Embed Size (px)

Citation preview

Domino’s Pizza Investor Presentation

Cowen and Company

7th Annual Consumer Conference

January 12, 2009

2

Forward-Looking Statements

This presentation and our accompanying comments include “forward-looking statements.”

These statements relate to future events or our future financial performance and are subject

to known and unknown risks, uncertainties and other factors that may cause our actual

results, levels of activity, performance or achievements to differ materially from those

expressed or implied by these forward-looking statements This presentation and our

accompanying comments do not purport to identify the risks inherent in an investment in

Domino’s Pizza and factors that could cause actual results to differ materially from those

expressed or implied in the forward-looking statements, include but are not limited to those

risk factors identified in Domino’s Pizza, Inc.’s Annual Report on Form10-K for the fiscal year

ended December 30, 2007, as well as other SEC reports filed by Domino’s Pizza, Inc. from

time to time. Although we believe that the expectations reflected in the forward-looking

statements are based upon reasonable estimates and assumptions, we cannot guarantee

future results, levels of activity, performance or achievements. We caution you not to place

undue reliance on forward-looking statements, which reflect our estimates and assumptions

and speak only as of the date of this presentation. We undertake no obligation to update the

forward-looking statements to reflect subsequent events or circumstances In light of the

above, you are urged to review the disclosures contained in the Domino’s Pizza, Inc. SEC

reports, including the risk factors contained therein.

This presentation contains trade names, trademarks and service marks of other companies.

We do not intend our use or display of other parties’ trade names, trademarks and service

marks to imply a relationship with, or endorsement or sponsorship of, these other parties.

