Embed Size (px)

Citation preview

ACCOUNTING WORKSHOP

“Do CEO Bonus Plans Serve a Purpose?”

By

Wayne Guay* John Kepler

The Wharton School

University of Pennsylvania

David Tsui

Marshall School of Business University of Southern California

Thursday, Oct. 13, 2016 1:20 – 2:50 p.m.

Room C06 *Speaker Paper Available in Room 447

Do CEO Bonus Plans Serve a Purpose?

Wayne Guay* [email protected]

The Wharton School University of Pennsylvania

John Kepler

[email protected] The Wharton School

University of Pennsylvania

David Tsui [email protected] Marshall School of Business

University of Southern California

October 6, 2016

Abstract: Given the substantial stock and option portfolios held by most CEOs, much recent literature on CEO incentives regards cash-based bonus plans as largely irrelevant. This begs the question of why nearly all CEO compensation plans include such bonuses. We re-examine the financial incentives provided by bonuses and their role in executive compensation packages. Using detailed data on bonus-plan performance measures, we document that the pay-performance sensitivity of CEO cash compensation is much greater than prior estimates and that cash-based pay provides a substantial portion of many CEOs’ total financial incentives early in their tenure. However, we find little evidence that boards adjust bonus plans over time in response to CEO-specific characteristics, such as the evolution of CEO equity holdings or liquidity needs. This “stickiness” results in growing disparity between the magnitudes of cash- and equity portfolio-based incentives over a typical CEO’s tenure. At the same time, we find evidence that bonus plans appear to consider liquidity and incentive issues for lower-level executives, leading us to conclude that cash-based plans are designed mainly for the overall management team, as well as perhaps new CEOs. Keywords: executive compensation; managerial incentives; pay-performance sensitivity

* Corresponding author. We gratefully acknowledge comments and suggestions from Matthew Cedergren (discussant) as well as seminar participants at Cornell, Wharton, the 2016 American Accounting Association Annual Meeting, and the 2016 UCI/UCLA/USC Accounting Research Conference.

- 1 -

1. Introduction

This paper re-examines the financial incentives provided by executive bonuses and their

role in firms’ incentive compensation packages.1 The vast majority of U.S. executive

compensation plans incorporate bonus payouts, and boards devote considerable time and expense

to designing these often complex plans. However, prior literature presents very different views

regarding the importance of bonuses in CEOs’ overall incentive schemes. One stream of literature

argues that bonus plans provide important incentives and influence CEOs’ investment, financing,

and financial reporting decisions.2 In contrast, other literature estimates the monetary incentives

that bonus awards provide and largely concludes that these incentives are modest, both in absolute

terms and compared to equity-based incentives (e.g., Jensen and Murphy, 1990; Hall and Liebman,

1998; Core et al., 2003).3 Based in part on these findings regarding the magnitude of incentives

from bonus plans, much of the recent literature on CEO incentives ignores bonus awards, due to

their presumed second-order importance, and instead focuses exclusively on “delta” and “vega”

incentives stemming from stock and option portfolio holdings. This latter view, if correct, raises

the question as to why bonus compensation is so pervasive at the CEO level and why boards devote

so much time and energy to designing these plans.

We shed light on this issue by first showing that the actual performance sensitivity of

bonuses is considerably larger than estimates in prior studies, and is comparable in scale to equity

1 We use the term “bonus” in this paper to refer to all forms of short-term cash-based incentive compensation (i.e., annual non-equity-based incentives). 2 Examples of studies emphasizing the importance of cash-based incentive plans include Healy (1985), Lambert and Larcker (1987), Gaver and Gaver (1993), Sloan (1993), Holthausen et al. (1995), Ittner et al. (1997), Matsunaga and Park (2001), and Leone et al. (2006). More recent examples include Murphy and Jensen (2011), Jayaraman and Milbourn (2012), Banker et al. (2012), Indjejikian et al. (2014), Bennett et al. (2015), Gipper (2015), Mukhopadhyay and Shivakumar (2015), and Rhodes (2016). 3 For example, Hall and Liebman (1998) find that for a 10 percent increase in shareholder value, the typical CEO’s cash compensation increases 2.2 percent (about $23,000 in their sample), 53 times less than the corresponding equity portfolio effect (about $1.25 million). Similarly, Core et al. (2003) find that equity portfolio variability is more than 100 times greater than cash pay variability for a typical CEO.

- 2 -

incentives for many CEOs early in their tenures. Prior studies typically estimate bonus

performance sensitivities by regressing bonus payouts (or total cash pay, including salary) on an

assumed measure of firm performance (e.g., stock return or earnings) and using the estimated

coefficient as a measure of the sensitivity of cash pay to performance (e.g., Jensen and Murphy,

1990; Hall and Liebman, 1998). Such regression-based measures invariably contain error and

attenuate the magnitude of the estimated sensitivity of cash pay to performance. To alleviate this

issue, we instead compute bonus performance sensitivities using data on the actual payout

structures defined in executive bonus plans.

Although direct comparisons between the magnitudes of cash- and equity-based incentives

are difficult due to the different underlying performance measures (i.e., bonuses are largely based

on earnings rather than stock price), we compare the two incentive structures based on one of two

alternative assumptions: (i) each firm’s marginal and average P/E ratios are equal (i.e., a one

percent increase in earnings also increases stock price by one percent), or (ii) all firms are subject

to the same marginal P/E ratio (i.e., $1 of additional earnings increases equity value by an equal

amount for all firms). Under either assumption, we find that the typical CEO in our sample receives

an extra 25 to 35 percent in bonus (about $300,000 to $450,000) for a 10 percent increase in

shareholder value, which is about one-sixth to one-ninth of the corresponding equity portfolio

sensitivity (about $2.9 million). For CEOs early in their tenures, who tend to have smaller equity

portfolios (e.g., Core and Guay, 1999; Armstrong et al., 2016), the gap between cash- and equity-

based incentives is considerably narrower: annual cash-based incentives are about one-third to

one-quarter total equity portfolio incentives among these executives.4

4 It is possible that the gap between equity-based and cash-based incentives is even smaller than the estimates above on a risk-adjusted basis. Risk-averse executives are expected to discount the expected payoffs of risky incentive structures, and although bonuses are risky, the volatility of equity is typically greater than the volatility of bonuses.

- 3 -

In supplemental tests, we confirm our conjecture that regression-based estimates severely

understate CEO incentives from bonus plans. Regression-based estimates used in prior literature

attempt to infer pay-performance sensitivities from either cross-sectional or time-series variation

in bonus payouts, where the researcher makes assumptions about the performance measure and

functional form of the payoff structure without detailed knowledge of the characteristics of the

actual underlying bonus plan. We find that the typical regression-based estimates of bonus plan

incentives understate actual incentives by a factor of 10 to 15, with significant portions of this

measurement error stemming from both errors in assumed performance measures and errors in the

functional form of the payoffs.5

We also consider the possibility that our finding of larger bonus incentives than prior work

may reflect a structural shift over time in the design of bonus contracts. In recent years, boards

have faced growing shareholder and political pressure to more strongly link executive annual pay

with firm performance, potentially resulting in increasing performance sensitivity of bonus plans

over time.6 However, we find no evidence of an upward trend in bonus performance sensitivities

over the past twenty years, which suggests that changes over time in actual performance sensitivity

do not explain why our results differ from prior literature.

Our findings suggest that boards design incentive compensation contracts at the start of the

CEO’s tenure with a relatively balanced mix of cash- and equity-based incentives. Over time,

however, equity holdings tend to accumulate because CEOs’ annual equity grants typically exceed

their stock sales (e.g., Core and Guay, 2010; Armstrong et al., 2016). Thus, for longer-tenured

For example, Murphy (2012) assumes a 10 percent risk-adjustment discount on bonus plans compared to a 33 to 67 percent discount for stock options. 5 This conclusion is analogous to the finding in the earnings response coefficient (ERC) literature that the ERCs are “too small” (e.g., Kothari, 2001) and, more generally, consistent with the notion that regression estimates typically understate actual sensitivities (e.g., Hausman, 2001). 6 See, for example, “‘Pay for Performance’ No Longer a Punchline” by Scott Thurm, Wall Street Journal, March 21, 2013.

- 4 -

CEOs, equity portfolio incentives come to dominate overall incentives, consistent with conclusions

from prior literature.

If bonuses are designed to provide CEOs with meaningful financial incentives earlier in

their tenure, one might ask why boards allow CEOs’ equity portfolio incentives to dominate bonus

incentives later in their career. For example, boards could increase cash-based incentives over time

to match increases in equity portfolio incentives, or perhaps encourage CEOs to sell more of their

equity over time to achieve balance. Alternatively, boards might view the dominance of equity

portfolio incentives as being optimal, but perhaps recognize that it takes some time before CEOs

can build up their equity portfolios, and so provide cash-based incentives in the interim. In this

latter case, boards might phase out the payments from CEOs’ cash-based incentives once their

relative importance becomes minor. However, we find no evidence of either pattern in our data.

We conjecture several reasons why boards may continue to provide CEOs with cash-based

bonus plans even after their incentive effects become relatively minor. One possibility is that the

buildup of significant equity incentives can come at the cost of liquidity, and annual cash-based

payouts can provide executives with cash flow to fulfill their consumption demands. Although

annual salary can also provide liquidity, U.S. tax laws discourage non-performance-based cash

payments to executives in excess of $1 million. Thus, cash-based bonuses that are somewhat

weakly tied to performance may serve to fulfill CEOs’ liquidity demands while avoiding the firm-

level tax penalty that would be incurred for providing similar levels of non-performance-based

cash salary.

Boards likely also face pressure from various constituencies to conform compensation

plans to certain norms. For example, compensation consultants and proxy advisors such as ISS

and Glass Lewis tend to focus heavily on CEOs’ annual pay when evaluating the incentives

- 5 -

inherent in executive compensation plans, especially in relation to other CEOs in their peer group

(e.g., Glass Lewis, 2015; ISS, 2016). Surprisingly, and in sharp contrast to the economics literature

in finance and accounting, these advisors largely ignore equity holdings when assessing whether

a given CEO has strong pay-for-performance incentives. Empirical evidence also suggests that

boards appear to modify compensation plans to satisfy the preferences of proxy advisory firms

(Larcker et al., 2015), and therefore bonus plan design may reflect this focus on annual pay over

portfolio incentives.

Finally, because most executive compensation plans have a large number of executive

participants, boards may feel that it is important for synergistic purposes and executive morale to

hold the CEO accountable for the same bonus plan payouts that are borne by other senior

executives (e.g., Edmans et al., 2013; Bushman et al., 2016).7 Lower-level executives typically

receive a lower proportion of their annual pay in the form of equity and have smaller accumulated

equity portfolios, and bonuses are therefore likely to represent a more important component of

these executives’ incentives.

Although it is difficult to determine precisely why boards structure bonus plans, we provide

several analyses that shed light on the possible roles played by CEO bonuses. First, we document

that bonus plans do not appear to evolve over time to accommodate CEO-specific characteristics.

For example, we do not find evidence that boards explicitly adjust cash-based incentives in

response to temporal changes in CEOs’ constrained or unconstrained equity portfolios. In addition,

we find no evidence that CEO-specific liquidity preferences influence the design of bonus plans.

At the same time, consistent with Jayaraman and Milbourn’s (2012) finding that stock-based

7 Murphy (2001) finds that that the median executive bonus plan has 123 participants.

- 6 -

compensation imposes liquidity costs on executives, we find a significant positive relation between

cash-based incentives and firm-level stock illiquidity.

Second, consistent with some external influences on bonus plan design, we find that cash-

based incentives are significantly positively related to bonus incentives for peer firm CEOs.

However, we do not find evidence that boards directly adjust bonus plans in response to other

forms of external pressure, such as “say on pay” votes, proxy advisor voting recommendations, or

greater shareholder monitoring. Finally, as an indication that boards design bonus plans for the

firm’s top management team as a whole rather than contracting with each executive individually,

we find that the relative importance of cash-based incentives is substantially greater for other (non-

CEO) top executives at the firm (about twice as important as for the CEO), and that boards tend to

provide very similar bonus plans across all of the firm’s top executives. For example, the CEO and

the fifth-highest-paid executive share an identical set of performance targets at approximately 75

percent of firms in our sample. Together with our finding that CEO cash-based incentives do not

vary with CEO-specific liquidity measures (but do vary with firm-level measures), these results

suggest that bonus plans are designed to consider overall top management incentive and liquidity

concerns as opposed to CEO-specific needs.

Collectively, our results help reconcile the perceived importance and widespread use of

executive bonus plans with conclusions from prior literature that CEOs’ financial incentives arise

almost exclusively from their equity portfolios. We document that the performance sensitivity of

CEO cash compensation is much greater than estimates in prior studies, and that bonuses provide

a significant portion of many CEOs’ total financial incentives early in their tenure. Our results also

suggest that boards place little emphasis on CEO-specific characteristics, such as liquidity or the

growth of equity portfolio incentives, when designing cash bonus plans. We conclude that CEO

- 7 -

cash-based bonuses persist primarily due to bonus plans designed to provide the top management

team as a whole with liquidity and incentives, and may have relatively little to do with providing

incentives specifically to the CEO, at least after the first few years in office.

This paper proceeds as follows. Section 2 describes our data, variable measurement, and

the procedure we use to estimate pay-performance bonus sensitivities. Section 3 presents our

results and compares our findings to prior literature. Section 4 examines how boards determine

cash-based incentives and Section 5 concludes.

2. Data and Variable Measurement

We obtain data on executive bonus contracts for 8,888 firm-years between 2006 and 2014

from Incentive Lab. The SEC considerably expanded mandatory disclosures regarding the

structure of these bonus contracts (as well as other forms of incentive compensation) in 2006 and

thus details on bonus structures are sparse prior to that year.8 Bonus contracts are typically

characterized by three pairs of values: a minimum (“threshold”) payment for some minimal

acceptable level of performance, a target payment for an expected level of performance, and a

maximum payment for performance sufficiently above expectations (see, e.g., Murphy, 1999;

Murphy and Jensen, 2011). For example, a CEO may receive a bonus equal to 50 percent of salary

if earnings are $1 billion (the threshold), 100 percent of salary if earnings are $5 billion (the target),

and 200 percent of salary if earnings are $16 billion (the maximum). Payments generally increase

linearly between each of these breakpoints (e.g., if earnings in the preceding example are $3

billion, the CEO would receive a bonus of 75 percent of salary).

