Embed Size (px)

Citation preview

directors' report

directors' report

Bismillahir Rahmanir Rahim

Dear Fellow Shareholders

The Board of Directors is pleased to welcome the honorable shareholders in the 14th Annual General Meeting of the Bank. The Directors' Report along with audited financial statements and auditors' report thereon for the year ended December 31, 2009 are presented before your kind self.

In the report, DBBL's operational performance of 2009 as compared to 2008 has been evaluated and analyzed within the prevailing business environment. The information and analysis may be read in conjunction with the DBBL's audited financial statements which have been prepared in accordance with Bangladesh Accounting Standards, Bangladesh Financial Reporting Standards and applicable legal and regulatory requirements.

REVIEW OF BUSINESS OPERATIONS AND STRATEGY

Principal activities

The principal activities of DBBL are to provide all kinds of commercial banking products and services to the customers including project finance, working capital finance and trade finance for corporate customers, SME loans to small traders & businesses; and house building loan, car loan and wide range of life style and need based loans for retail customers. There are various deposit products particularly suitable for retail and institutional customers. DBBL's state-of-the-art IT platform and online banking system provide the largest ATM network and POS services of the country through which customers are getting any-branch and anytime banking for 24 hours a day and 365 days a year. IT network also provides SMS banking, alert banking and internet banking services. Debit cards of MasterCard World wide debit and credit cards of VISA International and DBBL's proprietary cards are in operation. In addition, international cards (VISA & MasterCard) of different local & international banks are accepted at DBBL's ATMs for withdrawal of money and at POS terminals for payments of shopping, hotel and dining bills etc. DBBL introduced EMV based computer Chip Cards for the first time in Bangladesh in 2009. The EMV feature shields DBBL customers from any kind of frauds as per the guidelines provided by MasterCard & VISA.

Strategic plan for positioning the company for future growth through capacity building

As part of its strategic plan, DBBL continued to invest heavily to improve and expand IT network, ATM services and card services along with branch network, business promotion and CSR activities. Though expenses on such investments in 2009 apparently reduced expected profit growth, however, these will substantially improve our capacity to deliver customer services with a wide range of products and services that can be matched with the best in the industry by strengthening IT platform, expanding distribution channels and communication networks and improving productivity. DBBL's strategic objective is to have a clear competitive advantage over its competitors to provide the full range of banking services via multiple delivery channels through state-of-the-art-technology at the lowest cost.

Brand positioning

Throughout its operation for last 14 years, DBBL has established itself as a different bank from others. It has differentiated itself as a leader in technology by reaching the latest banking services to its customers through largest ATM network in the country at free or affordable cost. DBBL has created an unprecedented example by providing this unique service at subsidized cost not only to its own customers but also to customers of many other banks. It has also established itself as a bank that cares for the society. All the business activities of DBBL are done in full conformity with social, ethical and environmental standards. DBBL is the pioneer in CSR programs in the country. It has been intensifying its resources and efforts on a continuous basis to reach the distressed & needy people of the society to bring smile on their face and to improve their quality of life.

Customer focus and customers' right

DBBL's performance can not be judged by just looking at profit figures. DBBL considers that it is the customers' right to get modern, online and full ranges of banking services at an affordable price at anytime and anywhere. DBBL's service cost is the lowest in the industry and in many cases services provided through ATM are free. DBBL is committed to put the customers’ interest first. In line with its central vision, DBBL is promise-bound to extend personalized services to the full satisfaction of the customers that

should be the best in the industry.

Capital management plan and capital adequacy ratio

During 2009, Shareholders' equity (Tier-1 capital) increased to Taka 4,048.9 million being 7.95% of risk weighted assets (RWA) and supplementary capital (Tier 2 capital) increased to Taka 1,850.9 million being 3.64% of RWA. Tier-2 capital was also strengthened by revaluation of held to maturity securities and held for trading securities as of December 31, 2009. It will strengthen the capital base of the company and provide long-term growth and stability to the Bank. It may be noted that as per Bangladesh Bank regulation, subordinated loan is

eligible as Tier-2 capital up to 30% of Tier-1 capital and 50% of assets revaluation reserve and 50% of revaluation reserve on held for trading and held to maturity securities are eligible as Tier-2 capital. In line with long-term capital management plan of the Bank and keeping in view the implementation of Basel II requirement, strong capital adequacy ratio was maintained in 2009 which reached 11.59% under Basel I at the end of the year that was well above statutory requirement of 10.00%.

Expansion of branches

The Bank opened 15 new branches in 2009 to reach 79 branches at the end of the year spreading the branch network throughout the country. Five new SME Service Centres were opened in 2009 to reach 10 SME Service Centres at the end of 2009. More branches will be opened in 2010 to expand the branch and distribution network. These will bring up-to-date banking services to our existing and potential customers. At the same time it will optimize utilization of our strong delivery channels, increase our resource position and business potentials that will maximize profitability and shareholders' value. DBBL's strategy is to reach the doorsteps of customers to provide full range of banking services based on state- of -the- art- technology and IT platform at free or affordable cost.

IT infrastructure Dutch-Bangla Bank is the first and only bank in Bangladesh which invested more than Taka 2.0 billion in developing the largest ICT infrastructure in the banking sector of the country. Since its inception, the Bank has been continuously striving towards bringing world-class technology driven banking services, conveniences and satisfaction to its customers setting a milestone in the banking sector of the country.

As a technology driven Bank, we have implemented world reputed online banking software-Flexcube at all its 79 branches and 10 SME service centers with following delivery channels:

● Any Branch Banking● Online ATM/POS service ● Internet Banking service● Mobile Banking service● SMS and Alert banking service

The Bank has also implemented Online Synchronous Disaster Recovery Site (DRS) to provide uninterrupted and reliable banking convenience to

the customers. DBBL’s Synchronous DRS is the first of its kind in Bangladesh.

Dutch-Bangla Bank’s ATM is the largest ATM network in the country comprising of 700 units of ATMs at the end of 2009. DBBL has 1100 units of POS terminals at various merchant outlets. All the ATMs and POS terminals are made EMV (Europay, MasterCard and VISA) compliant which is again the first time in Bangladesh to ensure the security of our valued customers. The ATM / POS network of the DBBL accepts the following cards:

● EMV compliant chip cards of all the banks in the world;

● Non-EMV Visa & MasterCard cards of all the banks in the world;

● Proprietary cards for all the partner Banks in

Bangladesh.

