Embed Size (px)

Citation preview

1

Summer Workshopon

Distribution Theory & its Summability Perspective

16 17 18 18.9 20 21 220

5

10

15

20

25

30

35

40

45

50

|

Center of massAmount of Drink Mix (in ounces)

Freq

uenc

ies

M. Kazım KhanKent State University (USA)

Place: Ankara University, Department of Mathematics

Dates: 16 May - 27 May 2011

Supported by: The Scientific and Technical Research Council of Turkey (TUBITAK)

2

Preface

This is a collection of lecture notes I gave at Ankara University, department of math-ematics, during the last two weeks of May, 2011. I am greatful to Professor CihanOrhan and the Scientific and Technical Research Council of Turkey (TUBITAK)for the invitation and support.

The primary focus of the lectures was to introduce the basic components ofdistribution theory and bring out how summability theory plays out its role init. I did not assume any prior knowledge of probability theory on the part of theparticipants. Therefore, the first few lectures were completely devoted to buildingthe language of probability and distribution theory. These are then used freely inthe rest of the lectures. To save some time, I did not prove most of these results.

Then a few lectures deal with Fourier inversion theory specifically from thesummability perspective. The next batch consists of convergence concepts, whereI introduce the weak and the strong laws of large numbers. Again long proofs wereomitted. A noteable exception deals with the results that involve the uniformly in-tegrable sequence spaces. Since this is a new concept from summability perspective,I have tried to sketch some of the proofs.

I must acknowledge the legendary Turkish hospitality of all the people I cameto meet. As always, it was a pleasure visiting Turkey and I hope to have the chanceto visit again.

Mohammad Kazım Khan,Kent State UniversityKent, Ohio, USA.

4

List of Participants

1- AYDIN, Didem Ankara Universitesi

2- AYGAR, Yelda Ankara Universitesi

3- AYKOL, Canay Ankara Universitesi

4- BASCANBAZ TUNCA, Gulen Ankara Universitesi

5- CAN, Cagla Ankara Universitesi

6- CEBESOY, Serifenur Ankara Universitesi

7- COSKUN, Cafer Ankara Universitesi

8- CETIN, Nursel Ankara Universitesi

9- DONE, Yesim Ankara Universitesi

10- ERDAL, Ibrahim Ankara Universitesi

11- GUREL, Ovgu Ankara Universitesi

12- IPEK, Pembe, Ankara Universitesi

13- KATAR, Deniz Ankara Universitesi

14- ORHAN, Cihan Ankara Universitesi

15- SAKAOGLU, Ilknur Ankara Universitesi

16- SOYLU, Elis Ankara Universitesi

17- SAHIN, Nilay Ankara Universitesi

18- TAS, Emre Ankara Universitesi

19- UNVER, Mehmet Ankara Universitesi

20- YARDIMCI, Seyhmus Ankara Universitesi

21- YILMAZ, Basar Ankara Universitesi

22- YURDAKADIM, Tugba Ankara Universitesi

6

Contents

Preface 3

List of Participants 5

Contents 5

List of Figures 9

1 Modeling Distributions 11.1 Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Probability Space & Random Variables . . . . . . . . . . . . . . . . 8

2 Probability Spaces & Random Variables 11

3 Expectations 213.1 Properties of Lebesgue integral . . . . . . . . . . . . . . . . . . . . . 223.2 Covariance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

4 Various Inequalities 274.1 Holder & Minkowski’s Inequalities . . . . . . . . . . . . . . . . . . . 284.2 Jensen’s Inequality . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

5 Classification of Distributions 355.1 Absolute Continuity & Singularity . . . . . . . . . . . . . . . . . . . 41

6 Conditional Distributions 496.1 Conditional Expectations . . . . . . . . . . . . . . . . . . . . . . . . 52

7 Conditional Expectations & Martingales 577.1 Properties of E(X|Y ) . . . . . . . . . . . . . . . . . . . . . . . . . . 577.2 Martingales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

8 Independence & Transformations 638.1 Transformations of Random Variables . . . . . . . . . . . . . . . . . 638.2 Sequences of Independent Random Variables . . . . . . . . . . . . . 688.3 Generating Functions . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

8 CONTENTS

9 Ranks, Order Statistics & Records 75

10 Fourier Transforms 8310.1 Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

11 Summability Assisted Inversion 89

12 General Inversion 9712.1 Fourier & Dirichlet Series . . . . . . . . . . . . . . . . . . . . . . . . 99

13 Basic Limit Theorems 10713.1 Convergence in Distribution . . . . . . . . . . . . . . . . . . . . . . . 10813.2 Convergence in Probability & WLLN . . . . . . . . . . . . . . . . . . 111

14 Almost Sure Convergence & SLLN 117

15 The Lp Spaces & Uniform Integrability 12715.1 Uniform Integrability . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

16 Laws of Large Numbers 14116.1 Subsequences & Kolmogorov Inequality . . . . . . . . . . . . . . . . 142

17 WLLN, SLLN & Uniform SLLN 15117.1 Glivenko-Cantelli Theorem . . . . . . . . . . . . . . . . . . . . . . . 163

18 Random Series 16918.1 Zero-One Laws & Random Series . . . . . . . . . . . . . . . . . . . . 16918.2 Refinements of SLLN . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

19 Kolmogorov’s Three Series Theorem 183

20 The Law of Iterated Logarithms 189

List of Figures

1.1 A Histogram for the Drink Mix Distribution. . . . . . . . . . . . . . 41.2 Inverse Image of an Interval . . . . . . . . . . . . . . . . . . . . . . . 8

8.1 Inverse of a Distribution Function. . . . . . . . . . . . . . . . . . . . 66

11.1 Triangular Density . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

12.1 Dirichlet Kernels for n = 5 and n = 8. . . . . . . . . . . . . . . . . . 10112.2 Fejer Kernels for T = 5 and T = 8. . . . . . . . . . . . . . . . . . . . 10312.3 Poisson Kernels for r = 0.8 and r = 0.9. . . . . . . . . . . . . . . . . 105

14.1 Density of Random Harmonic Series . . . . . . . . . . . . . . . . . . 124

10 LIST OF FIGURES

Lecture 1

Modeling Distributions

A phenomenon when repeatedly observed gives rise to a distribution. In otherwords, a distribution is our way of capturing the variability in the phenomenon.Such distributions arise in almost all fields of endeavor. In social sciences they areused to keep tabs on social indicators, in finance they are used to study and qunatifythe financial health of corporations and pricing various assets and derived securitiessuch as options and bonds. Data distributions appear in statistics. In mathematicsdistributions of zeros of orthogonal polynomials appear and the distribution ofprimes are fundamental entities. In natural sciences about one and a half centureago Maxwell conjoured up a distribution to describe the speed of molecules inideal gas, which was later observed to be quite accurate. The genetic diversityand its quantification is still in its infency in terms of discovering the underlyingdistributions that it hides.

In this chapter we will collect the tools that are quite effective in studyingdistributions. We will present the following basic notions.

• Some examples of distributions,

• A framework by which distributions can be modeled,

• Transforms of distributions, such as moment generating functions and char-acteristic functions,

• Conditional probabilities and conditional expectations.

These results will be used in the remainder of the book.

1.1 Distributions

Any characteristic, when repeatedly measured, yields a collection of measured/collectedresponses. The word “variable” is used for the characteristic that is being measured,since it may vary from measurement to measurement. The collection of all the mea-sured responses is called the “distribution” of the variable. Sometimes, the worddata is also used to refer to the distribution of the variable. Distributions may bereal or just imagined entities. Here we collect a few examples of distributions ofthe following sorts to show their vast diversity.

2 Modeling Distributions

• (i) Distributions arising while measuring mass produced products.

• (ii) Distributions arising in categorical populations.

• (iii) Distribution of Stirling numbers.

• (iv) Distribution of zeros of orthogonal polynomials.

• (v) Distributional convergence of summability theory.

• (vi) Distributions of eigenvalues of Toeplitz matrices.

• (vii) Maxwell’s law of ideal gas.

• (viii) Distribution of primes.

• (ix) The Fineman-Kac formula and partial differential equations.

Of course, this is just a tiny sample of topics from an enormous field. One obviousomission being the field of Schwartz’s distributions. This is purely because thereare excellent books on the subject.1 We will, however, briefly visit this branch whilediscussing summability assisted Fourier inversion theory.

Example - 1.1.1 - (Measurement distributions — accuracy of automaticfilling machines) Kountry Times makes 20 ounce cans of lemonade drink mix.Due to unknown random fluctuations, the actual fill weight of each can is rarelyequal to 20 oz. Here is a collection of fill weights of 200 randomly chosen cans.

18.3 19.4 18.8 19.6 19.8 17.7 18.2 20.1 17.2 18.8 19.0

18.6 18.0 18.9 19.1 17.2 17.3 19.4 18.6 20.5 20.8 19.9

18.7 16.7 19.2 18.8 18.3 18.3 18.3 17.9 18.2 17.5 17.6

19.7 20.5 19.5 18.6 19.9 19.3 18.5 19.9 18.7 20.3 19.2

18.9 18.6 19.4 18.7 18.5 19.2 17.3 18.0 17.7 19.2 19.1

18.8 18.3 21.0 18.0 18.9 19.9 21.4 18.8 19.0 18.9 18.7

18.9 19.2 17.6 20.0 19.5 19.4 18.3 19.9 18.4 18.3 18.6

19.4 17.7 18.8 17.8 19.2 18.6 20.2 19.0 18.3 18.3 19.0

18.4 19.4 19.4 17.9 19.2 18.5 17.7 19.3 19.0 16.7 18.3

19.7 18.8 19.4 20.3 18.3 18.6 19.4 18.4 18.6 19.1 18.0

18.8 18.3 18.7 19.1 17.8 17.5 17.0 19.4 19.2 19.8 18.6

17.7 17.9 19.1 18.2 19.5 19.6 20.4 20.7 19.8 18.9 19.2

17.8 21.0 17.5 17.9 18.5 21.1 19.8 18.3 20.2 17.4 18.8

18.5 19.7 19.0 18.3 19.3 18.8 18.1 17.8 19.1 20.1 19.9

21.0 17.9 18.3 17.1 18.7 18.5 19.1 17.6 20.4 19.2 19.2

20.2 17.4 18.4 18.9 18.4 18.8 18.3 19.8 18.7 19.1 20.4

18.7 18.9 18.0 20.7 20.8 19.9 20.6 19.2 18.4 18.5 18.5

18.4 19.9 17.9 19.4 19.2 20.4 19.7 17.5 19.0 17.9 18.4

19.7 19.1

In this example, the feature being measured is the fill weight (measured in ounces).We see unexpectedly large amount of variability. The issue is:

“Does the distribution say anything about whether the advertised av-erage fill weight of 20 oz is being met or not”?

