Embed Size (px)

Citation preview

Doing businessin India

Suresh Surana & Associates

www.ss-associates.com

Suresh Surana & Associates

DOING BUSINESS IN INDIA

Foreword

Compiled by:

The Indian economy grew by about 7.2% p.a. during 2009-10 despite the challenges on account of slowdown faced by the global economies in the later part of 2008-09. The overall growth of the economy can directly be attributed to its strong fundamentals, renewed momentum in the manufacturing sector, infrastructure sector and growing contribution of the service sector. Increased emphasis has been laid by the policy makers on further integration of the economy with the global markets by laying a road map for implementation of the Goods and Services Tax (GST) and convergence of the financial reporting standards with International Financial Reporting Standards (IFRS).

The Indian Government plans to implement the Direct Taxes Code (DTC) from the fiscal year 2012-13 i.e. 1 April 2012. The basic purpose of the Direct Tax Code is to completely overhaul the complexities of the existing Income Tax Act, 1961 and to make the tax structure simple and also to provide a fair ground for collection and levy of taxes which would be light not only on the individual tax payers, but also corporate houses and also foreign residents.

India is fast becoming the “outsourcing destination of choice” of the world in sectors such as Information Technology, Pharmaceuticals, Banking and Finance, Insurance, Gem and Jewellery, Manufacturing etc. This is mainly due to the ample availability of competent and cost efficient workforce whereby setting up operations in India has become synonymous to efficient and cost effective operations. The growing Indian middle class population has placed India as “The market of the future”. As a result of these factors, many of the leading companies all over the world have already set up operations in India or are planning to do so.

We have compiled this guide to provide an overview of various social, legal, tax and commercial aspects in India, which can have a material impact on decision about doing business in India.

Given the limitations in compiling a booklet of this size, our intention is to offer a broad outline of the areas we feel are relevant to undertake business activities in India.

This guide cannot serve as a substitute for specific legal, tax or accounting advice concerning a business undertaking in India. Therefore, when specific issues occur in practice, it will be necessary to refer to the specific laws and regulations. Suresh Surana & Associates is not responsible for any action taken based on information contained in this guide and any liability arising from any statements or error contained in it.

Suresh Surana & Associates13th Floor, Bakhtawar,229, Nariman Point, Mumbai - 400 021.Tel: (+91-22) 6696 0644 Fax: (+91-22) 6121 4444Email: [email protected]: www.ss-associates.com

Suresh Surana & Associates

Doing businessin India

Suresh Surana & Associates

DOING BUSINESS IN INDIA

Economy

Tax Rates at a Glance (Financial Year 2010-11)

Foreign Investments

thØIndia is the 4 largest economy in the world in terms of Gross Domestic Product (GDP) based on Purchasing Power Parity (PPP) method. India's GDP of US$ 1.286 trillion at current prices makes it the twelfth largest economy in the world.

ØIndia witnessed a robust GDP growth in the last decade, averaging between 6-7% per annum and for the Financial Year 2010-11, the GDP growth rate of India is expected to be 8.4%.

ØExports for year ending on 31 March 2009 were US$ 185.3 billion and imports for the year ended on 31 March 2009 stood at US$ 303.7 billion.

ØAccording to the World Fact Book, India is among the world's youngest nations with a median age of 25 years as compared to 43 in Japan and 36 in USA. Of the BRIC—Brazil, Russia, India and China—countries, India is projected to stay the youngest with its working-age population estimated to rise to 70% of the total demographic by 2030, the largest in the world. India will see 70 million new entrants to its workforce over the next 5 years.

ØIndia continues to be the most preferred destination—among 50 top countries—for companies looking to offshore their information technology (IT) and back-office functions, according to global management consultancy, AT Kearney.

ØForeign Direct Investment (FDI) is permitted under automatic route except in certain prohibited activities and in certain activities with sectoral caps.

ØDividends and sale proceeds of shares are freely repatriable subject to payment of applicable taxes.

India - A Business Perspective

Income Tax Rates for Corporates, Firms:

1. Domestic Companies 33.2175% 30.90%

2. Foreign Companies 42.23% 41.20%

3. Partnership Firms 30.90% 30.90%

Income Tax Rates for Individuals, HUF, BOI, AOP

4. As per Income Slabs (INR) 0% to 30.90%

Sr.No. Particulars Income

exceedingRs. 1 crore

Incomeup to

Rs. 1 crore

Rate of Tax

Suresh Surana & Associates

Marine Drive, Mumbai

DOING BUSINESS IN INDIA

India - CEOs Speak

Olli-Pekka KallasvuoNokia

“India today is not an emerging economy. It has fully emerged, and it is in full bloom.”

Tom EndersAirbus

“You can't be global without being in India - with its large number of highly skilled, motivated and knowledgeable people.”

Andrew Holland

DSP Merrill Lynch

“I believe that India's growth is on the runway, ready to take off.”

Kensaku KonishiCanon India

“One of the fastest growing economies in the world, India is an excellent country for any company to be in.”

Karl-Heinz FloetherAccenture

"We are delighted and impressed with the growth we have been able to achieve in this country. India is a key node in Accenture's global delivery network.”

Michael DellDell Computers

"India can become a major part of Dell's operations and a major source of the human capital that Dell takes on as a company...and we are looking for further opportunities to take advantage of skilled labour."

International Monetary Fund

"India will be key engine of world economy in next decade"

Mike S. ZafirovskiMotorola Inc.

"Not only are there brilliant engineers here [in India], I've been seeing that the entrepreneurial spirit of the businesses is second to none.”

McKinsey & Co.

"India has an extraordinary talent pool with virtually limitless potential”

Jack WelchGeneral Electric

"A truly global company will be one that uses the intellect and resources of every corner of the world . India is a developed country as far as intellectual capital is concerned. The opening of (offshore) development centres mark a new level of commitment by GE in india."

Suresh Surana & Associates

Hawa Mahal, Jaipur

Contents

DOING BUSINESS IN INDIA

Co

nte

nts

CHAPTER 1 : INDIA A PROFILE

PHYSICAL FEATURESGeography............................................................................................................... 1Climate..................................................................................................................... 1

POPULATION AND SOCIAL PATTERNSPopulation............................................................................................................... 1Language ................................................................................................................ 2Religion.................................................................................................................... 2Education ................................................................................................................ 2

GOVERNMENT AND POLITICAL SYSTEMGovernment Structure......................................................................................... 2

LEGISLATIVE AND LEGAL ENVIRONMENTLegislation .............................................................................................................. 2Legal Environment................................................................................................ 3

INFRASTRUCTURETransport................................................................................................................. 3Communication...................................................................................................... 4

Suresh Surana & Associates

DOING BUSINESS IN INDIA

Education ................................................................................................................ 4Medical Services.................................................................................................... 4Housing.................................................................................................................... 4

INTERNATIONAL RELATIONS AND ASSOCIATIONS..................................... 4

CERTAIN KEY INFORMATION FOR VISITORS TO INDIAIndian Currency ..................................................................................................... 5Visitors' Visas......................................................................................................... 5Indian Standard Time ........................................................................................... 5Business Hours ...................................................................................................... 5Public Holidays ...................................................................................................... 6Tourism.................................................................................................................... 6Attire Code.............................................................................................................. 6

FRAMEWORK.......................................................................................................... 8

ECONOMIC TRENDS.............................................................................................. 9

ECONOMIC SECTORS ........................................................................................... 10

REGULATORY ENVIRONMENTInvestor Protection ............................................................................................... 10Price Controls......................................................................................................... 11Registration of Intellectual Property................................................................ 11Competition Policy................................................................................................ 13Environmental Regulation................................................................................... 13

FINANCIAL SECTORBanking System ..................................................................................................... 13Insurance Sector ................................................................................................... 14Capital Market........................................................................................................ 14Stock Exchanges ................................................................................................... 15Specialized Financial Institutions...................................................................... 16Investment Institutions........................................................................................ 16Mutual Funds .......................................................................................................... 16Non Banking Finance Companies ...................................................................... 17Credit Rating Agencies ........................................................................................ 17

INCENTIVES FOR INDUSTRIESConcessional Finance........................................................................................... 17Central Government Investment Study ........................................................... 17State Government Incentives............................................................................. 18

CHAPTER 2 : INDIAN BUSINESS AND INVESTMENT ENVIRONMENT

Suresh Surana & Associates

DOING BUSINESS IN INDIA

INCENTIVES FOR EXPORTS................................................................................ 18

ENERGY, MINERALS AND OTHER

NATURAL RESOURCES........................................................................................ 19

FOREIGN TRADE.................................................................................................... 19

OTHER FACTORS

Language ................................................................................................................ 19

Trained Manpower................................................................................................. 19

Low Research and Development Costs............................................................ 20

Financial Reliability............................................................................................... 20

FORMS OF BUSINESS ENTITIES

Companies .............................................................................................................. 22

