Embed Size (px)

Citation preview

DISABILITY INCOME INSURANCE

• Objectives• Discuss disability insurance as a risk transfer tool• Identify and describe the key product features of long-

term disability insurance (LTD)• Discuss the importance of how disability is defined and

identify the three main definitions of disability• Discuss the factors that impact on LTD premium• Discuss the features that address the issue of partial

disability• Identify the common exclusions found in the LTD

contract

1

Why Is Disability Income Insurance So Important?

• It replaces a portion of income lost due to illness or injury

• Helps provide peace of mind for family members who depend on your income

2

Can it Happen to You? Some Facts…

• According to the US Census Bureau, nearly seventeen percent of working-age Americans reported a disability in 2010

• Three in ten workers entering the work force today will become disabled before retiring.

• An illness or accident will keep one in five people out of work for at least a year during their working careers.

• One in 8 workers will be disabled for at least five years during their working years

• Of the over 6.8 million workers receiving SS disability benefits, almost half are under age 50.

• The average long-term disability absence lasts 2.5 years.• 63 percent of all disabling injuries occur outside of work. Workers

compensation does not apply.• According to the U.S. Bureau of Labor Statistics, 38 percent of all

workers in private industry were participating in short-term disability income insurance in 2012; 32 percent were participating in long-term disability income insurance.

• Sources:• NAIC, ACLI, CDA, BenefitsPro

3

4

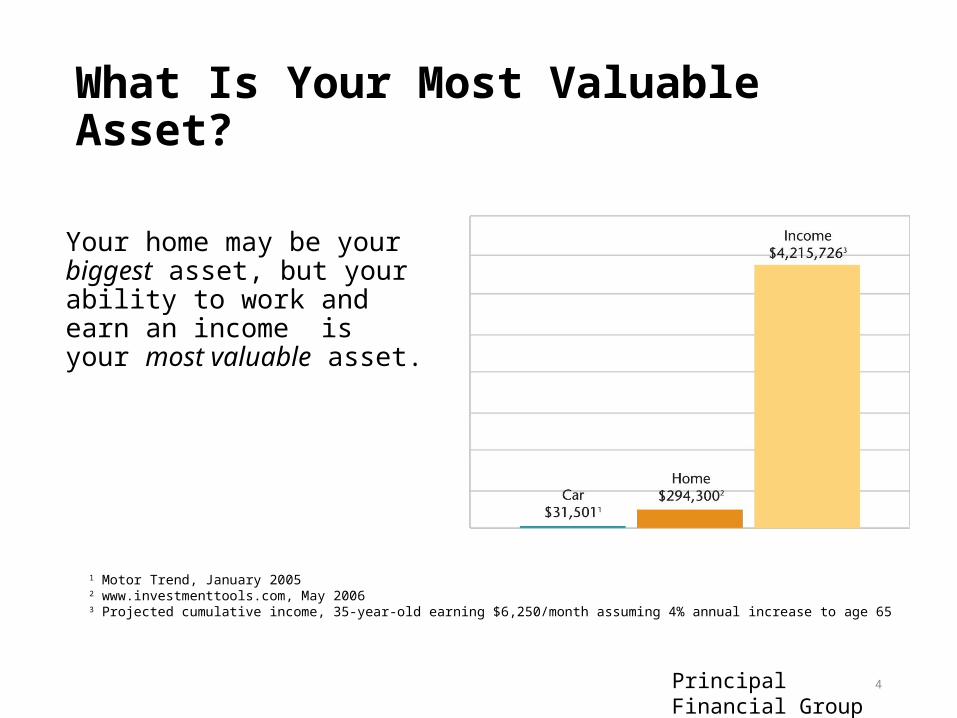

What Is Your Most Valuable Asset?

Your home may be your biggest asset, but your ability to work and earn an income is your most valuable asset.