DBBL has opted other banks to joining and enjoying its ATM/POS network. Customers of 18 (eighteen) partner banks in Bangladesh are enjoying the DBBL ATM/POS network.

DBBL pioneered EMV supported Chip Visa credit cards in Bangladesh. This highly secured credit card protects the cardholder from any type of fraud at home and abroad. A card with magnetic strip can easily be skimmed by the fraudsters. But DBBL Chip cards feature built-in encryption algorithms mandated by Visa and MasterCard Int’l which are impossible to duplicate or modify.

At present, DBBL is issuing Classic and Gold Visa EMV credit cards for local and international usages. We have multicurrency card supporting both USD and BDT. Besides EMV, the main features of our credit cards are competitive Interest Rate, 100% Cash Withdrawal facility from ATM booths, nil Cash Advance Fee in case of withdrawing cash from DBBL ATMs, maximum 50 days’ interest free period in case of purchase, etc.

We have also achieved the milestone of issuing Debit Cards in Bangladesh. Up to December 2009, we issued over 755,000 DBBL debit cards to our customers.

To provide baking services to the remote customers of the country, DBBL has planned to use the country’s Mobile network. With the help of the mobile network, all unbanked customers having cell numbers will be able to get some basic banking services like cash withdrawal, cash deposit, bill payment, local remittance etc. from all over the counrty. The customers will also get foreign remittance from all over the world. Even all Government payments, corporate salary payment can be disbursed through this service. DBBL is in the process of obtaining necessary permissions from regulatory bodies.

The Bank has undertaken a massive plan to relocate its present Data Center (occupying all kinds of IT infrastructure), from where all kinds of Bank’s IT related services , facilities are being controlled and monitored, to a new destination of the Bank’s own premises from the present rented building. This initiative will help the Bank to provide the customer services in a better and effective way as well as to enhance the safety & security of the Bank’s ever-increasing IT infrastructure.

Retail Banking and lending under SME Scheme

In order to achieve further growth and to serve the clients better, DBBL is emphasizing on the importance of identifying clients’ needs, better & smooth service delivery process, customized banking services and operation in accordance to the clients’ need.

In view of the potentials, DBBL launched Retail Loan/Consumer Loan in 2007. DBBL is now trying to focus on expansion of Retail Loans/Consumer Credit besides Corporate Credit. The management of the Bank is giving utmost emphasis to expand Retail Banking portfolio.

DBBL Life line loans under retail scheme covers the following:

● lHealth Line ● Education Line ● Professionals Line● lMarriage Line● Travel Line● Festival Line● Dreams Come True Line● Care Line● General Line● Auto Line● Home Line● Fully Secured Lines

As of 31 December, 2009 DBBL’s number of Retail Loan customers stood at 5,032 and aggregate disbursement stood at Taka 1,618.2 million against which outstanding balance stood at Taka 1,402.2 million with a growth of 125.2% over 2008.

To achieve long-term sustainable growth following are the strategies of DBBL in Retail Banking arena:

● Providing better service through expansionary distribution channels

● Meticulous customer segmentation

● Customer-centric product and service innovation

● High impact staff-customer engagement and total customer relationship management

● Proactive risk management

● Competitive pricing

● To focus on salaried person to minimize therisk

SME lending scheme was launched in 2008 as a priority sector with a separate division. It was further strengthened in 2009.Expansion of retail banking operation and SME lending will be strongly supported by adequate manpower, robust IT and ATM network, various promotional activities as well as faster and better customer services.

Human resources development

A competent, committed and fully motivated team of human resources is the main driving force for performing at the highest level in a fiercely competitive financial market like Bangladesh. Accordingly, the Bank's strategy is to attract, retain and motivate the most talented people. The Bank's HR policies are based on trust and relationship. The Bank's policy is to look after people who want to make a long-term career with the Bank because trust and relationship are built over time. Remuneration package may be an important factor to motivate for joining a company, but it is not the only one. In case of DBBL, it is excellence of DBBL with good values, fairness, potential for success, scope to develop a broad interesting career etc. which attract people to join and work with DBBL.

DBBL always encourages excellence in performance by rewards and recognition. In addition, a number of well thought out policies are in place for welfare of employees in the form of DBBL Superannuation Fund, DBBL Gratuity Fund, House Building Loan Scheme and Car Loan Scheme etc. In order to ensure better healthcare of employees there is a medical consultant at Head Office. In addition, a thorough medical check up facility is provided to each employee on a yearly basis. On the other hand, DBBL attaches utmost importance to the development of its employees through continuous training. We imparted training to 528 officers in 68 different courses during 2009. The training programs were organized by our own training institute. We also nominated 71 officers to undergo different training programs/courses organized by different organizations like Bangladesh Institute of Bank Management BIBM), Bangladesh Bank Training Academy (BBTA) and other similar organizations. In addition, eight executives were sent abroad for attending overseas training and workshop.

The number of DBBL staff increased by 556 in 2009. At the end of 2009, number of staff stood at 1,785 compared to 1,229 at the end of 2008. The corporate culture at DBBL as grew over last 14 years is such that the members of the staff have ample opportunities to take initiative and responsibilities. The challenge is to maintain a business like, committed corporate culture that matches DBBL's mission. Achieving results and taking responsibility are important components of the culture we pursue, one in which management and staff work together and are mutually accountable.

In addition, to strive hard for winning the challenges in a fiercely competitive market, the management has been constantly pursuing the following areas:

● To attract and retain best professionals in the industry.

● Job evaluation, job enrichment, performance target, performance evaluation, and performance based compensation and incentives.

● Evaluating the training need of individual employees including training need for introducing new products, services and technology.

● Arranging high quality training at home and abroad so that DBBL executives can have competitive advantage in the market.

● Encouraging its employees to develop and broaden existing knowledge and skills and to acquire new skills and expertise.

● Reviewing and updating organizational structure on a regular basis to have a structure which can give strong support to the strategic objectives of the Bank.

Correspondent banking relationship

At present, DBBL has 442 correspondent banking relationships covering 92 countries. As a result, we can route Letters of Credit (L/C) to all important business centers of the world. We are maintaining adequate number of nostro accounts in major currencies with the key players in the world market to facilitate export and import transaction needs of our valued clients. DBBL's excellent service with competitive charges provides a good correspondent banking solution for the valued clients of DBBL.

