon further external funding for their continuance.

6. Media: beyond these sources, farmers may also gather relevant information from the wider media. However, newspapers are not widely read and while there are relevant advertisements contained within them there are few user-friendly articles on vegetable production. Similarly, radio and television coverage is poor and their content of limited relevance. Within the above picture of the different providers of information, four main characteristics stood out:

(a) Farmers are often unsure of what information they can expect from whom but are certainly largely unhappy with what they are receiving! The relatively high rates of return available from vegetables in the last few years appear to have allowed farmers to “sit back” and wait for the market to deliver high prices rather than pursue greater efficiency. However, when vegetable prices begin to stabilize there will be more incentive to improve practices and therefore greater demand for information.(b) While farmers advising other farmers is a practical form of information provision, for this information to be new and relevant it needs to be up-dated and this requires access to other sources, external to farmers. (c) Existing public providers of information in government are regarded widely as irrelevant. Increasingly, their structures and operations are seen to be dysfunctional and, more simply, they are usually not there!(d) Private sector retailers, even though they interact with farmers regularly and farmers would like useful information from them, generally do not provide an appropriate service. In general, both retailers and input suppliers undervalue the importance of information within commercial relationships. From the above analysis, the most practical immediate focus to bring about significant impact lay with a KATALYST intervention to develop private sector capacities.

The intervention design and implementation

The underlying reasons for the weak level of information provision in the vegetable sector left KATALYST with a clear direction for intervention. The strategic challenge - given the players involved – was to build the capacity of the private sector to strengthen existing relationships and offer relevant knowledge and information services. The analysis provided the context for a future vision of farmers (consumers) demanding good quality information and providers offering this (on a sustainable basis) because it was in their commercial interests to do so.

In undertaking the project, KATALYST followed its market development approach to business services characterized by:

• Identification of the underlying cause: low levels of knowledge and information in the market (a key cause of poor productivity) can be attributed to weak private sector capacities. • A clear strategic focus of KATALYST was developing the capacities of retailers – with whom farmers interact regularly - and input suppliers (retailers’ main source of information) within the market system was therefore the main project goal.• Operational flexibility: within these strategic boundaries, engaging with appropriate players in an entrepreneurial manner that builds ownership with them. Indeed, the idea of retailer training emerged from such discussions. • Scaling up with other players: in order to promote change throughout the market system, encouraging other input providers to invest in knowledge and information. Around 480 retailers, 20% of all Rangpur retailers and serving approximately 350,000 farmers, were trained over the 2-year period. Taking account of both direct financial costs and staff time, overall cost per (retailer) trainee was $90- 100, with the effective Syngenta: KATALYST share of costs estimated around 60:40. Early results from the project show positive impacts on each of the market players:• Farmers’ perception of their experience with retailers’ service has improved.• Retailers have greater self-confidence, place more emphasis on advice and information, have better customer relations and, in most cases, increased sales.• Syngenta’s sales have grown 3-4 times faster than in other regions. The strategic importance of knowledge and information in the supply-chain has been re-emphasized. Syngenta plan to invest in retailer training throughout the country.

Other input suppliers, who have often lost out competitively in the short-term, are now showing positive signs of interest in retailer training. This is the critical issue – “crowding in” - in determining wider market change. The case highlights the importance of knowledge and information in improving agriculture performance - and the opportunity presented by this – and poses challenges for agencies in how to intervene effectively to stimulate more effectiveand large-scale market development.

Useful, capacity-building knowledge and information can be offered in supply chains as an integral element of companies’ operations within a market context and can be a successful strategy. The notion that information should be seen, somewhat preciously, as a “public good” that must be delivered by public agencies is incorrect – and such agencies can therefore be released to play other (still important) roles in markets.

It is possible to engage successfully with large private sector companies provided that this is done within a clear strategic framework, there is recognition of the (legitimate) differences between public and private aims and agencies intervene in a flexible and entrepreneurial manner.

2. Farmers’ Field School approach of DANIDA

The Objectives of Agriculture Sector Programme Suport II (ASPSII) of DANIDA aree:

• To support d ecentralised approach by delegating planning, decision-making and implementation to local authorities, NGO’s and Community Based Organisations (CBO).

• Develop the negotiating capacity of CBOs to formulate and demand an adequate agricultural extension service from the public and private sector.

