Embed Size (px)

Citation preview

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 48331-TH

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED

PUBLIC SECTOR REFORM DEVELOPMENT POLICY LOAN (PSRDPL)

IN THE AMOUNT OF US$1BILLION

TO THE

KINGDOM OF THAILAND

OCTOBER 21, 2010

Poverty Reduction and Economic Management Unit East Asia and Pacific Region

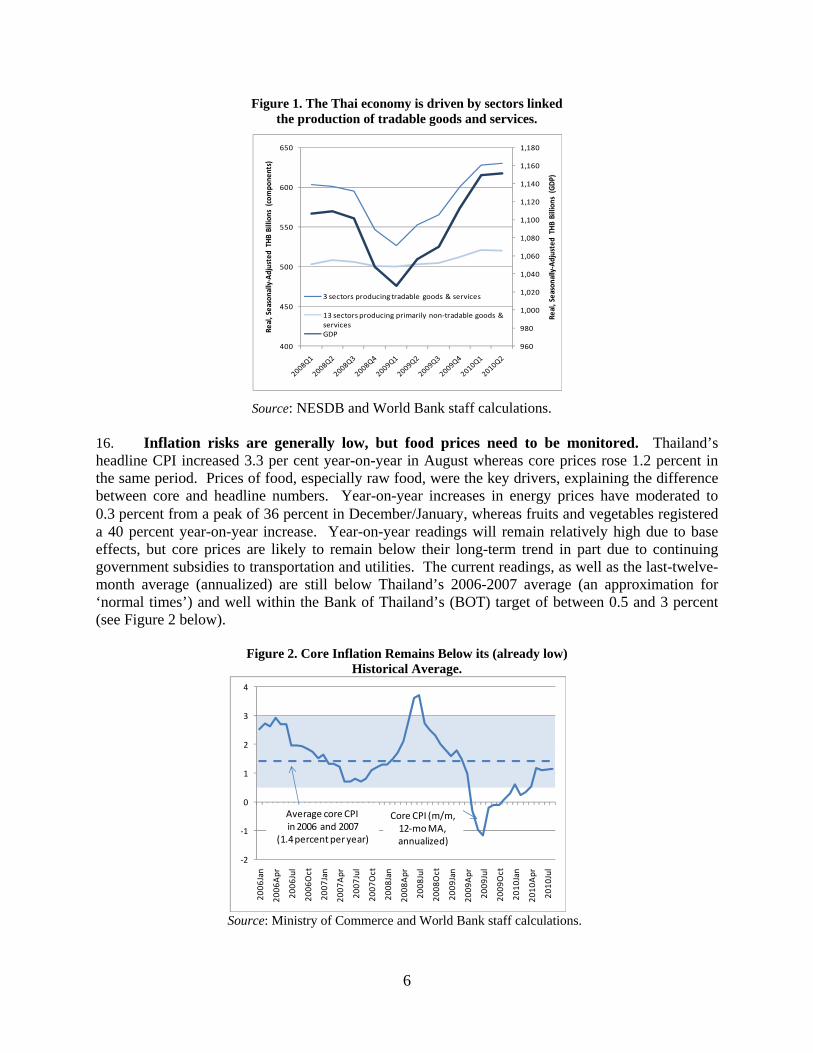

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

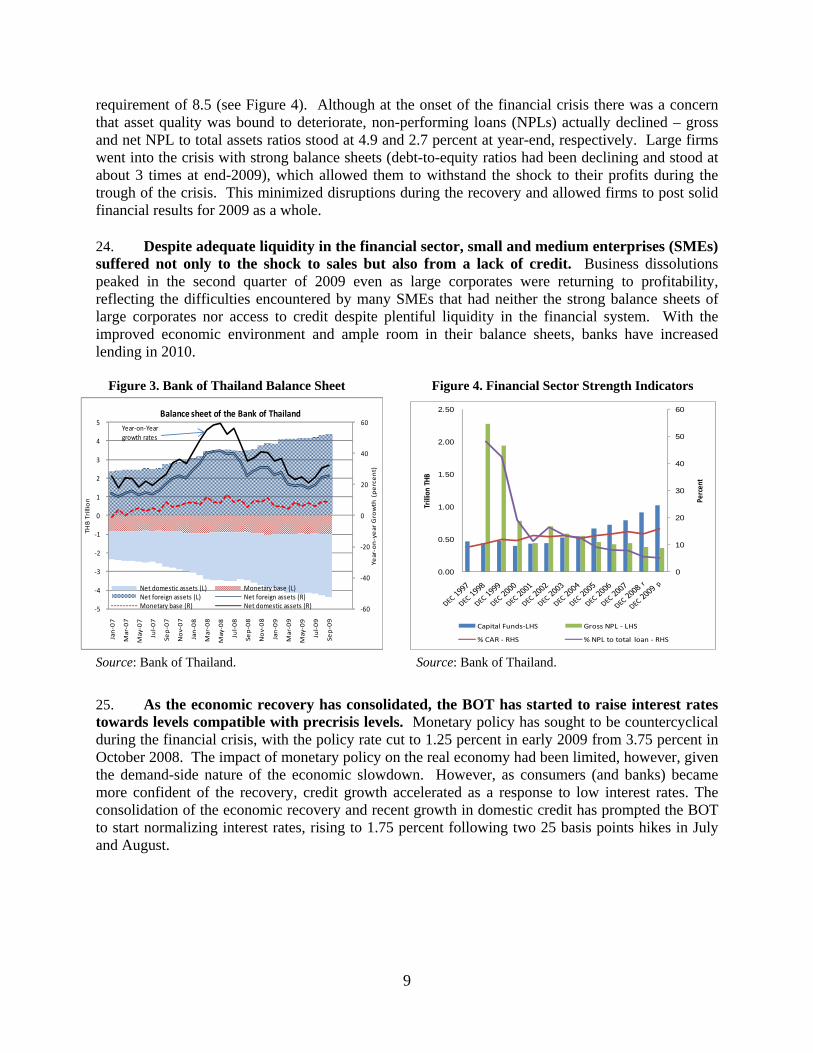

lic D

iscl

osur

e A

utho

rized

Pub

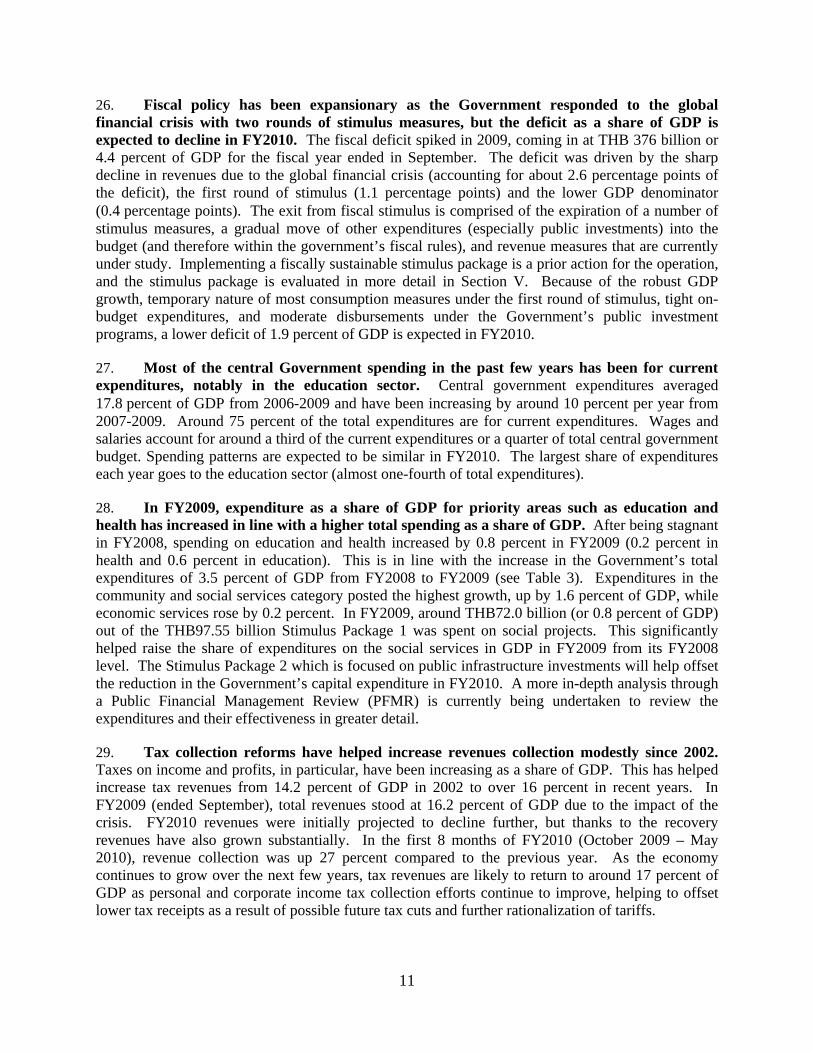

lic D

iscl

osur

e A

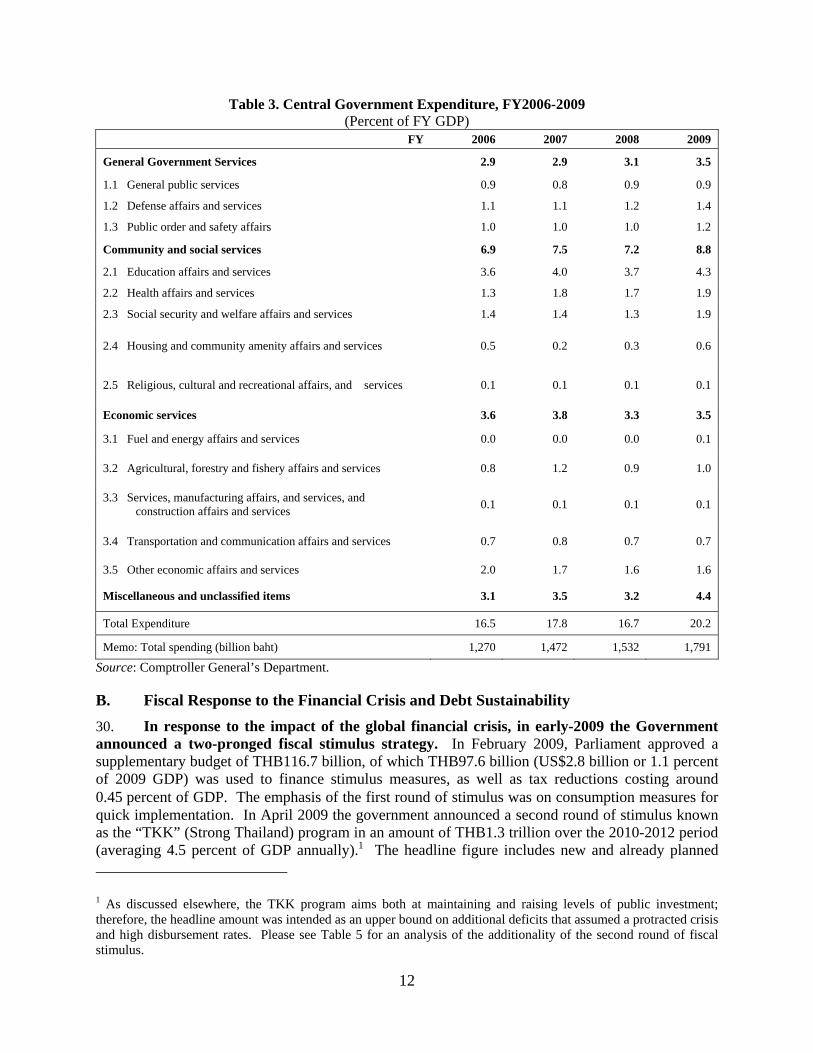

utho

rized

Pub

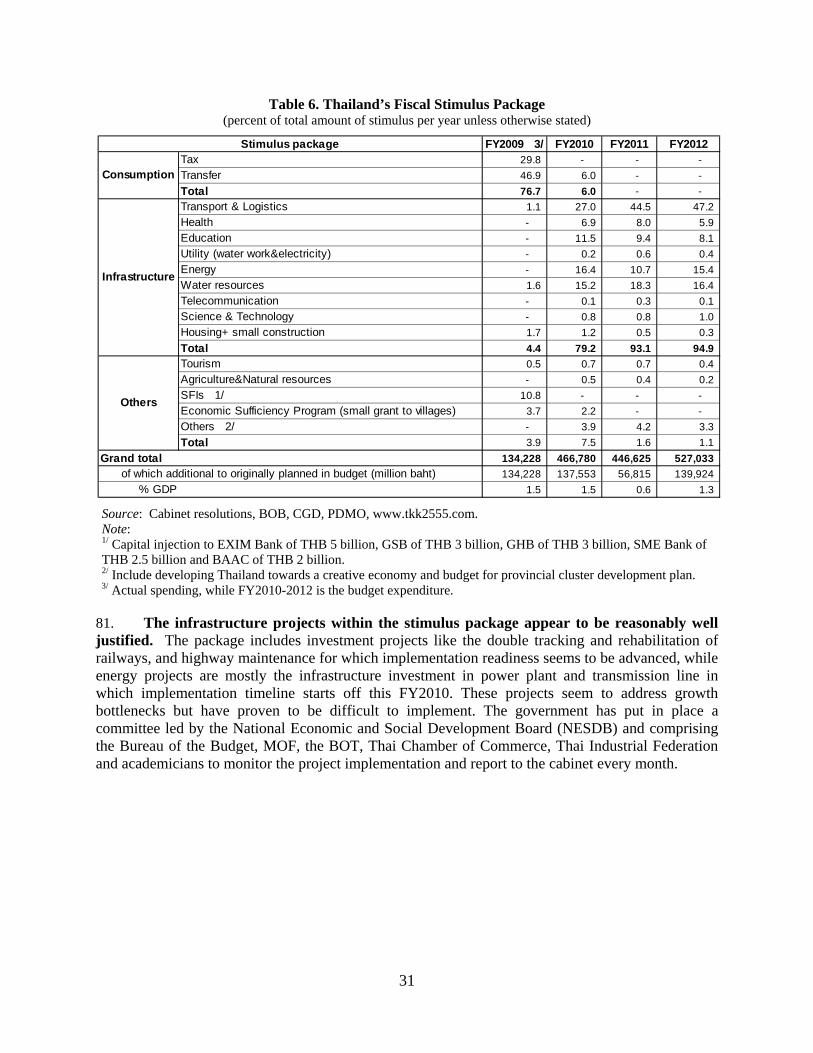

lic D

iscl

osur

e A

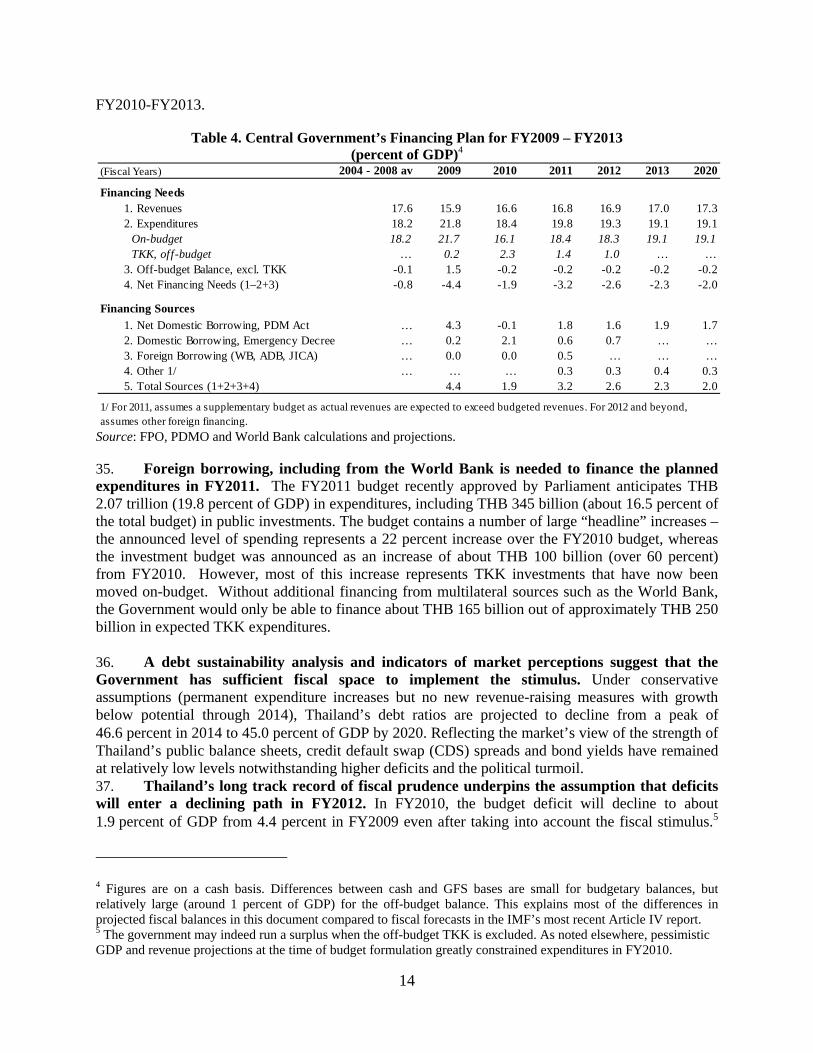

utho

rized

Pub

lic D

iscl

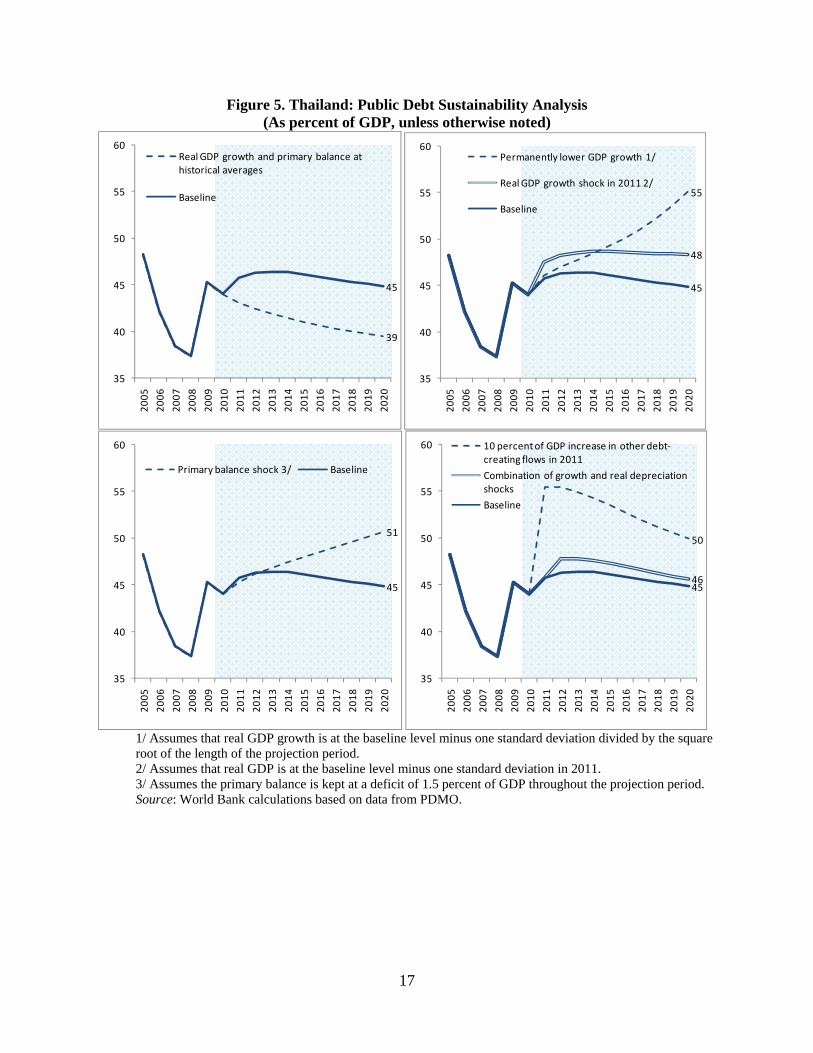

osur

e A

utho

rized

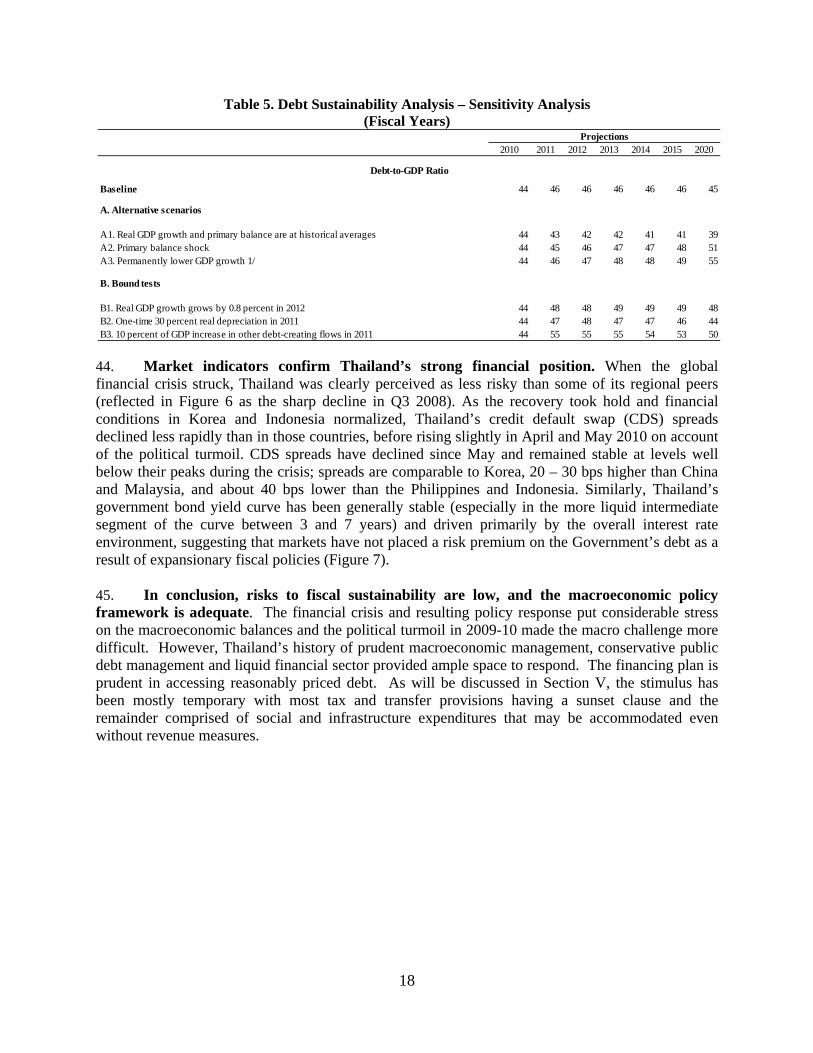

Pub

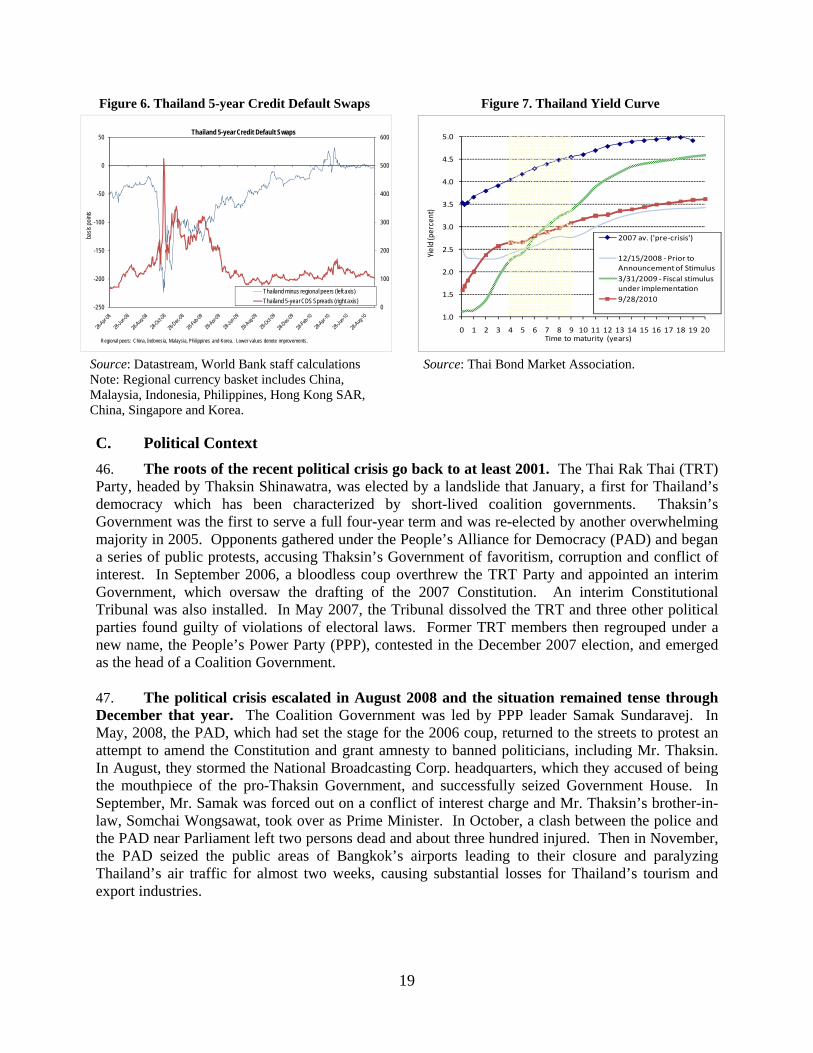

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

GOVERNMENT FISCAL YEAR October 1 – September 30

CURRENCY EQUIVALENTS (Exchange Rate Effective as at October 2010)

Currency Unit Thai Baht (THB)

US$1.00 29.89

ABBREVIATIONS

ADB Asian Development Bank NESDB National Economic and Social Development Board

BOB Bureau of the Budget OAG Office of the Auditor General’s BOP Balance of Payments OCSC Office of the Civil Service Commission BOT Bank of Thailand OPDC Office of the Public Sector Development

Commission CDP Country Development Partnership PAD People’s Alliance for Democracy CDP-G Country Development Partnership with

Thailand on Governance and Public Sector Reform

PAMP Public Administration Management Plan

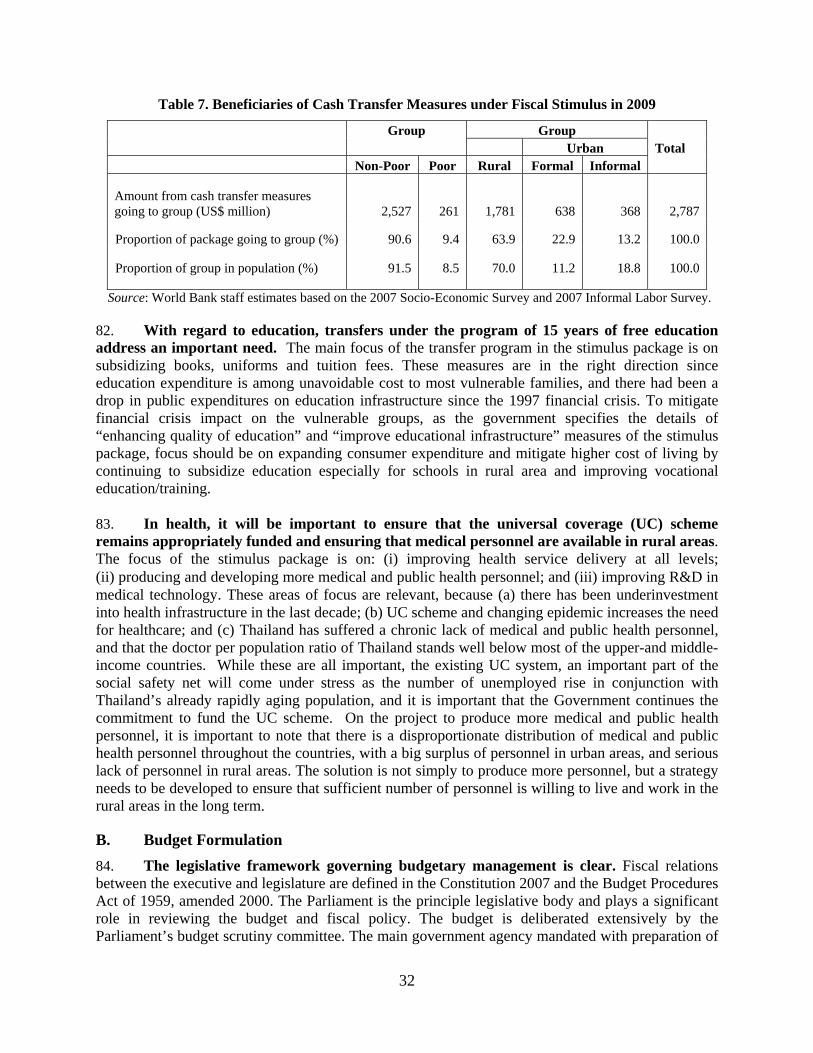

CGD Comptroller General’s Department PART Performance Assessment Rating Tool COA Chart of Accounts PDMO Public Debt Management Office DPL Development Policy Loan PEFA Public Expenditure and Financial Accountability DSA Debt Sustainability Analysis PFM Public Financial Management FDI Foreign Direct Investment PFMR Public Financial Management Report FPO Fiscal Policy Office PICS Productivity and Investment Climate Survey GFMIS Government Fiscal Management

