Embed Size (px)

Citation preview

2

EXECUTIVE SUMMARY

1. The consultation on future priorities for the Action Plan on Company Law and Corporate Governance has been successful. 266 responses were received from a wide variety of stakeholders from all around the EU and from Third Countries.

Strong support for application of better regulation principles

2. The consultation exercise in itself was praised. Respondents called for systematic consultations, with a minimum 12 week deadline. The application of the better regulation principles, as proposed in the consultation document, received overwhelming support (i.e. systematic regulatory impact assessments, legislation only when needed, light touch regulation, etc).

Views shared on continued relevance of the Action Plan

3. As regards the continued relevance of the Action Plan and, in particular, the measures proposed, respondents generally supported the work done since 2003. However, opinions were split on the detail of the measures proposed for the medium and long term. A number of respondents stated their "regulatory fatigue" and called for a stabilisation period. –But they also stated that such a moratorium should not cover "enabling legislation", such as the directive on the transfer of registered office or the Statute for a European Private Company.

Split views on Corporate Governance issues

4. There was clear support for addressing the "one share, one vote" issue at EU-level, at least for a fact-finding study. As to the form of a potential EU intervention, a small majority of respondents preferred a Recommendation to a Directive.

5. Regarding the rights of shareholders, a slight majority of respondents saw some added value in EU initiatives, in particular on the establishment of a mandatory special investigation right, on the issue of nomination and dismissal of directors and on shareholder communication rules. Those who opposed such initiatives considered that there was already sufficient protection of shareholders' interest in EU and national legislation.

6. Half of the respondents took a position on the disclosure of institutional investors' voting policies. Opinions on the need for action at EU level were split and many respondents did not actually clearly reply to the question as to whether action should be launched at EU level. Some considered that the matter should be left to contractual arrangements. Some considered that an EU rule would create excessive burdens for investors. Others considered that an EU intervention was needed to create a level playing field. A significant number of respondents insisted on the need to impose transparency and disclosure obligations on institutional investors. Among the supporters of an EU action, opinions were split on the appropriate instrument.

7. Respondents opposed the adoption of an EU wrongful trading rule, considering that such an issue does not raise substantial cross-border problems. Respondents also opposed the adoption of EU legislation on directors' disqualification, on the basis of the substantial differences existing between the national systems. However,

3

some voices considered such action necessary in order to avoid forum shopping. As regards transparency requirements for legal entities, a majority of private sector respondents was opposed to new EU intervention, while a majority of public sector respondents was in favour.

Company Law: EU intervention limited to "enabling legislation"

8. A very large majority of respondents called for the adoption of a 14th Company Law Directive. A minority, however, raised doubts about the practical value of the Directive since other obstacles, such as taxation and employee participation issues, would remain.

9. The issue of board structure did not raise strong enthusiasm. Respondents generally did not consider EU action as a high priority. Enthusiasm was also limited regarding groups and pyramids. The majority of respondents considered that no action was advisable or necessary.

10. As regards a squeeze out right, a slight majority of respondents considered that there was no need to introduce additional EU rules. As regards the sell out right, most respondents considered that any EU rule would put an undue burden on companies.

11. As regards the particular forms of companies, respondents considered it premature to launch an assessment of the European Company Statute. 40% of the respondents considered it partly or very useful. At the same time, almost half of the respondents called for the adoption of a European Private Company Statute. Finally, on the European Foundation Statute, a high number of foundations urged the Commission to carry out a feasibility study.

Shared views on modernisation and simplification of European Company Law

12. A majority of respondents supported the principle or the objective of simplification. However, most stakeholders considered a recasting exercise inappropriate. They proposed, instead, to launch a codification or consolidation of existing company law legislation. Few overlaps with existing initiatives or measures were reported and very few suggestions were made on the way to ensure coherence between various actions.

Views confirmed at the public hearing

13. The public hearing on future priorities for the Action Plan, organised in Brussels on 3 May, gathered about 300 participants. The views expressed in the replies to the consultation were confirmed. The speakers and participants agreed on the principles that should underpin any Commission action in the field of company law and corporate governance. They considered that EU initiatives should focus (a) on lifting obstacles to the free flow of capital between Member States and to right of establishment and (b) on granting additional flexibility to companies. Some considered regulatory competition in the field of company law as an effective tool to achieve efficiency. However, the 'regulatory fatigue' was mentioned as a factor to be taken into account. Nevertheless, a possible moratorium should not extend to the 'enabling legislation'.

4

INTRODUCTION

The present document provides a detailed report on the results of the written public consultation on future priorities for the Action Plan on Company Law and Corporate Governance (Section 1) as well as the minutes of the public hearing held on 3 May 2006 in Brussels (Section 2).

1. RESULTS OF THE PUBLIC CONSULTATION ON FUTURE PRIORITIES FOR THE ACTION PLAN ON COMPANY LAW AND CORPORATE GOVERNANCE

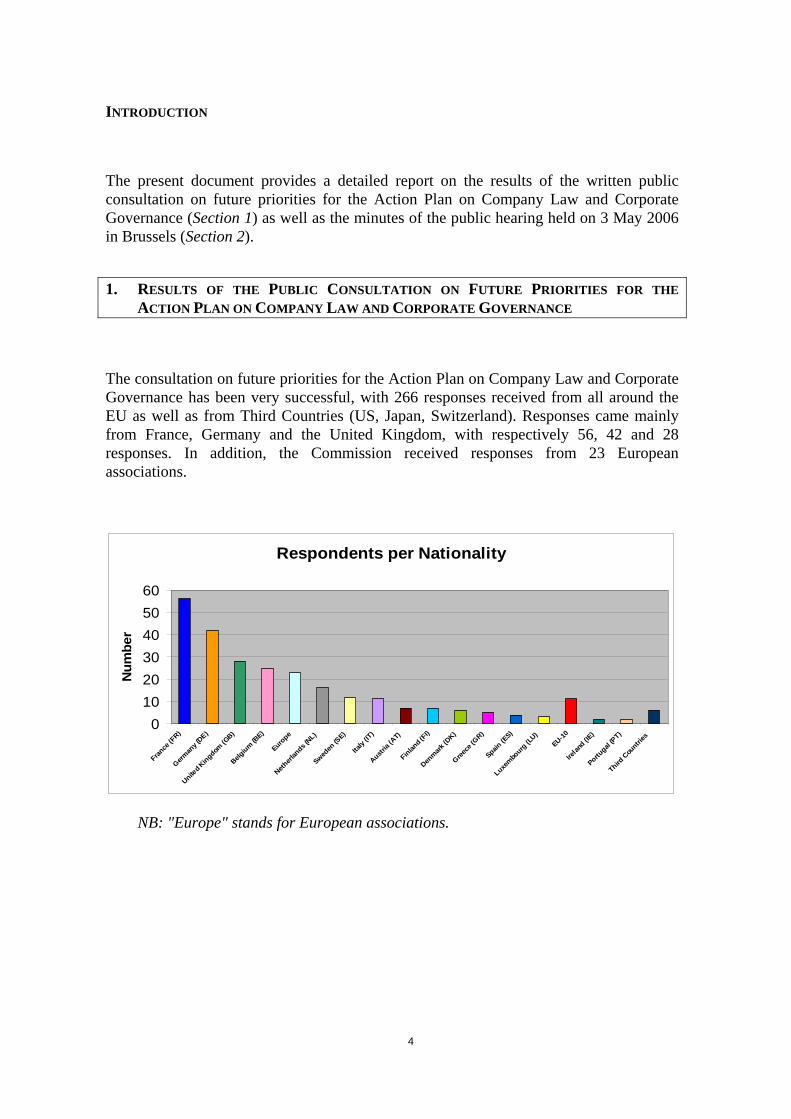

The consultation on future priorities for the Action Plan on Company Law and Corporate Governance has been very successful, with 266 responses received from all around the EU as well as from Third Countries (US, Japan, Switzerland). Responses came mainly from France, Germany and the United Kingdom, with respectively 56, 42 and 28 responses. In addition, the Commission received responses from 23 European associations.

Respondents per Nationality

0102030405060

France

(FR)

German

y (DE)

United K

ingdom (G

B)

Belgium (B

E)

Europe

Netherl

ands (

NL)

Sweden

(SE)

Italy

(IT)

Austria

(AT)

Finland (

FI)

Denmark

(DK)

Greece

(GR)

Spain (E

S)

Luxembo

urg (L

U)EU-10

Irelan

d (IE)

Portugal

(PT)

Third C

ountri

es

Num

ber

NB: "Europe" stands for European associations.

5

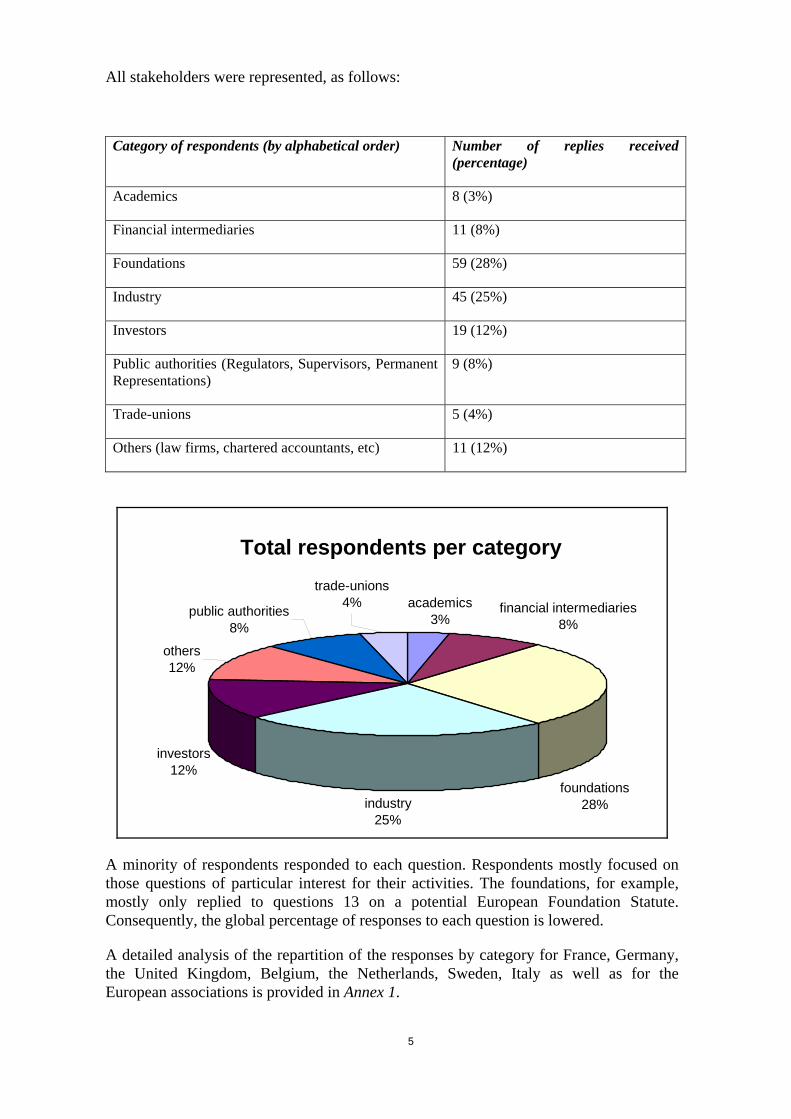

All stakeholders were represented, as follows:

Category of respondents (by alphabetical order) Number of replies received (percentage)

Academics 8 (3%)

Financial intermediaries 11 (8%)

Foundations 59 (28%)

Industry 45 (25%)

Investors 19 (12%)

Public authorities (Regulators, Supervisors, Permanent Representations)

9 (8%)

Trade-unions 5 (4%)

Others (law firms, chartered accountants, etc) 11 (12%)

Total respondents per category

academics3%

financial intermediaries8%

industry25%

investors12%

others12%

public authorities8%

foundations28%

trade-unions4%

A minority of respondents responded to each question. Respondents mostly focused on those questions of particular interest for their activities. The foundations, for example, mostly only replied to questions 13 on a potential European Foundation Statute. Consequently, the global percentage of responses to each question is lowered.

