Embed Size (px)

Citation preview

Document of

The World Bank

Report No. 52025-ME

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED LOAN

IN THE AMOUNT OF €59.1 MILLION (US$85 MILLION EQUIVALENT)

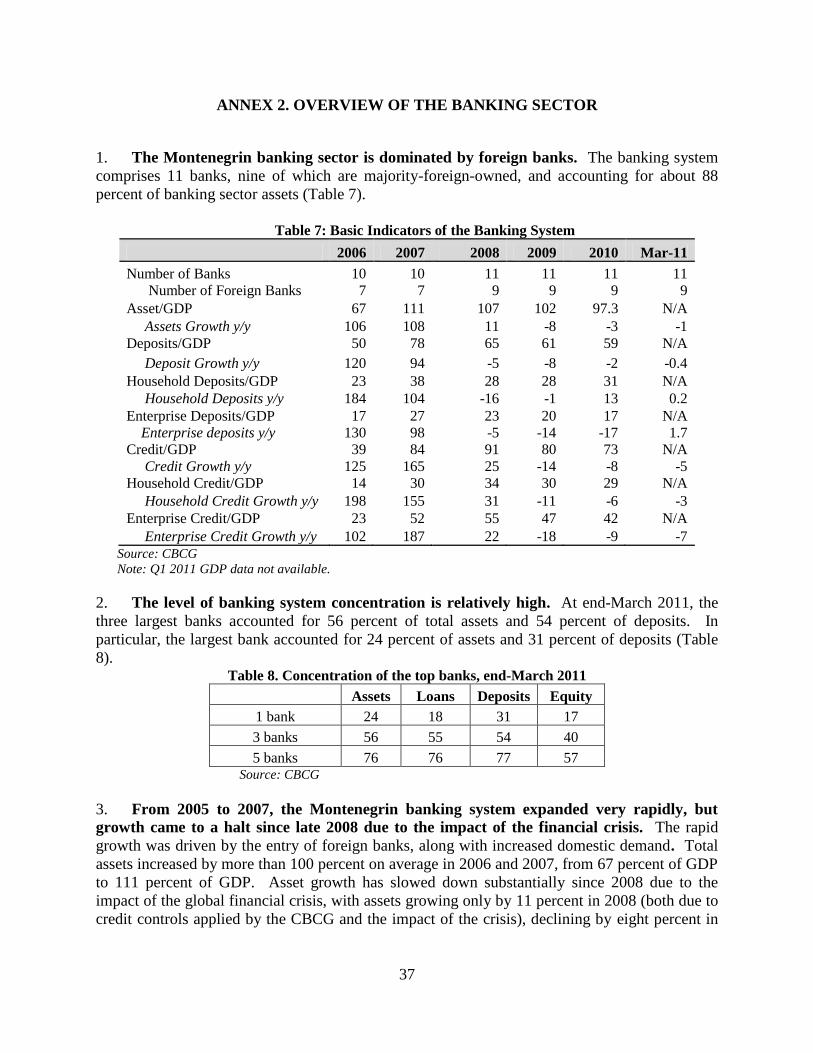

TO

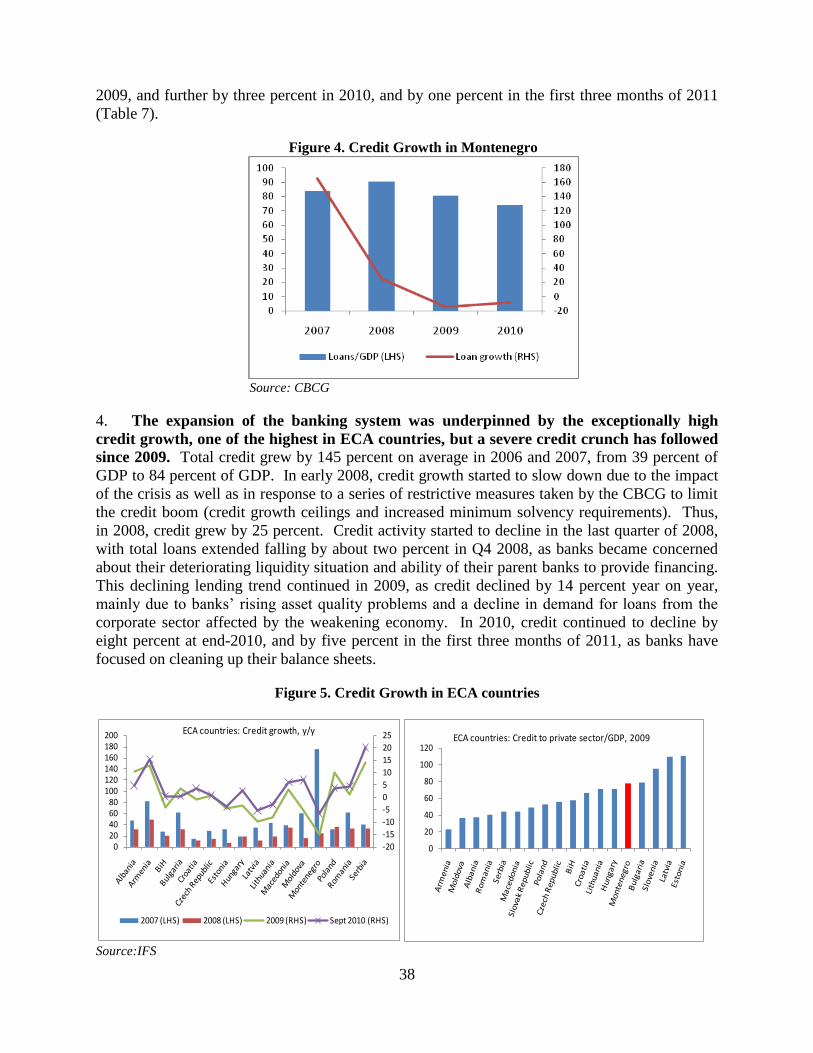

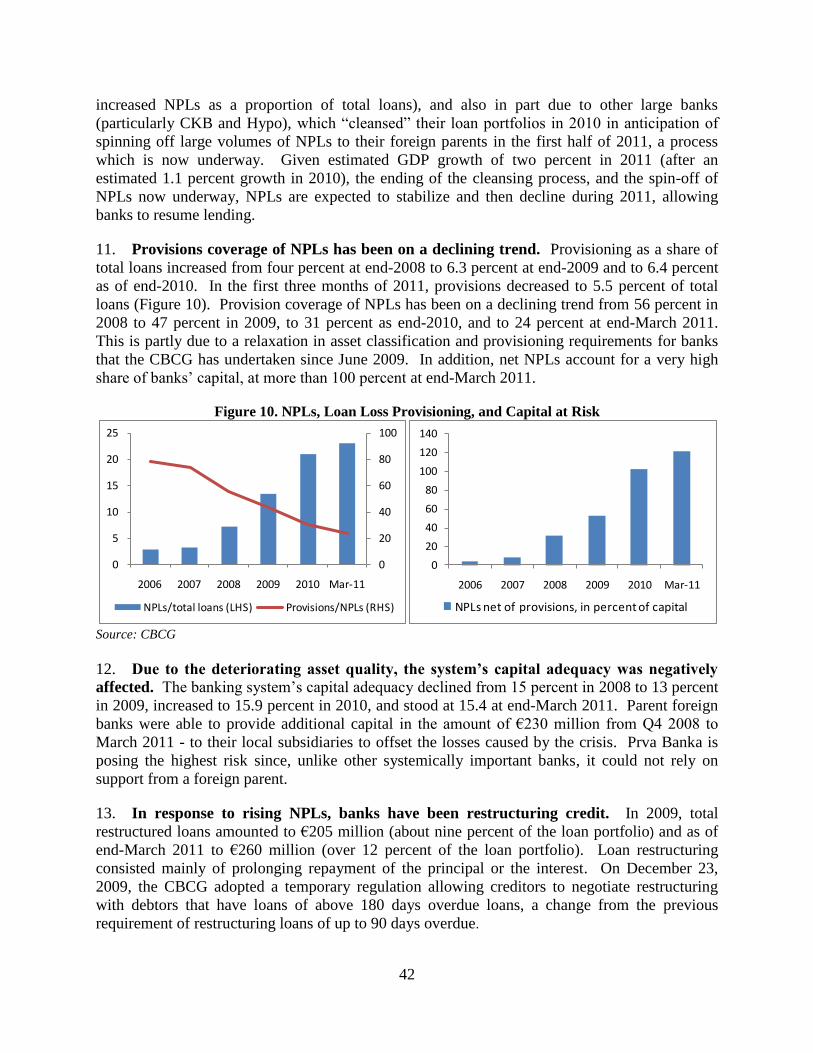

MONTENEGRO

FOR A

FIRST PROGRAMMATIC FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

July 22, 2011

Finance and Private Sectors Development Unit

South East Europe Country Unit

Europe and Central Asia Region

This document has a restricted distribution and may be used by recipients only in the performance of their official

duties. Its contents may not otherwise be disclosed without World Bank authorization.

