Embed Size (px)

Citation preview

Do Health Savings Account Generate Favorable Selection in a Large Employer Setting? Stephen T Parente, Ph.D.

Associate Professor of Finance and Director, Medical Industry Leadership

InstituteUniversity of Minnesota, Carlson School of

Management

Sponsored by the Robert Wood Johnson Foundation’s Health Care Financing &

Organization Initiative (HCFO), the U.S. Department of Health and Human Services

Presentation Overview

• CDHP Models– Health Reimbursement Arrangements (HRA)– Health Savings Account (HSA)

• Employer Study Setting– Plan design for 2006 HSA offer against

competing PPOs, EPOs and HRAs

• Descriptive Statistics• Plan Choice Results• Summary

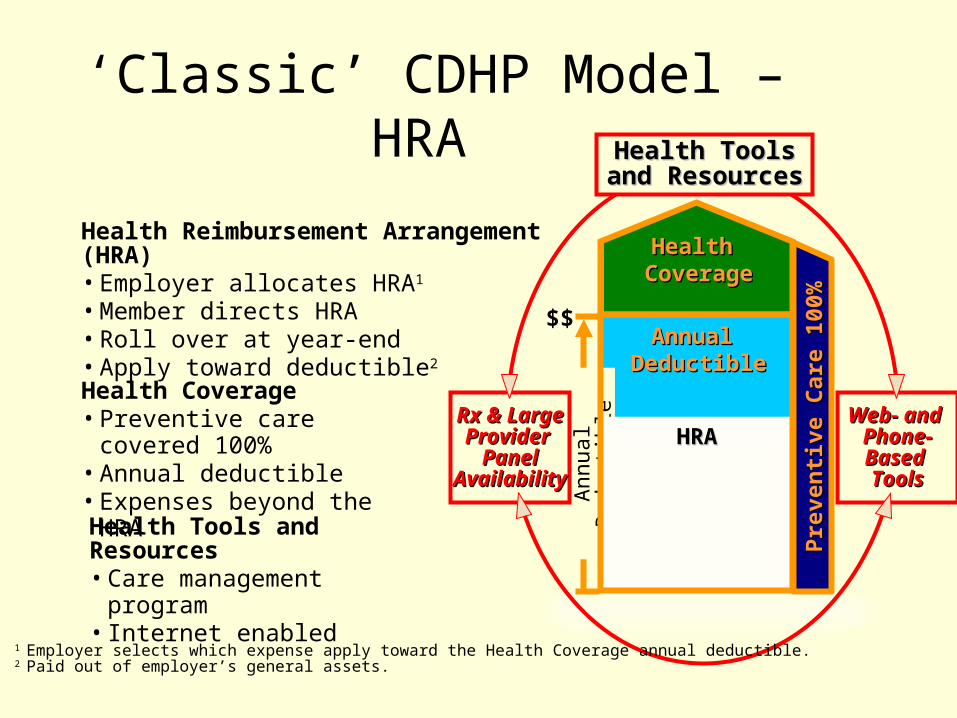

‘Classic’ CDHP Model – HRA

Rx & LargeRx & LargeProvider Provider

PanelPanelAvailabilityAvailability

Web- and Web- and Phone-Phone-Based Based ToolsTools

Health ToolsHealth Toolsand Resourcesand Resources

Health Tools and Resources• Care management

program• Internet enabled

Health Coverage• Preventive care covered

100%• Annual deductible• Expenses beyond the

HRA

Health Reimbursement Arrangement (HRA)• Employer allocates HRA1

• Member directs HRA• Roll over at year-end • Apply toward deductible2

Annual Annual DeductibleDeductible

Annual Annual DeductibleDeductible

Pre

ven

tive

Care

10

0%

Pre

ven

tive

Care

10

0%

Health Health CoverageCoverage

An

nu

al

Ded

uct

ible

1 Employer selects which expense apply toward the Health Coverage annual deductible.2 Paid out of employer’s general assets.