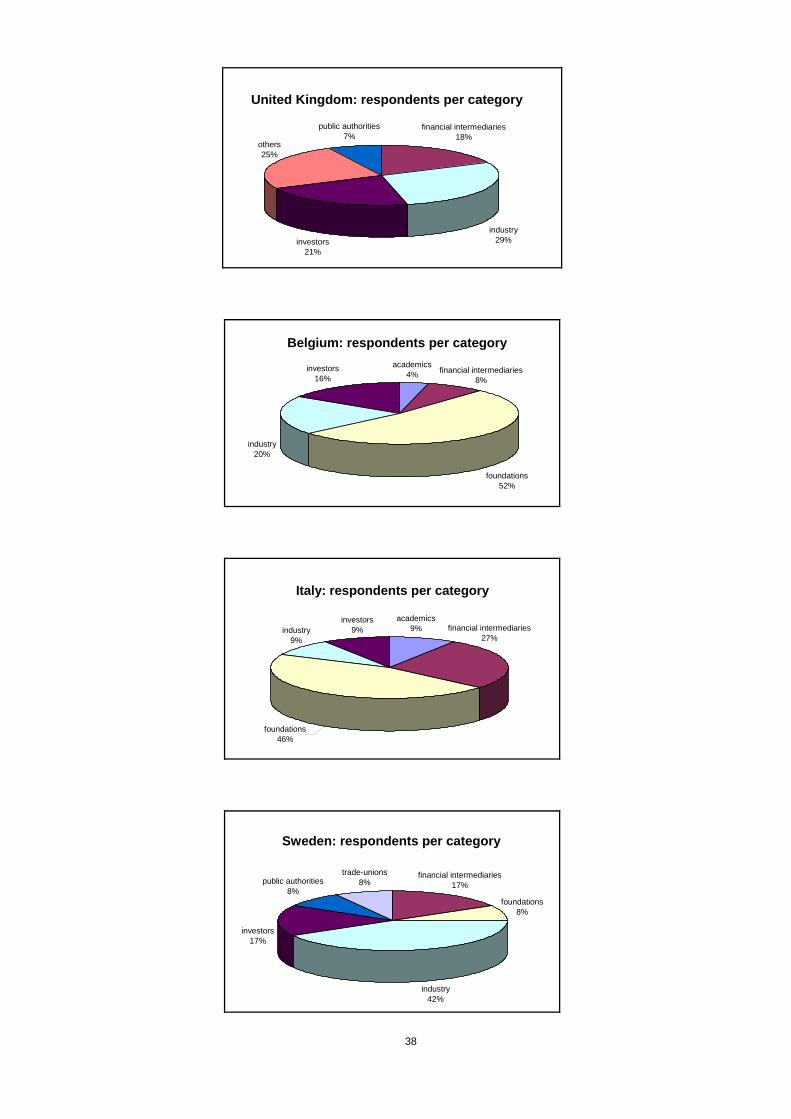

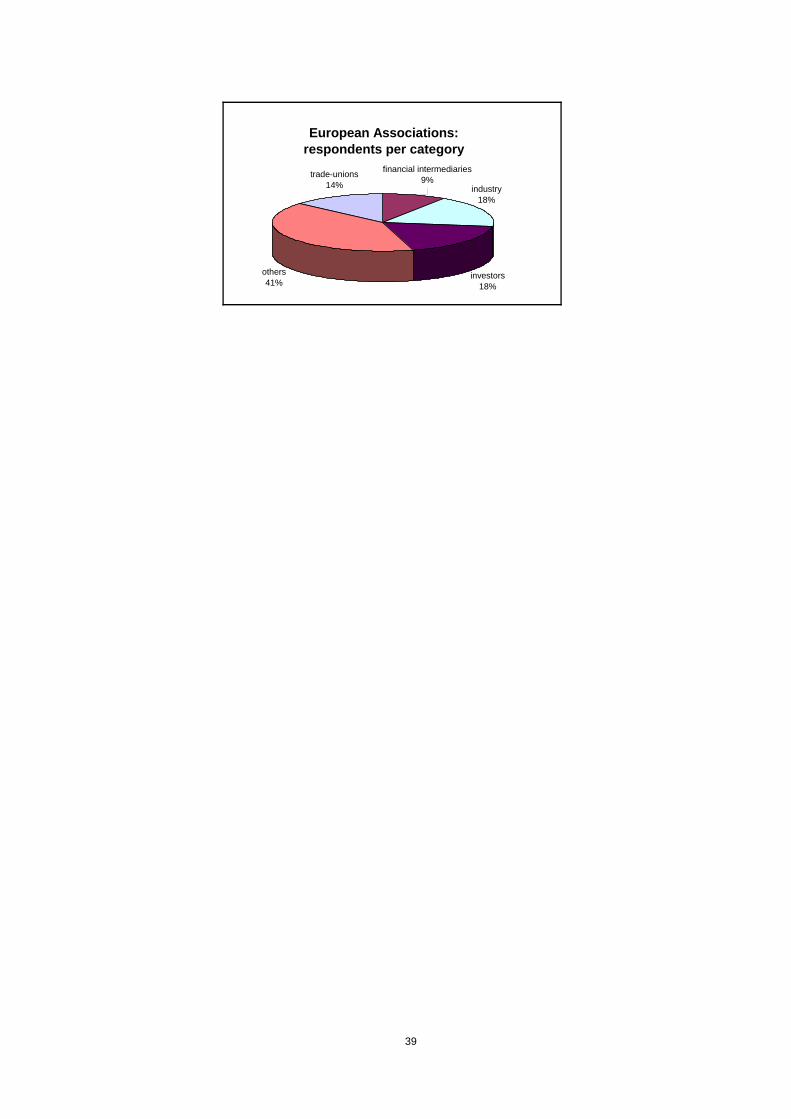

A detailed analysis of the repartition of the responses by category for France, Germany, the United Kingdom, Belgium, the Netherlands, Sweden, Italy as well as for the European associations is provided in Annex 1.

6

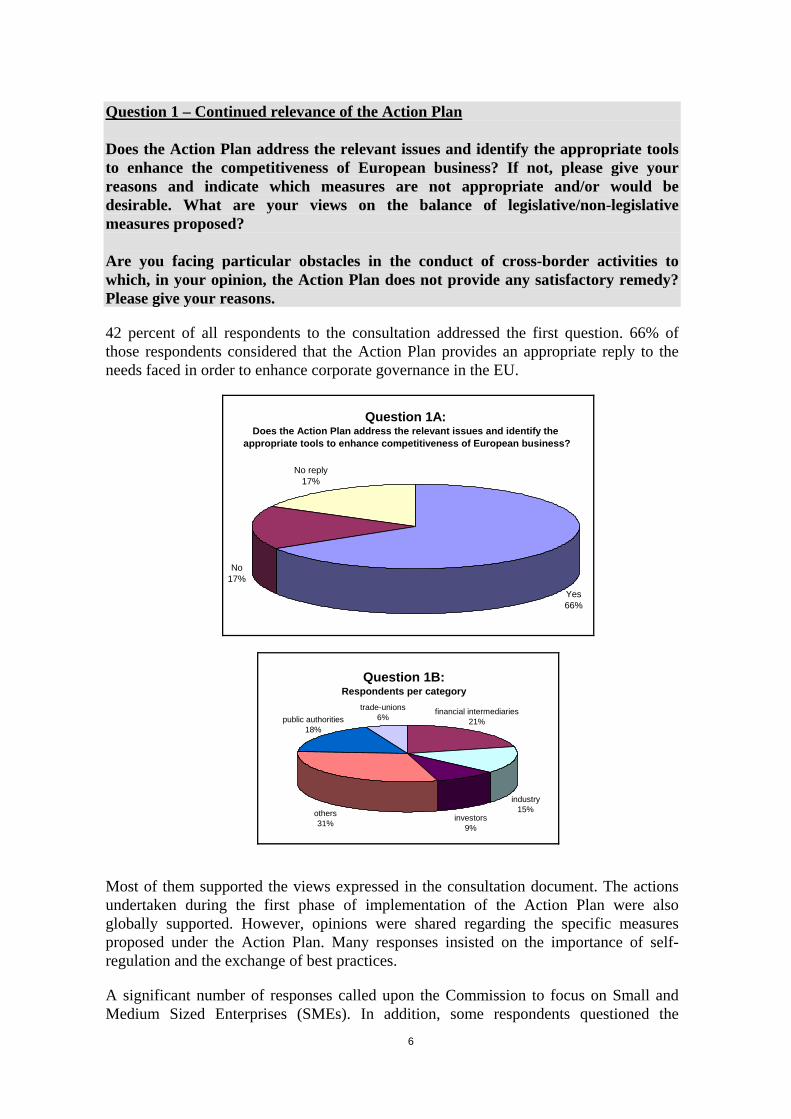

Question 1 – Continued relevance of the Action Plan Does the Action Plan address the relevant issues and identify the appropriate tools to enhance the competitiveness of European business? If not, please give your reasons and indicate which measures are not appropriate and/or would be desirable. What are your views on the balance of legislative/non-legislative measures proposed? Are you facing particular obstacles in the conduct of cross-border activities to which, in your opinion, the Action Plan does not provide any satisfactory remedy? Please give your reasons.

42 percent of all respondents to the consultation addressed the first question. 66% of those respondents considered that the Action Plan provides an appropriate reply to the needs faced in order to enhance corporate governance in the EU.

Question 1A: Does the Action Plan address the relevant issues and identify the

appropriate tools to enhance competitiveness of European business?

Yes66%

No17%

No reply17%

Question 1B: Respondents per category

others31%

industry15%

investors9%

public authorities18%

trade-unions6%

financial intermediaries21%

Most of them supported the views expressed in the consultation document. The actions undertaken during the first phase of implementation of the Action Plan were also globally supported. However, opinions were shared regarding the specific measures proposed under the Action Plan. Many responses insisted on the importance of self-regulation and the exchange of best practices.

A significant number of responses called upon the Commission to focus on Small and Medium Sized Enterprises (SMEs). In addition, some respondents questioned the

7

relevance of the distinction between listed and non-listed companies. All representatives of cooperatives and mutual societies invited the Commission to take account of all types of entrepreneurship and called for the adoption of specific statutes.

The views stated in the consultation document on the balance between legislative and non-legislative measures were generally supported by the small proportion of respondents who took position on this issue (12,5 % of respondents).

A very small minority of respondents identified obstacles encountered by companies to act cross-border. The most commonly quoted obstacles relate to taxation, accounting, social security/employment rights issues, the absence of a European company register and the continuity of business licences. Trade-unions considered that a social approach to corporate governance issues was missing.

Question 2 – Application of better regulation principles Do you have comments on the proposed application of better regulation principles in the area of corporate governance and company law? Are there other ways in which, in your view, the Commission should be seeking to improve its actions in this field?

41,5 percent of the respondents to the consultation took position on the application of better regulation principles.

All respondents to this question praised the views expressed in the consultation document on the application of better regulation principles to company law and corporate governance. The commitments to systematically consult stakeholders (with a 12-week period to submit comments) and to strictly apply the principles of subsidiarity and proportionality, as well as the systematic use of regulatory impact assessment received overwhelming support. Some suggested, in addition, undertaking systematic ex-post reviews.

Whilst underlining the current "regulatory fatigue" and calling for a "digestion/stabilisation period", a number of respondents pleaded for the adoption of enabling legislation (i.e. a proposal for a Directive on the transfer of registered office, a European Private Company Statute). 20% of the respondents expressed views on potential other ways to improve action. Some respondents suggested the Commission to undertake comparative studies and cost/benefit analysis in order to improve its action. Some also considered that company law should be more integrated with taxation, employment and accounting issues. In order to improve the quality of drafting of the European company law legislation, others suggested establishing an independent EU drafting team/office.

8

Question 3 – One share, one vote

What would be the added value of addressing the issue at EU level?

What would be the appropriate form for any EU instrument? Please give your reasons.

Are there, in your view, specific elements which any such instrument should cover?

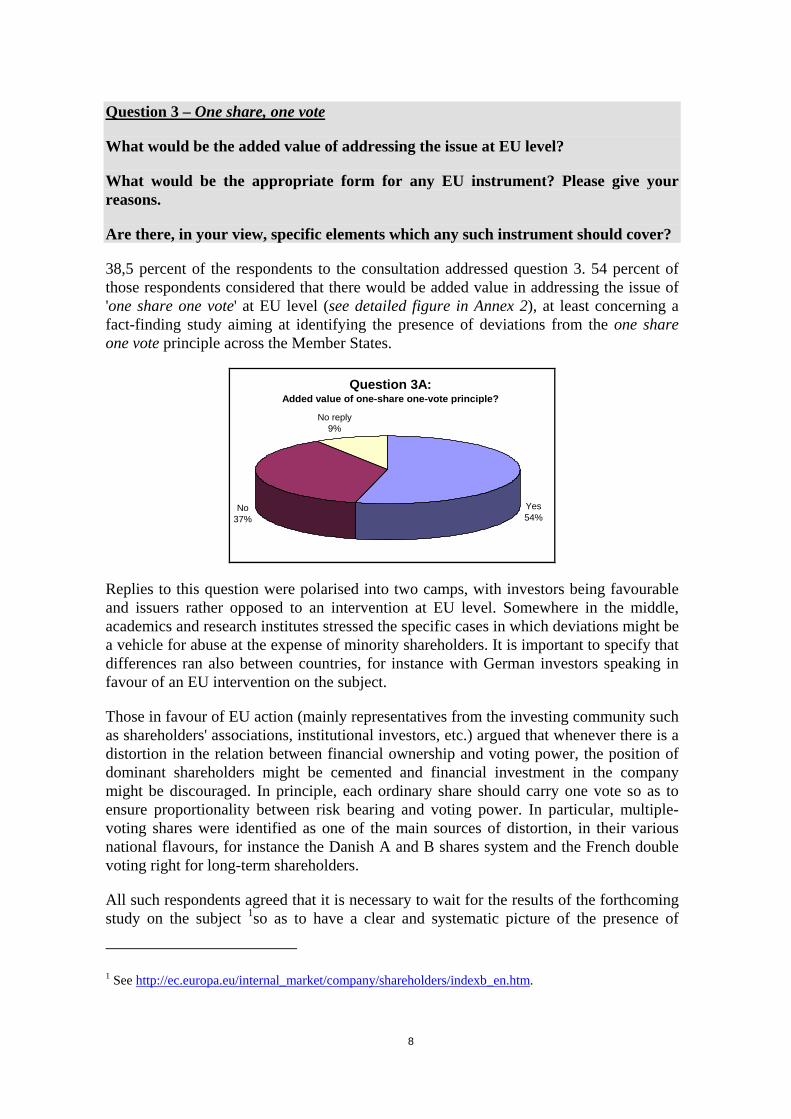

38,5 percent of the respondents to the consultation addressed question 3. 54 percent of those respondents considered that there would be added value in addressing the issue of 'one share one vote' at EU level (see detailed figure in Annex 2), at least concerning a fact-finding study aiming at identifying the presence of deviations from the one share one vote principle across the Member States.