Branches of Foreign Companies ........................................................................ 23

Liaison Offices ....................................................................................................... 24

Project Office ......................................................................................................... 25

Partnerships ........................................................................................................... 26

Trusts ....................................................................................................................... 26

Limited Liability Partnerships (LLPs)............................................................... 26

SETTING UP A COMPANY

Incorporation of a Company............................................................................... 29

Initial Capital Requirements ............................................................................... 31

Kinds of Shares...................................................................................................... 32

Debentures ............................................................................................................. 33

Public Deposits ...................................................................................................... 33

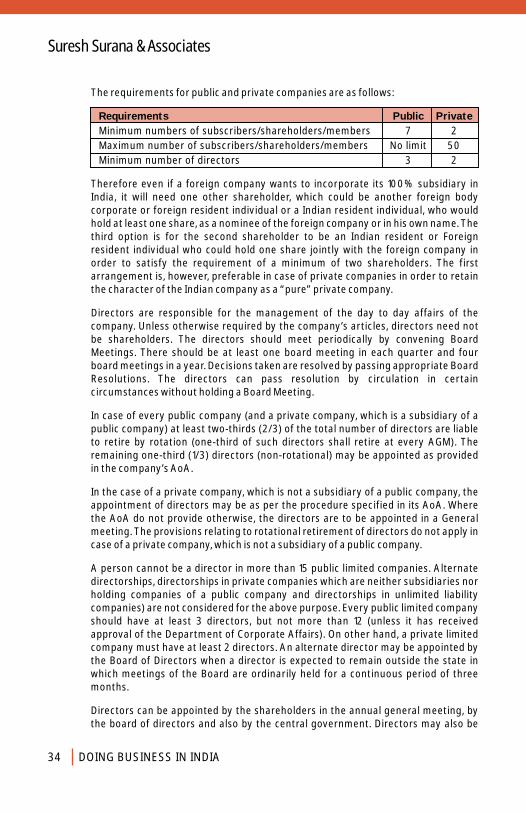

Directors.................................................................................................................. 33

Managing Director ................................................................................................ 35

Secretary................................................................................................................. 35

STATUTORY REQUIREMENTS FOR COMPANIES

Annual Reports...................................................................................................... 36

Audit Requirements.............................................................................................. 36

Shareholders' Meetings ....................................................................................... 37

Online Filing System............................................................................................. 38

Filing of Documents / Returns ........................................................................... 38

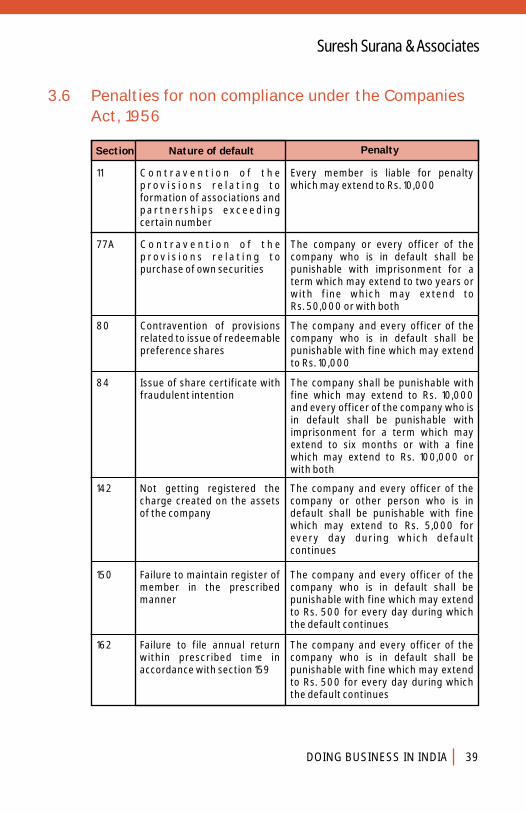

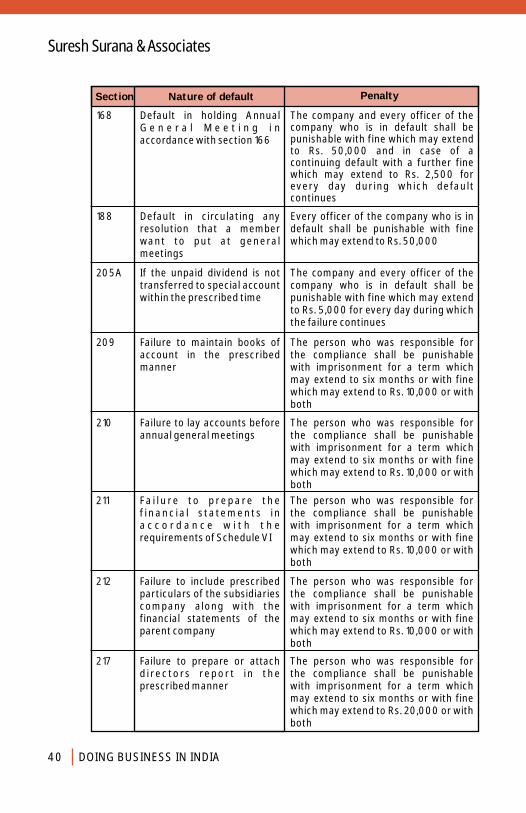

Penalties for non compliance under the Companies Act, 1956 ................. 39

CHAPTER 3 : BUSINESS ENTITIES

Suresh Surana & Associates

DOING BUSINESS IN INDIA

SIGNIFICANT COMPANY LAW REGULATIONS

Loans and Guarantees to Companies............................................................... 42

Loans and Guarantees to Directors .................................................................. 42

Disclosure of Interest by Directors.................................................................... 42

Dividends................................................................................................................. 42

Mergers.................................................................................................................... 43

Buy-back of shares ............................................................................................... 43

Audit Committee ................................................................................................... 44

Producer Companies ............................................................................................ 44

Takeovers ................................................................................................................ 44

Corporate Governance......................................................................................... 45

Winding Up.............................................................................................................. 47

BACKGROUND........................................................................................................ 49

LEGISLATIVE PROVISIONS

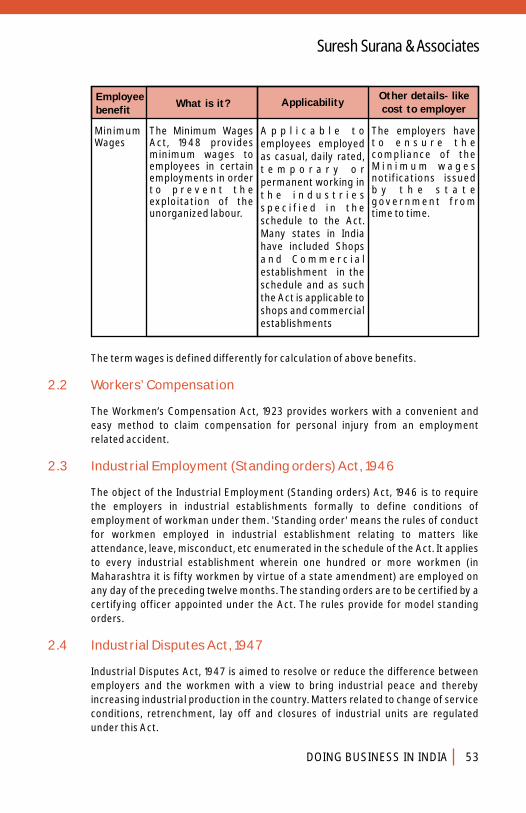

Mandatory Employee Benefits........................................................................... 49

Workers' Compensation....................................................................................... 53

Industrial Employment Act ................................................................................. 53

Industrial Disputes Act......................................................................................... 53

Equal Remuneration Act...................................................................................... 54

Contract Labour Act............................................................................................. 54

Trade Unions Act ................................................................................................... 54

Health and Safety.................................................................................................. 54

ENGAGEMENT OF FOREIGN NATIONALS........................................................ 56

INTRODUCTION ..................................................................................................... 58

EXCHANGE CONTROL REGULATIONS

Introduction............................................................................................................ 58

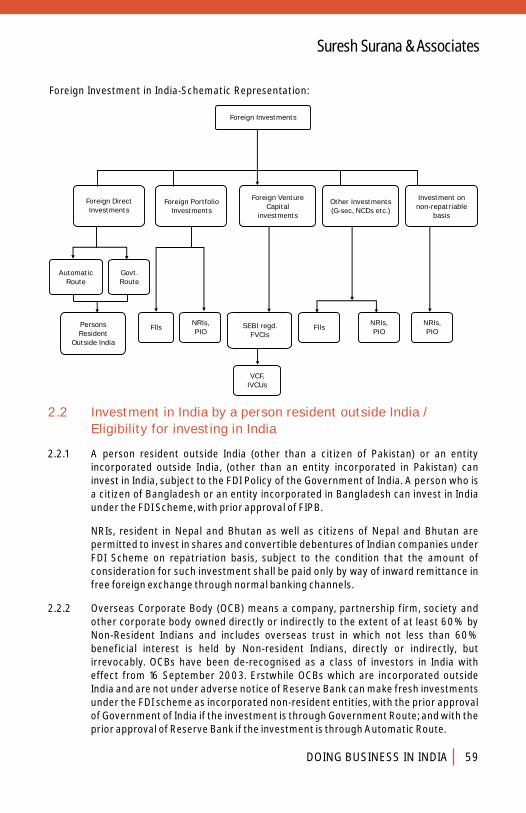

Investment in India by a person resident outside India ............................... 59