The components of ASPSII are:

i) Agricultural Extension Component (AEC):The target groups are groups of small and marginal farmers, and women, cultivating 0.5 – 2.5 acres of land with a focus on crop-based agricultural development, and with scope for integrating livestock and aquaculture production. Activities are concentrated in the poor districts in the north and northwest. Field activities will build on the positive experiences gained during ASPS I with respect to the Farmer Field Schools concept, the development of farmer groups and the use of Farmer Trainers. There will also be an increased use of mass media and information communication technology for the dissemination of extension messages and market information. The overall approach is integrated crop management covering the crops sub-sector, but with operational links established at field level to the livestock and aquaculture/fisheries sub-sectors.

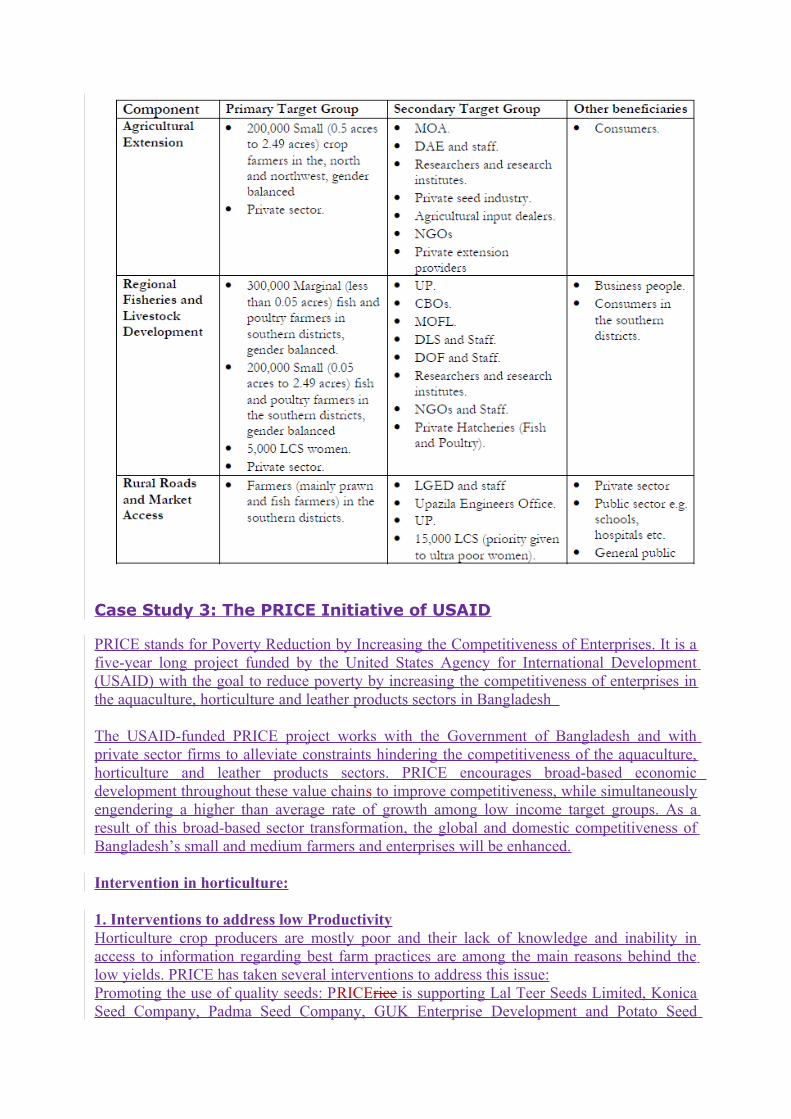

ii) Regional Fisheries and Livestock Development Component (RFLDC):The target groups are small and marginal farmers and the functionally landless, with focus on specific groups such as women-headed households, women poultry rearers, inshore fishers, Labour Contracting Society members, settlers on new char land, and women fish driers. The component built on the successful methodologies of the ASPS I aquaculture and livestock activities in the Noakhali and Patuakhali/Barguna areas. Uses made of the participatory learning approach of field schools adapted to integrated homestead production activities in aquaculture and livestock with a variety of technical options. NGOs assisted in capacity building of Union Parishads (UPs) and Community Based Organisations (CBOs), and facilitate micro-credit. UPs be supported to be responsive, accountable and transparent in providing services to the target group. Block grants, with performance based criteria made available to UPs for their support to CBOs. The private sector supported to provide inputs and markets, such as in food processing. Market linkages have been promoted in cooperation with the Rural Roads and Market Access Component The information on target groups and beneficiaries are presented in the Table #.

