Embed Size (px)

Citation preview

Digital Advertising SeminarDisruption, Consolidation and Growth

September 9, 2014

1

WCP Overview

Woodside Capital Partners is a global, independent investment bank that deliversworld-class strategic and financial advice to emerging growth companies intechnology sectors

Founded in 2001: over $10 billion in transaction value

M&A, private placement/strategic partnership and corporate finance advisory— Hardware: Semiconductors, Electronics, and Enabling Materials— Software, Digital Media/Advertising and Internet— Special Situations

30 professionals; backgrounds as entrepreneurs/CEOs and from top investmentbanks

Silicon Valley-based, with offices in London – 1/3 of transactions are cross-border

Silicon Valley headquarters of M&A International

WCP Research team offers technology research serving buy-side institutionalinvestors and technology industry executives

I. Disruption and Consolidation

II. Growth Drivers

III. The Holy Grail

IV. Industry Consolidation

V. Trends and Predictions

AGENDA

2

High Tech and Big Data Meet Don Draper

Shift to Digital Media (Internet and Mobile)Ongoing

Disruption of Advertiser / Agency / PublisherRelationship

Rapid Growth in Programmatic / RTB

Fragmented Landscape = Opportunity

Disruption and Consolidation

3

High Tech Meets Don Draper

4

5

Big Data Meets Don Draper

200MS: THE LIFE OF A PROGRAMMATIC RTB AD IMPRESSION

6%

14%

42%

26%

12%

23%

10%

43%

22%

3%0%

10%

20%

30%

40%

50%

Print Radio TV Internet Mobile

Ad Spending vs. Media Consumption% Time Spent

% Ad Spent $30B+ MarketOpportunity (USA)

% Ad Spending

More Spending Will Shift to Mobile

Source: KPCB, Internet Trends 2013 6Internet Ad = $37B Mobile Ad = $4B

4%

9%

$0.40$1.00

Self

Serv

e

DSP

Ad S

erve

r

Exch

ange

Othe

r

Data

Pla

tformDisplay

Mobile

Video

PublishersAdvertisers

Intermediary Tax $0.60

7

Disruption of Advertiser / Agency / Publisher Relationship

8

$2.9$3.8

$4.9$6.5 $7.1 $7.5

$0.1

$0.5

$1.4

$2.9

$4.9

$6.8

$0.1

$0.5

$1.1

$2.0

$3.1

$3.8

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2013 2014 2015E 2016E 2017E 2018E

RTB Ad Sales Market (US)