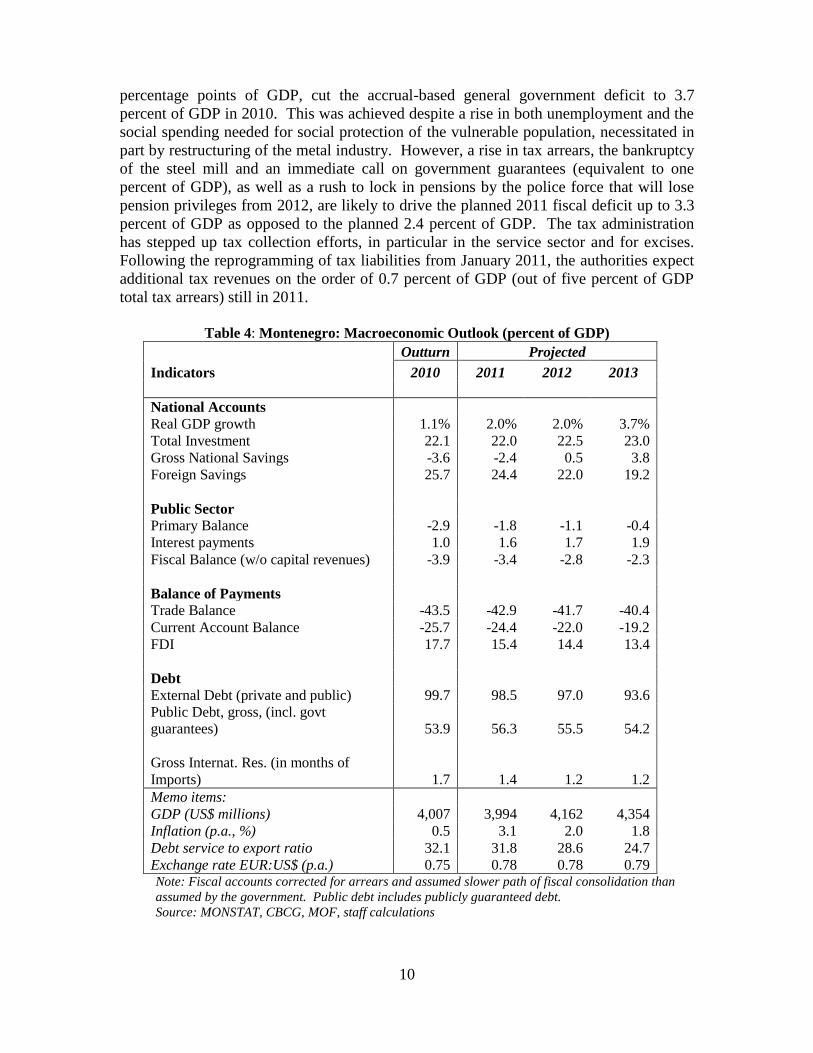

Pub

lic D

iscl

osur

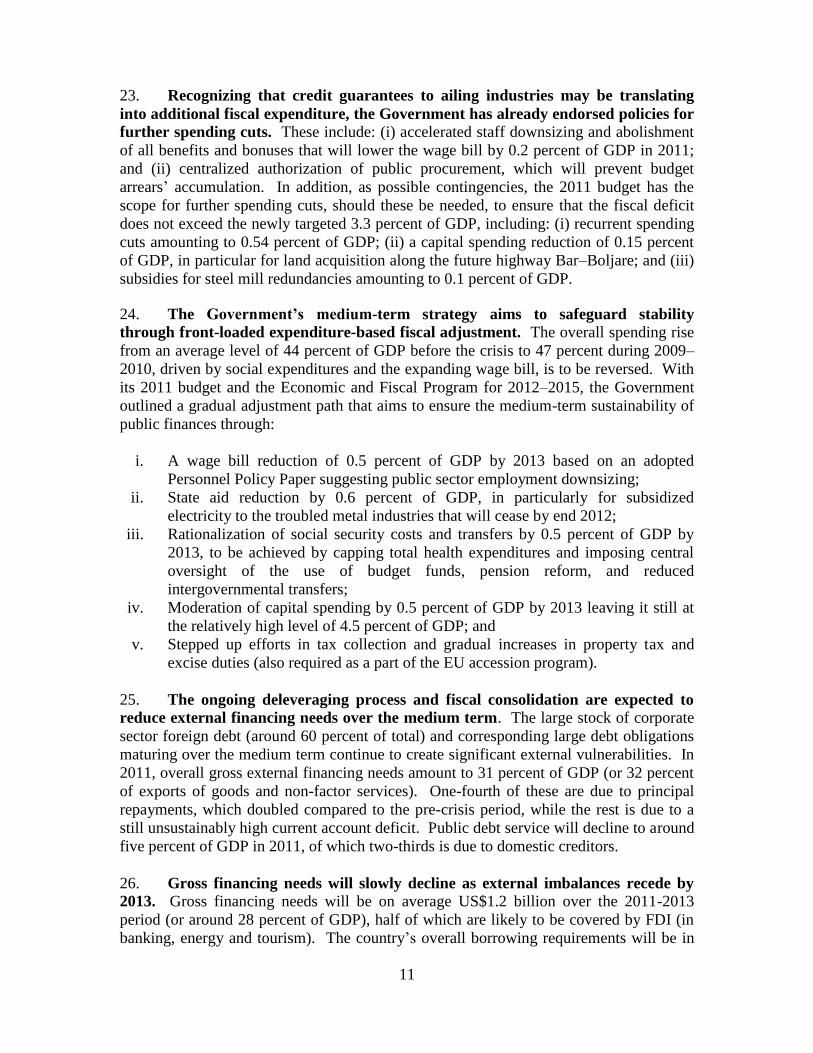

e A

utho

rized

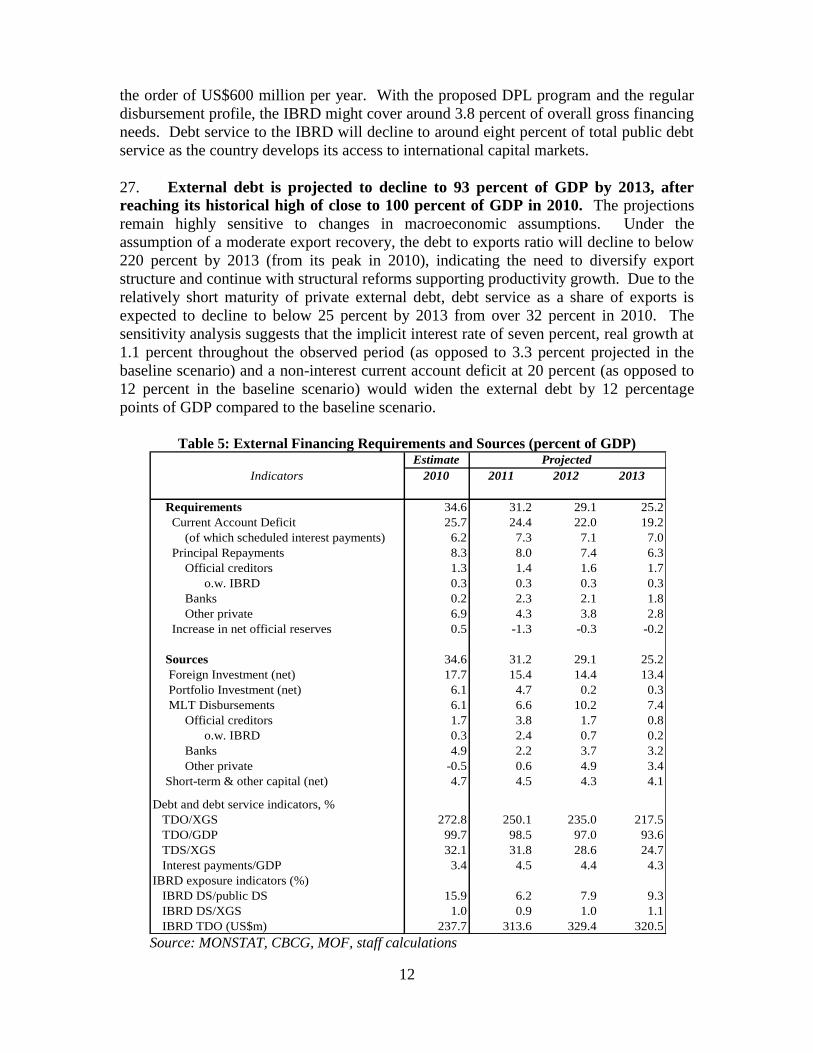

Pub

lic D

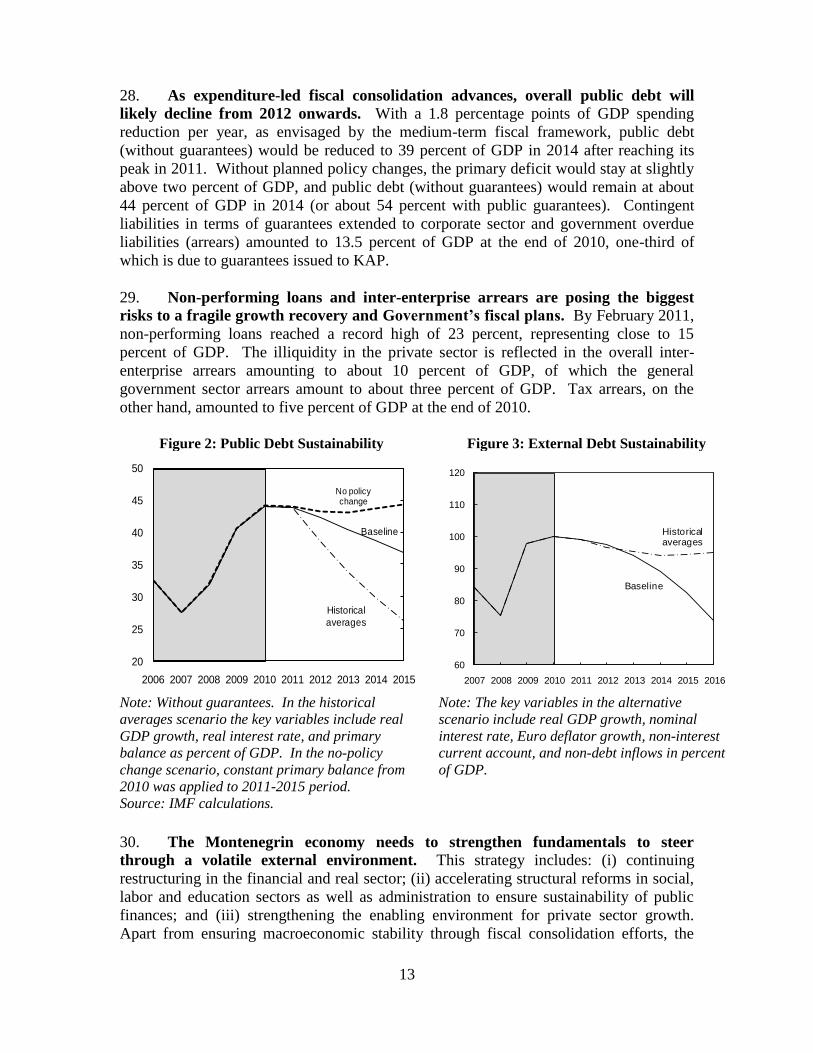

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

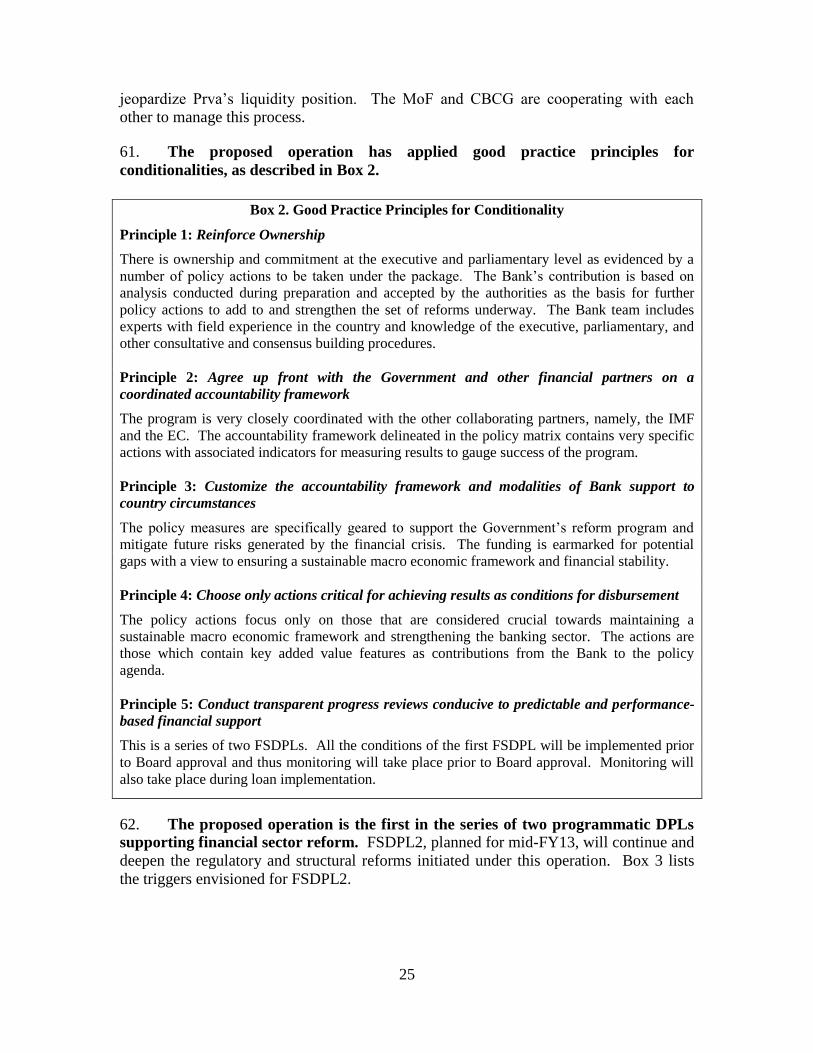

Pub

lic D

iscl

osur

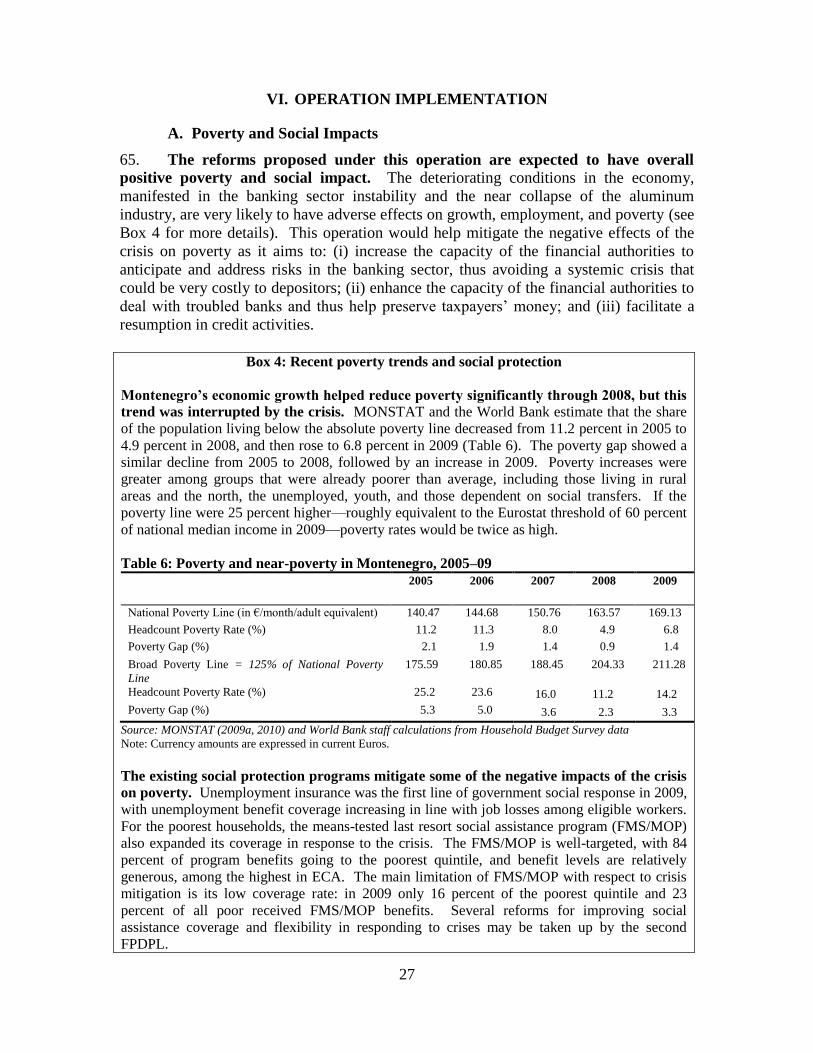

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

MONTENEGRO – GOVERNMENT FISCAL YEAR

January 1 – December 31

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of May 31, 2011)

Currency Unit EUR

US$1.00 €0.71

Weights and Measures

Metric System

ABBREVIATION AND ACRONYMS

CAMELS

Capital Adequacy, Asset Quality, Management,

Earnings and Liquidity and Sensitivity to market

risk IIA Institute of Internal Auditors

CAR Capital Adequacy Ratio IMF International Monetary Fund

CBCG Central Bank of Montenegro KAP Kombinat Aluminijuma Podgorica

CPS Country Partnership Strategy KfW

Kreditanstalt für Wiederaufbau / German

Development Bank

DPF Deposit Protection Fund LOLR Lender of Last Resort

DPL Development Policy Loan LTD Loan-to-deposit ratio

EBRD

European Bank for Reconstruction and

Development MoF Ministry of Finance

EC European Commission MPBS

Measures for Protection of the Banking

System

ECA Europe and Central Asia NPL Nonperforming Loan

EIB European Investment Bank PEFA

Public Expenditure and Financial

Accountability Assessment

EPCG Elektroprivreda Crne Gore AD PFM Public Financial Management

EU European Union PPI Producer Price Index

FDI Foreign Direct Investment RBN Rudnici Boksita Nikšić

FIRST

Financial Sector Reform and Strengthening

Initiative ROA Return on Assets

FMS Family Material Support ROE Return on Equity

FSAP Financial Sector Assessment Program ROSC

Report on The Observance of Standards

and Codes

FSDPL Financial Sector Development Policy Loan SAC Structural Adjustment Credit

FX Foreign Exchange SAI State Audit Institution

GDP Gross Domestic Product SAP Supervisory Action Plan

GoM Government of Montenegro SEE Southeast Europe

IBRD International Bank for Reconstruction and

Development TA Technical Assistance

IFC International Finance Corporation WB World Bank

Vice President:

Country Director:

Sector Director:

Sector Manager:

Task Team Leader:

Philippe Le Houérou

Jane Armitage

Gerardo Corrochano

Lalit Raina

Alexander Pankov

iii

MONTENEGRO

FIRST PROGRAMMATIC FINANCIAL SECTOR DEVELOPMENT POLICY

LOAN

TABLE OF CONTENTS

LOAN AND PROGRAM SUMMARY ............................................................................ iv I. INTRODUCTION ...................................................................................................1

II. COUNTRY CONTEXT...........................................................................................1 A. Recent Economic Developments ..........................................................1 B. Banking Sector Developments ..............................................................4 C. Macroeconomic Outlook and Debt Sustainability ................................9

III. THE GOVERNMENT’S REFORM PROGRAM .................................................14 A. Overall Reform Program .....................................................................14 B. Financial Sector Reforms ....................................................................15

IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM .............................18 A. Link to the Country Partnership Strategy ............................................18

B. Collaboration with the IMF and other Donors ....................................19 C. Relationship to Other Bank Operations ..............................................19

D. Analytical Underpinnings ...................................................................20 E. Lessons Learned ..................................................................................20

V. THE PROPOSED OPERATION ...........................................................................21

A. Objective and Rationale ......................................................................21 B. Operation Description and Policy Areas .............................................23

C. Expected Outcomes of the Operation .................................................26

VI. OPERATION IMPLEMENTATION ....................................................................27

A. Poverty and Social Impacts .................................................................27 B. Environmental Aspects .......................................................................28