Table # The information on primary target groups and beneficiaries under farmers’ field school of ASPSII of DANIDA.

Case Study 3: The PRICE Initiative of USAID

PRICE stands for Poverty Reduction by Increasing the Competitiveness of Enterprises. It is a five-year long project funded by the United States Agency for International Development (USAID) with the goal to reduce poverty by increasing the competitiveness of enterprises in the aquaculture, horticulture and leather products sectors in Bangladesh

The USAID-funded PRICE project works with the Government of Bangladesh and with private sector firms to alleviate constraints hindering the competitiveness of the aquaculture, horticulture and leather products sectors. PRICE encourages broad-based economic development throughout these value chains to improve competitiveness, while simultaneously engendering a higher than average rate of growth among low income target groups. As a result of this broad-based sector transformation, the global and domestic competitiveness of Bangladesh’s small and medium farmers and enterprises will be enhanced.

Intervention in horticulture:

1. Interventions to address low ProductivityHorticulture crop producers are mostly poor and their lack of knowledge and inability in access to information regarding best farm practices are among the main reasons behind the low yields. PRICE has taken several interventions to address this issue:Promoting the use of quality seeds: PRICErice is supporting Lal Teer Seeds Limited, Konica Seed Company, Padma Seed Company, GUK Enterprise Development and Potato Seed

Farmers Association to train seed dealers, agents and seed producing farmers on seed technology and the benefits of using high quality seeds of vegetables and potato. Field supervision , as well as technical support at different stages of production and post production was also provided to the seed farmers to ensure seed quality. PRICE partner enterprises also organized demonstration plots and field days to showcase the performance of good seeds and disseminate technical knowhow. Training, demonstrations, field days and meetings on seed technology is extremely useful for improvement of seed quality at the farm level which will eventually contribute to increase productivity. At the same time through these efforts, seed dealers and agents are able to explain to vegetable growing farmers how the use of quality seeds can increase their crop production. Through these training sessions, approximately 1000 seed farmers were exposed to seed production technology and 1,252 dealers and retailers became knowledgeable and are now able to promote the use of quality seeds to an estimated 60,000 farmers. Training on modern farming techniques: PRICE in conjunction with farmers’ associations such as the Murail Rural Development Multipurpose Co-operative Society Ltd, Kansat Mango Farmer Multipurpose Co-operative Society Limited (KMFMCSL), Bhaterchar Krishak Unnyan Bahumukhi Samabai Samity and also with small farmers groups organized by Agricultural Advisory Services and Environment Friendly Agriculture Development Foundation Agro-business is training smallholder farmers on modern farming techniques, specially focusing on proper planting, use of hybrid seeds and high quality planting material, judicial application of balanced fertilizer and compost, water and pest management and following proper harvesting index through which farmers are being benefitted in increasing productivity of potato, egg plant, other high value vegetables and mango substantially.

2. Interventions to address high post harvest lossesPoor post harvest handling, including poor packaging, absence of efficient cool chain management systems, lack of quality control and inadequate transport, leads to large losses within the sector. Post-harvest losses in the horticulture sector are estimated at 25 to 40 percent, depending on the crop. PRICE has taken initiatives to tackle this issue and help farmers increase their incomes by reducing post harvest losses. Working with partner organizations such as ANKUR, Kansat Mango Farmer Multipurpose Co-operative Society Limited (KMFMCSL), Golden Harvest Agro Industries Limited, EFADAF Agro- Business, Bhaterchar Krishak Unnyan Bahumukhi Samabai Samity, and Agricultural Advisory Society (AAS), PRICE is providing hands- on training and demonstrations to the farmers and wholesale agents on proper post harvest handling techniques. PRICE supported 240 farmers of Kansat Mango Farmers’ Multipurpose Cooperative Society Limited (KMFMCSL) on production and post production techniques, which led to minimizing fruit dropping and improving yields. PRICE also facilitated hands-on training for the farmers and association members on simple post harvest technologies like sorting, grading, cleaning, washing, drying, packing and transporting, which was not their usual practice. The outcome was visible as the association received around 20-40 percent per kg higher prices for their mangoes on average. Moreover, recently PRICE helped to organize 8 market outlets in Dhaka for the Kansat Mango Farmers Association of Chapainawabganj, who was extended technical support in post harvest handling to sell chemical free, properly cleaned and graded mangoes. PRICE also facilitated ANKUR - located at Chuadanga - to train 60 farmers in post harvest handling who later opened two sales outlets for their mango farmers, in Chudanga and Jibonnagar. Another PRICE initiative was the first soil testing for mango farmers in Bangladesh. This testing provided the nutrient status of the soil for farmers to apply individualized fertilizers based on the needs of the orchard.

