Embed Size (px)

Citation preview

Does the SOX Definition of an Accounting Expert Matter?The Association between Audit Committee Directors'Accounting Expertise and Accounting Conservatism*

GOPAL V. KRISHNAN, Lehigh University

GNANAKUMAR VISVANATHAN, George Mason University

1. Introduction

The Sarbanes-Oxley Act (SOX) (U.S. Congress 2002) mandates the disclosure ofwhether the audit committee includes a financial expert. ' However, the operation-alization of who is a financial expert was and still is a controversial issue (Plitchand Ceron 2003). Some have argued that effective audit committee members arethose who have general management experience rather than those who have anaccounting or financial background (Olson 1999). The Securities and ExchangeCommission (SEC) initially proposed a narrow definition to include only account-ing financial experts — that is, directors with experience as a certified public accoun-tant (CPA), auditor, chief financial officer (CFO), controller, or chief accountingofficer. Subsequently, the SEC defined financial expert broadly to include nonac-counting financial experts, such as directors with experience as a chief executiveofficer (CEO) or president (SEC 2003).2 Was the SEC correct in defining financialexperts to include both accounting and nonaccounting experts? Do accountingfinancial experts enhance the quality of financial reporting more than nonaccount-ing financial experts? These are important questions because the primary objectiveof SOX was to restore credibility to the U.S. financial reporting system, which wastarnished by several high-profile accounting scandals. Because the audit committeeis the ultimate monitor of the financial reporting process, the audit committee'sfinancial expertise is a key determinant of its effectiveness (Treadway 1987). Wecontribute to this debate by separately examining the association between the auditcommittee's accounting financial expertise and nonaccounting financial expertiseand several attributes of financial reporting quality.

Our primary measure of financial reporting quality is accounting conserva-tism. We focus on conservatism for several reasons. Several scholars recognize thelong-standing infiuence of accounting conservatism on accounting practice. Forexample, Basu (1997) notes that conservatism has infiuenced accounting practicefor at least 500 years. Sterling (1970) rates conservatism as the most infiuentialprinciple of valuation in accounting. Ball (2001) argues that conservatism is a

* Accepted by Peter Pope. We appreciate the helpful comments made by two anonymous referees,Andrew Felo, Chris Jones, Peter Pope (associate editor), and the seminar participants at AmericanUniversity, George Mason University, and the 2006 Annual Meeting of the American AccountingAssociation. We thank Anya Zyuzina for help with data collection.

Contemporary Accounting Research Vol. 25 No. 3 (Fall 2008) pp. 827-57 © CAAA

doi:10.1506/car.25.3.7

828 Contemporary Accounting Research

fundamental characteristic of financial reporting. Watts (2003a, b) emphasizes thatconservatism facilitates effective monitoring of managers and contracts by con-straining overpayments to managers and other parties.3 Furthennore, the recentaccounting scandals in the United States and elsewhere, and a record number ofrestatements of financial statements, have underscored the importance of conserva-tive financial reporting. Despite the long history and the importance associatedwith conservatism, surprisingly, there is limited empirical evidence of the relationbetween the audit committee characteristics and conservatism.'* We also examinethe relation between the audit committee's financial expertise and the Q scoredeveloped by Penman and Zhang 2002. Penman and Zhang refer to the Q score asan "eamings quality indicator", and provide evidence that the Q score has predic-tive power for one-year-ahead retum on net operating assets (RNOA) incrementalto past RNOA.

Audit committee members with accounting financial expertise are expected toenhance accounting conservatism through their better monitoring capability drivenby their knowledge base, job expectations as demanded by the audit committee char-ter, and economic incentives to mitigate the risk of litigation and protect their repu-tation capital.

We measure audit committee expertise in three ways: accounting financialexperts, nonaccounting financial experts, and nonfinancial experts (directors whoare neither accounting nor nonaccounting financial experts). We use multiple proxiesto capture conservatism. We use two accruals-based measures developed by Givoiyand Hayn 2000, a measure that is derived from the book-to-market ratio (Beaverand Ryan 2000), and a conservatism score developed by Penman and Zhang 2002to capture unrecorded assets on the balance sheet. We also use Ball and Shivakumar's2005 asymmetric loss recognition test, an altemative measure of conservatism.^Our control variables include several other characteristics of the audit committeeand the board.

Our sample firms come from the Standard & Poor's (S&P) 500, and the totalnumber of firm-year observations is 929 (633 for the conservative score measure)representing years 2000 through 2002. We find that, in general, accounting con-servatism is not correlated with nonaccounting financial expertise or nonfinancialexpertise. However, accounting financial expertise is positively and significantlycorrelated with all but one measure (book-to-market ratio) of conservatism.Results based on the Q score indicate a positive and significant relation betweenaccounting financial expertise and the Q score. We also find that the accountingfinancial experts on the audit committee are able to effectively perform their moni-toring function and promote conservative accounting only when they are in boardsthat are characterized by strong govemance. This finding holds for all four meas-ures of conservatism. It appears that in weak boards the presence of accountingfinancial expertise on the audit committee is ineffective in promoting conservativeaccounting — that is, the effect of accounting financial expertise is undermined byweak govemance mechanisms. We also consider the possibility that attributes ofcorporate boards and govemance mechanisms may be endogenously determined.When we control for endogeneity, results are significant for the book-to-market

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 829

measure as well as for the other measures of conservatism. Overall, the findingssuggest that accounting financial expertise has a broader impact on financialreporting beyond accounting conservatism.

We make several contributions. First, we contribute to the debate on the appro-priate definition of a financial expert under SOX. By including both accountingfinancial expertise and nonaccounting financial expertise in the same model, oursis the first study that directly tests the relation between these two types of financialexpertise with accounting conservatism. We provide empirical evidence that isconsistent with the SEC's initial narrow definition to include only accountingfinancial experts. This finding has implications for boards of directors and regula-tors in other countries who are considering measures to enhance the effectivenessof audit committees.

Second, DeFond, Hann, and Hu (2005) consider two competing explanationsfor the favorable market reaction to the appointment of experts to the audit commit-tee: monitoring (i.e., the appointment of an expert improves the committee's over-sight) and signaling (i.e., the appointment is a credible signal to the investors thatthe firm takes financial reporting seriously. The two explanations are not mutuallyexclusive and DeFond et al. (2005) interpret their evidence as consistent with themonitoring explanation. Engel (2005), however, notes that the market reaction isan expectation of value enhancement, not a direct measure of actual or ultimateimprovements associated with the appointment. Our finding that only accountingfinancial expertise is associated with conservatism is consistent with the monitor-ing explanation. That differentiation is important because it opens up the "blackbox" — that is, it contributes to our understanding of why the stock market reactsfavorably to the appointment of accounting experts but not nonaccounting expertsto the audit committee.

Third, we contribute to the growing literature on the consequences of the auditcommittee's expertise on financial reporting quality (Xie, Davidson, and Bodealt2003; Bedard, Chtourow, and Courteau 2004; Agrawal and Chadha 2005; J. Krishnan2005).6 Whereas prior research implies that financial expertise will have a favor-able impact on financial reporting quality for the average firm, we extend the liter-ature by providing evidence that overall govemance quality accentuates the effect ofaccounting expertise on conservatism. This finding has important implications forthe boards of directors, auditors, and investors.

Fourth, we also provide empirical evidence on the association between the Qscore, a measure of eamings quality, and the accounting expertise of the membersof the audit committee. Thus, by examining multiple measures of conservatism aswell as the Q score, we provide an analysis of the impact of the audit committee'sexpertise on financial reporting that is more comprehensive than prior studies thatexamined a single attribute of financial statements.

The rest of this paper is organized as follows. Section 2 reviews the relatedresearch and develops the hypothesis. Section 3 describes the research method andthe sample selection process. Section 4 provides our results and conclusions.

CAR Vol. 25 No. 3 (Fall 2008)

830 Contemporary Accounting Research

2. Hypothesis

Traditionally, the audit committee has oversight of financial reporting, includingthe annual and quarterly financial statements, disclosures in regulatory filings,eamings releases, pro forma information, and eamings guidance (Steinberg 2005).The Blue Ribbon Committee (1999) notes that the audit committee is the ultimatemonitor of the financial reporting process. Recently, a survey by Pricewaterhouse-Coopers 2005 asked directors to rank seven dimensions of an effective board. Theaudit committee's ability to monitor the accuracy of financial reporting was rankedas the most important dimension. This finding underscores the significance of auditcommittees as a govemance mechanism.