HRAHRAHRAHRA

$$

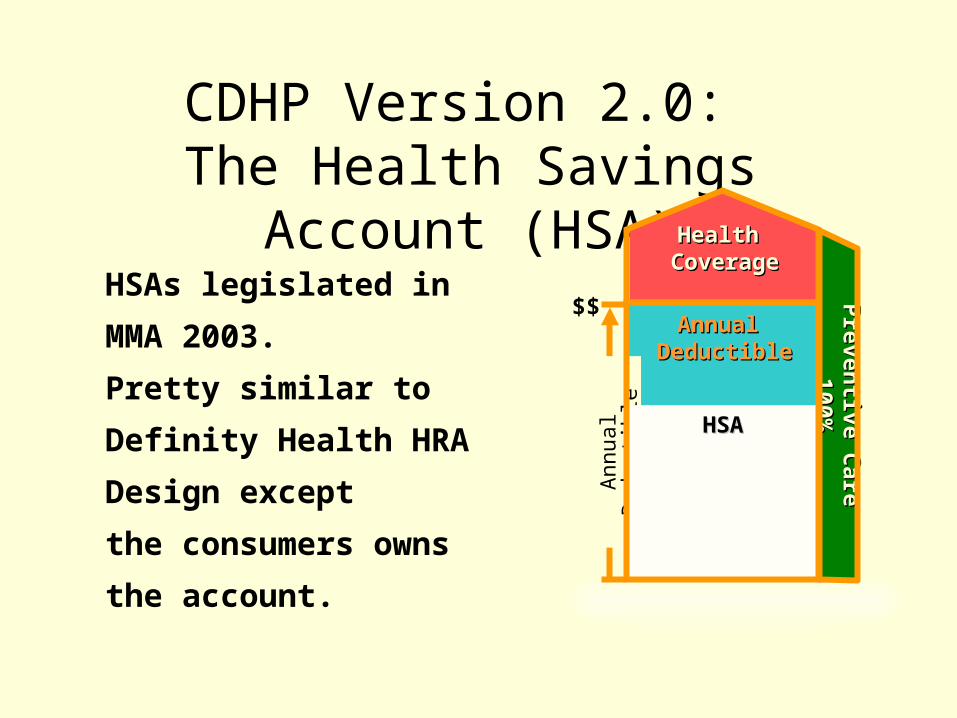

CDHP Version 2.0: The Health Savings Account

(HSA)HSAs legislated in

MMA 2003.

Pretty similar to

Definity Health HRA

Design except

the consumers owns

the account.

Annual Annual DeductibleDeductible

Annual Annual DeductibleDeductible

Pre

ven

tive C

are

P

reven

tive C

are

1

00

%1

00

%

Health Health CoverageCoverage

An

nu

al

Ded

uct

ible

HSAHSAHSAHSA

$$

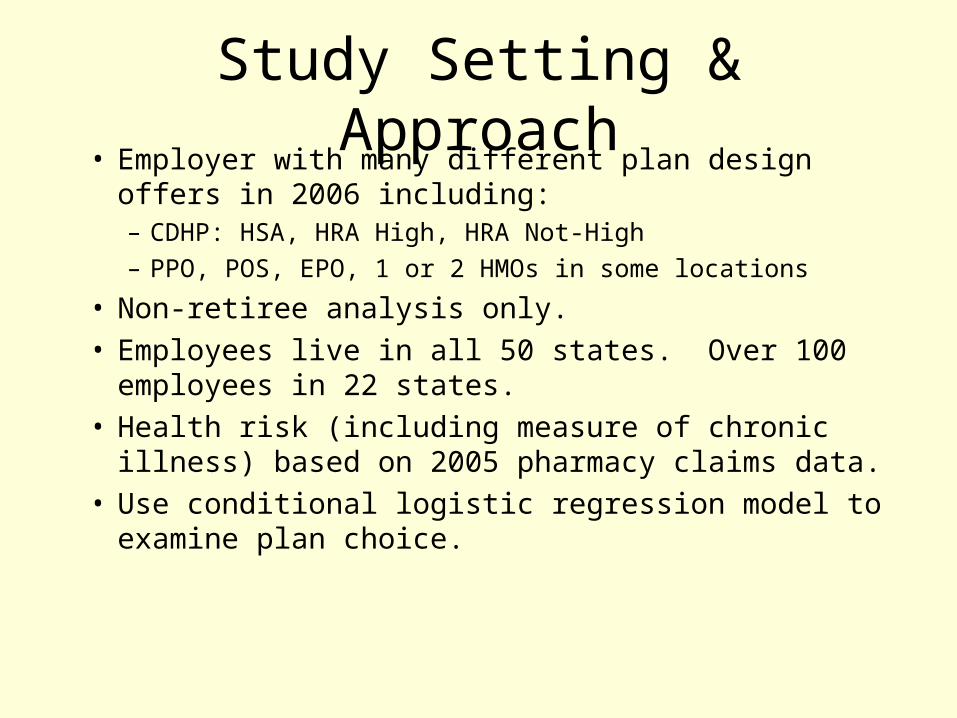

Study Setting & Approach• Employer with many different plan design offers

in 2006 including:– CDHP: HSA, HRA High, HRA Not-High– PPO, POS, EPO, 1 or 2 HMOs in some locations

• Non-retiree analysis only.• Employees live in all 50 states. Over 100

employees in 22 states.• Health risk (including measure of chronic illness)

based on 2005 pharmacy claims data.• Use conditional logistic regression model to

examine plan choice.

