Embed Size (px)

Citation preview

PREPRINT: P

LEASE D

O NOT Q

UOTE OR D

ISTRIB

UTE

Public Policy Sources and Welfare Consequences of Islamic Finance

Industry Formation Models

Mehmet Asutay

Professor of Middle Eastern and Islamic Political Economy and Finance

Director, Durham Centre for Islamic Economics and Finance

Durham University Business School, UK

Email: [email protected]

A paper proposed to be presented at the 10th International Conference on Islamic

Economics and Finance under the theme of “Institutional Aspects of Economic, Monetary

and Financial Reforms” jointly organized by the Center for Islamic Economics and

Finance at the Qatar Faculty of Islamic Studies, Hamad bin Khalifa University; Islamic

Research and Training Institute (IRTI); and the International Association for Islamic

Abstract: The Islamic moral economy (IME) is conceived by the founding fathers as a

developmentalist project with the objective of producing human-centred economic

development that aims for capacity development and individual empowerment. Islamic banks

and financial institutions, in accordance with this vision of a developmentalist project, are

expected to contribute to this process. Experience has, however, indicated the ‘social failure’

of Islamic finance. Although a number of reasons can be put forward to address the observed

issue of ‘social failure’, the notion of industry formation must be taken into consideration, as

the way the Islamic finance industry is formed may have consequences for economic

development and social welfare.

Three types of industry formation within the Islamic finance industry are observed in

the world: the Gulf model; the Malaysian model; and, the Indonesian and peripheral economy

model. In addition, a new model has been emerging; that is the Turkish model l;eading to

corporatist model of state oriented and dominated Islamic financial development. Each of

these models has its own welfare and development consequences. It is therefore the aim of

this paper to identify these models within the Islamic banking and finance industry and,

hence, locate their developmentalist and welfare consequences, which can then help to

identify the deadweight loss in the industry formation, enabling some conclusions to be drawn

on the countries that aim to develop their Islamic finance industry.

This research mainly follows a discursive method in developing its argument within the

framework of political economy, thereby ensuring that this debate benefits from a

deconstructive method as part of the discourse analysis. Further, the study should be

considered as part of emergent research.

The paper argues that the Malaysian model results in considerable welfare costs, yet

the bottom-up model, so far pursued by Indonesia, has positive welfare consequences. The

GCC model, however, does not have any particular effect on the welfare of the society and its

developmentalist impact is insignificant.

Keywords: Islamic banking and finance; industry formation models; welfare

consequences; Malaysian, Gulf, Indonesian and Turkish models.

Cover page (title of paper, name of authors, and author affiliations)

10th International Conference on Islamic Economics and Finance

2

I. Introduction

IBF in the modern period emerged as an alternative financing method within the Islamic

moral economy, as the latter aimed to construct a human-centred economic development

through individual and social empowerment, capacity building, and development. The initial

reading of Islamic economics, or of the IME, indicates a heavy emphasis on economic

development, rather than on financing and banking. This emphasis can be explained by the

dire contextual need for development in the 1960s, and through the Islamic response

developed by the founding fathers.

The development of IBF followed an entirely different trajectory, leading to Islamic

capitalism, by converging on the working mechanism of the conventional finance and

banking system, rather than remaining loyal to the spirit and substance of the IME.

Despite the increasing importance of Islamic banks and financial institutions, the

developmentalist need of the Muslim world has not decreased; on the contrary, both capitalist

desires and poverty continue to remain an issue in many Muslim countries, including some of

the oil-rich Arab countries. Thus, the causality between economic development and the rise in

the asset accumulation of IBF does not indicate any direct correlation.

With regard to the ‘social failure’ of IBF, this paper suggests that one of the reasons behind

this “social failure” could be located in the way that the Islamic finance industry is formed

within a particular country. It is therefore the aim of this paper to identify the observed

industry formation strategies in the Islamic finance and banking industry, and to assess the

welfare and developmentalism consequences of these same strategies on the welfare of that

particular society.

The rationale behind this study emerges from the reality that most of the Muslim states,

including the Arab Spring countries, are in dire need of development in terms of human

welfare, job opportunities, and capacity building. Since these countries intend to initiate and

expand their IBF industry based on these expectations, it is thus important to establish the

impact of various industry formation methods, so that the appropriate strategies and

institutionalisation of IBF are selected in order to produce the desired results. The importance

of this research is further seen in the need to ensure that a consistency between aims such as

developmentalism (through Islamic identity in economics and finance), and tools such as

Islamic banks and financial institutions, is established for an optimum outcome.

II. Aims, objectives, and methodology

This study aims to explore the nature of the identified Islamic finance industry formation

models, with the objective of highlighting both their political economies and their

consequences.

In order to attain this objective, the identified industry formation models are analysed by

referencing the following benchmarks or criteria:

(i) Motivational sources;

(ii) Sources of capital;

(iii) Corporate governance;

10th International Conference on Islamic Economics and Finance

3

(iv) The role of the state in industry formation;

(v) Welfare consequences;

(vi) Whether these models are market driven or community driven;

(vii) Developmentalist outcomes.

As a method of analysis, this paper first identifies the IBF industry formation models, as

experienced and observed in the world; it then discusses each one of these models according

to the aforementioned criteria. In this evaluation, however, unique characteristics of Islamic

banking and finance (IBF), akin to those discussed in the following section, are also utilised.

The paper ultimately and critically analyses the developmentalist and welfare consequences

of each of these models.

III. Locating the ‘social failure’ of Islamic banking and finance

Although the contribution of IBF to financial development, alongside its potentially positive

impact on economic growth, cannot be denied, the real economy and socio-economic

development consequences have been disappointing. For this assessment, the IME provides

the necessary benchmark with which the socio-developmentalist impact of IBF can be

evaluated.

The Islamic Moral Economy (IME) strives for the notion of human-centred economic

development; in accordance with this vision, IBF is expected to contribute to the ‘financing’

of development objectives. In other words, IBF is expected, beyond ‘commercialisation’ and

‘financialisation’, to contribute to socio-economic development objectives through locating

itself within an embedded moral economy.

In addition to a number of ethical features of IBF, such as the prohibition of riba, gharar, and

maysir, the IME also expects that IBF should remain embedded in relation to the real

economy and to the social formation of the society. To this end, both profit-and-loss sharing

and risk sharing are considered to be the most unique and salient features of Islamic

financing. Consequently, IBF is expected not to create money in the economy through the

credit system. The IME also expects that IBF should respond to substance related issues,

which are defined by the IME as the developmentalist contributions. In terms of institutional

and operational terms, such features are as follows (Khan, 2007):

(i) Community banking aimed at serving communities not markets;

(ii) Responsible finance, since it builds systematic checks on financial providers and

restrains consumer indebtedness, coupled with ethical investment and Corporate Social

Responsibility (CSR) initiatives;

(iii) An alternative paradigm in terms of stability, linking financial services to the

productive real economy, and which also provides a moral compass for capitalism;

(iv) Meeting aspirations so that the ownership base of society is widened and offers

success with authenticity

Despite these ethical and substance related expectations, a number of studies have shown that

such aspirational outcomes are not produced by IBF, even with its financial and commercial

10th International Conference on Islamic Economics and Finance

4

successes. Indeed, this raises an existential question with regard to how IBF functions as

opposed to aspirational expectation defined by IME.

The ‘social failure’ of IBF is expressed by the following areas (Asutay, 2007a; 2012): the

convergence between IBF and the conventional monetary system; the financialisation of IBF,

as opposed to ‘financing’ and thus ‘disembeddedness’; the overwhelming debt financing

within the IBF industry in contrast to the asset-based financing (or ‘embeddedness’) and the

real economy impact; the non-existence of such long-term development and real economy

financing in infrastructural, agricultural, and manufacturing investment related areas; the

limited financing of small and medium enterprises (SMEs) and other capacity development

financing; failures in social responsibility; and, shortcomings in corporate governance

performance in IBF industries.

A number of reasons can explain the observed ‘social failure’ of Islamic banks (Asutay,

2007a; 2012). For example, the legalistic and rational mind-set under Shari’ah compliancy

can be cited as one of these factors, since this approach prioritises ‘form’ over ‘substance’.

This situation results in ignoring or negating the outcomes of projects, financing, rather than

endogenising the consequences of projects as consequentialism would dictate. In other words,

optimality in individual and commercial interest and contributing to social good is not

achieved, contrary to the expectations of the IME, due to this legalistic and rational

methodology. Not using a moral filter and merely using technical Shari’ah compliancy terms

in relation to the decision making process for project objectives and outcomes is then one of

the reasons for ‘social failure’.

