Embed Size (px)

Citation preview

Dividend policy, dividend initiations, and governance

Micah S. Officer*

Marshall School of Business Department of Finance and Business Economics

University of Southern California Los Angeles, CA 90089

Phone: 213-740-6519

Email: [email protected]

This draft: October 5, 2006

Abstract: Dividend policy can either be an outcome of strong governance or a substitute for

weak governance. This paper provides evidence that dividend policy is a substitute for weak

internal and external governance by focusing on a sample of firms that should pay dividends.

Specifically, predicted dividend payers with weak governance are significantly more likely to pay

dividends than are predicted dividend payers with strong governance. Firms with weak

governance also have significantly higher dividend initiation announcement abnormal returns

than other firms, consistent with the notion that dividend policy is a substitute for other

governance attributes and that the market prices the decrease in agency costs resulting from the

initiation of dividends.

* I thank Harry DeAngelo, Linda DeAngelo, Ehud Kamar, Harold Mulherin, Mike Stegemoller, Ralph Walkling, and Mark Weinstein for comments, and Jim Linck for providing some of the data.

1

Introduction

While finance academics have long wondered why firms pay dividends when cash distributions

in the form of dividends are tax disadvantaged relative to retention or stock repurchases (e.g.

Black (1976)), recent theoretical and empirical work significantly expands our understanding of

whether, when, and why firms pay dividends (Fama and French (2001), DeAngelo, DeAngelo,

and Skinner (2004), DeAngelo and DeAngelo (2006), and DeAngelo, DeAngelo, and Stulz

(2006)).

The interaction of dividend policy and governance is central to the debate about the

agency costs of free-cash-flow (Easterbrook (1984) and Jensen (1986)). In particular, Easterbrook

(1984) argues that a policy of paying dividends reduces agency costs by improving the

monitoring and risk-taking incentives of managers. While the initiation of a policy of paying

dividends should reduce the agency costs of free-cash-flow ex post, the relation between ex ante

agency problems and the decision to pay dividends is not as clear.

La Porta et al (2000) discuss two models of the relation between ex ante agency problems

and dividend policy: the “outcome model” and the “substitute model.”1 In the outcome model, the

payment of dividends is the result of effective governance – well-governed firms pay dividends

because strong governance makes expropriation from shareholders (the worst manifestation of the

agency problems of free-cash-flow) more difficult and shareholders successfully pressure

managers to distribute excess cash.2 In the substitute model, the payment of dividends replaces

other governance characteristics in the portfolio of policies that firms employ to convince

shareholders that they will not be expropriated.3 The substitute model predicts that poorly-

1 La Porta et al (2000) discuss dividend policy in the context of shareholder protection in various legal regimes around the world. In this paper I take that discussion and apply it to differences in governance characteristics between firms in the same legal regime (United States). 2 Tse (2004) questions the logic of the relation between agency costs and dividend policy in the outcome model – if well-governed firms are more likely to pay dividends, then shareholders shouldn’t need to rely on the payment of dividends to reduce the agency costs of free-cash-flow because such costs should already be low for well-governed firms. 3 Also see Rozeff (1982).

2

governed firms make dividend payments because such firms need an alternate means of

establishing a reputation for acting in the interests of shareholders if they intend to raise capital

from public markets in the future, and therefore a policy of paying dividends is the most valuable

at the margin to firms with agency problems.

I identify a sample of firms with fundamentals that suggest that the firms should be

dividend payers, and test whether governance characteristics affect the decision to pay dividends

in that sample. This sample-selection strategy offers several advantages over the empirical

methods employed elsewhere in the literature. First, the outcome model predicts that well-

governed firms are more likely to pay dividends only when firm fundamentals (size, growth,

earned capital, etc.) support the adoption of a policy of paying dividends. In other words, the

outcome model doesn’t stand a chance against the alternative (the substitute model) unless one

conditions first on the appropriateness of adopting a policy of paying dividends. Second, a sample

of firms that are predicted dividend payers is likely to contain firms that, all else equal, have

higher-than-average agency costs of free cash flow. Therefore, this sample should provide a

strong empirical test of whether characteristics associated with strong governance are positively

(the outcome model) or negatively (the substitute model) correlated with a policy of paying

dividends, because the higher-than-average agency costs of free cash flow give shareholders

ample motivation to insist on payouts if the governance structure allows (the outcome model) and

managers ample motivation to voluntarily offer payouts to compensate for otherwise weak

governance structures (the substitute model).

I identify firms that should pay dividends (predicted dividend payers) using the models in

Fama and French (2001) and DeAngelo, DeAngelo, and Stulz (2006), and find that predicted

dividend payers with characteristics associated with weak governance and managerial

entrenchment are significantly more likely to pay dividends than are predicted dividend payers

with strong governance. For example, firms with large boards, CEO/Chairman duality, and low

ownership by insiders and institutional investors are significantly more likely to pay regular cash

3

dividends to shareholders. These results are consistent with the substitute model in La Porta et al

(2000), which predicts that firms use dividend policy as a substitute for otherwise weak

governance. I offer further support for the substitute model by demonstrating that firms with

weak governance have significantly more positive dividend initiation announcement returns than

do firms with characteristics consistent with strong governance. This suggests that the market

prices the reduction in agency costs associated with the initiation of dividends by firms with weak

governance, consistent with the hypothesis that dividend policy is one component of the firm’s

governance and bonding policies and therefore substitutable with other governance policies.

Endogeneity is certainly a concern in interpreting my results. However, the substitute

model in La Porta et al (2000) suggests that dividend policy and other governance characteristics

are endogenous choices that firms make as part of an equilibrium monitoring/bonding package to

reduce agency costs. While my empirical models are structured as tests of whether governance

proxies (implicitly exogenous in the regressions) affect dividend policy choices, the substitute

model does not suggest that any of these policy choices are truly exogenous. Therefore, the most

that can be concluded from my results (and the other results in this literature), is that dividend

policy choice and other policy choices that affect governance quality are negatively correlated.

Firms that choose governance policies that are associated with entrenchment (such as having

many anti-takeover provision insulating managers from hostile takeovers) are empirically more

likely to pay dividends, but it is impossible to conclude that one of these policy choices causes

the other. As discussed in Rozeff (1982), the data is most consistent with the interpretation that

dividend policy decisions are made as part of an endogenous package of governance choices that

optimally reduce the agency costs generated by the separation of ownership and control.

Recent empirical papers in this literature have offered consistent support for the substitute

model in La Porta et al (2000) (although few papers use that language). For example, Fenn and

Liang (2001) report that firms with low managerial stock-option holdings (and therefore lower-

powered incentives) have significantly higher dividend and total (including repurchases) payout

4

ratios, although this result could be due to the lack of “dividend protection” afforded by most

executive stock option contracts (Lambert, Lanen, and Larker (1989)). Hu and Kumar (2004) find

that the likelihood and level of dividend payouts is increasing when factors such as managerial

and outside blockholder ownership, CEO compensation policy, and board independence indicate

a high likelihood of managerial entrenchment and high agency costs.

John and Knyazeva (2006) report that dividend and total payouts (the sum of dividends

and repurchases) are significantly more likely when internal and external governance measures

indicate weak governance. Pan (2006) shows a similar association between the propensity to pay

dividends and measures of managerial entrenchment based on indices of anti-takeover charter

provisions. Several earlier studies report complementary evidence. Rozeff (1982) reports that

dividend payout ratios are significantly negatively associated with insider ownership and

positively associated with the dispersion of outside ownership. Essentially identical results are

found in a simultaneous-equations framework by Jensen, Solberg, and Zorn (1992). Gugler

(2003) examines Austrian firms and finds that state-controlled firms, for which agency problems

are likely to be severe, have higher target dividend payout ratios than other types of firms, and are

also the most reluctant to cut dividends when such cuts are warranted. On the other hand,

Renneboog and Szilagyi (2006) report that firms with strong shareholders appear to force higher

payouts in Dutch firms, and Michaely and Roberts (2006) conclude that strong governance

encourages higher and more consistent payouts using data on private firms in the UK.

One weakness with the empirical tests in the recent literature (e.g. Hu and Kumar (2004),

John and Knyazeva (2006), and Pan (2006)), however, is that none of these authors focus on

samples of firms that should pay dividends. As described above, this weakness biases tests in

favor of the substitute model. While these studies include firm fundamentals as control variables

in regressions of dividend policy choice on governance characteristics, holding fundamentals

constant in a regression using all available firm-years is very different from focusing on a sample

of firms that should pay dividends. Including firm fundamentals as control variables essentially

5

involves asking the following question: if two firms have the same fundamentals, does

governance affect the decision to pay dividends? But as a large fraction of the full sample of firm-

years used in most studies is comprised of firms that, according to fundamentals (size, growth,

retained earnings, and so on) should not be dividend payers,4 controlling for fundamentals can

result in a test of whether governance matters for dividend policy for two firms that are equally-

unlikely to be dividend payers.

A further omission from this literature is that none of the aforementioned studies examine

the relation between governance characteristics and the wealth effects of initiating a policy of

paying dividends. The substitute model predicts that dividends are used as a substitute for other

governance devices in order to reduce agency costs, and therefore that the announcement that a

firm with weak governance will begin paying dividends for the first time should be associated

with positive returns as the market prices the reduction in agency costs into the firm’s stock price.

In other words, initiating dividends offers the greatest reduction in agency costs, and

consequently the largest initiation announcement stock price reaction, for firms with weak

governance in the substitute model.

The contribution of this paper is to address these two weaknesses and omissions. First, by

examining firms that should be paying dividends (based on fundamentals) and exploring the

relation between whether those firms do pay or not and proxies for internal (board size and

composition) and external (takeover defenses, ownership by blockholders and activist investors)

governance characteristics, my research design provides a more robust test of the substitute model

by, if anything, biasing the test in favor of the outcome hypothesis. Second, I provide

complementary evidence by examining the relation between governance characteristics and

dividend initiation announcement returns – if a policy of paying dividends is chosen as a

substitute for other governance characteristics, then the reduction in agency costs should be

4 For example, less than one-third of the firms in the sample in DeAngelo, DeAngelo, and Stulz (2006) are dividend payers, and the empirical models in that paper have considerable success in predicting the propensity to pay.