DBBL has established Taka Drawing Arrangements with various exchange houses located in USA, UAE, Kuwait, Canada etc. Moreover, arrangements of DBBL with Western Union, USA and Xpress Money of UAE Exchange Center, UAE enable people to get direct inward remittances from every corners of the globe. Remittance inflow of DBBL rose significantly by 29.3 per cent from US $ 75.7 million in 2008 to US $ 97.9 million in 2009.

REVIEW OF FINANCIAL POSITION AND RESULTS

Summary

Healthy Business and profit growth despite global financial crises and slower business activities

Despite global economic crises and slower business activities in the country, DBBL registered healthy business and profit growth in 2009 while being cautious to protect against any risk that may be arising from the economic crises. The deposit of the Bank increased by 31.4% from Taka 51,575.7 million in 2008 to Taka 67,788.5 million in 2009, loans & advances increased by 16.1% from Taka 41,698.3 million in 2008 to Taka 48,410.9 million in 2009,

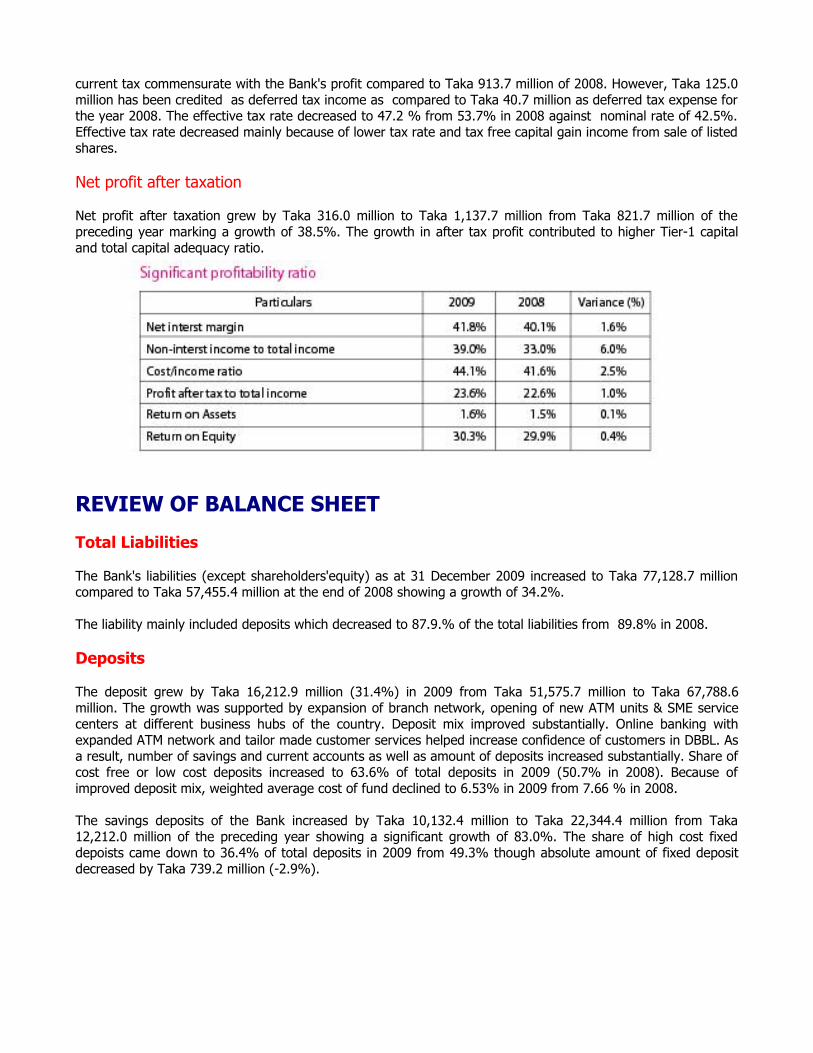

while import business increased by 20.7% and export business increased by 2.7%. Operating profit grew by 39.3% from Taka 1,935.9 million to Taka 2,695.7 million and net profit after tax increased from Taka 821.7 million to Taka 1,137.7 million showing a growth of 38.5%. Lower cost of fund resulting from improved deposit mix, higher net interest income, higher non-interest income mainly from gain on sale of HFT securities, capital gain from listed shares and service charges on deposits accounts contributed to notable growth in operating profit.Net profit after tax grew at a faster rate than operating profit for lower effective tax rate in 2009. Return on equity was 30.3% in 2009 compared to 29.9% in 2008.

Higher investments in branch expansion, IT platform, ATM network, card services and human resources though contained profit growth in 2009, however, these will increase resource capacity, increase distribution network, improve efficiency in operations, augment resource flow to expand customer base and to provide much better and faster customer services. As a result, in the long term it will bring substantial and sustainable benefits for the Bank.

Net interest income

During the year 2009, the net interest income of the Bank rose by Taka 249.2 million or 13.7% to Taka 2,066.8 million from Taka 1,817.7 million of the previous year. Net interest income increased mainly due to higher average loan portfolio and lower cost of fund resulting from improved depoist mix. Cost of fund declined from 7.66% of 2008 to 6.53% in 009 while yield on loans and advances declined from 13.62% in 2008 to 12.96% in 2009 mainly due to reduction in interst rate for regulatory compliance. However, the share of net interest income to the total income of the Bank decreased to 42.9% in 2009 compared to 49.9% of the previous year.

Investment Income

During the year 2009 the investment income of the Bank rose by Taka 712.4 million or 114.6% to Taka 1,334.2 million from Taka 621.7 million of the previous year. Investment income increased mainly due to Taka 347.5 million earned from gain on sale of HFT securities and Taka 112.6 million earned from capital gain on sale of listed shares.

Non- interest income

The non-interest income consists of the commission,

exchange and other operating income of the Bank. Total non- interest income of DBBL increased by Taka 217.4 million or 18.1% in 2009 over the previous year. Commission and exchange income increased by Taka 8.4 million or 1.0% during the year 2009. Notable growth was achieved in other operating income which grew by Taka 209.1 million to Taka 557.1 million in 2009 from Taka 348.0 million in 2008 marking a rise by 60.1%. Other operating income increased due to growing services provided by online banking network of the Bank.

