Embed Size (px)

Citation preview

Direct Loan Training

Wood Mason

U.S. Department of Education

Federal Student Aid

770/383-9662

1

What You Need To Know

Systems involvedCOD Common record

SAIGTG Mailbox – D/L Data Services and D/L

Servicing Delinquency Report

G5Funding

Drawdown funds

Return funds

22

What You Need To Know

Some things are the sameVirtually all Title IV regulations

Cash management regulations/policy

Interest rates*

Repayment plans**

Counseling

Promissory Note*FFELP PLUS 8.5%...D/L PLUS 7.9%

**Income Contingent/Alternative Repayment Plan unique to D/L

33

What You Need To Know

Some things are differentActual disbursementOrigination fee/rebate

Funding/Cash

ReconciliationProgram requirement

4

What You Need To Know

Benefits for schoolSingle Lender

Funds obtained from a single source

Processing commonality

One reporting system/database (COD)

One reporting vehicle - Common Record (CR)

5

What You Need To Know

Benefits to borrowersOne lender

Loan benefits unique to D/LPublic Service Repayment benefit

Direct Loan award integrated with other awardsOne source of information – the school

6

What You Need To Know

Keep this in mind…Schools control

Origination & Disbursement• Dates

• Adjustments

• Reduction to $0

Promissory notesOptions

7

Originate

DisburseReconciliation

Direct Loan Processing Cycle

MPN

8

Ent Cslg

What You Need To Know

Direct Loan Origination School determines eligibility Virtually same process as FFELP and Grants Same eligibility criteria

School calculates award Remember same loan types, amounts, and

annual/aggregate limits

School creates or “originates” the award in it’s resident system Originate is an event Create date is the date of origination

9

What You Need To Know

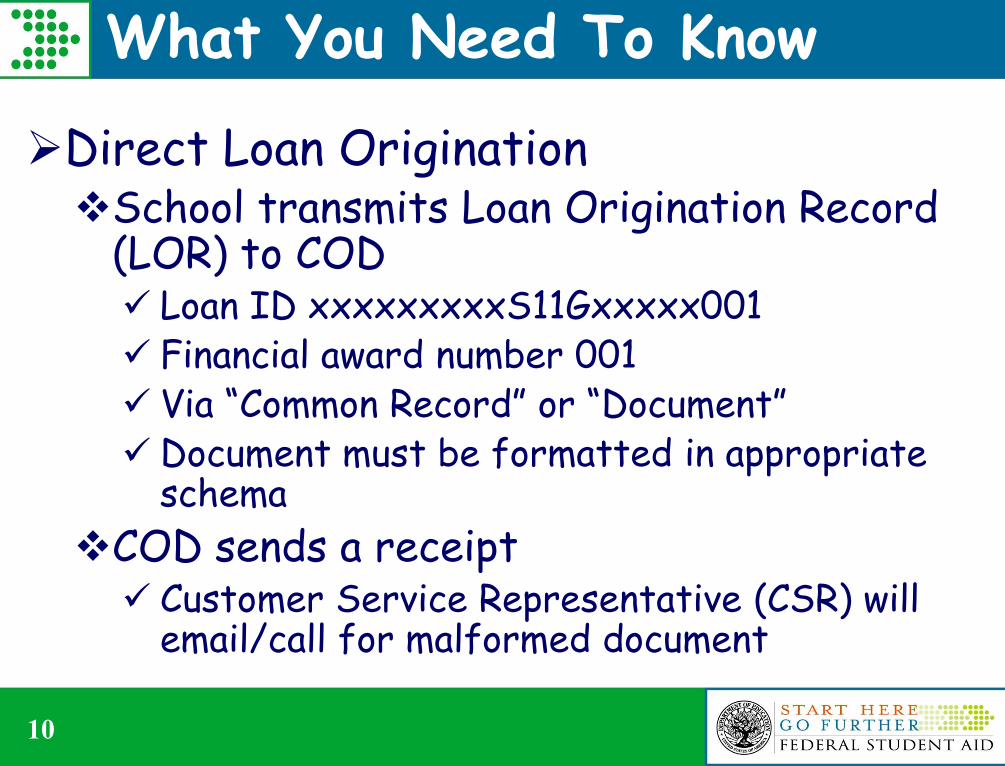

Direct Loan Origination School transmits Loan Origination Record

(LOR) to COD Loan ID xxxxxxxxxS11Gxxxxx001 Financial award number 001 Via “Common Record” or “Document” Document must be formatted in appropriate

schema

COD sends a receipt Customer Service Representative (CSR) will

email/call for malformed document

10

What You Need To Know

Direct Loan OriginationData is sent in “blocks” of informationEach block is reusable in the documentMultiple schools, borrowers, awards,

disbursements, etc

Data is edited in an “hierarchical” mannerData identified as accepted or rejected on

response Hard rejectWarning reject

11

What You Need To Know

Direct Loan OriginationCan be done via batch (Common Record)COD sends a common record response to

each submitted documentOnline individually All data entered field by field Creates loan IDWeb generated response option