Video

Mobile

Desktop Display

Rapid Growth in Programmatic

Source: BI Intelligence, The Programmatic Advertising Report; 8/29/2014

9

Fragmented Industry = Consolidation Opportunity

I. Disruption and Consolidation

II. Growth Drivers

III. The Holy Grail

IV. Industry Consolidation

V. Trends and Predictions

AGENDA

10

Programmatic and Real-Time Bidding

Cross-Screen Advertising

Growth in Mobile Usage

Video Advertising

Improved Analytics and Attribution

11

Major Growth Drivers

I. Disruption and Consolidation

II. Growth Drivers

III. The Holy Grail

IV. Industry Consolidation

V. Trends and Predictions

AGENDA

12

13

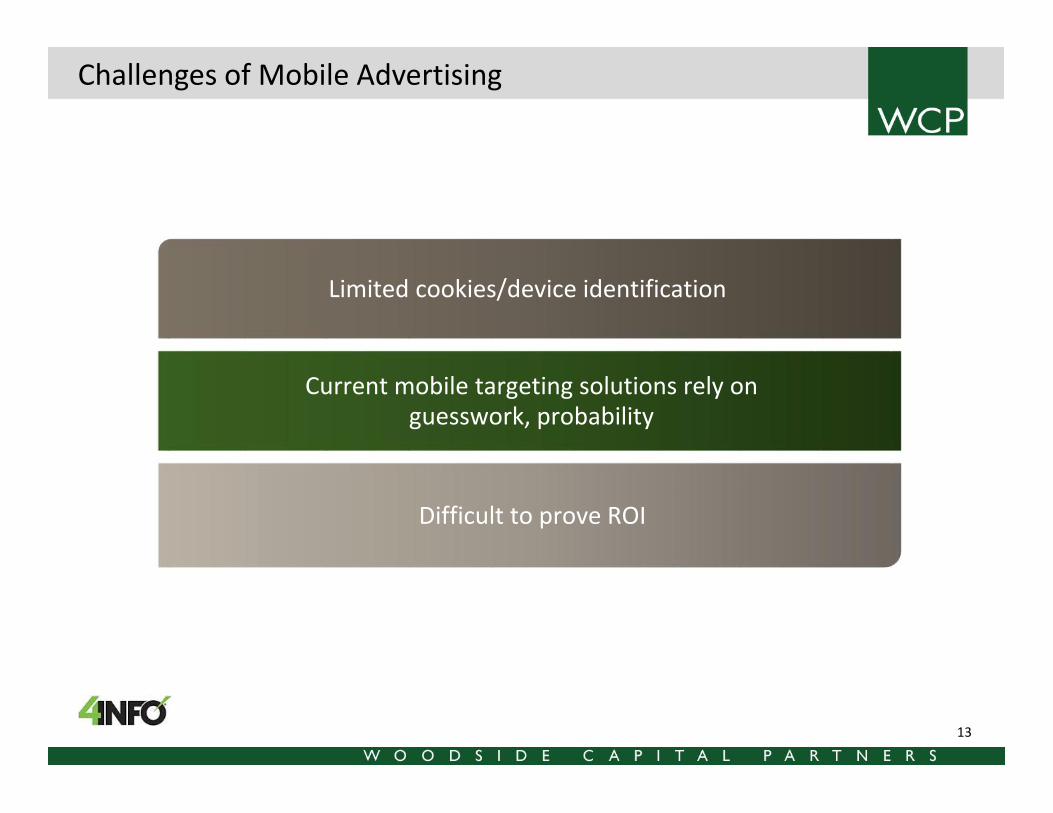

Limited cookies/device identification

Current mobile targeting solutions rely onguesswork, probability

Difficult to prove ROI

Challenges of Mobile Advertising

Ad Requests

Ad Requests

Ad Requests

Ad Requests

Ad Request(s)

Ad Requests

Ad Requests

Ad Requests

Ad RequestsAd Requests

Ad Requests

4Info used advanced technologies andgeocoding to map every U.S. household

to lat / long.

4Info analyzed billions of ad requests usingpatented clustering algorithms.

Ad Requests

14

Leveraging Big Data

Enabling Targeting and Attribution Across Screens

Frequent Shopper Data

Point-of-Sale Data

Warranty Registrations

Panels & Surveys

Credit Card Data

Attribution Platforms

152 Million

101 Million

300 Million

TargetingTargeting AttributionAttribution

15

Persistent Mobile ID Enables Cross-Screen Campaigns

Situation Challenge: New Product

Launch

Approach: Driveawareness

Success criteria: Paybackfor media spend,incremental volume

Source: NCS Sales-Effect Analysis

Custom CampaignCategory:Sports Drinks

Target: Target 1: Category A AND

Category B (75%) Target 2: Category B (25%)

Reach:2 MM Households

Impressions:8 M

ResultsThe average householdspend on mobile was almostdouble that of display

Payback(per $1spent)