Total operating expenses

Total operating expenses of the Bank during the year grew by Taka 610.5 million or 40.4%. Higher operating espenses were necesary to support the overall business and profit growth of the Bank during the year 2009. Higher expenses were required to support capacity building and expansion of

distribituion network and delevery channels. 15 new branches and 5 SME service centers were opened in 2009. 350 ATM units were installed in 2009. Recruitment of new personnel, maintenance and upgradation of IT network, Introduction of new retail products, increasing CSR activities are attributable to higher opearting expenses.

The Bank's cost (excluding the charges for loan losses) to income ratio increased to 44.1% in 2009 from 41.6% of the previous year.

Provision for loans and off-balance sheet exposures

Total provision for loans and off-balance sheet exposures increased by Taka 362.0 million or 557.7% during the year 2009. The specific provisions against loans substantailly increased by Taka 327.9 million during the year. However, close monitoring and supervision of the good and particularly non-performing loans continued to maintain overall quality of loan portfolio. The general provisions for unclassified loans and off-balance sheet exposures increased by Taka 34.2 million to Taka 150.2 million from Taka 116.1 million of the preceding year due to higher out standing balance of loans and off-balance sheet exposures.

Contribution to Dutch-Bangla Bank Foundation

DBBL established the Dutch-Bangla Bank Foundation in 2001 for carrying out CSR programs aimed at social causes and distressed people in the society.It is the Bank's policy to contributre 5% of its pre-tax profit to Dutch-Bangla Bank Foundation which increased to Taka 113.4 million in 2009 compared to Taka 93.5 million in the previous year.

Profit before taxes

During the year 2009, profit before taxes of the Bank increased by Taka 378.3 million or 21.3% to Taka 2,154.4 million from the previous year's amount of Taka 1,776.1 million. This increase was mainly attributed to higher opearting profit comprising both net-interest income and non-interest income.

Provision for taxation

As per Income Tax Ordinance, 1984, an amount of Taka 1,141.7 million has been charged as provision for

current tax commensurate with the Bank's profit compared to Taka 913.7 million of 2008. However, Taka 125.0 million has been credited as deferred tax income as compared to Taka 40.7 million as deferred tax expense for the year 2008. The effective tax rate decreased to 47.2 % from 53.7% in 2008 against nominal rate of 42.5%. Effective tax rate decreased mainly because of lower tax rate and tax free capital gain income from sale of listed shares.

Net profit after taxation

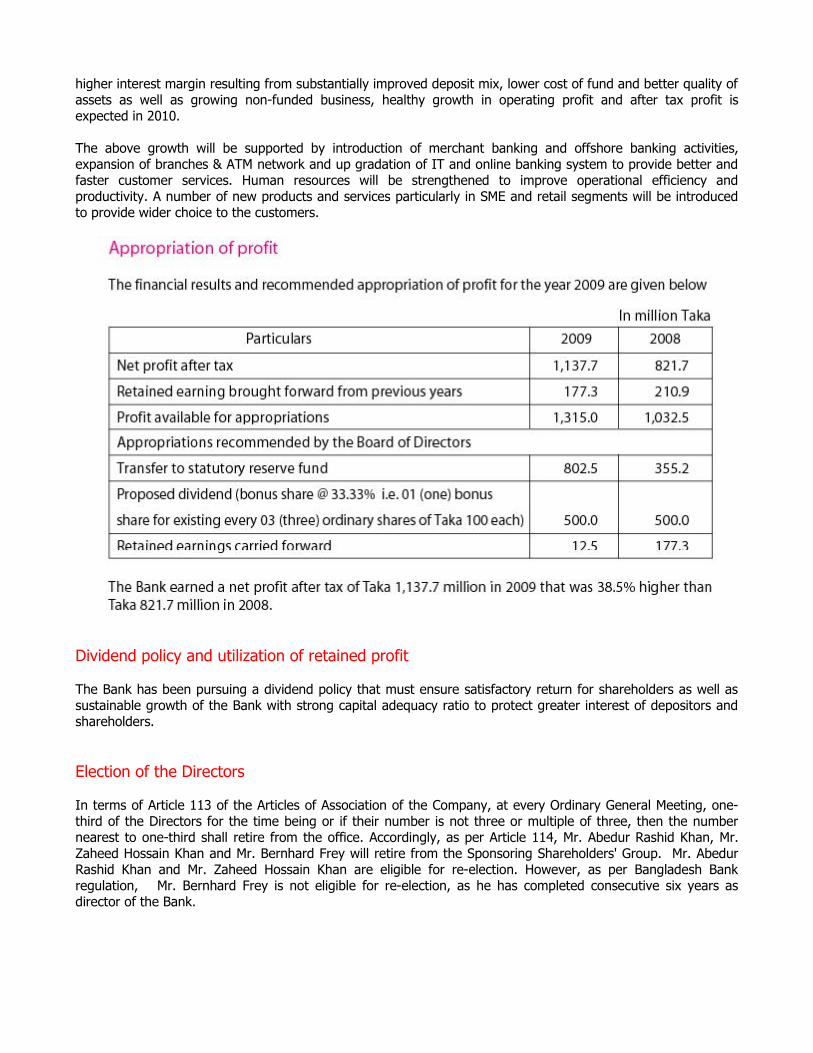

Net profit after taxation grew by Taka 316.0 million to Taka 1,137.7 million from Taka 821.7 million of the preceding year marking a growth of 38.5%. The growth in after tax profit contributed to higher Tier-1 capital and total capital adequacy ratio.