12

What To Watch For

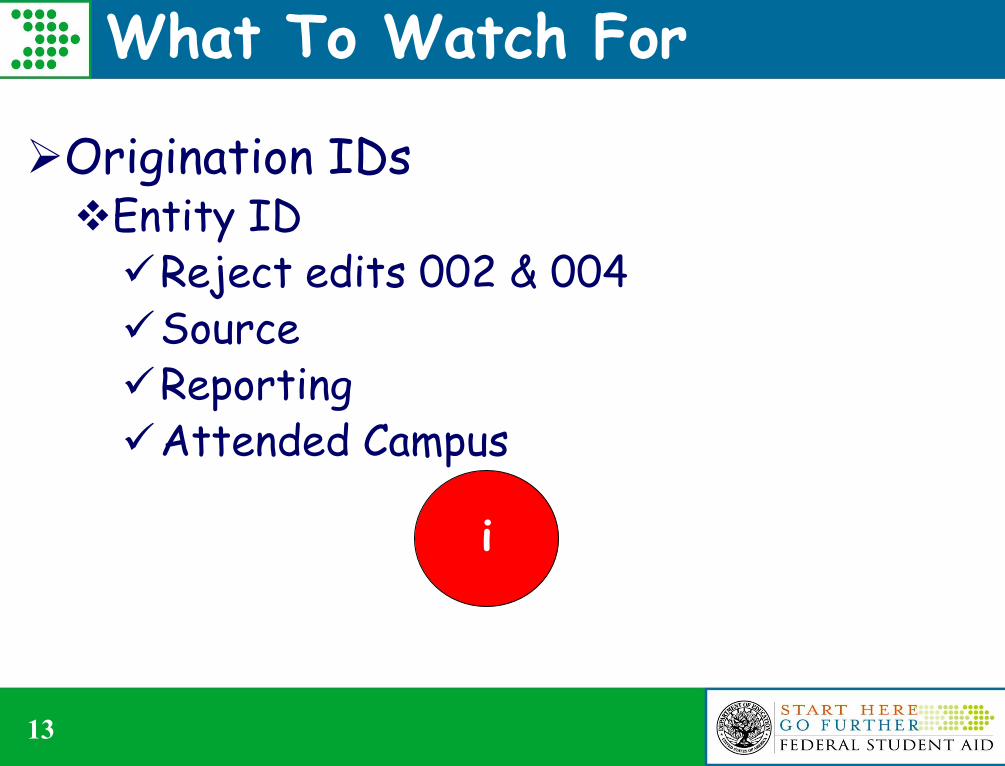

Origination IDsEntity IDReject edits 002 & 004SourceReportingAttended Campus

13

i

What You Need To Know

14

i

University of the Study of Zen & Tai ChiCOD School Id xxxxxxxx

Pell School Id xxxxxx

Direct Loan School Id Gxxxxx

OPE Id 0xxxxx00

GAPS School Id xxxx

DUNS School Id xxxxxxxxx

Previous GAPS Pell School Id Not Applicable

Previous GAPS Direct Loan School

IdNot Applicable

What To Watch For

Direct Loan Origination Duplicate Loan ID Reject edit 031

Abbreviated Applicant File Reject edits 012 & 024 Student identifier match on current SSN,

current DOB and current last name for all submissions

Process to change identifiers D/L second match on SSN, DOB and CPS

transaction number

15

What To Watch For

Direct Loan Origination Anticipated/Actual disbursement data

must = loan amount (reject edit 117)Loan limits (reject edit 039)Exceed Combined Base Limit (reject edit

157) Additional Unsubsidized Eligibility

Complete address (warning edit 120)Citizenship status (reject edit 013 for

PLUS and 014 for Stafford)

