Embed Size (px)

Citation preview

THE ACCOUNTING REVIEW American Accounting AssociationVol. 88, No. 3 DOI: 10.2308/accr-503812013pp. 1095–1127

Does Recognition versus Disclosure AffectValue Relevance? Evidence from Pension

Accounting

Kun Yu

University of Massachusetts Boston

ABSTRACT: This study examines whether institutional ownership and analyst following

affect the value relevance of disclosed versus recognized pension liabilities. Using a

sample of firms with pension liabilities that were disclosed under SFAS No. 87 and

subsequently recognized under SFAS No. 158 from 1999 to 2007, I find that off-balance-

sheet pension liabilities are more value relevant for firms with a higher level of institutional

ownership or analyst following in the pre-158 period. More importantly, I find that SFAS

No. 158 increases the value relevance of previously disclosed off-balance-sheet pension

liabilities for firms with a low level of institutional ownership or analyst following, and that

the increase in the value relevance becomes less pronounced for firms with a higher level

of institutional ownership or analyst following. Overall, the results are consistent with the

view that institutional ownership and analyst following affect the value relevance of

disclosed information as well as the valuation difference between disclosed and

recognized information. This study also highlights the importance of considering

institutional ownership and analyst following in the value-relevance research.

Keywords: pension; value relevance; recognition; disclosure; SFAS No. 158.

Data Availability: All data are publicly available from the sources indicated in the text.

I. INTRODUCTION

An important area of research is whether information disclosure in the footnotes is a

substitute for recognition in the financial statements. Since Johnson (1992), a large body

of accounting literature has examined whether and how recognition is distinct from

disclosure. The semi-strong form efficient market hypothesis suggests that recognition versus

disclosure of accounting information should make no difference, as long as the information is

This paper is based on my dissertation at Boston University. I gratefully acknowledge the comments and help of mydissertation chair, Kumar Sivakumar, and my committee members, Krishnagopal Menon and Donald J. Smith. I alsoappreciate comments from Kathryn Easterday, John Harry Evans (senior editor), Steven Kachelmeier (former senioreditor), Sally Wright, two anonymous referees, and the workshop participants at the 2010 AAA Annual Meeting.

Editor’s note: Accepted by John Harry Evans III, with thanks to Steven Kachelmeier for serving as editor on a previousversion.

Submitted: October 2010Accepted: December 2012

Published Online: December 2012

1095

publicly available. A few earlier accounting studies (e.g., Dhaliwal 1986) provide empirical support

for the ‘‘no difference’’ view. However, more recent accounting research generally finds that

recognition is different from disclosure in terms of value relevance (e.g., Ahmed et al. 2006) and

contracting costs (e.g., Espahbodi et al. 2002). This paper examines whether recognition versus

disclosure of pension liabilities affects investors’ valuation in the setting of SFAS No. 158 versus 87.

Prior studies (e.g., Davis-Friday et al. 1999; Ahmed et al. 2006) on the value relevance of

recognition versus disclosure generally assume that the value relevance of disclosed information is

the same across firms and that recognition of previously disclosed accounting items affects all the

firms homogenously. However, the extent to which users of financial reports understand disclosed

information may differ across firms. The FASB stated that only the most sophisticated investors

could understand the implication of disclosed stock option information, while individual investors

and other users could not (SFAS No. 123, para. 105). Similarly, the FASB argued that disclosure of

pension information may be a substitute for recognition only for sophisticated users, but not for

other users (SFAS No. 87, para. 116), suggesting that the impact of recognition of previously

disclosed pension information depends on the extent to which disclosed information has been

assimilated by various users.

This study is motivated by anecdotal evidence that institutional investors and financial analysts

attend to pension information disclosed in the footnotes and incorporate off-balance-sheet pension

liabilities disclosed under SFAS No. 87 into their decision-making process. For example, some

portfolio managers at Washington Trust Bank argued that SFAS No. 158 should not affect stock

valuation of firms with a high level of institutional ownership or analyst following because

off-balance-sheet pension liabilities had already been considered in the valuation analysis by

institutional investors and analysts.1 This anecdotal evidence suggests that the difference in value

relevance between disclosed and recognized pension liabilities may be conditional on institutional

ownership and analyst following. I examine whether institutional ownership and analyst following

affect the value relevance of off-balance-sheet pension liabilities under SFAS No. 87, and whether

the impact of SFAS No. 158 on the value relevance of previously disclosed pension liabilities

depends on institutional ownership and analyst following.

I find that, without considering the effects of institutional ownership and analyst following,

off-balance-sheet pension liabilities are not value relevant under SFAS No. 87, and SFAS No. 158

does not change the valuation coefficient on previously disclosed off-balance-sheet pension

liabilities. However, after taking into account institutional ownership and analyst following, I find

that the value relevance of off-balance-sheet pension liabilities under SFAS No. 87 depends on

institutional ownership and analyst following. Specifically, off-balance-sheet pension liabilities are

more value relevant for firms with a higher level of institutional ownership or analyst following.

More importantly, I find that SFAS No. 158 increases the value relevance of previously disclosed

off-balance-sheet pension liabilities for firms with a low level of institutional ownership or analyst

following, and that the increase in the value relevance becomes less pronounced for firms with a

higher level of institutional ownership or analyst following.

My results are robust to various specifications, and are not driven by other concurrent

regulation changes, such as the measurement date provision of SFAS No. 158 and the Pension

Protection Act of 2006. Additional analysis shows that for firms with a higher level of institutional

1 Washington Trust Bank (2006). In addition, PricewaterhouseCoopers states that ‘‘[w]e note that generally thefinancial analyst community currently uses the PBO and APBO measures when developing equity values anddetermining credit ratings’’ (Comment letter #87 to the exposure draft of SFAS No. 158). Moody’s ratingmethodology adjusts a company’s balance sheet by recording as a debt the unfunded status, measured as thedifference between the PBO and the fair value of pension assets, and removes all the pension assets andliabilities recognized under GAAP (Moody’s Investor Services 2006).

1096 Yu

The Accounting ReviewMay 2013

ownership or analyst following, the mispricing of the off-balance-sheet pension liabilities in the

pre-158 period is smaller and the decrease in the mispricing following SFAS No. 158 is less

pronounced, consistent with the view that off-balance-sheet pension liabilities are more likely to be

already reflected in stock prices for firms with a higher level of institutional ownership or analyst

following in the pre-158 period.

My paper contributes to the literature in the following ways. First, this study contributes to the

literature on recognition versus disclosure (e.g., Davis-Friday et al. 1999; Ahmed et al. 2006) by

suggesting that the difference in value relevance between disclosure and recognition depends on

institutional ownership and analyst following. This study highlights the importance and necessity of

considering institutional ownership and analyst following in the value-relevance research.

Researchers might draw incorrect inferences that recognition versus disclosure does not matter,

if they fail to take into account valuation differences between disclosure and recognition associated

with different levels of institutional ownership and analyst following.

Closely related to this study, Mitra and Hossain (2009; hereafter, MH) document a negative

association between stock returns and pension transition adjustments in the initial adoption year of

SFAS No. 158 (i.e., year 2006), which is inconsistent with my result that SFAS No. 158 does not

change the value relevance of previously disclosed off-balance-sheet pension liabilities without

considering institutional ownership and analyst following. Furthermore, they find that the negative

association is driven by large S&P 500 firms, suggesting that the impact of SFAS No. 158 on the

value relevance of off-balance-sheet pension liabilities depends on firm size.

I attribute these different findings to differences between the two samples, as well as

differences in the variable sets and the research methods. These differences are explored in the

‘‘Additional Analyses’’ section. My study examines the change in the value relevance of

off-balance-sheet pension liabilities following SFAS No. 158 from a perspective different from that

of the MH paper. In particular, this study documents differences in the valuation of

off-balance-sheet pension liabilities associated with institutional ownership and analyst following,

and these valuation differences cannot be explained by the size effect documented in the MH paper.

Second, this study also complements the literature on the market valuation of disclosed pension

information. Several earlier studies (Barth 1991; Gopalakrishnan 1994) suggest that investors treat

disclosed pension information similarly to recognized pension information. In contrast, more recent

studies (Franzoni and Marin 2006; Picconi 2006) suggest that investors may have difficulty in

understanding pension information disclosed in the footnotes, but not that recognized in the

financial statements. My study suggests that these contradictory findings may result from prior

literature’s failure to consider valuation differences across different levels of institutional ownership

and analyst following.

This study is subject to several caveats. First, although this study documents valuation

differences across different levels of institutional ownership and analyst following, my research

design cannot provide evidence on how institutional ownership and analyst following function to

affect information processing. Second, it is not clear from my results whether investors of firms

with a low level of institutional ownership or analyst following ignore disclosed pension

information or they notice the information but do not use it.2 These are interesting questions left for

future research.

Next, Section II reviews previous literature and describes the institutional background. Section

III outlines the research methodology. The sample is described in Section IV. Section V reports

2 Investors may not use disclosed pension information, either because they cannot understand it or because theyperceive it to be unreliable.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1097

The Accounting ReviewMay 2013

main empirical results and provides the explanations of the results. Additional analyses are

presented in Section VI. Section VII summarizes the paper and provides concluding remarks.

II. PRIOR RESEARCH AND INSTITUTIONAL BACKGROUND

Literature Review

Prior literature suggests two reasons for why users may treat disclosed and recognized

information differently. One stream of the literature suggests that recognized information is more

reliable than disclosed information (e.g., Davis-Friday et al. 2004; Libby et al. 2006). Davis-Friday

et al. (2004) find that the market perceives disclosed post-retirement benefits (PRB) liabilities as

less reliable than recognized PRB liabilities. Libby et al. (2006) find that auditors tolerate less

misstatement of recognized items than disclosed items. Frederickson et al. (2006) find that

mandatory income statement recognition of stock option expenses leads to higher user assessments

of reliability than either voluntary income statement recognition or voluntary footnote disclosure.

Another stream of the literature suggests that the differential treatment of disclosed versus

recognized information is due to information-processing-related factors (e.g., Barth et al. 2003;

Hirshleifer and Teoh 2003). In particular, users may treat disclosed and recognized items differently

because they lack competence to understand disclosure (e.g., Dearman and Shields 2005), pay

limited attention to disclosure (Hirshleifer and Teoh 2003), or are subject to cognitive biases

unrelated to user competence when processing disclosed information (e.g., Koonce et al. 2005;

Hobson and Kachelmeier 2005). Consistent with this view, experimental studies provide evidence

that users discount or ignore disclosed information, but not recognized information.3 For example,

users are more likely to understand information recognized in the income statement than

information presented more like a disclosure (disclosed in the statement of changes in stockholders’

equity) or disclosed in the footnotes (e.g., Maines and McDaniel 2000; Hirst and Hopkins 1998;

Hirst et al. 2004).

Pension Accounting under SFAS No. 87 and 158

In December 1985, FASB issued SFAS No. 87, Employers’ Accounting for Pensions. Under

SFAS No. 87, certain changes in pension liabilities and pension assets were not recognized as they

occurred, but recognized systematically and gradually in the following periods. These changes

include four items: (1) prior service costs, (2) unexpected return on pension assets, (3) actuarial

gains or losses, and (4) net transition assets or liabilities. Off-balance-sheet pension liabilities

disclosed under SFAS No. 87 are the sum of unrecognized prior service costs, unrecognized gains

or losses, and unrecognized net transition assets or liabilities. Net pension assets or liabilities

recognized on the balance sheet under SFAS No. 87 are the funded status of a pension plan adjusted

for off-balance-sheet pension liabilities.4

SFAS No. 158 requires a company to recognize its funded status as net pension assets or

liabilities on the balance sheet, and the previously disclosed off-balance-sheet pension liabilities

(i.e., the sum of unrecognized prior service costs, unrecognized gains or losses, and unrecognized

net transition assets or liabilities, pursuant to SFAS No. 87) as a component of other comprehensive

income (OCI). Since the funded status is the sum of the previously recognized accrued or prepaid

3 Although yielding rich insights into the differences between recognition and disclosure, experimental studiesgenerally focus on one group of experimental subjects, and the results may not generalize to the associationbetween stock prices and disclosed versus recognized items.