6

priced by the market at the margin. My results strongly support the substitute model and are

consistent with the hypothesis that a policy of paying dividends is used as a substitute for other

governance devices by firms with weak governance and high agency costs, and that the market

prices an anticipated reduction in agency costs around dividend initiation announcement dates.

The results in this paper are related to other findings in the literature. Harford, Mansi, and

Maxwell (2005) report that firms with weak governance hold substantially lower cash reserves

than do firms with strong governance. This is consistent with the notion that firms with weak

governance are more likely to pay dividends (thereby reducing cash balances).5 Gillan, Hartzell,

and Starks (2006) find evidence that governance structures are substitutes for one another – for

example, firms with more independent boards also tend to have more restrictive anti-takeover

provisions. Such substitutability between governance structures is consistent with the argument

that dividend policy and other governance attributes also serve as substitutes.

The remainder of this paper is organized as follows. In Section I, I develop the

hypotheses and empirical predictions. Section II describes the relation between the propensity to

pay dividends for firms that should be dividend payers and governance characteristics. Section III

examines the relation between governance measures and abnormal returns around dividend

initiation announcements, and Section IV discusses the implications of the findings and offers

concluding remarks.

I. Hypothesis development

A. Two models for the relation between agency costs and dividend policy

As outlined in La Porta et al (2000), there are two potential models for the relation

between agency costs and dividend policy. Although each is discussed in detail in La Porta et al,

the discussion in that paper centers on a cross-country (and legal system) framework. Therefore, I

5 Harford, Mansi, and Maxwell (2005) conclude, however, that firms with weak governance dissipate cash through acquisition activity rather than by returning it to shareholders.

7

adapt each of the La Porta et al models to a setting where firms are in a common legal system

(United States) but have attributes that offer shareholders a strong voice in the governance of the

corporation (“strong governance”) or a weak voice (“weak governance”):

A.1.The outcome model

Firms with strong governance are those with, for example, small boards that are more

difficult for insiders to manipulate (Jensen (1993) and Yermack (1996)), boards that are

dominated by non-executives or outsiders (Weisbach (1988) and Brickley, Coles, and Terry

(1994)), blocks of stock controlled by activist outsiders (Barclay and Holderness (1991) and Del

Guercio and Hawkins (1999)), and few anti-takeover provisions (Gompers, Iishi, and Metrick

(2003) and Bebchuk, Cohen, and Ferrell (2005)). Managers of companies with strong governance

systems will find it more costly to expropriate wealth from outside shareholders, raising the

relative attractiveness of paying out cash to stockholders. In such firms, shareholder insistence on

the distribution of excess cash is less likely to fall on deaf ears than in firms with attributes

associated with managerial entrenchment or weak governance. The “correct” dividend policy is

the outcome of the governance regime in this view because managers of firms with good

governance are more likely to act in the interests of shareholders and pursue value-maximizing

policies, such as the payment of dividends when the firm’s fundamentals warrant such a policy,

than are managers of firms with weak governance. In this model, strong governance and a policy

of paying dividends are complements.

A.2.The substitute model 6

This view of the relation between agency costs and dividend policy relies on the

assumption that firms and managers need to establish a reputation with public capital markets for

6 This model is derived from the discussion in La Porta et al (2000), but is also consistent with the predictions of the agency model in Allen, Bernado, and Welch (2000) (specifically, prediction #1 on p.2519 of that paper), the discussion in Myers (2000), and the agency model in Nielsen (2005).

8

not expropriating wealth from shareholders (whether actual cash transfers or over-consumption of

perquisites) because the firm will need to tap such markets to raise new external capital in the

future (Easterbrook (1984)) or because the managers’ reputation is important for their careers.

Dividend policy is one part of the optimal portfolio of choices that firms make as bonding

commitments to shareholders to reduce agency costs (Rozeff (1982)). A policy of paying

dividends reduces the agency costs of free-cash-flow, and such a policy choice is therefore most

valuable at the margin to firms with the highest agency costs. Managers of firms with weak

governance, such as those with large boards, few outside blockholders, low levels of ownership

by managers (Jensen and Meckling (1976)), and charter provisions making control-changes

costly, are most likely to prefer a policy of paying dividends, even if firm fundamentals do not

warrant such a policy, because dividend policy is a substitute for other forms of governance in the

maintenance of a good reputation with external capital markets.

B. Hypotheses

The outcome and substitute models have opposite predictions about the relation between

governance and dividend policy. Assuming for the moment that “governance” can be measured

empirically,7 the testable hypotheses are:

H1a (outcome): Firms with strong (weak) governance are more (less) likely to

pay dividends when firm fundamentals suggest that such a policy is warranted.

H1b (substitute): Firms with weak (strong) governance are more (less) likely to

pay dividends when firm fundamentals suggest that such a policy is warranted.

7 I will return to this issue in Section II, and use a variety of governance proxies that are commonly employed in the empirical governance literature.

9

The outcome and substitute models also offer differing predictions about the relation

between dividend initiation announcement returns and governance characteristics. In the outcome

model, firms with strong governance are predicted to be the most likely to initiate a policy of

paying dividends, and yet the value of that policy (reducing the agency costs of free cash flow,

for example) for such firms is lower than for firms with weak governance.8 On the other hand, the

substitute model predicts that dividends are used as a substitute for other governance devices in

order to reduce agency costs, and therefore that the market will price the anticipated reduction in

agency costs into the firm’s stock price upon the announcement that a firm with weak governance

will begin paying dividends for the first time (initiations). In other words, initiating dividends

offers the greatest reduction in agency costs for firms with weak governance in the substitute

model, and if the reduction in agency costs is reflected in returns around dividend initiation dates

then firms with weak governance will have significantly more positive initiation announcement

returns than will firms with strong governance. This suggests the following testable hypotheses:

H2a (outcome): There will be no significant difference in abnormal

announcement returns around dividend initiation announcements conditional on

governance characteristics.

H2b (substitute): Firms with weak governance will have significantly more

positive dividend initiation announcement returns than will firms with strong

governance.

8 See also Tse (2004).

10

II. Dividend payers and governance characteristics

A. Identifying firms that should be dividend payers

The first set of hypotheses (H1a and H1b) predicts differences in the proportion of

dividend payers amongst those firms that should pay cash out to stockholders. I identify those

firms that should be dividend payers using firm fundamentals that are associated with the

propensity to pay. Specifically, I rely on the empirical models employed in Fama and French

(2001) and DeAngelo, DeAngelo, and Stulz (2006) to identify firm-years in which the firm

should be a dividend payer, and then examine the propensity for those firms to pay dividends

conditional on various governance characteristics.

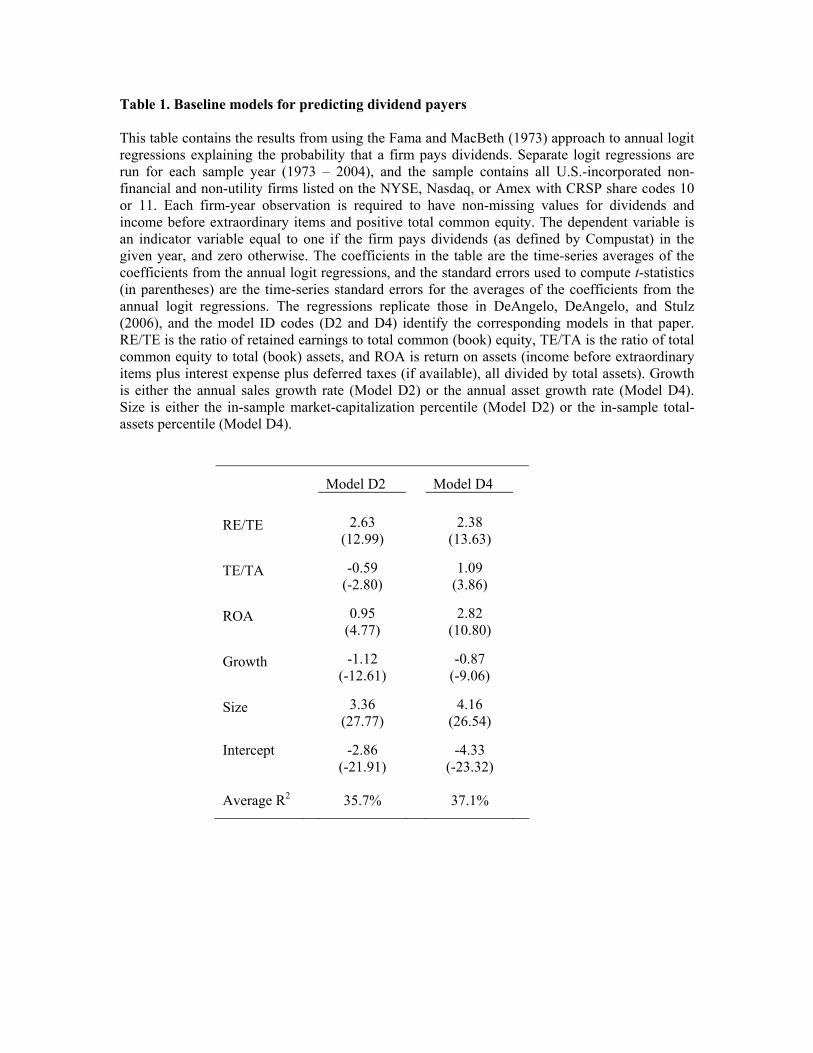

Table 1 replicates regressions D2 and D4 from Table 3 in DeAngelo, DeAngelo, and

Stulz (2006), which are extensions of the payer-prediction regressions in Table 5 of Fama and

French (2001). The logit regressions use the Fama and MacBeth (1973) method to explain the

probability that a firm pays dividends with fundamental characteristics such as size, growth,

profitability, and the ratio of retained earnings to total equity (the earned/contributed capital mix).

The latter explanatory variable is used solely in DeAngelo, DeAngelo, and Stulz (2006) (as a

proxy for the firm’s stage in its capital infusion/self-financing lifecycle), while the other variables

are common to both papers cited above.

The sample used for the logit regressions in Table 1 is the same as that described in

DeAngelo, DeAngelo, and Stulz (2006). Specifically, the sample contains all firm-year

observations for all US-incorporated industrial (non-financial and non-utility) firms that are both

in the Compustat database and in the Center for Research in Security Prices (CRSP) database

with publicly-traded equity (NYSE, Nasdaq, or Amex) with share code 10 or 11. The sample is

from 1973 – 2004, with the beginning of the sample period dictated by the fact that CRSP

expands its coverage to include Nasdaq firms in 1972. Each firm-year observation is required to

have non-missing values for dividends and income before extraordinary items and positive total

common equity.