1For instance, see ...

1.1 Distributions 3

The average, or the mean and the variance of this collected distribution now denotedas x1, x2, · · · , xn, is

xn =x1 + x2 · · ·+ xn

n=

1

n

n∑

i=1

xi = 18.940,

S2 =1

n− 1

n∑

i=1

(xi − x)2 =

∑ni=1 x2

i − n(x)2

n− 1= 0.8574.

The mean gives a feeling that the automatic filling machine may be malfunctioning.Since the units of variance are squared, we work with its positive square root, S,called the standard deviation. For our fill weights distribution S = 0.926 oz. Thestandard deviation typically gives a scale by which we can gauage the “width” ofthe distribution. Typically plus/minus three times the standard deviation aroundthe mean contains most of the values of the distribution. Note that the smallestvalue of our data distribution is 16.7 oz, and the largest value is 21.4. In this caseall the values of the distribution lie within 3S of the mean.

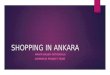

Of course knowing this distribution of 200 observations is only partially inter-esting. The real aim is to conclude someting about the source of these 200 obser-vations, called the population distribution, which is a mythical entity and repsentshow the automatic filling machine behaves. To get a feel for and then model theshape of the source distribution we resort to figures. We make some groups, alsocalled bins, say J1 = (16.5−17.0], J2 = (17.0−17.5], etc., and count the number ofobservations that fall into these bins. Dividing the frequencies by the total numberof observations gives the relative frequency distribution, which does not change theshape. A plot of this frequency distribution is called a histogram of the distribution.

Fill Weights Frequency Relative Frequency

16.5 − 17.0 2 0.01017.0 − 17.5 8 0.04017.5 − 18.0 23 0.11518.0 − 18.5 33 0.16518.5 − 19.0 44 0.22019.0 − 19.5 43 0.21519.5 − 20.0 23 0.11520.0 − 20.5 12 0.06020.5 − 21.0 7 0.03521.0 − 21.5 5 0.025

Total 200 1.000

Figure1.1 shows the resulting histogram for the distribution where the bins are onthe x-axis and the frequencies are on the y-axis so that the areas of the rectanglesare proportional to the frequencies. The general shape is captured by the super-imposed bell shaped curve. This form is a little more revealing than the originallong list of 200 data values. We clearly see that a majority of the cans had lessthan the advertised amount of 20 oz of drink mix in them. Also, only about0.06 + 0.035 + 0.025 = 12 percent of the observations were above 20 oz.

It is an amazing fact of life that most of the data sets which measure heights,weights or lengths of components produced by factories on a mass scale, one

4 Modeling Distributions

16 17 18 18.9 20 21 220

5

10

15

20

25

30

35

40

45

50

|

Center of massAmount of Drink Mix (in ounces)

Freq

uenc

ies

Figure 1.1: A Histogram for the Drink Mix Distribution.

tends to observe such bell shaped histograms. The superimposed curve is called anormal curve and is proportional to

f(x) =1

σ√

2πexp

−1

2σ2(x− µ)2

, −∞ < x <∞.

Most measurement type distributions are mathematically modeled by a normalcurve. Symbolically we denote this by X ∼ N(µ, σ2), where X represents thefill weight of a randomly chosen can. The letter N stands for the word “normaldistribution”, and µ is the center or mean and σ is the standard deviation. In words,the modeled density describes where will a randomly selected can’s fill weight fall.The histogram reflects the empirical2 evidence for our model.

The qunatity, P(a < X ≤ b), represents the model-predicted percentage of canswhose fill weights lie between a and b oz. Thanks to modern calculators,

P(18 < X ≤ 21) =1

σ√

2π

∫ 21

18

e−(x−µ)2/(2σ2) dx =1√2π

∫ (21−18.9)/0.926

(18−18.9)/0.926

e−u2/2 du

≈ 0.82.24%.

When we consult the observed distribution and actually count we find that

33 + 44 + 43 + 23 + 12 + 7

200=

162

200= 0.81 = 81%

cans had their fill weights between 18 and 21 ounces. The agreement is remarkablygood, indicating that our normal curve model is quite useful. We don’t have tocarry the n = 200 observations in our pocket anymore. One simple mathematical

2“Empirical” stands for “derived from experience”.

1.1 Distributions 5

curve captures it. Even more importantly the curve describes the fill weights ofall those cans that the automatic filling machine produced that we never checked.Due to the popularity of normal curves as models, they have been given specialemphasis in statistical literature.3

Example - 1.1.2 - (Modeling categorical populations — US voters) A weekbefore the 2000 US presidential elections, the voter preferences of the two presiden-tial candidates were as follows.

Bush,Bush, · · · ,Bush︸ ︷︷ ︸

80 million

, Gore,Gore, · · · ,Gore︸ ︷︷ ︸85 million

.

This is a very large categorical distribution. However, a very simple way to representthis distribution, without losing any information, is to write it in its frequenceyformat, namely write B (for Bush) once and put its frequence next to it and writeG (for Gore) once and put its frequence next to it. We may code the categories(letters) B,G by numbers, if we like. For instance, denoting B by 0 and G by 1,we may write the distribution of our coded variable, say X, as

Values of X 0 1Frequencies 80,000,000 85,000,000

The resulting relative frequency distribution is specified by the proportion

p =85, 000, 000

80, 000, 000 + 85, 000, 000=

85

165= 0.51515.

where X denotes the preference of an individual, represented in the coded form of0 or 1. Note that the population mean is p and the population variance is p(1− p).

Example - 1.1.3 - (Distribution of zeros of orthogonal polynomials) Sofar we talked about data distributions and their sources. As mentioned in thebeginning, distributions appear every where.

Consider a sequence of polynomials pn(x), n = 0, 1, 2, · · · , where p0(x) ≡ 1, andpn(x) is of degree n. Suppose there exist real constants an, bn such that an > 0 forall n ≥ 0,

an+1pn+1(x) + (bn − x)pn(x) + anpn−1(x) ≡ 0, n ≥ 1.

There is a result of Favard which says that each pn(x) has exactly n distinct realzeros, which we denote as

x1n < x2n < · · · < xnn.

The issue is what are they? Having these zeros gives us an extremely fast numericalintegration method (called the Gaussian quadrature) among other benefits. If it is

3Normal distributions are also called Gaussian distributions since the German math-ematician/astronomer, Carl Friedrich Gauss (1777 - 1855), showed their importance asmodels of measurement errors in celestial objects.

6 Modeling Distributions

too painful to write all of the zeros down for all n, then the next best thing to askis, what is their distribution, at least approximately? The answer is that the curve,

f(x) =

1

π√

(b+2a−x)(x−b+2a), for x ∈ (b− 2a, b + 2a),

0 otherwise,

has a lot to do with the approximate distribution of zeros. From summabilityperspective, we can say more. Suppose an and bn are two sequences of realnumbers so that, an ≥ 0 and for some constants a, b, and every ǫ > 0 we have

n∑

k: |ak−a|≥ǫ

1

n + 1→ 0,

n∑

k: |bk−b|≥ǫ

1

n + 1→ 0.

In the language of summability theory, ak is Cesaro-statistically convergent to aand bk is Cesaro-statistically convergent to b. If a > 0 then the histogram of thedistribution of zeros of pn(x) is approximately the curve f(x). This is just the tipof the iceberg. Much more can be deduced in much more general settings.

Example - 1.1.4 - (Convergence and summability) A matrix summability methodconsists of numbers ank, n, k = 0, 1, 2, · · · arranged in a matrix form, A = [ank].Such a matrix is constructed with the aim of converting a nonconvergent sequence,x0, x1, · · · into a convergent one. In other words, if

yn :=∞∑

k=0

ankxk, n = 0, 1, 2, · · ·

then our hope is that yn should converge. However, when (xk) is itself convergentto some number ℓ then we insist that (yn) should also be convergent to the sameℓ. A matrix A = [ank] which has this “convergence reproducing” property is calledregular. To handle the kind of examples we will present we need a bit more generalconcept that allows x = (xkn) to be a matrix as well and xkn need not be num-bers but could be functions. When xkn = xk for all n, we revert to the classicalsummability. There are four notions of convergence.

• (i) Let yn =∑∞

k=0 xkn ank be defined for all n called the A-transform of x.We way that x is A-summable to α if yn → α. This notion can be extendedto the case when xkn and α lie in a normed linear space.

• (ii) If xkn are real, and let F (t) be a distribution, i.e., nondecreasing rightcontinuous function with F (−∞) = 0 and F (+∞) = 1. We say x isA-distributionally convergent to F if for all t at which F is continuous wehave

limn→∞

∑

k:xkn≤t

ank = F (t).

This notion can be extended to higher dimensional forms when both xkn andt are d-dimensional vectors.

1.1 Distributions 7

• (iii) We say x = (xkn) is A-statistically convergent to α if for every ε > 0 wehave

limn→∞

∑

k:|xkn−α|>ε

ank = 0.

This notion can be extended to the case when xkn and α lie in a topologicalspace. Example 1.1.3 uses this notion of convergence for the ak and bksequences with the matrix A being the Cesaro matrix.

• (iv) We say x = (xkn) is A-strongly convergent to α if

limn→∞

∞∑

k=0

|xkn − α| ank = 0.

This notion can be extended to the case when xkn and α lie in a metric space.

Example - 1.1.5 - (Distribution of primes) Let π(n) be the prime countingfunction. That is, π(n) is the total number of primes that lie in the interval (0, n].Gauss as a teenager conjectured that

π(n) ∼ n

lnn.

The prime number theorem says that

π(n) ∼ Li(n) :=

∫ n

2

1

lnxdx ∼ n

∞∑

j=0

j!