$4.86

$587kIncremental

Sales

16

4INFO Case Study: BuyerVision Mobile

17

$0

$10

$20

$30

$40

$50

$60

$70

CRTO

MRIN

MM

FUEL

RUBI

SZMK

TRMR

TUBE

Public Companies Have Lost Value but Still Have Cash

Source: CapitalIQ and Woodside Capital Partners estimates; 9/4/2014

18

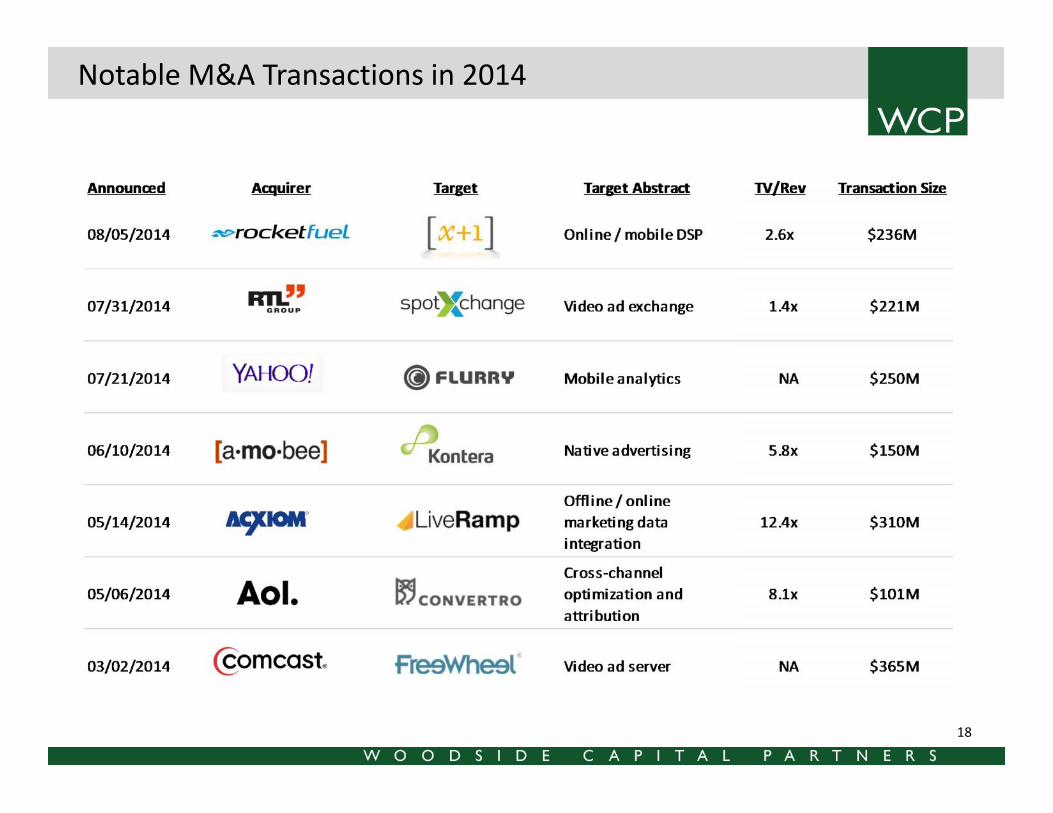

Notable M&A Transactions in 2014

I. Disruption and Consolidation

II. Growth Drivers

III. The Holy Grail

IV. Industry Consolidation

V. Trends and Predictions

AGENDA

19

Video, Mobile, Native Grow Faster Than Display, Search

Increased Verticalization by Brands and Agencies

Consolidation of Adjacent Players -> Enterprise AdvertisingManagement Systems (EAMS)

Programmatic Extends to Old School Television

Apple / Google Enter Mobile Payments with Attribution Loop

Google, Apple, Facebook, Amazon, Adobe, SFDC, AOL,Microsoft, Oracle, Yahoo Extend Their Reach

Waves of Acquisition: Ad Exchanges, DSPs, Video, Mobile,Cross-Screen, Attribution

20

Trends and Predictions

WCP Research

WCP Banking

21

Tricia SalineroManaging Director+1 650 421 6547

Ron HellerManaging Director+1 650 513 2762

Ed BierdemanSoftware Analyst and Managing Director

+1 650 387 [email protected]

Marshall SenkSoftware Analyst and Managing Director

+1 949 284 [email protected]

WCP Contact Info

22

WCP Office Info – Silicon Valley and UK Presence

Silicon Valley Offices1530 Page Mill Road, Suite 200Palo Alto, California 94304Tel: +1 650 513 2775

UK OfficesIbex House42-47 MinoriesLondon, EC3N 1DY, UKTel: +44 7989 384590

Q&A

23

Q&A

Internet of Things Seminar

-- November 2014, Date TBD

Open Stack Seminar

-- December 2014, Date TBD

Mergers and Acquisitions in Silicon Valley Gathering

-- January 21 & 22, 2015

24

Upcoming Events

25

MASiV Gathering – January 21 & 22, 2015

Representative 2014 Attendees:

Consumer Internet and Mobile:Andreessen Horowitz – Jamie McGurk, PartnerDeloitte – Garrett Herbert, Partner, M&AGoogle – Dave Sobota, Sr Dir, Corp DevIntuit – Kevin Jacques, Director, Corp DevOpera Software – Erik Harrell, CFOSquare – Rishi Garg, Head, Corp DevTelefonica Digital – Jennifer Vancini, Sr Dir, Bus DevVISA – Lester Liu, Global M&A and Corp DevYahoo! – Steven Fan, Mobile Corp Dev

Cloud and Enterprise:Autodesk – David Hindley, Sr Dir, Corp DevBox – Niall Wall, SVP, Business and Corp DevBMC Software – Clarence Hinton, VP, Corp DevCitrix – Mike Cristinziano, Corp VPEMC – Matt Olton, SVP, Corp DevIBM – Claudia Munce, VP, Strategy and VentureSalesforce – John Somorjai, SVP, Corp DevSamsung – Kevin Morrow, VP, Partnership & Bus DevSAP – Monty Gray, Corp DevSAP Cloud – Roy Ng, SVP and COOStorm Ventures – Jason Lemkin, Managing Director