Embed Size (px)

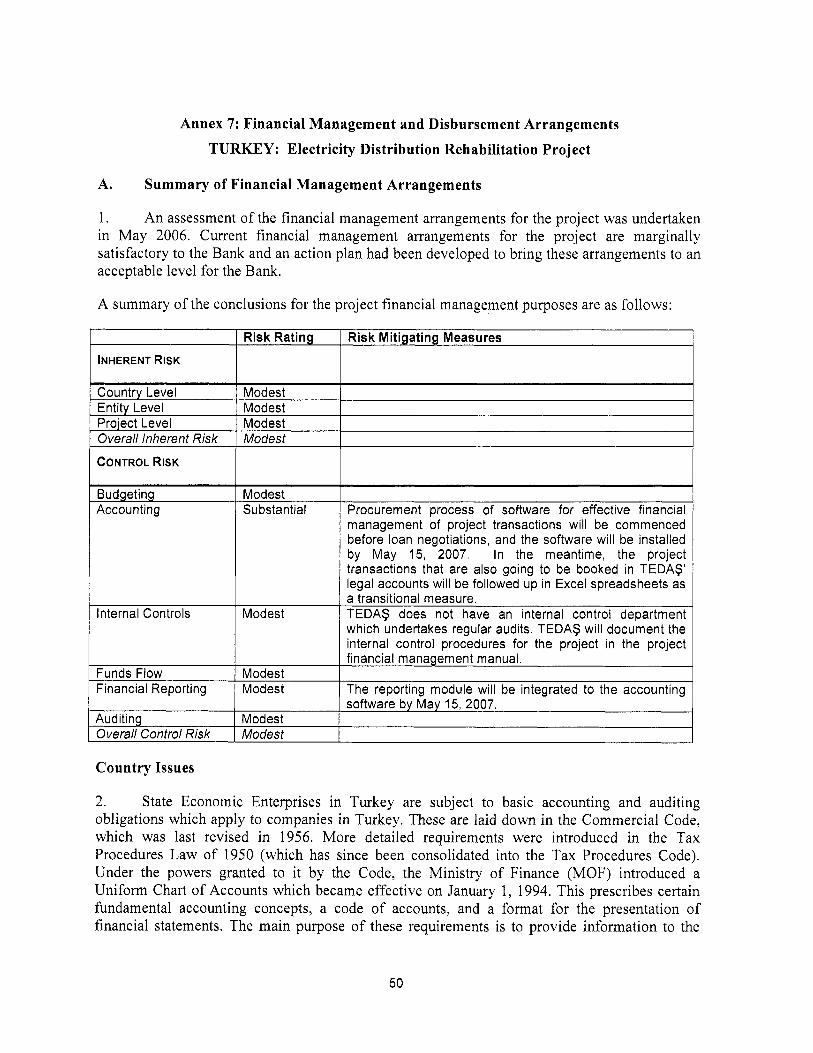

Citation preview

Document o f The World Bank

FOR OFFICIAL USE ONLY

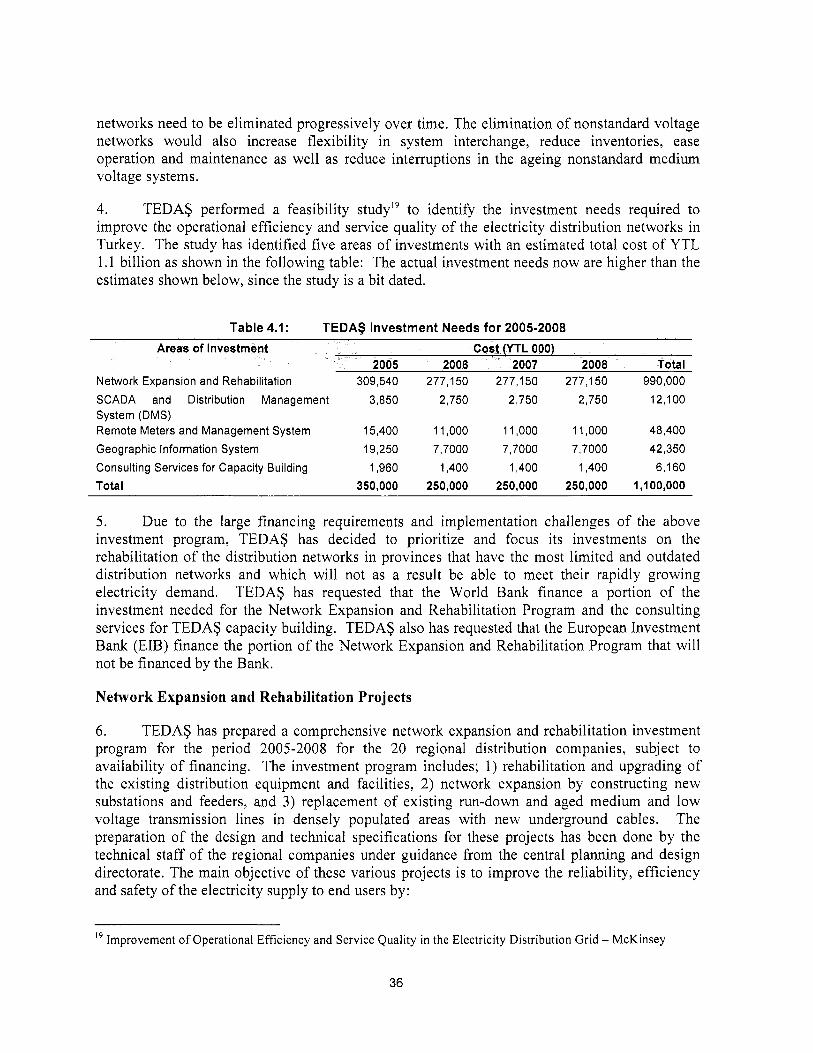

Report No: 36341-TR

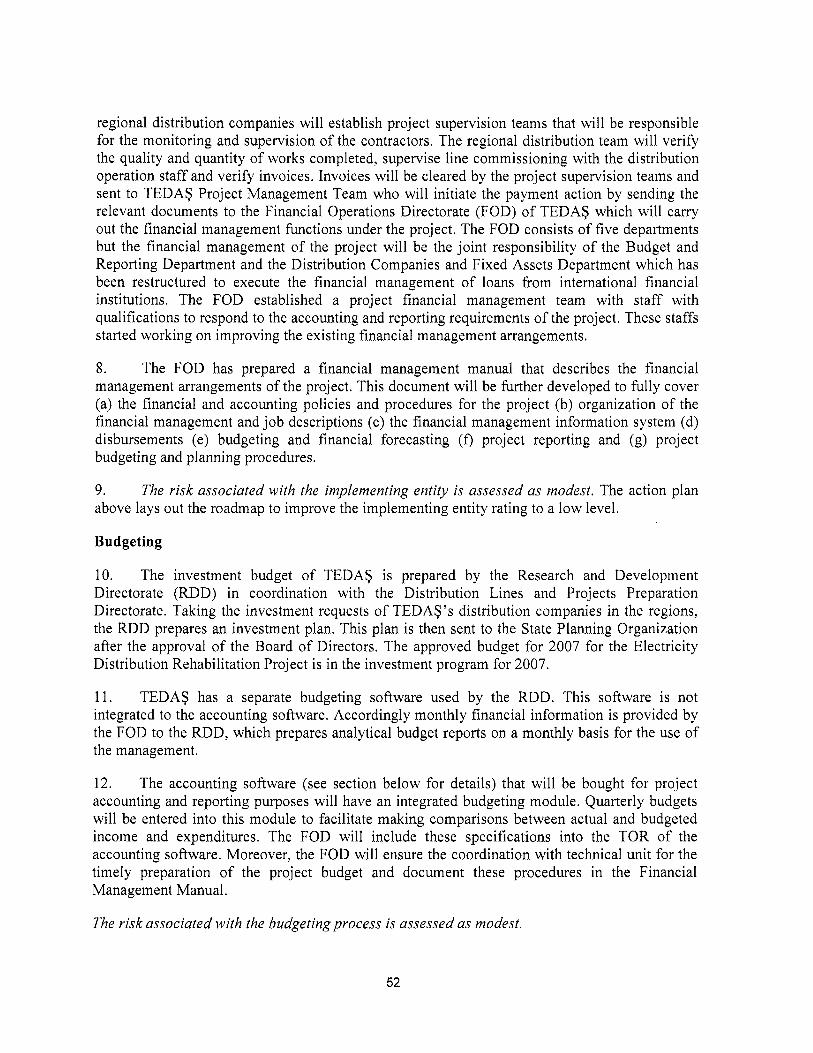

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF EURO 205 MILLION

(US$269.4 MILLION EQUIVALENT)

TO THE

TURKIYE ELEKTRIK DAGITIM A.S. (TEDAS)

WITH THE GUARANTEE OF THE REPUBLIC OF TURKEY

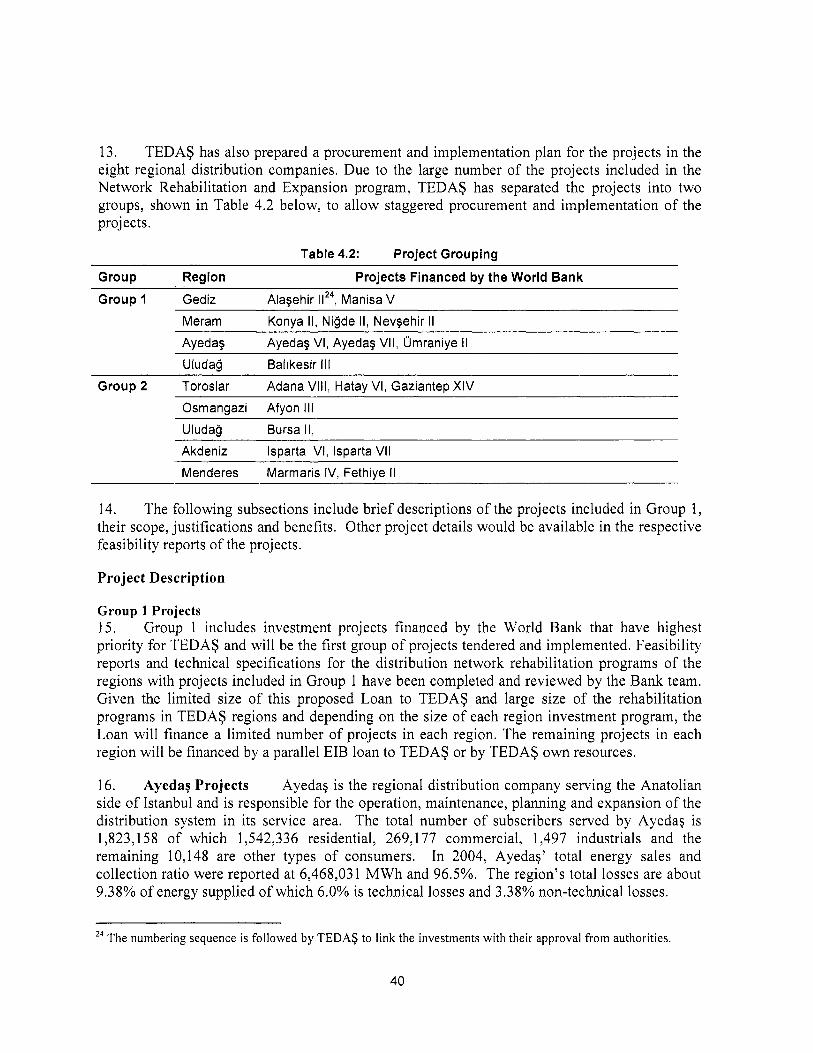

FOR AN

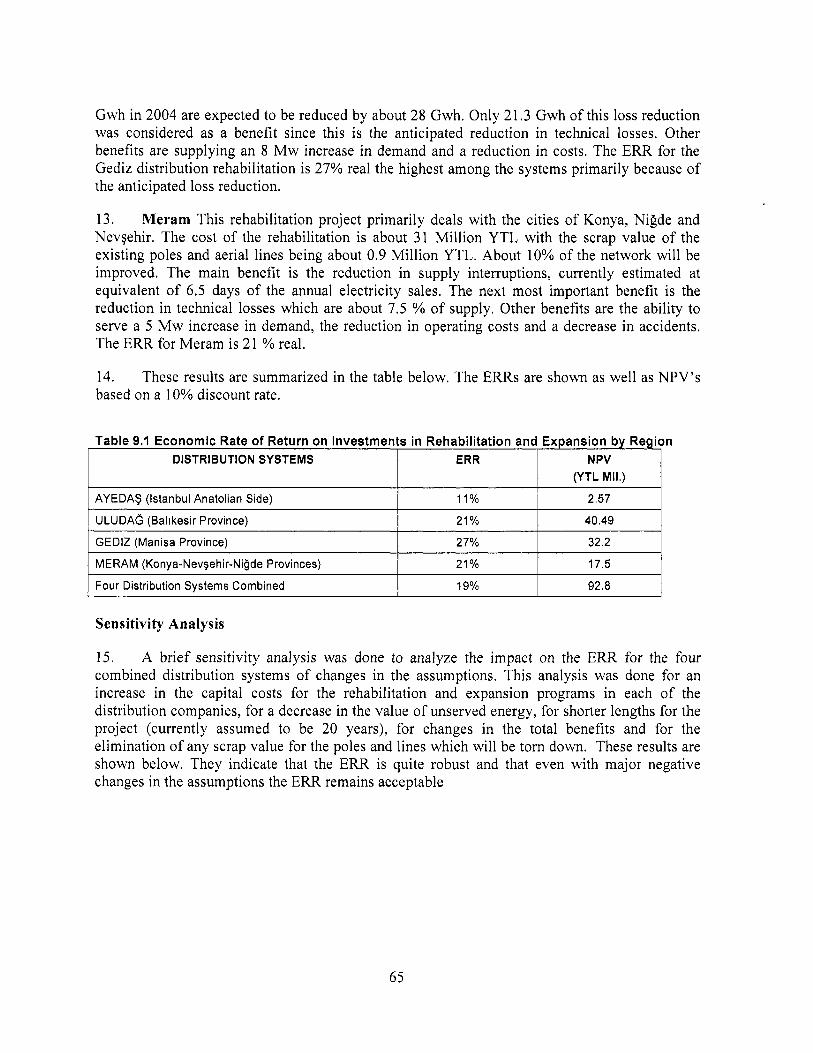

ELECTRICITY DISTRIBUTION REHABILITATION PROJECT

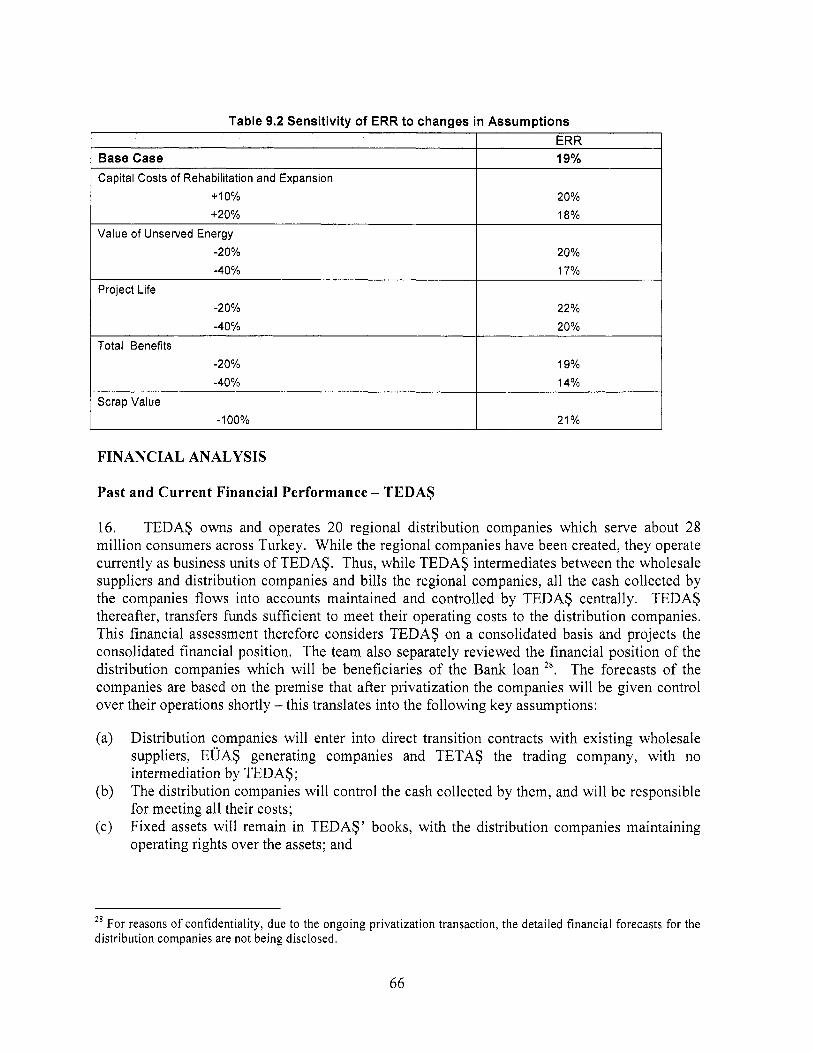

March 26, 2007

Sustainable Development Unit Europe and Central Asia Region (EC S S D)

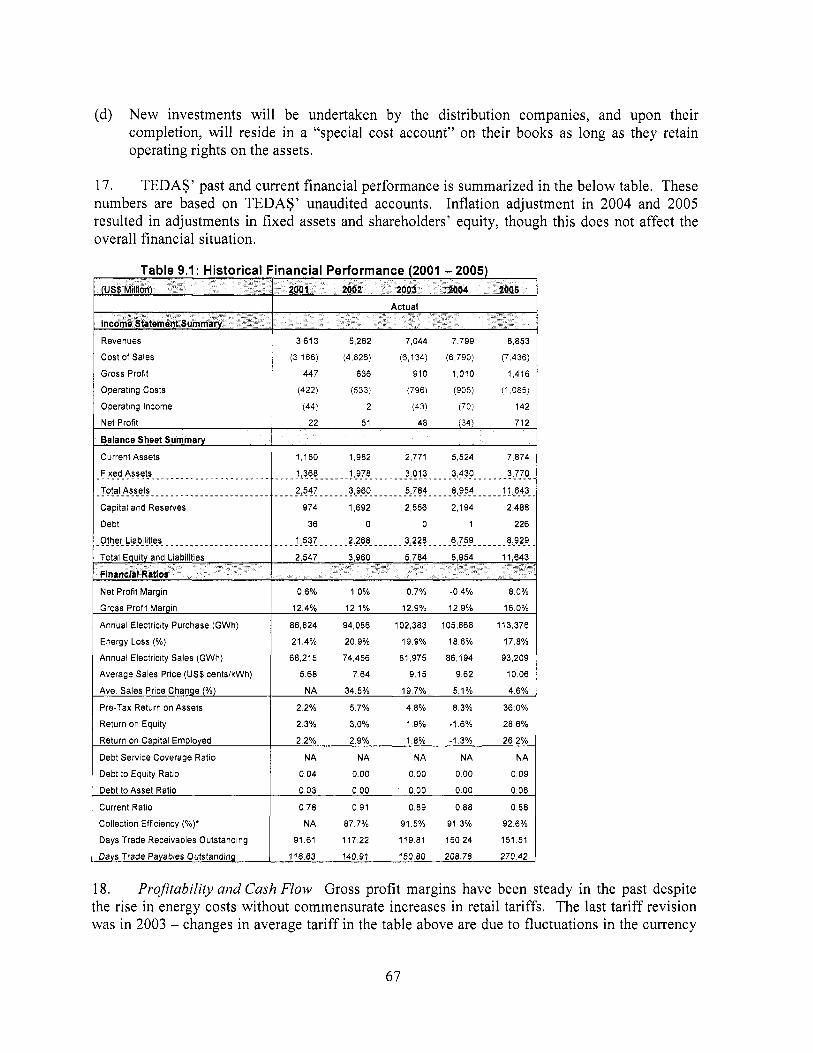

This document has a restricted distribution and may be used by recipients only in the performance o f their official duties. I t s contents may not otherwise be disclosed without World Bank authorization.

