Embed Size (px)

Citation preview

Dr. Anna MokgokongChairperson

To relentlessly innovate a new

integrated model of sustainable

healthcare that measurably

improves access to quality care

Empowering greater access to

sustainable quality healthcare

Antoine van BuurenGroup CEO

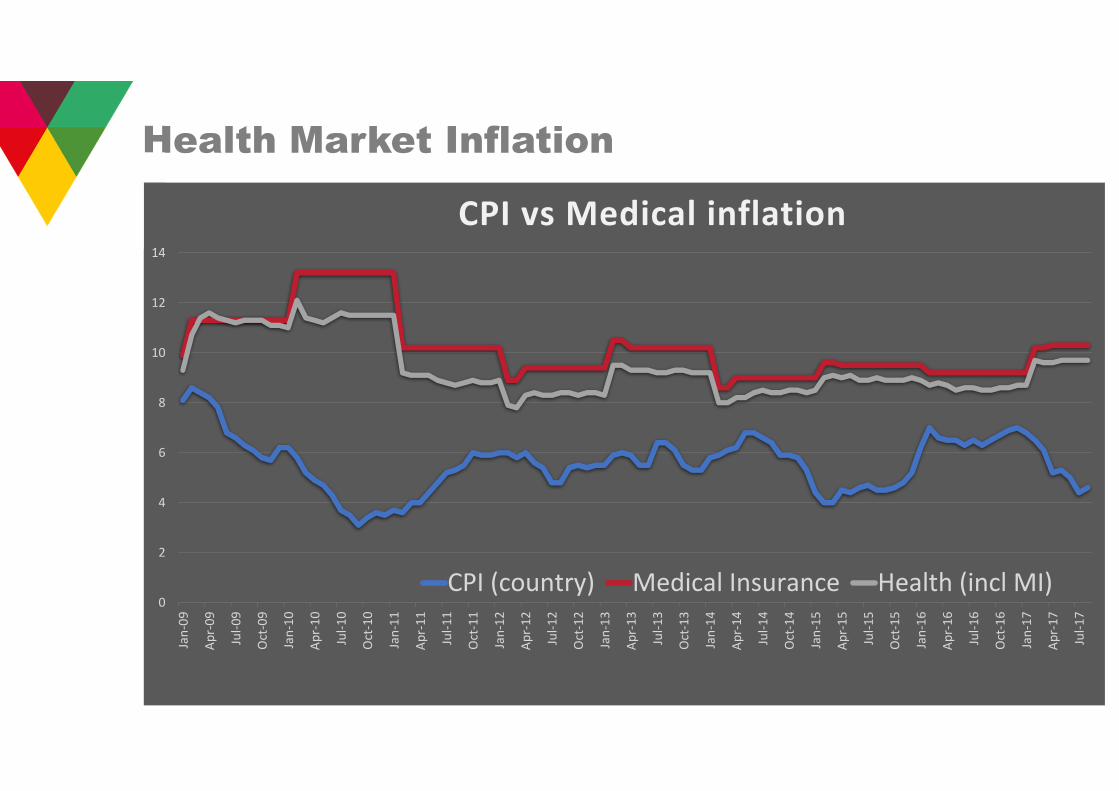

Health Market Inflation

0

2

4

6

8

10

12

14

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

CPI vs Medical inflation

CPI (country) Medical Insurance Health (incl MI)

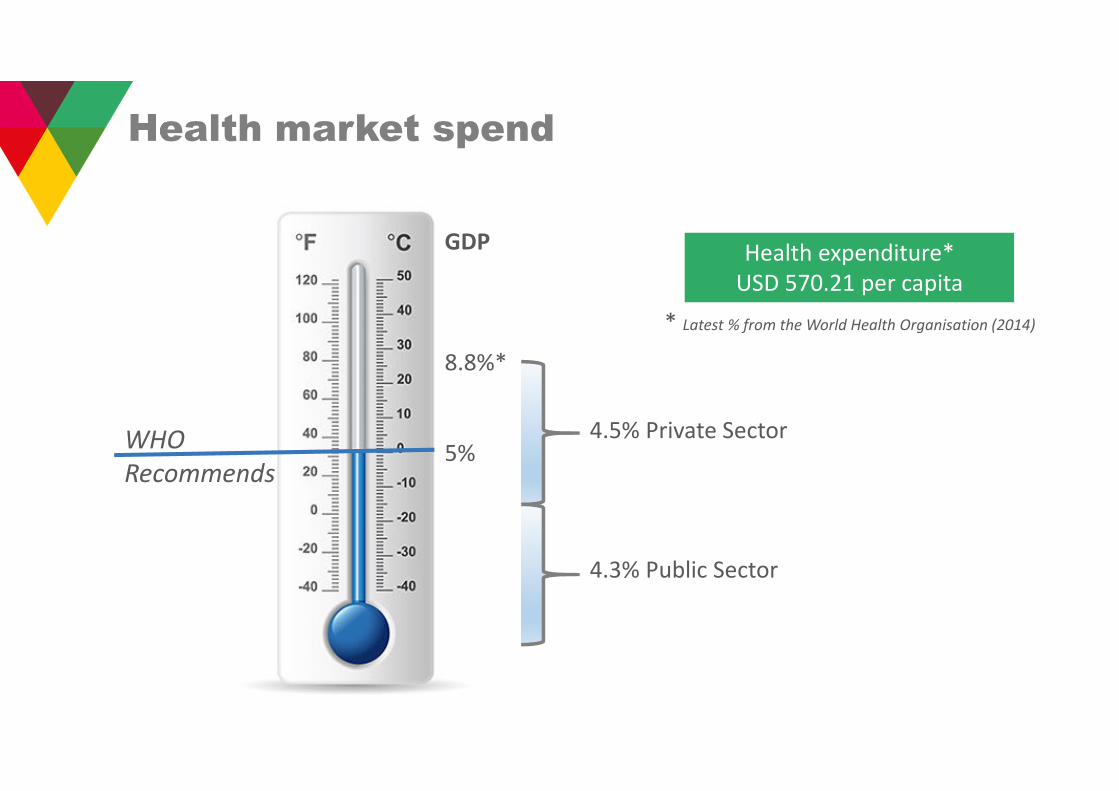

GDP

8.8%*

5%WHO

Recommends

4.5% Private Sector

4.3% Public Sector

* Latest % from the World Health Organisation (2014)