11

The explanatory variables in Table 1 are identical to those described in DeAngelo,

DeAngelo, and Stulz (2006) with one exception: the size percentile measures are based on the full

sample rather than NYSE break-points. Other than that, I employ identical measures of

earned/contributed capital (RE/TE), common equity/total capital (TE/TA), profitability (ROA),

and sales or asset growth (Growth) as described in DeAngelo, DeAngelo, and Stulz (2006). The

regressions are estimated separately for each sample year, and the coefficients in Table 1 are the

average of the 32 annual coefficients. The standard errors used to assess statistical significance

are the standard deviations of the annual coefficients scaled by the square root of 32.

While my sample period is slightly longer than theirs, the logit regression results reported

in Table 1 are practically identical to those in DeAngelo, DeAngelo, and Stulz (2006). The

propensity to pay dividends is significantly positively related to the earned/contributed capital

mix, profitability, and size (whether measured using equity market capitalization (D2) or total

assets (D4)), and negatively related to growth (whether measured as the growth rate of assets

(D4) or sales (D2)). The R2s reported in Table 1 are the average R2 for each model, and are 36%

for model D2 and 37% for D4. While the regressions are so similar that any choice between them

is arbitrary, as I use the regression for predictive purposes I rely on model D4 as it has a slightly

higher R2.

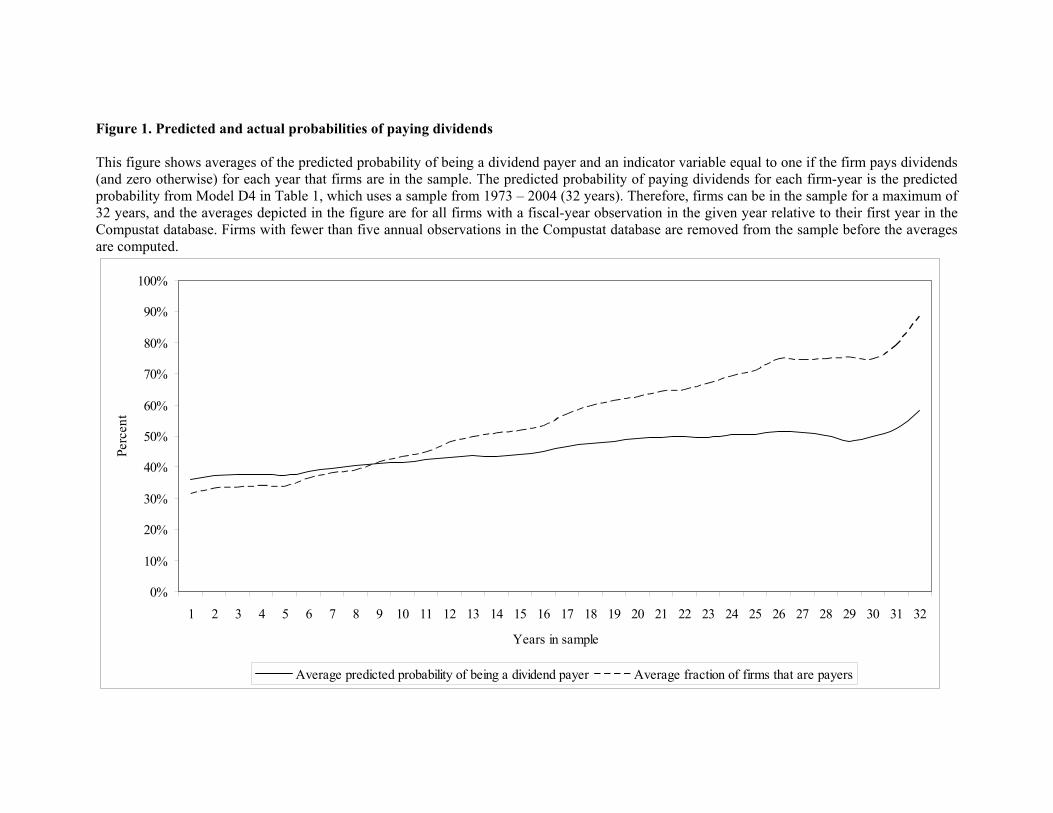

Figure 1 shows the dividend-payer lifecycle predictions derived from model D4 in Table

1. The figure plots the average predicted probability of paying dividends (solid line) and the

fraction of firms paying dividends (dashed line) for each year in the sample life of firms that have

at least five years of data in the sample.9 The “years in sample” in the figure is essentially an

event year, with year 1 being the first year that each firm appears in the sample. The average

predicted probability of paying dividends increases monotonically over the average firm’s

lifecycle, rising from a 36% probability of being a dividend payer in the first year that a firm

9 While “sample life” is not the same as “firm age,” the number of years in the sample (which is taken directly from the Compustat database) should be very close to the number of years as a public company for most firms that live at least five years and do not have a substantial number of missing observations.

12

appears in the sample to a 50% probability in the 22nd year. The actual fraction of payers in the

sample rises at a faster rate, but again reflects the lifecycle behavior described in Fama and

French (2001), Grullon, Michaely, and Swaminathan (2002), and DeAngelo and DeAngelo

(2006) – only 31% of firms are dividend payers in their first sample year, and that fraction passes

50% in the 13th year of sample life. As Figure 1 demonstrates, the propensity to pay dividends is

reasonably well captured by models, such as those in Table 1, that take account of the fact that as

a firm gets older its size, earned capital, and profitability increase (and sales or asset growth rate

decreases) to the point where the payment of dividends appears to be an optimal policy.

I use the predicted probabilities from model D4 in Table 1 to identify a sample of firm-

years in which firms should be paying dividends. Specifically, dividends should be paid in every

firm-year in which the predicted probability of being a dividend payer has exceeded 50% for two

consecutive years. Several examples will help highlight the sample derived from this selection

procedure. Microsoft Corp enters the sample in 1987 (the year after Microsoft’s IPO, allowing

one year for the calculation of Microsoft’s asset growth rate), at which time model D4 predicts

that its probability of being a dividend payer is 79%. The predicted probability of Microsoft being

a payer stays above the 50% threshold for all years until 2000, at which point it drops to 49% and

stays below 50% for three consecutive years until 2003 (and stays above that threshold until the

end of the sample). Therefore, Microsoft is considered to be a firm that should be paying

dividends from 1988 to 1999 and again in 2004. Microsoft initiates dividend payments in 2003.

Harley Davidson Inc. enters the sample in 1987 (again, the year after its IPO), at which time its

predicted probability of being a dividend payer is 46%. Harley Davidson’s predicted probability

of making dividend payments rises to 56% in the next year (1988), and stay above 50% for the

following 17 years (never dropping below 65%). Therefore, Harley Davidson should pay

dividends under the above definition from 1989 through 2004. Harley Davidson initiates dividend

payments in 1993 and does not omit a dividend for the remainder of the sample years. While the

lifecycle for every firm in the sample obviously does not follow this clean pattern, the results

13

depicted in Figure 1 illustrate that model D4 does a reasonable job of capturing the average

lifecycle pattern of dividend policy.

B. Governance characteristics

“Governance” is an extremely difficult concept to capture empirically. However, the

literature on governance has blossomed recently, potentially because governance appears to be

much more important to investors following the meltdowns of Enron, WorldCom, Adelphia, and

so on, but also potentially because several data sources (such as the IRRC data used by Gompers,

Iishi, and Metrick (2003)) have recently become available to researchers. In this paper I take as

broad and conservative approach as I can, sampling from much of the recent governance

literature and choosing variables that capture different aspects of “governance.” Whilst none of

these measures is individually perfect, if the majority of evidence points in one direction or the

other then reasonable conclusions can be drawn about the relation between dividend policy and

governance.

I divide the governance characteristics into “internal” and “external” measures. Both

internal and external measures of governance capture characteristics that could be expected to

entrench managers and isolate them from shareholder discipline (“weak” governance) or make

managers more responsive to their shareholders (“strong” governance). In other words, these

measures are empirical proxies for the degree of the agency problem at publicly traded

corporations.

The measures of internal governance are essentially measures of board structure and

ownership by insiders (CEO and executive directors), and are largely taken from the sample in

Linck, Netter, and Yang (2006).10 Linck, Netter, and Yang use a screened sample of all firms in

the Compact Disclosure database from 1990 to 2004, and the details of the data selection screens

used to generate the sample can be found in that paper. The final sample from Linck, Netter, and 10 I thank Jim Linck for allowing me to use these data.

14

Yang (2006) includes over 53,000 firm-year observations representing almost 7,000 firms. One

measure of internal governance is not taken from Linck, Netter, and Yang (2006), and that is a

measure of board “strength.” As in Harford and Li (2006), I follow Hermalin and Weisbach

(1998) and use CEO tenure as a proxy for the strength or independence of the board. Hermalin

and Weisbach (1998) argue that the board becomes less independent vis-à-vis the CEO as the

CEO’s tenure increases. The measures of board structure and insider ownership used in this paper

are:

Board size: The number of board members (minimum of 3);

Strong board: An indicator variable equal to one if the CEO’s tenure (in days) is below the

median tenure for CEOs of all firms in the Execucomp database in the given year, and zero

otherwise;

CEO is Chairman: An indicator variable equal to one if the CEO is also the Chairman of the

Board, and zero otherwise;

Board is insider dominated: an indicator variable equal to one if the percent of executive

directors on board is greater than 50%, and zero otherwise;

% ownership by of executive directors (officers): The fraction of the firm’s shares owned by

executive directors (officers);

% ownership by CEO: The fraction of the firm’s shares owned by the CEO.