Question 3A: Added value of one-share one-vote principle?

Yes54%

No37%

No reply9%

Replies to this question were polarised into two camps, with investors being favourable and issuers rather opposed to an intervention at EU level. Somewhere in the middle, academics and research institutes stressed the specific cases in which deviations might be a vehicle for abuse at the expense of minority shareholders. It is important to specify that differences ran also between countries, for instance with German investors speaking in favour of an EU intervention on the subject.

Those in favour of EU action (mainly representatives from the investing community such as shareholders' associations, institutional investors, etc.) argued that whenever there is a distortion in the relation between financial ownership and voting power, the position of dominant shareholders might be cemented and financial investment in the company might be discouraged. In principle, each ordinary share should carry one vote so as to ensure proportionality between risk bearing and voting power. In particular, multiple-voting shares were identified as one of the main sources of distortion, in their various national flavours, for instance the Danish A and B shares system and the French double voting right for long-term shareholders.

All such respondents agreed that it is necessary to wait for the results of the forthcoming study on the subject 1so as to have a clear and systematic picture of the presence of

1 See http://ec.europa.eu/internal_market/company/shareholders/indexb_en.htm.

9

deviations from the one share – one vote principle and their importance with regard to the total stock market capitalization across the EU.

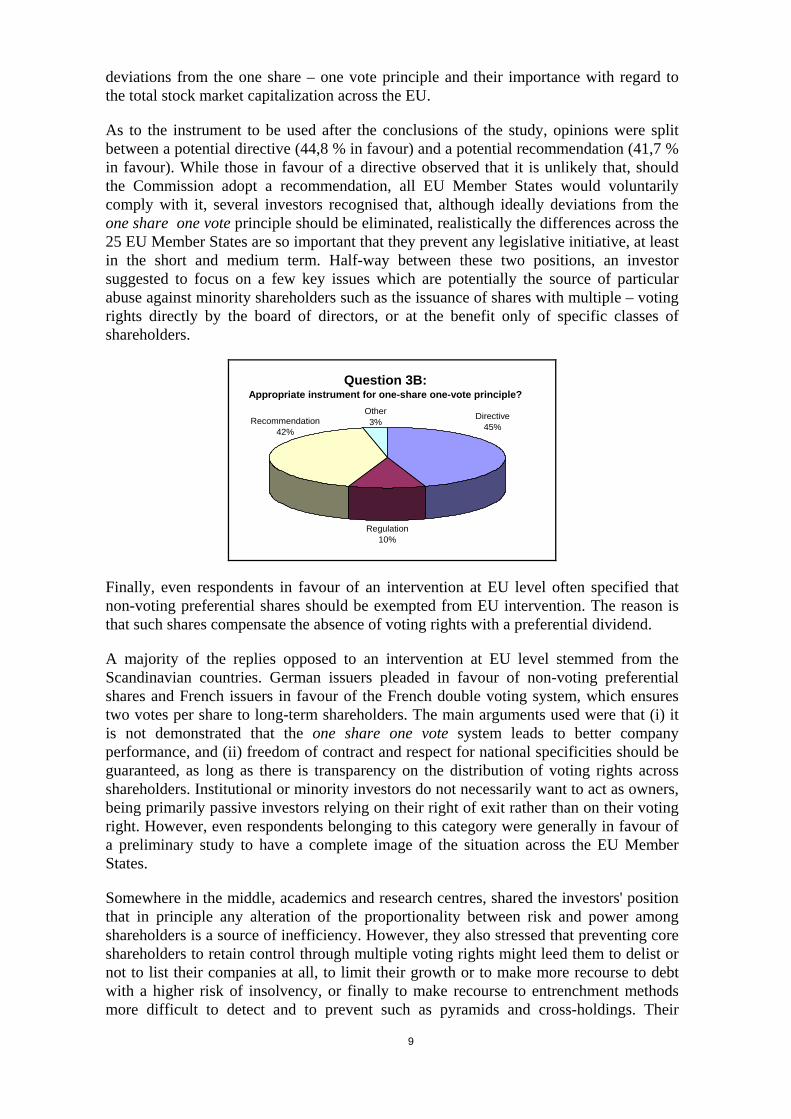

As to the instrument to be used after the conclusions of the study, opinions were split between a potential directive (44,8 % in favour) and a potential recommendation (41,7 % in favour). While those in favour of a directive observed that it is unlikely that, should the Commission adopt a recommendation, all EU Member States would voluntarily comply with it, several investors recognised that, although ideally deviations from the one share one vote principle should be eliminated, realistically the differences across the 25 EU Member States are so important that they prevent any legislative initiative, at least in the short and medium term. Half-way between these two positions, an investor suggested to focus on a few key issues which are potentially the source of particular abuse against minority shareholders such as the issuance of shares with multiple – voting rights directly by the board of directors, or at the benefit only of specific classes of shareholders.

Question 3B: Appropriate instrument for one-share one-vote principle?

Regulation10%

Other3%Recommendation

42%

Directive45%

Finally, even respondents in favour of an intervention at EU level often specified that non-voting preferential shares should be exempted from EU intervention. The reason is that such shares compensate the absence of voting rights with a preferential dividend.

A majority of the replies opposed to an intervention at EU level stemmed from the Scandinavian countries. German issuers pleaded in favour of non-voting preferential shares and French issuers in favour of the French double voting system, which ensures two votes per share to long-term shareholders. The main arguments used were that (i) it is not demonstrated that the one share one vote system leads to better company performance, and (ii) freedom of contract and respect for national specificities should be guaranteed, as long as there is transparency on the distribution of voting rights across shareholders. Institutional or minority investors do not necessarily want to act as owners, being primarily passive investors relying on their right of exit rather than on their voting right. However, even respondents belonging to this category were generally in favour of a preliminary study to have a complete image of the situation across the EU Member States.

Somewhere in the middle, academics and research centres, shared the investors' position that in principle any alteration of the proportionality between risk and power among shareholders is a source of inefficiency. However, they also stressed that preventing core shareholders to retain control through multiple voting rights might leed them to delist or not to list their companies at all, to limit their growth or to make more recourse to debt with a higher risk of insolvency, or finally to make recourse to entrenchment methods more difficult to detect and to prevent such as pyramids and cross-holdings. Their

10

conclusion is that clearer and enforceable rules on disclosure of voting and ownership positions deserve the highest priority.

Finally, all answers from cooperative entities and associations agreed that any initiative at EU level on the subject should exempt the one shareholder one vote system that characterizes the cooperative voting system.

Question 4 – Rights of shareholders

What would be the added value of addressing these questions, notably the nomination and dismissal of directors, shareholder communication and a special investigation right at EU level? Please give your reasons.

Which instrument would be best designed to deal with these matters? Please give your reasons.

Are there, in your view, specific elements which any such instrument should cover?

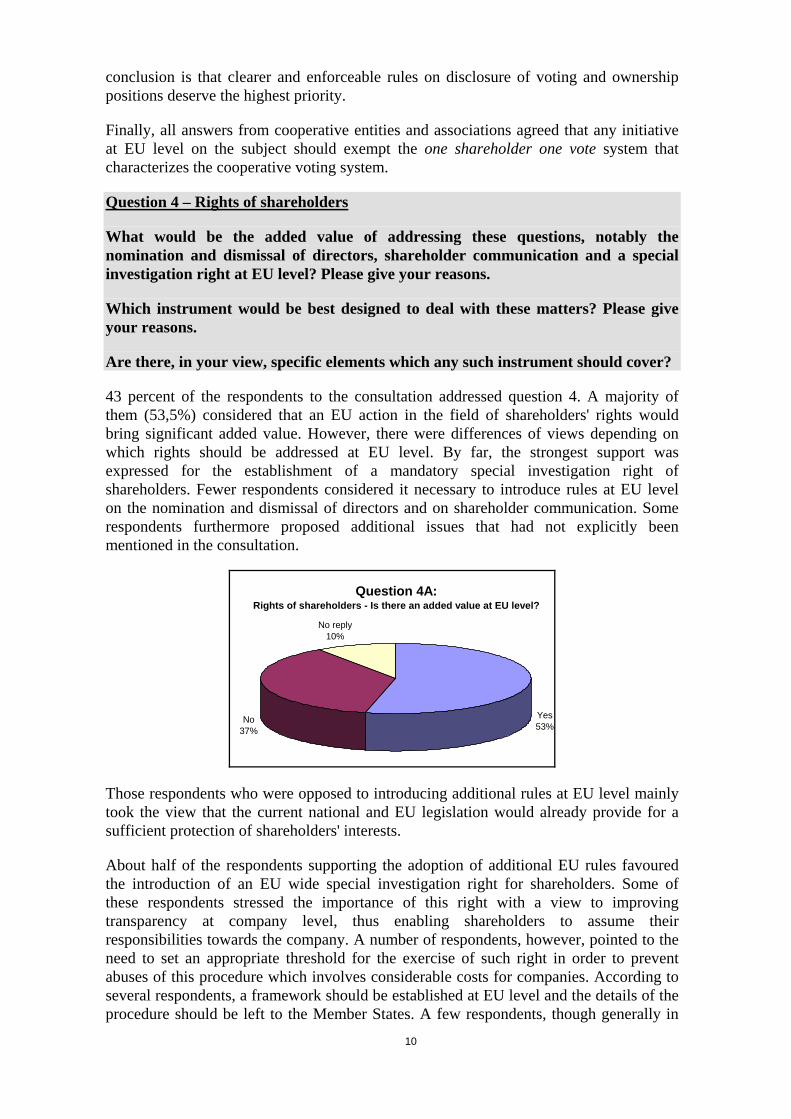

43 percent of the respondents to the consultation addressed question 4. A majority of them (53,5%) considered that an EU action in the field of shareholders' rights would bring significant added value. However, there were differences of views depending on which rights should be addressed at EU level. By far, the strongest support was expressed for the establishment of a mandatory special investigation right of shareholders. Fewer respondents considered it necessary to introduce rules at EU level on the nomination and dismissal of directors and on shareholder communication. Some respondents furthermore proposed additional issues that had not explicitly been mentioned in the consultation.

Question 4A: Rights of shareholders - Is there an added value at EU level?

Yes53%

No37%

No reply10%

Those respondents who were opposed to introducing additional rules at EU level mainly took the view that the current national and EU legislation would already provide for a sufficient protection of shareholders' interests.

About half of the respondents supporting the adoption of additional EU rules favoured the introduction of an EU wide special investigation right for shareholders. Some of these respondents stressed the importance of this right with a view to improving transparency at company level, thus enabling shareholders to assume their responsibilities towards the company. A number of respondents, however, pointed to the need to set an appropriate threshold for the exercise of such right in order to prevent abuses of this procedure which involves considerable costs for companies. According to several respondents, a framework should be established at EU level and the details of the procedure should be left to the Member States. A few respondents, though generally in

11

favour of a potential EU intervention, considered that further study is still necessary. Some respondents, finally, considered that this right should be accompanied by a special investigation rights for employee representatives. Those respondents that opposed EU action in this field in most cases took the view that the special investigation right would constitute only one aspect of the general control mechanisms provided for in Member States legislation and could therefore not be contemplated in an isolated way.

About one third of those respondents in favour of EU action in the area of shareholders rights supported potential measures on the nomination and dismissal of directors. These stakeholders generally considered these rights as fundamental. Some of them stressed in particular the need for individual nominations and dismissals. The opponents to such measure pointed to the existing differences between board structures in the Member States. Such differences would not, in their opinion, allow for a uniform EU regime.

Again, about one third of those in favour of EU action supported the introduction of rules on shareholder communication. Those respondents often put the emphasis on the cross-border aspect as only a coherent framework in that area would allow foreign shareholders to play an active role in the company. Several of them called for a clear distinction with the concept of 'acting in concert'. A number of respondents proposed to enhance the use of modern technologies, e.g. by setting up specific websites dedicated to the communication of the shareholders ("shareholders' fora"). The opponents to any EU action on shareholder communication considered the existing national frameworks to be sufficient. No additional burden should be imposed on companies for the setting up of a communication infrastructure.