Bonus contracts often also incorporate several non-earnings-based performance measures,

including financial metrics such as sales and cash flow as well as non-financial metrics such as

8 See SEC Final Rule Release No. 33-8732A (August 29, 2006).

- 8 -

customer satisfaction. For example, 60 percent of a particular CEO’s bonus might be linked to

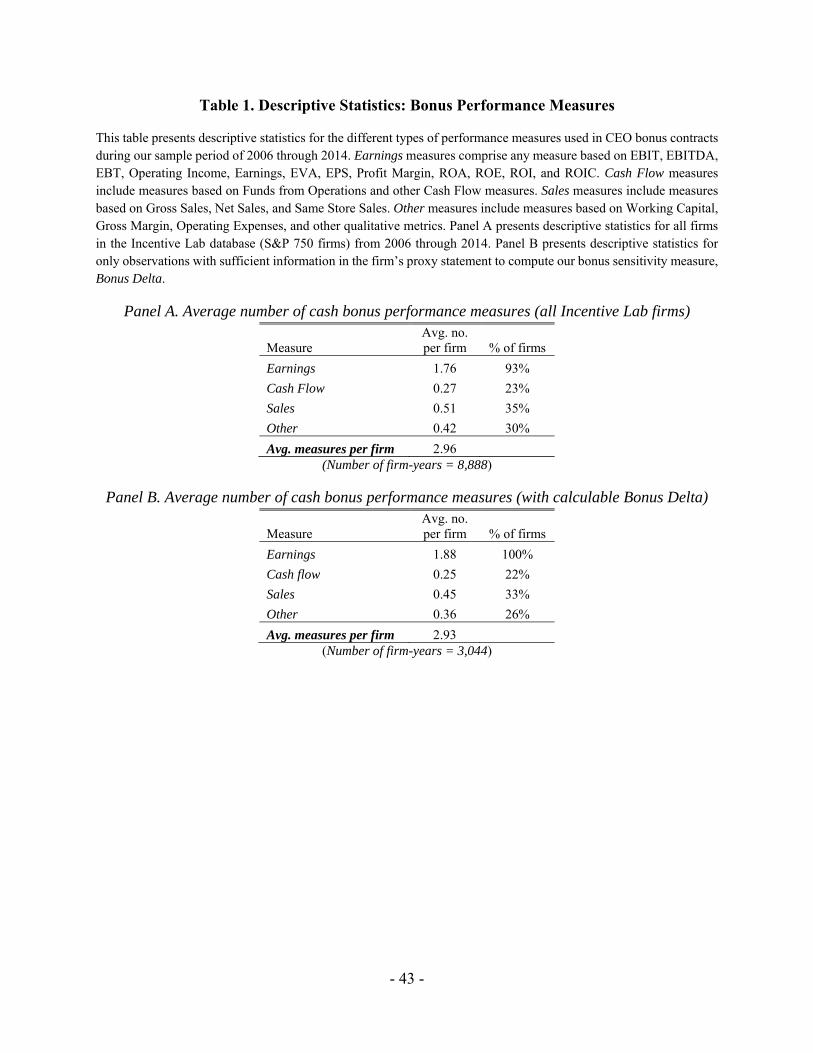

earnings, with 20 percent linked to sales and 20 percent to customer satisfaction. Table 1 Panel A

reports descriptive statistics for the different types of performance measures used in the bonus

contracts captured by Incentive Lab. The typical firm’s bonus plan includes 2.96 performance

measures. Earnings-based awards are the most common form of bonus plan: the typical bonus plan

includes more than one earnings-based metric, and 93 percent include at least one such metric.9

We focus only on earnings-based bonuses in our performance-sensitivity computations because

they are by far the most common and it is relatively straightforward to compare their incentives to

those from equity-based compensation. To the extent that the non-earnings-based components of

bonus plans also provide financial incentives, our earnings-based measures will understate the

overall performance sensitivity of the bonus contract (we attempt to quantify this potential

understatement in Section 3).

To calculate the performance sensitivity embedded in CEO bonus contracts, we collect

from Incentive Lab the minimum, target, and maximum performance goals disclosed by the board

and the bonus payouts that correspond to each of these objectives. Because firms are not required

to report the specific performance goals underlying their bonus plans, we are only able to obtain

these items for a subset of the full Incentive Lab sample. We gather financial data from Compustat,

stock return data from CRSP, institutional investor holdings from Thomson Reuters 13F filings,

and executive compensation from Execucomp. We also obtain shareholder voting data and

Institutional Shareholder Services (ISS) recommendations from ISS Voting Analytics. To reduce

the influence of extreme observations in the Incentive Lab data, we truncate our sample at the 5th

9 We use the term “earnings-based” to refer to metrics that are a function of the firm’s income. Examples include earnings per share, pretax income, and profit margin. Note that these earnings measures may include various non-GAAP adjustments, such as adding back restructuring charges or tax valuation allowances.

- 9 -

and 95th percentiles of the bonus performance sensitivity measures that we compute. All other

continuous variables are winsorized at the 1st and 99th percentiles. Our final sample (after

truncating) consists of 3,044 firm-years from 2006 to 2014 for which we have sufficient data to

perform the bonus performance sensitivity computations described below.

We define the CEO’s bonus performance sensitivity as the ratio of the payout and goal

ranges specified in the plan. Specifically, we compute the payout range as the maximum payout

offered under the plan, less the threshold amount, and the goal range as the performance goal

associated with the maximum payout, less the goal associated with the threshold payout.10 Our

performance sensitivity measure is the ratio of these two ranges, which represents a linear

approximation of the incremental bonus that the CEO receives for each unit of the underlying

performance metric when performance falls between the threshold and maximum performance

levels (thus, our measure does not capture the effects of any “jumps” in bonus payouts for reaching

threshold performance or “capping out” of payouts for exceeding maximum performance). To

illustrate, suppose the CEO in the example above has a salary of $1 million. The maximum payout

would therefore be $2 million (200 percent of salary) and the threshold payout would be $500,000

(50 percent of salary). We would estimate the performance sensitivity of the bonus contract as the

$1.5 million payout range ($2 million less $500,000) divided by $15 billion ($16 billion maximum

earnings goal less $1 billion threshold), or $100 per $1 million of earnings.

While earnings-based measures are the most common basis for CEO bonus plans, the

specific metric that a given board chooses to use varies somewhat between firms. For example,

one firm may base bonus payments on net income, while another may link bonus to EPS. To

10 Some firms report only two performance levels for their bonus contracts (e.g., only the target and maximum, or only the target and threshold). For such firms, we define the payout and goal ranges as the difference between the two levels that the firm specifies. Our findings are very similar if we instead omit such firms.

- 10 -

enhance comparability between firms, we convert all earnings-based sensitivities to net income

sensitivities – that is, the amount of bonus that the CEO receives for a dollar of net income, which

we refer to as unscaled bonus sensitivity. For example, if the bonus plan is based on EPS, we first

compute the CEO’s bonus sensitivity based on EPS (i.e., bonus per dollar of EPS), then convert

this sensitivity to bonus per dollar of net income by dividing by the number of shares outstanding.

Similarly, if the bonus is based on pretax income, we first compute the bonus sensitivity to pretax

income, then convert this pretax sensitivity to net income sensitivity by dividing by one minus the

firm’s effective tax rate. Appendix A provides the specific earnings-based measures we use and

describes this net income-conversion process in more detail.

Next, to facilitate comparisons with the dollars of pay for a one percent change in equity

value (i.e., portfolio delta) measures that are common in the equity incentive literature (e.g., Hall

and Liebman, 1998; Core and Guay, 1999), we convert these unscaled bonus-earnings sensitivities

(i.e., dollars of bonus per dollar of earnings) to bonus-stock price sensitivities (i.e., dollars of bonus

per one percent change in stock price), which we refer to as Bonus Delta. Specifically, we estimate

the change in earnings that would increase the firm’s market capitalization by one percent and

compute the corresponding effect on the CEO’s bonus payout. To do so, we convert a one percent

change in market capitalization into an earnings-equivalent amount under one of two alternative

assumptions: (i) each firm’s marginal and average price-to-earnings ratio are equal, and therefore

a one percent change in earnings corresponds to a one percent change in stock price;11 or (ii) all

firms are subject to the same marginal price-to-earnings ratio, and equate earnings and equity value

accordingly (i.e., $1 of earnings increases equity value by a fixed amount; for these computations,

11 For firms with negative earnings, we assume the firm’s marginal P/E ratio equals the industry-year median P/E. Our inferences are unchanged if we instead omit such firms.

- 11 -

we assume a marginal price-to-earnings ratio of 17, the median in our sample).12 We then compute

the amount of bonus the CEO would receive for this amount of earnings equivalent to a one percent

change in market capitalization.

To illustrate, suppose a firm has a market capitalization of $18 billion and earnings of $1

billion (i.e., the firm’s P/E ratio is 18). Under assumption (i), we would assume the firm’s marginal

P/E ratio is 18 and therefore a one percent change in earnings ($10 million) would increase equity

value by one percent ($180 million). Thus, we would multiply unscaled bonus-earnings sensitivity

by 10 million to estimate the bonus the CEO would receive for earnings equivalent to one percent

of equity value. Under assumption (ii), we would instead assume the firm’s marginal P/E ratio is

17 and therefore approximately $10.6 million of earnings would increase equity value by one

percent (again, $180 million). In this case, we would multiply unscaled bonus-earnings sensitivity

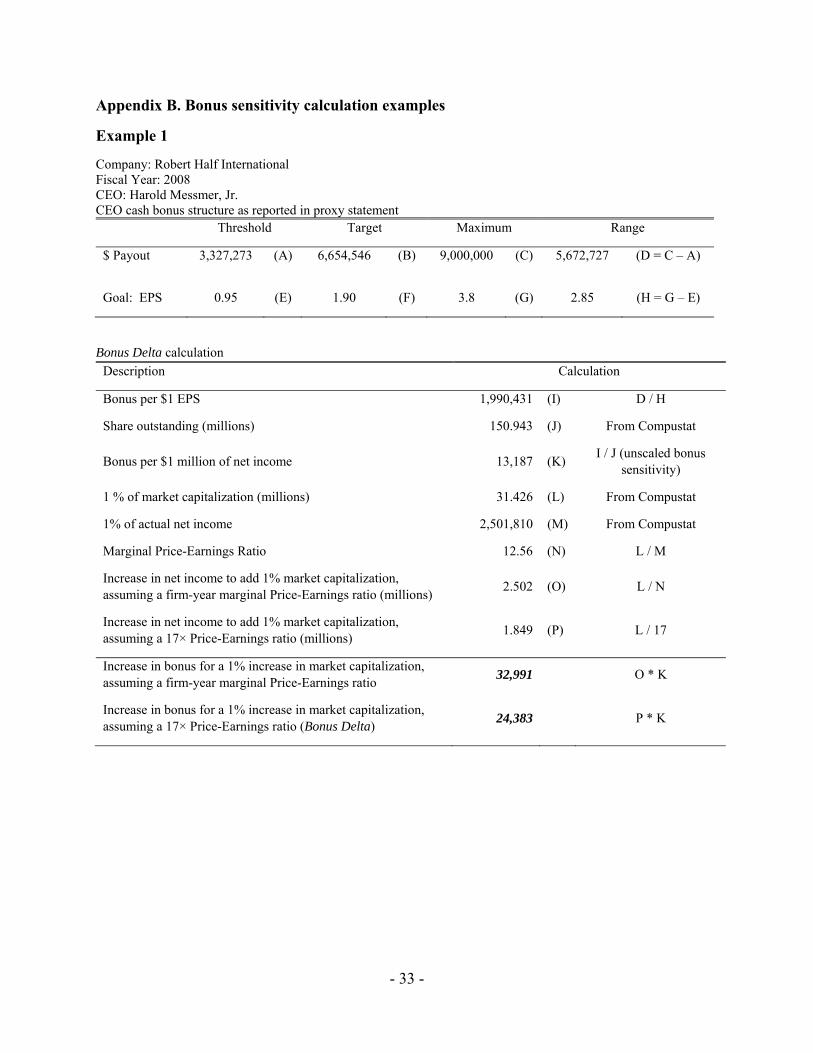

by 10.6 million to estimate the bonus the CEO would receive. Appendix B provides examples from

our sample of these bonus sensitivity computations.

Table 1 Panel B reports descriptive statistics for the performance measures used in the

bonus plans in our sample, which are very similar to the overall distribution reported in Table 1

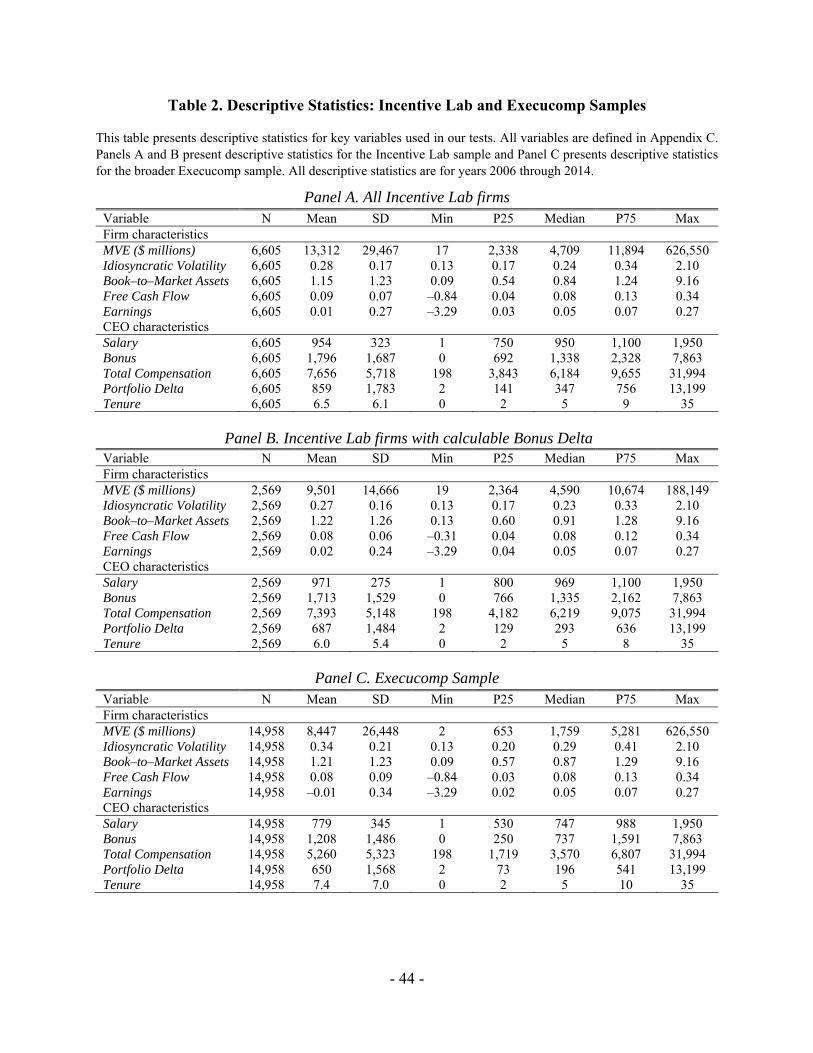

Panel A. Table 2 Panels A and B report descriptive statistics for the full sample of firms covered

by Incentive Lab and the sample of firms for which we have sufficient data to compute Bonus

Delta, respectively, for our sample period of 2006 through 2014. The median firm for which we

can compute Bonus Delta is generally comparable to the median firm in the broader Incentive Lab

sample; the primary differences are that the median firm in our Bonus Delta sample has a larger

12 A third possible assumption would be to use estimated earnings response coefficients (ERCs; i.e., the coefficient from a regression of stock return on earnings) to proxy for a firm’s marginal P/E ratio. We do not use ERCs because an extensive literature documents that they are generally in the range of 1 to 3, which is too small to be economically reasonable (see, e.g., Kothari, 2001). Nevertheless, for a sense of how using this alternative assumption would affect our results, note that assumption (ii) implicitly assigns an ERC of 17 to all firms. Thus, our Bonus Delta estimates would be approximately 5 to 15 times larger using ERCs to convert equity values to earnings.

- 12 -

book-to-market ratio (0.88 versus 0.82 for the overall Incentive Lab sample) and smaller CEO

portfolio delta ($292,000 versus $345,000). We also report descriptive statistics for Execucomp

firms during the same time period in Table 2 Panel C. Compared to Execucomp firms, firms in

Incentive Lab are larger (median Market Capitalization of $4.3 billion for Incentive Lab versus

$1.7 billion for all Execucomp firms), consistent with Incentive Lab’s stricter sample selection

criteria (i.e., 750 largest US firms, versus the 1,500 largest for Execucomp).