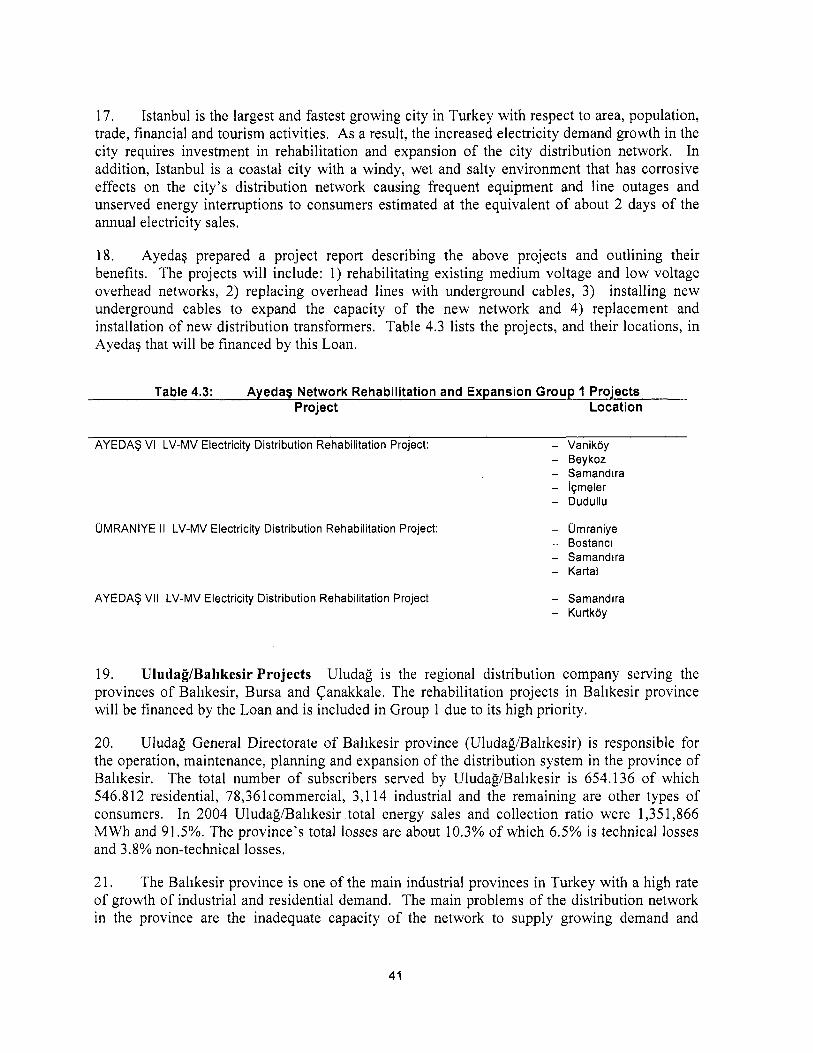

Pub

lic D

iscl

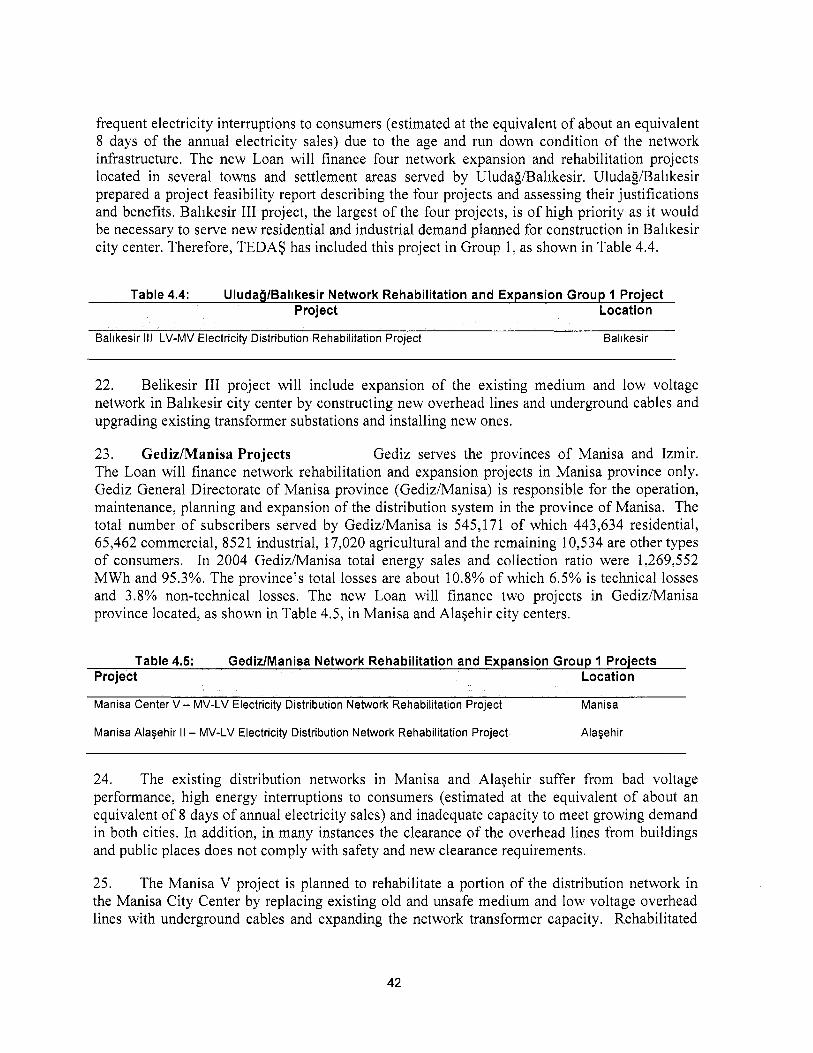

osur

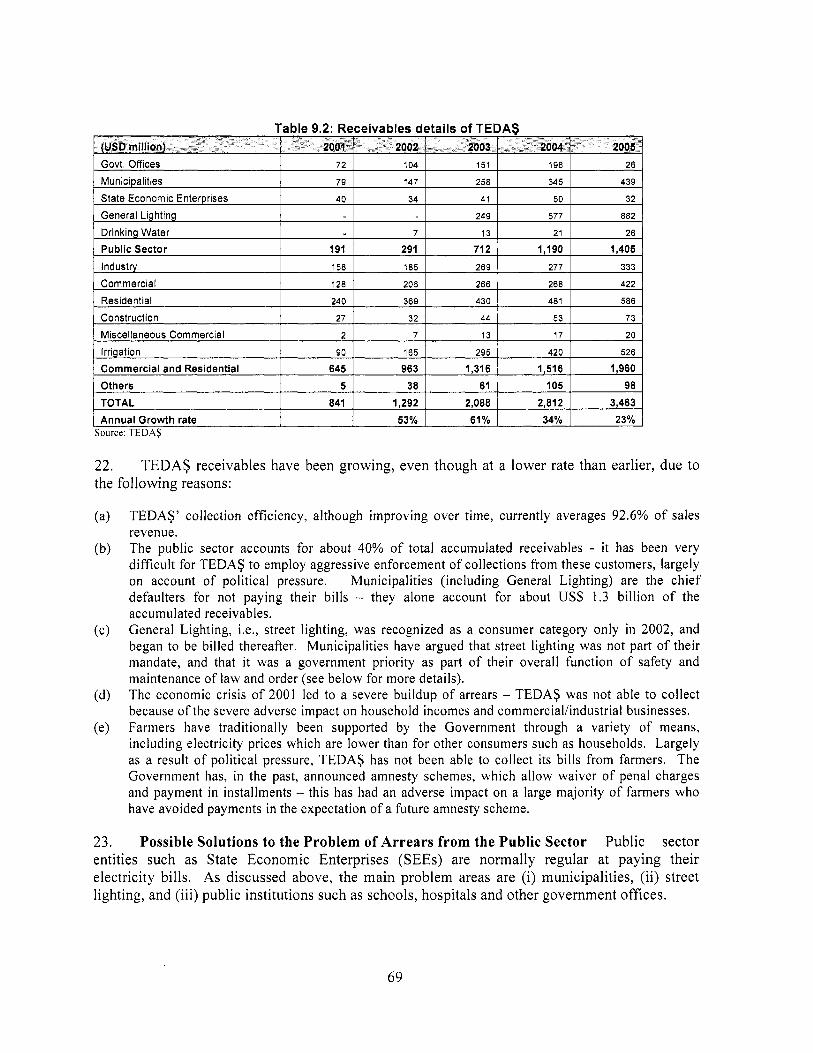

e A

utho

rized

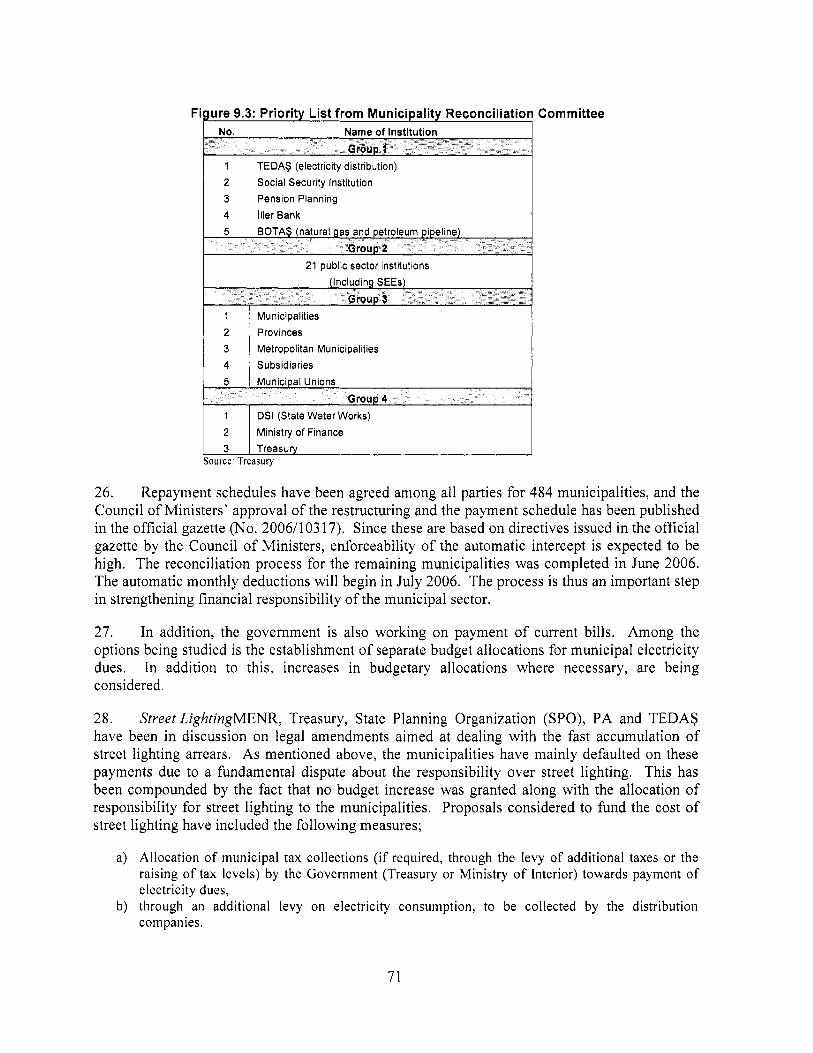

Pub

lic D

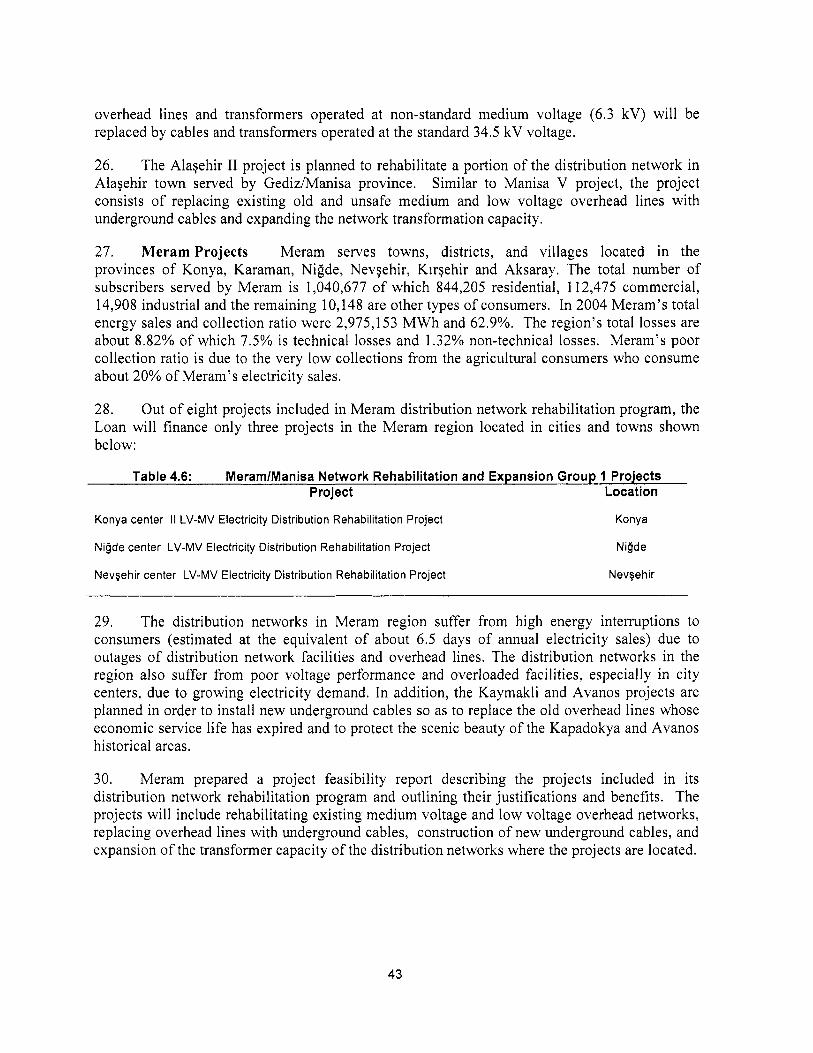

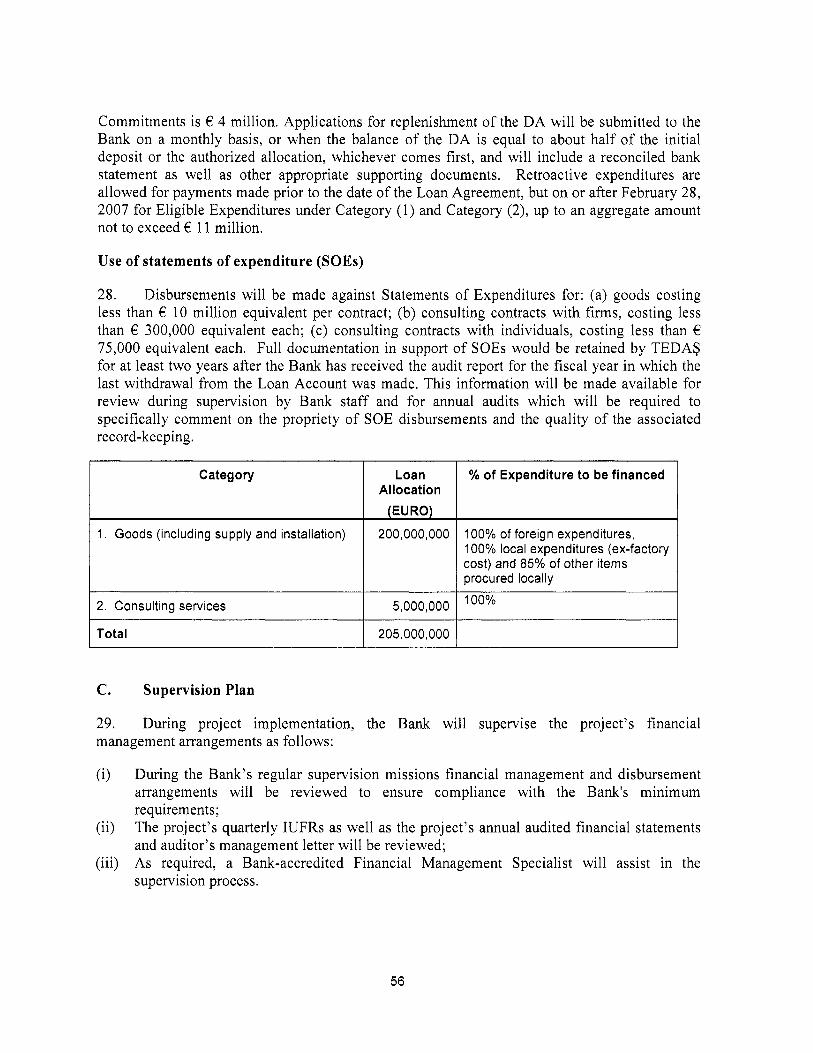

iscl

osur

e A

utho

rized

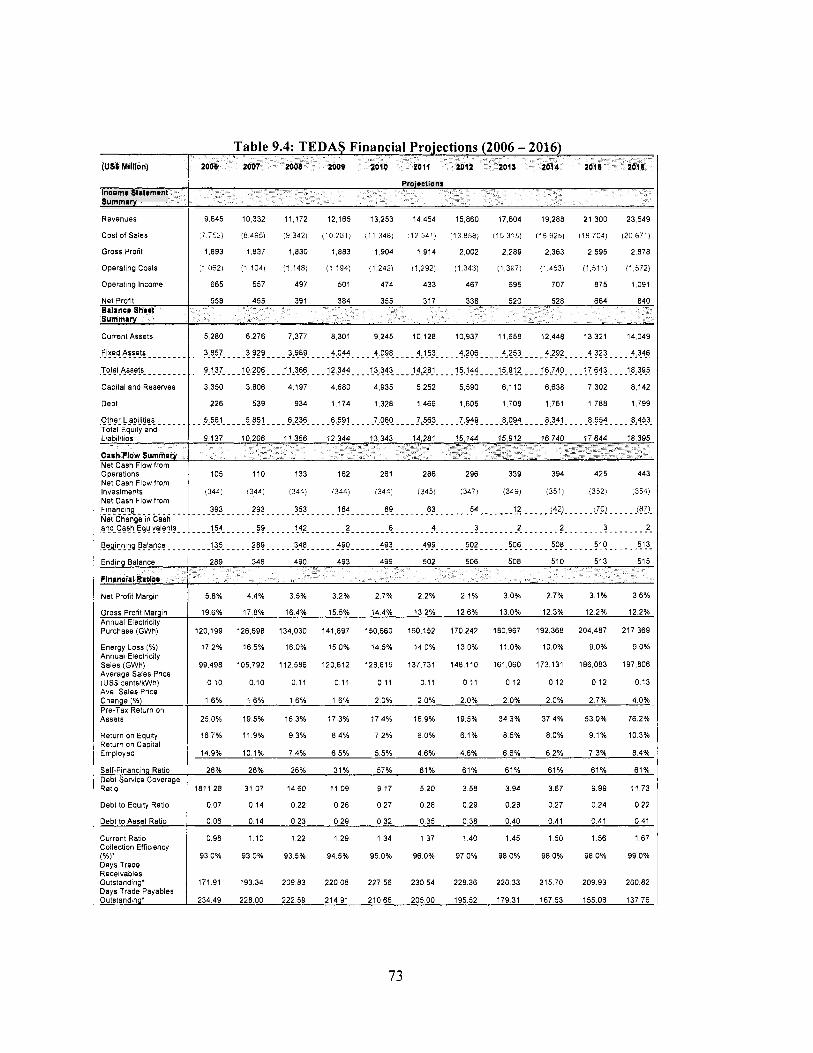

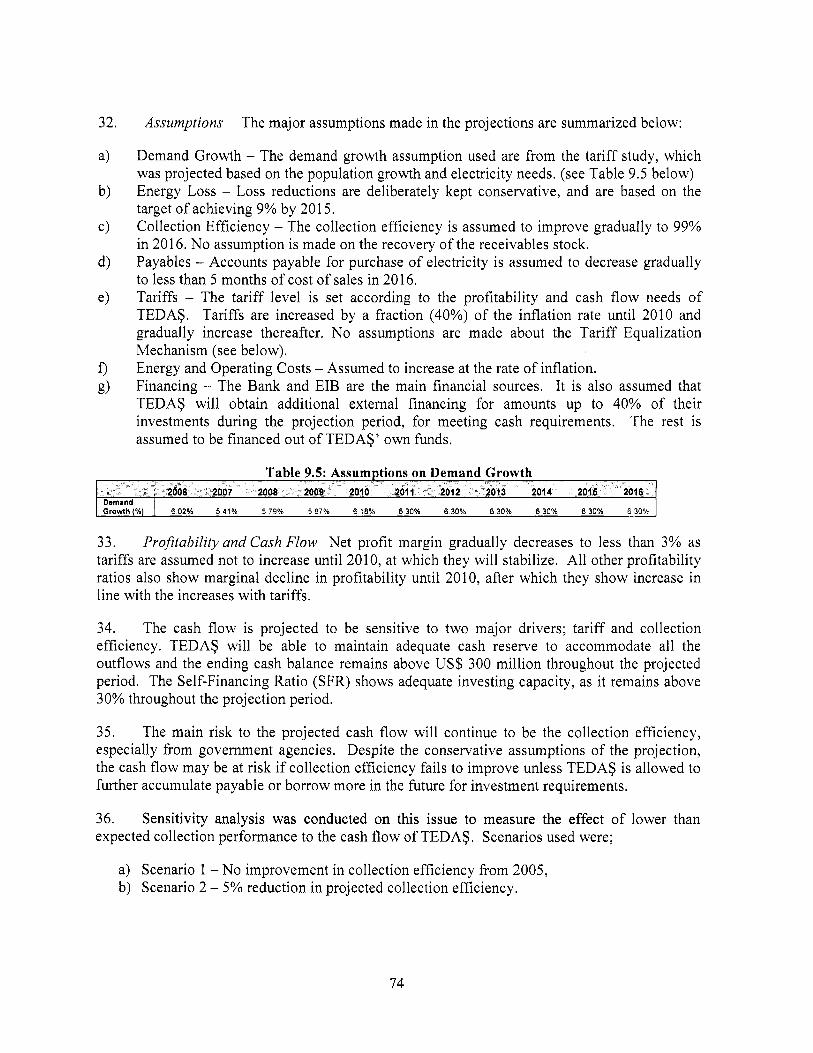

Pub

lic D

iscl

osur

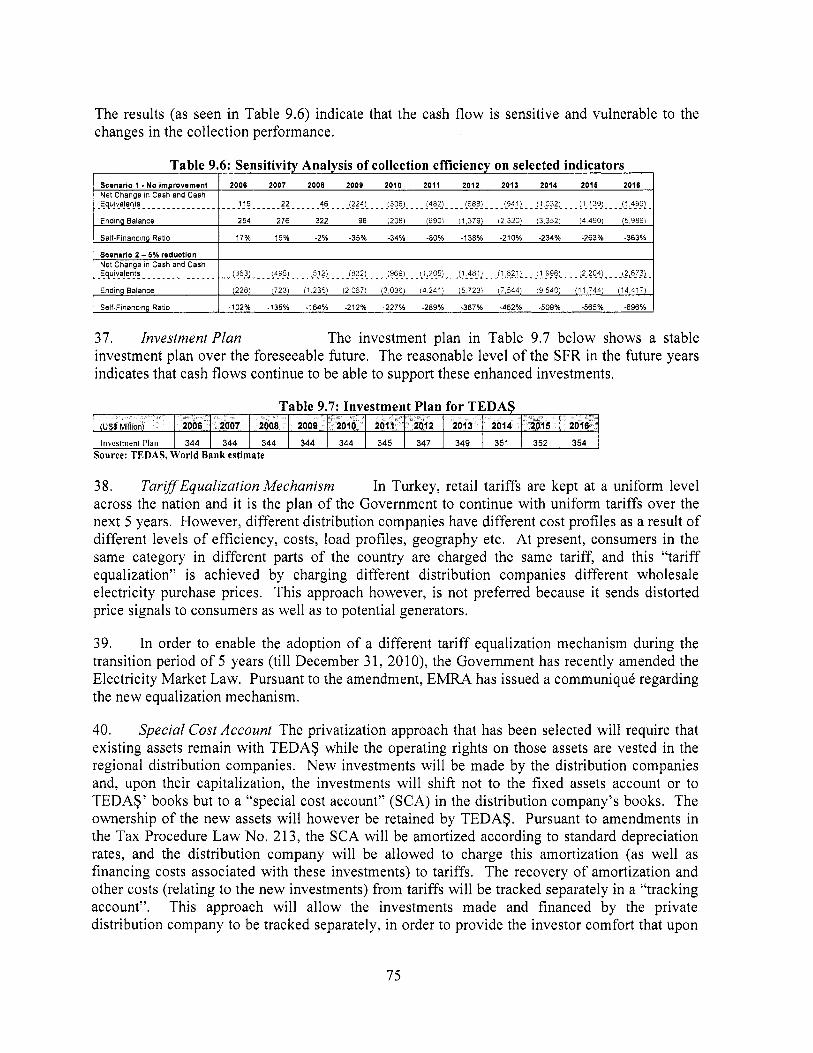

e A

utho

rized

Pub

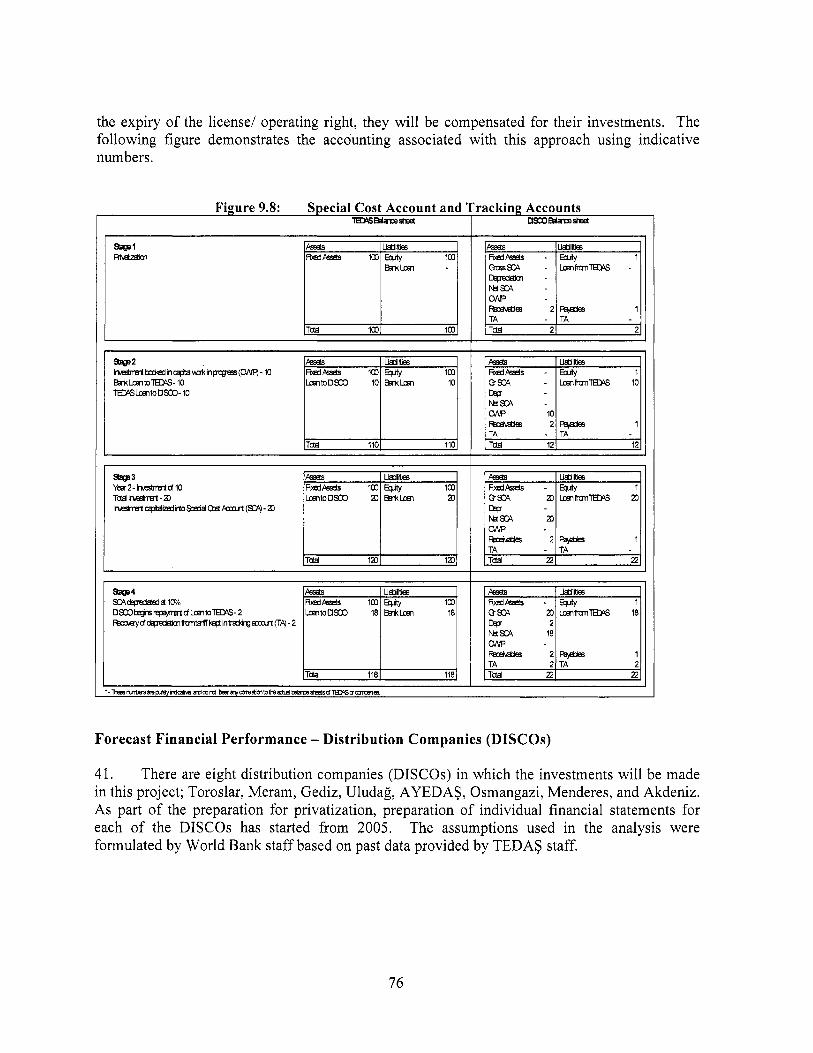

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS (Exchange Rate Effective February 28,2007)

YTL 1.4 = US$1 US$ 1.31 = €1

Currency Unit = New Turkish Lira (YTL)

APL BOOS BOTAS

BOTS CAS CFAA DISCO(s) DSI EA EC ECSEE EIA EIB EML EMP EMRA EPDK ERP EU EUAS GENCO(s) IBRD IDA IFC LNG MENR MOEF MOF PA PPA PPIAF SEE SIL SPO TEAS TEDAS TEK TEIAS UCTE

FISCAL YEAR January 1 - December 31

ABBREVIATIONS AND ACRONYMS Adaptable Program Loan Build Own and Operate Power Plants BORU HATLARI ILE PETROL TASIMA A.S. (Turkish Pipeline Company) Build Operate and Transfer Power Plants Country Assistance Strategy Country Financial Accountability Assessment Distribution company(ies) formed by restructuring TEDAS Devlet Su Ivleri (State Hydraulic Works) Environmental Assessment European Commission Energy Community o f South Eastern Europe Environmental Impact Assessment European Investment Bank Electricity Market Law, No. 4628, 2001 Environmental Management Plan Energy Market Regulatory Authority Enerji Piyasasi Duzenleme Kurumu (EMRA in Turkish) Enterprise Resource Planning program European Union Elektrik Uretim A,$. (Electricity Generation Corporation, Turkey)

nd Petroleum Tran mission

Portfolio generating companies to be created from the restructuring o f EUAS International Bank for Reconstruction and Development International Development Association International Finance Corporation Liquefied Natural Gas Ministry o f Energy and Natural Resources Ministry o f Environment & Forestry Ministry o f Finance Privatization Administration Power Purchase Agreement Public-Private Infrastructure Advisory Facility State Economic Enterprise Specific Investment Loan State Planning Organization Turkiye Elektrik A,$. (Turkish Electricity Corporation, Predecessor o f EUAS and TEIAS) Turkiye Elektrik Dagitim A.S. (Turkish Electricity Distribution Corporation) Turkiye Elektrik Kurumu (Turkish Electricity Corporation, Predecessor o f existing Corporations) Turkiye Elektrik Iletim A.S. (Turkish Electricity Transmission Corporation) Union for the Coordination o f Transmission o f Electricity in Europe

Vice President: Shigeo Katsu Country Director: Ulrich Zachau

Task Team Leader: Sameer Shukla Sector Manager: Charles Feinstein

FOR OFFICIAL USE ONLY TURKEY

Electricity Distribution Rehabilitation Project

CONTENTS

Page

A . STRATEGIC CONTEXT AND RATIONALE .................................................................. 5 Country and sector issues .................................................................................................... 5

Rationale for Bank involvement .......................................................................................... 9

Higher leve l objectives to which the project contributes .................................................. 10

1.

2 . 3 .

B . PROJECT DESCRIPTION ................................................................................................ 10 1 . 2 . 3 . 4 . 5 .