The continuous variables (Board size, % ownership by of executive directors (officers), and %

ownership by CEO) are expressed in terms of deviations from the median for the given year for

all firms in the Linck, Netter, and Yang (2006) sample. Firms are considered to have “weak”

internal governance (and therefore high agency costs) in any given year if board size is greater

15

than the median (Jensen (1993) and Yermack (1996)), the board is not strong (Hermalin and

Weisbach (1998)), the CEO is also Chairman of the Board (Jensen (1993) and Brickley, Coles,

and Jarrell (1997)), the board is insider dominated (Weisbach (1988) and Brickley, Coles, and

Terry (1994)), or executive directors or the CEO have low ownership stakes in the firm (Jensen

and Meckling (1976)).11

The measures of external governance are based on external ownership and corporate-

charter-provisions data. I consider two measures of external ownership: ownership by

institutional investors and by public pension funds. Large institutional investors (including public

pension funds) potentially act as external monitors forcing firms in their portfolios to improve

decision-making and control, and the incentive to monitor is increasing in the stake held in the

firm by these investors.12 To some extent these two categories overlap, as public pension funds

are institutional investors (but not vice versa). However, public pension funds are considered to

be some of the most activist institutional monitors (see, for example, Brickley, Lease, and Smith

(1988), Smith (1996), Wahal (1996), and Del Guercio and Hawkins (1999)), and so considering

these two categories separately may provide insight into whether the type of institutional investor

influences monitoring and, in turn, dividend policy. The percent ownership by institutional

investors is taken from the sample in Linck, Netter, and Yang (2006), from which data is

available at the annual frequency. The percent ownership by public pension funds is derived from

CDA/Spectrum (13F) data, and is the percent of the firm’s shares owned by the public pension

11 Fama and Jensen (1983) and Morck, Shleifer, and Vishny (1988) recognize that the agency costs of external equity may not be monotonically decreasing in the fraction of the firm that is owned by managers. For example, while low levels of ownership insulate executives from the economic consequences of their decisions (the classic agency problem), high levels of managerial ownership may insulate managers from discipline by the market for corporate control. I take the simple approach of assuming that managers’ interests are aligned with the interests of their shareholders to a greater extent (i.e. lower agency costs) as ownership by the CEO and executive directors increases, but the results of spline regressions accounting for the effects of different levels of managerial ownership on the propensity to pay dividends are discussed in footnote 15. 12 Brickley, Lease, and Smith (1988) show that institutional investors, especially public pension funds, are more likely to vote against management-sponsored charter-amendment proposals than other types of investors are. Chen, Harford, and Li (2005) argue that institutional blockholders have better monitoring incentives than other investors and present evidence that institutional blockholders respond to those incentives by forcing managers to abandon value-destroying acquisitions.

16

funds collectively identified in three recent studies of the impact of public pension fund holdings

on stock returns (Cremers and Nair (2005), Dittmar and Mahrt-Smith (2006), and Larker,

Richardson, and Tuna (2005)) at the quarterly reporting date closest to the end of the fiscal year.

I use data from the Investor Responsibility Research Center (IRRC) database of corporate

charter provisions to measure the strength of a firm’s anti-takeover provisions. Anti-takeover

provisions help shield managers from discipline from the market for corporate control,

entrenching managers and potentially weakening governance by reducing managers’ incentives to

act in the best interests of shareholders. Bebchuk, Cohen, and Ferrell (2005) consider an index

which equals the sum of six indicator variables that capture whether a firm has a staggered board,

limits to amend the bylaws or charter, supermajority-voting provisions, golden parachutes, or a

poison pill. Bebchuk, Cohen, and Ferrell define the sum of these six indicator variables as the

entrenchment index, which takes values from 0 to 6 and is increasing in the number of anti-

takeover charter provisions that a firm has. The IRRC data is available for a cross-section of firms

in the years 1990, 1993, 1995, 1998, 2000, 2002 and 2004, and the IRRC data contains date

ranges for which each observation is valid for each firm. Firm-years are matched to IRRC data by

selecting the observation for which the end of the fiscal year falls within the relevant date range.

This procedure does generate serial correlation in governance measures for individual firms (as a

1990 observation from the IRRC data, for example, could be matched to the 1990, 1991, and

1992 fiscal years), but as the empirical tests use the Fama and Macbeth (1973) approach this

serial correlation should have little effect on my results. Firms are defined as having managerial

entrenchment if the Bebchuk, Cohen, and Ferrell (2005) (BCF) entrenchment index is greater

than the (pooled time-series and cross-sectional) median of two. The measures of external

governance are therefore:

% ownership by institutions: The fraction of the firm’s shares owned by institutional investors;

17

% ownership by public pension funds: The fraction of the firm’s shares owned by public

pension funds;

Managerial entrenchment (BCF definition): An indicator variable equal to one if the BCF

entrenchment index is greater than two (the pooled time-series and cross-sectional median),

and zero otherwise.

The continuous variables (% ownership by institutions and % ownership by public pension funds)

are expressed in terms of deviations from the cross-sectional median. The median of % ownership

by institutions is computed each year using the firms in the Linck, Netter, and Yang (2006)

sample. The median of % ownership by public pension funds is computed for each quarterly

reporting date for all firms in the CDA/Spectrum (13F) database. Firms are considered to have

“weak” external governance in any given year if institutions or public pension funds hold low

stakes in the firm or if managers are entrenched using the BCF definition.

C. Sample and empirical results

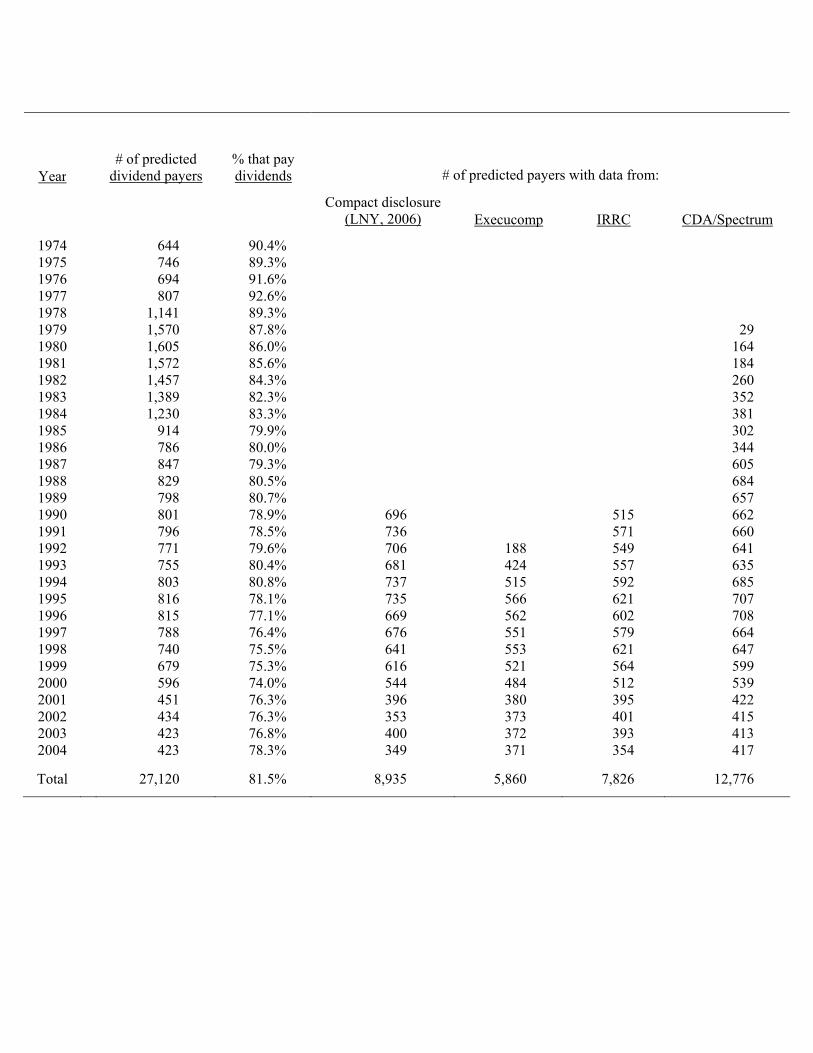

The sample of predicted dividend payers and matches to the various governance data

sources described above is depicted in Table 2. The first column contains the number of predicted

dividend payers each year from 1974 to 2004.13 The sample is well distributed over time, with

only minor clustering in the late 1970’s and early 1980’s. The second column contains the

percentage of the predicted payers that actually do pay dividends in each year. This percentage

averages 81.5% over the whole sample, but is markedly higher in the early years of the sample

than in the later years. It is possible that this reflects a declining propensity to pay dividends

(Fama and French (2001)), but could also be driven by the predictive content of the model

13 The sample in Table 2 starts in 1974 because the regression in Table 1 uses observations from 1973 onwards and it takes two consecutive years of greater than 50% predicted probability of being a dividend payer to enter the sample in Table 2. This implies that the first year that I should observe a predicted dividend payer will be 1974.

18

declining over time. On average in the full sample, however, 4 out of 5 firms that are predicted

payers do actually pay dividends – the main research question in this paper is whether governance

characteristics affect the propensity for firms to adopt the predicted financial policy.

The remaining four columns in Table 2 show how many firms in each year are matched

to the various governance data sources described above. Again, the distribution over time of each

series is relatively stable after the point that the first match occurs. Most of the governance

measures are available for a substantial fraction of predicted payers from 1990 onwards, although

the data from CDA/Spectrum on public pension fund ownership starts considerably earlier (1979)

than measures from the other data sources.

