Embed Size (px)

Citation preview

Regime Based U.S. Long Short Equity StrategyA Time Varying Risk Aversion Strategy Based on Macroeconomic Regimes

CONFIDENTIAL. Not for distribution. For Institutional and Accredited investor use only. See important disclosures on the final page of this document.

P

Kevin W. Shea, [email protected]+1 857 350 3958

Peter B. McManus, [email protected]+1 857 233 4075

Quantitative Equity Strategies

Disciplined Alpha LLC 60 State Street, Suite 3750 Boston, MA 02109 USAwww.disciplinedalpha.com

Discipline AlphAn authority on regime based investing

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 2

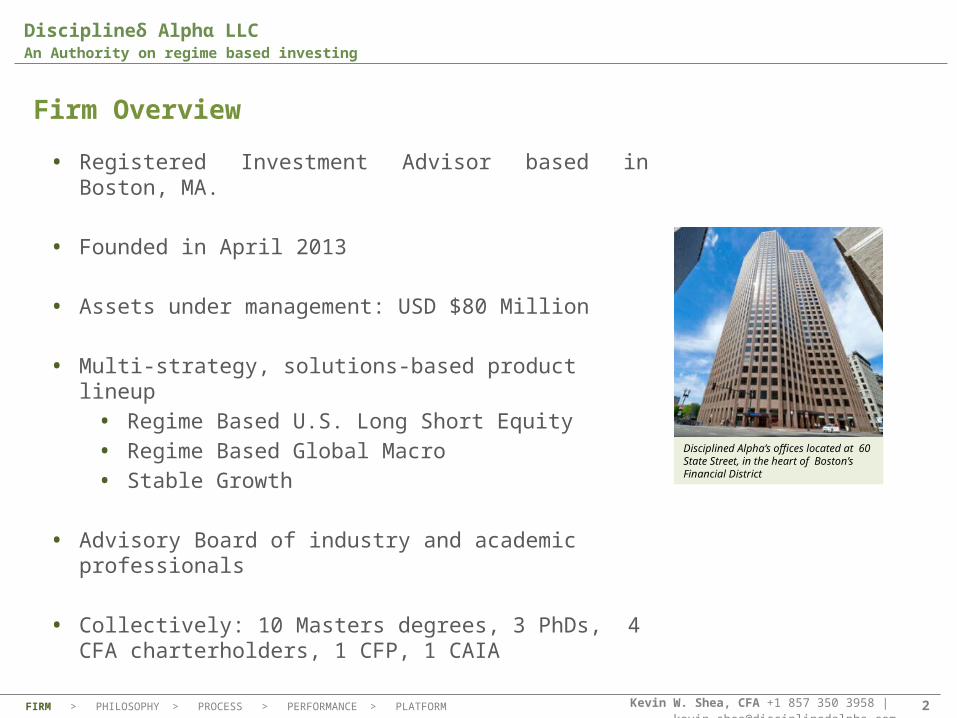

Disciplineδ Alphα LLCAn Authority on regime based investing

• Registered Investment Advisor based in Boston, MA.

• Founded in April 2013

• Assets under management: USD $80 Million

• Multi-strategy, solutions-based product lineup• Regime Based U.S. Long Short Equity• Regime Based Global Macro• Stable Growth

• Advisory Board of industry and academic professionals

• Collectively: 10 Masters degrees, 3 PhDs, 4 CFA charterholders, 1 CFP, 1 CAIA

Disciplined Alpha’s offices located at 60 State Street, in the heart of Boston’s Financial District

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

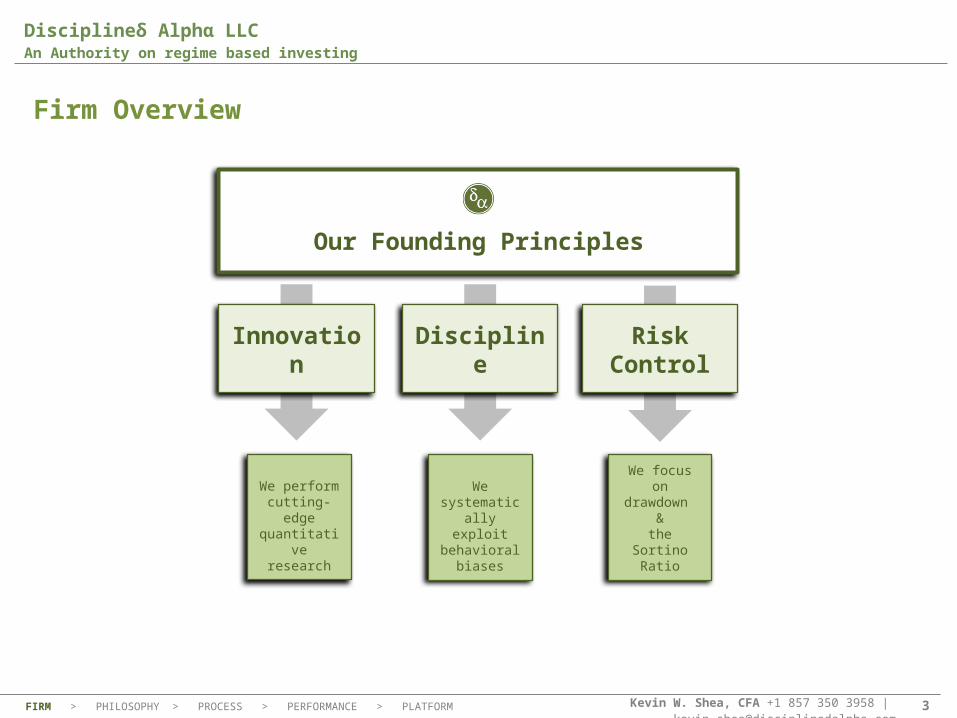

Firm Overview

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 3

Disciplineδ Alphα LLCAn Authority on regime based investing

We perform cutting-edgequantitative

research

Our Founding Principles

Innovation

DisciplineRisk

Control

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

We systematically

exploit behavioral

biases

We focus on drawdown

&the Sortino

Ratio

Firm Overview

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 4

Disciplineδ Alphα LLCAn Authority on regime based investing

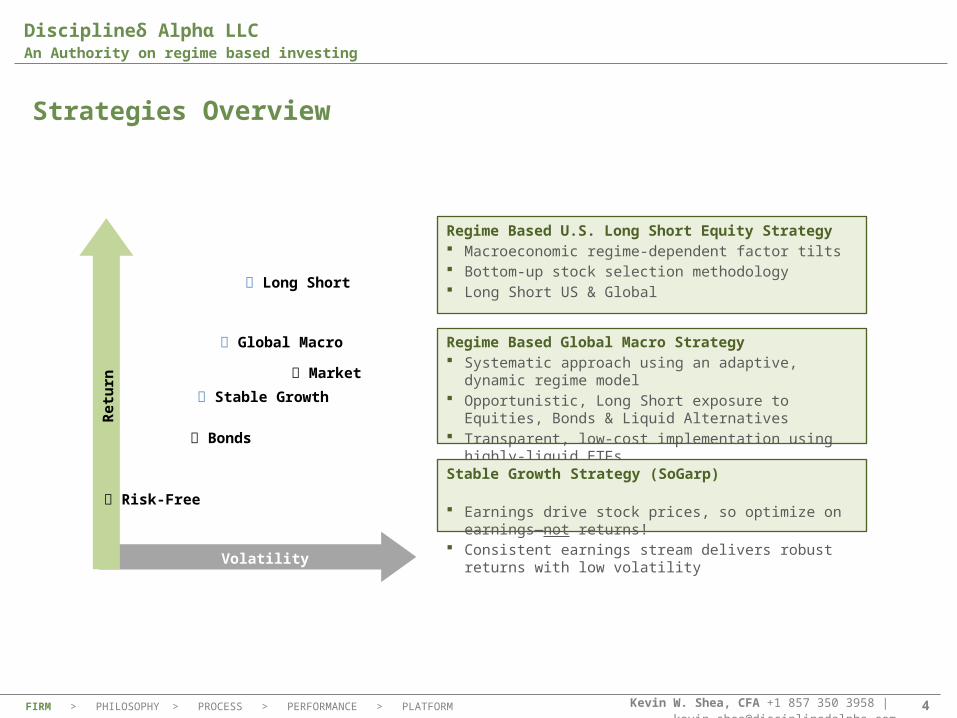

Strategies Overview

Regime Based U.S. Long Short Equity Strategy Macroeconomic regime-dependent factor tilts Bottom-up stock selection methodology Long Short US & Global

Regime Based Global Macro Strategy Systematic approach using an adaptive, dynamic

regime model Opportunistic, Long Short exposure to Equities,

Bonds & Liquid Alternatives Transparent, low-cost implementation using highly-

liquid ETFsStable Growth Strategy (SoGarp) Earnings drive stock prices, so optimize on earnings

—not returns! Consistent earnings stream delivers robust returns

with low volatility

Stable Growth

Retu

rn

Volatility

Risk-Free

Bonds

Market

Global Macro

Long Short

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 5

Disciplineδ Alphα LLCAn Authority on regime based investing

Investment Philosophy

Risk Aversion is Time Varying.

These Risk Aversion Preferences are tracked in a real time,

forward looking, Macroeconomic Regime Model and captured

through a Long Short Strategy.

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 6

Disciplineδ Alphα LLCAn Authority on regime based investing

Product Summary

Regime focused

Long Short Quantitative Large Cap Equity

Highly Liquid Russell 1000 Starting Universe

Capacity: $3 billion

Macroeconomic Regime Model determines factor weights and

exposures:• Dynamic factor weights

– Growth versus Value

• Exposures

– Gross Exposure 110% to 190%– Net Exposure 40% to 130%

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 7

Disciplineδ Alphα LLCAn Authority on regime based investing

Putting the “edge” in Hedge

Unique Features: The Macro Regime based model determines the dynamic factor

weights and exposures. A separate Short Model to optimally capture stocks that

underperform. The top 12 of the 24 GIC Industry Groups, in which the model

demonstrated the most robust results. Derives proprietary Industry Group based factors from

conversations with company managements and fundamental analysts.