Prohibition on investments................................................................................. 60

CHAPTER 4 : HUMAN RESOURCES

CHAPTER 5 : FOREIGN INVESTMENT IN INDIA

Suresh Surana & Associates

DOING BUSINESS IN INDIA

INVESTMENT UNDER VARIOUS FOREIGN INVESTMENT SCHEMES

Automatic Route of FDI ....................................................................................... 61

Investments in Sectors where 100% FDI Under Automatic

Route is not available........................................................................................... 61

Certain Important Aspects of the FDI Scheme .............................................. 62

Investments by Foreign Institutional Investors (FII) ..................................... 62

Investments by Non Resident Indians (NRI) ................................................... 63

Investments by Venture Capital Fund............................................................... 64

Purchase of Other Securities by FIIs ................................................................ 65

Purchase of Other Securities by NRIs.............................................................. 65

Foreign Investment in Tier I and Tier II instruments

issued by banks in India....................................................................................... 66

Issue of rights / bonus shares to erstwhile

Overseas Corporate Bodies (OCBs) .................................................................. 66

Additional allocation of rights shares by

resident to non-residents .................................................................................... 67

Issue and acquisition of shares after merger or de-merger

or amalgamation of Indian companies............................................................. 67

Issue of shares under Employee Stock Options Scheme to

persons resident outside India........................................................................... 67

Transfer of Securities of Indian Companies by a Person

Resident Outside India......................................................................................... 68

Transfer of Securities of Indian Companies by a Person

Resident in India.................................................................................................... 69

Conversion of ECB/Lumpsum Fees / Royalty /

Import of Capital Goods by SEZ into equity ................................................... 69

Issue of shares by Indian companies ADR / GDR ......................................... 70

Investment in firm or proprietary concern in India....................................... 70

Establishment in India of a Branch or Liaison Office

or Project Office ................................................................................................... 71

EXTERNAL COMMERCIAL BORROWINGS (ECB)

Automatic Route ................................................................................................... 73

Approval Route ...................................................................................................... 76

Time period for realization of Export payments ........................................... 80

Time period for payments towards Import obligation ................................. 80

EXCHANGE CONTROL REGULATIONS FOREIGN TECHNOLOGY

TRANSFER AND ROYALTY PAYMENTS............................................................ 80

Suresh Surana & Associates

DOING BUSINESS IN INDIA

ANNEXURE 1

Sectors Prohibited for FDI................................................................................... 81

ANNEXURE 2

Sector specific guidelines for FDI...................................................................... 81

INTRODUCTION ..................................................................................................... 93

INCOME TAX ON CORPORATIONS

General Structure and Scope ............................................................................. 93

Rates of Tax ............................................................................................................ 93

Minimum Alternate Tax........................................................................................ 94

Fringe Benefits Tax ............................................................................................... 94

Dividend Distribution Tax .................................................................................... 94

Taxable Income...................................................................................................... 97

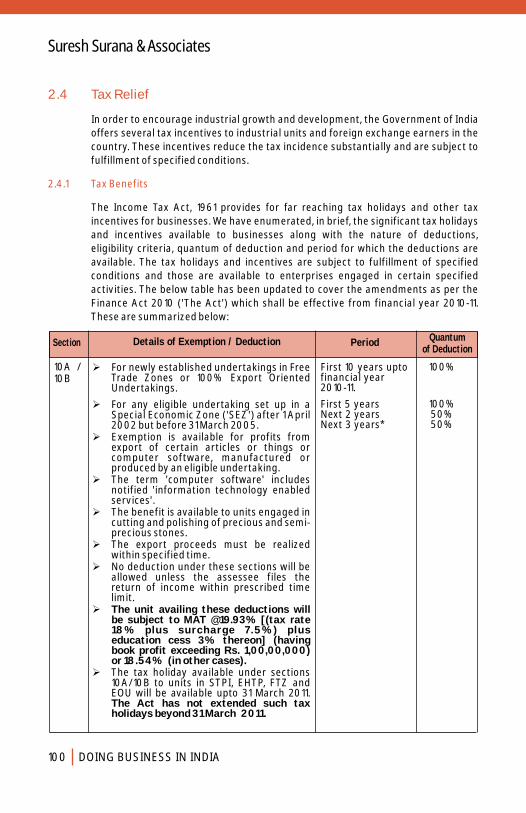

Tax Benefits / Reliefs............................................................................................ 100

Transfer Pricing Regulations .............................................................................. 114

Relief for Tax losses.............................................................................................. 115

Returns and Payment of Taxes .......................................................................... 115

INCOME TAX ON NON-CORPORATES

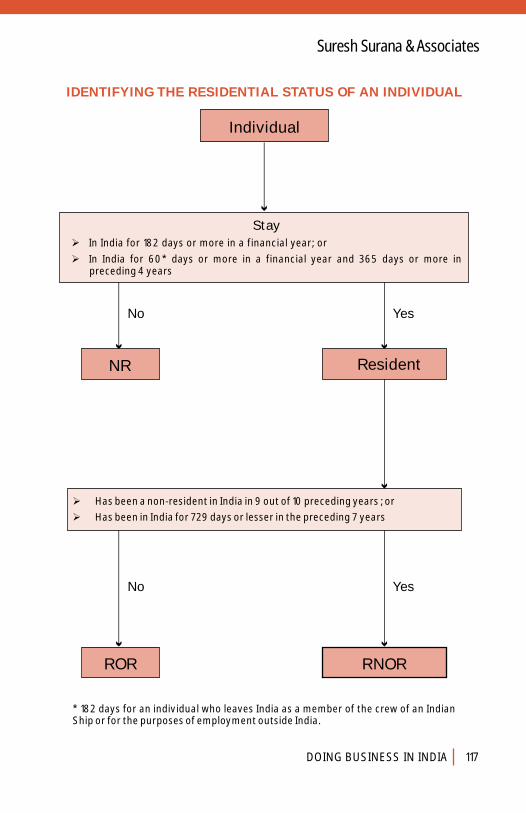

Residential Status ................................................................................................. 116

Rates of Tax ............................................................................................................ 118

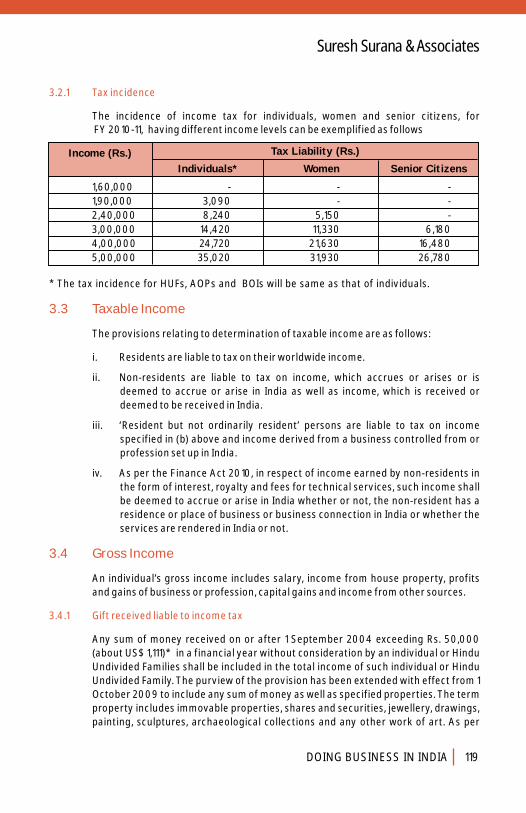

Taxable Income...................................................................................................... 119

Gross Income.......................................................................................................... 119

Capital Gains Tax ................................................................................................... 120

Deductions and Reliefs ........................................................................................ 120

Clubbing of Minor's Income ................................................................................ 121

Relief for Tax losses.............................................................................................. 121

Returns and Payments of Taxes ........................................................................ 121

Presumptive Scheme for Small Businesses .................................................... 121

SPECIAL PROVISIONS FOR COMPUTATION OF

TAXABLE INCOME OF NON-RESIDENTS

Non-residents engaged in Specified Business ............................................... 122

CHAPTER 6 : TAXATION SYSTEM

Suresh Surana & Associates

DOING BUSINESS IN INDIA

Income of Non-resident Indians......................................................................... 122