The paradigm shift from the IME to IBF, especially with the adoption of the commercial

institutionalisation of the IBF industry since the mid-1970s, should be considered as another

reason behind the aforementioned ‘social failure’. Indeed, this becomes a significant factor

given that the IME essentialises the embedded and real economy effect by developing an

‘Islamic-based environment’ as an operational framework for IBF.

Among the reasons for ‘social failure’, this study further suggests that commercial banking, as

an institutional format of IBF, is also of relevance. By definition, commercial IBF cannot

work towards socio-economic development beyond attempts at maximising profit. Non-

banking financial institutions should therefore be considered as the third stage of

institutionalisation, with the objective of responding to the development aims. This

arrangement is intended to overcome the observed conflict between aims referring to the

social economy and developmentalism, and instruments and institutions such as banks.

The ‘social failure’ of IBF is also partly attributable to the industry formation, combined with

its commercial institutional nature. This study thus argues that the nature and mechanism of

industry formation can have a deterministic effect on the delivery of developmentalism, in

addition to the welfare consequences that will be examined later in the course of this research.

IV. Industry formation models in Islamic banking and finance

The first institutionalisation in IBF can be traced back to the 1960s with the Mith Ghamr, an

Islamic social bank established during 1963 in Lower Egypt, and Tabung Haji, an Islamic

investment company established during 1967 in Malaysia. The main institutional

development, however, was not until the mid-1970s, for after the establishment of the Islamic

Development Bank in 1974, the Dubai Islamic Bank was established in 1975 as the first fully

fledged Islamic bank in the form of a commercial bank. This first attempt determined the

10th International Conference on Islamic Economics and Finance

5

institutional nature of Islamic banking over the course of the following years. As a result, the

prevailing institutional model for Islamic banking has been ‘commercial’, aside from the

exception of some investment banks operating in the industry. It is therefore important to

distinguish between the operational nature of Islamic banking in the contemporary period and

the initial form of Islamic banking: commercial banking has then replaced the social banking

paradigm, and it is now considered to be the only banking form within the IBF industry.

Although commercial Islamic banks have dominated the IBF industry, there are some

distinctions in the way that this industry has been established. A close politico-economic

analysis of the IBF industry formation thus demonstrates that the development trajectories of

the industry have predominantly followed four different models:

(i) Gulf model, a top-down, business-sector-dominated model;

(ii) Malaysian model, a top-down, state-centric model;

(iii) Indonesian model; a bottom-up, civil-society-oriented model (at the periphery);

(iv) Hybrid model.

Although the Gulf and Malaysian Islamic banking models are extensively mentioned in

critical literature, the Indonesian and hybrid models have not been explored. It should,

however, be emphasised that the Gulf and Malaysian models are discussed in the literature in

a comparative manner in relation to the different legal, regulative, and ultimately Shari’ah

implications of these models rather than in relation to the industry formations adopted by

these countries. This study extends the comparison and the debate beyond the implications of

Shari’ah, but rather aims to explore the developmentalist consequences with regard to

industry formation, by employing the various benchmarks or criteria that were previously

mentioned. In other words, this paper explores the potential correlation between

developmentalist and welfare outcomes of IBFs and the respective industry formation models.

The importance of exploring the industrial formation nature of IBF is perceived in the way

that each of these models followed a particular process and structure, thereby producing

different outcomes in relation to economic and developmentalist expectations. Among others,

Asutay (2007a; 2012) highlights the observed ‘social failure’ of IBF; one of the reasons for

this is attributed to the institutional, as well as the industry formation, nature of IBF. In other

words, if the chosen model for institutionalisation is commercial IBF in developing the

industry, by definition, the consequences of this would not be in favour of socio-economic

development, even if it is operated as shari’ah compliant institutions. These models are

explored in detail in the following sections by referencing the previously identified

benchmarks or criteria.

It should be noted that since the hybrid model, which can combine the Malaysian and Gulf

IBF formation, does not have any unique features beyond the combination of these two facets,

it will not be analysed in this paper.

When exploring the consequences of the IBF industry formation, alongside its socio-

economic impact, the salient features of IBF identified in this section are employed in

evaluating the performance of each of the specified models of the IBF industry formation.

V. GCC Islamic banking model: top-down/business-sector-dominated – model 1

10th International Conference on Islamic Economics and Finance

6

Although various forms of ‘Islamic financing’ have operated on the periphery of the Muslim

World for centuries, the institutionalisation of the Islamic bank, beyond ‘Islamic financing’ in

the modern sense, occurred in Dubai in 1975 with the establishment of the Dubai Islamic

Bank, after the formation of the Islamic Development Bank in 1974.

Islamic banking came into existence partly as a result of the Muslim world’s ‘Islamic identity

search’; for in this post-colonial period, IBF was considered to be an element of this identity

search. Equally, the Gulf countries were also not immune to these developments. The rise of

Islamic banking in the Gulf region was predominantly stimulated by the increased oil

revenues following the 1973 oil shock. Indeed, the oil shocks in 1973 and 1978 brought a

large amount of wealth for the Gulf countries to manage, with the objective of delivering

growth and development, which in turn hastened the creation of Islamic banks in the region.

It is worth mentioning that the expansion of the IBF industry has been largely linked to the

neo-liberalism of the 1990s, which labelled economic reform and financial liberalisation as

comprising the main axis of economic success. This not only provided an opportunity and

space within which to expand, but also a provided a growth-path for the IBF industry to

expand, as opposed to the initially adverse or neutral attitude displayed by the GCC countries.

A close examination of the IBFI formation in the region shows that it was commenced and

sustained by private initiatives for the most part; it was, moreover, established by ‘families’

forming Islamic banks as an aspect of their holding companies. Some of these banks are

owned by members of the royal families, yet this does not imply that these banks should be

considered as public sector banks, since they operate freely in the market on a similar basis to

any other Islamic bank, rather than acting as the state’s bank simply because the family who

owns it is in power.

When investigating the regulative environment of Gulf IBF, it can be seen that the state

remains regulative, with no special treatment for Islamic banks. This implies that Gulf

emirates and kingdoms do not provide a particular incentive system or get involved

proactively in the development of this sector. In this vested business interests plays an

important role, and regulative environment keep similar distance from each banking sector.

However, being open to ‘financial development’, the states in the region are open to IBF

development, and the legal and regulative environment in these countries considers IBF as

hybrid institutions and instruments of financial and capital markets rather than the institutions

of an alternative system.

Since the state is not involved in the development of the IBF industry and therefore does not

provide any particular tax and other type of incentive system to protect it from competition,

the state does not cause a particular deadweight cost on social welfare. In addition, since IBF

industry does not have aim to contribute to the social welfare, thus they do not have any

positive or negative consequences for social welfare. Indeed, as Freidman would say, IBF

remains very much a ‘private firm’ in terms of its social responsibility by ‘maximising their

profit’.

Due to the corporate governance nature of IBs, and also due to their ownership as well as their

distance from the state, they remain commercial in their objective functions, and therefore, the

social and economic development of the society is not part of the vision outlined for the

Gulf’s IBF. IBF institutions’ understanding, hence, remains within that of the ‘neo-classical’

firm; they therefore conduct their business according to their own objective function of

efficient and profitability. This does not mean that they do not contribute to charities and

10th International Conference on Islamic Economics and Finance

7

other philanthropic causes. These efforts and attempts, however, remain as ‘private’ and

‘individual’ initiatives, rather than representative of a particular Gulf country’s IBF sector

taking up this notion as a systematic strategy within the IME in order to contribute to the

social welfare and economic development, either in their own country or beyond its borders.

With regard to corporate governance, Gulf IBF mainly follows the shareholders interests by

maximising dividends and returns. In response, these countries always claim that IBF is not a

‘charitable’ institution and that they have to consider the interests of their shareholders. This

setup thus resembles the Anglo-Saxon model of corporate governance, which is far estranged

from either the Islamic or stakeholder model.

GCC Islamic banks, in their objective function, aim to achieve efficiency and to maximise

profit. This consequently locates them within the concept of a ‘neo-classical’ firm, as opposed

to the IME’s ‘social firm’, where there is a direct contribution to social good and the welfare

of the society.

An important consequence of the IBF industry in the Gulf has been its contribution towards

facilitating the penetration of capitalism into larger segments of GCC societies. The coupling

of this penetration of capitalism with a Calvinistic Muslim attitude, where a religious

pragmatism operates with the awareness that Islamic banks cleanse the wealth that they have,

has resulted in the expansion of homoeconomics at the expense of the development of

homoIslamicus in the Gulf. In other words, a puritanical attitude within the capitalist form has

been the defining identity in the Gulf, which has been supported by the IBF industries.

