Embed Size (px)

Citation preview

Dish TV India LimitedInvestor Presentation

Some of the statements made in this presentation are forward‐looking statements and are based on the current beliefs,assumptions, expectations, estimates, objectives and projections of the directors and management of Dish TV India Limitedabout its business and the industry and markets in which it operates.

These forward‐looking statements include, without limitation, statements relating to revenues and earnings. The words“believe”, “anticipate”, “expect”, “estimate", "intend”, “project” and similar expressions are also intended to identify forwardlooking statements.

These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some ofwhich are beyond the control of the Company and are difficult to predict. Consequently, actual results could differ materiallyfrom those expressed or forecast in the forward‐looking statements as a result of, among other factors, changes in economic andmarket conditions, changes in the regulatory environment and other business and operational risks. Dish TV India Limited doesnot undertake to update these forward‐looking statements to reflect events or circumstances that may arise after publication.

Disclaimer

2

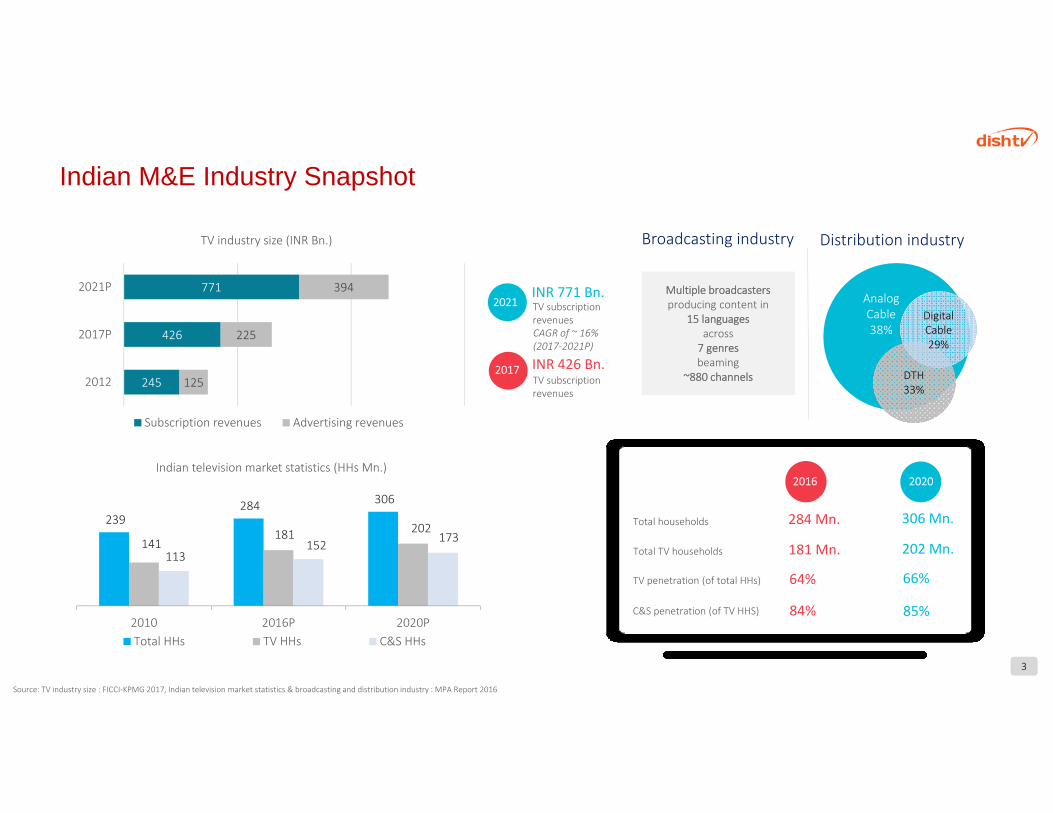

INR 771 Bn.TV subscription revenues

INR 426 Bn.TV subscription revenues

66%TV penetration (of total HHs) 64%

C&S penetration (of TV HHS)

Indian M&E Industry Snapshot

2017

2021

239 284 306

141 181 202

113 152 173

2010 2016P 2020PTotal HHs TV HHs C&S HHs

Indian television market statistics (HHs Mn.)

Source: TV industry size : FICCI‐KPMG 2017, Indian television market statistics & broadcasting and distribution industry : MPA Report 2016

2016 2020

Total households

84% 85%

CAGR of ~ 16% (2017‐2021P)

306 Mn.284 Mn.

Total TV households 202 Mn.181 Mn.

Distribution industry

DTH33%

Analog Cable38%

DigitalCable29%

Broadcasting industry

Multiple broadcastersproducing content in

15 languagesacross 7 genresbeaming

~880 channels

3

245

426

771

125

225

394

2012

2017P

2021P

TV industry size (INR Bn.)

Subscription revenues Advertising revenues

Distribution Industry

4

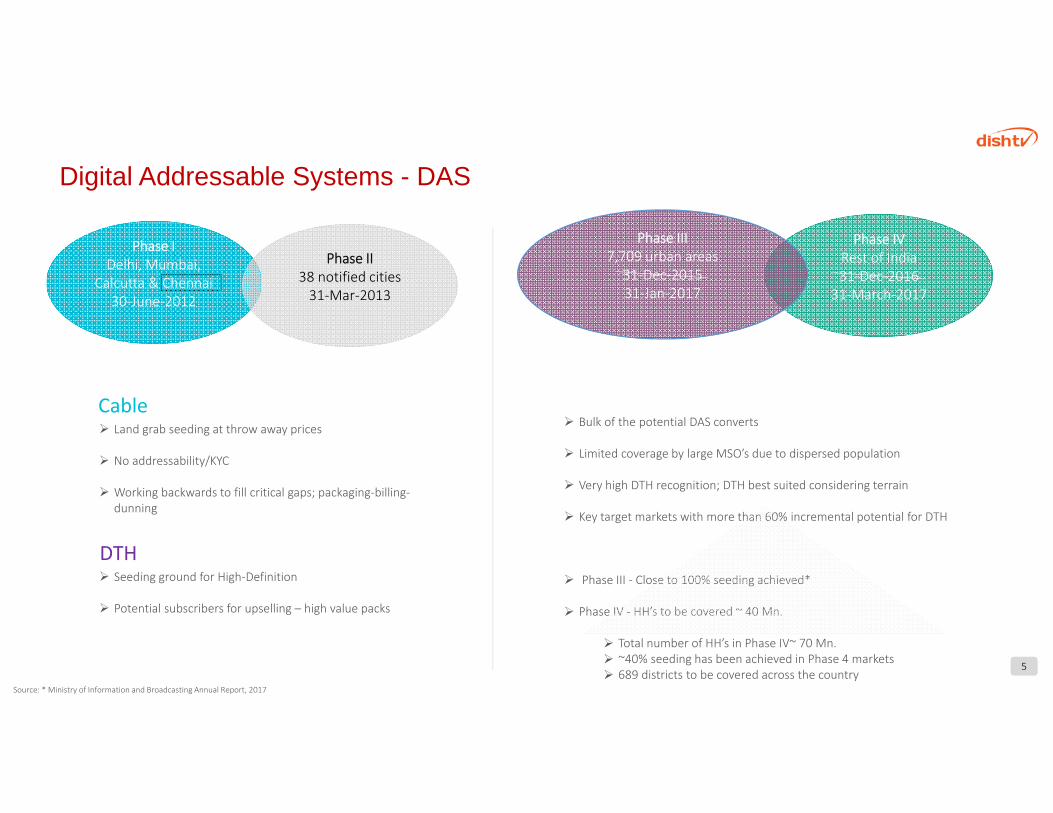

Digital Addressable Systems - DAS

Phase IDelhi, Mumbai,

Calcutta & Chennai30‐June‐2012

Phase II38 notified cities31‐Mar‐2013

Cable Land grab seeding at throw away prices

No addressability/KYC

Working backwards to fill critical gaps; packaging‐billing‐dunning

DTH Seeding ground for High‐Definition

Potential subscribers for upselling – high value packs

Bulk of the potential DAS converts

Limited coverage by large MSO’s due to dispersed population

Very high DTH recognition; DTH best suited considering terrain

Key target markets with more than 60% incremental potential for DTH

Phase III ‐ Close to 100% seeding achieved*

Phase IV ‐ HH’s to be covered ~ 40 Mn.

Total number of HH’s in Phase IV~ 70 Mn. ~40% seeding has been achieved in Phase 4 markets 689 districts to be covered across the country

5

Phase IVRest of India31‐Dec‐2016

31‐March‐2017

Phase III7,709 urban areas

31‐Dec‐2015 31‐Jan‐2017

Source: * Ministry of Information and Broadcasting Annual Report, 2017

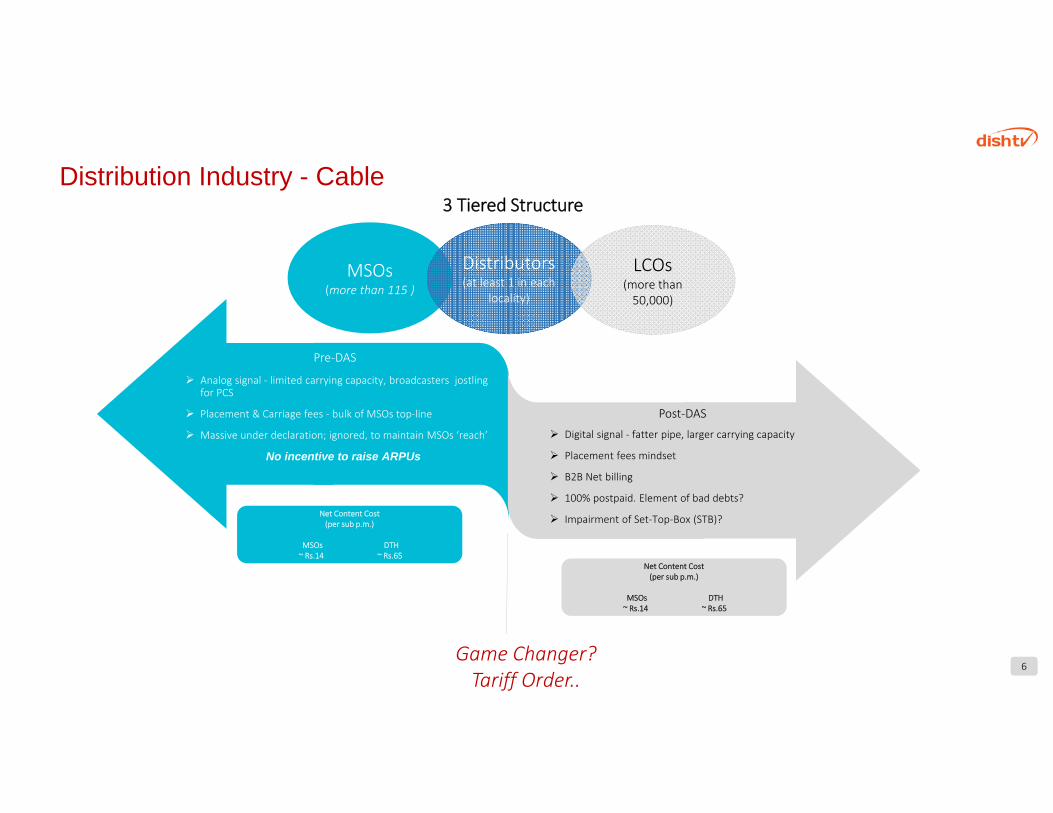

Distribution Industry - Cable 3 Tiered Structure

MSOs(more than 115 )

Distributors (at least 1 in each

locality)

LCOs (more than 50,000)

Pre‐DAS

Post‐DAS

6

Analog signal ‐ limited carrying capacity, broadcasters jostling for PCS

Placement & Carriage fees ‐ bulk of MSOs top‐line

Massive under declaration; ignored, to maintain MSOs ‘reach’

No incentive to raise ARPUs

Digital signal ‐ fatter pipe, larger carrying capacity

Placement fees mindset

B2B Net billing

100% postpaid. Element of bad debts?

