Embed Size (px)

Citation preview

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 1/9

A U D I T / T A X / A D V I S O R Y / L I N E O F B U S I N E S S

DOI Annual Business Conference

Audit Approach to

OMB Circular No. A-123

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 2/9

2

Agenda

• Auditors’ objective

• Consolidated level procedures

• Bureau level procedures

• Assurance statement procedures

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 3/9

3

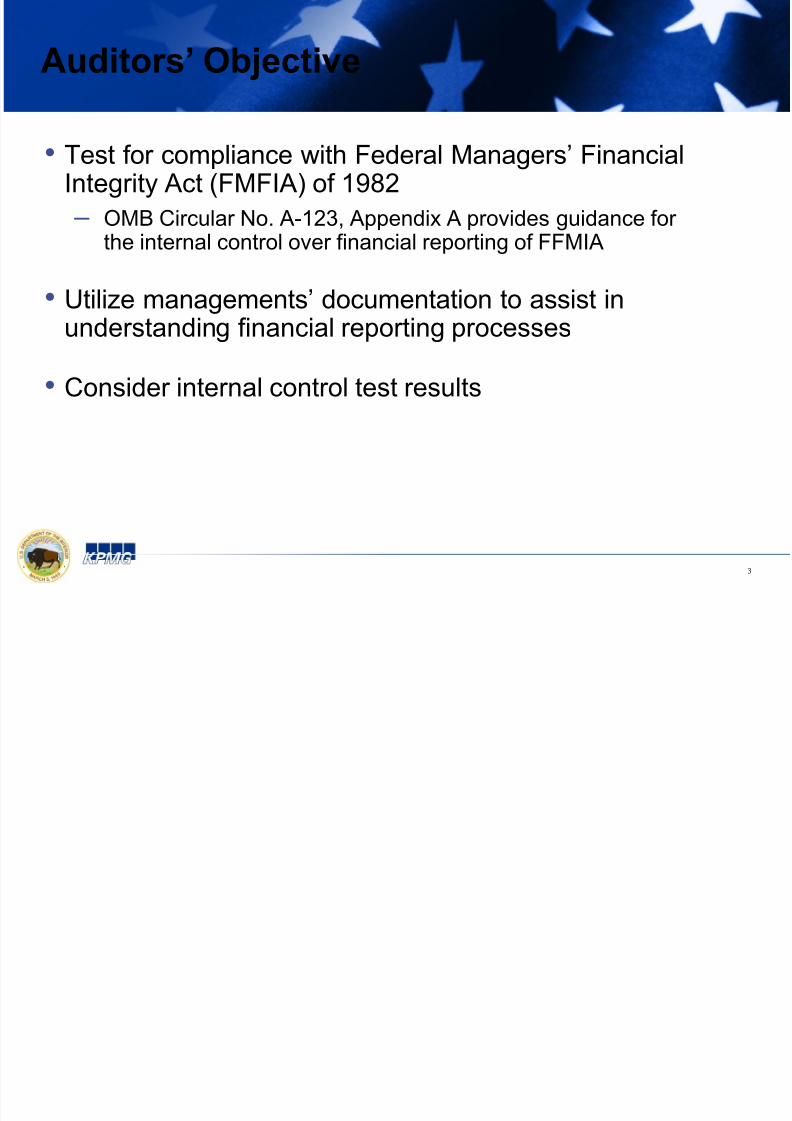

Auditors’ Objective

• Test for compliance with Federal Managers’ FinancialIntegrity Act (FMFIA) of 1982

– OMB Circular No. A-123, Appendix A provides guidance forthe internal control over financial reporting of FFMIA

• Utilize managements’ documentation to assist inunderstanding financial reporting processes