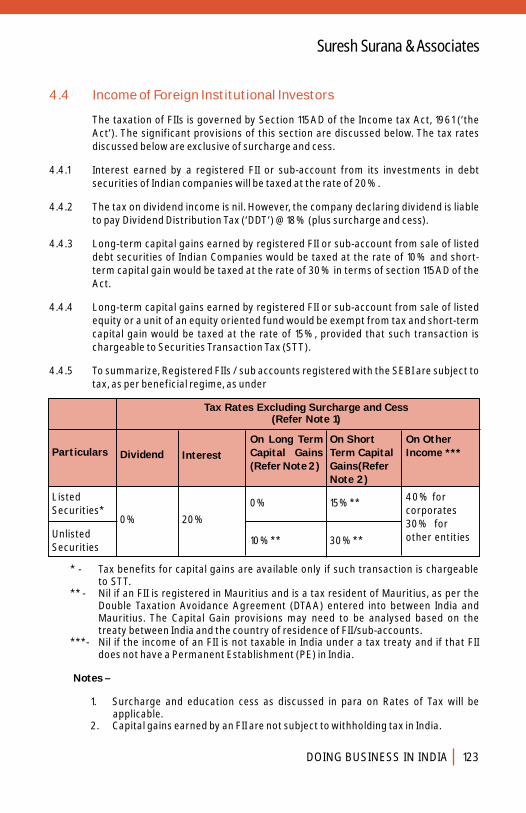

Income of Foreign Institutional Investors........................................................ 123

Income of Offshore Funds................................................................................... 124

WITHHOLDING TAXES.......................................................................................... 124

DOUBLE TAX TREATIES....................................................................................... 124

OTHER ADMINISTRATIVE ASPECTS

Audit Reports ......................................................................................................... 125

Assessment Procedure ........................................................................................ 125

Advance Rulings .................................................................................................... 126

OTHER DIRECT TAXES

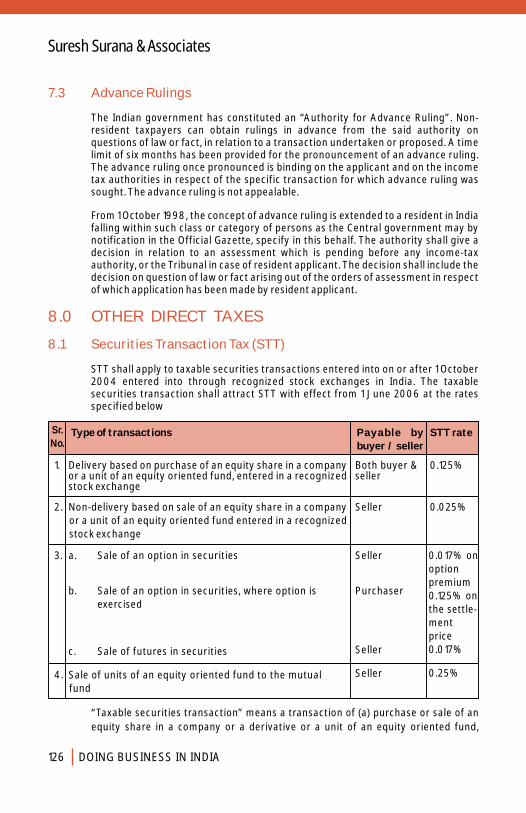

Securities Transaction Tax .................................................................................. 126

Wealth Tax............................................................................................................... 127

Gift Tax..................................................................................................................... 127

Estate Duty ............................................................................................................. 127

Interest Tax ............................................................................................................. 127

INDIRECT TAXES

Goods and Services Tax ('GST') ......................................................................... 128

Central Value Added Tax ('CENVAT') ................................................................ 128

Customs Duty......................................................................................................... 128

Service Tax.............................................................................................................. 129

DIRECT TAX CODE ('DTC') ................................................................................... 130

INTERNATIONAL FINANCIAL REPORTING STANDARDS ('IFRS') .............. 131

ANNEXURE I

Double Taxation Avoidance Agreements ('DTAA') Rates ............................. 133

ANNEXURE II

Tax Deduction At Source ('TDS') Rates............................................................ 140

Suresh Surana & Associates

Chapter 1India - A Profile

Golden Temple, Amritsar

DOING BUSINESS IN INDIA 1

CHAPTER 1

INDIA - A PROFILE

1.0 PHYSICAL FEATURES

1.1 Geography

1.2 Climate

2.0 POPULATION AND SOCIAL PATTERNS

2.1 Population

India is situated in the southern Peninsula of the Asian continent and is the seventh largest country in the world, in terms of size. It lies entirely in the northern hemisphere and extends from the snow-covered Himalayan heights in the north to the tropical rain forests of the south. India shares its borders with Afghanistan and Pakistan to the north-west, China, Bhutan and Nepal to the north, and Myanmar and Bangladesh to the east. Sri Lanka lies to south of India and is separated from India by a narrow sea channel formed by the Palk Strait and the Gulf of Mannar.

0 0 0 0India lies between latitudes 8 4’ and 37 6’ north and longitudes 68 7’ and 97 25’

east. It measures about 3,214 kilometers from north to south between its extreme latitudes and 2,933 kilometers from east to west between the extreme longitudes. India covers an area of 3,287,263 square kilometers and has a land frontier of 15,200 kilometers. India has a coastline of 7,516 kilometers.

The main land comprises of four regions: the mountain zone in the north, the plains of the Ganges and the Indus rivers, a small desert region in the west and the southern peninsula which consists of the Deccan plateau, mountains and coastal strips.

India’s climate is mainly tropical monsoon type and is affected by two seasonal winds: the north-east monsoon and the south-west monsoon. A year in India can be conveniently divided into four sessions viz. the winter (January and February), the hot weather summer (March through May), the rainy south-western monsoon (June through September) and the post-monsoon period (October through December), which is known as the north-east monsoon period in the southern Peninsula.

As per the data published for 2001 census, India’s population as on March 2001 was 1028 million (532 million males and 496 million females), making India the second most populated country in the world after China. The population comprises of 300 million people in the middle class bracket, which is a major consumer class in India. The population growth rate was around 2.22% in the 1980s, which decreased marginally to 2.14% in 1990s.

Suresh Surana & Associates

2.2 Language

2.3 Religion

2.4 Education

3.0 GOVERNMENT AND POLITICAL SYSTEM

3.1 Government Structure

4.0 LEGISLATIVE AND LEGAL ENVIRONMENT

4.1 Legislation

India is a land of many languages and dialects. Hindi is the official language of the Indian federation or union, while English is commonly used business language. English language is acceptable for all the legal, commercial and business documentation and communications.

More than 80% of India’s population is Hindus and around 13% are Muslims. The other major religious communities are Christian, Sikh, Buddhist and Jain.

Data published for 2001 census revealed that 64.80% of the total population are literate and consisted of 75.30% men and 53.70% women. Amongst the youth the literacy rate is 82%.

The Indian federation or union is organized into 28 states and 7 union territories with a single and uniform citizenship and a single judiciary. The capital of the Indian government is the state of Delhi.

India is a sovereign, socialist, democratic and secular republic with a parliamentary system of government, which is based on the U.K. parliamentary system. The parliament is headed by the President and consists of two houses - the Lok Sabha (the house of the people) and the Rajya Sabha (the council of states). Although the President is the constitutional head of the government, the real executive power resides with the Council of Ministers, with the Prime Minister as its head. The Council of Ministers is collectively responsible to the Lok Sabha.

The Indian Constitution provides for the independence of other government bodies for certain key areas like the judiciary, the Comptroller and Auditor General, the Public Service Commissions and the Election Commission.

Indian Constitution divides the various responsibilities into three categories: the Union list, the State list and the Concurrent list. Parliament can make laws on subjects in the Union list and the state legislature on subjects in the State list. Both, the parliament and the state legislature can make laws on the subjects included in the Concurrent list. This division helps in regulating the relations between the Union and the States.

DOING BUSINESS IN INDIA2

Suresh Surana & Associates

4.2 Legal Environment

5.0 INFRASTRUCTURE

5.1 Transport

The main sources of law in India are the Constitution statutes, customary laws and

case laws. The country’s constitution provides for a single integrated system of

courts to administer both Union and state laws. The judiciary in India is separated

from the executives.

At the apex of the entire judicial system is the Supreme Court of India, which

consists of the Chief Justice and other judges. The Supreme Court has original,

appellate and advisory jurisdiction and its decisions are binding on all courts within

the territory of India. Each state (or two or more states together) has a High Court, a

Chief Justice of the High Court and other judges who are appointed by the President

in consultation with the Governor of the state. There is a hierarchy of subordinate

courts under the various High Courts, which extend to the local courts, which decide

civil and criminal disputes of petty and local nature.