(lnn)j+1.

This was proved by both Hadamard and de la Vallee Poussin in 1896, by showingthat the Riemann zeta function ζ(z) has no zeros of the type 1 + it. Hardy andWright’s4 book provides more details.

In 1914 Littlewood5 showed that π(n)−Li(n) is positive and negative infinitelyoften. Since Li(n) ∼ n

ln n + n(ln n)2 + 2n

(ln n)2 + · · · , Chebyshev asked the behavior of

the ratio

Xn :=π(n)

n/ lnn, n = 1, 2, · · · .

Chebyshev showed that 78 < lim infn Xn ≤ lim supn Xn < 9

8 . The recent book ofHavil6 shows that if limn→∞ Xn exists then limn Xn = 1. As an evidence of deeproots of π(x), the Riemann hyphothesis is equivalent to the statement

|π(n)− Li(n)| = O((lnn)

√n).

For more, see Ingham.7

4Hardy, G. H. and Wright, E. M. An Introduction to the Theory of Numbers, 5th ed.Oxford University Press, 1979.

5”Sur les distribution des nombres premiers”, Comptes Rendus Acad. Sci. Paris, vol.158, pp. 1869-1872, 1914.

6Havil, J. Gamma: Exploring Euler’s Constant. Princeton University Press, NJ, 2003.7Ingham, A. E., The Distribution of Prime Numbers. Cambridge University Press,

London, 1990.

8 Modeling Distributions

Example - 1.1.6 - Of course there are many more examples, such as

• (i) Asymptotic normality of the Stirling numbers.

• (ii) Distributions of eigenvalues of Toeplitz matrices.

• (iii) Distributions of eigenvalues of random matrices — wigner’s law.

• (iv) Maxwell’s law of ideal gas — distribution of speed of molecules in idealgas.

• (v) Fineman-Kac formula. Solutions of many types of PDEs and Brownianmotion go hand in hand. The poster child being the heat equation. This linkhas found an unexpted admirer, namely the financial industry, since it tiesvery nicely into the price of various derived financial securities such as thecall and put and many other options.

The above examples give a glimpse of the importance of the concept of a dis-tribution. Probability theory provide the ideal language to express concepts ofdistribution theory. Therefore we start off by building some basic structures ofprobability theory.

1.2 Probability Space & Random Variables

Our aim is to construct a mathematical structure to house the concept of a distribu-tion. Distributions always describe some features of some variables. Since variablesmay have random components in them, distributions are often linked to probabilitytheory with a concept called a random variable. A random variable being a func-tion defined over a probability space. To see what we need, consider the followingdiagram in which ω belongs to some abstract set, Ω, shown as the horizontal axisfor convenience. To connect to the histogram of X, if J = (a, b] is any bin, the

X(w)

A

J=(a,b]

w

Figure 1.2: Inverse Image of an Interval

area of the rectangle over it represents the “size” of the event a < X ≤ b. So, weneed to require that the abstract set Ω should be such that for every J = (a, b],its inverse set A = X−(J) should have some concept of “size”, which we may callits “measure” or its “chance” or its “probability” of occurrence. To avoid logicalinconsistencies we set up some ground rules for the collection of all sets for which

1.2 Probability Space & Random Variables 9

the concept of size needs to be defined. To be precise denote this set by the symbolE .• (i) We insist that a concept of size be attached to each subset of the type

A = X−1(J), when J = (a, b] and a < b. That is, each such A ∈ E .• (ii) Since combining two or more J1 = (a1, b1], J2 = (a2, b2], · · · , makes

practical sense, the concept of size should apply to

X−1(∪iJi) =⋃

i

X−1(Ji) =⋃

i

Ai.

In general, ∪iAi ∈ E , whenever Ai ∈ E . In particular, since R = ∪i(−i, i], weinsist that Ω = ∪iX

−1((−i, i]) ∈ E .• (iii) Since Jc = (−∞, a] ∪ (b,∞) is a union of some other J ’s, we insist that

Ac = X−1(Jc) should also be in our collection. More generally, if A ∈ E thenAc ∈ E .

• (iv) The concept of size should be defined for all A ∈ E . Furthermore, theconcept of size should respect disjointness. That is, if A1, A2, · · · are pairwisedisjoint then their individual sizes should add up to the size attached to theirunion ∪iAi.

Around 1930 A. N. Kolmogorov realized that all of the above requirements werepart and parcel of the then newly discovered Lebesgue measure and integrationtheory. His 1933 book on the foundations of probability theory detailing this isnow a classic. Let us collect and freeze these notions for our future use.

Definition - 1.2.1 - (Probability space) A probability space (Ω, E , P ) consistsof the following items.

• Ω = The set of all possible outcomes of an experiment, also called thesample space.

• E = The set of all subsets of Ω for which a (probability) function (measure)P can be defined. Each member of E is called an event (or a measurable set).

The collection of all events, E , must obey the conditions

• (i) Ω ∈ E ,• (ii) if A ∈ E then Ac ∈ E ,• (iii) if A1, A2, · · · ∈ E then ∪iAi ∈ E .

Any collection of subsets of the space, Ω, that obeys the above conditions, is calleda sigma field. The probability measure, P, is a real valued function over E , withthe following requirements:

• (i) P(Ω) = 1,

• (ii) 0 ≤ P(A) ≤ 1, for any A ∈ E ,• (iii) if A1, A2, · · · ∈ E are disjoint then P(∪iAi) =

∑i P(Ai).

10 Modeling Distributions

The last property of P is called the (disjoint) countable additivity.

Any function X : Ω → R having the property that X−1((a, b]) ∈ E for alla < b, is called a random variable (or measurable function). Every such X has acumulative distribution associated with it, denoted as F (t) or FX(t). It is obtainedby

F (t) = P(X−1((−∞, t])) = P(X ≤ t), t ∈ R.

Remark - 1.2.1 - Note that the definition of P is tied to the collection of events(sigma field). Condition (i) of the definition of a sigma field is needed for Condition(i) of the definition of P to avoid logical inconsistencies. The same is the case withthe third conditions of the two concepts.

Exercise - 1.2.1 - Let (Ω, E , P) be a probability space for a random experiment.Show that P satisfies the following properties for any A,B ∈ E :

(i) P(∅) = 0,(ii) P(Ac) = 1− P(A),(iii) P(Ac ∩ B) = P(B)− P(A ∩B),(iv) P(A ∪B) = P(A) + P(B)− P(A ∩ B),(v) if A ⊆ B, then P(A) ≤ P(B).

Lecture 2

Probability Spaces &

Random Variables

Remark - 2.0.2 - (Is P a continuous function?) The ususual notio of continuitydoes not apply to the function P since its domain has not been given any topologicalstructure. The problem is that we cannot talk about limn→∞ An for an arbitrarysequence of sets (events) in E. For some special sequences of sets “convergence ofsets” can be defined. When A1 ⊆ A2 ⊆ · · · , then we define limn→∞ An =

⋃∞n=1 An.

Similarly, if A1 ⊇ A2 ⊇ · · · , then limn→∞ An =⋂∞

n=1 An. A question arises, “forsuch sets is P continuous in the sense that

P( limn→∞

An) = limn→∞

P(An)?

Here is a result that answers this question.

Theorem - 2.0.1 - (The continuity property of P) If An, n ≥ 1 and Bn, n ≥1 are sequences of events such that A1 ⊆ A2 ⊆ · · · and B1 ⊇ B2 ⊇ · · · , then

(i) limn→∞

P(An) = P

(lim

n→∞An

), and (ii) lim

n→∞P(Bn) = P

(lim

n→∞Bn

).

Proof: Note that limn→∞

An = ∪∞n=1An = A1 ∪ (A2 − A1) ∪ (A3 − A2) ∪ · · · , where

the unions on the right side are disjoint. Thus,

P

( ∞⋃

n=1

An

)= P(A1) + P(A2 − A1) + P(A3 −A2) + · · ·

= P(A1) + limn→∞

n−1∑

i=1

(P(Ai+1 − Ai))

= P(A1) + limn→∞

n−1∑

i=1

(P(Ai+1)− P(Ai))

= P(A1) + limn→∞

P(An)− P(A1).

12 Probability Spaces & Random Variables

The reader should prove part (ii) (cf. Exercise (2.0.2)). ♠As we saw above, a monotone sequence of sets has a limit. In general, if

A1, A2, · · · is any sequence of sets, the new sequence B1 = ∪k≥1Ak, B2 = ∪k≥2Ak,· · · , Bn = ∪k≥nAk, for n = 1, 2, · · · becomes monotone. That is, B1 ⊇ B2 ⊇ B3 ⊇· · · . Hence, the sequence, B1, B2, · · · has a limit, which is called the lim supn An

and stands for

lim supn

An := limn→∞

Bn = ∩∞n=1Bn = ∩∞n=1 ∪k≥n Ak.

Similarly, the new sequence Cn = ∩k≥nAk is a monotone sequence since C1 ⊆ C2 ⊆· · · . It also has a limit, called the lim infn An and stands for

lim infn

An = limn→∞

Cn = ∪∞n=1Cn = ∪∞n=1 ∩k≥n Ak.

Since Cn ⊆ Bn for every n, their respective limits also share the same relationship,namely lim infn An ⊆ lim supn An. Note that the definition of E ensures that bothlim infn An and lim supn An are in E whenever all An are in E .

In probability literature, the event ∪iAi is often read as “at least one of the

Ai occurs”. And similarly, the event ∩iAi is often read as “every one of the Ai

occurs”. Continuing this further, the event lim supn An stands for “infinitely many

of the Ai occur” and lim infn An stands for “all but finitely many of the Ai occur”.The reader should try to see why this interpretation is justified. Here is anotherconsequence of the definition of probability function.

Theorem - 2.0.2 - (The first Borel-Cantelli lemma) Let A1, A2, ... be a se-quence of events. If

∑n P(An) <∞ then P(lim supn An) = 0.

Proof: Note that if Bn =⋃

k≥n Ak then B1 ⊇ B2 ⊇ · · · . Thus, by the continuityproperty of P,

0 ≤ P

(lim sup

nAn

)= lim

nP (Bn) = lim

nP

⋃

k≥n

Ak

.