Watts (2003a) argues that the board of directors has at least two reasons to beinterested in conservatism: conservatism could restrain managers' ability to over-compensate themselves by aggressive accounting and conservatism could offsetmanagers' tendencies to report good news more than bad news. Although Watts'sarguments for the demand for conservatism are made from the overall boardperspective, there are several reasons why the members of the audit committee —specifically the directors with accounting expertise — would promote conserva-tism. Our arguments for the audit committee directors with expertise derive fromthe fact that they, among all board or audit committee members, have the best abilityto distinguish among accounting policies (as conservative or aggressive), and theyhave incentives, more so than other directors, to promote conservatism. More spe-cifically, audit committee members with accounting expertise could potentiallyenhance conservatism for three reasons: (a) having accounting expertise providesthe ability to assess the nature and the appropriateness of the accounting choicesmade by the managers; (b) provisions in audit committee charters frequentlyrequire the members to examine the aggressiveness or conservatism of accountingpolicies, thereby placing a demand on members' expertise; and (c) risk of litigationand in particular the potential loss of reputation capital for those with accountingexpertise provide further incentives for such members to promote accounting con-servatism. We elaborate on these reasons below.

Financial expertise

The Treadway Commission (1987) concluded that the experience and expertise ofthe members of an audit committee are an important dimension of an audit com-mittee's effectiveness. Audit committee members with accounting financial exper-tise can enhance conservatism by assessing the adequacy of provisions for matterssuch as warranty obligations, lawsuits, and other contingencies, and appraise theoverall quality of financial reporting. Also, they can examine the reasonableness ofexplanations provided by management, and in particular detect the nature of dis-agreements between management and the extemal auditor (DeZoort and Salterio2001). There is a long and growing literature on the relation between an audit com-mittee's financial expertise and attributes of financial reporting, and researchershave begun to examine the effects of accounting versus nonaccounting financialexpertise.

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 831

Kalbers and Fogarty (1993) examine whether an audit committee's power isassociated with its effectiveness. They argue that because audit committees arecomposed of individuals, the members' personal attributes influence the commit-tees' effectiveness. One dimension of power is "expert power"; that is, membersskilled in accounting and finance could contribute to the committee's effectiveness.Kalbers and Fogarty find that expert power is highly associated with financialreporting effectiveness. Similarly, McMuUen and Raghunandan (1996) provideevidence that firms with financial reporting problems are less likely to have CPAson the audit committee.

McDaniel, Martin, and Maines (2002) conduct an experiment to study theeffects of financial expertise and financial literacy on financial reporting. They useaudit managers and Executive MBA graduates as surrogates for financial expertsand financial literates, respectively. Borrowing from research on cognitive psy-chology, McDaniel et al. (2002) argue that experts' episodic knowledge aboutfinancial reporting quality represents both first-hand experiences (training and pro-fessional certification) with relevant problems and second-hand experiences — forexample, interactions with other experts. However, episodic knowledge of literatesis derived from second-hand information. McDaniel et al. point out that the second-hand exposure to a financial reporting issue is likely to be more limited and erodeover time because literates may not reinforce or further develop their frameworkthrough practical experience. In other words, relative to the literates, experts pos-sess experience-based and well-developed frameworks to raise concems regardingtreatment of items that may contribute to misstatement of financial statements orpoor reporting quality.'' Consistent with their predictions, McDaniel et al. find thatfinancial experts possess a framework for evaluating financial reporting qualitythat is more consistent with the Financial Accounting Standards Board's (FASB)conceptual framework. They conclude that having financial experts on the auditcommittee is likely to bring a focus on issues that may receive a lower priority ifonly financial literates were on the audit committee.

Several recent studies examine the relation between an audit committee'sfinancial expertise and eamings management, although the definition of financialexpertise varies. Xie et al. (2003) and Bedard et al. (2004) provide evidence thatthe financial sophistication of the board and the audit committee is an importantfactor in constraining the propensity of managers to engage in eamings manage-ment. Agrawal and Chadha (2005) find that the probability of restating financialstatements is significantly lower when the audit committee has an independentfinancial expert. This finding is consistent with the notion that independent direc-tors with financial expertise provide valuable oversight over financial reporting.DeFond et al. (2005) conduct an event study for a sample of firms appointingaccounting and nonaccounting financial experts to their audit committees and finda positive stock market reaction only for appointments of accounting experts. Thisfinding suggests that appointing a nonaccounting expert to the audit committee istreated as a nonevent by the market participants. Conversely, appointing an account-ing expert is expected to enhance corporate govemance through increased moni-toring. Karamanou and Vafeas (2005) study several attributes of audit committees,

CAR Vol. 25 No. 3 (Fall 2008)

832 Contemporary Accounting Research

including expertise, and find that firms with effective govemance mechanisms aremore likely to make or update a management forecast. This finding is stronger forbad news when investors are at most risk of suffering wealth losses. Finally,Zhang, Zhou, and Zhou (2007) provide evidence that firms are more likely to beidentified with an intemal control weakness under SOX if their audit committeeshave less accounting financial expertise. Overall, the empirical evidence reviewedhere supports the notion that members of the audit committee with accountingfinancial expertise possess experience-based and well-developed frameworks toassess accounts' conservatism, and can evaluate the explanations provided bymanagement.

Expectations of the audit committee charter

The roles and responsibilities of the members of the audit committee are usuallydescribed in the audit committee charter. We reviewed the audit committee charterfor several firms and generally found a high degree of consistency in terms of jobexpectations, including reference to accounting conservatism.^ We provide twoexamples from the audit committee charters below.

Ruby Tuesday:

As part of its oversight responsibility, the Committee shall provide for thefollowing to ensure the credibility of financial reporting: ... Ensure that man-agement and the Auditor discuss with the Committee their qualitative judgmentsabout the appropriateness, not just the acceptability, of accounting principlesand financial disclosure practices used or proposed to be adopted by the Com-pany and, particularly, about the degree of aggressiveness or conservatism ofits accounting principles and underlying estimates.

eBay:

The Audit Committee shall ... discuss with the independent auditors theresults of the annual audit, including the auditors' assessment of the qualityand conservatism [of accounting principles] ...

Thus, to fulfill the expectations of the audit committee charter, audit committeemembers need to understand not only the accounting principles and estimates usedbut also whether those principles and estimates are more conservative relative toother principles and estimates. Though meeting the expectations of the audit char-ter applies to all audit committee directors, it is natural that directors who lackaccounting financial expertise would tum to directors with accounting expertise forleadership on matters conceming financial reporting issues. This is the fundamen-tal reason for recruiting a financial expert to serve on the committee in the firstplace. Thus, the obligation to fulfill the expectations of the audit committee charter,particularly with regard to conservatism, is greater for those directors withaccounting financial expertise relative to directors who lack such expertise.

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 833

Economic incentives

Basu (1997) iu-gues that litigation risk against auditors is an important driver ofconservatism. We believe that the same argument also applies to the members of anaudit committee. Like auditors, members of the audit committee face an asymmet-ric loss function and bear significant reputation costs in the event of financial fraudor a material misstatement of financial statements. For example, KPMG's AuditCommittee Institute (2006) surveyed 1,200 audit committee members in 17 coun-tries and found that members of the audit committee felt that they are exposed to ahigher level of litigation risk and financial prosecution than any other members ofthe board. Furthermore, this sentiment of greater exposure to lawsuits is highest inNorth America. Do courts hold directors with financial expertise to a higher standardthan other directors? In a recent decision involving Emerging Communications,Inc., where the shareholders sued the board for breach of fiduciary duty, the Dela-ware Chancery Court held one director to a higher standard than the other directorsbecause he had specialized financial expertise while several other directors werenot found liable (Cost and Miller 2005). This is an interesting developmentbecause SOX provides a safe harbor for financial experts from additional liabilityfrom the federal securities laws. However, fiduciary obligations are imposed ondirectors by state law, and, thus, directors could be sued under the state law as inthe case of Emerging Communications, Inc. This example indicates that the riskof litigation could be higher for directors who are financial experts relative to otherdirectors.

In addition to fines and damages awarded against the members of the auditcommittee, outside directors with a poor track record of monitoring are disciplinedby the managerial labor market (Milgrom and Roberts 1992; Gerety and Lehn1997). Srinivasan (2005) examines the loss in the number of other directorshipsheld by the director in the three years following the announcement of a restatementof financial statements. He concludes that audit committee directors, on average,lose more other directorships than do nonaudit committee directors. This is consis-tent with the notion that audit committee directors bear more responsibility forfinancial reporting oversight relative to other directors. Furthermore, Srinivasanfinds that for a sample of firms with income-decreasing restatements, the coeffi-cient on financial experts is positive and statistically significant. In other words,financial experts lose more directorships than nonfinancial experts. Thus, in theevent of financial reporting failure, the market for directors appears to disciplinefinancial experts more than nonfinancial experts. Interestingly, the financial expertcoefficient is positive but not significant for firms with income-increasing restate-ments. This finding is consistent with the asymmetric loss function faced by themembers of the audit committee. Thus, members of the audit committee, particu-larly accounting financial experts, have incentives to enhance accounting conserva-tism to mitigate the risk of litigation and the consequential reputation loss.