Investment Questions for

Any Company in Today’s Environment

1. Is the business foundation strong?

• Business proposition

• Company position

2. Is the company stable?

3. Is the product attractive to consumers?

• Also needs to be affordable

4. Can the business grow?

5. Is the capital structure right for the business?

6. Does the company reward shareholders?3

4

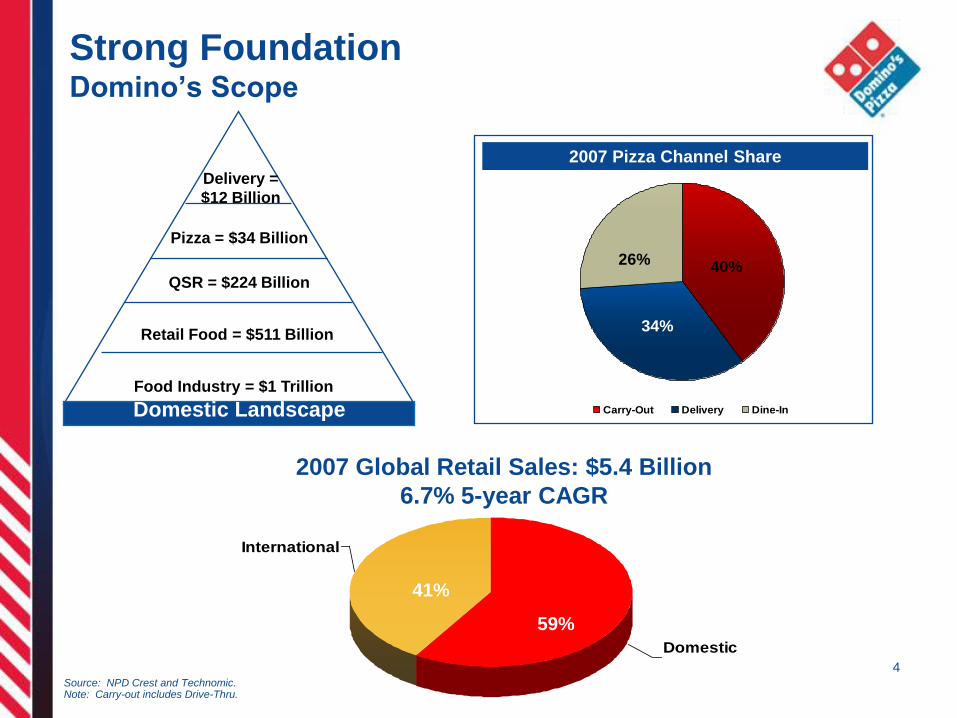

Strong FoundationDomino’s Scope

2007 Global Retail Sales: $5.4 Billion

59%

International

Domestic

2007 Global Retail Sales: $5.4 Billion

6.7% 5-year CAGR

41%

59%

2007 Pizza Channel Share

Carry-Out Delivery Dine-In

34%

40%26%

Delivery =

$12 Billion

Pizza = $34 Billion

QSR = $224 Billion

Retail Food = $511 Billion

Domestic LandscapeFood Industry = $1 Trillion

Source: NPD Crest and Technomic.Note: Carry-out includes Drive-Thru.

5

Domestic Stores Domestic Supply Chain International

Strong FoundationDomino’s Business Units

4,574 Franchised Stores

512 Company-Owned

Stores

17 Dough Manufacturing

& Distribution Facilities

1 Equipment and Supply

Facility

3,640 Franchised Stores

Currently no Company-

Owned Stores

6 Dough Manufacturing &

Distribution Facilities

As of Q3 2008

6

Strong FoundationDomino’s Unit Economics

○ Focused and efficient operating model1

• Delivery and carry-out…no dine-in

○ Low cost to open / operate

• $150K - $250K average cost range for new store

– Bargains available for purchase of turnaround stores

• Minimal square footage

• Makeline + oven

○ Steady cash-on-cash returns

Franchise Model Generates Sustainable Returns

¹ Statistics refer to domestic stores only

7

Strong Foundation The Franchise Model

• Franchisees drive Domino’s success

• “No Outside Business Interest” contract clause

– “Have to win with Domino’s Pizza”

• Down cycles as an opportunity to strengthen the system

• During the “perfect storm,” we experienced only nine

Chapter 11 bankruptcy proceedings in our franchise system¹

• Business model still works

– 70 new franchisees in the system through Q3 2008 (vs. 93 for FY

2007)

¹ Domino’s Franchise Service data November 2007 – January 2009

8

Stable Business

Proven 48-Year History

Strong and Consistent Cash Flow Generator

Able to Handle Leverage

Domino’s is a powerful global brand

#1 pizza delivery company in the U.S.

Strong and proven business model with superior returns

Large and growing international presence

Profitable, value-added supply chain

Experienced management team with proven track record

Stock is a value!

9

Stable Business Managing Commodities

Pricing pass-through on most items

– Provides stable dollar operating profit for Supply Chain

Multi-year purchasing agreement for cheese

– Lower volatility and improved budget planning

– Cheese prices have turned favorable in 2009

Supply Chain also manufactures dough

– Price of dough adjusted quarterly

Magnitude of Commodity Costs

Cheese

Meat

Boxes

Wheat

Sauce

Affordable Product High Household Penetration

• Virtually everyone eats pizza!