C. Implementation, Monitoring, and Evaluation .....................................28 D. Fiduciary Aspects ................................................................................28 E. Disbursement and Audit Arrangements ..............................................30 F. Risks and Risk Mitigation ...................................................................31

ANNEX 1. Policy Matrix ..................................................................................................35 ANNEX 2. Overview of the Banking Sector .....................................................................37 ANNEX 3. Letter of Development Policy .........................................................................45 ANNEX 4. Fund Relation Note .........................................................................................53 ANNEX 5. Country at a glance .........................................................................................56

ANNEX 6. Country Map ...................................................................................................57

The First Programmatic Financial Sector Development Policy Loan is prepared by a Bank team consisting of Alexander

Pankov (Task Team Leader, ECSPF/EASFP), Aquiles Almansi (FPDPO), Sanja Madzarevic-Sujster (ECSP2), Danijela

Vukajlovic-Grba (ECSP2), Martin Melecky, Aurora Ferrari (ECSF1), Bujana Perolli (ECSF2), Julie Rieger (LEGEM),

Angela Prigozhina (ECSF1), Aleksandar Crnomarkovic (ECSO3), Kenneth Simler (ECSP3), Andrew Lovegrove, Ross

Delston, and Djurdjica Ognjenovic (ECSPF expert consultants). Jan-Peter Olters (WB Resident Representative in

Montenegro) provided critical guidance.

iv

LOAN AND PROGRAM SUMMARY

MONTENEGRO

FIRST PROGRAMMATIC FINANCIAL SECTOR

DEVELOPMENT POLICY LOAN

Borrower The Government of Montenegro

Implementing Agency

The Ministry of Finance (MoF) of Montenegro will be responsible

for overall implementation of the proposed operation. The Central

Bank of Montenegro (CBCG) is closely involved in the work on

most prior actions.

Financing Data

IBRD Loan

Front end fee: 0.25%

Maturity: 20 years

Interest rate: 6 month EURIBOR for EUR plus fixed spread

Amount: €59.1 million

Operation Type

This operation is the first in the series of two Programmatic

Financial Sector Development Policy Loans (FSDPLs).

Main Policy Areas The proposed loan supports a comprehensive program of measures

to strengthen the banking sector, with a view to mitigating the

impact of the global financial crisis and increasing the resilience of

the sector to possible future shocks. The specific reforms proposed

to strengthen the banking sector are in the following areas: (i)

maintaining market confidence; (ii) strengthening the bank liquidity

framework; (iii) assessing and addressing banking sector

vulnerabilities; (iv) enhancing the regulatory framework; and (v)

problem bank restructuring. These reforms are an integral part of

Montenegro’s EU accession strategy insofar as they aim to bring the

supervisory and regulatory framework for the banking sector closer

to EU practices.

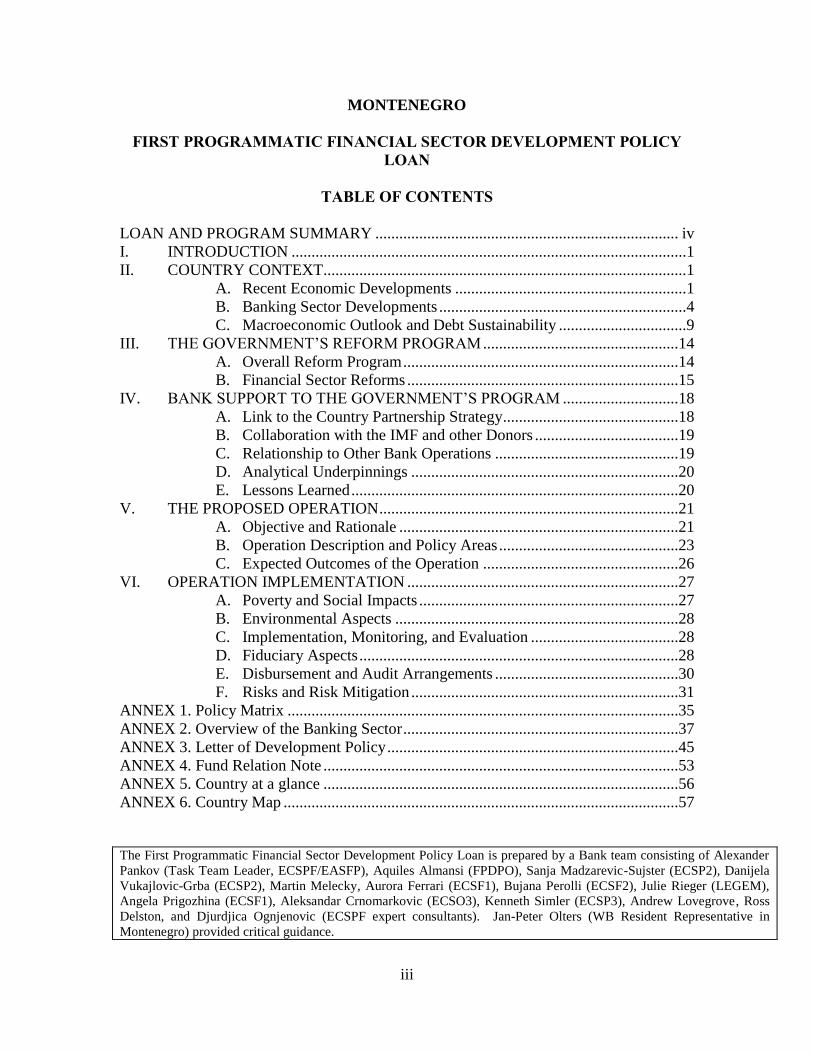

Key Outcome

Indicators

The expected outcomes of this operation are: (i) increased

confidence in the banking sector; (ii) enhanced ability of the CBCG

to provide emergency liquidity assistance; (iii) effective supervision

of the banking system consistent with Basel Core Principles; (iv)

strengthened legal authority of the CBCG for resolution of problem

banks according to international and EU good practices; and (v)

Prva Banka no longer poses a systemic and fiscal risk.

v

The key outcome indicators are:

Stabilization of deposits (baseline: -23 percent decline from

September 2008 to March 2011; target: positive growth);

Resumption of prudent lending activities (baseline: -26 percent

decline from September 2008 to March 2011; target: positive

growth);

Adequate liquidity in the banking sector (target: ratio of liquid

assets to due liabilities to remain in compliance with the CBCG

norms at a ratio of 1, calculated as an average for all working

days in a ten-day period);

Improved quality of loan portfolio (baseline: system’s NPL ratio

at 23 percent in March 2011; target: NPLs below 8 percent);

Well-capitalized banks (baseline: average CAR of banking

system at 11.9 percent in June 2009; target: average CAR of

banking system to remain above 12 percent);

Implementation of Supervisory Action Plan for Prva Banka and

withdrawal of central government deposits from this bank.