In summary, the combination of the audit committee members' accountingfinancial expertise, increasing expectations of the audit committee charter toensure the credibility of financial reporting — including maintaining conservatism

CAR Vol. 25 No. 3 (Fall 2008)

834 Contemporary Accounting Research

— and the economic incentives of the members of the audit committee to mitigatethe risk of litigation and to protect their reputation capital is likely to enhanceconservatism through increased monitoring. This line of reasoning leads to thefollowing hypothesis (in altemative form):

HYPOTHESIS. The audit committee's accounting financial expertise is positivelyassociated with accounting conservatism.

3. Research design and sample

Measures of audit committee's expertise

Following DeFond et al. 2005, we measure expertise in three ways. Accountingfinancial experts are directors with experience as a certified public accountant,auditor, principal or chief financial officer, controller, or principal or chief account-ing officer. Nonaccounting financial experts are directors with experience as thechief executive officer or president of a for-profit corporation. Nonfinancial expertsare directors who are neither accounting nor nonaccounting financial experts.

Measures of conservatism

Conservatism is a multifaceted constmct. We use multiple proxies to capture con-servatism. Our first measure of conservatism is an accrual-based measure. Givolyand Hayn (2000) state that conservative accounting leads to persistently negativeaccruals, in contrast with the expected pattern of accrual reversals. FollowingAhmed, Billings, Morton, and Stanford-Harris 2002, CONACRU equals incomebefore extraordinary items and discontinued operations plus depreciation expenseless operating cash flows deflated by total assets. CONACRU is averaged over athree-year period centered at period t.^ We multiply CONACRU by — 1 so that it isincreasing in the amount of negative accmals.

Our second measure of conservatism is designed to address the issue thataccruals in any given period contain accmals of prior periods that reverse duringthat period. To filter out effects of such reversals, Hui and Matsunaga (2004) use afirm fixed-effect procedure by regressing current period accmals on lagged accm-als for each of the prior six years. The coefficient on the lagged accmals wouldcapture the reversals of past accmals. The firm-specific intercept from this fixed-effect regression is thus at least partially free of the effect of past accmals that arereversing. This firm-specific intercept multiplied by — 1 is our second measure ofconservatism designated as CONACRUF.

Our third measure comes from Ryan 1995 and Beaver and Ryan 2000. Theydecompose the book-to-market ratio (BTM) into its bias and lag components. Biasmeans that the book value is persistently lower (higher) than market value, so thatBTM is persistently below (above) one. Lag refers to the unexpected economicgains and losses that are recognized in book value over time rather than immedi-ately. Thus, the BTM is temporarily lower but tends to its mean over time. Bothbias and lag result from joint effects of the accounting process and the economicenvironment. Beaver and Ryan estimate the firm-specific intercept, Xi, from thefollowing fixed-effect regression of book-to-market ratio (BTM) on current and six

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 835

lagged (k = 0-6) annual stock retums (RET). We multiply the firm-specific inter-cept by — 1.

BTM¡, = x+Xi + Xt + ^hRETi, _ k (1),

where i and t are firm and year subscripts; bias and lag are captured by Xi and 5^,respectively. Beaver and Ryan show that the bias component is associated withmeasures of accounting conservatism while lag is not. We refer to Xi as CONBM.

Penman and Zhang (2002) compute a conservatism index (C score) to capturethe effect of conservative accounting on the balance sheet. It is a measure of unre-corded reserves on the balance sheet. Following Penman and Zhang 2002, our finalmeasure of conservatism, CONCSCO, is the amount of LIFO (last-in, first-out)reserve, research and development (R&D), and advertising reserves scaled by netoperating assets for firms that have one or more of the three reserves. LIFO inven-tory reserve equals LIFO reserve as reported in financial statements. R&D andadvertising reserves are calculated based on procedures described in Penman &Zhang 2002. The advantage of this method is that it directly considers the role ofaccounting policy choice in conservatism — unlike the other measures. A short-coming, however, is that not all possible accounting choices are considered. Penmanand Zhang (2002) justify considering these three accounting policy choices in theC score because, unlike most other accounting choices, these are either mandatedby regulators or changed only rarely.

Empirical model

We estimate the following empirical model:

CON = ao + aiAFINEXP + a^^AFINEXP + a^BSIZE + a^^^ODUAL

+ a^BIND + OLf/iCSIZE + a-jAClND + a^ACMEET + a^IZE

+ a^CFO + ai2RDADV + ay^SGROW + ai^LlTI

+ ai^NOWN + ui-jINSTOWN (2).

We define the variables as follows:

CON = one of the four conservatism measures (CONACRU, CONACRUF,CONBM, and CONCSCO);

AFINEXP = the proportion of audit committee directors who qualify asaccounting financial experts to the total number of directors in theaudit committee;

NÁFINEXP = the proportion of audit committee directors who qualify as non-accounting financial experts to the total number of directors in theaudit committee;

BSIZE = the log of total number of directors in the board;

NODUAL = a dummy variable that equals 1 if the CEO is also not the chairmanof the board, and equals 0 otherwise;

CAR Vol. 25 No. 3 (Fall 2008)

836 Contemporary Accounting Research

BIND = the proportion of directors who are independent;

ACSIZE = the log of total number of directors in the audit committee;

ACIND = the proportion of independent directors in the audit committee;

ACMEET = the number of meetings by the audit committee dudng the year;

SIZE = the log of total assets;

DEBT = long-term debt divided by total assets;

CFO = cash now from operations, scaled by total assets;

RDADV = research and development expense plus advertising expense, scaledby sales;

SGROW = the atinual percentage change in sales;

LITI = a dummy variable that equals 1 for biotechnology, computers, elec-tronics, and retailing industries and equals 0 for other industries(Francis et al. 1994);

= a dummy variable that equals 1 if the company's auditor is one ofthe Big 4 audit firms and equals 0 for other auditors;

= the percentage of common stock owned by all officers of thecorporation and directors as a group;

BIG4

INOWN

INSTOWN = the percentage of common stock held by institutions.

A positive coefficient for a^ is consistent with our hypothesis that accountingfinancial expertise is associated with accounting conservatism. We do not offer aprediction for a^ We also do not offer a prediction for «3 or «g because the priorresearch is mixed. The literature on corporate governance generally suggests anegative consequence arising from larger boards (Jensen 1993; Hermalin andWeisbach 2003). However, Klein (2002b) finds that independent audit committeesare positively correlated with board size. Prior research finds that board independ-ence, audit committee independence, and separation of CEO and chairman of theboard are indicative of good governance (Jensen 1993; Beasley 1996; Dechow,Sloan, and Sweeney 1996; Klein 2002a). Therefore, a positive relation is predictedfor a^, a^, and aj. Prior research also finds that the frequency of audit committeemeetings is negatively associated with fraudulent reporting (Färber 2005). Thus, apositive relation is expected for «g. Following Ahmed et al. 2002, we expect ag,ajQ, 01 J, ai2, and 0)3 to be positive. We predict a positive relation for 014 and a j j .Firms operating in industries where the risk of litigation is high have incentives toadopt conservative financial reporting. Similarly, Big 4 auditors have greater market-based incentives than non-Big 4 auditors to protect their reputation capital andtherefore enhance eamings conservatism (Basu, Hwang, and Jan 2000). Finally,we predict ajg to be positive following Warfield, Wild, and Wild 1995, who findthat managerial ownership is associated with the informativeness of eamings. We

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 837

predict a negative sign for a]7 consistent with prior research that institutionalinvestors may emphasize short-term performance and, thus, greater likelihood ofeamings management (Bushee 2004; Kury 2006). When conservatism is defined asCONCSCO, we do not include RDADV in (2).

Sample and univariate analyses

Our search for sample firms begins with firms that are included in the S&P 500 forthe years 2000 through 2002. Like DeFond et al. 2005, our sample period mostlypredates SOX. We limit our sample to the pre-SOX period because more variationin audit committee appointments can be expected during the pre-SOX period. Ourfocus on larger firms is motivated by prior research (Klein 2002b; Karamanou andVafeas 2005). Furthermore, the likelihood of data availability on attributes ofboards of directors and attributes of audit committees' expertise is higher for largerfirms than for smaller firms, particularly before SOX. A search on COMPUSTATfor the S&P 500 firms yielded 389 firms or 1,167 firm-years (389 X 3 years). Weexclude 194 firm-years in financial services industries (Standard Industrial Classi-fication [SIC] codes 6000-6900) because accruals of these firms are likely to bedifferent from accruals of firms in other industries. Next, we exclude 44 firm-yearsfor which either the financial data or the govemance data are unavailable. We hand-collect data on the qualifications and experience of the members of the audit com-mittee from proxy statements, 10-K reports, company websites, and other publiclyavailable sources. Thus, the total number of firm-years available to estimate CON-ACRU, CONACRUE, and CONBM is 929 (310 firms). Finally, we exclude 296firm-years where data are unavailable for any of the three reserves (LIFO inven-tory, R&D expense, and advertising expense) needed to estimate our final measureof conservatism, CONCSCO (633 firm-years or 211 firms).