3. Results

3.1. Bonus pay-performance sensitivities

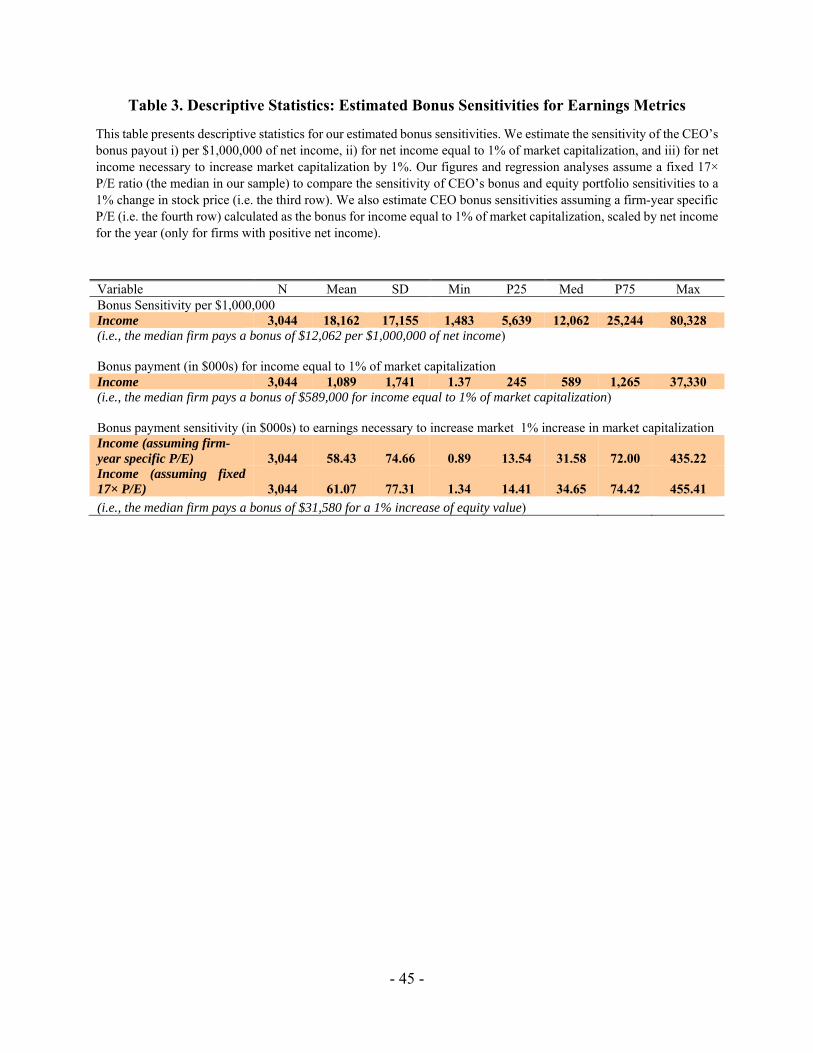

Table 3 presents our estimated bonus performance sensitivities. As in Hall and Liebman

(1998), we focus on medians due to the highly skewed distribution of executive compensation. We

first consider unscaled bonus sensitivity (i.e., dollars of bonus per dollar of net income). The

median CEO receives about $12,000 per $1 million of net income, or slightly more than one cent

for each dollar of income. That is, the median CEO in our sample’s bonus reflects “fractional

ownership” of about one percent of earnings. At the median P/E ratio in our sample of 17 (i.e., $1

of income increases equity value by $17), this implies that the CEO receives approximately $0.60

in bonus for a $1,000 increase in firm value. For comparison, this is approximately 40 times greater

than the estimate from Jensen and Murphy (1990) that CEOs receive $0.0135 in salary and bonus

for a $1,000 increase in firm value and suggests that the performance sensitivity of bonuses is

much higher than previously estimated.

Next, we consider Bonus Delta (i.e., dollars of bonus for a one percent increase in equity

value). Table 3 indicates that, under either of the assumptions linking earnings and equity value

described in Section 2, the median CEO receives about $30,000 in bonus for a one percent increase

in equity value. Relative to the median CEO’s bonus of $1.3 million, this CEO receives an increase

- 13 -

in bonus of approximately 2.3 percent for earnings equivalent to a one percent increase in equity

value.13 In contrast, Hall and Liebman (1998) estimate that the median CEO’s cash pay increases

by about $2,300, or 0.2 percent, for a one percent increase in equity value. Again, these results

suggest that the true performance sensitivity of executive bonus contracts is at least an order of

magnitude larger than prior studies have estimated.

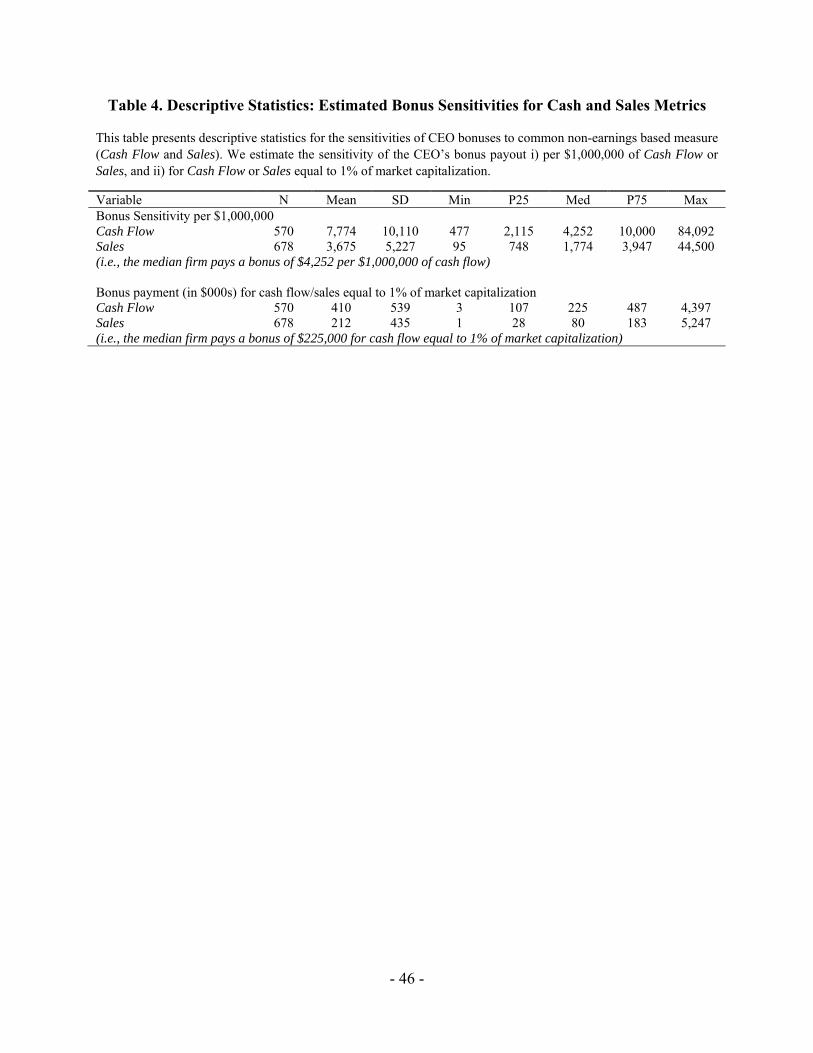

As we note in Section 2, our tests are conducted using bonus sensitivities from earnings-

based plans, and therefore exclude the performance sensitivity of non-earnings-based plans. To

examine the potential influence of this research design choice, we compute bonus sensitivities for

two relatively common non-earnings-based performance metrics (cash flow and sales) and present

the results in Table 4. We compute these sensitivities under the same method as the earnings

sensitivities we describe in Section 2 (i.e., ratio of payout range to goal range). We find that

although sales and cash flow sensitivities are smaller than for earnings, for many CEOs these

sensitivities are economically significant. In untabulated analysis, we estimate that for the typical

bonus contract, earnings-based payouts comprise approximately 67 percent of the total cash award.

Thus, this descriptive analysis suggests that overall cash-based bonus incentives are perhaps about

50 percent greater than those reported in Table 3 for the typical CEO (e.g., perhaps about $45,000

for a one percent change in market capitalization rather than the roughly $30,000 reported in Table

3 for the median CEO).

3.2. Bonus versus equity incentives

Having documented that the performance sensitivity of executive bonus contracts appears

to be much greater than prior literature estimates, we next examine how this result influences the

conclusion in prior literature that equity-based compensation accounts for the vast majority of total

13 Relative to total cash compensation (i.e., salary plus bonus), this is an increase of approximately 1.3 percent.

- 14 -

executive incentives.14 As discussed above, we estimate that the typical CEO receives

approximately $30,000 to $45,000 in bonus for a one percent increase in equity value. In

comparison, the same CEO would receive about $290,000 from increased equity portfolio value,

about six to nine times larger.15 Thus, while equity portfolios do provide the majority of a typical

CEO’s overall financial incentives, the relative incentive weights that we estimate for earnings and

equity are somewhat more balanced than estimates in prior studies. For example, Jensen and

Murphy (1990) find that equity portfolio incentives are about 100 times larger than cash pay

incentives, while Hall and Liebman (1998) conclude the ratio is approximately 50 times.

We also note that, on a risk-adjusted basis, the gap between equity-based and cash-based

incentives may be even smaller than the estimates discussed above. Risk-averse executives are

expected to discount the expected payoffs of risky incentive structures, and although both bonuses

and equity holdings are risky, the volatility of equity holdings is typically greater than the volatility

of bonuses. For example, Murphy (2012) assumes a 10 percent risk-adjustment discount on bonus

plans, compared to a 33 percent to 67 percent discount for stock options.

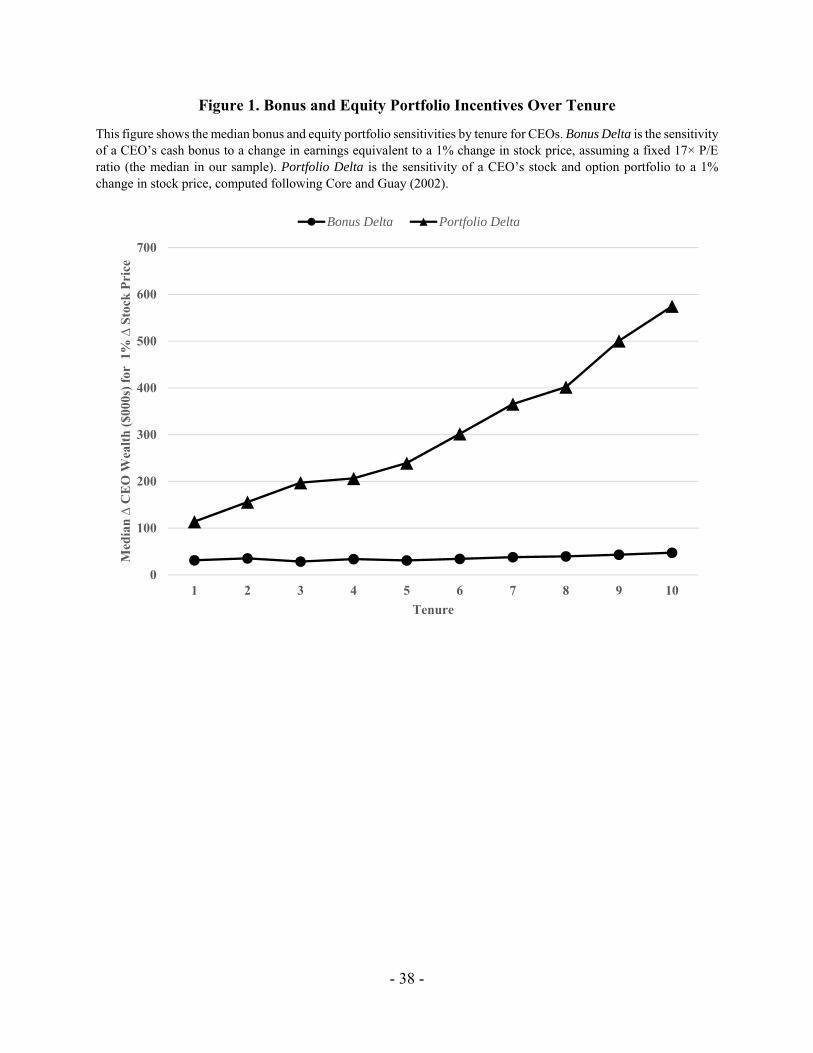

Figure 1 compares the relative balance between cash and equity portfolio incentives over

the course of a CEO’s tenure. Notably, when the CEO is first hired, equity portfolio incentives

(about $100,000 for a one percent change in equity value) are about three times cash incentives

($30,000 for a one percent change in equity value). However, this balance shifts over time and,

consistent with prior studies (e.g., Core and Guay, 1999; Armstrong et al., 2016), we find that

equity portfolio incentives increase substantially (and approximately linearly) with tenure. In

contrast, cash bonus incentives are largely unchanged over the course of a CEO’s tenure; there is

a modest increase over time, but the scale is dramatically smaller than the increase in equity

14 Jensen and Murphy (1990); Hall and Liebman (1998); Murphy (1999, 2012); Core and Guay (2010). 15 We compute this equity portfolio effect following Core and Guay (2002).

- 15 -

portfolio incentives. The net effect is that equity portfolio incentives become increasingly

dominant as tenure increases. For executives with median tenure (about five years), the balance

between cash and equity incentives is comparable to the ratio across our overall sample, and the

importance of equity incentives continues to grow as tenure extends beyond this point.

Taken as a whole, our results indicate that initial CEO compensation contracts contain a

balanced mix of short- and long-term – as well as cash- and non-cash – incentives, but this

compensation mix becomes increasingly skewed as the CEO’s tenure increases. However, we also

draw a distinction between “constrained” and “unconstrained” equity holdings, as defined by

Armstrong et al. (2016). Those authors document that the majority of CEOs’ equity portfolio

incentives are “unconstrained” in the sense that there are no explicit constraints on sales (e.g., stock

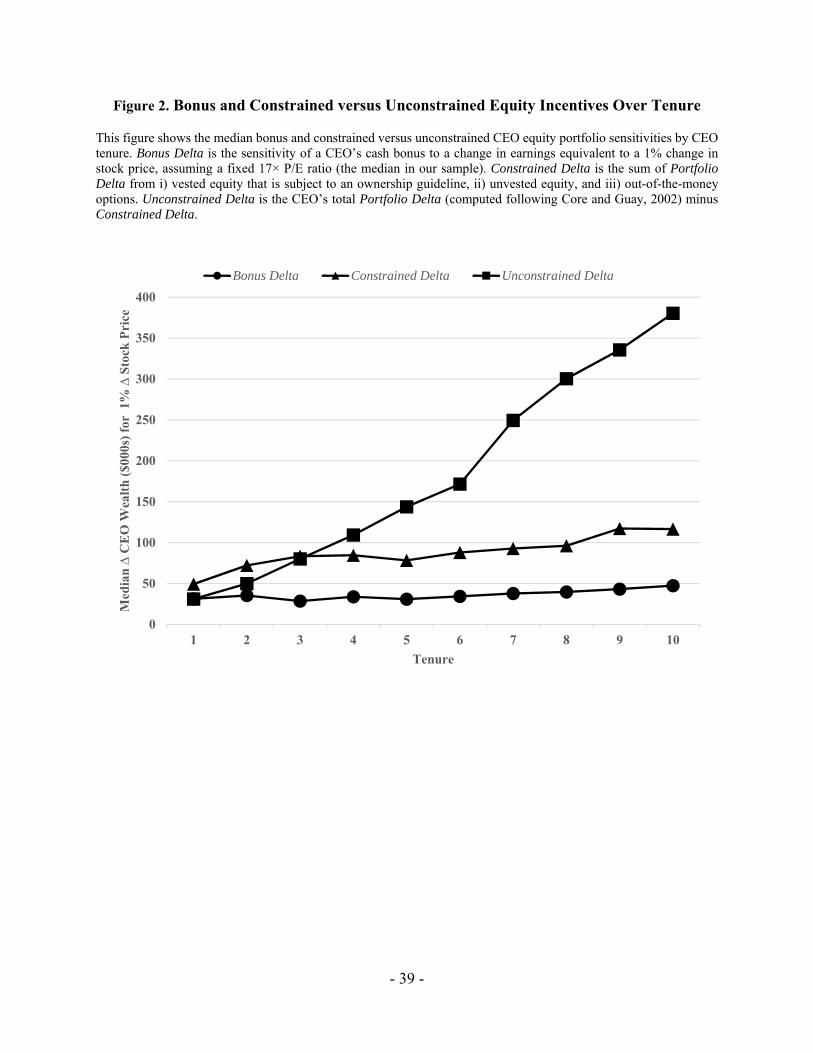

grants or in-the-money options with vesting provisions that have lapsed). In Figure 2, we show

that “constrained” equity, which the CEO cannot sell either because it is unvested or due to a

minimum equity ownership guideline, remains relatively constant over a CEO’s tenure and is

reasonably balanced with cash bonus incentives, while unconstrained equity incentives grow

rapidly and are principally responsible for the growing disparity between cash- and equity-based

incentives as CEO tenure increases.