REVIEW OF BALANCE SHEET

Total Liabilities

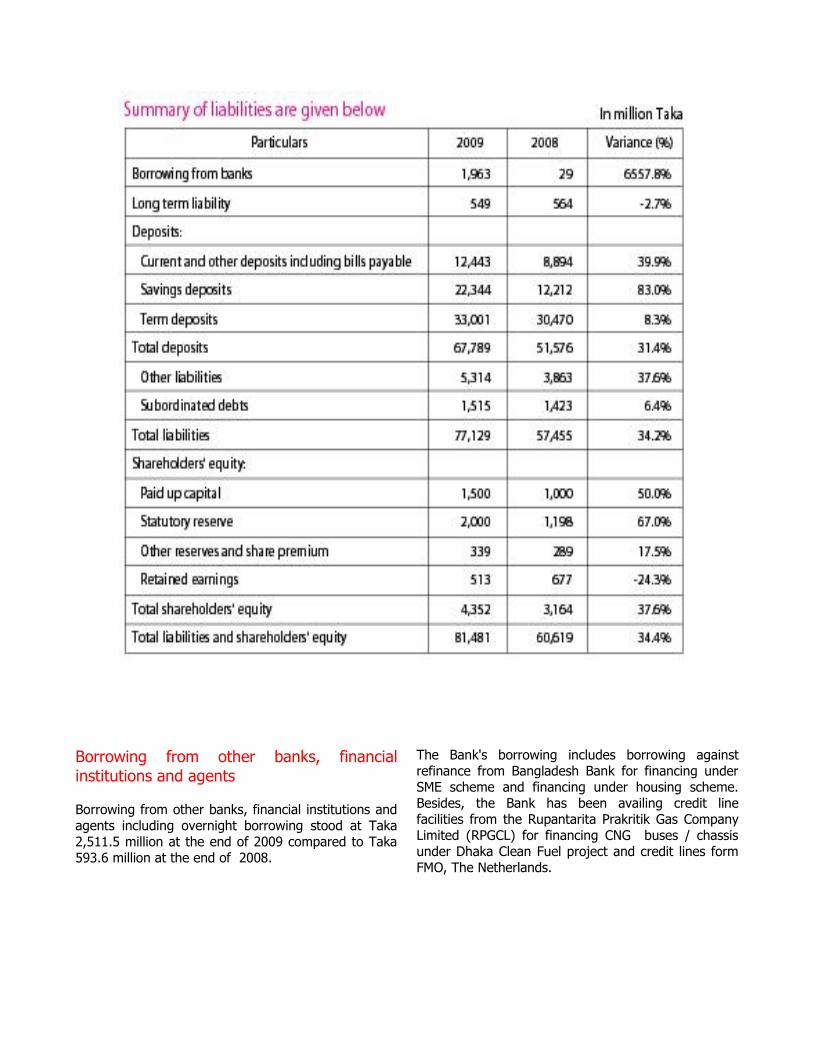

The Bank's liabilities (except shareholders'equity) as at 31 December 2009 increased to Taka 77,128.7 million compared to Taka 57,455.4 million at the end of 2008 showing a growth of 34.2%.

The liability mainly included deposits which decreased to 87.9.% of the total liabilities from 89.8% in 2008.

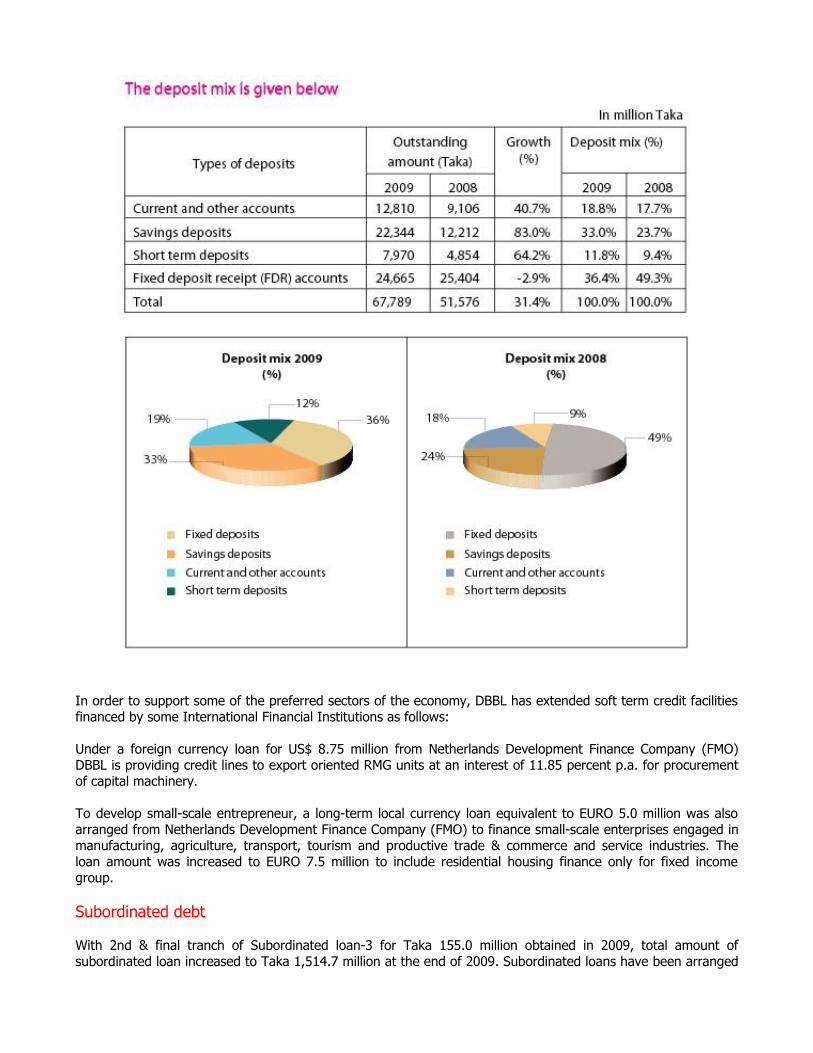

Deposits

The deposit grew by Taka 16,212.9 million (31.4%) in 2009 from Taka 51,575.7 million to Taka 67,788.6 million. The growth was supported by expansion of branch network, opening of new ATM units & SME service centers at different business hubs of the country. Deposit mix improved substantially. Online banking with expanded ATM network and tailor made customer services helped increase confidence of customers in DBBL. As a result, number of savings and current accounts as well as amount of deposits increased substantially. Share of cost free or low cost deposits increased to 63.6% of total deposits in 2009 (50.7% in 2008). Because of improved deposit mix, weighted average cost of fund declined to 6.53% in 2009 from 7.66 % in 2008.

The savings deposits of the Bank increased by Taka 10,132.4 million to Taka 22,344.4 million from Taka 12,212.0 million of the preceding year showing a significant growth of 83.0%. The share of high cost fixed depoists came down to 36.4% of total deposits in 2009 from 49.3% though absolute amount of fixed deposit decreased by Taka 739.2 million (-2.9%).

