Embed Size (px)

Citation preview

DistinctionsbetweenBoomers’andSilentGeneration’sFinancialSecurity

TheFundamentalsThischapterassessesthefinancialsecurityofAmericansaged55+duringtheperiodof1992-2014,usingtheHealthandRetirementStudy(HRS)data.

• Wefollowthefinancialwell-beingofolderhouseholdsindifferentbirthcohorts,startingintheir50sandwellintothelastyearsoflife.

• BabyboomersarecomparedwiththeSilentGeneration.• Babyboomers’retirementsecurityoutlookisbleak.

o Babyboomers,withsubstantiallylesssavingsandmoredebt,arefoundtobefinanciallyvulnerableandinadequatelypreparedfortheirretirementandlongevity.

OverviewRelativetotheworkingpopulation,retireeshavefewersourcesofongoingincometoutilize.TheyrelyprimarilyonSocialSecurity,employer-sponsoredretirementaccounts,andIndividualRetirementAccounts(IRAs).Theopportunitiestofurtheraccumulateincome-generatingassets,suchasstocksandbonds,diminishformostpeoplepost-retirement.LifeexpectancyintheUShasalsoincreasedfrom69.7yearsin1960to78.7yearsin2015[1].However,theretirementagehasnotchangedaccordingly[2],whichmeansthatfundshavetobestretchedthinneracrossalongerlifespan.Healthcareexpendituresarealsoexpectedtocontinuerisingtoadegreethatcouldbepotentiallyprohibitiveformanyretirees.Whetherolderadultsaretrulyfinanciallypreparedfortheirretirementandlongevityhasbecomeahighlydebatabletopic[3,4,5,6,7,8,9,10,11,12].Thischapterfocusesprimarilyonthefollowingbirthcohorts:• CODA/AHEADcohort,Bornbefore1930• HRSInitialCohort,Born1931-1941• WarBabies,Born1942-1947• EarlyBabyBoomers,Born1948-1953• MidBabyBoomers,Born1954-1959

Mainfindings:• Babyboomersareinaworsefinancialpositionthanearliergenerationsof

retirees,intermsofhomeequityaccumulation,financialwealth,andtotalwealth.

o In2014,mid-boomershad30%lessintotalnetwealthand40%lessinhomeequitythanretirees10yearsolder.

o Onethirdofbabyboomershadnoretirementplanin2014whentheywereage58onaverage.Evenforthosewithplans,theiraveragebalancewaslessthan$300k.

• Whencomparedtoearliercohorts,babyboomershavealreadylaggedbehindwhenreachingtheir50s,withlowerlevelsofhomeequityandtotalwealth.

• The2008financialcrisisexacerbatedbabyboomers’under-preparednessforretirement.

o Thehousingmarketcrashcoincidedwithbabyboomers’beginningofretirement,whichdeprivedthemofhomeequitygrowthopportunities.

• Adistinctionwasfoundinpost-recessionrecoverybetweenearly-andmid-boomers.

o Forearly-boomers(theolderboomers):Onlythepoorearlyboomersexperiencedaroughandslowrecovery.

o Formid-boomers(theyoungerboomers):Thepoor,middle-class,andrichmid-boomersallexperiencedweak,orevenstagnant,recovery.