Why does this matter to our clients?Strategy HFRI Peer

Groups Superior Long Term Returns (1990 - 2013): 18% 12% to 13% Lower Drawdowns in 2008 - 2009: -13% -31% Risk Adjusted Returns: Sharpe (12/2007 - 5/2013) 0.7

0.0 Risk Adjusted Returns: Sortino (12/2007 - 5/2013) 1.3 0.0

to 0.1 Lower Correlations to Market in Bear Markets: 0.04 0.79

to 0.88

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 8

Disciplineδ Alphα LLCAn Authority on regime based investing

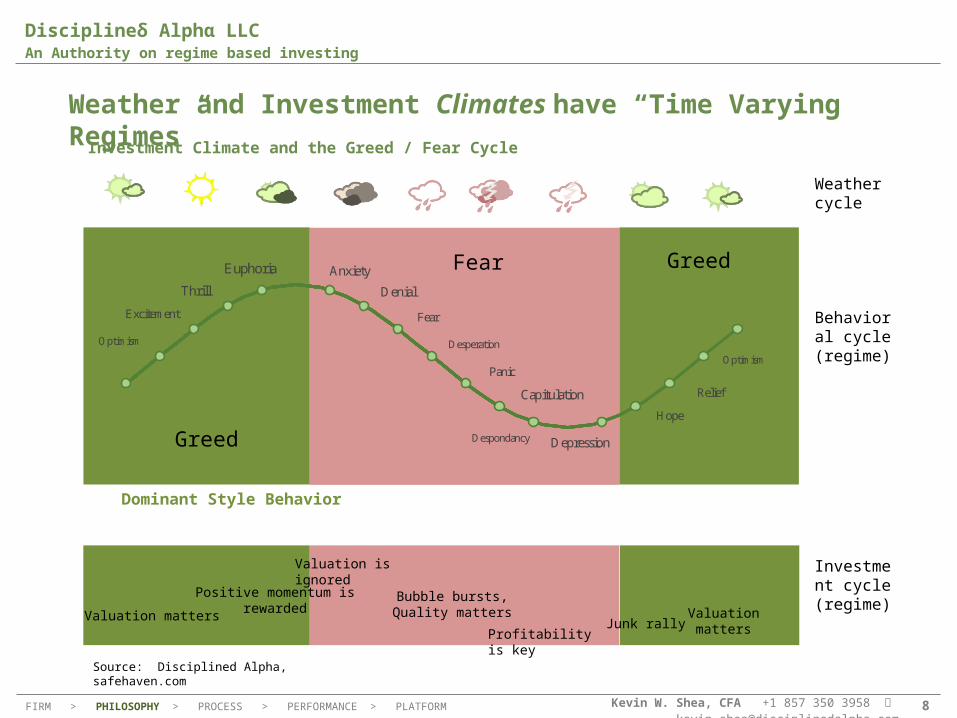

Weather and Investment Climates have “Time Varying Regimes” Investment Climate and the Greed / Fear Cycle

Source: Disciplined Alpha, safehaven.com

Dominant Style Behavior

Optimism

Excitement

Thrill

Euphoria Anxiety

Denial

Fear

Desperation

Panic

Capitulation

Despondancy Depression

Hope

Relief

Optimism

Greed

Fear Greed

Weather cycle

Behavioral cycle(regime)

Investment cycle(regime)

Valuation matters

Positive momentum is rewarded

Valuation is ignored

Bubble bursts,Quality matters

Profitability is keyJunk rally

Valuation matters

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 9

Disciplineδ Alphα LLCAn Authority on regime based investing

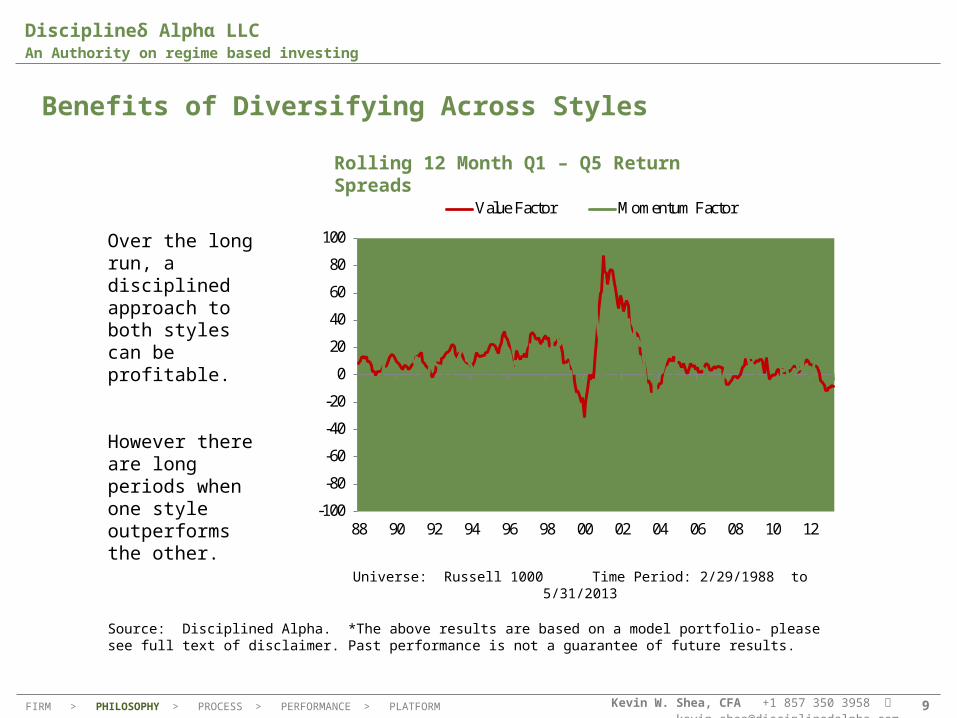

Over the long run, a disciplined approach to both styles can be profitable.

However there are long periods when one style outperforms the other.

Benefits of Diversifying Across Styles

Source: Disciplined Alpha. *The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

-100

-80

-60

-40

-20

0

20

40

60

80

100

88 90 92 94 96 98 00 02 04 06 08 10 12

Value Factor Momentum Factor

Universe: Russell 1000 Time Period: 2/29/1988 to 5/31/2013

Rolling 12 Month Q1 – Q5 Return Spreads

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 10

Disciplineδ Alphα LLCAn Authority on regime based investing

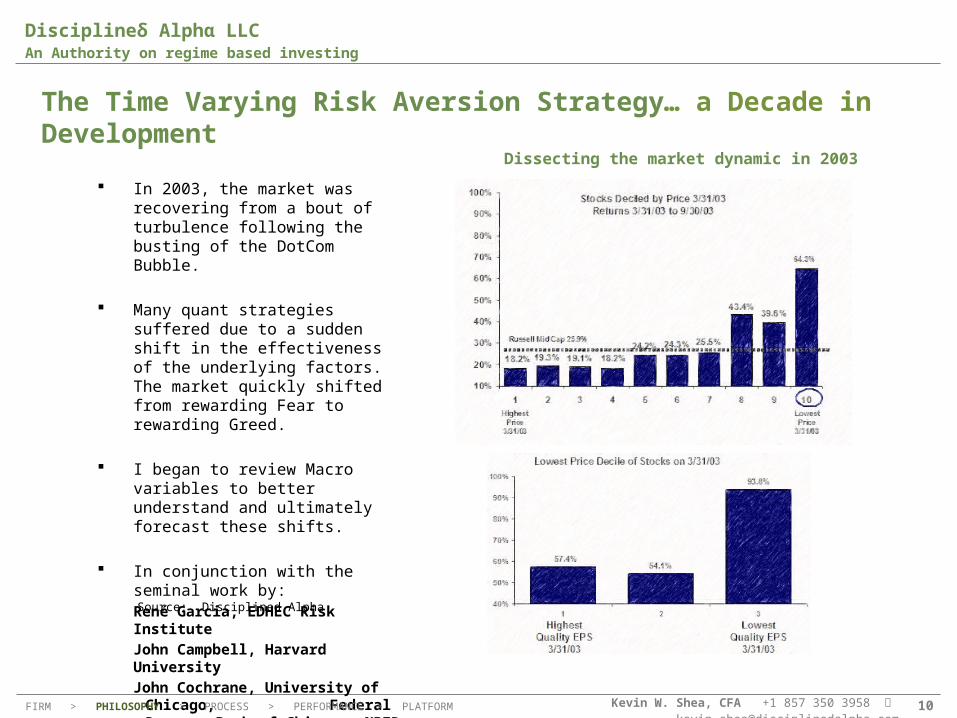

The Time Varying Risk Aversion Strategy… a Decade in Development

In 2003, the market was recovering from a bout of turbulence following the busting of the DotCom Bubble.

Many quant strategies suffered due to a sudden shift in the effectiveness of the underlying factors. The market quickly shifted from rewarding Fear to rewarding Greed.

I began to review Macro variables to better understand and ultimately forecast these shifts.

In conjunction with the seminal work by:René Garcia, EDHEC Risk InstituteJohn Campbell, Harvard UniversityJohn Cochrane, University of

Chicago, Federal Reserve Bank of Chicago, NBER

Source: Disciplined Alpha

Dissecting the market dynamic in 2003

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 11

Disciplineδ Alphα LLCAn Authority on regime based investing

05

101520253035404550

Value Factor Weight

Growth Fac-tor Weight

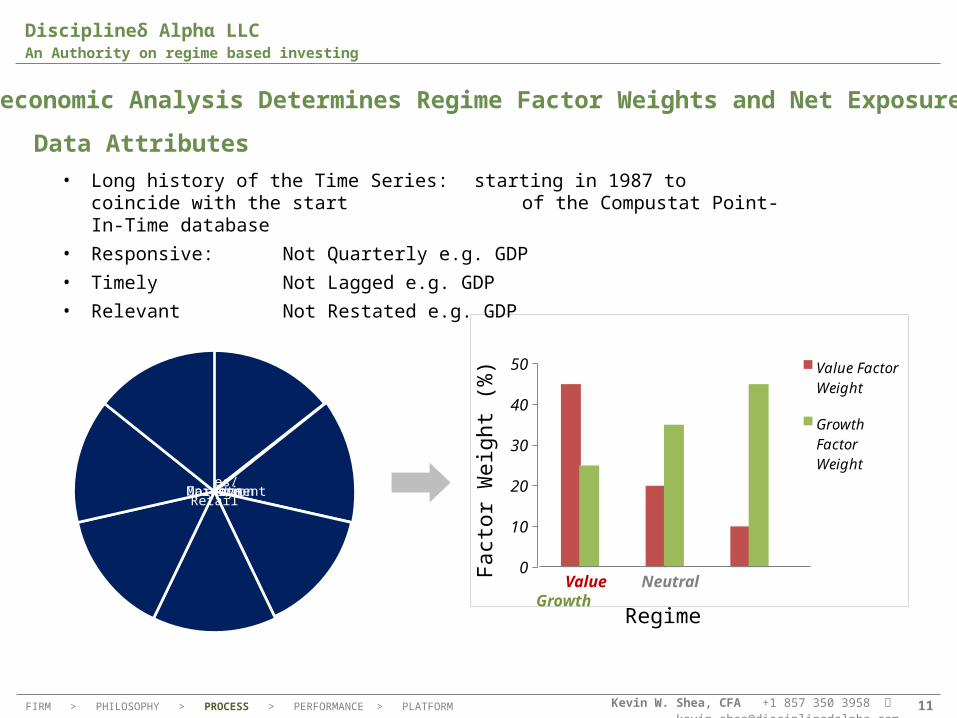

Macroeconomic Analysis Determines Regime Factor Weights and Net Exposures

Fact

or

Weig

ht

(%)