Health expenditure*

USD 570.21 per capita

Health market spend

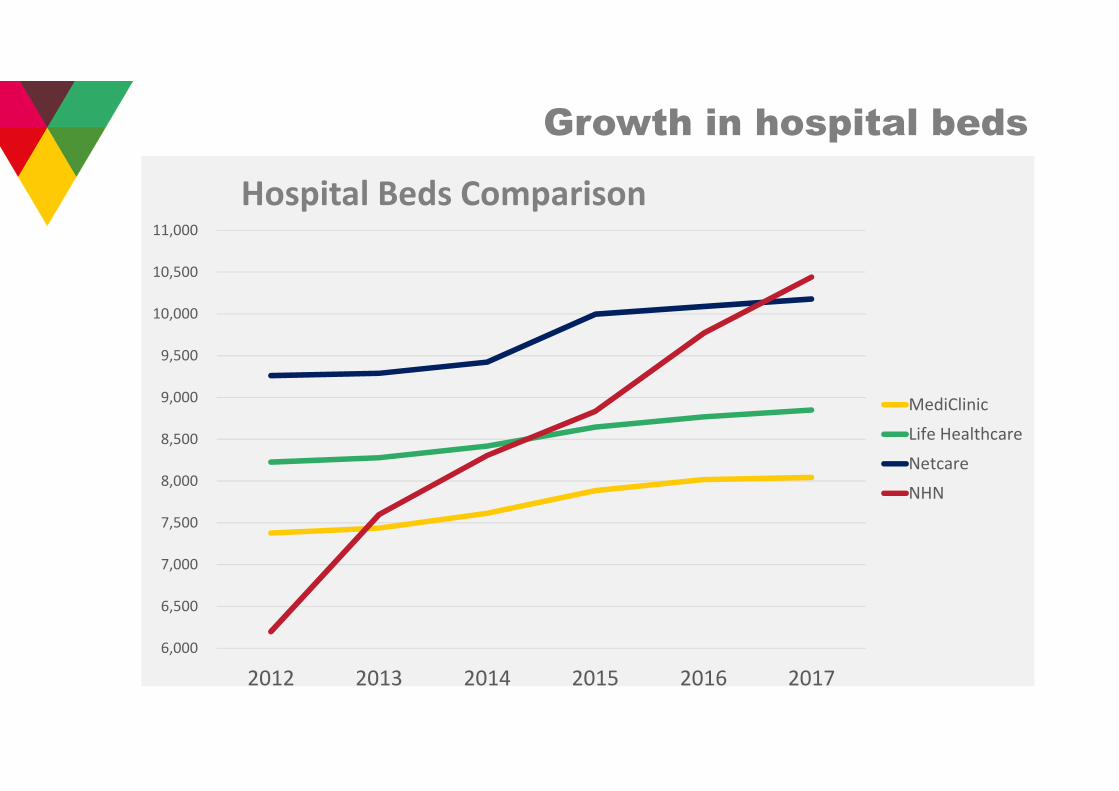

Growth in hospital beds

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

10,000

10,500

11,000

2012 2013 2014 2015 2016 2017

Hospital Beds Comparison

MediClinic

Life Healthcare

Netcare

NHN

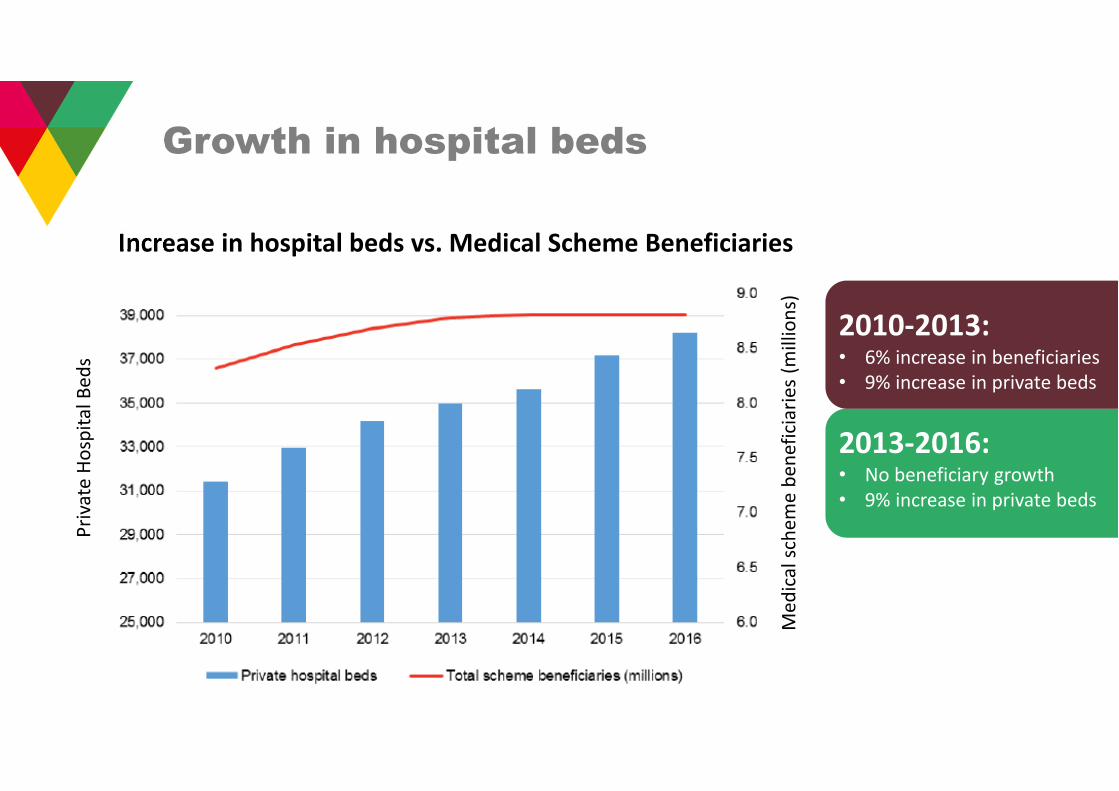

Growth in hospital beds

2010-2013:• 6% increase in beneficiaries

• 9% increase in private beds

2013-2016:• No beneficiary growth

• 9% increase in private beds

Increase in hospital beds vs. Medical Scheme Beneficiaries

Pri

vate

Ho

spit

al

Be

ds

Me

dic

al

sch

em

e b

en

efi

cia

rie

s (m

illi

on

s)