Industry distribution for the sample appears in Table 1. Business equipment,manufacturing, and retail industries collectively represent 48 percent of the totalfirm-years for conservatism measures CONACRU, CONACRUE, and CONBM and61 percent for the CONCSCO measure.

Information conceming the presence of financial experts on the audit commit-tee for the sample firms is summarized in Table 2. It appears that the proportion offirms with at least one accounting financial expert has been gradually increasingover time. Panel B reports the proportion of experts as a percentage of audit com-mittee. For the first year of SOX, accounting experts constitute a little more than afourth of the audit committees of the sample firms with an accounting expert. It isclear that there are more nonaccounting financial experts than accounting financialexperts on the audit committees of the sample firms.

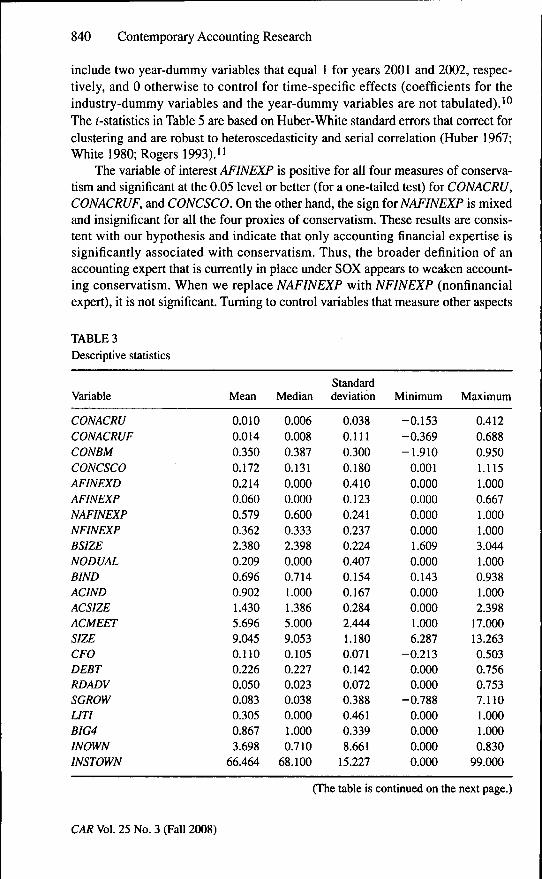

Descriptive statistics for the pooled sample are in Table 3. The median valuefor the CONCSCO measure of 0.13 is comparable to the median value reported byPenman and Zhang 2002 for the entire COMPUSTAT sample over the period1975-97 of 0.11. About 21 percent of the firm-years have at least one accountingfinancial expert. Only 6 percent of the total audit committee directors qualify asaccounting financial experts. The proportion of audit committee directors who areneither accounting financial experts nor nonaccounting financial experts is 36.2

CAR Vol. 25 No. 3 (Fall 2008)

838 Contemporary Accounting Research

percent. The mean and median values oi ACIND (audit committee independence) arehigher than those oí BIND (board indepetidence). The tnean value for NODUAL is0.21, indicating that for 79 percent of the firm-years, the CEO and the chairman ofthe board are the same individual. About 87 percent of the total firm-years areaudited by the Big 4 auditors. The mean percentages of common stock held byinsiders and institutions are, respectively, 3.70 percent and 66.5 percent.

Untabulated correlation coefficients indicate that, as expected, CONACRU andCONACRUE are highly correlated. The correlations between CONCSCO and othermeasures of conservatism are positive and significant at the 0.01 level. However,CONBM is not significantly correlated with CONACRU or CONACRUF. Turningto the variable of interest, AFINEXP is positively and significantly correlated at the0.01 level (for a two-tailed test) with all proxies for conservatism except CONBM.The correlation between AEINEXP and CONBM is positive but not significant atthe 0.10 level. Also, the correlations between the proxies for conservatism andNEINEXP (the proportion of audit committee directors who are nonfinancialexperts) are negative but not significant. Similarly, the correlations betweenNAEINEXP and the proxies are negative except for CONBM, and only the correla-tion between NAEINEXP and CONCSCO is significant at the 0.10 level. Overall,these results are consistent with the hypothesis that accounting financial expertiseof the audit committee is positively associated with conservatism.

TABLE 1Industry distribution

Industry

Consumer nondurablesConsumer durablesManufacturingEnergyChemicals and allied productsBusiness equipmentTelephone and telephone transmissionUtilitiesShopsHealth careOther

Firm-years

For conservatismmeasures other For CONCSCO

than CONCSCO

7533

15742

,471603479

12973

100929

measure

4624

1432147

15120

0906328

633

Note:

Industry classification is based on 11 Fama and French industries excluding money andfinance (see http://mba.tuck.dartmouth.edu/pages/faculty/ken.french).

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 839

Next, we examine whether differences in mean and median values of the variousconservatism measures between accounting and nonaccounting financial expertsare significant. Those results are reported in Table 4. AFINEXD equals 1 for firm-years with at least one accounting financial expert and 0 for firm-years with onlynonaccounting or nonfinancial experts. Both mean and median values of conserva-tism are higher for firm-years with at least one accounting financial expert relativeto firm-years that have only nonaccounting financial experts for all measuresexcept CONBM. Furthennore, the differences in mean and median values are sig-nificant at the 0.01 level. These results suggest that greater conservatism is associ-ated with accounting financial experts.

4. Results

Multivariate results

Results of the multivariate model are reported in Table 5. To control for industry-specific effects, we include 10 industry-dummy variables based on Fama-Frenchindustry classifications (excluding money and finance — see Table 1). We also

TABLE 2Presence of financial experts on the audit committee for sample firms

Panel A: Proportion of firms (as a percentage of total sample)

With at least With at least one With at least oneone accounting nonaccounting nonfinancial

Year financial expert financial expert expert

200020012002

19.7521.4023.10

96.5095.9097.10

83.7584.3084.60

Panel B: Proportion of experts as a percentage of audit committee in firms that have at leastone financial expert

Accounting Nonaccounting NonfinancialYear financial expert financial expert exjjert

200020012002

28.5028.0027.20

45.6047.6047.10

25.9024.4025.70

Notes:

Following DeFond et al. 2005, members of the audit committee are classified into threecategories. Accounting financial experts are directors with experience as a certifiedpublic accountant, auditor, principal or chief financial officer, controller, or principalor chief accounting officer. Nonaccounting financial experts are all directors withexperience as the chief executive officer or president of a for-profit corporation.Nonfinancial experts are directors who are neither accounting nor nonaccountingfinancial experts.

CAR Vol. 25 No. 3 (Fall 2008)

840 Contemporary Accounting Research

include two year-dummy variables that equal 1 for years 2001 and 2002, respec-tively, and 0 otherwise to control for time-specific effects (coefficients for theindustry-dummy variables and the year-dummy variables are not tabulated).'^The i-statistics in Table 5 are based on Huber-White standard errors that correct forclustering and are robust to heteroscedasticity and serial correlation (Huber 1967;White 1980; Rogers 1993). 11

The variable of interest AFINEXP is positive for all four measures of conserva-tism and significant at the 0.05 level or better (for a one-tailed test) for CONACRU,CONACRUF, and CONCSCO. On the other hand, the sign for NAFINEXP is mixedand insignificant for all the four proxies of conservatism. These results are consis-tent with our hypothesis and indicate that only accounting financial expertise issignificantly associated with conservatism. Thus, the broader definition of anaccounting expert that is currently in place under SOX appears to weaken account-ing conservatism. When we replace NAFINEXF with NFINEXF (nonfinancialexpert), it is not significant. Turning to control variables that measure other aspects

TABLE 3Descriptive statistics

Variable

CONACRUCONACRUFCONBMCONCSCOAFINEXDAFINEXPNAFINEXPNFINEXPBSIZENODUALBINDACINDACSIZEACMEETSIZECFODEBTRDADVSGROWLITIBIG4INOWNINSTOWN

Mean

0.0100.0140.3500.1720.2140.0600.5790.3622.3800.2090.6960.9021.4305.6969.0450.1100.2260.0500.0830.3050.8673.698

66.464

Median

0.0060.0080.3870.1310.0000.0000.6000.3332.3980.0000.7141.0001.3865.0009.0530.1050.2270.0230.0380.0001.0000.710

68.100

Standarddeviation

0.0380.1110.3000.1800.4100.1230.2410.2370.2240.4070.1540.1670.2842.4441.1800.0710.1420.0720.3880.4610.3398.661

15.227

Minimum

-0.153-0.369-1.910

0.0010.0000.0000.0000.0001.6090.0000.1430.0000.0001.0006.287

-0.2130.0000.000

-0.7880.0000.0000.0000.000

Maximum

0.4120.6880.9501.1151.0000.6671.0001.0003.0441.0000.9381.0002.398

17.00013.2630.5030.7560.7537.1101.0001.0000.830

99.000

(The table is continued on the next page.)

