Embed Size (px)

Citation preview

DISCLAIMER AND COPYRIGHT

DISCLAIMERThis information is for general information only. It should not be used as a substitute for specific and

professional advice. Responsibility is disclaimed for any inaccuracies, errors or omissions. All expressions of opinion or advice are published on the basis that they are not to regarded as expressing the official opinion of Rose Guerin Chartered Accountants ( RGCA) unless expressly stated. RGCA accepts no responsibility for the accuracy of the opinions of information contained in this presentation.

COPYRIGHTThis presentation is copyright. Subject to the conditions prescribed under the Copyright Act, no part of

it may, in any form, or by any means ( electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced or transmitted without permission by the author – Rose Guerin CA. Inquiries should be addressed to Rose Guerin Chartered Accountants, PO Box 622 Rose Bay 2029. © Rose Guerin Chartered Accountants A CN 103 081 456

1

INSERT LOGO

WHAT IS A SELF MANAGED SUPER FUND?

LEARNING OBJECTIVES

Superannuation is compulsory savings

The different ways of saving your super

Deciding if a self managed superannuation fund is for you

Understanding the requirements of setting up a SMSF

2

INSERT LOGO

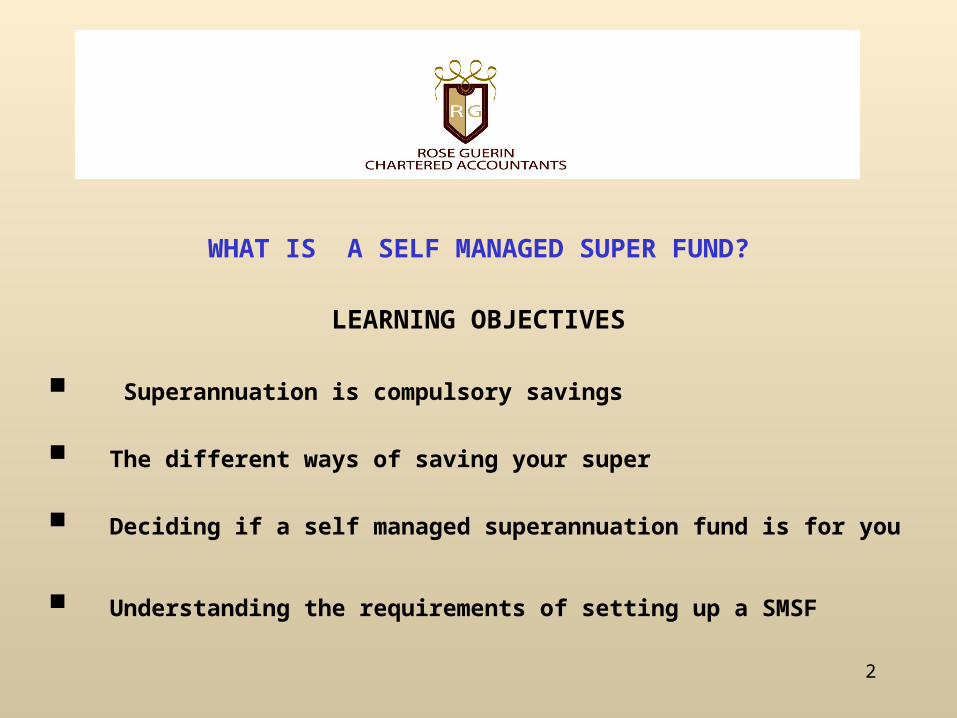

INTRODUCTION

SMSF POPULATION TABLE - ANNUAL DATA[1]

•

Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09

Establishments 30,239 22,547 24,191 44,584 32,498 28,995

Wind ups 4,849 5,088 4,923 3,862 4,558 2,310

Net establishments 25,390 17,459 19,268 40,722 27,940 26,685

Total number of SMSFs 278,244 295,703 314,971 355,693 383,633 410,318

Total members of SMSFs 534,941 568,285 604,333 680,154 721,469 772,299

[1] http://www.ato.gov.au/superfunds/content.asp?doc=/content/00214157.htm&page=6&H6