Program Development

Objective(s) and

Contribution to CAS

The overarching objective of the operation is to strengthen the

banking sector, which is a critical pre-condition for sustainable

economic recovery and balanced private sector-led growth.

The reform program supported by this operation falls under Pillar I

of the Country Partnership Strategy (CPS), namely, to support EU

integration through strengthening institutions and competitiveness in

line with EU accession requirements. The proposed operation

contributes to this strategic priority by supporting reforms in the

legal, regulatory, and supervisory framework for the banking sector

that are in line with international good practices and EU standards.

Risks and Risk

Mitigation

The proposed First Programmatic Financial Sector Development

Policy Loan (FSDPL1) is a high risk operation. The key risks are as

follows:

1. Economic risk. Economic risks are substantial given

Montenegro’s high external vulnerability and the volatile external

environment in which the country operates. Slower than expected

growth in Southeast Europe and the EU could dampen

Montenegro’s recovery, which would further strain the fiscal stance.

Slower recovery would affect the corporate sector performance and

consequently the financial sector. Montenegro’s heavy reliance on

tourism revenues and exports to Europe makes it vulnerable to any

deterioration in regional stability or slowdown of growth in the EU.

This could jeopardize the achievement of planned medium-term

vi

macroeconomic and social outcomes. Furthermore, the country’s

euroization, high level of external debt and large debt service

requirements over the medium term render the Montenegrin

financial sector vulnerable to a slowdown in capital inflows and call

for more prudent fiscal policy. Finally, given the small size of the

country, even a small shock may have a sizeable impact on the

economy.

These risks are partially mitigated by the proposed program of

strengthening the banking sector to enable it to resume lending to

the private sector, and thus encouraging economic growth. In

addition, the Government is committed to tightening fiscal policy

more than provided for in the medium-term fiscal framework for

2012-2015 should macroeconomic conditions turn out to be worse

than currently estimated. Finally, the implementation of the Action

Plan for opening negotiations with the EU, which would lead to a

legal system comparable to that of EU countries, and the

Government’s structural reform program that aims to increase

competitiveness, will contribute to improved investor confidence.

2. Financial instability risk. The banking sector remains

fragile and financial instability can return as a result of external or

internal shocks. Prva Banka in particular remains vulnerable and

lacks the support of a strong strategic investor or a parent foreign

bank, which is provided to the other three systemic banks. This risk

is directly mitigated by the proposed reforms of strengthening the

liquidity framework, the regulatory framework, the deposit

insurance scheme, implementing supervisory action plans, and

dealing with problem banks.

3. Governance risk. EU and domestic observers have raised

concerns in the past about the lack of transparency, and the

influence of the organized crime on politics and the economy. With

encouragement from the EU and other international observers

(including the Bank), Montenegrin authorities are making a

concerted effort to correct this perception. Specifically, the

legislative changes and more robust supervision efforts supported by

this operation are expected to strengthen the regulator’s standing and

improve governance standards in the banking sector.

4. Implementation risk. Implementation of the program is

dependent on consistent collaboration amongst authorities,

especially between the MoF and the CBCG. While there seems to

be broad support for the restoration of banking sector stability and

its relevance for the EU accession agenda, the long preparation

process for the FSDPL1 reflects the politically sensitive and

technically complex nature of the proposed reforms. Going forward,

vii

the CBCG will need to use its strengthened mandate to enforce

prudential norms, require sound capital buffers, and take appropriate

supervisory measures on problem banks. Its actions need to be fully

coordinated with, and supported by the Government, without

jeopardizing its operational independence. To mitigate this risk, the

authorities and the Bank have jointly promoted an inclusive,

consultative approach in designing the program, seeking to foster a

mutual understanding and agreement on the content of the reforms.

The programmatic approach, with the second operation scheduled

for FY13, is also expected to mitigate the implementation risk.

Operation ID P116787

1

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT FOR A PROPOSED FIRST PROGRAMMATIC

FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

I. INTRODUCTION

1. This document describes the first in the series of two Programmatic

Financial Sector Development Policy Loans (FSDPLs) to Montenegro in support of

a comprehensive banking sector reform program. The objective of the operation is to

support the authorities’ efforts to strengthen the banking sector, in order to mitigate the

impact of the global financial crisis and increase the resilience of the sector to possible

future shocks. The main areas of reform are: (i) maintaining market confidence; (ii)

strengthening the bank liquidity framework; (iii) assessing and addressing banking sector

vulnerabilities; (iv) enhancing the regulatory framework; and (v) problem bank

restructuring. The program supported by the proposed operation would be implemented

primarily by the Ministry of Finance (MoF) and the Central Bank of Montenegro

(CBCG). The proposed operation is in the amount of €59.1 million (US$85 million

equivalent). The second FSDPL is planned for early FY13 and would be in the amount

of US$20 million equivalent.

II. COUNTRY CONTEXT

A. Recent Economic Developments

Pre-crisis Developments

2. Following the country’s independence in 2006, the Montenegrin economy

grew rapidly averaging nine percent per year, well above the country’s long-term

potential of around 3.5 percent. The growth was largely fuelled by a significant inflow

of foreign direct investment (FDI) and foreign bank loans that amounted to an average of

24 percent of GDP over 2007-2008. Over the same period, a gross fixed investment to

GDP ratio of 37 percent almost doubled compared to the period since 2001, paralleled

with significant rise in household and government consumption.

3. Pro-cyclical fiscal policy contributed to the economic boom. Although the

general government balance was in surplus (four percent of GDP on average in both 2006

and 2007), cyclically adjusted balances point to the existence of a loose fiscal policy

stance. Good revenue performance was driven by high indirect tax revenues collected on

booming imports. High revenues allowed an increase in spending (from 42 percent of

GDP in 2006 to over 50 percent of GDP in 2008), but the Government of Montenegro

(GoM) also took advantage of the additional revenues to prepay some of its debt,

reducing it to 29 percent of GDP by end-2008. The expenditure growth was to a large

extent attributed to a surge in capital expenditure, although current expenditures

increased as well, especially the wage bill and current transfers (at 11 and 19 percent of

GDP in 2008, respectively).

2

4. Domestic demand growth fuelled large macroeconomic imbalances. Given

the limited domestic production of tradables, increased consumption led to a rise in

imports and widening of the current account deficit (from 8.5 percent of GDP in 2005 to

50.7 percent of GDP in 2008)1. The current account deficit was exacerbated by

exponential credit growth, largely financed by lending from foreign parent banks to their

Montenegrin subsidiaries. As a result, the loan to deposit ratio increased to 169 percent

in 2008, contributing to the overheating of the economy. Real gross wages grew by 18

percent on average in the three-year period preceding the crisis, which paralleled

international food and energy price increases, and contributed to an inflation rate of 7.4

percent in 2008.

Crisis Impact and Recent Trends

5. Montenegro was hit hard by the global financial crisis in late 2008. External

demand for Montenegrin exports (in particular for aluminum and steel) declined by

double digits, which coupled with domestic problems in the financial and corporate

sectors, led to an abrupt economic slowdown. A double-digit fall of manufacturing,

construction, transport and tourism in 2009 was only partially compensated by growth in

energy production and agriculture, leading to an estimated economic decline of around

5.7 percent in 20092. The massive drop in production in the heavily indebted and over-

staffed Aluminum Company (KAP) alone, the country’s largest exporter and industrial

producer, accounted for about 1¼ percent decline in GDP.

6. The economic downturn reduced previous gains made in living standards.

Total employment declined by almost seven percent from the second half of 2009 to end-

2010, despite of the moderation of wages and shortened working hours. Unemployment

increased to 13 percent, two percentage points up from its low in 20083. A recent poverty

analysis confirmed that the poverty rate increased to 6.8 percent in 2009, after having

declined from 11.3 percent in 2006 to below five percent in 2008. Almost a quarter of

employees were affected by deteriorating labor market conditions during the crisis,

including 10 percent that experienced wage arrears and another 10 percent that suffered

salary reductions. About 30 percent of crisis-impacted households increased labor

supply, either by having a non-working member seek work or having working members

seek additional work4.

1 However, balance of payments statistics are likely exaggerating these numbers. Namely, the 2009

decision by MONSTAT to change the trade statistics from 2007 to a special regime led to a deterioration of

the current account estimate in 2008 by some 18 percentage points of GDP. Statistics of service exports,

private sector financial and capital transactions also require further strengthening, although some initial

efforts have been made to address the shortcomings. 2 The National Accounts data require further strengthening to produce higher frequency estimates

(quarterly data) and reliable annual data based on the financial reports, which business entities have been

required to submit starting in 2009. The existence of a substantial unofficial or unobserved economy in

Montenegro also affects the accuracy and reliability of statistical information. 3 The biggest factor was the implementation of the social program at KAP and affiliated companies, which

cut the work force by half from the pre-crisis level of more than 4,000 workers. 4 Bank-supported rapid living standard assessment (2009).

3

Figure 1: Montenegro: Crisis and Its Aftermath

Rapid growth following country’s

independence…

…driven by capital inflows and real estate

booms…

…led to enormous build-up of external

vulnerability…

…further amplified by expansionary fiscal

policy.

Source: MONSTAT, CBOM, MOF, staff calculations

7. Owing to an abrupt decline in capital inflows and a large fall in external and

domestic demand, significant external adjustment took place. The current account

deficit was reduced by half between 2008 and 2010 as imports contracted. However, it

remained high at about 26 percent of GDP in 2010, as exports and tourism hardly

recovered. During 2006–2010, net FDI financed on average 70 percent of the current

account deficit, excluding one-off inflows from the recapitalization and partial

privatization of Montenegro’s power utility in 2009. Access to capital was retained

through foreign banks’ increased financial support to their Montenegrin subsidiaries,

which contributed to a rise in external debt to 94 percent of GDP in 2009.

8. Fiscal imbalances widened from late 2008 and fiscal adjustment was

necessary to ensure macro stability. With GDP contracting by about five percent in

2009, the overall fiscal deficit would have risen to above eight percent of GDP without

the budget revision. Revenues declined by around one-fourth in 2009, partially led by

declining tax compliance as liquidity problems of KAP, the state power utility (EPCG)

and other large companies intensified. The budget revision included a downward

adjustment of 4.7 percentage points of GDP on the spending side, resulting in a fiscal

-6

-4

-2

0

2

4

6

8

10

12

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Montenegro

Western Balkans

Central and Eastern Europe

European Union

Real G

DP

gro

wth

, in

perc

en

t

0

500

1,000

1,500

2,000

2,500

3,000

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2010 2011

MO

ST

E s

tock

mark

et in

dex

Billio

ns

of e

uro

MOSTE Index,

monthly averages(left-hand scale)

Stock of bank credits

to the private sector(right-hand scale)

Stock of bank deposits

from the private sector(right-hand scale)

2004 2005 2007 20082006 2009

0

10

20

30

40

50

60

70

80

90

100

2006 2007 2008 2009 2010

Current-

account

deficit

Other credits/debits

Credits/debits (services)

Exports/imports

In p

erc

en

t o

f G

DP

0

5

10

15

20

25

30

35

40

45

50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

7.5

6.0

4.5

3.0

1.5

0.0

−1.5

−3.0

−4.5

−6.0

−7.5

Overall budget deficit(in percent of GDP, right-hand scale)

Expenditures

Revenues

(both in percent of GDP, left-hand scale)

Tax

Cap.