– Each man, woman and child in America eats an average of 46 slices

(23 pounds) of pizza each year¹

– 67% of the U.S. population eats pizza once a month²

• Domino’s Pizza can feed a family of four for $25

– Average ticket for a party of four eating QSR pizza: $25.11³

– Average ticket for a party of four at a casual dining restaurant: $54.20³

10

¹ Packaged Facts, New York

² Technomic

³ NPD / CREST through Sep 2008

11

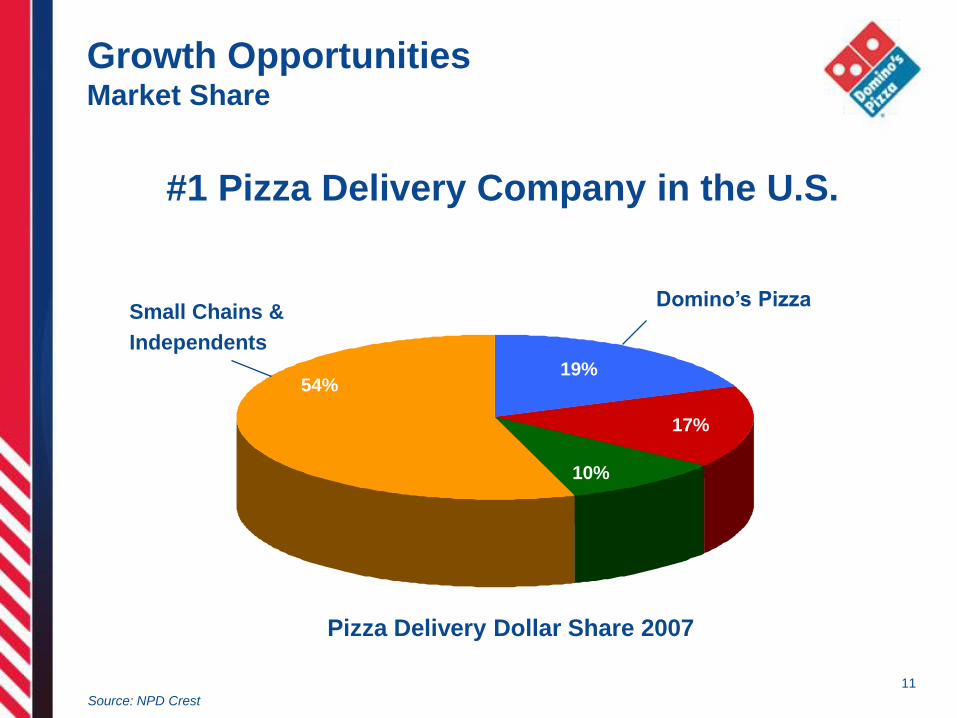

Pizza Delivery Dollar Share 2007

19%

17%

10%

54%

#1 Pizza Delivery Company in the U.S.

Still Room to Grow

Domino’s PizzaSmall Chains &

Independents

Source: NPD Crest 11

Pizza Delivery Dollar Share 2007

19%

17%

10%

54%

Growth Opportunities Market Share

#1 Pizza Delivery Company in the U.S.

Domino’s PizzaSmall Chains &

Independents

Source: NPD Crest

12

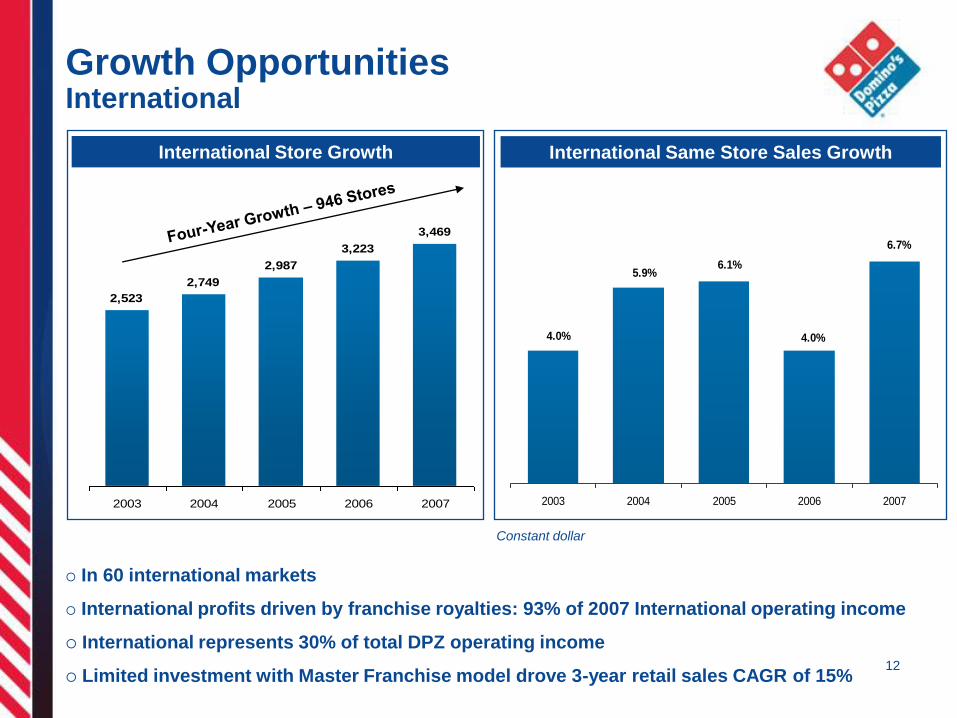

Growth OpportunitiesInternational

In 60 international markets

International profits driven by franchise royalties: 93% of 2007 International operating income