4 Under SFAS No. 87, for firms with underfunded accumulated benefit obligation (ABO), the firm had to recognize anadditional minimum liability, equal to the excess of underfunded ABO over the accrued or prepaid pension cost on thebalance sheet if (1) an asset had been recognized as the prepaid pension cost, or (2) the accrued pension cost was lessthan the underfunded ABO, or (3) no accrued or prepaid pension cost had been recognized.

1098 Yu

The Accounting ReviewMay 2013

pension cost and the previously disclosed off-balance-sheet pension liabilities, SFAS No. 158

essentially requires a company to recognize the previously disclosed pension liabilities aggregately

with the previously recognized pension liabilities on the balance sheet by an adjustment to OCI.5

SFAS No. 158 does not change the measurement of pension expenses recognized in the income

statement.

III. RESEARCH METHODOLOGY

Barth et al. (2001) suggest that a levels model should be used if researchers intend to

investigate what is reflected in firm value, while a changes model is appropriate if the timeliness of

accounting amounts is part of the research question. My study involves determining how SFAS No.

158 changes the way off-balance-sheet pension liabilities are reflected in firm value, suggesting that

a levels approach may be more appropriate for my research question. In addition, Kothari and

Zimmerman (1995) argue that although a levels model is more likely to have econometric

problems, such as omitted variables, when compared to a changes model, the levels model is

economically better specified.6 Consistent with prior pension research (Landsman 1986; Barth

1991; Barth et al. 1992; Hann et al. 2007a; Hann et al. 2007b), I use levels models in my main

analyses, and report the results based on changes models in the sensitivity analysis section. Table 1

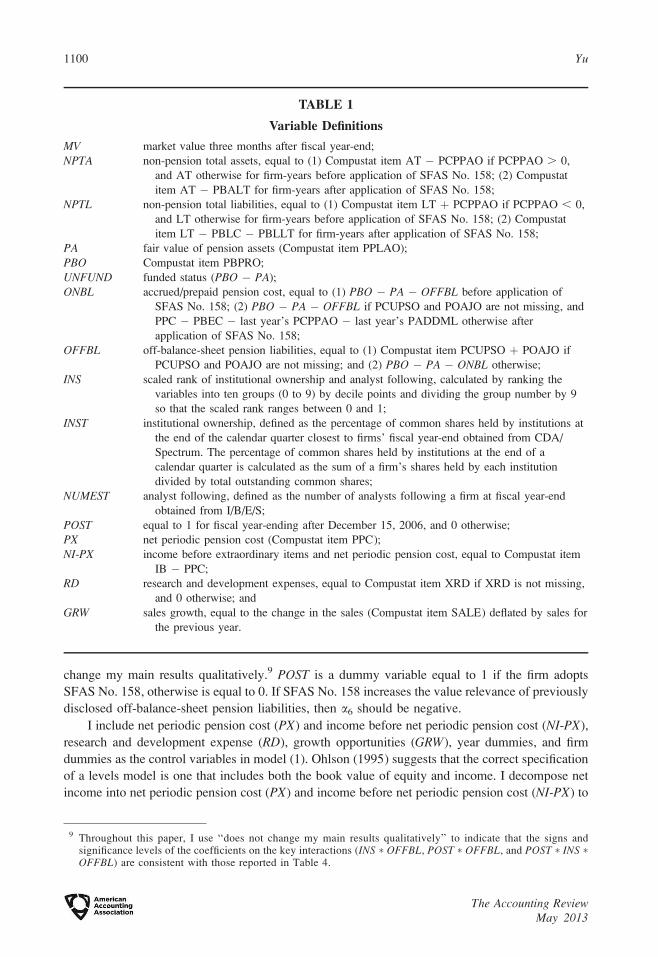

provides the detailed definition of the main variables used in my analysis.

Levels Model without Considering Institutional Ownership and Analyst Following

Consistent with Hann et al. (2007a) and Hann et al. (2007b), the following model is used to

examine whether SFAS No. 158 increases the value relevance of the previously disclosed off-

balance-sheet pension liabilities without considering institutional ownership and analyst following:7

MVit ¼ a0 þ a1POST þ a2NPTAit þ a3NPTLit þ a4ONBLit þ a5OFFBLit

þ a6POST�OFFBLit þ a7PX þ a8NI-PX þ a9RDþ a10GRW þ eit: ð1Þ

MVit is the market value of firm i three months after the fiscal year-end of year t (hereafter I drop the

subscripts), NPTA is non-pension total assets, and NPTL is non-pension total liabilities. ONBL is

accrued pension liabilities or prepaid pension assets defined by SFAS No. 87 in both pre-158 and

post-158 periods. OFFBL is the sum of unamortized prior service costs, unamortized gains or

losses, and unamortized net transition assets defined by SFAS No. 87 in both pre-158 and post-158

periods. OFFBL (ONBL) is coded as a positive number if it is a net liability, and as a negative

number if it is a net asset.8 Excluding the observations with net off-balance-sheet assets does not

5 I randomly select a sample of 100 firms with defined benefit pension plans, and find that only 22 (12) firms reportpension liabilities as a single item on the balance sheet in the pre-158 (post-158) period. This suggests that forthe majority of the firms, pension liabilities may be aggregated with other liability items and investors may notknow the exact amount of recognized pension liabilities without looking at the footnotes.

6 The variables of interest in this study are the interactions among POST, INS, and OFFBL. Nizalova andMurtazashvili (2011) suggest that although the main effect of OFFBL may be subject to the omitted variablebias, interactions terms are likely to be consistent if the endogenous factor (OFFBL) and the omitted variable arejointly independent of the treatment or policy variable (INS and POST).

7 I do not have any specific predictions regarding the theoretical values of the coefficients on assets and liabilitiesin the value relevance models. Barth (1994) argues that only if the accounting variables in the value relevancemodels equal the amounts implicit in stock prices and there are no omitted variables, the coefficients shouldequal 1. However, since the book value of assets and liabilities is unlikely to equal the market value of assets andliabilities, the coefficients on assets and liabilities in the models are unlikely to be 1.

8 For my levels sample, OFFBL is a net off-balance-sheet pension asset for 1,603 out of 7,887 observations, and ONBL isa net on-balance-sheet pension asset for 3,656 out of 7,887 observations. This coding method allows OFFBL (ONBL) tohave a negative valuation multiple in the value-relevance regression, regardless of whether it is a net asset or netliability. This treatment is also consistent with prior research (Hann et al. 2007a; Picconi 2006).

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1099

The Accounting ReviewMay 2013

change my main results qualitatively.9 POST is a dummy variable equal to 1 if the firm adopts

SFAS No. 158, otherwise is equal to 0. If SFAS No. 158 increases the value relevance of previously

disclosed off-balance-sheet pension liabilities, then a6 should be negative.

I include net periodic pension cost (PX) and income before net periodic pension cost (NI-PX),

research and development expense (RD), growth opportunities (GRW), year dummies, and firm

dummies as the control variables in model (1). Ohlson (1995) suggests that the correct specification

of a levels model is one that includes both the book value of equity and income. I decompose net

income into net periodic pension cost (PX) and income before net periodic pension cost (NI-PX) to

TABLE 1

Variable Definitions

MV market value three months after fiscal year-end;

NPTA non-pension total assets, equal to (1) Compustat item AT � PCPPAO if PCPPAO . 0,

and AT otherwise for firm-years before application of SFAS No. 158; (2) Compustat

item AT � PBALT for firm-years after application of SFAS No. 158;

NPTL non-pension total liabilities, equal to (1) Compustat item LT þ PCPPAO if PCPPAO , 0,

and LT otherwise for firm-years before application of SFAS No. 158; (2) Compustat

item LT � PBLC � PBLLT for firm-years after application of SFAS No. 158;

PA fair value of pension assets (Compustat item PPLAO);

PBO Compustat item PBPRO;

UNFUND funded status (PBO � PA);

ONBL accrued/prepaid pension cost, equal to (1) PBO � PA � OFFBL before application of

SFAS No. 158; (2) PBO � PA � OFFBL if PCUPSO and POAJO are not missing, and

PPC � PBEC � last year’s PCPPAO � last year’s PADDML otherwise after

application of SFAS No. 158;

OFFBL off-balance-sheet pension liabilities, equal to (1) Compustat item PCUPSO þ POAJO if

PCUPSO and POAJO are not missing; and (2) PBO � PA � ONBL otherwise;

INS scaled rank of institutional ownership and analyst following, calculated by ranking the

variables into ten groups (0 to 9) by decile points and dividing the group number by 9

so that the scaled rank ranges between 0 and 1;

INST institutional ownership, defined as the percentage of common shares held by institutions at

the end of the calendar quarter closest to firms’ fiscal year-end obtained from CDA/

Spectrum. The percentage of common shares held by institutions at the end of a

calendar quarter is calculated as the sum of a firm’s shares held by each institution

divided by total outstanding common shares;

NUMEST analyst following, defined as the number of analysts following a firm at fiscal year-end

obtained from I/B/E/S;

POST equal to 1 for fiscal year-ending after December 15, 2006, and 0 otherwise;

PX net periodic pension cost (Compustat item PPC);

NI-PX income before extraordinary items and net periodic pension cost, equal to Compustat item

IB � PPC;

RD research and development expenses, equal to Compustat item XRD if XRD is not missing,

and 0 otherwise; and

GRW sales growth, equal to the change in the sales (Compustat item SALE) deflated by sales for

the previous year.

9 Throughout this paper, I use ‘‘does not change my main results qualitatively’’ to indicate that the signs andsignificance levels of the coefficients on the key interactions (INS � OFFBL, POST � OFFBL, and POST � INS �OFFBL) are consistent with those reported in Table 4.

1100 Yu

The Accounting ReviewMay 2013

allow different valuation coefficients on pension and non-pension income. Consistent with Hann et

al. (2007a) and Hann et al. (2007b), I include RD to reduce the service cost anomaly first

documented by Barth et al. (1992)10 and GRW, measured by sales growth, to control for growth

opportunities not reflected in the financial statements.11 Year dummies and firm dummies are

included to control for fixed year effects and fixed firm effects, respectively. Following Hann et al.

(2007b), all the variables except POST and GRW are deflated by sales in the levels model.