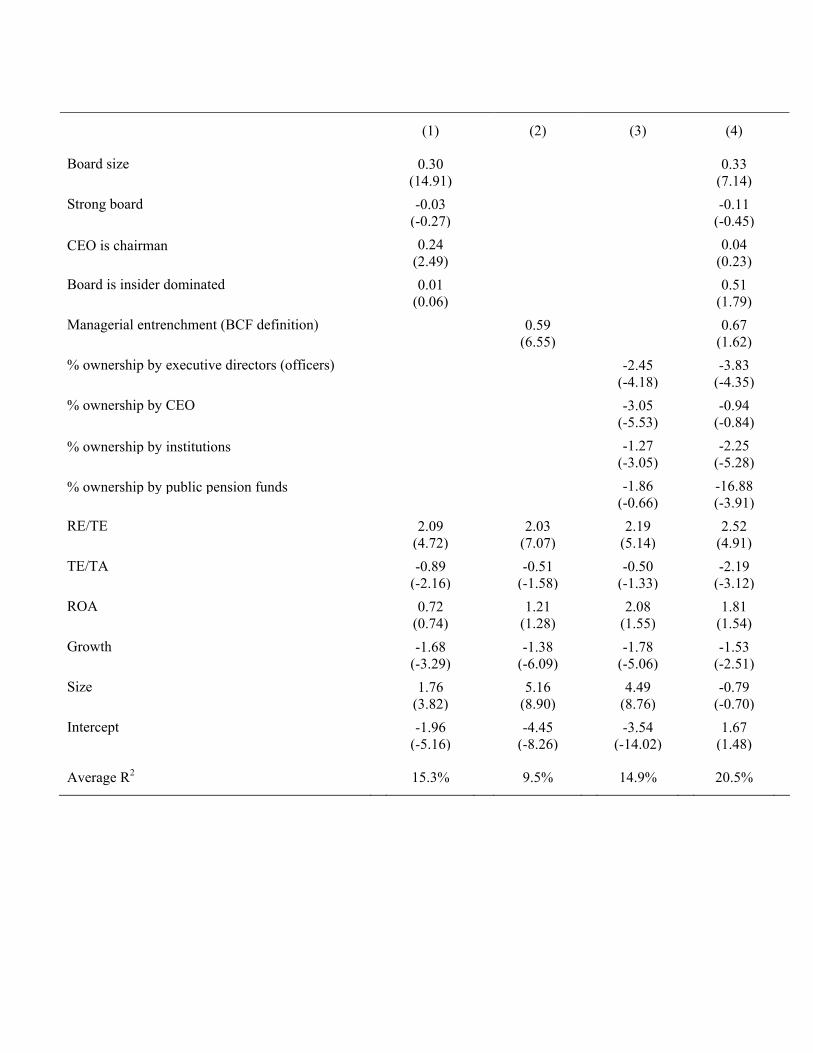

Table 3 contains the principal empirical results in this section, and demonstrates the

empirical relation between the propensity to pay dividends for predicted dividend payers and

governance characteristics. The regressions are similar to those in Table 1, with Fama and

Macbeth (1973) methods used to analyze annual logit regressions with an indicator variable equal

to one if dividends are paid (and zero otherwise) as the dependent variable. The difference

between the regressions in Table 1 and those in Table 3 is that in Table 3 the sample is

constrained to predicted dividend payers only and the governance variables described above are

included as explanatory variables. I include the same explanatory variables as used in Table 1

(RE/TE, TE/TA, ROA, and so on) as control variables because even though all firm-years in the

sample for Table 3 have high (>50%) predicted probability of paying dividends, cross-sectional

dispersion in firms’ fundamentals may still affect the decision to adopt the predicted dividend

policy.

The first three columns introduce the governance variables into the regression in groups:

board characteristics in column 1, the anti-takeover-provision-based entrenchment index in

column 2, and the ownership variables in column 3. The regressions use all available observations

with non-missing data over the longest time span possible. For example, the regressions in

column 1 use a total of 5,141 observations for 13 annual logit regressions (1992 – 2004), with an

19

average of 395 firm-specific observations per year. The number of observations used and the time

span over which the logits are estimated are similar for the other columns in Table 3, but the loss

in sample size (to 3,113 total observations with an annual average of 259) is the most serve in the

final column where all governance attributes are included at the same time

The regression in column 1 shows that board size and CEO/Chairman duality

significantly14 influence dividend policy in the direction predicted by the substitute model (H1b):

firms with larger boards and firms with one individual sharing the title of CEO and Chairman are

significantly more likely to pay dividends to shareholders. Jensen (1993) and Yermack (1996)

suggest that large boards are easier for the CEO to manipulate, and even more so if the CEO is

also Chairman, consistent with the notion that these characteristics are associated with weaker

monitoring of insiders and higher agency costs. Consistent with the substitute model, predicted

dividend payers with weaker governance or greater agency problems are more likely to actually

pay dividends than are predicted payers with strong governance. The same is true in column 2, in

which the entrenchment index from Bebchuk, Cohen, and Ferrell (2005) is the only governance

variable. The coefficient on the entrenchment index is strongly statistically different from zero

and positive (as in Pan (2006)), suggesting that predicted payers with entrenched managers are

more likely to pay dividends.

The coefficients on the ownership variables in column 3 also support the substitute model

(H1b) and offer little support for the outcome model (H1a). Firms in this sample with low

ownership (relative to the median) by officers of the firm, the CEO, and institutional investors are

significantly more likely to adopt a policy of paying dividends. Executive ownership levels

greatly affect the extent to which executives share with stockholders the economic costs and

benefits of their actions, thereby influencing the extent of the agency problem (Jensen and

Meckling (1976)), and institutional investors potentially provide important external monitoring of

14 The 5% (1%) two-sided cutoff value from the t-distribution with 12 degrees of freedom (there are 13 coefficients averaged to produce each coefficient in Table 3) is approximately 2.18 (3.06).

20

executives and the board. Therefore, the ownership evidence is again consistent with the notion

that firms with weak governance are more likely to pay dividends as a commitment device.15

The regression in column 4 includes all the governance proxies at the same time. The

sign and significance of the coefficients on board size and ownership by executive directors and

institutions do not change. However, the statistical significance of the coefficients on the

CEO/Chairman duality, managerial entrenchment, and CEO ownership variables is reduced to the

point where those coefficients are not reliably different from zero at conventional levels.

However, the coefficient on the indicator variable for an insider dominated board is positive

(consistent with H1b) and statistically significant at the 10% level in this specification, and the

effect of public pension fund ownership levels on the propensity to pay dividends is statistically

significantly different from zero at the 1% level. The latter result suggests that predicted payers

with low ownership levels by the most activist institutional investors are more likely to make

dividend payments to stockholders.16

Taken together, these results are the most consistent with the substitute model described

above (H1b). There is no evidence that strong governance makes dividends more likely to be paid

when firm fundamentals support such a policy, as predicted by the outcome model in La Porta et

al (2000). Instead, firms with weak governance appear more likely to pay dividends when they

should: predicted payers are more likely to make dividend payments if board size is large, the

15 The negative coefficients on CEO and executive director ownership variables are driven by CEO and executive director ownership below a 25% threshold. Specifically, the results of unreported spline regressions suggest that the propensity for firms in this sample to pay dividends is decreasing as CEO ownership increases between zero and five percent and as executive director ownership increases between five and 25 percent. These results are consistent with the assumption that increased ownership by insiders improves governance only when such ownership begins at a relatively low (less than 25%) base. Interestingly, the coefficient on CEO ownership in unreported spline regressions is positive (but statistically insignificant, t = 1.01) for CEO ownership levels in excess of 25%, consistent with the notion that increases in CEO ownership starting from a high base (over 25%) makes governance weaker because managers are already entrenched at high ownership levels. 16 The control variables in Table 3 are relatively stable in terms of sign and significance across all specifications. The earned/contributed capital mix (RE/TE), return on assets, growth, and size have similar effects on dividend paying behavior as seen in Table 1 and described in DeAngelo, DeAngelo, and Stulz (2006).

21

CEO is also Chairman of the Board, anti-takeover provisions protect managers from external

discipline, and when ownership levels by executives and important external monitors are low.

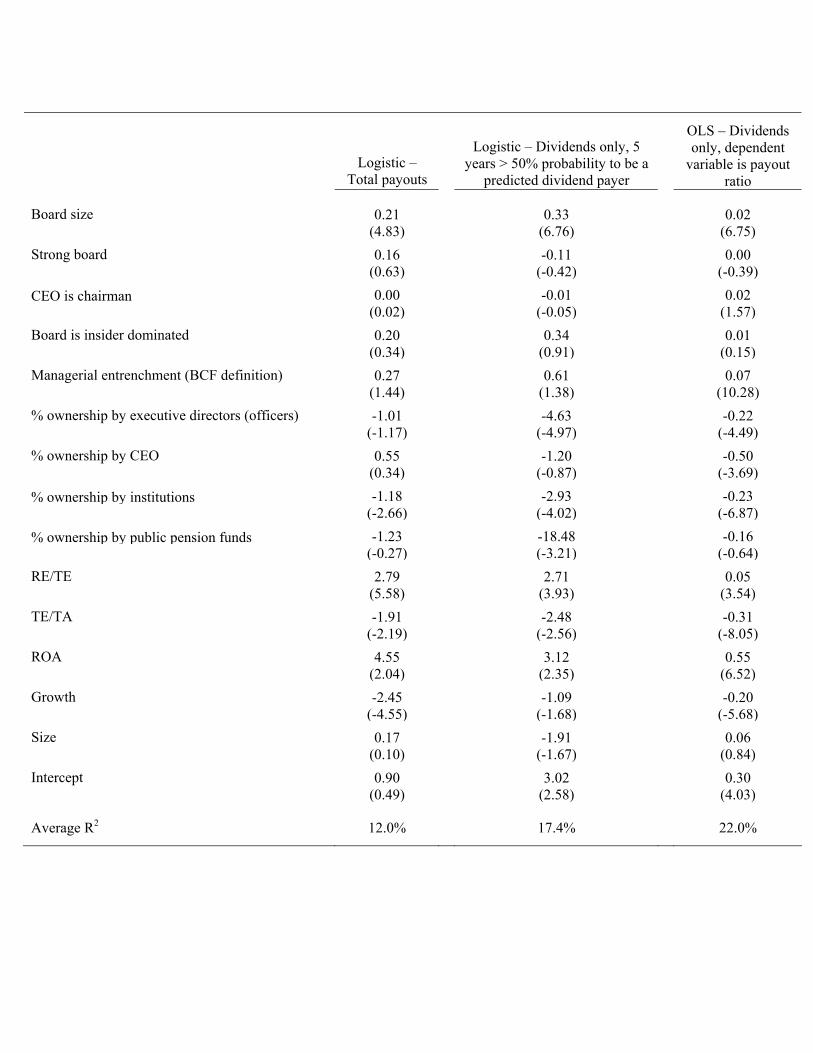

D. Robustness tests

There are several alternative specifications that can be used to test the robustness of the

conclusions derived from Table 3. One concern about the results presented in Table 3 is that the

effect of governance characteristics on payout policy may be different than the effect on dividend

policy. In other words, firms with strong governance may be less likely to pay dividends when

fundamentals suggests they should, but that may be because managers at such firms act in the

interests of their shareholders and distribute cash in the form of repurchases (which are tax-

advantaged) instead of tax-disadvantaged dividends.