Cu

rren

t

Oth

er

Overall budget balance

(in percent of GDP, right-hand scale)

4

deficit of 5.3 percent of GDP. Consequently, public debt rose to 42 percent of GDP in

2009. With containment of the wage bill and a decline in capital spending, the fiscal

deficit further declined to 3.7 percent of GDP in 2010, leaving the spending-to-GDP ratio

at a high 47 percent. The Government issued Eurobonds for its financing needs5.

Reflecting the Government’s support to the restructuring efforts by major companies in

the industrial sector (in exchange for an equity position in these companies, including

KAP), public debt with guarantees increased to 54 percent of GDP by 2010.

Table 1: Montenegro: Key Economic Indicators, 2006-2010 (percent of GDP)

Note: Public debt includes publicly guaranteed debt. E.g., the share of public debt to GDP for 2010

includes 11.6 percentage points of publicly guaranteed debt - of which 10.3 and 1.3 percentage points

refer to guarantees of foreign and of domestic debt, respectively. External private debt does not include

any private debt guaranteed by the state.

Source: MONSTAT, CBOM, MOF, staff calculations

B. Banking Sector Developments

9. The rapid expansion of the Montenegrin banking system came to a halt in

late 2008 due to the impact of the global financial crisis on the overheated domestic

economy. The system’s rapid growth was driven by the entry of foreign banks, along

with increased domestic demand coming in particular from the real estate sector6. Total

assets of the banking system increased by more than 100 percent on average in 2006 and

5Its first ever five-year, €200-million Eurobond was issued in September 2010 at a rate of 7.875 percent and

was followed by another issuance of €180-million Eurobonds in April 2011 at a lower rate after receiving

positive outlook by Moody’s. 6 A proportion of increased real estate development financing activity was driven by the development of the

tourism sector.

2006 2007 2008 2009 2010

Real GDP growth (%) 8.6 10.7 6.9 -5.7 1.1

Consumer prices (period average, %) 3.0 4.2 7.4 3.4 0.5

Gross national savings 0.7 -5.8 -10.1 -2.9 -3.6

Gross investment 25.4 33.8 40.6 27.1 22.1

Fiscal sector

Revenues and grants 45.0 49.2 49.9 44.0 43.3

Expenditures 42.0 42.8 50.2 49.3 47.0

Overall balance 3.0 6.4 -0.3 -5.3 -3.7

Primary balance 4.1 7.4 0.5 -4.5 -2.7

Public Debt (gross) 34.2 28.3 29.0 41.8 53.9

External sector

External Debt 52.4 76.2 77.7 93.4 99.7

Private debt, % of total 42.7 67.7 74.4 68.5 59.6

Current account balance -24.7 -39.6 -50.7 -30.1 -25.7

Foreign Direct Investment (net) 21.7 20.8 17.9 30.6 17.7

5

2007, growing from 67 percent of GDP to 111 percent of GDP. Asset growth has slowed

down substantially since 2008 due to the impact of the global financial crisis, with assets

growing by only 11 percent in 2008 (both due to credit controls applied by the CBCG and

the impact of the crisis), and then contracting by eight percent in 2009, a further three

percent in 2010, and by a further one percent in the first three months of 2011 (Table 2).

Table 2: Basic Indicators of the Banking System

2006 2007 2008 2009 2010 Mar-11

Number of Banks 10 10 11 11 11 11

Number of Foreign Banks 7 7 9 9 9 9

Asset/GDP 67 111 107 102 97.3 N/A

Assets Growth y/y 106 108 11 -8 -3 -1

Deposits/GDP 50 78 65 61 59 N/A

Deposit Growth y/y 120 94 -5 -8 -2 -0.4

Credit/GDP 39 84 91 80 73 N/A

Credit Growth y/y 125 165 25 -14 -8 -5 Source: CBCG

Note: Q1 2011 GDP data not available

10. The expansion of the banking system was underpinned by the exceptionally

high rate of credit growth, which was one of the highest in ECA countries, but a

severe credit crunch has followed since late 2008. Total credit grew by 145 percent

annually on average in 2006 and 2007, with credit increasing from 39 percent of GDP to

84 percent of GDP in the same period. Credit growth started to slow down in early 2008

in response to a series of restrictive measures taken by the CBCG to limit the credit boom

(credit growth ceilings and increased minimum solvency requirements). Credit activity

then started to contract in the last quarter of 2008 due to the impact of the crisis, with

total loans outstanding falling by about two percent in Q4 2008, as banks became

concerned about their deteriorating liquidity situation and the ability of their foreign

parent banks to provide additional financing. This declining lending trend continued in

2009, as loans outstanding declined by 14 percent year on year, mainly due to banks’

increasing asset quality problems and a decline in demand for loans from the corporate

sector, which was affected by the weakening economy. In 2010, credit continued to

decline by eight percent in 2010, and by five percent in the first three months of 2011, as

banks have focused on cleaning up their balance sheets.

11. High rates of credit growth were largely financed by foreign parent banks’

lending to their Montenegrin subsidiaries, resulting in high loan-to-deposit ratios

and exposing the banking sector to substantial liquidity shocks. Financing from

parent banks is a critical source of funding for many banks, because the banking sector is

largely foreign-owned (88 percent of system’s assets at end- 2010). Funding from parent

banks (borrowings from parent banks as a share of total liabilities) increased from eight

percent in 2006 to 14 percent in 2007, peaked at 21 percent in 2008, and has since then

decreased to 20 percent in 2009, 17 percent in 2010, and 16 percent in the first three

6

months of 20117. The high loan-to-deposit ratio (LTD) exposed the banking sector to

substantial liquidity shocks. The LTD ratio increased from 87 percent in 2006, to 121

percent in 2007, and further to 169 percent in 2008. The LTD started to decrease in 2009

at 154 percent, and then decreased further to 140 percent at end-2010. The LTD ratio in

Montenegro still remained higher than in many ECA countries at end-2010.

12. As uncertainty increased with the advent of the global financial crisis, banks

lost significant deposits in late 2008, which have not fully recovered yet. The massive

deposit withdrawals were much larger and longer lasting than in neighboring countries.

Over Q4 2008, deposits declined by 18 percent. The anti-crisis measures implemented

by the authorities (see Section III below) helped slow deposit withdrawals, although they

were not successful in stopping the outflow completely. Between September 2008 and

June 2009 there was a loss of about 25 percent of total deposits (with a significant

proportion of this attributed to the depositor run on Prva Banka discussed below). In the

second half of 2009, deposits showed some signs of recovery, signaling a return of

confidence, and the decline in deposits of two percent in 2010 (13 percent increase from

households and 17 percent decline from enterprises) was likely driven by a contracting

GDP rather than by a renewed loss of confidence. In the first three months of 2011,

deposit showed some signs of recovery increasing slightly for both households and

enterprises and mirroring improvements in the overall economy. Overall, between

September 2008 at the onset of the crisis and March 2011, the banking sector lost more

than 23 percent of its total deposits and deposits have not yet recovered to pre-crisis

levels.

13. A massive withdrawal of deposits severely undermined the liquidity of the

system in late 2008, although the situation has improved since then. The system’s

liquid assets to short term liabilities ratio declined from 32 percent in 2007 to 21 percent

in 2008. Since then, system wide liquidity has improved to 26 percent in 2009 and to 33

percent in 2010 and in the first three months of 2011.8 The liquidity situation was helped

by large cash inflows into the banking system as a result of partial privatization of

electricity production and distribution, and by substantial capital injections from the

foreign parents of Montenegrin banks.

14. Asset quality in the banking system has been steadily deteriorating since

2008, although it is expected to stabilize in 2011 as the economy recovers. The

weakened economy (especially the poor performance of the construction sector and the

real estate market) contributed to a rapid increase in non-performing loans (NPLs). NPLs

as a share of total loans increased from seven percent in 2008, to 14 percent in 2009, 21

percent in 2010, and increased again to 23 percent at end-March 2011. At the same time,

past due loans (loans overdue by more than 30 days) increased from 11.5 percent in 2008

to 23 percent in 2009, 24 percent in 2010, and increased again to 30 percent at end-March

7 Loans extended to domestic banks by their parent banks amounted to approximately 24 percent of GDP in

2008 and to 18 percent of GDP in 2009. 8 The minimum level of liquidity is the ratio of liquid assets to due liabilities of 1 when calculated as an

average for all working days in a ten-day period. Due liabilities include: loan payables; interest and fee

payables; due time deposits; 30 percent of demand deposits; 10 percent of liabilities for granted but not-

performed irrevocable loan liabilities (credit lines); other due liabilities.

7

2011. In response to rising NPLs, banks were forced to increase loan loss provisioning,

and draw on their capital buffers. Nine out of 11 banks had to be recapitalized by their

shareholders as a result. The rapid rise in NPLs during 2010 was driven by numerous

factors, including: (i) Prva Banka’s delay in recognizing the extent of its NPLs (which

did not occur until after an onsite inspection in December 2010); (ii) the contraction in

total loans as banks ceased lending (and thus increased NPLs as a proportion of total

loans); and (iii) large banks (particularly CKB and Hypo) ―cleansing of‖ their loan

portfolios in 2010 in anticipation of spinning off large volumes of NPLs to their foreign

parents in the first half of 2011, a process which is now underway. Given an estimated

GDP growth of two percent in 2011 (after an estimated 1.1 percent growth in 2010), the

ending of the cleansing process, and the spin-off of NPLs now underway, NPLs are

expected to stabilize and then decline during 2011, allowing banks to resume lending.

15. As in other countries, the crisis had a rapid and dramatic impact on bank

profitability. The banking sector has incurred heavy losses since December 2008. The

return on assets (ROA) decreased from -0.6 percent in 2008 to -0.7 percent in 2009, to -

2.8 percent in 2010, and improved slightly to -2.4 percent at end-March 2011. The return

on equity (ROE) declined from -6.9 percent in 2008 to -7.8 percent in 2009, declined

dramatically in 2010 reaching -28 percent, and improved to -23 percent in the first three

months of 2011. The banking sector incurred heavy losses throughout 2010, reaching

€82 million at end-2010 mainly due to an increase in provisions by about 69 percent from

end-2009. However, in the first three months of 2011, the rate of losses declined as

banks absorbed €17 million in losses by end-March 2011, reflecting the impact of

tightened bank supervision and banks’ own efforts to clean up their loan portfolios and

complete recording of the required provisions in 2010.