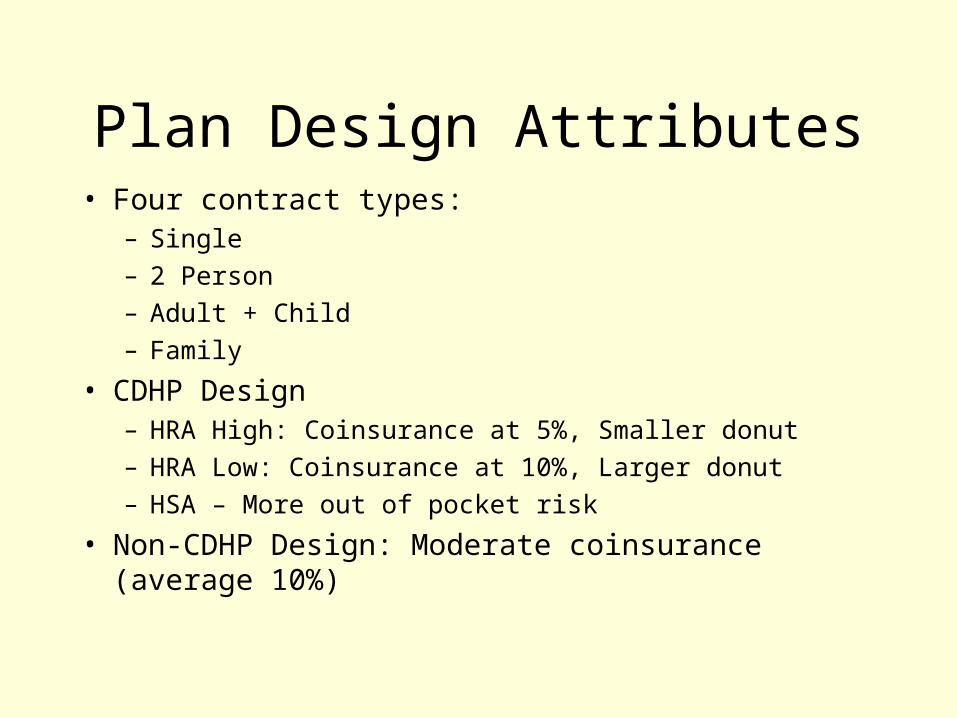

Plan Design Attributes• Four contract types:

– Single– 2 Person– Adult + Child– Family

• CDHP Design – HRA High: Coinsurance at 5%, Smaller donut– HRA Low: Coinsurance at 10%, Larger donut– HSA – More out of pocket risk

• Non-CDHP Design: Moderate coinsurance (average 10%)