3

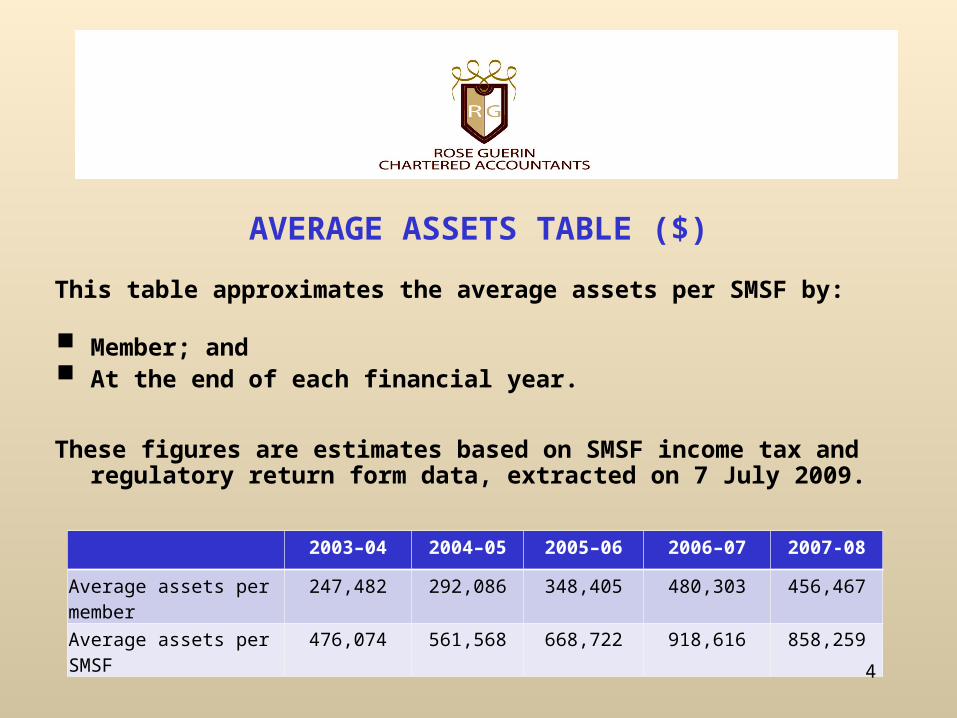

AVERAGE ASSETS TABLE ($)

This table approximates the average assets per SMSF by:

Member; and

At the end of each financial year.

These figures are estimates based on SMSF income tax and regulatory return form data, extracted on 7 July 2009.

2003–04 2004–05 2005–06 2006–07 2007-08

Average assets per member 247,482 292,086 348,405 480,303 456,467

Average assets per SMSF 476,074 561,568 668,722 918,616 858,259

4

Super is the way most Australians save money to retire. Usually, you start saving for your retirement when you start work and your employer pays super for you –

the ‘super guarantee’.

Generally, there are three ways you can save your super:

1. Australian Prudential Regulation Authority (APRA) regulated super funds - your super is pooled together with large numbers of other members and the fund professionally managed by trustees in compliance with super law. This is where most people have their employer paid super.

2. Retirement savings accounts ( RSA’s) - you have your own special deposit account with a bank or other deposit-taking institution. These are not commonly held.

3. Self-Managed Super Funds (SMSF’s) - you are responsible and the trustee of your own fund and need to comply with super law and make your own investment decisions. The Australian Taxation Office is the regulator of SMSF’s.

•[1] http://www.ato.gov.au/superfunds/content.asp?doc=/content/00214157.htm&page=6&H65

Add logo here

IS A SMSF FOR ME?

You should carefully consider which option is best to provide for your retirement.

If you’re thinking about setting up an SMSF, there are six points to consider to work out:

If this type of fund is right for you

The things you will need to do to set it up and run it successfully.

6

Add logo

POINT 1:

CONSIDER YOUR OPTIONS AND SEEK PROFESSIONAL ADVICE

There are many professionals who specialise in SMSFs. They can provide advice to help you understand:

■ What an SMSF is

■ The requirements for and the costs of setting one up and keeping one going

■ Your investment options and risks. They can also help you set up and run your fund if this type of fund is right for you.

7

Add logo

FINANCIAL ADVISERS AND FINANCIAL PLANNERS

A licensed financial adviser will consider your personal situation and recommend a suitable product for you. By using a financial adviser, you get extra protection if anything goes wrong.

TAX AGENTS AND QUALIFIED ACCOUNTANTS

Tax agents or accountants can help you set up an SMSF and advise you on the establishment, operation, structuring and valuation of an SMSF. However, they cannot advise you about which super fund best suits you or which investments should be in your fund, unless they are also a licensed financial advisory business.

Remember, if you decide to set up an SMSF, you will either be a trustee of the fund or a director of the company that is a corporate trustee for the fund. Therefore, you are legally responsible for all the decisions made even if you get help. A professional can provide advice and assistance but you’re ultimately you are responsible. 8

SMSF CAN BE USED STRATEGICALLY FOR

Estate Planning/intergenerational business succession planning

Asset protection

Strategies to minimize tax on death

9

Add logo

POINT 2

MAKE SURE YOU HAVE ENOUGH ASSETS, TIME AND SKILLS

Consider the amount of time, money and skill you’ll need to devote to managing your own super fund and whether it’s

worth your while.