Table 3: Key Prudential Indicators of the Banking System

2007 2008 2009 2010 Mar-11

Liquidity

Liquid assets to short term liabilities 32 21 26 33 33

Liquid assets to total assets 22 11 15 19 19

Liquid assets to total liabilities 24 12 17 21 22

Capital Adequacy

Regulatory capital to risk-weighted assets 17 15 16 16 15

Capital to Assets 8 8 11 11 10

Asset Quality

NPLs / loans 3 7 13 21 23

Past due loans (above 30 days)/ loans 4 12 23 24 30

Provisions/ NPLs 74 56 43 31 24

Provisions/ loans 2 4 6 6 6

NPLs net of provisions, in percent of capital 8 32 52 103 122

Earnings and Profitability

ROA 1 -1 -1 -3 -2

ROE 6 -7 -8 -27 -23 Source: CBCG

8

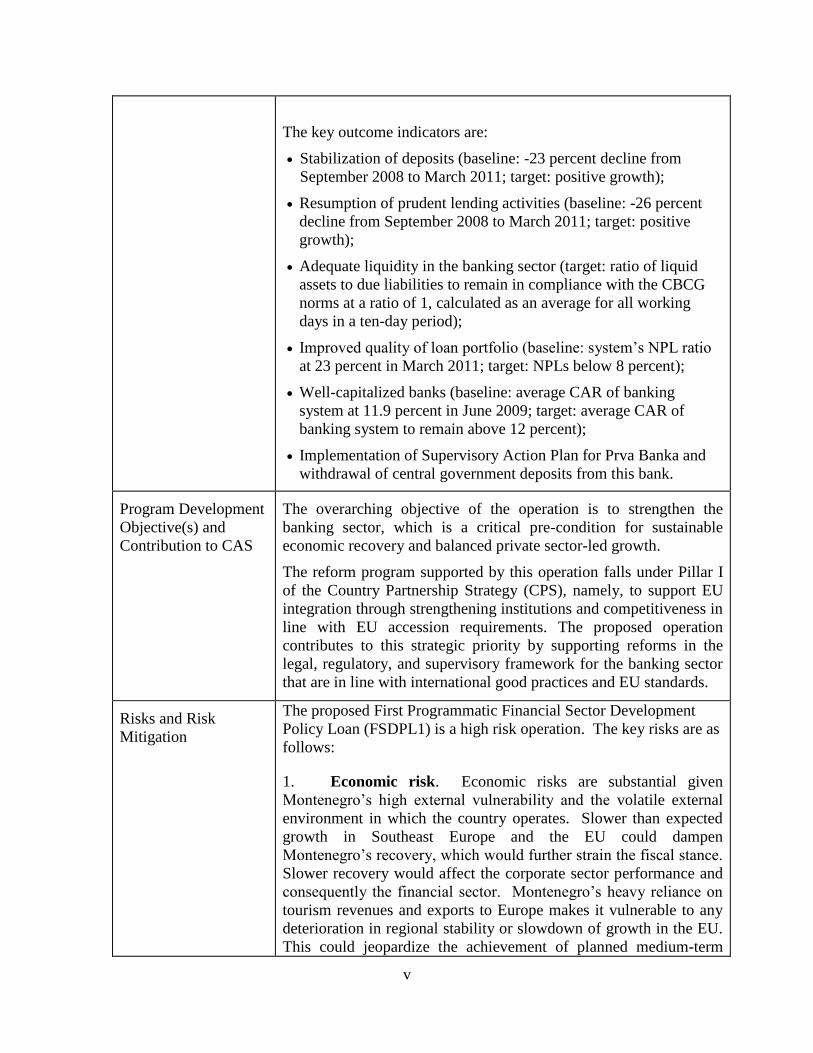

16. Parent banks have so far supported their Montenegrin subsidiaries with

substantial additional funding and capital injections, thus helping to partially offset

declining domestic deposits and capital erosion. The overwhelming majority of

Montenegrin banks are owned by foreign banking groups, most of which provided some

form of liquidity support throughout the acute stage of the crisis. Equally importantly,

the parent banks provided about €230 million in new capital from Q4 2008 to March

2011. As a result, the capital adequacy ratio (CAR) of the system stood at 15.4 percent at

end- March 2011, above the prudential minimum requirement of 10 percent. Subsidiaries

of foreign banks also had an opportunity to manage their NPLs through transferring them

to the Asset Management Companies (AMCs) of their parent banks. However, domestic

banks have had to maintain their NPLs on their balance sheets.

17. Prva Banka - the largest domestically owned bank - experienced the most

significant outflow of deposits and was the only bank to receive emergency support

from the state. A controlling interest in Prva Banka was acquired in 2006 by a group of

local investors related to the then Prime Minister. Subsequently, the bank’s assets grew

explosively (by 1,600 percent from 2006 to end-2008) to make it the country’s second

largest bank and the only domestically owned bank of systemic importance. Following a

massive outflow of deposits, the bank started to experience severe liquidity problems at

end-2008 that threatened to undermine confidence in the entire banking system. Faced

with chronic asset-liability mismatches and the rapid withdrawal of deposits, Prva Banka

ceased to function as a normal commercial bank as of the fall of 2008, when the CBCG

imposed a freeze on new lending activities. The management of the bank was replaced in

late 2008, at the same time as Prva received a €44 million emergency loan from the GoM.

The loan was repaid in 2009, but underlying asset quality problems remained, with a

negative impact on the bank’s capital position. The bank also continued to rely heavily

on deposits from the Central Government and other majority state-owned entities. The

authorities are now implementing a comprehensive restructuring strategy for Prva Banka

(see Section III and Section V), including a staged withdrawal of Government deposits

and recapitalization of the bank.

18. As of the first quarter of 2011, the priorities for Montenegro’s banking sector

are further improvements in capitalization of banks and their liquidity positions,

amid persistent NPL ratios and fragile depositor confidence. Although increasing

deposits could suggest strengthening confidence in banks, they still remain below their

end-2007 levels. Furthermore, NPLs show some improvement due to loan restructuring

and write-offs, but with new lending still subdued and new NPLs creeping in the situation

remains challenging for banks. Overall, the financial soundness indicators suggest that

the banking sector recovery still has a long way to go. Thus, restoring soundness across

the system remains a priority in order to resurrect new lending to creditworthy enterprises

and projects. In this regard, through the recently strengthened legal framework, the

CBCG is adequately empowered to safeguard financial stability.

9

C. Macroeconomic Outlook and Debt Sustainability

19. The macroeconomic environment has been steadily improving since mid-

2010, although it remains risky given Montenegro’s high external vulnerability and

a volatile external environment (see Risk Section for more detail). Growth resumed

in 2010, and has been accelerating in the first half of 2011. A double-digit rise in

manufacturing, construction, agriculture and retail trade suggests a recovery of around

two percent in the first three months of 2011, despite reductions in energy production,

transport and the financial sector. The CBCG revised upward the 2011 growth projection

to 2.7 percent, as credit activity slowly resumed. From 2011 onwards, economic activity

is projected to be supported by FDI in the construction, energy, and tourism sectors9.

Also, improved terms of trade and the rise in global demand for aluminum and steel are

supporting an upward economic trend. Growth is expected to become more diversified,

and also driven by moderate domestic demand growth. The inflation projection is set at

two percent on average throughout 2011-2013, suggesting a gradual closure of the output

gap.

20. Growth recovery has yet to translate into labor market improvements. Although the tourism sector is on the rise, according to employment statistics as of April

2011 total employment was still eight percent lower than a year ago. However, the

number of newly employed from the unemployment registry almost doubled in the first

quarter of 2011, suggesting a potential decline of unemployment in the second half of

2011.

21. External imbalances are projected to moderate over the medium term. In the

first quarter of 2011, the current account deficit declined to 23 percent of GDP on a four-

quarter rolling basis, led by a surge in exports of goods (60 percent rise led by aluminum

and electricity), transport services (27 percent), and a still moderate rise in imports (7.5

percent). The current account deficit is expected to decline towards 19 percent of GDP

by 2013. Given the important role of FDI in the Montenegrin economy, such level of

external imbalances would be closer to what could be viewed as the country’s debt-

stabilizing level (i.e., 16 percent of GDP). Export growth, which is projected at around

11 percent on average over 2011-2013, will help moderate the current account deficit.

FDI is expected to remain strong at around 15 percent of GDP per year, mostly as a result

of needed recapitalization of the banking sector and the earlier announced investments

taking the form of public-private partnerships. This would cover approximately two-

thirds of the current account deficit and thus reduce financing pressures.

22. Fiscal consolidation efforts have continued despite large tax arrears and

reduced tax collection. The recovery, coupled with a freeze in public sector wages10

and

further expenditure restraints in social transfers and the capital budget, equivalent to three

9 Potential investments at various stages of discussion include a highway connecting the coastline areas to

the Corridor X; hydro-power plants with an undersea energy cable to Italy; and leasing of largely

undeveloped beaches for the construction and management of high-end tourist facilities. 10

Except for the gradual adjustment to gross amounts of integrated meal and holiday bonuses into the basic

wage from December 2010 until end-2012. Given they were not subject to taxes and contributions in 2010,

this will lead to a three percent rise in public sector wage over the two years.

10

percentage points of GDP, cut the accrual-based general government deficit to 3.7

percent of GDP in 2010. This was achieved despite a rise in both unemployment and the

social spending needed for social protection of the vulnerable population, necessitated in

part by restructuring of the metal industry. However, a rise in tax arrears, the bankruptcy

of the steel mill and an immediate call on government guarantees (equivalent to one

percent of GDP), as well as a rush to lock in pensions by the police force that will lose

pension privileges from 2012, are likely to drive the planned 2011 fiscal deficit up to 3.3

percent of GDP as opposed to the planned 2.4 percent of GDP. The tax administration

has stepped up tax collection efforts, in particular in the service sector and for excises.

Following the reprogramming of tax liabilities from January 2011, the authorities expect

additional tax revenues on the order of 0.7 percent of GDP (out of five percent of GDP

total tax arrears) still in 2011.

Table 4: Montenegro: Macroeconomic Outlook (percent of GDP)

Outturn Projected

Indicators 2010 2011 2012 2013

National Accounts

Real GDP growth 1.1% 2.0% 2.0% 3.7%

Total Investment 22.1 22.0 22.5 23.0

Gross National Savings -3.6 -2.4 0.5 3.8

Foreign Savings 25.7 24.4 22.0 19.2

Public Sector

Primary Balance -2.9 -1.8 -1.1 -0.4

Interest payments 1.0 1.6 1.7 1.9

Fiscal Balance (w/o capital revenues) -3.9 -3.4 -2.8 -2.3

Balance of Payments

Trade Balance -43.5 -42.9 -41.7 -40.4

Current Account Balance -25.7 -24.4 -22.0 -19.2

FDI 17.7 15.4 14.4 13.4

Debt

External Debt (private and public) 99.7 98.5 97.0 93.6

Public Debt, gross, (incl. govt

guarantees) 53.9 56.3 55.5 54.2

Gross Internat. Res. (in months of

Imports) 1.7 1.4 1.2 1.2

Memo items:

GDP (US$ millions) 4,007 3,994 4,162 4,354

Inflation (p.a., %) 0.5 3.1 2.0 1.8

Debt service to export ratio 32.1 31.8 28.6 24.7

Exchange rate EUR:US$ (p.a.) 0.75 0.78 0.78 0.79 Note: Fiscal accounts corrected for arrears and assumed slower path of fiscal consolidation than

assumed by the government. Public debt includes publicly guaranteed debt.

Source: MONSTAT, CBCG, MOF, staff calculations

11

23. Recognizing that credit guarantees to ailing industries may be translating

into additional fiscal expenditure, the Government has already endorsed policies for

further spending cuts. These include: (i) accelerated staff downsizing and abolishment

of all benefits and bonuses that will lower the wage bill by 0.2 percent of GDP in 2011;

and (ii) centralized authorization of public procurement, which will prevent budget

arrears’ accumulation. In addition, as possible contingencies, the 2011 budget has the

scope for further spending cuts, should these be needed, to ensure that the fiscal deficit

does not exceed the newly targeted 3.3 percent of GDP, including: (i) recurrent spending

cuts amounting to 0.54 percent of GDP; (ii) a capital spending reduction of 0.15 percent

of GDP, in particular for land acquisition along the future highway Bar–Boljare; and (iii)

subsidies for steel mill redundancies amounting to 0.1 percent of GDP.

