Embed Size (px)

Citation preview

6/19/2014

1

Brian Nixon, Chief Executive

NDA Scottish SME Steering Team

Dounreay, Thursday 13 February 2014

market

challenges

opportunities

the role for Decom North Sea

courtesy Peterson SBS / Veolia

oil & gas decommissioning ‐ agenda

6/19/2014

2

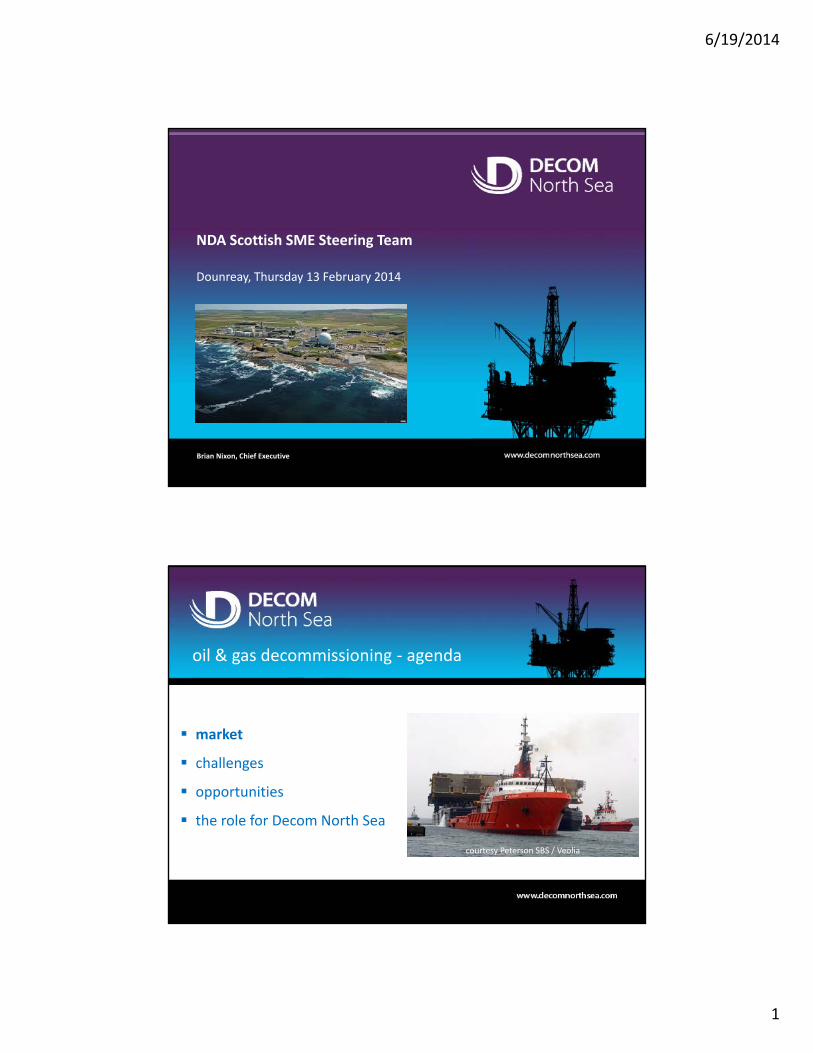

general situation in UK Continental Shelf

£11.4 billion CAPEX in 2012 with forecast of £13.5 billion in 2013 £44 billion of capital investment approved and under development 45 new projects approved in 2011 & 2012

however:‐ production in UKCS has fallen for 11 straight years (10.7% in 2012 alone) concerns over unplanned shutdowns, reliability of equipment etc. operating costs rising – produced water, energy consumption, asset integrity, etc. production efficiency falling only 13 new exploration wells started in 2013

resulting in several assets nearing CoP and decommissioning

The Convention for the Protection of the marine Environment of the north

east Atlantic ‐ ‘OSPAR Convention‘.

Signed and ratified by all Contracting Parties to the original Oslo or Paris Conventions (Belgium, Denmark, the European Union, France, Germany, Iceland, Ireland, the Netherlands, Norway, Portugal, Spain, Sweden and the United Kingdom and Northern Ireland) and by Luxembourg and Switzerland.