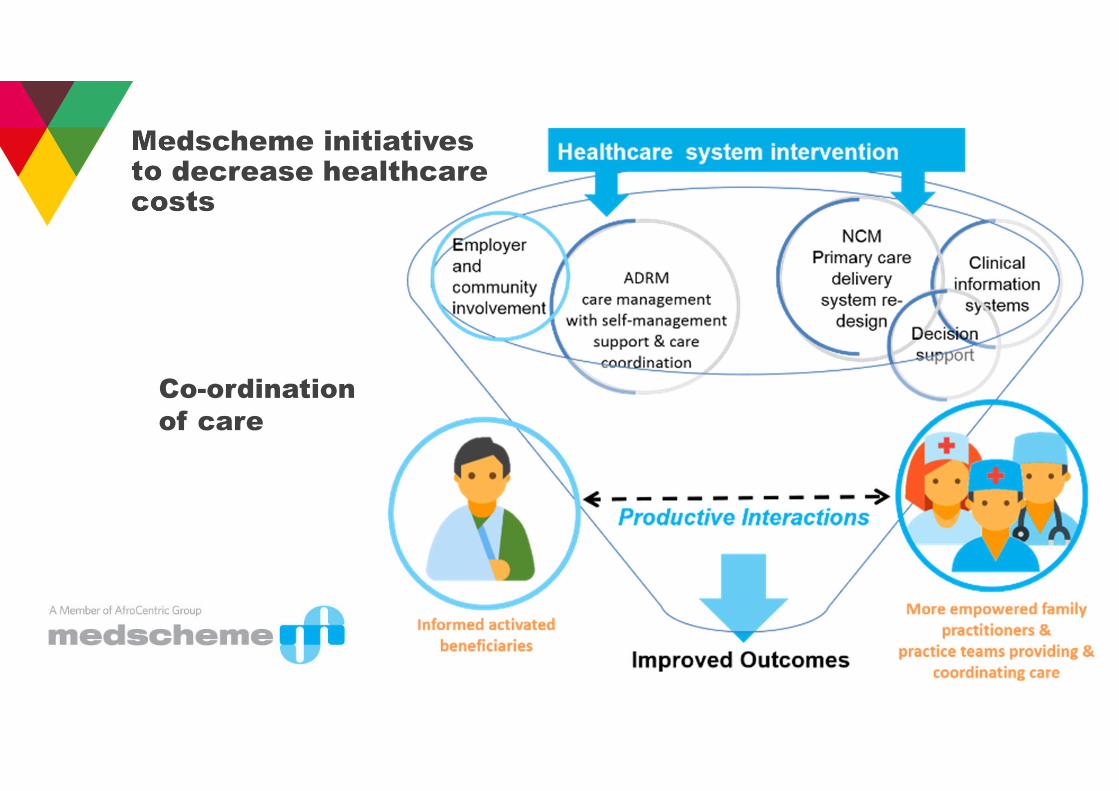

Co-ordination

of care

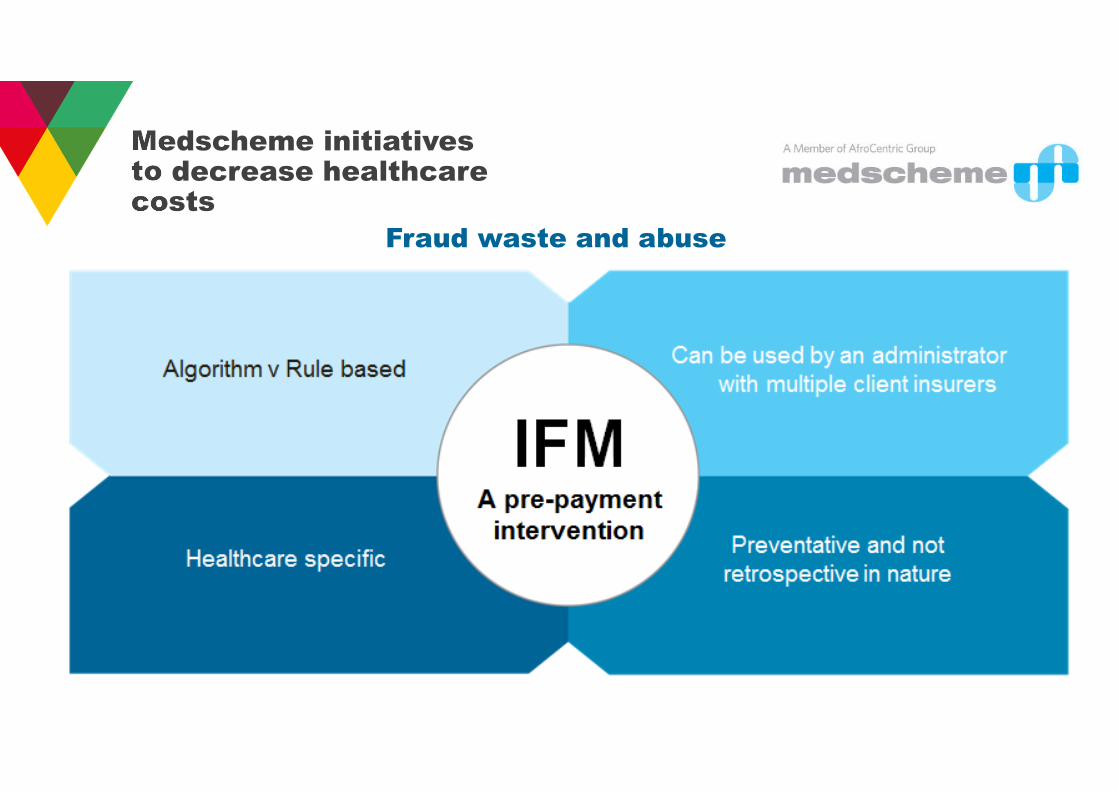

Medscheme initiatives to decrease healthcare costs

Fraud waste and abuse

Medscheme initiatives to decrease healthcare costs

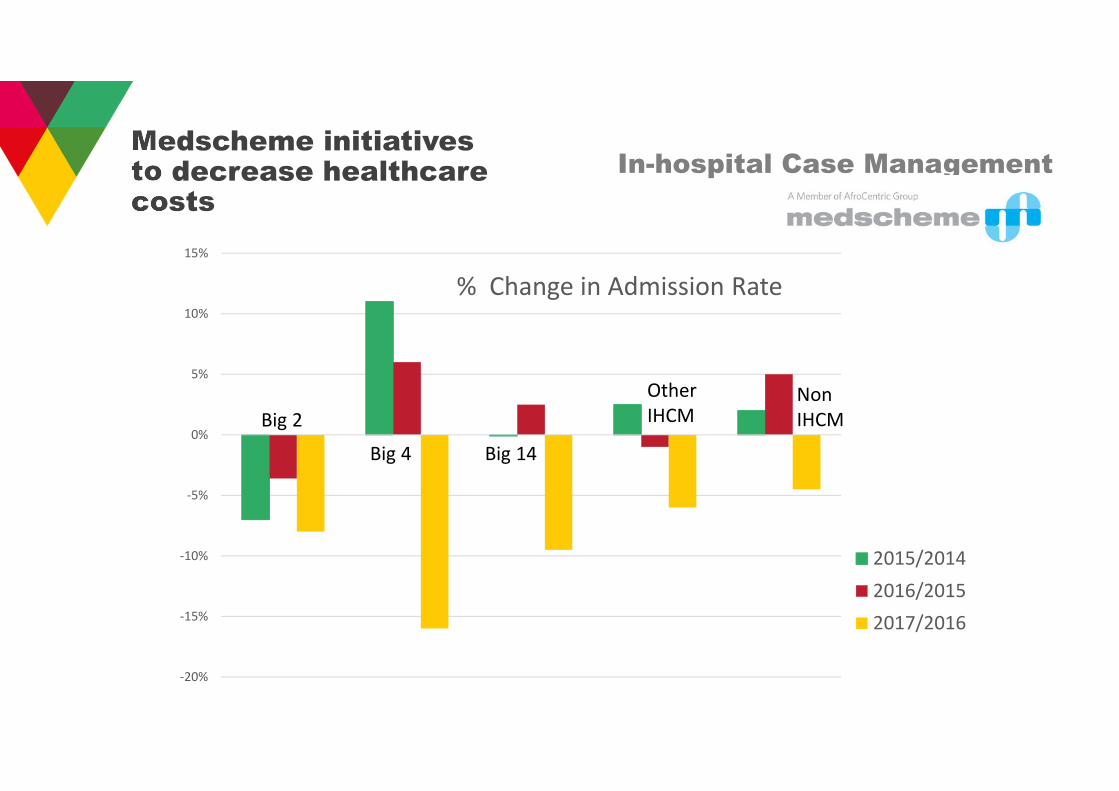

In-hospital Case ManagementMedscheme initiatives to decrease healthcare costs

-20%

-15%

-10%

-5%

0%

5%

10%

15%

% Change in Admission Rate

2015/2014

2016/2015

2017/2016

Big 2

Big 4 Big 14

Other

IHCMNon

IHCM

Medscheme initiatives to decrease healthcare costs

Activo, Curasana and Pharmacy Direct

Reducing pharma costs

Increasing access to care

Klinikka

Reducing pain, increasing mobility

Reducing back and neck surgery

Wellness Odyssey

Lifestyle interventions for

non-communicable diseases

Opticlear

Addressing high margins in optometry