VI. Malaysian Islamic banking model: top-down/state-centric–model 2

Malaysia is an emerging country that has demonstrated an unprecedented level of success

through its economic performance, especially over the last twenty years. It is also always

cited as an example of a country where the combination of modernity and Islam determines

the nature of everyday life, for both the individual and society, thereby implying that “Islamic

modern” or “modern Islam” is reproduced through a negotiating and re-negotiating process in

the country to ameliorate the lives of the Muslim constituents. A more notable characteristic

of Malaysia in the last four decades is that of its efforts to construct an Islamic identity

through a merger of modern and traditional religious values. The country has therefore

witnessed the rise of new institutions constructed on Islamic principles and values, including

Islamic banks and financial institutions, takaful, and other non-banking financial institutions.

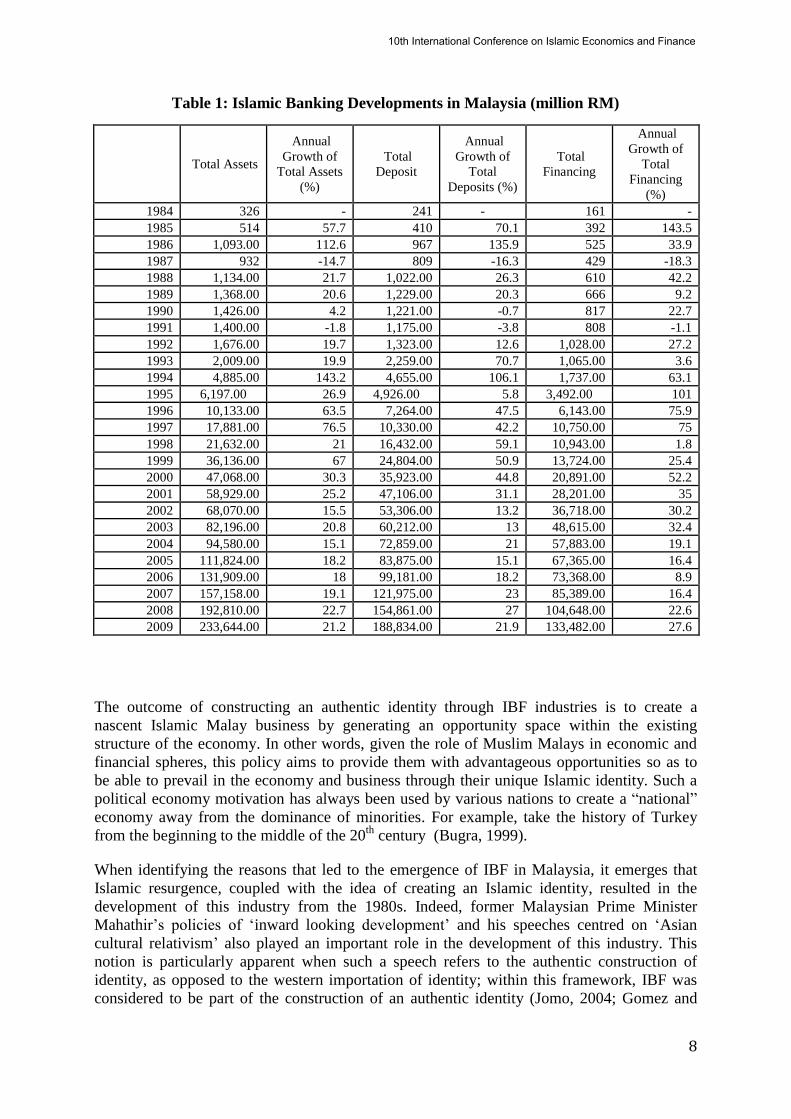

As can be seen in Table 1, the total assets, deposits, and financing of Malaysian Islamic

banking institutions continued to grow gradually. In 1984, the total assets were only RM 326

million, which then increased to RM 233,6 billion in 2009. This figure is also expected to

exceed RM 350 billion in 2012.

Critical analysis indicates that the strong commitment to the development of IBF is mainly

motivated by the idea of creating an authentic Islamic identity that aims to define what being

Malay signifies in the modern world. The IBF industry thus represents the extension of this

construct of authentic identity in terms of economic and financial existence, and hence, the

search for identity has played an important role in the creation of these institutions.

10th International Conference on Islamic Economics and Finance

8

Table 1: Islamic Banking Developments in Malaysia (million RM)

Total Assets

Annual

Growth of

Total Assets

(%)

Total

Deposit

Annual

Growth of

Total

Deposits (%)

Total

Financing

Annual

Growth of

Total

Financing

(%)

1984 326 - 241 - 161 -

1985 514 57.7 410 70.1 392 143.5

1986 1,093.00 112.6 967 135.9 525 33.9

1987 932 -14.7 809 -16.3 429 -18.3

1988 1,134.00 21.7 1,022.00 26.3 610 42.2

1989 1,368.00 20.6 1,229.00 20.3 666 9.2

1990 1,426.00 4.2 1,221.00 -0.7 817 22.7

1991 1,400.00 -1.8 1,175.00 -3.8 808 -1.1

1992 1,676.00 19.7 1,323.00 12.6 1,028.00 27.2

1993 2,009.00 19.9 2,259.00 70.7 1,065.00 3.6

1994 4,885.00 143.2 4,655.00 106.1 1,737.00 63.1

1995 6,197.00 26.9 4,926.00 5.8 3,492.00 101

1996 10,133.00 63.5 7,264.00 47.5 6,143.00 75.9

1997 17,881.00 76.5 10,330.00 42.2 10,750.00 75

1998 21,632.00 21 16,432.00 59.1 10,943.00 1.8

1999 36,136.00 67 24,804.00 50.9 13,724.00 25.4

2000 47,068.00 30.3 35,923.00 44.8 20,891.00 52.2

2001 58,929.00 25.2 47,106.00 31.1 28,201.00 35

2002 68,070.00 15.5 53,306.00 13.2 36,718.00 30.2

2003 82,196.00 20.8 60,212.00 13 48,615.00 32.4

2004 94,580.00 15.1 72,859.00 21 57,883.00 19.1

2005 111,824.00 18.2 83,875.00 15.1 67,365.00 16.4

2006 131,909.00 18 99,181.00 18.2 73,368.00 8.9

2007 157,158.00 19.1 121,975.00 23 85,389.00 16.4

2008 192,810.00 22.7 154,861.00 27 104,648.00 22.6

2009 233,644.00 21.2 188,834.00 21.9 133,482.00 27.6

The outcome of constructing an authentic identity through IBF industries is to create a

nascent Islamic Malay business by generating an opportunity space within the existing

structure of the economy. In other words, given the role of Muslim Malays in economic and

financial spheres, this policy aims to provide them with advantageous opportunities so as to

be able to prevail in the economy and business through their unique Islamic identity. Such a

political economy motivation has always been used by various nations to create a “national”

economy away from the dominance of minorities. For example, take the history of Turkey

from the beginning to the middle of the 20th

century (Bugra, 1999).

When identifying the reasons that led to the emergence of IBF in Malaysia, it emerges that

Islamic resurgence, coupled with the idea of creating an Islamic identity, resulted in the

development of this industry from the 1980s. Indeed, former Malaysian Prime Minister

Mahathir’s policies of ‘inward looking development’ and his speeches centred on ‘Asian

cultural relativism’ also played an important role in the development of this industry. This

notion is particularly apparent when such a speech refers to the authentic construction of

identity, as opposed to the western importation of identity; within this framework, IBF was

considered to be part of the construction of an authentic identity (Jomo, 2004; Gomez and

10th International Conference on Islamic Economics and Finance

9

Jomo, 1999). This process and the accompanying discourse developed by Mahattir were

further substantiated by the Asian financial crisis, which, according to Mahattir’s

understanding, provided evidence for his ‘cultural relativist’ position in economic and

financial spheres (Jomo, 2001). The discursive management of the crisis offered by Mahathir

should then be considered as an important political factor in the development of the IBF

industry within Malaysia. Malaysia has thus had a special and emergent political economy

approach towards its attempt to develop the IBF industry.