Information System PPP People’s Power Party

GoT Government of Thailand PSRDPL Public Sector Reform Development Policy Loan ISN ICA

Interim Strategy Note Investment Climate Assessment

RBM Results Based Management

JICA Japan International Cooperation Agency RD Revenue Department KPI Key Performance Indicators ROSC Report on Observance of Standards and Codes LIBOR London Inter-Bank Offered Rate RTG Royal Thai Government LTO Large Taxpayer Office SDDS Special Data Dissemination Standards MOF Ministry of Finance SME Small and Medium Enterprises MoNRE Ministry of Natural Resources and the

Environment TKK “Thai Kem Kaeng” (Strong Thailand)

MTEF Medium Term Expenditure Framework TRA Treasury Reserve Account NACC National Anti-Corruption Commission TRT Thai Rak Thai Party NEER Nominal Effective Exchange Rate UDD United Front for Democracy against Dictatorship

Vice President: Country Director:

Sector Director and Chief Economist: Lead Economist and Task Team Leader:

James Adams Annette Dixon Vikram Nehru Mathew Verghis

The Thailand Public Sector Reform Development Policy Loan was prepared by a team consisting of Shabih Ali Mohib, Kirida Bhaopichitr, Frederico Gil Sander, Vatcharin Sirimaneetham, Nattaporn Triratanasirikul, Ruangrong Thongampai, Ton-Thang Long, Angkanee Luangpenthong, Ratchada Anantavrasilpa, Lynn Gross (EASPR), Zhi Liu, Chanin Manopiniwes (EASTE), Clive Harris (EASOP), Jitendra Shah, James Monday (EASRE), Blanca Moreno-Dodson (PRMVP), Ahsan Ali, Chinnakorn Chantra, Ronald Points (EAPCO), Vikram Raghavan, Roche Levesque (LEGES), Malcolm Holmes, Michael Engelschalk, John Wiggins, David Shand (Consultants), and led by Mathew Verghis (EASPR).

The peer reviewers were Stephan Koeberle (LSCOS), Dana Weist (PRMED) and Ijaz Nabi (SARVP). Useful comments were received from Ed Mountfield (OPCCE) and Wolfgang Fengler (EASPR). The team worked under the guidance of Vikram Nehru (Sector Director, EASPR) and Annette Dixon (Country Director), and earlier from Ian Porter (former Country Director).