Value Neutral Growth

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

• Long history of the Time Series: starting in 1987 to coincide with the start of the Compustat Point-In-Time database

• Responsive: Not Quarterly e.g. GDP

• Timely Not Lagged e.g. GDP

• Relevant Not Restated e.g. GDP

Regime

Data Attributes

Housing

Banks/Loans

Un-employment

Production

Sales/Retail

Markets

Opinion

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 12

Disciplineδ Alphα LLCAn Authority on regime based investing

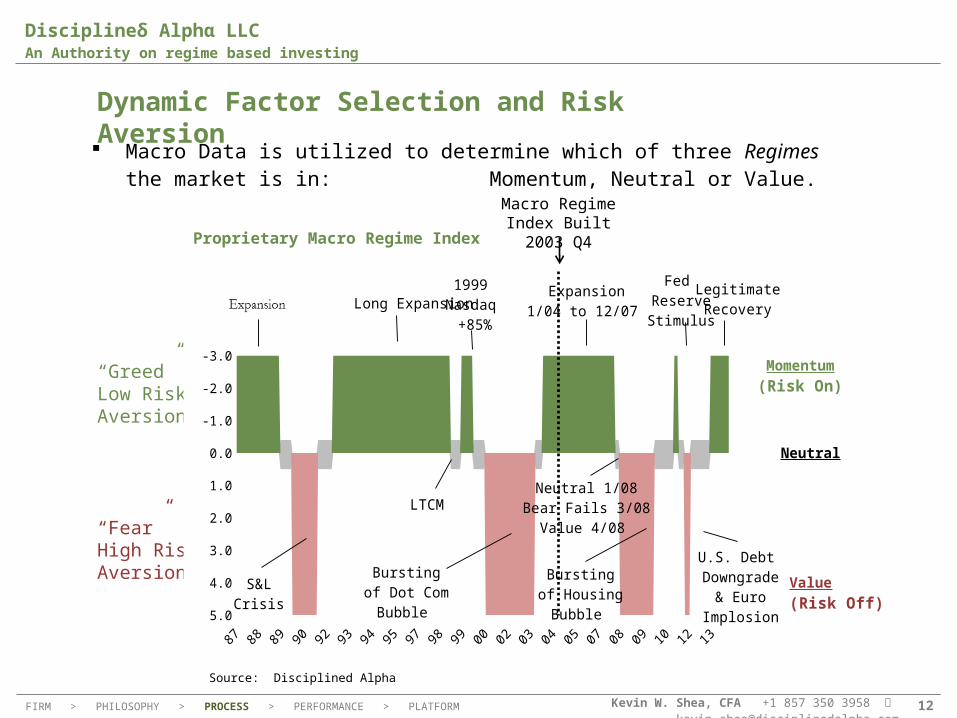

Macro Data is utilized to determine which of three Regimes the market is in: Momentum, Neutral or Value.

Dynamic Factor Selection and Risk Aversion

“Greed”Low Risk Aversion

“Fear”High Risk Aversion

Source: Disciplined Alpha

Proprietary Macro Regime Index

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Neutral

Value(Risk Off)

Long Expansion

LTCM

1999 Nasdaq +85%

Burstingof Dot Com

Bubble

Expansion1/04 to 12/07

Neutral 1/08Bear Fails 3/08

Value 4/08

Burstingof Housing

Bubble

Fed ReserveStimulus

U.S. Debt Downgrade

& EuroImplosion

LegitimateRecovery

S&LCrisis

Momentum(Risk On)

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Macro Regime Index Built2003 Q4

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 13

Disciplineδ Alphα LLCAn Authority on regime based investing

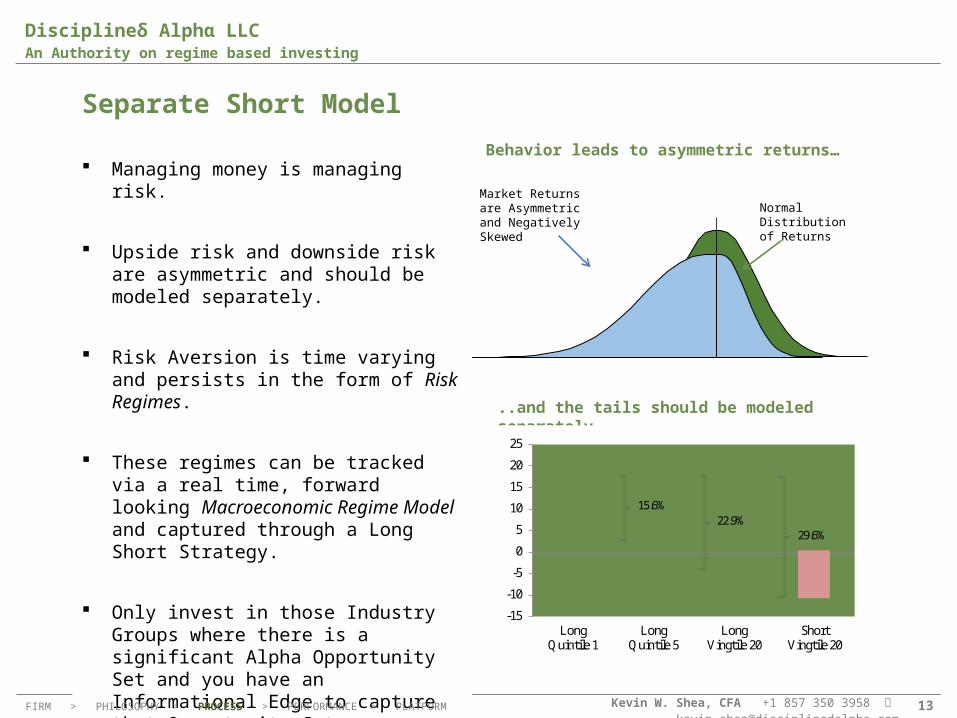

Separate Short Model

Source: Disciplined Alpha

Behavior leads to asymmetric returns…

..and the tails should be modeled separately

Market Returns are Asymmetricand Negatively Skewed

Normal Distribution of Returns

Managing money is managing risk.

Upside risk and downside risk are asymmetric and should be modeled separately.

Risk Aversion is time varying and persists in the form of Risk Regimes.

These regimes can be tracked via a real time, forward looking Macroeconomic Regime Model and captured through a Long Short Strategy.

Only invest in those Industry Groups where there is a significant Alpha Opportunity Set and you have an Informational Edge to capture that Opportunity Set.

-15

-10

-5

0

5

10

15

20

25

LongQuintile 1

LongQuintile 5

LongVingtile 20

ShortVingtile 20

15.6%22.9%

29.6%

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 14

Disciplineδ Alphα LLCAn Authority on regime based investing

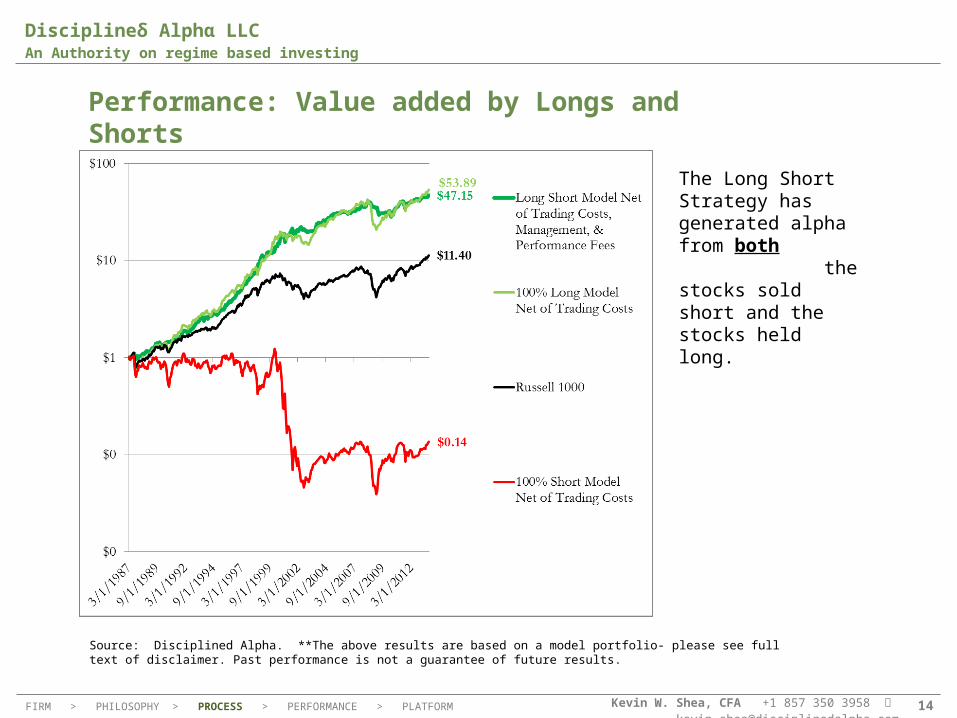

Performance: Value added by Longs and Shorts

Source: Disciplined Alpha. **The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

The Long Short Strategy has generated alpha from both the stocks sold short and the stocks held long.