About one fourth of the supporters of a possible EU action proposed other possible measures, alternatively or in addition to all or some of the actions mentioned explicitly in the consultation document. Such proposals concerned in particular the establishment of a right of shareholders to vote on key issues concerning the company (e.g. large transactions and changes to the articles of association or the capital structure), a right to be registered as a shareholder in the company and to receive subsequently dividends, information etc. directly from the issuer and general rules on the protection of minority shareholders. Other proposals concerned rules on stock lending, on the recognition of shareholder associations, disclosure of investors' identities and on information duties between the institutional investor and the beneficial owner.

Those respondents who were opposed to introducing any additional rules at EU level mainly considered that the current national and EU legislation already provides sufficient protection of shareholders' interests. In this regard, they often referred to the Commission proposal for a Directive on the exercise of voting rights by shareholders2.

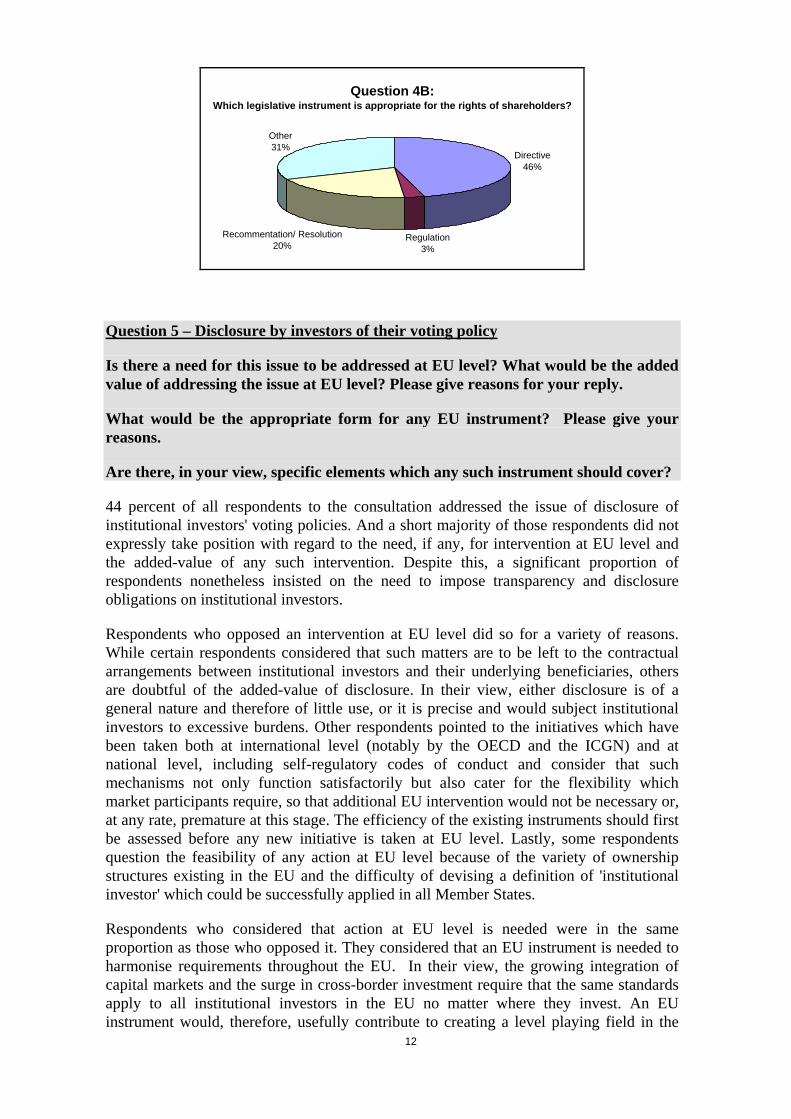

A directive was considered by half of the respondents as the best suited instrument in this area. About one fourth gave preference to a recommendation whereas most of the others pointed to the need for further prior study before addressing the question of the instrument to be used.

2 Proposal for a Directive of the European Parliament and of the Council on the exercise of voting rights by shareholders of companies having their registered office in a Member State and whose shares are admitted to trading on a regulated market and amending Directive 2004/109/EC (COM (2005) 685 final).

12

Question 4B: Which legislative instrument is appropriate for the rights of shareholders?

Directive46%

Regulation3%

Other31%

Recommentation/ Resolution20%

Question 5 – Disclosure by investors of their voting policy

Is there a need for this issue to be addressed at EU level? What would be the added value of addressing the issue at EU level? Please give reasons for your reply.

What would be the appropriate form for any EU instrument? Please give your reasons.

Are there, in your view, specific elements which any such instrument should cover?

44 percent of all respondents to the consultation addressed the issue of disclosure of institutional investors' voting policies. And a short majority of those respondents did not expressly take position with regard to the need, if any, for intervention at EU level and the added-value of any such intervention. Despite this, a significant proportion of respondents nonetheless insisted on the need to impose transparency and disclosure obligations on institutional investors.

Respondents who opposed an intervention at EU level did so for a variety of reasons. While certain respondents considered that such matters are to be left to the contractual arrangements between institutional investors and their underlying beneficiaries, others are doubtful of the added-value of disclosure. In their view, either disclosure is of a general nature and therefore of little use, or it is precise and would subject institutional investors to excessive burdens. Other respondents pointed to the initiatives which have been taken both at international level (notably by the OECD and the ICGN) and at national level, including self-regulatory codes of conduct and consider that such mechanisms not only function satisfactorily but also cater for the flexibility which market participants require, so that additional EU intervention would not be necessary or, at any rate, premature at this stage. The efficiency of the existing instruments should first be assessed before any new initiative is taken at EU level. Lastly, some respondents question the feasibility of any action at EU level because of the variety of ownership structures existing in the EU and the difficulty of devising a definition of 'institutional investor' which could be successfully applied in all Member States.

Respondents who considered that action at EU level is needed were in the same proportion as those who opposed it. They considered that an EU instrument is needed to harmonise requirements throughout the EU. In their view, the growing integration of capital markets and the surge in cross-border investment require that the same standards apply to all institutional investors in the EU no matter where they invest. An EU instrument would, therefore, usefully contribute to creating a level playing field in the

13

EU. Others consider that any such EU standards would reinforce confidence in cross-border investment and incite institutional investors to exercise their voting rights responsibly.

Views were split on the appropriate EU instrument to address the voting policies of institutional investors. The respondents who favoured a legislative instrument, generally a directive (28,3% in favour), considered that only binding measures will cater for the requisite level of harmonisation. A few argued that a regulation would be more appropriate (10% in favour) as it would avoid the discrepancies between Member States that may appear during transposition. The other respondents considered that a recommendation (23,3 % in favour) would push towards convergence whilst promoting market-led solutions- thus giving necessary flexibility to market participants.

As regards the specific elements that should form part of an EU instrument, if any, the two suggestions most commonly made were that the instrument should impose an obligation on institutional investors to disclose their voting policies to the public and the records of the execution of their votes to their beneficial owners. In this last instance, however, some respondents argued that this is not feasible in practice, in light of the very high number of investments. In their view, records of executed votes should be given to beneficial owners upon request. Other suggestions include an obligation to give information on stock lent and recalled and to justify votes cast against management or decision not to vote.

Question 6

Do you consider that

a) the question of the wrongful trading rules and

b) the issue of directors’ disqualification

should be addressed at EU-level? Please give your reasons.

Which instrument would, in your opinion, be most appropriate? Please give your reasons.

If so, are there, in your view, specific elements which any such instrument should cover?

Do you consider that any additional measures are needed to enhance transparency for legal entities and/or legal arrangements (e.g. trusts)?

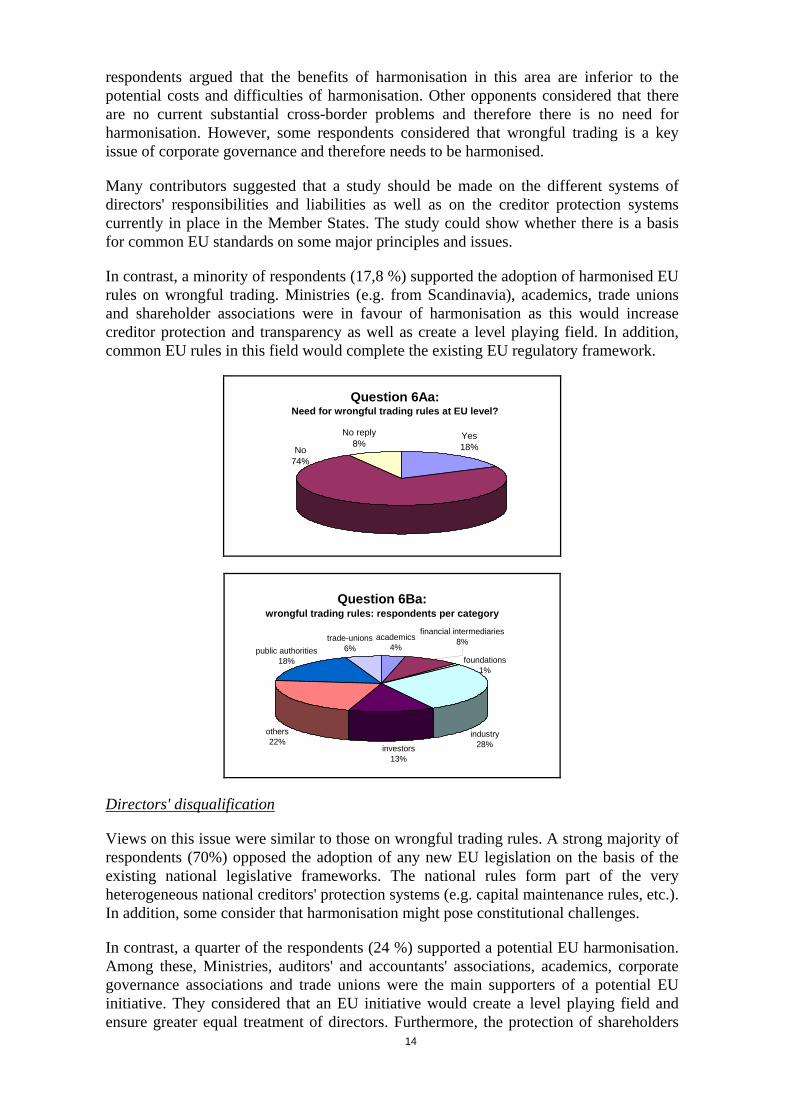

40,3 percent of the respondents to the consultation addressed the question on wrongful trading rules and directors qualification.

Wrongful trading rules

Concerning wrongful trading rules, a vast majority (73,8%) opposed any EU initiative. The opponents mostly based their argumentation on the existing detailed national regulations. Common EU rules would lead to legal uncertainty as a result of the overlap with national regulations. Furthermore, the issue is closely related to private law, especially solvency law, criminal law, bankruptcy law and procedural law, and can therefore not be dealt with at EU level in a pure company law context. In addition, some

14

respondents argued that the benefits of harmonisation in this area are inferior to the potential costs and difficulties of harmonisation. Other opponents considered that there are no current substantial cross-border problems and therefore there is no need for harmonisation. However, some respondents considered that wrongful trading is a key issue of corporate governance and therefore needs to be harmonised.

Many contributors suggested that a study should be made on the different systems of directors' responsibilities and liabilities as well as on the creditor protection systems currently in place in the Member States. The study could show whether there is a basis for common EU standards on some major principles and issues.

In contrast, a minority of respondents (17,8 %) supported the adoption of harmonised EU rules on wrongful trading. Ministries (e.g. from Scandinavia), academics, trade unions and shareholder associations were in favour of harmonisation as this would increase creditor protection and transparency as well as create a level playing field. In addition, common EU rules in this field would complete the existing EU regulatory framework.

Question 6Aa: Need for wrongful trading rules at EU level?