Ensuring clinical care

Supply Chain Optimisation

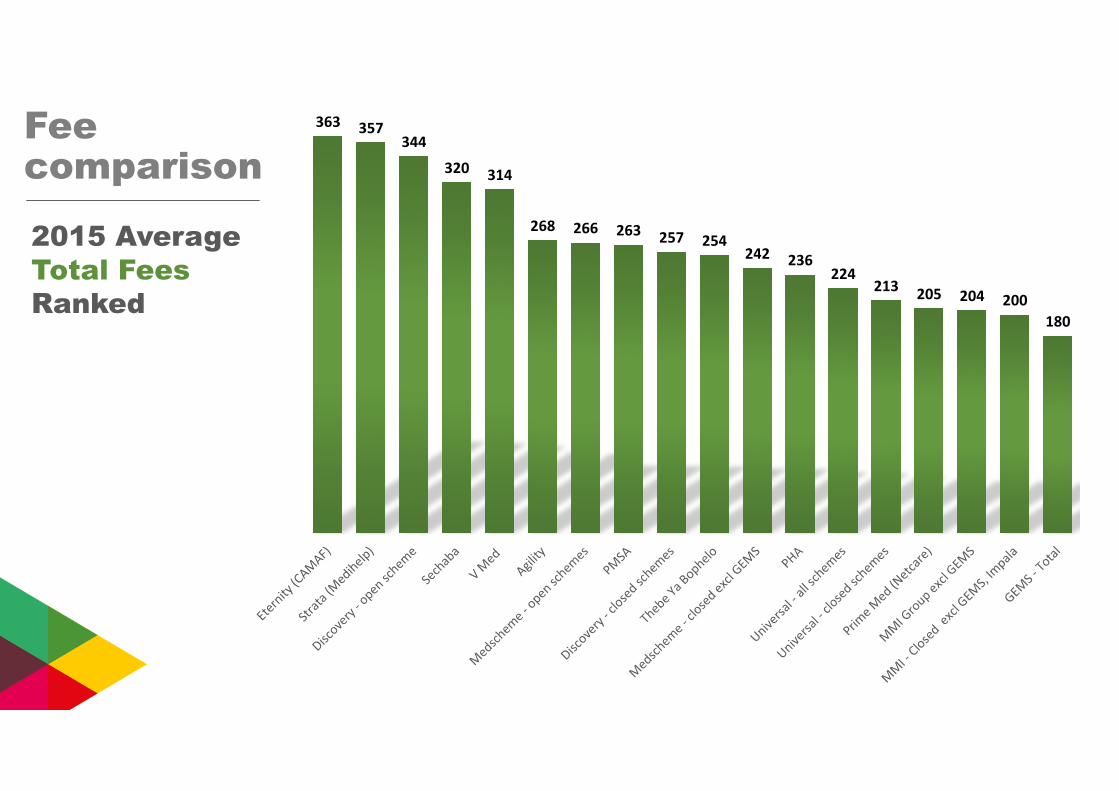

363 357344

320314

268 266 263257 254

242 236224

213205 204 200

180

Fee comparison

2015 Average

Total Fees

Ranked

Hannes BoonzaaierGroup CFO

Column1

0

500

1000

1500

2000

2500

3000

3500

4000

2 0 1 32 0 1 4

2 0 1 52 0 1 6

2 0 1 7

1,7701,958

2,098

3,148

3,7852

01

3

20

16

20

15

20

14

20

17

Total Revenue

R’m

illi

on

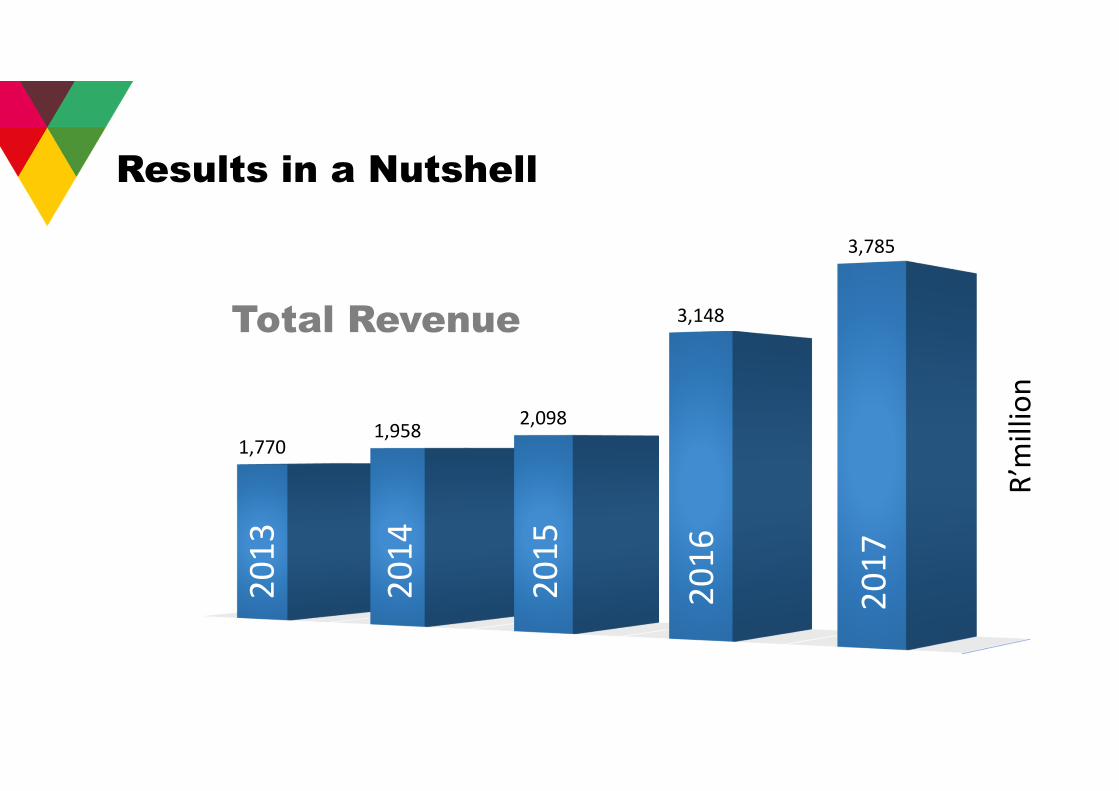

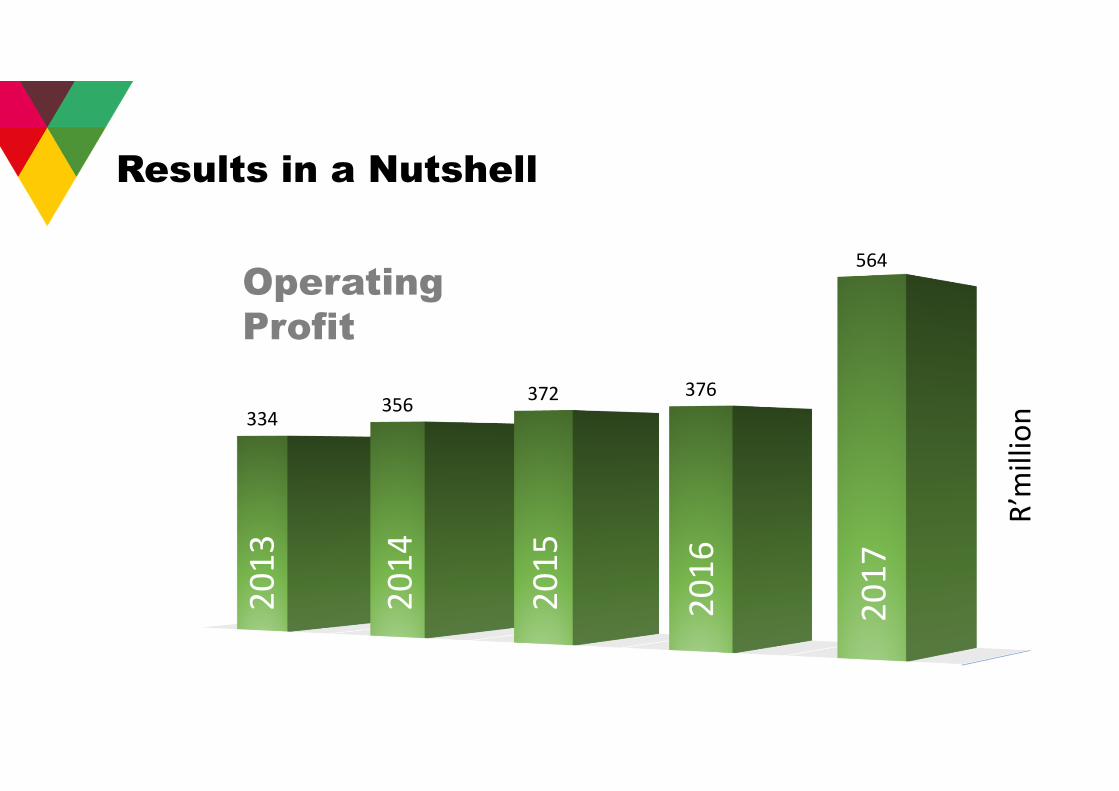

Results in a Nutshell

Column1

0

100

200

300

400

500

600

2 0 1 32 0 1 4

2 0 1 52 0 1 6

2 0 1 7

334356

372 376

5642

01

3

20

16

20

15

20

14

20

17

Operating

Profit

R’m

illi

on

Results in a Nutshell

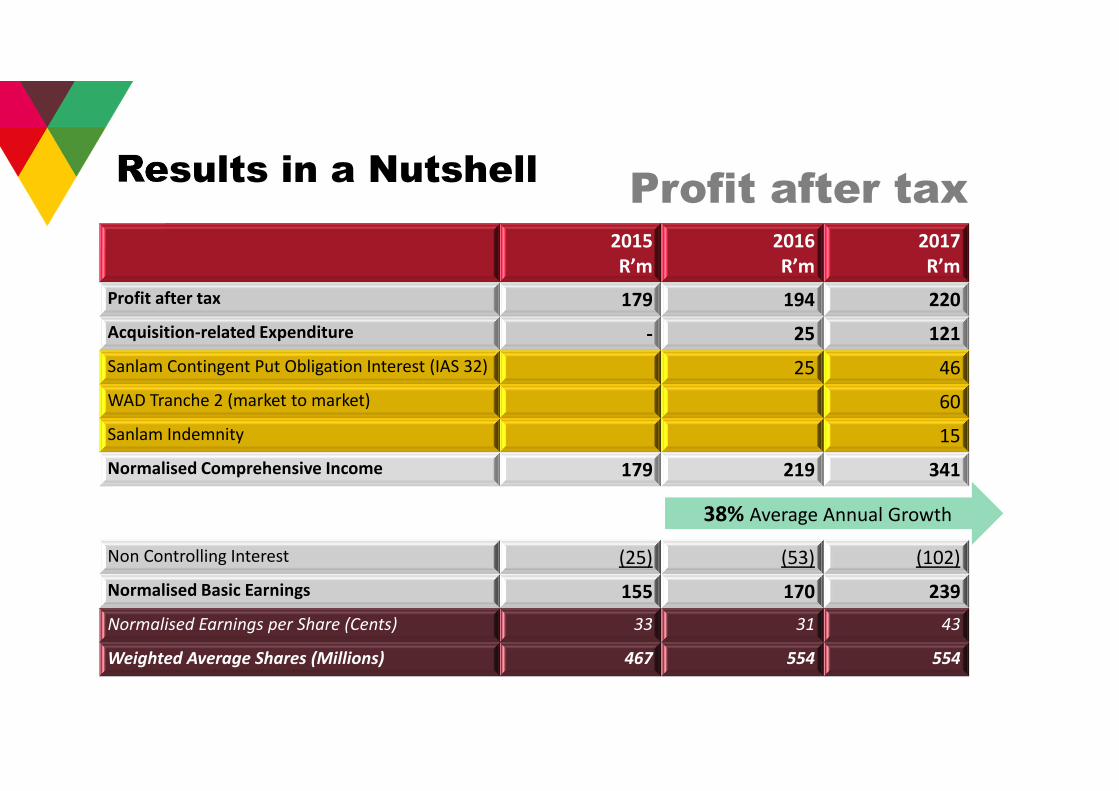

2015

R’m

2016

R’m

2017

R’m

Profit after tax 179 194 220

Acquisition-related Expenditure - 25 121

Sanlam Contingent Put Obligation Interest (IAS 32) 25 46

WAD Tranche 2 (market to market) 60

Sanlam Indemnity 15

Normalised Comprehensive Income 179 219 341

Non Controlling Interest (25) (53) (102)

Normalised Basic Earnings 155 170 239

Normalised Earnings per Share (Cents) 33 31 43

Weighted Average Shares (Millions) 467 554 554

Results in a NutshellProfit after tax

38% Average Annual Growth

Other highlights

Conditional Put Option Liability of R728m

removed after Sanlam profit targets were

achieved

Cash balances stable at R770m after

significant investment in IT development

Financially

healthy to

grow!

Subsequent to year end, the WAD tranche 2

acquisition payment was settled in cash of

R140m (R195m less Sanlam’s contribution to

the acquisition).