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 15

Disciplineδ Alphα LLCAn Authority on regime based investing

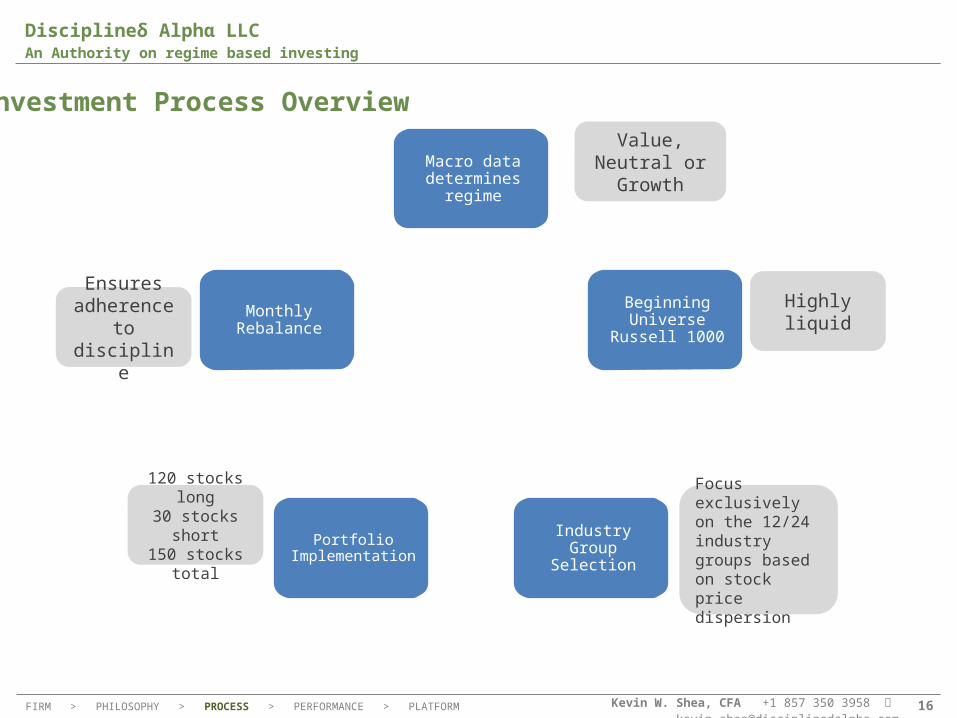

Our investment process:

We analyze a number of the macroeconomic data series that we have tracked and modelled for over a decade. This data determines which macroeconomic regime the overall economy is currently in. The regime determines the respective weight given to value and growth factors.

Once the regime has been determined, we rank a subset of the Russell 1000 based on the regime dependent factor weights. We rank only 12 of the 24 Industry Groups within the Russell 1000 based upon our analysis of stock price dispersion. Several of the factors are unique to each Industry Group. These unique factors are based on hundreds of conversations with company managements.

These analyses result in a portfolio of approximately 150 stocks, which consist of 120 long positions and 30 short positions.

This portfolio is then rebalanced on a monthly basis. FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 16

Disciplineδ Alphα LLCAn Authority on regime based investing

Investment Process Overview

Macro data determines regime

Beginning Universe Russell 1000

Industry Group Selection

Portfolio Implementation

Monthly Rebalance

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Value,Neutral or

Growth

Highly liquid

Focus exclusively on the 12/24 industry groups based on stock price dispersion

120 stocks long30 stocks short150 stocks total

Ensures adherence to

discipline

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 17

Disciplineδ Alphα LLCAn Authority on regime based investing

Performance

$ 49.80

$ 16.29$ 14.00$ 7.97

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Long Short Strategy

HFRI: Equity Hedge

HFRI: Equity Hedge Quantitative Directional

Russell 1000

$ 50.00

$ 25.00

$ 12.50

$ 6.75

$ 3.38

$ 1.00

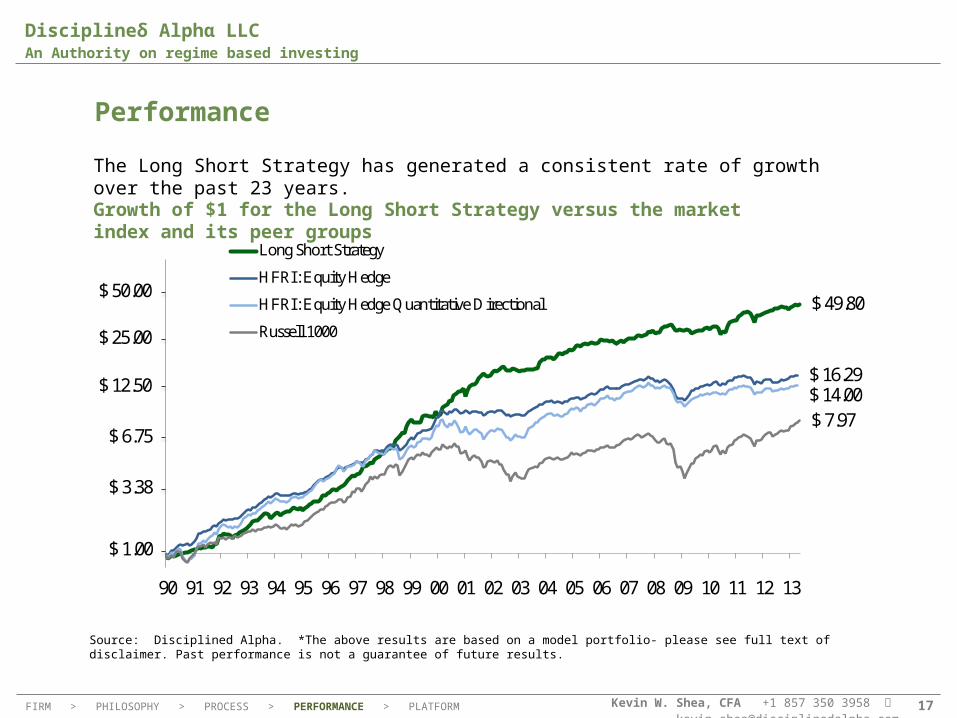

Source: Disciplined Alpha. *The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

The Long Short Strategy has generated a consistent rate of growth over the past 23 years.Growth of $1 for the Long Short Strategy versus the market index and its peer groups

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 18

Disciplineδ Alphα LLCAn Authority on regime based investing

Source: Disciplined Alpha. *The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

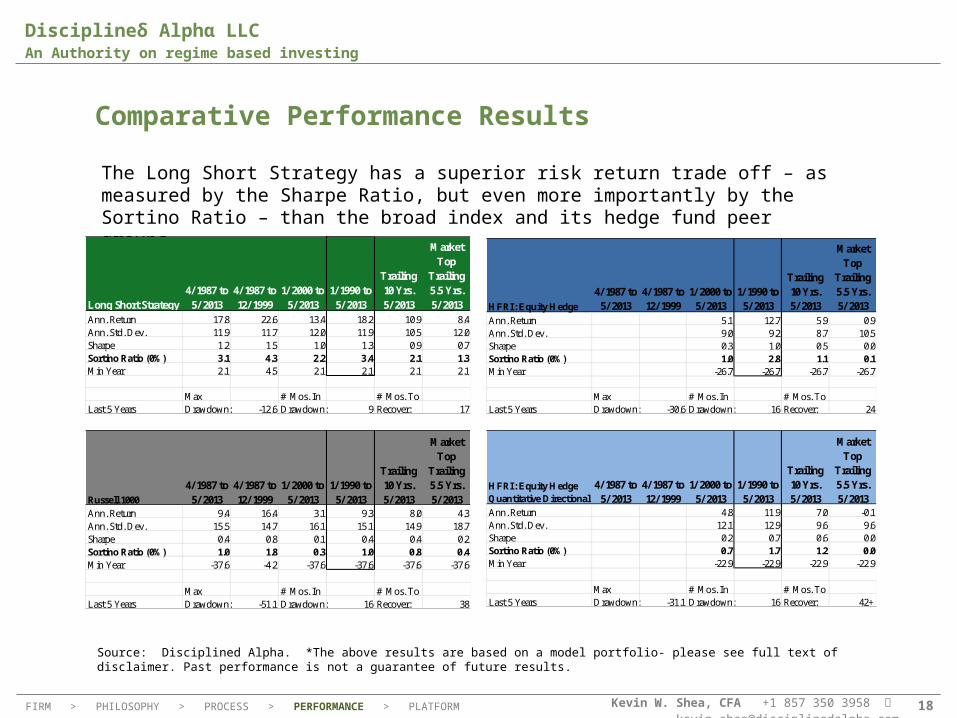

The Long Short Strategy has a superior risk return trade off – as measured by the Sharpe Ratio, but even more importantly by the Sortino Ratio – than the broad index and its hedge fund peer groups.

Comparative Performance Results

Long Short Strategy4/ 1987 to 5/ 2013

4/ 1987 to 12/ 1999

1/ 2000 to 5/ 2013

1/ 1990 to 5/ 2013

Trailing 10 Yrs. 5/ 2013

Since Market Top

Trailing 5.5 Yrs. 5/ 2013

Ann. Return 17.8 22.6 13.4 18.2 10.9 8.4Ann. Std. Dev. 11.9 11.7 12.0 11.9 10.5 12.0Sharpe 1.2 1.5 1.0 1.3 0.9 0.7Sortino Ratio (0%) 3.1 4.3 2.2 3.4 2.1 1.3Min Year 2.1 4.5 2.1 2.1 2.1 2.1

Max # Mos. In # Mos. ToLast 5 Years Drawdown: -12.6 Drawdown: 9 Recover: 17

Russell 1000

4/ 1987 to 5/ 2013

4/ 1987 to 12/ 1999

1/ 2000 to 5/ 2013

1/ 1990 to 5/ 2013

Trailing 10 Yrs. 5/ 2013

Market Top

Trailing 5.5 Yrs. 5/ 2013

Ann. Return 9.4 16.4 3.1 9.3 8.0 4.3Ann. Std. Dev. 15.5 14.7 16.1 15.1 14.9 18.7Sharpe 0.4 0.8 0.1 0.4 0.4 0.2Sortino Ratio (0%) 1.0 1.8 0.3 1.0 0.8 0.4Min Year -37.6 -4.2 -37.6 -37.6 -37.6 -37.6

Max # Mos. In # Mos. ToLast 5 Years Drawdown: -51.1 Drawdown: 16 Recover: 38

HFRI: Equity Hedge

4/ 1987 to 5/ 2013

4/ 1987 to 12/ 1999

1/ 2000 to 5/ 2013

1/ 1990 to 5/ 2013

Trailing 10 Yrs. 5/ 2013

Market Top

Trailing 5.5 Yrs. 5/ 2013

Ann. Return 5.1 12.7 5.9 0.9Ann. Std. Dev. 9.0 9.2 8.7 10.5Sharpe 0.3 1.0 0.5 0.0Sortino Ratio (0%) 1.0 2.8 1.1 0.1Min Year -26.7 -26.7 -26.7 -26.7