To make sure that the results from model (1) are not driven by the omission of the interactions

between POST and the variables other than OFFBL, I expand model (1) by adding these

interactions and allowing the valuation coefficients on the variables other than OFFBL to vary

between pre- and post-158 periods:

MVit ¼ b0 þ b1POST þ b2NPTAit þ b3NPTLit þ b4ONBLit þ b5POST�ONBLþ b6OFFBLit

þ b7POST�OFFBLit þ b8PX þ b9POST�PX þ b10NI-PX þ b11RDþ b12GRWþ b13POST�NPTAþ b14POST�NPTL þ b15POST�NI-PX þ b16POST�RDþ b17POST�GRW þ eit:

ð2Þ

Levels Model Considering Institutional Ownership and Analyst Following

I use the following model to examine whether institutional ownership and analyst following

affect the value relevance of previously disclosed off-balance-sheet pension liabilities and whether

the difference in value relevance between recognition and disclosure depends on institutional

ownership and analyst following:

MVit ¼ h0 þ h1POST þ h2INSit þ h3NPTAit þ h4NPTLit þ h5ONBLit þ h6INS�ONBLþ h7POST�ONBL þ h8POST�INS�ONBLþ h9OFFBLit þ h10INSit�OFFBLit

þ h11POST�OFFBLit þ h12POST�INSit�OFFBLit þ h13PXit þ h14INSit�PXit

þ h15POST�PXit þ h16POST�INSit�PXit þ h17NI-PX þ h18RDþ h19GRWþ h20INS�NPTAþ h21POST�NPTA þ h22POST�INS�NPTAþ h23INS�NPTLþ h24POST�NPTLþ h25POST�INS�NPTLþ h26INS�NI-PX þ h27POST�NI-PXþ h28POST�INS�NI-PX þ h29INS�RDþ h30POST�RDþ h31POST�INS�RDþ h32INS�GRW þ h33POST�GRW þ h34POST�INS�GRW þ eit: ð3Þ

Following the prior literature (e.g., Bhushan 1994; Walther 1997; Collins et al. 2003), I use the

rank of institutional ownership or analyst following to facilitate the interpretation of the results and

to allow for a nonlinear association between institutional ownership (analyst following) and value

relevance. In particular, I calculate the scaled rank of institutional ownership or analyst following

for each firm by ranking these variables into ten groups (0 to 9) by decile points and dividing the

group number by 9, so that the scaled rank ranges between 0 and 1.12 INS is the scaled rank of

either institutional ownership (INST) or analysts following (NUMEST). NUMEST is defined as the

10 Hann et al. (2007a) and Hann et al. (2007b) also include number of employees (EMP) to control for the servicecost anomaly. Because both EMP and RD are used to control the same effect, I exclude EMP in my main analysesto avoid deleting firms simply because of missing values for number of employees. Including EMP and theinteractions among POST, INS, and EMP as additional control variables does not change my main resultsqualitatively.

11 Using the market-to-book ratio to measure growth opportunities does not change my main results qualitatively.12 The main effect of INS measures the association between MV and INS when other independent variables except

POST in model (3) are zero. The interpretation of this main effect is potentially misleading, because the otheraccounting variables are generally not zero in the sample.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1101

The Accounting ReviewMay 2013

number of analysts following a firm at the fiscal year-end.13 The other variables are as defined in

model (1). The interactions among POST, INS, and the non-pension variables, and fixed year and

firm effects are included but not reported.

The coefficients of interest are h9, h10, h11, and h12. h9 measures the value relevance of off-

balance-sheet pension liabilities for firms with the lowest INS rank (INS¼ 0) in the pre-158 period.

h10 measures the incremental effect of INS on the value relevance of off-balance-sheet pension

liabilities in the pre-158 period. h11 measures the change in the value relevance of off-balance-sheet

pension liabilities due to SFAS No. 158 for firms with the lowest INS rank. h12 measures the

incremental effect of INS on the change in the value relevance of off-balance-sheet pension

liabilities due to SFAS No. 158.

Because INS ranges between 0 and 1, the sum of the coefficients on OFFBL and INS � OFFBL(h9þ h10) represents the value relevance of OFFBL for firms with the highest INS rank (INS¼ 1) in

the pre-158 period, and the sum of the coefficients on POST � OFFBL and POST � INS � OFFBL(h11þ h12) represents the change in the value relevance of OFFBL due to SFAS No. 158 for firms

with the highest INS rank. If off-balance-sheet pension liabilities have been fully understood in the

pre-158 period for firms with the highest INS rank, then SFAS No. 158 should have no impact on

the value relevance of OFFBL for these firms. Therefore, the sum of the coefficients on OFFBL and

INS � OFFBL (h9þh10) should be negative, and the sum of the coefficients on POST � OFFBL and

POST � INS � OFFBL (h11 þ h12) should be zero.

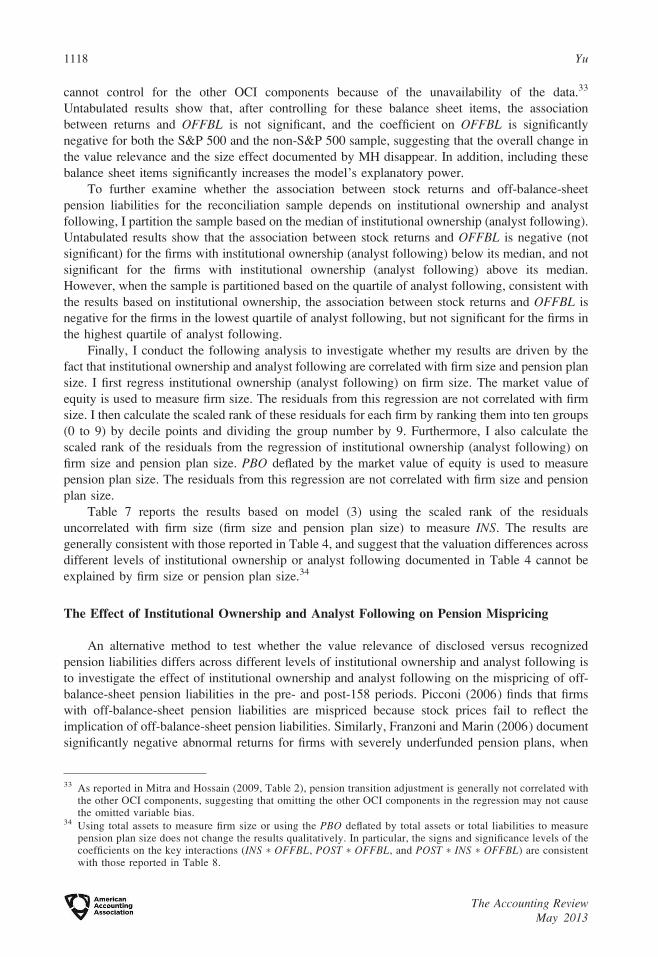

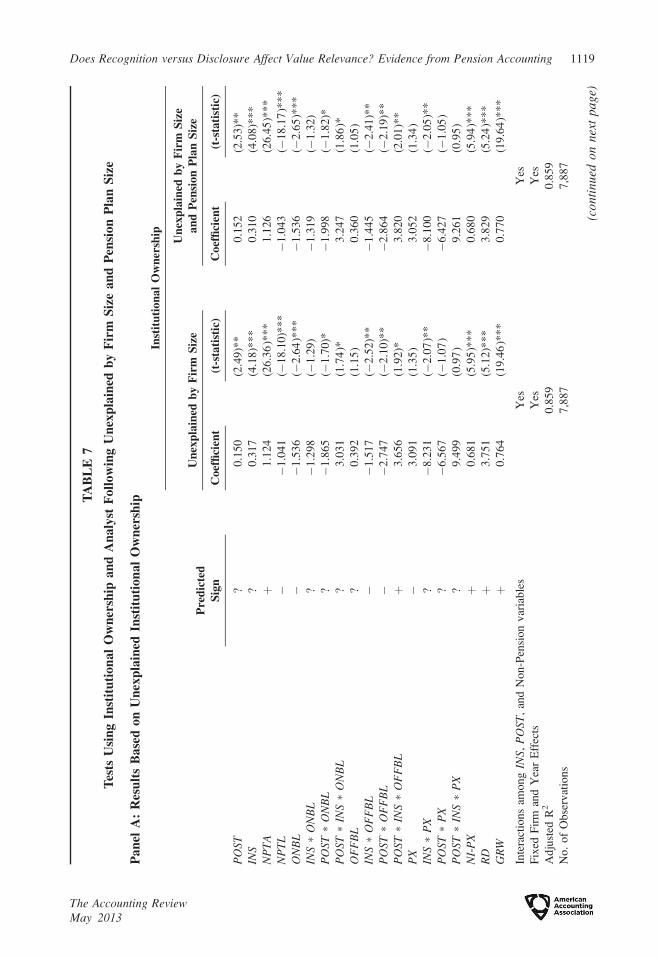

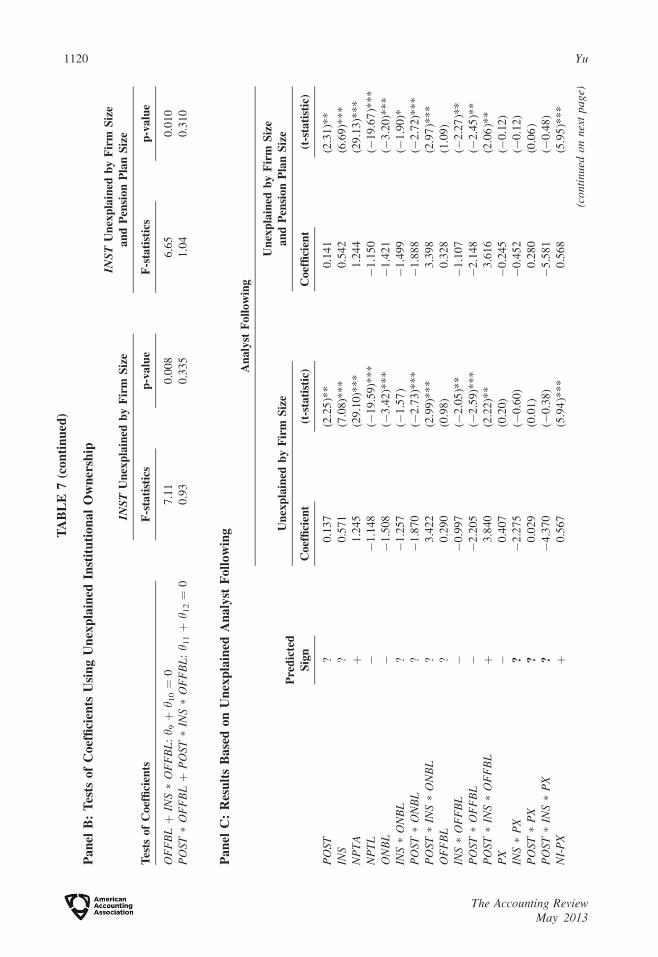

IV. SAMPLE SELECTION AND DESCRIPTIVE STATISTICS

My initial sample consists of all the firm-year observations from 1999 to 2007 in Compustat

Fundamentals Annual database. I select 1999 as the beginning fiscal year of the pre-SFAS No. 158

period to control for the possible effect of SFAS No. 132 on investors’ valuation of pension

liabilities.14 I then obtain pension information from the Compustat Pension database, institutional

ownership from CDA/Spectrum S34, analyst following from I/B/E/S, and stock prices three months

after fiscal year-end from CRSP. I delete all the observations with missing values needed for stock

prices. I eliminate foreign firms, firms not traded on NYSE, AMEX, and NASDAQ, and firms

without defined benefit pension plans. I also eliminate observations with missing values to calculate

independent variables. I only include firms with both pre- and post-158 data available so that the

same set of firms is compared between the pre- and post-158 periods. Finally, I delete all the

financial firms with two-digit SIC codes from 60 to 69.15 The final sample includes 7,887

observations with 991 unique firms.

Panel A of Table 2 shows descriptive statistics of the main variables. The Q1 of the unfunded

status is positive (Q1 of UNFUND¼ 0.3), suggesting that more than three quarters of the sample

firms are underfunded. In contrast, and interestingly, the median of on-balance-sheet pension

liabilities is negative (median of ONBL¼�0.7), suggesting that more than one half of the sample

firms recognize prepaid pension assets on their balance sheets. This finding supports the criticism of

13 Using the number of analysts, averaged across the fiscal year, following a firm to measure analyst following doesnot change my main results qualitatively.

14 SFAS No. 132 changed the disclosure requirements of defined benefit pension plans and was effective for thefiscal year beginning after Dec. 15, 1997. Fiscal year 1999 is the first year that all the firms adopted SFAS No.132.

15 I delete financial firms to be consistent with the prior literature (e.g., Davis-Friday et al. 1999; Picconi 2006).Davis-Friday et al. (1999) argue that the additional accounting regulation for financial firms may affect theassociation between stock prices and accounting items. However, including financial firms does not change anyof my inferences.