To that end, the first column of Table 4 replicates the regression in the final column of

Table 3 except that the dependent variable is an indicator variable equal to one if the firm makes a

payout in the form of dividends or repurchases (and zero otherwise). Stock repurchases are

identified as described in Fama and French (2001). Considering total payouts instead of just

dividends does weaken the relation between governance characteristics and payout policy, as

three of the coefficients that are statistically significantly related to dividend payments in Table 3

(Board is insider dominated, ownership by executive directors, and ownership by public pension

funds) are not significantly related to total payouts in the first column of Table 4. However, the

coefficients on board size and ownership by institutional investors have signs and significance

levels consistent with Table 3 and the predictions of the substitute model. The fact that including

repurchases in total payout policy weakens the relation between payout policy and governance

measures is consistent with the findings in Knyazeva and John (2006).

A further concern with the results in Table 3 is that the definition of “predicted payer”

may not accurately identify those firms that should be paying dividends. The second column of

Table 4 replicates the last column in Table 3 for a sample of firm-years for which a firm is only

22

considered to be a predicted payer after five consecutive years with the probability of being a

payer (from Table 1) above 50%. While this reduces the sample size (the set of firms with five

consecutive years of probability above 50% is a subset of the set of firms with two consecutive

years of probability above 50%), the results in the second column of Table 4 are qualitatively

similar to those in the last column of Table 3. The only significance level affected by the more

stringent definition of predicted payers is for the coefficient on the insider-dominated board

indicator variable, which is marginally significant in Table 3 but insignificant in the second

column of Table 4.

It is also true that dividend policy is not a binary decision – firms can choose to pay out

more or less of (free) cash flow or holdings once the decision to pay dividends has been made.

The last column in Table 4 analyzes the effect of governance characteristics on a continuous

measure of dividend policy – the dividend payout ratio. The dividend payout ratio is defined here

as the total amount of dividends paid in the fiscal year divided by the firm’s pre-dividend cash

balance (sum of the firm’s cash balance at the end of the fiscal year plus the total amount of

dividends paid in the fiscal year). This continuous variable ranges from zero to 1.27, and

measures both whether dividends are paid and how much of the firm’s pre-dividend cash balance

is paid out to stockholders in the form of dividends. As can be seen in the final column of Table

4, the relation between governance measures and a continuous measure of dividend policy are

practically identical to those in the fourth column of Table 3, with the only substantial difference

being the loss of significance of the coefficient on public pension fund ownership and the

dramatic increase in the statistical significance of the coefficient on the managerial entrenchment

index.

Overall, the results in Tables 3 and 4 are strongly supportive of the substitute model for

the relation between governance and dividend policy (H1b). It appears that firms with

characteristics associated with weak governance (large boards, more anti-takeover charter

amendments, and low ownership by both insiders (CEO and executive directors) and institutional

23

investors) are both more likely to pay dividends and pay out more of their pre-dividend cash

balances when they do pay dividends. This evidence suggests that dividend payments substitute

for other forms of governance by removing free cash flow from managers’ control, and offers

little support for the outcome model in La Porta et al (2000).

III. Dividend initiation announcement returns and governance characteristics

A long-established stylized-fact in the corporate finance literature is that dividend

initiations are associated with positive stock returns on average (for example, Asquith and

Mullins (1983), although similar findings persist in studies using larger and different sample

periods). These positive announcement returns are typically interpreted as implying that dividend

initiation announcements communicate valuable and positive information to investors, although

the evidence that such information relates to future increases in profitability is relatively weak

(Watts, 1973; DeAngelo, DeAngelo, and Skinner, 1996).

A possibility raised by the evidence in Section II, and until now relatively unexplored in

the literature despite hints at its importance (for example, Easterbrook (1984) and Lang and

Litzenberger (1989)), is that positive stock-price reactions to dividend initiation announcements

can be explained by variation in the governance policies of initiating firms. In other words, if

firms use dividend payments as a substitute for alternative governance characteristics to diminish

the agency problem between managers and shareholders, then the announcement that a firm is

initiating dividends should be associated with a positive stock price reaction as the market adjusts

its estimate of firm value to account for the lower agency costs. Furthermore, as the reduction in

agency costs is the greatest for firms with the weakest pre-initiation governance, returns around

initiations should be significantly more positive for firms with weak governance than for firms

with strong governance (H2b).

24

A. Dividend initiations and initiation announcement returns

I form a sample of dividend initiations from the CRSP database. Specifically, dividend

initiation announcements are defined as the first announcement by a firm listed in CRSP of an

ordinary, taxable, cash dividend payable at the quarterly, semi-annual, or annual frequency to

holders of ordinary common stock (share codes 10 and 11) listed on the NYSE, Nasdaq, or

Amex. Each firm is in the sample only once (subsequent dividend initiations following an

omission are ignored), and financial (SIC codes 6000 to 6999) and utility (SIC codes 4900 to

4949) firms are discarded. All firms in the sample of dividend initiators must have a stock price

on CRSP 365 calendar days prior to the initiation announcement and be covered by the

Compustat database (with no dividends recorded by Compustat in the prior five fiscal years).

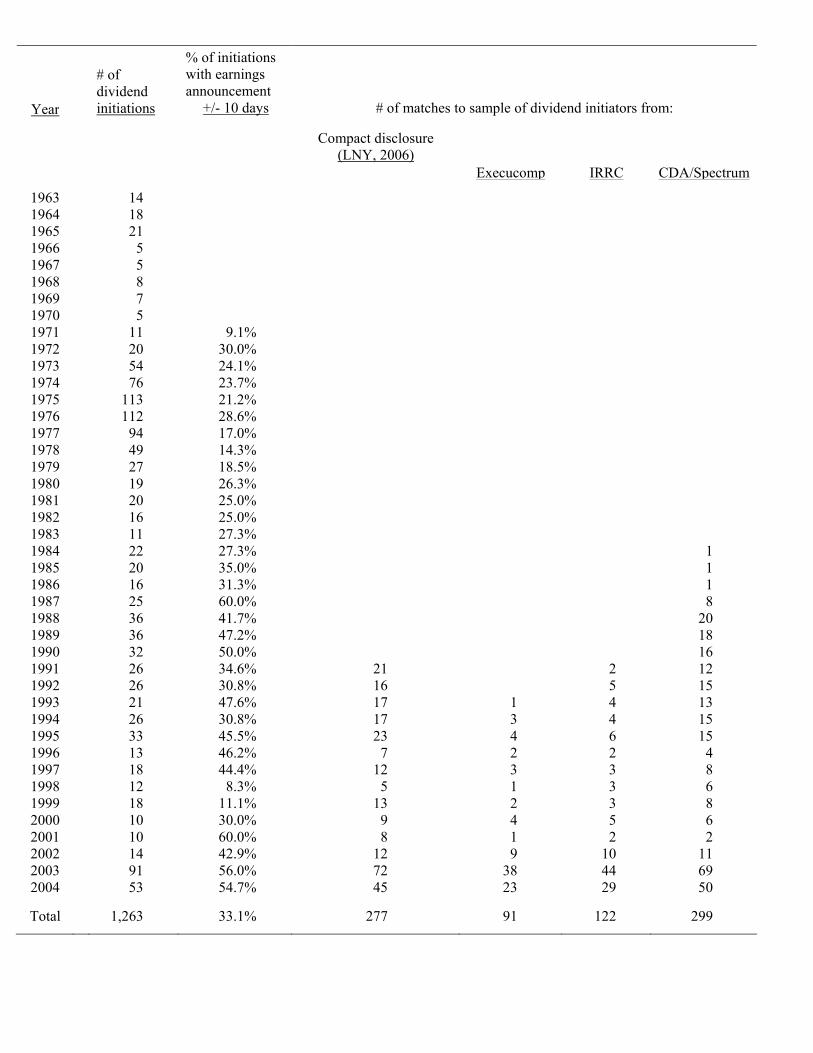

Table 5 shows the distribution of initiation announcements by year of announcement.

There are 1,263 dividend initiation announcements between 1963 and 2004 that meet the criteria

described above. The second column in Table 5 contains the percentage of those announcements

for which there is a quarterly earnings announcement date within a 21-day window centered on

the dividend initiation announcement date.17 33% of the initiation announcements have a

quarterly earnings announcement in the preceding or following ten days, although that fraction is

considerably higher nearer the end of the sample period.18 As documented later in this paper (and

in Asquith and Mullins (1983)), the incidence of an earnings announcement in the window

surrounding a dividend initiation announcement has almost no perceptible effect on the average

dividend initiation announcement return. For most of the analysis, therefore, I ignore the fact that

a substantial fraction of dividend initiation announcements are timed with quarterly earnings

releases.

The final four columns in Table 5 document how many of the firms initiating dividends

are covered in the various databases used to obtain governance data. Most of the matches between

17 Compustat begins recording quarterly earnings announcement dates in 1971. 18 Asquith and Mullins (1983) report that 66 of their 160 dividend initiations announcements (41%) from 1963 – 1980 have an earnings announcement within ± 10 days.

25

dividend initiators and governance data span the 1991 – 2004 period, and therefore this is the

effective sample period for my analysis of the relation between governance characteristics and

dividend initiation announcement returns.