3.3. Why do prior studies find weaker performance sensitivity?

Next, we evaluate potential reasons why our bonus performance sensitivity estimates differ

so significantly from prior literature. One possibility is that, in recent years, the actual performance

sensitivity embedded in bonus contracts is greater than in the samples considered in prior literature.

For example, the sample in Hall and Liebman (1998) spans from 1980 through 1994 and the

sample in Jensen and Murphy (1990) covers 1969 through 1983. In contrast, our bonus sensitivity

computations are based on data from 2006 through 2014. Boards have been under growing

- 16 -

pressure from shareholders and regulators to strengthen the link between pay and performance,

and our larger estimates may capture increased bonus performance sensitivity since the mid-1990s

in response to this pressure.

Another possibility is that the regression-based estimates in prior literature are unable to

reliably detect the underlying performance sensitivity reflected in executive bonus plans. These

estimates rely on linking cross-sectional or time-series variation in firm performance to variation

in bonus pay and may be quite noisy because of several potential sources of measurement error in

the performance measures underlying bonus contracts. For example, boards may modify

performance targets based on prior results (e.g., Leone and Rock, 2002) or exclude various

expenses when computing earnings (e.g., Bradshaw and Sloan, 2002), both of which could

attenuate the correlation between bonus pay and underlying firm performance and therefore

potentially cause regression-based sensitivities to underestimate the bonus plan’s actual

performance incentives. As we discuss in Section 2, bonus plans also tend to have non-linear

payout structures and zero performance sensitivity above or below certain thresholds (e.g.,

Murphy, 1999; Murphy and Jensen, 2011), which could further attenuate regression-based

estimates of performance sensitivities.

We conduct two series of tests to examine the validity of these two alternative explanations

for the gap between our bonus performance sensitivity estimates and those in prior literature. First,

to evaluate potential time trends in bonus performance sensitivity, we estimate annual bonus-

performance regressions based on the specifications used in prior literature and examine how the

estimated coefficients change over time. Specifically, for each year from 1994 to 2014, we estimate

models of the following form, as in Hall and Liebman (1998):

, (1)

- 17 -

where Compensation is salary plus bonus (i.e., total cash pay) and Performance is either the firm’s

stock return or earnings scaled by market value. We use stock return as a performance measure for

consistency with prior literature (e.g., Jensen and Murphy, 1990; Hall and Liebman, 1998) and

earnings because, as discussed in Section 2, earnings are the primary performance measure used

in bonus contracts. As in Hall and Liebman (1998), we use the current period performance

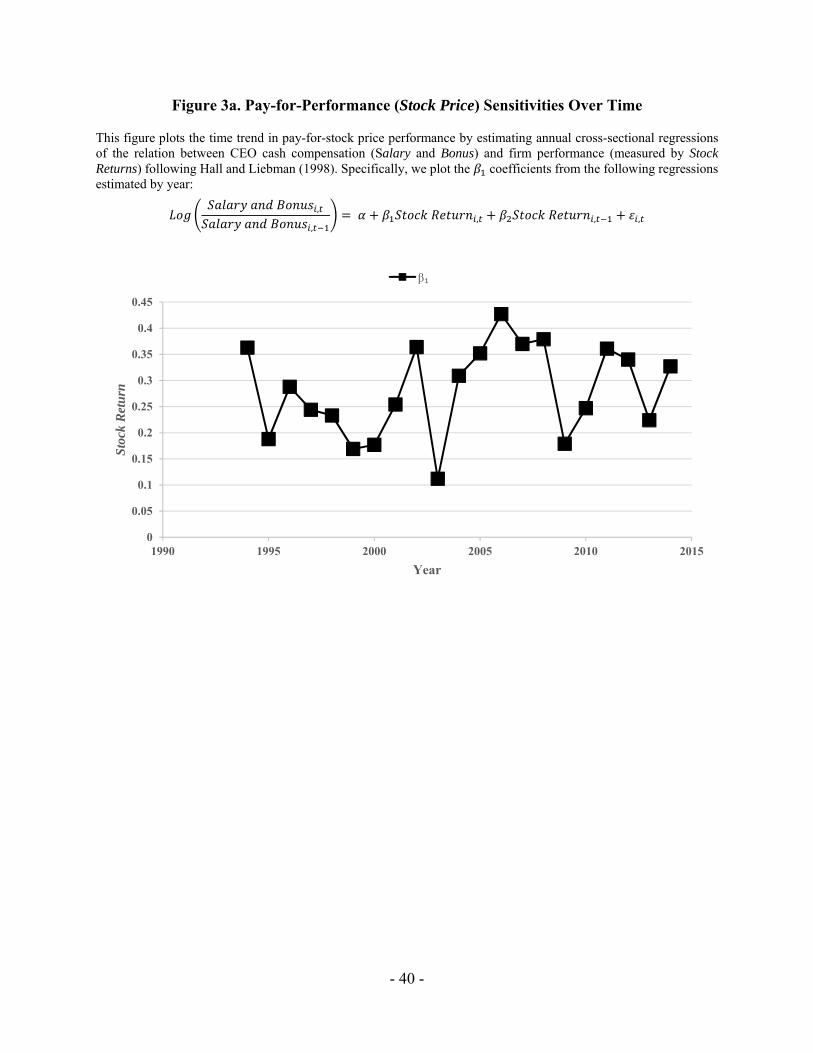

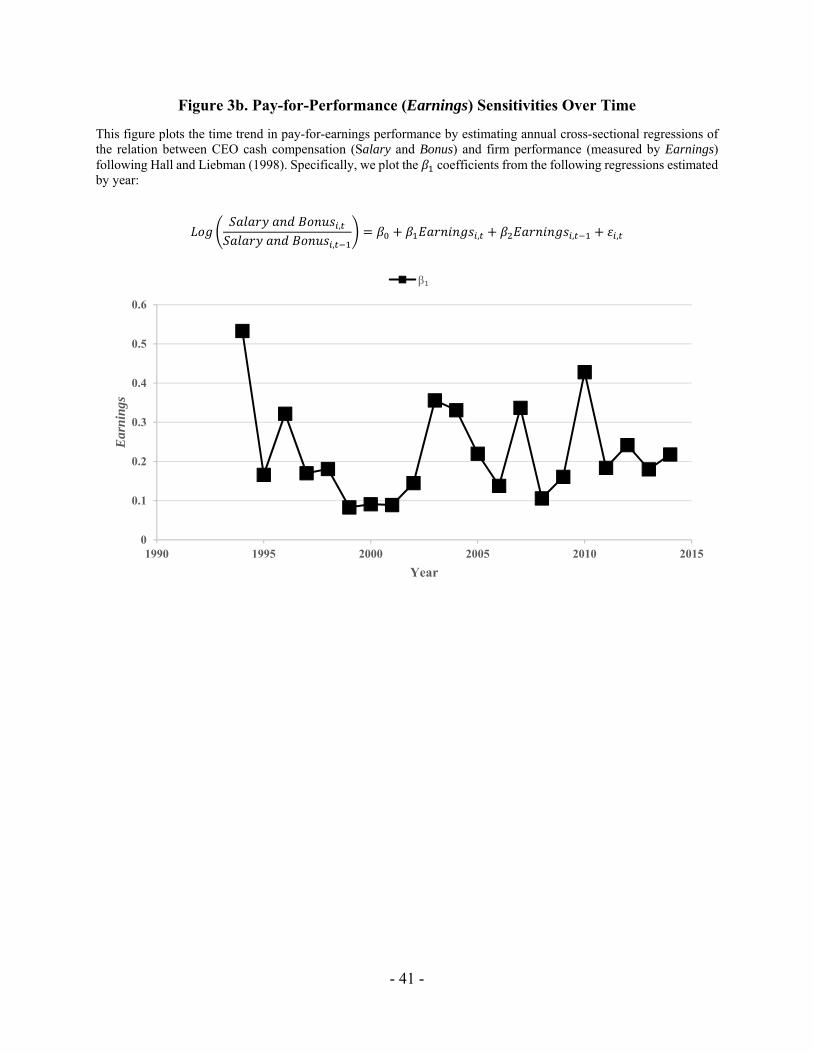

coefficient (i.e., ) to proxy for the performance sensitivity of the bonus plan. Figures 3a and 3b

plot our annual performance sensitivity estimates using stock return and earnings as the

performance measure, respectively. Our sensitivity estimates using stock return as the performance

measure are generally in the range of 0.2 to 0.4 (i.e., a 10 percent increase in stock price

corresponds to a 2 to 4 percent increase in cash pay), comparable to the estimates in Hall and

Liebman (1998). For both performance measures, there is no clear upward pattern: sensitivities in

more recent years are approximately the same as those in the mid-1990s, and casual inspection

suggests that much of the variation in these sensitivities may reflect economic cycles and overall

stock market performance rather than a persistent long-term trend.16

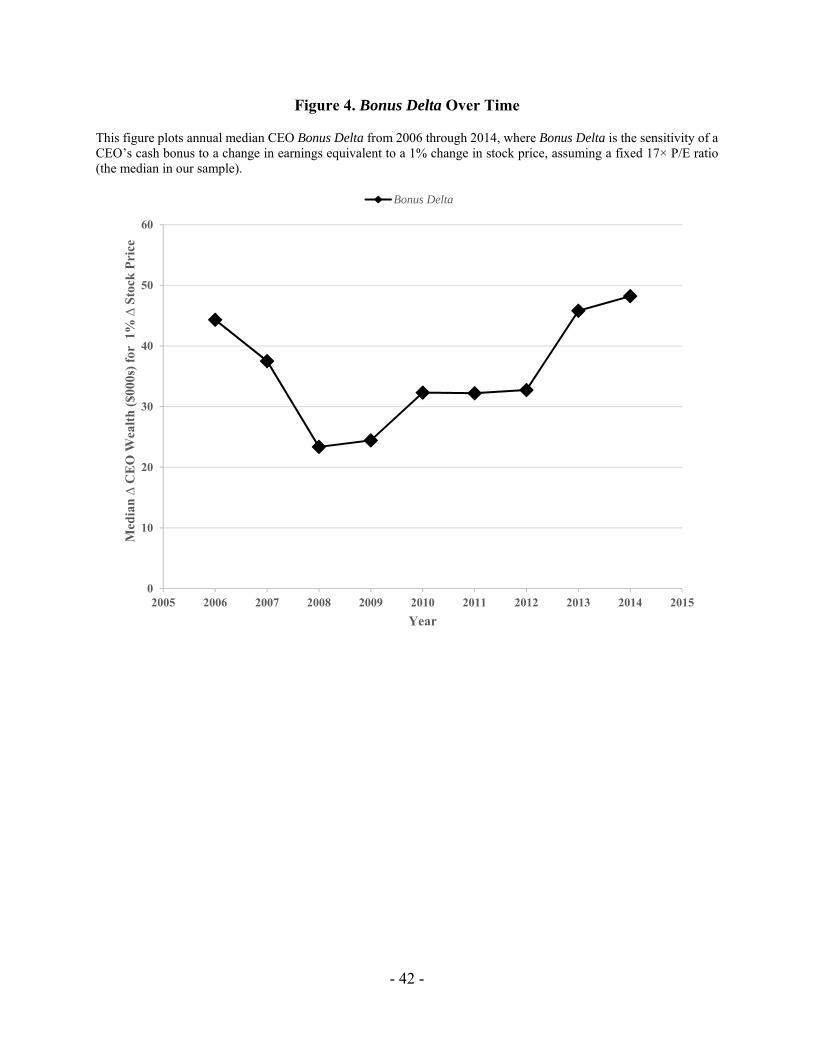

To further explore potential time trends in bonus sensitivities, we examine how the

sensitivities that we directly compute based on bonus plan data have changed over time. Due to

disclosure requirements, our time series for this analysis spans only from 2006 through 2014,

rather than starting from 1994 as in Figure 3. Figure 4 depicts how the median bonus sensitivity

we compute has evolved over this time period. Similar to the regression results, we find no clear

upward pattern, and again the primary source of variation in these sensitivities appears to be driven

by business cycles rather than a secular trend toward greater performance sensitivity. Together,

16 In untabulated analyses, we also examine the variability of cash-based pay relative to the variability of equity-based pay, as in Core et al. (2003), and find no evidence of an upward trend over time.

- 18 -

Figures 3 and 4 suggest that our larger bonus performance sensitivity estimates compared to prior

literature are not driven by differences between sample periods.

Next, we examine how accurately regression-based performance sensitivity estimates

capture the underlying bonus plan’s incentives. We do so by estimating the following variant of

Eq. (1) using only firms for which we can compute an actual bonus performance sensitivity, which

allows us to compare the estimated coefficient to the performance sensitivity that we directly

compute:

, (2)

where Compensation is bonus pay and Performance is earnings scaled by market value. Note that

the performance coefficient in this model is directly proportional to our scaled bonus sensitivity

measure (i.e., Bonus Delta, or how many dollars a CEO receives for earnings of one percent of

market value). Recall that in Table 3, we find mean Bonus Delta of approximately $60,000, which

corresponds to an estimated performance sensitivity coefficient (i.e., ) of about 100,000.17 That

is, if Eq. (2) accurately estimates the underlying performance sensitivity of the bonus contract, the

estimated coefficient should be in the range of 100,000.