In terms of ownership, the very first institution, Tabun Haji, was established as a social bank

and civil society institution with the objective of doing ‘social good’. Since 1983, however,

Islamic banks in Malaysia (and elsewhere) functioned in the manner of a commercial bank,

based on private initiative as corporate entities. IBF has, however, received various large state

incentives in an attempt to consolidate its development. This support has been in the form of

financial, tax, and regulative incentives. For example, to make sukuk more competitive,

Malaysian authorities provide tax incentives; this protective incentive system resembles the

‘import institution policies of the 1970s’, which were adopted by developing countries to

ensure the healthy development of ‘infant industries’. On a similar note, IBF institutions are

protected in Malaysia as elements of infant industry, which results in unfair competition. It is

also important to explore the ‘import substitution policies of the 1970s’ in order to understand

the potential consequences of such an incentive system. For despite this incentive system, the

‘infant industries’ failed to develop efficient production, resulting in huge deficits for the

national governments in these developing countries, thereby leading to economic

restructuring during the post-Washington Consensus period in 1979. Although this situation is

not expected to happen to IBF institutions, there are good reasons to believe that due to

‘incentives’ Islamic banks and financial institutions will not be able to learn to survive and

produce outcomes within the efficiency frontier. The initial empirical results provide some

evidence in this direction, but it is also important to note that those studies have not taken into

account the impact of the incentive system in enhancing the observed efficiency of IBF.

With the state providing an incentive mechanism, there is then an implication that it remains

an important stakeholder in the development of IBF, proactively shaping the industry through

the incentive system, and dominating it via its agencies in order to identify strategies and

issue regulations and standards in an attempt to determine its future shape; IFSB among

others, for example. The state’s involvement in developing human resources for the IBF

industry through education and training has also been instrumental, such as with INCEIF,

ISRA, and many other institutions which are directly funded by the Bank Negara Malaysia

and other similar state agencies.

The state’s use of public funds for the development of private industry, namely the IBF

industry, is a matter of economic concern. This is because such a policy causes welfare losses

for the general public, as the opportunity costs of those public funds that are allocated to the

areas related to Islamic finance are an unacknowledged reality. In other words, instead of

using the funds for the development of the society as a whole in order to bring

developmentalism to the rural areas, they are deployed from the public treasury for private

interest in the form of Islamic banks. Public money is therefore used for private sector

development, without any major social return from these banks to the public, which implies

an inconsistency; this directly results in welfare costs to the society. If, however, the Islamic

finance industry had worked to deliver social and developmentalist outcomes to the

underprivileged and unbanked, then the welfare costs could have been overcome or alleviated

by the additional benefits. To surpass this inconsistency and the accompanying welfare costs

associated with developing the Islamic finance industry, the Bank Negara Malaysia has

10th International Conference on Islamic Economics and Finance

10

recently been working to develop structures through which the social impact of Islamic banks

can be generated.

The dilemma for the Malaysian authorities in their IBF policy-making has then been that of

the trade-off between the private interest for political objectives and the development needs

on the periphery of Malaysia. The evidence, however, indicates that the weighting in this

dilemma has shifted towards private interest. Therefore, it is essential that a realistic

evaluation of the costs of building an IBF industry should be conducted, so as to identify the

associated opportunity costs and, by extension, the welfare costs.

In this state-centric IBF industry formation model, the state creates social disequilibrium by

allocating the resources to a private sector, whereas the IBF industry, as a private sector

initiative, does not contribute to counteract this disequilibrium, even though it is (in the

aspirational sense) expected to do so.

An important implicit cost of the nature of the development of the IBF industry in Malaysia is

that of the foregone conclusion reached on the search for authentic Islamic identity. In other

words, with the consolidation of the IBF industry in Malaysia, the search for identity is still

not complete, for IBF follows an efficiency-oriented, neo-classical understanding, rather than

an idea of social equilibrium as defined by the ‘attached identity’ defined by IME. A quick

analysis of the balance sheets of Islamic banks would reveal that they are heavily directed

towards debt financing in Malaysia (over 92.5%), yet in an aspirational sense, they are

expected to develop PLS structures to overcome debtness. By extension, the embedded

financing approach promoted by the IME is no longer a principle that is connected to this

notion. In addition, structures such as tawarruq are utilised without any concerns, since these

‘liberally’ justified products bring about further financialisation, as opposed to the financing

orientation of aspirational Islamic finance.

It is also important to note that with the emergence of IBF in Malaysia, a strong claim was

made on socio-economic development and it was exemplified by the case of Tabung Hajj in

the 1960s. When comparing the current development of the industry, especially since the

1980s, with the initial socio-economic-development-related identity through

consequentialism, it is, however, apparent that the IBF industry has not fulfilled its initial

objective function. To understand this initial ‘socio-economic claim’, reference should be

made to the discourse centred on ‘religion and development within Malaysia’ in the 1980s in

an attempt to respond to Weber (Jomo, 1977). Despite the original position on the importance

of Islamic identity for economic development, it now seems that the hybrid identity of

Muslim-Calvinism has emerged as victorious over the identity of homoIslamicus.

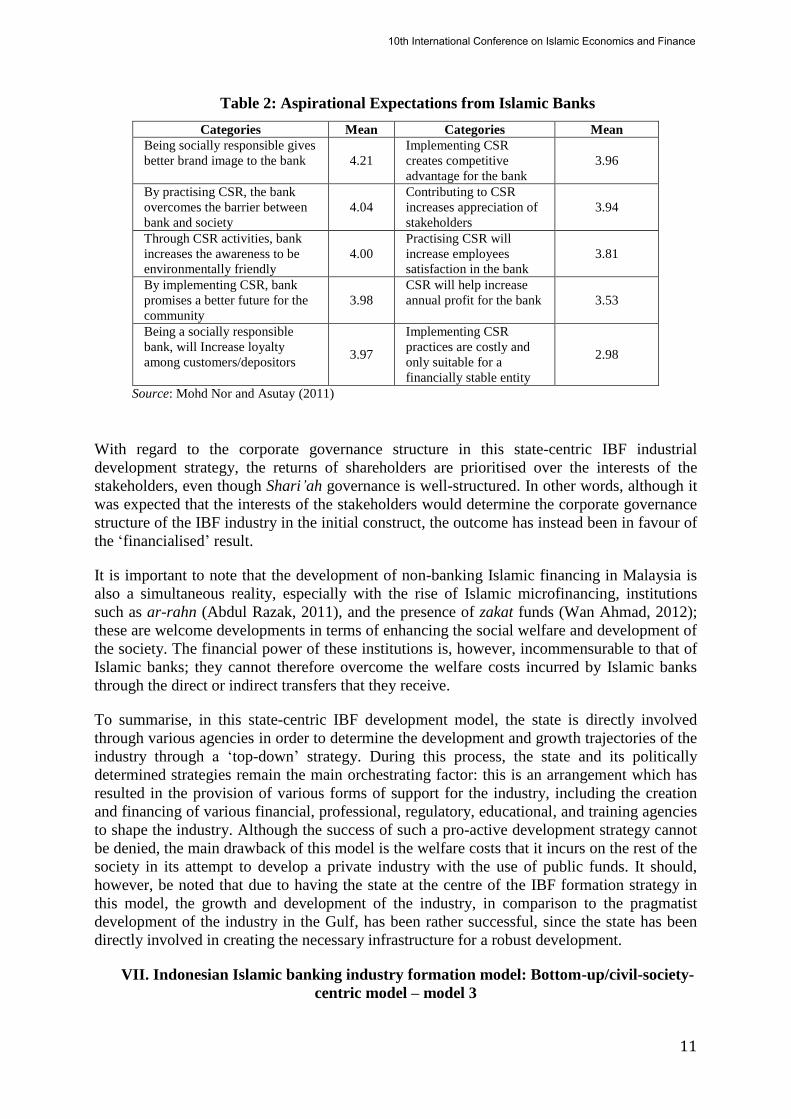

It should also be noted that despite the development of the Malaysian IBF industry beyond the

aspirational IME, clients of Islamic banks still expect IBF to respond to these aspirational

expectations. Thus, the construct of Islamic identity still appears to motivate the individuals

within the country.

10th International Conference on Islamic Economics and Finance

11

Table 2: Aspirational Expectations from Islamic Banks

Categories Mean Categories Mean

Being socially responsible gives

better brand image to the bank 4.21

Implementing CSR

creates competitive

advantage for the bank

3.96

By practising CSR, the bank

overcomes the barrier between

bank and society

4.04

Contributing to CSR

increases appreciation of

stakeholders

3.94

Through CSR activities, bank

increases the awareness to be

environmentally friendly

4.00

Practising CSR will

increase employees

satisfaction in the bank

3.81

By implementing CSR, bank

promises a better future for the

community

3.98

CSR will help increase

annual profit for the bank 3.53

Being a socially responsible

bank, will Increase loyalty

among customers/depositors 3.97

Implementing CSR

practices are costly and

only suitable for a

financially stable entity

2.98

Source: Mohd Nor and Asutay (2011)

With regard to the corporate governance structure in this state-centric IBF industrial

development strategy, the returns of shareholders are prioritised over the interests of the

stakeholders, even though Shari’ah governance is well-structured. In other words, although it

was expected that the interests of the stakeholders would determine the corporate governance

structure of the IBF industry in the initial construct, the outcome has instead been in favour of

the ‘financialised’ result.