Impairment of Set‐Top‐Box (STB)?

Game Changer? Tariff Order..

Net Content Cost (per sub p.m.)

MSOs DTH~ Rs.14 ~ Rs.65

Net Content Cost (per sub p.m.)

MSOs DTH~ Rs.14 ~ Rs.65

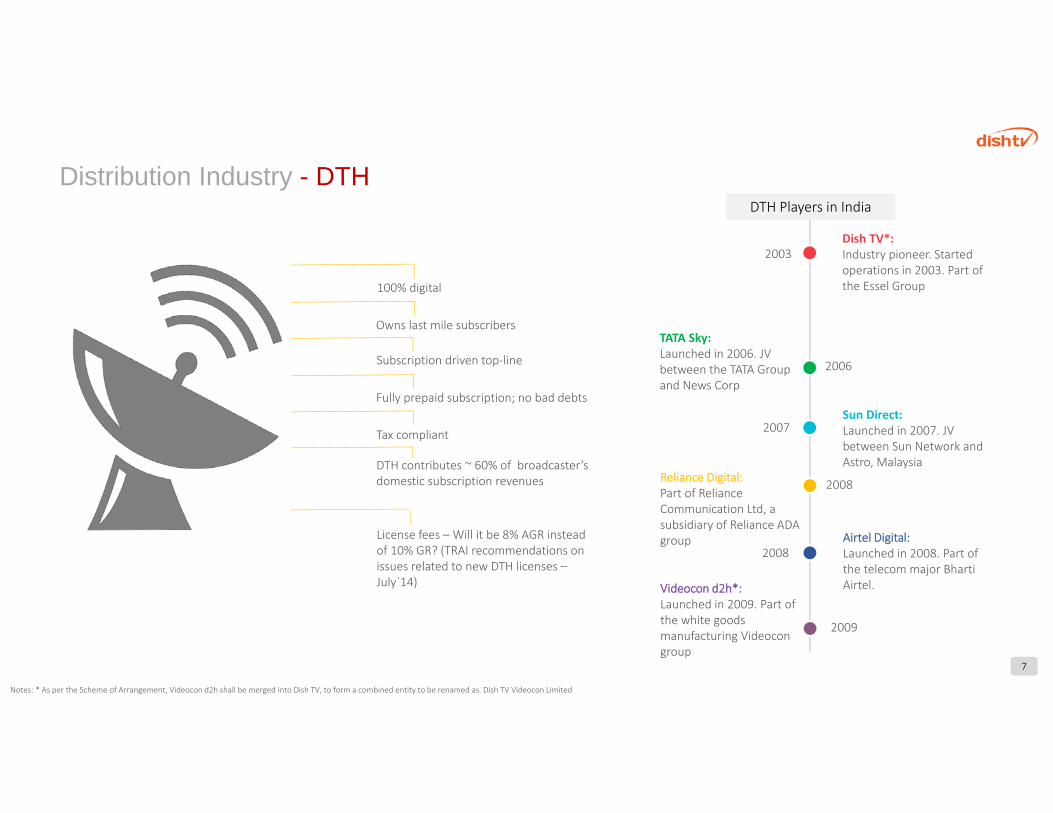

Dish TV*:Industry pioneer. Started operations in 2003. Part of the Essel Group

TATA Sky:Launched in 2006. JV between the TATA Group and News Corp

Sun Direct:Launched in 2007. JV between Sun Network and Astro, Malaysia

Reliance Digital:Part of Reliance Communication Ltd, a subsidiary of Reliance ADA group Airtel Digital:

Launched in 2008. Part of the telecom major Bharti Airtel.Videocon d2h*:

Launched in 2009. Part of the white goods manufacturing Videocon group

Distribution Industry - DTH

2003

2006

2007

2008

2009

100% digital

Owns last mile subscribers

Subscription driven top‐line

Fully prepaid subscription; no bad debts

DTH contributes ~ 60% of broadcaster’s domestic subscription revenues

License fees – Will it be 8% AGR instead of 10% GR? (TRAI recommendations on issues related to new DTH licenses –July`14)

Tax compliant

2008

7

DTH Players in India

Notes: * As per the Scheme of Arrangement, Videocon d2h shall be merged into Dish TV, to form a combined entity to be renamed as Dish TV Videocon Limited

8

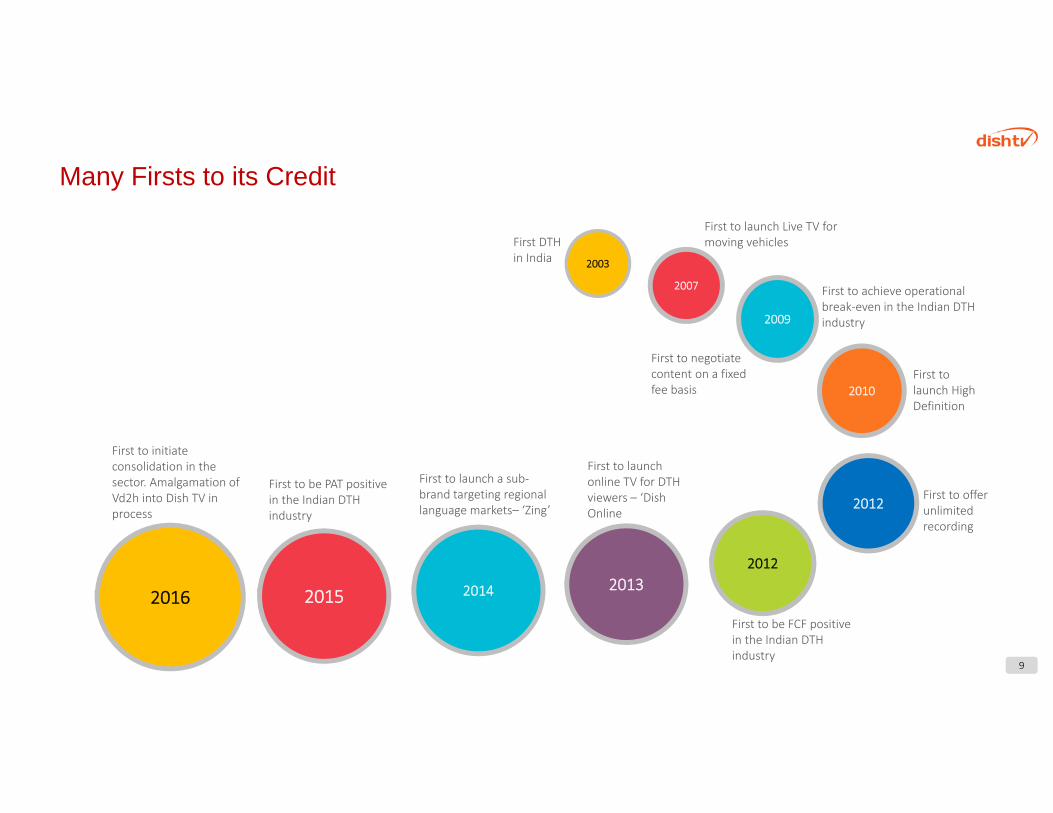

Many Firsts to its Credit

9

2007

2009

2010

2012

2012201320142015

2003

2016

First DTH in India

First to negotiate content on a fixed fee basis

First to launch Live TV for moving vehicles

First to achieve operational break‐even in the Indian DTH industry

First to launch High Definition

First to offer unlimited recording

First to be FCF positive in the Indian DTH industry

First to launch online TV for DTH viewers – ‘Dish Online

First to launch a sub‐brand targeting regional language markets– ‘Zing’

First to be PAT positive in the Indian DTH industry

First to initiate consolidation in the sector. Amalgamation of Vd2h into Dish TV in process

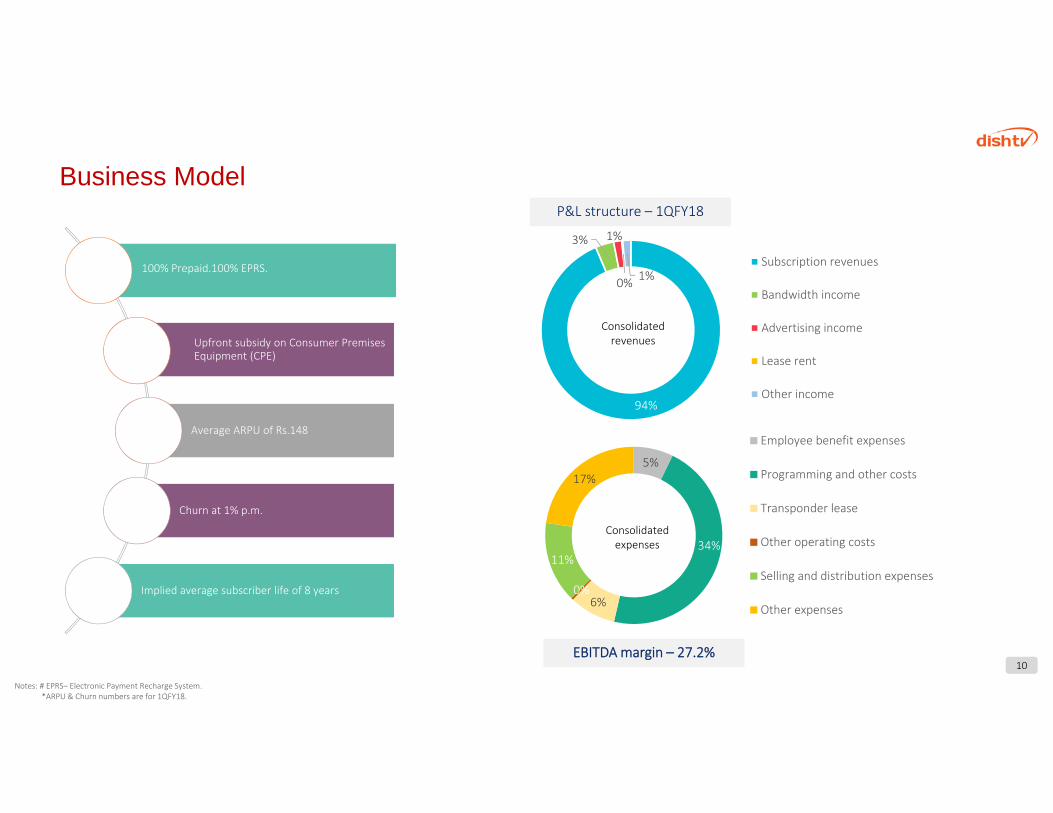

94%

3% 1%

0% 1%Subscription revenues

Bandwidth income

Advertising income

Lease rent

Other income

Consolidated revenues

5%

34%

6%0%

11%

17%

Employee benefit expenses

Programming and other costs

Transponder lease

Other operating costs

Selling and distribution expenses

Other expenses

Consolidated expenses

Dish TV India Limited

Business Model

10

P&L structure – 1QFY18

EBITDA margin – 27.2%

Notes: # EPRS– Electronic Payment Recharge System.*ARPU & Churn numbers are for 1QFY18.

100% Prepaid.100% EPRS.

Upfront subsidy on Consumer Premises Equipment (CPE)

Average ARPU of Rs.148

Churn at 1% p.m.