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 841

TABLE 3 (Continued)

Notes:

CONACRU = mean total accruals (net income before extraordinary items plusdepreciation less cash flow from operations) scaled by total assets,averaged over three-year period centered on the year of interest andmultiplied by - 1 (Givoly and Hayn 2000);

CONACRUF = fixed-effect measure of total accruals estimated as the firm-specificintercept from a fixed-effect regression of current accruals on laggedaccruals for each of the prior six years (Hui and Matsunaga 2004). Thefirm-specific intercept is multiplied by — 1 ;

CONBM = firm-specific intercept, a,, from the following fixed-effect regression ofbook-to-market ratio (BTM) on current and six lagged (k = 0-6) annualstock retums (RET) (Beaver and Ryan 2000), multiplied by - 1 :

RTA4 = V -I- V + VajMj, — X ^ Xi ^ Xtwhere i and t are firm and year subscripts;

CONCSCO = amount of inventory, R&D, and advertising reserves scaled by netoperating assets for firms that have one or more of the three reserves(Penman and Zhang 2002);

AFINEXD = a dummy variable that equals 1 if the audit committee has at least oneaccounting financial expert, and 0 otherwise;

AFINEXP = proportion of audit committee directors who qualify as accountingfinancial experts to the total number of directors in the audit committee;

NAFINEXP = proportion of audit committee directors who qualify as nonaccountingfinancial experts to the total number of directors in the audit committee;

NFINEXP - proportion of audit committee directors who qualify as nonfinancialexperts to the total number of directors in the audit committee;

BSIZE = log of total number of directors in the board;

NODUAL = a dummy variable that equals 1 if the CEO is also not the chairman of theboard, and equals 0 otherwise;

BIND = proportion of directors that are independent in the board of directors;

ACIND = proportion of directors that are independent in the audit committee;

ACSIZE = log of total number of directors in the audit committee;

ACMEET = number of meetings by the audit committee during the year;

SIZE = log of total assets;

CFO = cash flow from operations, scaled by total assets;

DEBT = long-term debt divided by total assets;

RDADV = R&D plus advertising expense, scaled by sales;

SGROW = annual percentage change in sales;

LITI = a dummy variable that equals 1 for biotechnology, computers, electronics,and retailing and equals 0 for other industries;

(The table is continued on the next page.)

CAR Vol. 25 No. 3 (Fall 2008)

842 Contemporary Accounting Research

TABLE 3 (Continued)

BIG4 = a dummy variable that equals 1 if the company's auditor is one of the Big 4audit firms and equals 0 otherwise;

INOWN = percentageofcommonstockownedby all officers of the corporation anddirectors as a group (Karamanou and Vafeas 2005);

INSTOWN = percentage of common stock held by institutions (Karamanou and Vafeas2005).

of corporate govemance, the sign for BSIZE is mixed and significant at the 0.10level in two cases. NODUAL, as predicted, is positive except for CONBM and sig-nificant for two measures of conservatism. BIND is positive in all four cases andsignificant in three cases. ACSIZE and ACMEET are not significant in any of thecases. This is consistent with Bedard et al. 2004, who find that size of the auditcommittee and the frequency of the meetings are not associated with the likelihoodof earnings management. The sign for ACIND is mixed and not significant.INSTOWN is negative, as predicted, and suggests that institutions have a prefer-ence for more positive eamings.

Does strong governance enhance the relation between accounting financialexpertise and conservatism?

DeFond et al. (2005) report that the positive investor response to accounting financialexperts on the audit committee is conditional upon the firm's corporate govemance— that is, accounting expertise is more effective when other govemance mecha-nisms are already in place. This finding motivates us to examine whether ourresults are also conditional upon the strength of govemance for the sample firms.'2Following DeFond et al. 2005, we construct a measure of strong governance{SGOV) that equals 1 if GOV is greater than or equal to the sample median, and 0otherwise.

We define the variables as follows:

GOV = a summary measure of corporate govemance that is equal to the sumof the following six dichotomous govemance variables: LBSIZE,HBIND, H ACSIZE, H ACIND, LGINDEX, and HINSTOWN;

LBSIZE = a dummy variable that equals 1 if the board size is less than thesample median, and 0 otherwise;

HBIND = a dummy variable that equals 1 if the proportion of outside directorsis greater than 60 percent, and 0 otherwise;

H ACSIZE = a dummy variable that equals 1 if the proportion of the number ofdirectors on the audit committee to the total number of directorson board is greater than the sample median, and 0 otherwise;

H ACIND = a dummy variable that equals 1 if the audit committee is composedof solely independent directors, and 0 otherwise;

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 843

00

c

§

'S

II

§

it

Sc§

p H «

u

Î

0 C^Tt en

Ö d d ci

« rt 00 rt—' fO C\ "Op p en -Hd d d d

00 vo

d oiI

00 ON ON -^O O ^ voÖ Ö Ö Ö

00 —" 00 r-— 3 •>«• Op p f<^ fsd d d d

O O O O<j u u o

CA(1>

. 25 No. 3 (Fall 2008)

844 Contemporary Accounting Research

TABLE 5

OLS regressions of conservatism measures on audit committee's financial expertise andcontrol variables

Intercept

AFINEXP

NAFINEXP

BSIZE

NODUAL

BIND

ACSIZE

ACIND

ACMEET

SIZE

DEBT

CFO

RDADV

SGROW

LITl

B1G4

INOWN

Predictedsign

?

+

?

?

-1-

+

7

+

-1-

-1-

-1-

+

+

+

+

+

+

CONACRUCoefficient§(/-statistic)

0.029(1.10)0.022(L73)t

0.001(0.20)

-0.008(-0.92)

0.009(2.36)*0.006(0.57)0.003(0.46)0.002(0.27)

-0.001(-0.75)-0.002(-0.79)

0.012(1.04)0.114(3.52)*0.100(3.15)*

-0.007(-1.68)t

0.001(0.15)0.003(0.70)0.001(0.83)

Conservatism measures

CONACRUFCoefficient^(i-statistic)

0.102(1.40)0.082(1.94)t

0.002(0.13)

-0.053(-1.99)t

0.026(2.60)*0.059(1.66)t

0.012(0.63)

-0.007(-0.23)-0.002(-1.07)

0.003(1.43)0.029(0.79)0.296(3.54)*0.254(2.75)*

-0.012(-1.21)

0.010(0.44)0.007(0.60)0.001(0.93)

CONBMCoefficient?(i-statistic)

0.149(1.02)0.001(0.30)

-0.016(-0.39)

0.090(1.83)*

-0.022(-0.85)

0.121(1.37)*

-0.003(-0.10)-0.110(-1.23)-0.002(-0.57)-0.004(-0.41)

0.133(1.60)*0.983(6.26)*0.177(1.36)*

-0.048(-1.32)*

0.017(0.40)

-0.067(-1.29)-0.001(-0.90)

CONCSCOCoefficient?(r-statistic)

-0.104

(-0.78)0.162(1.78)t

-0.028(-0.88)

0.010(0.21)0.007(0.38)0.181(2.73)*

-0.039(-1.27)

0.052(1.25)0.003(1.03)0.007(0.82)

-0.124(-1.85)t

0.060(1.58)*

-0.056(-1.74)t

0.040(1.60)*0.023(1.16)0.001

(0.17)

(The table is continued on the next page.)

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 845

TABLE 5 (Continued)

INSTOWN

Adj. /?2

Predictedsign

CONACRUCoefficient^(i-statistic)

-0.002(-1.91)t

0.16

Conservatism measures

CONACRUFCoefficient^(i-statistic)

-0.001(-1.74)t

0.24

CONBMCoefficient^(i-statistic)

-0.002(-2.93)i

0.26

CONCSCOCoefficient^(/-statistic)

-0.001(-1.92)t

0.46

Notes:

Data are for the years 2000 through 2002. Total number of firm-year observations is 929 forall measures of conservatism except CONCSCO. For CONCSCO, it is 633. Variablesare as defined in Table 3. Each model includes, but does not tabulate, 10 industrydummies based on 11 Fama-French industries (see Table 1) and two year dummiesthat equal 1 for years 2001 and 2002, respectively, and 0 otherwise. For theCONCSCO measure, no observations are available in the utilities industry and thusthat model uses only 9 industry dummies.