Borrowing from other banks, financial institutions and agents

Borrowing from other banks, financial institutions and agents including overnight borrowing stood at Taka 2,511.5 million at the end of 2009 compared to Taka 593.6 million at the end of 2008.

The Bank's borrowing includes borrowing against refinance from Bangladesh Bank for financing under SME scheme and financing under housing scheme. Besides, the Bank has been availing credit line facilities from the Rupantarita Prakritik Gas Company Limited (RPGCL) for financing CNG buses / chassis under Dhaka Clean Fuel project and credit lines form FMO, The Netherlands.

In order to support some of the preferred sectors of the economy, DBBL has extended soft term credit facilities financed by some International Financial Institutions as follows: Under a foreign currency loan for US$ 8.75 million from Netherlands Development Finance Company (FMO) DBBL is providing credit lines to export oriented RMG units at an interest of 11.85 percent p.a. for procurement of capital machinery.

To develop small-scale entrepreneur, a long-term local currency loan equivalent to EURO 5.0 million was also arranged from Netherlands Development Finance Company (FMO) to finance small-scale enterprises engaged in manufacturing, agriculture, transport, tourism and productive trade & commerce and service industries. The loan amount was increased to EURO 7.5 million to include residential housing finance only for fixed income group.

Subordinated debt

With 2nd & final tranch of Subordinated loan-3 for Taka 155.0 million obtained in 2009, total amount of subordinated loan increased to Taka 1,514.7 million at the end of 2009. Subordinated loans have been arranged

from FMO for financing housing sector of the country and to strengthen Tier-2 capital of the Bank. Subordinated loan is eligible as Tier -2 capital of the Bank subject to regulatory limit.

Shareholders' equity

As at 31 December 2009, DBBL's shareholders' equity increased to Taka 4,351.8 million from Taka 3,163.5 million of 2008 registering an increase by Taka 1,188.2 million (37.6%). The increase resulted from Taka 1,137.7 million after tax profit and Taka 50.6 million reserve against HTM securities. After issuing bonus shares @ 1:0.5, Paid up share capital of the Bank increased by Taka 500.0 million and stood at Taka 1,500.0 million at the end of 2009. The statutory reserve increased to Taka 2,000.0 million at the end of 2009 from Taka 1,197.5 million of 2008. The paid-up share capital and statutory reserve together stood at Taka 3,500.0 million as at December 31, 2009. As per Bangladesh Bank regulation, Paid up share capital and statutory reserve should be increased to at least Taka 4,000.0 million latest by August 11, 2011 of which paid up share capital should be minimum Taka 2,000.0 million. DBBL is well positioned to meet the requirment much earlier before the deadline.

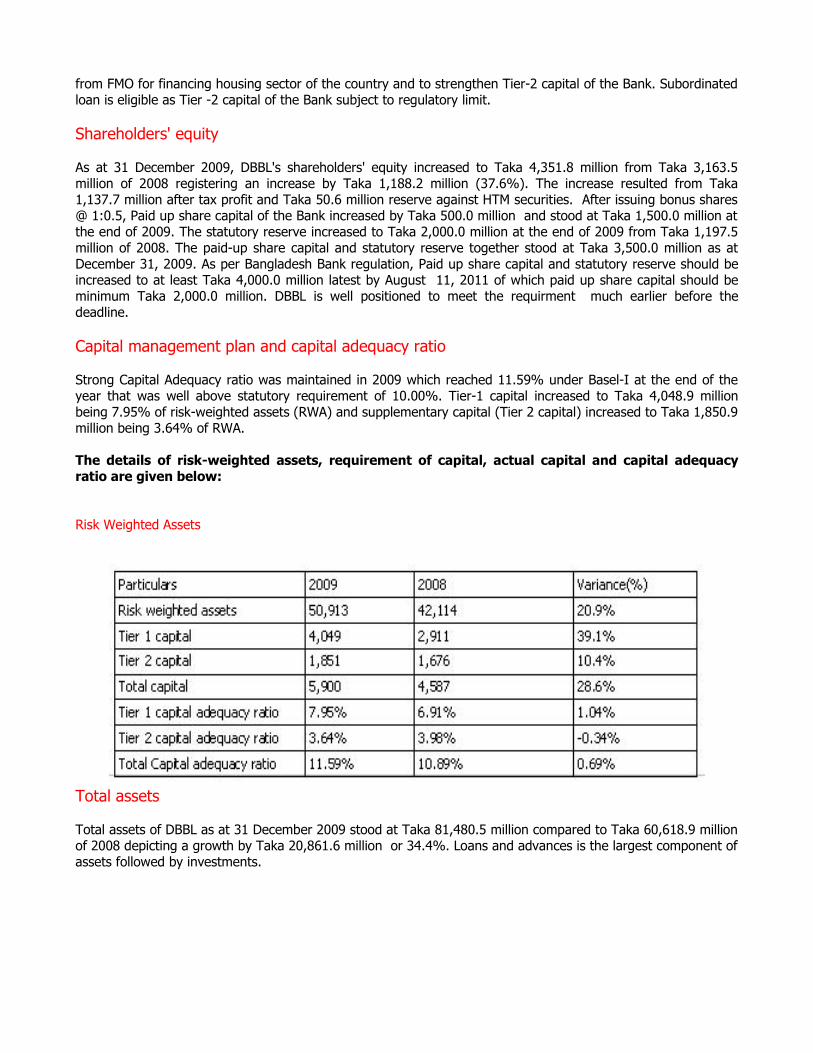

Capital management plan and capital adequacy ratio

Strong Capital Adequacy ratio was maintained in 2009 which reached 11.59% under Basel-I at the end of the year that was well above statutory requirement of 10.00%. Tier-1 capital increased to Taka 4,048.9 million being 7.95% of risk-weighted assets (RWA) and supplementary capital (Tier 2 capital) increased to Taka 1,850.9 million being 3.64% of RWA.