Implied average subscriber life of 8 years

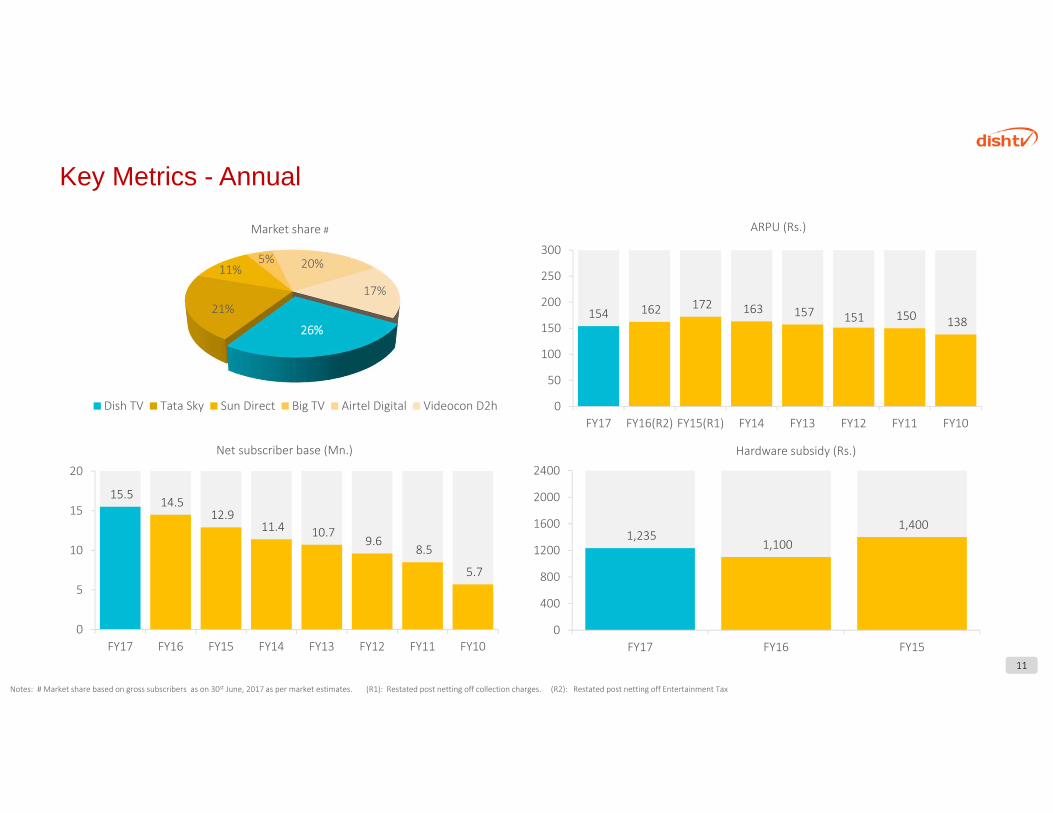

Key Metrics - Annual

Notes: # Market share based on gross subscribers as on 30st June, 2017 as per market estimates. (R1): Restated post netting off collection charges. (R2): Restated post netting off Entertainment Tax

154 162 172 163 157 151 150 138

0

50

100

150

200

250

300

FY17 FY16(R2) FY15(R1) FY14 FY13 FY12 FY11 FY10

ARPU (Rs.)

26%

21%

11%5% 20%

17%

Dish TV Tata Sky Sun Direct Big TV Airtel Digital Videocon D2h

Market share #

1,235 1,100

1,400

0

400

800

1200

1600

2000

2400

FY17 FY16 FY15

Hardware subsidy (Rs.)

15.5 14.5

12.9 11.4 10.7

9.6 8.5

5.7

0

5

10

15

20

FY17 FY16 FY15 FY14 FY13 FY12 FY11 FY10

Net subscriber base (Mn.)

11

Key Metrics - Annual

Notes: (R1) Restated, post netting off collection charges. (R2) Restated post netting off Entertainment Tax. * Including deferred tax assets of Rs. 740 and Rs. 4,360 mn. for FY17 and FY16 respectively

9,728 10,249

7,331 6,240 5,794

4,960

2,380 1,117

‐20000

2000400060008000100001200014000

FY17 FY16 FY15 FY14 FY13 FY12 FY11 FY10

EBITDA (Rs. Mn.)

30% 29.6% 30% 31% 30% 31%35%

40%

0%

10%

20%

30%

40%

50%

60%

FY17 FY16(R2) FY15(R1) FY14 FY13 FY12 FY11 FY10

27,696 26,617 24,499

22,681 19,228

16,639

11,927 8,353

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY17 FY16(R2) FY15(R1) FY14 FY13 FY12 FY11 FY10

Subscription revenues (Rs. Mn.)

Programming and other costs as % of revenues

1,093

6,924

31

(1,576)(660) (1,331)

(1,920)(2,622)

‐5500

‐3500

‐1500

500

2500

4500

6500

8500

FY17 FY16 FY15 FY14 FY13 FY12 FY11 FY10

Net profit/(loss) (Rs. Mn.)

12

*

*

Key Metrics - Quarterly

0.186 0.165

0.402

00.10.20.30.40.50.6

1QFY18 4QFY17 1QFY17

Net subscriber additions (Mn.)

148

134

165

110120130140150160170180

1QFY18 4QFY17 1QFY17

ARPU (Rs.)

6,917 6,205

7,282

0

2000

4000

6000

8000

10000

1QFY18 4QFY17 1QFY17

Subscription revenues (Rs. Mn.)

2,012 1,951

2,610 27.2%

27.5%

33.5%

20.0%21.0%22.0%23.0%24.0%25.0%26.0%27.0%28.0%29.0%30.0%31.0%32.0%33.0%34.0%35.0%36.0%37.0%38.0%39.0%40.0%41.0%42.0%43.0%44.0%45.0%

0

500

1000

1500

2000

2500

3000

1QFY18 4QFY17 1QFY17

EBITDA (Rs. Mn.) & EBITDA margin

(139) (291)

361

‐300

1200

2700

4200

1QFY18 4QFY17 1QFY17

Net profit (Rs. Mn.)

108 160

622

0

300

600

900

1200

1500

1QFY18 4QFY17 1QFY17

FCF (Rs. Mn.)

13Notes: *4QFY17 & 1QFY17 figures are restated to comply with Ind‐AS

#

Strategy and Outlook

14

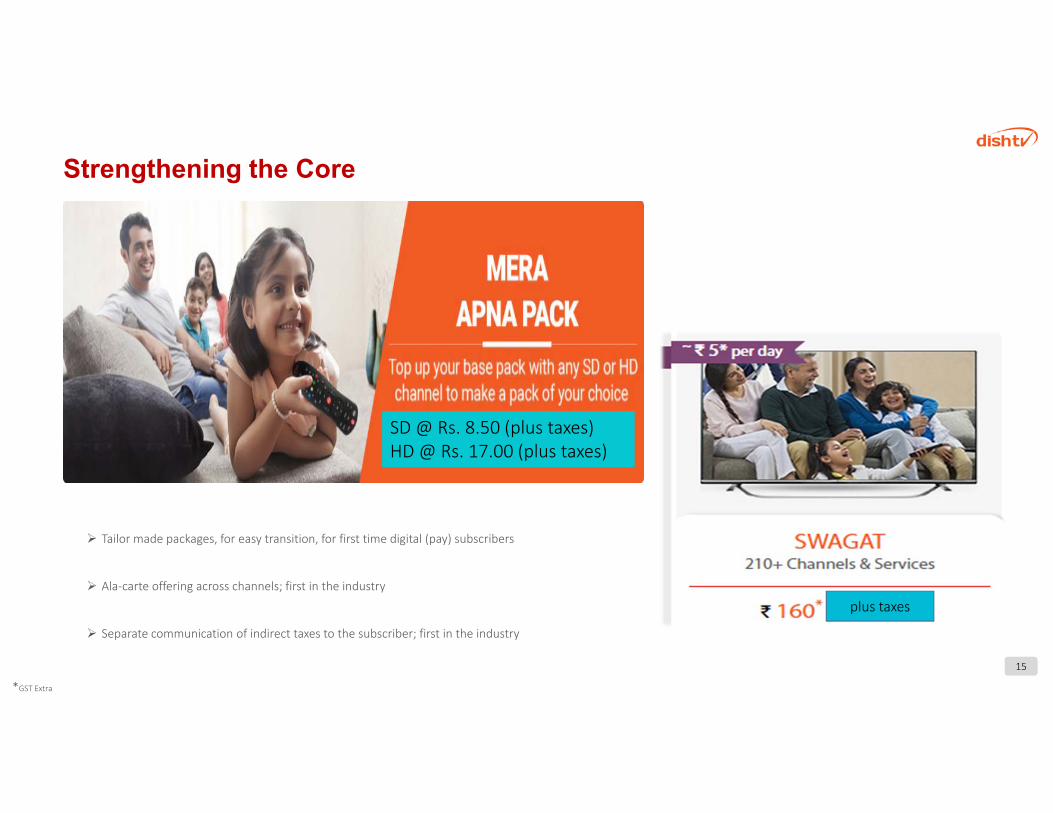

Strengthening the Core

15

Tailor made packages, for easy transition, for first time digital (pay) subscribers

Ala‐carte offering across channels; first in the industry

Separate communication of indirect taxes to the subscriber; first in the industry

*GST Extra

SD @ Rs. 8.50 (plus taxes)HD @ Rs. 17.00 (plus taxes)

plus taxes

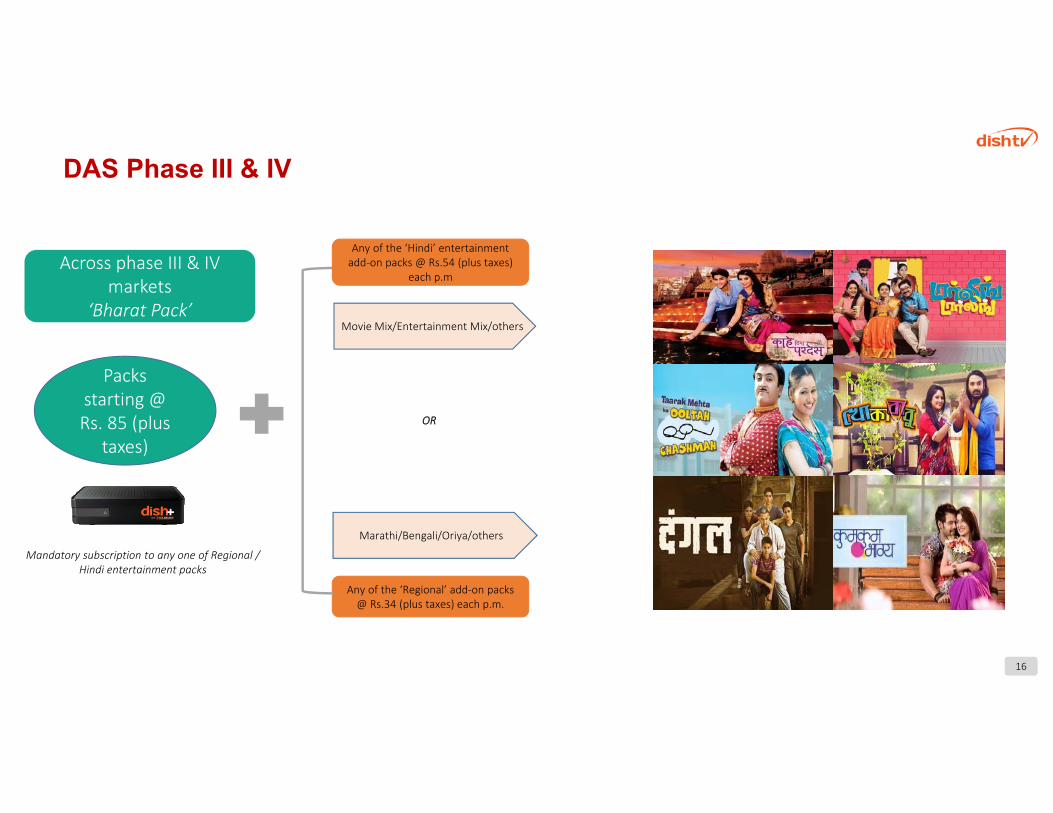

DAS Phase III & IV

16

Across phase III & IV markets

‘Bharat Pack’

Mandatory subscription to any one of Regional / Hindi entertainment packs

Any of the ‘Regional’ add‐on packs @ Rs.34 (plus taxes) each p.m.