Max # Mos. In # Mos. ToLast 5 Years Drawdown: -30.6 Drawdown: 16 Recover: 24

HFRI: Equity Hedge Quantitative Directional

4/ 1987 to 5/ 2013

4/ 1987 to 12/ 1999

1/ 2000 to 5/ 2013

1/ 1990 to 5/ 2013

Trailing 10 Yrs. 5/ 2013

Market Top

Trailing 5.5 Yrs. 5/ 2013

Ann. Return 4.8 11.9 7.0 -0.1Ann. Std. Dev. 12.1 12.9 9.6 9.6Sharpe 0.2 0.7 0.6 0.0Sortino Ratio (0%) 0.7 1.7 1.2 0.0Min Year -22.9 -22.9 -22.9 -22.9

Max # Mos. In # Mos. ToLast 5 Years Drawdown: -31.1 Drawdown: 16 Recover: 42+

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 19

Disciplineδ Alphα LLCAn Authority on regime based investing

Performance: Regimes Matter

Source: Disciplined Alpha. **The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

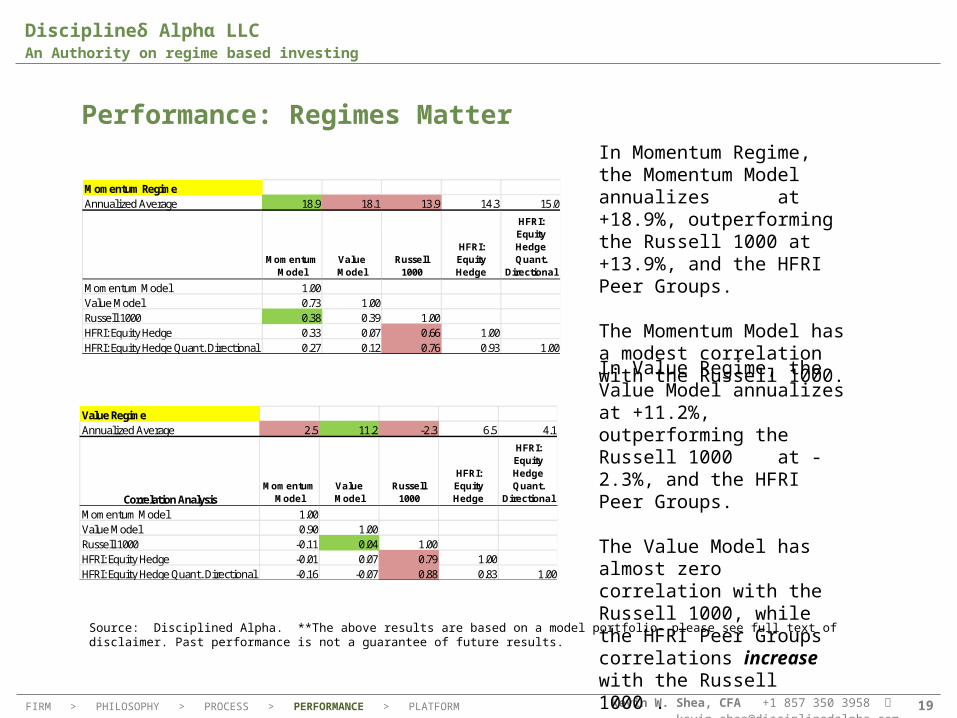

In Momentum Regime, the Momentum Model annualizes at +18.9%, outperforming the Russell 1000 at +13.9%, and the HFRI Peer Groups.

The Momentum Model has a modest correlation with the Russell 1000.

Value RegimeAnnualized Average 2.5 11.2 -2.3 6.5 4.1

Correlation AnalysisMomentum

ModelValue Model

Russell 1000

HFRI: Equity Hedge

HFRI: Equity Hedge Quant.

Directional

Momentum Model 1.00Value Model 0.90 1.00Russell 1000 -0.11 0.04 1.00HFRI: Equity Hedge -0.01 0.07 0.79 1.00HFRI: Equity Hedge Quant. Directional -0.16 -0.07 0.88 0.83 1.00

Momentum RegimeAnnualized Average 18.9 18.1 13.9 14.3 15.0

Momentum Model

Value Model

Russell 1000

HFRI: Equity Hedge

HFRI: Equity Hedge Quant.

Directional

Momentum Model 1.00Value Model 0.73 1.00Russell 1000 0.38 0.39 1.00HFRI: Equity Hedge 0.33 0.07 0.66 1.00HFRI: Equity Hedge Quant. Directional 0.27 0.12 0.76 0.93 1.00

In Value Regime, the Value Model annualizes at +11.2%, outperforming the Russell 1000 at -2.3%, and the HFRI Peer Groups.

The Value Model has almost zero correlation with the Russell 1000, while the HFRI Peer Groups correlations increase with the Russell 1000 .

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 20

Disciplineδ Alphα LLCAn Authority on regime based investing

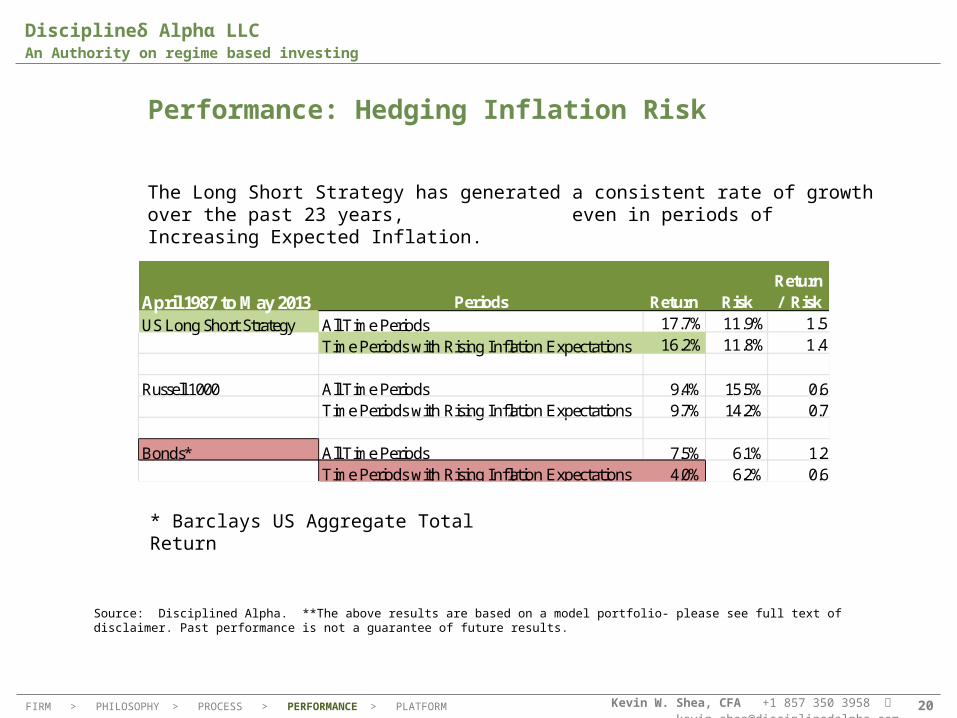

Performance: Hedging Inflation Risk

Source: Disciplined Alpha. **The above results are based on a model portfolio- please see full text of disclaimer. Past performance is not a guarantee of future results.

The Long Short Strategy has generated a consistent rate of growth over the past 23 years, even in periods of Increasing Expected Inflation.

* Barclays US Aggregate Total Return

April 1987 to May 2013 Periods Return RiskReturn / Risk

US Long Short Strategy All Time Periods 17.7% 11.9% 1.5

Time Periods with Rising Inflation Expectations 16.2% 11.8% 1.4

Russell 1000 All Time Periods 9.4% 15.5% 0.6Time Periods with Rising Inflation Expectations 9.7% 14.2% 0.7

Bonds* All Time Periods 7.5% 6.1% 1.2Time Periods with Rising Inflation Expectations 4.0% 6.2% 0.6

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 21

Disciplineδ Alphα LLCAn Authority on regime based investing

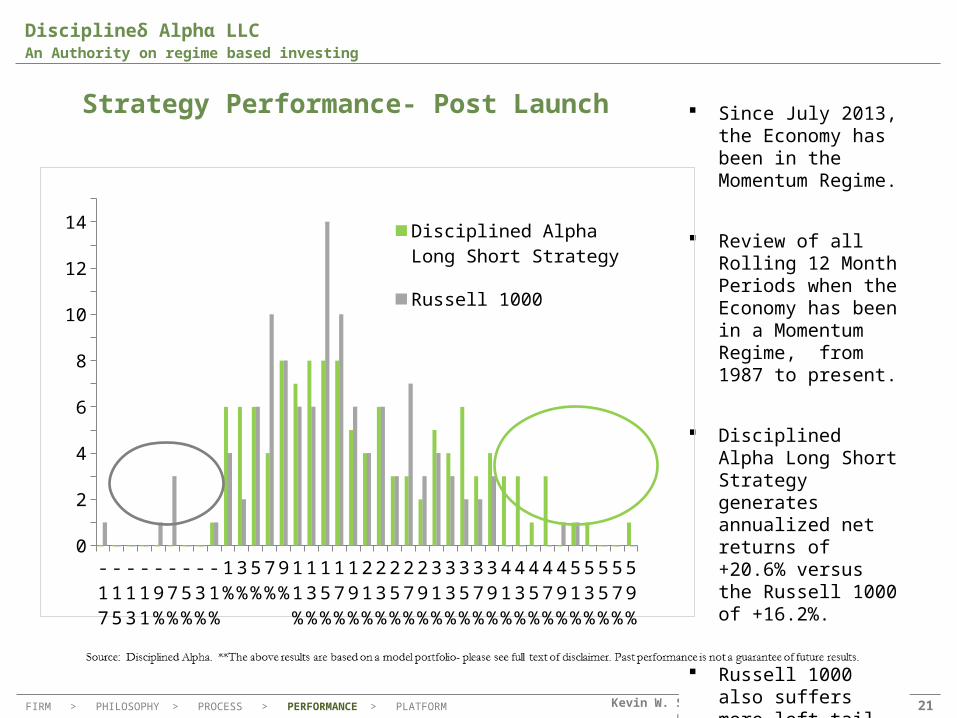

Strategy Performance- Post Launch Since July 2013, the Economy has been in the Momentum Regime.

Review of all Rolling 12 Month Periods when the Economy has been in a Momentum Regime, from 1987 to present.

Disciplined Alpha Long Short Strategy generates annualized net returns of +20.6% versus the Russell 1000 of +16.2%.

Russell 1000 also suffers more left tail events.