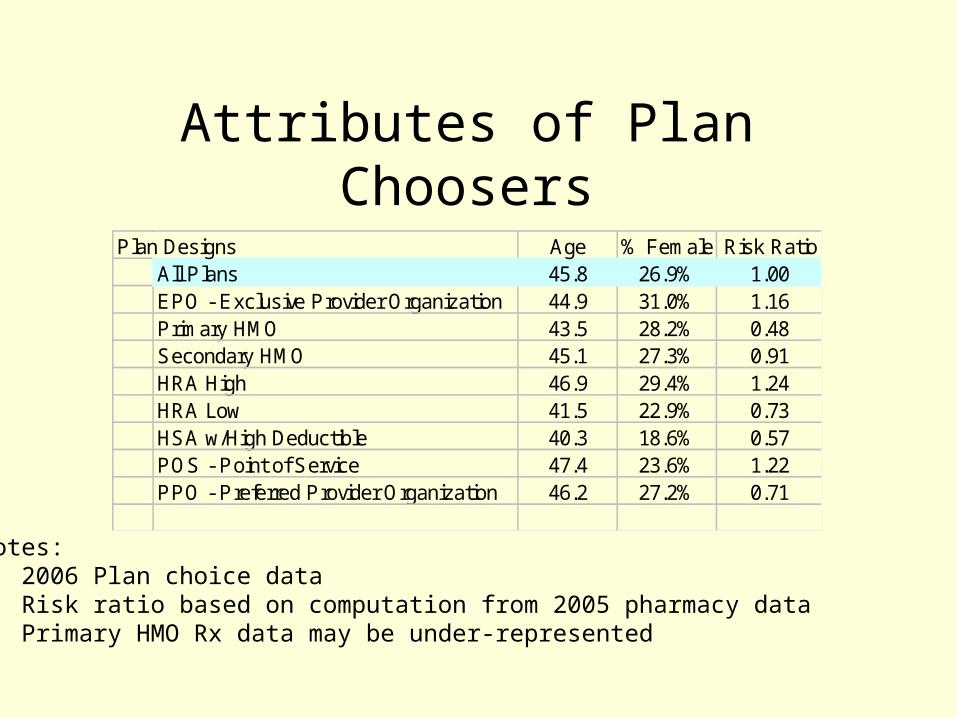

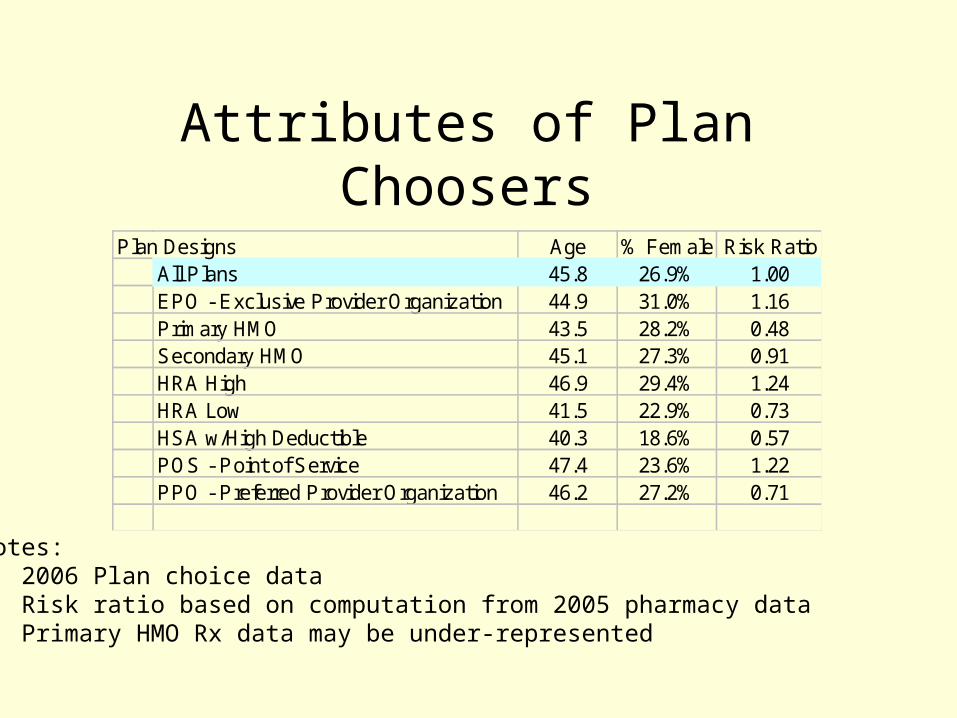

Attributes of Plan Choosers

Plan Designs Age % Female Risk RatioAll Plans 45.8 26.9% 1.00EPO - Exclusive Provider Organization 44.9 31.0% 1.16Primary HMO 43.5 28.2% 0.48Secondary HMO 45.1 27.3% 0.91HRA High 46.9 29.4% 1.24HRA Low 41.5 22.9% 0.73HSA w/High Deductible 40.3 18.6% 0.57POS - Point of Service 47.4 23.6% 1.22PPO - Preferred Provider Organization 46.2 27.2% 0.71

Notes: • 2006 Plan choice data• Risk ratio based on computation from 2005 pharmacy data• Primary HMO Rx data may be under-represented