International represents 30% of total DPZ operating income

Limited investment with Master Franchise model drove 3-year retail sales CAGR of 15%

2,523

2,749

2,987

3,223

3,469

2003 2004 2005 2006 2007

4.0%

5.9%6.1%

4.0%

6.7%

2003 2004 2005 2006 2007

International Store Growth International Same Store Sales Growth

Constant dollar

13

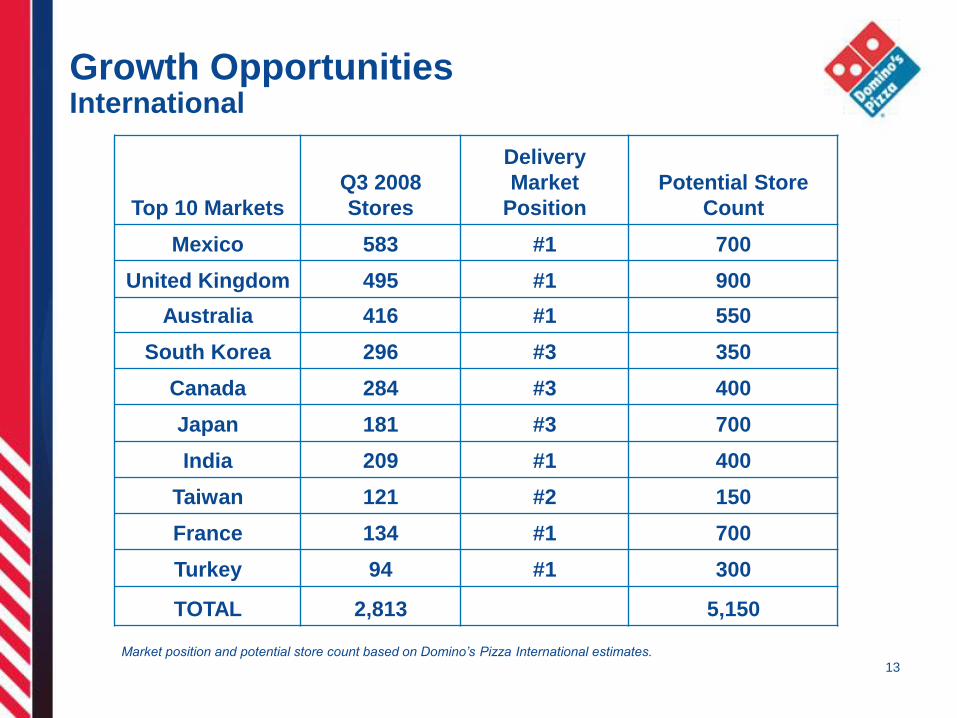

Growth OpportunitiesInternational

Market position and potential store count based on Domino’s Pizza International estimates.

Top 10 Markets

Q3 2008

Stores

Delivery

Market

Position

Potential Store

Count

Mexico 583 #1 700

United Kingdom 495 #1 900

Australia 416 #1 550

South Korea 296 #3 350

Canada 284 #3 400

Japan 181 #3 700

India 209 #1 400

Taiwan 121 #2 150

France 134 #1 700

Turkey 94 #1 300

TOTAL 2,813 5,150

Domestic Growth Opportunities…

• Traffic growth is key – bring excitement back to

Domino’s Pizza

– Sustainable, organic growth

– Today’s traffic = tomorrow’s same-store sales results

• Product platforms, not “product-of-the-month”