Internal public transportation in India is fairly well developed. The country is

extensively covered by rail and road networks. This surface transport network is

fairly supplemented by airline routes connecting the major cities.

The Indian Railways, which is the largest public sector undertaking in India, is the

backbone of the Indian Economy. It caters to both freight and passenger traffics and

has a vast network of 6,867 stations spread over route length of about 62,900 kms.

It is Asia’s largest and the world’s second largest railway system under a single

management.

India has the second largest road network in the world with total road length of 3.3

million kms. In 2009, freight traffic on the road is also fairly high and remains almost

exclusively in the private sector.

Inland water transport has not grown appreciably in the country because of poor

port or landing infrastructure. However, the industry is now growing and the

government is ambitiously developing coastal shipping.

India has bilateral air services agreements with over 100 countries. Air India is

India’s official national carrier operating across both domestic and international

routes. In 2007, Indian Airlines the domestic national carrier was merged with Air

India. Indian Airlines also operates on some international routes. Upon the

liberalization of the economy, an open sky policy was announced which has resulted

in a number of private air taxi companies operating on some of the major trunk

routes. Some of the major private air transport companies, operating on domestic

and international routes are Jet Airways, Kingfisher Airlines, Indigo, Spice jet etc.

DOING BUSINESS IN INDIA 3

Suresh Surana & Associates

DOING BUSINESS IN INDIA4

5.2 Communication

5.3 Education

5.4 Medical Services

5.5 Housing

6.0 INTERNATIONAL RELATIONS AND ASSOCIATIONS

The Indian telephone, telex and facsimile services both within India and to international locations are fair. Total fixed and cellular connections in India was exceeding 494 million as on August 2009 and are expected to cross 500 million mark by 2010. An electronic mail service is also available and is fast catching up in the leading cities. The total number of internet connections in India are exceeding 14 million and the broadband subscribers are about 6 million. The number of internet users is estimated to be around 81 million in India.

Apart from the above services, India has a fairly well developed postal services department. In fact India has the highest number of post offices in any country (155,000 post offices). Major international courier service companies are also well represented in India.

Apart from schools, which provide education in the local language, India has good day schools and boarding schools that offer a high standard of education in English. In addition, special expatriate schools provide education for American, French, German and Japanese children.

Scholarships are available under grants from the Ministry of External Affairs for foreign students from select countries for graduate and postgraduate courses in engineering, technology, management, medicine, pharmacy and general courses.

India has a fairly widespread and reasonably developed network of medical facilities. However, private enterprises and trusts operate a well-developed infrastructure of hospitals and polyclinics in major metropolitan areas and medium-sized towns.

Adequate housing is available in most of the major metropolitan areas and in large and medium-size towns. The rates tend to be higher in areas closer to the central business district and lower in the suburbs. Apartments and houses are usually available for outright purchase or on rent for maximum renewable periods of 60 months. Deposits equivalent to 10 or 15 times a month’s rent are generally required in case of premises to be rented.

India has entered into bilateral agreements with a number of countries and is a member of several international organizations, such as the United Nations, the Commonwealth, the GSTP, UNCTAD, WTO and GATT. India has always taken initiatives to develop friendly relations with its neighbours and has adopted a policy

Suresh Surana & Associates

DOING BUSINESS IN INDIA 5

of non-alignment to promote co-operation amongst all the nations. India has had an active role in the Non-Aligned Movement and is also an active member of the South Asian Association for Regional Cooperation (SAARC). India is a member of Multilateral Investment Guarantee Agency (MIGA). MIGA serves as an insurer of investments made in member countries against stipulated political risks in the host country and also offers assistance in attracting new investment.

Apart from the Indo-EC Joint Commission, India has separate bilateral commissions with Belgium, Cyprus, Finland, France, Germany, Italy, Netherlands, Spain, Sweden, Switzerland, Turkey and the United Kingdom.

The Indian monetary unit is the Rupee (Rs. or INR). The Indian central bank viz. Reserve Bank of India (RBI), is the sole authority for issuing currency in India. Currency converting agencies have a reasonably spread network across all major cities, tourist destinations and airports, where all leading currencies can be converted to Indian rupees and vice versa.

From March 1993 the government has permitted a floating exchange rate for the rupee, which is expressed in terms of the US dollar. The exchange rate for the rupee as on 13 May 2010 was US $ 1 = Rs. 44.99 and Euro 1 = Rs 56.98.

Every foreigner entering India is required to possess a passport and visa. Visas (tourist, business or entry) are issued on application to the Indian High Commission. The visas normally expire six months from the date of issue. If the visa allows more than one entry into the country, it must be used for the first time within six months from the issue date.

Indian Standard Time (IST) is five and one-half hours ahead of Greenwich Mean Time.

The normal working week in India is usually Monday through Friday (9.30 a.m. to 5.30 p.m.). However, there are many organizations, which also work half day on Saturdays or work on alternate Saturdays. Sunday is a public holiday. Banking hours are generally between 10 a.m. and 3.00 p.m. on weekdays and 10 a.m. to 1.00 p.m. on all Saturdays, though some of the banks are now offering 24 hours banking. Internet banking and telephone banking is also offered by most of the leading banks.

7.0 CERTAIN KEY INFORMATION FOR VISITORS TO INDIA

7.1 Indian Currency

7.2 Visitors’ Visas

7.3 Indian Standard Time

7.4 Business Hours

Suresh Surana & Associates

DOING BUSINESS IN INDIA6

7.5 Public Holidays

7.6 Tourism

7.8 Attire Code

The statutory public holidays vary from state to state and number around 20 in a year. Holidays in private sector organizations generally vary from 10 to 15.

There are various historic sites available to visitors. Hundreds of ancient temples and mosques as well as other monuments provide a view not only of India’s past but also its cultural and trade connections with the rest of the world.

There are several wildlife and game sanctuaries, winter sports facilities in the northern region and water sports facilities in beach towns. The states of Maharashtra, Goa, Kerala, Tamil Nadu and Orissa have attractive beaches, which are popular destinations of visiting foreign tourists. Some of the world’s large hotel chains as well as leading time-sharing leisure resort groups have a presence in India.

In an effort to promote tourism in the country, both the Indian Railways and Indian Airlines offer round trip passes to tourists making payment in foreign currency.

Being a tropical country, clothing is often light, including formal office wear. Suits and jackets are common in the cities but are usually restricted to senior corporate executives.

Suresh Surana & Associates

Bombay Stock Exchange, Mumbai

Chapter 2Indian Business AndInvestment Environment

DOING BUSINESS IN INDIA8

CHAPTER 2

INDIAN BUSINESS ANDINVESTMENT ENVIRONMENT

1.0 FRAMEWORK

India adopted a mixed economy after independence, resulting in the public and private sectors’ co-existence in industrial activity. In the past, the public sector had a dominant role in the economy. However, with the recent liberalization, the trend is clearly towards a larger role for the private sector. The government has restricted fresh public investments to only strategic and essential infrastructure areas. The government is also divesting its equity in public sector enterprises outside these areas.

The majority of business in India has been controlled by state-owned corporations, business families and groups under multinational control. However, this dominance is getting eroded with the entry of technocrats and successful first-generation entrepreneurs. In many substantial private sector companies, the promoters hold a minority stake but are able to retain control because of the widely dispersed holdings. The public financial institutions hold large chunks of equity in many major Indian private sector companies, but their involvement in the management decisions is very limited and neutral. India also has a huge base of closely held small and medium sized businesses, which cater to the local and regional markets.

The Indian government earlier exercised considerable control over the private sector through licensing of the setting up of manufacturing capacities; approval procedures for importing foreign capital, technology, capital goods, and raw materials and allocation procedures for basic raw materials. However, the new policies launched in the 1990s and continued thereafter in the new millennium by the Government are dismantling many of the regulations and restrictions that have previously made business operations in India difficult. Now, the Government has initiated steps for introducing second-generation structural reforms to keep pace with the global environment of competition after removal of trade barriers as per the agreement entered into with World Trade Organization and correct the various distortions in the economy. The emerging economic environment is more competitive, dynamic and inviting to foreign investment and technology. Recently, the Government of India significantly liberalized the foreign direct investment policy for crucial sectors including banks, drugs, pharmaceuticals, construction, arms and ammunitions and certain areas of telecommunication.

The Indian rupee has been made fully convertible on the trade and current account and full convertibility on the capital account has been recommended. This full convertibility will allow free convertibility of Indian financial assets to foreign financial assets and vice versa at market determined rates. In order to create a suitable legal framework for the implementation of full convertibility on capital

Suresh Surana & Associates

DOING BUSINESS IN INDIA 9

account and to liberalize the movement of foreign capital, a new law called the Foreign Exchange Management Act (FEMA) has come into effect from 1 June 2000.