regulations for offshore decommissioning

6/19/2014

3

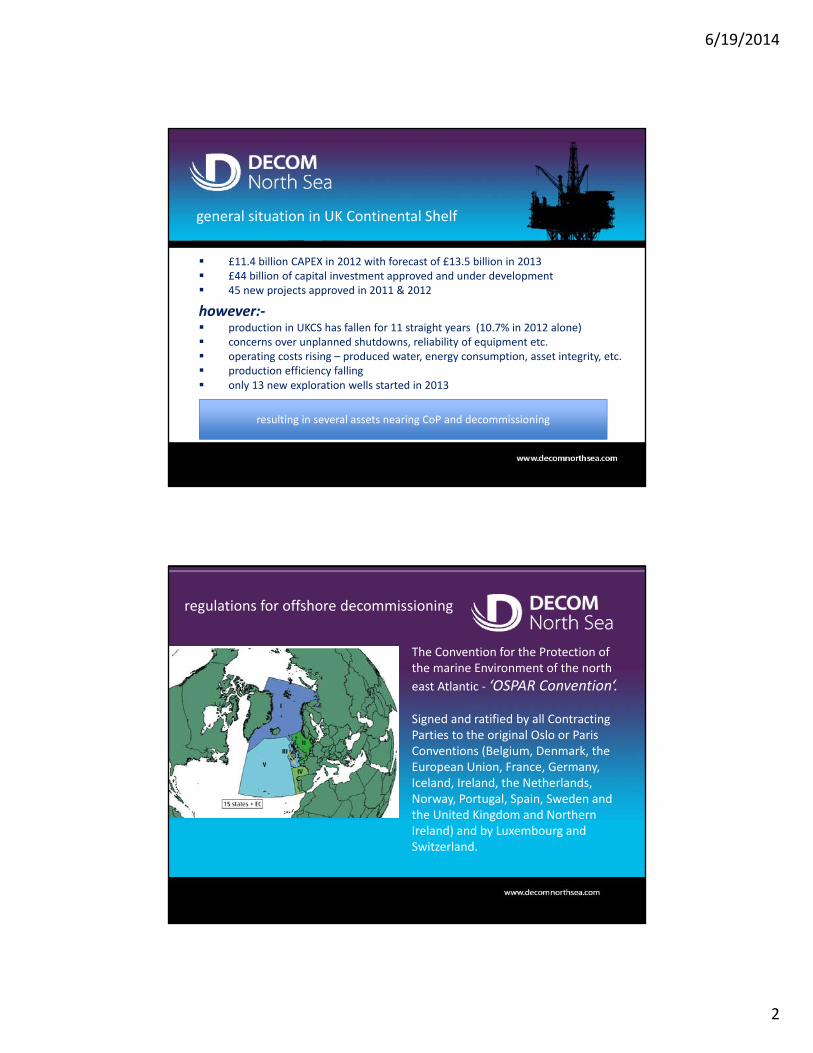

little thought of decommissioning at design and build stage, or through life of asset

most operators preparing for first project

forecast costs rising

multiple drivers to defer

limited experience – operators or contractors

decommissioning projects unique and stand alone

some market observations

0

1000

2000

3000

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042

£m (Real 2011)