Operating an SMSF means you’re responsible for the fund. You need to make sure you have enough assets, time and appropriate skills to:

■ Make the best investment decisions■ Meet all your obligations as a trustee of your fund. As a trustee of an SMSF, your primary

responsibility is to ensure you have invested your fund’s money appropriately, so ask yourself the following questions

■ Am I a confident and knowledgeable investor? ■ Will an SMSF do as well as or better than other super funds after I pay all the costs?

10

ADD LOGO

OTHER COSTS

All SMSFs are subject to an annual supervisory levy designed to fund the regulatory costs of making sure funds comply with their super obligations. An annual levy of $150 is currently payable as part of the fund’s income tax liability. If you set up or join an SMSF, you need to make sure you have adequate life insurance in case you die or you’re unable to work because of an illness or accident. You should also consider the amount of time you will need to devote to managing your own super.

11

ADD LOGO

POINT 3 UNDERSTAND THE RISKS AND LAWS

All financial decisions carry risk, so it is important to think carefully about how you choose your investment options to balance the level of risk against the level of financial return. You also need to be sure your super investments are legal.

It’s important to think carefully about how you choose your investment options when thinking about how to manage the risks associated with your investment options, we recommend you also consider:

■ Your age

■ What level of risk you are comfortable with

■ The objectives you have for your fund

A QUALIFIED FINANCIAL PLANNER CAN PROVIDE ADVICE ON INVESTMENT OPTIONS12

SPREADING THE RISK

Avoid risking all your retirement savings in one or a few investments. By spreading your

investments (diversifying) you can help control the total risk of your investment portfolio. If

one or more of your investments perform poorly or fail, the other investments may be

performing better to help cover the loss.

Effectively spreading your risk means investing not just in different companies or different

sectors of the market, but in different sectors of the economy.

A QUALIFIED FINANCIAL PLANNER CAN PROVIDE ADVICE ON DIVERSIFYING YOUR

INVESTMENTS

13

COMPLIANCE WITH TAX AND SUPERFUND LAWS

Super funds, including SMSFs, receive significant tax concessions as an incentive for

members to save for their retirement. However, you need to follow the tax and superfund

laws to receive these concessions.

The assets and money in your fund are solely for your retirement benefits, and are not to

benefit you or anyone else outside your fund. This means that the personal use of funds

for holiday homes, art to decorate your house, and your golf club membership almost

certainly will not comply.

14

HIGH TAX RATE FOR NON-COMPLYING FUNDS

A recent case[1] at the Administrative Appeals Tribunal found against a couple who ran their own SMSF. The couple borrowed money from their superfund to finance their small business. This loan breached the “ in-house assets rule” and were fined the maximum 45% which is assessed on the funds income of the year, excluding any un-deducted contributions.

A superfund asset will have an In-house asset (IHA) if it has any of the following with a related party:

1. A loan2. An investment in the related party including a related trust3. A fund asset subject to a lease or lease arrangement4. Regulator decides that asset should be IHA

There are a number of exemptions to this rule, including business real property and trusts set up for installment warrants.

[1] http://www.smh.com.au/small-business/finance/ruling-sends-reminder-to-selfmanaged-super-funds-20090727-dy1v.html

15

FRAUDULENT SCHEMES

Schemes that try to get your super money out of existing funds early

are usually illegal and fraudulent. Because of this, if you are caught in

one of these schemes you will pay heavy tax and legal penalties.

IT IS RECOMMENDED THAT YOU SPEAK TO YOUR ACCOUNTANT AND

FINANCIAL ADVISOR BEFORE JOINING SUCH SCHEMES

16

ADD LOGO

POINT 4

MAKE SURE YOUR TRUST DEED AND INVESTMENT STRATEGY ARE TAILORED TO SUIT THE MEMBERS OF YOUR SMSF

Regularly review whether the trust deed and investment strategy still meet the needs of your fund and update them when required.

A QUALIFIED ACCOUNTANT CAN ASSIST YOU WITH ALL SMSF ADMINISTRATION AND A FINANCIAL PLANNER CAN ASSIST YOU WITH YOUR INVESTMENT STRATEGY.