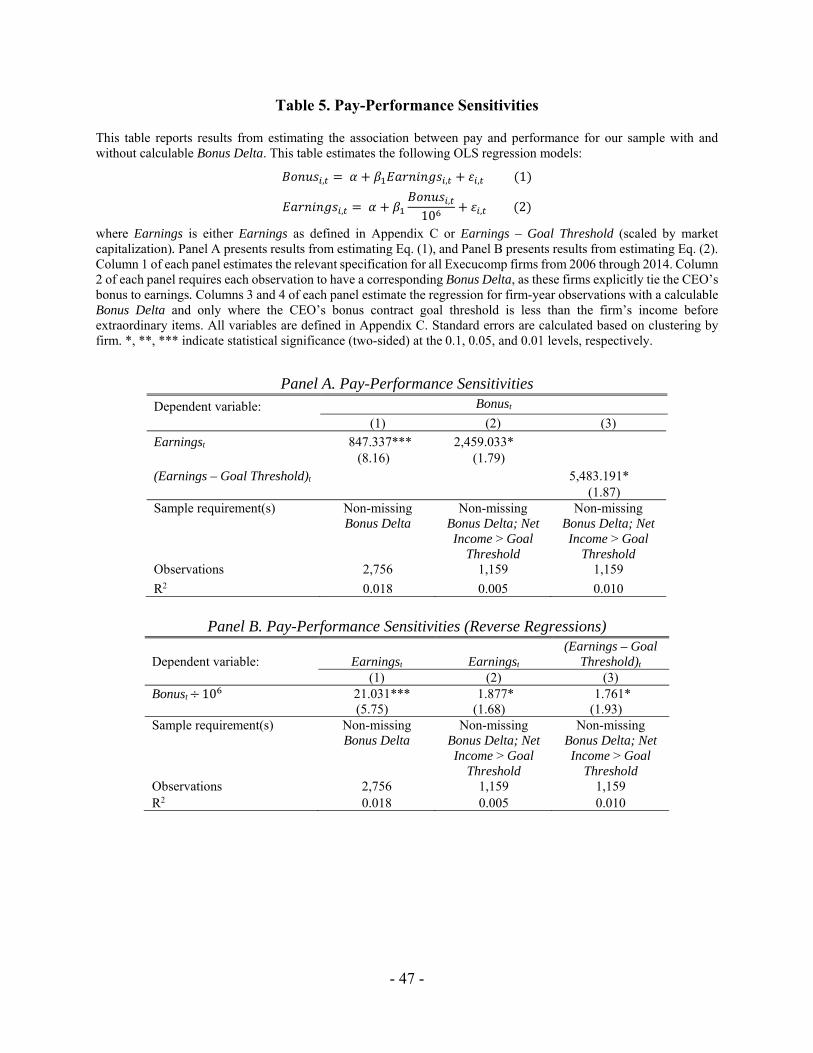

Column 1 of Table 5 Panel A reports results from estimating Eq. (2). In contrast to the

“true” coefficient of 100,000, the estimated performance sensitivity coefficient is approximately

800. That is, our regression estimates indicate that for increasing earnings by one percent of market

value, the CEO receives about $8,000, approximately 100 times less than our measure would

indicate. This result suggests that regression-based performance sensitivity estimates may

17 At a 17× P/E ratio, our mean Bonus Delta of approximately $60,000 implies that the CEO receives $1,020,000 (60,000 x 17) for increasing earnings by one percent of market value. That is, increasing Performance (i.e., earnings scaled by market value) by 0.01 increases Compensation by $1,020,000. We measure Compensation in thousands, so this corresponds to a coefficient of 102,000 (1,020,000 / 1000 / 0.01).

- 19 -

significantly understate the actual incentives embedded in the bonus contract and provides one

plausible explanation for why our estimates vary so substantially from those in prior literature.

To explore why these regression coefficient estimates differ so much from the performance

sensitivities that we directly compute, we re-estimate Eq. (2) using two alternative specifications.

First, to examine the potential effect of non-linearities due to earnings falling outside of the

performance range defined by the bonus plan, we restrict the sample to firms where reported

earnings exceed the specified “threshold” earnings goal. That is, we estimate Eq. (2) using only

firms where reported earnings were sufficiently high for the CEO to receive at least some bonus

payout during the year. Column 2 of Table 5 Panel A reports the results. We find that the

coefficient on earnings under this specification is approximately 2,500, three times greater than in

column 1 and consistent with non-linearities in bonus contracts attenuating regression estimates of

bonus performance sensitivities. Second, to examine the effect of varying performance targets, we

redefine the performance measure as earnings in excess of the threshold goal, rather than raw

earnings (we continue to restrict the sample to this subset of firms with above-threshold earnings).

Column 3 of Table 5 Panel A reports the results. We find that the estimated performance

coefficient is approximately 5,500, twice as large as in column 2 and about six times larger than

in column 1. These results suggest that not accounting for differences in performance targets

between firms also contributes to attenuated performance sensitivity coefficient estimates.

Lastly, to further examine how measurement error may affect our regression-based

performance sensitivity estimates, we re-estimate the three specifications of Eq. (2) described

above as “reverse regressions” (i.e., earnings regressed on bonus). The inverse of the coefficient

from these regressions provides an upper bound estimate of bonus-earnings performance

sensitivity and should not be attenuated by measurement error in the performance measure (i.e,

- 20 -

earnings). Table 5 Panel B presents the results from these reverse regressions.18 In column 1, we

estimate a coefficient of approximately 21, which corresponds to a bonus-earnings coefficient of

approximately 50,000. This is comparable in order of magnitude to our “expected” coefficient of

around 90,000, though still somewhat smaller, consistent with measurement error accounting for

much, but not all, of the attenuated performance sensitivity estimates from Eq. (2). In columns 2

and 3, where we also attempt to control for non-linearity by restricting the sample to firms with

earnings in excess of the bonus payout threshold, we estimate reverse-regression coefficients of

1.9 and 1.8, respectively. These estimates correspond to bonus-earnings coefficients of

approximately 500,000, consistent with them serving as an upper bound on our “expected”

performance coefficients. Collectively, the results in Table 6 suggest that both measurement error

and non-linearity are important factors that attenuate regression estimates of bonus performance

sensitivity.

4. How do boards determine bonus structures?

The results in Section 3 suggest that boards do not substantially alter the magnitude of

bonus incentives over the course of a CEO’s tenure as equity portfolio incentives grow. These

findings raise the question of what factors boards do consider when designing bonus plans and

what the purpose is for such plans. For example, if boards aim to maintain a consistent balance

between cash- and equity-based incentives over a CEO’s tenure, we would expect bonus

sensitivities to increase with equity portfolio incentives. Alternatively, boards could also choose

to eliminate cash-based incentives once equity portfolio incentives become sufficiently large.

However, as we show in Figure 1, neither of these outcomes tends to occur – rather, bonus

18 For expositional purposes, we scale the coefficients by a factor of 1,000,000. This implies that a reverse regression coefficient of 20 would be equivalent to a coefficient of 50,000 in Eq. (2) (1,000,000 / 20).

- 21 -

sensitivities remain quite stable over a typical CEO’s tenure and do not appear to vary

meaningfully with changes in equity portfolio incentives. In this section, we examine several

potential factors that may influence how boards design CEOs’ cash-based incentives to provide

some insight into the intended purposes of these plans.

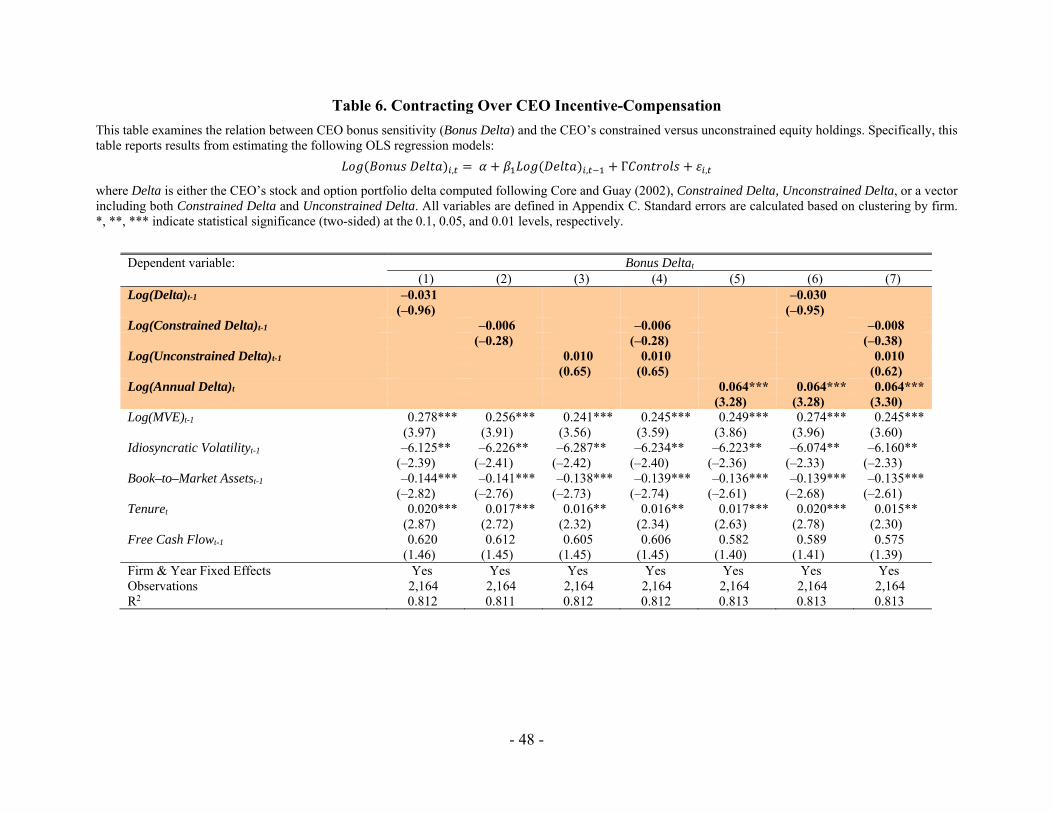

4.1. CEO equity portfolios

We first more directly examine whether boards attempt to coordinate cash- and equity-

based incentives by modeling CEO bonus incentives (Bonus Delta) as a function of a CEO’s equity

portfolio incentives as well as standard economic determinants of CEO incentives from prior

literature (e.g., Core and Guay, 1999; Armstrong et al., 2016):

, ,

, , ,

, , , (3)

where Delta is the CEO’s stock and option portfolio delta as computed in Core and Guay (2002).19

We also consider whether boards differentially incorporate incentives stemming from

“constrained” equity that the CEO is required to hold due to vesting or minimum stock ownership

requirements and “unconstrained” equity that the CEO can sell without restriction (Armstrong et

al., 2016). For example, boards may focus on incentives from constrained equity, which reflect

equity incentives deliberately required by the board, and largely ignore unconstrained equity. We

decompose Delta in Eq. (3) into Constrained Delta and Unconstrained Delta, where Constrained

Delta is Delta from: 1) vested equity that is subject to an ownership guideline, 2) unvested equity,

and 3) out-of-the-money options, and Unconstrained Delta is Delta minus Constrained Delta, as

in Armstrong et al. (2016). Finally, to examine whether boards emphasize incentives from annual

19 Unless noted otherwise, we include firm- and year- fixed effects ( and , respectively) in all estimations in this section.

- 22 -

pay over portfolio incentives, we also consider Annual Delta, the delta of the CEO’s stock and

option grants in the current year.

The results from estimating Eq. (3) are reported in Table 6. Consistent with the descriptive

results from Figure 1, there is no significant relation between Bonus Delta and Delta, suggesting

that boards do not appear to consider equity portfolio incentives when determining CEOs’ cash-

based incentives.20 We also find no significant relation between Bonus Delta and either

Constrained Delta or Unconstrained Delta. Collectively, these results are striking in that they

suggest that boards largely ignore CEOs’ equity portfolio incentives when designing cash-based

incentives. In contrast, we do find a significant positive relation between Bonus Delta and Annual

Delta, suggesting that boards may focus on balancing cash-based incentives with annual equity

grants rather than overall portfolio incentives.

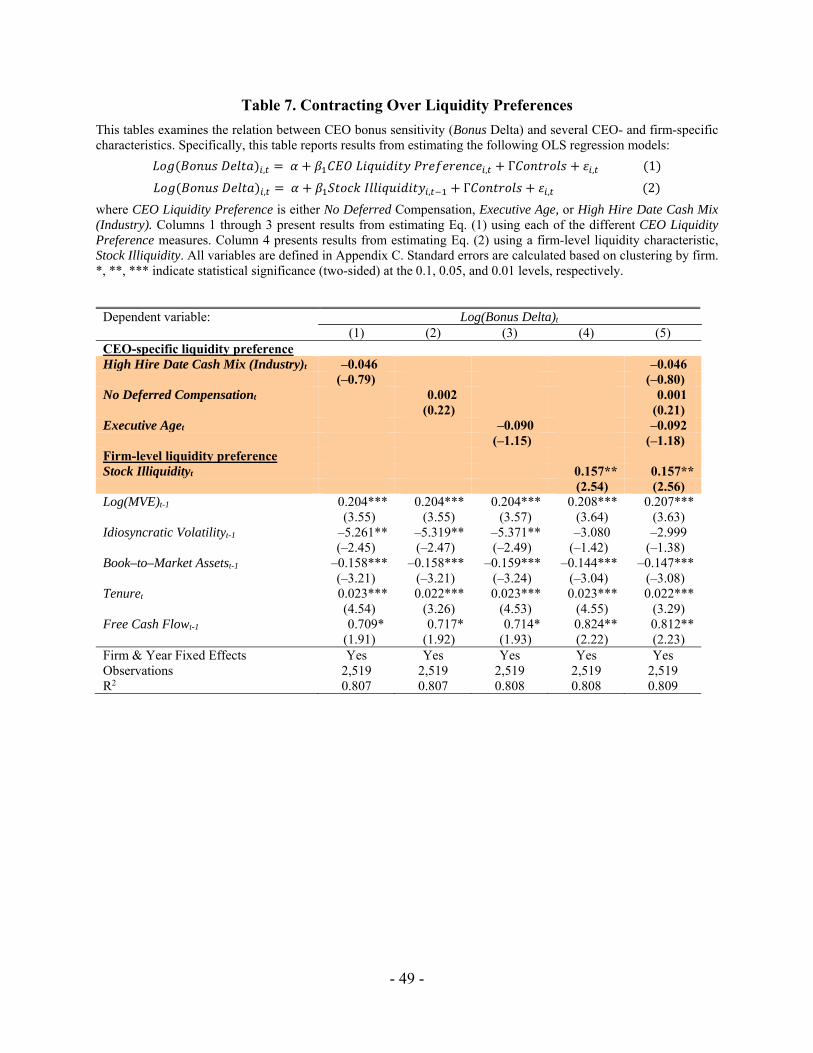

4.2. Liquidity preferences

Next, we examine whether CEO-specific liquidity preferences, or firm-level liquidity

preferences that might affect all executives, appear to influence bonus plan design. We estimate

the following variant of Eq. (3):

, , ,

, , ,

, , (4)

We use four measures for Liquidity Preference in Eq. (4): three proxies for the CEO’s

individual liquidity preferences and one proxy for firm-level liquidity characteristics. Our first

CEO-level liquidity preference measure is based on the “cash mix” (i.e., salary and bonus as a

percent of total compensation) of the CEO’s first-year compensation, High Hire Date Cash Mix

20 In untabulated analyses, we use insider trading and stock and option vesting as instruments for Delta and continue to find no evidence that boards adjust CEO bonus sensitivity in response to CEO equity holdings.