3. Intervention to address inadequate compliancePoor compliance with food safety and quality standards is a huge roadblock to the development of the sector. PRICE is working with its partners to implement initiatives to address these issues. Promoting safe vegetable production: In 2008 the NGO Pathikrit disbursed loans of approximately BDT 375,000 to its members in Khulna to increase vegetable production. In addition to the lack of technical knowledge, information and quality inputs, Pathikrit found that the excessive use of chemical fertilizers and pesticides was creating a potential health hazard to consumers, while also increasing farmers’ costs of farming. In order to address this problem Pathikrit created a separate organization, “Organix”, specifically chartered to help farmers produce and market safe vegetables free from excessive chemicals. Organix signed an MOU with PRICE in September 2009 in order to develop a contract farming model for safe vegetable production, following the basic concepts of Good Agricultural Practices (GAP). PRICE is working with Organix and other partners to develop and provide training to farmers on safe crop protection and integrated pest management (IPM). PRICE is reaching to more than 2000 horticultural farmers by working with Muktir Alo and EFADF Agro Business, Agricultural Advisory Society and Grammen Krishok Unyon Sangstha Enterprise to train farmers and create awareness on following good agricultural practices, adoption of more environment friendly crop husbandry by using compost, clean cultivation approach, use of biological pesticides and bio control agents instead of harmful chemicals. PRICE has been supporting Grammen Krishok Unyon Sangstha Enterprise (GKSSE) of Bogra and Riya Fertilizer of Sirajganj in the promotion of organic fertilizer through training, meeting, organizing field days and strengthening market linkages.

4. Poor Market LinkagesPRICE has helped link the GUK Enterprise Development and Vater Char Farmers’ Development Cooperative Society, in Norsingdi, with Golden Harvest Agro Industries Limited. PRICE has also supported Golden Harvest Agro Industries Limited to attend Gulfood Fair in February 2010, one of the largest food fair of the region, creating opportunity for the company to get access to new market in the Gulf and beyond. Promoting contract farming. Contract farming is a powerful tool to convert the weak and fragmented supply chain into a strong integrated value chain. PRICE is supporting a number of contract farming initiatives in the horticulture sector with the aim to enhance farmers’ access to quality farming inputs, knowledge and information required to practice improved farming techniques, better access to value chain financing, and guaranteed market for their produce. Working alongside partners such as Organix, GUK Enterprise Development, Ankur, Muktir Alo, PRIDE, PRICE is facilitating trainings for small hold farmers to implement good farming practices in order to meet the quality and quantity needs of their large contract farming partners. In Bogra, 1500 potato and high value crop farmers and in Khulna 650 egg plant and other safe vegetable producers and in Chudanga 500 mango farmers were introduced into the contract farming system and are receiving training to learn good farm practices.

Interventions in aquaculture sector

Shrimp Compliance issues: Shrimp and prawn are high-value export commodities that mostly go to Europe and the USA, and have stringent quality specifications as food items. Standard hygiene and food safety is a prime issue for the shrimp subsector. The other important issue for export market access is compliance with local labor laws. Labor Practices. The perception of improper labor practices in Bangladeshi processing plants is a key issue for exporting

shrimp and prawn to the U.S.A. To address the situation PRICE implemented an initiative to audit and validate the compliance initially of 10 processing plants with all aspects of Bangladeshi labor law. After this review and improvement of labor-related procedures, PRICE developed and implemented labor standards compliance courses for workers, managers and owners of shrimp processing plants.

Food Safety and Quality Compliance. The presence of antibiotic residues is one of the main issues hindering the export of shrimps to Europe and the U.S.A. PRICE assisted the Ministry of Fisheries with its Department of Fisheries Inspection and Quality Control (FIQC) Labs, so that consignments can be tested and screened accurately before export. PRICE arranged five training programs for 100 FIQC trainees in compliance with EU food safety requirements. Additionally, PRICE and BFRI completed a year long experiment and found that supplemental feed causes accumulation of nitrofuran metabolites in farmed prawn and the metabolites may be removed from contaminated prawn by withdrawing the contaminated feed for a couple of weeks while under rearing.