The global economic meltdown and the consequent recession in the developed countries over the past year, has adversely impacted the Indian economy. In 2009-10, the Gross Domestic Product (GDP) is expected to grow at 7.2% which is quite encouraging considering in retrospect the decline in GDP to 6.7% in 2008-09 representing a drop of 2.1% from the average growth rate of 8.8% in the previous five years (2003-04 to 2007-08). Inspite of this, India is likely to remain the second fastest growing major economy. India was able to sustain a respectable growth rate and is expected to bounce back quickly, mainly due to its reliance on domestic demand and largely unaffected banking sector.

The Inflation as measured by the Wholesale Price Index (WPI) for the 2008-09 was 5.9%. A noteworthy development during 2008-09 was a sharp rise in the WPI inflation followed by an equally sharp fall, with the WPI inflation falling to unprecedented level of close to 0% by March 2009. The inflation WPI index for the period April-December 2009 has decreased to 1.6%.

Foreign exchange reserves which had declined to US$ 252 billion as on 31 March

2009 from US$ 309 billion as on 31 March 2008, has increased to US$ 283.5 billion as on 31 December 2009.

The total exports for 2008-09 increased by 13.6% to US$ 185 billion. The total imports for 2008-09 was about US$ 304 billion wherein the growth in imports was 20.47% in 2008-09.

There has been a sharp decline in the Rupee exchange rates during 2008-09, wherein the currency depreciated by over 21% against the US$. The exchange rate as on 15 August 2009 was Rs. 48.79 against 1 US$. However, the rupee has strengthened in the latter period and the exchange rate as on 13 May 2010 was Rs. 44.99 against 1 US$. The fiscal deficit during the period shot up from 5.9% to 6.5% of the GDP.

Indian stock markets experienced a downturn after having experienced a long spell of growth between 2005 to early 2008 which is directly attributable to the current international crisis resulting in an immediate effect of withdrawal of FII Investments.

2.0 ECONOMIC TRENDS

2006-07 2007-08 2008-09

10

12

8

6

4

2

0

GDP Growth Rate

9

6.7

9.8

2009-10

7.2

2006-07 2007-08 2008-09 2009-10

1400

1200

1000

800

600

400

200

0

GDP (US$ Billion)

Suresh Surana & Associates

DOING BUSINESS IN INDIA10

This resulted in a fall in the Bombay Stock Exchange indices (Sensex) from its closing of 17,578 on 28 February 2008 to a low of 7,697, on 27 October 2008. However, due to improvement in the economic scenario, high sentiments and positive election results and emphasis of government policies on growth, the Sensex has regained some lost ground and reached a level of 16,430 as on 26 February 2010.

Although India was primarily an agricultural country, the service sector is rapidly increasing its share in the economy. The share of agriculture and allied sectors in GDP has declined gradually from 18.9% in 2004-05 to 14.6% in 2009-10, whereas the share of industry has remained the same at about 28% and services has gone up from 53.2% to 57.2%.

The Indian Regulatory policy is driven by three objectives: to promote competition, to protect consumers and investors from restrictive and unfair trade practices, and to maintain the ecological balance and protect the environment. The major governing statutes for trading, commercial and industrial enterprises in the country are the Foreign Exchange Management Act, 1999; the Companies Act, 1956; Competition Act, 2002; Securities and Exchange Board of India, 1992 (SEBI); Regulations for Listed Companies and the Banking Regulation Act, 1949; which governs the operations of banks including foreign banks. Since, the Foreign Exchange Management (FEMA) Act, 1999 regulates foreign investment in India, it has the greatest effect on foreign companies operating in India.

SEBI was constituted as a statutory body under the SEBI Act, with effect from 30 January 1992 to monitor the activities of stock exchanges, merchant bankers, mutual funds, brokers and other intermediaries. All applications for share issues must be vetted by SEBI to ensure that the offer documents disclose the required information. SEBI has also issued guidelines for disclosure and investor protection, monitoring the work of merchant bankers, grading of prospectus, responsibilities of lead managers, number of lead managers in every issue, etc.

The legal framework for protecting the interests of investors is provided by the Companies Act, 1956 and the Securities Contracts (Regulation) Act, 1956. In order to protect the interests of investors in the securities market and to develop the capital market, SEBI was established. SEBI controls the securities market through its detailed guidelines issued to all the players in the securities market. SEBI regulations have rendered insider trading a punishable offence in specified circumstances. The guidelines governing takeovers, public issues, capital adequacy requirements, disclosure norms, etc. are being increasingly streamlined. Investors having grievances have the option of either applying to the Monopolies and Restrictive Trade Practices Commission or writing to the SEBI Investor Grievance Cell and informing the concerned stock exchange. They can also file complaints with various authorities under the Consumer Protection Act, 1986.

3.0 ECONOMIC SECTORS

4.0 REGULATORY ENVIRONMENT

4.1 Investor Protection

Suresh Surana & Associates

DOING BUSINESS IN INDIA 11

4.2 Price Controls

4.3 Registration of Intellectual Property

4.3.1 Trademarks

4.3.2 Patents

Prices of certain essential consumption goods, raw materials and intermediate products are directly regulated by the government. The government amended the Monopolies and Restrictive Trade Practices Act in 1991 to increase protection for consumers. In addition, the Consumer Protection Act, 1986 created quasi-judicial mechanisms at the district, state and national levels to settle consumer grievances. There is, however, a distinct trend towards reduction in pricing and distribution controls, and the government’s policy is to do away with administered prices as far as possible. At present, the new free market has transferred economic power to the more aware and demanding consumer.

India being one of the signatories to Trade Related Aspects of Intellectual Property Rights (TRIPS) under the General Agreement on Tariffs and Trade (GATT) under the World Trade Organization (WTO) it has to comply with the provisions of TRIPS which aims to rationalize the laws of Intellectual Property Rights of all member countries which includes Trademarks, Patents, Industrial Designs, Copyrights, Geographical Indications, etc. In view of the above, India has amended its Intellectual Property Laws (IPR) namely, Trade Marks Act, Industrial Designs Act, Copyrights Act and Patents Act in line with TRIPS Agreement.

The Trade Marks Act 1999, allows registration of marks not only used in connection with goods but also in respect of marks in relation to services. Trademarks once registered will be valid for a period of 10 years and the same can be renewed for successive periods of 10 years thereafter. Registration of trademarks confers on the registered proprietor of the trade mark the exclusive right to use the trademark in relation to its goods / services in respect of which the trademark is registered and to obtain relief in respect of infringement of the trademark by others. Infringement of trademarks is a cognizable and non-bailable offence. However, all infringement of trade marks are not treated as cognizable and non-bailable offence.

The Patents Act, 1970 as amended by the Patents (Amendment) Act, 2002 and Patent (Amendment) Act, 2005 provides for the grant of a patent for any “invention”. Invention means a new product or process involving an inventive step and capable of industrial application. Inventive step means a feature that makes the invention not obvious to a person skilled in the art. Protection under the Patents Act is available for a period of 20 years for every patent.

There is no distinction between Indian nationals and foreign nationals concerning the right to obtain patents. Every international application under the Patents Corporation Treaty for a patent, designating India shall be deemed to be an application under the Patents Act, 1970, provided a corresponding application is filed before the Controller in India. The government has the power to acquire patents for a public purpose. In the said event, the act preserves the patent holder’s right to be compensated adequately.

Suresh Surana & Associates

After expiry of three years from the date of grant of the patent, any person may make a request for grant of licence to work on the patented invention by making an application to the Controller of Patents alleging that reasonable requirements of the public with respect to the patented invention have not been satisfied or the patented invention is not available to the public at a reasonable price.

With a view to fulfill the requirements of any treaty, convention or arrangement between India and any other country, the Patents Act allows the Indian government to declare a country as a “convention country”. India has entered into bilateral arrangements with Canada, Ireland, Australia, New Zealand, Sri Lanka and the United Kingdom to accord their citizens priority in respect of grant of patents and the protection of patent rights and on reciprocal basis similar privileges to Indian Citizens.

In line with TRIPS, the Patents Act, 1970 has been amended by Patent (Amendment) Act, 2002 and Patent (Amendment) Act, 2005. The Amendment provides the period of patent in all cases shall be for a term of 20 years instead of 14 years and 7 years.

The Designs Act, 2000 protects all features of shapes, configurations, patterns or ornaments in a design that appeal to the eye in the finished article. Registration of a design with the Controller General of Patents and Designs confers on the registered proprietor a right to take action against third parties if the design is used fraudulently. The act provides protection to a registered design for 10 years at first instance which can be further renewed for a period of 5 years (altogether for maximum 15 years) and thereafter it becomes public property.

Copyrights vest in authors on the creation of their works and require no registration. If registered, however, registration provides prima facie evidence of a copyright’s validity. Copyright is regulated as per the provisions of The Copyright Act, 1957.

Copyrights subsist in the following classes of work:ØOriginal literary, dramatic, musical and artistic worksØCinematograph filmsØSound recordingØPhotographs.

