Embed Size (px)

Citation preview

Diminished Capacity: How to Deal with the Emerging

Regulatory Structure

Jonathan Cyprys – Associate, Greenberg Traurig, LLP

Ben Marzouk – Associate, Sutherland Asbill & Brennan LLP

Louis Dempsey – President, Renaissance Regulatory Services, Inc.

Overview Background

Comparison of:

◦ NASAA Model Act to Protect Seniors and Vulnerable Adults

◦ Proposed FINRA Rules 4512 & 2165

◦ Senior Safe Act

◦ Chapter 415 of FL Statutes – Adult Protective Services

Training Registered Representatives

◦ SEC and FINRA National Senior Initiative

◦ IRA Rollovers

Implementing Firm Policies

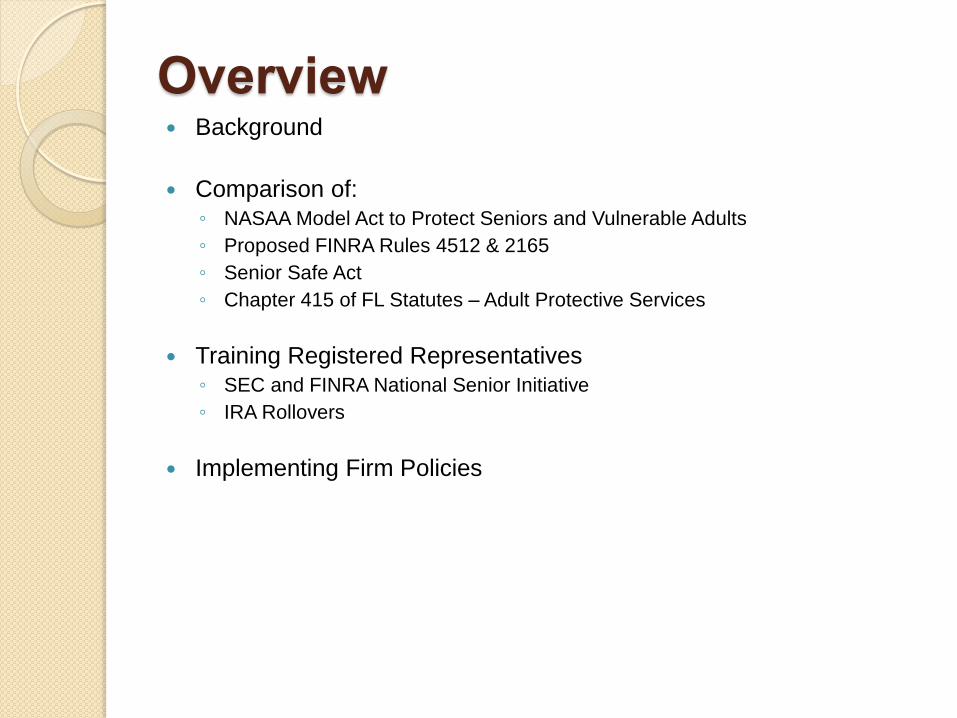

Background How did we get here?

◦ 2013 - 44.7MM people

reported to be over 65+

82.3MM by 2040

◦ 2012 - 86% of seniors reported

social security as primary

source of income

◦ Risk investing in retirement

accounts

◦ Fewer employer pensions

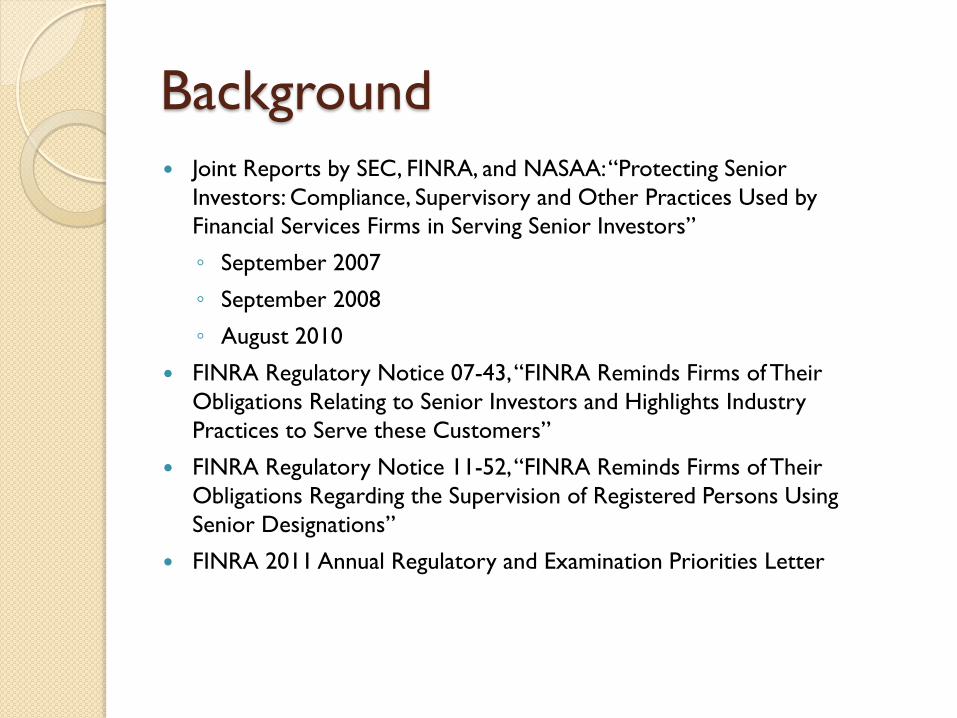

Background

Joint Reports by SEC, FINRA, and NASAA: “Protecting Senior

Investors: Compliance, Supervisory and Other Practices Used by

Financial Services Firms in Serving Senior Investors”