The details of risk-weighted assets, requirement of capital, actual capital and capital adequacy ratio are given below:

Risk Weighted Assets

Total assets

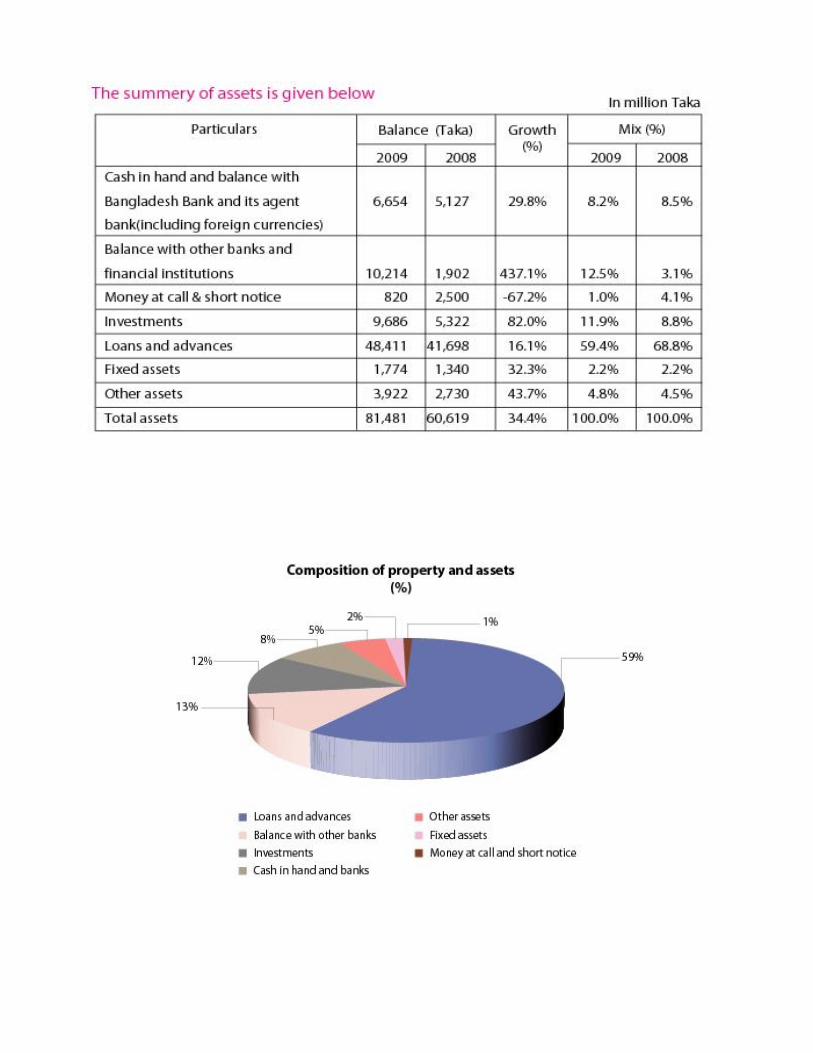

Total assets of DBBL as at 31 December 2009 stood at Taka 81,480.5 million compared to Taka 60,618.9 million of 2008 depicting a growth by Taka 20,861.6 million or 34.4%. Loans and advances is the largest component of assets followed by investments.

Cash in hand and balances with Bangladesh Bank and its agent bank (s) (including foreign currencies)

As at 31 December 2009, cash in hand and balances with Bangladesh Bank and its agent banks (including foreign currencies) stood at Taka 6,653.9 million as against Taka 5,126.7 million of 2008 registering a growth by Taka 1,527.2 million or 29.8%. The increased cash was required to provide uninterrupted cash services to our growing customers. Online transaction facilities with 79 branches, 600 units of ATM and growing number of accounts substantially increased cash requirement in branches and ATMs. Growth in deposits, increased balance with Bangladesh Bank to maintain CRR Ratio.

Balance with other banks and financial institutions

The Treasury Division of the Bank has to maintain some short term deposit (STD) accounts and current deposit (CD) accounts with other banks in and outside the country for the smooth functioning of treasury operations and trade finance. A portion of the excess fund, if any, after meeting the requirement to finance loan portfolio and investments including SLR, is placed with other banks and financial institutions as term deposits for optimizing the profit of the Bank. As at 31 December 2009, balance outstanding with other banks and financial institutions substantially increased to Taka 10,213.8 million from Taka 1,901.5 million at the end of 2008 for lower utilisation of funds in loan portfolio.

Money at call & short notice

Money at call and short notice stood at Taka 820.0 million at the end of 2009 compared to Taka 2,500.0 million at the end of 2008. The average yield on fund placement at call & short notice of the Bank was 8.06% for 2009 as aganist 8.45% of 2008. Short term excess fund is placed in money market to augment return on fund.

Investments

The Bank's investment stood at Taka 9,685.9 million at the end of 2009 that was higher by 82.0% from Taka 5,322.3 million in 2008. The investments mainly included Government securities for Taka 9,669.9 million (99.8% of total investment) maintained mainly to cover SLR requirement. In addition, investments were planned in a way to provide sufficient iquidity and flexibility in treasury operations and to boost aggregate yield which increased from 9.7% in 2008 to 14.6% in 2009.

Treasury team of the Bank was very much watchful to manage market risk & uncertainty and ensure maximum return from investments in security, term deposits and call money market though there was higher level slower business activities. During the year under review, the Bank was able to maintain cash reserve requirements (CRR) and statutory liquidity requirements (SLR) successfully. Loans and Advances