KINGDOM OF THAILAND

PROPOSED PUBLIC SECTOR REFORM DEVELOPMENT POLICY LOAN (PSRDPL)

TABLE OF CONTENTS

LOAN AND PROGRAM SUMMARY

I. INTRODUCTION ......................................................................................................................... 1

II. COUNTRY CONTEXT AND DEVELOPMENT CHALLENGES .......................................... 4

A. Recent Economic Developments and Outlook ....................................................................... 4

B. Fiscal Response to the Financial Crisis and Debt Sustainability ......................................... 12

C. Political Context ................................................................................................................... 19

III. THE GOVERNMENT’S PROGRAM AND PRIORITIES ..................................................... 21

A. Public Financial Management and Service Delivery ........................................................... 22

B. Improving National Competitiveness .................................................................................. 22

C. Increasing social protection and health policy reforms ........................................................ 24

IV. BANK’S SUPPORT TO THE GOVERNMENT’S PROGRAM ............................................. 24

A. Thailand’s Interim Strategy Note ......................................................................................... 24

B. Analytical Underpinnings .................................................................................................... 25

C. Collaboration with the IMF and Other Donors .................................................................... 27

V. THE GOVERNMENT’S REFORM PROGRAM .................................................................... 27

A. The Fiscal Stimulus Package ............................................................................................... 28

B. Budget Formulation ............................................................................................................. 32

C. Reforming Budget Execution, Accounting and Reporting .................................................. 34

D. External Audit ...................................................................................................................... 36

E. Internal Controls and Internal Audit .................................................................................... 37

F. Public Procurement .............................................................................................................. 38

G. Debt Management ................................................................................................................ 39

H. Anti-Corruption .................................................................................................................... 40

I. Revenue Management .......................................................................................................... 41

J. Results-Based Management ................................................................................................. 42

K. Civil Service Management ................................................................................................... 43

L. Areas of Focus for Future Reforms ...................................................................................... 44

VI. THE PROPOSED OPERATION ............................................................................................... 45

VII. OPERATIONAL AND IMPLEMENTATION ISSUES .......................................................... 49

A. Poverty and Social Aspects .................................................................................................. 49

B. Implementation, Monitoring and Evaluation ....................................................................... 52

C. Fiduciary Aspects, Disbursement and Auditing ................................................................... 53

D. Risks and Risk Mitigation .................................................................................................... 54

E. Environmental and Social Aspects ....................................................................................... 56

FIGURES

Figure 1. The Thai economy is driven by sectors linked the production of tradable goods and services. .... 6 Figure 2. Core Inflation Remains Below its (already low) Historical Average. ........................................... 6 Figure 3. Bank of Thailand Balance Sheet ................................................................................................... 9 Figure 4. Financial Sector Strength Indicators .............................................................................................. 9 Figure 5. Thailand: Public Debt Sustainability Analysis ............................................................................ 17 Figure 6. Thailand 5-year Credit Default Swaps ........................................................................................ 19 Figure 7. Thailand Yield Curve .................................................................................................................. 19 Figure 8. Thailand Poverty Headcount Ratio and Economic Growth: 1988-2007 ..................................... 49 Figure 9. Proportion of Poor Households Classified by Economic Activities, 2007 .................................. 49 Figure 10. The decline in agricultural prices was the main channel through which the crisis affected vulnerable households. ................................................................................................................................ 51 Figure 11. Labor initially shifted to agriculture during the crisis, but as the recovery took hold manufacturing employment gained. ............................................................................................................ 51