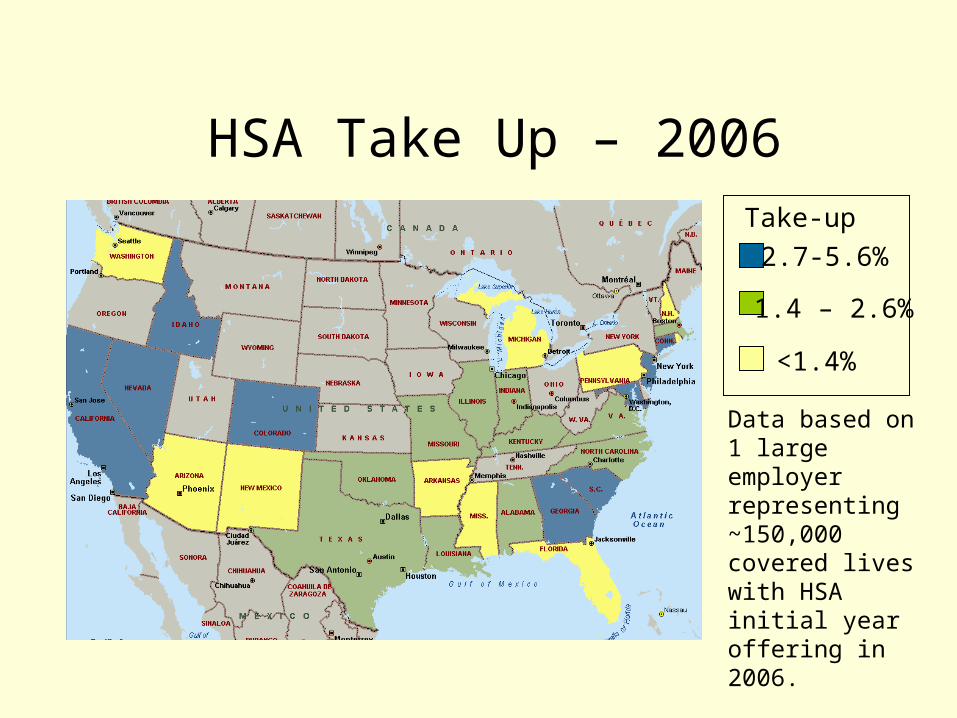

HSA Take Up – 2006

2.7-5.6%

1.4 – 2.6%

<1.4%

Take-up

Data based on 1 large employer representing ~150,000 covered lives with HSA initial year offering in 2006.

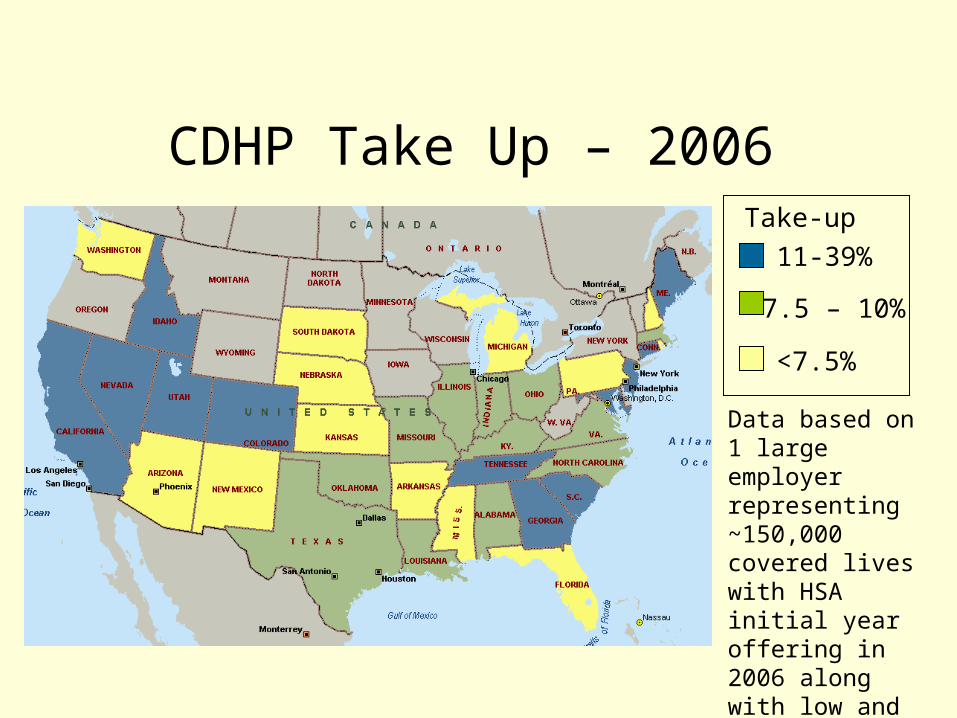

CDHP Take Up – 2006

Data based on 1 large employer representing ~150,000 covered lives with HSA initial year offering in 2006 along with low and high HRAs.