1102 Yu

The Accounting ReviewMay 2013

TA

BL

E2

Va

rio

us

Des

crip

tiv

eS

tati

stic

s

Pa

nel

A:

Des

crip

tiv

eS

tati

stic

s

Va

ria

ble

Mea

nM

inim

um

Q1

Med

ian

Q3

Ma

xim

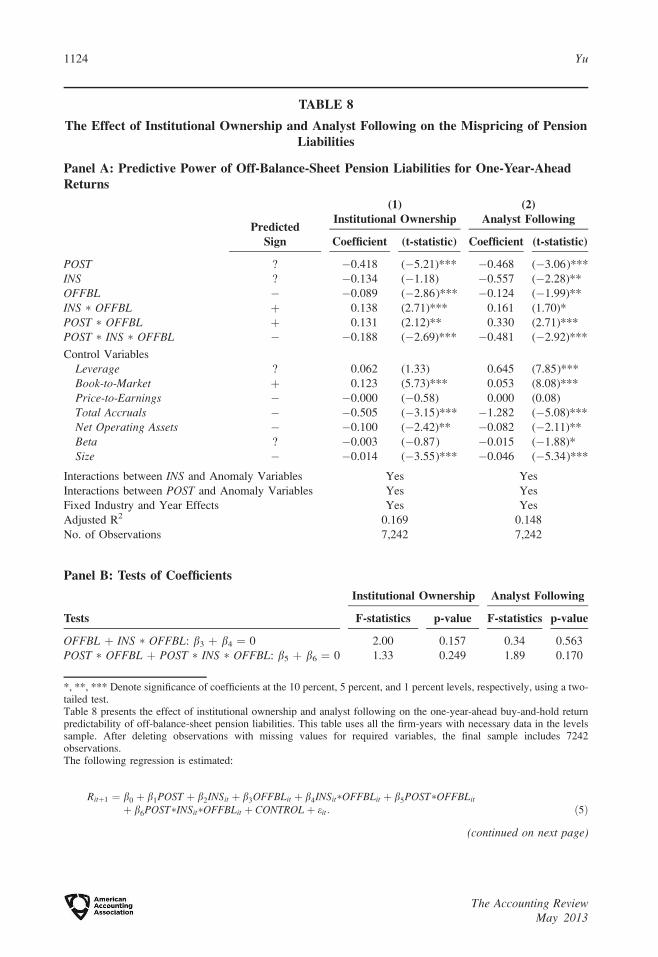

um

Std

.D

ev.

MV

75

00

.80

.13

62

.81

30

7.0

43

80

.65

11

20

3.7

25

53

9.5

NP

TA

78

91

.04

.45

29

.41

68

5.5

54

50

.07

74

88

9.0

29

76

8.9

NP

TL

54

68

.00

.92

85

.39

92

.23

57

7.2

66

64

76

.02

47

78

.2

PA

13

45

.80

.03

2.1

14

9.5

62

7.2

11

73

78

.05

86

6.7

PB

O1

41

0.7

0.1

41

.11

74

.36

89

.01

09

77

4.0

58

24

.5

UN

FU

ND

64

.9�

24

72

1.0

0.3

14

.27

2.5

25

44

0.0

10

92

.9

ON

BL

�1

62

.3�

36

57

8.0

�3

5.8

�0

.77

.98

94

0.0

13

32

.6

OF

FB

L2

27

.2�

17

54

6.0

0.6

14

.99

6.3

46

75

3.0

15

95

.5

INST

0.6

0.0

0.4

0.7

0.8

1.0

0.3

NU

ME

ST6

.90

.01

.05

.01

1.0

41

.06

.9

Pa

nel

B:

Mea

ns

of

the

Ma

inV

ari

ab

les

for

Ea

chF

isca

lY

ear

Fis

cal

Yea

rN

o.

of

Ob

s.M

VN

PT

AN

PT

LP

AP

BO

UN

FU

ND

ON

BL

OF

FB

LIN

ST

NU

ME

ST

19

99

76

47

11

1.9

59

24

.54

28

2.6

13

69

.21

08

4.8

�2

84

.46

6.6

�2

17

.80

.47

.1

20

00

78

77

18

3.9

68

16

.04

89

8.4

13

65

.61

14

4.2

�2

21

.41

10

.1�

11

1.3

0.5

6.6

20

01

80

77

37

3.8

75

96

.25

36

5.5

12

04

.21

22

4.6

20

.31

33

.31

53

.60

.56

.2

20

02

84

55

60

4.7

75

90

.45

57

8.3

10

41

.41

32

0.6

27

9.2

15

0.4

42

9.5

0.5

6.4

20

03

88

16

93

0.8

78

19

.85

63

9.3

12

11

.01

43

2.5

22

1.5

18

8.0

40

9.5

0.5

7.0

20

04

92

17

46

9.4

81

91

.35

71

9.5

13

01

.01

52

2.0

22

1.1

19

6.6

41

7.7

0.6

7.0

20

05

97

77

77

6.7

82

28

.55

67

8.8

13

51

.21

55

4.5

20

3.2

19

9.7

40

3.0

0.6

6.9

20

06

99

08

71

8.4

86

76

.85

56

8.2

15

07

.91

58

9.6

81

.71

92

.32

73

.90

.77

.3

20

07

91

58

92

9.6

95

50

.86

18

4.8

17

09

.01

67

9.1

�2

9.9

19

2.2

16

2.2

0.8

7.5

To

tal

7,8

87

(con

tinu

edo

nn

ext

pa

ge)

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1103

The Accounting ReviewMay 2013

TA

BL

E2

(co

nti

nu

ed)

Pan

elC

:P

ears

on

an

dS

pea

rman

Corr

elati

on

MV

NP

TA

NP

TL

PA

PB

OU

NF

UN

DO

NB

LO

FF

BL

INS

TN

UM

ES

T

MV

0.8

8*

**

0.8

1*

**

0.7

0*

**

0.7

2*

**

0.3

2*

**

�0

.23

**

*0

.43

**

*0

.32

**

*0

.74

**

*

NP

TA

0.7

2*

**

0.9

8*

**

0.8

0*

**

0.8

3*

**

0.3

7*

**

�0

.21

**

*0

.47

**

*0

.20

**

*0

.63

**

*

NP

TL

0.6

0*

**

0.9

7*

**

0.8

1*

**

0.8

4*

**

0.3

7*

**

�0

.22

**

*0

.47

**

*0

.16

**

*0

.58

**

*

PA

0.5

1*

**

0.7

2*

**

0.7

5*

**

0.9

9*

**

0.3

1*

**

�0

.39

**

*0

.51

**

*0

.12

**

*0

.45

**

*

PB

O0

.49

**

*0

.71

**

*0

.74

**

*0

.98

**

*0

.42

**

*�

0.3

3*

**

0.5

7*

**

0.1

5*

**

0.4

7*

**

UN

FU

ND

�0

.12

**

*�

0.0

7*

**

�0

.08

**

*�

0.1

3*

**

0.0

6*

**

0.1

9*

**

0.7

0*

**

0.2

0*

**

0.2

0*

**

ON

BL

�0

.34

**

*�

0.6

2*

**

�0

.68

**

*�

0.8

6*

**

�0

.84

**

*0

.15

**

*�

0.3

2*

**

0.0

0�

0.1

8*

**

OF

FB

L0

.20

**

*0

.47

**

*0

.51

**

*0

.63

**

*0

.74

**

*0

.56

**

*�

0.7

4*

**

0.2

1*

**

0.3

1*

**

INST

0.0

1�

0.0

1�

0.0

10

.01

0.0

10

.03

**

*�

0.0

20

.03

**

*0

.49

**

*

NU

ME

ST0

.42

**

*0

.28

**

*0

.22

**

*0

.26

**

*0

.26

**

*0

.02

*�

0.1

7*

**

0.1

5*

**

0.4

0*

**

***

Den

ote

signifi

cance

of

coef

fici

ents

atth

e1

per

cent

level

,usi

ng

atw

o-t

aile

dte

st.

The

sam

ple

incl

udes

7,8

87

obse

rvat

ions

wit

h991

firm

s.A

llth

evar

iable

sar

edefi

ned

inT

able

1.

Pan

elA

report

sth

edes

crip

tive

stat

isti

csfo

rth

em

ain

var

iable

s.A

llof

the

des

crip

tive

stat

isti

csar

ein

mil

lion

doll

ars,

exce

pt

those

for

INST

and

NU

ME

ST

.P

anel

Bre

port

sth

em

eans

of

the

mai

nvar

iable

sfo

rea

chfi

scal

yea

rin

the

sam

ple

.P

anel

Cre

port

sco

rrel

atio

nco

effi

cien

tsof

the

mai

nvar

iable

s.T

he

upper

and

low

erdia

gonal

ssh

ow

the

Spea

rman

and

Pea

rson

corr

elat

ions,

resp

ecti

vel

y.

1104 Yu

The Accounting ReviewMay 2013

pension accounting under SFAS No. 87 that a net pension asset could be reported on the balance

sheet for an underfunded defined benefit pension plan.

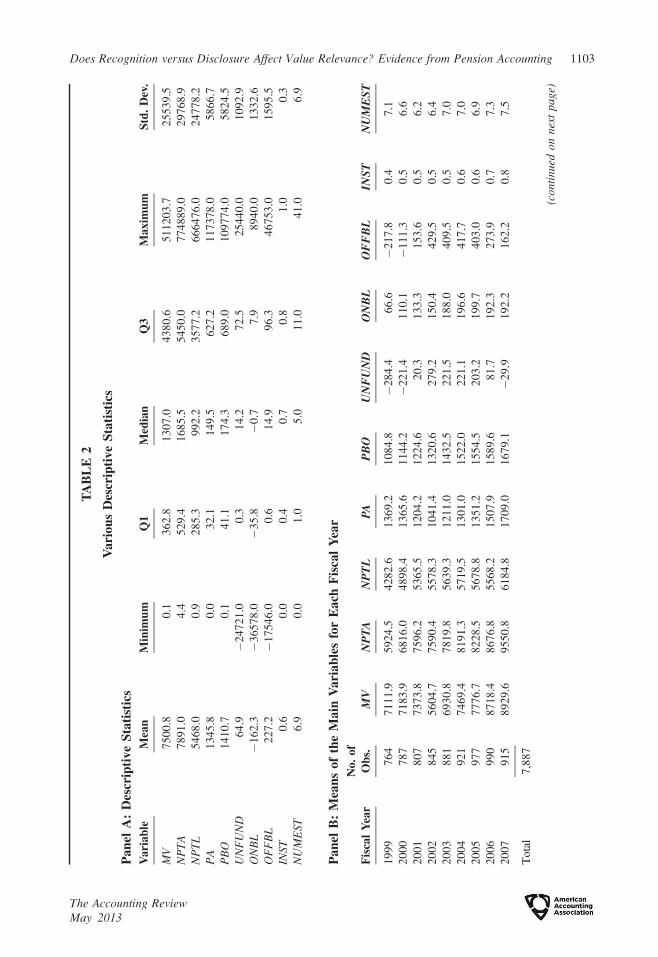

Panel B of Table 2 shows the means of the main variables for each fiscal year. There was a

sharp decrease in the mean of the market value of equity in 2002, due to the stock market downturn

of 2002. While the mean fair value of pension assets reached the lowest point in 2002 during the

nine-year sample period, the mean value of the PBO has been increasing from year to year.

Consequently, the mean unfunded status is the largest in 2002. Interestingly, the unfunded status

improved significantly in 2006 and 2007, and the mean fair value of pension assets exceeded the

mean PBO in fiscal year 2007, likely due to the accelerated funding requirement of the Pension

Protection Act of 2006 and the recognition requirement of SFAS No. 158.