It is important to note that the development of non-banking Islamic financing in Malaysia is

also a simultaneous reality, especially with the rise of Islamic microfinancing, institutions

such as ar-rahn (Abdul Razak, 2011), and the presence of zakat funds (Wan Ahmad, 2012);

these are welcome developments in terms of enhancing the social welfare and development of

the society. The financial power of these institutions is, however, incommensurable to that of

Islamic banks; they cannot therefore overcome the welfare costs incurred by Islamic banks

through the direct or indirect transfers that they receive.

To summarise, in this state-centric IBF development model, the state is directly involved

through various agencies in order to determine the development and growth trajectories of the

industry through a ‘top-down’ strategy. During this process, the state and its politically

determined strategies remain the main orchestrating factor: this is an arrangement which has

resulted in the provision of various forms of support for the industry, including the creation

and financing of various financial, professional, regulatory, educational, and training agencies

to shape the industry. Although the success of such a pro-active development strategy cannot

be denied, the main drawback of this model is the welfare costs that it incurs on the rest of the

society in its attempt to develop a private industry with the use of public funds. It should,

however, be noted that due to having the state at the centre of the IBF formation strategy in

this model, the growth and development of the industry, in comparison to the pragmatist

development of the industry in the Gulf, has been rather successful, since the state has been

directly involved in creating the necessary infrastructure for a robust development.

VII. Indonesian Islamic banking industry formation model: Bottom-up/civil-society-

centric model – model 3

10th International Conference on Islamic Economics and Finance

12

Despite being in the same geographical region and sharing the same ethnic traits (generally

speaking), the development trajectories for Indonesia have been considerably different to

those shown in Malaysia. Indeed, having a different political economy of trajectory, Indonesia

had to follow a difficult developmentalist path with pronounced dictatorial tendencies until

the end of the last century. Further, with the existence of a strong cult of personality, marked

by secularism, that dominated the political development model, Indonesia had a rather

difficult political culture and economic development strategy. In recent years, it has been

perceived as an emerging economy; Indonesia is not only the largest populated Muslim

country, but it is also now the largest economy in the Muslim world, despite having a very

low per capita income.

Due to this political economy, the Indonesian IBF industry has followed a slow development

trajectory, a predicament that resembles Turkey’s situation; the causes of this particular

trajectory should be attributed to the political (and secular) culture at an elite level, which

existed until recently. In other words, the development of the IBF industry is considered to

result in the construction of Islamic identity and be a result of Islamic identity; the authorities

therefore avoided engaging with, and facilitating, the IBF industry.

The development trajectory of the IBF industry formation has thus followed two different

routes in Indonesia, for as a result of financial liberalisation policies adopted by the country in

the 1980s, IBF was considered to be an alternative financial institution, which resulted in the

formation of Islamic banks later in the 1990s. This was, and still is, a top-down IBF formation

model. Further, the development of the IBF industry on the periphery of Indonesia was

intended to create an authentic development strategy based on human and community

development understanding. Such a strategy considered Islamic finance as a source for

capacity building, and as a tool for individual and social empowerment in the economic

development process. Hence, non-banking Islamic financial institutions, mainly in the form of

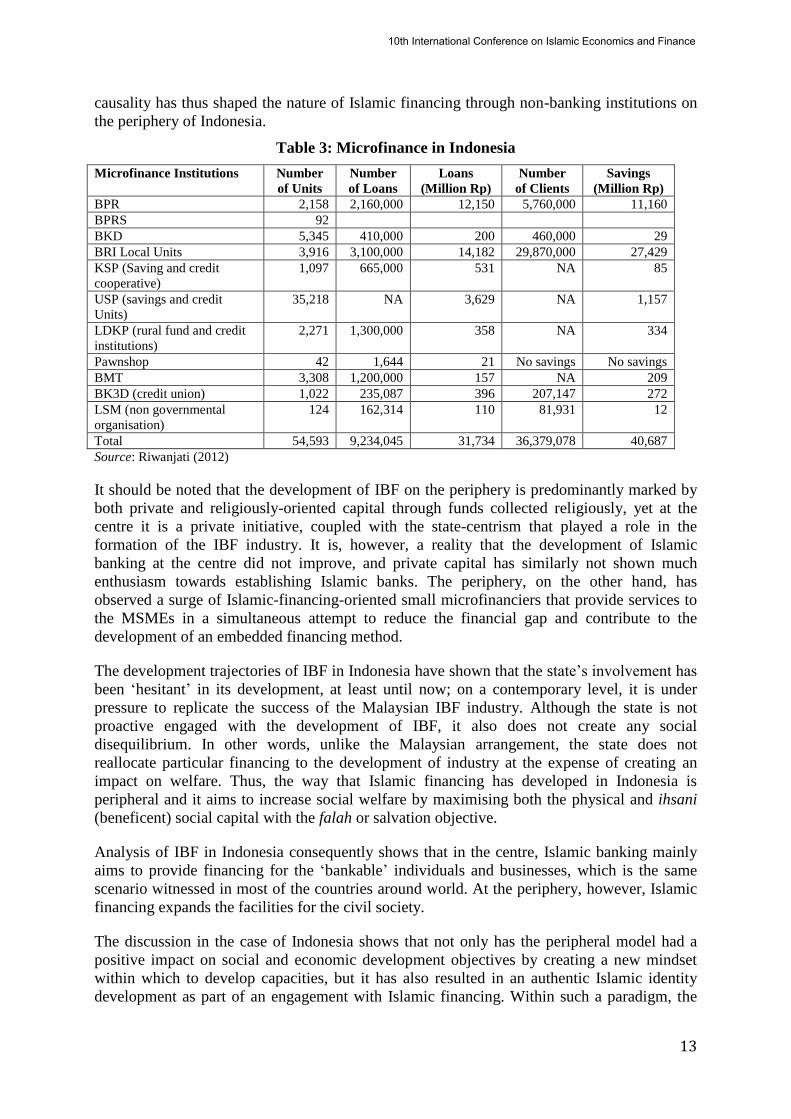

microfinancing institutions, have been successfully run in Indonesia. As evidence of this,

Table 3 depicts the size of the microfinance industry, including Islamic alternative.

As can be seen in Table 3, both the magnitude and importance of microfinance, including

Islamic microfinance, are identified. This directly illustrates the civil society nature of Islamic

financing in the form of microfinancing, and which should also be compared with the

approximately 3% attributed to the role of Islamic banking in Indonesia. The widespread

availability of Islamic microfinancing is an important contribution to individual and social

empowerment in Indonesia.

Given that Islamic banking has a matter of the ‘centre’, thus, at the centre the search for

Islamic identity did not play any role in Indonesia, whereas the existence of IBF is mainly due

to the conception and creation of an authentic Islamic development model in actuality on the

periphery of Indonesia. In other words, the search for an authentic Islamic identity resulted in

various forms and institutions of Islamic micro-financing on the periphery, which in turn

further supported the development of this institutionalisation. For this process, the

involvement of religious groups at the community level as part of new social movements

contributed to the advancement of Islamic finance (Anthonio, 2012). As is also identified by

Anthonio (2012) and Rudnyckyj (2012), those involved in this ethical business and finance as

clients underwent religious training, in addition to skills-oriented training, so as to be able to

run their medium-and-small-sized-enterprises (MSMEs). Although this procedure is expected

to develop an efficient business culture by substantiating it with a religious identity, this

identity formation precipitates further involvement in Islamic financing. Bi-directional

10th International Conference on Islamic Economics and Finance

13

causality has thus shaped the nature of Islamic financing through non-banking institutions on

the periphery of Indonesia.