11-39%

7.5 – 10%

<7.5%

Take-up

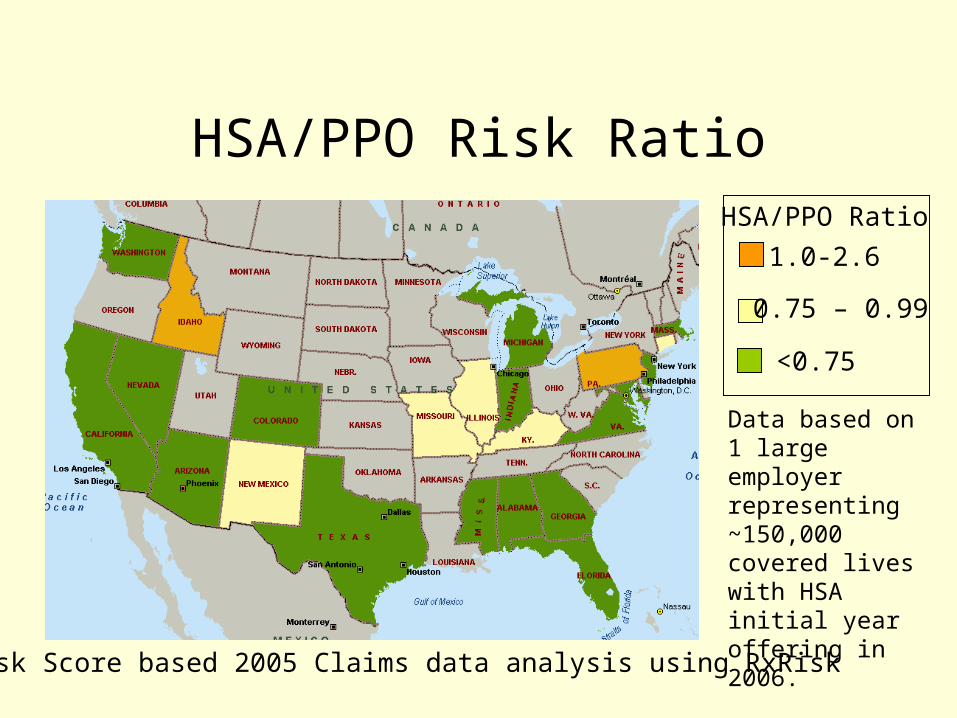

HSA/PPO Risk Ratio

Data based on 1 large employer representing ~150,000 covered lives with HSA initial year offering in 2006.

1.0-2.6

0.75 – 0.99

<0.75

HSA/PPO Ratio

Risk Score based 2005 Claims data analysis using RxRisk

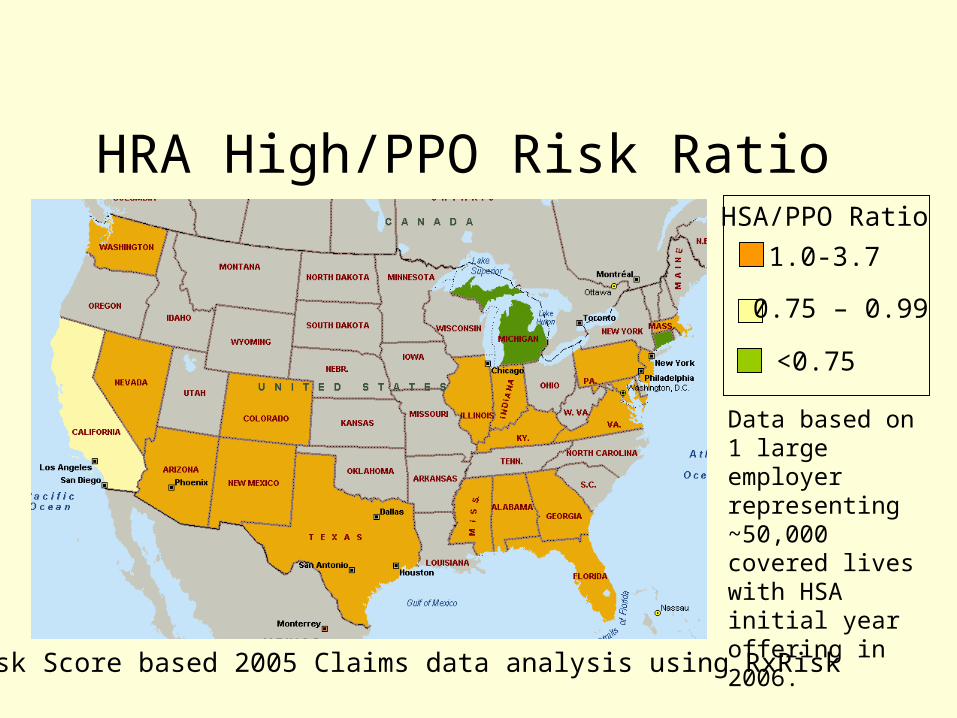

HRA High/PPO Risk Ratio

Data based on 1 large employer representing ~50,000 covered lives with HSA initial year offering in 2006.