TABLES

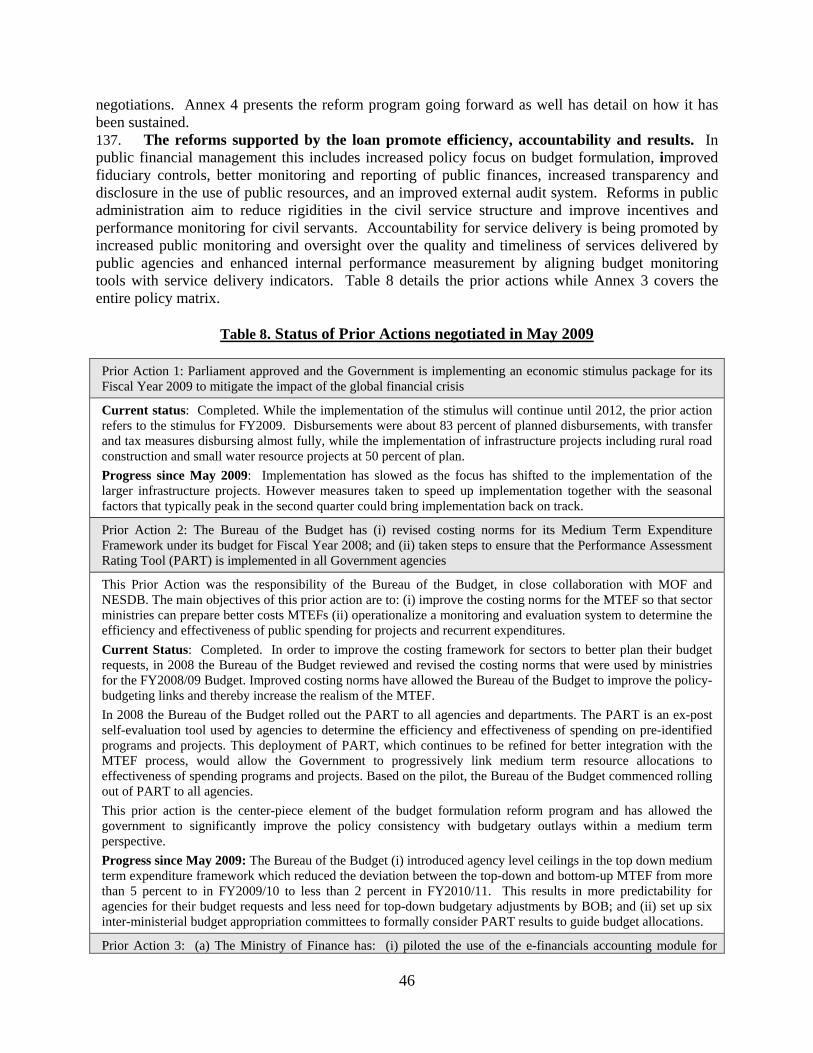

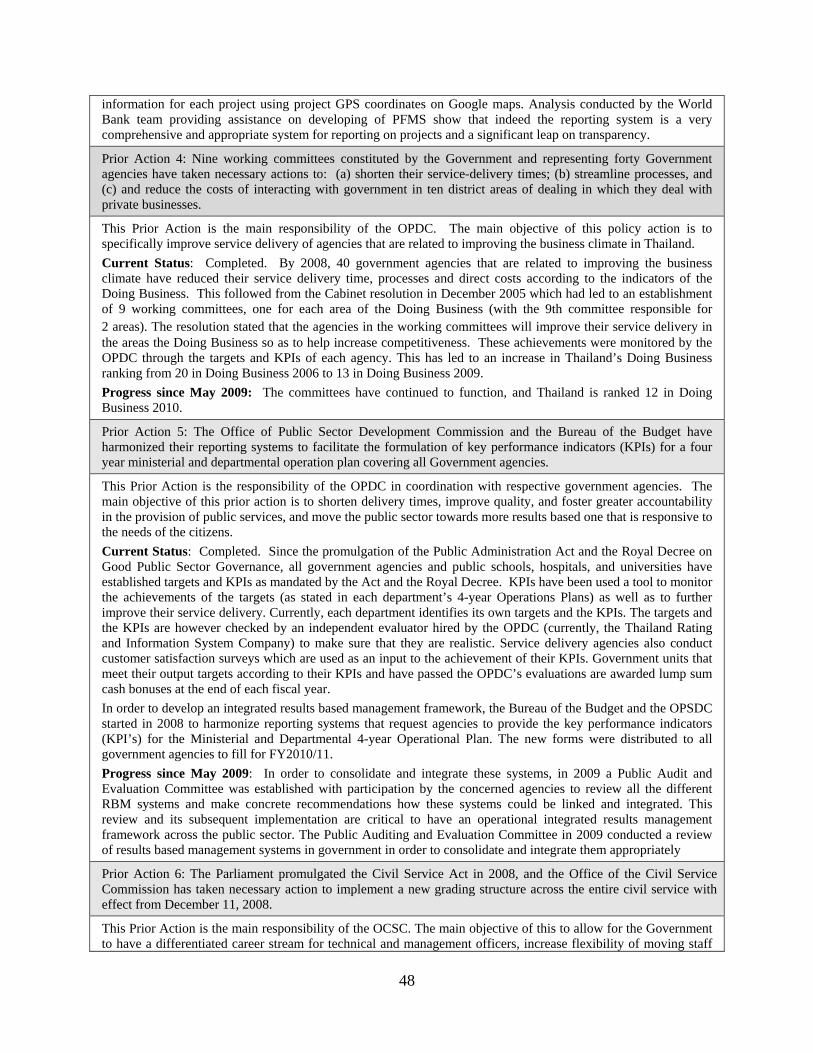

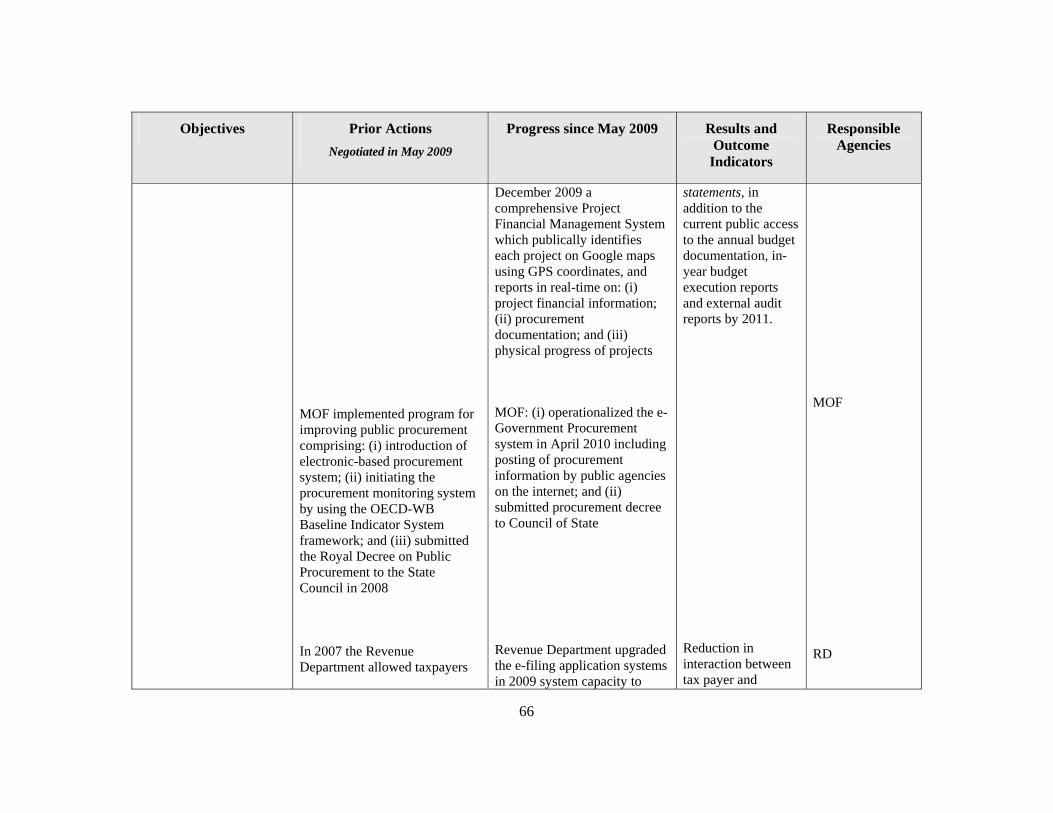

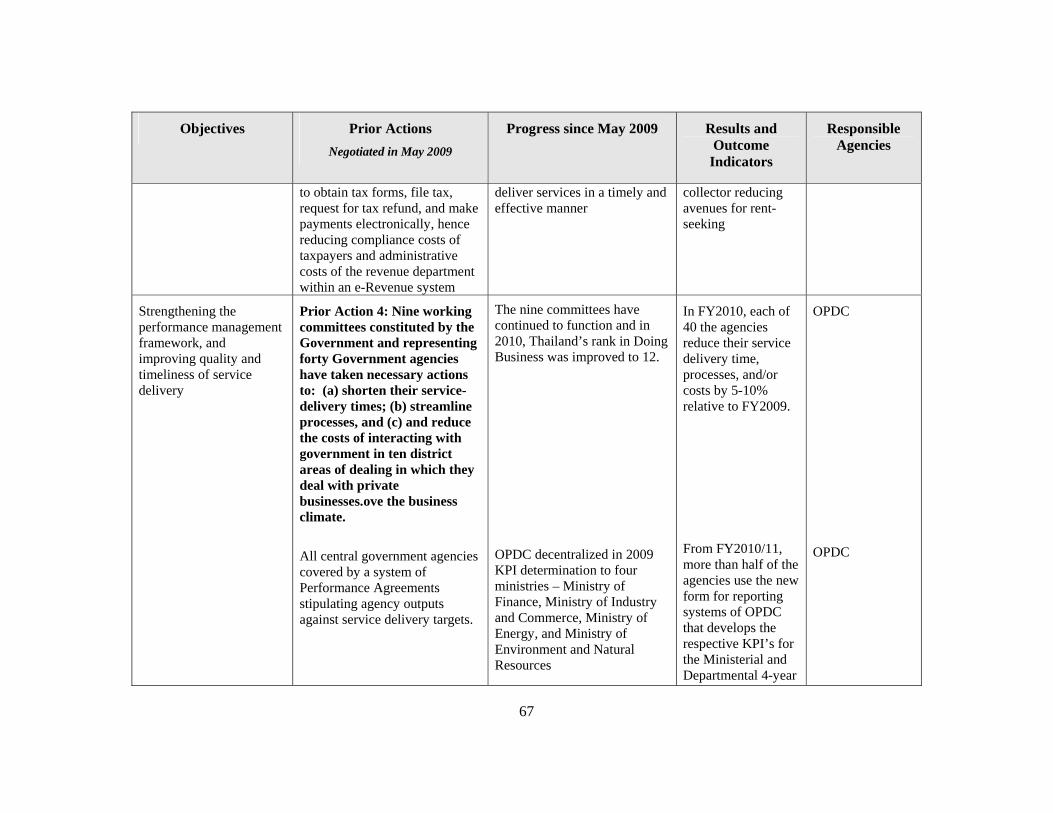

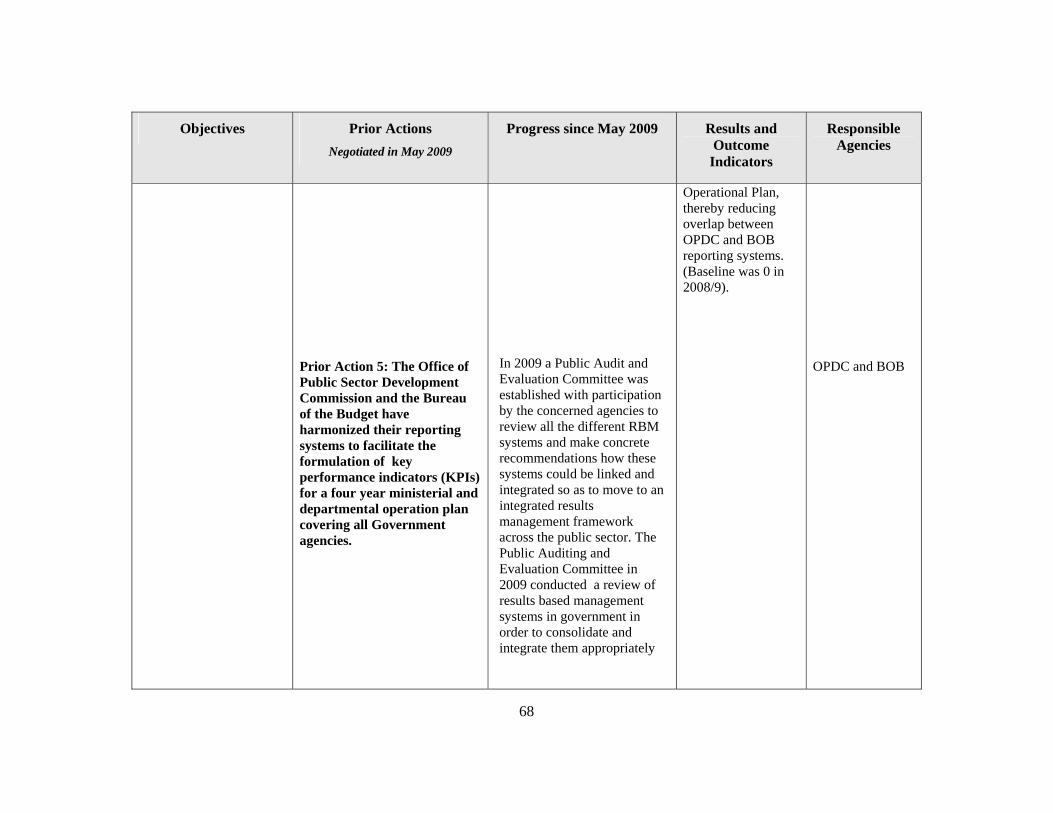

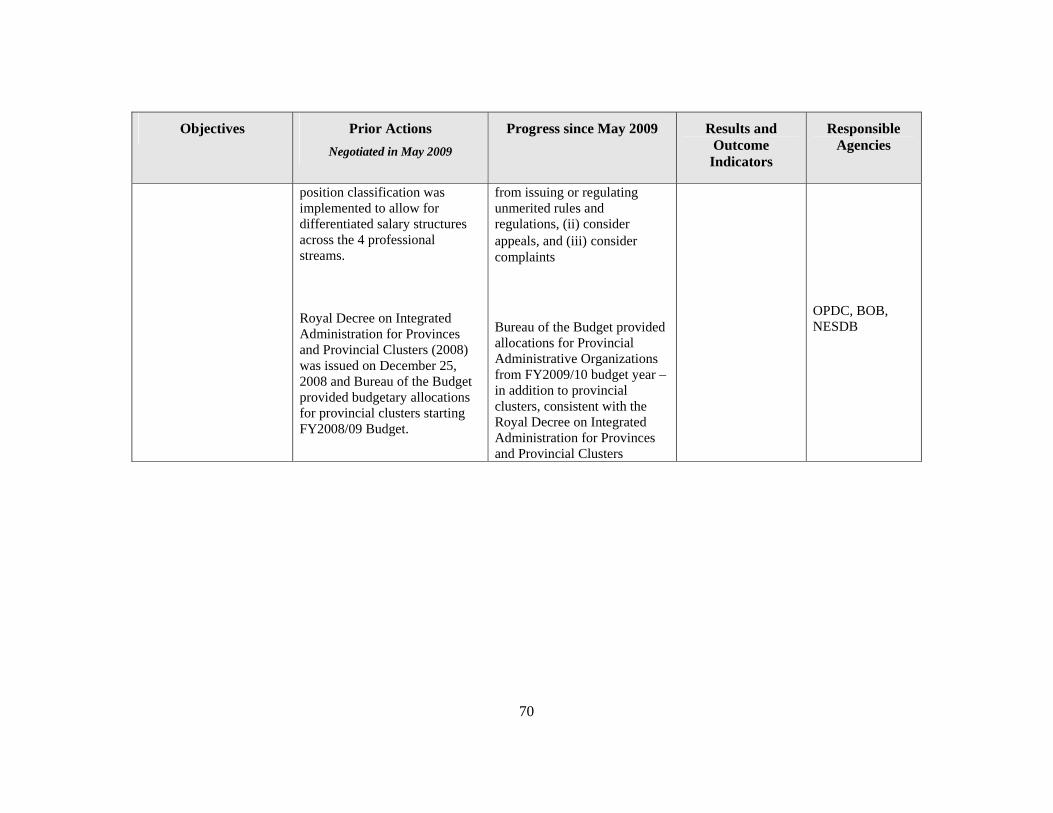

Table 1. Real GDP Growth, 2009-2011 (Percent, year-on-year) ................................................................. 5 Table 2: Key Economic Indicators .............................................................................................................. 10 Table 3. Central Government Expenditure, FY2006-2009 ......................................................................... 12 Table 4. Central Government’s Financing Plan for FY2009 – FY2013 (percent of GDP) ....................... 14 Table 5. Debt Sustainability Analysis – Sensitivity Analysis ..................................................................... 18 Table 6. Thailand’s Fiscal Stimulus Package ............................................................................................. 31 Table 7. Beneficiaries of Cash Transfer Measures under Fiscal Stimulus in 2009 .................................... 32 Table 8. Status of Prior Actions negotiated in May 2009 ........................................................................... 46 Table 9. Thailand Poverty Headcount and Number of Poor, 2000-2007 .................................................... 50

ANNEXES

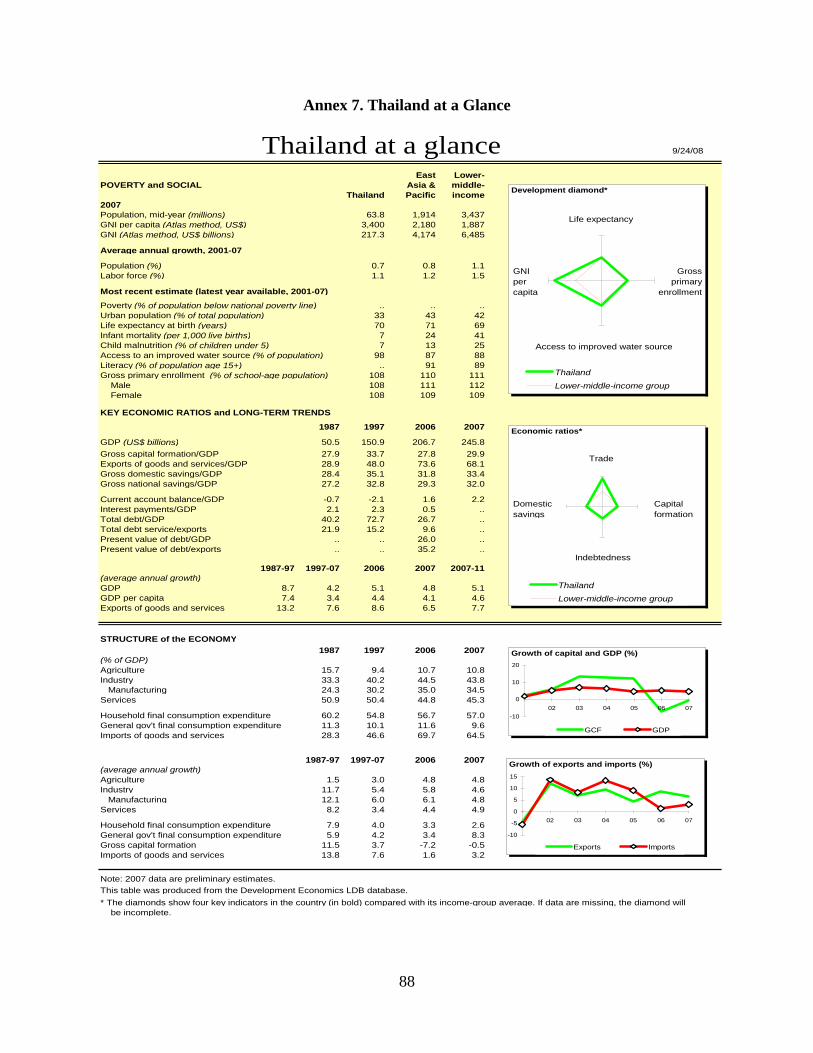

Annex 1. Letter of Development Policy ..................................................................................................... 58 Annex 2. Application of Good Practice Principles on Conditionality ........................................................ 62 Annex 3. Development Policy Matrix ........................................................................................................ 63 Annex 4. Governments Public Sector Reform Program –Key Reforms and Plans .................................... 71 Annex 5. World Bank Support to Thailand’s Public Sector Reform Program (1998-2008): Inputs (TAs and ESWs) .................................................................................................................................................. 80 Annex 6. IMF Public Information Notice ................................................................................................... 84 Annex 7. Thailand at a Glance .................................................................................................................... 88