TheSpecifics

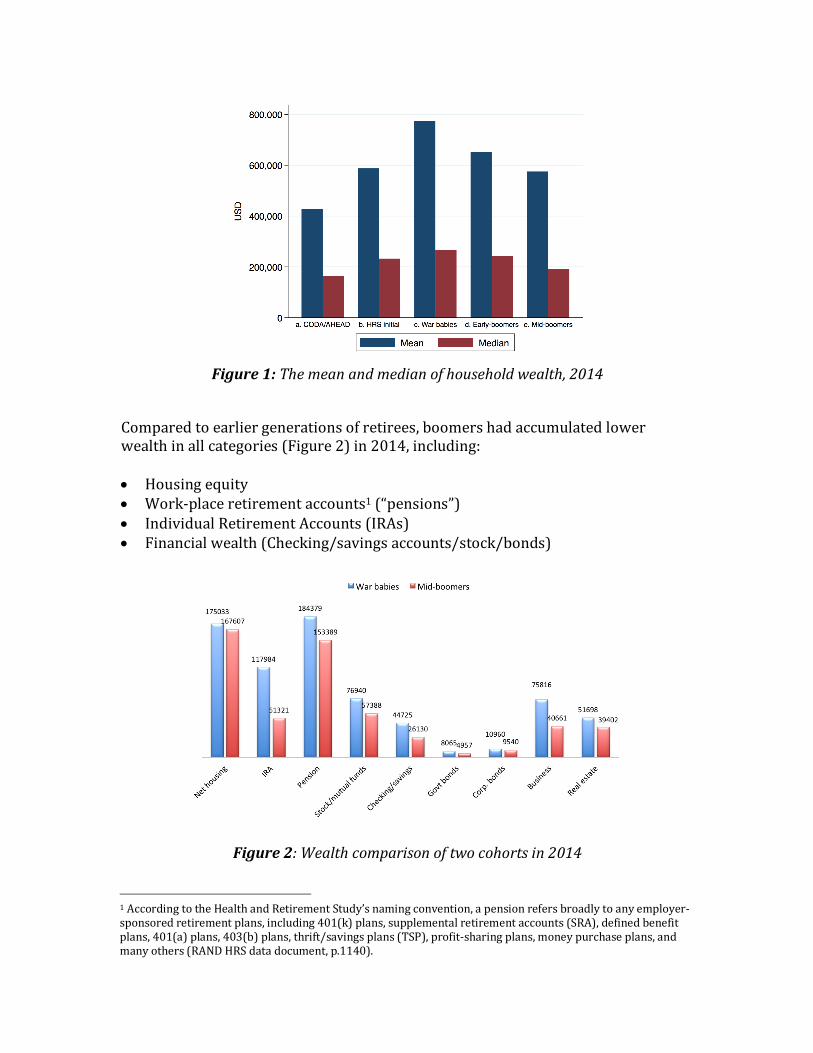

(1)ASnapshotOf2014(1.1)BoomersMeasuredLowInAllWealthCategoriesFigure(1)compareswealthbycohorts,highlightingbabyboomer’sinadequatesavings.Thisdifferenceisevenmorepronouncedthanitappears,asboomersshouldhavemoreinsavingsthantheiroldercounterparts,duetolesstimeinretirement.Theyoungestgroupinthesurvey,mid-boomers,havelesstotalwealthmeasuredbybothmeanandmedian,andtheirmedianhousingequityis40%lessthanthatoftheHRSinitialcohortandthewarbabiescohort.

Figure1:Themeanandmedianofhouseholdwealth,2014

Comparedtoearliergenerationsofretirees,boomershadaccumulatedlowerwealthinallcategories(Figure2)in2014,including:• Housingequity• Work-placeretirementaccounts1(“pensions”)• IndividualRetirementAccounts(IRAs)• Financialwealth(Checking/savingsaccounts/stock/bonds)

Figure2:Wealthcomparisonoftwocohortsin2014

1AccordingtotheHealthandRetirementStudy’snamingconvention,apensionrefersbroadlytoanyemployer-sponsoredretirementplans,including401(k)plans,supplementalretirementaccounts(SRA),definedbenefitplans,401(a)plans,403(b)plans,thrift/savingsplans(TSP),profit-sharingplans,moneypurchaseplans,andmanyothers(RANDHRSdatadocument,p.1140).

(1.2)BoomersMeasuredHighInDebtTotaldebtisthesumofhousingandnon-housingdebtobligations.Ahighdebtlevelrelativetowealthrendersfamiliesfinanciallyvulnerable,especiallyineconomichardtimes.Further,householdsthatconcentratewealthinhousingaremoresusceptibletohousingmarketfluctuations.AccordingtoLusardi,etal.[10],ahouseholdisfinanciallyvulnerableifithasahighdebt-to-assetratio,lowsavings,orcannotmeetitsdebtobligations.Comparedtoearliercohorts,boomersaremorelikelytobeindebt,andtheyhaveahigherdebtbalance(Figure3).