Lending instrument ........................................................................................................... -10

Project development objective and key indicators ............................................................ 10

Project components ............................................................................................................ 10 Lessons learned and reflected in the project design .......................................................... 11

Alternatives considered and reasons for rejection ............................................................. 12

C . IMPLEMENTATION ........................................................................................................ -13 1 . 2 . 3 . 4 . Sustainability ..................................................................................................................... 14

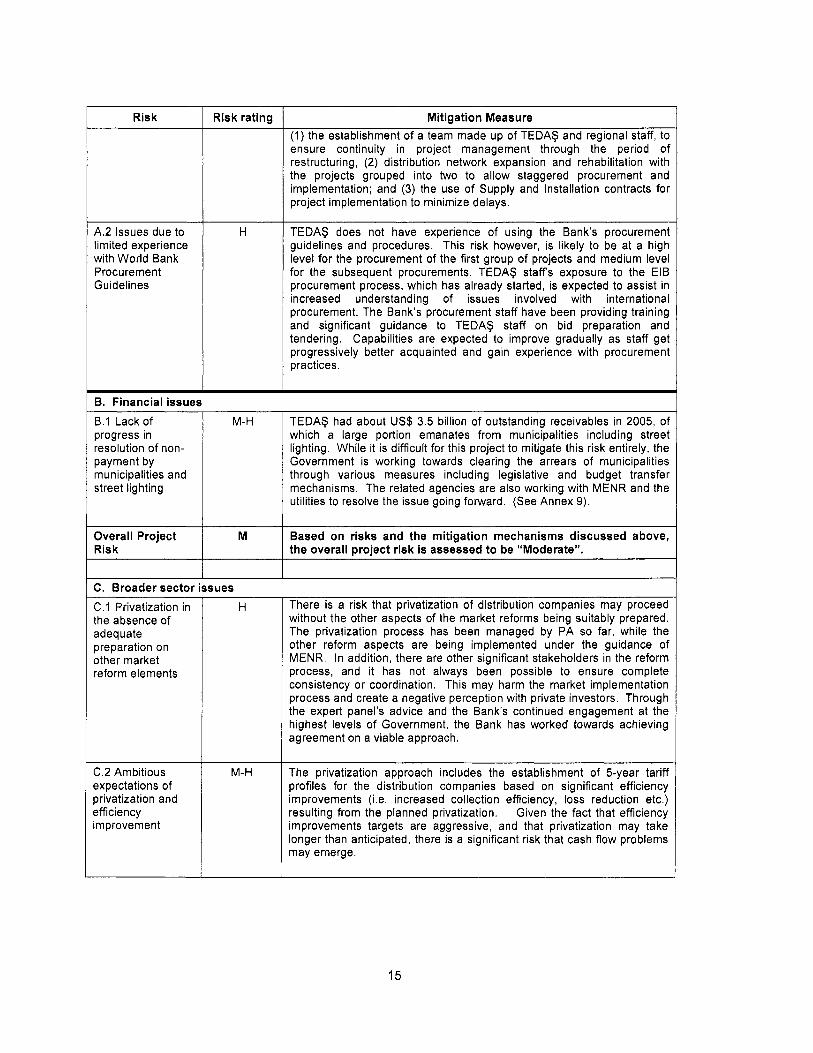

5 . Critical risks and possible controversial aspects ............................................................... 14

6 . Loadcredit conditions and covenants ............................................................................... 16

Partnership arrangements (if applicable) ........................................................................... 13

Institutional and implementation arrangements ................................................................ 13

Monitoring and evaluation o f outcomes/results ................................................................ 14

D . APPRAISAL SUMMARY .................................................................................................. 17 1 . Economic and financial analysis ....................................................................................... 17

2 . Technical ........................................................................................................................... 19

3 . Fiduciary ............................................................................................................................ 20

4 . Social ................................................................................................................................. 20

5 . Environment ...................................................................................................................... 21

6 . Safeguard policies .............................................................................................................. 21

7 . Policy Exceptions and Readiness ...................................................................................... 21

This document has a restricted distribution and may be used by recipients only in the performance o f their off icial duties . I t s contents may not be otherwise disclosed without Wor ld Bank authorization .

Annex 1: Country and Sector or Program Background .......................................................... 22

Annex 2: Majo r Related Projects Financed by the Bank and/or other Agencies .................. 29

Annex 3: Results Framework and Monitor ing ......................................................................... 32

Annex 4: Detailed Project Description ...................................................................................... 35

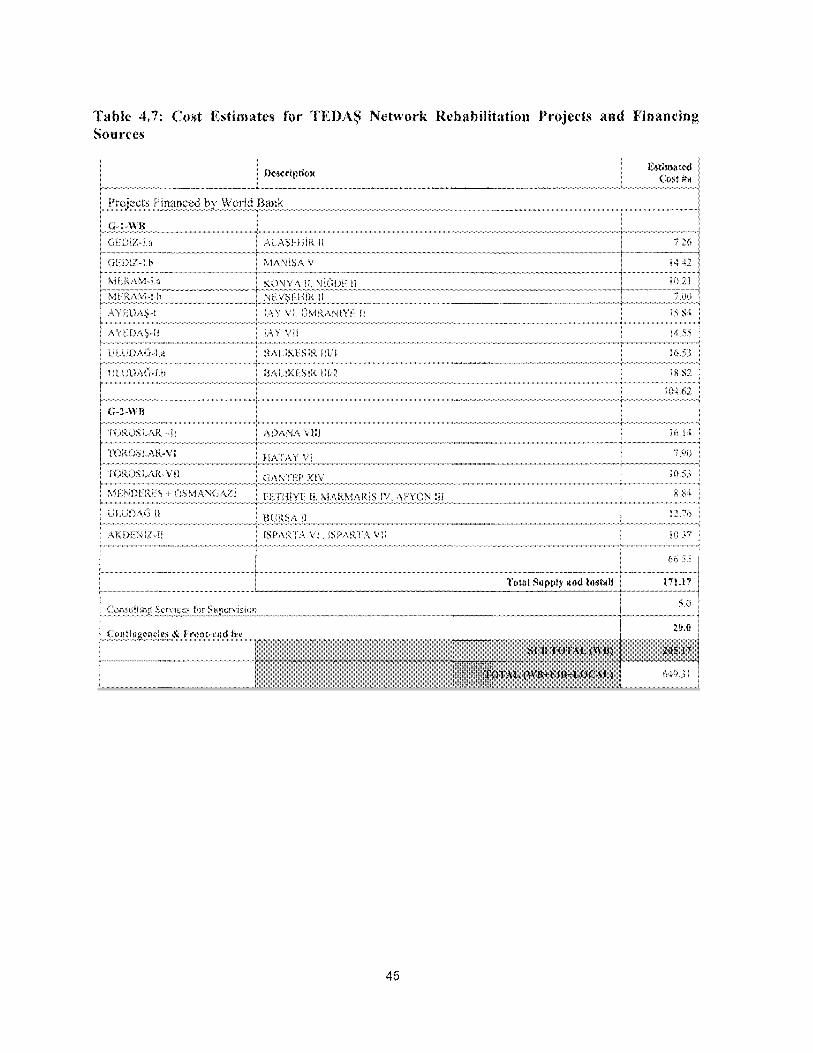

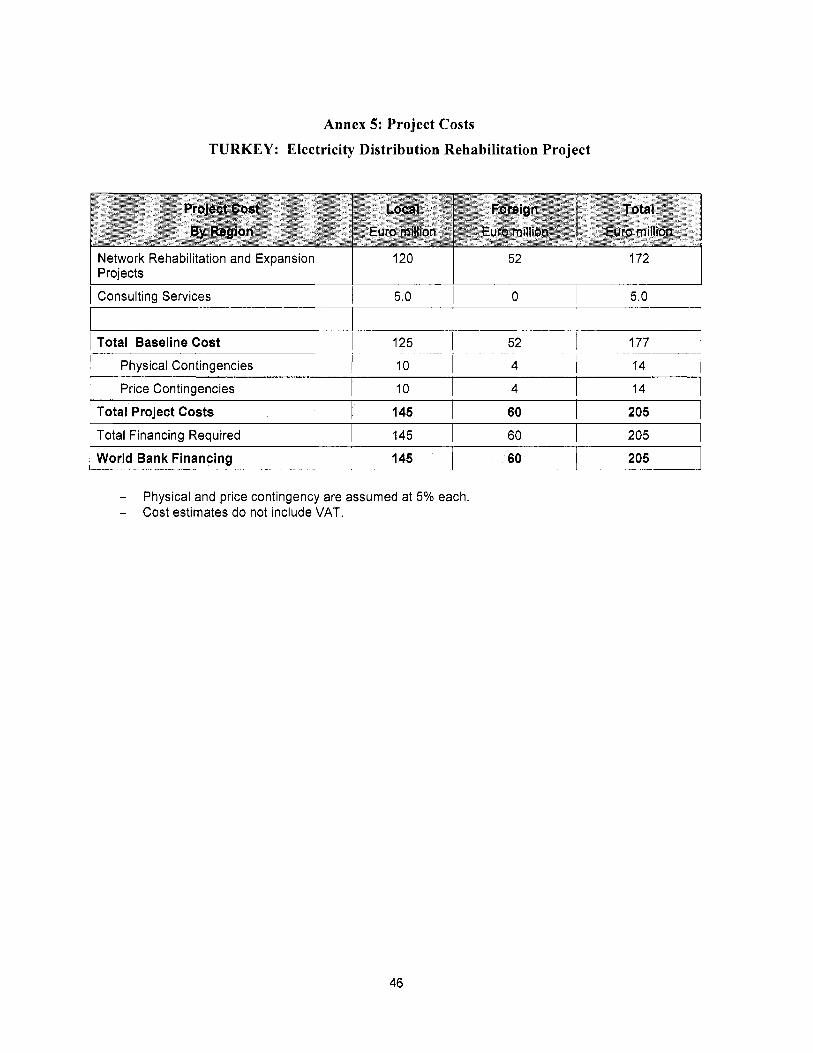

Annex 5: Project Costs ................................................................................................................ 46