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

-17%

-15%

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

45%

47%

49%

51%

53%

55%

57%

59%

0123456789

101112131415

Disciplined Alpha Long Short Strategy

Russell 1000

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 22

Disciplineδ Alphα LLCAn Authority on regime based investing

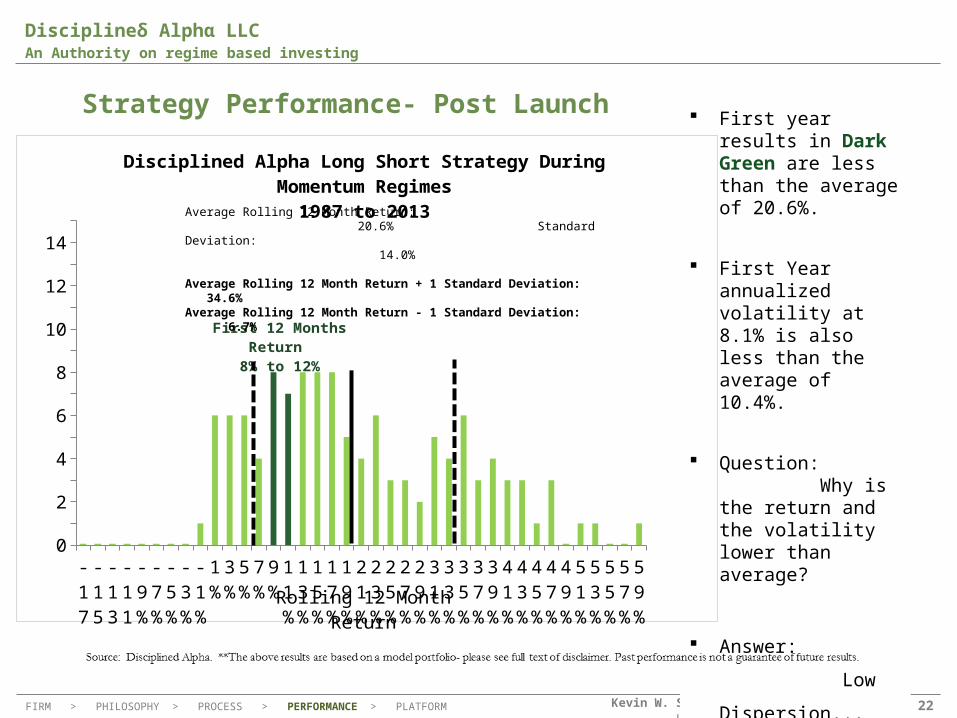

Strategy Performance- Post Launch First year results in Dark Green are less than the average of 20.6%.

First Year annualized volatility at 8.1% is also less than the average of 10.4%.

Question: Why is the return and the volatility lower than average?

Answer:

Low Dispersion...

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

-17%

-15%

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

45%

47%

49%

51%

53%

55%

57%

59%

0123456789

101112131415

Disciplined Alpha Long Short Strategy During Momentum Regimes1987 to 2013

Rolling 12 Month Return

First 12 Months Return 8% to 12%

Average Rolling 12 Month Return: 20.6% Standard Deviation: 14.0%

Average Rolling 12 Month Return + 1 Standard Deviation: 34.6%Average Rolling 12 Month Return - 1 Standard Deviation: 6.7%

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 23

Disciplineδ Alphα LLCAn Authority on regime based investing

Appendix

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 24

Disciplineδ Alphα LLCAn Authority on regime based investing

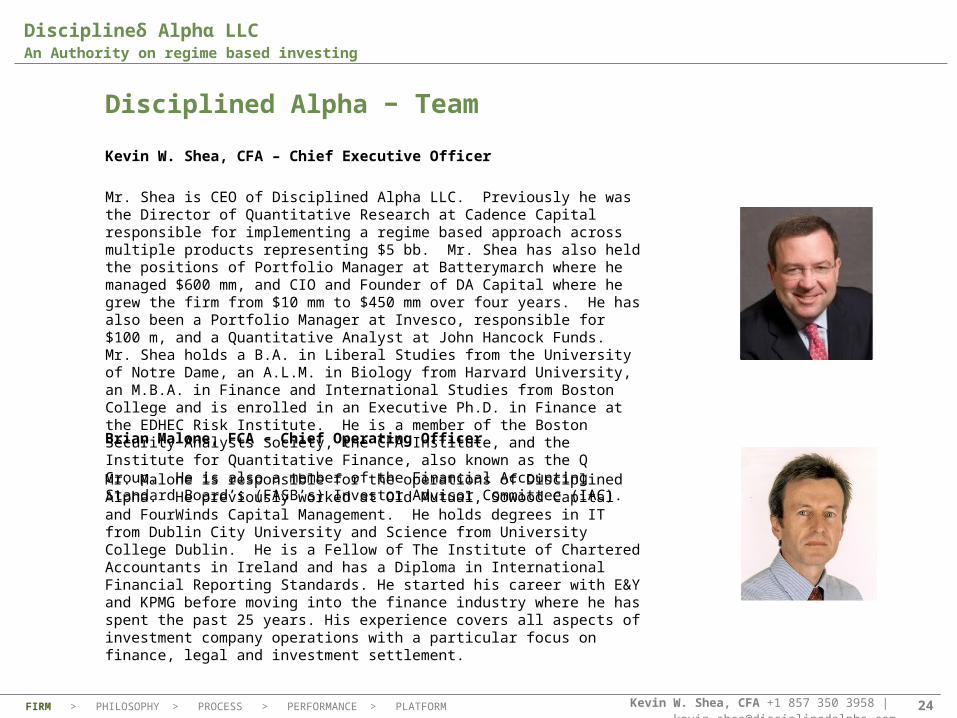

Kevin W. Shea, CFA – Chief Executive Officer

Mr. Shea is CEO of Disciplined Alpha LLC. Previously he was the Director of Quantitative Research at Cadence Capital responsible for implementing a regime based approach across multiple products representing $5 bb. Mr. Shea has also held the positions of Portfolio Manager at Batterymarch where he managed $600 mm, and CIO and Founder of DA Capital where he grew the firm from $10 mm to $450 mm over four years. He has also been a Portfolio Manager at Invesco, responsible for $100 m, and a Quantitative Analyst at John Hancock Funds. Mr. Shea holds a B.A. in Liberal Studies from the University of Notre Dame, an A.L.M. in Biology from Harvard University, an M.B.A. in Finance and International Studies from Boston College and is enrolled in an Executive Ph.D. in Finance at the EDHEC Risk Institute. He is a member of the Boston Security Analysts Society, the CFA Institute, and the Institute for Quantitative Finance, also known as the Q Group. He is also a member of the Financial Accounting Standard Board’s (FASB’s) Investor Advisor Committee (IAC).

Brian Malone, FCA – Chief Operating Officer

Mr. Malone is responsible for the operations of Disciplined Alpha. He previously worked at Old Mutual, Sowood Capital and FourWinds Capital Management. He holds degrees in IT from Dublin City University and Science from University College Dublin. He is a Fellow of The Institute of Chartered Accountants in Ireland and has a Diploma in International Financial Reporting Standards. He started his career with E&Y and KPMG before moving into the finance industry where he has spent the past 25 years. His experience covers all aspects of investment company operations with a particular focus on finance, legal and investment settlement.

Disciplined Alpha − Team

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 25

Disciplineδ Alphα LLCAn Authority on regime based investing

Disciplined Alpha − Team

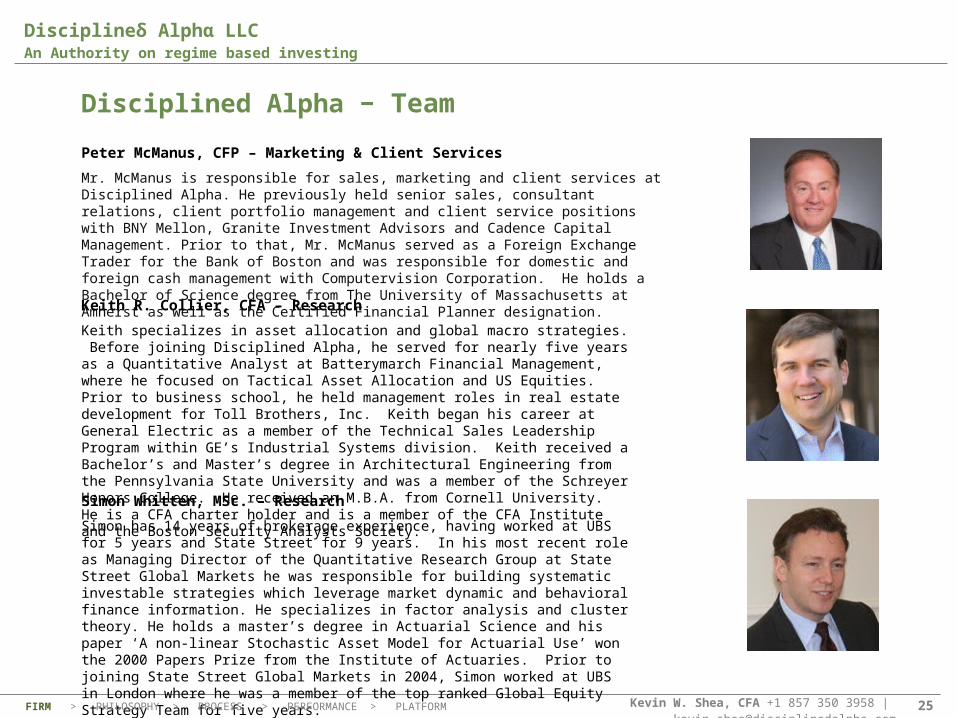

Simon Whitten, MSc. – Research

Simon has 14 years of brokerage experience, having worked at UBS for 5 years and State Street for 9 years. In his most recent role as Managing Director of the Quantitative Research Group at State Street Global Markets he was responsible for building systematic investable strategies which leverage market dynamic and behavioral finance information. He specializes in factor analysis and cluster theory. He holds a master’s degree in Actuarial Science and his paper ‘A non-linear Stochastic Asset Model for Actuarial Use’ won the 2000 Papers Prize from the Institute of Actuaries. Prior to joining State Street Global Markets in 2004, Simon worked at UBS in London where he was a member of the top ranked Global Equity Strategy Team for five years.