Figure3:Boomersmeasuredhighindebt

• About70%ofmid-boomershadatleastsomedebtin2014,comparedtoonly

20%and40%fortheCODA/AHEADandtheHRSinitialcohorts.• Amonghouseholdswithnon-zerodebt,mid-boomers’averagedebtreached

$120,000,threetimesthatoftheoldestcohort.• Moreboomerscrossedthreedangerousdebtthresholds(Figure4).

o 18%ofmid-boomershaddebtoverhalfofnetwortho 12%ofmid-boomershaddebtover80%ofnetwortho 9%ofmid-boomershaddebtover100%ofnetworth

Figure4:Debtburdensandthresholds

(1.3)BoomersHaveTheLowestBalancesInRetirementPlansWewouldexpectboomerstohavemoreonaverageintheirretirementplansthantheiroldercounterpartsin2014,asboomershadbeeninretirementforlesstime.However,datashowinadequacyinboomers’retirementplanlevels:

• About30%ofmid-boomershavezerobalancesinretirementaccounts• Amongthosewithpositiveretirementplanbalances:

o Mid-boomershaveonly$291,453onaverageo Early-boomershave$369,004onaverageo Warbabieshave$492,077onaverage.

Table1:Holdingofretirementplans,andbalances

(2)Multi-CohortComparisonsThecross-sectionalanalysisintheprevioussectionprovidesasnapshotofwealthanddebtforolderhouseholdsin2014.Thoughusefulinitsownways,itunderestimatesthesavingsinadequacyfortheboomergeneration,asitfailstotakeintoaccounttheeffectofage.Inthefollowing,wemakemulti-cohortcomparisonstoevaluatedifferentgenerationsofretireeswhentheywereatthesameage.(2.1)Wealth,Income,AndDebtFigures(5)and(6)showthedistinctionsinwealth,incomeanddebt,andhousingequityacrossfourbirthcohorts,theHRSinitialcohort,warbabies,early-boomers,andmid-boomers.Severalnotabledistinctionsacrosscohorts:

• Differentinitialconditions-o Byage55,boomerswerealreadylaggingbehindthewealthlevel

reachedbyearliergenerationsatthesameage.• Differentgrowthtrajectories-

o Earliercohortshadsignificantwealthgrowthafterage55;o Boomers’wealthstayedrelativelystagnantafterage55.

• Homeequity–o Earliercohortsenjoyedalongandsteadygrowthinhomeequity,

withstandingtheburstofthehousingbubbleinthelate2000s;o Boomerswerehitrelativelyhardbythehousingmarketcrash,with

greaterlossinequityandslowerrecovery.• Debtburdens–

o Earliercohortshadlessdebtintheir50s(about$9,000),andwereabletocutdowndebtobligationsquicklyinthefollowingyears;

o Boomershadasignificantlygreateramountofdebtintheir50s(about$43,000-46,000in2010),andasof2014,mid-boomersstillhadabout$20,000debt.

