Embed Size (px)

Citation preview

March 2015

Doing Business in Brazil

Lauro Fiuza, JrVice President of ABEEólica

Top 10 Cummulative Capacity 2014

2

2012

15th

2.5 GW

2013

13th

3.4 GW

2014

10th

5.9 GW

1 China 114.76

2 USA 65.88

3 Germany 39.16

4 Spain 22.99

5 India 22.46

6 UK 12.44

7 Canada 9.69

8 France 9.28

9 Italy 8.66

10 Brazil 5.96

11 Sweden 5.42

12 Portugal 4.91

13 Denmark 4.84

14 Poland 3.83

15 Australia 3.81

16 Turkey 3.76

17 Romania 2.95

18 Poland 2.80

19 Japan 2.79

20 Mexico 2.38

Source: GWEC/ABEEólica

2012

8th

1.08 GW

2013

7th

0.95 GW

2014

4th

2.50 GW

Top 10 New Installed Capacity 2014

3

4th

position

Source: GWEC/ABEEólica

Accumulated Installed Capacity (MW)

44Source: ABEEólica

Capacity

already

contracted

(16.5 GW)

Capacity Contracted Additional Capacity (EPE) Additional Capacity (Sector)Forecast Forecast

Growth of Capacity Contracted and Forecast (MW)

5Source: ABEEólica/MME/EPE

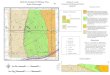

Installed Capacity

66

4 (88.0 MW)

Piauí

13 (69.0 MW)

Paraíba

8 (104.7 MW)

Pernambuco

1 (34.5 MW)

Sergipe

1 (28.0 MW)

Rio de Janeiro

1 (2.5 MW)

Paraná

80% Renewable 20% Nonrenewable

83 (2,345.2 MW)

Rio Grande do Norte

1

45 (1,256.3 MW)

Ceará

2

40 (1,049.0 MW)

Bahia

4

43 (1,148.5 MW)

Rio Grande do Sul

3

13 (238.5 MW)

Santa Catarina

5

Able to Operate plants: 11 (310.8 MW)

Source: ABEEólica

Energy Auctions

7

Results – Auctions of 2014

AuctionContracted

(MW)

MaximumPrice

($/MWh)

AveragePrice

($/MWh)

Negativegoodwill

(%)

Investment(in billions)

($/MWh)

CapacityFactor

(%)

WTGestimative

(2MW)

Blades

Estimative

A-3 2014 551.0 59.11 57.76 2.28 1.10 50 276 827

LER 2014 769.1 59.50 58.82 1.15 1.43 43 385 1,154

A-5 2014 926.0 51.89 51.52 0.73 1.58 47 463 1,389

Total 2,246.1 -- -- -- 4.11 -- 1,123 3,369

Average -- 56.84 56.03 1.39% -- 47 -- --

Up

da

ted P

rice

s (

De

c/1

4)

Source: ABEEólica/cceeExchange rate at the auction date.

Auction Results per Year

Energy Auctions (New plants)

All Sources

Energy Auctions (New plants)

Wind Energy

YearCapacity

(GW)

2009 1.81

2010 2.05

2011 2.91

2012 0.28

2013 4.71

2014 2.25

Total 14.00

Annual Average 2.33

Target 2.0

Atypical year

Average without 2012 =

2.7 GW/year

YearCapacity

(GW)

2009 1.88

2010 5.95

2011 5.17

2012 0.57

2013 7.15

2014 7.61

Total 28.32

Annual Average 4.72

Atypical year

Average without 2012 =

5.5 GW/year

Source: ABEEólica/CCEE 8

Wind Power representes 50% of all new PPAs (2009-2014)

• Realization: 04/27/2015

• Sources:

o Wind

o Biomass

• Begin of Energy Supply (Wind): 07/01/2017

• PPA supply period: 20 years

• Registration:

Alternative Source Auction (LFA)

• Realization: 07/24/2015

• Sources:

o Wind

o Small Hydro

o Biomass

o Natural Gas thermal

• Begin of Energy Supply (Wind): 01/01/2018

• PPA supply period: 30 years for Small Hydro

and 20 year for all others

• Registration :

New Energy Auction (A-3)

Auctions - 2015

SourceNumber of

plantsCapacity (MW) %

Wind 475 11,476 60.6%

Small Hydro 15 201 1.1%

Biomass 13 604 3.2%

Natural Gas Thermal 18 6,648 35.1%

TOTAL 521 18,929 100%

SourceNumber of

plantsCapacity (MW) %

Wind 530 12,895 86.2%

Biomass 40 2,067 13.8%

TOTAL 570 14,962 100%

9Source: ABEEólica/MME/EPE

• Realization: 08/14/2015

• Sources:

o Solar

• Begin of Energy Supply (Wind): 08/01/2017

• PPA supply period: 20 years

1st Reserve Energy Auction (LER)

• Realization: 11/13/2015

• Sources:

o Wind

o Solar

• Begin of Energy Supply (Wind): 01/11/2018

• PPA supply period: 20 years

2nd Reserve Energy Auction (LER)

Auctions - 2015

10Source: ABEEólica/MME/EPE

Operating Performance

“On 11/25/2014 there was another record of wind generation at Northeast subsystem, 2,315 MW,

with 81% of capacity factor, representing 21% of total power generation.”