16

Person Menu

17

What You Need To Know

18

PLUS loans

What You Need To Know

PLUS loan requires credit checkD/L credit check looks for adverse credit

NOT credit worthinessAbsence of credit is not evidence of

adverse creditBorrower choice of follow-up

EndorserAppeal Pass on PLUS loanNot sure

19

What You Need To Know

PLUS loan requires credit checkCredit decision “stands” for 90 days on

COD websiteDenial linked to academic year submittedApproval linked to submitted loan

FFELP denial for same period of enrollment can offer Unsubsidized funds to now D/L borrower*

*School option

2020

What You Need To Know

PLUS loan requires credit checkSchool processWritten authorization requiredOnline via COD website

• Instant response

Loan Origination Record (LOR)Result returned on CR responseLoan can be accepted and built but credit

reject…edit code #036

21

What You Need To Know

PLUS loan requires credit checkStudentLoans.govSelf servicePLUS loan request includes instant credit

checkSeparate from eMPN for PLUS borrowerOptions for PLUS borrower

• Credit balance• Amount or up to COA• Appeal – Endorser – Pass – Don’t Know

22

What You Need To Know

23

What You Need To Know

24

What To Watch For

Direct Loan adverse credit criteria same as FFELPFFELP lenders could hold PLUS

borrower to higher standard*FICO scoreDebt to income ratioLoan amount

25

*Some borrowers could surprise you and pass the D/L credit check

What To Watch For

PLUS loan “Category of borrower” Reject edits 147, 148, and 149, Parent Graduate student No Grad Stafford requirement

• Must offer/explain

Parent dependent child “pair” uniqueUnique PLUS loan MPN

26

What To Watch For

PLUS loan acceptedAdverse credit decision (reject edit 036) Loan is built Stands for academic year Second Parent credit history not required Can be used for additional dependent child

PLUS loan• CFR 685.203

Credit Override• Successful appeal• Endorser amount

27

Originate

DisburseReconciliation

Direct Loan Processing Cycle

MPN

28

Ent Cslg

What You Need To Know

29

What You Need To Know

All MPNs have a 10-year “life”Paper and electronic

Status/Expiration returned on response file

Actual disbursement within 12 months of receipt at COD extends expiration date

30

What You Need To Know

Multi-year functionalityCan link to any “active” MPN

Single-year functionalityNew MPN each academic year

Single loan MPNEndorsed PLUS loan

MPN status “Inactive” when endorser linked to loan

31

What You Need To Know

eMPNBorrower driven

Fast and accurate

Viewable/retrievable/printable

Instant data to COD from StudentLoans.gov

32

What You Need To Know

Paper MPNCOD can printSend to borrower

Send to school

School can printMust mail to processing center

Must print manifest

Responsible for note

33

What You Need To Know

COD notificationCOD prints paper noteBorrower credit acceptance email

Send email to direct borrower to StudentLoans.gov

15th day send email reminder

30-day and 60-day mailed reminders of no response

34

Search for Promissory Notes

35

What To Watch For

COD will link incoming LOR to MPN with latest expiration date

Loan links to MPN on SSN, DOB and first two characters of first nameSYF school must match Direct Loan

School Code and academic dates

COD will, under certain circumstances, link an actual disbursement to an expired MPN

36

What To Watch For

Multiple MPNs on the COD database not an issue

COD will reject actual disbursement without accepted/linked MPNReject edit 081

MPN IDxxxxxxxxxM11Gxxxxx001

xxxxxxxxxN11Gxxxxx001

37

What To Watch For

MPN status/link and expiration date returned on LOR response“A” accepted

“R” rejected or no MPN on file

“I” inactive

“P” pending note…no LOR on file to link to

38

Originate

DisburseReconciliation

Direct Loan Processing Cycle

MPN

39

EntCslg

What You Need To Know

40

What You Need To Know

Entrance counseling required for first-year, first-time borrowerFFELP counseling will stand for D/L*

Doesn’t have to be ED website/materials

MUST appropriate to loan type/program

SCHOOL determines if counseling is valid or not

*Same loan type

41

What You Need To Know

42

Export Results to .csv Format

What To Watch For

43

Entrance counseling completed

StudentLoans.gov the place to go

Feeds directly to COD

Same loan type

Meets criteria for appropriate program

Person Information

44

Barbara DavisXxxxx123401/01/1900

12 Happy LaneMountain View, GA [email protected](202) 821-3953

Originate

DisburseReconciliation

Direct Loan Processing Cycle

45

What You Need To Know

Pending vs. Actual DisbursementPending disbursement and date is

“anticipated” future disbursement and datePart of LORNo impact on fundingDisbursement Release Indicator = FALSE