1 Motor Trend, January 20052 www.investmenttools.com, May 20063 Projected cumulative income, 35-year-old earning $6,250/month assuming 4% annual increase to age 65

Principal Financial Group

5

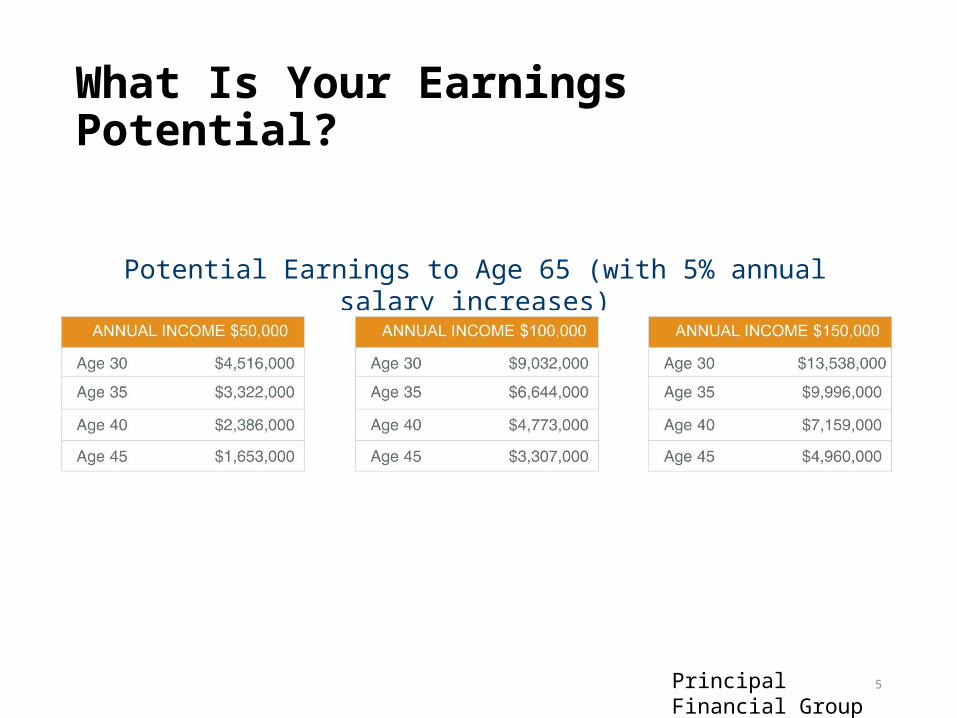

Potential Earnings to Age 65 (with 5% annual salary increases)

What Is Your Earnings Potential?

Principal Financial Group

6

The Need

Approximately 30% of all people aged 35 to 65 will suffer a disability for at least 90 days, and about

one in seven can expect to become disabled for five

years or more.*

*Health Insurance of America, 2000

Principal Financial Group

7

Times Are Different Now.

What used to cause death, now causes disability…

For example, deaths due to hypertension are down 73%, while disabilities due to hypertension have increased by 70%.

Principal Financial Group

8

Leading Causes of Disability Claims, 2013

Cancer Back Disorders Injuries Cardiovascular Joint Disorders0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Leading Causes of Disability Claims: Long-Term

Source: Unum/BenefitsPro

19.50%

10.10%

8.30%

7.80%

7.10%

Leading Causes of Disability Claims: Short-Term

Pregancies (Normal)

Non-back Insuries

Pregancies (Complications)

Digestive/Intestinal

Back

9

Source: Principal Life Disability Insurance claims incurred as of March 2007. The above is for illustration purposes only and is not intended as an inclusive representation of all claims.

Real claims, it can happen ….