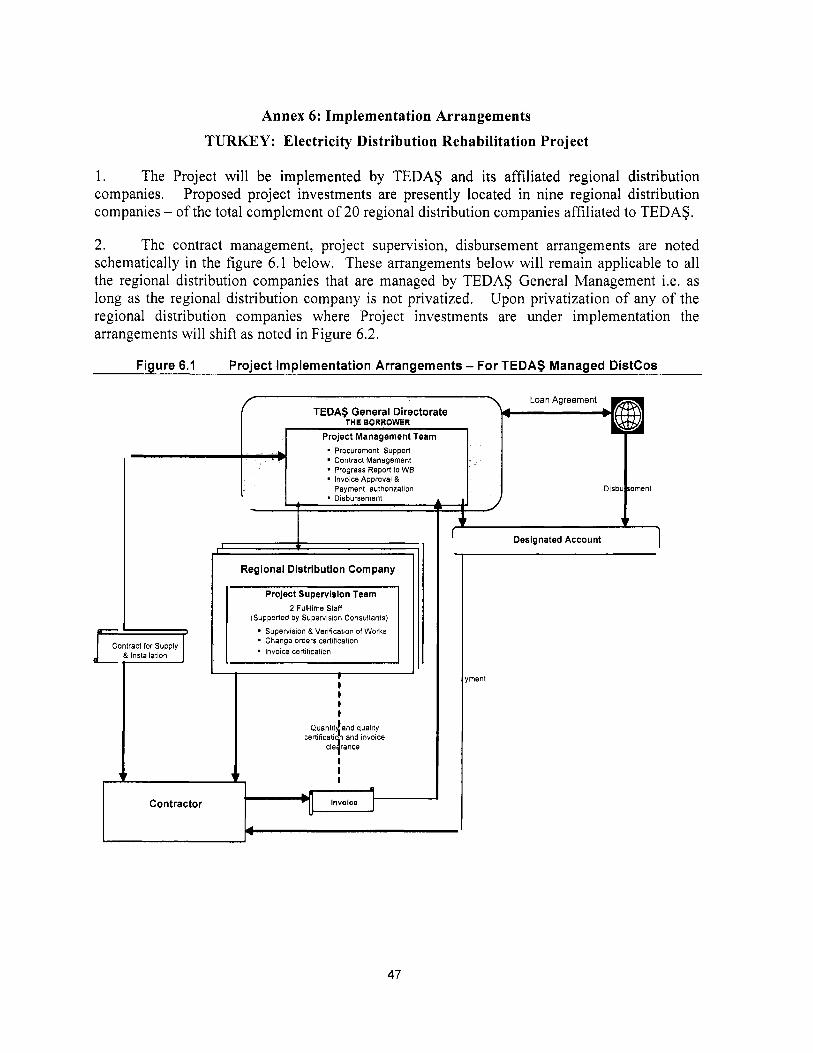

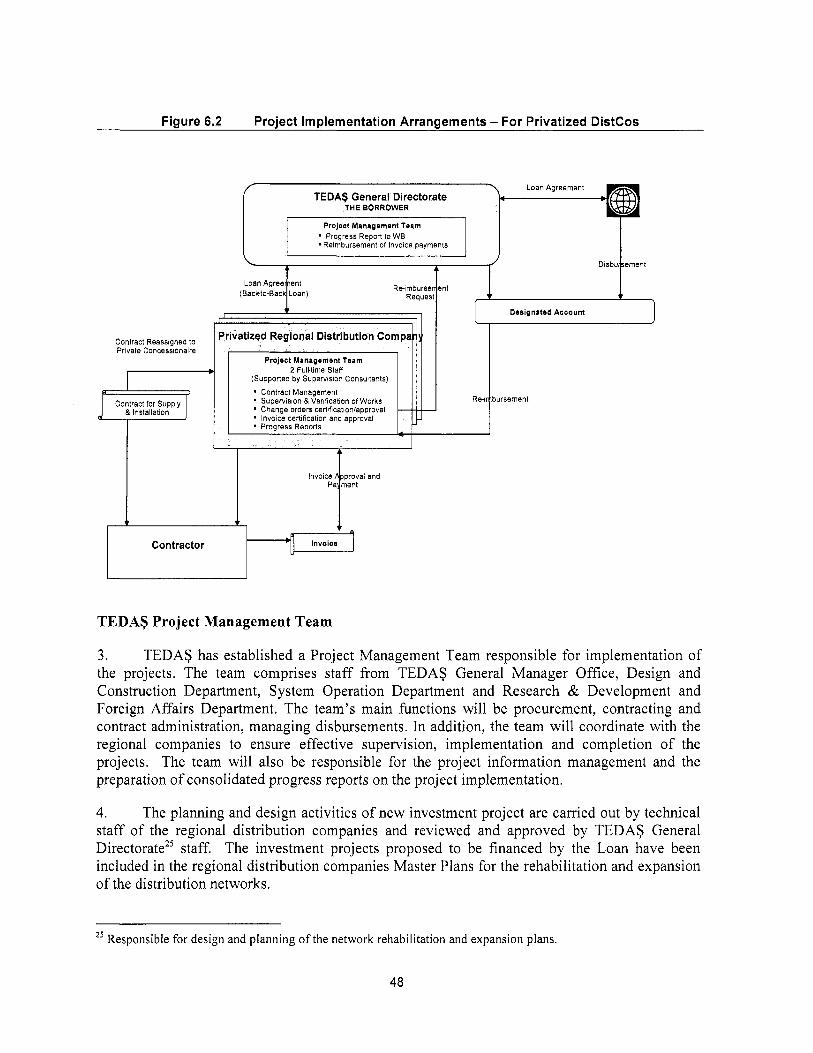

Annex 6: Implementation Arrangements .................................................................................. 47

Annex 7: Financial Management and Disbursement Arrangements ..................................... 50

Annex 8: Procurement Arrangements ....................................................................................... 57

Annex 9: Economic and Financial Analysis .............................................................................. 62

Annex 10: Safeguard Policy Issues ............................................................................................. 78

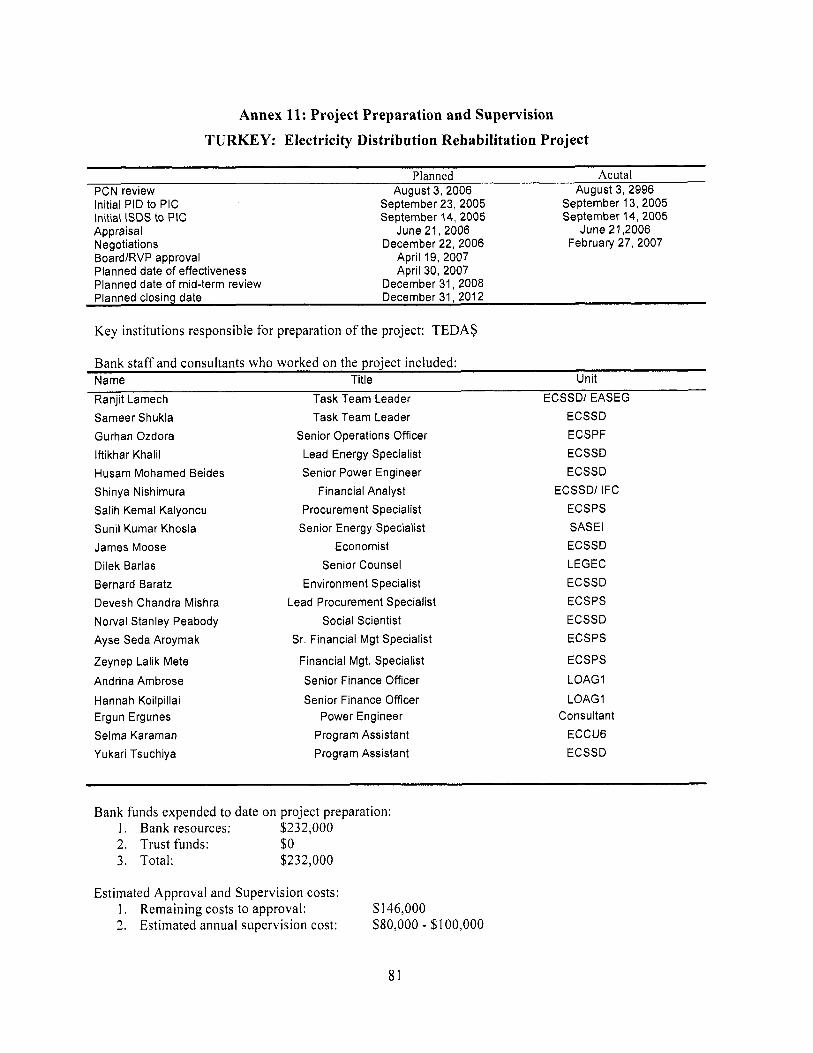

Annex 11: Project Preparation and Supervision ...................................................................... 81

Annex 12: Documents in the Project F i l e .................................................................................. 82

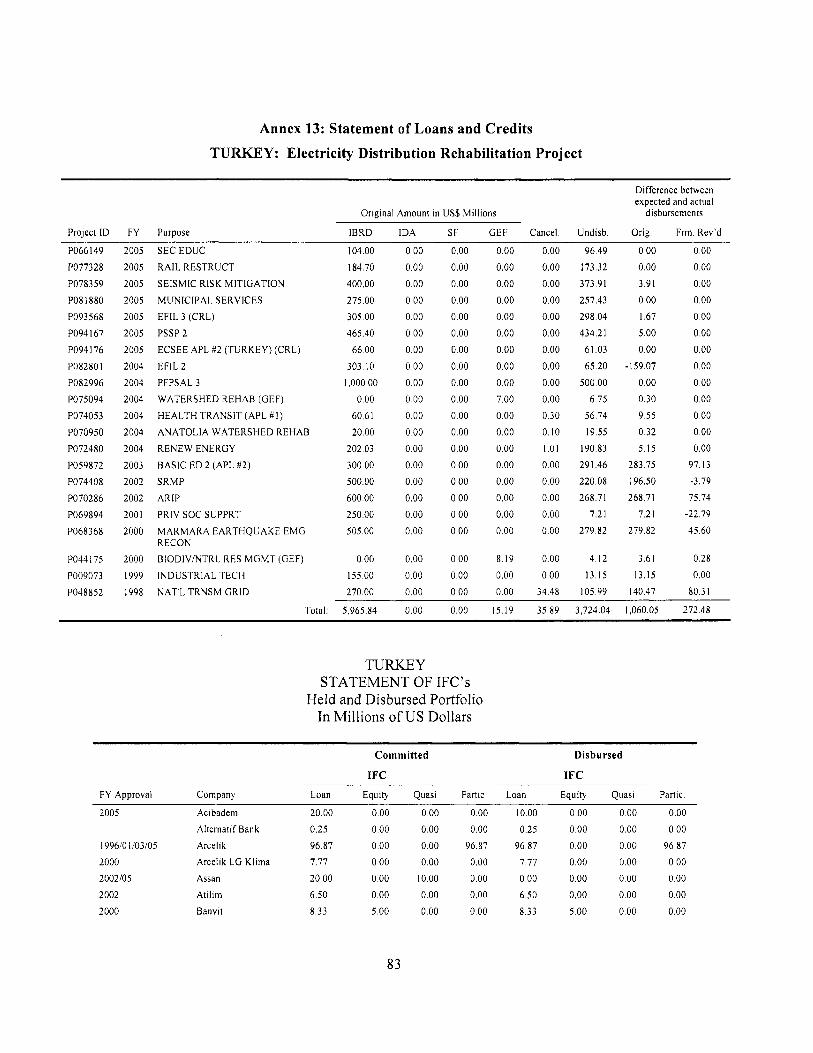

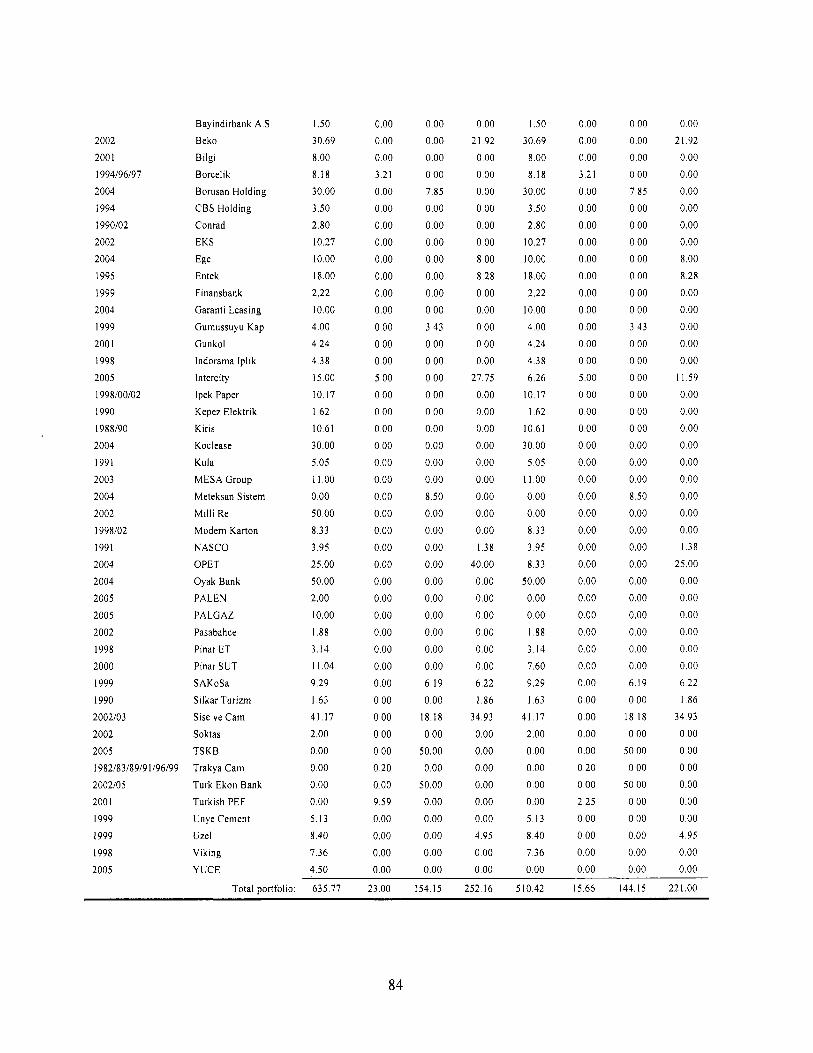

Annex 13: Statement o f Loans and Credits ............................................................................... 83

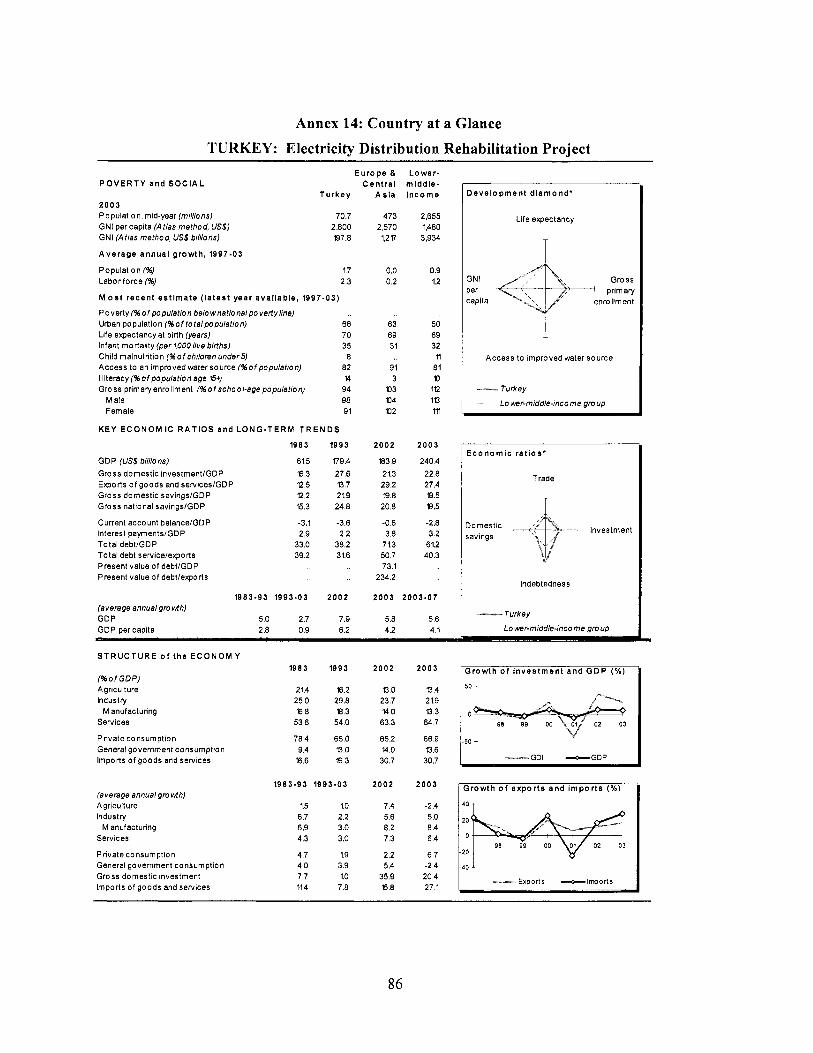

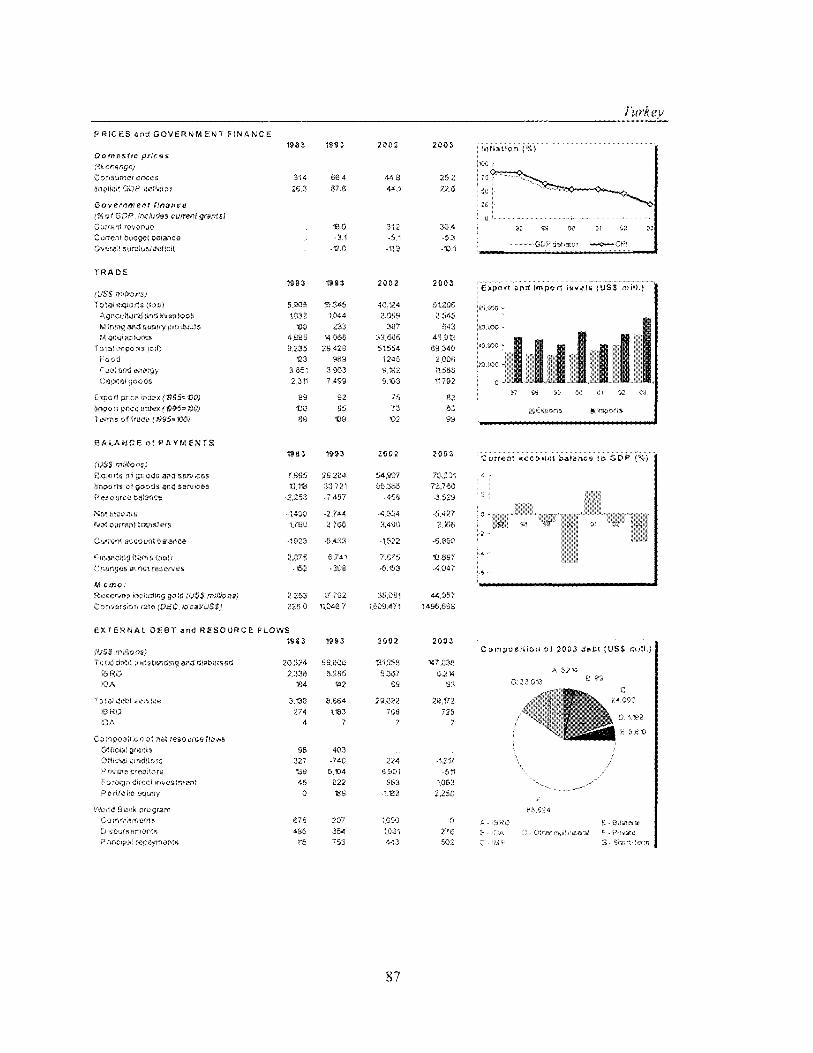

Annex 14: Country at a Glance .................................................................................................. 86