Overall strengthening of current assets and

liabilities

Results in a Nutshell

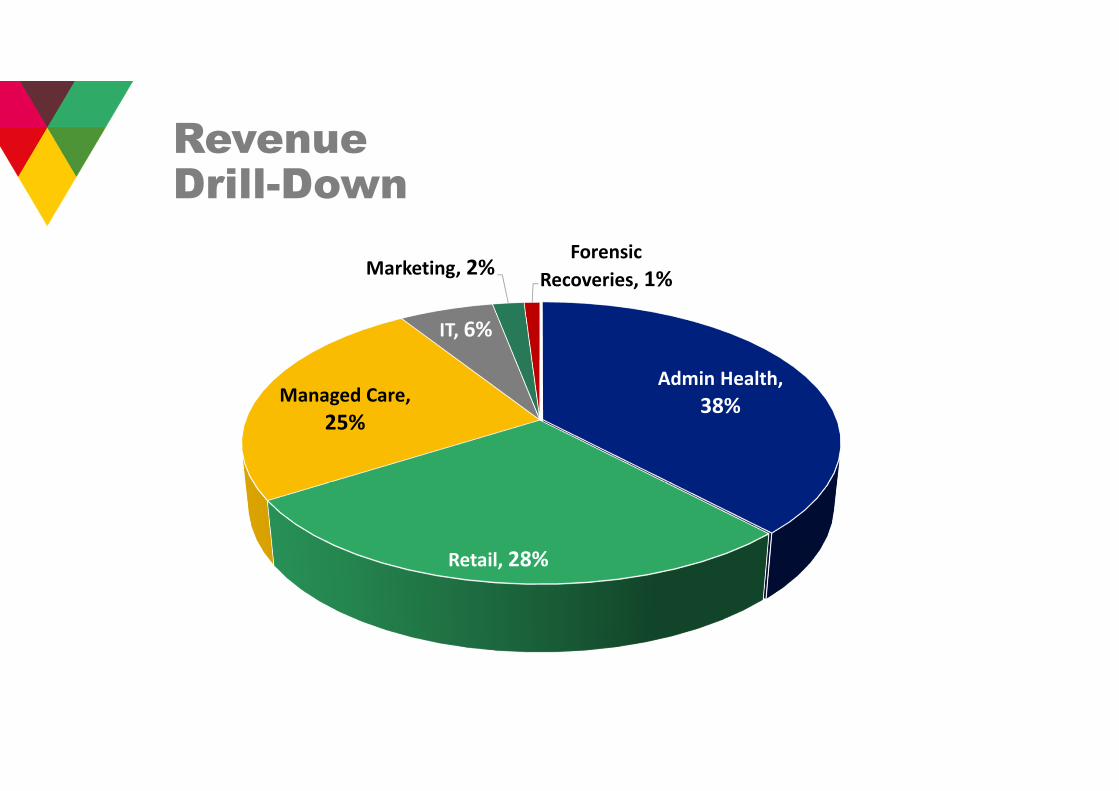

Revenue Drill-Down

Admin Health,

38%

Retail, 28%

Managed Care,

25%

IT, 6%

Marketing, 2%Forensic

Recoveries, 1%

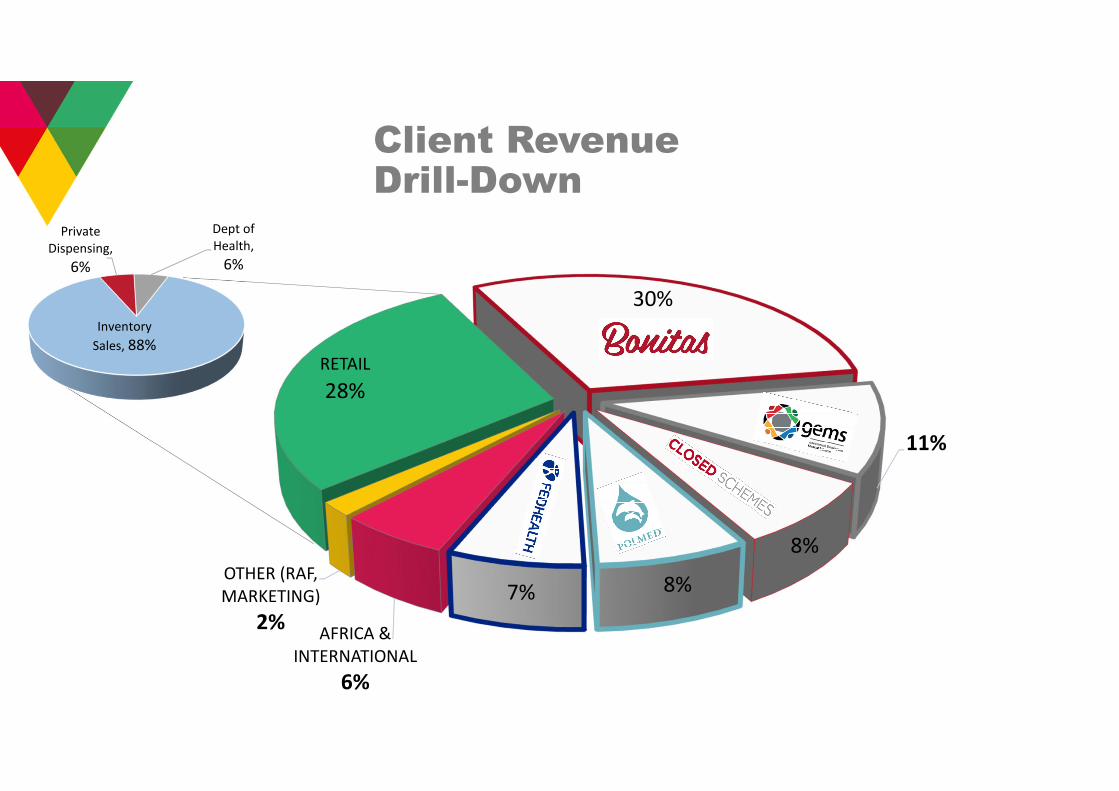

RETAIL

28%

30%

11%

8%

8%7%

AFRICA &

INTERNATIONAL

6%

OTHER (RAF,

MARKETING)