Table 3: Microfinance in Indonesia

Microfinance Institutions Number

of Units

Number

of Loans

Loans

(Million Rp)

Number

of Clients

Savings

(Million Rp)

BPR 2,158 2,160,000 12,150 5,760,000 11,160

BPRS 92

BKD 5,345 410,000 200 460,000 29

BRI Local Units 3,916 3,100,000 14,182 29,870,000 27,429

KSP (Saving and credit

cooperative)

1,097 665,000 531 NA 85

USP (savings and credit

Units)

35,218 NA 3,629 NA 1,157

LDKP (rural fund and credit

institutions)

2,271 1,300,000 358 NA 334

Pawnshop 42 1,644 21 No savings No savings

BMT 3,308 1,200,000 157 NA 209

BK3D (credit union) 1,022 235,087 396 207,147 272

LSM (non governmental

organisation)

124 162,314 110 81,931 12

Total 54,593 9,234,045 31,734 36,379,078 40,687

Source: Riwanjati (2012)

It should be noted that the development of IBF on the periphery is predominantly marked by

both private and religiously-oriented capital through funds collected religiously, yet at the

centre it is a private initiative, coupled with the state-centrism that played a role in the

formation of the IBF industry. It is, however, a reality that the development of Islamic

banking at the centre did not improve, and private capital has similarly not shown much

enthusiasm towards establishing Islamic banks. The periphery, on the other hand, has

observed a surge of Islamic-financing-oriented small microfinanciers that provide services to

the MSMEs in a simultaneous attempt to reduce the financial gap and contribute to the

development of an embedded financing method.

The development trajectories of IBF in Indonesia have shown that the state’s involvement has

been ‘hesitant’ in its development, at least until now; on a contemporary level, it is under

pressure to replicate the success of the Malaysian IBF industry. Although the state is not

proactive engaged with the development of IBF, it also does not create any social

disequilibrium. In other words, unlike the Malaysian arrangement, the state does not

reallocate particular financing to the development of industry at the expense of creating an

impact on welfare. Thus, the way that Islamic financing has developed in Indonesia is

peripheral and it aims to increase social welfare by maximising both the physical and ihsani

(beneficent) social capital with the falah or salvation objective.

Analysis of IBF in Indonesia consequently shows that in the centre, Islamic banking mainly

aims to provide financing for the ‘bankable’ individuals and businesses, which is the same

scenario witnessed in most of the countries around world. At the periphery, however, Islamic

financing expands the facilities for the civil society.

The discussion in the case of Indonesia shows that not only has the peripheral model had a

positive impact on social and economic development objectives by creating a new mindset

within which to develop capacities, but it has also resulted in an authentic Islamic identity

development as part of an engagement with Islamic financing. Within such a paradigm, the

10th International Conference on Islamic Economics and Finance

14

embedded nature of Islamic financing in the social formation of the society in on the

periphery relates financing with real economic activity by touching the lives of individuals.

By comparing and contrasting different development strategies in the case of Indonesia, one

can state that in a Weberian sense, Calvinistic attitudes play an important role in articulating

the formation of the IBF industry, yet on the periphery, ‘religion is at play with development’

and it facilitates development through its own principles.

With regard to the corporate governance issues within the IBF industry in Indonesia, it is very

much the approach of the stakeholders that is followed on the periphery with Islamic

financing, whereas the approach offered by shareholders dominates the central aspect of

Islamic banking. Since this situation has welfare implications, the former is considered to be

contributing to the social welfare in a positive manner. Indeed, this is the aspiration of the

IME, aiming to finance the means of production and the social formation of a particular

society in its own way.

The peripheral and horizontal outreaching Islamic financing methods through non-banking

financial institutions can ultimately result in more effective outcomes in terms of

developmentalist objectives, including the alleviation of poverty and capacity building, yet

vertical financing, such as is demonstrated by the banking institutions and even Islamic banks,

is only growth-oriented.

It is clear that such objectives can only be fulfilled by a civil-society-oriented IBF

development strategy, as is indicated by the Indonesian model.

VIII. Emergence of a new model: The rise of Islamic banking and finance in Turkey –

emergence of model 4

Islamic banking in Turkey began in 1985 as part of the liberalization programme pursued by

Turgut Özal’s premiership (1983-1989). However, due to the laicist political culture of the

time, Islamic banks were called ‘Special Finance Houses’ (SFHs), without any express

reference to their Islamic nature. This political disfavour towards the label ‘Islamic’ persisted

in 2005, when SFHs were converted into ‘Participation Banks’ (PBs), and continues to exist

today despite the ‘Islamically friendly’ government being in power in the last ten years. Not

only the development of the market has been hampered by an adverse political environment,

but also the secularization of Turkish society has to be taken into consideration for a

comprehensive analysis.

The regulatory development of Islamic banking in Turkey went through different stages

determined by economic and financial factors as well as by the political attitude towards the

sector. Generally speaking, anyway, the potential of Islamic banking in Turkey has not been

fully explored yet.

Looking at its performances since 1985, in fact, the growth has been sluggish in comparison

to the Gulf and South East Asian countries. The recent data demonstrates that the total assets

of Islamic banks in the financial system of Turkey has risen to 4.3 per cent, while the same

ratio for Bahrain is 57 per cent, for Kuwait is 50 per cent, for Qatar 49 per cent, Malaysia 18

per cent, UAE 16 per cent, Egypt 10 per cent, and Indonesia 2 per cent (TKBB 2010: 29).

The progress of Islamic banking in Turkey can better be understood in comparison with

Malaysia, as Malaysia and Turkey began having Islamic banking around the same time, i.e.

10th International Conference on Islamic Economics and Finance

15

1983 and 1985 respectively. However, the developments in the Islamic financial services of

both countries have followed entirely different trends. Malaysia has aimed at becoming the

leading country in the Islamic financial markets, through investments in institutional

developments, as well as the government’s commitment for educational and skill

improvements in the sector. This is due to the Malaysian strategic perception of Islamic

finance, as manifested by a supportive political will. In opposition to this commitment, the

use of the term ‘Islamic’ in the banking sector in Turkey is still considered as a ‘taboo’ by

both the outsiders, i.e. the political establishment, and the insiders, namely those working in

the industry. This hesitation can be seen in the publication materials by the TKBB, the

Association of Participant Banks of Turkey (www.tkbb.org.tr), which insist and repeat

continuously that PBs are ‘not an alternative, but an integral component of the Turkish

banking sector’, with the objective of not disturbing the ‘apple cart’.

In terms of international comparison, Shari‘ah compliant assets of Turkey within the ten

leading Islamic banking countries is depicted in Table 4, which shows that Turkey is ranked

as 9th in 2009 and, by increasing its Shari’ah asset base in Islamic banking by 26.5 per cent,

Turkey managed to move to 8th rank in 2010, which remained the same through 2012. As

mentioned before, considering that Turkey is the 2nd largest and most dynamic Muslim

economy, its place in the ranking does not do justice to the size of its economy.

Table 1: Top 15 Countries by Shari’ah-Compliant Assets

2009 2010 2011 2012

Rank Country

Shari’ah-

Compliant

Assets $m

Rank Country

Shari’ah-

Compliant

Assets $m

Rank Country

Shari’ah-

Compliant

Assets $m

Rank Country

Shari’ah-

Compliant

Assets $m

1 Iran 293,165.80 1 Iran 314,897.40 1 Iran 387,952.57 1 Iran 465,574.92

2 Saudi

Arabia 127,896.10 2 Saudi Arabia 138,238.50 2

Saudi Arabia 150,945.43 2 Malaysia 221,025.52

3 Malaysia 86,288.20 3 Malaysia 102,639.40 3 Malaysia 133,406.38 3 Saudi Arabia 185,223.00

4 UAE 84,036.50 4 UAE 85,622.60 4 UAE 94,126.66 4 UAE 89,309.38

5 Kuwait 67,630.20 5 Kuwait 69,088.80 5 Kuwait 79,647.85 5 Kuwait 78,587.25

6 Bahrain 46,159.40 6 Bahrain 44,858.30 6 Bahrain 78,857.47 6 Bahrain 62,171.53

7 Qatar 27,515.40 7 Qatar 34,676.00 7 Qatar 52,322.38 7 Qatar 45,301.30

8 UK 19,410.50 8 Turkey 22,561.30 8 Turkey 28,015.20 8 Turkey 29,292.86

9 Turkey 17,827.50 9 UK 18,949.00 9 UK 19,041.79 9 UK 18,605.43

10 Bangladesh 7453.3 10 Bangladesh 9,365.50 10 Sudan 12,139.45 10 Indonesia 15,963.97

11 Sudan 7151.1 11 Sudan 9,259.80 11 Bangladesh 11,677.10 11 Bangladesh 12,572.97

12 Egypt 6299.7 12 Egypt 7,227.70 12 Indonesia 10,531.61 12 Sudan 9,825.23

13 Pakistan 5126.1 13 Indonesia 7,222.20 13 Syria 8,690.20 13 Egypt 8,296.32

14 Jordan 4621.6 14 Pakistan 6,203.10 14 Egypt 7,888.22 14 Pakistan 7,328.34

15 Syria 3838.8 15 Syria 5,527.70 15 Switzerland 6,582.48 15 Switzerland 6,551.37

Source: The Banker (various issues).