Significances below are for one-tailed tests where predicted signs are specified and for two-tailed tests otherwise.

* Significant at the 10 percent level.

1' Significant at the 5 percent level.

i Significant at the 1 percent level.

§ /-statistics (indicated within parentheses) are computed based on Huber-White robuststandard errors that correct for serial correlation among multiple-year observations.

LGINDEX = a dummy variable that equals 1 if the GINDEX is below the samplemedian, and 0 otherwise; GINDEX, developed by Gompers, Ishii,and Metriek 2003, measures the strength of a firm's governancesystem and is constructed based on a simple counting of 24 cor-porate govemance provisions — a low (high) GINDEX means thata firm has a strong (weak) govemance system;

HINSTOWN = a dummy variable that equals 1 if the percentage of institutionalownership (¡NSTOWN) is greater than the sample median, and 0otherwise.

We interact SGOV with AFINEXP and NAFINEXP to test whether the relationbetween accounting financial expertise and conservatism is accentuated by stronggovemance. Because SGOV includes a variety of govemance variables that weseparately consider in the prior analysis, we do not include these other govemancevariables in this analysis. Results are reported in Table 6. Recall that SGOV is adummy variable that equals 1 for strong governance and 0 otherwise; thus, the

CAR Vol. 25 No. 3 (Fall 2008)

846 Contemporary Accounting Research

coefficients on AFINEXP and NAFINEXF in this model represent the coefficients onthese expertise variables for firms with weak govemance, and the sum of the coef-ficients for AFINEXP and AFINEXP*SGOV (NAFINEXP and NAFINEXP*SGOV)represents the coefficients on expertise for firms with strong govemance. We reportthe significance testing for the combined coefficients at the bottom of Table 6.

Results show that neither AFINEXP nor NAFINEXP is significant for three ofthe four conservatism measures. Thus, for firms with weak govemance mechan-isms, audit committee members' accounting financial expertise does not appear toenhance conservatism. For CONBM, the AFINEXP and NAFINEXP variables arenegative and significant, implying that the presence of such experts is associatedwith lower conservatism in firms with weak govemance. In contrast, the incremen-tal effect of strong govemance captured by AFINEXP*SGOV is positive for all fourmeasures of conservatism and statistically significant for three of the four measures.The coefficient on NAFINEXP*SGOV, the incremental effect of nonaccountingfinancial expertise, is not significant for any of the conservatism measures, nor isthe sum of the coefficients NAFINEXP and NAFINEXP*SGOV (not reported).Note that the sum of the coefficients AFINEXP and AFINEXP*SGOV reported atthe bottom of the table represents the coefficients for firms with strong govemanceand it is positive and significant for all four measures of conservatism, includingCONBM. These results indicate that accounting financial experts on the auditcommittee are able to effectively perform their monitoring function and promoteconservative accounting only when they are in boards that are characterized bystrong govemance. It appears that in weak boards the presence of financial exper-tise on the audit committee is ineffective in promoting conservative accounting —that is, the effect of accounting financial expertise is undermined by weak govem-ance mechanisms. Also, it appears that even in the presence of strong govemance,nonaccounting financial experts are not able to enhance conservatism. 13 in sum-mary, our results corroborate the findings in DeFond et al. 2005 and underscore thecontextual nature of the relation between audit committees' accounting financialexpertise and accounting conservatism.

Sensitivity ehecks

We conduct a variety of sensitivity checks to assess the robusmess of our results tooutliers, altemative variables, and model specifications. We describe our sensitivitychecks as follows. When (2) is estimated annually for the years 2000, 2001, and2002, the untabulated results show that for CONACRU, AFINEXP is positiveand significant at the 0.05 level or better for all the three years. When CONACRUFis the dependent variable, AFINEXP is positive and significant at the 0.10 level forthe years 2000 and 2002 and significant at the 0.01 level in 2001. When CONCSCOis the dependent variable, AFINEXP is positive and significant at the 0.10 level for2000 and significant at the 0.01 level for 2001 and 2002. On the other hand,NAFINEXP is negative for all four measures in 2000 and positive for all measuresexcept CONBM in 2001 and positive in 2002 for all measures except CONACRU.However, NAFINEXP is not significant for any of the conservatism measures exceptfor CONCSCO, where it is marginally significant for 2000. Overall, these results

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 847

TABLE 6OLS regressions of conservatism measures on audit committee's financial expertise andcontrol variables conditioned on the role of govemance

rVedictedsign

Intercept ?

AFINEXP +

AFINEXP*SGOV ?

NAFINEXP ?

NAFINEXP*SGOV ?

SGOV +

SIZE +

DEBT +

CFO +

RDADV +

SGROW +

UTl +

BIG4 +

INOWN +

Adj. ^2

/-statistic forAFINEXP

+ AF1NEXP*SGOV

CONACRUCoefficient?(/-statistic)

-0.003

(-0.19)0.010(0.55)0.008(0.32)

-0.007(-0.71)

0.009(0.80)

-0.005(-0.70)-0.001(-0.74)

0.011(1.13)0.137(3.46)*0.107(3.25)*

-0.006(-1.70)t

0.001(0.19)0.001(0.27)0.001(1.89)t

0.16

(2.05)t

Conservatism measures

CONACRUFCoefficient?(/-statistic)

0.007(0.18)0.001(0.03)0.102(1.74)*

-0.019(-0.76)

0.046(1.28)

-0.023(-1.03)

0.002(0.58)0.002(0.08)0.345(3.48)*0.309(2.77)*0.003(0.38)0.010(0.83)0.006(0.60)0.001(1.54)*0.24

(3.01)*

CONBMCoefficient?(/-statistic)

0.256(2.37)t

-0.553(-2.18)t

0.719(2.39)t

-0.134(-1.69)*

0.219(1.38)

-0.159(-1.25)

0.001(0.07)0.142(1.77)t0.967(4.15)*0.104(0.58)

-0.047(-1.71)t

0.017(0.50)

-0.076(-1.19)-0.001(-1.08)

0.26

(1.50)*

CONCSCOCoefficient?(/-statistic)

-0.075(-1.09)

0.001(0.06)0.211(2.06)t0.032(0.76)

-0.066(-1.32)

0.057(1.80)*0.011(2.02)t

-0.173(-1.99)t

0.070(1.78)t

-0.064(-1.94)t

0.039(1.80)t

0.027(1.44)*

-0.001(-0.22)

0.46

(3.49)*

(The table is continued on the next page.)

CAR Vol. 25 No. 3 (Fall 2008)

848 Contemporary Accounting Research

TABLEÓ (Continued)

Notes:

Data are for the years 2000 through 2002. Total numher of firm-year ohservations is 929 forall measures of conservatism except CONCSCO. For CONCSCO, it is 633. Variablesare as defined in Table 3. Each model includes, but does not tabulate, 10 industrydummies based on 11 Fama-French industries (see Table 1) and two year dummiesthat equal 1 for years 2001 and 2002, respectively, and 0 otherwise. For theCONCSCO measure, no observations are available in the utilities industry and thusthat model uses only 9 industry dummies.

SGOV = a dummy variable that equals 1 if GOV is greater than or equal to the samplemedian, and 0 otherwise;

GOV = a summary measure of corporate govemance that is equal to the sum of thefollowing six dichotomous govemance variables: LBSIZE, HBIND,

HACSIZE, HACIND, LGINDEX, and HINSTOWN;

LBSIZE = a dummy variable that equals 1 if the board size is less than the samplemedian, and 0 otherwise;

HBIND = a dummy variable that equals 1 if the proportion of outside directors isgreater than 60 percent, and 0 otherwise;

HACSIZE = a dummy variable that equals 1 if the proportion of the number of memberson the audit committee to the total number of directors on the board isgreater than the sample median, and 0 otherwise;

HACIND = a dummy variable that equals 1 if the audit committee is composed of solelyindependent directors, and 0 otherwise;

LGINDEX = a dummy variable that equals 1 if the GINDEX is below the sample median,and 0 otherwise; GINDEX, developed by Gompers et al. 2003, measures thestrength of a firm's govemance system and is constmcted based on a simplecounting of 24 corporate govemance provisions — a low (high) GINDEXmeans that a firm has a strong (weak) govemance system;

HINSTOWN = a dummy variable that equals 1 if the percentage of institutional ownership(¡NSTOWN) is greater than the sample median, and 0 otherwise.