System Operator - ONS

11Source: ABEEólica

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Wind Characteristics in Brazil

12

Northeast South

Wind Direction – Oct, 2013 Wind Direction – Oct, 2013

Wind Speed (m/s) – Oct, 2013 Wind Speed (m/s) – Oct, 2013

Direction Direction

Time (%) Time (%)

Ave

rag

e Sp

ee

d (

m/s

)

Ave

rag

e Sp

ee

d (

m/s

)

Fre

qu

en

cy (

%)

Fre

qu

en

cy (

%)

Source: AMA/EPE

Operating Performance

13Source: ABEEólica

(Without PROINFA)

Average = 43%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Benefits and Indexes of Wind 2014

3 millions of tons of CO2

avoided

US$ 1.8 billions ofeconomic charges avoided

Exchange rate = US$ 2.35

6 millions ofhouses supplied monthy, average

12 TWh of wind

generation

US$ 6.2 billions wereinvested on wind sector

14Source: ABEEólica/ccee/BNEF

Certificate of Renewable Energy

• Goal: foster energy market generated from renewable and encouraged sources with high performance

in terms of sustainability.

• Types of certification:

➢ Certification of renewable energy generation plants eligible;

➢ Stamp concession facing consumers of certified energy.

15

ElectricalEnergy

Social and environmental

attributes

WindGenerator

Advantages

• Long Term Credit

• BNDES: competitive long terms

• Credit Lines for Manufacturers

• FINAME from BNDES

• Tax Incentives (Federal, State and Municipal)

16

FINAME (Financing for machinery and equipment)

• What is this? FINAME’s resource is earmarked for financing purchase and sales operations and

exports of Brazilian machinery and equipment, as well as imports of goods of the same nature produced

overseas.

• How to get it? There are goals to be achieved gradually to register the equipment as a FINAME

equipment.

Starting Point

• January 1st, 2013

Stage A-2

• July 1st, 2013

Stage A-3

• January 1st, 2014

Stage A-4

• July 1st, 2014*

Stage A-5

• January 1st, 2015*

Stage A-6

• January 1st, 2016

* Some goals of these stages were postpone.

FINAME Rules

Starting Point

(Reach 3 of 4)

•TowerFabrication (70%)

- itself unit or third

parties

•BladesFabrication - itself

unit or third

parties

•Hub Assembly -

itself unit

•Nacell Assembly

- itself unit

Stage A-2

•TowerFabrication (70%)

- itself unit or third

parties

•Hub Assembly

with national

internal

components -

itself unit

•Nacell Assembly

- itself unit

Stage A-3

•TowerFabrication with

national internal

components -

itself unit or third

parties

•BladesFabrication (40%)

- itself unit or third

parties

•Hub Assembly

with national

internal

components -

itself unit

•Nacell Assembly

- itself unit

Stage A-4

•BladesFabrication (50%)

- itself unit or third

parties

•Hub Assembly

with national

internal

components -

itself unit

•Nacell Assembly

- itself unit

Stage A-5

•TowerFabrication with

60% of national

forged - itself unit

or third parties

•BladesFabrication (60%)

- itself unit or third

parties

•Hub Assembly

with national

internal

components -

itself unit

•Nacell Assembly

- itself unit

Stage A-6

•Nacell Assembly

with national

components -

itself unit

Wind portfolio of BNDES - Evolution

19

2,000,000

1,800,000

1,600,000

1,400,000

1,200,000

1,000,000

800,000

600,000

400,000

200,000

Approvals Financing Wind Farms

Forecast 2014: Growth of 15% compared to 2013 approvals

Exch

an

ge ra

te =

US$

2.5

Opportunities

• Local Content Demand

• Consistent Growth of Wind Power within the Power Matrix

• High Demand for Business Services and Consulting

• Independent O&M Players

• Training Programs for Industry Professionals

20

Challenges

• Early Stage Industry

• Labor Opportunities

• Technology

• Adjustment to Brazilian wind conditions

• R&D

• Grid

• Infrastructure

21

Members

22

23

Bons Ventos Aracati

Wind Farm

CONTACT:

Lauro Fiuza Junior

+ 55 11 2368-0680

www.abeeolica.org.br

Thank You!