– LTOs don’t drive sustained traffic

– Day part expansion

• Timely consumer insight and strategic response

– Delivery charge “management”

– Flexible pricing model (“barbell”)

– Menu strategy

14

Proven Traffic Builder

• New product appeal

• New day part

• Beat Subway 2-to-1 in a national taste test 15

16

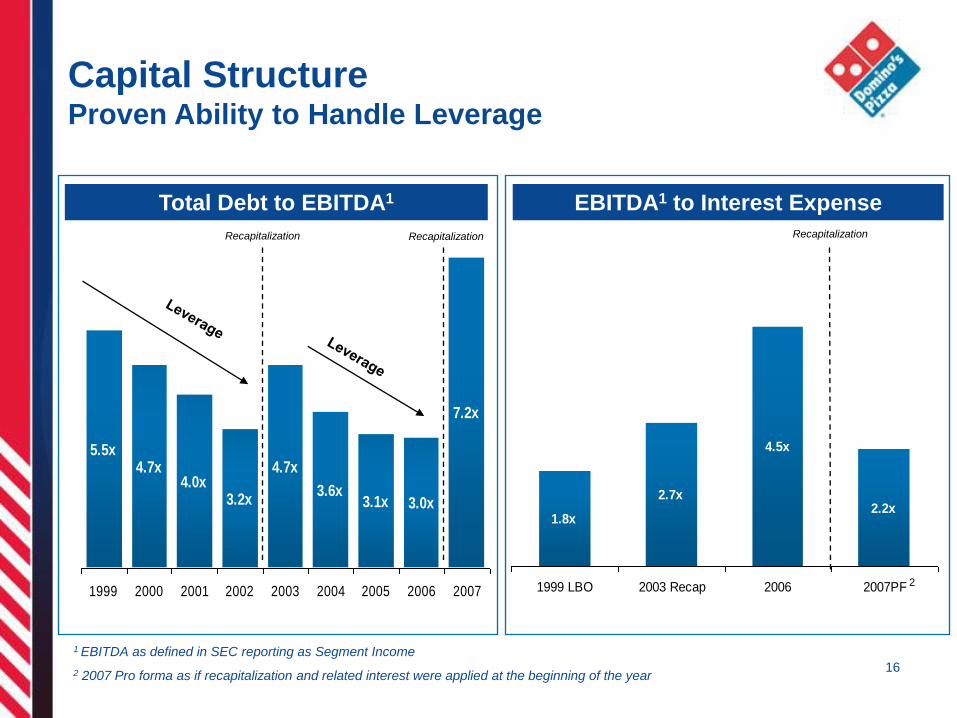

Capital Structure Proven Ability to Handle Leverage

5.5x4.7x

4.0x3.2x

4.7x

3.6x3.1x 3.0x

7.2x

1999 2000 2001 2002 2003 2004 2005 2006 2007

1.8x

2.7x

4.5x

2.2x

1999 LBO 2003 Recap 2006 2007PF

1 EBITDA as defined in SEC reporting as Segment Income

2 2007 Pro forma as if recapitalization and related interest were applied at the beginning of the year