No need to change until ready to disburse

46

What You Need To Know

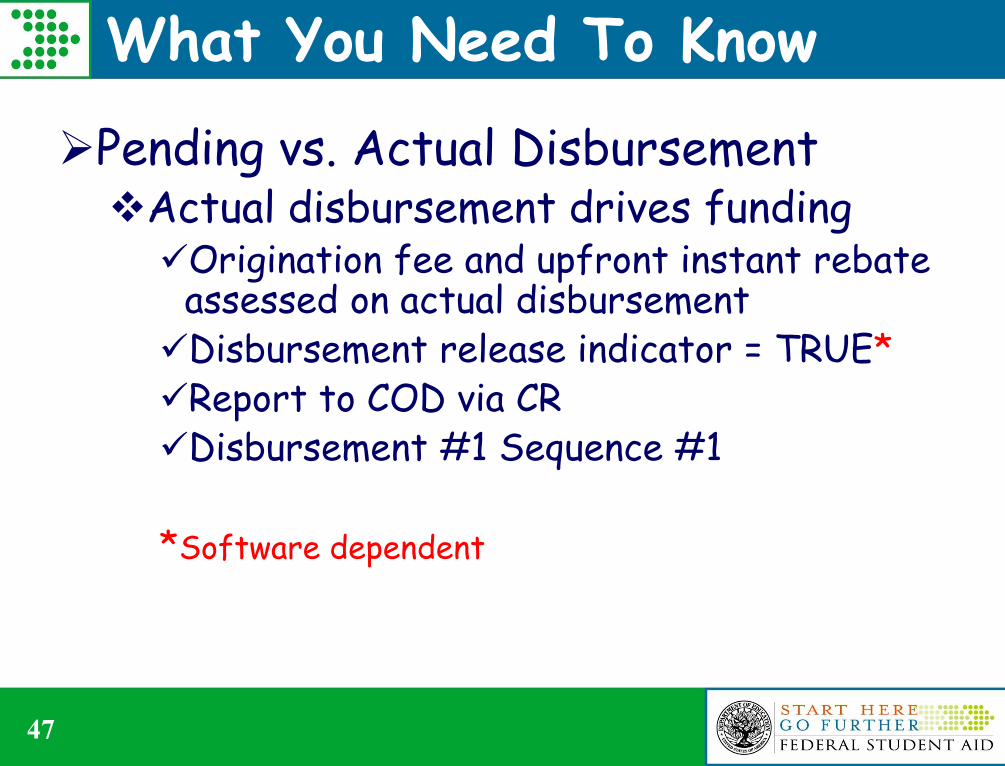

Pending vs. Actual DisbursementActual disbursement drives fundingOrigination fee and upfront instant rebate

assessed on actual disbursementDisbursement release indicator = TRUE*Report to COD via CRDisbursement #1 Sequence #1

*Software dependent

47

What To Watch For

Report ACTUAL DATE OF DISBURSEMENT AND AMOUNTChange if necessaryBorrower requestWithdrawalNo-showMistake

• Date• Amount• Can’t change date and amount in same

transaction

48

What To Watch For

Report ACTUAL DATE OF DISBURSEMENT AND AMOUNTMust report within 30 days of eventWarning edit 055

Can report actual disbursement up to 7 days prior to eventReject edit 050

49

What To Watch For

“Booked” LoanAccepted Origination record, MPN and

1st DisbursementBinding obligation between borrower

and EDBN document type under batch searchSystem generated file on first actual

disbursement only

Liability for funds with ED

50

What To Watch For

Advanced Funded SchoolsCurrent Funding Level (CFL)Corresponding available balance in G5

Calculate immediate needDraw funds from G5Award ID P268K11xxxxNet amountNOT student specific

Flexibility to avoid excess cash

51

Originate

DisburseReconciliation

Direct Loan Processing Cycle

52

Exit Cslg

What You Need To Know

Exit counseling required when no longer attending or drop below half-timeDoesn’t have to be ED website/materials

MUST be appropriate to loan type/program

SCHOOL determines if counseling is valid or not

NSLDS NewsLetter #26

53

What You Need To Know

54

Originate

DisburseReconciliation

Direct Loan Processing Cycle

55

Reconciliation – 3 Key Players

BusinessOffice

FinancialAid

Office

COD

G5

56

Direct Loan Reconciliation

The process by which the Direct Loan Cash Balance recorded on the Department of Education system is reviewed and compared with a school’s internal records on a monthly basisIdentify and resolve discrepancies