17

TRUST DEEDS

A trust deed is a legal document that sets out the rules for establishing and operating your

fund. Together with the super laws, they form the fund’s governing rules. The trust deed

needs to be: • Tailored to your fund • Correctly drafted to meet:

• Legal requirements

• The fund’s objectives

• The members’ needs

AN ACCOUNTANT CAN ASSIST YOU WITH YOUR TRUST DEEDS18

INVESTMENT STRATEGIES

An investment strategy sets out the fund’s investment objectives and your plan to achieve them. It provides you and the other trustees with a framework for making investment decisions to increase member benefits for their retirement. Your investment strategy needs to take into account the personal circumstances of all the fund members including:

■ Risk tolerance and attitudes to risk■ Age

One strategy may not suit every member, especially where the fund consists of people at different stages of life. In these situations you need to select and manage investments well enough so they grow in value and meet the investment objectives of all members. A financial planner can advise you on how to make asset allocation decisions by choosing from a range of investment assets including:

Cash

Bonds

Property

Shares. 19

ADD LOGO

“DEFENSIVE” INVESTMENTS

Often described as “defensive investments” Cash and bonds are

investments, with practically no risk of losing money, and the returns may

seem reasonably high. However, you will lose some of the return in taxes

and some to the effect of inflation. These safer (defensive) investments

don’t provide long-term capital growth.

A FINANCIAL PLANNER WILL PROVIDE FURTHER ADVICE ON THIS FORM

OF INVESTMENT

20

CAPITAL GROWTH INVESTMENTS

Property and shares are capital growth investments and tend to be more tax

effective. This means the value of your investment should grow faster than inflation,

creating real wealth. However, capital growth is not guaranteed and there can be a lot

of ups and downs over the investment time period. Each year, the amount and

frequency of your gains or losses will be uncertain and could differ, perhaps

significantly, from reasonable long-term estimates. Specific assets may lose value

and never regain it.

A FINANCIAL PLANNER AND A PROPERTY INVESTOR SPECIALIST CAN PROVIDE ADVICE AND ASSIST YOU ON THIS FORM OF INVESTMENT

21

ADD LOGO

BORROWING STRATEGIES TO PURCHASE A PROPERTY IN YOUR SMSF

Restrictions on superfunds borrowing have been in place for over 20 years,

however, in recent years these restrictions have been relaxed.

PROHIBITED

Superfunds must not borrow or maintain existing borrowings ( there are some exemptions).

22

INSTALMENT WARRANTS – HISTORY

Instalment receipts first appeared in Australia with privatizations of the CBA and Telstra 2 and 3:

Two instalments

If 2nd not paid, government could take other assets to pay debt

Superfunds allowed to participate

23

INSTALMENT WARRANTS THE NEW RULES

Trustee may borrow money ( or maintain borrowing)

Purpose to acquire asset allowed to be purchased under SIS ACT

Asset is held on trust and trustee has beneficial interest

Trustee has the right to acquire legal ownership if one or two payments made after acquiring beneficial interest

Lender rights against trustee for default on borrowing and related charges is limited to rights relating to asset ( non-recourse loans)

AN ACCOUNTANT CAN ASSIST YOU WITH SETTING UP THE NECESSARY STRUCTURE FOR AN INSTALMENT WARRANT. A SPECIALIST BROKER

AND LENDER CAN ARRANGE FOR SMSF FINANCE.24

POINT 5

MAKE SURE YOU CAN MEET YOUR RECORD KEEPING AND REPORTING OBLIGATIONS

One of your responsibilities as a trustee of an SMSF is to keep proper and accurate tax and super records to manage your fund efficiently

It’s a good idea to take minutes of all investment decisions, including:

■ Why a particular investment was chosen

■ Whether all trustees agreed with the decision

AN ACCOUNTANT CAN ASSIST YOU WITH ENSURING THAT YOUR RECORD KEEPING AND REPORTING REQUIREMENTS ARE COMPLIANT 25

MAKE SURE YOU CAN MEET YOUR RECORD KEEPING AND REPORTING OBLIGATIONS

If, as one of the fund’s trustees, you invest the SMSF’s money in an investment that fails, the other trustee(s) could take action against you for failing to be diligent in your duties. However, if your investment decision was recorded in meeting minutes that were signed by the other trustees, you will have a record to show the other trustees agreed with your actions

You need to make certain records available to your fund’s approved auditor when they audit your fund each year

You may also need to provide accurate records to the Tax Office if they ask to see them

You need to report changes in certain aspects of your fund to the Tax Office when they happen and you also have annual reporting obligations.

AN ACCOUNTANT CAN ASSIST YOU WITH THE ABOVE 26

POINT 6• MAKE SURE YOU UNDERSTAND THE AUDITING OBLIGATIONS

You have a legal obligation to have your SMSF independently audited annually.

You need to appoint an approved auditor, who will:

■ Provide you with a report on your SMSF

■ Report to the Tax Office if your fund has breached any super rules

Approved auditors play an important role in maintaining the health of SMSF’s

ROSE GUERIN CHARTERED ACCOUNTANTS IS QUALIFIED TO UNDERTAKE SMSF AUDITS. 27