By the subadditivity property of P, we get P

⋃

k≥n

Ak

≤∑

k≥n

P (Ak). Since, the

tail of a convergent series goes to zero,

0 ≤ P

(lim sup

nAn

)= lim

nP

⋃

k≥n

Ak

≤ limn

∑

k≥n

P (Ak) = 0. ♠

Remark - 2.0.3 - (Inclusion-exclusion principle) It is a natural question toask, “can one find the probability of union of events when one knows only the

probabilities of the individual events?” The answer is yes, provided probabilities of

Probability Spaces & Random Variables 13

their intersections are known, and is called the inclusion-exclusion principle and isdue to H. Poincare.)

P

(n⋃

i=1

Ai

)

=n∑

i=1

P (Ai)−∑

i<j

P (Ai ∩Aj) +∑

i<j<k

P (Ai ∩Aj ∩Ak)

+ · · · + (−1)n+1P

(n⋂

i=1

Ai

)

= B1 −B2 + B3 − · · ·+ (−1)n+1Bn,

where, Bj =∑

1≤i1<i2<···<ij≤n

P (Ai1 ∩ Ai2 ∩ · · · ∩ Aij); j = 1, 2, · · · , n.

Therefore, P (Ac1 ∩ Ac

2 ∩ · · · ∩Acn) = 1− P (A1 ∪A2 ∪ · · · ∪An)

= 1−n∑

j=1

(−1)j−1Bj

=n∑

j=0

(−1)jBj where B0 = 1,

and it represents the probability of none of the Ai’s occurring. This is a specialcase of a yet more general result due to Jordan who proved it in 1927. It says that

P (exactly k events among A1, · · ·An will occur) =n∑

j=k

(−1)j−k

(j

k

)Bj ,

which reduces to the result of Poincare for k = 0. Both of these results can beproved by induction and are left for the reader as exercises.

Remark - 2.0.4 - (Various assignment methods) How should one define thefunction P : E → [0, 1] so that the three requirements of its defintion are fulfilledand at the same time is realistic? The word “realistic” points towards our desirethat it should be applicable in various real life situations. This is a modelingissue. Typically any one of the following four techniques is invoked due to variousreasonings:

• (Counting method). When Ω has only finitely many members we take E tobe the power set of Ω. Now if one can justify that each member should havethe same chance assigned to it then, by the third requirement of probabilityfunction, we get

P(A) =number of elements of A

number of elements of Ω.

In this case (Ω, E , P) is called an equilikely probability space. It

• (Lengths/areas/volumes method). When Ω is too large, such as aninterval or a subset of the plane or Rk, even when one may be able to justify

14 Probability Spaces & Random Variables

that the outcomes should show no preference, the above counting methodbreaks down. Its natural analog then becomes

P(A) =size of A

size of Ω,

where the “size” is taken to mean the length in case Ω is a bounded subsetof R, or area or volume for Rk when k > 1. In this case, typically E is takento be the smallest sigma field containg the bounded rectangles, called theBorel sigma field (cf. Exercise (2.0.6)).

• (Weighted versions). A large class of probability models come in weightedform of the above two items. In the following several standard models of prob-ability and statistics of this sort are listed. Such models are often justifiedbased either on analytic derivations or preponderence of empirical evidence.

• (Independence). Another distinct modeling technique that sets probabilitytheory apart from other disciplines is the modeling tool of independence. Wewill briefly describe this concept a bit later.

Example - 2.0.1 - (Secretary’s matching problem — equilikely probabil-ity space) Here we illustrate the use of the inclusion-exclusion principle applied to aparticular equilikely probability space and solve the secretary’s matching problem.A secretary types n letters addressed to n different people. Then he types n en-velopes with the same n addresses. However, while putting the letters into theenvelopes, he randomly puts letters into the envelopes. (This word “random” herestands for no preference to any particular letter going any particular envelope.This then can be interpreted to mean that the resulting probability space is equi-likely.) We would like to know the probability that at least one of the lettersis correctly put into its own envelope.1 Let Ai be the event that letter i goesinto its own envelope (1 ≤ i ≤ n) (i.e., a match occurs for the ith letter). Wewant the probability of at least one of the Ai’s occur, i.e., P (∪n

i=1Ai). To findout P(Ai), P(Ai ∩ Aj), P(Ai ∩ Aj ∩ Ak), , i 6= j 6= k, etc., we proceed as follows.There are n! ways to place the letters into the n envelopes. Therefore, we see that,

P(Ai) = (n−1)!n! = 1

n , i = 1, 2, · · · , n. Similarly, P(Ai ∩ Aj) = (n−2)!n! = 1

n(n−1) and

P(Ai ∩ Aj ∩Ak) = 1n(n−1)(n−2) , etc. So, by the result of Poincare,

P

(n⋃

i=1

Ai

)

=

n∑

i=1

1

n−∑

i<j

1

n(n− 1)+∑

i<j<k

1

n(n− 1)(n− 2)+ · · ·

= 1−(

n2

)

n(n− 1)+

(n3

)

n(n− 1)(n− 2)+ · · ·+ (−1)n+1

(nn

)

n!

= 1− 1

2!+

1

3!− · · ·+ (−1)n+1 1

n!=

n∑

j=1

(−1)j+1 1

j!.

1B. D. Choi gives a generalization of the matching problem in which we only select asubset of the recipients and see how many of them got the correct letters. For this, see hispaper “Limiting distribution for the generalized matching problem”, (1987), The Amer.

Math. Monthly, vol. 94, no. 4, pp. 356-360.

Probability Spaces & Random Variables 15

Example - 2.0.2 - (Random selection) Pick a point “at random” from (0, 2π].What does this mean? Well, it might be painful to construct an experiment whichwill do just that. At least approximately it can be performed with the help ofa spinner which does not have any preferential stopping spots. Mathematicallyspeaking it stands for the following probability space.

• Ω = (0, 2π]

• E is the smallest sigma field of subsets of (0, 2π] which contains all the inter-vals of (0, 2π]. We will call it the Borel sigma field, over (0, 2π].

• P((a, b]) = b−a2π−0 for any 0 ≤ a < b ≤ 2π.

Note that the actual act of selection of a point from the interval (0, 2π], or as tohow does one physically perform this operation, are none of our concerns. This isan idealization and the phrase “selection of a point at random” points towards thismathematical model (abstraction) of the physical act. The resulting cumulativedistribution is

F (t) =

0 if t ≤ 0,t

2π if 0 < t < 2π,1 if t ≥ 2π.

Exercise - 2.0.2 - Finish the proof of part (ii) of Theorem (2.0.1).

Exercise - 2.0.3 - By using induction, prove the result of Poincare.

Exercise - 2.0.4 - (Continuity property of P revisited) Show that for anysequence of events An, n ≥ 1, we have

P (lim infn

An) ≤ lim infn

P (An) ≤ lim supn

P (An) ≤ P (lim supn

An).

Hence, deduce that if lim infn An = lim supn An =: limn An, then P (limn An) =limn P (An), giving a slight extension of the continuity property of P.

Exercise - 2.0.5 - (Intersection of sigma fields is a sigma field) Let Ω be anonempty set and let Gα, α ∈ Λ be any nonempty collection of sigma fields ofsubsets of Ω. Show that F = ∩α∈ΛGα is again a sigma field.

Exercise - 2.0.6 - (Smallest sigma field containing a class) Let Ω be a nonemptyset and let A be a collection of of subsets of Ω. (Note that A need not have anyproperties.) Show that FA = ∩G⊃AG is again a sigma field, where the intersectionis over all sigma fields G that contain A. [Example: On R the smallest sigma fieldcontaining the collection of all intervals is called the Borel sigma field.]

Exercise - 2.0.7 - (Generated sigma field) The collection,

σ(X) :=X−1(B) : B ∈ B

,

is always a sigma field (as can be verified easily), and is called the sigma fieldgenerated by X. So, a real valued function, X, over Ω, is a random variable forthe probability space (Ω, E , P) if and only if σ(X) ⊆ E . Verify that σ(X) is a sigmafield when X is any real valued function on Ω.

16 Probability Spaces & Random Variables

Remark - 2.0.5 - (Whats observable?) The actual elements of Ω may or maynot be observable. Even worse is that the probability of events, P(A), is NEVERobservable. Often the observables are the values of certain random variables thatturn up as a result of performing the experiment.

• Probabilists propose models for the unknown (unobservable) probability func-tion P and then, using those models, deduce results by knowing some partialinformation concerning the experiment or without performing the randomexperiment at all. The results are only as good as the models.

• Statisticians test the validity of the proposed models for P after perform-ing the experiment a large number of times and observing certain randomvariables (called data analysis and statistical inference).

Every random variable has its own (unique) distribution function (or distribu-tion, for short). All the probabilistic properties of the random variable are storedin its distribution. Probability theory essentially is the study of these distributionalproperties.

Definition - 2.0.2 - (Multivariate distribution) Let X be a d-dimensional ran-dom vector (i.e, d number of random variables, X1,X2, · · · ,Xd, all defined over thesame probability space (Ω, E , P)). The multivariate (or joint) distribution of X isa function,

F (x1, x2, · · · , xd) = P(X ≤ x) = P

X1

X2

...Xd

≤

x1

x2

...xd

, x ∈ Rd,

= P(X1 ≤ x1, X2 ≤ x2, · · · , Xn ≤ xn).

Here the inequality between vectors means componentwise inequalities must holdfor all the components, and the commas separating the events, Xi ≤ xi, standfor the intersection operations.

Distributions are nonnegative, right continuous functions, (in each variable)which may or may not be differentiable. Even more, some distributions may havejumps, but the points of jump can always be counted (i.e., is a countable set). Fora distribution, F , of one random variable, a point x is a point of jump of F if

P(X = x) = F (x)− F (x−) > 0.

For a distribution, F , of two random variables, a point (x1, x2) is a point of jumpof F if

P(X1 = x1, X2 = x2) = F (x1, x2)− F (x−1 , x2)− F (x1, x

−2 ) + F (x−

1 , x−2 ) > 0.

Most of the commonly used distributions fall into two categories: The differentiablekind, which are (strangely) given the name “continuous”, and the jump type, whichare given the name “discrete”. However, there are other types of distributions whichdo not fit into these two categories.