Document reasons for their Ending Cash Balance

57

The process by which schools complete final processing at the end of a Direct Loan program year$0 Ending Cash Balance$0 unsubstantiated cash

$0 Unbooked disbursements

* PYCO date July 31st of the year following end of the award year

Program Year Closeout (PYCO)*

58

Tools and Resources

School Account Statement

COD Web site

DL Tools

Student Files

Financial Aid Office Reports

Business Office Reports

59

Tools and Resources

COD School Relations CenterCustomer Service Representative

Issue Resolution Specialists

COD web screensSummary Financial Information

Cash Activity

60

Tools and Resources

COD School Relations CenterWeekly monitoring e-mailsUnsubstantiated cash

30-day reporting monitoring

COD Reconciliation TeamDedicated reconciliation specialists

Problem solving

G5 assistance

61

School Account Statement

Generated on 1st weekend of the monthContains data through end of previous

month

Separate School Account Statement for each open award year

Different report format options

62

School Account Statement

Five Primary SAS ComponentsCash Summary

Disbursement Summary by Loan Type

Cash Detail

Loan Detail - Loan Level

Loan Detail – Disbursement Level

63

64

School Monitoring Email

64

65

School Monitoring

65

66

School Monitoring

66

Program Year Closeout

67

July 31 of the year following the award yearCOD website-balance confirmation

screen

No unsubstantiated cash

No unbooked disbursements

No reporting of disbursements, no draws of cash, no reports

Reopening the year if necessary

67

Balance Confirmation

6868

What To Watch For

69

Work rejected data and submit corrections immediately

Report accurately and timely

Reconcile each and every month

Close your Program Year as soon as possible – DON’T WAIT UNTIL NEXT YEAR!

69

Originate

DisburseServicing

Direct Loan Processing Cycle

70

What You Need To Know

Slide 71

Contracted 4 additional Servicers for incoming volumeACS (Current Servicer)NelnetSallie MaeGreat Lakes Education Loan ServicesFedLoan Servicing (PHEAA)

COD generated D/Ls distributed at booking

71

What You Need To Know

Slide 72

Performance via competitionServicers are rewarded for providing

excellent default aversion techniques that deliver the desired results

Allocation of volume is performance based % of “In Repayment” Portfolio Dollars that go

into default % of unique “In Repayment” Portfolio

borrowers that go into defaultBorrower/school/FSA surveys

72

What You Need To Know

Slide 73

Will schools work with multiple Servicers?Yes, but FSA will attempt to keep your

borrowers “whole”

Will reports/reporting vary from Servicer to Servicer?Yes…we have chosen to allow the

Servicers to uniquely “brand”

73

What You Need To Know

Slide 74

Can a school select the Servicer with whom they wish to work?No. Loans will be dispersed to all

Servicers systemically as they book

How will a school know which Servicer has a particular loan?By looking at the loan in NSLDS

74

What You Need To Know

Borrower Services

Date due flexibility for all repayment plans

Electronic billing/correspondence

EDA and on-line payment options

Self-Service tools for borrowers

75

What You Need To Know

Slide 76

Default/Delinquency ManagementDedicated services to assist schools

with Cohort Default RateExceeds minimum regulatory due diligence requirementsEducates and informs borrowers as to the tools and options available to assist them in the management of their student loans

76

What You Need To Know

Slide 77

Default/Delinquency ManagementProvides outbound targeted calling campaigns along with inbound call center representatives to help borrowers become current Utilizes electronic communication methods such as email to keep borrowers informed about account status

77

What You Need To Know

Slide 78

Default/Delinquency ManagementDefault management results publishedServicers will partner with financial

literacy advocacy groups to educate borrowers and assist schools

Each servicer is encouraged to continually improve and compete among one another to deliver the best results for borrowers, schools, and FSA

78

Servicing FutureServicer SchoolContact

Borrower Contact

FedLoan Servicing (PHEAA)

NSLDS Servicer Code: 700579

School Phone:

800-655-3813

Web: www.myfedloan.org

Borrower Phone:

800-699-2908

Web: www.myfedloan.org

Great Lakes Educational Loan Services

NSLDS Servicer Code: 700581

School Phone:

888-686-6919

Web: www.mygreatlakes.org

Borrower Phone:

