Embed Size (px)

Citation preview

Dr. Raymond N. Johnson, CPA

MODERN AUDITING 7th MODERN AUDITING 7th EditionEdition

MODERN AUDITING 7th MODERN AUDITING 7th EditionEdition

Developed by:Raymond N. JohnsonPortland Sate University John Wiley & Sons, Inc.

William C. BoyntonWilliam C. BoyntonCalifornia Polytechnic State California Polytechnic State University at San Luis ObispoUniversity at San Luis Obispo

Raymond N. JohnsonRaymond N. JohnsonPortland State UniversityPortland State University

Walter G. KellWalter G. KellUniversity of MichiganUniversity of Michigan

Dr. Raymond N. Johnson, CPA

Understanding AssertionsUnderstanding Assertions

• Transaction class

• Account balances

• Disclosures

Dr. Raymond N. Johnson, CPA

Understanding the Business and IndustryUnderstanding the

Business and Industry• Key Questions

– How material is the transaction class to the audit client?

– What business risks exist within the transaction class?

– What expectations do you have regarding industry norms?

• Business practices

• Expected controls

• Expected ratios

Dr. Raymond N. Johnson, CPA

Understanding the Business and IndustryUnderstanding the

Business and IndustryExample Industries• Retail grocery• Household appliance

manufacturer• Computer manufacturer• Hotel / Resort• School district

Key Issues• Significance of

transaction class• Business risks• Expectations

– Business practices

– Controls

– Ratios

Dr. Raymond N. Johnson, CPA

Audit Risk ModelAudit Risk Model

AR = IR x CR x AP x TD

1. Assess IR

2. Consider preliminary audit strategy

3. Perform analytical procedures

4. Evaluate internal controls

5. Assess TD and perform remaining substantive tests

Dr. Raymond N. Johnson, CPA

Inherent RiskInherent Risk

• Purchases and accounts payable– “Short-term” completeness problems

• Inventory– Net realizable value of inventory– Obsolete inventory– Overstatement of inventory to overstate profits

• Payroll– Employee fraud and payroll overstatements

Dr. Raymond N. Johnson, CPA

Analytical ProceduresAnalytical Procedures

• Accounts payable– AP Turns– Evidence of understated payables

• Inventory – Inventory turns– Inventory growth relative to CGS– Manufacturing inputs to finished goods output– Quality control

• Payroll– Average payroll in key employee classes– Payroll costs per units of output (accomplishment)– Benefits and taxes to gross payroll

Dr. Raymond N. Johnson, CPA

5 Elements of Internal Control5 Elements of

Internal Control• Control Environment

• Risk Assessment

• Information and Communication

• Control Activities

• Monitoring

Dr. Raymond N. Johnson, CPA

Control EnvironmentControl Environment

• Establishes the tone that ensures a high level of control consciousness

• Establishes a tone of accountability for use of resources

• You must assume a strong control environment to place reliance on specific control activities

Dr. Raymond N. Johnson, CPA

Control ActivitiesControl Activities

• Authorization

• Segregation of duties

• Safeguarding of assets

• Information processing controls– Computer general controls– Computer application controls

• Performance reviews

Dr. Raymond N. Johnson, CPA

Direct Tests of User ControlsDirect Tests of User ControlsFigure 10-2Figure 10-2

Direct Tests of User ControlsDirect Tests of User ControlsFigure 10-2Figure 10-2

Dr. Raymond N. Johnson, CPA

Low CR Assessment based on Application Controls Low CR Assessment based on Application Controls Figure 10-2Figure 10-2

Low CR Assessment based on Application Controls Low CR Assessment based on Application Controls Figure 10-2Figure 10-2