Yes18%

No reply8%

No74%

Question 6Ba: wrongful trading rules: respondents per category

investors13%

others22%

trade-unions6%

academics4%

financial intermediaries8%

foundations1%

industry28%

public authorities18%

Directors' disqualification

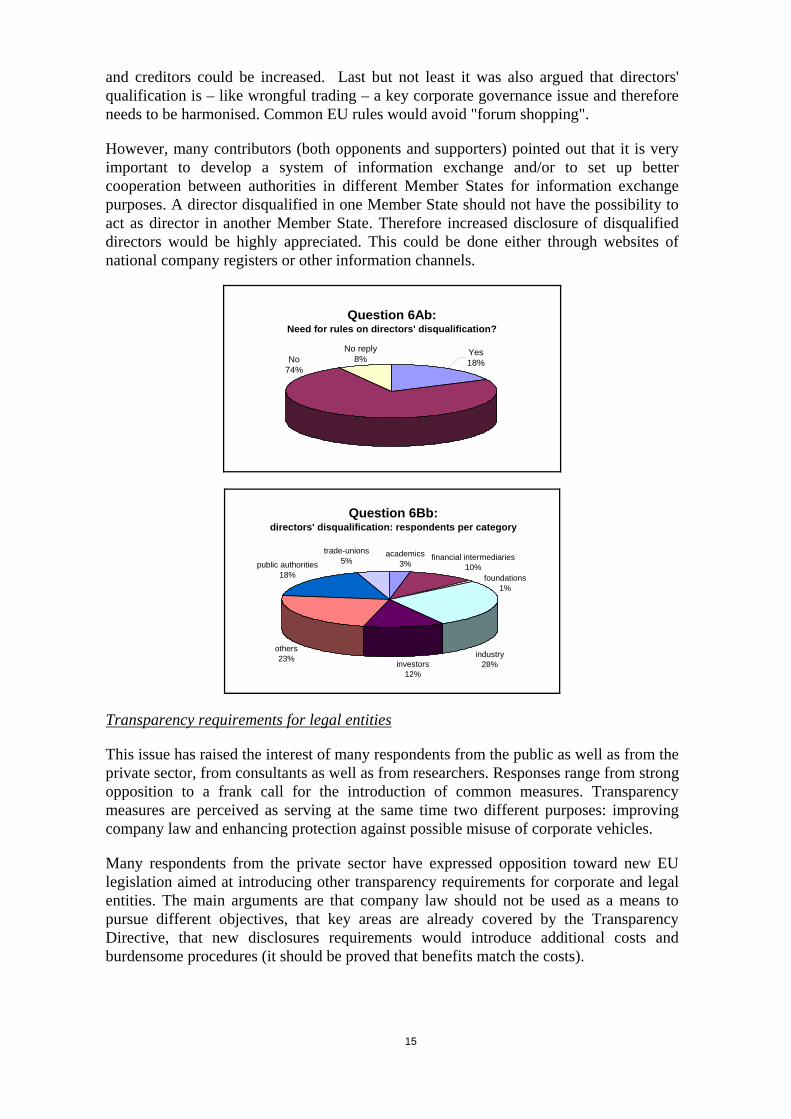

Views on this issue were similar to those on wrongful trading rules. A strong majority of respondents (70%) opposed the adoption of any new EU legislation on the basis of the existing national legislative frameworks. The national rules form part of the very heterogeneous national creditors' protection systems (e.g. capital maintenance rules, etc.). In addition, some consider that harmonisation might pose constitutional challenges.

In contrast, a quarter of the respondents (24 %) supported a potential EU harmonisation. Among these, Ministries, auditors' and accountants' associations, academics, corporate governance associations and trade unions were the main supporters of a potential EU initiative. They considered that an EU initiative would create a level playing field and ensure greater equal treatment of directors. Furthermore, the protection of shareholders

15

and creditors could be increased. Last but not least it was also argued that directors' qualification is – like wrongful trading – a key corporate governance issue and therefore needs to be harmonised. Common EU rules would avoid "forum shopping".

However, many contributors (both opponents and supporters) pointed out that it is very important to develop a system of information exchange and/or to set up better cooperation between authorities in different Member States for information exchange purposes. A director disqualified in one Member State should not have the possibility to act as director in another Member State. Therefore increased disclosure of disqualified directors would be highly appreciated. This could be done either through websites of national company registers or other information channels.

Question 6Ab: Need for rules on directors' disqualification?

No74%

No reply8%

Yes18%

Question 6Bb: directors' disqualification: respondents per category

academics3%

investors12%

others23% industry

28%

financial intermediaries10%

foundations1%

trade-unions5%public authorities

18%

Transparency requirements for legal entities

This issue has raised the interest of many respondents from the public as well as from the private sector, from consultants as well as from researchers. Responses range from strong opposition to a frank call for the introduction of common measures. Transparency measures are perceived as serving at the same time two different purposes: improving company law and enhancing protection against possible misuse of corporate vehicles.

Many respondents from the private sector have expressed opposition toward new EU legislation aimed at introducing other transparency requirements for corporate and legal entities. The main arguments are that company law should not be used as a means to pursue different objectives, that key areas are already covered by the Transparency Directive, that new disclosures requirements would introduce additional costs and burdensome procedures (it should be proved that benefits match the costs).

16

However, the importance of increased transparency as a safeguard against misuse of corporate vehicles or legal arrangements for fraud, money laundering and other financial crimes is widely acknowledged.

It is noted that enhanced transparency would be helpful not only to prevent criminals from misusing legal entities but also to protect shareholders.

Several respondents have observed that transparency tools should be introduced to identify undisclosed shareholders when the ultimate investors use third parties (who are registered shareholders) or hide using other techniques (trusts, securities lending, etc.).

Many respondents, particularly from the public and consultancy sector, as well as academics, supported the adoption of enhanced transparency requirements, as those would be beneficial for the fight against financial crime. Some replies focused specifically on the issue of bearer shares, relevant both for shareholders' disclosure and prevention of criminal misuse.

Amongst these respondents, some suggested establishing an enhanced transparency regime on an EU wide basis. Such regime would be based on a common set of rules on the type of information to be filed with national or local registries and to be made publicly available.

Question 7 – Transfer of a company's registered office

In the light of existing instruments, is there still a need for a directive on the transfer of registered office? Please give your reasons.

Are there, in your view, specific elements which any such Directive should cover?

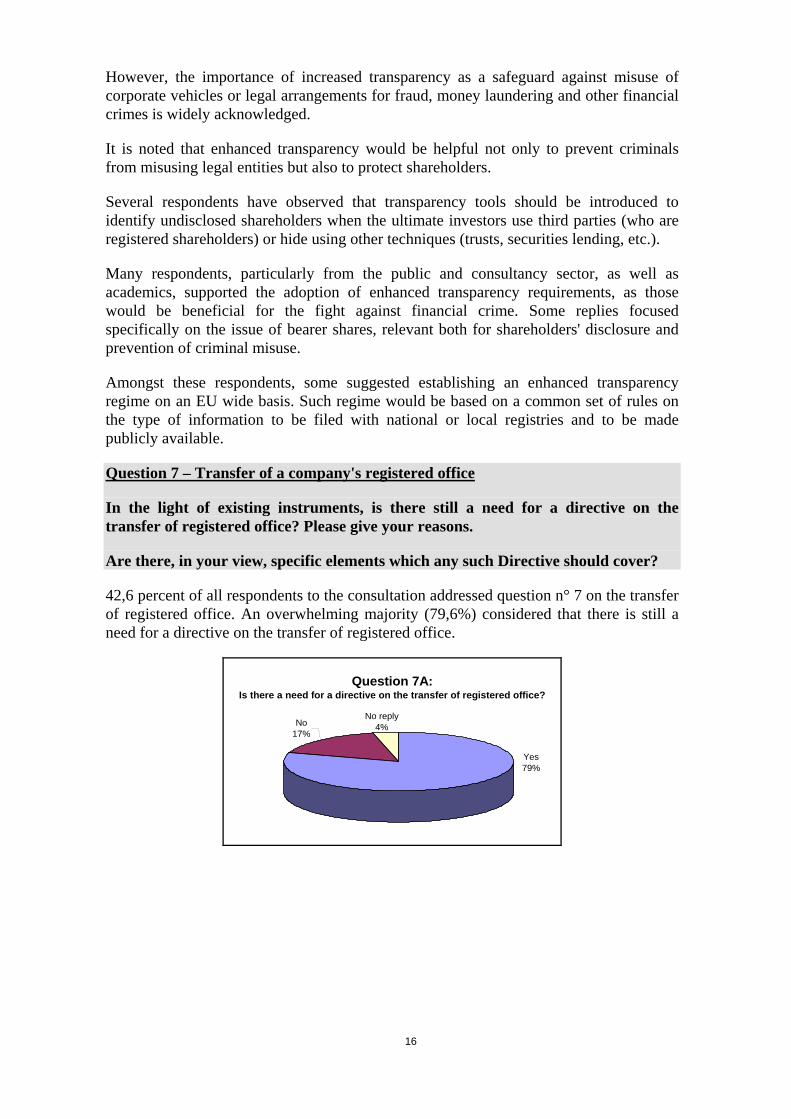

42,6 percent of all respondents to the consultation addressed question n° 7 on the transfer of registered office. An overwhelming majority (79,6%) considered that there is still a need for a directive on the transfer of registered office.

Question 7A: Is there a need for a directive on the transfer of registered office?

Yes79%

No reply4%No

17%

17

Question 7A: 14th directive: resondents per category

academics4%

industry32%

investors12%

others19%

financial intermediaries8%

foundations1%

trade-unions7%public authorities

17%

Such directive would facilitate the mobility of European companies, in particular SMEs, and allow them to locate their business in the Member State that best suits their needs. Several of them stated that it should be a high priority to come forward with a long-awaited proposal. Some found it less urgent in the light of the recent developments, i.e. the entry into force of a Statute on a European Company (SE) and the recent adoption of the 10th Company Law Directive on cross-border mergers, which have made the mobility of SEs easier. Many of the respondents mentioned that the existing measures still do not provide for a straightforward transfer of the registered office (the transfer of registered office is only possible through a conversion into an SE or a cross-border merger) and, therefore, a European legislation is necessary. Several respondents also emphasised that there is still uncertainty on the legal and tax consequences of transfer under present law and jurisprudence of the European Court of Justice on the freedom of establishment. Therefore, enhanced certainty is therefore needed. The need for a directive to ensure a proper protection of the interests of creditors, shareholders and employees in relation to the transfer as well as a formal procedure for the transfer was also underlined.

Those few that opposed the initiative or did not consider it as a priority, stated that either the problem did not concern them directly or that the existing measures and the case law are sufficient for the time being and that no new initiatives should be undertaken before the practical implications of those measures have been properly assessed. Some suggested focusing on the facilitation and adaptation of existing measures. A few respondents questioned the practical value of a potential directive due to obstacles such as taxation or employee participation issues.

Half of the respondents indicated specific elements to be covered by a directive. A considerable number of respondents stressed that for the practical usefulness of the directive it is necessary to clarify and regulate taxation issues related to the transfer of registered office and ensure tax neutrality of such transfer. One fourth of the respondents suggested that a possible directive should afford sufficient protection for the interest of stakeholders, in particular creditors and shareholders (including minority shareholders) in the case of transfer. Two respondents suggested that the minimum protection of shareholders should be ensured either by the directive or by other specific European measures and not leave this issue to the Member States' discretion.

Many mentioned the need to regulate the procedure for the transfer and to ensure transparency and necessary supervision through proper cooperation and information exchange between the home and host Member States (e.g. in the area of insolvency or in the case of disqualification of directors). One respondent stressed that the registration procedure should not be burdensome for companies. Some underlined that the directive should allow companies to change legal statute while providing guarantees in order to

18

make sure that the freedom of establishment is not misused to circumvent mandatory regulations.

Several stakeholders took position on employee participation, calling for a satisfactory standard of employee participation. A number of industry representatives opposed the inclusion of the employee participation regime in a directive, in particular the one agreed for SE Statute or the 10th Company Law Directive on cross-border mergers as this would very much reduce the attractiveness of a cross-border transfer of registered office.

Two respondents suggested clarifying and possibly harmonising the concept of seat which should determine the law applicable to the company.

Question 8 – Choice of board structure

Should the question of the choice of board structure be addressed at EU level? Please give your reasons.

Which instrument would be best designed to deal with this matter? Please give your reasons.

Are there, in your view, specific elements which any such instrument should cover?

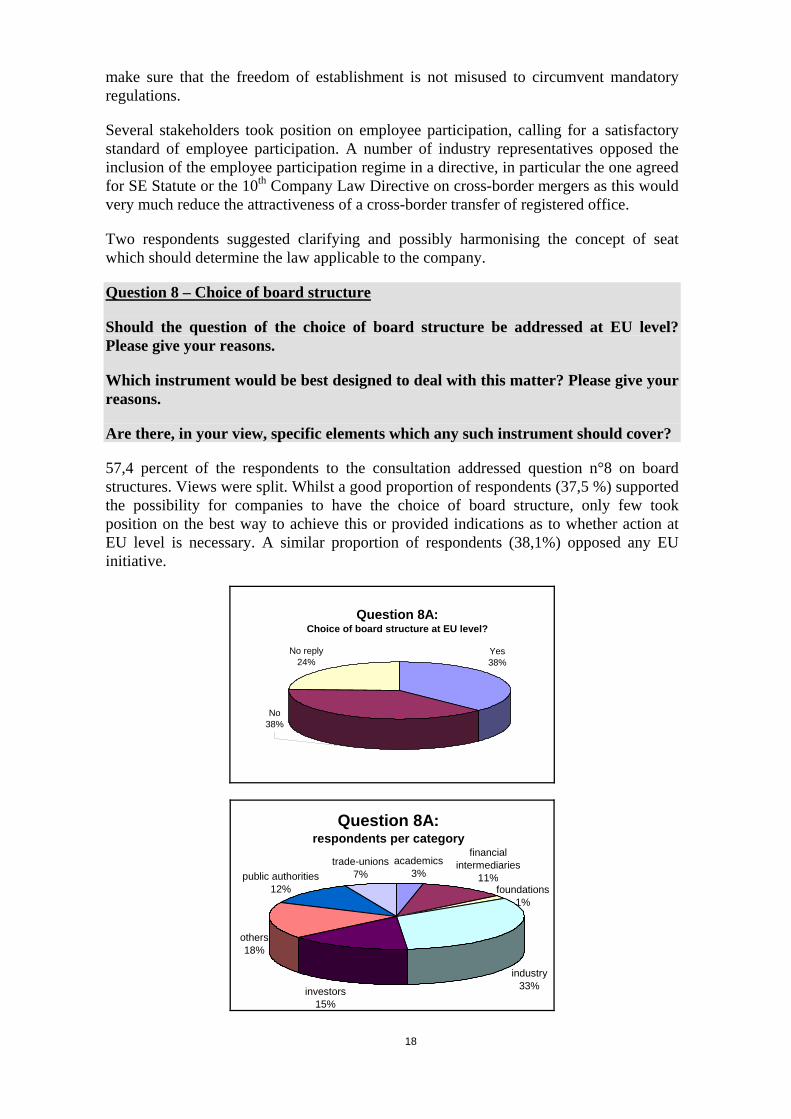

57,4 percent of the respondents to the consultation addressed question n°8 on board structures. Views were split. Whilst a good proportion of respondents (37,5 %) supported the possibility for companies to have the choice of board structure, only few took position on the best way to achieve this or provided indications as to whether action at EU level is necessary. A similar proportion of respondents (38,1%) opposed any EU initiative.