800-236-4300

Web: www.mygreatlakes.org

Nelnet

NSLDS Servicer Code: 700580

School Phone:

866-463-5638

Web: www.nelnet.com

Borrower Phone:

888-486-4722

Web: www.nelnet.com

Sallie Mae

NSLDS Servicer Code: 700578

School Phone:

888-272-4665Web:

www.opennet.salliemae.com

Borrower Phone:

800-722-1300

Web: www.salliemae.com79

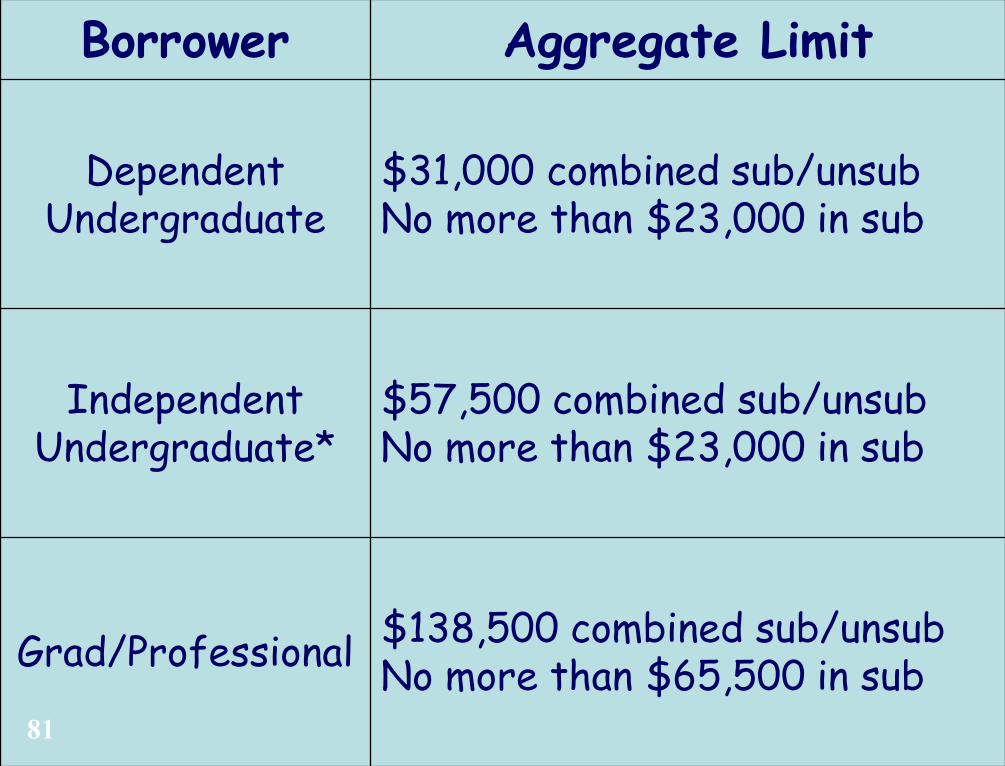

Annual Loan Limits

YearDependent

Undergraduate

Independent Undergraduate

And Dep. Undergrad whose parent can’t borrow PLUS

Graduate/ Professional

1st $5,500(maximum $3,500

subsidized)

$9,500(maximum $3,500

subsidized)

Up to $20,500 each academic year

(maximum $8,500 subsidized)

2nd $6,500(maximum $4,500

subsidized)

$10,500(maximum $4,500

subsidized)

3rd and Beyond

$7,500(maximum $5,500

subsidized)

$12,500(maximum $5,500

subsidized)

Aggregate Loan LimitsBorrower Aggregate Limit

Dependent Undergraduate

$31,000 combined sub/unsubNo more than $23,000 in sub

IndependentUndergraduate*

$57,500 combined sub/unsubNo more than $23,000 in sub

Grad/Professional$138,500 combined sub/unsubNo more than $65,500 in sub

81

Interest RatesDirect Subsidized Loans for Undergraduate Borrowers

1st DisbursedOn or After

And Before Interest Rate

July 1, 2009 July 1, 2010 5.6%

July 1, 2010 July 1, 2011 4.5%

July 1, 2011 July 1, 2012 3.4%

All Other Direct Subsidized and Unsubsidized Loans 6.8%

Direct PLUS for Parents and Grad/Professional Students

7.9%

Direct ConsolidationWeightedAverage

8.25% Cap82

What You Need To Know

83