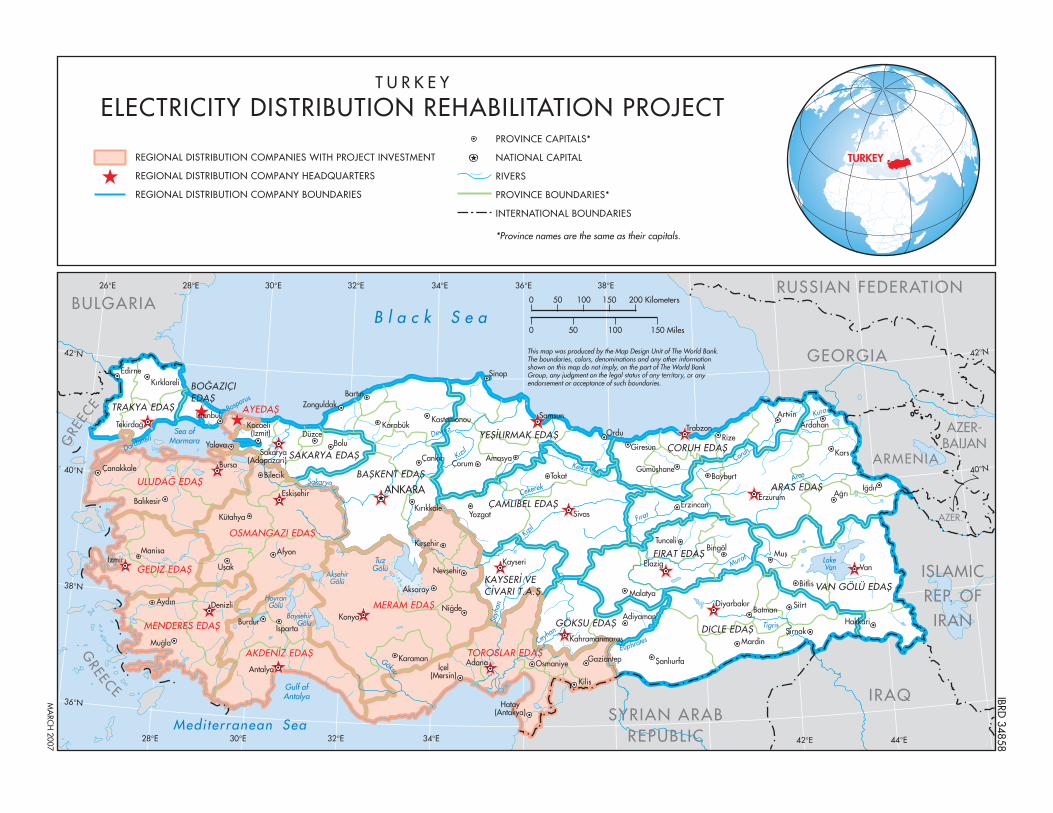

Annex 15: Map IBRD 34858 ...................................................................................................... 88

TURKEY

Source Borrower International Bank for Reconstruction and Development Total:

ELECTRICITY DISTRIBUTION REHABILITATION PROJECT

Local Foreign Total 75.00 0.00 75.00

126.90 142.50 269.40

20 1.90 142.50 344.40

PROJECT APPRAISAL DOCUMENT

EUROPE AND CENTRAL ASIA

ECSSD

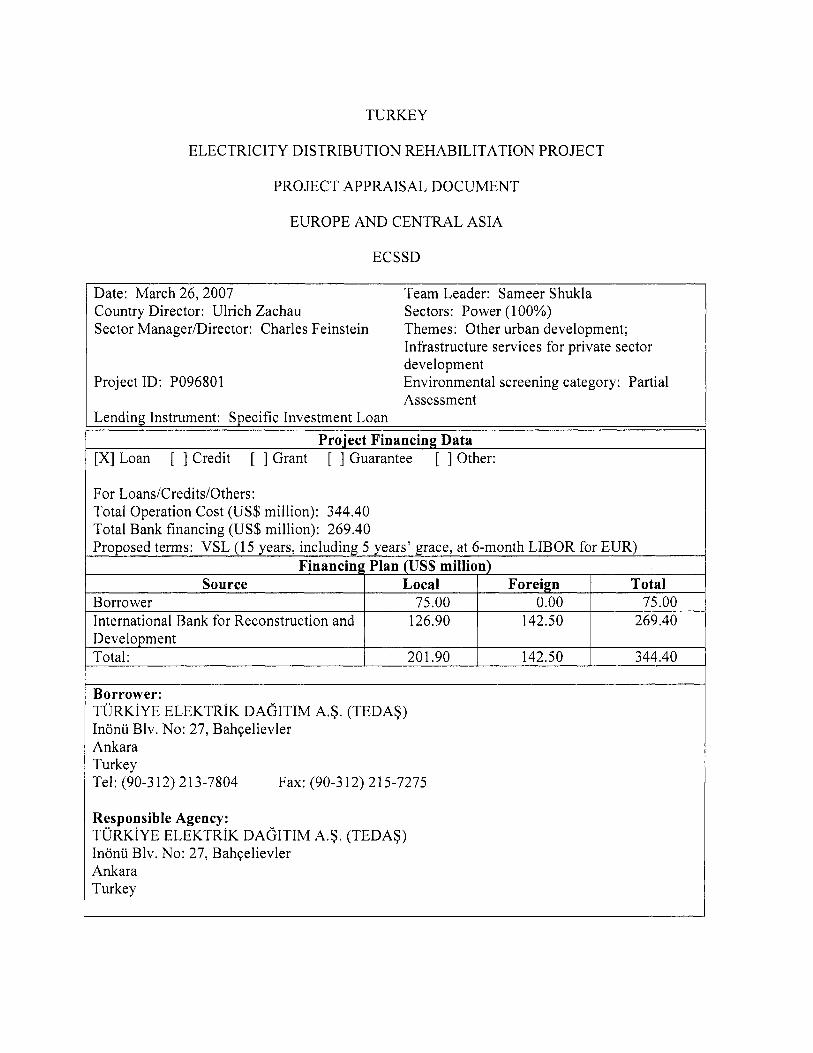

Date: March 26, 2007 Country Director: Ulrich Zachau Sector ManagerDirector: Charles Feinstein

Team Leader: Sameer Shukla Sectors: Power (1 00%) Themes: Other urban development; Infrastructure services for private sector development Environmental screening category: Partial Assessment

Project Financing Data

Project ID: PO96801

Lending Instrument: Specific Investment Loan

[XI Loan [ ] Credit [ 3 Grant [ ] Guarantee [ 3 Other:

Borrower: TURKIYE ELEKTRIK DAGITIM A.S. (TEDAS) Inonu Blv. No: 27, Bahqelievler Ankara Turkey Tel: (90-3 12) 2 13-7804 Fax: (90-3 12) 2 15-7275

Responsible Agency: TURKIYE ELEKTRIK DAGITIM A.S. (TEDAS) Inonu Blv. No: 27, Bahqelievler Ankara Turkey

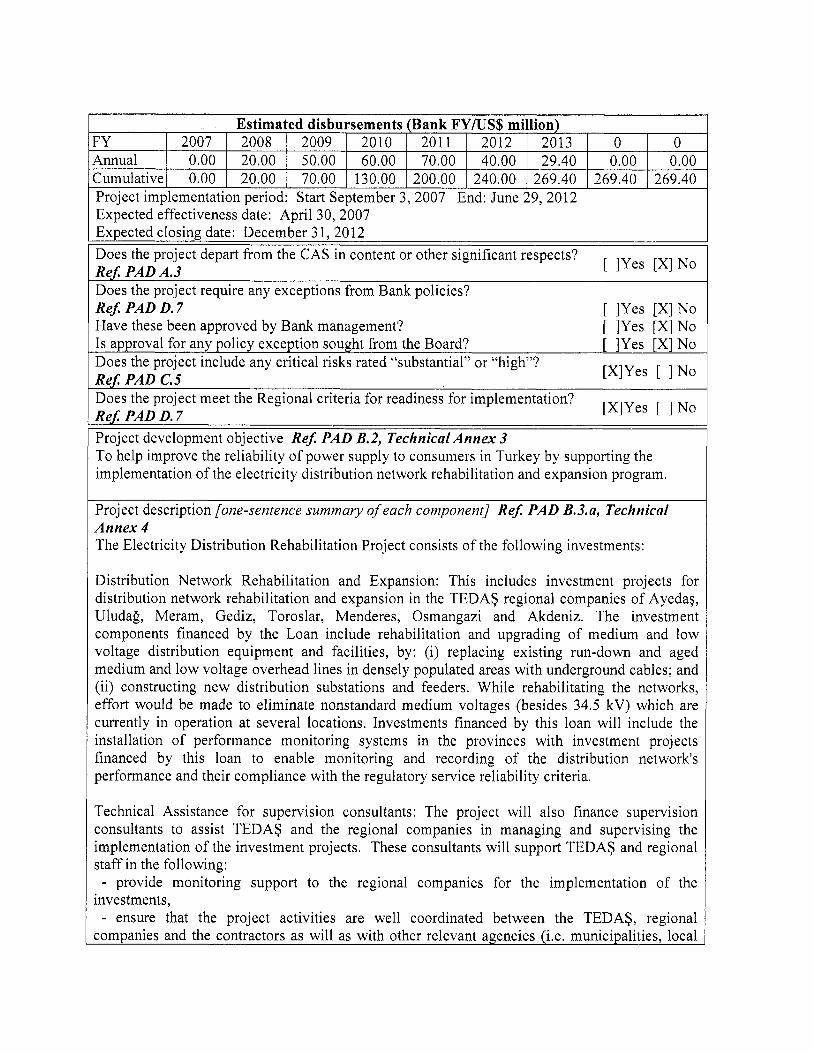

FY Annual Cumulative Project implementation period: Start September 3,2007 End: June 29,2012 Expected effectiveness date: April 30, 2007 Expected closing date: December 3 1, 20 12 Does the project depart from the CAS in content or other significant respects? Ref: PAD A.3 Does the project require any exceptions from Bank policies? Ref: PAD D. 7 Have these been approved by Bank management? I s approval for any policy exception sought from the Board? Does the project include any critical risks rated “substantial” or “high”? Ref: PAD C.5 Does the project meet the Regional criteria for readiness for implementation? Ref: PAD D. 7 Project development objective Ref: PAD B.2, Technical Annex 3 To help improve the reliability o f power supply to consumers in Turkey by supporting the implementation o f the electricity distribution network rehabilitation and expansion program.

Project description [one-sentence summary of each component] Ref: PAD B.3.a, Technical Annex 4 The Electricity Distribution Rehabilitation Project consists o f the following investments:

Distribution Network Rehabilitation and Expansion: This includes investment projects for distribution network rehabilitation and expansion in the TEDAS regional companies o f Ayedav, Uludag, Meram, Gediz, Toroslar, Menderes, Osmangazi and Akdeniz. The investment components financed by the Loan include rehabilitation and upgrading o f medium and low voltage distribution equipment and facilities, by: (i) replacing existing run-down and aged medium and low voltage overhead l ines in densely populated areas with underground cables; and (ii) constructing new distribution substations and feeders. While rehabilitating the networks, effort would be made to eliminate nonstandard medium voltages (besides 34.5 kV) which are currently in operation at several locations. Investments financed by this loan will include the installation o f performance monitoring systems in the provinces with investment projects financed by this loan to enable monitoring and recording o f the distribution network’s performance and their compliance with the regulatory service reliability criteria.

[ ]Yes [XINO

[ ]Yes [XINO [ ]Yes [XINO [ ]Yes [XINO

[XIYes [ ]No

[XIYes [ ]No

2007 2008 2009 2010 2011 2012 2013 0 0 0.00 20.00 50.00 60.00 70.00 40.00 29.40 0.00 0.00 0.00 20.00 70.00 130.00 200.00 240.00 269.40 269.40 269.40

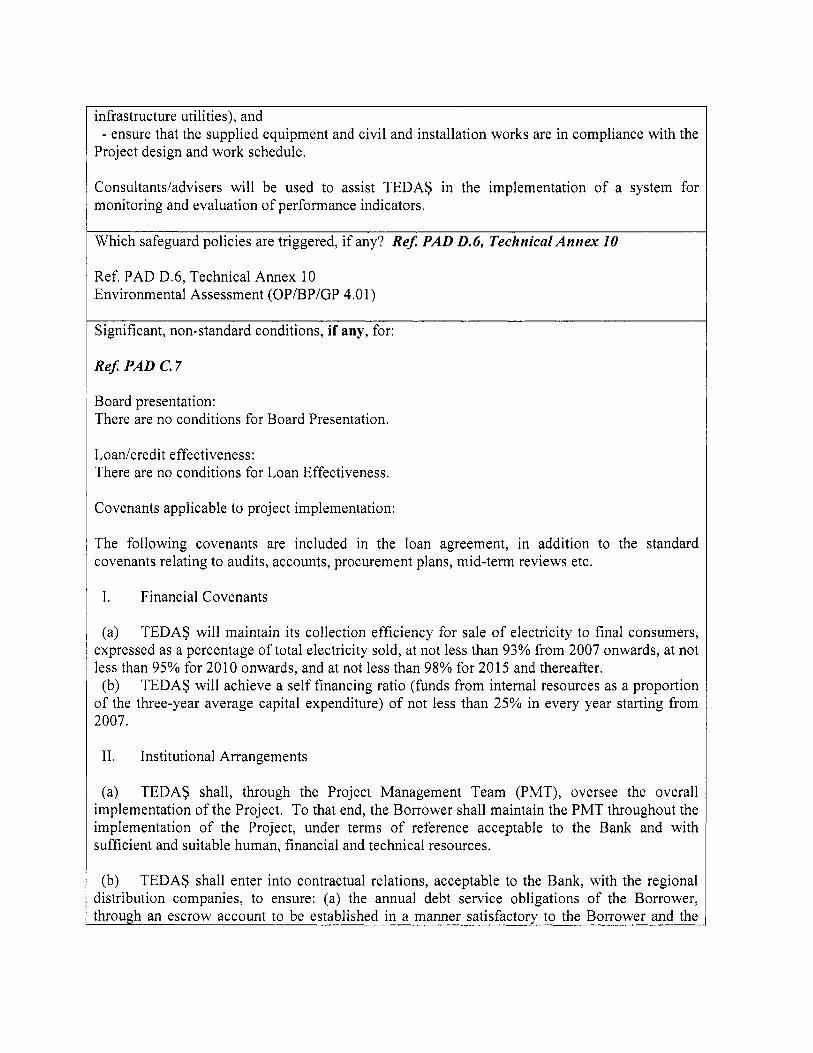

Technical Assistance for supervision consultants: The project will also finance supervision consultants to assist TEDAS and the regional companies in managing and supervising the implementation o f the investment projects. These consultants will support TEDAS and regional staff in the following: - provide monitoring support to the regional companies for the implementation o f the

investments, - ensure that the project activities are well coordinated between the TEDAS, regional

companies and the contractors as will as with other relevant agencies (Le. municipalities, local

infrastructure utilities), and

Project design and work schedule. - ensure that the supplied equipment and c iv i l and installation works are in compliance with the

Consultants/advisers will be used to assist TEDAS in the implementation o f a system for monitoring and evaluation o f performance indicators.

Which safeguard policies are triggered, if any? Re$ PAD 0 .6 , Technical Annex 10

Ref. P A D D.6, Technical Annex 10 Environmental Assessment (OP/BP/GP 4.0 1)

Significant, non-standard conditions, if any, for:

Re$ PAD C. 7

Board presentation: There are no conditions for Board Presentation.

Loadcredit effectiveness: There are no conditions for Loan Effectiveness.

Covenants applicable to project implementation:

The following covenants are included in the loan agreement, in addition to the standard covenants relating to audits, accounts, procurement plans, mid-term reviews etc.

I. Financial Covenants

(a) TEDAS will maintain its collection efficiency for sale o f electricity to final consumers, expressed as a percentage o f total electricity sold, at not less than 93% from 2007 onwards, at not less than 95% for 20 10 onwards, and at not less than 98% for 20 15 and thereafter. (b) TEDAS will achieve a s e l f financing ratio (funds from internal resources as a proportion

o f the three-year average capital expenditure) o f not less than 25% in every year starting from 2007.

11. Institutional Arrangements

(a) TEDAS shall, through the Project Management Team (PMT), oversee the overall implementation o f the Project. To that end, the Borrower shall maintain the P M T throughout the implementation o f the Project, under terms o f reference acceptable to the Bank and with sufficient and suitable human, financial and technical resources.

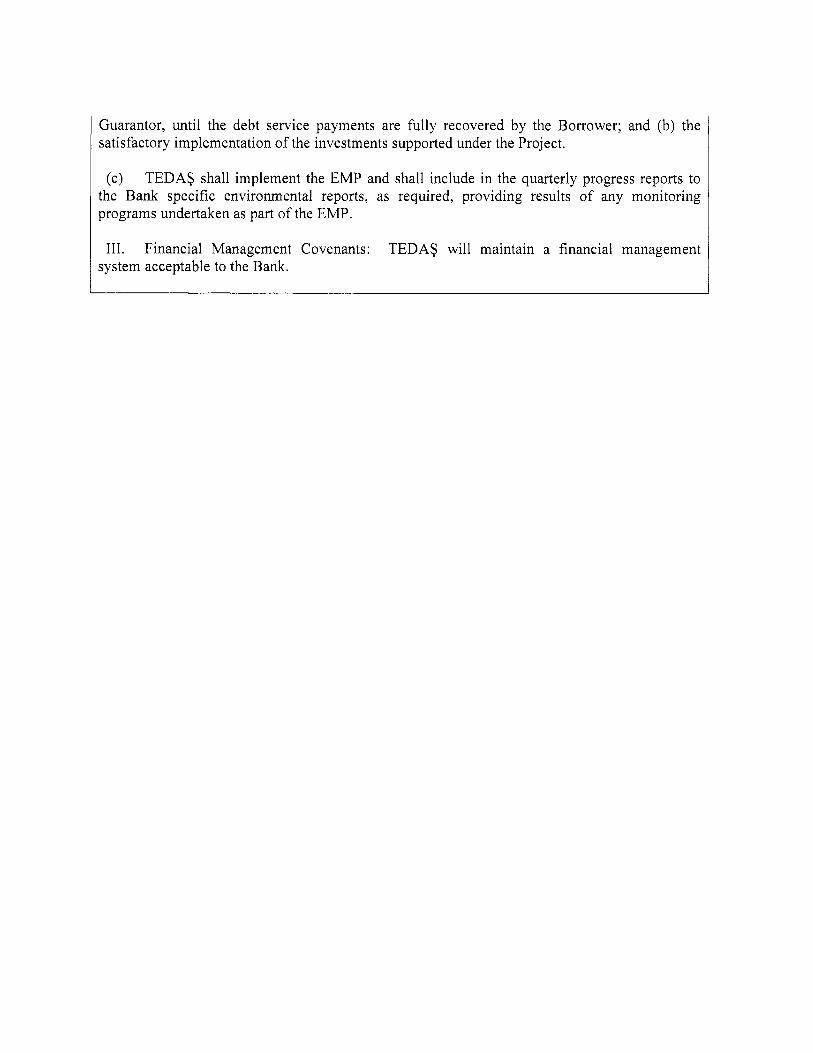

(b) TEDAS shall enter into contractual relations, acceptable to the Bank, with the regional distribution companies, to ensure: (a) the annual debt service obligations o f the Borrower, through an escrow account to be established in a manner satisfactory to the Borrower and the

Guarantor, until the debt service payments are fully recovered by the Borrower; and (b) the satisfactory implementation o f the investments supported under the Project.