Potential Decommissioning Expenditure$70/bbl and 40p/therm

Hurdle : Real NPV @ 10% / Devex @ 10% > 0.3

Cns Irish Sea MF NNS SNS WoS

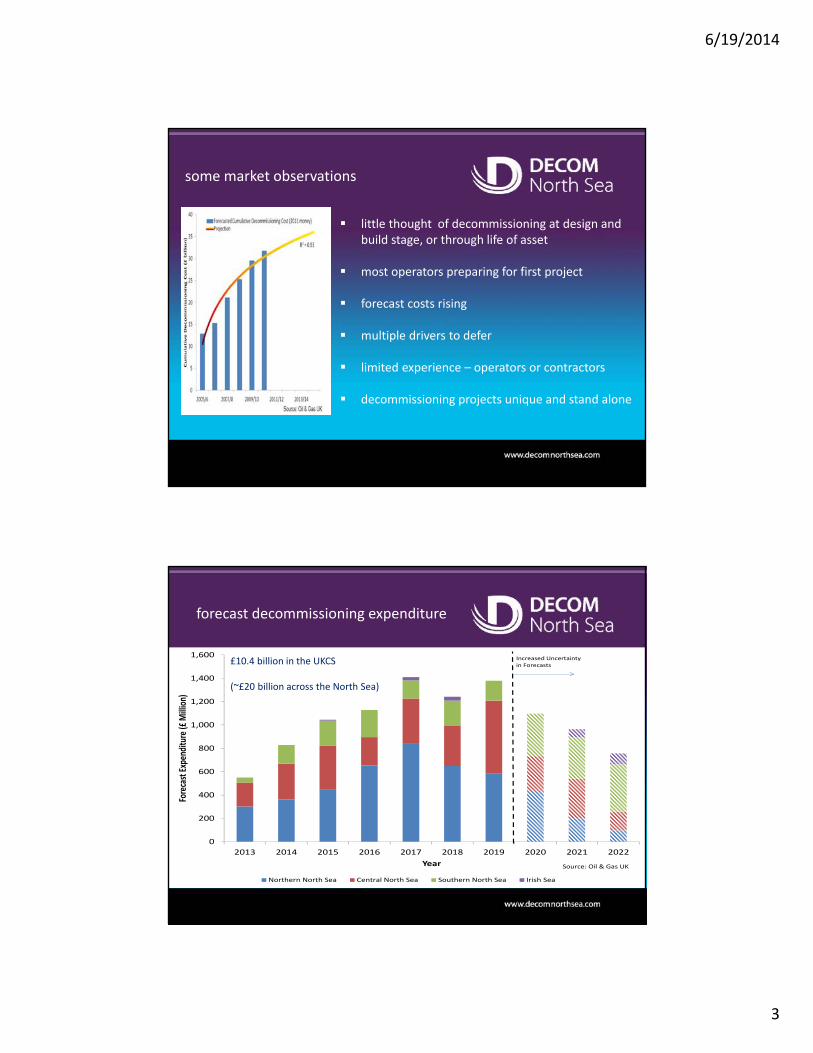

forecast decommissioning expenditure

0

200

400

600

800

1,000

1,200

1,400

1,600

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Forecast Expen

diture (£

Million)

Year

Northern North Sea Central North Sea Southern North Sea Irish Sea

Source: Oil & Gas UK

Increased Uncertainty in Forecasts£10.4 billion in the UKCS

(~£20 billion across the North Sea)

6/19/2014

4

0

1000

2000

3000

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042

£m (Real 2011)

Potential Decommissioning Expenditure$70/bbl and 40p/therm

Hurdle : Real NPV @ 10% / Devex @ 10% > 0.3

Cns Irish Sea MF NNS SNS WoS

decommissioning expenditure ‐ UKCS

11%

43%

13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Prop

ortion

of Total Expen

diture For Each Work

Breakdo

wn Structure Co

mpo

nent

Monitoring

Topsides and SubstructureRecycling

Site Remediation

Subsea Infrastructure

Topsides Removal

Substructure Removal

Topsides Preparation

Facility/Pipeline Making Safe

Wells

Facility Running/Owners'Costs

Operator ProjectManagement

Source: Oil & Gas UK

Overheads:19%

Wells: 43%

Removal:21*%

*This relates to expenditure clearly identified as removal

1% of > £30 billion= £300 million

market

challenges

opportunities

the role for Decom North Sea

courtesy Peterson SBS / Veolia

oil & gas decommissioning ‐ agenda

6/19/2014

5

•Exploration & appraisal

+$

Years

-$

development

abandonment

production

operations

challenge - the oil & gas life cycle

exploration & appraisal

regular industry perception of life cycle

decommissioning often overlooked

programme to DECC June 2013 – CoP in 2014

topsides ‐ 24,548 tonnes – 26 modules

steel jacket ‐ 24,640 tonnes (excl piles)