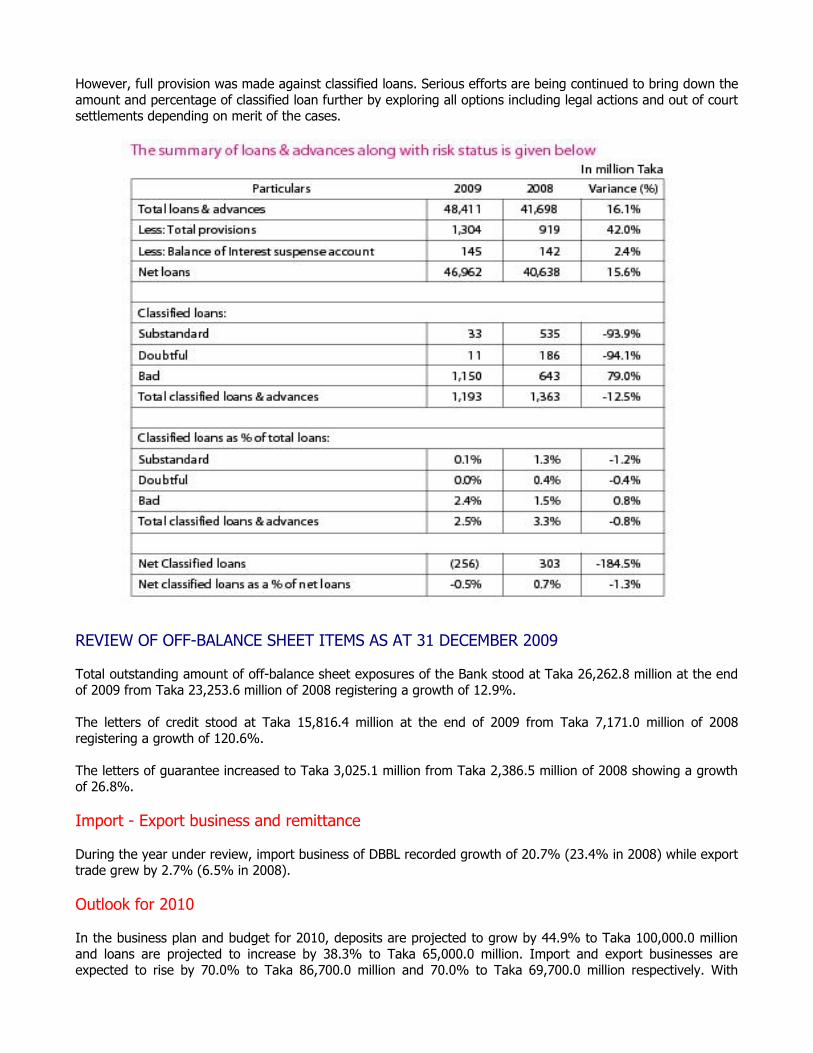

Loans and advances stood at Taka 48,410.9 million at the end of 2009, a growth of 16.1% over Taka 41,698.3 million in 2008. The Bank continued to consolidate and diversify its portfolio in 2009 to have a diversified client base and portfolio distributed across the sectors to reduce client specific and industry specific concentration and to reduce overall portfolio risk. Considering future market direction and to capitalize on our robust IT platform and the strongest ATM network, a number of retail and SME loan products aimed at specific target group were launched in 2009 to augment fee income and improve yield and spread on total loan portfolio. At the end of 2009, DBBL's total outstanding retail portfolio stood at Taka 1,402.2 million compared to Taka 622.5 million of 2008.

Weighted average rate of return on total loans & advances decreased to 12.96% in 2009 from 13.62% in 2008.

Classified loan as a percentage of portfolio significantly decreased to 2.46% in 2009 from 3.27 % in 2008.

However, full provision was made against classified loans. Serious efforts are being continued to bring down the amount and percentage of classified loan further by exploring all options including legal actions and out of court settlements depending on merit of the cases.

REVIEW OF OFF-BALANCE SHEET ITEMS AS AT 31 DECEMBER 2009

Total outstanding amount of off-balance sheet exposures of the Bank stood at Taka 26,262.8 million at the end of 2009 from Taka 23,253.6 million of 2008 registering a growth of 12.9%.

The letters of credit stood at Taka 15,816.4 million at the end of 2009 from Taka 7,171.0 million of 2008 registering a growth of 120.6%.

The letters of guarantee increased to Taka 3,025.1 million from Taka 2,386.5 million of 2008 showing a growth of 26.8%.

Import - Export business and remittance

During the year under review, import business of DBBL recorded growth of 20.7% (23.4% in 2008) while export trade grew by 2.7% (6.5% in 2008).

Outlook for 2010

In the business plan and budget for 2010, deposits are projected to grow by 44.9% to Taka 100,000.0 million and loans are projected to increase by 38.3% to Taka 65,000.0 million. Import and export businesses are expected to rise by 70.0% to Taka 86,700.0 million and 70.0% to Taka 69,700.0 million respectively. With

higher interest margin resulting from substantially improved deposit mix, lower cost of fund and better quality of assets as well as growing non-funded business, healthy growth in operating profit and after tax profit is expected in 2010.

The above growth will be supported by introduction of merchant banking and offshore banking activities, expansion of branches & ATM network and up gradation of IT and online banking system to provide better and faster customer services. Human resources will be strengthened to improve operational efficiency and productivity. A number of new products and services particularly in SME and retail segments will be introduced to provide wider choice to the customers.

Dividend policy and utilization of retained profit

The Bank has been pursuing a dividend policy that must ensure satisfactory return for shareholders as well as sustainable growth of the Bank with strong capital adequacy ratio to protect greater interest of depositors and shareholders.

Election of the Directors

In terms of Article 113 of the Articles of Association of the Company, at every Ordinary General Meeting, one-third of the Directors for the time being or if their number is not three or multiple of three, then the number nearest to one-third shall retire from the office. Accordingly, as per Article 114, Mr. Abedur Rashid Khan, Mr. Zaheed Hossain Khan and Mr. Bernhard Frey will retire from the Sponsoring Shareholders' Group. Mr. Abedur Rashid Khan and Mr. Zaheed Hossain Khan are eligible for re-election. However, as per Bangladesh Bank regulation, Mr. Bernhard Frey is not eligible for re-election, as he has completed consecutive six years as director of the Bank.

Meetings of the Directors

Eleven (11) meetings of the Board of Directors and fifty one (51) meetings of the Executive Committee of the Board were held during the year under review.

The Audit Committee of the Board also held seven (07) meetings during the year under review.

Appointment of Auditors

Our existing Auditors, M/s. Hoda Vasi Chowdhury & Co., Chartered Accountants (Independent Correspondent Firm to Deloitte Touche Tohmatsu) has completed audit of 2009 as third year of their audit and as per Bangladesh Bank's BRPD Circular Letter No.12 dated July 11, 2001, they are not eligible for re- appointment. Therefore, another auditor will be appointed and their remuneration will be fixed for the year 2010 by the honorable shareholders in the 14th annual general meeting.

Gratitude

The members of the Board of Directors of DBBL would like to express their gratitude to all shareholders, valued clients, patrons, all employees and well-wishers for their continued support and cooperation, without which the Bank would not be able to achieve its present amazing position. We are also indebted to the Government of Bangladesh, Bangladesh Bank, Securities and Exchange Commission, Office of the Registrar of Joint Stock Companies and Firms, the Stock Exchanges for their continued support and co-operation.

We look forward for your continuous support and best wishes for meeting the challenges that await us in days to come.

With best regardsOn behalf of the Board of the Directors

Abedur rashid KhanChairman