Panel C of Table 2 reports the correlation coefficients of the main variables. Spearman

(Pearson) correlations are shown above (below) the diagonal. The market value of equity (MV) is

positively correlated with NPTL and OFFBL, suggesting the existence of the scale effect and the

importance of controlling for other accounting items. Davis-Friday et al. (1999) document a similar

result that the market value is positively correlated with various liability variables, and attribute the

result to the failure to control for the other variables, especially the book value of assets, when

calculating the individual correlations with the market value. Furthermore, institutional ownership

and analyst following are positively correlated (Pearson correlation ¼ 0.40 and Spearman

correlation ¼ 0.49), consistent with O’Brien and Bhushan’s (1990) argument that analysts are

motivated to follow firms with higher institutional ownership because of the information demand by

institutions, and institutional investors are attracted to invest in firms with more analysts because of

the marketing of the brokerage service.

The Pearson correlations between INS (INST or NUMEST) and the other variables except

ONBL are generally smaller or insignificant compared to the corresponding Spearman correlations.

Pearson correlations assume that the relation between two variables is linear, while Spearman

correlations accommodate a nonlinear relation. The difference between the Pearson and Spearman

correlations between MV and INS suggests that the relation between MV and INS may not be linear

and thus using the rank of INS may be more appropriate for my analysis.16 Furthermore, the

positive correlation between institutional ownership (analyst following) and MV or PBO suggests

that it is important to rule out the alternative explanation of the value relevance of recognition

versus disclosure depending on firm size or pension plan size. This issue is examined in the

‘‘Additional Analyses’’ section.

V. EMPIRICAL RESULTS

Main Results

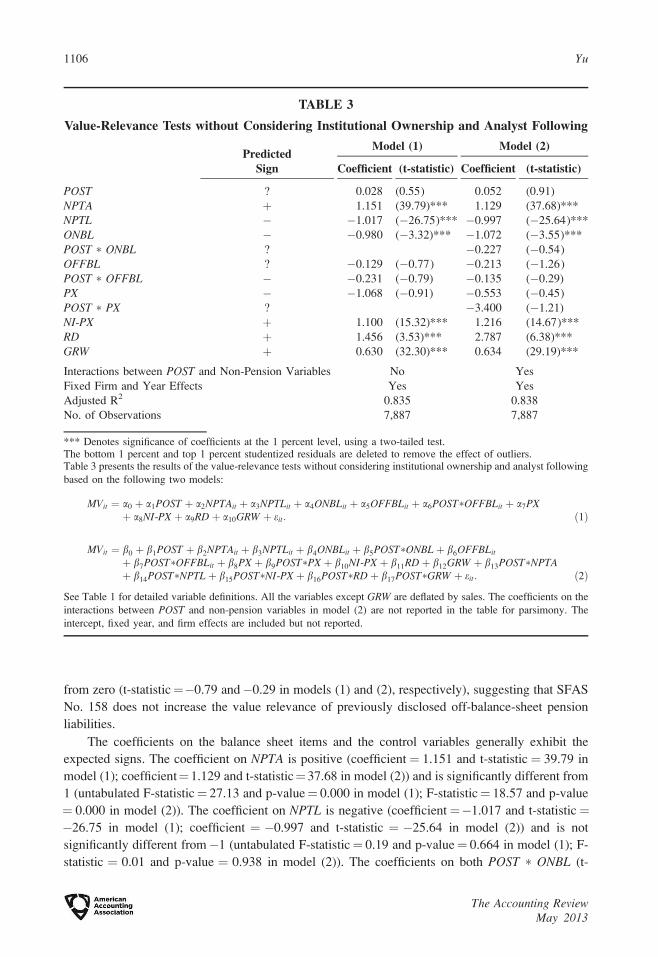

Table 3 presents the results of the value-relevance tests without considering institutional

ownership and analyst following. Panel A of Table 3 reports the estimation results based on models

(1) and (2). The coefficient on OFFBL is not significant (t-statistic¼�0.77 and�1.26 in models (1)

and (2), respectively), suggesting that investors appear to ignore off-balance-sheet pension

liabilities disclosed in the footnotes. The coefficient on POST � OFFBL is not significantly different

16 Prior research either uses a log transformation of the market value (e.g., Gompers and Metrick 2001) or convertsINS into ranks (e.g., Ayers and Freeman 2003) to address the nonlinear effect of INS on the market value or othervariables. Consistent with prior research, the natural logarithm of MV is positively correlated with bothinstitutional ownership (Pearson correlation ¼ 0.35 and Spearman correlation ¼ 0.32) and analyst following(Pearson correlation¼ 0.72 and Spearman correlation¼0.74) at the 0.01 significance level for my sample. Usingthe log transformation of MV results in the Pearson correlations similar to the Spearman correlations, and doesnot change the Spearman correlation between the market value and INS.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1105

The Accounting ReviewMay 2013

from zero (t-statistic¼�0.79 and�0.29 in models (1) and (2), respectively), suggesting that SFAS

No. 158 does not increase the value relevance of previously disclosed off-balance-sheet pension

liabilities.

The coefficients on the balance sheet items and the control variables generally exhibit the

expected signs. The coefficient on NPTA is positive (coefficient¼ 1.151 and t-statistic ¼ 39.79 in

model (1); coefficient¼1.129 and t-statistic¼37.68 in model (2)) and is significantly different from

1 (untabulated F-statistic¼ 27.13 and p-value¼ 0.000 in model (1); F-statistic¼ 18.57 and p-value

¼ 0.000 in model (2)). The coefficient on NPTL is negative (coefficient¼�1.017 and t-statistic¼�26.75 in model (1); coefficient ¼ �0.997 and t-statistic ¼ �25.64 in model (2)) and is not

significantly different from�1 (untabulated F-statistic¼ 0.19 and p-value¼ 0.664 in model (1); F-

statistic ¼ 0.01 and p-value ¼ 0.938 in model (2)). The coefficients on both POST � ONBL (t-

TABLE 3

Value-Relevance Tests without Considering Institutional Ownership and Analyst Following

PredictedSign

Model (1) Model (2)

Coefficient (t-statistic) Coefficient (t-statistic)

POST ? 0.028 (0.55) 0.052 (0.91)

NPTA þ 1.151 (39.79)*** 1.129 (37.68)***

NPTL � �1.017 (�26.75)*** �0.997 (�25.64)***

ONBL � �0.980 (�3.32)*** �1.072 (�3.55)***

POST � ONBL ? �0.227 (�0.54)

OFFBL ? �0.129 (�0.77) �0.213 (�1.26)

POST � OFFBL � �0.231 (�0.79) �0.135 (�0.29)

PX � �1.068 (�0.91) �0.553 (�0.45)

POST � PX ? �3.400 (�1.21)

NI-PX þ 1.100 (15.32)*** 1.216 (14.67)***

RD þ 1.456 (3.53)*** 2.787 (6.38)***

GRW þ 0.630 (32.30)*** 0.634 (29.19)***

Interactions between POST and Non-Pension Variables No Yes

Fixed Firm and Year Effects Yes Yes

Adjusted R2 0.835 0.838

No. of Observations 7,887 7,887

*** Denotes significance of coefficients at the 1 percent level, using a two-tailed test.The bottom 1 percent and top 1 percent studentized residuals are deleted to remove the effect of outliers.Table 3 presents the results of the value-relevance tests without considering institutional ownership and analyst following

based on the following two models:

MVit ¼ a0 þ a1POST þ a2NPTAit þ a3NPTLit þ a4ONBLit þ a5OFFBLit þ a6POST�OFFBLit þ a7PXþ a8NI-PX þ a9RDþ a10GRW þ eit: ð1Þ

MVit ¼ b0 þ b1POST þ b2NPTAit þ b3NPTLit þ b4ONBLit þ b5POST�ONBLþ b6OFFBLit

þ b7POST�OFFBLit þ b8PX þ b9POST�PX þ b10NI-PX þ b11RDþ b12GRW þ b13POST�NPTAþ b14POST�NPTLþ b15POST�NI-PX þ b16POST�RDþ b17POST�GRW þ eit: ð2Þ

See Table 1 for detailed variable definitions. All the variables except GRW are deflated by sales. The coefficients on the

interactions between POST and non-pension variables in model (2) are not reported in the table for parsimony. The

intercept, fixed year, and firm effects are included but not reported.

1106 Yu

The Accounting ReviewMay 2013

statistic¼�0.54) and POST � PX (t-statistic¼�1.21) are not significant, suggesting that SFAS No.

158 does not change the value relevance of previously recognized pension amounts on average. In

addition, the coefficients on NI-PX, RD, and GRW are significantly positive, suggesting the

importance of controlling for these variables.

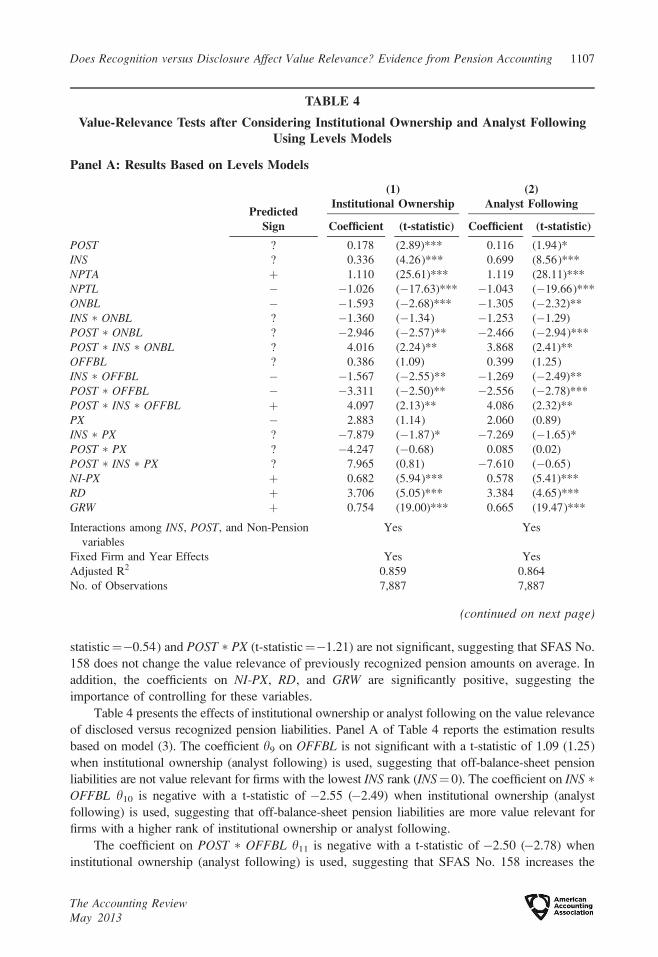

Table 4 presents the effects of institutional ownership or analyst following on the value relevance

of disclosed versus recognized pension liabilities. Panel A of Table 4 reports the estimation results

based on model (3). The coefficient h9 on OFFBL is not significant with a t-statistic of 1.09 (1.25)

when institutional ownership (analyst following) is used, suggesting that off-balance-sheet pension

liabilities are not value relevant for firms with the lowest INS rank (INS¼ 0). The coefficient on INS �OFFBL h10 is negative with a t-statistic of �2.55 (�2.49) when institutional ownership (analyst

following) is used, suggesting that off-balance-sheet pension liabilities are more value relevant for

firms with a higher rank of institutional ownership or analyst following.