water depth 156m – 150 km NE of Shetland

33 platform & subsea wells

drill cuttings pile – degrade naturally in time

export pipeline – remedial rock placement

infield pipelines & branches ‐ removed

Steel Piled Jacket (SPJ) structuresCNR International – Murchison Platform

6/19/2014

6

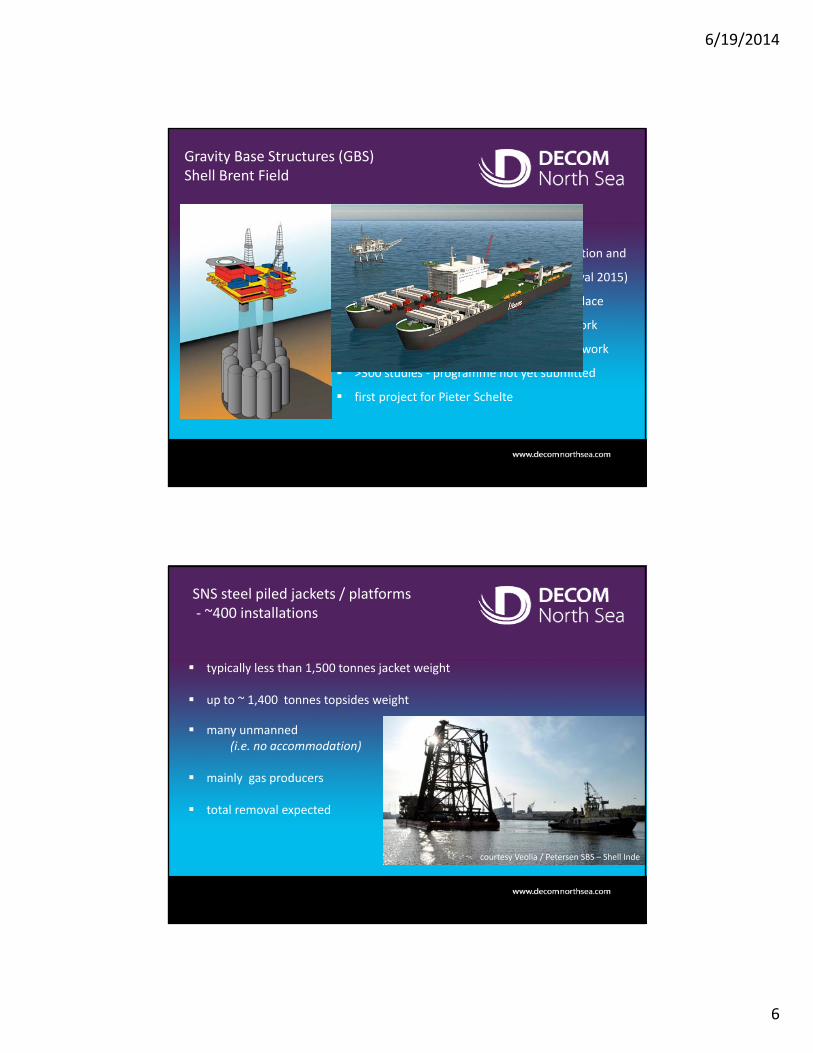

Gravity Base Structures (GBS) Shell Brent Field

production ceased December 2011

contracts for topsides removal, transportation and

onshore disposal recently awarded (removal 2015)

GBS ~ 400,000 tonnes likely to remain in place

P&A of wells underway – many years of work

topsides preparation underway – years of work

>300 studies ‐ programme not yet submitted

first project for Pieter Schelte

SNS steel piled jackets / platforms‐ ~400 installations

typically less than 1,500 tonnes jacket weight

up to ~ 1,400 tonnes topsides weight

many unmanned (i.e. no accommodation)