2%

Client Revenue Drill-Down

Inventory

Sales, 88%

Private

Dispensing,

6%

Dept of

Health,

6%

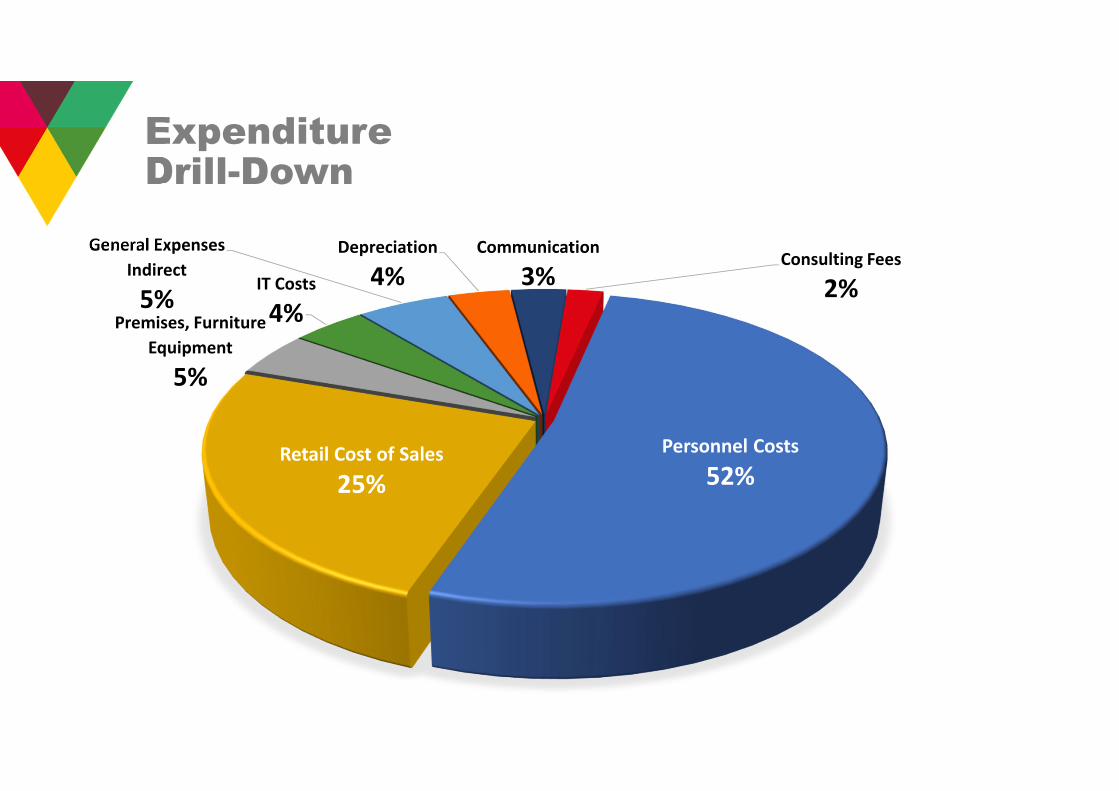

Personnel Costs

52%Retail Cost of Sales

25%

Premises, Furniture

Equipment

5%

IT Costs

4%

General Expenses

Indirect

5%

Depreciation

4%

Communication

3%Consulting Fees

2%

Expenditure Drill-Down

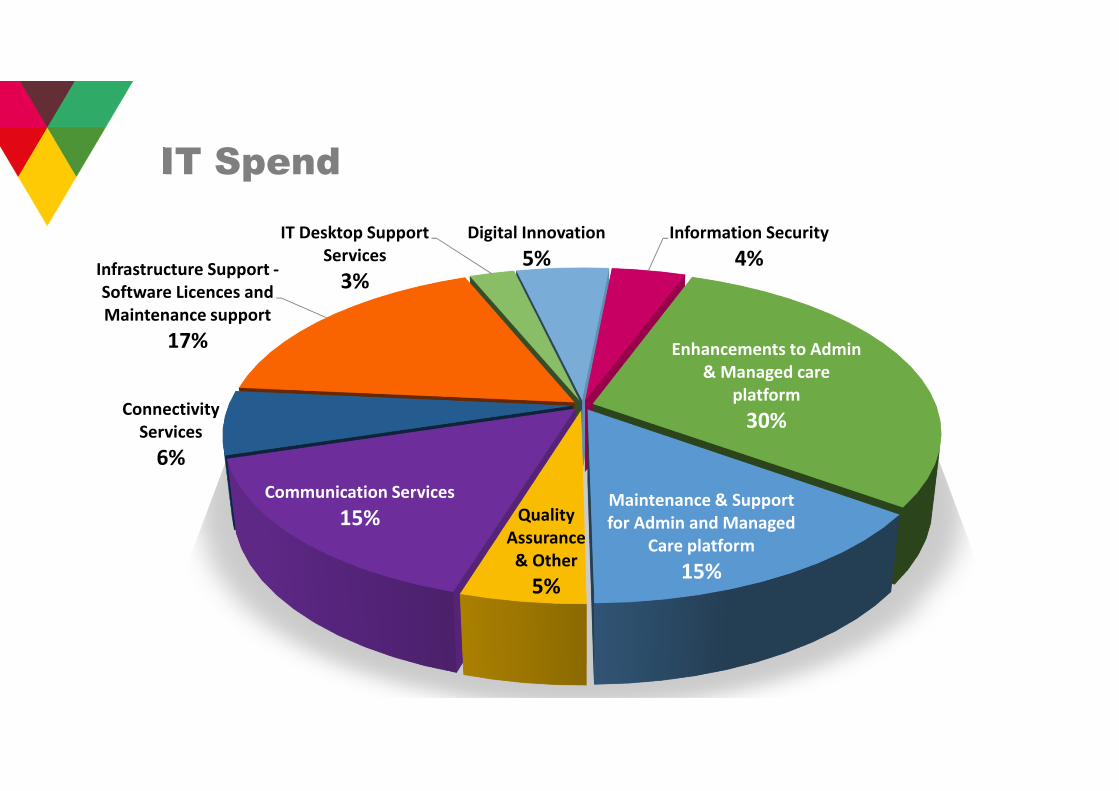

IT Spend

Enhancements to Admin

& Managed care

platform

30%

Maintenance & Support

for Admin and Managed

Care platform

15%

Quality

Assurance

& Other

5%

Communication Services

15%

Connectivity

Services

6%

Infrastructure Support -

Software Licences and

Maintenance support

17%

IT Desktop Support

Services

3%

Digital Innovation

5%

Information Security

4%

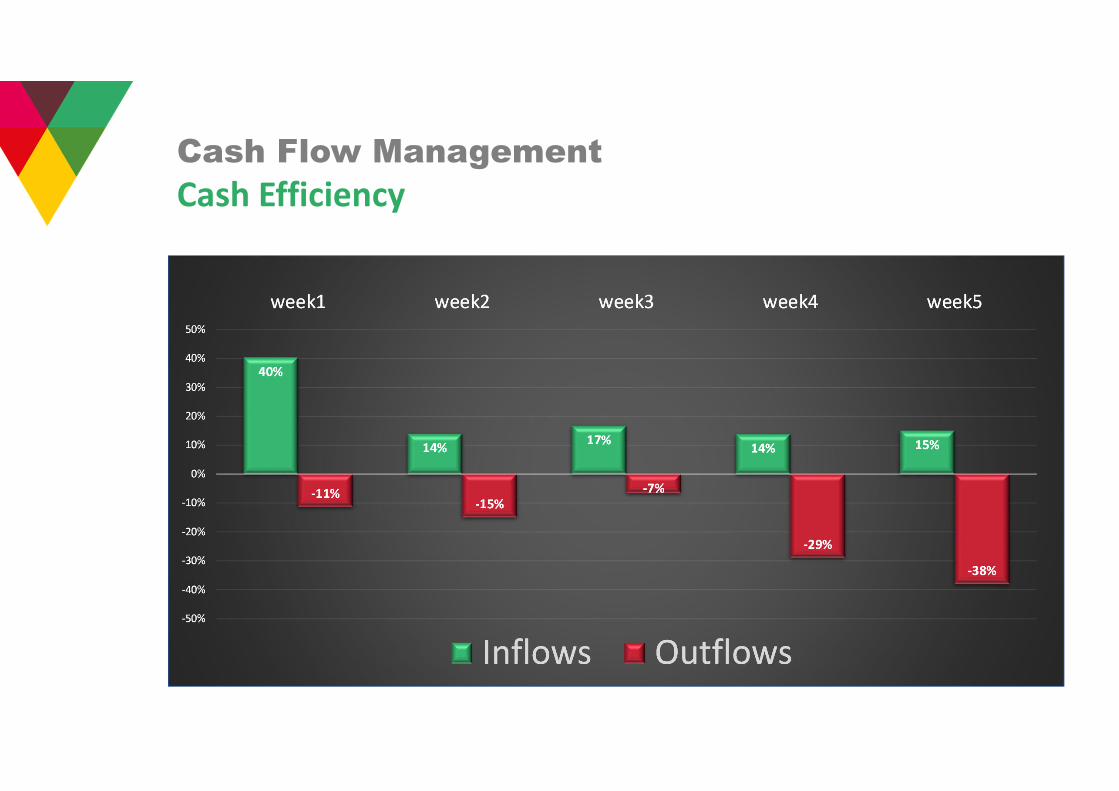

Cash Flow Management

40%

14%17%

14% 15%

-11%-15%

-7%

-29%

-38%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

week1 week2 week3 week4 week5

Inflows Outflows

Cash Efficiency

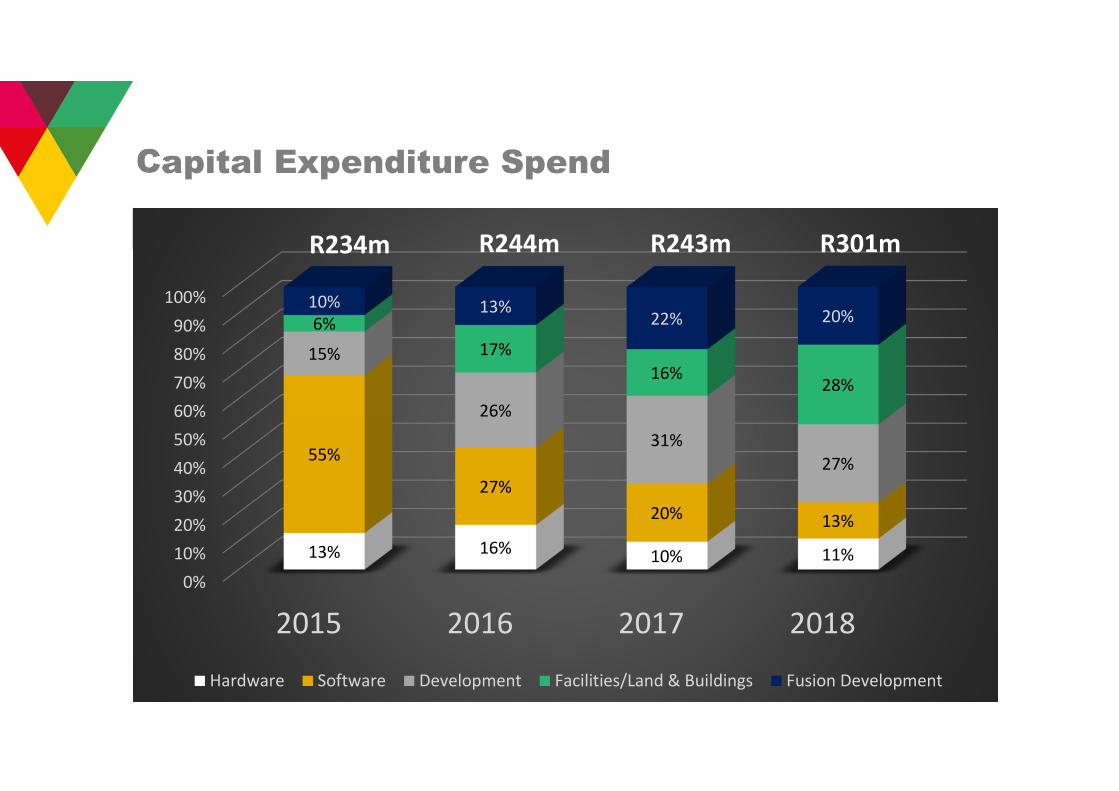

Capital Expenditure Spend

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018

13% 16%10% 11%

55%

27%

20% 13%

15%

26%

31%

27%

6%

17%

16%28%