Figure5:Multicohortcomparisonofwealth,debt,andincome

Figure6:Homevalueandnetworth

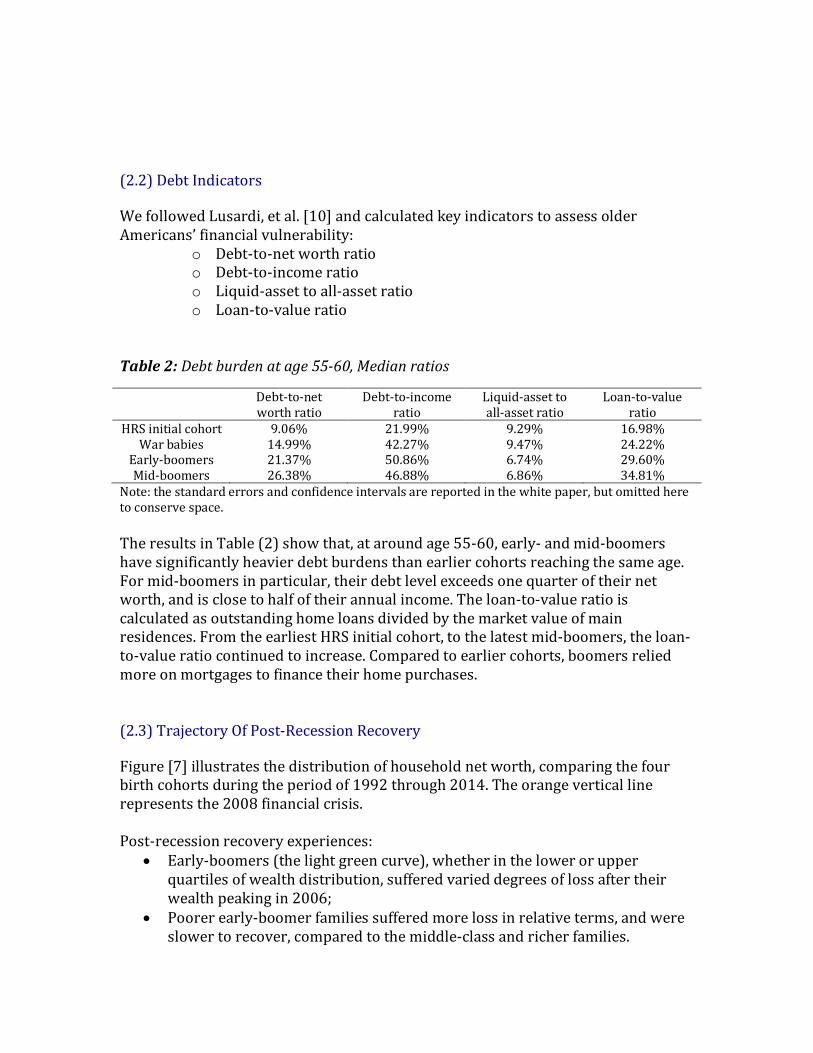

(2.2)DebtIndicatorsWefollowedLusardi,etal.[10]andcalculatedkeyindicatorstoassessolderAmericans’financialvulnerability:

o Debt-to-networthratioo Debt-to-incomeratioo Liquid-assettoall-assetratioo Loan-to-valueratio

Table2:Debtburdenatage55-60,Medianratios

Debt-to-networthratio

Debt-to-incomeratio

Liquid-assettoall-assetratio

Loan-to-valueratio

HRSinitialcohort 9.06% 21.99% 9.29% 16.98%Warbabies 14.99% 42.27% 9.47% 24.22%

Early-boomers 21.37% 50.86% 6.74% 29.60%Mid-boomers 26.38% 46.88% 6.86% 34.81%

Note:thestandarderrorsandconfidenceintervalsarereportedinthewhitepaper,butomittedheretoconservespace.

TheresultsinTable(2)showthat,ataroundage55-60,early-andmid-boomershavesignificantlyheavierdebtburdensthanearliercohortsreachingthesameage.Formid-boomersinparticular,theirdebtlevelexceedsonequarteroftheirnetworth,andisclosetohalfoftheirannualincome.Theloan-to-valueratioiscalculatedasoutstandinghomeloansdividedbythemarketvalueofmainresidences.FromtheearliestHRSinitialcohort,tothelatestmid-boomers,theloan-to-valueratiocontinuedtoincrease.Comparedtoearliercohorts,boomersreliedmoreonmortgagestofinancetheirhomepurchases.(2.3)TrajectoryOfPost-RecessionRecoveryFigure[7]illustratesthedistributionofhouseholdnetworth,comparingthefourbirthcohortsduringtheperiodof1992through2014.Theorangeverticallinerepresentsthe2008financialcrisis.Post-recessionrecoveryexperiences:

• Early-boomers(thelightgreencurve),whetherinthelowerorupperquartilesofwealthdistribution,sufferedvarieddegreesoflossaftertheirwealthpeakingin2006;

• Poorerearly-boomerfamiliessufferedmorelossinrelativeterms,andwereslowertorecover,comparedtothemiddle-classandricherfamilies.

• Thewealthiestearly-boomers(the90thpercentile)bouncedbackquicklyafterthecrisis,butthepoorestearly-boomershadyettoregaintheirpre-crisiswealthlevelby2014.

• Mid-boomersacrossthedistribution–poororrich–allhadstagnantwealthgrowthbetween2010and2014.