2

Total Debt to EBITDA1 EBITDA1 to Interest Expense

RecapitalizationRecapitalizationRecapitalization

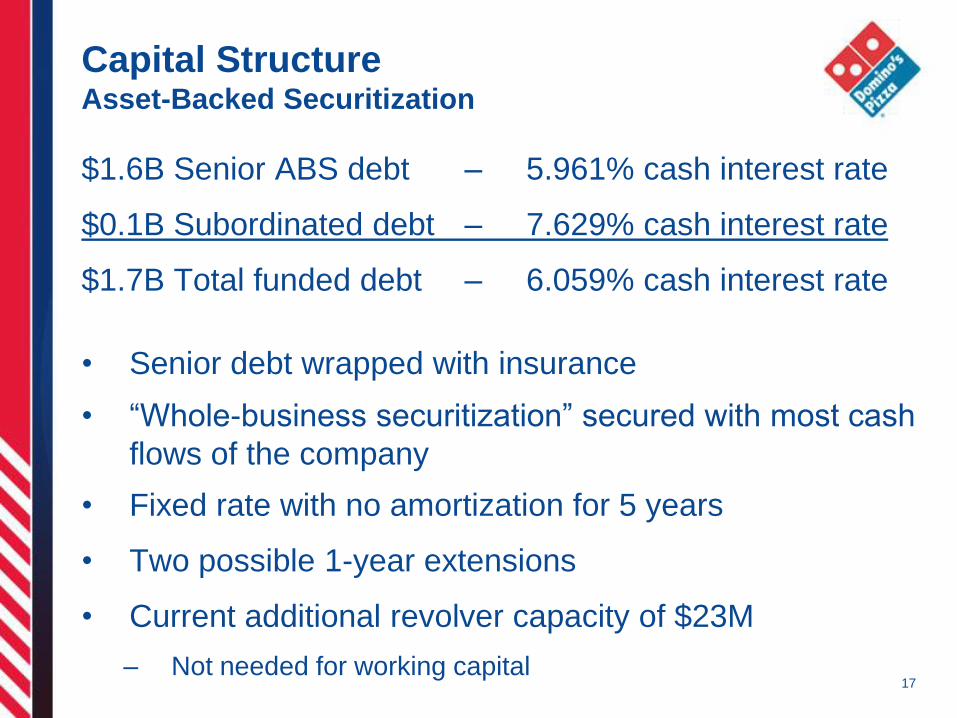

Capital StructureAsset-Backed Securitization

$1.6B Senior ABS debt – 5.961% cash interest rate

$0.1B Subordinated debt – 7.629% cash interest rate

$1.7B Total funded debt – 6.059% cash interest rate

• Senior debt wrapped with insurance

• “Whole-business securitization” secured with most cash

flows of the company

• Fixed rate with no amortization for 5 years

• Two possible 1-year extensions

• Current additional revolver capacity of $23M

– Not needed for working capital 17

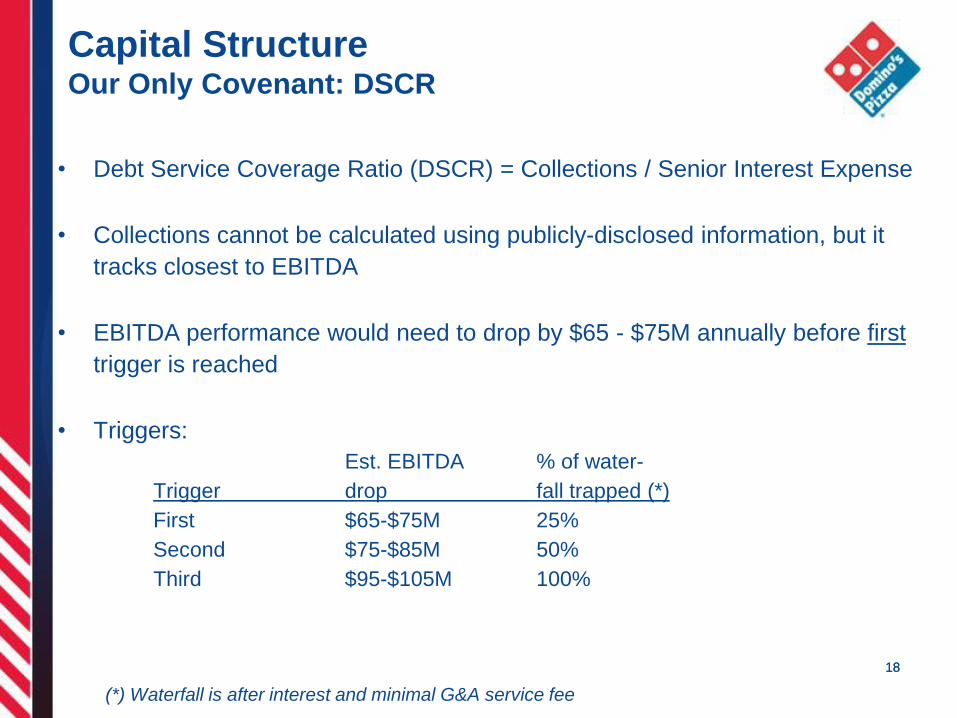

• Debt Service Coverage Ratio (DSCR) = Collections / Senior Interest Expense

• Collections cannot be calculated using publicly-disclosed information, but it

tracks closest to EBITDA

• EBITDA performance would need to drop by $65 - $75M annually before first

trigger is reached

• Triggers:

Est. EBITDA % of water-

Trigger drop fall trapped (*)

First $65-$75M 25%

Second $75-$85M 50%

Third $95-$105M 100%

(*) Waterfall is after interest and minimal G&A service fee

1818

Capital StructureOur Only Covenant: DSCR

19

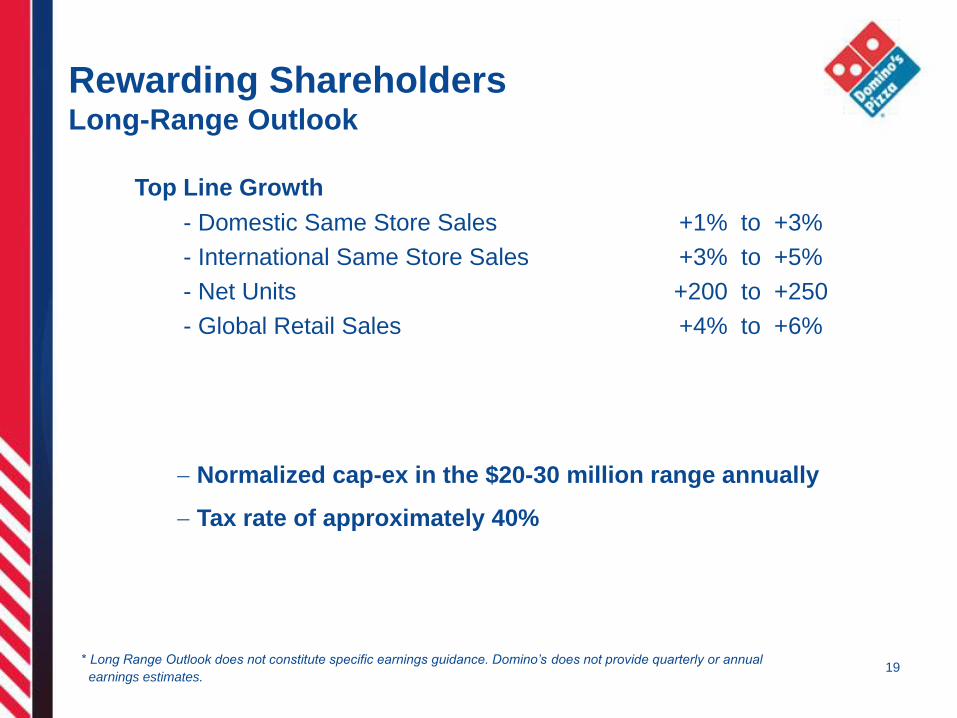

Rewarding ShareholdersLong-Range Outlook

Top Line Growth

- Domestic Same Store Sales +1% to +3%

- International Same Store Sales +3% to +5%

- Net Units +200 to +250

- Global Retail Sales +4% to +6%

* Long Range Outlook does not constitute specific earnings guidance. Domino’s does not provide quarterly or annual

earnings estimates.

Normalized cap-ex in the $20-30 million range annually

Tax rate of approximately 40%

20

Opportunities to Deploy Capital to Build

Shareholder Value

○ Investment in Growing Business

○ Pay Significant Dividends– Paid out $14.45 / share in quarterly and special dividends since

IPO, or over $900 million

○ Repurchase Shares– Repurchased 16.8 million shares for $315.5 million since IPO

– Authorized for a $200 million Open Market Repurchase Program

• Disbursed approximately 48% of authorized amount

○ Deleverage

Domino’s Pizza

Thank you!