OR

Movie Mix/Entertainment Mix/others

Marathi/Bengali/Oriya/others

Any of the ‘Hindi’ entertainment add‐on packs @ Rs.54 (plus taxes)

each p.m

Packs starting @ Rs. 85 (plus

taxes)

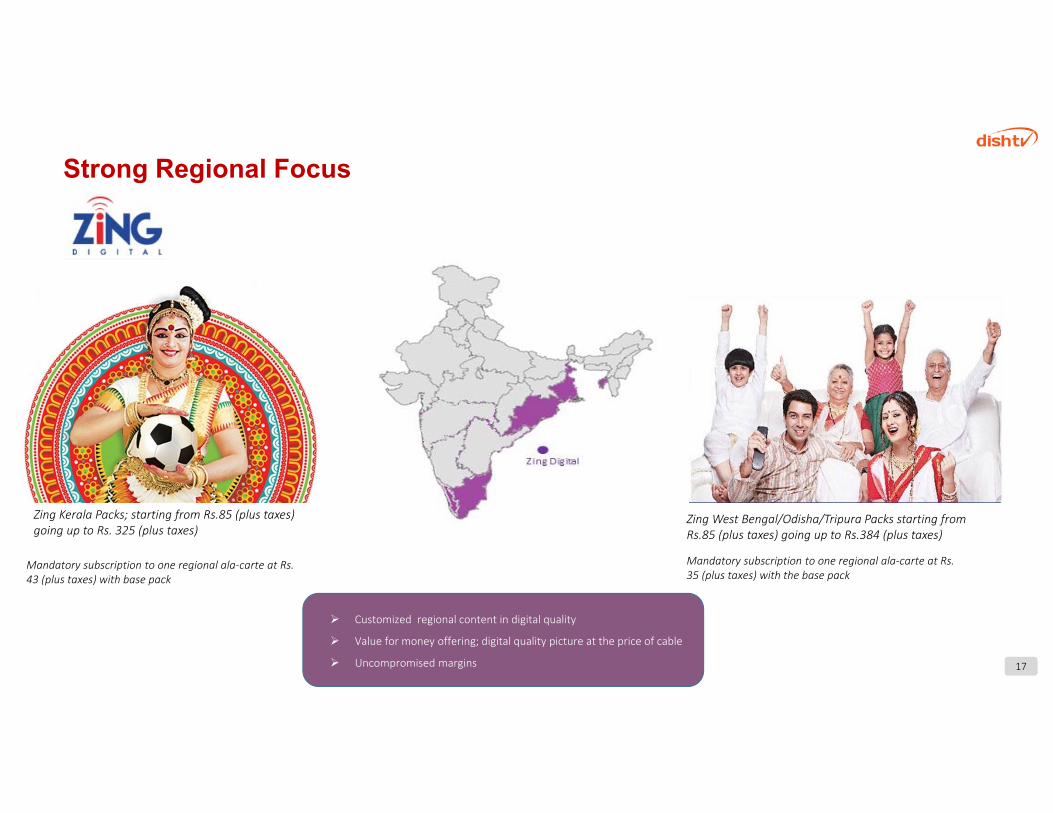

Strong Regional Focus

17

Customized regional content in digital quality

Value for money offering; digital quality picture at the price of cable

Uncompromised margins

Zing West Bengal/Odisha/Tripura Packs starting from Rs.85 (plus taxes) going up to Rs.384 (plus taxes)

Zing Kerala Packs; starting from Rs.85 (plus taxes) going up to Rs. 325 (plus taxes)

Mandatory subscription to one regional ala‐carte at Rs. 43 (plus taxes) with base pack

Mandatory subscription to one regional ala‐carte at Rs. 35 (plus taxes) with the base pack

High Definition

18

Family HD English Club HD

All Sports HD Infotainment, Lifestyle & Kids

Maxi Sports HD Sports HD South

All Sports HD South

HI-DEFINITION SACHETS STARTING AT ₹ 84 (plus taxes) EACH PER MONTH

Enjoy Stadium like experience with 5X better picture clarity and surround sound

Panel TV sales volumes to grow by ~9-11% CAGR in between 2016-2021

Increasing demand for OLED TV sets to drive growth of HD viewership

Dish TV had ~25% HD incremental market share in FY17

HD Channels

66+

ARPU driver

Key differentiator vis‐

à‐vis cable

Box Cost Rationalization

HD ADD‐ONS Game on HD @ ₹ 140 (plus taxes)

Game on HD Regional @ ₹ 148 (plus taxes)

(Sports and Hindi entertainment)

Full on HD @ ₹ 186 (plus taxes)Full On HD Regional @ ₹ 195 (plus

taxes)(Complete dose of entertainment)

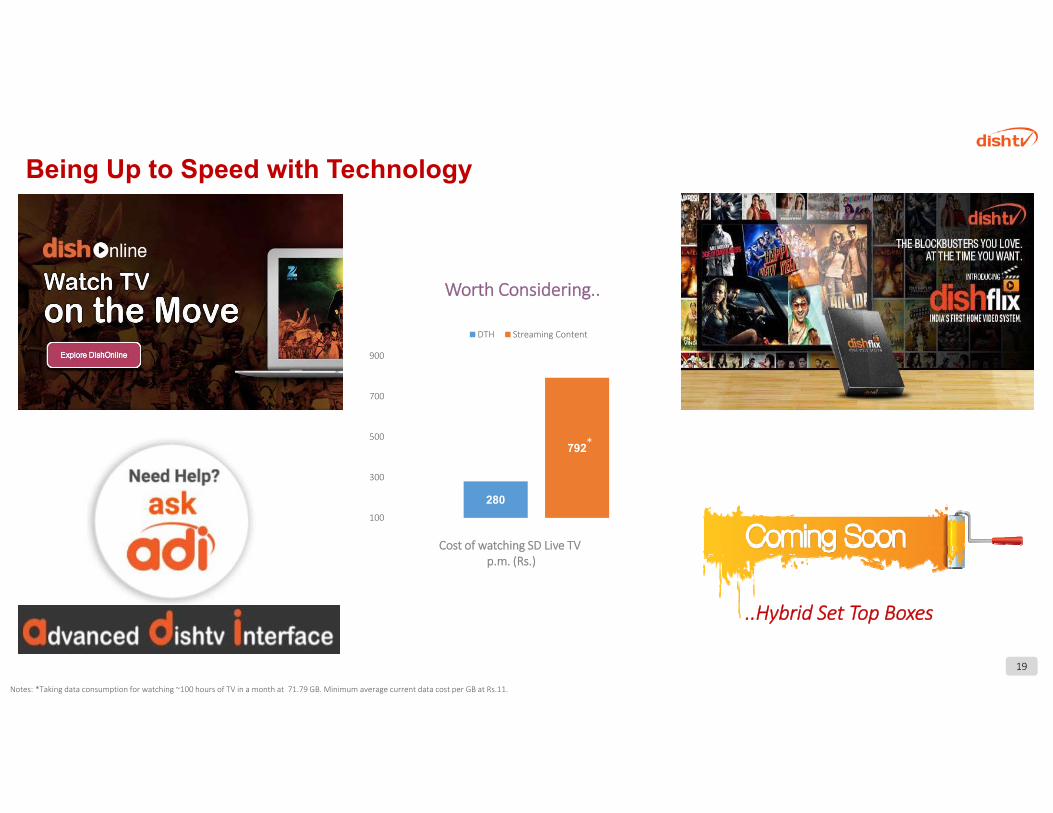

Being Up to Speed with Technology

Worth Considering..

280

792

100

300

500

700

900

DTH Streaming Content

*

Notes: *Taking data consumption for watching ~100 hours of TV in a month at 71.79 GB. Minimum average current data cost per GB at Rs.11.

..Hybrid Set Top Boxes

Cost of watching SD Live TV p.m. (Rs.)

19

Financials

20

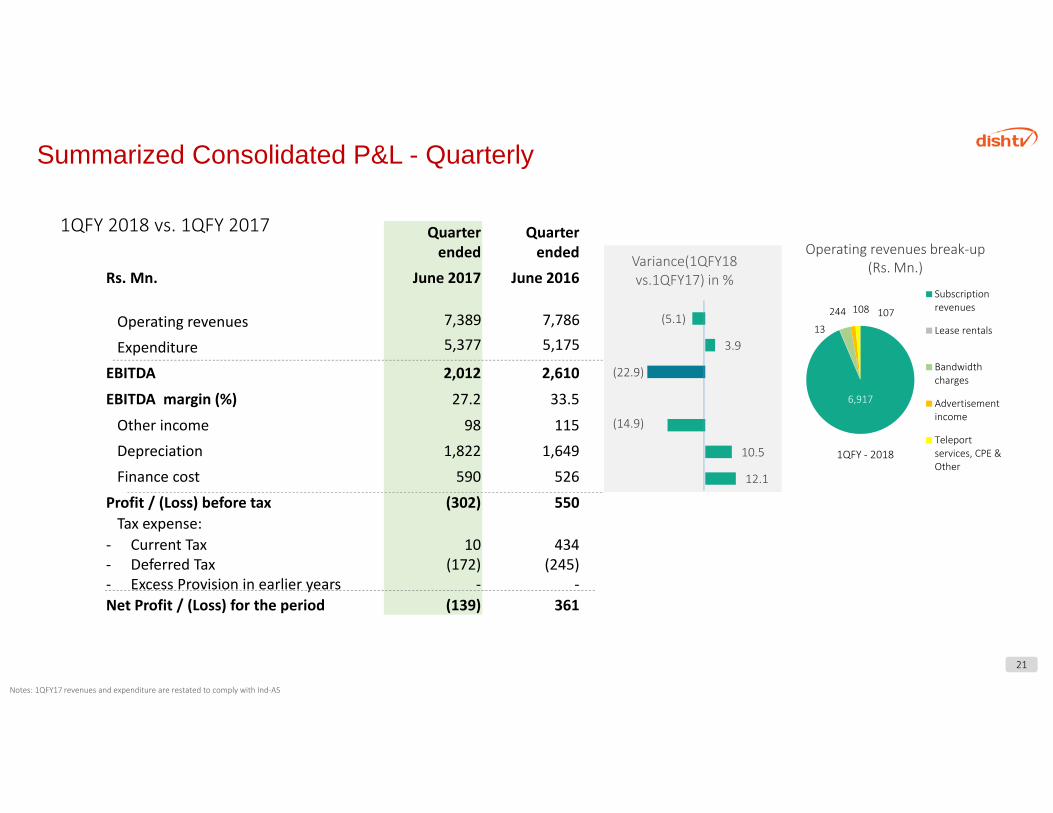

Quarter ended

Quarter ended

Rs. Mn. June 2017 June 2016

Operating revenues 7,389 7,786

Expenditure 5,377 5,175

EBITDA 2,012 2,610

EBITDA margin (%) 27.2 33.5

Other income 98 115

Depreciation 1,822 1,649

Finance cost 590 526

Profit / (Loss) before tax (302) 550Tax expense:

‐ Current Tax‐ Deferred Tax‐ Excess Provision in earlier years

10(172)

‐

434(245)

‐Net Profit / (Loss) for the period (139) 361

1QFY 2018 vs. 1QFY 2017Operating revenues break‐up

(Rs. Mn.)