Low productivity: Productivity of shrimp farms in Bangladesh is very low. To address the issue PRICE teamed with World Fish Center (WFC) to launch the Greater Harvest and Economic Return from Shrimp (GHERS) initiative. The key objective of this program is to increase the productivity of shrimp farming through strengthening its value chain while following a contract farming scheme. GHERS works with depots to transmit information, knowledge and skills, as well as quality inputs like screened seeds to farmers to facilitate the production of disease-free shrimps. GHERS will work with 23,000 farmers by the end of 2011.

Inadequate farmers’ access to markets: The quantity produced by any individual smallholder farm is quite small and lacks economies of scale, resulting in increased transaction costs and reduced competitive advantages. PRICE assists groups of farmers to organize synchronized harvesting and bulk supply of shrimp to depots. The scale enhances their bargaining strength, price and profitability.

FishThe average production of fish per hectare in pond-based aquaculture was 2.66 metric tons (MT) in 2007-8, which – according to the Department of Fisheries - has the potential to increase to 7 or 8 MT. PRICE has identified key constraints to the development of the finfish sector and is working with farmers, processors and government in order to overcome those, in the following areas:

Improving farm productivity: Working with 25 farmers associations, seven NGO-based farmers groups and two community-based organizations, PRICE will assist more than 30,000 farmers – almost 35 percent of them female – to understand and apply best practices in farm methods and management by the end of 2011. On a cost-share basis PRICE is providing technical assistance and training on improved farming, feed, water & health management, and access to better inputs. PRICE has helped establish demonstration ponds and is encouraging information sharing to build the capacity of association members.

Improving fish farming inputs: PRICE is in partnership with nine hatcheries, two feed mills, one fish seed traders association, and one input seller to ensure quality grade inputs to farmers. In the process hatcheries are getting training and linkages to better quality brood sources to produce quality grade and inbreed-free fish seeds; fish seed traders linking with

farmers to supply quality seeds and carry the fish seeds in a responsible way to reduce mortality and increase yield, feed millers supply quality grade feeds and input sellers supply allowed growth promoters, vitamins, minerals and micronutrients to enhance production.

Hygienic dry fish production and marketing: Dry fish production is an age-old method of fish preservation in Bangladesh. Dry fish is consumed locally as well as exported abroad to cater the demand of the ethnic market. Fish are sundried in the country and often done under unhygienic conditions and traded poorly or without packaging. PRICE has partnered with one dry fish association in Cox’s Bazar and is negotiating with another to train roughly 500 entrepreneurs and 2,500 workers by the end of 2011 to produce hygienic dry fish and marketing those with better packaging.

Improving access to markets: PRICE facilitates trainings on group procurement of inputs and group marketing for better access to markets so that organized farming groups can procure inputs cost-effectively and sell their produce collectively with better prices.

Generating access to finance: Low transaction cost, easy access and reasonable cost of capital are necessary to enhance investment, and thereby productivity and competitiveness. As institutional credits are difficult to access in the fish sector, PRICE initially assisted farmers in getting micro credits from NGOs and so far, 1,327 received microfinance ranging between BDT 3,000 to BDT 120,000.

Chapter 5

Rural organizations and membership aimed at strengthening the innovation system for the rural sector

This section presents case study about rural farmers organizations that aimed at improving farmers capacity, productivity and strengthening the innovation system for the rural sector.

Smallholder Milk Producers Organizations

Smallholder milk producers play a key role in dairy markets in Bangladesh. They supply all the domestic milk for the informal or traditional market and three quarters for the formal or processed market. A more detailed description of the characteristics of smallholder milk producers is given in annex I. Milk Vita and Grameen/CLDDP institutionally practice capacity development and empowerment of smallholder dairy farmers, both men and women, in the value chain and business ownership and management process.