Probability Spaces & Random Variables 17

Definition - 2.0.3 - (Continuous case) The (joint) density, of a random vectorwith (joint) distribution F , when it exists, is a nonnegative function

f(x) =∂d

∂x1 · · · ∂xdF (x), with

∫

Rd

f(x) dx = 1.

In this case, for any (Borel) subset B of Rd, we take P(X ∈ B) =∫

B f(x) dx.

(Discrete case) The joint (discrete) density, of a random vector with (joint)distribution F , when it exists, is a nonnegative function , f , with a countable subsetD ⊆ Rd, so that

f(x) = P(X = x) > 0, x ∈ D, with∑

all x∈D

f(x) = 1.

Remark - 2.0.6 - (Notation) X ∼ F or X ∼ f . The actual probability space(Ω, E , P), over which X is defined, is often suppresed once the distribution F (orthe density f) is obtained. One may safely assume that there is some probabilityspace from where the specified random variable with its distribution, came from.This observation was proved by Kolmogorov. Hence, X,F and f are related as

P(X ≤ t) = F (t), f(x) =

ddxF (x), continuous case,

F (x)− F (x−), discrete case.

Example - 2.0.3 - Here are some commonly used (discrete and continuous) modelsfor distributions (actually densities) of random variables.

• (Normal). X ∼ N(µ, σ2) stands for X having the density

f(x) =1

σ√

2πe−(x−µ)2/(2σ2), −∞ < x <∞.

The parameters, µ, σ > 0, control the shape of the density.

• (Lognormal). X ∼ LN(µ, σ2) stands for X having the density

f(x) =1

xσ√

2πe−(ln x−µ)2/(2σ2), x > 0.

The parameters, µ, σ > 0, control the shape of the density.

• (Chi square). X ∼ χ2(k) stands for X having the density

f(x) =1

2k/2Γ(k2 )

xk2−1e−x/2, 0 < x <∞.

Here the single parameter, k > 0, called the degree of freedom, controls theshape of the density. By the way,

Γ( 12) =

√π, Γ(1) = Γ(2) = 1, Γ(x + 1) = xΓ(x), x > 1. (0.1)

18 Probability Spaces & Random Variables

• (Exponential). X ∼ Exp(λ) stands for X having the density

f(x) = λe−λx, x > 0.

Here λ > 0, is the parameter of the density.

• (Gamma). X ∼ Gamma(λ, α) (also sometimes denoted as X ∼ G(λ, α))stands for X having the density

f(x) =λα

Γ(α)xα−1 e−λx, x > 0.

Here λ, α > 0, are the parameters of the density. When α = 1 we get theexponential density as a special case. If we take λ = 1

2 and α = k2 , we get

the chi square density with k degrees of freedom.

• (Multivariate normal). X ∼ N(µ,V) stands for the X = [X1, · · · ,Xd]′

having the (joint) density

f(x) =1

(2π)d/2√

det(V)exp

−1

2(x− µ)′V−1(x− µ)

; x ∈ Rd.

Actually, a multivariate normal random variable is defined through its mo-ment generating function (mgf) since it uses V only, even when V is notinvertible. The vector µ = [µ1, · · · , µd]

′ controls the center of the densityand the d × d positive-definite matrix, V, controls the spread and shape ofthe density.

• (Binomial). X ∼ B(n, p) stands for X having the (discrete) density,

f(x) =

(n

x

)px(1− p)n−x, x = 0, 1, 2, · · · , n.

• (Poisson). X ∼ Poisson(λ) represents a random variable whose (discrete)density is

f(x) = e−λ λx

x!, x = 0, 1, 2, · · · .

• (Geometric). X ∼ Geometric(p) represents a random variable whose (dis-crete) density is

f(x) = p (1− p)x, x = 0, 1, 2, · · · .

Definition - 2.0.4 - (Independence) Two events, A,B, are called independent if

P(A ∩ B) = P(A)P(B).

This is a distinguishing concept of probability theory. The early literature of prob-ability theory heavily relied on it. Much of the modern probability theory evolvedwhile proving old results that assumed this structure by trying relaxing it as muchas possible.

Probability Spaces & Random Variables 19

Definition - 2.0.5 - (Independence of events) A (finite or infinite) sequence ofevents, A1, A2, · · · is called independent if for any finite subset of them their jointprobability is the product of the individual probabilities. That is

P(∩i∈JAi) =∏

i∈J

P(Ai),

for any finite subset J of positive integers.

Theorem - 2.0.3 - (2nd Borel-Cantelli lemma) If A1, A2, · · · are independent

events such that∞∑

n=1

P(An) =∞, then P

(lim sup

nAn

)= 1.

Proof: By the continuity property of P, we have

P

(lim sup

nAn

)= P

⋂

k≥1

⋃

n≥k

An

= limk→∞

P

⋃

n≥k

An

, and,

P

⋃

n≥k

An

= limm→∞

P

(m⋃

n=k

An

)

.

Now, the independence of events gives that

P

(m⋃

n=k

An

)

= 1− P

(m⋂

n=k

Acn

)

= 1−m∏

n=k

(1− P(An))

= 1− exp

m∑

n=k

ln(1− P(An))

.

Here, if P(An) = 1, then the equality remains valid if we agree to take ln 0 = −∞.

By the Taylor series∑∞

k=1xk

k = − ln(1− x), we see that

ln (1− P(An)) = −(

P(An) +(P(An))2

2+ · · ·

)

≤ −P(An).

This inequality remains valid when P(An) = 1 since ln 0 = −∞ < −1. Thus,m∑

n=k

ln (1− P(An)) ≤ −m∑

n=k

P(An). This implies that

0 ≤ limm→∞

exp

m∑

n=k

ln (1− P(An))

≤ limm→∞

exp

−m∑

n=k

P(An)

= 0.

This gives that

P

⋃

n≥k

An

= limm→∞

(1− exp

m∑

n=k

ln (1− P(An))

)= 1.

Since this is true for all k, P (lim supn An) = 1. ♠

20 Probability Spaces & Random Variables

Remark - 2.0.7 - (Zero-one property) When A1, A2, · · · is a sequence of in-dependent random variables the two Borel-Cantelli lemmas together show thatP(lim supn An) is always either 0 or 1. It cannot have any other value. This fact isa special case of a more general result, known as Kolmogorov’s zero-one law.

Definition - 2.0.6 - (Independence of random variables) When the distribu-tion of X = [X1, · · · ,Xd]

′ can be written as a product, i.e.,

F (x) = P(X ≤ x) = P

X1

X2

...Xd

≤

x1

x2

...xd

=

d∏

i=1

P(Xi ≤ xi); x ∈ Rd,

we say that X1,X2, · · · ,Xd are mutually independent (or just independent). Iffor every pair, (Xi,Xj), i 6= j, the two random variables are independent thenX1,X2, · · · ,Xd are called pairwise independent. The single word “independent”will always refer to mutual independence.

Remark - 2.0.8 - (The iid notation & the notion of random sample) The

notation X1,X2, · · · ,Xdiid∼ stands for the case when

F (x) = P(X ≤ x) = P

X1

X2

...Xd

≤

x1

x2

...xd

=

d∏

i=1

P(X1 ≤ xi), x ∈ Rd.

If we denote the common function P(X1 ≤ t) by G(t), then the above iid notation

takes the form X1,X2, · · · ,Xdiid∼ G, or G is replaced by the name given to G. In

this case the collection X1,X2, · · · ,Xd is called a random sample from G, and Gis called the population distribution.

Example - 2.0.4 - Recall that N(0, 1) is the name given to the standard normal

distribution. So, the notation, X1,X2, · · · ,Xdiid∼ N(0, 1), uses the (common) dis-

tribution function

G(t) = P(X1 ≤ t) =1√2π

∫ t

−∞e−u2/2du, with density f(u) =

e−u2/2

√2π

, u ∈ R.

Remark - 2.0.9 - (Independence of events, & sigma fields) For a probabilityspace (Ω, E , P), two events, A,B ∈ E , are independent if P(A ∩ B) = P(A)P(B).Extending this idea, if F ,G are subsigma fields of E , then F ,G are called indepen-dent if for any A ∈ F , and any B ∈ G, we have P(A ∩ B) = P(A)P(B). Using thisnotion of independence of sigma fields, it turns out that two random variables X,Yare independent if and only if their respectively generated sigma fields, σ(X), σ(Y )are independent. For the most part we will not work at this generality.

Exercise - 2.0.8 - When X ∼ N(0, 1), by rewriting P(X2 ≤ t) as P(−√

t ≤ X ≤√t) and then differentiating with respect to t, show that Y = X2 ∼ χ2

(1).

Lecture 3

Expectations

The concept of an average or a mean of values of h(X), when X is a random variableand h is a function of interest, is captured by the Lebesgue integral. We present abrief heuristic argument here along with collecting its basic properties that we willneed.

We illustrate the basic idea with the help of the distribution FX of any randomvariable X defined over some probability space (Ω, E , P). The Riemann-Stieltjes in-

tegral∫ b

a h(t) dFX(t) partitions the x-axis using intervals, while Lebesgue’s methodof integration, instead partitions the y-axis using intervals. Then the two methodsperform distinctly different actions. When (xi−1, xi] is one of the partitioning in-tervals, the Riemann-Stieltjes integral measures its size by using the distributionas FX(xi) − FX(xi−1). Furthermore it uses an arbitrary point ai ∈ [xi−1, xi] andevaluates h(ai) to create the Riemann-Stieltjes sum

R(h, FX ,P) =

n∑

i=1

h(ai) (FX(xi)− FX(xi−1)) =

n∑

i=1

h(ai) P(xi−1 < X ≤ xi).

Instead Lebesgue suggested partitioning the y-axis into intervals and constructingthe integral for nonnegative functions first. If J is one of such partitioning intervalson the y-axis, the inverse image need not be a nice interval at all. Nor do we needit to be an interval to measure its size! All we want is to find the probability ofthe inverse set, A, which is given by the relationship P(A) = P(h(X) ∈ J). So,let A1, A2, · · · , An be such inverse sets for intervals J1 := (0, y1], J2 = (y1, y2], · · · ,Jn := (yn,∞) and take y0 = 0. For some choice of ai ∈ Ai, when h is nonnegativeand bounded, we create the Lebesgue sum as

n∑

i=1

h(ai) P(X ∈ Ai) =n∑

i=1

h(ai) P(h(X) ∈ Ji) =n∑

i=1

h(ai) P(yi−1 < h(X) ≤ yi).