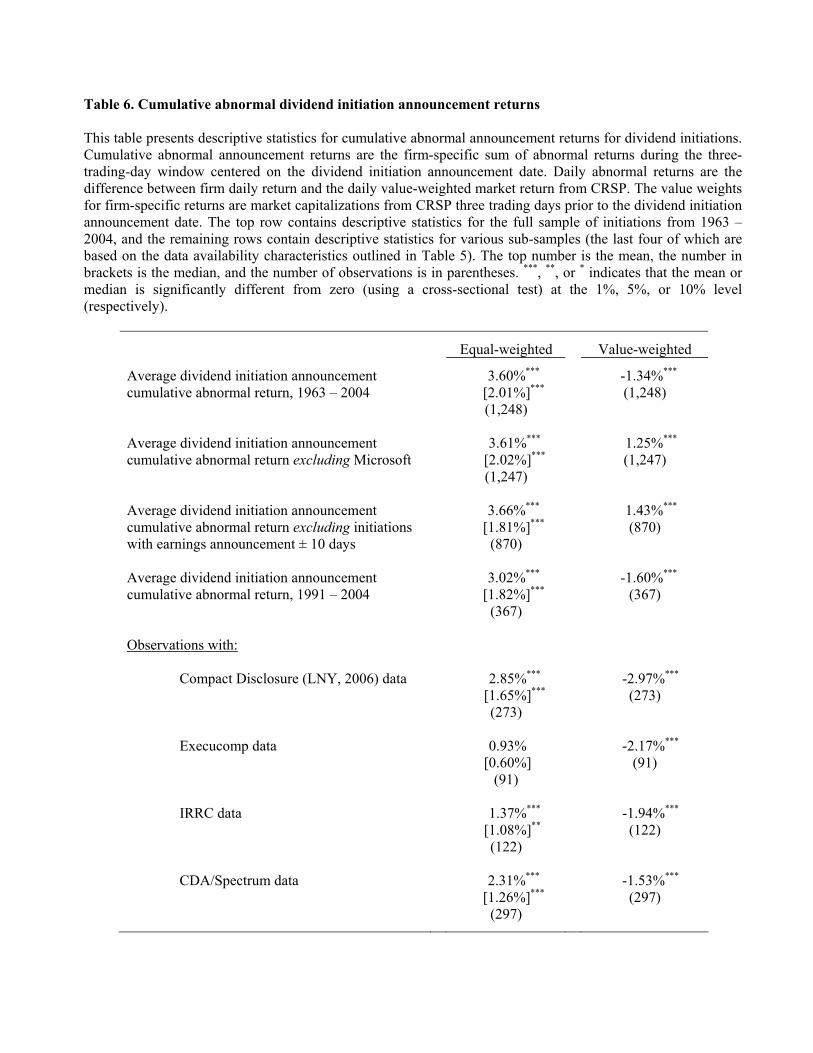

Table 6 contains descriptive statistics for dividend initiation announcement abnormal

returns. Cumulative abnormal announcement returns are the firm-specific sum of abnormal

returns during the three-trading-day window centered on the dividend initiation announcement

date, and daily abnormal returns are the difference between firm return and the value-weighted

market return from CRSP. The two columns in Table 6 show equal- and value-weighted averages

of cumulative abnormal announcement returns for various subsamples of the data, where the

value weights are market capitalizations from CRSP three trading-days prior to the dividend

initiation announcement date.

The first entry in the first column is the usual result for dividend initiation announcement

returns (see, for example, Asquith and Mullins (1983)). For the full sample from 1963 – 2004,

three-day equally-weighted average initiation announcement abnormal returns are 3.6%, which is

statistically significantly different from zero at the 1% level (median of 2%, also statistically

significantly different from zero). The corresponding value-weighted average (second column),

however, is significantly negative. As can be seen in the second row, this is almost entirely due to

the over-weighting of Microsoft (cumulative abnormal return of -7% for the three-trading-day

period surrounding Microsoft’s dividend initiation announcement on January 16th, 2003) in the

value-weighted average. Excluding Microsoft from the sample leaves the equal-weighted average

initiation return virtually unchanged, but causes the value-weighted return to revert to being

significantly positive. While the full-sample average-return characteristics are consistent with

much of the prior literature, it is notable that one observation (Microsoft) has such a dramatic

effect on value-weighted dividend initiation return averages.

26

Excluding initiations within ±10 days of an earnings announcement (third row in Table 6)

has little effect on the average initiation announcement returns,19 which are significantly positive

regardless of the weighting scheme. Clearly, some of the proximate earnings announcements are

“good news” and some “bad news,” suggesting that the proximity of earnings announcements

does not dramatically change the overall distribution of initiation returns. The fourth row in Table

6 shows average dividend initiation returns for the sample period during which most governance

data is available (1991 – 2004), and the returns during that subsample are very similar to those in

the full sample.

The last four rows of Table 6 contain descriptive statistics for the subsamples of initiation

announcements for which the initiating firm can be matched to the various databases containing

governance data. All these subsamples contain the Microsoft initiation, explaining the

significantly negative value-weighted average returns. However, apart from the limited

subsample with Execucomp data (used to form the Strong board variable), the other subsamples

have significantly positive equal-weighted mean and median initiation announcement abnormal

returns, with little difference between the data-availability subsamples and the main sample

averages in the upper half of the table. All average initiation announcement abnormal returns

reported in the remainder of this paper are equal-weighted and for the largest subsamples

available (including the Microsoft initiation).

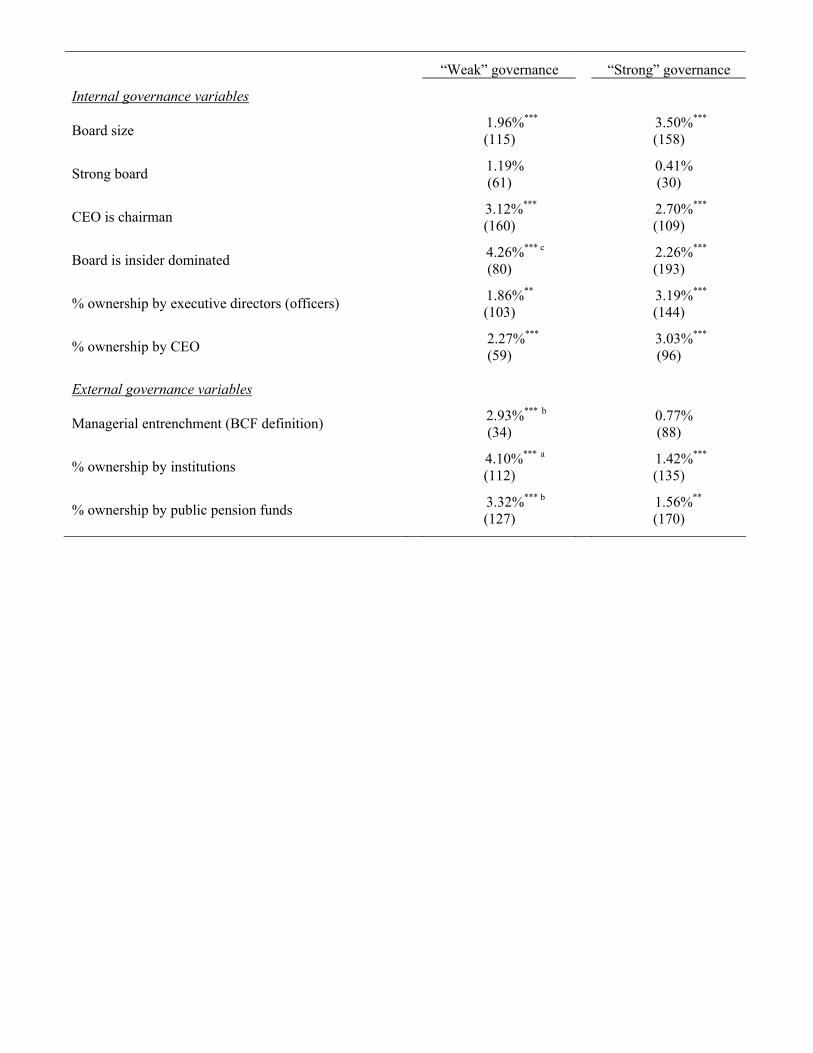

Table 7 contains comparisons of average abnormal dividend initiation announcement

returns for subsamples of initiators with “weak” and “strong” governance. As hypothesized in

H2b, I expect to observe significantly more positive initiation announcement returns for firms

with weak governance than for firms with strong governance. The set of governance measures

used to proxy for “weak” and “strong” governance are the same as those outlined in Section II.

Dividend initiators are defined as having “weak” governance if board size is above the median,

19 Microsoft’s 2003 dividend initiation announcement (1/16/2003) occurred on exactly the same day as the second-quarter earnings announcement.

27

strong board equals zero, the CEO is also chairman, the board is insider dominated (percent of

executive directors (officers) on board > 50%), the BCF index indicates managerial

entrenchment, or the percent ownership by executive directors, the CEO, institutional investors,

or public pension funds is below the median. All medians are for all firms from the same data

source in the same year or reporting period. Dividend initiators that are not defined as having

“weak” governance (in each row) are defined as having “strong” governance.

Average abnormal announcement returns for dividend initiators with weak governance

are insignificantly different from average announcement returns for initiators with strong

governance when the strength of governance is measured using most of the internal governance

characteristics shown in Table 7. The sole exception is when the sample is split based on the

Board is insider dominated indicator variable: in that case, firms with weak internal governance

(insider dominated boards) have average dividend initiation announcement returns of 4.3%,

which is significantly greater (at the 10% level) than the average initiation announcement returns

of 2.3% for firms with strong governance by the same metric. This is the only result in the

internal governance panel that supports the substitute hypothesis (H2b).

However, a much more consistent pattern emerges when the external governance metrics

are employed in the bottom panel of Table 7. Dividend initiators with entrenched managers under

the BCF definition and low institutional and public pension fund ownership have significantly

more positive abnormal dividend initiation returns than do firms with strong governance by those

criteria. For example, the 34 firms for which the BCF index indicates managerial entrenchment

have average dividend initiation announcement returns of 2.9% (statistically significantly

different from zero at the 1% level), which is reliably different from the average dividend

initiation return of 0.8% (not statistically significantly different from zero) for firms without

entrenched managers. The same result holds when institutional or public pension fund ownership

is considered as an external governance proxy, with below-median ownership by important

28

outside investors hypothesized to reduce the monitoring of managers and increase the potential

for agency problems.20

The results in Table 7 also hold in a multivariate regression setting, although these results

are omitted for brevity.21 Lie (2000) shows that the two most important control variables in

regressions explaining dividend-change abnormal announcement returns are firm size and

dividend yield. Introducing each of the significant variables in Table 7 (insider dominated boards,

the BCF entrenchment index, and the ownership levels of external monitors) into a multivariate

regression explaining initiation returns while controlling for size and dividend yield results in

qualitatively identical results to those presented in a univariate setting in Table 7.

The results in Table 7 also suggest that variation in governance policies do not

completely explain the positive stock price reactions to initiation announcements. In other words,

while firms with weak governance appear to have significantly higher initiation announcement

abnormal returns, firms with strong governance do experience significantly positive

announcement returns (the last column in Table 7). At the margin, variation in governance

policies does contribute to positive dividend initiation announcement returns, but clearly there are

factors other than the governance variables measured here that contribute to initiation

announcement returns. The literature has failed to provide convincing evidence that a signal about

future earnings is one of these factors, leaving open the possibility that some measure of agency

costs that is orthogonal to the measures presented here will provide an important explanation for

dividend initiation announcement returns.