- 23 -

(Industry). Assuming CEOs have some degree of bargaining power in establishing the parameters

of their compensation when they are first hired, a CEO choosing to receive greater cash mix in his

first year may indicate a stronger preference for liquidity. Specifically, we compute cash mix in a

CEO’s first year and define that CEO’s liquidity preference as low (high) if this first-year mix is

below (above) the industry-year median cash mix (i.e., this measure is constant over time for the

same CEO). Second, we define No Deferred Compensation as low (high) for CEOs who

contributed (did not contribute) to a deferred compensation plan in a given year, as CEOs willing

to defer a portion of their current compensation presumably do not have pressing liquidity needs.

Third, we define measure liquidity preferences using the CEO’s age (Executive Age), as older

CEOs have stronger demands for liquidity (e.g., Lewellen et al., 1987). Finally, we measure firm-

level liquidity preferences following Jayaraman and Milbourn (2012), who find that boards put

greater emphasis on cash- (equity-) based incentives when their firm’s stock is less (more) liquid,

Specifically, consistent with Jayaraman and Milbourn (2012), we measure illiquidity (Stock

Illiquidity) as the negative log ratio of the firm’s annual trading volume to shares outstanding.

Table 7 presents results from estimating Eq. (4). We find no evidence that boards consider

CEO-specific liquidity preferences, as there is no significant relation between Bonus Delta and

Delta, High Hire Date Cash Mix (Industry), No Deferred Compensation, or Executive Age. We

do, however, find evidence that boards consider firm-level liquidity characteristics when designing

CEO bonus contracts. In particular, there is a significant positive relation between Bonus Delta

and Stock Illiquidity. Together with the results from Table 6, these findings suggest that boards

may implement bonus plans that consider liquidity preferences across all of the firms’ executives,

rather than tailoring these plans around executive-specific characteristics and preferences, a

possibility we examine further below.

- 24 -

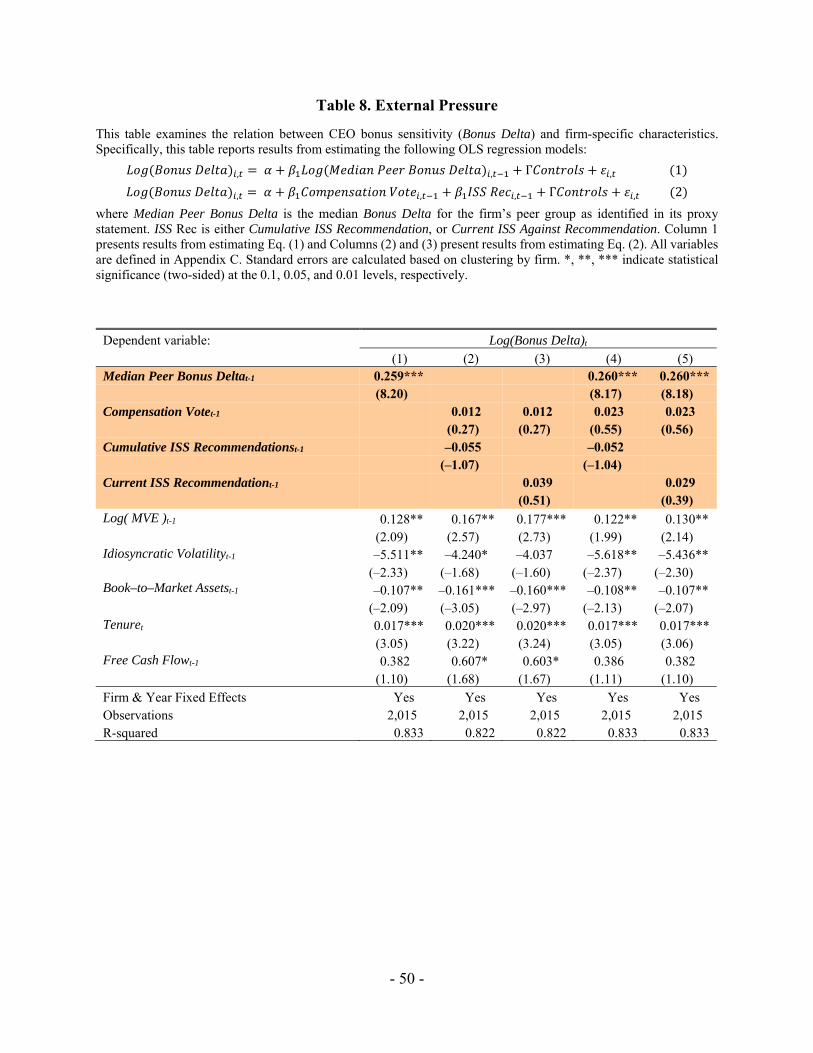

4.3. External pressure and monitoring

We next consider the influence of pressure from external parties on the design of CEO

bonus plans. For example, boards frequently refer to peer-group comparisons when explaining and

justifying their compensation decisions, and Bizjak et al. (2008) and Faulkender and Yang (2010)

find evidence that boards adjust the level of their CEO’s compensation in response to variation in

compensation at peer firms. Furthermore, proxy advisors such as ISS and Glass Lewis also tend to

focus heavily on CEOs’ relative annual pay when evaluating the incentives inherent in executive

compensation plans (e.g., Glass Lewis, 2015; ISS, 2016). As a result, boards may attempt to

benchmark the incentives provided by their CEO’s annual compensation contract to peer group

firms. To examine this possibility, we modify Eq. (3) to include the log of the median Bonus Delta

of the firm’s peer group (Median Peer Bonus Delta):

, ,

, , ,

, , , (5)

To further evaluate the effect of external scrutiny from proxy advisors on the design of

CEOs’ bonus plans, we examine whether these plans respond to proxy advisor recommendations

on executive compensation votes (or, more generally, the existence of such a vote). Specifically,

we estimate the following model:

, , ,

, , ,

, , , (6)

where Compensation Vote indicates whether a shareholder vote on executive compensation

occurred at the annual meeting and ISS Rec indicates whether ISS recommended voting “against”

the compensation plan. We separately consider both the ISS recommendation in the current year

as well as cumulative number of “against” recommendations to account for the possibility that

- 25 -

negative recommendations have persistent effects, rather than only influencing compensation in

the subsequent year. We also consider whether other forms of external monitoring, such as the

presence of institutional investors or blockholders, may influence how boards design CEOs’ bonus

plans by estimating the following model:

, ,

, , ,

, , , (7)

We use three measures for Monitoring in Eq. (7): an indicator for whether the firm is included in

the S&P 500 index (S&P 500), the percentage of shares outstanding owned by institutional

investors (% Institutional Ownership), and the number of investors who own at least one percent

of shares outstanding (Number of Blockholders).

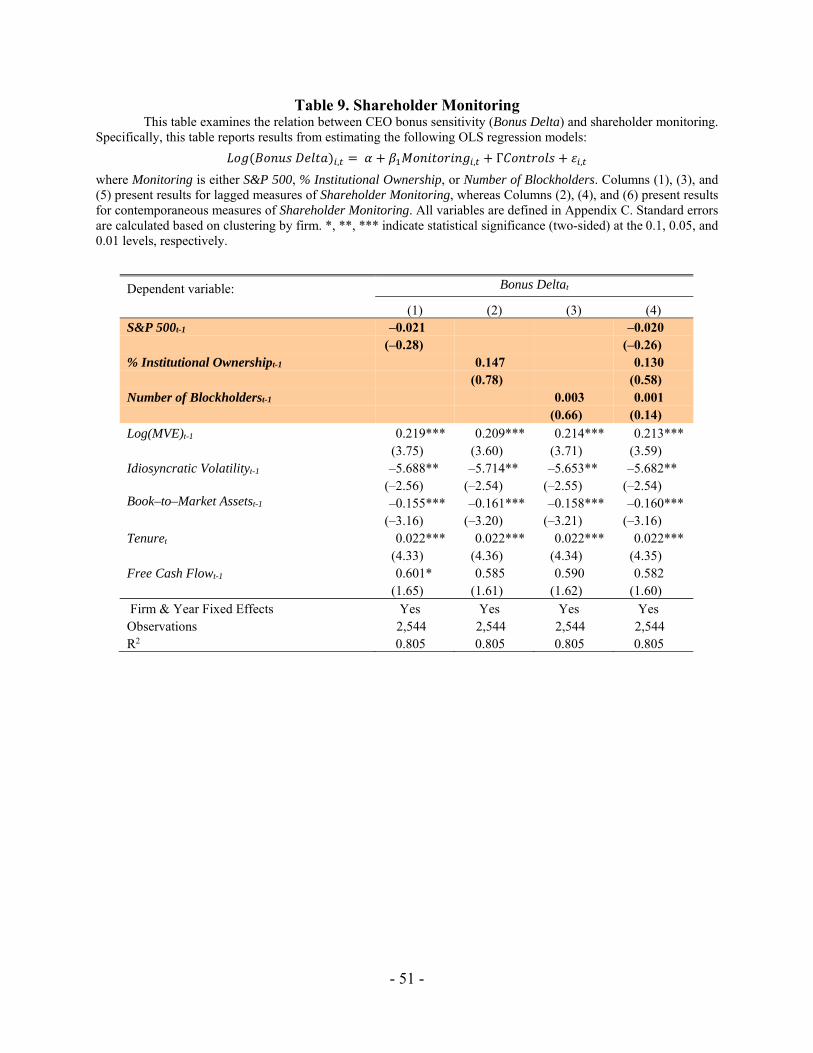

Table 8 displays results from estimating Eq. (5) and (6) and Table 9 displays results from

estimating Eq. (7). In Table 8, we find a significantly positive relation between the firm’s Bonus

Delta and Bonus Delta for peer firms’ CEOs, consistent with peer group effects influencing bonus

plan design. However, we find no evidence that boards respond to shareholder votes on executive

compensation or negative ISS recommendations regarding executive compensation plans.

Similarly, in Table 9, we find no evidence that boards alter bonus plans in response to changes in

the degree of external monitoring. Collectively, these results suggest that while proxy advisors and

institutional investors may have some influence on the factors that boards consider when designing

bonus plans (e.g., focusing on annual or relative pay rather than portfolio incentives), boards do

not appear to deliberately adjust the incentive levels in bonus plans in response to these monitors.

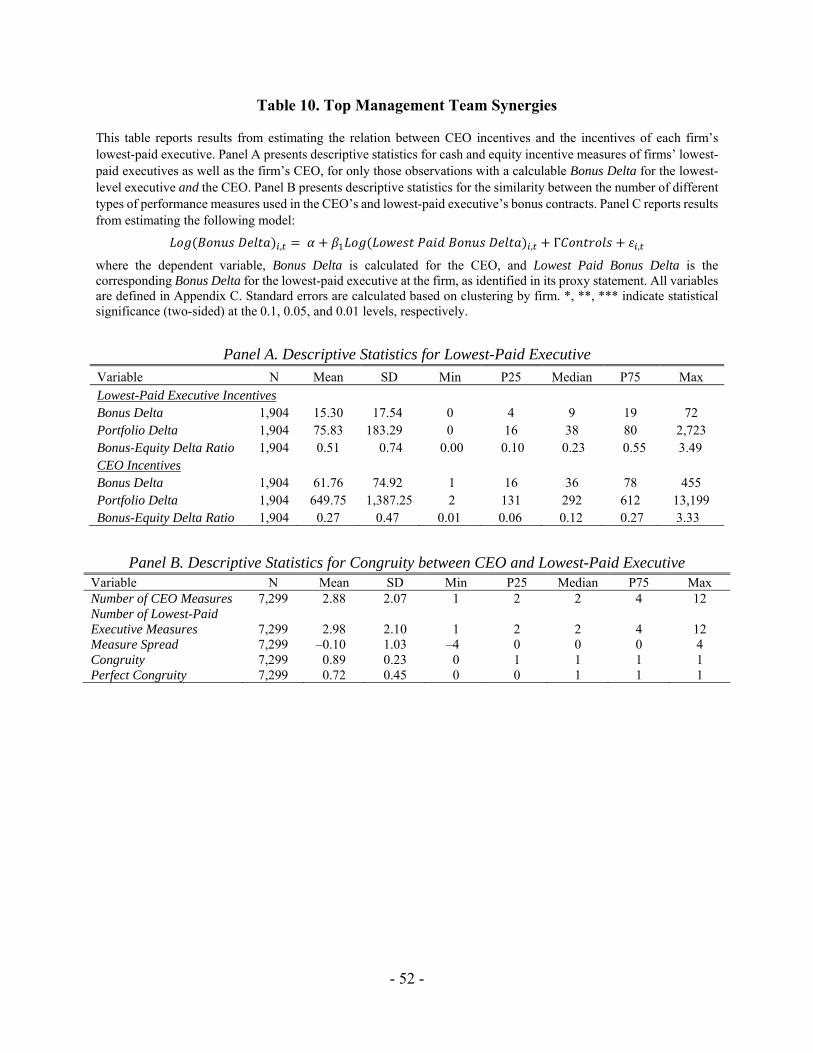

4.4. Top management team synergies

As noted above, boards may primarily intend for bonus plans to motivate the firm’s top

management team as a whole, rather than incentivizing each executive individually. For example,

- 26 -

Edmans et al. (2013) and Bushman et al. (2016) discuss how, due to cost of effort synergies,

managers sharing a common set of performance measures may be incentivized to exert greater

effort than if each manager were paid on a distinct measure. Thus, boards may continue to include

CEOs in bonus plans as part of collectively incentivizing the firm’s top executives, even if the

CEO’s direct financial incentives from these bonuses are relatively modest. To shed light on the

possibility that boards design “firm-wide” executive bonus plans with the intent of covering the

entire top management team and these bonuses are relatively more important for non-CEO

executives, we recompute Bonus Delta and Delta for the lowest-paid executive for which the firm

discloses compensation data (typically the fifth-highest-paid executive at the firm).21 Table 10

Panel A provides descriptive statistics for these results. Consistent with cash-based incentives

being relatively more important to these executives, we find that Bonus Delta for the median

“lowest-paid executive” is about one-fourth of equity Delta (as discussed in Section 3.3, the

median CEO’s Bonus Delta is about one-ninth of equity Delta). If boards design and implement

similar bonus contracts across the firm’s top management, choosing to provide these cash-based

incentives to the firm’s other executives could also result in CEOs receiving similar bonuses even

after their relative incentive effect diminishes.

To explore how closely compensation structure is tied across executives within a firm, we

examine the number of unique (and total) performance measures used in the CEO’s as well as the

lowest-paid executive’s bonus contracts. We define Measure Spread as the difference between the

number of total measures used in the CEO’s bonus contract and the number of total measures used

in the lowest-paid executive’s bonus contract. We also define Congruity as the proportion of

21 In certain cases, the CEO is the lowest-paid executive at the firm. We omit such observations from this analysis. These situations generally arise when the CEO is a founder of the company and holds a very large equity stake in the firm (e.g., Mark Zuckerberg has consistently been the lowest-paid top executive at Facebook).

- 27 -

measures in the lowest-paid executive’s bonus contract that are also included in the CEO’s bonus

contract and Perfect Congruity as an indicator that equals 1 if the CEO’s and lowest-paid

executive’s bonuses are based on exactly the same performance measures (i.e., Measure Spread

equals 0 and Congruity equals 1), and 0 otherwise. Table 10 Panel B provides descriptive statistics

for these results. Consistent with boards designing similar bonus contracts across the firm’s top

management, bonus payouts for both the CEO and the lowest-paid executive are based on exactly

the same measures at the vast majority of firms – Perfect Congruity is 1 at almost 75 percent of

firms and Congruity is 1 at 90 percent of firms.