Question 8A: Choice of board structure at EU level?

No38%

No reply24%

Yes38%

Question 8A: respondents per category

academics3%

investors15%

industry33%

foundations1%

financial intermediaries

11%trade-unions

7%public authorities12%

others18%

19

The opponents to any EU initiative based their opinion on the application of the subsidiarity principle. Some referred to the numerous tools allowing companies to circumvent the absence of choice of board structure by setting up a SE, by taking advantage of the possibilities offered by the 10th Company Law Directive on cross-border mergers or by the recent case-law of the European Court of Justice. Interestingly, economic sectors like the cooperative sector consider that there is no need for further action, to the extent that the choice between board structures is already granted to the European Cooperative.

Two respondents called for a preliminary comparative analysis of the operation of board structures across the EU (e.g. respective role of the committees in the unitary board structure and balance of responsibilities between the supervisory/administrative boards in a two-tier system).

The freedom of choice of board structure attracted wide support from companies and issuers as well as, to a lesser extent, from shareholders. Some respondents considered that the choice between different board structures should be related to the company and the ownership structure, and not the country of the registered office.

Many companies or their representative organisations supported the idea of offering organisational freedom to listed companies, considering that this flexibility would contribute to increasing companies' competitiveness. This would, in particular, enable groups to apply a similar board structure to the one of the parent company, independently of the system in place in the Member States where the subsidiaries are located. Greater freedom of choice to companies concerning their board structure could facilitate cross-border corporate restructuring and mobility. This would also contribute to reducing the costs thereof by letting companies keep their original form after moving their registered office to another Member State. Furthermore, some respondents saw no major reason why such choice should be limited to the SE, and not be granted to companies with a national corporate form. However, some other respondents recommend waiting until more experience has been gained with the SE.

Whilst most of the proponents of this proposal considered that this option should be granted to all listed EU companies, some considered that it should be extended to unlisted companies as well.

One third of the proponents of an EU initiative took position on the best way to achieve the needed flexibility. Opinions were divided: some respondents considered that it is for Member States to act, others that an impulse should be given at EU level in the form either of a recommendation or of a principles-based directive.

Proponents of an EU action nevertheless unanimously considered that the EU should refrain from legislating in detail but rather follow a principles-based approach. A potential directive could require Member States (1) to allow companies to choose their board structure and (2) to adopt accompanying measures so that companies are clear as to the consequences of adopting a particular structure taking account of the local traditions and legal systems of their respective Member States. Furthermore, a potential directive should leave room for self-regulation, to make intermediate alternatives within

20

both types of board structure possible3 and to allow for the adaptation of national law to the evolution of corporate organisation techniques.

The proponents of a directive vs. a recommendation considered a directive as the only reasonable and effective tool to make progress, because of its binding character.

Very few respondents gave indications on potential elements to be covered by a possible EU instrument. Two respondents referred to the composition of and attribution of powers to the organs of the company, a reminiscence of the Commission proposal for a 5th Company Law Directive, which legislated in detail such issues and was withdrawn in 2001, as it did not match the regulatory expectations of market participants. The issue of worker participation is also mentioned by two other respondents as an element to be specifically examined.

Question 9 – Squeeze out and sell out rights

Do you think that a squeeze out and a sell out right should be introduced at EU-level? Please give your reasons.

If so, should these rights be limited to companies which shares are traded on a regulated market (“listed companies”)? Please give your reasons.

Which instrument would be best designed to deal with this matter? Please give your reasons.

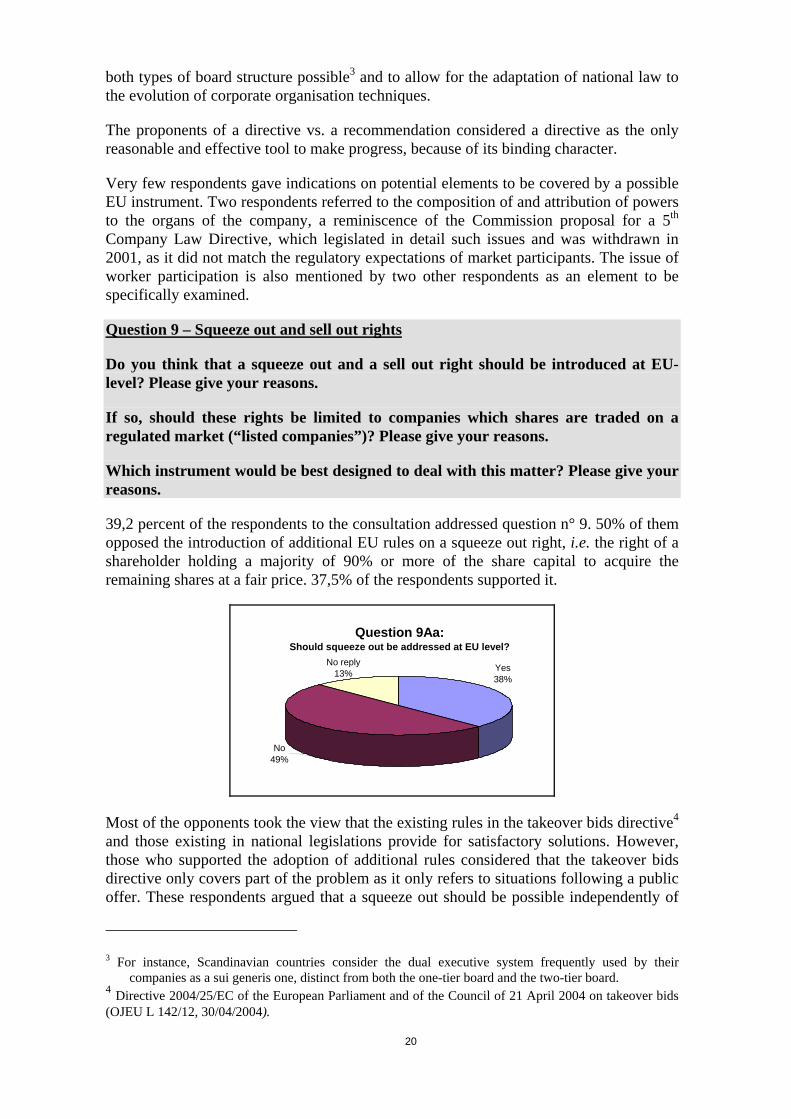

39,2 percent of the respondents to the consultation addressed question n° 9. 50% of them opposed the introduction of additional EU rules on a squeeze out right, i.e. the right of a shareholder holding a majority of 90% or more of the share capital to acquire the remaining shares at a fair price. 37,5% of the respondents supported it.

Question 9Aa: Should squeeze out be addressed at EU level?

No49%

Yes38%

No reply13%

Most of the opponents took the view that the existing rules in the takeover bids directive4 and those existing in national legislations provide for satisfactory solutions. However, those who supported the adoption of additional rules considered that the takeover bids directive only covers part of the problem as it only refers to situations following a public offer. These respondents argued that a squeeze out should be possible independently of

3 For instance, Scandinavian countries consider the dual executive system frequently used by their

companies as a sui generis one, distinct from both the one-tier board and the two-tier board. 4 Directive 2004/25/EC of the European Parliament and of the Council of 21 April 2004 on takeover bids (OJEU L 142/12, 30/04/2004).

21

how the majority has been acquired, e.g. as an instrument to facilitate the integration of an acquired company. A number of respondents finally stressed that in any case employee shareholders would have to be exempted from the application of the squeeze out right.

The proponents of potential additional EU rules considered that a sell out right should established at the same time, in order to achieve a balance between the interests of the majority shareholder and those of the minority shareholders5. A number of these respondents stressed however that appropriate safeguards should be put in place in order to counter the risk of potential sell out requests by minority shareholders.

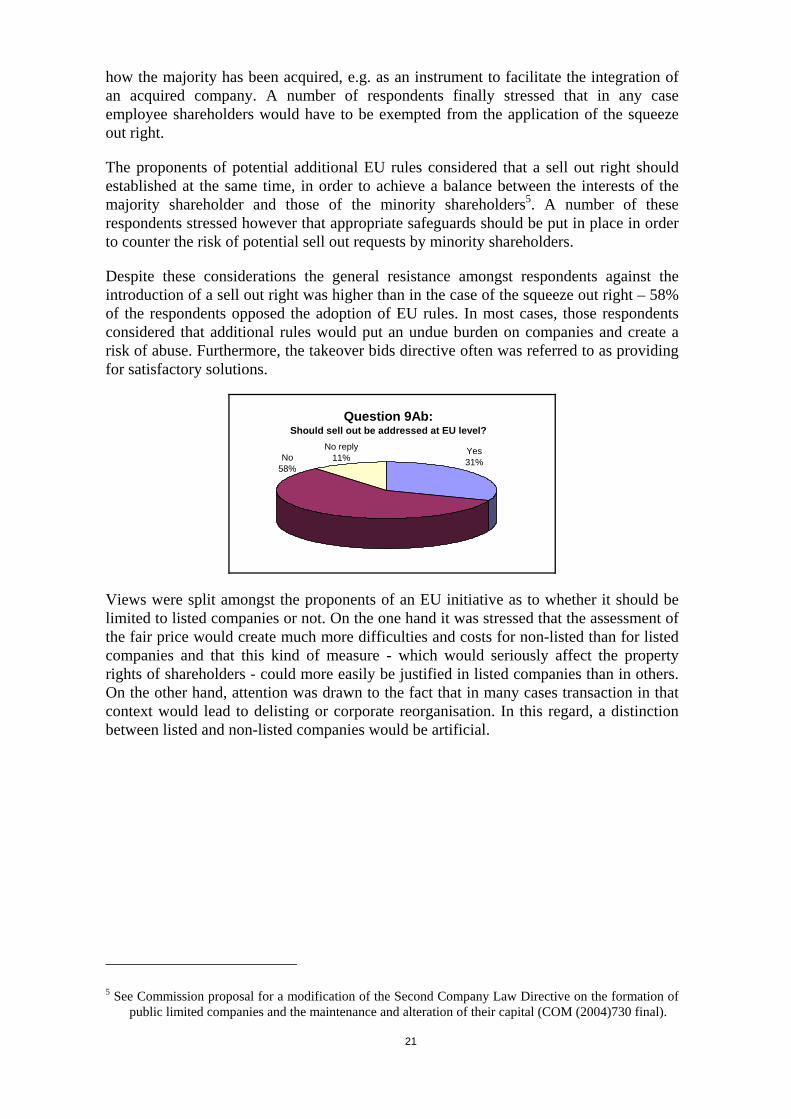

Despite these considerations the general resistance amongst respondents against the introduction of a sell out right was higher than in the case of the squeeze out right – 58% of the respondents opposed the adoption of EU rules. In most cases, those respondents considered that additional rules would put an undue burden on companies and create a risk of abuse. Furthermore, the takeover bids directive often was referred to as providing for satisfactory solutions.

Question 9Ab: Should sell out be addressed at EU level?

Yes31%

No reply11%No

58%

Views were split amongst the proponents of an EU initiative as to whether it should be limited to listed companies or not. On the one hand it was stressed that the assessment of the fair price would create much more difficulties and costs for non-listed than for listed companies and that this kind of measure - which would seriously affect the property rights of shareholders - could more easily be justified in listed companies than in others. On the other hand, attention was drawn to the fact that in many cases transaction in that context would lead to delisting or corporate reorganisation. In this regard, a distinction between listed and non-listed companies would be artificial.