MAP IBRD 33495

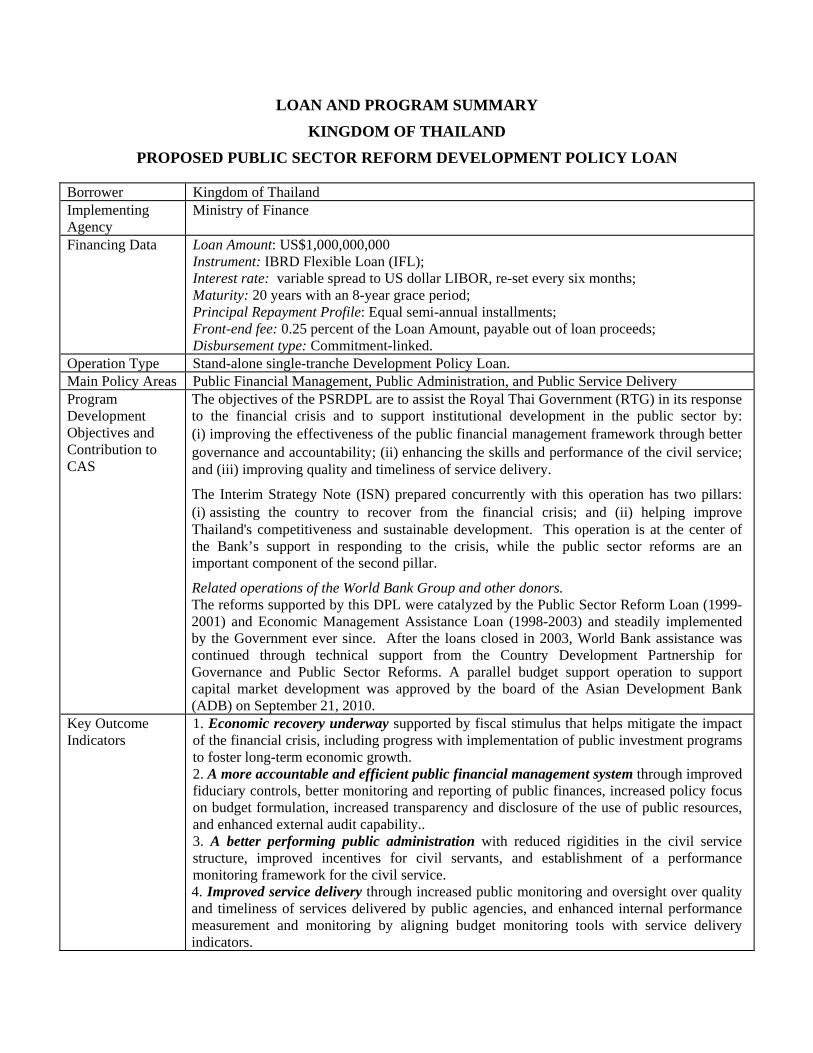

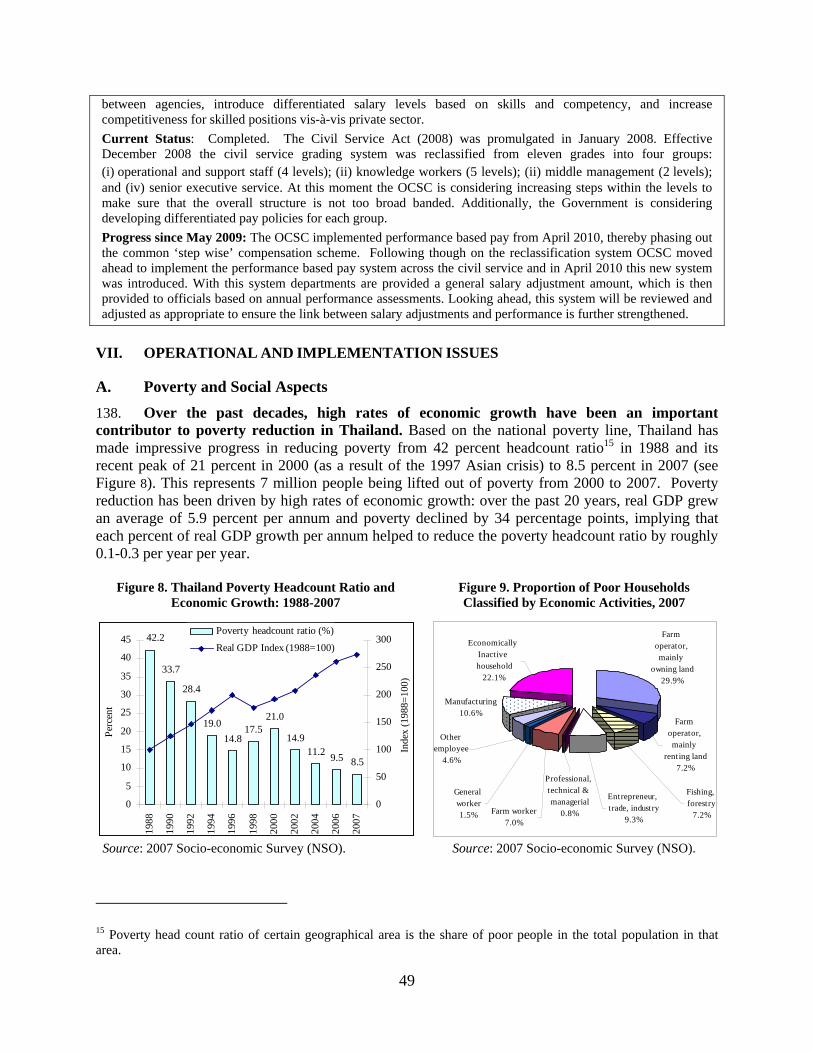

LOAN AND PROGRAM SUMMARY

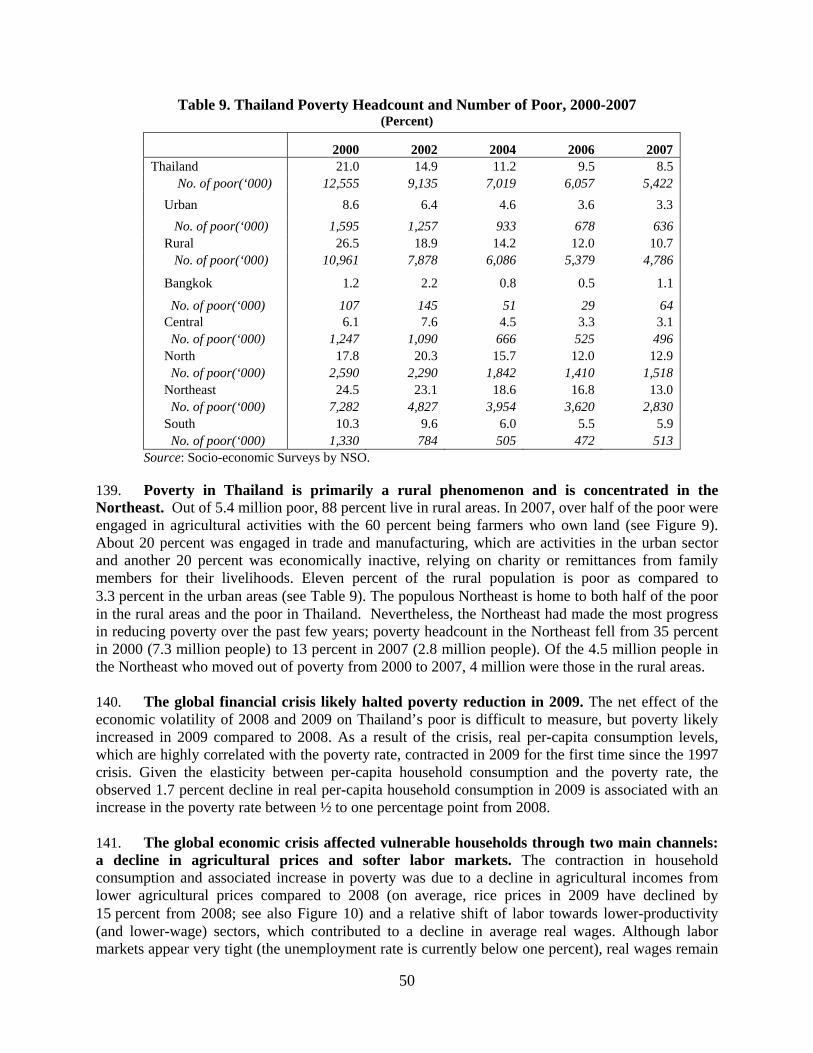

KINGDOM OF THAILAND

PROPOSED PUBLIC SECTOR REFORM DEVELOPMENT POLICY LOAN

Borrower Kingdom of Thailand Implementing Agency

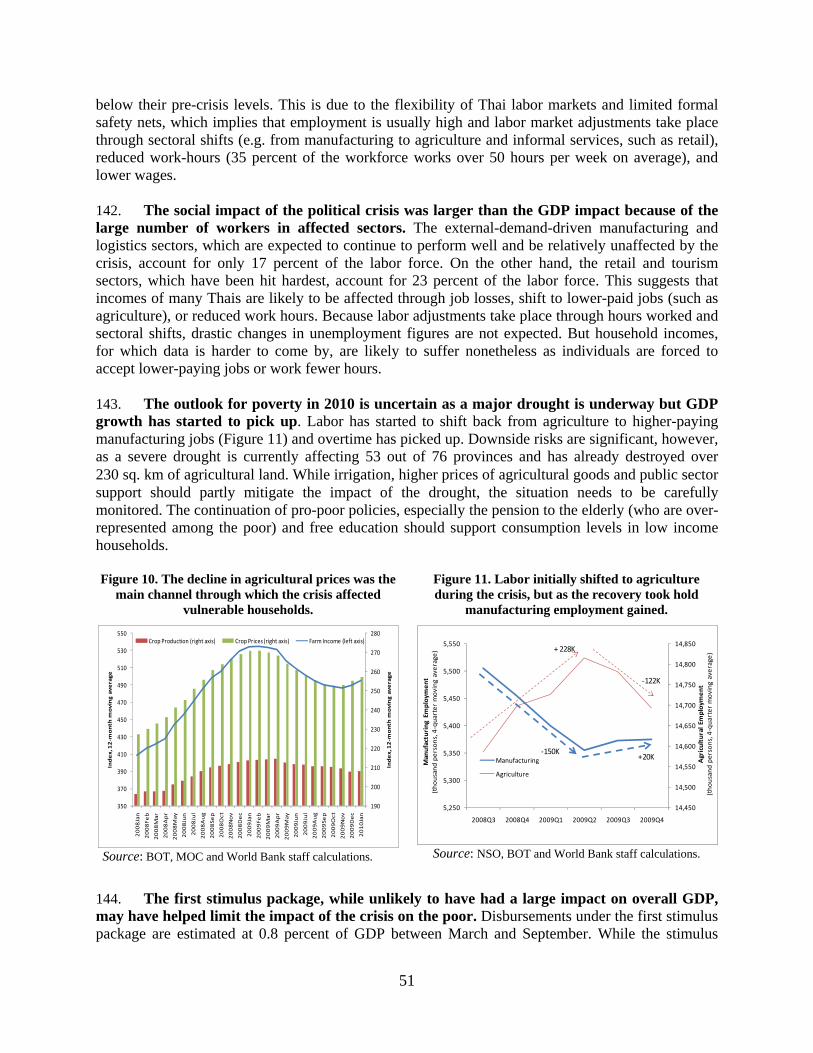

Ministry of Finance

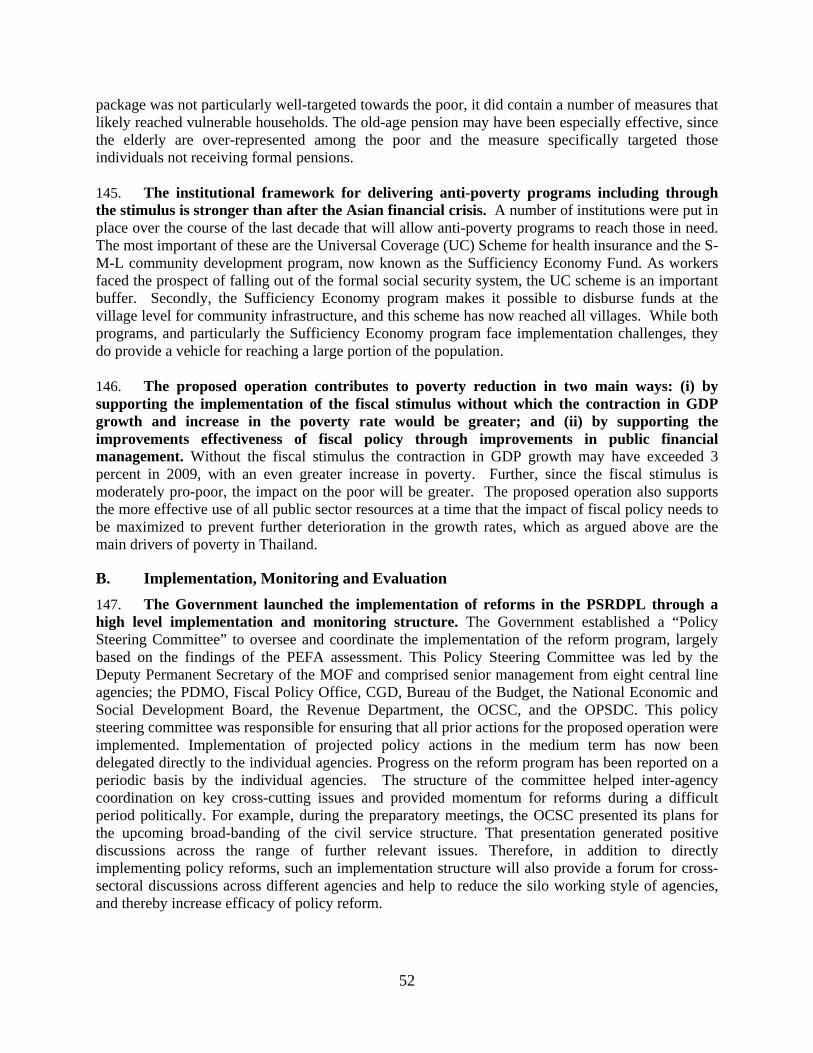

Financing Data

Loan Amount: US$1,000,000,000 Instrument: IBRD Flexible Loan (IFL); Interest rate: variable spread to US dollar LIBOR, re-set every six months; Maturity: 20 years with an 8-year grace period; Principal Repayment Profile: Equal semi-annual installments; Front-end fee: 0.25 percent of the Loan Amount, payable out of loan proceeds; Disbursement type: Commitment-linked.

Operation Type Stand-alone single-tranche Development Policy Loan. Main Policy Areas Public Financial Management, Public Administration, and Public Service Delivery Program Development Objectives and Contribution to CAS

The objectives of the PSRDPL are to assist the Royal Thai Government (RTG) in its response to the financial crisis and to support institutional development in the public sector by: (i) improving the effectiveness of the public financial management framework through better governance and accountability; (ii) enhancing the skills and performance of the civil service; and (iii) improving quality and timeliness of service delivery.

The Interim Strategy Note (ISN) prepared concurrently with this operation has two pillars: (i) assisting the country to recover from the financial crisis; and (ii) helping improve Thailand's competitiveness and sustainable development. This operation is at the center of the Bank’s support in responding to the crisis, while the public sector reforms are an important component of the second pillar.

Related operations of the World Bank Group and other donors. The reforms supported by this DPL were catalyzed by the Public Sector Reform Loan (1999-2001) and Economic Management Assistance Loan (1998-2003) and steadily implemented by the Government ever since. After the loans closed in 2003, World Bank assistance was continued through technical support from the Country Development Partnership for Governance and Public Sector Reforms. A parallel budget support operation to support capital market development was approved by the board of the Asian Development Bank (ADB) on September 21, 2010.

Key Outcome Indicators

1. Economic recovery underway supported by fiscal stimulus that helps mitigate the impact of the financial crisis, including progress with implementation of public investment programs to foster long-term economic growth. 2. A more accountable and efficient public financial management system through improved fiduciary controls, better monitoring and reporting of public finances, increased policy focus on budget formulation, increased transparency and disclosure of the use of public resources, and enhanced external audit capability.. 3. A better performing public administration with reduced rigidities in the civil service structure, improved incentives for civil servants, and establishment of a performance monitoring framework for the civil service. 4. Improved service delivery through increased public monitoring and oversight over quality and timeliness of services delivered by public agencies, and enhanced internal performance measurement and monitoring by aligning budget monitoring tools with service delivery indicators.

Risks and Risk Mitigation

Political uncertainty. The political outlook is subject to significant risk, but there are also important mitigating factors. A coalition of opposition groups, the United Front for Democracy against Dictatorship (UDD), staged large protests in Bangkok in April and May that culminated in violence. The ruling coalition is working on a national reconciliation agenda, which may involve an early dissolution of Parliament. While relative calm has followed the end of the protests, the underlying political divisions remain and are likely to have been exacerbated by the violence. The Government’s parliamentary majority was unaffected, and Parliament has approved the FY2011 budget and financing plan in August 2010. The financing plan includes borrowing from ADB and the Japan International Cooperation Agency (JICA) in addition to borrowing from the World Bank. Although plans to borrow from international financial institutions (IFIs) were approved in Parliament by a wide margin, the vote was largely along party lines and there is a risk that borrowing from IFIs may be politicized, and that these institutions are seen as supporting the ruling coalition. Several factors mitigate this risk: (i) the loan was originally requested by a finance minister currently in the opposition; (ii) the Ministry of Finance (MOF) has carried out public consultations on the operation and solicited comments on its website; (iii) the loan is being submitted to the World Bank Board only after parliamentary approval has been received; and (iv) designing the operation as a standalone operation rather than a programmatic one helps the Government manage the political risk.

Implementation risks. Notwithstanding the political instability, the public sector reform agenda has been maintained under different political administrations. This has been the case over the past twelve months as the reform program has been sustained despite the political turmoil. This is because the underlying reform program has broad support across the political spectrum and is owned by senior civil servants in respective agencies. Therefore the risk to reform program implementation is modest. Inevitably, continued political turmoil will have some impact on the implementation of the program, and especially through delays in passage of needed legislation.

Macroeconomic risks. Thailand is recovering strongly from the global financial crisis with year-on-year GDP growth at 10.6 percent in the first half of 2010 and projected to reach over 7 percent for the year as a whole. However, growth remains largely dependent on external demand conditions, and a new slowdown in world trade would have a substantive negative impact on Thailand’s economy. A track record of prudent macroeconomic management and conservative banking practice means that the likelihood of a balance of payments or banking crises is relatively low, and that the authorities will continue to manage debt prudently. Given the strong macroeconomic fundamentals, markets have reacted calmly to political events in Thailand, although a renewed escalation in violence may lead to a market reappraisal.

Operation ID P114154

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED PUBLIC SECTOR REFORM DEVELOPMENT POLICY LOAN

TO THE KINGDOM OF THAILAND

I. INTRODUCTION 1. The Royal Thai Government (RTG) is requesting this US$1 billion Public Sector Reform Development Policy Loan (PSRDPL) to sustain economic recovery from the global financial crisis. Discussions on a possible loan that would supplement Government funds to implement a larger development budget began in mid-2008 and a formal request was made before the 2008 Annual Meetings. During loan preparation in late 2008 and early 2009, Thailand became one of the countries in Asia most affected by the global financial crisis making more urgent the need for resources. Around this time, the political climate also deteriorated significantly. The loan was negotiated in May 2009, but the government did not submit it to Parliament as the political situation did not allow parliamentary discussion as required by the Constitution. The economy began to recover in late 2009, and there has been a period of relative political calm since June 2010. As a result, the government initiated the process for parliamentary discussion of the loan, Parliament approved the loan in August, and the Government has now requested the Bank for final approval. The reforms supported by the loan are summarized in paragraph 4 and in Table 8. The delay in Parliamentary approval meant a relatively long gap between negotiations and final Board consideration. During this period, the government continued to make significant progress in implementation of the forward-looking reform program discussed during negotiations, in addition to the standard consideration of implementation of the prior actions (see Table 8 and Annex 3). 2. The Thai government’s renewed interest in borrowing reflects widespread consensus across the political spectrum on the need to increase spending on public investment. Public investment had never fully recovered from the 1997 Asian financial crisis, raising concerns about the sustainability of growth over the long term. Increasing public investment was viewed by the authorities as important to both sustain Thailand’s recovery from the global financial crisis as well as to support structural change and medium term growth. As a result, the stimulus packages emphasized public investment in critically needed infrastructure, health, and education. In addition to the World Bank, the Asian Development Bank (ADB) and the Japan International Cooperation Agency (JICA) have also been asked for support. The ADB Board approved a program loan focusing on capital market development on September 21, 2010, while JICA is preparing a number of investment loans for infrastructure, supporting among others the construction of mass transit in Bangkok. 3. Accessing World Bank funds supports prudent debt management and policy reforms. Thailand’s financing needs are largely met through the domestic debt market (Table 4). However, foreign financing from the World Bank, ADB and JICA is viewed as an important component of the financing plan to (i) prevent crowding out of the private sector in the debt market and to diversify funding sources to manage risk; (ii) allow the Government to access long term finance to match long gestation investment projects that are planned (as in many countries, the global financial crisis led to reliance on debt of shorter maturities - the amount of government debt with maturities of less than three years increased from 31 percent of the portfolio in June 2008 to 38 percent in December 2009);

2

and (iii) benefit from the policy components of IFI financing that will help maximize the development impacts of the planned investments. 4. The Government’s reform program supported by this loan seeks to strengthen public sector institutions that foster efficiency, good governance, accountability, and results – a focus that fits well with the government’s accelerated public investment program. The public financial management reforms supported by the loan promote improved fiduciary controls, better monitoring and reporting of public finances, increased policy focus on budget formulation, increased transparency and disclosure in the use of public resources, and an improved external audit system. Parallel reforms in public administration aim to reduce rigidities in the civil service structure and improve incentives and performance monitoring for civil servants. Accountability for service delivery is being promoted by increased public monitoring and oversight over the quality and timeliness of services delivered by public agencies and enhanced internal performance measurement by aligning budget monitoring tools with service delivery indicators. 5. The public sector reform program has been implemented over a number of years despite long-standing political instability. Public sector reforms were launched in the aftermath of the Asian financial crisis, and were initially supported by World Bank policy-based lending and technical assistance (TA). The last policy-based loan closed in 2001 and the corresponding TA loan closed in 2003. Although the Bank has remained substantively involved in key policy discussions over the entire period since these loans closed (see paragraph 10), Thailand’s reform program evolved without conditionality from the international financial community. This reflects the fact that while Government policy actions have benefitted from Bank analytical work and advice, these reforms are clearly owned by senior civil servants in the key agencies. While the focus of the diagnostic work described in Section V is on the areas of the program needing improvement, it is important to note that in some areas such as civil service reform the Thailand program is already serving as a model for regional peers and in some areas, such as the program and performance budgeting, Thailand compares well with OECD countries. Inevitably, the political instability has led to some slowdown in the program – typically through a delay in the passage of needed legislation. Notwithstanding such slowdown, reforms have continued during 2009 and 2010 with reasonable progress. The level of ownership by Government and its demonstration of steady implementation, in spite of a political change in leadership, clearly support a judgment that the public sector reform program will continue, regardless of the status of subsequent operations and political instability. 6. The Bank will be able to continue to support the medium-term reform program. In parallel with the PSRDPL, World Bank support to the Government’s public sector reform program will continue. Ongoing work includes an important study on central-local fiscal relations, technical assistance to implement the results-based management, and strategic performance-based budgeting reforms. In addition, the Government has also indicated that it intends to continue borrowing at modest levels for investments in specific bottleneck areas over the next three years as described in the Interim Strategy Note. 7. The political situation in Thailand remains challenging and adds uncertainty to the prospects for the Thai economy. In end-2008 a new coalition Government led by the Democrat Party took office after the previous ruling party was dissolved by the Constitutional Court on violations of electoral law. The opposition has been staging protests since, which in 2009 led to the cancellation of an ASEAN+6 summit in Pattaya and riots in Bangkok, and in April/May 2010 an outbreak of violence that led to nearly 100 deaths and over one thousand injured. However, since

3

early-June a level of stability has returned and Parliament has met and supported the borrowing under PSRDPL. Nevertheless, it seems likely that it will take some time before full political stability is restored. 8. The economy is recovering strongly from the financial crisis, although political strife highlights that the recovery is still fragile. The Government’s fiscal stimulus prevented a more significant decline in domestic demand in the face of a substantial external shock as well as ongoing political tensions. In addition, the Government is using the crisis response as an opportunity to also increase social sector spending and to alleviate infrastructure bottlenecks through a medium-term scaling up of public investments. The political crisis has severely affected tourism and both domestic and foreign investment, and the continued dependence on exports adds urgency to implementing policies to support growth in both the short- and medium-terms. Nevertheless, even with such policies in place, the combination of crises has lowered growth prospects. 9. Request for Bank support has come from Thai governments led by parties on either side of the political spectrum and has been confirmed twice by Parliament. The request for this proposed PSRDPL was initially made by the People’s Power Party (PPP) Government led by the late Mr. Samak Sundaravej, was reconfirmed by the following PPP Government of Mr. Somchai Wongsawat, and has again been reconfirmed by the Democratic led Government of Mr. Abhisit Vejjajiva. The main drivers of the underlying reform program and the request for World Bank support have come from senior civil servants. On March 24 2009, Parliament authorized the Government to negotiate with the World Bank, ADB and JICA, and on August 17, 2010, Parliament authorized the Government to conclude the borrowings that had been negotiated under the previous authorization. 10. There have been public consultations on the PSRDPL. Government has solicited feedback on the PSRDPL as well as the ADB and JICA loans through the websites of the Ministry of Finance, Prime Minister, Parliament and Senate in March 2009. The Ministry of Finance also conducted a series of public consultative forums in May 2009 in Bangkok, Khonkkean (Northeastern), Surrathani (South), and Pitsanulok (North) to solicit views from the public. Participants included academics, community leaders and representatives of professional groups. Surveys were conducted at the end of each session. There have also been consultations in the context of the preparation of the Interim Strategy Note.

