Embed Size (px)

Citation preview

8/4/2019 DNH Market Watch Daily 05.10

http://slidepdf.com/reader/full/dnh-market-watch-daily-0510 1/1

Daily

5th October 2011Market Indices Market Performance

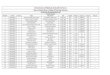

05.10.2011 04.10.2011 %Chg.ASPI 6,706 6,722 -0.2MPI 5,967 5,983 -0.3Turnover (bn) 1.3 2.0 -33.1Foreign Purchases (mn) 67.8 98.1 -30.9Foreign Sales (mn) 155.8 166.7 -6.5Traded Companies 234 245 -4.5Market PER (X) 17.3 17.3 0.0Market Cap (LKR bn) 2,408 2,414 -0.2Market Cap (US$ bn) 21.7 21.7 -0.2Dividend Yield (%) 1.6 1.6 0.0Price to Book (X) 2.2 2.2 0.0

Market Outlook Market Turnover

Gainers /Losers (%)

Significant Trades (Turnover in LKR Mn)

Global Markets Interest Rates & CurrenciesIndex %Chg. . .05.10.2011

Sri Lanka - ASPI 6706 -0.22 Prime Lending Rate (Avg. Weighted) 9.1%India - Sensex 15792 -0.46 Deposit Rate (Avg. Weighted) 6.5%Pakistan - KSE 100 11868 0.55 Treasury Bill Rate (360 Days) 7.3%Taiwan Weighted 6989 -0.83 Dollar Denominated Bond Rate 6.3%Singapore - Straits Times 2529 -0.09 LKR/US$ (Avg. Rate) 111.1Hong Kong - Hang Seng N/A N/A LKR/EURO (Avg. Rate) 148.4

Disclaimer

D N H M A R K E T W

A T C H

0

100

200

300

400

ECL RGEM HPFL REG

13.8

12.6

11.4

9.6

-10.0

-9.8

-9.4

-9.1

Alliance Finance

E-Channelling

Hayleys Exports

Ceylon & Foreign Trades

Associated Motor Finance

Singer Industries

Ceylon Hospitals

Trans Asia Hotels

5,700

5,900

6,100

6,300

6,500

6,700

6,900

2 9 / 9 / 2 0 1 1

3 0 / 9 / 2 0 1 1

3 / 1 0 / 2 0 1 1

4 / 1 0 / 2 0 1 1

5 / 1 0 / 2 0 1 1

ASI

MPI

DNH Financial (Pvt) Ltd.www.dnhfinancial.com

+94115700777

This Reviewis prepared andissued by DNHFinancial (Pvt.)Ltd.(DNH)based on information in thepublic domain, internally developedand othersources,believed to be

correct. Although allreasonable care hasbeen taken to ensure thecontentsof theReview are accurate, DNHand/or itsDirectors, employees, are notresponsible forthe

correctness,usefulness, reliabilityof same. DNHmayact asa Brokerin theinvestments whichare thesubjectof this documentor related investments andmayhaveacted

on or used the information contained in this document, or the research or analysis on which it is based, before its publication. DNH and/or its principal , their

respective Directors, orEmployees mayalsohavea positionor beotherwise interested inthe investmentsreferredto inthisdocument. This isnot anofferto sell orbuy the

investmentsreferredto in this document.ThisReview maycontaindatawhich areinaccurate andunreliable. Youhereby waive irrevocably anyrights orremedies in law

or equity you have or may have against DNH with respect to the Review and agree to indemnify and hold DNH and/or its principal, their respective directors and

employeesharmless to thefullestextent allowed by lawregarding allmattersrelatedto youruse of thisReview.

Trading on the bourse today was anything but inspiringwith the ASPI and the MPI dropping a notch to 6706 and5967 on the back of lackluster investment sentiment.Turnover declined to a two week low, falling to LKR1.3 bn

with trading in E-Channelling, Radiant Gems and HydroPower Free Lanka accounting for 34% of the day’s total.Losers outpaced gainers, with Associated MotorFinance, Singer Industries and Ceylon Hospitals decliningby 10.0%, 9.8% and 9.4% offsetting gains in AllianceFinance, E-Channelling and Hayleys Exports which rose by13.8%, 12.6% and 11.4% respect ively. Global marketsmeanwhile ended mixed following a stronglate rebound onWall Street, as investors welcomed a report suggesting EUleaders may recapitalize the region’s banks and take theopportunity to pick up recently battered stocks.

Almost a year after the strong bull market rally when theASPI achieved new all-time highs, investment in the bourseappears radically different especially over the last fewweeks. Investors and speculators alike appear to havetaken a back seat regardless of fundamental merit.However, we believe that the current consolidation process

provides the ideal opportunity for investors to benefit fullyfrom a prolonged market rise and to adopt a highlyselective approach when re-entering the market. We adviseinvestors to commence their cherry picking now rather thanlater by identifying companies with strong and sustainabletop line revenue growth that will filter down into qualitybottomline growth and outperform the market in themedium to longer term.