(c) TEDAS shall implement the EMP and shall include in the quarterly progress reports to the Bank specific environmental reports, as required, providing results o f any monitoring programs undertaken as part o f the EMP.

111. Financial Management Covenants: TEDAS will maintain a financial management system acceptable to the Bank.

A. STRATEGIC CONTEXT AND RATIONALE 1. Country and sector issues

Country Economic Overview 8 The Turkish economy has rebounded from the 2001 crisis which had serious

economic and social impacts: by the end o f 2001, the currency had devalued by 50 percent, nominal interest rates were about 100 percent, and the banking system had virtually collapsed. GNP growth has been strong since 2001 close to 8 percent on average during the last 4 years. Inflation was also brought under control, reaching single digits in 2004 for the first time in 35 years, although i t i s expected to be around 10 percent at end-2006. Several factors contributed to the improved macroeconomic performance - key amongst them are: strong fiscal discipline which has allowed the maintenance o f a large primary surplus in the order o f 6.5 percent o f GNP; on-going structural reform; and political stability since 2002.

been an important signal to financial markets and has created a firm anchor for the country’s development and structural reforms in the years ahead, notwithstanding the fact that the process i s expected to be long and difficult.

8

The EU’s decision to open accession negotiations with Turkey in October 2005 - has

The Electricity Sector in Turkey: Transition to a Competitive, Privatized Market 8 Legislative basis - The Government has embarked upon a comprehensive reform and

restructuring program o f the electricity sector to create a liberalized, efficient and economic sector. This reform program was initiated by the Electricity Market Law (Law No. 4628) promulgated in February 2001 and reflected in the Strategy Paper accepted by the High Planning Council in March 2004, which accelerated the reform process. The principles and goals o f the reform program defined by this L a w are substantially in l ine with EC Directives (1 996/92/EC and 2003/54/EC) concerning rules for the internal market for electricity.

the EC initiated to develop the regional electricity and gas market in South East Europe and eventually integrate it with the internal electricity and gas market o f the European Union. The regional market development process commonly referred to as the “Athens process” was initiated by 2002 Athens Memorandum. The Athens Memorandum 2003 which superseded the 2002 document included provisions relating to natural gas market development. While other regional members signed the resulting Energy Community o f South Eastern Europe (ECSEE) Treaty on October 25, 2005, Turkey did not, owing to reservations on some o f the Treaty provisions. With the EU decision o f October 3, 2005 to begin negotiations for full accession, some reservations on the Treaty now become intertwined with the negotiations on the Energy Chapter o f the Acquis Communautaire. Turkey however remains committed to, and continues to implement the provisions o f the 2003 Athens Memorandum.

Market Law, TEAS, the former integrated generation and transmission corporation, was restructured into a generating corporation EUAS, a trading corporation TETAS and a transmission corporation TEIAS. TEDAS, the Government-owned distribution corporation had been earlier separated from TEAS’ predecessor, TEK. In 2004, TEDAS

ECSEE Treaty - Turkey i s a signatory o f the Athens Memoranda o f 2002 and 2003 that

8 Functional and corporate restructuring of the sector - Pursuant to the Electricity

5

was restructured into separate regional distribution companies (DISCOS) in preparation for their privatization. The generation sector i s also in the process o f being restructured into one holding company which will retain the major hydroelectric power plants, and six separate portfolios o f generation assets that wi l l be later formed into companies (portfolio companies) that would be privatized once distribution i s substantially privatized.

authority, the Energy Market Regulatory Authority (EMRA) with jurisdiction over electricity, gas, petroleum and LPG. EMRA has powers over licensing, tari f f setting and customer service issues.

G W h are considered eligible, Le., they can choose their own supplier - this represents more than 30% o f the total Turkish electricity market.

competitive bilateral contract market with a balancing and settlement system. Cash-based market operations began in August 2006, and i t i s expected that the final market structure will be in place once daily settlements supported by hourly metering i s implemented. TEIAS, the transmission company i s the independent system operator and the market operator. The market i s expected to provide the necessary price signals for potential new generation.

Independent Regulatory Framework - Turkey has set up an independent regulatory

Retail Competition in Electricity - Consumers whose annual consumption exceeds 6.0

Competitive Market Structure - Market simulations are in progress to introduce a

The Electricity Distribution Business

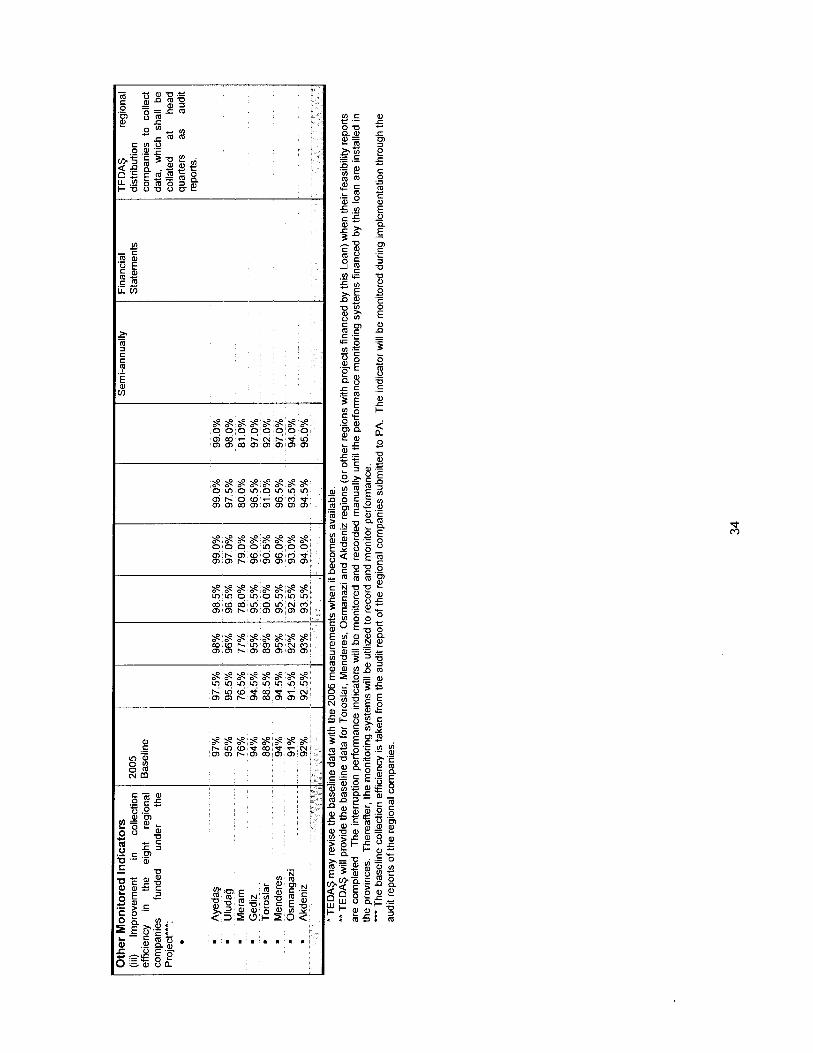

1. The electricity distribution system in Turkey i s owned by TEDAS (except Kayseri), a corporation created from the restructuring o f TEK, an integrated electricity utility, in 1993, and operated by 20 regional distribution companies under transfer o f operating rights (TOOR) contracts. TEDAS was shifted to the “privatization program ”’ o f the Privatization Administration (PA) in April 2004 and was restructured into 20 regional companies in 2005. In addition to TEDAS, eligible consumers are supplied by IPPs, autoproducers, wholesalers and other private producers. One region, Kayseri, i s operated by a separate company in which the municipality holds the largest stake. TEDAS sales made up about 75% o f total consumption o f electricity in Turkey in 2005, with the remaining attributable largely to autoproducers eligible consumers. TEDAS sold about 93 T W h in 2005 to about 28 mi l l ion consumers. About 30% o f total consumption was by industrial consumers in 2005, with residential consumers making up another 30%.

2. TEDAS estimates its system losses (technical and commercial, including theft o f electricity) at about 17.8% in 2005. Losses rose consistently from about 10.7% in 1990 to 21.6% in 2000, but have declined gradually since then, as a result o f several measures by TEDAS to improve metering and bi l l ing and curtailment o f theft. In 2004 for instance, loss detection teams set up at headquarters and in the regions inspected about 6 mi l l ion consumers and recorded 320,000 cases o f theft - this resulted in a revenue assessment o f US$ 230 mi l l ion and cash collection o f US$ 78 mil l ion. In several places, metering, bi l l ing and collections are outsourced,

The term “privatization proguam” refers to the transfer o f a state-owned enterprise to the ownership and financial oversight o f the Privatization Administration in preparation for eventual privatization, Typically, State Owned Enterprises are owned and supervised by the Undersecretariat o f Treasury.

I

6

and the outsourcing agencies are provided added incentives for theft prevention. TEDAS’ staff have also developed an internet-based system to improve retail services such as subscription, metering, billing and collections - for instance, the system enables bill payment through banks, and also facilitates consumption to be tracked to identify potential theft, remote disconnections and reconnections.

3. While TEDAS’ collection efficiency has been rising, to about 93% in 2005, arrears for sale o f electricity stood at US$ 3.5 billion at the end o f 2005. A significant part o f the arrears, about 53% o f the total, arise from non-payment by government agencies, particularly municipalities and particularly for street lighting. The Government i s however, trying various options to deal with the problem o f accumulated arrears (See Annex 9). For municipalities in particular, laws have been amended in order to enable the Government to allocate central tax devolutions through Iller Bank2, towards meeting electricity dues. The dues o f about 2500 municipalities and 8 metropolitan municipalities were reconciled and rescheduled in June 2006, and i t i s expected that from July 2006, monthly deductions from central devolutions will commence. For street lighting bills, which have been a particularly serious problem since municipalities have by and large refused to accept these bills as their responsibility, the Government has prepared amendments in related legislation to allow the use o f municipal taxes and additional electricity tax for recovery o f these dues (and future bills) over time.

4. The electricity distribution network in Turkey i s in poor condition and system reliability i s declining. Investment in the distribution sector has been constrained for over a decade and the system i s now showing signs o f this lack o f investment, with high system losses and system reliability declining over time. Between 1994 and 2003, TEDAS requested an investment budget o f US$ 7.6 billion and was allocated less than half that amount3. In about the same period, the number o f consumers increased by 9.5 million (a compounded annual growth o f 5.1%); staff strength reduced from 38,351 to 32,140 in 2004; and system losses rose from about 15.5% to 19.9%. The distribution sector also went through a phase o f poorly structured and failed privatization from 1997-2002 which exacerbated system inefficiencies, as the sector remained in limbo with very l i t t le attention being given to the physical condition o f the system. Average annual interruption levels per consumer4 are much higher than EU countries with similar climate and geography, and the performance’ o f the distribution networks in Turkey i s also below average performance amongst other EU countries. The Bank’s Investment Climate Survey6 for Turkey shows that nearly 82% o f the 1,300 firms surveyed experienced an average o f 28 power outages in 2005, leading to a loss o f more than 4% o f annual revenues. 47% o f the

Central tax and other devolutions to municipalities are routed through I ler Bank, a government-owned bank. Up to 20% o f these monthly devolutions to any particular municipality will be deducted for payments to TEDAS.

Improvement o f Operational Efficiency and Service Quality in the Electricity Distribution Grid - Feasibility Report by McKinsey for TEDAS General Directorate

See footnote ## 3 . A record o f actual energy interruptions to consumers i s not available. However, according to the distribution feeder outage records (number and durations), TEDAS approximate calculations show that unserved energy due to interruptions in some regional companies could be equivalent to as high as 8 days o f the regional company’s annual energy sales..

Losses in the distribution networks vary from about 5.0% in Bursa province to as high as 71.6% in Mardin province. Voltage drops in the distribution network could be as high as 10% during peak demand.

The Bank conducts Investment Climate Surveys (ICs) in many countries on a regular basis, with the objective o f assessing the main factors which constrain growth by manufacturing firms. The Turkey ICs covered 1,323 firms representing nearly every industry and ownership structure.

3

6

7

surveyed firms own a generator as a result. In comparison, 64% o f firms in Brazil reported having faced outages, at an average o f less than 5 outages per firm during 2005.

5. In many regional distribution companies, the urban distribution network poses a safety risk. Turkish towns and cities have urbanized rapidly, and in several places, urban housing and commercial developments have expanded with l i t t l e regard for environmental or safety considerations vis-a-vis existing distribution networks. Rapid urbanization has thus come with poorly regulated construction, and clearances between distribution overhead lines and buildings are significantly below the levels prescribed in the electricity regulations and pose serious safety risks.

Turkey’s distribution privatization strategy

6. PA’s privatization strategy i s a modified Transfer-of-Operating Rights (TOR) approach backed by a sale o f shares to private investors. In this approach, TEDAS will continue to own the assets, and wil l transfer the right to operate the distribution networks in specific regions to the relevant regional distribution companies. These distribution companies will have al l the rights that an owner would have, including the right to invest in network maintenance and expansion. These operating rights will be co-terminus with the distribution and retail licenses provided by EMRA. These distribution companies wil l then be privatized through a sale o f a majority o f the shares on a competitive basis.

7. After intense debate over the preferred privatization strategy and approach’, the relevant agencies have agreed to the strategy proposed by PA. Preparation for privatization has proceeded at a fast pace, and in September 2006, P A commenced the privatization transaction for three distribution companies - Ayedag, Bagkent and Sakarya. Key procedural and legislative requirements for commencing privatization have been completed: (i) significant amendments have been made in the Electricity Market Law (EML) No. 4628 and other relevant laws, (ii) 5- year tari f f profiles have been approved, and (iii) transition contracts between EUAS, portfolio gencos, TETAS and the distribution companies were signed in June 2006. The Law has been amended fairly significantly, most recently in M a y 2006. These amendments seek to reduce the perceived risks in the agreed privatization approach, and to make it consistent with the overall reform program. The changes include mainly provisions enabling (i) the transfer o f operating rights, (ii) tariff equalization and 5-year tari f f profiles, and (iii) transition contracts. Perhaps most significantly, the amendments further require that the 5-year transitional tariff profiles for each regional company can be changed only by the Government through a Council o f Ministers’ decree.

8. The investor will be obliged to make a pre-defined level o f investments in the network, and to demonstrate the achievement o f pre-defined performance criteria such as loss reduction, improved collection efficiency, and improved customer service. The tender documentation for the privatization will reflect the availability o f the Bank loan for the rehabilitation o f distribution systems. Upon completion, it i s expected that these investments will improve reliability and reduce energy disruptions.

The other main alternative, outright asset sale was seen to carry serious legal impediments and was hence not 7

considered feasible.

a

9 . The tariff profiles are based on the Government’s decision to maintain uniform national tariffs and to achieve a degree o f stability in the tariff level. However, future changes in either fuel prices or power purchase costs will be passed through. The tariffs also factor in the targeted performance criteria and investments required by the distribution companies.

10. Since different distribution companies have different cost structures, each distribution company will require a different tariff profile. In order to enable the implementation o f uniform tariffs, a tariff equalization mechanism i s being established. This mechanism will aim to equalize across distribution companies to ensure that they recover the revenues that they require to cover eligible costs, after factoring in performance targets. I t i s envisaged that this equalization will be done through TETAS (See Annex 9).

1 1. Prerequisites for privatization: The Government has agreed that privatization will be completed after the following elements o f market and regulatory reforms have been tested and implemented: (i) the implementation o f a balancing and settlement system on a cash-settlements basis with the multiple DISCOS and the transition contract arrangements; and (ii), the tariff equalization mechanism and 5-year tariff profiles for distribution companies. The balancing market was implemented in August 2006 and has been in operation since then. Transition contracts are in place, and are currently being fine-tuned. The tariff equalization mechanism has been finalized, and will be implemented over the next few months.

2. Rationale for Bank involvement

There are two main reasons for the Bank engaging in the Turkish electricity distribution sector:

(a) Ensuring completion of deferred rehabilitation and upgrades - The distribution sector in Turkey has postponed essential investments in upgrades and rehabilitation for several years. Two factors contributed to this. First, the distribution sector went through a five year hiatus from 1997-2002 during which attempts at privatization failed. Consequently, the expectation that the private sector would make the necessary investments was not realized. Second, the Government faced budget pressures during repeated fiscal crises and curtailed investments in the distribution sector. The government remains committed to privatizing the distribution sector, but i s against continuing to defer important distribution system investments in anticipation o f a rapid privatization. Bank engagement at this stage would assist in financing essential distribution system upgrades that can help the sector ensure reliable supply to a growing electricity demand in the country, reduce losses, meet performance criteria established by the regulator, and achieve compliance with safety regulations. Some o f the regional companies that will utilize the Bank loan may be privatized over the l i f e o f the Project. I t i s expected that since the projects are technically and economically justified, the availability o f financing for these projects will not adversely affect the privatization process.

(b) Consistency with the overall Bank support for electricity reforms in Turkey - The World Bank has played an important policy support role in the reform process. The Bank has, through PPIAF and the Spanish Trust Fund, established an expert panel that advises the Government on the adequacy o f market rules, pre-privatization preparation, vesting contract arrangements, etc. In addition, through the National Transmission Grid

9

Project (2002) - the Bank financed consulting firms to assist the implementing agencies (TEIAS, TETAS, TEDAS, EMRA). By engaging directly with TEDAS which i s currently in the portfolio o f PA, the Bank can engage more directly in finding solutions to pre-privatization issues noted above.

3. Higher level objectives to which the project contributes

12. The project i s part o f the overall support currently being provided to the electricity sector in Turkey by the Bank. Through the project, the Bank will assist in improving the distribution system in critical areas, reduce interruptions in supply, expand capacity and assist in improving the potential for privatization. Moreover, the investments will enable the distribution network to become more compliant with safety regulations. A reliable and efficient electricity distribution system i s important for Turkey’s economic growth.

13. for the period FY 2004-07 (Report No. 33995-TU, dated November 8,2005).

The Project i s consistent with the overall Country Assistance Strategy (CAS) for Turkey

B. PROJECT DESCRIPTION

1. Lending instrument

14. This project will use a Specific Investment Loan (SIL). The loan will be borrowed directly by TEDAS, under a sovereign guarantee from the Republic o f Turkey. TEDAS i s expected to use the variable spread loan (VSL) - the financial terms and arrangements will be finalized at negotiations.

2. Project development objective and key indicators

The Project Development Objective is:

T o help improve the reliability o f power supply to consumers in Turkey by supporting the implementation o f the electricity distribution network rehabilitation and expansion program.