Copyright also subsists in computer programs (which are defined as “programs recorded on any disc, tape, perforated media or other information storage device that is fed into or located in a computer or computer-based equipment capable of reproducing any information”).

The Copyrights Act, 1957 provides for copyright enforcement. A person whose copyright is infringed may sue for civil relief such as an injunction and damages, and may institute criminal proceedings for infringement in certain cases.

4.3.3 Designs

4.3.4 Copyrights

DOING BUSINESS IN INDIA12

Suresh Surana & Associates

The Central Government by order may direct that all or any provisions of this Act shall apply to works of other countries. This means that any person who enjoys a copyright in one of the convention countries automatically enjoys a statutory protected copyright in India.

The newly enacted Competition Act, 2002, has constituted the Competition Commission of India (‘CCI’) which is empowered to ensure free and fair competition in the market. The Competition Act aims at preventing practices having adverse effect on competition, to promote and sustain competition in markets, to protect the interest of consumers and to ensure freedom of trade carried on by the other participants in the markets in India. The main purposes of the Competition Act are (a) Prohibition of anti-competitive agreements, (b) Prohibition of abuse of dominant position, and (c) Regulation of combinations.

All proposed industrial units have to obtain environmental clearance from the relevant air and water pollution control boards, which operate under the Ministry of Environment and Forests.

India has a vast network of about 88,408 bank branches that held deposits of about Rs. 38,341 billion as of 31 March 2009.

The Indian central bank is the Reserve Bank of India (RBI) and its primary function is to act as the banker and financial adviser to the government, the commercial banks and some of the other financial institutions. It is the sole authority for the issue of bank notes and the supervisory body for all banking operations in the country. Its other functions include execution of the government’s monetary policy, regulating the money flow in the economy and acting as the custodian of India’s foreign exchange reserves.

The commercial banks may be classified into the following five categories:

i. The State Bank of India and its associate banksii. Other nationalized banksiii. Private sector banksiv. Regional rural banks and v. Foreign banks

The commercial banks transact all types of commercial banking business. They are also allowed to set up (with the prior approval of the RBI) subsidiaries to engage in

4.4 Competition Policy

4.5 Environmental Regulation

5.0 FINANCIAL SECTOR

5.1 Banking System

5.1.1 Reserve Bank of India (RBI)

5.1.2 Commercial Banks

DOING BUSINESS IN INDIA 13

Suresh Surana & Associates

non-banking finance activities viz. merchant banking, equipment leasing etc. The Commercial banks, apart from providing working capital facilities for various sectors of the economy, also provide capital market advisory services, foreign exchange services, investment consultancy and personal banking services.

Regional Rural Banks: The regional rural banks are set up to increase the flow of credit to smaller borrowers in the rural areas. They may be said to be special purpose banks catering primarily to the rural agricultural sector.

Foreign Banks: Most of the major banks from major countries are represented in India through branches, network offices, representative office or agency arrangements. Foreign banks offer a variety of services including foreign-currency loan syndication, foreign exchange risk management and other innovative financial products. Approximately 42 foreign banks operate through the major cities in India.

Private Sector Banks: Private sector banks have gained a strong foothold in the Indian banking scenario in the last decade. The private banks in India offer a wide gamut of banking and financial services.

The primary legislation that deal with insurance business in India are Insurance Act, 1938 and Insurance Regulatory & Development Authority (IRDA) Act, 1999. Government of India has opened up the sector to private participation in recent past. Details of permissible foreign investment in this sector is discussed separately. There are more than 10 companies in life insurance business including government corporation i.e. Life Insurance Corporation of India and almost equal number of companies in non-life insurance business including government corporation i.e. General Insurance Corporation of India.

The Indian capital market is very well-developed, and it provides a very important source of finance to both public and private sector companies. The major developments in the capital market include the following:

ØThe Securities and Exchange Board of India (SEBI) was empowered to oversee the operations of the exchanges, regulate the capital market and protect investors.

ØTrading introduced in derivative based on index and in stock options of the certain companies satisfying certain parameters.

ØTrading in listed company on stock exchanges in dematerialized form has been made mandatory to reduce the settlement cycle to 2 days.

ØThe interest rates on convertible and non-convertible debentures are allowed to be market determined.

ØFree-market pricing of share issues has increased activity on the stock exchanges.

5.2 Insurance Sector

5.3 Capital Market

DOING BUSINESS IN INDIA14

Suresh Surana & Associates

ØThe concepts of book building and market making have been introduced.

ØUnder the Portfolio Investment Scheme, the RBI has permitted investment in shares and debentures of Indian companies by Non-Resident Indians (NRIs).

ØPortfolio investments are permitted by Foreign Institutional Investors (FIIs).

ØVarious tax incentives have been offered to encourage foreign institutional investment.

ØThe government plans to offer up to 49% equity of many public sector companies to private investors.

ØA new takeover code has been introduced to protect the interests of the small investors and to strengthen the regulatory framework of takeovers.

ØDomestic shares are allowed to be reconverted to American Depository Receipt/ Global Depository Receipt.

India currently has about 30 million shareholders and 23 recognized stock exchanges. These stock exchanges deal in securities issued by the central and state governments, public sector companies and public limited companies. Most activities on the stock exchanges occur in corporate securities. Gilt-edged securities consisting of securities issued by the central, state and other government bodies are also listed on recognized stock exchanges. Bombay Stock Exchange and National Stock Exchange accounts for more than 97% of the total turnover. Foreign Institutional Investors are permitted to also invest in corporate and government debt.

SEBI is the regulatory authority for all the stock exchanges. In order to facilitate stock exchange transactions, India has been modernizing the operations of its stock exchanges by introducing screen based trading. The trading on stock exchange has been made mandatory in dematerialized form for all scrip commencing from April 2002.

SEBI has also laid down eligibility criteria for setting up dedicated stock exchanges for the Small and Medium Enterprises (SME) sector. Apart from fulfilling other criteria, the exchange should have a balance sheet networth of atleast Rs. 1000 million (about US$ 22.23 million).

Bombay Stock Exchange (BSE) is India’s premier stock exchange. It lists over 4,900 companies. BSE has trading terminals in about 300 cities. The market capitalization of the Bombay Stock Exchange in August 2009 was US$ 1.08 trillion. BSE introduced

5.4 Stock Exchanges

5.4.1 Bombay Stock Exchange

DOING BUSINESS IN INDIA 15

Suresh Surana & Associates

DOING BUSINESS IN INDIA16

trading in derivative based on BSE Sensex from 9 June 2000 and trading in stock options of certain companies from 9 July 2001.

National Stock Exchange (NSE) started operations in 1994 with a view to facilitating transparent trading. The NSE provides nation-wide trading facilities to investors through established network linkages in about 350 cities nationwide. The NSE had 1587 listed companies as on 31 March 2009 with a market capitalization of Rs. 47,019 billion (US$ 950 billion) and average daily volume of Rs. 45 billion (US$ 1.03 billion). The NSE is India’s primary exchange for wholesale debt. NSE introduced trading in derivative based on Nifty Index from 12 June 2000 and trading in stock options of certain companies from 2 July 2001.

There is no statutory requirement for public limited companies in India to have their shares listed on a recognized stock exchange. However, the companies have to be listed if their shares or debentures are offered to the public for subscription by prospectus. Companies have to fulfill the stock exchange requirements in order to have their shares listed. In case the company does not satisfy the prescribed conditions of the stock exchange and is not admitted to the exchange, it has to refund the amounts paid by subscribers.

There are numbers of specialized financial institutions in India at the national as well as the state level. India has an integrated structure of financial institutions known as All India Financial Institutions (AFIs), which provide term finance and other assistance to industries. Some of the most important financial institutions, which play a very instrumental role in India’s development are the Industrial Development Bank of India (IDBI), the Industrial Finance Corporation of India (IFCI) and the Industrial Reconstruction Bank of India (IRBI).

India also has other financial institutions, which are set up for specific purposes. These include the National Bank for Agricultural and Rural Development (NABARD), the Shipping Credit Corporation of India, the National Housing Bank and the Discount and Finance House of India, which is a specialized institution to develop an active secondary market for money market instruments.

Most of the specialised investment institutions in India are in the public sector. These include the Unit Trust of India, the Life Insurance Corporation of India, General Insurance Corporation, mutual funds set up by subsidiaries of the State Bank of India and other nationalised banks and other financial institutions.

Mutual funds play a significant role in the capital market. They are established in the form of trusts under the Indian Trusts Act and are operated by separate asset

5.4.2 National Stock Exchange

5.4.3 Listing Requirements

5.5 Specialized Financial Institutions

5.6 Investment Institutions

5.7 Mutual Funds

Suresh Surana & Associates

DOING BUSINESS IN INDIA 17

management companies. The mutual fund market was dominated by public sector financial institutions and public sector banks till 1993, when the government opened up the sector to private participation. The gross mobilization of resources by all mutual fund schemes during July 2009 was around Rs. 9,288 billion (about US$ 190 billion).