1QFY ‐ 2018

Summarized Consolidated P&L - Quarterly

21

(5.1)

3.9

(22.9)

(14.9)

10.5

12.1

Variance(1QFY18 vs.1QFY17) in %

6,917

13

244 108 107

Subscriptionrevenues

Lease rentals

Bandwidthcharges

Advertisementincome

Teleportservices, CPE &Other

Notes: 1QFY17 revenues and expenditure are restated to comply with Ind‐AS

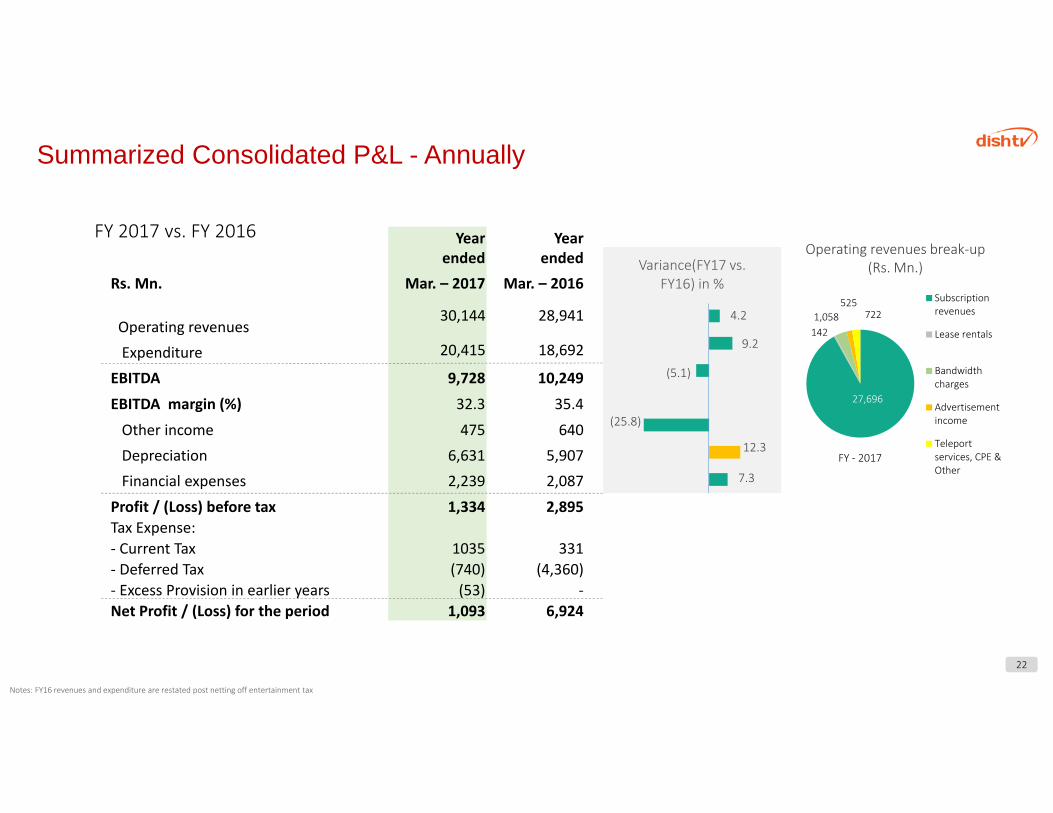

Yearended

Yearended

Rs. Mn. Mar. – 2017 Mar. – 2016

Operating revenues 30,144 28,941

Expenditure 20,415 18,692

EBITDA 9,728 10,249

EBITDA margin (%) 32.3 35.4

Other income 475 640Depreciation 6,631 5,907Financial expenses 2,239 2,087

Profit / (Loss) before tax 1,334 2,895Tax Expense:‐ Current Tax 1035 331‐ Deferred Tax (740) (4,360)‐ Excess Provision in earlier years (53) ‐Net Profit / (Loss) for the period 1,093 6,924

FY 2017 vs. FY 2016Operating revenues break‐up

(Rs. Mn.)

FY ‐ 2017

22

4.2

9.2

(5.1)

(25.8)

12.3

7.3

Variance(FY17 vs. FY16) in %

27,696

142 1,058

525 722

Subscriptionrevenues

Lease rentals

Bandwidthcharges

Advertisementincome

Teleportservices, CPE &Other

Notes: FY16 revenues and expenditure are restated post netting off entertainment tax

Summarized Consolidated P&L - Annually

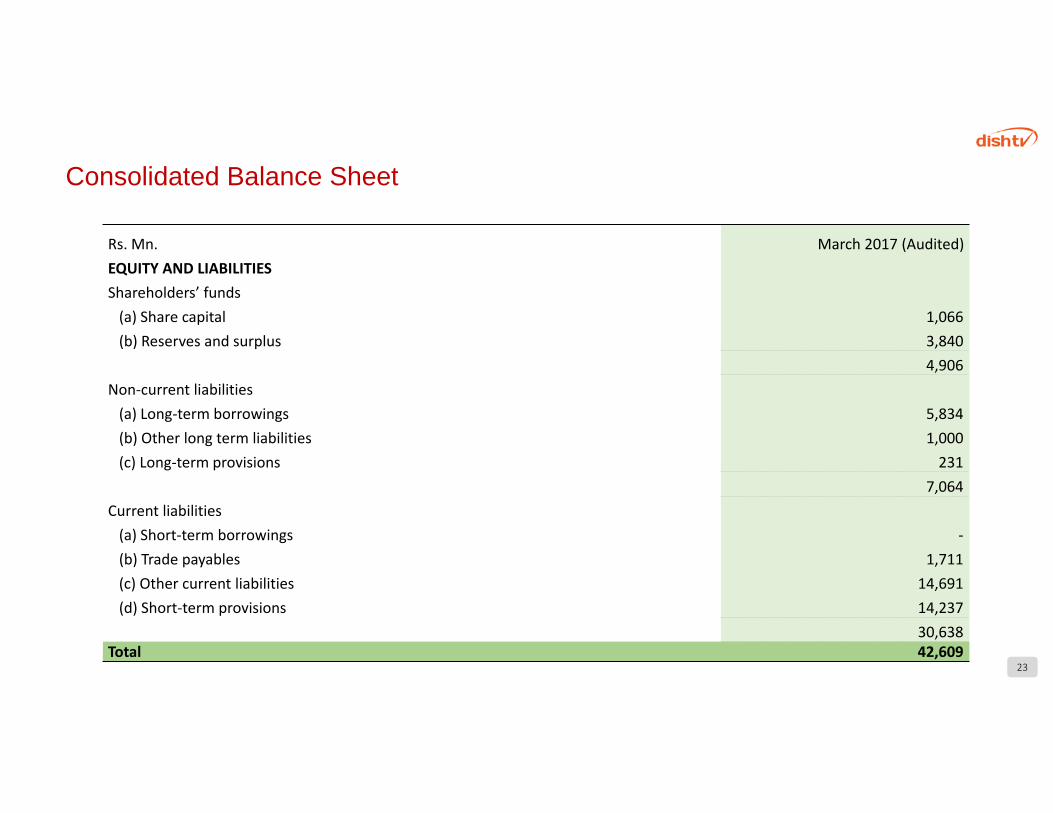

Rs. Mn. March 2017 (Audited)EQUITY AND LIABILITIESShareholders’ funds(a) Share capital 1,066(b) Reserves and surplus 3,840

4,906Non‐current liabilities(a) Long‐term borrowings 5,834(b) Other long term liabilities 1,000(c) Long‐term provisions 231

7,064Current liabilities(a) Short‐term borrowings ‐(b) Trade payables 1,711(c) Other current liabilities 14,691(d) Short‐term provisions 14,237

30,638Total 42,609

Consolidated Balance Sheet

23

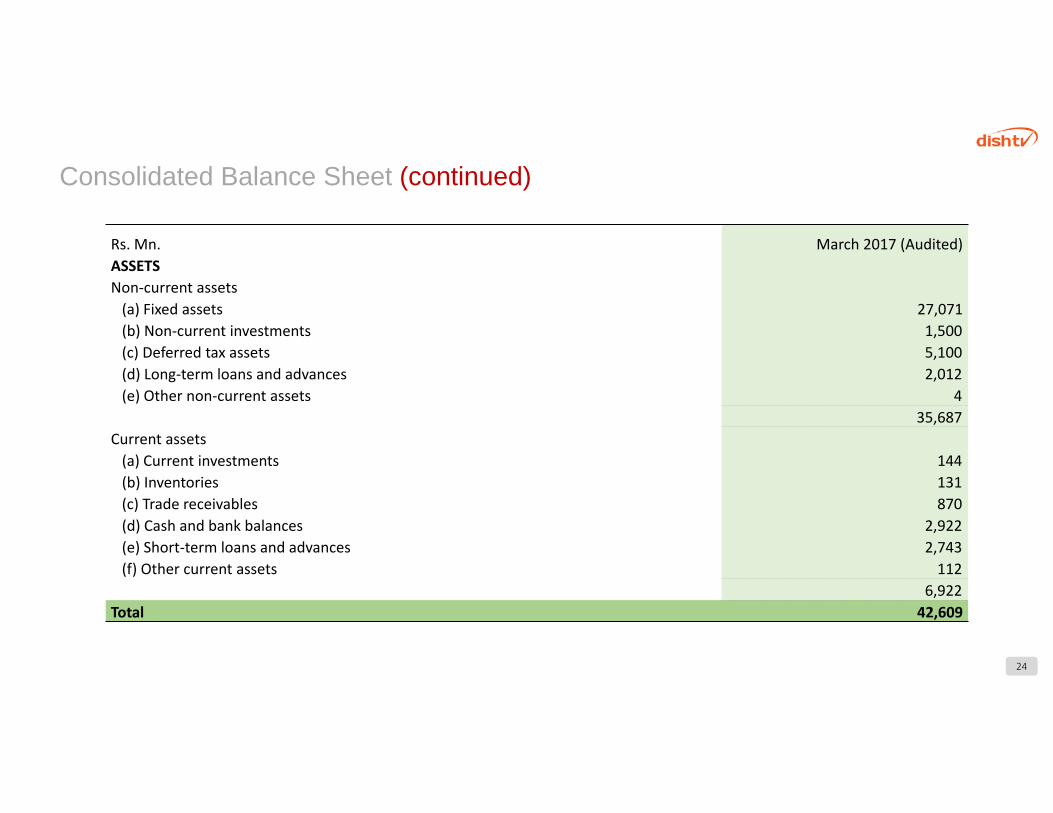

Rs. Mn. March 2017 (Audited)ASSETSNon‐current assets (a) Fixed assets 27,071(b) Non‐current investments 1,500(c) Deferred tax assets 5,100(d) Long‐term loans and advances 2,012(e) Other non‐current assets 4

35,687Current assets (a) Current investments 144(b) Inventories 131(c) Trade receivables 870(d) Cash and bank balances 2,922(e) Short‐term loans and advances 2,743(f) Other current assets 112

6,922Total 42,609

Consolidated Balance Sheet (continued)

24

Annexure

25

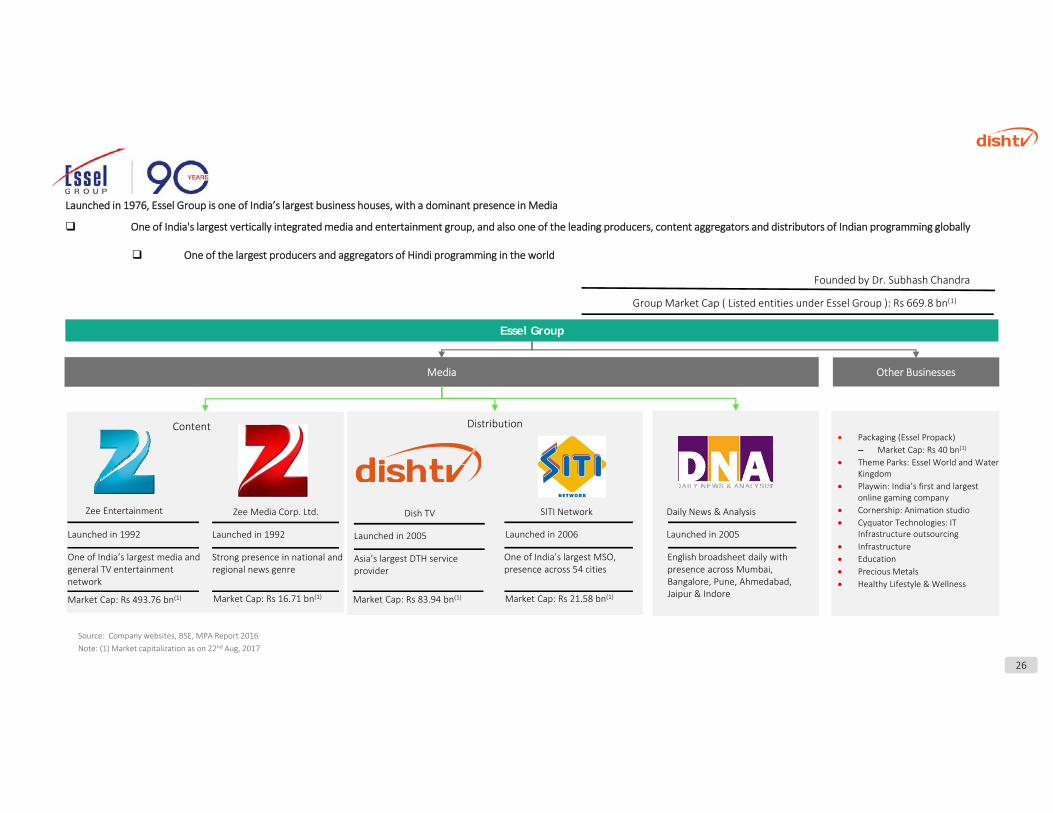

One of India's largest vertically integrated media and entertainment group, and also one of the leading producers, content aggregators and distributors of Indian programming globally