Figure7:Householdwealthpercentile,bycohortandyear

ConclusionThispaperanalyzedtheretirementpreparednessofolderAmericanhouseholds,byexaminingtheirnetworth,income,anddebt,anddiscussedanumberofalarmingsignsforbabyboomersregardingtheirretirementsecurityoutlook.Itiscrucialforresearchersandpolicymakerstoacknowledgethefactthatbabyboomersarefinanciallyvulnerablebasedontheircurrentsavingsanddebtburdensaselaboratedabove.Thatmessagemustbedeliveredloudandclear,becauseonlythenmayweconvincebabyboomersofthecriticalneedtocutspending,putasideemergencyfunds,andavoidpilingupnewdebts.Cuttingspendingafterretirementissomethingeasiersaidthandone.Infact,householdsspendmostoftheextramoneythattheyhaveonhand,ratherthansavingit,afterthechildrenleavehome[15].Whenitcomestoborrowing,manyolderAmericanswhooncefeltfinanciallysecurecouldeasilygodowntheslippery

slopeofaccumulatingexcessivecreditcarddebt[16].Facinghighinterestrates,someolderadultsmaybetooproudtoaskforhelpbutthenfindthemselvesunabletokeepupwiththerisingminimumpayment.Babyboomersmayalsoconsidertheoptionofworkinglonger,full-timeorpart-time,whichexpandstheiropportunitiestoaccumulatefinancialresources.AsAmericanshavebeenspendingmoretimereceivingeducationandareexpectedtolivelonger,itisnotunreasonableforthemtoconsiderthepossibilityofalaterretirementage.Theacademicworldhaspaidalotofattentiontothisissue-researchersattheStanfordCenteronLongevity,theStanfordInstituteforEconomicPolicyResearch,theCenteronAgingandWork,theCenteronRetirementResearchatBostonCollege,andtheAgeBoomAcademyatColumbiaUniversityhavealladvocatedforworkinglongerandencorecareers[16,17].Unfortunately,thecallfordelayingretirementpast65hasnotbeenwellreceivedbythepublic.MorethanhalfofAmericansretirebetweenaged61and65asof2015,and73%ofretireesreportbeingunconcernedaboutoutlivingassets;theretirementageamongmalesin2015isevenslightlybelowthatin1962[2,18].Amongthebrightspotshoweveristhatentrepreneurshipamongboomersisstrongwhencomparedtoyoungeragegroups[19],whichinvitesdiscussionsonhowpolicymakerscanhelpboomersenterandsustainsuccessfulentrepreneurship[20].Forrecentretireesandthosegettingreadytostopworking,aprogressivestrategyisindispensabletoensurefinancialsecurityforthenextthirtyyearsormore.ResearchershaveemphasizedthebenefitsofdelayingSocialSecurityretirementincome,theoptimalstrategytodrawdownonretirementassets,andadditionalstrategiestomanageexistinghousingandnon-housingassets[21,22,23,24,25].

References1.WorldBank(2017)Lifeexpectancyatbirth,total(years).Retrievedfromhttp://data.worldbank.org/indicator/SP.DYN.LE00.IN?locations=US2.Munnell,A.(2017).Whytheaverageretirementageisrising.MarketWatch.Oct15.https://www.marketwatch.com/story/why-the-average-retirement-age-is-rising-2017-10-093.Scholz,J.K.,Seshadri,A,,andKhitatrakun,S.(2006).AreAmericansSavingOptimallyforRetirement?JournalofPoliticalEconomy.August,607-643.