1.0-3.7

0.75 – 0.99

<0.75

HSA/PPO Ratio

Risk Score based 2005 Claims data analysis using RxRisk

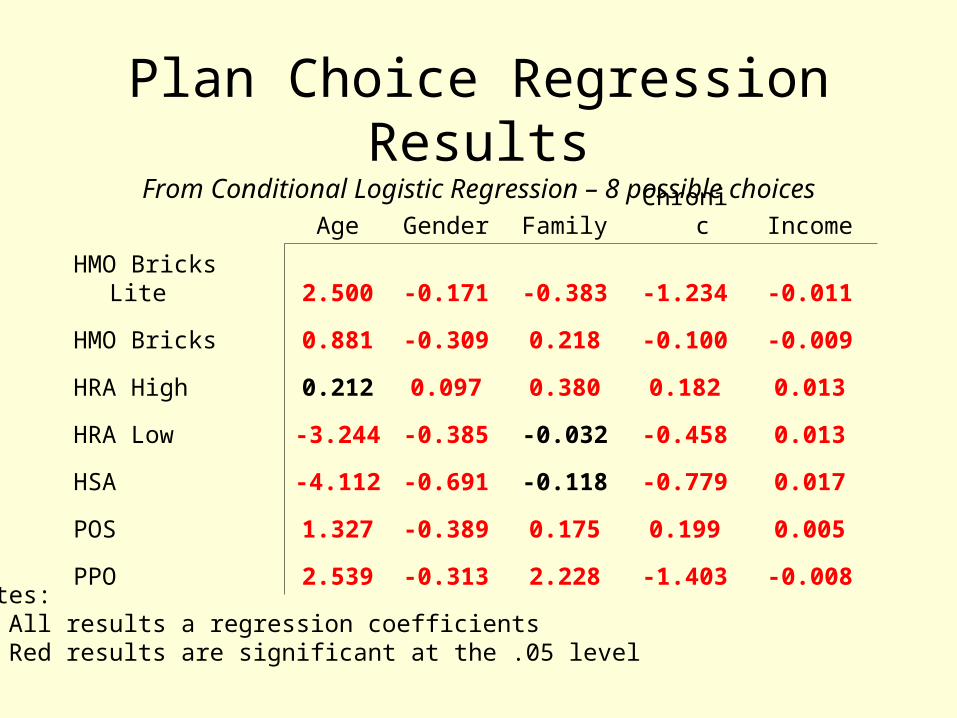

Plan Choice Regression Results

From Conditional Logistic Regression – 8 possible choices

Notes: • All results a regression coefficients• Red results are significant at the .05 level

Age Gender FamilyChroni

c Income

HMO Bricks Lite 2.500 -0.171 -0.383 -1.234 -0.011

HMO Bricks 0.881 -0.309 0.218 -0.100 -0.009

HRA High 0.212 0.097 0.380 0.182 0.013

HRA Low -3.244 -0.385 -0.032 -0.458 0.013

HSA -4.112 -0.691 -0.118 -0.779 0.017

POS 1.327 -0.389 0.175 0.199 0.005

PPO 2.539 -0.313 2.228 -1.403 -0.008

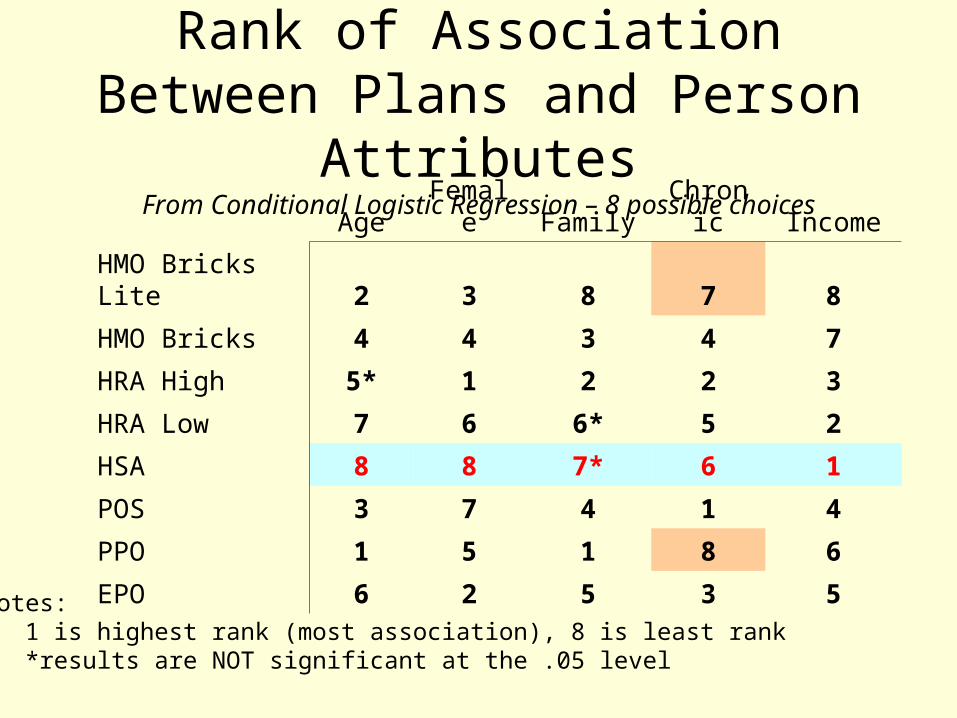

Rank of Association Between Plans and Person Attributes

From Conditional Logistic Regression – 8 possible choicesAge

Female Family

Chronic Income

HMO Bricks Lite 2 3 8 7 8

HMO Bricks 4 4 3 4 7

HRA High 5* 1 2 2 3

HRA Low 7 6 6* 5 2

HSA 8 8 7* 6 1

POS 3 7 4 1 4

PPO 1 5 1 8 6

EPO 6 2 5 3 5Notes: • 1 is highest rank (most association), 8 is least rank• *results are NOT significant at the .05 level