One of the largest producers and aggregators of Hindi programming in the world

Other Businesses

Essel Group

Media

Launched in 1992

One of India’s largest media and general TV entertainment network

Launched in 1992

Strong presence in national and regional news genre

Founded by Dr. Subhash Chandra

Group Market Cap ( Listed entities under Essel Group ): Rs 669.8 bn(1)

Source: Company websites, BSE, MPA Report 2016Note: (1) Market capitalization as on 22nd Aug, 2017

Market Cap: Rs 493.76 bn(1) Market Cap: Rs 16.71 bn(1)

Launched in 2005

Asia’s largest DTH service provider

Launched in 2006

One of India’s largest MSO, presence across 54 cities

Daily News & Analysis

Market Cap: Rs 83.94 bn(1) Market Cap: Rs 21.58 bn(1)

Launched in 2005

English broadsheet daily with presence across Mumbai, Bangalore, Pune, Ahmedabad, Jaipur & Indore

Content Distribution

Zee Entertainment Zee Media Corp. Ltd. Dish TV SITI Network

Packaging (Essel Propack)– Market Cap: Rs 40 bn(1)

Theme Parks: Essel World and Water Kingdom

Playwin: India’s first and largest online gaming company

Cornership: Animation studio Cyquator Technologies: IT

Infrastructure outsourcing Infrastructure Education Precious Metals Healthy Lifestyle & Wellness

26

Launched in 1976, Essel Group is one of India’s largest business houses, with a dominant presence in Media

Videocon D2H to Merge with Dish TV Creating A Leading Cable & Satellite

Distribution Platform

27

Transaction Summary

28

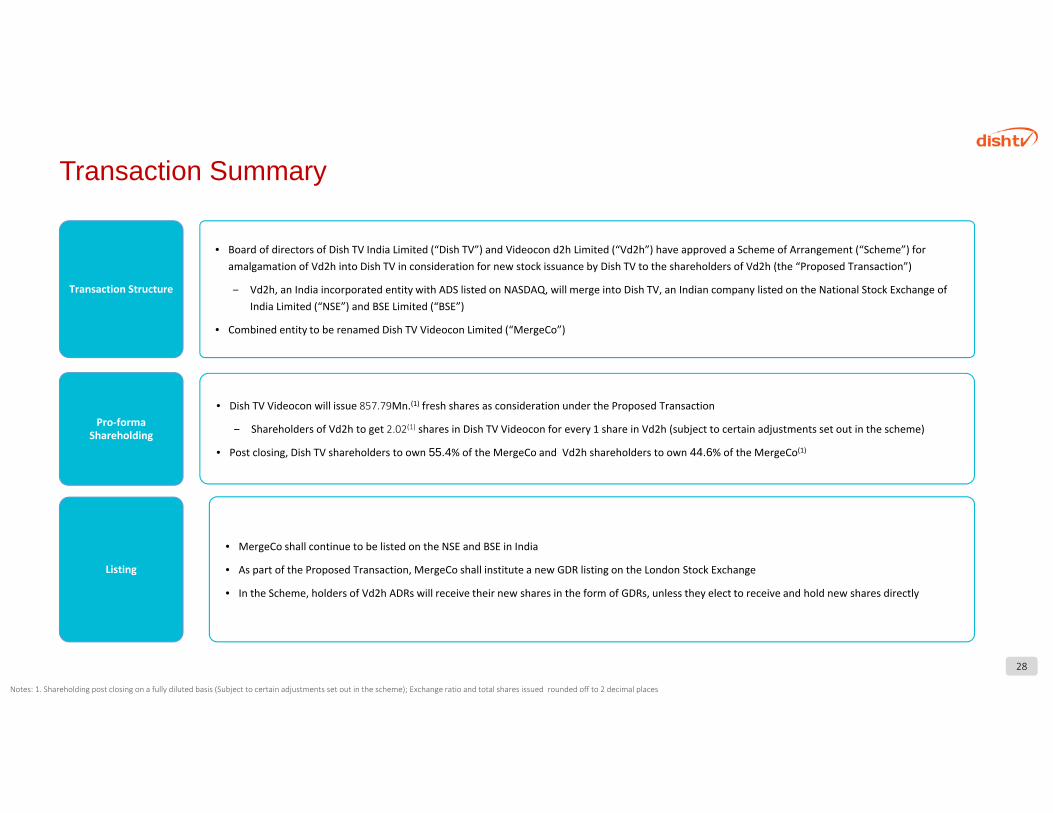

• Board of directors of Dish TV India Limited (“Dish TV”) and Videocon d2h Limited (“Vd2h”) have approved a Scheme of Arrangement (“Scheme”) for amalgamation of Vd2h into Dish TV in consideration for new stock issuance by Dish TV to the shareholders of Vd2h (the “Proposed Transaction”)

‒ Vd2h, an India incorporated entity with ADS listed on NASDAQ, will merge into Dish TV, an Indian company listed on the National Stock Exchange of India Limited (“NSE”) and BSE Limited (“BSE”)

• Combined entity to be renamed Dish TV Videocon Limited (“MergeCo”)

• MergeCo shall continue to be listed on the NSE and BSE in India

• As part of the Proposed Transaction, MergeCo shall institute a new GDR listing on the London Stock Exchange

• In the Scheme, holders of Vd2h ADRs will receive their new shares in the form of GDRs, unless they elect to receive and hold new shares directly

• Dish TV Videocon will issue 857.79Mn.(1) fresh shares as consideration under the Proposed Transaction

‒ Shareholders of Vd2h to get 2.02(1) shares in Dish TV Videocon for every 1 share in Vd2h (subject to certain adjustments set out in the scheme)

• Post closing, Dish TV shareholders to own 55.4% of the MergeCo and Vd2h shareholders to own 44.6% of the MergeCo(1)

Transaction Structure

Pro‐forma Shareholding

Listing

Notes: 1. Shareholding post closing on a fully diluted basis (Subject to certain adjustments set out in the scheme); Exchange ratio and total shares issued rounded off to 2 decimal places

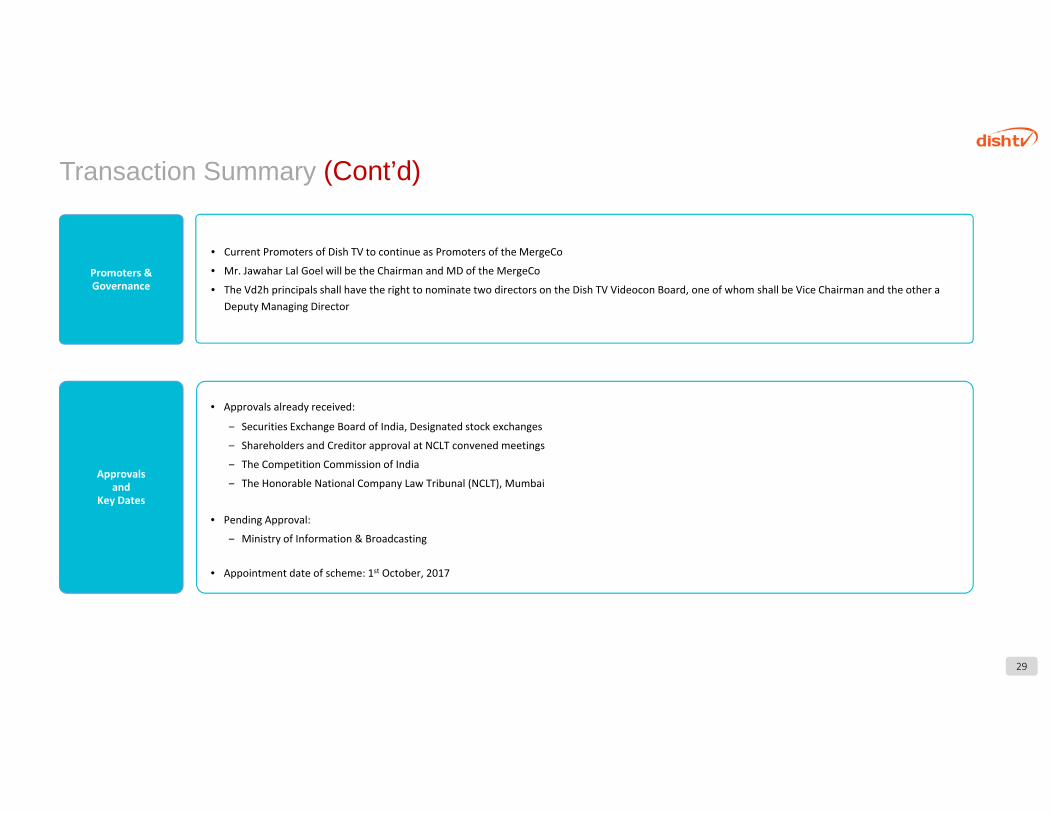

• Approvals already received:

‒ Securities Exchange Board of India, Designated stock exchanges

‒ Shareholders and Creditor approval at NCLT convened meetings

‒ The Competition Commission of India

‒ The Honorable National Company Law Tribunal (NCLT), Mumbai

• Pending Approval:

‒ Ministry of Information & Broadcasting

• Appointment date of scheme: 1st October, 2017

Approvals and

Key Dates

• Current Promoters of Dish TV to continue as Promoters of the MergeCo

• Mr. Jawahar Lal Goel will be the Chairman and MD of the MergeCo

• The Vd2h principals shall have the right to nominate two directors on the Dish TV Videocon Board, one of whom shall be Vice Chairman and the other a Deputy Managing Director

Promoters & Governance

Transaction Summary (Cont’d)

29

Transaction Overview

30

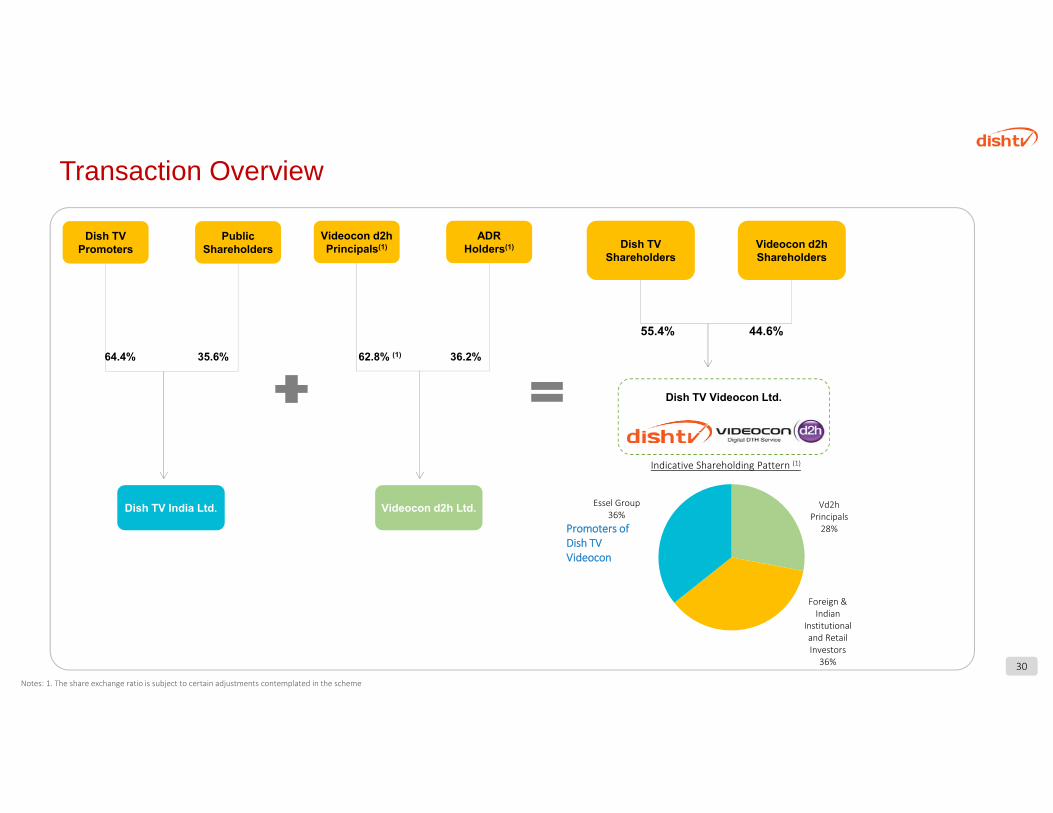

Vd2h Principals

28%

Foreign & Indian

Institutional and Retail Investors36%

Essel Group36%

Dish TV Promoters

Public Shareholders

Dish TV India Ltd.