Mutual Funds are now permitted to make investment in short term as well as long term foreign debt securities with highest foreign currency credit rating by accredited / registered credit rating agencies in the countries with fully convertible currencies including government securities of the countries having AAA rating.

The Non Banking Finance Companies (NBFCs) form an integral part of the Indian financial system. They have to conform to the overall framework of the monetary and credit policy of the government. The government has permitted foreign direct investment in NBFCs in merchant banking, underwriting, portfolio management services, investment advisory services, financial consultancy, stock broking, asset management, venture capital, custodial services, factoring, credit rating agencies, leasing and finance and housing finance. Foreign direct investment in the NBFC sector is put on automatic route subject to compliance with guidelines to be issued by Reserve Bank of India.

The credit rating agencies rate corporate debt and equity securities such as debentures, shares and commercial paper. They also rate the credit risk of companies, a factor often used by nationalized banks in evaluating loan applications. Credit ratings have become all the more necessary because it has become mandatory for companies to obtain a credit rating before issuing convertible and non-convertible debentures. The Credit Rating Information Services of India Limited (CRISIL), the first credit rating agency in India was established in January 1988 and the Investment Information and Credit Rating Agency of India (ICRA) was established in March 1991. Credit Analysis and Research Ltd. (CARE) is another leading credit rating agency and was set up in November 1993.

New and existing businesses established in specified backward areas of the country are able to obtain finance for major expansion plans at below normal interest rates. Other benefits may include low commitment fees and extended repayment periods.

Industrial undertakings located in specified backward areas, which are largely the

5.8 Non-Banking Finance Companies

5.9 Credit Rating Agencies

6.0 INCENTIVES FOR INDUSTRIES

6.1 Concessional Finance

6.2 Central Government Investment Subsidy

Suresh Surana & Associates

DOING BUSINESS IN INDIA18

same as those where concessional finance is available, are eligible for a Central Government subsidy towards the cost of land, buildings, machinery and equipment.

In keeping with a federal structure, many State Governments operate their own incentive programmes to attract industrial investments. Details of incentive packages often vary from one state to another but would broadly include subsidized power, availability of low-cost land, assistance in feasibility studies, tax breaks and exemptions/ deferment of specific duties.

Exporters are eligible for a number of special incentives.

Duty Drawback: Exporters are entitled to drawback import duties and excise duties paid by them on material inputs of products exported at specified rates, depending upon the type of product exported.

Freight Concessions: Freight rate reductions and priority wagon booking facilities are made available on the railways for transport of raw material for export production and finished products for export.

Export Credit Guarantee: This guarantee is provided by the Export Credit Guarantee Corporation at low rates of premium to banks and other financial institutions to enable exporters to obtain better credit facilities.

Advance Licences: These are issued to exporters for import of raw materials for manufacture of finished products, without payment of custom duties. Duty free import of capital goods may also be permitted if the product to be manufactured is for export.

Special Import Licences: These licences for items in the negative list of imports are made available to specified categories of exporters.

Royalty Payment: There is no restriction on the payment of royalty from India and can be remitted without any approval of government or Reserve Bank of India. In addition, a commission on exports can also be paid to agents outside India.

Special Incentives: These are available to units set up in Special Economic Zones (SEZs), Export Processing Zones (EPZs) and 100% Export Oriented Units (EOUs). While EOUs can be set up anywhere in the country, there are designated SEZs and EPZs which provide internationally competitive duty free environment for low cost export production through basic infrastructure facilities like: developed land, standard design factory buildings, roads, power, water supply, drainage, customs clearance and telecommunications. Presently, these units are eligible to credit 100% of their eligible export receipts of foreign exchange to their Exchange Earners’ Foreign Currency (EEFC) account. These tax incentives are discussed in details in chapter on Taxation System.

6.3 State Government Incentives

7.0 INCENTIVES FOR EXPORTS

Suresh Surana & Associates

DOING BUSINESS IN INDIA 19

EOUs/EPZs have to achieve specified value addition norms. Apart from tax holidays, EOUs/EPZs can import capital goods and industrial inputs free of custom duty and are exempt from payment of Central and State sales tax. Supplies by domestic tariff area units to EOUs/EPZs are regarded as deemed exports and are exempt from excise duty.

Special Economic Zones: To create stimulating infrastructure facilities of international standards in export production, Special Economic Zones (SEZ) can now be set up in the private, public, joint sector or by state governments. Certain EPZ have now be been converted into SEZ. Units in SEZ have comparably better incentives from units in EPZ.

Energy is an essential input for economic development and improving the quality of life. The primary source of commercial energy in India is coal, which provides about 63% of India’s commercial requirements. Nuclear and solar energy are developing, but still have a long way to go to be truly accepted in India as a major energy provider.

The government has announced various policies with the intention of reducing the protection of domestic industry. These policies included substantial reduction in import licensing, decanalization of imports and exports, and lowering of tariffs. However, international trade has not been completely freed with the primary aim of avoiding a drain of foreign exchange reserves and to discourage the importing of non-essential and luxury items.

Major commodities exported from India are gems, jewellery, ready-made garments,

machinery, tools, transportation equipment, manufactured metal goods, electronics, software, cotton, leather, drugs, iron ore, marine products and tea. India’s exports amounted to US $ 185 billion during the financial year 2008-09. India’s imports in the 2008-09 financial year were US $ 304 billion.

The government as well as the industry conducts their activities in English, India has the second largest English speaking population after the United States.

India has one of the largest pool of trained, scientific and technical manpower in the world. This manpower is available very cheap when compared to the manpower costs prevailing in developed countries.

8.0 ENERGY, MINERALS AND OTHER NATURAL RESOURCES

9.0 FOREIGN TRADE

10.0 OTHER FACTORS

10.1 Language

10.2 Trained Manpower

Suresh Surana & Associates

DOING BUSINESS IN INDIA20

10.3 Low Research and Development Costs

10.4 Financial Reliability

Research and development costs in India are generally very low when compared to the costs that would be incurred in any major industrialized countries. In the present scenario, it is possible for the foreign companies to establish 100% foreign-owned research and development (R&D) companies in India, and import the laboratory equipments and other facilities required for R&D. Further to encourage R&D across all sectors of the economy, the Finance Act 2010 introduced by the Finance Ministry of the Government of India has increased weighted deduction on expenditure incurred on approved in-house R&D from 150% to 200%.

Repatriation of capital or dividends for investments made in India is freely allowed. The fiscal deficit which was at 5.9% during the period 2008-09 is envisaged to touch 6.5% of the GDP during 2009-10. Foreign exchange reserves of India which were about US $ 252 billion on 31 March 2009 has increased to US$ 277 billion as on 26 March 2010.

India is a member of the convention of the Multilateral Investment Guarantee Agency, which provides insurance to foreign investors against political risks.

Suresh Surana & Associates

Charminar, Hyderabad

Chapter 3Business Entities

DOING BUSINESS IN INDIA22

CHAPTER 3

BUSINESS ENTITIES

1.0 FORMS OF BUSINESS ENTITIES

1.1 Companies

The principal forms of business organizations in India, apart from government organizations and sole proprietary concerns are:

i. Companies - public and privateii. Branches of foreign companiesiii. Liaison/Branch/Project offices of foreign companiesiv. Partnershipsv. Trustsvi. Limited Liability Partnerships (LLP)

At present, the legislative provisions governing companies are contained in the Companies Act, 1956.

Companies in India are broadly classified into public sector companies’ viz. with predominant government shareholding and private sector companies’ viz. with predominant private shareholding. Private sector companies may further be classified as public limited companies or private limited companies. Companies can also be classified into companies limited by shares, companies limited by guarantee and unlimited liability companies. However, for business purposes, generally companies limited by shares are used and consequently, the discussion regarding companies in this guide is pertaining to such companies. The shares of public companies may or may not be listed on stock exchanges in India. (e.g. The National Stock Exchange of India Ltd (NSE), Bombay Stock Exchange Ltd (BSE), etc.) The regulatory provisions for private limited companies are less stringent than those relating to public limited companies. Public limited companies whose shares are listed on stock exchanges are subject to the regulations of the Securities and Exchange Board of India (SEBI) and the respective stock exchanges.

Private companies that are subsidiaries of public companies (i.e. where shareholding of Public companies is more than 50%) are however treated at par with public companies.

Shares of public limited companies are freely transferable, whereas it is subject to restrictions in case of private limited companies. However, transfer of shares to non-residents is regulated by Foreign Exchange Management Act, 1999.

The system of depository has been introduced by the Depositories Act and Securities Exchange Board of India (Depository & Participants) Regulations, 1996 which has smoothened the transfer of shares in case of listed companies.

Suresh Surana & Associates

DOING BUSINESS IN INDIA 23

1.2 Regulations