11. The Ministry of Finance has summarized the main messages received from the public consultations. These were grouped into four main areas:

(i) Rationale for borrowing from abroad: Given the current economic situation in Thailand,

most participants agreed on the importance of borrowing to restore the economy and develop infrastructure in Thailand.

(ii) Use of the funds: There should be a focus on value for money; since domestic borrowing is larger than foreign borrowing, domestically financed spending should also be monitored closely and local infrastructure projects should have high priority.

(iii) Debt management: Debt should be managed efficiently so as not to cause a fiscal burden in the future

4

(iv) Monitoring: There should be close monitoring of the expenditures from loan proceeds to ensure efficiency, transparency and accountability; expenditures financed by domestic debt should also be monitored closely.

II. COUNTRY CONTEXT AND DEVELOPMENT CHALLENGES

A. Recent Economic Developments and Outlook

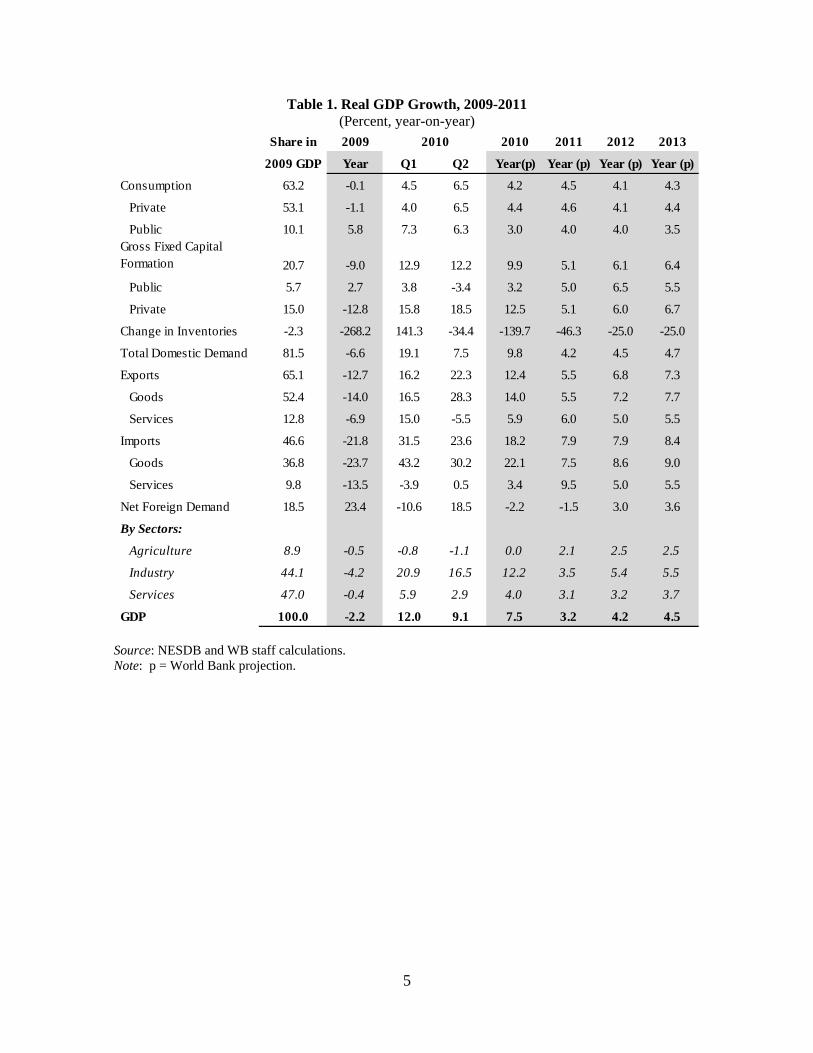

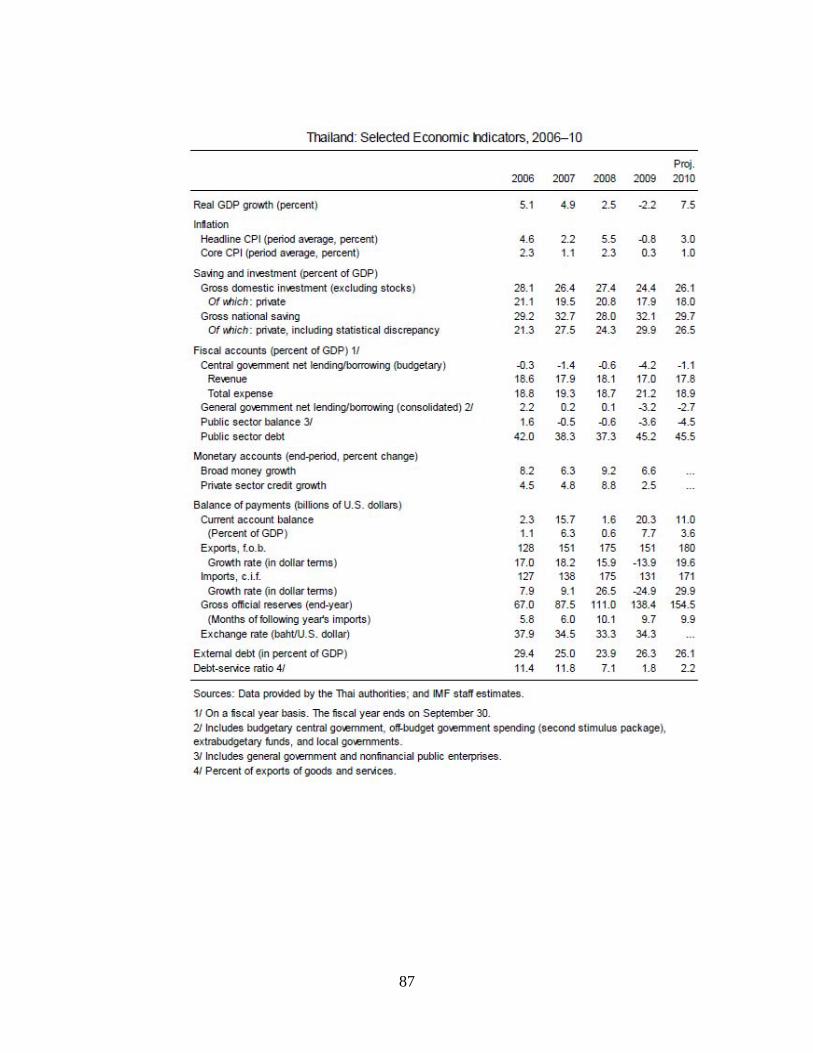

12. Thailand’s open and globally integrated economy experienced a V-shape contraction and recovery from late 2008 through the first quarter of 2010. Driven by the manufacturing-for-exports sector, Thailand’s real GDP fell 6.3 percent between the third quarter of 2008 and the first quarter of 2009, as global demand slumped, before rebounding by 12 percent over the following four quarters. The rebound was primarily due to the recovery in global demand (exports were up 16.2 percent), while private consumption grew at a more modest 4 percent during the period. Real GDP returned to pre-crisis levels by the end of 2009 (as measured in seasonally adjusted terms); although for 2009 as a whole real GDP fell by 2.2 percent. 13. The recent political turmoil of April/May 2010 had a limited effect on the economy, although the social impact was larger. The critical manufacturing-for-exports sector was little affected by the turmoil and performed extremely well given buoyant export demand in the second quarter of 2010 and a surge in domestic demand for cars, which jumped as much as 50 percent over the period. The tourism sector, on the other hand, suffered substantial losses, and service receipts contracted by over 18 percent from the previous quarter (seasonally-adjusted). The retail sector also contracted in the quarter, suggesting it was also affected by the turmoil. Since the retail and tourism-related sectors employ about 25 percent of the workforce compared to 15 percent in manufacturing, the social impact of the crisis was likely greater than its impact on GDP. 14. Despite a pick-up in household consumption in the second quarter of 2010, exports will remain the main driver of growth in the near term. Sectors linked to the production of tradable goods and services (namely, manufacturing, hotels and transport) have been the main contributors to growth since the Thai economy recovered from the 1997 financial crisis and also accounted for most of the economic dynamism since the onset of the global financial crisis (Figure 1). A change to this pattern is unlikely in the near term, implying that the outlook for exports will continue to be the key determinant of GDP performance. 15. The economy will slowdown in the second half of 2010 as the inventory cycle fades and the recovery of advanced economies proceeds at a modest pace. The Thai economy grew by 10.6 percent in the first half of 2010 from the previous year, but quarterly growth already slowed down substantially in the second quarter and is expected to contract modestly in the second half. The outlook for external demand is subdued: global trade has rebounded, but growth was likely concentrated in the first half of the year as activity indicators in the US, Japan and China point to slowdown in global demand. This moderation is due to the waning of the global inventory cycle and fiscal policy stimulus, as well as the continued slow pace of growth in advanced economies. Because of the low base of GDP in 2009 and robust performance in the first half of 2010, the year-on-year growth rate is expected to come at 7.5 percent in 2010 before slowing to 3.2 percent in 2011.

5

Table 1. Real GDP Growth, 2009-2011 (Percent, year-on-year)

Source: NESDB and WB staff calculations. Note: p = World Bank projection.

Share in 2009 2010 2010 2011 2012 2013

2009 GDP Year Q1 Q2 Year(p) Year (p) Year (p) Year (p)

Consumption 63.2 -0.1 4.5 6.5 4.2 4.5 4.1 4.3

Private 53.1 -1.1 4.0 6.5 4.4 4.6 4.1 4.4

Public 10.1 5.8 7.3 6.3 3.0 4.0 4.0 3.5Gross Fixed Capital Formation 20.7 -9.0 12.9 12.2 9.9 5.1 6.1 6.4

Public 5.7 2.7 3.8 -3.4 3.2 5.0 6.5 5.5

Private 15.0 -12.8 15.8 18.5 12.5 5.1 6.0 6.7

Change in Inventories -2.3 -268.2 141.3 -34.4 -139.7 -46.3 -25.0 -25.0

Total Domestic Demand 81.5 -6.6 19.1 7.5 9.8 4.2 4.5 4.7

Exports 65.1 -12.7 16.2 22.3 12.4 5.5 6.8 7.3

Goods 52.4 -14.0 16.5 28.3 14.0 5.5 7.2 7.7

Services 12.8 -6.9 15.0 -5.5 5.9 6.0 5.0 5.5

Imports 46.6 -21.8 31.5 23.6 18.2 7.9 7.9 8.4

Goods 36.8 -23.7 43.2 30.2 22.1 7.5 8.6 9.0

Services 9.8 -13.5 -3.9 0.5 3.4 9.5 5.0 5.5

Net Foreign Demand 18.5 23.4 -10.6 18.5 -2.2 -1.5 3.0 3.6

By Sectors:

Agriculture 8.9 -0.5 -0.8 -1.1 0.0 2.1 2.5 2.5

Industry 44.1 -4.2 20.9 16.5 12.2 3.5 5.4 5.5

Services 47.0 -0.4 5.9 2.9 4.0 3.1 3.2 3.7

GDP 100.0 -2.2 12.0 9.1 7.5 3.2 4.2 4.5

6

Figure 1. The Thai economy is driven by sectors linked the production of tradable goods and services.

Source: NESDB and World Bank staff calculations. 16. Inflation risks are generally low, but food prices need to be monitored. Thailand’s headline CPI increased 3.3 per cent year-on-year in August whereas core prices rose 1.2 percent in the same period. Prices of food, especially raw food, were the key drivers, explaining the difference between core and headline numbers. Year-on-year increases in energy prices have moderated to 0.3 percent from a peak of 36 percent in December/January, whereas fruits and vegetables registered a 40 percent year-on-year increase. Year-on-year readings will remain relatively high due to base effects, but core prices are likely to remain below their long-term trend in part due to continuing government subsidies to transportation and utilities. The current readings, as well as the last-twelve-month average (annualized) are still below Thailand’s 2006-2007 average (an approximation for ‘normal times’) and well within the Bank of Thailand’s (BOT) target of between 0.5 and 3 percent (see Figure 2 below).

Figure 2. Core Inflation Remains Below its (already low) Historical Average.

Source: Ministry of Commerce and World Bank staff calculations.

960

980

1,000

1,020

1,040

1,060

1,080

1,100

1,120

1,140

1,160

1,180

400

450

500

550

600

650

Real, Seasonally‐Adjusted THB Billions (GDP)

Real, Seasonally‐Adjusted THB Billions (components)

3 sectors producing tradable goods & services

13 sectors producing primarily non‐tradable goods & servicesGDP

‐2

‐1

0

1

2

3

4

2006Jan

2006Apr

2006Jul

2006Oct

2007Jan

2007Apr

2007Jul

2007Oct

2008Jan

2008Apr

2008Jul

2008Oct

2009Jan

2009Apr

2009Jul

2009Oct

2010Jan

2010Apr

2010Jul

Core CPI (m/m, 12‐mo MA, annualized)

Average core CPI in 2006 and 2007

(1.4 percent per year)

7

17. A slowdown in export growth from the breakneck pace of the first half is likely. Merchandise exports grew by 42 percent year-on-year in nominal terms in the second quarter of 2010, acceleration from the 32 percent pace registered in the first quarter. Growth was driven almost entirely (92 percent) by exports of manufactured goods, and it is likely that much of this growth was linked the global restocking cycle, which is expected to have been largely completed. This is likely to lead to a stabilization of demand for Thai exports at a lower level, consistent with slow growth in advanced economies. Although emerging markets have been a growing source of demand for Thai exports, they have yet to fully compensate for the shortfall in the demand from developed countries, especially as their economies are also sensitive to developments in OECD countries. The outlook for services exports, notably tourism, is more favorable in large part due to the low base set in the second quarter. Indeed, tourist arrivals have already rebounded strongly and as of July were already at 84 percent of the (seasonally-adjusted) pre-crisis peak Thailand remains a competitive destination and the recovery in consumer spending in advanced economies -- while slow -- will continue to drive growth. Key risks include a new deterioration of sentiment in Europe, as European tourists comprise the largest percentage of visitors from high-income countries, as well as renewed politics-related violence. 18. The outlook for private investment is positive in the near term, but uncertainty due to Thailand’s political situation and the speed of global recovery could dampen investment beyond 2010. The rebound in manufacturing production has implied an increase in capacity utilization from its low level in February 2009 and a resumption of capital expenditures that had been all but frozen during the trough of the crisis. Private investment grew by 18.5 percent year-on-year in the second quarter, mostly imported equipment (capital goods imports grew by 32 percent in real terms over the same period) for machine maintenance and upgrades by existing firms. The prospect for ‘greenfield’ investments in new plants or by new investors is more limited, although recent announcements by auto makers bode well for the sector, which is of increasing important to exports and the economy overall. Remaining excess capacity on a global scale, a related highly competitive environment for foreign direct investment, and the weight of the ongoing political turmoil and regulatory uncertainty from the Map Ta Phut and 3G auction court cases will limit the potential growth rate of investment in the medium term. Construction investment, long subdued, has picked up modestly thanks to the low interest rate environment and economic recovery. The rebound in private investment is seen in the first quarter of 2010, when private investment grew by nearly 16 percent. 19. Public investment grew by 2.7 percent in 2009 and growth is expected to accelerate to 3.2 percent in 2010. Investment projects under two government stimulus packages helped raise public investment slightly in 2009 – around 2.7 percent of total public investment or 0.3 percent of GDP, but this contribution is expected to pick up in 2010, making up for a reduction of on-budget investments. The investment budget from the first stimulus package that was carried forward to 2010 is expected to add about THB 11 billion in new public investments, and approximately two-thirds of the “Thai Kem Kaeng” (TKK) budget is allocated to construction and equipment investments. Although on-budget capital expenditures of the central government are expected to decrease by 50 percent from the previous year, investment projects under the off-budget stimulus package more than compensate for this reduction. Slow disbursements in the initial months of 2010 and lower investment by state-owned enterprises caused public investment to contract in the second quarter. Nevertheless, an acceleration of public investment growth is expected in the second half of 2010 thanks to the availability of financing for, and advanced stage of, most projects under the TKK program, as well as a recovery of investments from state-owned enterprises and an increase in the capital budget.