Keith R. Collier, CFA – Research

Keith specializes in asset allocation and global macro strategies. Before joining Disciplined Alpha, he served for nearly five years as a Quantitative Analyst at Batterymarch Financial Management, where he focused on Tactical Asset Allocation and US Equities. Prior to business school, he held management roles in real estate development for Toll Brothers, Inc. Keith began his career at General Electric as a member of the Technical Sales Leadership Program within GE’s Industrial Systems division. Keith received a Bachelor’s and Master’s degree in Architectural Engineering from the Pennsylvania State University and was a member of the Schreyer Honors College. He received an M.B.A. from Cornell University. He is a CFA charter holder and is a member of the CFA Institute and the Boston Security Analysts Society.

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Peter McManus, CFP – Marketing & Client Services

Mr. McManus is responsible for sales, marketing and client services at Disciplined Alpha. He previously held senior sales, consultant relations, client portfolio management and client service positions with BNY Mellon, Granite Investment Advisors and Cadence Capital Management. Prior to that, Mr. McManus served as a Foreign Exchange Trader for the Bank of Boston and was responsible for domestic and foreign cash management with Computervision Corporation. He holds a Bachelor of Science degree from The University of Massachusetts at Amherst as well as the Certified Financial Planner designation.

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 26

Disciplineδ Alphα LLCAn Authority on regime based investing

Disciplined Alpha − Team

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

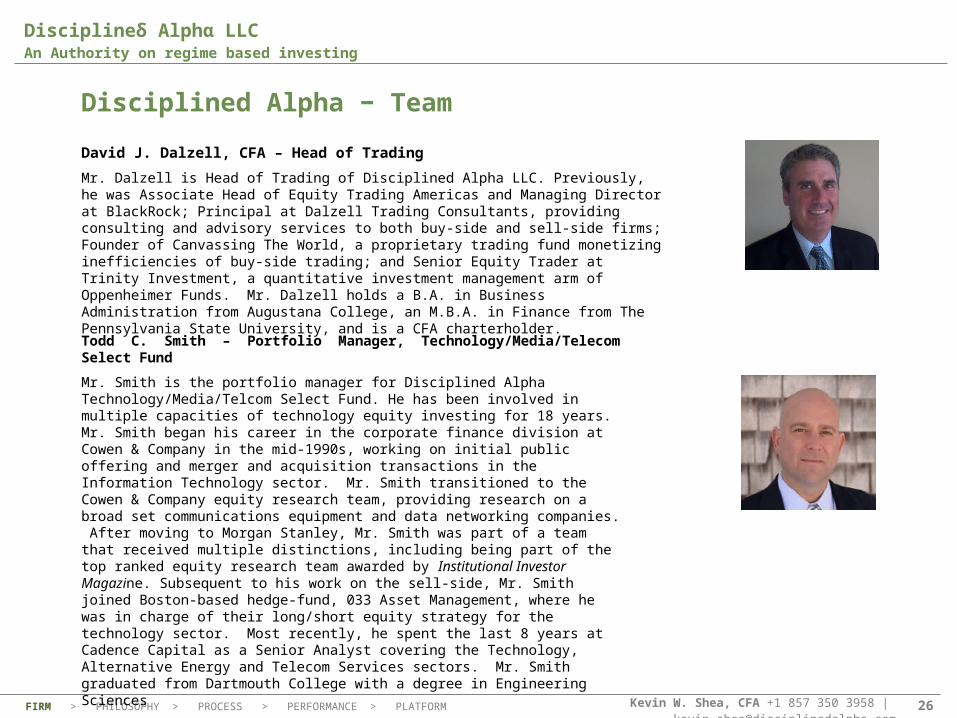

David J. Dalzell, CFA – Head of Trading

Mr. Dalzell is Head of Trading of Disciplined Alpha LLC. Previously, he was Associate Head of Equity Trading Americas and Managing Director at BlackRock; Principal at Dalzell Trading Consultants, providing consulting and advisory services to both buy-side and sell-side firms; Founder of Canvassing The World, a proprietary trading fund monetizing inefficiencies of buy-side trading; and Senior Equity Trader at Trinity Investment, a quantitative investment management arm of Oppenheimer Funds. Mr. Dalzell holds a B.A. in Business Administration from Augustana College, an M.B.A. in Finance from The Pennsylvania State University, and is a CFA charterholder.

Todd C. Smith – Portfolio Manager, Technology/Media/Telecom Select Fund

Mr. Smith is the portfolio manager for Disciplined Alpha Technology/Media/Telcom Select Fund. He has been involved in multiple capacities of technology equity investing for 18 years. Mr. Smith began his career in the corporate finance division at Cowen & Company in the mid-1990s, working on initial public offering and merger and acquisition transactions in the Information Technology sector. Mr. Smith transitioned to the Cowen & Company equity research team, providing research on a broad set communications equipment and data networking companies. After moving to Morgan Stanley, Mr. Smith was part of a team that received multiple distinctions, including being part of the top ranked equity research team awarded by Institutional Investor Magazine. Subsequent to his work on the sell-side, Mr. Smith joined Boston-based hedge-fund, 033 Asset Management, where he was in charge of their long/short equity strategy for the technology sector. Most recently, he spent the last 8 years at Cadence Capital as a Senior Analyst covering the Technology, Alternative Energy and Telecom Services sectors. Mr. Smith graduated from Dartmouth College with a degree in Engineering Sciences

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 27

Disciplineδ Alphα LLCAn Authority on regime based investing

Disciplined Alpha − Team

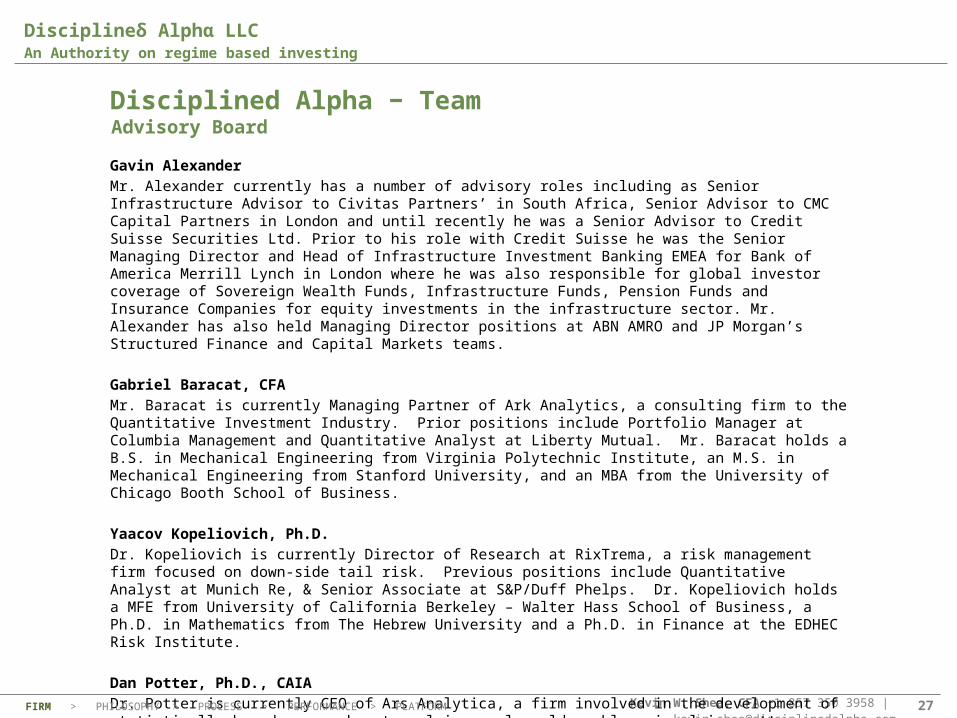

Gavin Alexander Mr. Alexander currently has a number of advisory roles including as Senior Infrastructure Advisor to Civitas Partners’ in South Africa, Senior Advisor to CMC Capital Partners in London and until recently he was a Senior Advisor to Credit Suisse Securities Ltd. Prior to his role with Credit Suisse he was the Senior Managing Director and Head of Infrastructure Investment Banking EMEA for Bank of America Merrill Lynch in London where he was also responsible for global investor coverage of Sovereign Wealth Funds, Infrastructure Funds, Pension Funds and Insurance Companies for equity investments in the infrastructure sector. Mr. Alexander has also held Managing Director positions at ABN AMRO and JP Morgan’s Structured Finance and Capital Markets teams.

Gabriel Baracat, CFAMr. Baracat is currently Managing Partner of Ark Analytics, a consulting firm to the Quantitative Investment Industry. Prior positions include Portfolio Manager at Columbia Management and Quantitative Analyst at Liberty Mutual. Mr. Baracat holds a B.S. in Mechanical Engineering from Virginia Polytechnic Institute, an M.S. in Mechanical Engineering from Stanford University, and an MBA from the University of Chicago Booth School of Business.

Yaacov Kopeliovich, Ph.D. Dr. Kopeliovich is currently Director of Research at RixTrema, a risk management firm focused on down-side tail risk. Previous positions include Quantitative Analyst at Munich Re, & Senior Associate at S&P/Duff Phelps. Dr. Kopeliovich holds a MFE from University of California Berkeley – Walter Hass School of Business, a Ph.D. in Mathematics from The Hebrew University and a Ph.D. in Finance at the EDHEC Risk Institute.

Dan Potter, Ph.D., CAIADr. Potter is currently CEO of Ars Analytica, a firm involved in the development of statistically based approaches to solving real world problems involving pattern recognition and data modeling for the healthcare, financial and technology sectors. Dr. Potter is also an Adjunct Professor at Brown University. Previous positions include Managing Partner at Gotham Research and Chief Technology Officer for Third Level Data. Dr. Potter holds a B.S. in Mathematics & Computer Science as well as an M.S. and Ph.D. in Applied Mathematics from Brown University. Dr. Potter is also a former National Science Foundation Fellow.