24. The Government’s medium-term strategy aims to safeguard stability

through front-loaded expenditure-based fiscal adjustment. The overall spending rise

from an average level of 44 percent of GDP before the crisis to 47 percent during 2009–

2010, driven by social expenditures and the expanding wage bill, is to be reversed. With

its 2011 budget and the Economic and Fiscal Program for 2012–2015, the Government

outlined a gradual adjustment path that aims to ensure the medium-term sustainability of

public finances through:

i. A wage bill reduction of 0.5 percent of GDP by 2013 based on an adopted

Personnel Policy Paper suggesting public sector employment downsizing;

ii. State aid reduction by 0.6 percent of GDP, in particularly for subsidized

electricity to the troubled metal industries that will cease by end 2012;

iii. Rationalization of social security costs and transfers by 0.5 percent of GDP by

2013, to be achieved by capping total health expenditures and imposing central

oversight of the use of budget funds, pension reform, and reduced

intergovernmental transfers;

iv. Moderation of capital spending by 0.5 percent of GDP by 2013 leaving it still at

the relatively high level of 4.5 percent of GDP; and

v. Stepped up efforts in tax collection and gradual increases in property tax and

excise duties (also required as a part of the EU accession program).

25. The ongoing deleveraging process and fiscal consolidation are expected to

reduce external financing needs over the medium term. The large stock of corporate

sector foreign debt (around 60 percent of total) and corresponding large debt obligations

maturing over the medium term continue to create significant external vulnerabilities. In

2011, overall gross external financing needs amount to 31 percent of GDP (or 32 percent

of exports of goods and non-factor services). One-fourth of these are due to principal

repayments, which doubled compared to the pre-crisis period, while the rest is due to a

still unsustainably high current account deficit. Public debt service will decline to around

five percent of GDP in 2011, of which two-thirds is due to domestic creditors.

26. Gross financing needs will slowly decline as external imbalances recede by

2013. Gross financing needs will be on average US$1.2 billion over the 2011-2013

period (or around 28 percent of GDP), half of which are likely to be covered by FDI (in

banking, energy and tourism). The country’s overall borrowing requirements will be in

12

the order of US$600 million per year. With the proposed DPL program and the regular

disbursement profile, the IBRD might cover around 3.8 percent of overall gross financing

needs. Debt service to the IBRD will decline to around eight percent of total public debt

service as the country develops its access to international capital markets.

27. External debt is projected to decline to 93 percent of GDP by 2013, after

reaching its historical high of close to 100 percent of GDP in 2010. The projections

remain highly sensitive to changes in macroeconomic assumptions. Under the

assumption of a moderate export recovery, the debt to exports ratio will decline to below

220 percent by 2013 (from its peak in 2010), indicating the need to diversify export

structure and continue with structural reforms supporting productivity growth. Due to the

relatively short maturity of private external debt, debt service as a share of exports is

expected to decline to below 25 percent by 2013 from over 32 percent in 2010. The

sensitivity analysis suggests that the implicit interest rate of seven percent, real growth at

1.1 percent throughout the observed period (as opposed to 3.3 percent projected in the

baseline scenario) and a non-interest current account deficit at 20 percent (as opposed to

12 percent in the baseline scenario) would widen the external debt by 12 percentage

points of GDP compared to the baseline scenario.

Table 5: External Financing Requirements and Sources (percent of GDP)

Source: MONSTAT, CBCG, MOF, staff calculations

Estimate

Indicators 2010 2011 2012 2013

Requirements 34.6 31.2 29.1 25.2

Current Account Deficit 25.7 24.4 22.0 19.2

(of which scheduled interest payments) 6.2 7.3 7.1 7.0

Principal Repayments 8.3 8.0 7.4 6.3

Official creditors 1.3 1.4 1.6 1.7

o.w. IBRD 0.3 0.3 0.3 0.3

Banks 0.2 2.3 2.1 1.8

Other private 6.9 4.3 3.8 2.8

Increase in net official reserves 0.5 -1.3 -0.3 -0.2

Sources 34.6 31.2 29.1 25.2

Foreign Investment (net) 17.7 15.4 14.4 13.4

Portfolio Investment (net) 6.1 4.7 0.2 0.3

MLT Disbursements 6.1 6.6 10.2 7.4

Official creditors 1.7 3.8 1.7 0.8

o.w. IBRD 0.3 2.4 0.7 0.2

Banks 4.9 2.2 3.7 3.2

Other private -0.5 0.6 4.9 3.4

Short-term & other capital (net) 4.7 4.5 4.3 4.1

Debt and debt service indicators, %

TDO/XGS 272.8 250.1 235.0 217.5

TDO/GDP 99.7 98.5 97.0 93.6

TDS/XGS 32.1 31.8 28.6 24.7

Interest payments/GDP 3.4 4.5 4.4 4.3

IBRD exposure indicators (%)

IBRD DS/public DS 15.9 6.2 7.9 9.3

IBRD DS/XGS 1.0 0.9 1.0 1.1

IBRD TDO (US$m) 237.7 313.6 329.4 320.5

Projected

13

28. As expenditure-led fiscal consolidation advances, overall public debt will

likely decline from 2012 onwards. With a 1.8 percentage points of GDP spending

reduction per year, as envisaged by the medium-term fiscal framework, public debt

(without guarantees) would be reduced to 39 percent of GDP in 2014 after reaching its

peak in 2011. Without planned policy changes, the primary deficit would stay at slightly

above two percent of GDP, and public debt (without guarantees) would remain at about

44 percent of GDP in 2014 (or about 54 percent with public guarantees). Contingent

liabilities in terms of guarantees extended to corporate sector and government overdue

liabilities (arrears) amounted to 13.5 percent of GDP at the end of 2010, one-third of

which is due to guarantees issued to KAP.

29. Non-performing loans and inter-enterprise arrears are posing the biggest

risks to a fragile growth recovery and Government’s fiscal plans. By February 2011,

non-performing loans reached a record high of 23 percent, representing close to 15

percent of GDP. The illiquidity in the private sector is reflected in the overall inter-

enterprise arrears amounting to about 10 percent of GDP, of which the general

government sector arrears amount to about three percent of GDP. Tax arrears, on the

other hand, amounted to five percent of GDP at the end of 2010.

Figure 2: Public Debt Sustainability Figure 3: External Debt Sustainability

Note: Without guarantees. In the historical

averages scenario the key variables include real

GDP growth, real interest rate, and primary

balance as percent of GDP. In the no-policy

change scenario, constant primary balance from

2010 was applied to 2011-2015 period.

Source: IMF calculations.

Note: The key variables in the alternative

scenario include real GDP growth, nominal

interest rate, Euro deflator growth, non-interest

current account, and non-debt inflows in percent

of GDP.

30. The Montenegrin economy needs to strengthen fundamentals to steer

through a volatile external environment. This strategy includes: (i) continuing

restructuring in the financial and real sector; (ii) accelerating structural reforms in social,

labor and education sectors as well as administration to ensure sustainability of public

finances; and (iii) strengthening the enabling environment for private sector growth.

Apart from ensuring macroeconomic stability through fiscal consolidation efforts, the

Historical

averages

Baseline

No policy change

20

25

30

35

40

45

50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Historical averages

Baseline

60

70

80

90

100

110

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

14

Government is proactively addressing competitiveness issues. To that extent, an action

plan for removing administrative burden to investments has been developed, jointly with

the IBRD, implementation of which has been advanced with: (i) the simplification of

business and tax registration under the one-stop-shop concept; (ii) the reduction in

complexity and duration of requesting construction permits; (iii) the adoption of the new

bankruptcy and enforcement laws; and (iv) the reduction in non-tax fees and time for

connection to electricity grids. After amendments to the Pension Insurance Act that

increased the retirement age to 67 over a 20-year period, discussions with social partners

over the amendments to the Labor Law have commenced with a view to reducing

dismissal costs and allow for flexible employment contracts. The Government has also

adopted the 2011 Privatization Plan that targets tourist and transport companies with a

view to unlock unused assets in these companies for more productive use by the private

sector.

31. The overall macroeconomic policy framework, although subject to

significant risks, is considered adequate for the purposes of the proposed DPL. The

set of macroeconomic policies proposed in the Government’s program, if implemented,

should enable sustainable recovery in 2011 and beyond. The public sector deficit is

declining throughout the observed period, which reduces financing risks, but not pursuing

the proposed fiscal strategy makes the medium-term outlook risky, as increased debt

service kicks in from 2015. The country’s euroization, high level of external debt, and

large debt service requirements over the medium term call for a prudent fiscal policy. In

addition, the heavy reliance on tourism revenues and exports to Europe makes the

country vulnerable to any slowdown of growth in the EU. Thus, if any of the risks

materialize and underlying macroeconomic assumptions change, further efforts would be

required to achieve the desired fiscal targets, which the Government is committed to

undertake, as laid out in the Letter of Development Policy (Annex 3).

III. THE GOVERNMENT’S REFORM PROGRAM

A. Overall Reform Program

32. Since the beginning of the crisis in the Fall of 2008, the authorities have

formulated a coherent policy response aimed at restoring long-term macroeconomic

and financial sector stability, and encouraging a sustainable economic recovery. In

the fiscal area, to respond to the crisis and contain the widening fiscal deficit, the

Government undertook politically difficult expenditure cuts to consolidate Government

and expenditure growth, including by privatizing selected state assets and concessions.

In the financial sector, the authorities gave priority to restoring depositor confidence and

stepping up the supervisory effort, including restructuring of problem banks. In parallel,

the authorities pursued a longer term effort towards strengthening the entire regulatory

framework for the banking sector in order to bring it in line with international practices

and EU directives, and thus make the sector and regulatory bodies better prepared for

possible future shocks. These reforms are consistent with the Economic and Fiscal

Program for the three-year period that the Government was obliged to prepare as part of

the EU accession, starting from 2007. The need for a stronger regulatory and institutional

15

framework for the banking sector was also highlighted by the EC in the 2010

Commission Opinion on Montenegro’s Application for Membership of the EU.

B. Financial Sector Reforms

33. To restore consumer confidence in the banking sector, the authorities

adopted an emergency anti-crisis law in October 2008, the Law on Measures for

Protection of the Banking System (MPBS). The provisions of the law were generally

consistent with crisis responses seen in other countries, giving the Government the

authority to: (i) fully guarantee the deposits of all individuals and legal persons; (ii)

facilitate credit guarantees for interbank loans; (iii) provide liquidity support to a bank in

need of additional funds for a period of up to one year; (iv) upon a bank’s request, make a

prepayment of state borrowings from that bank (including loans carrying a government

guarantee); and (v) provide funds for the increase of a bank’s capital, with a view to

protecting and ensuring the stability of the banking system. The law also provided for the

CBCG to: (i) approve the use of funds of the reserve requirements; and (ii) use up to 50

percent of its capital for granting short-term loans to banks. The MPBS has served its

intended purpose and expired at the end of 2009.

34. Confidence in the banking sector was maintained by the MPBS and by

support given by parents of foreign-owned banks to their subsidiaries. Only one

domestic bank (Prva Banka) received emergency loan from the state, which was repaid

within 12 months. A number of banks benefited from state guarantees given by the MoF

for credit lines provided by the European Investment Bank (EIB) and KfW totaling €122

million to support lending to small and medium enterprises (SMEs). In the meantime, the

CBCG has been proactive in introducing a number of temporary changes in prudential

regulations to respond to the special challenges presented by the global financial crisis,

such as lowering reserve requirements to ease liquidity pressures on banks and revising

loan loss provisioning rules to facilitate loan restructuring.