64.4% 35.6%

Videocon d2h Principals(1)

ADRHolders(1)

Videocon d2h Ltd.

62.8% (1) 36.2%

Dish TV Shareholders

Videocon d2h Shareholders

Dish TV Videocon Ltd.

44.6%55.4%

Promoters of Dish TV Videocon

Indicative Shareholding Pattern (1)

Notes: 1. The share exchange ratio is subject to certain adjustments contemplated in the scheme

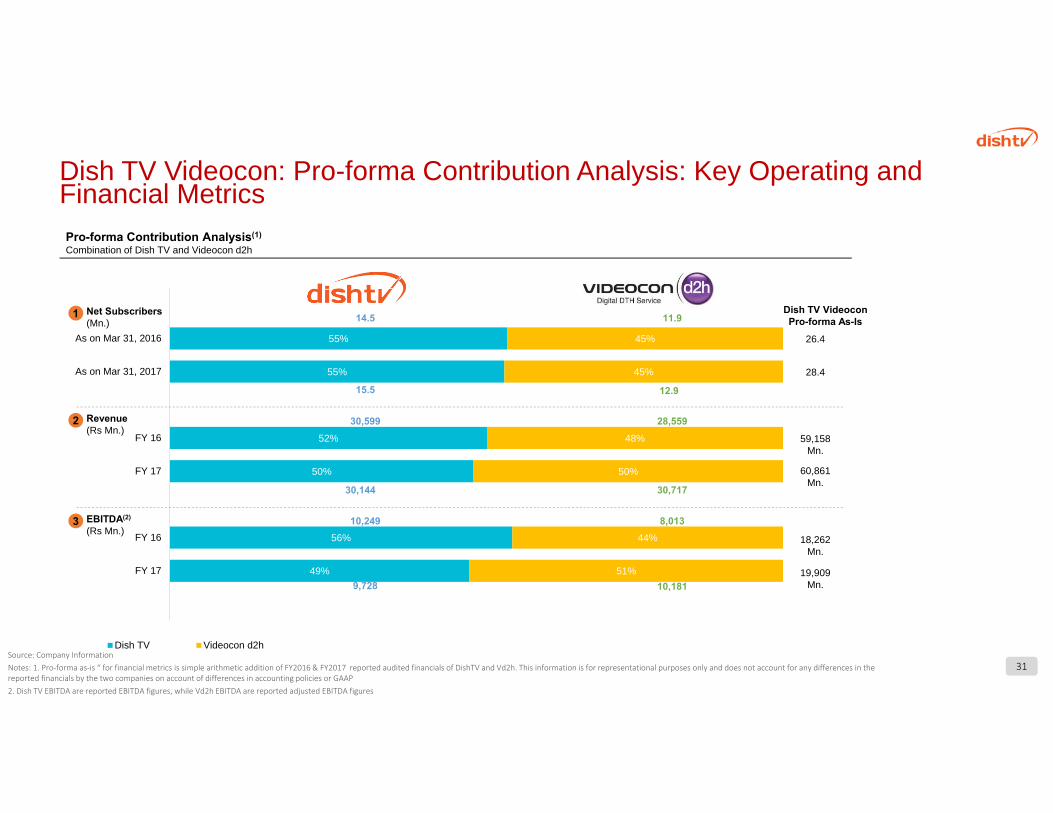

Dish TV Videocon: Pro-forma Contribution Analysis: Key Operating and Financial MetricsPro-forma Contribution Analysis(1)

Combination of Dish TV and Videocon d2h

55%

55%

52%

50%

56%

49%

45%

45%

48%

50%

44%

51%

As on Mar 31, 2016

As on Mar 31, 2017

FY 16

FY 17

FY 16

FY 17

Dish TV Videocon d2h

Net Subscribers(Mn.)

1 Dish TV VideoconPro-forma As-Is

26.4

28.4

14.5 11.9

15.5 12.9

Revenue(Rs Mn.)

2

EBITDA(2)

(Rs Mn.)3

59,158 Mn.

60,861 Mn.

18,262 Mn.

19,909 Mn.

30,599

30,144

10,249

28,559

30,717

8,013

9,728 10,181

Source: Company InformationNotes: 1. Pro‐forma as‐is “ for financial metrics is simple arithmetic addition of FY2016 & FY2017 reported audited financials of DishTV and Vd2h. This information is for representational purposes only and does not account for any differences in the reported financials by the two companies on account of differences in accounting policies or GAAP2. Dish TV EBITDA are reported EBITDA figures, while Vd2h EBITDA are reported adjusted EBITDA figures

31

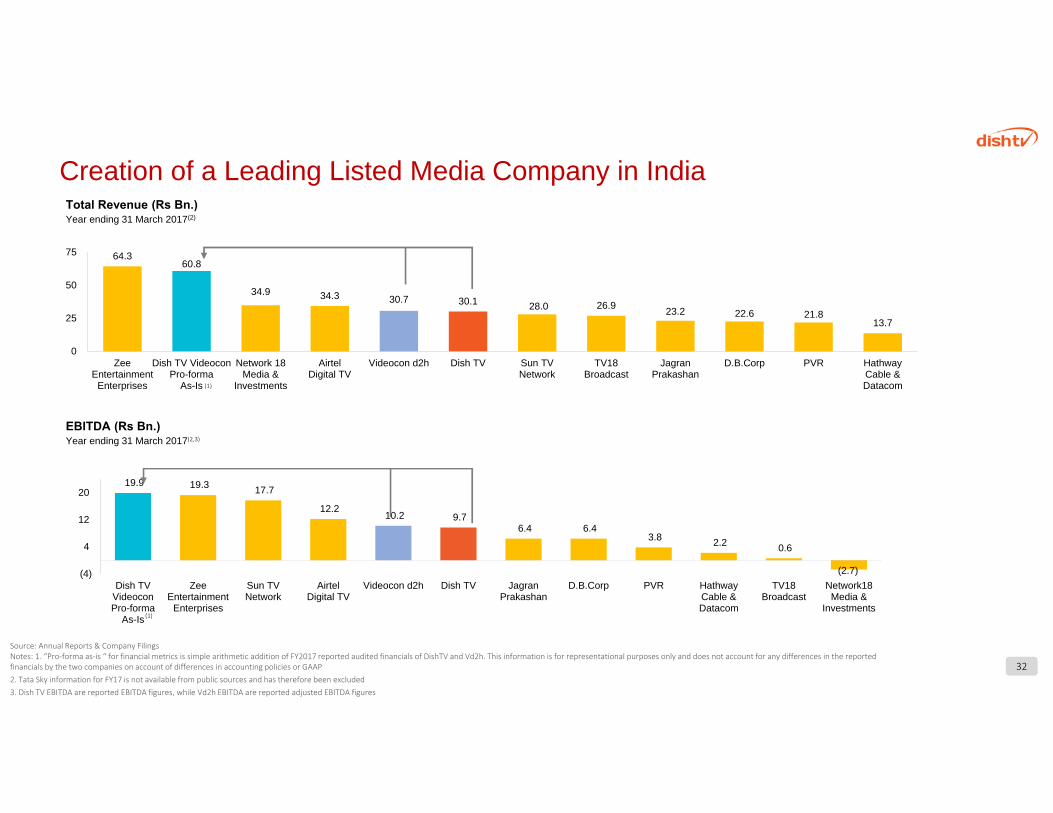

Creation of a Leading Listed Media Company in IndiaTotal Revenue (Rs Bn.)Year ending 31 March 2017(2)

64.360.8

34.9 34.3 30.7 30.1 28.0 26.9 23.2 22.6 21.813.7

0

25

50

75

ZeeEntertainment

Enterprises

Dish TV VideoconPro-forma

As-Is

Network 18Media &

Investments

AirtelDigital TV

Videocon d2h Dish TV Sun TVNetwork

TV18Broadcast

JagranPrakashan

D.B.Corp PVR HathwayCable &Datacom

EBITDA (Rs Bn.)Year ending 31 March 2017(2,3)

19.9 19.3 17.7

12.2 10.2 9.7

6.4 6.4 3.8 2.2 0.6

(2.7)(4)

4

12

20

Dish TVVideoconPro-forma

As-Is

ZeeEntertainment

Enterprises

Sun TVNetwork

AirtelDigital TV

Videocon d2h Dish TV JagranPrakashan

D.B.Corp PVR HathwayCable &Datacom

TV18Broadcast

Network18Media &

Investments(1)

32

Source: Annual Reports & Company FilingsNotes: 1. “Pro‐forma as‐is “ for financial metrics is simple arithmetic addition of FY2017 reported audited financials of DishTV and Vd2h. This information is for representational purposes only and does not account for any differences in the reported financials by the two companies on account of differences in accounting policies or GAAP2. Tata Sky information for FY17 is not available from public sources and has therefore been excluded3. Dish TV EBITDA are reported EBITDA figures, while Vd2h EBITDA are reported adjusted EBITDA figures

(1)

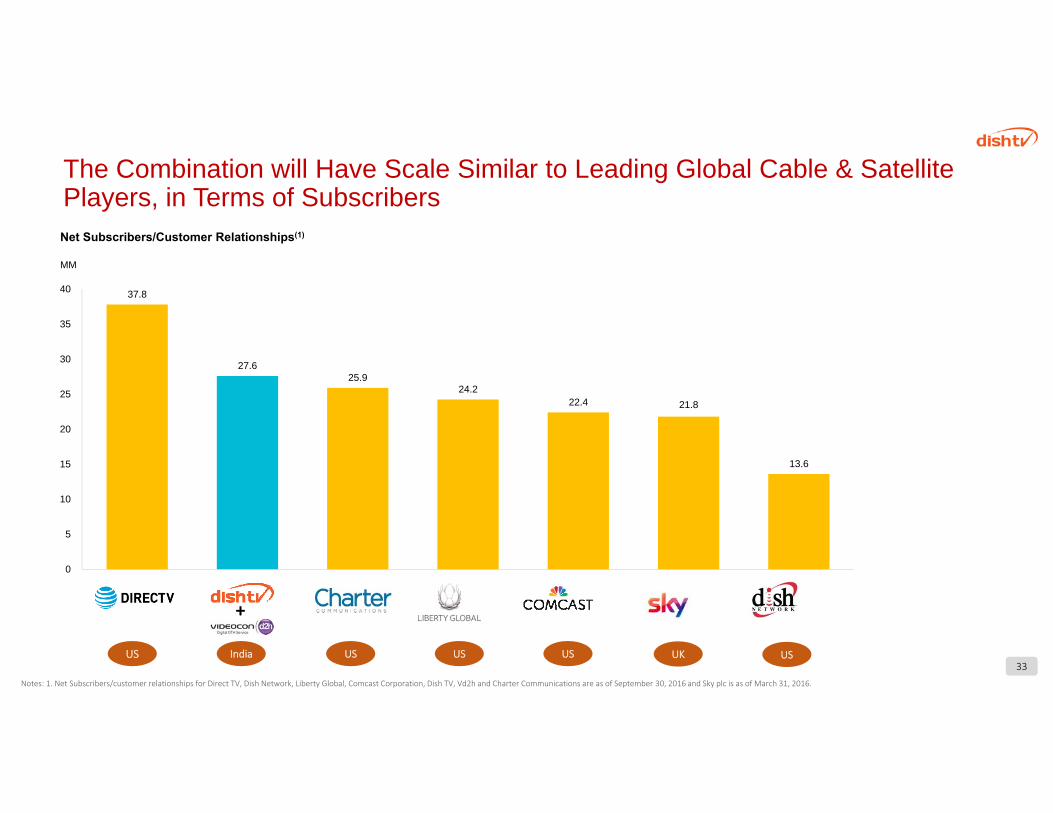

The Combination will Have Scale Similar to Leading Global Cable & Satellite Players, in Terms of SubscribersNet Subscribers/Customer Relationships(1)

MM

37.8

27.625.9

24.222.4 21.8

13.6

0

5

10

15

20

25

30

35

40

+

US India US US US UK US33

Notes: 1. Net Subscribers/customer relationships for Direct TV, Dish Network, Liberty Global, Comcast Corporation, Dish TV, Vd2h and Charter Communications are as of September 30, 2016 and Sky plc is as of March 31, 2016.