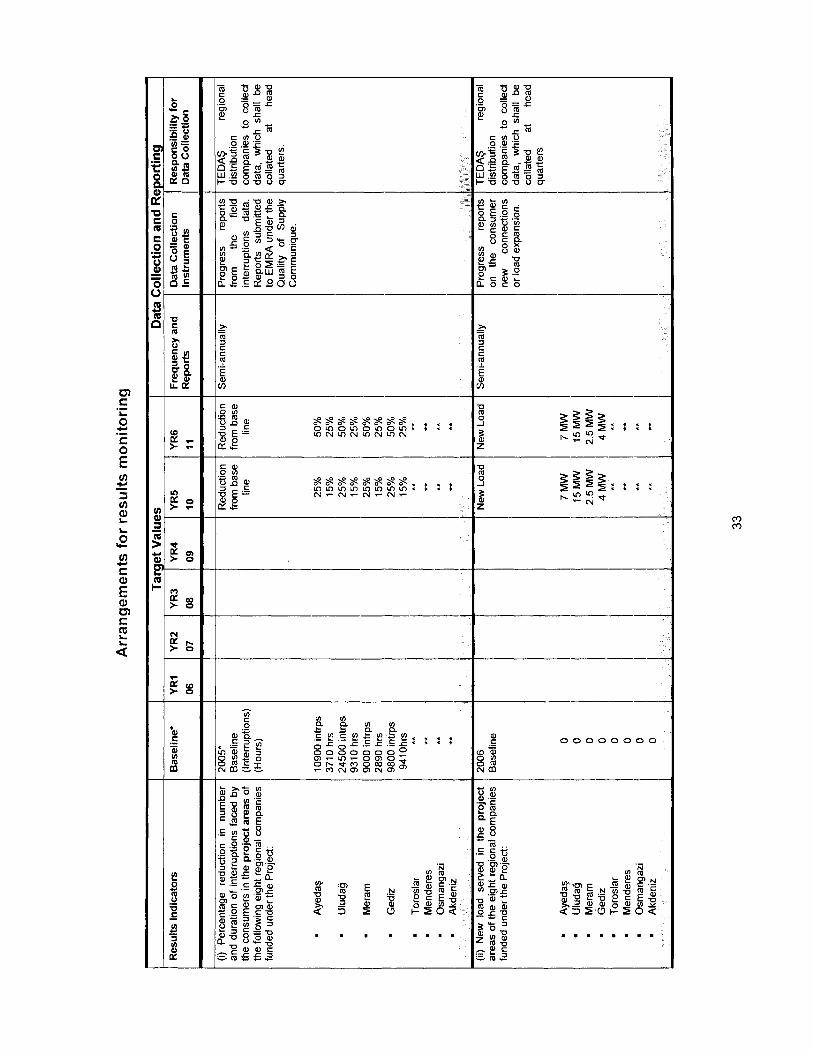

15. Achievement o f this objective would be monitored through the following indicators:

Reduction in number and average duration o f annual interruptions in power supply to consumers in the areas served by the nine regional distribution companies where investment projects are funded by the Bank project. New load served in the project areas o f the eight regional distribution companies funded under the Project. Improvement in collection efficiency in the eight regional distribution companies.

3. Project components

The Electricity Distribution Rehabilitation Project consists o f the following investments:

10

16. Distribution Network Rehabilitation and Expansion: This includes investment projects for distribution network rehabilitation and expansion in the TEDAS regional companies o f Ayedav, Uludag, Meram, Gediz, Toroslar, Menderes, Osmangazi, and Akdeniz.

17. The investment components financed by the Loan include rehabilitation and upgrading o f medium and low voltage distribution equipment and facilities, by: (i) replacing existing run- down and aged medium and low voltage overhead lines in densely populated areas with underground cables; and (ii) constructing new distribution substations and feeders. While rehabilitating the networks, effort would be made to eliminate non-standard medium voltages (besides 34.5 kV) which are currently in operation at several locations. Network rehabilitation will help reduce: distribution system losses; network operation and maintenance costs; and, supply interruptions caused by equipment and facilities outages. The conversion o f overhead lines to underground cable would also improve the safety o f the network by reducing the potential for faults and accidents - and the associated compensation payments made for material damage and loss o f l i fe . These investments will also ensure compliance with the Electricity Power Current Facilities Regulation o f 2000 which has increased the minimum allowable distance between overhead power lines and buildings.

18. Technical Assistance for supervision consultants: The project will also finance supervision consultants to assist TEDAS and the regional companies in managing and supervising the implementation of the investment projects. These consultants will support TEDAS and regional staff in the following:

0

0

provide monitoring support to the regional companies for the implementation o f the investments, ensure that the project activities are well coordinated between the TEDAS, regional companies and the contractors as well as with other relevant agencies (Le. municipalities, local infrastructure utilities), and ensure that the supplied equipment and civil and installation works are in compliance with the Project design and work schedule.

0

19. Under the project consultantdadvisers will be used to assist TEDAS in the implementation o f a system for monitoring and evaluation o f performance indicators.

A detailed description o f the project components and their scope i s presented in Annex 4,

4. Lessons learned and reflected in the project design

20. Project design, preparation and procurement have benefited from the extensive experience that the Bank has in developing large infrastructure investment operations, and specifically in rehabilitation o f generating plants and power transmission and distribution networks. These include:

(a) Detailed technical review of project feasibility The project design and scope have been developed after a detailed feasibility study o f each proposed investment. The review was supplemented by intensive field visits by Bank technical specialists to several

11

o f the provinces, where investment projects are proposed to be financed by the loan’. The Bank team was supported by an experienced engineer from Turkey. The Bank’s review assisted in assessing overall project design and the scope, and resulted in the identification o f eligibility criteria for future investments to be financed by the Bank loan. Where necessary, the Bank recommended changes in the project design and scope to meet established selection criteria.

(b) Project implementation based on Supply and Installation Contracts and Supervision of Implementation Given the large scale o f the Distribution Network Rehabilitation Program, the Bank team and TEDAS agreed that the projects will be procured and implemented using mainly supply and installation contracts to minimize the risk o f project non-completion due to any lack o f coordination and implementation capacity o f the regional companies. Furthermore, supervision o f the project implementation by the regional companies will be assisted by hiring qualified consultants.

(c) Flexibility in policy dialogue and recognition of macroeconomic priorities project will follow the overall philosophy o f addressing key energy sector priorities through a combination o f project based lending and advisory support. Lending focuses on addressing key bottlenecks (e.g. reliability, energy security, etc) and overall sector level policy dialogue on issues like electricity market implementation, sector restructuring and privatization i s continued through specific advisory and policy review activities with the Government and implementation agencies. These activities include an international expert panel that reviews reform implementation on a regular basis. These activities are financed through World Bank budget and parallel trust funds (e.g. ESMAP, PPIAF, and CTFs). This approach has proved successful in several countries (e.g. China, Vietnam, and Turkey) where lending complements a portfolio o f advisory activities that address government policy priorities and provide “how-to” implementation advice. In addition, given that Turkey i s about to commence negotiations on the EU Acquis on Energy, separate Bank conditionality in this loan was kept at a minimum.

The

5. Alternatives considered and reasons for rejection

21. As discussed in Section A.2 the investments supported under the proposed project as priority upgrades to increase system reliability that are necessary to compensate for the years o f deferred maintenance and investments in the distribution network. The Government and World Bank undertook an assessment o f whether the proposed investments should be undertaken prior to privatization. I t was determined that the investments should not await the completion of. privatization as much o f the rehabilitation and expansion work i s urgently needed to prevent the system from becoming progressively less efficient and there was no value in delaying these investments further. On this basis, the Government and TEDAS have chosen to carry out some o f the rehabilitation works in advance o f privatization. In addition, i t was anticipated that the commencement o f these investments, and the availability o f financing for them from EIB and the

Bank staff visited, or met regional staff from, the following provinces: Avanos, Nigde and Nevqehir in Meram region; Adana, Mersin and Kozan in Toroslar region; Samsun, Ordu and Amasya in Yeqilirmak region; Balikesir, Bursa and Canakkale in Uludag region; Sakarya and Kocaeli in Sakarya region; Erdine in Trakya region and Istanbul (Anatolian side) in Ayeday region.

8

12

World Bank, will enhance the attractiveness o f the beneficiary regions for their future privatization.

22. Another alternative considered was the co-financing o f the total investments o f YTL 900 million with EIB. Given the implementation and procurement difficulties associated with co- financing, i t was decided that the World Bank supported investments should be undertaken in coordination with, but separately from the EIB funded investments.

23. Once the above decisions were made, the possibility o f lending directly to the regional distribution companies was assessed. I t was determined that the regional distribution companies as affiliates o f TEDAS did not presently have the financial independence to be effective borrowers o f the World Bank loan. The necessary financial independence would be achieved only when the regional distribution companies had been privatized. I t was consequently decided to implement the project with the TEDAS holding company as the borrower o f the World Bank loan with appropriate project implementation responsibilities assigned to the regional distribution companies.

C. IMPLEMENTATION

1. Partnership arrangements (if applicable)

24. The Bank i s working closely with the European Investment Bank (EIB) which has prepared a parallel operation with the same broad objectives as this project. EIB’s project preparation and appraisal benefited from the Bank’s indepth work, and overall, the cooperation has been very productive for al l the parties involved. It i s envisaged that the Bank and EIB will continue to liaise during project implementation. In addition, PPIAF grants and the Spanish Trust Fund are being used to support the overall reform program, which also includes support for the initial work on restructuring o f generation, and preparation o f transition contracts between the generation and trading businesses.

2. Institutional and implementation arrangements

25. The project will be implemented by TEDAS and the regional companies. A Project Management Team (PMT) has been set up at TEDAS headquarters to oversee project implementation, and key staff have been identified within the regional companies to monitor the project on a more operational basis. The supervision effort will be supported through the use o f qualified consulting f i r m s / individuals to be recruited by TEDAS through the Bank loan.

26. Onlending arrangements: TEDAS will remain the Borrower for the l i f e o f the loan. TEDAS will enter into contractual agreements with the regional distribution companies, to (a) ensure the annual debt service obligations o f the Borrower, through an escrow account to be established in a manner satisfactory to the Borrower and the Guarantor, until the debt service payments are fully recovered by the Borrower; and (b) ensure the satisfactory implementation o f the investments supported under the Project.

13

3. Monitor ing and evaluation of outcomeshesults

27. The PMT and key staff from the regional companies, with the assistance o f the implementation consultants, will monitor progress against the agreed performance indicators specified in Annex 3. Besides this other indicators shall be developed with TEDAS to capture the progress on project and institutional level. The PMT will provide, on a quarterly basis, 45 days after the end o f each quarter, consolidated reports on project implementation progress in the Bank’s FMR format. The Bank will conduct regular supervision missions about once a quarter, during the initial years o f the project implementation. The PMT will prepare a detailed mid-term report to serve as the basis for a project mid-term review. The PMT will also help prepare the Borrower’s contribution to an Implementation Completion Report (ICR), so that the Bank could complete the ICR within six months o f the closing date o f the Loan. The ICR would involve a complete assessment o f project costs and benefits, project execution and performances o f the parties involved.

4. Sustainability

The project i s considered sustainable for the following reasons:

Intensive review o f feasibility and strict criteria for eligibility - The overall project concept and design has been based on a very intensive appraisal o f the existing network, the critical system requirements, and the feasibility studies prepared for specific projects. Detailed field trips with TEDAS team further refined the overall appraisal and implementation preparedness o f the sub-projects. Candidate projects in the future will have to meet strict eligibility criteria, and adequate justifications will have to be submitted in order for the projects to be considered.

Detailed ongoing supervision of project implementation - TEDAS will recruit qualified engineering consultants/ firms to assist in supervising project implementation at field level on regular basis. The Bank will supplement the supervision effort with regular visits to the field by consultants recruited specially for the purpose.

Adequate tar i f f to recover cost of investments - The tariff profiles approved by EMRA in October 2006 are expected to provide adequate margin for TEDAS and the private operating companies to recover the cost o f the rehabilitation and expansion investments. The rehabilitation investments under the project represent about 15% o f total distribution investments over the 5-year tariff period.

5. Cri t ical risks and possible controversial aspects

I Risk I Risk rating 1 Mitigation Measure 1 A. Project implementation issues

Issues due to Inadequate Institutional Capacity

M TEDAS is embarking on a large rehabilitation investment program for which it needs to allocate adequate staff and resources to manage implementation. At the same time, TEDAS itself is undergoing restructuring and privatization. The risk is proposed to be mitigated by use of qualified consultants at field to assist TEDAS and the regional companies in project supervision. Further, during project preparation, a detailed strategy for implementation has been drawn up, which includes:

14

Risk

A.2 Issues due to limited experience with World Bank Procurement Guidelines

Risk rating Mitigation Measure

H

I (1) the establishment of a team made up of TEDAS and regional staff, to ensure continuity in project management through the period of restructuring, (2) distribution network expansion and rehabilitation with the projects grouped into two to allow staggered procurement and implementation; and (3) the use of Supply and Installation contracts for project implementation to minimize delays.

TEDAS does not have experience of using the Bank’s procurement guidelines and procedures. This risk however, is likely to be at a high level for the procurement of the first group of projects and medium level for the subsequent procurements. TEDAS staffs exposure to the EIB procurement process, which has already started, is expected to assist in increased understanding of issues involved with international procurement. The Bank’s procurement staff have been providing training and significant guidance to TEDAS staff on bid preparation and tendering. Capabilities are expected to improve gradually as staff get progressively better acquainted and gain experience with procurement practices.

B. Financial issues

Overall Project Risk

B . l Lackof progress in resolution of non- payment by municipalities and street lighting

M Based on risks and the mitigation mechanisms discussed above, the overall project risk is assessed to be “Moderate”.

M-H

C . l Privatization in the absence of adequate preparation on other market reform elements

TEDAS had about US$ 3.5 billion of outstanding receivables in 2005, of which a large portion emanates from municipalities including street lighting. While it is difficult for this project to mitigate this risk entirely, the Government is working towards clearing the arrears of municipalities through various measures including legislative and budget transfer mechanisms. The related agencies are also working with MENR and the utilities to resolve the issue going forward. (See Annex 9).

H

C.2 Ambitious expectations of privatization and efficiency improvement

M-H The privatization approach includes the establishment of 5-year tariff profiles for the distribution companies based on significant efficiency improvements (Le. increased collection efficiency, loss reduction etc.) resulting from the planned privatization. Given the fact that efficiency improvements targets are aggressive, and that privatization may take longer than anticipated, there is a significant risk that cash flow problems may emerge.

There is a risk that privatization of distribution companies may proceed without the other aspects of the market reforms being suitably prepared. The privatization process has been managed by PA so far, while the other reform aspects are being implemented under the guidance of MENR. In addition, there are other significant stakeholders in the reform process, and it has not always been possible to ensure complete consistency or coordination. This may harm the market implementation process and create a negative perception with private investors. Through the expert panel’s advice and the Bank’s continued engagement at the highest levels of Government, the Bank has worked towards achieving agreement on a viable approach.

15

6. Loadcredit conditions and covenants

Other than standard requirements, there are no conditions for presentation to the Board and Loan Effectiveness.

29. Covenants in the Loan Agreement The fo l lowing covenants are included in the loan agreement, in addition to the standard covenants relating to audits, accounts, procurement plans, mid-term reviews etc.

I. Financial Covenants (a) TEDAS will maintain i t s collection efficiency for sale o f electricity to f inal

consumers, expressed as a percentage o f total electricity sold, at not less than 93% f rom 2007 onwards, at not less than 95% for 2010 onwards, and at not less than 98% for 201 5 and thereafter.

(b) TEDAS will achieve a self financing ratio (funds f rom internal resources as a proportion o f the three-year average capital expenditure) o f not less than 25% in every year starting f rom 2007.

11. Institutional Arrangements

TEDAS shall, through the Project Management Team (PMT), oversee the overall implementation o f the Project, and take necessary actions to cause the distribution companies to implement the Project after their privatization. T o that end, the Borrower shall maintain the P M T throughout the implementation o f the Project, under terms o f reference acceptable to the Bank and with sufficient and suitable human, financial and technical resources.

TEDAS shall enter in to contractual relations, acceptable to the Bank, with the regional distribution companies, to (a) ensure the annual debt service obligations o f the Borrower, through an escrow account to be established in a manner satisfactory to the Borrower and the Guarantor, until the debt service payments are fully recovered by the Borrower; and (b) ensure the satisfactory implementation o f the investments supported under the Project.

TEDAS shall implement the E M P and shall include in the quarterly progress reports to the Bank specific environmental reports, as required, prov id ing results o f any monitoring programs undertaken as part o f the E M P .

111. Financial Management Covenants TEDAS will maintain a financial management system acceptable to the Bank.

16

D. APPRAISAL SUMMARY

1. Economic and financial analysis

30. Economic analysis An economic analysis o f the proposed rehabilitation and expansion program was undertaken by the Bank, based on the feasibility studies prepared by the regional distribution companies. The feasibility studies were for the Group 1 projects in four individual regional distribution companies. These companies are Gediz, Meram, Ayedag and Uludag. The economic analysis was done for the Group 1 projects only. Feasibility studies for most o f Group 2 projects have been largely completed - the economic analyses o f these projects will be reviewed using the same assessment framework.

31. for these regional distribution companies:

There are five major economic benefits from the rehabilitation and expansion program

1.

2.

3.

4.

5.

32.

Reduction in accident risk through compliance with the new safety regulations as a result o f the rehabilitation o f distribution equipment and the replacement o f overhead distribution lines with underground cables. Although an extremely important benefit, i t cannot be fully quantified going forward. However, there have been serious accidents in the system for which compensation was paid. In the absence o f better information on the risk levels these compensation benefits have been taken as a measure o f the safety benefits o f the project. Furthermore, replacement o f overhead l ines with underground cables i s also expected to reduce the adverse impacts and supply disruption caused by ice storms and events like earthquakes. Decrease in supply interruptions as a result o f the rehabilitation and expansion program. The value o f this decrease in interruptions varies among the distribution systems depending on the level o f current interruptions. These range from the equivalent o f 2 days o f the annual electricity sales for Ayedag to around 8 days for Gediz and Uludag (Balikesir province). The value o f a 1 kWh reduction in interrupted energy supply (unserved energy) i s taken to be 0.65 YTL (equivalent to US 50 cents). Ability to serve additional load growth. The expanded and rehabilitated systems will serve new urban developments that are being built and need to be supplied. This benefit has been assessed conservatively using only identified load growth. Reduction in operating cost. The rehabilitation o f the distribution systems will reduce costs since the new underground cables will require fewer repairs than the older overhead l ines they replace. This benefit i s estimated as the reduction in materials and hired labor costs. No reduction in TEDAS direct labor cost or staff i s assumed. Reduction in system technical losses and theft. The distribution systems being rehabilitated typically have significant losses ranging from around 5% to 12% o f power supplied. As a result o f the rehabilitation, both technical losses and theft will be reduced in the project areas. The reduction in technical losses i s valued at the cost o f power purchased by TEDAS o f 0.082 YTL per kWh. The ERR calculation does not assign any economic value to the reduction in non-technical losses.

Taking into account these benefits and the net cost o f the expansion and rehabilitation program in each regional company an economic rate o f return (Em-) was calculated for each regional company program and for the four regional company programs together. The ERRS for

17

the regional company programs varied between 13% real for Ayedag to 34% real for Gediz. The composite ERR for the four companies i s 22% real. This indicates that given the benefits, especially the high cost o f supply interruptions, the distribution rehabilitation and expansion program i s quite attractive economically.

33. Financial models were constructed for both TEDAS and the seven out o f eight distribution companies which will use Bank funds’. TEDAS’ current and anticipated tariffs are sufficient to cover i t s operating costs and service any l i ke ly debt that will be procured for investments. The last tar i f f increase was in 2003, but TEDAS has been able to make modest profits o n i t s books despite the lack o f any revisions since then. In the last two years, TEDAS’ collection efficiency has improved to about 92.6% and i t s system losses have reduced to about 17.8% due to extraordinary efforts f rom TEDAS staff. TEDAS has traditionally not borrowed externally for i t s capital expenditures, and has no debt o n its books. I t has essentially deferred payments to electricity suppliers and used the credit to finance i t s activities.

Financial analysis

34. TEDAS has however had a major problem with trade receivables f rom consumers, wh ich stood at US$ 3.5 b i l l i on at the end o f 2005, representing about 15 1 days o f sale o f electricity o r about 41% o f sales (total o f trade and other receivables). The problem stems primari ly f rom municipalit ies and government agencies which make up about 40% o f total receivables. Poor collection f rom the public sector i s the most significant risk in the cash f lows o f TEDAS. The Government i s evaluating various options to address this problem, including legislation to enable deduction o f central devolutions to municipalities. Some o f these measures are expected to be enforced f rom July 2006 onwards.