Principal Financial Group

10

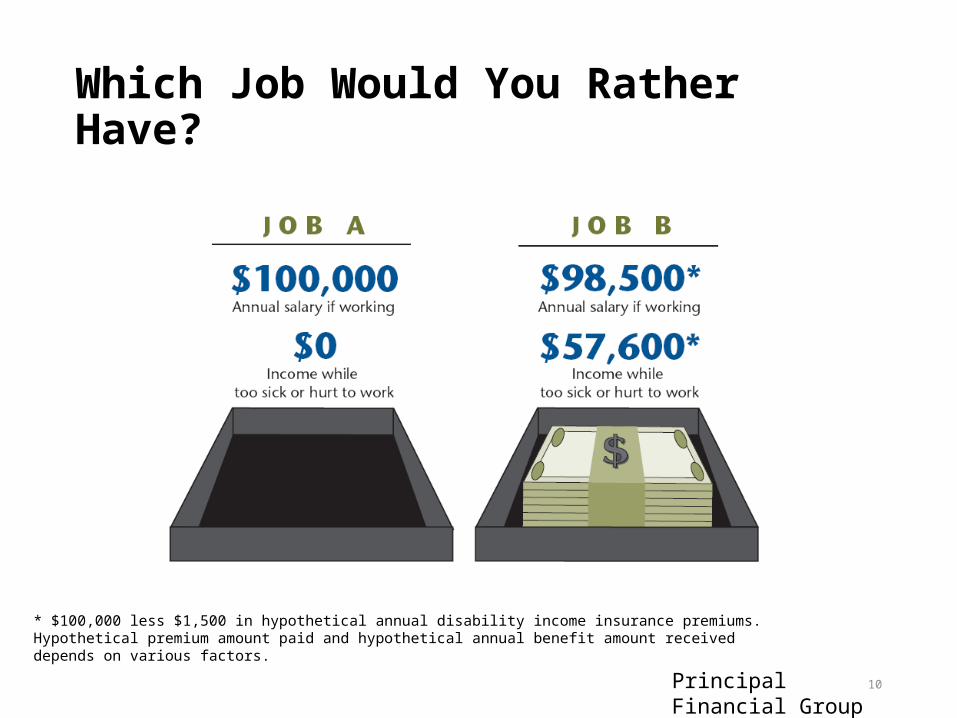

Which Job Would You Rather Have?

* $100,000 less $1,500 in hypothetical annual disability income insurance premiums. Hypothetical premium amount paid and hypothetical annual benefit amount received depends on various factors.

Principal Financial Group

11

Could You Afford Your Home Without Your Income?

Unexpected illnesses and injuries cause 350,000 personal bankruptcies each year.

Nearly 50% of all home foreclosures are due to a disability.

1 out of every 18 mortgages are not being paid because of a disability to the mortgage holder.

Source: National Underwriter, HUD

Principal Financial Group

Can you live on 42% of your income?

Is employer-provided group long-term disability (LTD) insurance coverage enough?

12

Chart based on $6,250 gross monthly income ($75,000 annual), with 60% Group long-term disability program, assuming a 30% tax bracket for Federal, State and FICA

Principal Financial Group

What If You Were Unable To Work?

• What would happen to your income?• How would you maintain your lifestyle?• Where would the money come from to pay for

bills?• What happens to your retirement savings and

other financial goals?

13

Addressing the Problem: Non-Insurance Options

• Borrow money from family or friends• Sell property or investment assets• Use savings, credit cards or home equity• Move from your home• Social Security Disability Benefits only if strict

eligibility requirements are met, e.g.,• you must first have worked in jobs covered by Social

Security• you must have a medical condition that meets Social

Security's definition of disability.

14

15

Insuring the Exposure

• Individual• Short-term or cause related• Long-term disability (LTD)

• Employer• Group STDI• Group LTD• Worker’s Comp• Others?