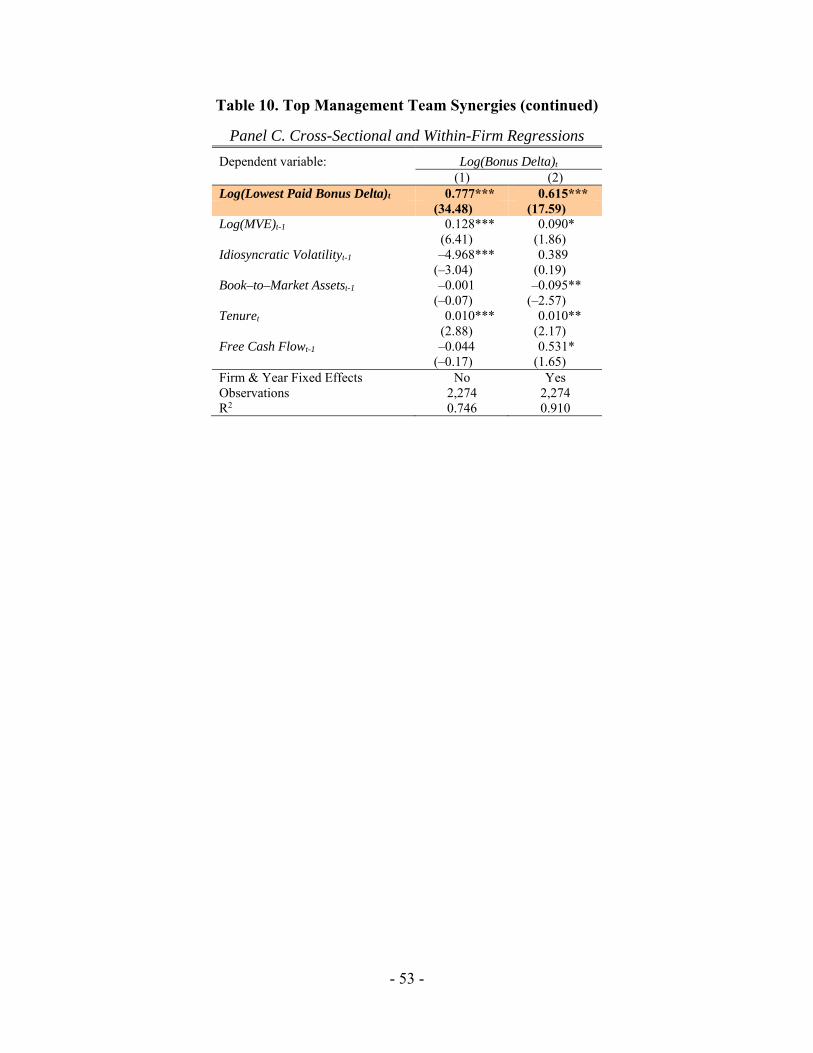

Finally, to further explore the cash-based incentive structure homogeneity across the top

management team at the same firm, we estimate the following variant of Eq. (3):

,

, , ,

, , , (8)

where Lowest Paid Bonus Delta is the Bonus Delta for the lowest-paid executive for which the

firm provides data. Table 10 Panel C reports the results from estimating Eq. (8). Consistent with

top executives within a firm sharing similar incentive compensation structures, we find a strong

association between the bonus structure of the CEO and the lowest-paid executive at the firm.

Collectively, the results from Table 10 are consistent with firms designing “firm-wide” bonus

plans to cover the entire top management team.

5. Conclusion

We document that financial incentives provided by executive bonus contracts are

significantly greater than estimated in previous academic literature. We show executive bonus

contracts can provide meaningful incentives, particularly for CEOs early on in their tenure,

suggesting that boards design incentive compensation contracts at the start of the CEO’s tenure

- 28 -

with a relatively balanced mix of cash- and equity-based pay, but these bonus incentives are

eclipsed by accumulated equity incentives as the CEO’s tenure increases. These results raise the

question of why boards to not adjust executive bonus contracts as CEOs’ equity portfolios grow

over their tenure. We explore several possible explanations, including liquidity preferences,

pressure from shareholders and proxy advisors, and top management team synergies. We find

evidence consistent with some of these explanations, but find no evidence that boards consider

executive-level characteristics when designing cash-based incentive compensation. Collectively,

our results help reconcile the ubiquitous use of bonus plans in executive compensation contracts

with prior literature documenting that CEOs’ financial incentives arise almost exclusively from

their equity portfolios.

- 29 -

References

Armstrong, Chris, John E. Core, and Wayne R. Guay. "Why do CEOs hold equity?" Available at SSRN 2544792 (2016).

Banker, Rajiv D., Masako N. Darrough, Rong Huang, and Jose M. Plehn-Dujowich. "The relation between CEO compensation and past performance." The Accounting Review 88, no. 1 (2012): 1-30.

Bennett, Benjamin, Carr Bettis, Radhakrishnan Gopalan, and Todd Milbourn. "Costs of including accounting performance goals in executive compensation." Working Paper (2015).

Bizjak, John M., Michael L. Lemmon, and Lalitha Naveen. "Does the use of peer groups contribute to higher pay and less efficient compensation?" Journal of Financial Economics 90.2 (2008): 152-168.

Bradshaw, Mark T., and Richard G. Sloan. "GAAP versus the street: An empirical assessment of two alternative definitions of earnings." Journal of Accounting Research 40.1 (2002): 41-66.

Bushman, Robert M., Zhonglan Dai, and Weining Zhang. "Management Team Incentive: Dispersion and Firm Performance." The Accounting Review91.1 (2016): 21-45.

Core, John, and Wayne Guay. "The use of equity grants to manage optimal equity incentive levels." Journal of Accounting and Economics 28.2 (1999): 151-184.

Core, John, and Wayne Guay. "Estimating the value of employee stock option portfolios and their sensitivities to price and volatility." Journal of Accounting Research (2002): 613-630.

Core, John E., and Wayne R. Guay. "Is CEO pay too high and are incentives too low? A wealth-based contracting framework." The Academy of Management Perspectives 24.1 (2010): 5-19.

Core, John E., Wayne R. Guay, and Robert E. Verrecchia. "Price versus non-price performance measures in optimal CEO compensation contracts." The Accounting Review 78.4 (2003): 957-981.

Edmans, Alex and Goldstein, Itay and Zhu, John, Contracting with Synergies (2013). ECGI - Finance Working Paper No. 320/2011. Available at SSRN: http://dx.doi.org/10.2139/ssrn.1958708

Faulkender, Michael, and Jun Yang. "Inside the black box: The role and composition of compensation peer groups." Journal of Financial Economics 96.2 (2010): 257-270.

Gaver, Jennifer J., and Kenneth M. Gaver. "Additional evidence on the association between the investment opportunity set and corporate financing, dividend, and compensation policies." Journal of Accounting and Economics 16.1 (1993): 125-160.

Graham, John R., Si Li, and Jiaping Qiu. "Managerial attributes and executive compensation." Review of Financial Studies 25.1 (2012): 144-186.

- 30 -

Gipper, Brandon. "Assessing the Effects of Disclosing Management Compensation." Working Paper. Available at SSRN 2514578 (2015).

Hausman, Jerry. "Mismeasured variables in econometric analysis: problems from the right and problems from the left." The Journal of Economic Perspectives 15.4 (2001): 57-67.

Hall, Brian J., and Kevin J. Murphy. "Stock options for undiversified executives." Journal of Accounting and Economics 33.1 (2002): 3-42.

Hall, Brian J., and Jeffrey B. Liebman. Are CEOs really paid like bureaucrats? The Quarterly Journal of Economics Vol. CXIII.3 (1998): 653-691.

Healy, Paul M. "The effect of bonus schemes on accounting decisions." Journal of Accounting and Economics 7.1 (1985): 85-107.

Holthausen, Robert W., David F. Larcker, and Richard G. Sloan. "Annual bonus schemes and the manipulation of earnings." Journal of Accounting and Economics 19.1 (1995): 29-74.

Indjejikian, Raffi J., Michal Matejka, Kenneth A. Merchant, and Wim A. Van der Stede. "Earnings targets and annual bonus incentives." The Accounting Review 89.4 (2014): 1227-1258.

Ittner, Christopher D., David F. Larcker, and Madhav V. Rajan. "The choice of performance measures in annual bonus contracts." The Accounting Review (1997): 231-255.

Jayaraman, Sudarshan, and Todd T. Milbourn. "The role of stock liquidity in executive compensation." The Accounting Review 87.2 (2011): 537-563.

Jensen, Michael C., and Kevin J. Murphy. "Performance pay and top-management incentives." Journal of Political Economy (1990): 225-264.

Kaplan, David S., and Brooks Pierce. "Firmwide versus establishment-specific labor market practices." Review of Economics and Statistics 87.3 (2005): 569-578.

Kothari, S. P. "Capital markets research in accounting." Journal of Accounting and Economics 31.1 (2001): 105-231.

Lambert, Richard A., and David F. Larcker. "An analysis of the use of accounting and market measures of performance in executive compensation contracts." Journal of Accounting Research (1987): 85-125.

Lambert, Richard A., David F. Larcker, and Robert E. Verrecchia. "Portfolio considerations in valuing executive compensation." Journal of Accounting Research (1991): 129-149.

Larcker, David F., Allan L. McCall, and Gaizka Ormazabal. "Outsourcing shareholder voting to proxy advisory firms." Journal of Law and Economics 58.1 (2015): 173-204.

Leone, Andrew J., and Steve Rock. "Empirical tests of budget ratcheting and its effect on managers’ discretionary accrual choices." Journal of Accounting and Economics 33.1 (2002): 43-67.

Leone, Andrew J., Joanna Shuang Wu, and Jerold L. Zimmerman. "Asymmetric sensitivity of CEO cash compensation to stock returns."Journal of Accounting and Economics 42.1 (2006): 167-192.

- 31 -

Lewellen, Wilbur, Claudio Loderer, and Kenneth Martin. "Executive compensation and executive incentive problems: An empirical analysis." Journal of Accounting and Economics 9.3 (1987): 287-310.

Matsunaga, Steven R., and Chul W. Park. "The effect of missing a quarterly earnings benchmark on the CEO's annual bonus." The Accounting Review76.3 (2001): 313-332.

Mukhopadhyay, Tathagat, and Lakshmanan Shivakumar. "Do Compensation Disclosures Matter for SoP Voting?." Working Paper. Available at SSRN 2718438 (2015).

Murphy, Kevin J. "Executive compensation." Handbook of Labor Economics 3 (1999): 2485-2563.

Murphy, Kevin J., and Michael C. Jensen. "CEO bonus plans: And how to fix them." Harvard Business School NOM Unit Working Paper (2011): 12-022.

Murphy, Kevin J. "Executive compensation: Where we are, and how we got there." Handbook of the Economics of Finance. Elsevier Science North Holland (Forthcoming) (2012).

Rhodes, Adrienne. "The relation between earnings-based measures in firm debt contracts and CEO pay sensitivity to earnings." Journal of Accounting and Economics 61.1 (2016): 1-22.

Sloan, Richard G. "Accounting earnings and top executive compensation. "Journal of Accounting and Economics 16.1 (1993): 55-100.

- 32 -

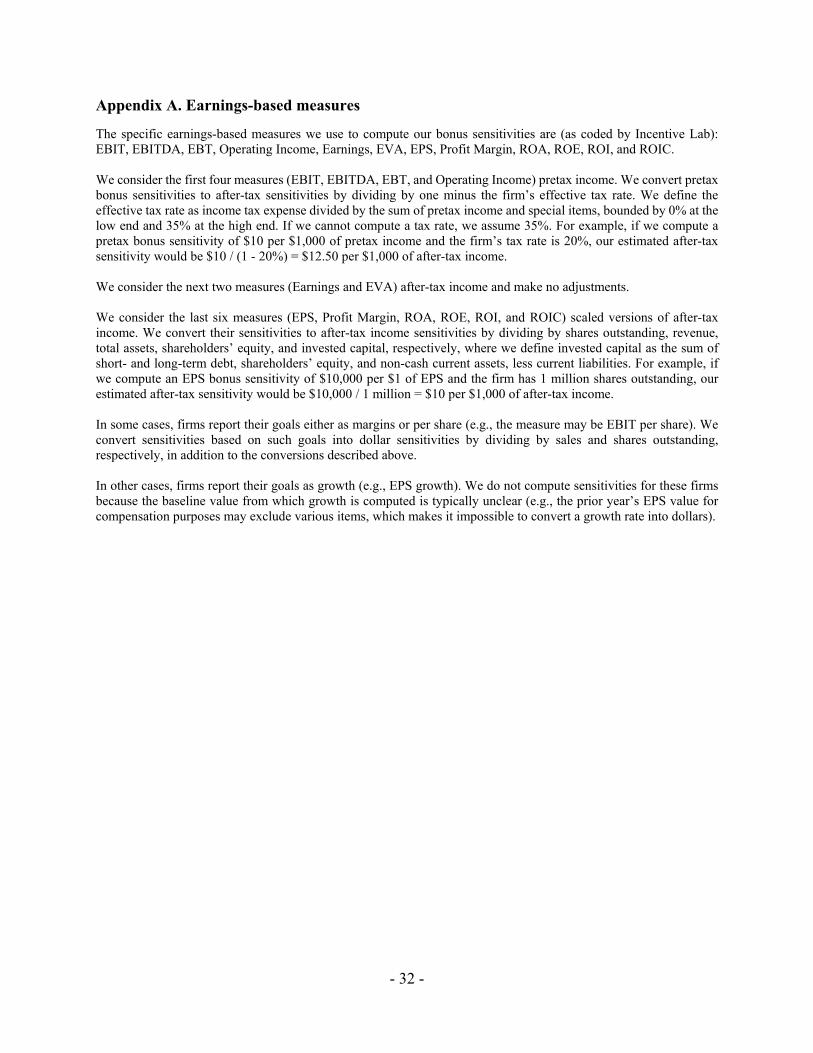

Appendix A. Earnings-based measures

The specific earnings-based measures we use to compute our bonus sensitivities are (as coded by Incentive Lab): EBIT, EBITDA, EBT, Operating Income, Earnings, EVA, EPS, Profit Margin, ROA, ROE, ROI, and ROIC. We consider the first four measures (EBIT, EBITDA, EBT, and Operating Income) pretax income. We convert pretax bonus sensitivities to after-tax sensitivities by dividing by one minus the firm’s effective tax rate. We define the effective tax rate as income tax expense divided by the sum of pretax income and special items, bounded by 0% at the low end and 35% at the high end. If we cannot compute a tax rate, we assume 35%. For example, if we compute a pretax bonus sensitivity of $10 per $1,000 of pretax income and the firm’s tax rate is 20%, our estimated after-tax sensitivity would be $10 / (1 - 20%) = $12.50 per $1,000 of after-tax income. We consider the next two measures (Earnings and EVA) after-tax income and make no adjustments. We consider the last six measures (EPS, Profit Margin, ROA, ROE, ROI, and ROIC) scaled versions of after-tax income. We convert their sensitivities to after-tax income sensitivities by dividing by shares outstanding, revenue, total assets, shareholders’ equity, and invested capital, respectively, where we define invested capital as the sum of short- and long-term debt, shareholders’ equity, and non-cash current assets, less current liabilities. For example, if we compute an EPS bonus sensitivity of $10,000 per $1 of EPS and the firm has 1 million shares outstanding, our estimated after-tax sensitivity would be $10,000 / 1 million = $10 per $1,000 of after-tax income. In some cases, firms report their goals either as margins or per share (e.g., the measure may be EBIT per share). We convert sensitivities based on such goals into dollar sensitivities by dividing by sales and shares outstanding, respectively, in addition to the conversions described above. In other cases, firms report their goals as growth (e.g., EPS growth). We do not compute sensitivities for these firms because the baseline value from which growth is computed is typically unclear (e.g., the prior year’s EPS value for compensation purposes may exclude various items, which makes it impossible to convert a growth rate into dollars).