The coefficient on POST � OFFBL h11 is negative with a t-statistic of �2.50 (�2.78) when

institutional ownership (analyst following) is used, suggesting that SFAS No. 158 increases the

TABLE 4

Value-Relevance Tests after Considering Institutional Ownership and Analyst FollowingUsing Levels Models

Panel A: Results Based on Levels Models

PredictedSign

(1)Institutional Ownership

(2)Analyst Following

Coefficient (t-statistic) Coefficient (t-statistic)

POST ? 0.178 (2.89)*** 0.116 (1.94)*

INS ? 0.336 (4.26)*** 0.699 (8.56)***

NPTA þ 1.110 (25.61)*** 1.119 (28.11)***

NPTL � �1.026 (�17.63)*** �1.043 (�19.66)***

ONBL � �1.593 (�2.68)*** �1.305 (�2.32)**

INS � ONBL ? �1.360 (�1.34) �1.253 (�1.29)

POST � ONBL ? �2.946 (�2.57)** �2.466 (�2.94)***

POST � INS � ONBL ? 4.016 (2.24)** 3.868 (2.41)**

OFFBL ? 0.386 (1.09) 0.399 (1.25)

INS � OFFBL � �1.567 (�2.55)** �1.269 (�2.49)**

POST � OFFBL � �3.311 (�2.50)** �2.556 (�2.78)***

POST � INS � OFFBL þ 4.097 (2.13)** 4.086 (2.32)**

PX � 2.883 (1.14) 2.060 (0.89)

INS � PX ? �7.879 (�1.87)* �7.269 (�1.65)*

POST � PX ? �4.247 (�0.68) 0.085 (0.02)

POST � INS � PX ? 7.965 (0.81) �7.610 (�0.65)

NI-PX þ 0.682 (5.94)*** 0.578 (5.41)***

RD þ 3.706 (5.05)*** 3.384 (4.65)***

GRW þ 0.754 (19.00)*** 0.665 (19.47)***

Interactions among INS, POST, and Non-Pension

variables

Yes Yes

Fixed Firm and Year Effects Yes Yes

Adjusted R2 0.859 0.864

No. of Observations 7,887 7,887

(continued on next page)

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1107

The Accounting ReviewMay 2013

value relevance of previously disclosed off-balance-sheet pension liabilities for firms with the

lowest INS rank. The coefficient on POST � INS � OFFBL h12 is positive with a t-statistic of 2.13

(2.32) when institutional ownership (analyst following) is used, suggesting that the increase in the

value relevance of off-balance-sheet pension liabilities due to SFAS No. 158 is less pronounced for

firms with a higher level of institutional ownership or analyst following.

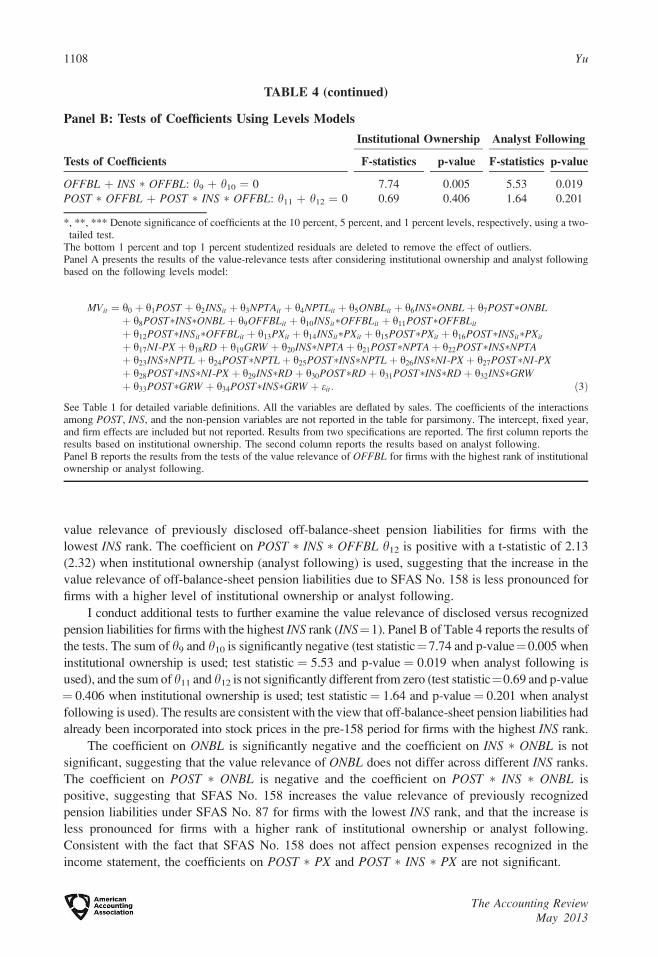

I conduct additional tests to further examine the value relevance of disclosed versus recognized

pension liabilities for firms with the highest INS rank (INS¼1). Panel B of Table 4 reports the results of

the tests. The sum of h9 and h10 is significantly negative (test statistic¼7.74 and p-value¼0.005 when

institutional ownership is used; test statistic ¼ 5.53 and p-value ¼ 0.019 when analyst following is

used), and the sum of h11 and h12 is not significantly different from zero (test statistic¼0.69 and p-value

¼ 0.406 when institutional ownership is used; test statistic¼ 1.64 and p-value¼ 0.201 when analyst

following is used). The results are consistent with the view that off-balance-sheet pension liabilities had

already been incorporated into stock prices in the pre-158 period for firms with the highest INS rank.

The coefficient on ONBL is significantly negative and the coefficient on INS � ONBL is not

significant, suggesting that the value relevance of ONBL does not differ across different INS ranks.

The coefficient on POST � ONBL is negative and the coefficient on POST � INS � ONBL is

positive, suggesting that SFAS No. 158 increases the value relevance of previously recognized

pension liabilities under SFAS No. 87 for firms with the lowest INS rank, and that the increase is

less pronounced for firms with a higher rank of institutional ownership or analyst following.

Consistent with the fact that SFAS No. 158 does not affect pension expenses recognized in the

income statement, the coefficients on POST � PX and POST � INS � PX are not significant.

TABLE 4 (continued)

Panel B: Tests of Coefficients Using Levels Models

Tests of Coefficients

Institutional Ownership Analyst Following

F-statistics p-value F-statistics p-value

OFFBL þ INS � OFFBL: h9 þ h10 ¼ 0 7.74 0.005 5.53 0.019

POST � OFFBL þ POST � INS � OFFBL: h11 þ h12 ¼ 0 0.69 0.406 1.64 0.201

*, **, *** Denote significance of coefficients at the 10 percent, 5 percent, and 1 percent levels, respectively, using a two-tailed test.

The bottom 1 percent and top 1 percent studentized residuals are deleted to remove the effect of outliers.Panel A presents the results of the value-relevance tests after considering institutional ownership and analyst followingbased on the following levels model:

MVit ¼ h0 þ h1POST þ h2INSit þ h3NPTAit þ h4NPTLit þ h5ONBLit þ h6INS�ONBLþ h7POST�ONBLþ h8POST�INS�ONBLþ h9OFFBLit þ h10INSit�OFFBLit þ h11POST�OFFBLit

þ h12POST�INSit�OFFBLit þ h13PXit þ h14INSit�PXit þ h15POST�PXit þ h16POST�INSit�PXit

þ h17NI-PX þ h18RDþ h19GRW þ h20INS�NPTAþ h21POST�NPTAþ h22POST�INS�NPTAþ h23INS�NPTLþ h24POST�NPTLþ h25POST�INS�NPTLþ h26INS�NI-PX þ h27POST�NI-PXþ h28POST�INS�NI-PX þ h29INS�RDþ h30POST�RDþ h31POST�INS�RDþ h32INS�GRWþ h33POST�GRW þ h34POST�INS�GRW þ eit: ð3Þ

See Table 1 for detailed variable definitions. All the variables are deflated by sales. The coefficients of the interactionsamong POST, INS, and the non-pension variables are not reported in the table for parsimony. The intercept, fixed year,and firm effects are included but not reported. Results from two specifications are reported. The first column reports theresults based on institutional ownership. The second column reports the results based on analyst following.Panel B reports the results from the tests of the value relevance of OFFBL for firms with the highest rank of institutionalownership or analyst following.

1108 Yu

The Accounting ReviewMay 2013

Interpretation of the Results

My results are subject to several alternative interpretations. If institutional ownership and

analyst following are indicative of investor sophistication17 (e.g., O’Brien 1988; Walther 1997;

Barth et al. 2003) or firms’ information environment18 (see Beyer et al. [2010] for a review), the

results in Table 4 suggest that stock prices of firms with higher investor sophistication or better

information environment are more likely to reflect disclosed pension liabilities, and are less likely to

be affected by the subsequent recognition of off-balance-sheet pension liabilities. This

interpretation is also consistent with the view that unsophisticated investors have difficulty in

understanding disclosed off-balance-sheet pension liabilities because they lack expertise or pay

limited attention to disclosed information (e.g., Barth et al. 2003; Hirshleifer and Teoh 2003).19

Specifically, the insignificant coefficient on OFFBL suggests that for firms with low investor

sophistication or poor information environment, stock prices do not reflect off-balance-sheet pension

liabilities. The negative coefficient on INS � OFFBL suggests that for firms with higher investor

sophistication or better information environment, stock prices are more likely to incorporate disclosed

pension liabilities. The positive coefficient on POST � INS � OFFBL suggests that recognition of

previously disclosed pension information has a less pronounced impact on the value relevance of

OFFBL for firms with higher investor sophistication or better information environment.

Furthermore, if institutional ownership and analyst following are proxies for investor

sophistication, the negative coefficients on POST � ONBL and POST � OFFBL and the positive

coefficients on POST � INS � ONBL and POST � INS � OFFBL are consistent with Barth et al.’s

(2003) analytical results. Barth et al. (2003) suggest that SFAS No. 158 may change the value

relevance of both the previously recognized item (ONBL) and the previously disclosed item

(OFFBL), and the magnitudes of the changes in the value relevance of ONBL and OFFBL are

negatively associated with investor sophistication.20

Another possible explanation of the results is that the increase in the reliability of off-balance-

sheet pension liabilities due to SFAS No. 158 is larger for firms with lower institutional ownership

or analyst following. While I cannot rule out this alternative explanation, it is not clear why SFAS

No. 158 should increase the reliability of off-balance-sheet pension liabilities significantly and why

this increase differs across different levels of institutional ownership and analyst following.

17 Prior literature suggests that institutional investors and analysts have an advantage in gathering and processinginformation (e.g., Bartov et al. 2000; Ayers and Freeman 2003) and have stronger motivation to build theirexpertise (e.g., Bonner et al. 2003; Callen et al. 2005).

18 The information environment includes the effects of corporate reporting, private information acquisition, andinformation dissemination (Lang et al. 2003). Prior literature suggests that institutional investors and analystsmay increase information efficiency and reduce information asymmetry by acquiring private information (e.g.,El-Gazzar 1998; Balsam et al. 2002; Frankel and Li 2004) and increasing information dissemination (e.g., Honget al. 2000; D’Souza et al. 2010).

19 Several studies suggest that even analysts may not understand information that is not presented directly on thebalance sheet (e.g., Hirst et al. 2004; Picconi 2006). Although contrary to the notion that analyst following isindicative of investor sophistication, this effect should operate against my finding valuation differences acrossdifferent levels of analyst following.

20 Barth et al. (2003) suggest that following SFAS No. 158, the valuation coefficients on ONBL and OFFBL changes

by k1(1� u) and k2(1� u), respectively. k1 ¼r2

y2

r2y1þr2

y2

A1 � A2ð Þ and k2 ¼r2

y1

r2y1þr2

y2

A1 � A2ð Þ þ A2: A1 and A2 are the

coefficients on ONBL and OFFBL, respectively, in the regression of the firm’s terminal value on ONBL andOFFBL. r2

y1and r2

y2are the variances of ONBL and OFFBL respectively. u ranges from 0 to 1, and is

monotonically increasing in investor sophistication. See Barth et al. (2003, Table 3) for details. The magnitudes

of the changes in the value relevance of ONBL and OFFBL are negatively associated with u and investor

sophistication.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1109

The Accounting ReviewMay 2013

Off-balance-sheet pension liabilities possess a unique feature different from other disclosed

items. That is, in the pre-158 period, net pension liabilities are divided into on-balance-sheet

pension liabilities and off-balance-sheet pension liabilities, and the same set of pension assumptions

determines both disclosed and recognized pension amounts.21 Therefore, the reliability of off-

balance-sheet pension liabilities should be similar to that of recognized pension information in both

the pre-158 and post-158 periods.22 In addition, the extensive pension disclosure requirements

under SFAS No. 132 and 132R, such as the reconciliation of the funded status with the amount

recognized, also help decrease the misstatements of off-balance-sheet pension liabilities in the pre-

158 period.23 More importantly, if SFAS No. 158 increases the reliability of OFFBL for all the

firms, then we should observe a significant negative coefficient on POST � OFFBL. The

insignificant coefficient on POST � OFFBL reported in Table 3 suggests that the increase in the

reliability of OFFBL due to SFAS No. 158, if any, is likely to be small.