Key Provisions of LTD Insurance

•Definitions•Benefits•Waiting/Elimination Periods•Rating Factors

16

Definition of Disability is a Key Contract Feature

• The four most common definitions of total disability are:

1. Inability to perform the duties of the insured’s occupation2. Inability to perform the duties of any occupation for whichthe insured is reasonably fitted by education, training, andexperience3. Inability to perform the duties of any gainful occupation4. Loss-of-income test, i.e., your income is reduced as a result of sickness

or accident

Most insurers use a combination of 1 & 2

17

Other Definitions

Partial disability is defined as the inability of the insured to perform one or more important duties of his or her occupationSome policies offer partial disability benefitsUsually, partial disability benefits must follow total disabilityPartial disability benefits are paid at a reduced rate for a

shorter periodResidual disability means a pro rata disability benefit is

paid to an insured whose earned income is reduced because of an accident or sicknessThe typical provision has a time and duties test that

considers (compares) both income and occupation

18

Presumptive Disability

• Within the contract• Waiting Period waived• Loss of sight, hearing, limbs

• Presumptive Disability under the Social Security Administration

• The Social Security Administration may (but not required) to pay benefits to a person while it gathers the evidence needed to make a decision on his or her case.

• disabled people with little or no income or low benefits from State Disability Insurance (SDI) or Social Security Disability Insurance (SSDI)..

19

Benefit Issues

• Monthly Amount (“Benefit”)• Replacing “earned” income• ~ 2/3 maximum

• Duration (“Benefit Period”)• the length of time that disability payments are payable after the elimination

period is met• 2-5-age65-age70-lifetime• Given that most disabilities have durations of less than two years what

benefit period should be selected?• Individual policies normally contain an elimination (or waiting)

period, during which time benefits are not paid• The typical elimination period is 30 days

• A waiver-of-premium provision allows for future premiums to be waived as long as the insured remains disabled

• Policies typically include a rehabilitation provision

Elimination or Waiting Period

• Length• 30-60-90-180-360

• Compare to a property insurance deductible • Recurrence Period

• 6 months same cause

21

Other Features

• Waiver of Premium• Insuring Clause

• Guaranteed Renewable• Policy cannot be cancelled• Other provisions of the contract cannot be changed.• Rates can be adjusted, as long as its for the entire class of insureds

• Noncancellable• Policy cannot be cancelled• Rates will not change• Other policy provisions will not change• costly but great feature

• Cancelable policies• Benefits/Exposure to consumer?

22

Rehabilitation Incentives

Rehabilitation BenefitBoosts your benefit (to some %) when you work within

a participating rehabilitation programFamily Care Expense Reimbursement

Reimburses for eligible expenses incurred for the care of each qualified family member when working or participating in an approved rehabilitation program

Work Incentive BenefitLets you receive up to 100% of your pre-disability

earnings including your disability benefit, rehabilitative work earnings, rehabilitation incentives and other income sources.

23

Common Exclusions

• Normal pregnancy• Self-inflicted intentional injuries• War or military duty• Injury in illegal occupation or commiting crime• Non-passenger flying• Drug abuse

24

Rating Factors

AgeGenderOccupation ClassCurrent health statusPrior disabilities?Location?Marital Status?

25

26

Premium Factors

Rate (see above)Benefit amountBenefit periodDefinitionRiders/Optional CoveragesInsurer profitability/experience/goalsUncertainty about current/future disability

markets

27

Example: Cost of Disability Income Insurance policy

Age Monthly Premium 30 $37.8435 $45.1640 $54.85 45 $63.72 50 $70.55

The average cost for a disability income insurance policy is 1% - 3% of your annual income.

Assumptions and Optional Benefits: $50,000 Annual Salary, $2,500/Monthly Benefit, Colorado Resident, Male, Occupation Class 4A,

Non-Smoker, 90 Day Elimination Period, To Age 67 Benefit Period, Your Occupation Protection, and Residual/Partial Disability Benefit rider.

How much coverage?

• Most insurance companies will insure only those with a minimum income, i.e., $15,000

• They also look for stable earnings power. • An insurance company will allow higher earners to

purchase larger amounts of coverage, on a percentage, the ratio of coverage provided to earned income tends to decrease as one’s income goes up.

• This is because higher earners have more ‘discretionary income’ and can afford a lower replacement ratio.

28

29

Guide to Disability Income Insurance

• http://www.ahip.org/Issues/Documents/2009/Guide-to-Disability-Income-Insurance.aspx