• Consider internal control test results

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 4/9

4

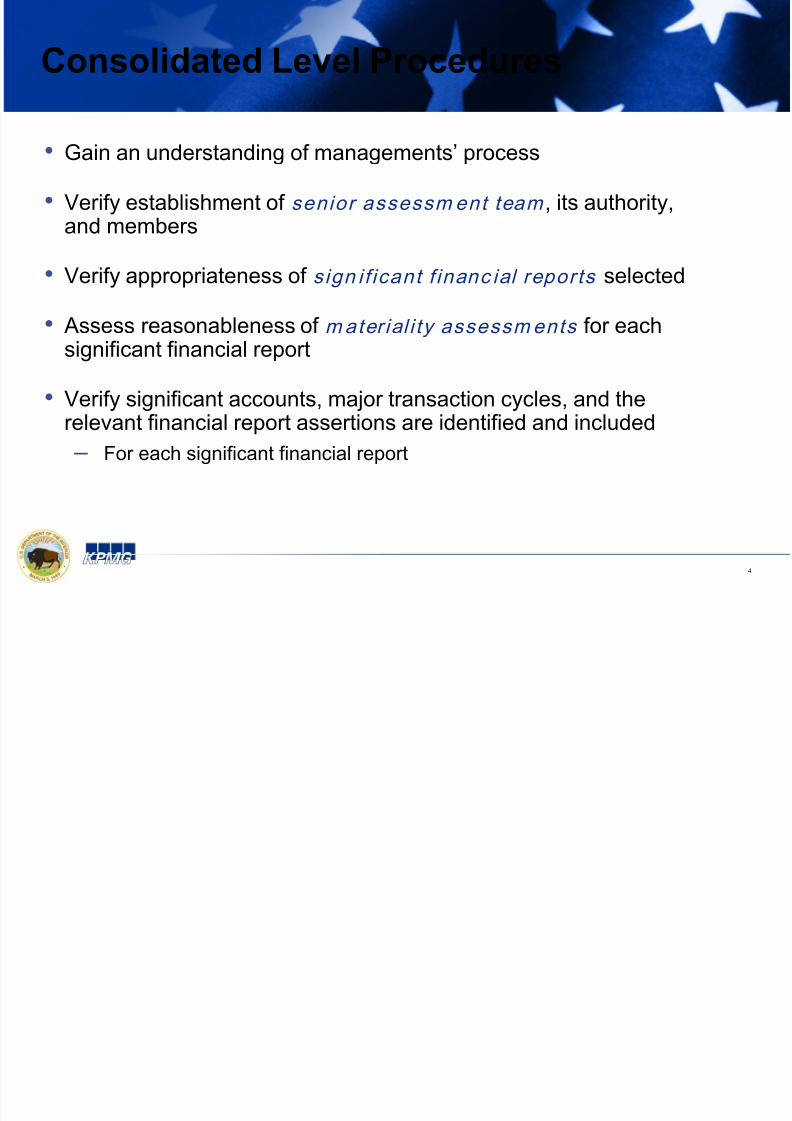

Consolidated Level Procedures

• Gain an understanding of managements’ process

• Verify establishment of senior assessm ent team , its authority,and members

• Verify appropriateness of sign i f icant f inanc ial reports selected

• Assess reasonableness of mater ial i ty assessments for eachsignificant financial report

• Verify significant accounts, major transaction cycles, and therelevant financial report assertions are identified and included

– For each significant financial report

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 5/9

5

Bureau Level Procedures

• Inspect a sample of bureaus’ contro ldocumentat ion to verify that it includes controls atthe:

– Entity level

– Control environment, risk assessment, monitoring, control activity,and information and communication processes

– Process, transaction, and application level

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 6/9

6

Bureau Level Procedures

• Inspect a sample of the bureau contro l

documentat ion for consistency with CFO Council’sImplementation Guide

– Controls to mitigate the risk of financial statement errors

– Data characteristics: source; receipt; processing; andtransmission

– Supervisor review; process and calculations performed inpreparation of financial reporting; and process outputs

– Use of computer application controls and controls over

spreadsheets used in the preparation of financial reporting – Identification of errors: types of errors found; reporting

errors; and resolving errors

– Ability of personnel to override the process or controls

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 7/97

Bureau Level Procedures

• Inspect a sample of the internal control test ing documentat ion to verify that it includes

– Management’s assessment of the design of key controls

– Nature, timing, and extent of testing of key controls

– Assessment of operating effectiveness of key controlstested

– Response and conclusions for deficiencies identified

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 8/98

Assurance Statement Procedures -

Bureaus

• Read bureau assurance statement for conformancewith Department guidance

– Based on Department materiality

• Compare managements’ and auditors’ testing resultsto bureau assurance statement to verify that:

– Managements’ results support the assurance statement

– Management identified all material weaknesses

7/27/2019 DOI Plenary A123 Norris

http://slidepdf.com/reader/full/doi-plenary-a123-norris 9/9

9

Assurance Statement Procedures -

Consolidated

• Inspect the assurance statement to verify that itincludes:

– Results of the bureau level assurance statements

– Any material weaknesses that are identified

– Statement of management’s responsibility forestablishing and maintaining adequate internal controls

– Statement identifying OMB Circular A-123 as thef ramework used by management to conduct theassessment

– An assessment of the effectiveness of the agency’sinternal control