However, SFAS No. 158 may increase the perceived reliability of off-balance-sheet pension

liabilities, even if the actual reliability remains the same between the pre-158 and post-158 periods.

Frederickson et al. (2006) find that users perceive stock option expenses to be more reliable when

these expenses are moved from footnotes to the income statement with no change in specific inputs,

suggesting that recognition of previously disclosed items may increase user assessments of

reliability, even if the underlying assumptions remain unchanged. Thus, the increase in perceived

reliability due to SFAS No. 158 might, in part, account for the increase in the value relevance of

off-balance-sheet pension liabilities following SFAS No. 158.

VI. ADDITIONAL ANALYSES

Sensitivity Analysis

I perform the following sensitivity tests. First, the results reported in Table 4 may be driven by

the extreme deciles. Thus, I repeat my analysis using the rank based on the tertiles and quintiles of

institutional ownership or analyst following. The untabulated results are qualitatively similar to

those reported in Table 4,24 suggesting that my main findings are unlikely to be driven by extreme

values of institutional ownership or analyst following.

Second, prior literature argues that the results of value-relevance research may be sensitive to

the choice of deflators. I consider the book value of equity and the number of shares outstanding as

alternative deflators in levels models. The book value of equity is affected by certain pension

liabilities through accumulated OCI and pension expenses through retained earnings. Similarly, the

number of shares outstanding affects institutional ownership by definition (i.e., the number of

shares held by institutions divided by the number of shares outstanding). Therefore, the book value

21 This feature does not apply to the setting of SFAS No. 123 or 123R, because stock-based compensation expensewas not divided into a recognized component and a disclosed component in the pre-123 (123R) period.

22 This argument appears to contradict the findings in Libby et al. (2006) that auditors tolerate less misstatements ofrecognized items than disclosed items. I argue that Libby et al.’s (2006) argument is less likely to apply to off-balance-sheet pension liabilities because of the unique feature of off-balance-sheet pension liabilities as well asthe extensive pension disclosure requirements under SFAS No. 132 and 132R.

23 The FASB also expressed a similar view regarding the reliability of disclosed pension liabilities, whenresponding to the concern that ABO or PBO cannot be measured with sufficient reliability. The board argued thatthe measurements of recognized pension items, such as net periodic pension cost or on-balance-sheet pensionliabilities, are no more or less precise than measurements of disclosed pension liabilities, such as ABO or PBO,because they are based on the same assumptions (SFAS No. 87, para. 146).

24 Specifically, when the quintiles (tertiles) of institutional ownership are used, h10 is negative with a p-value of0.046 (0.021), h11 is negative with a p-value of 0.007 (0.008), and h12 is positive with a p-value of 0.020 (0.021).When the quintiles (tertiles) of analyst following are used, h10 is negative with a p-value of 0.009 (0.016), h11 isnegative with a p-value of 0.005 (0.008), and h12 is positive with a p-value of 0.013 (0.012).

1110 Yu

The Accounting ReviewMay 2013

of equity and the number of shares may not be appropriate deflators in models featuring pension

items and institutional ownership as the variables of interest.25 Nevertheless, I repeat my analysis

using the book value of equity and the number of shares outstanding as the deflators. The

untabulated results are qualitatively similar to those reported in Table 4.26

Third, one of the two years in the post-158 period for my sample is the transition year. To

examine whether my results are sensitive to the issue of the transition year, I conduct the value-

relevance tests for two subsamples. The first subsample excludes from the full sample the

observations in year 2007 and the observations in year 2006 if 2006 is not the transition year. The

second subsample excludes the observations in the transition year. Results based on both

subsamples are similar to those reported in Table 4,27 suggesting that my results are due to both the

transition year and the other year in the post-158 period.

Fourth, in addition to requiring an employer to recognize the unfunded status on the balance

sheet, SFAS No. 158 also requires the employer to measure pension assets and benefit obligations

as of the date of the fiscal year-end. Previously, a company was allowed to measure its plan assets

and benefit obligations as of a date no more than three months before the fiscal year-end. To

investigate whether my results are driven by the change in measurement dates, I repeat my analyses

based on a sample of firms without changes in measurement dates. The signs and significance levels

of the coefficients on the key interactions (INS � OFFBL, POST � OFFBL, and POST � INS �OFFBL) are consistent with those reported in Table 4, except that when institutional ownership is

used, h10 is significantly negative at the 0.01 level instead of the 0.05 level as reported in Table 4.

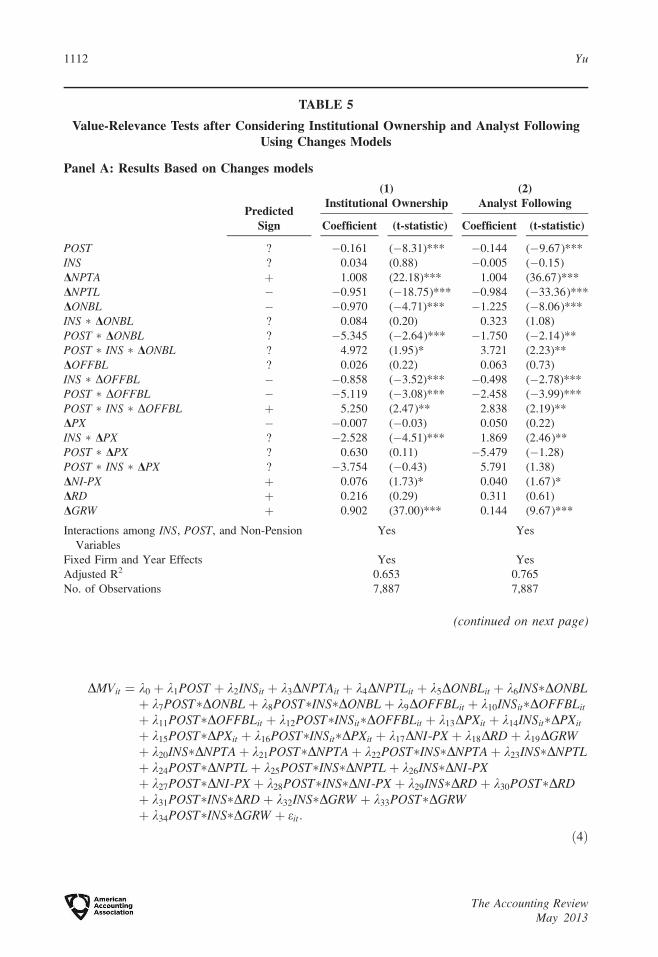

Finally, I repeat my main analyses using the changes model. The changes sample is formed by

taking all the firms in the levels sample, and deleting the firm-years that lack data to calculate

changes in relevant variables in both the pre-158 and the post-158 periods. The changes sample has

4,570 observations with 713 unique firms.28 Table 5 presents the results based on the following

changes model:

25 Furthermore, the Spearman correlation between the market value deflated by sales (the number of sharesoutstanding) and institutional ownership is 0.14 (0.31) and the Spearman correlation between the market valuedeflated by sales (the number of shares outstanding) and OFFBL is 0.07 (0.17), suggesting that using sales as thedeflator may reduce the size effect more than using the number of shares outstanding.

26 Specifically, when institutional ownership (analyst following) is used, h10 is negative with a p-value of 0.002(0.000), h11 is negative with a p-value of 0.001 (0.023), and h12 is positive with a p-value of 0.000 (0.000). Wheninstitutional ownership (analyst following) is used, h10 is negative with a p-value of 0.090 (0.022), h11 is negativewith a p-value of 0.000 (0.011), and h12 is positive with a p-value of 0.000 (0.081).

27 In particular, for the first subsample, regardless of whether institutional ownership or analyst following is used,h10, h11 and h12 carry signs consistent with those reported in Table 4 and are all significant at the 0.05 level; forthe second subsample, when institutional ownership (analyst following) is used, h10 is negative with a p-value of0.054 (0.010), h11 is negative with a p-value of 0.026 (0.065), and h12 is positive with a p-value of 0.023 (0.050).

28 Untabulated results show that firms in the changes sample generally have larger market capitalization, largerNPTA and NPTL, and larger on-balance-sheet and off-balance-sheet pension liabilities, compared to firms thatare in the levels sample but not in the changes sample.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1111

The Accounting ReviewMay 2013

DMVit ¼ k0 þ k1POST þ k2INSit þ k3DNPTAit þ k4DNPTLit þ k5DONBLit þ k6INS�DONBLþ k7POST�DONBLþ k8POST�INS�DONBL þ k9DOFFBLit þ k10INSit�DOFFBLit

þ k11POST�DOFFBLit þ k12POST�INSit�DOFFBLit þ k13DPXit þ k14INSit�DPXit

þ k15POST�DPXit þ k16POST�INSit�DPXit þ k17DNI-PX þ k18DRDþ k19DGRWþ k20INS�DNPTA þ k21POST�DNPTAþ k22POST�INS�DNPTAþ k23INS�DNPTLþ k24POST�DNPTLþ k25POST�INS�DNPTLþ k26INS�DNI-PXþ k27POST�DNI-PX þ k28POST�INS�DNI-PX þ k29INS�DRDþ k30POST�DRDþ k31POST�INS�DRDþ k32INS�DGRW þ k33POST�DGRWþ k34POST�INS�DGRW þ eit:

ð4Þ

TABLE 5

Value-Relevance Tests after Considering Institutional Ownership and Analyst FollowingUsing Changes Models

Panel A: Results Based on Changes models

PredictedSign

(1)Institutional Ownership

(2)Analyst Following

Coefficient (t-statistic) Coefficient (t-statistic)

POST ? �0.161 (�8.31)*** �0.144 (�9.67)***

INS ? 0.034 (0.88) �0.005 (�0.15)

DNPTA þ 1.008 (22.18)*** 1.004 (36.67)***

DNPTL � �0.951 (�18.75)*** �0.984 (�33.36)***

DONBL � �0.970 (�4.71)*** �1.225 (�8.06)***

INS � DONBL ? 0.084 (0.20) 0.323 (1.08)

POST � DONBL ? �5.345 (�2.64)*** �1.750 (�2.14)**

POST � INS � DONBL ? 4.972 (1.95)* 3.721 (2.23)**

DOFFBL ? 0.026 (0.22) 0.063 (0.73)

INS � DOFFBL � �0.858 (�3.52)*** �0.498 (�2.78)***

POST � DOFFBL � �5.119 (�3.08)*** �2.458 (�3.99)***

POST � INS � DOFFBL þ 5.250 (2.47)** 2.838 (2.19)**

DPX � �0.007 (�0.03) 0.050 (0.22)

INS � DPX ? �2.528 (�4.51)*** 1.869 (2.46)**

POST � DPX ? 0.630 (0.11) �5.479 (�1.28)

POST � INS � DPX ? �3.754 (�0.43) 5.791 (1.38)

DNI-PX þ 0.076 (1.73)* 0.040 (1.67)*

DRD þ 0.216 (0.29) 0.311 (0.61)

DGRW þ 0.902 (37.00)*** 0.144 (9.67)***

Interactions among INS, POST, and Non-Pension

Variables

Yes Yes

Fixed Firm and Year Effects Yes Yes

Adjusted R2 0.653 0.765

No. of Observations 7,887 7,887

(continued on next page)

1112 Yu

The Accounting ReviewMay 2013

D represents the changes in the following variables at the end of year t relative to the end of year

t�1. All the changes in the variables are deflated by the beginning year market value. The main

results are generally consistent with those using levels models.