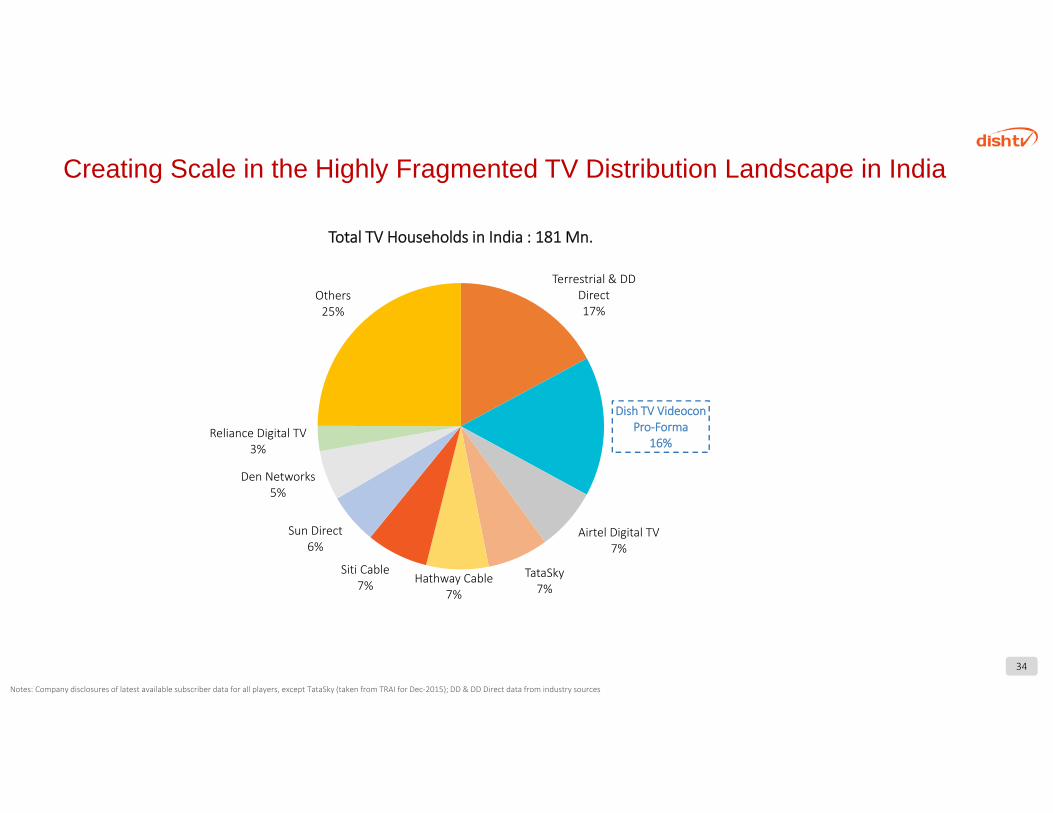

Creating Scale in the Highly Fragmented TV Distribution Landscape in India

Terrestrial & DD Direct17%

Dish TV Videocon Pro‐Forma

16%

Airtel Digital TV7%

TataSky7%

Hathway Cable7%

Siti Cable7%

Sun Direct6%

Den Networks5%

Reliance Digital TV3%

Others25%

Total TV Households in India : 181 Mn.

34

Notes: Company disclosures of latest available subscriber data for all players, except TataSky (taken from TRAI for Dec‐2015); DD & DD Direct data from industry sources

A Compelling and Transformational Combination

Creating a leading cable & satellite distribution platform, with room for growth1

Bringing together two well known brands in cable & satellite distribution2

Bouquet of offerings across the spectrum of subscribers3

Potential value creation from synergies generated through the combination4

Potential to offer new services to the large subscriber universe viz. broadband services etc. 5

Healthy financials535

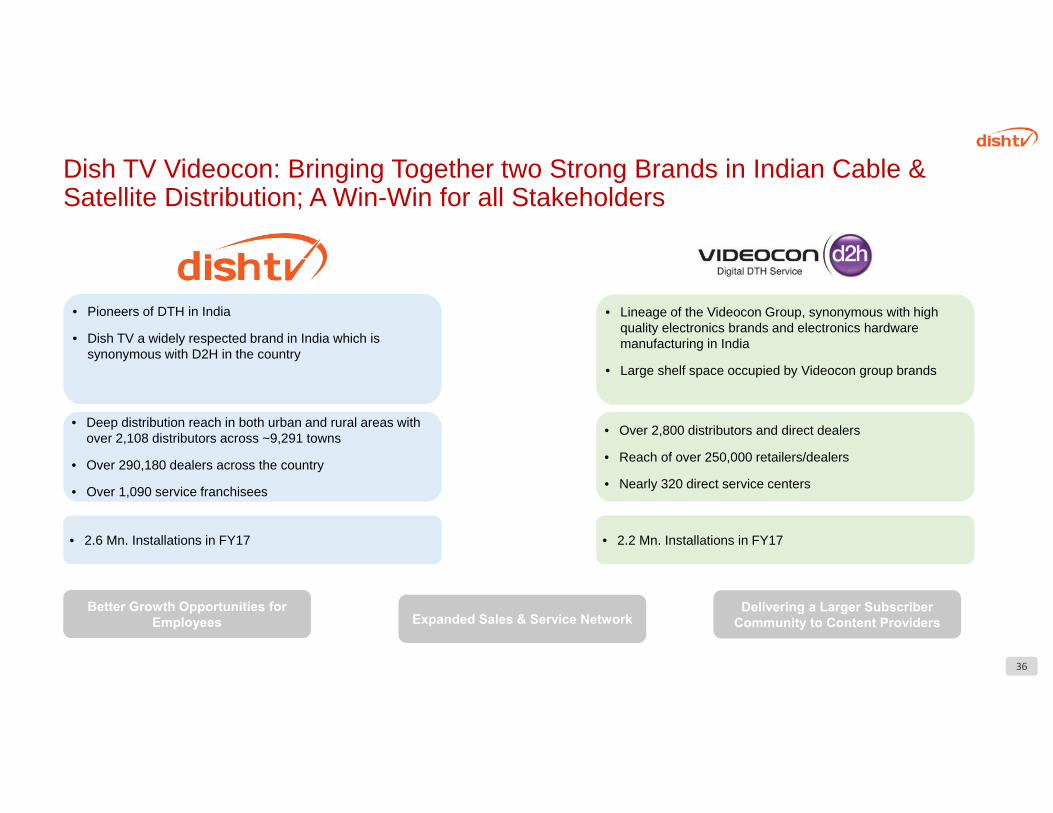

Dish TV Videocon: Bringing Together two Strong Brands in Indian Cable & Satellite Distribution; A Win-Win for all Stakeholders

• Pioneers of DTH in India

• Dish TV a widely respected brand in India which is synonymous with D2H in the country

• Lineage of the Videocon Group, synonymous with high quality electronics brands and electronics hardware manufacturing in India

• Large shelf space occupied by Videocon group brands

• Deep distribution reach in both urban and rural areas with over 2,108 distributors across ~9,291 towns

• Over 290,180 dealers across the country

• Over 1,090 service franchisees

• Over 2,800 distributors and direct dealers

• Reach of over 250,000 retailers/dealers

• Nearly 320 direct service centers

• 2.6 Mn. Installations in FY17 • 2.2 Mn. Installations in FY17

Better Growth Opportunities for Employees

Delivering a Larger Subscriber Community to Content ProvidersExpanded Sales & Service Network

36

Dish TV Videocon: Bouquet of Offerings Across The Full Chain of Consumer Spectrum

Value Conscious Subscribers

Brand ProductsCPE

High ARPU Subscribers

37

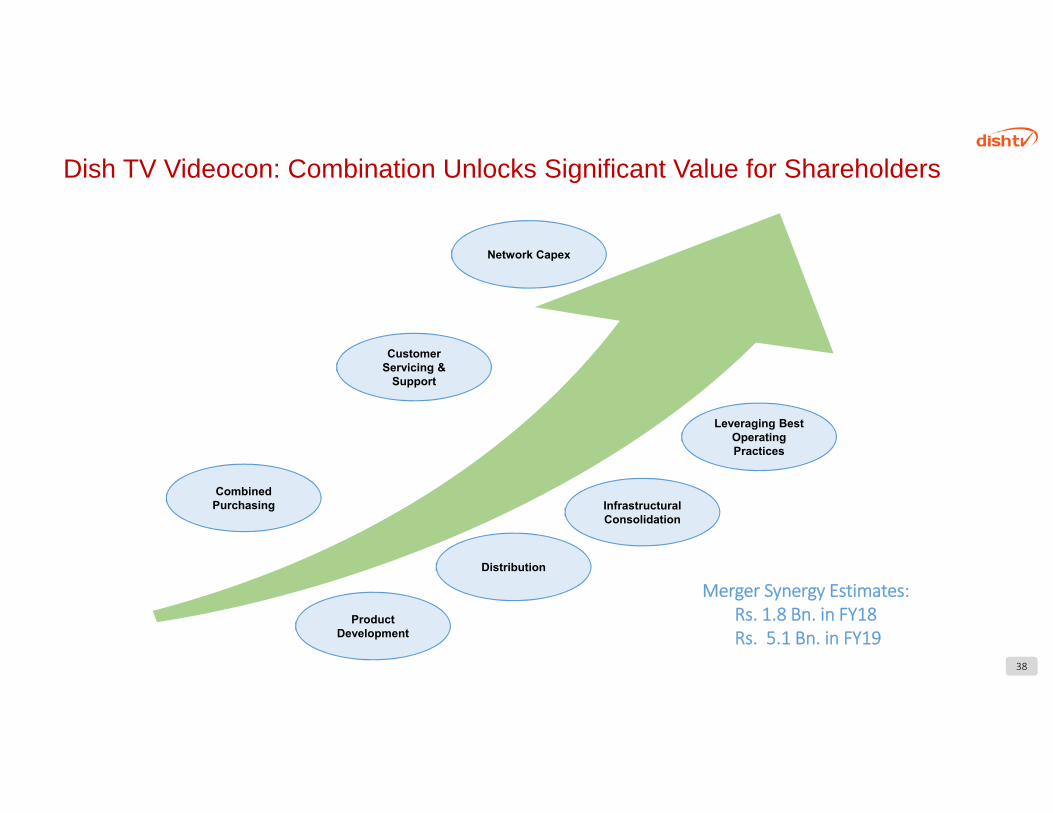

Dish TV Videocon: Combination Unlocks Significant Value for Shareholders

Customer Servicing &

Support

Leveraging Best Operating Practices

Infrastructural Consolidation

Combined Purchasing

Network Capex

Distribution

Product Development

Merger Synergy Estimates:Rs. 1.8 Bn. in FY18Rs. 5.1 Bn. in FY19

38

Thank you

39