When the partition of the y-axis is made finer and if the resulting limit exists we callthe limit as the Lebesgue integral. The left side’s limit appropriately is denoted as∫Ω h(X) dP while the right side is denoted as

∫R

h(t) dFX (t). But the two integralsare the same. The general case is then handled by writing h(t) = h+(t)−h−(t), the

22 Expectations

difference of positive and negative parts of h. This not only gives us the change ofvariables formula, but more importantly, this way we are able to construct integralsover abstract probability spaces. Using this inegral, we define the expectation (ormean) of a random variable X to be

E(X) =

∫

Ω

X dP =

∫

R

t dFX(t), whenever E|X| =∫

Ω

|X| dP <∞.

Higher order moments are defined by using h(X) = Xk, by using positive integersfor k. In particular, the variability of a distribution is captured by

V ar(X) = E(X2)− (E(X))2, Std(X) =√

V ar(X),

called the variance and standard deviation respectively.

3.1 Properties of Lebesgue integral

Ignoring some technical details the resulting integral has the usual properties:

• (Linearity) E(ah(X) + bg(X) + c) = aE(h(X)) + bE(g(X)) + c for anyconstants a, b, c. The multivariate extensions go along the same lines. Forinstance, for two random variables, X,Y ,

E(ah(X,Y ) + bg(X,Y ) + c) = aE(h(X,Y )) + bE(g(X,Y )) + c.

• (Positivity) If h1(t, s) ≥ h2(t, s) then E(h1(X,Y )) ≥ E(h2(X,Y )), and

|E(h(X,Y ))| ≤ E|h(X,Y )|.

• (Change of variable formula CVF) If Z = h(X,Y ) with distributionFY (t) then

E(Z) =

∫

Ω

Z dP =

∫

R

t dFZ(t) =

∫

R2

h(x, y) dFX,Y (x, y).

In particular, E(Xn) is called the n-th moment of X.

• (Integration by parts) When F,G are nondecreasing right continuous,∫

[a,b]

F (x) dG(x) +

∫

[a,b]

G(x−) dF (x) = F (b)G(b) − F (a−)G(a−).

• (Fatou’s lemma) For any sequence of nonnegative rvs, Xn, n ≥ 1,

E

(lim inf

nXn

)=

∫

Ω

lim infn

Xn dP ≤ lim infn

∫

Ω

Xn dP = lim infn

E(Xn).

• (Monotone convergence theorem) If 0 ≤ Xn(ω) ≤ Xn+1(ω) → X(ω)and E(X) <∞ then

E(X) =

∫

Ω

X dP = limn

∫

Ω

Xn dP = limn

E(Xn).

3.2 Covariance 23

• (Lebesgue dominated convergence theorem) If Xn(ω) → X(ω) and|Xn| ≤ Y for some random variable Y with E(Y ) <∞ then

E(X) =

∫

Ω

X dP = limn

∫

Ω

Xn dP = limn

E(Xn).

• (Fubini-Tonelli’s theorem) If F,G are distributions of X,Y respectively,then Tonelli’s theorem says that

∫

R

∫

R

|h(x, y)| dF (x) dG(y) =

∫

R

∫

R

|h(x, y)| dG(y) dF (x).

Fubini’s theorem says that if either side of above equation is finite then theabove interchange of integrals can be performed without the absolute valuesaround h(x, y) as well.

The integral has some further properties which we will mention as they are needed.

Example - 3.1.1 - When X ≥ 0 with distribution F (x) and E|X| < ∞, Tonelli’stheorem gives

E(X) =

∫

Ω

X dP =

∫

Ω

∫ X

0

1dx dP =

∫ ∞

0

∫

ω:X(ω)>x1dP dx =

∫ ∞

0

(1−F (x)) dx.

3.2 Covariance

Definition - 3.2.1 - (Variance-covariance matrix) If E(|X1|2 + · · · + |Xd|2) isfinite, the variance-covariance matrix of the random vector X = [X1,X2, · · · ,Xd]

′

is

V = E

X1

...Xd

[X1 · · ·Xd]

−

EX1

...EXd

[EX1 · · ·EXd]

=

V ar(X1) Cov(Xi,Xj)

. . .

Cov(Xi,Xj) V ar(Xd)

,

where V ar(Xi) = EX2i − (EXi)

2, and Cov(Xi,Xj) = E(XiXj) − (EXi)(EXj).

We take the correlation Corr(X,Y ) = Cov(X,Y )/√

V ar(X)V ar(Y ) wheneverthe variances are finite.

Remark - 3.2.1 - (Hoeffding formula) There is an old result of Wassily Hoeffding(1914-1991), that he proved1 in 1940, which says that

Cov(X,Y ) =

∫ ∞

−∞

∫ ∞

−∞(H(x, y)− F (x)G(y)) dx dy,

1Hoeffding, Wassily (1940), “Masstabinvariante Korrelationstheorie”. Schriften des

Math. Instituts und des Instituts hir Angewandte Mathematik der Universitat Berlin 5,pp. 179-233.

24 Expectations

for any bivariate distribution, H, as long as the variances of the random variablesexist and F and G were the marginal distributions of H”. Note that this approachdoes not need the joint density to compute the covariance.

Note from the definition that the covariance obeys the following properties,known as the symmetry and blinearity properties:

• (i) Cov(X,Y ) = Cov(Y,X),

• (ii) Cov(cX, Y ) = Cov(X, cY ) = cCov(X,Y ), for any constant c,

• (iii) Cov(X1 + X2, Y ) = Cov(X1, Y ) + Cov(X2, Y ),

• (iii) Cov(c, Y ) = 0, for any constant c.

In particular, V ar(X) = Cov(X,X) when E(X2) <∞. We say that X and Y areuncorrelated if Cov(X,Y ) = 0. Next, we turn our attention towards inequalities.

Proposition - 3.2.1 - (Existence of moments) Let h : [0,∞)→ R be a strictlyincreasing continuous function. Then for any nonnegative random variable X wehave

∞∑

n=1

P(X ≥ h(n)) ≤∫

S

h−1 X(s) dP =

∫

R

h−1(t) dFX(t)

= E(h−1(X)

)≤

∞∑

n=0

P(X ≥ h(n)).

Proof: Just note that

∞∑

n=1

P (X ≥ h(n)) =

∞∑

n=1

P (h−1(X) ≥ n) =

∞∑

n=1

∞∑

i=n

P (i ≤ h−1(X) < i + 1)

=

∞∑

i=1

i∑

n=1

P (i ≤ h−1(X) < i + 1)

=

∞∑

i=1

iP (i ≤ h−1(X) < i + 1).

Use the notation Ai = i ≤ h−1(X) < i + 1, for i = 0, 1, 2, · · · . Then Ai aredisjoint events with ∪iAi = S. Therefore,

∞∑

n=1

P (X ≥ h(n)) =∞∑

i=1

iP (Ai) =∞∑

i=1

∫

Ai

i dP ≤∞∑

i=1

∫

Ai

h−1(X(s)) dP (s)

≤∞∑

i=0

∫

Ai

h−1(X(s)) dP (s)

=

∫

S

h−1(X(s)) dP (s), completing half of the proof,

3.2 Covariance 25

=

∞∑

i=0

∫

Ai

h−1(X(s)) dP (s)

≤∞∑

i=0

∫

Ai

(i + 1) dP (s) =

∞∑

i=0

(i + 1)P (Ai)

=

∞∑

i=0

i∑

n=0

P (i ≤ h−1(X) < i + 1)

=

∞∑

n=0

∞∑

i=n

P (i ≤ h−1(X) < i + 1)

=

∞∑

n=0

P (h−1(X) ≥ n) =

∞∑

n=0

P (X ≥ h(n)).

This finishes the proof. ♠

Example - 3.2.1 - If X ∼ N(0, σ2) and Y = X2, then E(X) = 0 and E(Y ) =E(X2) = σ2. Here are the justifications.

E(X) =1

σ√

2π

∫ ∞

−∞u e−u2/(2σ2) du = 0,

since the integrand is an odd function. Next,

E(Y ) = E(X2) =1

σ√

2π

∫ ∞

−∞u2e−u2/(2σ2) du

=2

σ√

2π

∫ ∞

0

u2e−u2/(2σ2) du, intengrand is an even function,

=σ2

√2π

∫ ∞

0

t1/2 e−t/2 dt, by substituting t = u2/σ2,

=σ2

√2π

23/2Γ( 32 ), since total area under χ2

(3) density is one,

= σ2, by (0.1).

26 Expectations

Lecture 4

Various Inequalities

A useful inequality involving a random variable is due to Jensen. It says that if fis a convex function over an interval and a random variable X takes values in thatinterval, then

E(f(X)) ≥ f(E(X)),

when the expectation on the left side exists. In particular, by taking f(t) = t2, weget

E(X2)≥ (E(|X|))2 .

This implies that V ar(X) ≥ 0.Let X be a random variable with variance σ2. Chebyshev’s inequality says that

P (|X − E(X)| > ε) ≤ σ2

ε2, for any ε > 0.

This is a bit crude inequality and surprisingly pervasive in probability theory andanalysis. Here we collect some of the standard inequalities from analysis.

Exercise - 4.0.1 - For any p > 0, show that the following statements are equivalent.

• (i) E|Y |p <∞,

• (ii)∑∞

n=1 P (|Y |p ≥ n) <∞,

• (iii)∫[0,∞) P (|Y |p ≥ t) dt <∞,

• (iv)∑∞

n=1 np−1P (|Y | ≥ n) <∞.

Then show that

E(|Y |p) = p

∫ ∞

0

tp−1P (|Y | > t) dt = p

∫ ∞

0

tp−1P (|Y | ≥ t) dt.

Example - 4.0.2 - (AM-GM inequality) The arithmetic mean µ of n numbers,

a1, a2, · · · an, is µ =a1 + a2 + · · ·+ an

n. If these numbers are positive, their geomet-

ric mean is

µ = antiloge

log a1 + log a2 + · · ·+ log an

n

=

(n∏

i=1

ai

) 1n

.