Roles of Different Types of Institutional Investors

Bushee (1998) classifies institutions into transient, quasi-indexer, and dedicated institutions.

Quasi-indexer institutions generally follow index investment strategies and do not conduct

fundamental analysis. Therefore, the ownership of quasi-indexers may not capture differential

information processing associated with investor sophistication or the information environment.

Prior literature provides mixed evidence regarding the information-processing ability of transient

institutional investors. Bushee (1998, 2001) finds that transient institutional investors are short-

term-focused, and are more likely to follow momentum trading strategies, suggesting that transient

institutions may not use information disclosed in the footnotes. In contrast, Xue and Zhang (2011)

find that transient institutions also conduct fundamental analysis. Similarly, several other studies

find that transient institutional investors can predict a bad news break in a string of consecutive

earnings increases (Ke and Petroni 2004) and can mitigate stock mispricing (Ke and

Ramalingegowda 2005; Collins et al. 2003), suggesting that they are better informed and have

superior ability to process information.

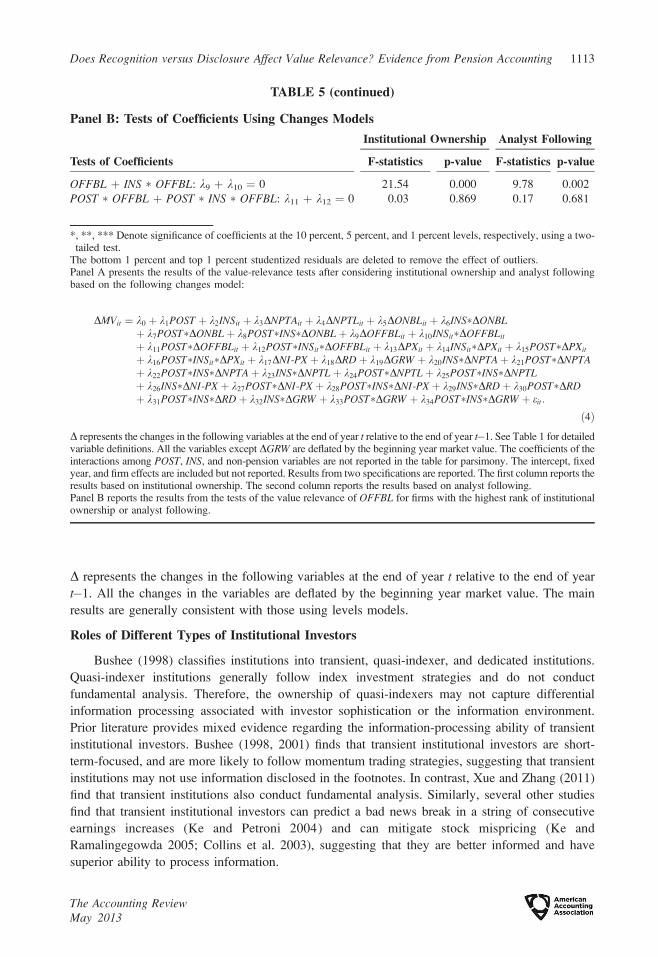

TABLE 5 (continued)

Panel B: Tests of Coefficients Using Changes Models

Tests of Coefficients

Institutional Ownership Analyst Following

F-statistics p-value F-statistics p-value

OFFBL þ INS � OFFBL: k9 þ k10 ¼ 0 21.54 0.000 9.78 0.002

POST � OFFBL þ POST � INS � OFFBL: k11 þ k12 ¼ 0 0.03 0.869 0.17 0.681

*, **, *** Denote significance of coefficients at the 10 percent, 5 percent, and 1 percent levels, respectively, using a two-tailed test.

The bottom 1 percent and top 1 percent studentized residuals are deleted to remove the effect of outliers.Panel A presents the results of the value-relevance tests after considering institutional ownership and analyst followingbased on the following changes model:

DMVit ¼ k0 þ k1POST þ k2INSit þ k3DNPTAit þ k4DNPTLit þ k5DONBLit þ k6INS�DONBLþ k7POST�DONBLþ k8POST�INS�DONBLþ k9DOFFBLit þ k10INSit�DOFFBLit

þ k11POST�DOFFBLit þ k12POST�INSit�DOFFBLit þ k13DPXit þ k14INSit�DPXit þ k15POST�DPXit

þ k16POST�INSit�DPXit þ k17DNI-PX þ k18DRDþ k19DGRW þ k20INS�DNPTAþ k21POST�DNPTAþ k22POST�INS�DNPTAþ k23INS�DNPTLþ k24POST�DNPTLþ k25POST�INS�DNPTLþ k26INS�DNI-PX þ k27POST�DNI-PX þ k28POST�INS�DNI-PX þ k29INS�DRDþ k30POST�DRDþ k31POST�INS�DRDþ k32INS�DGRW þ k33POST�DGRW þ k34POST�INS�DGRW þ eit:

ð4Þ

D represents the changes in the following variables at the end of year t relative to the end of year t�1. See Table 1 for detailedvariable definitions. All the variables except DGRW are deflated by the beginning year market value. The coefficients of theinteractions among POST, INS, and non-pension variables are not reported in the table for parsimony. The intercept, fixedyear, and firm effects are included but not reported. Results from two specifications are reported. The first column reports theresults based on institutional ownership. The second column reports the results based on analyst following.Panel B reports the results from the tests of the value relevance of OFFBL for firms with the highest rank of institutionalownership or analyst following.

Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting 1113

The Accounting ReviewMay 2013

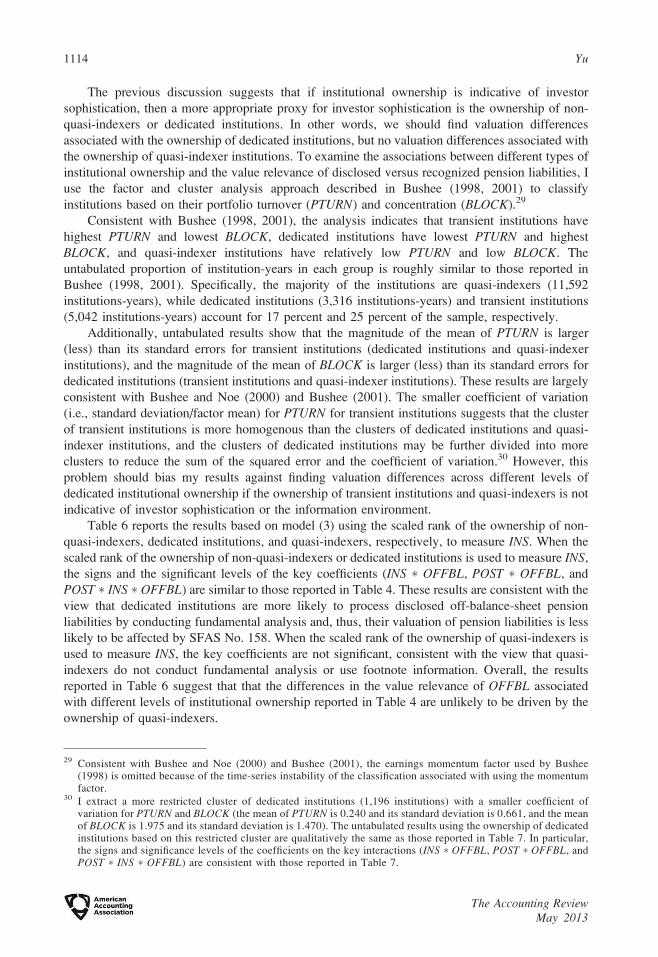

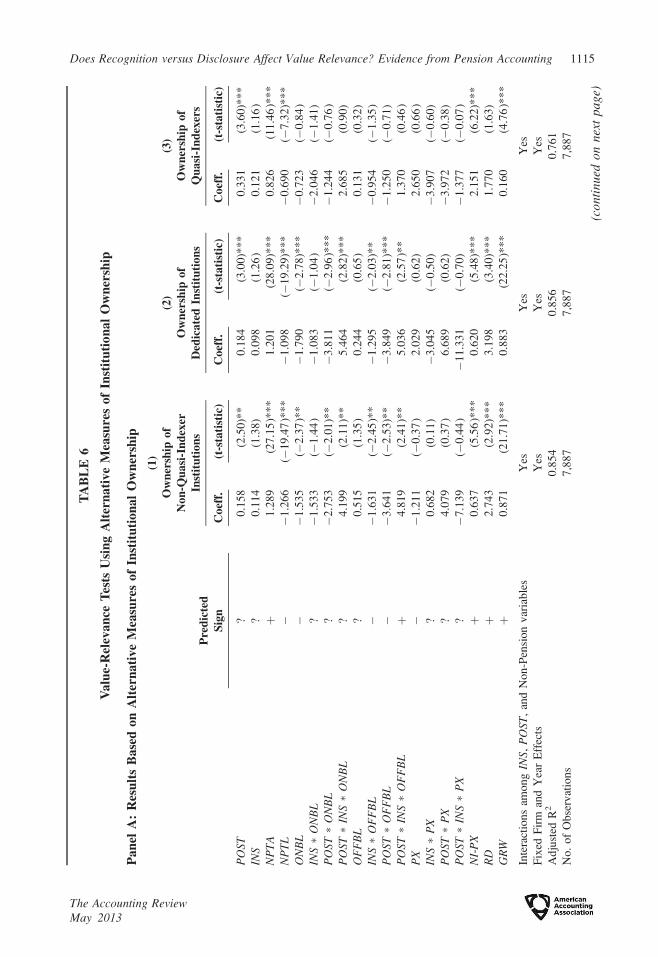

The previous discussion suggests that if institutional ownership is indicative of investor

sophistication, then a more appropriate proxy for investor sophistication is the ownership of non-

quasi-indexers or dedicated institutions. In other words, we should find valuation differences

associated with the ownership of dedicated institutions, but no valuation differences associated with

the ownership of quasi-indexer institutions. To examine the associations between different types of

institutional ownership and the value relevance of disclosed versus recognized pension liabilities, I

use the factor and cluster analysis approach described in Bushee (1998, 2001) to classify

institutions based on their portfolio turnover (PTURN) and concentration (BLOCK).29

Consistent with Bushee (1998, 2001), the analysis indicates that transient institutions have

highest PTURN and lowest BLOCK, dedicated institutions have lowest PTURN and highest

BLOCK, and quasi-indexer institutions have relatively low PTURN and low BLOCK. The

untabulated proportion of institution-years in each group is roughly similar to those reported in

Bushee (1998, 2001). Specifically, the majority of the institutions are quasi-indexers (11,592

institutions-years), while dedicated institutions (3,316 institutions-years) and transient institutions

(5,042 institutions-years) account for 17 percent and 25 percent of the sample, respectively.

Additionally, untabulated results show that the magnitude of the mean of PTURN is larger

(less) than its standard errors for transient institutions (dedicated institutions and quasi-indexer

institutions), and the magnitude of the mean of BLOCK is larger (less) than its standard errors for

dedicated institutions (transient institutions and quasi-indexer institutions). These results are largely

consistent with Bushee and Noe (2000) and Bushee (2001). The smaller coefficient of variation

(i.e., standard deviation/factor mean) for PTURN for transient institutions suggests that the cluster

of transient institutions is more homogenous than the clusters of dedicated institutions and quasi-

indexer institutions, and the clusters of dedicated institutions may be further divided into more