4.Scholz,J.K.,andSeshadri,A.(2008).AreAllAmericansSavingOptimallyforRetirement?UniversityofMichiganRetirementResearchCenter,workingpaper,2008-189.5.Biggs,A.andSchieber,S.(2014).Retireesaren'theadedforthepoorhouse.AmericanEnterpriseInstitute.January24.6.Biggs,A.(2017).Newresearchconfirms:nocrisisfortoday'sretirees.Forbes.August1,2017.Opinionsection.Retrievedfromhttps://www.forbes.com/sites/andrewbiggs/2017/08/01/new-research-confirms-no-crisis-for-todays-retirees/#560562203ac17.Munnell,A.H.,Webb,A.,andGolub-Sass,F.(2007).IsThereReallyARetirementSavingCrisis-AnNRRIAnalysis.AnIssueinBrief.CenterforRetirementResearchatBostonCollege,August,No.7-11.8.Poterba,J.(2014).RetirementSecurityinanAgingPopulation.AmericanEconomicReview:Papers&Proceedings,104(5).9.Munnell,A.,Hou,W,andSanzenbacher,G.(2018).NationalRetirementRiskIndexShowsModestImprovementin2016.CenterforRetirementResearch,BostonCollege.Retrievedfromhttp://crr.bc.edu/briefs/national-retirement-risk-index-shows-modest-improvement-in-2016/10.Lusardi,A.,Mitchell,O.,andOggero,N.(2017).DebtandFinancialVulnerabilityontheVergeofRetirement.GlobalFinancialLiteracyExcellenceCenter,workingpaperseriesWP2017-1.Retrievedfromhttp://gflec.org/wp-content/uploads/2017/06/WP-2017-1-Debt-and-Financial-Vulnerability-on-the-Verge-of-Retirement.pdf?x8765711.Lusardi,A.,andMitchell,O.(2007).BabyBoomerRetirementSecurity:TheRolesofPlanning,FinancialLiteracyandHousingWealth.JournalofMonetaryEconomics,54(1),205-224.12.Lusardi,A.,andMitchell,O.(2011).FinancialLiteracyandRetirementPlanningintheUnitedStates.JournalofPensionEconomicsandFinance,10(4),509-525.13.Lusardi,A.,Mitchell,O.,andOggero,N.(2018).TheChagingFaceofDebtandFinancialFragilityatOlderAges.AEAPapersandProceedings,108:407–41114.Dushi,I.,Munnell,A.H.,Sanzenbacher,G.T.,,Webband,A.,Chen,A.(2016).DoHouseholdsSaveMoreWhentheKidsLeaveHome?CenterforRetirementResearchatBostonCollege,Brief,IB16-8.

15.Pham,S.(2011).RetirementsSwallowedbyDebt.NewYorkTimes,January26.Retrievedfromhttps://newoldage.blogs.nytimes.com/2011/01/26/retirements-swallowed-by-debt/16.Clark,R.,Hammond,R.,Morrill,M.,andPathak,A.(2015).Workafterretiring:work-lifetransitionsofpublicemployeesinNorthCarolina.Workingpaper.2015SIEPRConferenceonWorkingLongerandRetirement.StanfordUniversity.17.Goldin,C.,andKatz,L.F.(2018).WomenWorkingLonger,IncreasedEmploymentAtOlderAges.TheUniversityofChicagoPressBook.18.LIMRASecureRetirementInstitute(2015).RetirementIncomeReferenceBook.PresentationtoFederalAdvisoryCommitteeonInsurance.19.Ozkal,D.(2016)MillennialsCan’tKeepupWithBoomerEntrepreneurs.KauffmanFoundation.Retrievedfromhttps://www.kauffman.org/blogs/currents/2016/07/age-and-entrepreneurship20.Lusardi,A.,Christelis,D,andScheresberg,C.(2016).EntrepreneurshipamongBabyBoomers:RecentevidencefromtheHealthandRetirementStudy.GlobalFinancialLiteracyExcellenceCenter,PolicyBrief.21.Ramnath,S.,Shoven,J.,andSlavov,S.(2017).Pathwaystoretirementandtheself-employed.StanfordInsituteforEconomicPolicyResearch,discussionpaperNo.17-002.22.Nyce,S.,Schieber,S.,Shoven,J.,Slavov,S,andWise,D.(2015).SurveyresultsforDBretirees:lump-sumvs.annuitiesandsocialsecurityclaimingbehavior.2015SIEPRConferenceonWorkingLongerandRetirement.StanfordUniversity.23.Bronshtein,G.,Scott,J.,Shoven,J.,andSlavov,S.(2016).Leavingbigmoneyonthetable:arbitrageopportunitiesindelayingsocialsecurity.NBERworkingpaperno.22853.24.Pfau,W.,Tomlinson,J.,andVernon,S.(2017).OptimizingRetirementIncomebyIntegratingRetirementPlans,IRAs,andHomeEquity-Aframeworkforevaluatingretirementincomedecisions.StanfordCenteronLongevity,workingpaper.Retrievedfromhttp://longevity.stanford.edu/wp-content/uploads/2017/11/Optimizing-Retirement-Income-Solutions-November-2017-SCL-Version.pdf25.Armour,P.,andHung,A.(2017).Drawingdownretirementwealth:interactionsbetweensocialsecuritywealthandprivateretirementsavings.RANDworkingpaper1165.