In addition, domestic comparison with conventional banking can help to develop a better

understanding regarding the place of Islamic banks in Turkey. Table 5, therefore, depicts the

trends in the assets of Islamic banks over the years.

10th International Conference on Islamic Economics and Finance

16

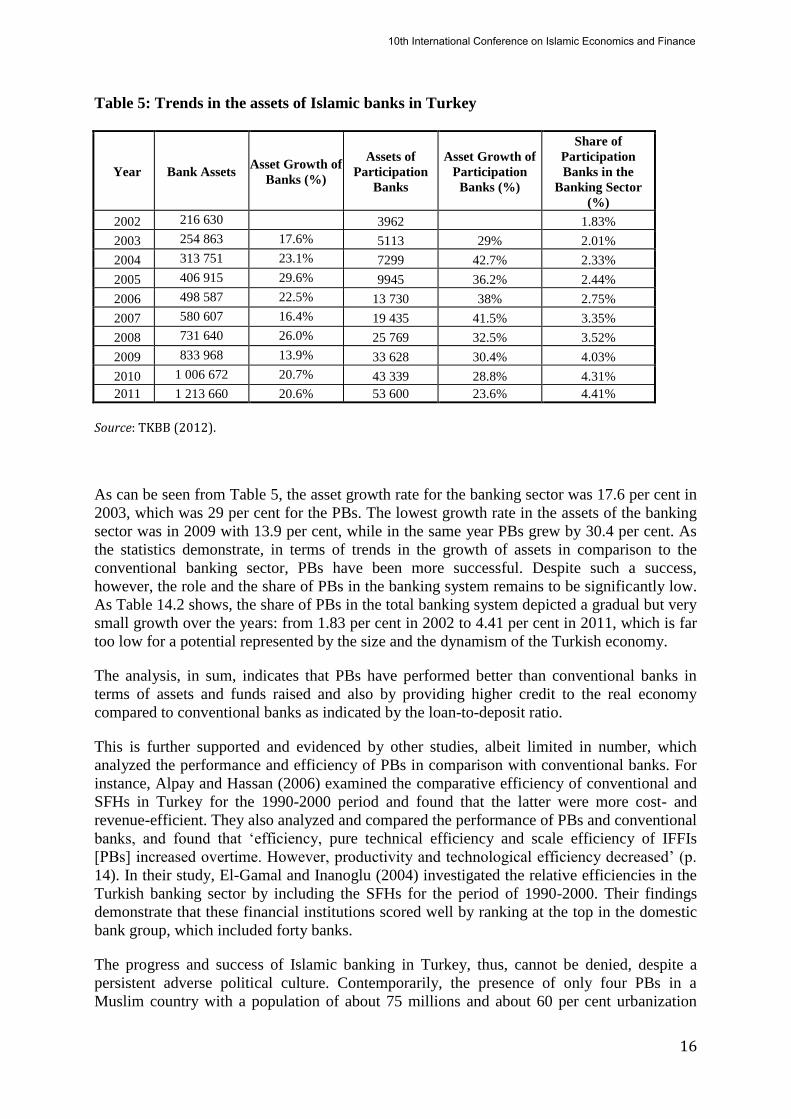

Table 5: Trends in the assets of Islamic banks in Turkey

Year Bank Assets Asset Growth of

Banks (%)

Assets of

Participation

Banks

Asset Growth of

Participation

Banks (%)

Share of

Participation

Banks in the

Banking Sector

(%)

2002 216 630 3962 1.83%

2003 254 863 17.6% 5113 29% 2.01%

2004 313 751 23.1% 7299 42.7% 2.33%

2005 406 915 29.6% 9945 36.2% 2.44%

2006 498 587 22.5% 13 730 38% 2.75%

2007 580 607 16.4% 19 435 41.5% 3.35%

2008 731 640 26.0% 25 769 32.5% 3.52%

2009 833 968 13.9% 33 628 30.4% 4.03%

2010 1 006 672 20.7% 43 339 28.8% 4.31%

2011 1 213 660 20.6% 53 600 23.6% 4.41%

Source: TKBB (2012).

As can be seen from Table 5, the asset growth rate for the banking sector was 17.6 per cent in

2003, which was 29 per cent for the PBs. The lowest growth rate in the assets of the banking

sector was in 2009 with 13.9 per cent, while in the same year PBs grew by 30.4 per cent. As

the statistics demonstrate, in terms of trends in the growth of assets in comparison to the

conventional banking sector, PBs have been more successful. Despite such a success,

however, the role and the share of PBs in the banking system remains to be significantly low.

As Table 14.2 shows, the share of PBs in the total banking system depicted a gradual but very

small growth over the years: from 1.83 per cent in 2002 to 4.41 per cent in 2011, which is far

too low for a potential represented by the size and the dynamism of the Turkish economy.

The analysis, in sum, indicates that PBs have performed better than conventional banks in

terms of assets and funds raised and also by providing higher credit to the real economy

compared to conventional banks as indicated by the loan-to-deposit ratio.

This is further supported and evidenced by other studies, albeit limited in number, which

analyzed the performance and efficiency of PBs in comparison with conventional banks. For

instance, Alpay and Hassan (2006) examined the comparative efficiency of conventional and

SFHs in Turkey for the 1990-2000 period and found that the latter were more cost- and

revenue-efficient. They also analyzed and compared the performance of PBs and conventional

banks, and found that ‘efficiency, pure technical efficiency and scale efficiency of IFFIs

[PBs] increased overtime. However, productivity and technological efficiency decreased’ (p.

14). In their study, El-Gamal and Inanoglu (2004) investigated the relative efficiencies in the

Turkish banking sector by including the SFHs for the period of 1990-2000. Their findings

demonstrate that these financial institutions scored well by ranking at the top in the domestic

bank group, which included forty banks.

The progress and success of Islamic banking in Turkey, thus, cannot be denied, despite a

persistent adverse political culture. Contemporarily, the presence of only four PBs in a

Muslim country with a population of about 75 millions and about 60 per cent urbanization

10th International Conference on Islamic Economics and Finance

17

rate is a clear indicator of a persistent sluggish growth, the reasons of which can be explained

through a political economy and behavioural approach.

However, since 2013, after the AKP government has fully established itself in the power, a

new strategy has been developed in relation to Islamic finance in line with the

‘conservatisation process’ in the country. Hence, a positive political economy impact has set

to have impact on the development of Islamic finance in the country. This may create new

opportunities; but importantly will provide legitimacy for Islamic finance in Turkey.

However, further considerations on the political use of banks in Turkey causing further

anxiety, as the government aims to develop ‘state owned Islamic banks’ which is an entirely

new experiement in the Muslim world beyond the Islamic banks owned by royal families in

the GCC. However, with the creation of state-owned Islamic banks, neo-corporatist state will

also incorporate Islamic bank within its domain and this will lead to a new model beyond

hybrid model. This causes anxiety; as the use of public banks in the developing democracies

for patronage and clientelism purpose is well documented; having the use of Islamic banks

within state domain in the same way is not something that provides confidence; however, this

for sure will provide legitimacy for Islamic finance in a laicist Turkey.

In conclusion, the contrast with the Malaysian model would be in the top-down Malaysian

model state shapes and regulates the development of Islamic finance industry but has never

attempted establishing a state-owned Islamic banks; in the Turkish case, state will have its

own Islamic banks, which represent a unique experience. In addition, the formation of mega

Islamic bank for investment only jointly by IDB and Turkey will further enhance Turkey’s

position in Islamic finance and will also shape the nature of this new model.

IX. Conclusion

IBF industries emerged in the early 1970s as part of the Islamic economics discourse, which,

as a discourse, was mainly constructed around developmentalist objectives. Further, the IME

should be considered as a reactionary response to the underdevelopment in the Muslim world,

since it aimed to construct an authentic development project on a social level through the

enhancement of the economic system of Islam. In the light of this concept, Islamic banks

were perceived as complementary institutions of this politico-economic system in terms of

financing the economic activity.

Although it was envisaged that IBF would be a central alternative model, it has failed to act

accordingly, as has been demonstrated so far, especially since the preceding discussion

indicated that a ‘commercial’ Islamic bank, by its very nature, cannot produce this outcome.

On the contrary, a civil-society-oriented model based on non-banking financial institutions

has the potential to deliver these expectations.