Dr. Raymond N. Johnson, CPA

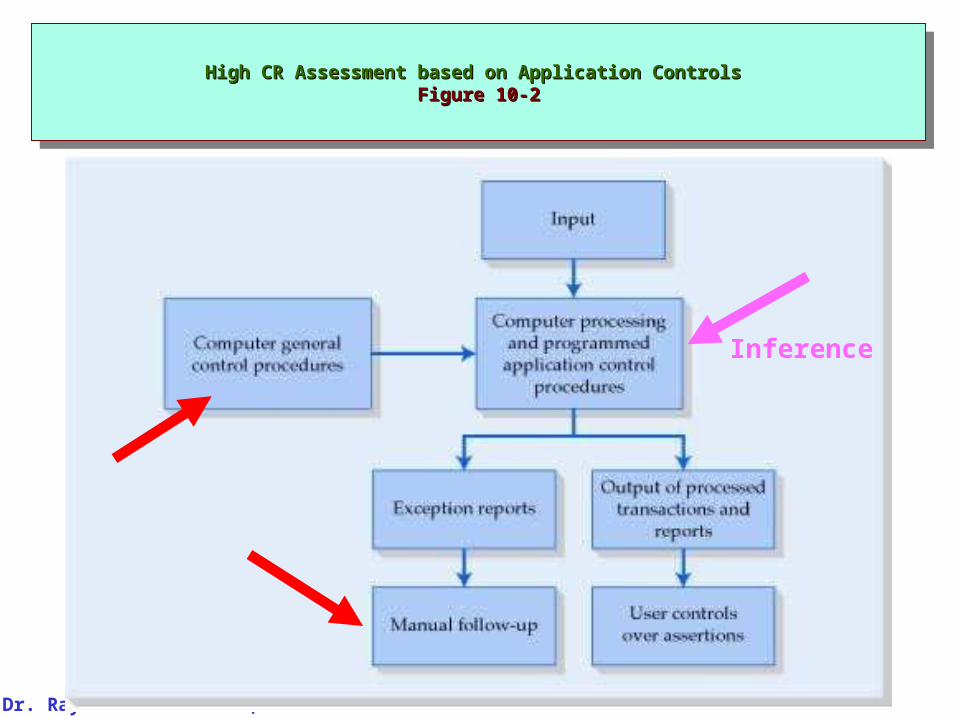

High CR Assessment based on Application Controls High CR Assessment based on Application Controls Figure 10-2Figure 10-2

High CR Assessment based on Application Controls High CR Assessment based on Application Controls Figure 10-2Figure 10-2

Inference

Dr. Raymond N. Johnson, CPA

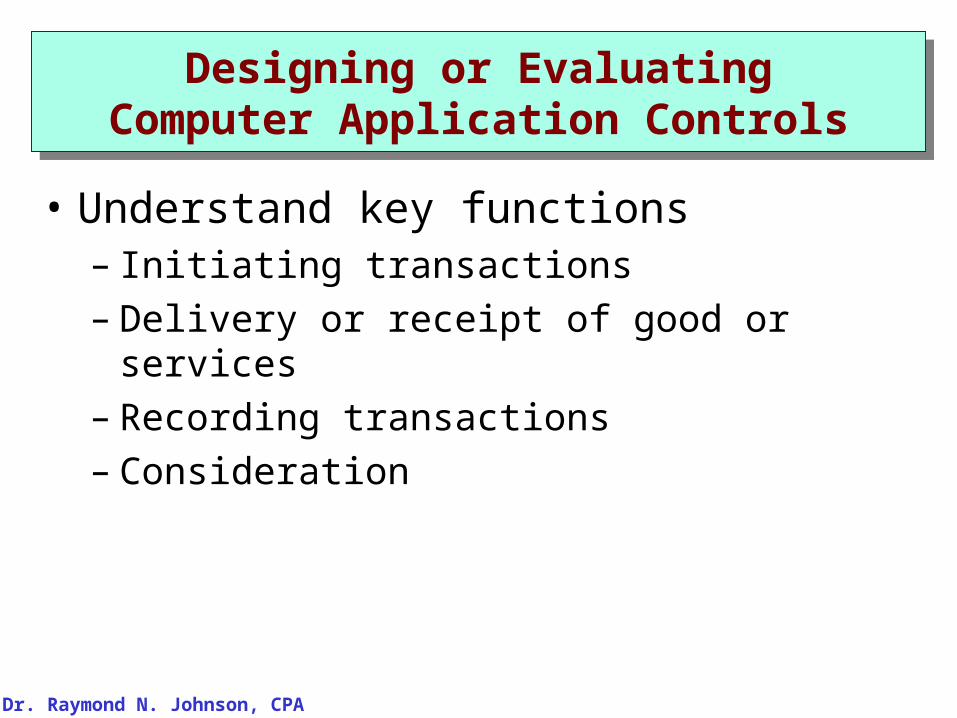

Designing or EvaluatingComputer Application Controls

Designing or EvaluatingComputer Application Controls

• Understand key functions– Initiating transactions– Delivery or receipt of good or services– Recording transactions– Consideration