mainly gas producers

total removal expected

courtesy Veolia / Petersen SBS – Shell Inde

6/19/2014

7

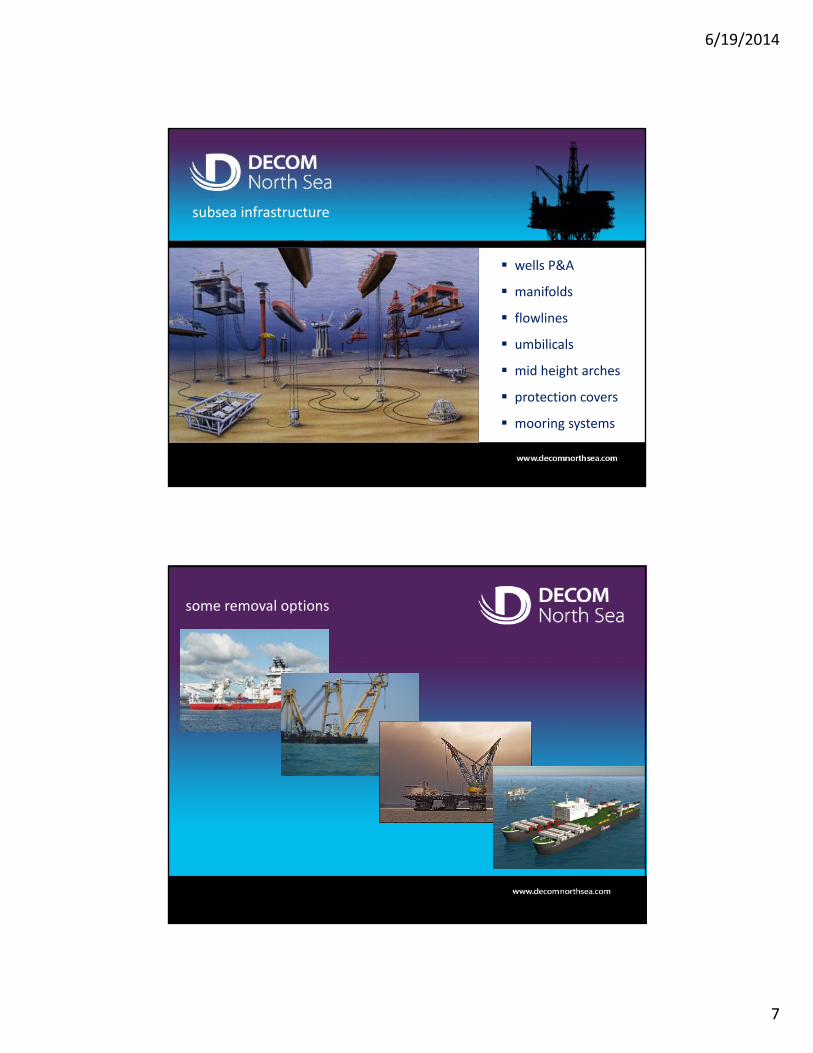

subsea infrastructure

wells P&A

manifolds

flowlines

umbilicals

mid height arches

protection covers

mooring systems

some removal options

6/19/2014

8

market

challenges

opportunities

the role for Decom North Sea

courtesy Peterson SBS / Veolia

oil & gas decommissioning ‐ agenda

decommissioningwork breakdown

structure

suspension live

cleaning & decommissioning

suspension cold (NUI/MMI)

onshore disposal

continuing liability

disconnectionwell

abandonmentpreparation for CoP

removal

ReservoirConceptsImpact sRisksInventorySurveysInspectionsRe‐useTechnicalSocietalEnvironment

Tier 1 contractorsCare and maintenanceInspectionIntegrity

P&A of wellsRig upgradesWaste and scale treatmentPost productionops. supportRig‐less options

Isolation/PurgingCleaning & treatingWaste disposal Waste accountingPost productionops. support

DisconnectionSplit modulesRemove small &loose itemsPrepare for NUI/MMIPost productionops. support

MaintenanceStructural integrityMonitoringWaiting for removal

Hook downModule separationPadeye refurbishmentSea bed clean‐upRemoval :‐Single liftReverse engineeringPiece small

OffloadingCleaning & handlinghazardous materialsDeconstructionRecycle and disposalPossible re‐use

Monitoring programme :‐remainingstructuresor subsea

typical phases indecommissioning programmes

6/19/2014

9

market

challenges

opportunities

the role for Decom North Sea

courtesy Peterson SBS / Veolia

oil & gas decommissioning ‐ agenda

since 2010 ‐the industry forum for decommissioning

not‐for‐profit organisation, privately funded

230 member companies from Denmark, Germany, Norway, The Netherlands, the UK and USA

membership across the whole sector:‐operators (large & small), contractors, marine, subsea, onshore disposal, wells P&A, legal, environmental, specialist services, consultants etc

6/19/2014

10

Decom North Sea’s role in the industry

stimulating a vibrant, efficient and cost effective industry

promoting collaboration and the sharing of knowledge and learning

developing models, templates and guidelines for the decommissioning sector

responding to economic and technical challenges facing the sector

researching other sectors for synergies and experience (GoM, nuclear, salvage)

stimulating a vibrant, efficient and cost effective industry

promoting collaboration and the sharing of knowledge and learning

developing models, templates and guidelines for the decommissioning sector

responding to economic and technical challenges facing the sector

researching other sectors for synergies and experience (GoM, nuclear, salvage)

joint industry initiatives

standard template for decommissioning programmes

standard template for decommissioning programmes

research greater re‐use of plant and equipment

research greater re‐use of plant and equipment

model template for EIAsmodel template for EIAs

compensation models in different phases and types of decommissioning compensation models in different

phases and types of decommissioning

North Sea map of onshore disposal facilities

North Sea map of onshore disposal facilities

Southern North Seaspecial interest groupSouthern North Seaspecial interest group

work together earlier & betterwork together earlier & better

more reliable activity forecasts to support industry investment

more reliable activity forecasts to support industry investment

multi‐party approach ‐ start with wells P&Amulti‐party approach ‐ start with wells P&A raise awareness & profile of

decommissioningraise awareness & profile of

decommissioning

6/19/2014

11

benefits of membership

operator programme update events

training courses

industry lunch ‘n learns

learning journeys around the North Sea

2 annual conferences (one with Oil & Gas UK)

work groups and steering groups on JIPs

website with industry capability matrix

regular newsletters

market intelligence reports

business advice

operator programme update events

training courses

industry lunch ‘n learns

learning journeys around the North Sea

2 annual conferences (one with Oil & Gas UK)

work groups and steering groups on JIPs

website with industry capability matrix

regular newsletters

market intelligence reports

business advice