8

20. A recovery in agricultural prices and improved consumer sentiment will support growth in household consumption in 2010. Household consumption contracted by 1.1 percent in 2009, the first contraction since the 1997 crisis. The global economic crisis affected household consumption in at least three ways: first, incomes in agriculture, which employs nearly 40 percent of the workforce, declined in 2009 along with the prices of agricultural commodities; second, agriculture served as a safety net to workers displaced from the manufacturing and trade-related sectors, which placed downward pressure on wages and incomes; finally, the crisis affected consumer confidence. In response to these shocks, the Government implemented a consumption-focused fiscal stimulus package, which was implemented quickly, and likely prevented a further decline in consumption. Moreover, as consumer confidence returned in early 2010, accommodative monetary policy started to have a greater impact as households took advantage of low interest rates to purchase durable goods, especially autos. As a consequence, household consumption grew a robust 6.5 percent in the second quarter of 2010. Although this was driven by car sales made prior to the political turmoil, consumer confidence and value-added tax (VAT) receipts have picked up in June and July from a dip during the crisis. Given base effects and firm agricultural prices, household consumption should post modest growth in 2010. The Government’s farm support schemes have expanded their reach to more farmers, providing sizeable transfers to a larger number of agricultural households and further supporting consumption growth in 2010. 21. A strong rebound in imports is expected to lead to a sharp narrowing of the current account surplus from 7.7 percent of GDP in 2009 to 2.3 percent in 2010. Imports plummeted 25 percent in US dollar terms in 2009, and are expected to jump by 29 percent in 2010 as exports and equipment investment pick up. Importantly, given that a large portion of manufacturing firms’ inventories are comprised of imported inputs for production, a rebuilding of inventories depleted in 2009 is also likely to drive up imports. The result will be a substantial narrowing of the current account from 2009, although a surplus is still expected given the sizeable value added of exports (approximately 50 percent of gross exports) and import prices (especially of energy products) that are still below the 2008 levels. 22. As interest rates head higher and the current account surplus persists, the BoT announced two rounds of measures to promote outflows and help manage pressures on the exchange rate. Until recently, the BOT managed pressures for exchange rate appreciation by accumulating reserves and mopping up the resulting liquidity through sterilization. The cost of this policy has been limited because rates have been at historical lows and credit demand sufficiently subdued to raise concerns about inflation or asset price bubbles; moreover, foreign inflows were limited by the heightened political risk. Given the beginning of interest rate normalization (which leads to an increase of the interest differential with OECD economies) and stabilization of the political situation, sterilization costs are likely to increase while inflows of foreign capital (and repatriation of Thai investments) may increase. This has led the Bank of Thailand to announce two sets of measures to facilitate capital outflows facilitating the operations of regional operating headquarters and supporting direct investments overseas by Thais. As a result, the financial account is expected to post outflows in 2010, even as foreign direct investment (FDI) grows at a higher pace than private investment. Reserves currently cover over about 10 months of imports and are expected to decline marginally in nominal terms. 23. The Thai financial and corporate sectors remain sound, and bank balance sheets continued to strengthen through the crisis. Banks exceed statutory capital adequacy ratios, with the average capital adequacy ratio standing at 15.8 percent at end-2009, compared to the BIS

9

requirement of 8.5 (see Figure 4). Although at the onset of the financial crisis there was a concern that asset quality was bound to deteriorate, non-performing loans (NPLs) actually declined – gross and net NPL to total assets ratios stood at 4.9 and 2.7 percent at year-end, respectively. Large firms went into the crisis with strong balance sheets (debt-to-equity ratios had been declining and stood at about 3 times at end-2009), which allowed them to withstand the shock to their profits during the trough of the crisis. This minimized disruptions during the recovery and allowed firms to post solid financial results for 2009 as a whole. 24. Despite adequate liquidity in the financial sector, small and medium enterprises (SMEs) suffered not only to the shock to sales but also from a lack of credit. Business dissolutions peaked in the second quarter of 2009 even as large corporates were returning to profitability, reflecting the difficulties encountered by many SMEs that had neither the strong balance sheets of large corporates nor access to credit despite plentiful liquidity in the financial system. With the improved economic environment and ample room in their balance sheets, banks have increased lending in 2010.

Figure 3. Bank of Thailand Balance Sheet Figure 4. Financial Sector Strength Indicators

Source: Bank of Thailand.

Source: Bank of Thailand.

25. As the economic recovery has consolidated, the BOT has started to raise interest rates towards levels compatible with precrisis levels. Monetary policy has sought to be countercyclical during the financial crisis, with the policy rate cut to 1.25 percent in early 2009 from 3.75 percent in October 2008. The impact of monetary policy on the real economy had been limited, however, given the demand-side nature of the economic slowdown. However, as consumers (and banks) became more confident of the recovery, credit growth accelerated as a response to low interest rates. The consolidation of the economic recovery and recent growth in domestic credit has prompted the BOT to start normalizing interest rates, rising to 1.75 percent following two 25 basis points hikes in July and August.

‐60

‐40

‐20

0

20

40

60

‐5

‐4

‐3

‐2

‐1

0

1

2

3

4

5

Jan‐07

Mar‐07

May‐07

Jul‐07

Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐08

Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐09

Sep‐09

Year‐on‐year Growth (percent)

THB Trillion

Net domestic assets (L) Monetary base (L)Net foreign assets (L) Net foreign assets (R)Monetary base (R) Net domestic assets (R)

Year‐on‐Yeargrowth rates

Balance sheet of the Bank of Thailand

0

10

20

30

40

50

60

0.00

0.50

1.00

1.50

2.00

2.50

Percen

t

Trillion TH

B

Capital Funds‐LHS Gross NPL ‐ LHS

% CAR ‐ RHS % NPL to total loan ‐ RHS

10

Table 2: Key Economic Indicators

Historical Projected 2007 2008 2009 2010 2011 2012

Output, Employment and Prices Real GDP (% change year to year) 4.9 2.5 -2.2 7.5 3.2 4.2 Industrial production index (2000=100) 180.7 190.2 180.4 .. .. .. (% change year to year) 8.2 5.3 -5.1 .. .. .. Unemployment (%) 1.4 1.4 1.5 1.3 1.3 1.3 Real wages (% change year to year)1/ 0.7 4.8 -1.6 .. .. .. Consumer price index (% change year to year) 2.2 5.5 -0.8 3.5 3.0 3.0 Public Sector Government balance (% GDP)2/ -2.5 -1.9 -3.8 -2.7 -3.0 -2.1 Public sector debt (% GDP) 37.5 38.2 43.8 43.0 44.9 45.1 Foreign Trade, BOP and External Debt Trade balance (Billions US$) 12.8 -0.4 19.4 5.2 0.3 -2.6 Exports of goods (Billions US$) 151.3 175.2 150.7 175.3 192.2 216.1 (% change year to year) 18.2 15.9 -14.0 16.3 9.7 12.5 Key Export (% change year to year)3/ 16.4 7.6 -15.2 .. .. .. Imports of goods (Billion US$) 138.5 175.6 131.4 170.0 191.9 218.8 (% change year to year) 9.1 26.8 -25.2 29.4 12.9 14.0 Current account balance (Billion US$) 15.7 1.2 20.3 7.0 1.4 -0.8 (% GDP) 6.3 0.4 7.7 2.3 0.4 -0.2 Foreign direct investment (Billion US$)4/ 10.3 7.6 5.3 7.6 9.3 11.3 (% GDP) 4.1 2.8 2.0 2.5 2.6 3.0 External debt (Billion US$)5/ 61.9 65.2 69.5 .. .. .. (% GDP) 24.8 24.0 26.4 .. .. .. Short term external debt (Billion US$)5/ 21.6 24.2 27.4 .. .. .. Debt service ratio (% exports of goods/services) 11.8 7.1 6.7 .. .. .. Foreign exchange reserves, gross (Billion US$) 87.5 111.0 138.4 143.1 .. .. (months of imports of goods/services) 7.9 7.9 13.2 10.1 Financial Markets Domestic credit (% change year to year)6/ 4.9 9.3 3.1 .. .. .. Short term interest rate (% p.a.)7/ 3.69 3.40 1.35 .. .. .. Exchange rate (Baht/US$, average) 34.2 33.4 34.3 32.5 30.0 30.0 Real effective exchange rate (2000=100)8/ 112.2 112.8 108.8 .. .. .. Stock market index (December 1996=100) 858 450 735 .. .. .. Memo Items Nominal GDP (Billion US$) 249.0 272.0 263.7 309.8 356.9 383.1 Nominal GDP (Billion Baht) 8,529.8 9,075.5 9,050.7 10,070.0 10,705.7 11,492.6 Real per capita GNI (2000 US$) 2,876.3 3,055.0 2,950.1 3,391.0 3,772.9 3,912.7

Source: BOT, NESDB, MOF, NSO, MOC, Stock Exchange of Thailand, and staff calculations. 1/ Average wage of employed person (Labor Force Survey; NSO) deflated by CPI inflation. 2/ Cash balance of central Government for the calendar year. 3/ Machinery and mechanical appliances 4/ Non-bank foreign direct investment. 5/ Source: Bank of Thailand (BOT) 6/ IFS definition (net credit to the non-financial public sector, credit to the private sector and other accounts). 7/ BOT Policy Rate (end of day liquidity adjustment window; average of borrowing and lending facilities). 8/ Source: Bank for International Settlements

11

26. Fiscal policy has been expansionary as the Government responded to the global financial crisis with two rounds of stimulus measures, but the deficit as a share of GDP is expected to decline in FY2010. The fiscal deficit spiked in 2009, coming in at THB 376 billion or 4.4 percent of GDP for the fiscal year ended in September. The deficit was driven by the sharp decline in revenues due to the global financial crisis (accounting for about 2.6 percentage points of the deficit), the first round of stimulus (1.1 percentage points) and the lower GDP denominator (0.4 percentage points). The exit from fiscal stimulus is comprised of the expiration of a number of stimulus measures, a gradual move of other expenditures (especially public investments) into the budget (and therefore within the government’s fiscal rules), and revenue measures that are currently under study. Implementing a fiscally sustainable stimulus package is a prior action for the operation, and the stimulus package is evaluated in more detail in Section V. Because of the robust GDP growth, temporary nature of most consumption measures under the first round of stimulus, tight on-budget expenditures, and moderate disbursements under the Government’s public investment programs, a lower deficit of 1.9 percent of GDP is expected in FY2010.

27. Most of the central Government spending in the past few years has been for current expenditures, notably in the education sector. Central government expenditures averaged 17.8 percent of GDP from 2006-2009 and have been increasing by around 10 percent per year from 2007-2009. Around 75 percent of the total expenditures are for current expenditures. Wages and salaries account for around a third of the current expenditures or a quarter of total central government budget. Spending patterns are expected to be similar in FY2010. The largest share of expenditures each year goes to the education sector (almost one-fourth of total expenditures).

28. In FY2009, expenditure as a share of GDP for priority areas such as education and health has increased in line with a higher total spending as a share of GDP. After being stagnant in FY2008, spending on education and health increased by 0.8 percent in FY2009 (0.2 percent in health and 0.6 percent in education). This is in line with the increase in the Government’s total expenditures of 3.5 percent of GDP from FY2008 to FY2009 (see Table 3). Expenditures in the community and social services category posted the highest growth, up by 1.6 percent of GDP, while economic services rose by 0.2 percent. In FY2009, around THB72.0 billion (or 0.8 percent of GDP) out of the THB97.55 billion Stimulus Package 1 was spent on social projects. This significantly helped raise the share of expenditures on the social services in GDP in FY2009 from its FY2008 level. The Stimulus Package 2 which is focused on public infrastructure investments will help offset the reduction in the Government’s capital expenditure in FY2010. A more in-depth analysis through a Public Financial Management Review (PFMR) is currently being undertaken to review the expenditures and their effectiveness in greater detail.

29. Tax collection reforms have helped increase revenues collection modestly since 2002. Taxes on income and profits, in particular, have been increasing as a share of GDP. This has helped increase tax revenues from 14.2 percent of GDP in 2002 to over 16 percent in recent years. In FY2009 (ended September), total revenues stood at 16.2 percent of GDP due to the impact of the crisis. FY2010 revenues were initially projected to decline further, but thanks to the recovery revenues have also grown substantially. In the first 8 months of FY2010 (October 2009 – May 2010), revenue collection was up 27 percent compared to the previous year. As the economy continues to grow over the next few years, tax revenues are likely to return to around 17 percent of GDP as personal and corporate income tax collection efforts continue to improve, helping to offset lower tax receipts as a result of possible future tax cuts and further rationalization of tariffs.

12

Table 3. Central Government Expenditure, FY2006-2009 (Percent of FY GDP)

FY 2006 2007 2008 2009

General Government Services 2.9 2.9 3.1 3.5

1.1 General public services 0.9 0.8 0.9 0.9

1.2 Defense affairs and services 1.1 1.1 1.2 1.4

1.3 Public order and safety affairs 1.0 1.0 1.0 1.2

Community and social services 6.9 7.5 7.2 8.8

2.1 Education affairs and services 3.6 4.0 3.7 4.3

2.2 Health affairs and services 1.3 1.8 1.7 1.9

2.3 Social security and welfare affairs and services 1.4 1.4 1.3 1.9

2.4 Housing and community amenity affairs and services 0.5 0.2 0.3 0.6

2.5 Religious, cultural and recreational affairs, and services 0.1 0.1 0.1 0.1

Economic services 3.6 3.8 3.3 3.5

3.1 Fuel and energy affairs and services 0.0 0.0 0.0 0.1

3.2 Agricultural, forestry and fishery affairs and services 0.8 1.2 0.9 1.0

3.3 Services, manufacturing affairs, and services, and construction affairs and services

0.1 0.1 0.1 0.1

3.4 Transportation and communication affairs and services 0.7 0.8 0.7 0.7

3.5 Other economic affairs and services 2.0 1.7 1.6 1.6

Miscellaneous and unclassified items 3.1 3.5 3.2 4.4

Total Expenditure 16.5 17.8 16.7 20.2

Memo: Total spending (billion baht) 1,270 1,472 1,532 1,791

Source: Comptroller General’s Department.

B. Fiscal Response to the Financial Crisis and Debt Sustainability

30. In response to the impact of the global financial crisis, in early-2009 the Government announced a two-pronged fiscal stimulus strategy. In February 2009, Parliament approved a supplementary budget of THB116.7 billion, of which THB97.6 billion (US$2.8 billion or 1.1 percent of 2009 GDP) was used to finance stimulus measures, as well as tax reductions costing around 0.45 percent of GDP. The emphasis of the first round of stimulus was on consumption measures for quick implementation. In April 2009 the government announced a second round of stimulus known as the “TKK” (Strong Thailand) program in an amount of THB1.3 trillion over the 2010-2012 period (averaging 4.5 percent of GDP annually).1 The headline figure includes new and already planned

1 As discussed elsewhere, the TKK program aims both at maintaining and raising levels of public investment; therefore, the headline amount was intended as an upper bound on additional deficits that assumed a protracted crisis and high disbursement rates. Please see Table 5 for an analysis of the additionality of the second round of fiscal stimulus.