35 . The forecasts are based o n conservative assumptions. Collections and system losses are expected to improve only gradually, at a more conservative pace than i s currently assumed in the 5-year ta r i f f profiles. Tarif fs are forecast to remain stable except for passing through power purchase cost increases over the next 5 years, and thereafter increase marginally. The 5-year tariff profi les also provide for the agreed investment program (including the Bank-financed portions), and for the recovery o f debt servicing and other l iabil i t ies associated with the program. As Annex 9 shows therefore, while prof i tabi l i ty i s forecast to remain robust, the cash f lows remain particularly sensitive to risks o f continued non-payment by government agencies.

36. The risk to cash flows i s clearer f rom the forecasts for the 7 distribution companies”. In the case o f 3 companies - Toroslar, Meram and Osmangazi - cash f lows are l i ke ly to continue to be affected by poor collection efficiency. Sensitivities done to simulate the impact o f improved collections however show that the three companies turn around in the medium term, and begin generating adequate levels o f cash. The problem o f collections arises mostly f rom street lighting in the case o f most companies. In the case o f Meram, Toroslar and Gediz, collections f rom agricultural consumers are an additional problem - in the case o f Meram, agriculture dues are the more serious problem, accounting for about 40% o f total receivables o n the company’s books in 2005.

The regional companies o f Akdeniz wi l l be analyzed when the feasibility studies o f these companies are made available to the Bank.

The forecasts are based on assumptions made by Bank staff and past data t i l l 2005 received from TEDAS, and do not represent official forecasts. For reasons o f confidentiality, due to the ongoing privatization transaction, the detailed financial forecasts for the distribution companies are not being disclosed. The regional company o f Akdeniz wi l l be analyzed when the feasibility study and financial data o f this company are made available to the Bank.

I O

18

37. The other four companies are forecast to be able to manage their financial requirements reasonably comfortably with minimal increases in tariffs in the later years. Most o f these companies are also forecast to begin paying down their accounts payable by the end o f the forecast period.

3 8. In summary, i t appears that under conservative assumptions on collection efficiency, some o f the distribution companies may require continued cash support from the Government. As has happened in the past, most recently in March 2006, the Government has injected cash into TEDAS in order to enable payment o f power purchase bills to TETAS. This may create some residual risk for the tariff equalization mechanism, which would in turn create cash flow problems for TETAS, which i s expected to operate the equalization mechanism.

2. Technical

39. TEDAS has implemented investment projects o f a similar nature with acceptable standards o f quality. While there has been exposure and attempt to introduce modern technologies in the electricity distribution area to improve service standards and reduce losses, these efforts have been budget constrained. TEDAS companies have well-qualified staff to do the design engineering, planning and implementation o f the investment components under the project. The project will employ modern technological practice in rehabilitating the distribution networks including (i) utilizing underground cabling technology to replace rundown overhead electric l ines in urban areas, (ii) replacing old equipment with more efficient and standard equipment, and (iii) continuing the phasing out o f non-standard medium voltages to provide more reliable and eff icient operation o f the distribution system and to minimize the costs o f network maintenance and future expansion. The Bank team reviewed the feasibility reports for the identified investment projects in four regions (Ayedag, Uludag, Meram and Gediz) included in Group 1” o f projects planned for procurement and implementation. The preparation o f the feasibility reports for other projects proposed for financing by the Loan as part o f project Group 2 i s under way. The Bank team also carried out detailed technical field visits, supported by an experienced consultant and TEDAS’ design and planning team in some cases, and these visits assisted significantly in assessing the technical viability o f the proposed projects. In several cases, the Bank team suggested, and TEDAS agreed, on changes to the project design and/or scope, to increase the viability and sustainability o f the projects.

40. Criteria fo r future projects:TEDA$ and the Bank have reached agreement on the overall design philosophy for the investment components based on the reviews and completion o f the feasibility studies for Group 1 projects. The agreed design philosophy will be applied to future projects in Group 2. TEDAS will have the flexibility to add or remove projects currently being prepared for Group 2, as long as proposed projects are economically justified and comply with the following eligibility criteria agreed during appraisal:

(a) Underground conversion and network expansion investment pro jects in large c i t ies selected for safety reasons, because o f the need for compliance with clearance regulations, or for increased load growth. Large ci t ies with buildings and structures close to existing overhead lines, and where load growth i s likely are ideal candidates for these investments.

Annex 4 contains the detailed description o f projects included in Group 1, and potential projects for Group 2. I I

19

(b)

(c)

Investment to continue the ongoing replacement o f non-standard medium-voltages by the standard medium voltage o f 34.5 kV. Investment projects aimed at improving system control and at reducing system losses and energy interruptions in provinces or distribution systems with high losses and energy interruptions.

41. The main technical issue anticipated by the team i s the implementation capacity o f TEDAS to simultaneously undertake investments at much larger levels than in the last five years. The team has agreed with TEDAS on several steps to mitigate risk on this account (also see Annex 6). These steps include:

(a) identification o f key members at the regional level and at headquarters for implementation o f the project,

(b) supply and installation contract packaging to reduce the coordination responsibilities and risks o f project non completion, and

(c) recruitment o f qualified consultants to support TEDAS in implementation and monitoring o f the projects.

3. Fiduciary

42. A procurement capacity assessment carried out by the Bank found that TEDAS staff have limited experience o f the Bank’s procurement rules. Bank Staff have been working intensively with TEDAS staff training them in Bank procurement. Furthermore, TEDAS staff are preparing procurement documents according to Bank rules and these documents are expected to be ready by the time o f Board presentation.

43. The Bank’s review o f TEDAS’ financial management arrangements has also been undertaken and they were found to be generally satisfactory. The financial management arrangements o f the project are therefore acceptable to the Bank, subject to the installation o f a project budgeting and accounting system. The annual audited project and entity financial statements wil l be provided to the Bank within six months o f the end o f each fiscal year, and project financial statements wil l be provided also at the closing o f the project. Financial statements for TEDAS and regional companies will be audited by an auditor acceptable to the Bank.

44. TEDAS and the regional companies will produce a full set o f interim unaudited financial reports (IUFRs or Financial Monitoring Reports - FMRs) for each calendar quarter throughout the l i f e o f the project. The reporting i s based on TEDAS’ own reporting systems. The project will use transaction based disbursements.

45. commercial bank acceptable to the Bank.

The designated account (DA) for administering the project funds will be opened in a

4. Social

46. The population o f each o f the respective areas wil l benefit from these projects. Existing electricity users wil l experience fewer accidents and safety risks as well as more reliable electricity supply; and consumers in expansion areas wil l immediately gain from the reliable

20

distribution network. In several places, the existing overhead lines are hazardous and inconveniently located, due to inadequately planned investments. Three o f the companies reported approximately 180 accidents during the last year, including one fatality, for which they paid more than 500,000 YTL in compensation. The incidence o f accidents i s expected to decrease markedly in project areas. There will be some temporary inconvenience as the overhead lines are buried in the streets but this should be minor. Underground cabling and rehabilitation o f the network i s expected to improve the reliability and safety o f electricity supply in the areas during normal operation, but also during calamities like storms and earthquakes. These investments are also expected to enable the regional companies to serve more loads. Electricity tariffs may increase over time in order to cover r ise in costs, and with better efficiency, bill collections should increase and illegal connections should decrease. Tariffs however are not expected to r ise due to the project. N o land acquisition i s expected, as the underground cables will be located under public land (streets, sidewalks).

5. Environment

47. The environmental benefits significantly outweigh any potential environmental drawbacks. The environmental benefits consist o f removing a large number o f the wires on city streets which are unsightly and lead to accidents for people, birds and animals. The scrap material obtained from the removal o f these wires and any distribution substations will be recycled. Environmental Management Plans have been prepared for each o f the regional rehabilitation and expansion programs. The Project i s classified as an Environment Category B, because o f i t s limited environmental impact.

6. Safeguard policies

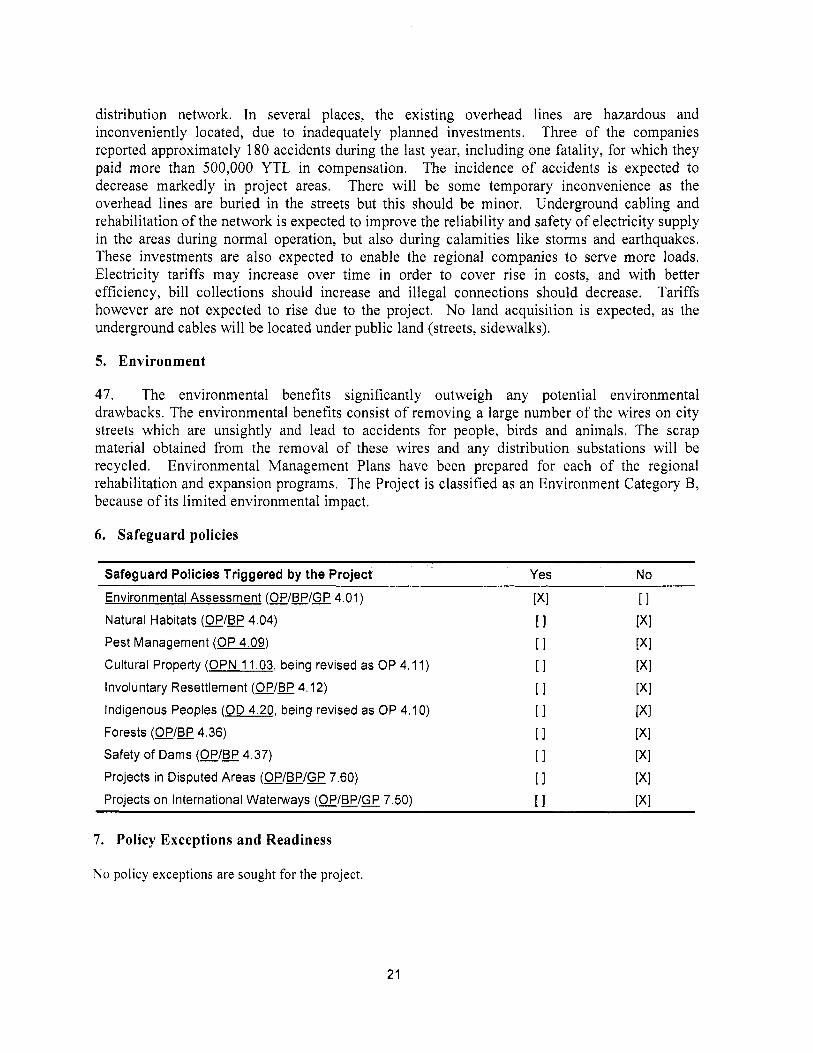

Safeguard Policies Triggered by the Project Yes No

Environmental Assessment (OP/BP/GP 4.01) [XI [ I Natural Habitats (OP/BP 4.04) [I [XI

Pest Management (OP 4.09) [ I [XI Cultural Property (OPN 11.03, being revised as OP 4.1 1) [ I [XI

Involuntary Resettlement (OP/BP 4.12) [ I [XI Indigenous Peoples (OD 4.20, being revised as OP 4. IO) 11 [XI

Forests (OP/BP 4.36) [ I [XI

Safety of Dams (OP/BP 4.37) [ I [XI

Projects in Disputed Areas (OP/BP/GP 7.60) [ I [XI

Projects on International Waterways (OP/BP/GP 7.50) [I [XI

7. Policy Exceptions and Readiness

N o policy exceptions are sought for the project.

21

Annex 1: Country and Sector o r Program Background

TURKEY: Electricity Distribution Rehabilitation Project

Country Economic Overview I T h e Turkish economy has rebounded from the 2001 crisis which had serious

economic and social impacts: by the end o f 2001, the currency had devalued by 50 percent, nominal interest rates were about 100 percent, and the banking system had virtually collapsed.

years. Inflation was also brought under control, reaching single digits in 2004 for the first time in 35 years, and was 9.8 percent at end-2006.

amongst them are: strong fiscal discipline which has allowed the maintenance o f a large primary surplus in the order o f 6.5 percent o f GNP; on-going structural reform; and political stability since 2002.

been an important signal to financial markets and has created a firm anchor for the country’s development and structural reforms in the years ahead, notwithstanding the fact that the process i s expected to be long and difficult.

I GNP growth has been strong since 2001 close to 8 percent on average during the last 4

Several factors contributed to the improved macroeconomic performance - key I

I T h e EU’s decision to open accession negotiations wi th Turkey in October 2005 - has

The Electricity Sector in Turkey: Transition to Competitive, Privatized M a r k e t Legislative basis - The Government has embarked upon a comprehensive reform and restructuring program o f the electricity sector to create a liberalized, efficient and economic sector. This was initiated by the Electricity Market Law (Law No. 4628) promulgated in February 2001 and reflected in the Strategy Paper accepted by the H igh Planning Council in March 2004, which accelerated the reform process. The principles and goals o f the reform program defined by this Law are substantially in l ine with EC Directives (1 996/92/EC and 2003/54/EC) concerning rules for the internal market for electricity.

the EC initiated to develop the regional electricity and gas market in South East Europe and eventually integrate i t with the internal electricity and gas market o f the European Union. The 2002 Athens Memorandum initiated the regional market development process commonly referred to as the “Athens process”. With the inclusion o f natural gas, a more detailed version o f the memorandum was signed, which i s referred to as the Athens Memorandum 2003, and supersedes the 2002 document. While other regional members signed the Treaty on October 25, 2005, Turkey did not, owing to reservations on some o f the Treaty provisions. With the EU decision o f October 3, 2005 to begin negotiations for full accession, some reservations on the Treaty now become intertwined with the negotiations on the Energy Chapter o f the Acquis Communautaire. Turkey however remains committed to, and continues to implement the provisions o f the 2003 Athens Memorandum.

the former integrated generation and transmission corporation, was restructured into a generating corporation EUAS, a trading corporation TETAS and a transmission corporation TEIAS. TEDAS, the Government-owned distribution corporation had been earlier separated from TEAS’ predecessor, TEK. In 2005, TEDAS was restructured into

I E C S E E Treaty - Turkey i s a signatory o f the Athens Memoranda o f 2002 and 2003 that

I Functional and corporate restructuring of the sector - Pursuant to the Law, TEAS,

22

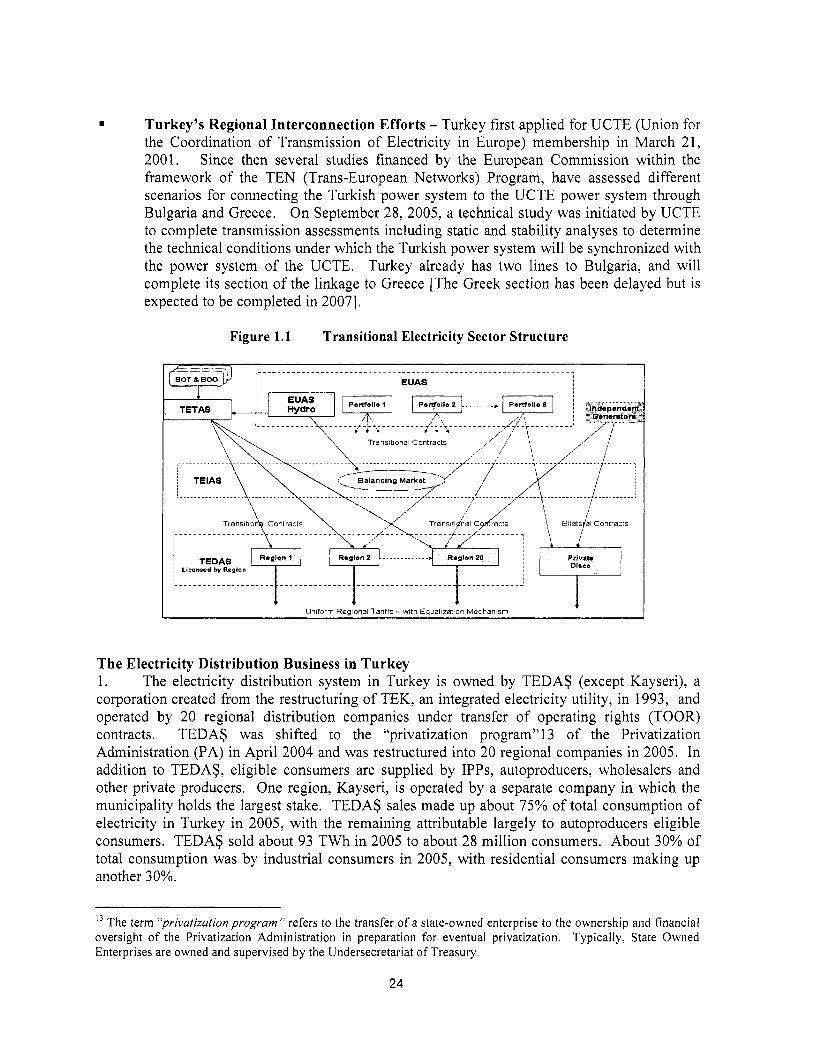

separate companies (DISCOS) in preparation for their privatization. The generation sector i s also in the process o f being restructured into one holding company which will also retain the major hydroelectric power plants, and six separate portfolios o f generation assets that will be later formed into companies (portfolio companies) that would be privatized once distribution i s substantially privatized. See Figure 1.1 below on the currently planned transitional sector structure.

authority, the Energy Market Regulatory Authority (EMRA) with jurisdiction over electricity, gas, petroleum and LPG. EMRA has powers over licensing, tariff setting and customer service issues. EMRA i s currently involved in setting multi-year tariff principles for the distribution business, and a tariff equalization mechanism across regions in order to enable national uniform retail tariffs. The Law was amended in May 2006 to allow uniform national tariffs and to enable an equalization mechanism. EMRA has also conducted the expansion o f gas distribution reasonably successfully over the last few years, through tendering procedures run by itself.

distribution companies in phases over the next two years. The regional companies have been created in preparation for privatization, and in September 2006, PA commenced the privatization transaction for three distribution companies - Ayedag, Bagkent and Sakarya. This process has been delayed from the original timeline since Turkey i s keen to avoid a repeat o f earlier difficulties in privatization'2.Turkey also plans to privatize i t s existing generating assets, once a substantial part o f the distribution business i s privatized. The configuration o f the generation portfolio companies has been decided, and EUAS will be restructured into 7 companies, one o f which will be the holding company retaining the large hydroelectric projects and i s not expected to be privatized in the medium term.

GWh can choose their own supplier - this represents more than 30% o f the total Turkish electricity market.

competitive bilateral contract market with a balancing and settlement system. Cash-based market operations began in August 2006, and, when fully implemented, the Turkish electricity market will consist o f an organized Day-Ahead market operated by TEIAS as Market Operator, a real-time system balancing and operational mechanism operated by TEIAS as the Transmission System Operator, and a bilateral contracts market. In addition, there will be one or more organized markets for procurement o f ancillary services. The market i s currently operating in a transition phase with day-ahead scheduling and real time balancing o f energy. In December 2007, the final balancing market i s expected to become operational. The current practice o f monthly settlements with three metering periods i s expected to move eventually to daily settlements supported by hourly metering.

operator. The market i s expected to provide the necessary price signals for potential new generation.

I Independent Regulatory Framework - Turkey has set up an independent regulatory

Privatization of Distribution and Generation - Turkey's plan i s to privatize its

I Retail Competition in Electricity - Consumers whose annual consumption exceeds 6.0

Competitive Market Structure - Market simulations are in progress to introduce a I

I TEIAS, the transmission corporation i s the independent system operator and the market

Turkey attempted to privatize distribution in the 1998-2000, but the process was challenged in Court and the I 2

transactions resulted in being cancelled.

23

Turkey’s Regional Interconnection Efforts - Turkey first applied for UCTE (Union for the Coordination o f Transmission o f Electricity in Europe) membership in March 21, 2001. Since then several studies financed by the European Commission within the framework o f the TEN (Trans-European Networks) Program, have assessed different scenarios for connecting the Turkish power system to the UCTE power system through Bulgaria and Greece. O n September 28, 2005, a technical study was initiated by UCTE to complete transmission assessments including static, and stability analyses to determine the technical conditions under which the Turkish power system will be synchronized with the power system o f the UCTE. Turkey already has two lines to Bulgaria, and will complete its section o f the linkage to Greece [The Greek section has been delayed but i s expected to be completed in 20071,