35. In parallel to the emergency anti-crisis measures, the authorities have also

implemented, with support from the World Bank, the following legislative and

institutional reforms in the banking sector, aiming to ensure longer term stability:

(a) maintaining depositor confidence; (b) strengthening the bank liquidity framework; (c)

assessing and addressing vulnerabilities in the banking sector; (d) enhancing the

regulatory framework; and (e) problem bank restructuring. Details of the program in the

different areas are summarized below. These reforms support Montenegro’s EU

accession strategy as they aim to bring the supervisory and regulatory framework for the

banking sector closer to EU practices.

Maintaining market confidence

36. A new Deposit Protection Law was enacted in mid-2010 to replace the

blanket deposit guarantee, which was a temporary measure in the emergency anti-

crisis Law on Measures for Protection of the Banking System. The law aims to

maintain confidence in the banking system by: (i) gradually increasing the ceiling for

deposit insurance coverage in line with regional norms and EU directives; (ii) shortening

16

the timeframe allowed for insured deposit payouts; and (iii) providing a legal instrument

to mobilize external funding sources that would enhance the Deposit Protection Fund’s

(DPF) financial capacity make large deposit insurance payouts. The latter change

allowed an approval later in 2010 of a stand-by credit line from EBRD for the DPF (with

a sovereign guarantee), which can be drawn upon in the event the DPF’s own funds are

not sufficient to deal with a large insured deposit payout.

Strengthening the liquidity framework

37. A new law on the Central Bank of Montenegro (CB Law) was enacted in

mid-2010 that provides the CBCG with expanded powers to act as the lender of last

resort (LOLR). Under the previous CB Law, the CBCG had very limited emergency

liquidity lending capacity. Under the new CB Law, emergency liquidity loans can be

made to solvent banks for 90 days against collateral, extendable to a maximum of 180

days when necessary to preserve the stability of the financial system. The other

important features of the new law include providing legal protection to the CBCG and its

staff from prosecution for acts taken during the performance of their duties, and reflecting

the establishment of a permanent Financial Stability Council (with representation from

the CBCG, MoF, Security and Exchange Commission, and Agency for Insurance

Supervision), a coordination body whose functions are described under a separate law.

The new CB Law has been widely acclaimed as bringing Montenegro closer to the EU’s

sound practices for central bank governance and operations. With one caveat11

, the new

law generally upholds the operational independence of the Central Bank.

Assessing and addressing banking sector vulnerabilities

38. The CBCG has employed a range of supervisory techniques to identify

vulnerabilities in the banking sector and has required bank owners and

management to undertake prompt corrective action as necessary. The supervisory

framework combines full scope on-site examinations, targeted on-site examinations, off-

site monitoring, and quarterly stress testing for credit, liquidity, and market risks. The

CAMELS rating system is in place and is updated for all systemically important banks at

least quarterly. With technical assistance provided by the World Bank, the CBCG has

also now introduced an improved credit assessment and risk rating methodology. The

CBCG conducts periodic on-site examinations of banks, with all of the four largest banks

(Prva Banka, CKB, NLB Montenegro Banka, and Hypo Alpe Adria Banka) and a number

of smaller banks subject to full-scope examinations in both 2009 and 2010. Supervisory

Action Plans (SAPs) were prepared for banks of special concern, approved by CBCG

management, and periodically updated. In the context of SAP implementation, the

CBCG maintains an ongoing dialogue with management and shareholders of the banks to

address specific weaknesses, including requiring capital increases to offset both shortfalls

identified during the inspection process and projected capital needs identified by stress

tests.

11

The new CB Law included a provision, which terminated the mandates of the CBCG Council, including

the CBCG Governor, and required the appointment of a new Council. As communicated by the WB and

the IMF to the authorities, this move could be perceived as an infringement upon the independence of

central bank.

17

Enhancing the regulatory framework

39. In collaboration with the World Bank and IMF, the authorities have taken

steps to bring the Montenegrin regulatory framework for the banking sector in line

with relevant EU Directives and practices in EU member states. A key dimension of

this effort has been to provide the CBCG with the full range of instruments and authority

for effective supervision and, in particular, for dealing with problem banks in a timely

and efficient manner. In mid-2010 a set of amendments to the Law on Banks were

enacted, which enhance the CBCG’s enforcement powers, improve corporate governance

in banks, and strengthen the interim administration process for troubled banks. More

specifically, the deficiencies that were addressed in the amendments to the Law on Banks

included, inter alia: (i) harmonizing fit and proper requirements with the EC directive; (ii)

clarifying the definition of related parties in line with international good practices; (iii)

strengthening the CBCG’s enforcement powers by increasing the types of enforcement

actions available to the CBCG; (iv) limiting the powers of the courts to suspend or revoke

CBCG decisions; and (v) establishing legal protection for the CBCG as a supervisory

authority and its personnel.

40. In parallel, amendments to the Bank Bankruptcy and Liquidation Law were also

enacted to ensure that insolvent banks can be promptly resolved using least cost

solutions. As confirmed in a recent report by the EC12

, the new set of laws has brought

Montenegro substantially closer to compliance with EU countries’ regulatory frameworks

for bank supervision and resolution.

Problem bank restructuring

41. As the only sizeable domestic bank with severe liquidity and asset quality

problems, Prva Banka represented the most critical challenge facing the authorities

during the crisis. Suffering from chronic asset-liability mismatches and rapid

withdrawal of deposits, Prva Banka ceased to function as a normal commercial bank in

the Fall of 2008, when the CBCG imposed a freeze on new lending activities and

subsequently installed a special representative at the bank with the right to attend all

management and board meetings in order to provide close monitoring of its activities.

The management of the bank was replaced in late 2008, when Prva received a €44

million emergency loan from the GoM, which was subsequently repaid. Strong loan

collection efforts by the new management have resulted in a dramatic downsizing of the

bank, with its assets cut almost in half over the past two years, and the bank dropping

from second to fourth largest in Montenegro. By early 2011, the CBCG assessed that

Prva’s condition had stabilized with adequate liquidity, and allowed the bank to resume

limited lending activities, in order to attract new deposits and begin increasing operating

income.

42. Notwithstanding the recent stabilization of Prva Banka, the authorities

recognize that it remains a significant fiscal risk due to its reliance on state-related

deposits, and a potential threat to the stability of the banking system. The bank

12

European Commission Opinion on Montenegro's application for membership of the European Union,

November 2010.

18

continues to rely heavily on deposits from Central Government and majority state-owned

enterprises, primarily EPCG (the second largest shareholder of Prva Banka)13

. The full-

scope examination conducted by the CBCG in late 2010 disclosed that the bank’s asset

quality problems persisted, with the solvency ratio remaining well below the minimum

requirement of 10 percent. In March 2011, the CBCG adopted a new supervisory

strategy (Supervisory Action Plan) for Prva, which, inter alia, required the bank to reach

the minimum solvency ratio of 10 percent by end-April 2011, to reach and maintain

thereafter a minimum solvency ratio of 12 percent by end-December 2011, and develop a

plan to improve the maturity mismatch of its assets and liabilities and excessive

concentration of deposits. Prva met the first of these capital increase targets on time by

means of a new share issue and recovery of NPLs.

43. In parallel, the MoF initiated a gradual withdrawal of central government

deposits from Prva Banka. Total exposure of €28 million was reduced by 25 percent by

end-April 2011. Furthemore, a time-bound schedule was adopted which calls for the

withdrawal, in equal monthly tranches of €1.5 million, of a further 40 percent by end-

December 2011, and all remaining deposits by end-June 2012. This schedule was

coordinated by the MoF with the CBCG in order to ensure that the withdrawal of

government deposits would not destabilize the bank’s liquidity position. Furthermore,

the GoM issued guidance to all majority state-owned enterprises, municipalities and other

state-sponsored institutions to use clearly defined eligibility criteria for procurement of

financial services from commercial banks14

and set a limit for the maximum share of

deposits that should be kept with a single bank. This guidance, whose impact is already

being felt by Prva Banka, should make a major contribution to ensuring that Prva Banka

no longer receives a disproportionate share of state-related financial services business.

IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM

A. Link to the Country Partnership Strategy

44. The objectives of the FSDPL1 are consistent with key priorities and expected

outcomes supported under the current Country Partnership Strategy (CPS). The

FY11-FY14 CPS for Montenegro, endorsed by the Board in January 2011, envisages a

series of two programmatic financial sector DPLs. These operations constitute over half

the CPS lending envelope and fall under the first of the two main priority areas, namely,

―support EU accession through strengthening institutions and competitiveness.‖ The

CPS clearly states that one of the key outcomes of the CPS is expected to be ―a stronger

banking system governed by a modern regulatory framework and central institutions,

which is more resilient to future shocks.‖

13

Following its partial privatization in the Fall of 2009, EPCG is under a management contract with the

private strategic investor (Italy’s A2A utility company), which also has a representative on Prva’s Board of

Directors. 14

Specifically, the document instructs to use bank solvency and profitability as criteria for placement of

deposits, in addition to deposit interest rates.

19

B. Collaboration with the IMF and other Donors

45. This operation has been prepared in close collaboration with the IMF. The

Bank team has maintained close working relations with the Fund team for the purpose of

harmonizing policy recommendations and coordinating technical assistance (TA) efforts.

In general, the IMF has taken the lead on discussing with the authorities the

macroeconomic adjustments needed in view of the changed international and domestic

environment, while the Bank has focused primarily on helping the authorities address the

largest systemic threats to the banking sector. The two institutions have been working

together on improving the legal and regulatory environment for the banking sector, in line

with the joint recommendations recorded in the most recent Financial Sector Assessment

Program (FSAP) Update Report (FY07). Specifically, the Bank and the IMF have jointly

reviewed and provided technical assistance to the authorities on the legal amendments to

the draft Law on Banks and the Bank Bankruptcy and Liquidation Law. The IMF has

taken the lead on reviewing the draft law on the Central Bank, while the Bank has played

the same role for the Law on Deposit Protection Fund. The lack of a formal IMF

program is also contributing to risks albeit the IMF is active on policy matters (mainly

banking and fiscal) and is working closely with the Bank.

46. The Bank is coordinating its policy program under this FSDPL1 with the

European Union, Montenegro’s most important current and future development

partner. The structural and regulatory reforms supported by this operation are essential

for achieving the goals set by the Stabilization and Association Agreement, which aims at

the gradual convergence of Montenegro’s economy with the EU. The ongoing large

twinning project financed by the EU and implemented by Central Bank of Bulgaria

provides extensive TA to the CBCG for further strengthening its supervision capacity.

47. The Bank has also maintained a robust dialogue with other donors active in

Montenegro, in order to avoid the duplication of efforts and leverage support for the

GoM’s reforms. In the context of a joint International Financial Institutions initiative,

the EBRD has been very pro-active in providing additional debt and equity support to the

Montenegrin banking sector since the start of the crisis. Following consultations with the

Bank team and enactment of the law on protection of deposits, the EBRD approved a €30

million stand-by loan to the DPF. Germany’s KfW has also provided several lines of

credit to commercial banks, and is providing a TA program for the DPF.

C. Relationship to Other Bank Operations

48. This loan is not directly related to any recent Bank operation in Montenegro.

However, earlier operations supported the development of Montenegro’s financial and

enterprise sector. The series of Structural Adjustment Credits (SAC 1 approved in 2002

and SAC 2 approved in 2004) supported key structural reforms to enhance fiscal

sustainability and promote private-sector led growth. The SACs supported reforms in a

number of areas including the business environment, financial sector and public

administration. The financial sector component sought to resolve non-performing assets

carved out of the banking sector, and complete the privatization of large banks.

20

D. Analytical Underpinnings