28 Various Inequalities

The AM-GM inequality says that µ ≥ µ. To prove this, define a random variableX ∈ ∆ = a1, a2, · · · , an with equal probabilities assigned to the elements of ∆(the set ∆ contains the given positive numbers and repetitions are allowed). Then,it is obvious to see that E(X) = µ. Also, by CVF, we have

Elog(X) =log a1 + log a2 + · · ·+ log an

n= logµ.

Since − log x is a convex function, Jensen’s inequality gives

− logµ = − logE(X) ≤ −Elog(X) = − logµ.

Multiplying both sides by −1 and then taking the antilogs give µ ≥ µ.

Exercise - 4.0.2 - (AGH inequality) Let a, b be two positive numbers. The

quantity

((1/a) + (1/b)

2

)−1

is called the harmonic mean of the two numbers. Use

the AM-GM inequality to prove the following AGH inequality:

Arithmetic Mean ≥ Geometric Mean ≥ Harmonic Mean.

4.1 Holder & Minkowski’s Inequalities

An extension of the CBS inequality is known as the Holder inequality. For this weneed an extended version of the AM-GM inequality — known as Young’s inequality.

Proposition - 4.1.1 - (Young’s inequality) Let X ∈ ∆ = a, b with densityf(a) = p, f(b) = 1− p, where 0 < p < 1 and a, b ≥ 0. Then

ap + b(1− p) = E(X) ≥ ap · b1−p,

where the equality holds if and only if a = b. (For p = 12 this reduces to the AM-GM

inequality.)

Proof: Look at the inequality backwards. We need to show that

ap + b(1− p) ≥(a

b

)p

b, assuming that b 6= 0.

(The inequality is trivially true when either a = 0 or b = 0.) So, we need to prove

thata

bp + (1− p) ≥

(a

b

)p

or equivalently,

f(t) = −tp + tp + (1− p) ≥ 0, for all t > 0.

The minimum of this function can be obtained with brute force, and we leave it forthe reader. Instead, there is an easier way. Define a random variable U that takestwo values, a

b and 1, with respective probabilities, p and (1 − p). Now apply theAM-GM inequality to get

a

bp + (1− p) = µ ≥ µ =

(a

b

)p

. ♠

4.1 Holder & Minkowski’s Inequalities 29

Proposition - 4.1.2 - (Holder’s inequality)1 Let p, q be numbers such that p, q >1 and 1

p + 1q = 1. If X,Y are random variables with E(|X|p) <∞ and E(|Y |q) <∞

then

E|XY | ≤ (E|X|p) 1p · (E|Y |q) 1

q .

Equality holding if and only if α|X|p = β|Y |q for some constants α, β.

Proof: If E|X|p = 1 and E|Y |q = 1 then take a = |X|p and b = |Y |q and replacep by our 1

p in Young’s inequality2 to get

a

(1

p

)+ b

(1

q

)≥ a1/p b1/q or

( |X|pp

)+

( |Y |qq

)≥ |XY |.

Taking expectations of both sides we get

E|XY | ≤ 1

pE|X|p +

1

qE|X|q =

1

p+

1

q= 1 = (E|X|p)

1p (E|Y |q)

1q .

If E|X|p = 0 or if E|Y |q = 0 then one of the random variables is identically zeroand the inequality is trivially true. Otherwise, define

U :=X

(E|X|p)1p

, V :=Y

(E|Y |q)1q

.

This gives that E|U |p = 1 and E|V |q = 1 . Thus, we have

E|UV | ≤ 1 or E|XY | ≤ (E|X|p) 1p · (E|Y |q) 1

q . ♠

Exercise - 4.1.1 - Finish the proof of the above proposition by showing when theequality holds.

Proposition - 4.1.3 - (Minkowski’s inequality) Let X,Y be two random vari-ables with E|X|p <∞, and E|Y |p <∞. Then E|X + Y |p <∞ and

(E|X + Y |p) 1p ≤ (E|X|p) 1

p + (E|Y |p) 1p ; for any p ≥ 1.

Proof: The case of p = 1 is trivial, so assume that p > 1. The triangle inequality,|X + Y | ≤ |X|+ |Y |, gives that

|X + Y |p ≤ (|X|+ |Y |)p ≤ (2max|X|, |Y |)p

= 2p max|X|p, |Y |p ≤ 2p (|X|p + |Y |p) .

1In mathematics texts, the quantity (E|X|p)1/p is often represented as ||X||p and iscalled the p-norm of X.

2Note that 1−p of Young’s inequality is now 1/q of this proposition. That is either wework with p, 1−p where 0 < p < 1 as we did in Young’s inequality or we work with p > 1,q > 1 with 1

p+ 1

q= 1 as we do in this proposition. This is just using different notations.

30 Various Inequalities

This gives that E|X + Y |p < ∞. Since 1p + 1

q = 1, we have 1 + pq = p which gives

that p = (p − 1)q. Note E(|X + Y |p−1

)q= E(|X + Y |p) < ∞. Now apply the

Holder inequality to get

E|X + Y |p−1|X| ≤ (E|X|p)1p

(E(|X + Y |p−1

)q) 1q

.

Similarly, we get E|X + Y |p−1|Y | ≤ (E|Y |p) 1p (E|X + Y |p) 1

q . Now we put thesepieces together as follows.

E|X + Y |p = E(|X + Y |p−1|X + Y |

)

≤ E|X + Y |p−1|X|+ E|X + Y |p−1|Y |

≤ (E|X|p)1p (E|X + Y |p)

1q + (E|Y |p)

1p (E|X + Y |p)

1q

= (E|X + Y |p) 1q (E|X|p) 1

p + (E|Y |p) 1p .

Dividing by the first expression of the right hand side (and noting that 1p = 1− 1

q )

gives that (E|X + Y |p)1−1q ≤ (E|X|p)

1p + (E|Y |p)

1p . If E|X + Y |p = 0 then there

was nothing to prove in the first place. ♠

4.2 Jensen’s Inequality

Now explain the Jensen inequality in a bit more detail.

Definition - 4.2.1 - (Convex functions) Let f be a real valued function on aninterval (α, β). We say f is convex on (α, β) if, for any subinterval [a, b] ⊆ (α, β),the graph of f on [a, b] lies on or below the line segment connecting (a, f(a)) and(b, f(b)). This is equivalent to saying that

f(θa + (1− θ)b) ≤ θf(a) + (1− θ)f(b), (0 ≤ θ ≤ 1),

for all a, b ∈ (α, β), a < b.

HW1 Exercise - 4.2.1 - If φ is a convex function over (a, b) then show that φ is contin-uous.

Proposition - 4.2.1 - A function f defined over an interval (α, β) is convex if andonly if for every random variable, say Xn, taking values in (α, β) and having a finiterange a1, a2, · · · , an we have f(E(Xn)) ≤ Ef(Xn).

Proof: The only if part follows easily by taking n = 2. The if part is obtained byrepeated use of the definition and induction. We illustrate the induction argumentfor n = 3 only.

f(E(X)) = f(p1a1 + p2a2 + p3a3)

4.2 Jensen’s Inequality 31

= f

((1− p3)

p1a1 + p2a2

1− p3+ p3a3

)

≤ (1− p3)f

(p1

1− p3a1 +

p2

1− p3a2

)+ p3f(a3)

≤ (1− p3)

p1

1− p3f(a1) +

p2

1− p3f(a2)

+ p3f(a3)

= p1f(a1) + p2f(a2) + p3f(a3) = Ef(X).

The same argument goes for higher values of n. ♠

Proposition - 4.2.2 - Let f be a convex function over an interval I and let X bea random variable taking values in I with E|X| <∞ so that E|f(X)| <∞. Thenthere exists a sequence of simple random variables Xn taking values in I so thatXn → X, E(Xn)→ E(X), E|f(Xn)| → E|f(X)| as well as Ef(Xn)→ Ef(X).

Proof: As in approximating any random variable by a sequence of simple ran-dom variables, we subdivide the real line R by considering intervals [ i

2n , i+12n )

for i = 0, 1, 2 · · · , n2n to cover [0, n) and considering the intervals [ i2n , i+1

2n ) fori = −1,−2, · · · ,−n2n to cover the interval [−n, 0). We need only consider thosesubintervals that intersect with I and ignore the rest. Now over each such subin-terval the value of X is approximated by a value taken by Xn as follows. Since|f | is a continuous function, over the closed interval [ i

2n , i+12n ], let an be the point

of minimum of |f(t)| and let Xn = an over this subinterval. When X falls in theinterval [n,∞), even though the minimum |f(t)| may not exist, inft∈[n,∞) |f(t)| isstill a finite value. (Draw all five possible shapes of f and then all eight or socorresponding shapes of |f(t)|. There are only two shapes, corresponding to thosef which are always nonnegative and monotone and convex and the decreasing sidehas a finite asymptote, these shapes are the ones where the minimum of f(t) over[n,∞) or (−∞,−n] does not occur at t = ±n. For all the rest of the shapes, andlarge enough n, we have that |f(t)| will have its minimums at t = ±n.) Considerthe rest of the six shapes first. In these cases, take Xn = n when X ≥ n and takeXn = −n when X < −n. Hence, we see that by construction |f(Xn)| ≤ |f(X)| forall n. Furthermore, |Xn −X|χ

|X|<n≤ 1

2n and

E(|Xn −X|χ

|X|≥n

)= E

(|n−X|χ

|X|≥n

)≤ 2E

(|X|χ

|X|≥n

)→ 0.