Significances below are for one-tailed tests where predicted signs are specified and for two-tailed tests otherwise.

* Significant at the 10 percent level.

t Significant at the 5 percent level.

* Significant at the 1 percent level.

§ i-statistics (indicated within parentheses) are computed based on Huber-White robuststandard errors that correct for serial correlation among multiple-yearobservations.

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 849

once again support the hypothesis that only accounting financial expertise is associ-ated with accounting conservatism. Furthermore, the results indicate that the resultsbased on the pooled model do indeed persist for each of the sample years examined. •'*

We also define ACMEET, ACSIZE, and ACIND as categorical variables ratherthan as continuous variables as in Abbott, Parker, and Peters 2004 and our resultsare consistent with the results in Table 5. G. Krishnan (2005) finds that auditors'industry expertise is associated with conservatism. When we include auditors'industry expertise and auditor tenure in (2), they are not significant. We follow pro-cedures recommended by Belsley, Kuh, and Welsch 1980 in identifying outliersand our results are not sensitive to the exclusion of outliers.

Q score

The CONCSCO measure is based on Penman and Zhang's 2002 C score conserva-tism index. They also offer a measure of conservatism that impacts the incomestatement, designated as the Q score. It is a combination of the change in theC score and the industry (median) adjusted C score. Penman and Zhang (2002)refer to the Q score as an "eamings quality indicator". The Q score can be thoughtof as the unexpected C score and captures the effects of past conservatism. Penmanand Zhang provide evidence that the Q score has predictive power for one-yearahead retum on net operating assets (RNOA) incremental to past RNOA. We usethe Q score as an altemative measure of conservatism and estimate (2). The untab-ulated results indicate that the coefficient on AFINEXP is 0.112 and significant atthe 0.05 level. NAFINEXP is negative and insignificant.'^

Control for Arthur Andersen and exchange listing

Next, we examine whether our results are driven by former clients of ArthurAndersen or firms not listed on the NYSE. We use a dummy variable that equals 1for former Arthur Andersen clients and 0 for non-Andersen clients. We interact thedummy with AFINEXP and NAFINEXP. Untabulated results show that neitherinteraction is significant. The dummy variable is also insignificant. However,AFINEXP is positive and significant for CONACRUF, CONCSCO, and CONACRU.NAFINEXP is not significant. These results indicate that our results are not sensitiveto former Andersen clients. A similar test indicates that our results are not sensitive toexchange listing.

Asymmetric loss recognition test

We also use Ball and Shivakumar's 2005 asymmetric loss recognition test, an alter-native measure of conservatism. We run a regression of total accruals over totalassets at the beginning of the year on positive cash flows, a dummy variable thatequals 1 for negative cash fiows and 0 for positive cash fiows, and include AFINEXPand NAFINEXP as main effects and interact both variables with positive and nega-tive cash fiows. The untabulated results indicate that although the interactionbetween NAFINEXP and negative cash fiows is insignificant, the interaction betweenAFINEXP and negative cash fiows is positive and significant at the 0.01 level,indicating that timely recognition of losses via accruals is greater, that is, more

CAR Vol. 25 No. 3 (Fall 2008)

850 Contemporary Accounting Research

conservative for accounting financial experts. In short, these results are consistentwith the notion that higher conservatism is associated with accounting financialexpertise but not nonaccounting expertise.

Control for endogeneity

Prior research recognizes that attributes of corporate boards and govemance mech-anisms are endogenously determined (Klein 2002b). Building on a model developedby Agrawal and Chadha 2005, we examine whether our results persist after con-trolling for endogeneity. For firm performance we use an accounting measure(ROA) rather than stock retums. Similarly, for volatility we measure eamings vola-tility because one of our proxies for conservatism, CONBM, is highly correlatedwith any stock-related measure. We also add the GINDEX as of the beginning ofthe year. A high (low) GINDEX implies weak (strong) govemance. DeFond et al.(2005) find that the market reactions to the appointment of a financial expert to theaudit committee are contingent upon existing govemance structure as measured bythe GINDEX. Thus, we estimate the following model:

FINEX = ßo + ßiSIZE + ß2PR0A + ß^DEBT + ß^SGROW + ßßSIZE+ ß(,AEMF + ß^GINDEX -H ß^EVOL + ßgAGE (3),

where FROA is the prior three-year average retum on assets; AEMP is a measure ofcapital intensity, computed as total assets divided by number of employees; EVOLis eamings volatility for the past six years; and AGE is the age of the firm from thedate of listing in number of years. Other variables are the same as defined before.Following Agrawal and Chadha 2005, we predict a negative sign for ßi and ß^ anda positive sign for ß2, J83, ß^, ß^, ß^, and ßg. A negative relation is expected for ßjbecause a low GINDEX is consistent with good governance, including havingexperts on the audit committee.

We run two specifications. Model (3A) does not include eamings volatilityand firm age because both are strongly correlated with the book-to-market ratio.Model (3B) is the full model. Untabulated results indicate that, with the exceptionof DEBT and AEMF, signs for all the variables are in the expected direction. SIZE,PROA, BSIZE, GINDEX, EVOL, and AGE are significant at the 0.10 level or bet-ter. The pseudo R^for the full model is modest, but higher than the R^in Agrawaland Chadha 2005.16

Next, we replace AFINEXD with FFINEX, the predicted probability of havinga financial expert on the audit committee and estimate (2). PFINEX is estimatedusing model (3B) for CONACRU, CONACRUF, and CONCSCO. For CONBM, weuse both models (3A) and (3B). The untabulated results indicate that FFINEX ispositive and significant at the 0.01 level for the accmal-based measures of conserv-atism and significant at the 0.10 level for CONCSCO. More importantly, results aresignificant at the 0.05 level for CONBM when earnings volatility and age areexcluded in the first stage. NAFINEXF is not significant except for CONBM, whereit is negative and significant at the 0.10 level. Overall, these findings are consistentwith our hypothesis and alleviate concems that the reported results are driven bythe endogenous relationship between conservatism and board attributes.

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 851

5. Conclusions

In response to several well-publicized accounting scandals and increases in restate-ments of financial statements, the U.S. Congress passed the Sarbanes-Oxley Act toenhance corporate govemance mechanisms and restore investor confidence infinancial reporting. One aspect of corporate govemance that has received consider-able attention is improving the effectiveness of the audit committee, the ultimatemonitor of the financial reporting process. The SOX mandates the disclosure ofwhether at least one member of the audit committee is a financial expert. However,the final version of the rule adopted by the SEC defined experts to include bothaccounting and nonaccounting experts. Did the SEC do the right thing? Are thenonaccounting experts just as competent as the accounting experts in enhancing thequality of financial reporting? We examine the composition of the audit committeesfor a sample of S&P 500 firms and our results suggest that an audit committee'saccounting financial expertise is positively associated with conservatism, a funda-mental property of financial statements. This finding does not hold for nonaccountingfinancial experts or nonfinancial experts. We also find that the audit committee'sfinancial experts are able to effectively perform their monitoring function and pro-mote conservative accounting only when they are in boards that are characterizedby strong govemance. In other words, the effect of accounting financial expertise isundermined by weak govemance mechanisms. The results are robust to altemativemeasures of conservatism iind controls for other characteristics of boards of direc-tors. We also find that only accounting financial expertise is positively associatedwith Penman and Zhang's 2002 Q score, a measure of eamings quality. Overall,our findings are consistent with the notion that accounting expertise contributes togreater monitoring by the members of the audit committee, which in tum enhancesmultiple attributes of financial reporting quality.

Our findings add to the growing literature on the relation between auditcommittee's expertise and other measures of financial reporting quality, such asaccmals-based eamings management and eamings restatements (Klein 2002a; Xieet al. 2003; Bedard et al. 2004; Agrawal and Chadha 2005). Our findings haveimplications for regulators, corporate boards, and the accounting profession. Find-ings from concurrent research and this study suggest that adopting a narrower def-inition of a financial expert is likely to enhance the audit committees' effectiveness.Our findings are also relevant to regulators in other countries who are consideringadopting measures to enhance corporate govemance, particularly the effectivenessof audit committees. The implication for boards of directors is that merely appoint-ing an accounting expert to the audit committee without improving the overallgovemance quality is not likely to enhance the effectiveness of the audit commit-tee. Finally, our findings document an association rather than causation between anaudit committee's expertise and conservatism. Our sample does not permit us toexamine whether firms that replace nonaccounting experts with accounting expertsexhibit greater conservatism. When more data become available, future researchcould examine whether and how our results change in the post-SOX period.