Given that for most of the Muslim world, even those countries which are not as high liquid as

the Gulf countries or Malaysia have moved into, or are considering, developing their IBF

industry; these countries expect that the hegemonic top-down models will bring about

developmentalism, as development needs to remain an urgent and high priority. Such nations

also include the Arab Spring countries, which have expressed their commitment towards IBF;

as a result, people in these societies have great expectations with regard to IBF in terms of job

creation, capacity developments, and poverty alleviation. A commercial bank development

path means that both the GCC and the Malaysian model will not be able to deliver this result,

since Islamic banks remain as financial intermediaries. Therefore, when attempting to meet

these expectations, the future of IBF in those countries can only be possible with community-

10th International Conference on Islamic Economics and Finance

18

oriented Islamic financing that aims to develop functioning individuals and capacity

development. This, however, requires a bottom-up process with non-banking financial

institutions as part of the civil-society-oriented development project. Thus, a consistency

between the expected aims (relating to development) and the specified institutions should be

formed, as is demonstrated by the bottom-up model of IBF formation or by the non-banking

institutionalisation method. Indeed, this is evidenced by the first experiment in IBF during the

1960s and it is further echoed by the contemporary Indonesian situation.

In concluding, it should be noted that, as a first attempt to conceptualise the industry

formation, its impact on welfare, and the developmentalist consequences of Islamic banking

and finance (IBF), this paper should be considered as a novel contribution to the field. Indeed,

it is particularly pertinent given that many people in the developing world and the Arab

Spring countries are looking to Islamic finance as a tool for economic salvation, yet in its

current, and commercial, institutionalisation, it will not be able to deliver what is expected of

it. This study therefore argues that IBF should follow a bottom-up process, beyond

commercial Islamic banks and financial institutions, in order to produce economic

development, whereby individual and social empowerment, capacity building, and

development can be achieved.

IX. Bibliography

Abdul Razak, Azila (2011). Economic and Religious Significance of the Islamic and

Conventional Pawnbroking in Malaysia: Behavioural and Perception Analysis. Unpublished

Ph.D Thesis, Durham Islamic Finance Programme, Durham University.

Antonio, Muhammad Syafii (2012). Islamic Finance in Indonesia. Lecture delivered at the

Durham Islamic Finance Programme, School of Government and International Affairs,

Durham University, UK, 2nd

May, 2012.

Asutay, M. (2007a). “Conceptualisation of the Second Best Solution in Overcoming the

Social Failure of Islamic Banking and Finance: Examining the Overpowering of

Homoislamicus by Homoeconomicus”, IIUM Journal of Economics and Management 15 (2):

167-195.

Asutay, M. (2007b). “A Political Economy Approach to Islamic Economics: Systemic

Understanding for an Alternative Economic System”, Kyoto Bulletin of Islamic Area Studies,

Special Issue: Islamic Economics- Theoretical and Practical Perspectives in a Global

Context 1 (2): 3-18.

Asutay, M. (2012). “Conceptualising and Locating the Social Failure of Islamic Finance:

Aspirations of Islamic Moral Economy vs the Realities of Islamic Finance”, Journal of Asian

and African Studies, 11(2) (Special Issue): 93-113

Asutay, M. (2013). “Developments in Islamic Banking in Turkey: Emergence, Regulation and

Performance”, in Cattelan, V. (ed.), Islamic Finance in Europe: Towards a Plural Financial

System. Cheltenham: Edward Elgar Publishing.

Azid, Toseef; Asutay, M. and Burki, U. (2007). “The Theory of Firm, Management and

Stakeholders: An Islamic Scenario”, Islamic Economics Studies, 15 (1): 1-30.

Beck, Thorsten and Levibe, Ross (2000). New Firm Formation and Industry Growth: Does

Having a Market- or Bank-Based System Matter? Washington, D.C.: World Bank, Financial

Sector Strategy and Policy Group.

Boscheck, R. (2008). Strategies, Markets and Governance: Exploring Commercial and

Regulatory Agendas. Cambridge: Cambridge University Press.

10th International Conference on Islamic Economics and Finance

19

Bugra, Ayse (1994). State and Business in Modern Turkey. Albany, NY.: State University of

New York Press.

Claessens, Stijn (2003). Corporate Governance and Development. Washington, D.C.: World

Bank.

Feldman, M. P and Francis, J. (2001). Entrepreneurs and the Formation of Industrial

Clusters. Paper presented at the Conference on Complexity and Industrial Clusters:

Dynamics, Models, National Cases, organized by the Fondazione Montedison under the aegis

of the Accademia Nazionale dei Lincei, held in Milan, Italy on June 19 and 20, 2001.

Funk, Jeffry (2010). “Complexity, Critical Mass, and Industry Formation: A Comparison of

Selected Industries, Industry and Innovation”, Industry and Innovation, 17 (5): 511-530.

Gomez, T. and Jomo, K. S. (1999). Malaysia’s Political Economy: Politics, Patronage and

Profits. Cambridge: Cambridge University Press.

Hasan, Zulkifli (2012). Shari'ah Governance in Islamic Banks. Edinburgh: Edinburgh

University Press.

Herring, Richard and Carmassi, Jacopo (2012). The Corporate Structure of International

Financial Conglomerates: Complexity and its Implications for Safety and Soundness. Oxford:

Oxford University Press.

Jomo, K. S. (1977). “Islam and Weber: Rodinson on the Implications of Religion for

Capitalist Development.”, The Developing Economies, 15 (2): 240–250.

Jomo, K. S. (2004). M Way: Mahathir’s Economic Legacy. Forum, Kuala Lumpur.

Jomo, K. S. (2001). Malaysian Eclipse: Economic Crisis and Recovery. London: Zed Books.

Kuchiki, Akifumi and Tsuji, Masatsugu (2008). The Formation of Industrial Clusters in Asia

and Regional Integration. Research Project 2008 No. 1-11, Institute of Developing

Economies – JETRO, Japan.

Mohd Nor, Shifa and Asutay, Mehmet (2011). Re-Considering CSR and Sustainability

Identity of Islamic Banks in Malaysia: An Empirical Analysis. Paper presented at the Eighth

International Conference on Islamic Economics & Finance: Sustainable Growth and Inclusive

Economic Development From an Islamic Perspective, in Doha, Qatar, on December 18-20,

2011, organised by Qatar Faculty of Islamic Studies, IAIE, IRTI and SESRIC.

Murtha, T. P. and Lenway, S. A. (2001). Managing New Industry Creation: Global

Knowledge Formation and Entrepreneurship in High Technology. Stanford: Stanford

University Press.

Peaucelle, Irina (2008). The Formation of Financial Industries in USA, France and Russia.

Working Paper No: 2008-8, Paris School of Economics, France.

Riwanjati, Nur Indah. Islamic Microfinance: Exploring Customer Behaviours and

Perceptions Indonesia (2012). Paper presented at the 6th Kyoto-Durham International

Workshop in Islamic Economics and Finance - New Horizons in Islamic Economics: Islamic

Finance & Economy and Finance in the Muslim World: Theories and Realities, 17th-18th

July 2012, jointly organised by Center for Islamic Area Studies at Kyoto University, KIAS,

Japan; and Durham Islamic Finance Doctoral Training Centre (SGIA&DBS) Durham

University, UK, held at the Durham Islamic Finance Doctoral Training Centre, Durham

University, UK.

Rudnyckyj, Daromir (2011). Spiritual Economies: Islam, Globalization, and the Afterlife of

Development. Ithaca, N.Y.: Cornell University Press.

10th International Conference on Islamic Economics and Finance

20

Tang, John P. (2006). The Role of Financial Conglomerates in Industry Formation: Evidence

from Early Modern Japan. University of California, Berkeley, mimeo. Available at:

<http://www. emlab.berkeley.edu/users/webfac/eichengreen/e211.../tang-paper.pdf>.

Walker, Gordon; Kogut, Bruce and Weijian, Shan (1997). “Social Capital, Structural Holes

and Formation of an Industry Network”, Organization Science, 8 (2): 109-125.

Wan Ahmad, Wan Marhaini (2012). Investment of Zakat in Malaysia: a Study of

Contemporary Policy and Practice in Relation to Sharia. Unpublished Ph.D Thesis, The

University of Edinburg.

Yoshida, Kentaro and Nakanishi, Machiko (2005). Factors Underlying the Formation of

Industrial Clusters in Japan and Industrial Cluster Policy: A Quantitative Survey. Discussion

Paper No. 45, Institute of Developing Economies, Japan.

Zaman, N. and Asutay, M. (2009). “Divergence between Aspirations and Realities of Islamic

Economics: A Political Economy Approach to Bridging the Divide”, IIUM Journal of

Economics and Management, 17 (1): 73-96.

10th International Conference on Islamic Economics and Finance