Hence, not only Xn → X but also E|Xn − X| → 0. Furthermore, the continuityof f implies that f(Xn) → f(X). Since |f(Xn)| ≤ |f(X)| and E|f(X)| < ∞,the Lebesgue dominated convergence theorem gives that E|f(Xn)| → E|f(X)|.Now consider those two shapes in which f(t) ≥ 0 and convex and either entirelyincreasing or entirely decreasing. For simplicity consider the case when f is de-creasing and let a be the right asymptote. Then consider another convex functiong(t) = f(t)−a−1. Now this g is one of those considered above and hence we can findsimple random variables Xn → X with E(Xn) → E(X) and Eg(Xn) → Eg(X),which is another way of saying Ef(Xn)→ Ef(X). But since f ≥ 0, it is the sameas saying that E|f(Xn)| → E|f(X)|. Similar argument takes care of the increasing,

32 Various Inequalities

positive convex function. Finally to show that Ef(Xn) → Ef(X), just note that,by our construction (since all constructions |f(Xn)| ≤ |f(X)| or using g instead off and having the same property),

|f(Xn)− f(X)| ≤ |f(X)|+ |f(Xn)| ≤ 2|f(X)|

The left side goes to zero, the right side has finite expectation. Hence, the Lebesguedominated convergence theorem gives that E|f(Xn)− f(X)| → 0. ♠

HW2 Exercise - 4.2.2 - Let f be a convex function over an interval I and let X be arandom variable taking values in I and E|X| < ∞. Prove that Ef(X) is welldefined by showing that Ef−(X) <∞.

Proposition - 4.2.3 - (Convexity & Jensen’s inequality) Let I be an interval.The following statements are equivalent

• (i) f is convex over I,

• (ii) E(f(X)) ≥ f(E(X)) ∀ simple r.v. X on I,

• (iii) E(f(X)) ≥ f(E(X)) ∀ r.v. X on I with E|X| <∞.

Proof: It is clear that (iii) implies (ii) since a simple random variable automat-ically has a finite expectation. Proposition (4.2.1) gives that (ii) implies (i). Thestatement (i) implies (iii) is known as Jensen’s inequality, which we now prove.So, let f be a convex function and let X be a random variable taking values in Iwith E|X| < ∞. Since Ef(X) is always well defined, (cf. Exercise (4.2.2)) andEf−(X) < ∞, the only possibility is that Ef(X) = ∞, in which case we havenothing to prove. So, assume that E|f(X)| < ∞. Take a sequence of simple ran-dom variables Xn taking values in I so that Xn → X, and E(Xn) → E(X) andEf(Xn)→ Ef(X) (cf. Proposition (4.2.2)). Note that

f(E(X)) = f(

limn→∞

E(Xn))

, by construction of X,

= limn→∞

f (E(Xn)) , continuity of f

≤ limn→∞

E (f(Xn)) , by Proposition (4.2.1),

= E (f(X)) , by Proposition (4.2.2).

This finishes the proof. ♠

Remark - 4.2.1 - (Carefull) Now we consider more than one random variable ata time. When X,Y have a induced measure on R2, (and without loss of general-ity, ignoring the inifinite values of X and Y ) then for any real valued measurablefunction h over R2, the change of variable formula (once again) gives that

E(h(X,Y )) =

∫

S

h(X(s), Y (s)) dP (s) =

∫

R2

h(x, y) dPX,Y (s, y)

=:

∫

R2

h(x, y) dFX,Y (x, y),

4.2 Jensen’s Inequality 33

provided the first integral exists. In particular, if X,Y have finite means then bythe linearity of Lebesgue integral,

E(X + Y ) = E(X) + E(Y ).

If X,Y are two random variables (defined over a probability space) the covarianceof X and Y is given by the expectation

Cov(X,Y ) = E(X −E(X))(Y − E(Y ))

which can be defined when E|X|, E|Y | and E|XY | exist as finite numbers, sincethe linearity of expectations allows us to write it as,

Cov(X,Y ) = E(XY )− E(X)E(Y ).

Note that the existence of the first moments of X,Y do not imply that E|XY | <∞.For instance, take U ∼ Uniform(0, 1) and then let X = Y = U−1/2. It is clearthat E|X| < ∞ but E|XY | = E(U−1) = ∞. Similarly, assuming the existenceof E|X|, E|Y | and E|XY | does not imply the existence of E(X2). For instance,take U ∼ Uniform(0, 1) and let X = U−1/2 and let Y = U−1/4. In some books,covariance is defined only when V ar(X) and V ar(Y ) is finite. However, we separatethis case by defining a closely related concept and correlation for which we assumethe existence of the second moments of X and Y . Correlation eliminates the unitsof measurements for X and Y and gives an absolute constant.

HW3 Exercise - 4.2.3 - Prove that E|Y | < ∞ if and only if for any constant c > 0,∑∞n=1 P (|Y | ≥ cn) <∞. Deduce that P (|Y | ≥ cn i.o.) = 0.

HW4 Exercise - 4.2.4 - (Lyapunov inequality) For any s > 1, from the Holder in-equality deduce that

E(|X|) ≤ (E|X|s)1/s.

And deduce the Lyapunov inequality

(E|X|r)1/r ≤ (E|X|s)1/s ; for any 0 < r < s.

HW5 Exercise - 4.2.5 - Let X,Y be two nonnegative random variables and let p ≥ 0 bea number. Prove the following

E(X + Y )p ≤

E(Xp) + E(Y p) if p ∈ [0, 1],2p−1 (E(Xp) + E(Y p)) if p > 1.

HW6 Exercise - 4.2.6 - If X is a nonnegative random variable with distribution F andfinite variance then show that

E(X2)

=

∫ ∞

0

2x (1− F (x)) dx.

34 Various Inequalities

D Exercise - 4.2.7 - Let X be (any) random variable and define a sequence of discreterandom variables,

Xn =j

nif

j

n< X ≤ j + 1

n; j = 0, ±1, ±2, · · · .

If E(Xn) exists for some n = 1, 2, · · · then show that E(Xn) exists for every valueof n and lim

n→∞E(Xn) exists. [Hint: Writing Xn = XN +(Xn−XN) and verifying

that Xn −XN is bounded by 2, show E(Xn) forms a Cauchy sequence.]

Exercise - 4.2.8 - Continuing Exercise (4.2.7), for any continuous random variableX, for which E(Xn) exists for some n, show that E(X) = limn→∞ E(Xn). Thatis, our old definition of expectation for a continuous random variable matches withthe limit obtained from Exercise (4.2.7).

Exercise - 4.2.9 - Redo Exercise (4.2.8) for discrete random variables.

Lecture 5

Classification of

Distributions

First, let us recall some elemantry facts about non-decreasing functions and leftand right limits.

Definition - 5.0.2 - (Discontinuties of type I and type II) Let f be any realvalued function over an interval I ⊆ R. For any x ∈ I, the symbol f(x+) and f(x−)are defined as

f(x+) := limh↓0

f(x + h), f(x−) := limh↑0

f(x + h),

when the limits exist and are called the right limit and left limit of f at x respec-tively. We say f is right continuous at x if f(x+) = f(x) and f is left continuousat x if f(x−) = f(x). (If I = [a, b], then by default f is right continuous at b andleft continuous at a.) The quantities

f(x+)− f(x), f(x)− f(x−), f(x+)− f(x−)

are called the right jump, left jump and the jump of f at x respectively.A point x ∈ I is called a point of discontinuity of the first kind if f(x+) and

f(x−) both exist and f is not continuous at x. All other points of discontinuity areconsidered to be of the second kind.

For example, let f be the Dirichlet function on [0,1], i.e.,

f(x) :=

1 if x is rational, x ∈ [0, 1],

0 otherwise.

Then all points are points of discontiuity of the second kind. For χ 12(t) the point

t = 12 is a point of discontinuity of the first kind.As a second example, let an be an enumeration of the rationals and let bn

be a sequence of non-negative numbers so that the series∑

n bn converges. Define

36 Classification of Distributions

a function

f(x) =∞∑

n=1

bnχ[an,∞)

(x); x ∈ R.

It is easy to see that f is non-decreasing and the series is uniformly convergent.The following proposition implies that all points of discountinuity of f are of thefirst kind.

Proposition - 5.0.4 - (Basic facts for nondecreasing functions) Let f be non-decreasing on an interval I ⊆ R. Then the following results hold.

• (First kind discontinuities) Then all points of discontinuity, if any, of fare of the first kind. Therefore, we may write

f(x−) = supt<x

f(t); f(x+) = infx<t

f(t).

• (Discontinuities are countable) The set D ⊆ I over which f is discontin-uous is at most countably infinite.

• (Continuity) f is continuous at x if and only if f(x−) = f(x) = f(x+).

Proof: Since f is non-decreasing, for any 0 < h′

< h

f(x) ≤ f(x + h′

) ≤ f(x + h).

That is, f(x + h) is decreasing when h is decreasing and it is bounded below byf(x). Thus the limit must exist. Similar argument goes for the left limit.

Any non-decreasing function has discontinuities only of the first kind (i.e., jumpdiscontinuities). Note that when f is bounded,

D = ∪∞n=1

x ∈ I : f(x+)− f(x−) ≥ 1/n

= ∪∞n=1Dn.

Each Dn is a finite set, since, it consists of those points where f has a jump of atleast 1/n. (If Dn had infinite points, adding all these jumps would become infinitewhich would violate the boundedness of f). Hence, D must be countable.

When f is not bounded, let En = [−n, n] and let Dn be the points of disconti-nuities of f which are in En. Since f , when restricted on the inverse image of En ,is a bounded non-decreasing function, Dn is a countable set. Taking union over allDn gives that D must be countable as well.

Finally, for any ǫ > 0, we have f(x− ǫ) ≤ f(x) ≤ f(x + ǫ). Letting ǫց 0 givesthat f(x−) ≤ f(x) ≤ f(x+). So, if f is continuous at x then the left side must equalthe right side. Conversely, when the left side equal the right side, then f must becontinous at x. ♠

Proposition - 5.0.5 - Let f1 and f2 be non-decreasing functions over R. If overa dense subset D ⊆ R, f1(x) = f2(x) for x ∈ D, then f1 and f2 must have thesame points of jump (if any) and f1(x) = f2(x) for all x at which f1 and f2 arecontinuous.

Classification of Distributions 37

Proof: Let x ∈ R be fixed and let tn ր x, then

f1(x−) = lim

tn↑xf1(tn) = lim

tn↑xf2(tn) = f2(x

−).

Similarly, we see that f1(x+) = f2(x

+). Hence, we see that

f1(x+)− f1(x

−) = f2(x+)− f2(x

−).

So, f1 and f2 must have the same points of jump and at the points of continuitywe have f1(x) = f2(x). ♠