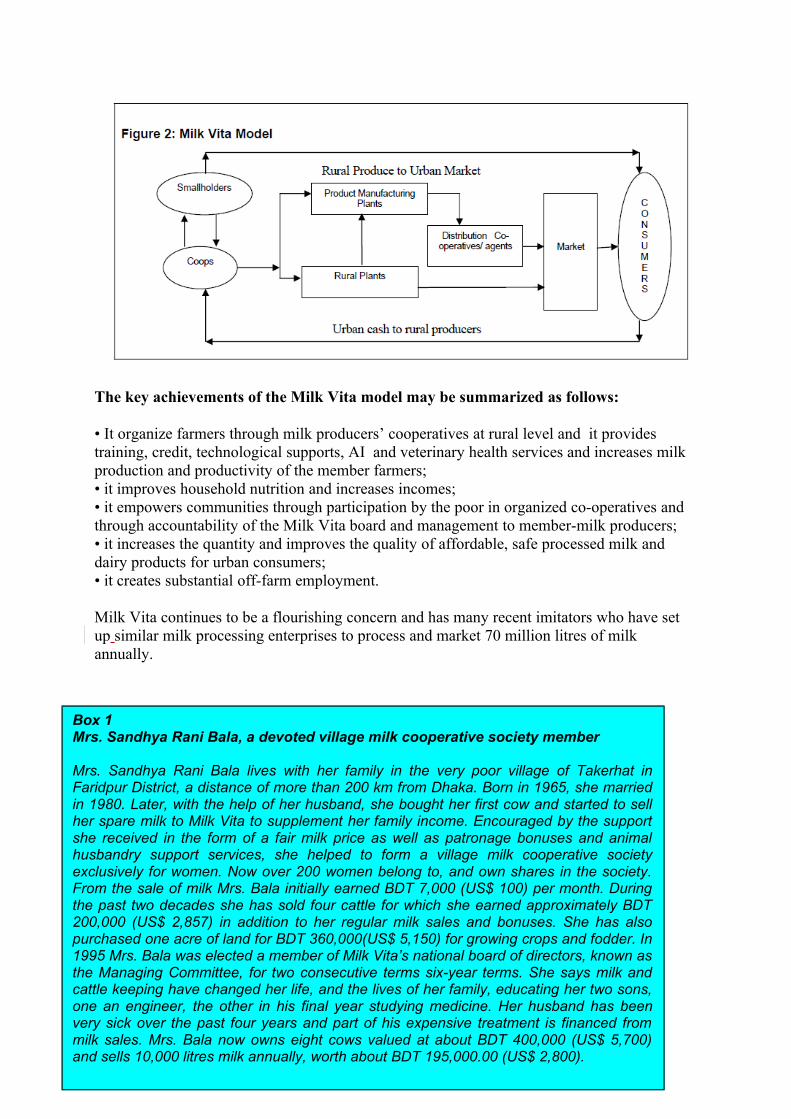

The Milk Vita co-operative dairying model was adapted from the world-renowned Anand pattern model in India. From a modest start in the mid-1970s that involved providing 4,300 very poor, often landless, households in remote rural areas with a complete package of milk production enhancing technologies, village level organizational skills and a milk collection-processing-marketing system, the two-tier Milk Vita dairy cooperative model has grown into a successful commercial dairy enterprise. Today, milk is collected from over 100,000 smallholder members organised into 1,200 primary village co-operatives, then processed and distributed to all the major cities in the country. In 2006, smallholder milk producers sold 75 million litres of milk surplus to their household requirements. They also earned patronage dividends from Milk Vita’s profits. The resultant increase in milking cow numbers and savings generated also serves as a cushion against the devastating effects of severe flooding that regularly afflict the country.

The Milk Vita model creates many jobs, reduces collection and distribution costs and has improved milk quality by cutting delivery times, especially in congested city areas. One off-farm job has been created for each 35 litres of milk collected, processed and marketed. More than half the jobs are in rural areas. Democratically elected milk producer and distributor co-operative members are now in the majority on the Milk Vita Board of Directors. This encouraged the Government to withdraw from day-to-day management enabling the Board to hire professional managers, which led to improved performance and created a platform for further expansion to bring more poor people in to the dairy value chain. Since the late 1990s Milk Vita has invested more than USD10 million in expanding its milk collection, processing and marketing network and now delivers safe and affordable milk and dairy products to some five million low-income urban dwellers.

The key achievements of the Milk Vita model may be summarized as follows:

• It organize farmers through milk producers’ cooperatives at rural level and it provides training, credit, technological supports, AI and veterinary health services and increases milk production and productivity of the member farmers;• it improves household nutrition and increases incomes;• it empowers communities through participation by the poor in organized co-operatives and through accountability of the Milk Vita board and management to member-milk producers;• it increases the quantity and improves the quality of affordable, safe processed milk anddairy products for urban consumers;• it creates substantial off-farm employment.

Milk Vita continues to be a flourishing concern and has many recent imitators who have set up similar milk processing enterprises to process and market 70 million litres of milk annually.