13

items from the central government’s public investment plan as well as investments by state owned enterprises. The TKK program emphasizes public investments, especially in small-scale infrastructure, favoring projects that could be implemented in the three-year timeframe. 31. The first round of stimulus measures had been largely implemented by September 2009, while execution of the second round is currently underway. Progress on the stimulus is a prior action for this operation and is described in paragraphs 72-83. This section assesses the financing of the fiscal stimulus and its compatibility with fiscal sustainability. 32. The first round of stimulus was financed through domestic borrowing under the Public Debt Management Law. Thailand’s Public Debt Management Act of 2005 authorizes the Government to borrow domestically in any fiscal year up to 20 percent of approved expenditures (including the supplementary budget) plus 80 percent of budgeted principal repayments.2 For 2009, this ceiling limited borrowing to THB440 billion. Although initially there were concerns that the Government’s financing needs would exceed this ceiling, thanks to a recovery of revenues towards the end of the fiscal year the deficit came in at THB420 billion, below the borrowing ceiling. 33. The TKK program was originally intended to be financed outside the budgetary framework due to the limits imposed by the PDM Act, but projects have been increasingly moved on-budget as revenues recovered. Because expenditures cannot exceed expected revenues plus financing, the borrowing ceiling imposed by the Public Debt Management Act effectively limits expenditures to 125 percent of expected revenues. Since the budget for FY2010 was prepared at the height of the financial crisis, revenue estimates were low and greatly constrained expenditures. In light of these severe constraints to the budget envelope and wishing not only to maintain the level of public investments but also to provide a boost that would stimulate the economy, the Government decided to finance the TKK program outside the budgetary framework. Thus the borrowing authority for initial TKK expenditures comes from an Emergency Decree passed in May 2009. An amount of THB 400 billion was originally authorized, of which THB 50 billion were used to replenish the Treasury account and THB 15 billion were used to recapitalize certain state-owned financial institutions. Although the Government originally anticipated the need to borrow an additional THB 400 billion through another exceptional borrowing authorization, the recovery in revenues has led many TKK expenditures to be moved back on budget. 34. The Government’s total financing requirements for TKK expenditures in FY2011 may be as high as THB 470 billion, depending on the pace of implementation of the underlying projects. Financing requirements after taking into account expected disbursement rates as well as those projects moved on-budget are estimated to be approximately THB 150 billion. The Government plans to meet these financing requirements through the remaining funds from the Emergency Decree, as well as borrowing from official creditors (ADB, JICA and World Bank), to which a separate borrowing ceiling applies.3 In addition, actual revenues are likely to exceed the revenue target, which would allow the government to finance additional expenditures through a supplementary budget. Table 4 below summarizes the Government’s financing needs and sources for

2 Each year, approximately 3 percent of the overall budget is earmarked for principal repayments, with any additional principal payments coming due that year being rolled over “off budget”. The 80 percent ceiling applies to the on-budget principal repayments. 3 In addition to the borrowing ceiling of 20 percent of overall expenditures, the government may borrow up to 10 percent of expenditures from foreign sources.

14

FY2010-FY2013.

Table 4. Central Government’s Financing Plan for FY2009 – FY2013 (percent of GDP)4

Source: FPO, PDMO and World Bank calculations and projections. 35. Foreign borrowing, including from the World Bank is needed to finance the planned expenditures in FY2011. The FY2011 budget recently approved by Parliament anticipates THB 2.07 trillion (19.8 percent of GDP) in expenditures, including THB 345 billion (about 16.5 percent of the total budget) in public investments. The budget contains a number of large “headline” increases – the announced level of spending represents a 22 percent increase over the FY2010 budget, whereas the investment budget was announced as an increase of about THB 100 billion (over 60 percent) from FY2010. However, most of this increase represents TKK investments that have now been moved on-budget. Without additional financing from multilateral sources such as the World Bank, the Government would only be able to finance about THB 165 billion out of approximately THB 250 billion in expected TKK expenditures. 36. A debt sustainability analysis and indicators of market perceptions suggest that the Government has sufficient fiscal space to implement the stimulus. Under conservative assumptions (permanent expenditure increases but no new revenue-raising measures with growth below potential through 2014), Thailand’s debt ratios are projected to decline from a peak of 46.6 percent in 2014 to 45.0 percent of GDP by 2020. Reflecting the market’s view of the strength of Thailand’s public balance sheets, credit default swap (CDS) spreads and bond yields have remained at relatively low levels notwithstanding higher deficits and the political turmoil. 37. Thailand’s long track record of fiscal prudence underpins the assumption that deficits will enter a declining path in FY2012. In FY2010, the budget deficit will decline to about 1.9 percent of GDP from 4.4 percent in FY2009 even after taking into account the fiscal stimulus.5

4 Figures are on a cash basis. Differences between cash and GFS bases are small for budgetary balances, but relatively large (around 1 percent of GDP) for the off-budget balance. This explains most of the differences in projected fiscal balances in this document compared to fiscal forecasts in the IMF’s most recent Article IV report. 5 The government may indeed run a surplus when the off-budget TKK is excluded. As noted elsewhere, pessimistic GDP and revenue projections at the time of budget formulation greatly constrained expenditures in FY2010.

(Fiscal Years) 2004 - 2008 av 2009 2010 2011 2012 2013 2020

Financing Needs1. Revenues 17.6 15.9 16.6 16.8 16.9 17.0 17.32. Expenditures 18.2 21.8 18.4 19.8 19.3 19.1 19.1

On-budget 18.2 21.7 16.1 18.4 18.3 19.1 19.1TKK, off-budget … 0.2 2.3 1.4 1.0 … …

3. Off-budget Balance, excl. TKK -0.1 1.5 -0.2 -0.2 -0.2 -0.2 -0.24. Net Financing Needs (1–2+3) -0.8 -4.4 -1.9 -3.2 -2.6 -2.3 -2.0

Financing Sources

1. Net Domestic Borrowing, PDM Act … 4.3 -0.1 1.8 1.6 1.9 1.72. Domestic Borrowing, Emergency Decree … 0.2 2.1 0.6 0.7 … …3. Foreign Borrowing (WB, ADB, JICA) … 0.0 0.0 0.5 … … …4. Other 1/ … … … 0.3 0.3 0.4 0.35. Total Sources (1+2+3+4) 4.4 1.9 3.2 2.6 2.3 2.0

1/ For 2011, assumes a supplementary budget as actual revenues are expected to exceed budgeted revenues. For 2012 and beyond,assumes other foreign financing.

15

This is in sharp contrast to the 5.5 percent deficit expected in early 2009. While the deficit is expected to increase in FY2011, the analysis suggests that Government can afford the stimulus package without jeopardizing debt sustainability as deficits are expected to decline starting in FY2012.This assumption is supported by the Thai Government’s consistent pursuit of a conservative fiscal stance of low budget deficits or surpluses. Since 2002, budget deficits were no more than 2 percent of GDP and the primary balance was in surplus twice between 2005 and 2008. In addition, the Ministry of Finance has recently signed a memorandum of understanding with the bureau of the budget committing to balancing the budget within five years. 38. As a result of Thailand’s prudent fiscal stance, public debt stocks had been declining until the onset of the financial crisis and the debt composition had been managed to minimize the impact of external shocks. Public and publicly-guaranteed debt, including non-guaranteed debt of state-owned enterprises, has been falling as a share of GDP from a peak of 58 percent in 2000 to 38 percent at end-2008. Due to the financial crisis, debt levels rose to 44 percent at end-2009, but remain below the 60-percent indicative ceiling under Thailand’s fiscal sustainability framework and earlier forecasts. The composition of the debt stock has also shifted. Foreign-currency debt, which accounted for about 39 percent of public debt in 1999, was reduced to about 10 percent of the portfolio by end-2009. In addition, 40 percent of the government’s external debt has been swapped back into local currency, so that risks from exchange rate fluctuations are minimal. There has also been a move towards issuing fixed-rate government bonds, therefore minimizing risks from interest rate volatility. The average time to maturity had been increasing, but due to the financial crisis the Government was forced to borrow primarily in shorter tenors in 2009. The maturity profile started to be extended again in 2010. 39. The baseline scenario is relatively conservative, assuming a return to pre-crisis levels of growth only by 2014, permanently higher expenditures and no new revenue-raising measures. In addition to the projections described in Table 4 above, the baseline scenario assumes that real GDP growth converges to its potential of 5.0 percent by 2014 and the primary public sector balance moderates to a deficit of two percent of GDP – above historical averages of about 0.8 percent of GDP. This permanent increase in the deficit is driven by the government’s adoption of new social policies (some initiated as part of the stimulus package) while as a conservative assumption revenues as a share of GDP are only expected to (slowly) return to pre-crisis levels. The baseline scenario incorporates the impact of the stimulus packages, which can be seen in the high budget deficit of 2009-2012 averaging 3.0 percent of GDP, well above the post-98 crisis average of 0.9 percent of GDP. Levels of new foreign and domestic borrowing are consistent with the Government’s proposed funding sources. 40. Thailand’s external debt is owed primarily to official creditors and is therefore at below-market terms. Even considering the projected shift in financing towards a greater share of external debt and ignoring the fact that much of the external debt has been hedged, Thailand’s public external debt-to-GDP ratio does not exceed 17 percent under the most severe standard shock (an unlikely 30 percent depreciation). This is in contrast to foreign reserves amounting to 48 percent of GDP. Given Thailand’s high levels of exports, debt-to-export ratios are very low. 41. Overall external debt (both public and private) is also low at 26 percent of GDP (US$74 billion). About 40 percent of the external debt is short-term, but trade credits represent almost two-thirds of private short-term debt, while another 18 percent are inter-company loans. Public external debt (primarily owed by state-owned enterprises) comprises 19 percent of total external debt and

16

only 1.9 percent is short-term. External debt service ratios are manageable at 5.2 percent of exports overall and total external debt was 51 percent of international reserves as of end-March 2010. 42. Under the baseline scenario, Thailand’s public debt-to-GDP ratio does not exceed 46 percent of GDP and ratios start to decline (albeit slowly) in 2015. After an initial spike due to the substantial financing needs that arise from the fiscal stimulus, debt ratios resume their downward trend. The debt-to-GDP ratio is expected to be approximately 45 percent of GDP by 2020 following a peak of 46.6 percent in 2014. The slow decline under the baseline arises from conservative assumptions on fiscal balances, which remain lower than their post-financial crisis average throughout the projection period. Debt projections are substantially lower compared to April 2009, indicating the magnitude of the recovery. 43. Public debt sustainability is resilient to worse-than-expected outcomes in 2011-2012, but a permanent shock to growth could lead to an upward path of public debt. The Debt Sustainability Analysis (DSA) considered the effect on debt ratios of (i) a real GDP contraction of 0.9 percent in FY2011; (ii) a 30 percent nominal depreciation of the Thai baht; (iii) the realization of contingent liabilities adding up to ten percent of GDP; and (iv) a combination of the growth and exchange rate shocks (Table 5). The contingent liability shock is the most severe, leading the debt-to-GDP ratio to peak at 55 percent, but favorable debt dynamics lead to a declining debt path. The greatest risks to debt sustainability come from protracted growth slowdown and lack of fiscal consolidation following the resumption of growth. If primary deficits remain at 1.5 percent of GDP – high for historical standards but almost 1 percentage point of GDP below FY2009 levels – the debt-to-GDP ratio would remain on a rising trend in the longer term and would exceed 50 percent by the end of the projection period. The scenario with permanently low growth also leads to rapidly increasing debt ratios. This emphasizes the importance of taking advantage of the crisis to enhance competitiveness and ensure a return to sustainable growth.

17

Figure 5. Thailand: Public Debt Sustainability Analysis (As percent of GDP, unless otherwise noted)

1/ Assumes that real GDP growth is at the baseline level minus one standard deviation divided by the square root of the length of the projection period. 2/ Assumes that real GDP is at the baseline level minus one standard deviation in 2011. 3/ Assumes the primary balance is kept at a deficit of 1.5 percent of GDP throughout the projection period. Source: World Bank calculations based on data from PDMO.

39

45

35

40

45

50

55

602005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Real GDP growth and primary balance at historical averages

Baseline 55

48

45

35

40

45

50

55

60

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Permanently lower GDP growth 1/

Real GDP growth shock in 2011 2/

Baseline

51

45

35

40

45

50

55

60

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Primary balance shock 3/ Baseline

50

4645

35

40

45

50

55

602005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

10 percent of GDP increase in other debt‐creating flows in 2011

Combination of growth and real depreciation shocks

Baseline

18

Table 5. Debt Sustainability Analysis – Sensitivity Analysis (Fiscal Years)

44. Market indicators confirm Thailand’s strong financial position. When the global financial crisis struck, Thailand was clearly perceived as less risky than some of its regional peers (reflected in Figure 6 as the sharp decline in Q3 2008). As the recovery took hold and financial conditions in Korea and Indonesia normalized, Thailand’s credit default swap (CDS) spreads declined less rapidly than in those countries, before rising slightly in April and May 2010 on account of the political turmoil. CDS spreads have declined since May and remained stable at levels well below their peaks during the crisis; spreads are comparable to Korea, 20 – 30 bps higher than China and Malaysia, and about 40 bps lower than the Philippines and Indonesia. Similarly, Thailand’s government bond yield curve has been generally stable (especially in the more liquid intermediate segment of the curve between 3 and 7 years) and driven primarily by the overall interest rate environment, suggesting that markets have not placed a risk premium on the Government’s debt as a result of expansionary fiscal policies (Figure 7). 45. In conclusion, risks to fiscal sustainability are low, and the macroeconomic policy framework is adequate. The financial crisis and resulting policy response put considerable stress on the macroeconomic balances and the political turmoil in 2009-10 made the macro challenge more difficult. However, Thailand’s history of prudent macroeconomic management, conservative public debt management and liquid financial sector provided ample space to respond. The financing plan is prudent in accessing reasonably priced debt. As will be discussed in Section V, the stimulus has been mostly temporary with most tax and transfer provisions having a sunset clause and the remainder comprised of social and infrastructure expenditures that may be accommodated even without revenue measures.

2010 2011 2012 2013 2014 2015 2020

Baseline 44 46 46 46 46 46 45

A. Alternative scenarios

A1. Real GDP growth and primary balance are at historical averages 44 43 42 42 41 41 39A2. Primary balance shock 44 45 46 47 47 48 51A3. Permanently lower GDP growth 1/ 44 46 47 48 48 49 55

B. Bound tests

B1. Real GDP growth grows by 0.8 percent in 2012 44 48 48 49 49 49 48B2. One-time 30 percent real depreciation in 2011 44 47 48 47 47 46 44B3. 10 percent of GDP increase in other debt-creating flows in 2011 44 55 55 55 54 53 50

Debt-to-GDP Ratio

Projections

19

Figure 6. Thailand 5-year Credit Default Swaps Figure 7. Thailand Yield Curve

Source: Datastream, World Bank staff calculations Note: Regional currency basket includes China, Malaysia, Indonesia, Philippines, Hong Kong SAR, China, Singapore and Korea.

Source: Thai Bond Market Association.

C. Political Context

46. The roots of the recent political crisis go back to at least 2001. The Thai Rak Thai (TRT) Party, headed by Thaksin Shinawatra, was elected by a landslide that January, a first for Thailand’s democracy which has been characterized by short-lived coalition governments. Thaksin’s Government was the first to serve a full four-year term and was re-elected by another overwhelming majority in 2005. Opponents gathered under the People’s Alliance for Democracy (PAD) and began a series of public protests, accusing Thaksin’s Government of favoritism, corruption and conflict of interest. In September 2006, a bloodless coup overthrew the TRT Party and appointed an interim Government, which oversaw the drafting of the 2007 Constitution. An interim Constitutional Tribunal was also installed. In May 2007, the Tribunal dissolved the TRT and three other political parties found guilty of violations of electoral laws. Former TRT members then regrouped under a new name, the People’s Power Party (PPP), contested in the December 2007 election, and emerged as the head of a Coalition Government. 47. The political crisis escalated in August 2008 and the situation remained tense through December that year. The Coalition Government was led by PPP leader Samak Sundaravej. In May, 2008, the PAD, which had set the stage for the 2006 coup, returned to the streets to protest an attempt to amend the Constitution and grant amnesty to banned politicians, including Mr. Thaksin. In August, they stormed the National Broadcasting Corp. headquarters, which they accused of being the mouthpiece of the pro-Thaksin Government, and successfully seized Government House. In September, Mr. Samak was forced out on a conflict of interest charge and Mr. Thaksin’s brother-in-law, Somchai Wongsawat, took over as Prime Minister. In October, a clash between the police and the PAD near Parliament left two persons dead and about three hundred injured. Then in November, the PAD seized the public areas of Bangkok’s airports leading to their closure and paralyzing Thailand’s air traffic for almost two weeks, causing substantial losses for Thailand’s tourism and export industries.

0

100

200

300

400

500

600

-250

-200

-150

-100

-50

0

50

basis

poi

nts

Thailand 5-year Credit Default Swaps

Thailand minus regional peers (left axis)

Thailand 5-year CDS Spreads (right axis)

Regional peers: China, Indonesia, Malaysia, Philippines and Korea. Lower values denote improvements.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Yield (percent)

Time to maturity (years)

2007 av. ('pre‐crisis')

12/15/2008 ‐Prior to Announcement of Stimulus

3/31/2009 ‐ Fiscal stimulus under implementation