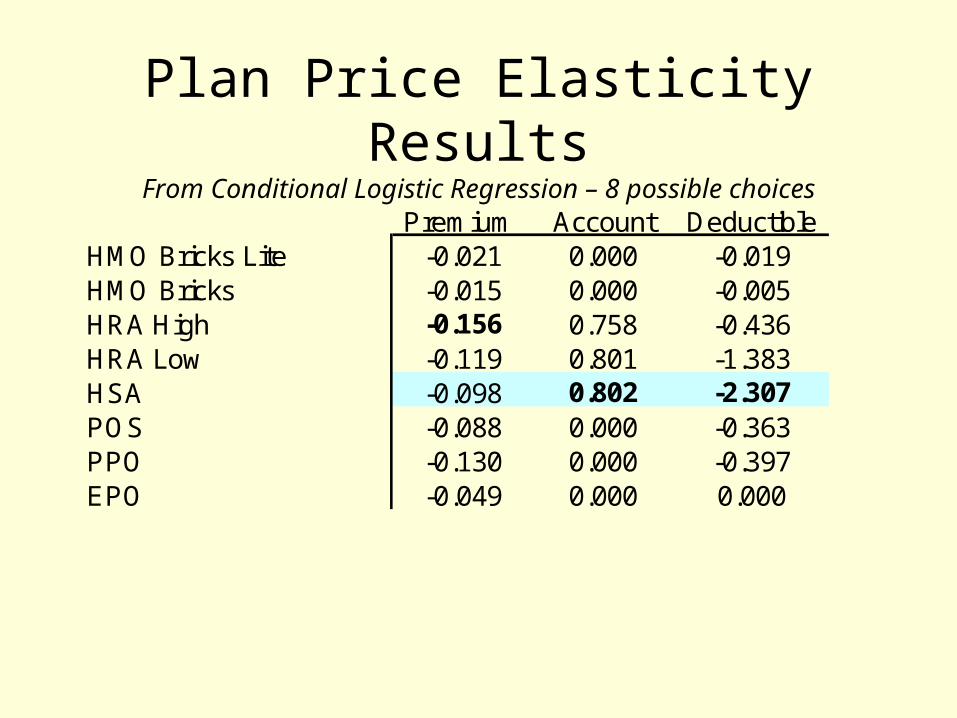

Plan Price Elasticity ResultsFrom Conditional Logistic Regression – 8 possible choices

Premium Account DeductibleHMO Bricks Lite -0.021 0.000 -0.019HMO Bricks -0.015 0.000 -0.005HRA High -0.156 0.758 -0.436HRA Low -0.119 0.801 -1.383HSA -0.098 0.802 -2.307POS -0.088 0.000 -0.363PPO -0.130 0.000 -0.397EPO -0.049 0.000 0.000

Attributes of Plan Choosers

Plan Designs Age % Female Risk RatioAll Plans 45.8 26.9% 1.00EPO - Exclusive Provider Organization 44.9 31.0% 1.16Primary HMO 43.5 28.2% 0.48Secondary HMO 45.1 27.3% 0.91HRA High 46.9 29.4% 1.24HRA Low 41.5 22.9% 0.73HSA w/High Deductible 40.3 18.6% 0.57POS - Point of Service 47.4 23.6% 1.22PPO - Preferred Provider Organization 46.2 27.2% 0.71

Notes: • 2006 Plan choice data• Risk ratio based on computation from 2005 pharmacy data• Primary HMO Rx data may be under-represented

Summary of HSA Choice when HRA and PPO are

Also Choices• Risk-splitting between HRA and HSA• Clearly an issue of benefit design.• Selection not only limited to HSAs.

Favorable selection goes to the HMOs too.• Is the risk segmentation of value? Is too

difficult to fix short of full-replacement?• Next big question: Do HSAs have

better/neutral outcomes and satisfaction, adjusted for risk?

Thank You!For more information on our

research, please visit:

www.ehealthplan.org

and come to Johns Hopkins next week (6/14 & 6/15)

Stephen T. Parente, Ph.D., M.P.H., M.S.Associate Professor, Department of Finance

Director, Medical Industry Leadership InstituteCarlson School of Management

University of Minnesota321 19th Ave. South, Room 3-122

Minneapolis, MN 55455612-624-1391 (v), [email protected]

http://www.tc.um.edu/~paren010