Dividend initiation announcement returns lend support to the substitute hypothesis (H2b).

Firms with characteristics indicative of weak governance (insider dominated boards, entrenched

20 The negative relation between institutional holdings and dividend initiation abnormal returns is consistent with the results in Amihud and Li (2006), who find that dividend announcement returns are lower for firms with higher institutional shareholdings. Amihud and Li interpret this finding as consistent with the hypothesis that institutional investors are more sophisticated and informed than other investors, and therefore that their information is reflected in prices prior to dividend announcement dates. Amihud and Li do not specifically consider dividend initiations in their analysis. 21 But available from the author by request.

29

managers, and low ownership by institutional investors and activist public pension funds) have

significantly more positive initiation announcement abnormal returns than do dividend initiators

with characteristics suggestive of strong governance. These results are consistent with the notion

that dividend policy is one component of the package of policies that firms use to bond with

stockholders, and that the abnormal returns to initiating a policy of paying dividends reflect an

anticipated reduction in the agency costs of external equity.

IV. Conclusion

This paper provides evidence that corporate governance affects both the willingness of

firms to pay dividends and the market reaction to dividend initiation announcements. Firms with

characteristics that are thought to proxy for weak internal and external governance (large, insider

dominated boards, entrenched managers, and low ownership levels by insiders and important

external monitors) are more likely to pay cash out to stockholders in the form of dividends,

although there is some evidence that these firms are also less likely to pay cash out to

stockholders in the form of stock repurchases. Such firms also experience significantly more

positive stock price reactions to dividend initiation announcements. Taken together, these results

suggest that firms use dividend policy to compensate for other characteristics that have the

potential to create agency problems between managers and outside equity holders. Dividend

policy, therefore, appears to be a substitute for other control mechanisms in the equilibrium

monitoring/bonding package chosen by firms, and the market values the anticipated reduction in

agency costs resulting from the choice to begin paying dividends.

The results in this paper suggest several avenues for future research. While initiation

announcement returns are significantly more positive for firms with weak governance, initiation

returns are significantly different from zero (and positive) even for firms that traditional proxies

suggest have strong internal and external governance mechanisms. Clearly, something other than

an anticipated reduction in agency costs also drives abnormal equity returns around dividend

30

initiation announcements. Given that most empirical evidence in the literature does not support a

signaling explanation (Watts, 1973; DeAngelo, DeAngelo, and Skinner, 1996), a more thorough

analysis of dividend initiation announcement returns appears warranted. One possibility,

suggested by Grullon, Michaely, and Swaminathan (2002), is that abnormal stock price

appreciations around dividend initiation announcements are driven by lower risk premiums:

initiating dividend payments may signal financial maturity and therefore lower risk. However,

dividend initiations also frequently signal operating maturity, in terms of lower future growth,

earnings (Grullon, Michaely, and Swaminathan (2002)), and cash flows. An analysis of how

maturity (both financial and operational) interacts with the governance implications of dividend

initiations, and the fact that the governance implications will be different for growing firms than

for “harvesting” firms, has the potential to significantly expand our understanding of dividend

policy and the market reaction to dividend policy changes.

31

References

Allen, F., Bernado, A., Welch, I., 2000. A theory of dividends based on tax clienteles. Journal of

Finance 55, 2499-2536.

Amihud, Y., Li, K., 2006. The declining information content of dividend announcements and the

effect of institutional holdings. Journal of Financial and Quantitative Analysis 41, 637-

660.

Asquith, P., Mullins. D., 1983. The impact of initiating dividend payments on shareholders’

wealth. Journal of Business 56, 77-96.

Barclay, M., Holderness, C., 1991.Negotiated block trades and corporate control. Journal of

Finance 46, 861-878.

Bebchuk, L., Cohen, A., Ferrell, A., 2005. What matters in corporate governance? Harvard Law

School John M. Olin Center Discussion Paper No. 491.

Black, F., 1976. The dividend puzzle. Journal of Portfolio Management 2, 5-8.

Brickley, J., Coles, J., Jarrell, G., 1997. Leadership structure: Separating the CEO and Chairman

of the Board. Journal of Corporate Finance 3, 189-220.

Brickley, J., Coles, J., Terry, R., 1994. Outside directors and the adoption of poison pills. Journal

of Financial Economics 35, 371-390.

Brickley, J., Lease, R., Smith, C., 1988. Ownership structure and voting on antitakeover

amendments. Journal of Financial Economics 20, 267-291.

Chen, X., Harford, J., Li, K., 2005. Monitoring: Which institutions matter? Working paper,

University of British Columbia.

Cremers, M., Nair, V., 2005. Governance mechanisms and equity prices. Journal of Finance 60,

2859-2894.

DeAngelo, H., DeAngelo, L., 2006. The irrelevance of the MM dividend irrelevance theorem.

Journal of Financial Economics 79, 293-315.

32

DeAngelo, H., DeAngelo, L., Skinner, D., 1996. Reversal of fortune: Dividend signaling and the

disappearance of sustained earnings growth. Journal of Financial Economics 40, 341-

371.

DeAngelo, H., DeAngelo, L., Skinner, D., 2004. Are dividends disappearing? Dividend

concentration and the consolidation of earnings. Journal of Financial Economics 72, 425-

456.

DeAngelo, H., DeAngelo, L., Stulz, R., 2006. Dividend policy and the earned/contributed capital

mix: a test of the life-cycle theory. Journal of Financial Economics, forthcoming.

Del Guercio, D., Hawkins, J., 1999. The motivation and impact of pension fund activism. Journal

of Financial Economics 52, 293-340.

Dittmar, A. Mahrt-Smith, J., 2005. Corporate governance and the value of cash holdings. Journal

of Financial Economics, forthcoming.

Easterbrook, F., 1984. Two agency-cost explanations of dividends. American Economic Review

74, 650-659.

Fama, E., French, K., 1997. Industry costs of equity. Journal of Financial Economics 43, 153-

193.

Fama, E., French, K., 2001. Disappearing dividends: changing firm characteristics or lower

propensity to pay? Journal of Financial Economics 60, 3-43.

Fama, E., Jensen, M., 1983. Separation of ownership and control. Journal of Law and Economics

26, 301-325.

Fama, E., MacBeth, J., 1973. Risk, return, and equilibrium: empirical tests. Journal of Political

Economy 81, 607–636.

Fenn, G., Liang, N., 2001. Corporate payout policy and managerial stock incentives. Journal of

Financial Economics 60, 45-72.

33

Gillan, S., Hartzell, J., Starks, L., 2006. Tradeoffs in corporate governance: Evidence from board

structures and charter provisions. Working paper, University of Texas at Austin.

Gompers, P., Iishi, J., Metrick, A., 2003. Corporate governance and equity prices. Quarterly

Journal of Economics 118, 107-155. Grullon, G., Michaely, R., Swaminathan, B., 2002. Are dividend changes a sign of firm maturity?

Journal of Business 75, 387-424.

Gugler, K., 2003. Corporate governance, dividend payout policy, and the interrelation between

dividends, R&D, and capital investment. Journal of Banking and Finance 27, 1297-1321.

Harford, J., Li, K., 2006. Decoupling CEO wealth and firm performance: The case of acquiring

CEOs. Journal of Finance, forthcoming.

Harford, J., Mansi, S., Maxwell, W., 2005. Corporate governance and a firm’s cash holdings.

Working paper, University of Washington.

Hermalin, B., Weisbach, M., 1998. Endogenously chosen boards of directors and their monitoring

of the CEO. American Economic Review 88, 96-118.

Hu, A., Kumar, P., 2004. Managerial entrenchment and payout policy. Journal of Financial and

Quantitative Analysis 39, 759-790.

Jensen, M., 1986. Agency costs of free cash flow, corporate finance, and takeovers. American

Economic Review 76, 323-329.

Jensen, M., 1993. The modern industrial revolution, exit, and the failure of internal control

systems. Journal of Finance 48, 831-880.

Jensen, M., Meckling, W., 1976. Theory of the firm: Managerial behavior, agency costs, and

ownership structure. Journal of Financial Economics 3, 305-360.

Jensen, G., Solberg, D., Zorn, T., 1992. Simultaneous determination of insider ownership, debt,

and dividend policies. Journal of Financial and Quantitative Analysis 27, 247-263.

John. K., Knyazeva, A., 2006. Payout policy agency conflicts, and corporate governance.

Working paper, New York University.

34

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., Vishny, R, 2000. Agency problems and dividend

policies around the world. Journal of Finance 55, 1-33.

Lambert, R., Lanen, W., Larcker, D., 1989. Executive stock option plans and dividend policy.

Journal of Financial and Quantitative Analysis 24, 409-425.

Lang, L., Litzenberger, R., 1989. Dividend announcements: Cash flow signaling vs. free cash

flow hypothesis. Journal of Financial Economics 24, 181-191.

Larcker, D., Richardson, S., Tuna, A., 2005. How important is corporate governance? Working

paper, University of Pennsylvania.

Lie, E., 2000. Excess funds and agency problems: An empirical study of incremental cash

disbursements. Review of Financial Studies 13, 219-248.

Linck, J., Netter, J., Yang, T., 2006. The determinants of board structure. Working paper,

University of Georgia.

Michaely, R., Roberts, M., 2006. Dividend smoothing, agency costs, and information asymmetry:

Lessons from the dividend policies of private firms. Working paper, Cornell University.

Morck, R., Shleifer, A., Vishny, R., 1988. Management ownership and market valuation: An

empirical analysis. Journal of Financial Economics 20, 293-315.

Myers, S., 2000. Outside equity. Journal of Finance 55, 1005-1037.

Nielsen, A., 2005. Corporate governance, leverage, and dividend policy. Working paper,

Princeton University.

Pan, C., 2006. Why are firms with entrenched managers more likely to pay dividends? Working

paper, Ohio State University.

Renneboog, L., Szilagyi, P., 2006. How relevant is dividend policy under low shareholder

protection? Working paper, Tilburg University.

35

Rozeff, M., 1982. Growth, beta, and agency costs as determinants of dividend payout ratios.

Journal of Financial Research 5, 249-259.

Smith, M., 1996. Shareholder activism by institutional investors: Evidence for CalPERS. Journal