Dr. Raymond N. Johnson, CPA

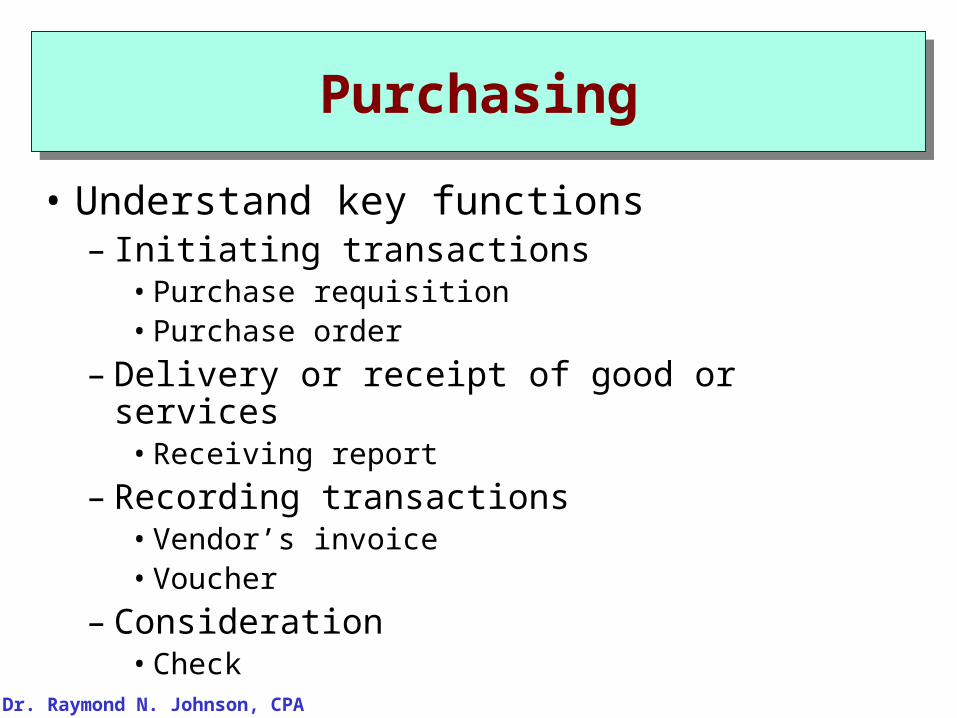

PurchasingPurchasing

• Understand key functions– Initiating transactions

• Purchase requisition• Purchase order

– Delivery or receipt of good or services• Receiving report

– Recording transactions• Vendor’s invoice• Voucher

– Consideration• Check

Dr. Raymond N. Johnson, CPA

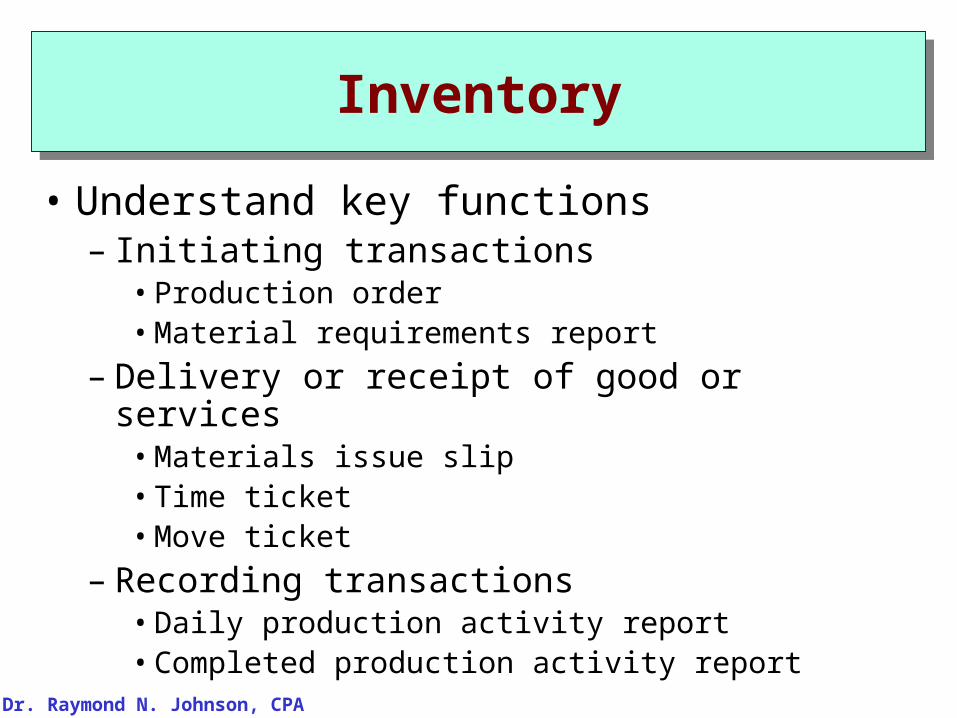

InventoryInventory

• Understand key functions– Initiating transactions

• Production order• Material requirements report

– Delivery or receipt of good or services• Materials issue slip• Time ticket• Move ticket

– Recording transactions• Daily production activity report• Completed production activity report

Dr. Raymond N. Johnson, CPA

PayrollPayroll

• Understand key functions– Initiating transactions

• Personnel authorization

– Delivery or receipt of good or services• Clock card

• Time ticket

– Recording transactions & consideration• Payroll register (journal)

• Payroll Check (from imprest bank account)

Dr. Raymond N. Johnson, CPA

Substantive TestsSubstantive Tests

• Initial procedures– Understand the business and industry

– Test accuracy of data provided for audit

• Analytical procedures• Tests of details of transactions• Tests of details of balances• Tests of details of balances – accounting estimates• Procedures required by GAAS• Tests of presentation and disclosure

Dr. Raymond N. Johnson, CPA

CHAPTER 15CHAPTER 15AUDITING THE EXPENDITURE CYCLEAUDITING THE EXPENDITURE CYCLE

CHAPTER 15CHAPTER 15AUDITING THE EXPENDITURE CYCLEAUDITING THE EXPENDITURE CYCLE

Dr. Raymond N. Johnson, CPA

CopyrightCopyrightCopyrightCopyright

Copyright 2001 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make backup copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.