- 33 -

Appendix B. Bonus sensitivity calculation examples

Example 1

Company: Robert Half International Fiscal Year: 2008 CEO: Harold Messmer, Jr. CEO cash bonus structure as reported in proxy statement

Threshold Target Maximum Range

$ Payout 3,327,273 (A) 6,654,546 (B) 9,000,000 (C) 5,672,727 (D = C – A)

Goal: EPS 0.95 (E) 1.90 (F) 3.8 (G) 2.85 (H = G – E)

Bonus Delta calculation

Description Calculation

Bonus per $1 EPS 1,990,431 (I) D / H

Share outstanding (millions) 150.943 (J) From Compustat

Bonus per $1 million of net income 13,187 (K) I / J (unscaled bonus

sensitivity)

1 % of market capitalization (millions) 31.426 (L) From Compustat

1% of actual net income 2,501,810 (M) From Compustat

Marginal Price-Earnings Ratio 12.56 (N) L / M

Increase in net income to add 1% market capitalization, assuming a firm-year marginal Price-Earnings ratio (millions)

2.502 (O) L / N

Increase in net income to add 1% market capitalization, assuming a 17× Price-Earnings ratio (millions)

1.849 (P) L / 17

Increase in bonus for a 1% increase in market capitalization, assuming a firm-year marginal Price-Earnings ratio

32,991 O * K

Increase in bonus for a 1% increase in market capitalization, assuming a 17× Price-Earnings ratio (Bonus Delta)

24,383 P * K

- 34 -

Appendix B. Bonus sensitivity calculation examples

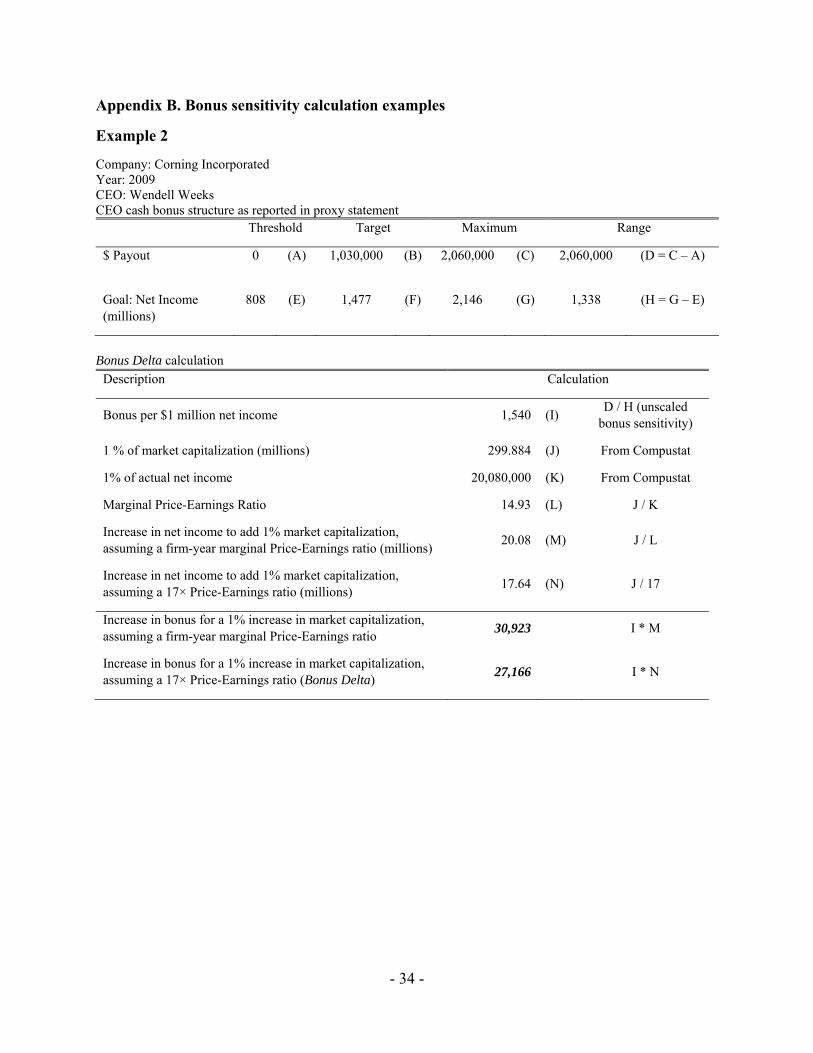

Example 2

Company: Corning Incorporated Year: 2009 CEO: Wendell Weeks CEO cash bonus structure as reported in proxy statement

Threshold Target Maximum Range

$ Payout 0 (A) 1,030,000 (B) 2,060,000 (C) 2,060,000 (D = C – A)

Goal: Net Income (millions)

808 (E) 1,477 (F) 2,146 (G) 1,338 (H = G – E)

Bonus Delta calculation

Description Calculation

Bonus per $1 million net income 1,540 (I) D / H (unscaled

bonus sensitivity)

1 % of market capitalization (millions) 299.884 (J) From Compustat

1% of actual net income 20,080,000 (K) From Compustat

Marginal Price-Earnings Ratio 14.93 (L) J / K

Increase in net income to add 1% market capitalization, assuming a firm-year marginal Price-Earnings ratio (millions)

20.08 (M) J / L

Increase in net income to add 1% market capitalization, assuming a 17× Price-Earnings ratio (millions)

17.64 (N) J / 17

Increase in bonus for a 1% increase in market capitalization, assuming a firm-year marginal Price-Earnings ratio

30,923 I * M

Increase in bonus for a 1% increase in market capitalization, assuming a 17× Price-Earnings ratio (Bonus Delta)

27,166 I * N

- 35 -

Appendix B. Bonus sensitivity calculation examples

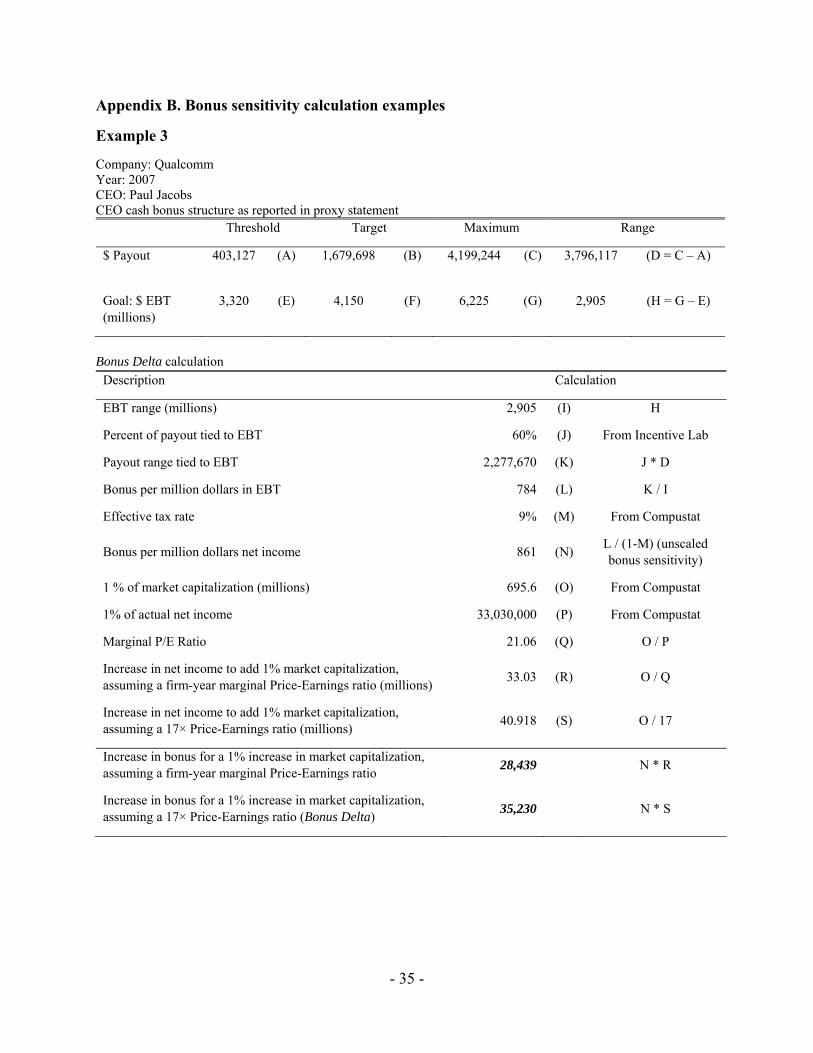

Example 3

Company: Qualcomm Year: 2007 CEO: Paul Jacobs CEO cash bonus structure as reported in proxy statement

Threshold Target Maximum Range

$ Payout 403,127 (A) 1,679,698 (B) 4,199,244 (C) 3,796,117 (D = C – A)

Goal: $ EBT (millions)

3,320 (E) 4,150 (F) 6,225 (G) 2,905 (H = G – E)

Bonus Delta calculation

Description Calculation

EBT range (millions) 2,905 (I) H

Percent of payout tied to EBT 60% (J) From Incentive Lab

Payout range tied to EBT 2,277,670 (K) J * D

Bonus per million dollars in EBT 784 (L) K / I

Effective tax rate 9% (M) From Compustat

Bonus per million dollars net income 861 (N) L / (1-M) (unscaled bonus sensitivity)

1 % of market capitalization (millions) 695.6 (O) From Compustat

1% of actual net income 33,030,000 (P) From Compustat

Marginal P/E Ratio 21.06 (Q) O / P

Increase in net income to add 1% market capitalization, assuming a firm-year marginal Price-Earnings ratio (millions)

33.03 (R) O / Q

Increase in net income to add 1% market capitalization, assuming a 17× Price-Earnings ratio (millions)

40.918 (S) O / 17

Increase in bonus for a 1% increase in market capitalization, assuming a firm-year marginal Price-Earnings ratio

28,439 N * R

Increase in bonus for a 1% increase in market capitalization, assuming a 17× Price-Earnings ratio (Bonus Delta)

35,230 N * S

- 36 -

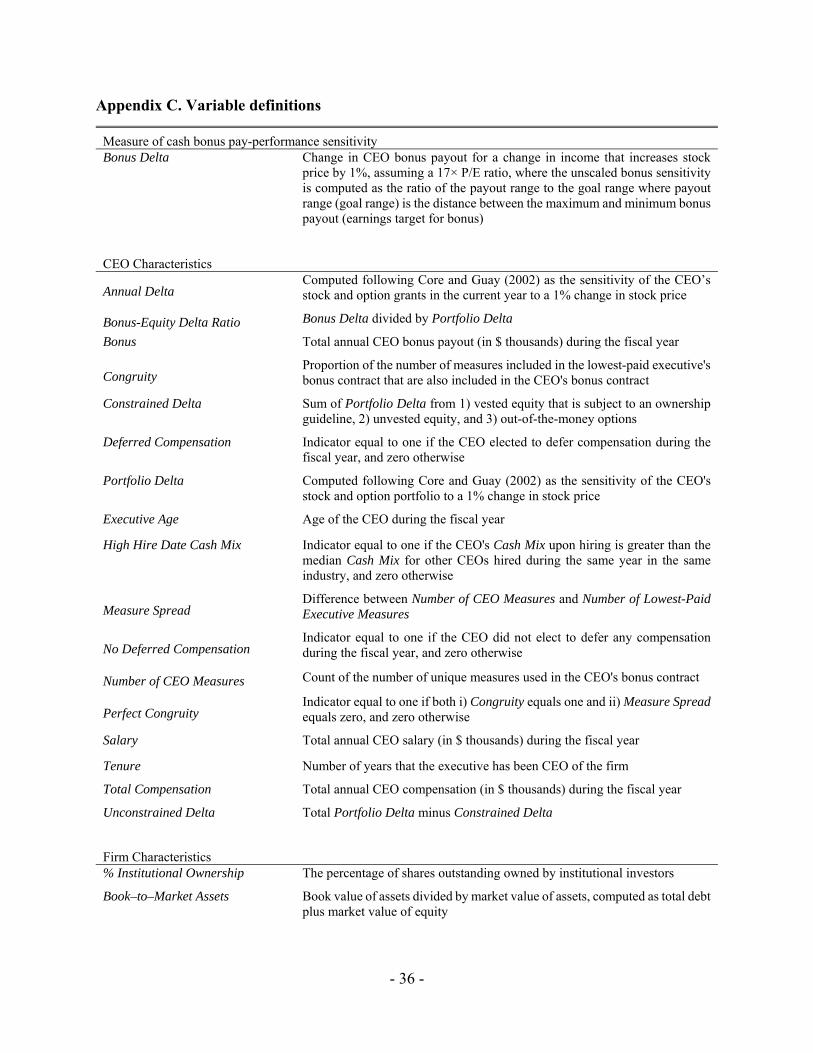

Appendix C. Variable definitions

Measure of cash bonus pay-performance sensitivity Bonus Delta Change in CEO bonus payout for a change in income that increases stock

price by 1%, assuming a 17× P/E ratio, where the unscaled bonus sensitivity is computed as the ratio of the payout range to the goal range where payout range (goal range) is the distance between the maximum and minimum bonus payout (earnings target for bonus)

CEO Characteristics

Annual Delta Computed following Core and Guay (2002) as the sensitivity of the CEO’s stock and option grants in the current year to a 1% change in stock price

Bonus-Equity Delta Ratio Bonus Delta divided by Portfolio Delta

Bonus Total annual CEO bonus payout (in $ thousands) during the fiscal year

Congruity Proportion of the number of measures included in the lowest-paid executive's bonus contract that are also included in the CEO's bonus contract

Constrained Delta Sum of Portfolio Delta from 1) vested equity that is subject to an ownership guideline, 2) unvested equity, and 3) out-of-the-money options

Deferred Compensation Indicator equal to one if the CEO elected to defer compensation during the fiscal year, and zero otherwise

Portfolio Delta Computed following Core and Guay (2002) as the sensitivity of the CEO's stock and option portfolio to a 1% change in stock price

Executive Age Age of the CEO during the fiscal year

High Hire Date Cash Mix Indicator equal to one if the CEO's Cash Mix upon hiring is greater than the median Cash Mix for other CEOs hired during the same year in the same industry, and zero otherwise

Measure Spread Difference between Number of CEO Measures and Number of Lowest-Paid Executive Measures

No Deferred Compensation Indicator equal to one if the CEO did not elect to defer any compensation during the fiscal year, and zero otherwise

Number of CEO Measures Count of the number of unique measures used in the CEO's bonus contract

Perfect Congruity Indicator equal to one if both i) Congruity equals one and ii) Measure Spread equals zero, and zero otherwise

Salary Total annual CEO salary (in $ thousands) during the fiscal year

Tenure Number of years that the executive has been CEO of the firm

Total Compensation Total annual CEO compensation (in $ thousands) during the fiscal year

Unconstrained Delta Total Portfolio Delta minus Constrained Delta

Firm Characteristics

% Institutional Ownership The percentage of shares outstanding owned by institutional investors

Book–to–Market Assets Book value of assets divided by market value of assets, computed as total debt plus market value of equity

- 37 -

Compensation Vote Indicator equal to one if a shareholder vote on executive compensation occurred at the annual meeting during the fiscal year, and zero otherwise