Advisory Board

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 28

Disciplineδ Alphα LLCAn Authority on regime based investing

The Model is diversified across styles and always includes exposure to the following factors:

– Valuation– Quality– Profitability– Momentum

Long Short strategy– Long Positions typical range: 100 to 130– Short Positions typical range: 25 to 35

Position sizes– Equally weighted, avoiding the multiple regime problem inherent in

most risk models– Position weights are not modified if within 0.2% of the target weight

Portfolio Construction & Risk Control

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 29

Disciplineδ Alphα LLCAn Authority on regime based investing

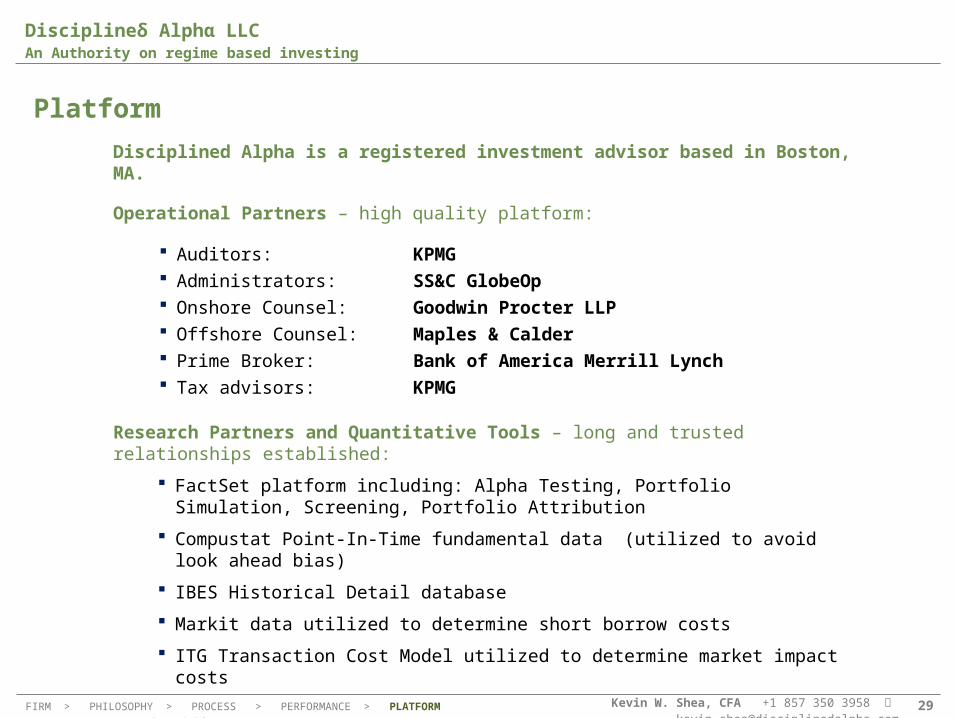

Disciplined Alpha is a registered investment advisor based in Boston, MA.

Operational Partners – high quality platform:

Auditors: KPMG Administrators: SS&C GlobeOp Onshore Counsel: Goodwin Procter LLP Offshore Counsel: Maples & Calder Prime Broker: Bank of America Merrill Lynch Tax advisors: KPMG

Research Partners and Quantitative Tools – long and trusted relationships established:

FactSet platform including: Alpha Testing, Portfolio Simulation, Screening, Portfolio Attribution

Compustat Point-In-Time fundamental data (utilized to avoid look ahead bias)

IBES Historical Detail database

Markit data utilized to determine short borrow costs

ITG Transaction Cost Model utilized to determine market impact costs

Head Office: 60 State Street, Suite 3750, Boston, MA 02109 USA

Platform

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 30

Disciplineδ Alphα LLCAn Authority on regime based investing

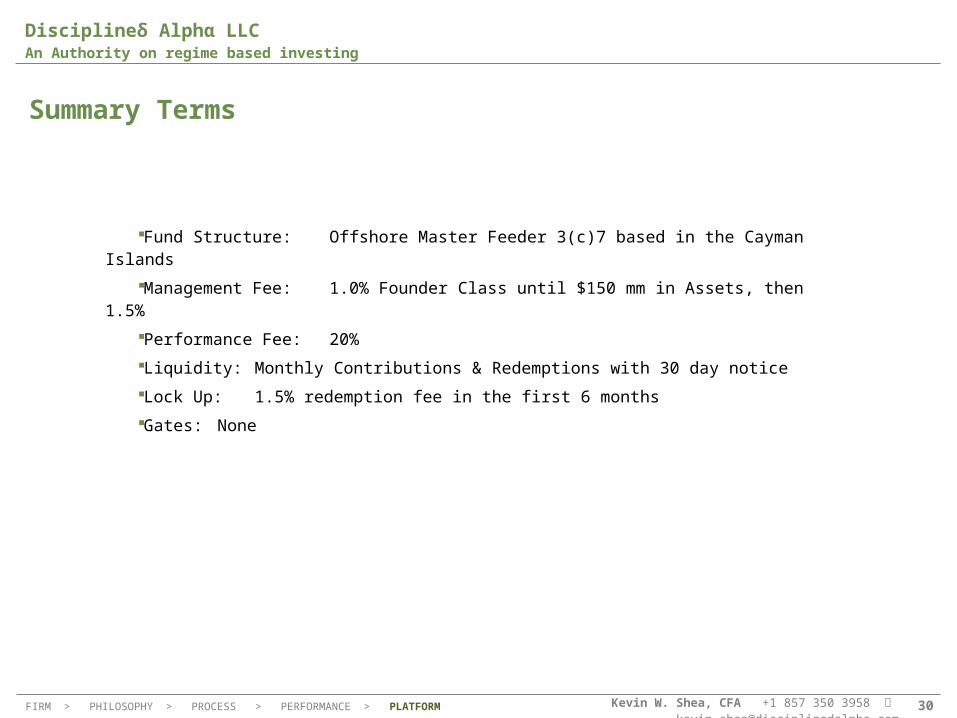

Fund Structure: Offshore Master Feeder 3(c)7 based in the Cayman Islands

Management Fee: 1.0% Founder Class until $150 mm in Assets, then 1.5%

Performance Fee: 20%Liquidity: Monthly Contributions & Redemptions with 30 day noticeLock Up: 1.5% redemption fee in the first 6 monthsGates: None

Summary Terms

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Kevin W. Shea, CFA +1 857 350 3958 | [email protected] 31

Disciplineδ Alphα LLCAn Authority on regime based investing

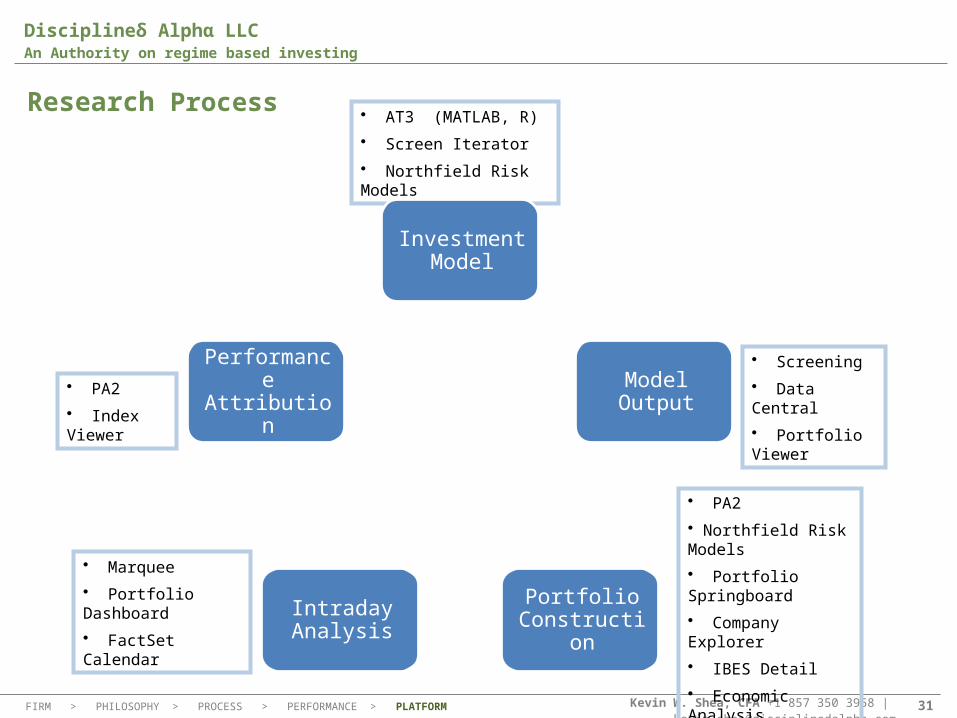

Research Process • AT3 (MATLAB, R)

• Screen Iterator

• Northfield Risk Models

• Screening

• Data Central

• Portfolio Viewer

• PA2

• Northfield Risk Models

• Portfolio Springboard

• Company Explorer

• IBES Detail

• Economic Analysis

• Marquee

• Portfolio Dashboard

• FactSet Calendar

• PA2

• Index Viewer

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM

Investment Model

Model Output

Portfolio Construction

Intraday Analysis

Performance Attribution

Kevin W. Shea, CFA +1 857 350 3958 [email protected] 32

Disciplineδ Alphα LLCAn Authority on regime based investing

This document may not be reproduced in any form without the prior written authorization of Disciplined Alpha LLC. It is intended only for the exclusive use of the recipient, who agrees not to distribute or disclose its contents to another party.

This document is only a summary of several discussion points about Disciplined Alpha LLC and the fund it manages and is not intended to be an offer to sell or a solicitation to invest in any such vehicle. At the date of this presentation, there are no funds actively managed by Disciplined Alpha LLC. The results presented in this documents refer to a model portfolio managed by Kevin Shea and not to any actually traded fund or portfolio. Therefore there is no guarantee that these or even similar results would have been obtained had such a portfolio been traded.

Past performance does not guarantee future returns and potential for gains is accompanied by the possibility of loss. Leverage will be employed, which can make investment performance volatile and amplify potential gains or losses. An investor should not make an investment unless they are prepared to lose a substantial portion of their investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. Opportunities for withdrawal and transferability of interests are restricted, so investors may not have access to capital when it is needed. The Fund/s managed may be concentrated and a lack of diversification may result in higher risk. A more complete description of these entities, and the inherent risks involved, can be found in a Private Placement Memorandum for each Fund, which a prospective investor should review thoroughly before investing. Fund interests are intended to be non-public and remain unregistered under the Securities Act of 1933 (the Act) and therefore offer and sale of interests must be conducted in accordance with legal restrictions. By accepting delivery of this document, the recipient represents that they are an accredited investor as defined by Regulation D of the Act and a qualified purchaser as defined by Section 3(c)(1) or Section 3(c)(7), whichever may apply, of the Investment Company Act of 1940.

Prospective investors should consult their own legal and financial advisors to determine the suitability of an investment for their particular situation and to be aware of and comply with any legal or other restrictions. This document is for illustrative and discussion purposes only and may not accurately or completely represent any Disciplined Alpha Fund. Furthermore, there is no guarantee that information will be correct after the date this document has been distributed and Disciplined Alpha LLC will not notify you of any changes to the information contained in this document. Prospective investors are encouraged to ask for additional materials and ask further questions about any proposed Fund investment.

Important Information – Please Read

FIRM > PHILOSOPHY > PROCESS > PERFORMANCE > PLATFORM