5 See Commission proposal for a modification of the Second Company Law Directive on the formation of

public limited companies and the maintenance and alteration of their capital (COM (2004)730 final).

22

Question 10 – Groups and pyramids

Should the issues of framework rules for groups and abusive pyramids, in your view, be addressed at EU-level? Please give your reasons.

Which instrument would be best designed to deal with this matter? Please give your reasons.

Are there, in your view, specific elements which any such instrument should cover?

29 percents of the respondents to the consultation addressed the issue of a potential EU initiative on groups. 67,5 percent of them were opposed to the adoption of EU rules. Even the respondents supporting an EU intervention (31,1 %) specified that this should only concern transparency issues, especially for cross-border groups.

24,9 percent of the respondents to the consultation addressed the issue of abusive pyramids. 71% of the respondents considered that no action was advisable or that the subject should be dealt with by the forthcoming study on shareholder democracy and that in any case an intervention at EU level would be justified only with regard to ensuring full transparency on cross-border pyramidal groups.

Question 11 – European Company Statute

How useful do you judge the ECS to be in practice? Do you consider any modifications are appropriate and desirable? Please give your reasons.

38 percent of the respondents to the consultation addressed question n° 11 on the European Company Statute. A majority of them considered it premature to assess the usefulness of an SE in practice and suggested that more experience be gained before considering any revisions of the Regulation on the statute of the European Company. Some respondents stated that in some Member States the necessary legislation has not been transposed yet and/or that they have not had any practical experience with the SE.

Still about 40% of the respondents considered the European Company Statute to be very useful or partly useful. Among the main advantages of the SE form the respondents mentioned the possibility to:

- integrate business bases from several countries in one company which leads to improved operational efficiency, reduced operational risk and enhanced capital efficiency;

- implement supranational mergers when founding the SE, - transfer registered office cross-border, - choose the management structure (one-tier/two-tier). Some stated, however, that the adoption of 10th and 14th Company Law Directives on cross border mergers and on the transfer of registered office may cause the SE Statute to be less attractive for the companies.

23

According to a few respondents, however, the European Company Statute is clearly not useful. Among the shortcomings of the Statute which may have caused a limited interest of the stakeholders in the European Company the following were mentioned:

- the lengthy and complex formation process,

- the employee participation issue (considered by some as an obstacle to investment) and the related complicated and unclear rules on negotiations;

- the uncertainty of the legislative regime (divided between EU and national law),

- the lack of uniformity of the SE form (28 different SE forms, depending on the state in which the company is registered, which leads to considerable high costs of legal advice and legal compliance),

- the lack of a suitable tax regime,

- a practical problem of non-recognition by the host Member State of certain types of shares (bearer shares) allowed in the home Member States in the case of transfer of the registered office of the SE;

- the issue of the location of the registered and head office in the same Member State (some respondents stated that it is contrary to the case law of the European Court of Justice);

- the inappropriateness to SMEs’ needs.

Approximately one third of the respondents considered that amendments should be brought to the regulation. One fourth of them suggested that the possibility should be given to have a head office and registered office in different Member States (especially in the light of the recent European Court of Justice case law).

The respondents who had some experience with the European Company identified the following practical problems with the application of the SE Regulation which should be clarified or modified:

- the issue of whether an SE incorporated in one Member State which has operations in another Member State (which would require it to register a branch in that Member State if it were a public limited company) should be required to register a branch (practice seems to vary between Member States);

- the tax regime;

- the rules on employee participation (they should be simplified and made more flexible);

- consider new ways of creation of SE, e.g. the possibility to set up SE by a formation of a new company;

- the solution at EU level for the situation where an SE transfers its seat/takes part in the formation of an SE by merger if the seat of the other merging company is registered in another Member State during an ongoing accounting period;

- stricter rules on information and publicity (one respondent suggests a centralised control over the registration of SEs by a European body);

- co-ordination of other Community legislation which may obstruct creation of an SE (in particular the rules relating to VAT and deposit guarantee schemes were mentioned).

24

Question 12 – European Private Company (EPC)

Do you see value in developing an EPC Statute in addition to the existing European (e.g. Societas Europaea, European Interest Grouping) and national legal forms? Please give your reasons.

If so, are there, in your view, specific elements which any such statute should cover?

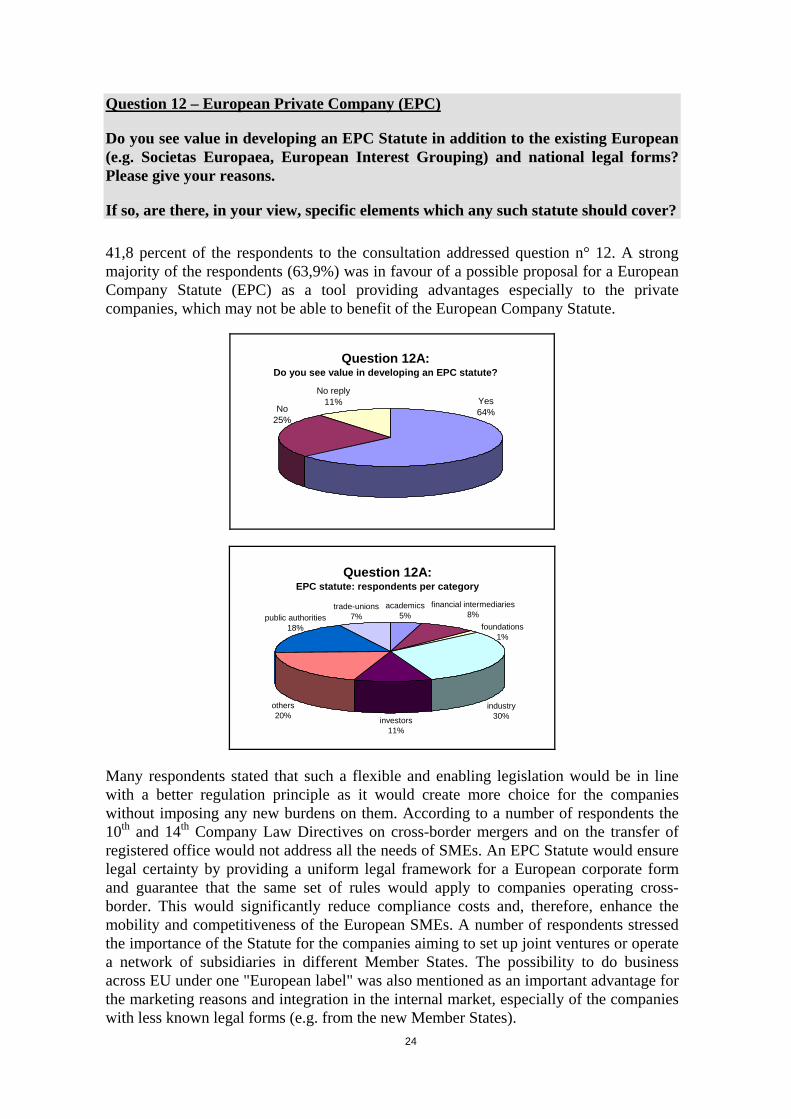

41,8 percent of the respondents to the consultation addressed question n° 12. A strong majority of the respondents (63,9%) was in favour of a possible proposal for a European Company Statute (EPC) as a tool providing advantages especially to the private companies, which may not be able to benefit of the European Company Statute.

Question 12A: Do you see value in developing an EPC statute?

No reply11% Yes

64%No25%

Question 12A: EPC statute: respondents per category

investors11%

others20%

public authorities18%

trade-unions7%

academics5%

financial intermediaries8%

foundations1%

industry30%

Many respondents stated that such a flexible and enabling legislation would be in line with a better regulation principle as it would create more choice for the companies without imposing any new burdens on them. According to a number of respondents the 10th and 14th Company Law Directives on cross-border mergers and on the transfer of registered office would not address all the needs of SMEs. An EPC Statute would ensure legal certainty by providing a uniform legal framework for a European corporate form and guarantee that the same set of rules would apply to companies operating cross-border. This would significantly reduce compliance costs and, therefore, enhance the mobility and competitiveness of the European SMEs. A number of respondents stressed the importance of the Statute for the companies aiming to set up joint ventures or operate a network of subsidiaries in different Member States. The possibility to do business across EU under one "European label" was also mentioned as an important advantage for the marketing reasons and integration in the internal market, especially of the companies with less known legal forms (e.g. from the new Member States).

25

A minority of the opponents (25,2%) mentioned the lack of interest in the industry in such corporate form. They also considered that before introducing a new European form the practical application of the existing measures, in particular the SE Statute, the 10th and 14th Company Law Directives, should be assessed and the need for yet another European corporate form further examined. Several respondents argued that the national corporate forms and the existing European measures are sufficient to ensure the choice and mobility for companies. Two respondents stressed that reaching an agreement on the uniform EPC Statute would prove even more difficult than in the case of SE Statute due to even greater differences in the Member States legislations on private companies than those on public companies.

Some respondents questioned the usefulness of the EPC given the limited up-take of the existing SE and/or doubted practical value of the Statute due to other obstacles to corporate mobility such as taxation, accounting, insolvency or employee participation issues.

There was a consistency of views among the respondents in favour of the EPC that (unlike the European Company Statute) the Statute for private companies should provide for a uniform, genuinely supranational form with as few references to the national laws as possible. Some suggested that the issues not resolved by the Statute or the articles of association should be solved by reference to the general principles underlying the regulation (of which coherent interpretation would be ensured by the European Court of Justice). Two respondents underlined that the adoption of a Model law for the EPC would not be sufficient as it could create legal uncertainty due to inconsistent application in the Member States.

A number of respondents suggested that the Statute should contain mandatory rules on the protection of creditors, shareholders (including minority shareholders) and the public interest, while ensuring flexibility and leaving contractual freedom to the parties in other aspects. Some respondents proposed that a standard form of articles of association be annexed to the EPC regulation as guidance.

Opinions were shared on minimum capital requirement. Some suggested that no such requirement should be included in the directive, whilst others considered that the minimum capital of €25.000 would be an appropriate level for SMEs. An intermediate solution was proposed to set the requirement at €1.000-2.000, serving as a minimum seriousness test but not creating a real obstacle in access to the EPC. As regards the minimum capital regime, conflicting solutions were suggested: leaving the issue to be regulated at the national level or designing a separate, simpler and more flexible, regime on minimum capital in a directive.

About 10% of those who responded to the question suggested the inclusion of the rules on employee participation in the proposed regulation. Among the respondents who referred to that issue there were proposals to either follow the rules of the SE in that respect, limit the application of the Statute to the companies having less than 500 employees or choosing a compromise solution (i.e. different rules depending on the size of the company). A number of industry representatives clearly opposed the inclusion of the employee participation rules in the regulation (especially as agreed for the 10th Company Law Directive) and stated that this issue should be left for the national law.

A number of respondents underlined the need to ensure that the tax regime is advantageous if the EPC is to be used in practice.

26

Several stakeholders proposed that the regulation should provide the possibility to set up an EPC ab initio and be available for the companies/persons active only in one Member State.

A few stakeholders suggested to consider the creation of a special (possibly on-line) register for the EPCs with a uniform registration forms and harmonised registration procedures.

Question 13 – European Foundation Statute

Do you consider it useful to carry out an examination on the feasibility of a European Foundation Statute? Please give your reasons.

55 percent of all respondents to the consultation addressed question n° 13 on the European Foundation Statute. A high number of foundations from a wide range of sectors (science, research, education, culture, health, social welfare, finance, etc.) addressed this issue exclusively. The foundation sector unanimously urged the Commission to carry out the feasibility study on a European Foundation Statute. Contributors emphasised that an optional European legal tool for foundations would facilitate the cross-border activity of foundations in areas where the pooling of expertise and resources is badly needed (e.g. research and development, the promotion of scientific and technological advance, education, and environment). The European Foundation Statute would contribute to the European objectives and policies in various areas.

Many respondents highlighted that foundations and founders are increasingly affected by the globalisation of the economy and a growing number of foundations operate across borders. However, the current environment for cross-border giving and cross-border operations lags behind. Administrative burdens during the procedure of setting up a branch in another country, problems with the recognition of legal personality, difficulties with running operations abroad are effective barriers to foundations' trans-national work. Discriminative tax provisions hinder cross-border giving and receiving of funds. The European Foundation Statute would help overcoming these difficulties.

A relatively low number of respondents to the consultation from outside the foundation sector have expressed views on this issue. These respondents were somewhat less enthusiastic about the Statute. More than half of them (mainly from the public sector, industry associations, representatives of the financial sector and some professional services providers) were sceptical as to the usefulness of such an instrument or would prefer other solutions to address the foundations' requests.

Some of these respondents questioned whether there is a real demand for such a Statute. Some argued that the main difficulties foundations are currently facing could be resolved in much simpler ways by ensuring mutual recognition and facilitating cross-border fund-raising. Harmonisation of rules applying to foundations should be avoided. One respondent expressed doubts as to whether the EFS would have supporters if the fiscal framework conditions are not harmonised at EU level.