10% 13%22% 20%

Hardware Software Development Facilities/Land & Buildings Fusion Development

R234m R244m R243m R301m

7.4 million Phone Calls 719 000

Customer Surveys

65.6 millionMember/Provider

emails sent 43.5 millionSMS’s sent

R30.8 billion Value of claims

processed

3.6 million Lives

Managed

590 000Member Cards

Distributed

925 000Hospital

Authorisations

In a year…

61.9 million Claims Processed

5 millionMobi Statements

sent out

6 millionChronic Scripts

processed and

delivered

R56.9 billion Contributions

Collected

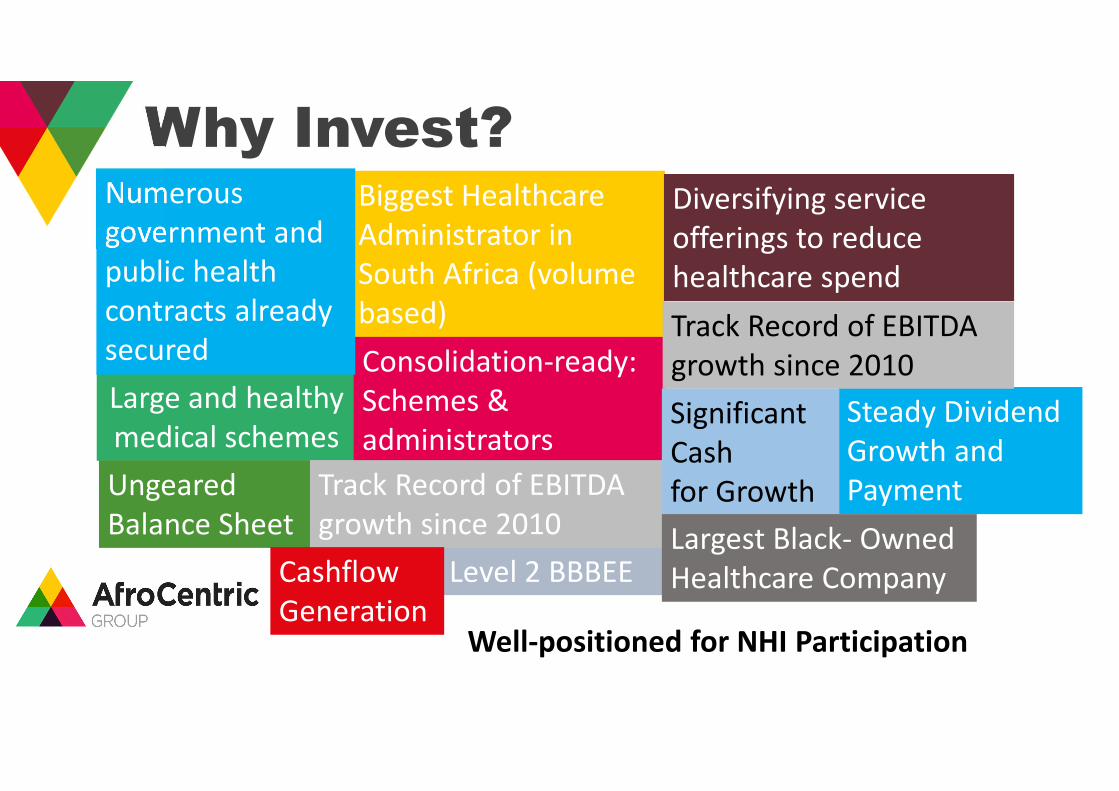

Level 2 BBBEE

Steady Dividend

Growth and

Payment

Why Invest?

Large and healthy

medical schemes

Ungeared

Balance Sheet

Well-positioned for NHI Participation

Biggest Healthcare

Administrator in

South Africa (volume

based)

Consolidation-ready:

Schemes &

administrators

Numerous

government and

public health

contracts already

secured

Diversifying service

offerings to reduce

healthcare spend

Track Record of EBITDA

growth since 2010

Track Record of EBITDA

growth since 2010

Cashflow

Generation

Significant

Cash

for Growth

Largest Black- Owned

Healthcare Company

Thank you for your time