CAR Vol. 25 No. 3 (Fall 2008)

852 Contemporary Accounting Research

Endnotes

1. In contrast, the NYSE requires that at least one member of the audit committee haveaccounting or related financial management expertise and that all members of the auditcommittee be financially literate or become financially literate within a reasonableperiod of time after their appointment to the audit committee. Similarly, the NASDAQrules require that all members of the audit committee be able to read and understandfinancial statements at the time of their appointment. Furthermore, companies mustcertify whether at least one member of the audit committee has past employmentexperience in finance or accounting, requisite professional certification in accounting,or any other comparable experience or background that results in the individual'sfinancial sophistication, including being or having been a CEO, CFO, or other seniorofficer with financial oversight responsibilities (NYSE 2004; NASDAQ 2004).

2. Dennis Beresford, a former chairman of the Financial Accounting Standards Board,expresses concern that a large number of companies may have appointednonaccounting experts to the audit committees. He further cautions that most CEOs donot have specific knowledge of generally accepted accounting principles, SECregulations, or Public Company Accounting Oversight Board auditing standards andmust depend heavily on the finance executives and auditors of the companies on whoseboards they sit (Beresford 2005).

3. There is a growing literature on accounting conservatism (Ball, Kothari, and Robin2000; Givoly and Hayn 2000; Bushman and Piotroski 2006; Givoly, Hayn, andNatarajan 2007; Lobo and Zhou 2006).

4. Beekes, Pope, and Young (2004) find evidence that U.K. firms with a higher proportionof outside directors tend to recognize bad news in eamings on a timely basis. Theauthors do not examine audit committee characteristics, such as independence, numberof meetings, and members' accounting expertise.

5. We use Ball and Shivakumar's 2005 asymmetric loss recognition test (conditionalconservatism) because it is less controversial than Basu's 1997 reverse regressionframework. Following Givoly, Hayn, and Natarajan's 2007 suggestion, we use multipleproxies to measure conservatism.

6. Our study differs from prior research in many ways. Xie et al. (2003) do not distinguishbetween accounting and nonaccounting financial expertise. Unlike Bedard et al. 2004,we include board independence and CEO duality in our models to tease out theincremental effect of the audit committee's expertise. Also, both Xie et al. (2003) andBedard et al. (2004) do not address endogeneity issues in board characteristics andgovemance mechanisms. Furthermore, Bedard et al. (2004) focus on a sample of 200firms with extreme positive and negative abnormal accruals and caution that theirresults may not be generalizable for firms with lower levels of eamings management.Agrawal and Chadha (2005) also do not distinguish between accounting andnonaccounting financial expertise. Also, they study only firms restating their financialstatements. Thus, it is not clear whether their findings are generalizable to firms thatare not involved in aggressive forms of financial reporting. A focus on firms that do notrestate financial statements but might otherwise engage in less aggressive financialreporting is important because those firms are representative of the population of firms.

CAR Vol. 25 No. 3 (Fall 2008)

Does the SOX Definition of an Accounting Expert Matter? 853

Finally, J. Krishnan (2005) focuses only on firms that changed their auditors. We do notimpose such a restriction.

7. This argument is consistent with evidence from behavioral research that individualswith significant financial experience have knowledge of misstatement occurrences infinancial statement accounts and underlying causes of misstatements (Libby 1985;Ashton 1991; Solomon, Shields, and Whittington 1999).

8. Carcello, Hermanson, and Neal (2002) analyze disclosures in audit committee chartersand find that about half of the audit committee charters examined disclose that theaudit committee reviews or approves accounting changes, indicating that auditcommittees attempt to infiuence financial reporting quality. Furthermore, Statement onAuditing Standards (SAS) No. 90, Audit Committee Communications, requires that theauditor discuss with the audit committee the auditor's judgement about the quality, notjust the acceptability, of the company's accounting principles employed in its financialreporting and encourages a three-way discussion among the auditor, management, andthe audit committee.

9. Ahmed et al. (2002) average over a six-year period. We use a three-year period becausewe do not have COMPUSTAT data for all firms for the year 2005.

10. See Petersen 2007 for a discussion of year dummies.

11. The Huber-White i-statistic is lower than the OLS unadjusted /-statistic for AFINEXP.For example, when the dependent variable is CONACRU, the unadjusted i-statisticsand White t for AFINEXP are, respectively, 2.25 and 2.20 (compared with the Huber-White/of 1.73).

12. We thank an anonymous referee for this suggestion.

13. We also consider altemative cutoff values to provide some evidence on the sensitivityof our results to specific thresholds. We remeasure SGOV with the followingmodifications. For BSIZE and ACSIZE, instead of the median we use a 66 percentcutoff; for BIND we change the cutoff from 60 percent to 50 percent or 70 percent; forGINDEX and INSTOWN we use 66 percent instead of the median cutoff. The resultsare not sensitive to these modifications. Finally, without modifying the individualcomponents of SGOV, we modify the cutoff for SGOV from the median to 66 percent.Again, the results are similar. These findings provide some assurance that the resultsreported in Table 6 also hold when altemative cutoff values are used.

14. We also attempt to examine the association between the changes in an auditcommittee's expertise and the change in conservatism. However, the ability to do thisanalysis is limited by the small number of changes in members of the audit committee,specifically members who are accounting financial experts. We find that allconservatism measures, except CONACRUF, register a higher increase for firms thatappoint a new director with accounting financial expertise as compared with firms thatlet go of such directors. Although this is consistent with expectations, the differencesare not statistically significant.

15. We also conduct tests of real eamings management (Roychowdhury 2006) and findthat only accounting financial expertise consu-ains real eamings management. Thoseresults are not reported for the sake of brevity.

16. The percentage correctly classified by the model is 79 percent for model (3 A) and80 percent for model (3B).

CAR Vol. 25 No. 3 (Fall 2008)

854 Contemporary Accounting Research

ReferencesAbbott, L., S. Parker, and G. Peters. 2004. Audit committee characteristics and restatements.

Auditing: A Journal of Practice & Theory 23 (1): 69-87.Agrawal, A., and S. Chadha. 2005. Corporate govemance and accounting scandals. Journal

of Law and Economics 48 (2): 371-406.Ahmed, A., B. Billings, R. Morton, and M. Stanford-Harris. 2002. The role of accounting

conservatism in mitigating bondholder-shareholder conflicts over dividend policy andin reducing debt costs. The Accounting Review 11 (4): 867-90.

Ashton, A. H. 1991. Experience and error frequency knowledge as potential determinants of

audit expertise. The Accounting Review 66 (2): 218-39.Ball, R. 2001. Infrastructure requirements for an economically efficient system of public

financial reporting and disclosure. Brookings-Wharton Papers on Financial Services:

127-82.Ball, R., S. P. Kothari, and A. Robin. 2000. The effect of intemational institutional factors on

properties of accounting eamings. Journal of Accounting and Economics 29 ( 1 ): 1-51.Ball, R., and L. Shivakumar. 2005. Earnings quality in UK private firms: Comparative loss

recognition timeliness. Journal of Accounting & Economics 39 (1): 83-128.Basu, S. 1997. The conservatism principle and the asymmetric timeliness of eamings.

Journal of Accounting and Economics 24 (1): 3-37.Basu, S., L. Hwang, and C. Jan. 2000. Differences in conservatism between big eight and

non-big eight auditors. Working paper. City University of New York and Califomia

State University.Beasley, M. 1996. An empirical analysis of the relation between the board of director

composition and financial fraud. The Accounting Review 71 (4): 443-65.Beaver, W., and S. Ryan. 2000. Biases and lags in book value and their effects on the ability

of the book-to-market ratio to predict book retum on equity. Journal of Accounting

Research 38 (1): 127-48.Bedard, J., S. M. Chtourou, and L. Courteau. 2004. The effect of audit committee expertise,

independence, and activity on aggressive eamings management. Auditing: A Journal of

Practice & Theory 23 (2): 13-35.Beekes, W., P. Pope, and S. Young. 2004. The link between eamings timeliness, eamings

conservatism and board composition: Evidence from the U.K. Corporate Governance:

An International Review 12 (1): 47-59.Belsley, D., E. Kuh, and R. Welsch. 1980. Regression diagnostics: Identifying influential

data and sources of collinearity. New York: John Wiley & Sons.Beresford, D. Take a seat in the boardroom. 2005. Journal of Accountancy 200 (4): 104-8.Blue Ribbon Committee. 1999. Report and recommendations of the Blue Ribbon Committee

on improving the effectiveness of corporate audit committees. New York StockExchange and National Association of Securities Dealers.

Bushee, B. 2004. Identifying and attracting the "right" investors: Evidence on the behaviorof institutional investors. Journal of Applied Corporate Finance 16 (4): 28-35.

Bushman, R. M., and J. D. Piotroski. 2006. Financial reporting incentives for conservativeaccounting: The influence of legal and political institutions. Journal of Accounting and

Economics 42 {\): 107-48.