A few respondents, mainly from the private sector, considered that the Commission should focus on issues which directly relate to enhancing the competitiveness of profit-making entities and the improvement of the functioning of the internal market.

A few respondents from the public sector pointed to the need to analyse the effectiveness of existing European Statutes before launching the EFS.

27

Question 14 – Modernisation and simplification of European Company Law

Do you agree that there would be added value in modernising and simplifying European Company Law? Please give your reasons.

Are there, in your view, areas of actual or potential overlap between the Action Plan and other initiatives or measures in related sectors? What, if anything, should be done in order to ensure coherence between the various fields of action? Please give your reasons.

What should be the extent of simplification in the interests of improving the regulatory environment and rendering the text more user-friendly? Please give your reasons.

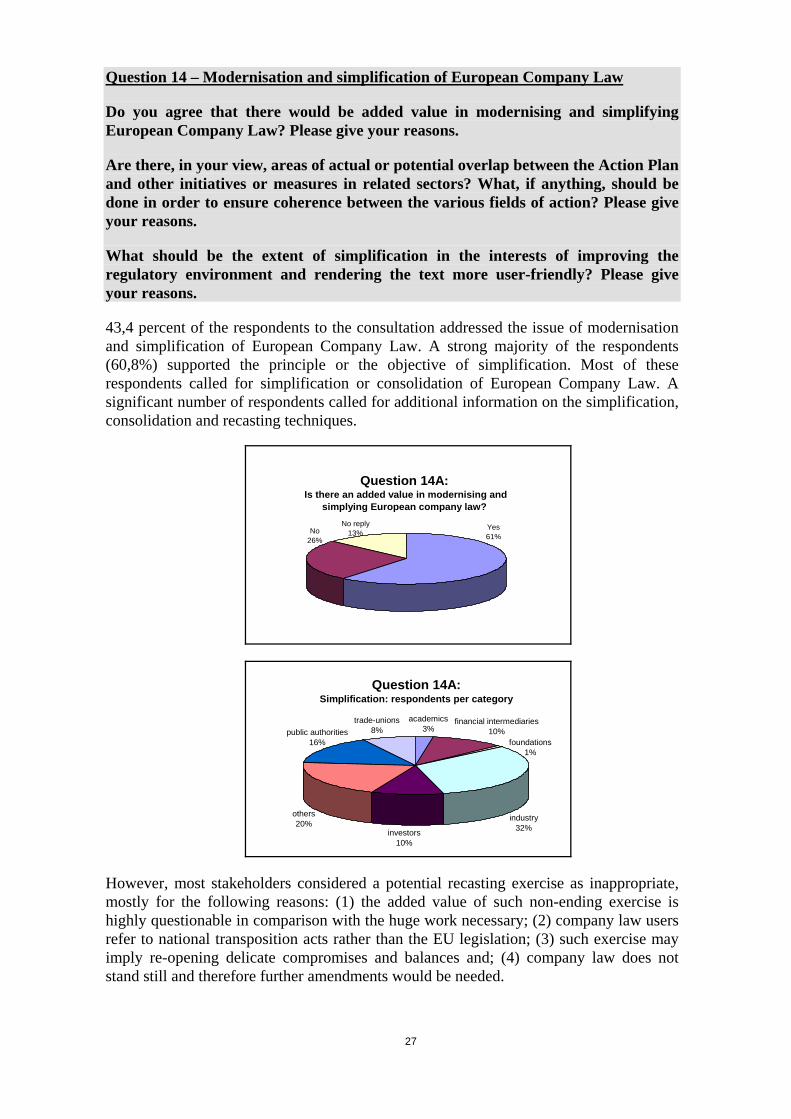

43,4 percent of the respondents to the consultation addressed the issue of modernisation and simplification of European Company Law. A strong majority of the respondents (60,8%) supported the principle or the objective of simplification. Most of these respondents called for simplification or consolidation of European Company Law. A significant number of respondents called for additional information on the simplification, consolidation and recasting techniques.

Question 14A: Is there an added value in modernising and

simplying European company law?

No26%

Yes61%

No reply13%

Question 14A: Simplification: respondents per category

academics3%

investors10%

others20%

industry32%

financial intermediaries10%

foundations1%

trade-unions8%public authorities

16%

However, most stakeholders considered a potential recasting exercise as inappropriate, mostly for the following reasons: (1) the added value of such non-ending exercise is highly questionable in comparison with the huge work necessary; (2) company law users refer to national transposition acts rather than the EU legislation; (3) such exercise may imply re-opening delicate compromises and balances and; (4) company law does not stand still and therefore further amendments would be needed.

28

Only 4,9 percent of the respondents identified areas of actual or potential overlap between the Action Plan and other initiatives or measures. The most commonly quoted actual or potential overlap related to the Directive on takeover bids, the Directive on transparency requirements6 and the Prospectus Directive7. One respondent alleged existing inconsistencies between the IAS Regulation8 and the Company Law Accounting Directives. However, no concrete example of inconsistency between the provisions of the regulation/directives mentioned was reported.

A very small number of respondents submitted ideas on the way to ensure coherence between various actions. One respondent suggested creating a common electronic network grouping useful data on companies in order to improve market transparency.

Finally, 14 percent of the respondents addressed the issue of the extent of a potential simplification. The respondents expressed varying suggestions. Some respondents suggested undertaking a codification in a single directive. Some referred to the European Business Register and the BRITE9 project as concrete initiatives which would simplify the companies' cross-border activities. One respondent suggested concentrating on ensuring a correct implementation of the directives; another one suggested envisaging a Lamfalussy-type framework approach. Finally, one respondent suggested harmonising the differences between the various Directives, in order to improve their readability.

6 Directive 2004/109/EC of the European Parliament and of the Council of 15 December 2004 on the harmonisation of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market and amending Directive 2001/34/EC (OJEU L 390/38, 31/12/2004). 7 Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading and amending Directive 2001/34/EC (OJEU L 345/64, 31/12/2003). 8 Regulation (EC) No 1606/2002 of the European Parliament and of the Council of 19 July 2002 on the application of international accounting standards (OJEC L 243/1, 11/09/2002). 9 Business Register Interoperability Throughout Europe.

29

2. MINUTES OF THE PUBLIC HEARING ON FUTURE PRIORITIES FOR THE ACTION PLAN ON COMPANY LAW AND CORPORATE GOVERNANCE

Around 300 stakeholders participated to the public hearing organised on 3 May in the follow-up to the public consultation on future priorities for the Action Plan on Company Law and Corporate Governance. See programme of the hearing in Annex 2.

Following the opening speech delivered by Mr. Schaub, keynote speaker Mr. Antonio Borges welcomed the Commission's leadership in the quest for better Corporate Governance10. Mr. Borges considered that the Action Plan should focus on everything that leads to powerful externalities at the European level. According to Mr. Borges, "to enhance competition, increased transparency is a must; higher corporate mobility is a strong catalyst; and the simplification of legislation, whenever possible, brings clearer choices for investors and business leaders".

Four panels successively examined the issues of (1) shareholders' rights and obligations, (2) modernisation and simplification of European Company Law, (3) responsibility of directors / internal control and (4) corporate mobility and restructuring.

Panel 1 – Shareholders' rights and obligations

In his introduction, the moderator, Mr. Montagnon, emphasised the importance of the inversed relationship between the accountability of companies to shareholders and the need for regulation. The discussion on the future of the action plan offers an opportunity to act in a different and more efficient path than that followed in the US.

As regards the continued relevance of the Action Plan, Mr. Ross Goobey considered that it had achieved most of its goals. Hence, a "digestion" period would be appropriate. Similarly, Mr. Bouwyn considered that legislation should be a "last resort" instrument.

In this regard, priority should be given, in the short term, to the proposal for a Directive on the exercise of shareholders' rights, the definition of substantial shareholders' rights as mentioned in the consultation document, including the issue of one share – one vote, and the mandatory disclosure of voting policies of institutional investors. According to Mr. Ross Goobey, short term action should focus on stock lending, the identification of "ultimate investor" and shareholders' responsibilities.

Mr. Müller-von Pilchau, from MünchnerRück/Arbeitskreis Namensaktie, expressed the view that the current initiative on shareholders' rights would not have any effect if the EU would not at the same time introduce an obligation for intermediaries to pass on information to and votes from their client to the issuer. Ms. Weber-Rey considered that the EU should rather concentrate on improving the relevant technology in a cross-border context.

As regards the practical exercise of shareholders' rights, Ms. Neuville pointed to several practical difficulties, such as a lack of control of the votes cast in General Meetings or the influence of major shareholders on companies' boards. She denounced existing 10 Speech available at http://ec.europa.eu/internal_market/company/consultation/index_en.htm.

30

practices of protectionism based on the notion of corporate social interest. She questioned the impact of shareholders democracy on shareholders equality, particularly in companies with important institutional investors. Ms; Neuville called for an adaptation of European company law in order to rule new creditors' practices in corporate governance. Deminor considered that it would be important to clarify the concept of 'acting in concert' and define common criteria, so as to avoid imposing an undue obligation on shareholders to launch a bid, when trying to influence the board. The representative of the German Notaries Association (Deutscher Notarverein) pointed out to the practical problems that a general verification of vote counting would create and questioned the need for any such rule.

The issue of shareholder democracy, and in particular one share, one vote gave rise to different opinions. Mr. Bouwyn considered that any action in this field would have to be approached cautiously and would necessitate thorough prior study. Mr. Micossi strongly opposed any EU initiative on shareholder democracy. In his opinion, rights acquired on the market have no relationship with democracy. Existing practices should be respected. In addition, some pyramidal structures could achieve the same effects as multiple voting rights. The European Policy Forum, in the same sense, stated that harmonisation measures on shareholder structures would be more beneficial in practice than the introduction of the one share – one vote principle.

Ms. Weber-Rey focused on shareholder obligations and avoidance of abuse of shareholder rights. Transparency would be the overriding principle and Better Regulation would have to be about achieving transparency and creating a level playing field with minimal interference. Therefore, conceivable measures would lie in the field of a certain disclosure of voting behaviour by institutional investors, a duty for intermediaries and institutional investors to contact the beneficial owners to grant powers of attorney, or to obtain voting instructions, to ask whether the beneficial owners wishes or accepts to be disclosed to the issuer and to offer to inform – upon request – about the votes cast. On the other hand, certain shareholders' rights such as the right to ask questions at general meetings and special investigation rights should be left to the Member States. This view was supported by the BDI representative.

Mr. Massie, representative of the French Corporate Governance Association (Association Française de Gouvernement d'Entreprise) supported the view that the focus would also need to be on shareholders' obligations, in particular to monitor the company's actions throughout the year and to push the alarm button in case of problems. Mr. Montagnon specified that the ICGN Code actually covers such obligations.

Mr Becht, from ECGI (European Corporate Governance Institute), raised the issue of a potential need for a "Lamfalussy process" in the area of corporate governance.

Panel 2: Modernisation and simplification of European company law

The moderator, Ms. Simon, raised the issue of a potential conflict between the regulatory pause called for by many stakeholders and the project of a simplification of existing EU law. She invited the panel members to express their views on such issue as well as on the methods and main beneficiaries of a potential simplification initiative.

She also suggested addressing the following issues: (1) the potential risk of recasting, (2) the necessity to pay more attention to SMEs’ needs, and (3) the usefulness of codification and asked the members of the panel to select one emblematic measure of modernisation of company law.

31

According to Ms. Van den Berghe, simplification might provide an appropriate remedy to face the regulatory fatigue caused by the different layers of regulation (not only hard law but also self regulation, corporate governance codes etc.). The codification of the acquis would improve the readability and clearness of terms and definitions. However, recasting the legislation would risk opening the Pandora's box. To achieve the Lisbon Agenda competitiveness objective, Ms. Van den Berghe proposes to take optimal advantage of the European diversity, within a context of minimal European harmonisation. Rather than imposing a unique corporate governance system in Europe, one should rely on regulatory competition and mutual recognition. Given that each governance model faces specific weaknesses, the EU should make sure that each type of governance model has an - appropriate set of governance mechanisms guaranteeing the necessary countervailing powers and checks and balances. However important self-regulation may be to achieve this goal, one should be aware that self-regulation without any form of supervision is not a workable solution, at least for civil law countries.

According to Mr. Radwan, the usefulness of a simplification exercise would need to be assessed by topic. National transposition measures of European company law are of immediate relevance for the users. In this regard, there are significant differences between Member States, particularly with respect to enforcement and importance of courts (judicial interpretation and legal development). A liberalisation of the legislation would be appreciated, but a complete recasting of existing EU law should be avoided. Future legislation should take account of the ECJ case-law. As regards potential future initiative, the adoption of a statute for a European Private Company would entail significant advantages for SMEs. Easy available and genuinely European legal form is likely to have spill-over effect prompting national lawmakers to be more responsive to entrepreneurs’ needs. In Poland and some other CEE countries the Centros/Inspire Art-doctrine has not attracted enough attention to trigger off discussion capable of challenging entrenched national legal doctrines. Introduction of pan-European legal form would entail imminent confrontation. Another form of inspiring persuasion would be more frequent use of recommendations.