◦ September 2007

◦ September 2008

◦ August 2010

FINRA Regulatory Notice 07-43, “FINRA Reminds Firms of Their

Obligations Relating to Senior Investors and Highlights Industry

Practices to Serve these Customers”

FINRA Regulatory Notice 11-52, “FINRA Reminds Firms of Their

Obligations Regarding the Supervision of Registered Persons Using

Senior Designations”

FINRA 2011 Annual Regulatory and Examination Priorities Letter

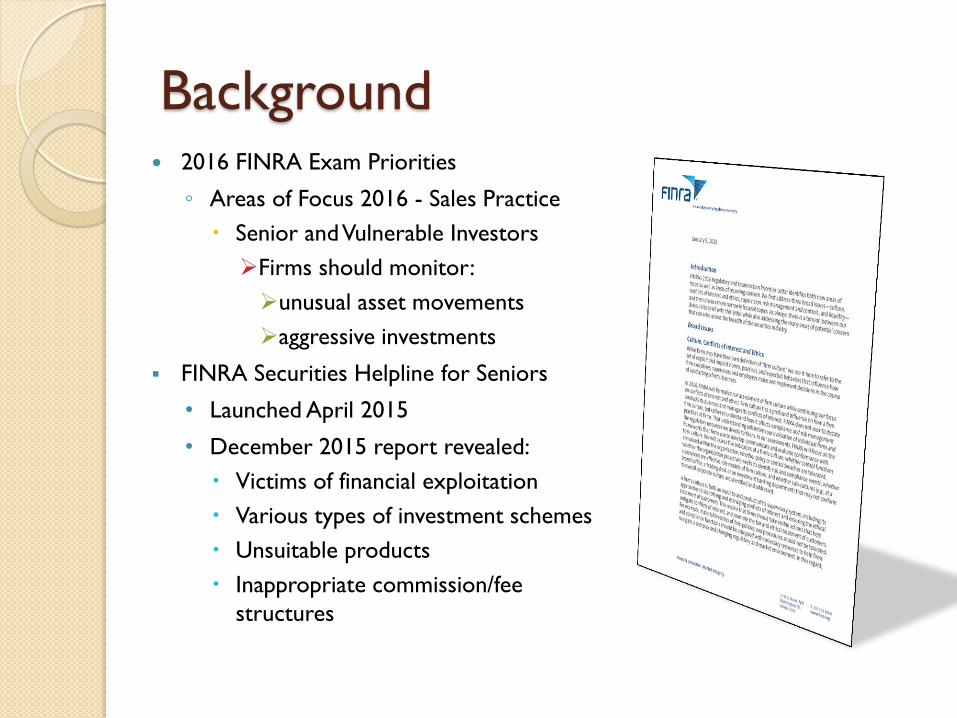

Background 2016 FINRA Exam Priorities

◦ Areas of Focus 2016 - Sales Practice

Senior and Vulnerable Investors

Firms should monitor:

unusual asset movements

aggressive investments

FINRA Securities Helpline for Seniors

• Launched April 2015

• December 2015 report revealed:

Victims of financial exploitation

Various types of investment schemes

Unsuitable products

Inappropriate commission/fee

structures

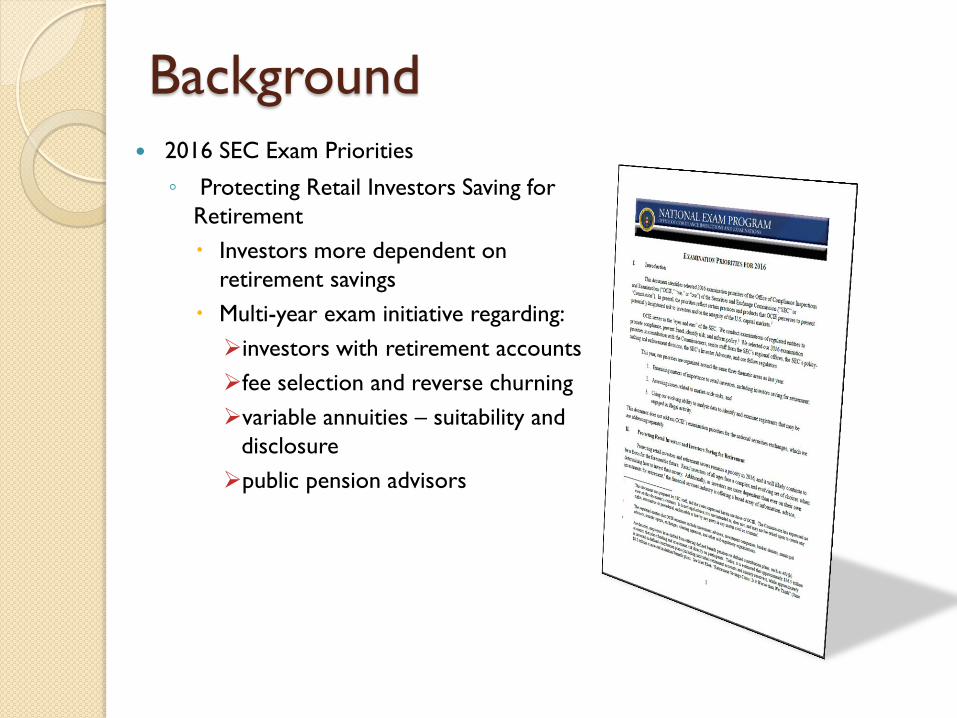

Background 2016 SEC Exam Priorities

◦ Protecting Retail Investors Saving for

Retirement

Investors more dependent on

retirement savings

Multi-year exam initiative regarding:

investors with retirement accounts

fee selection and reverse churning

variable annuities – suitability and

disclosure

public pension advisors

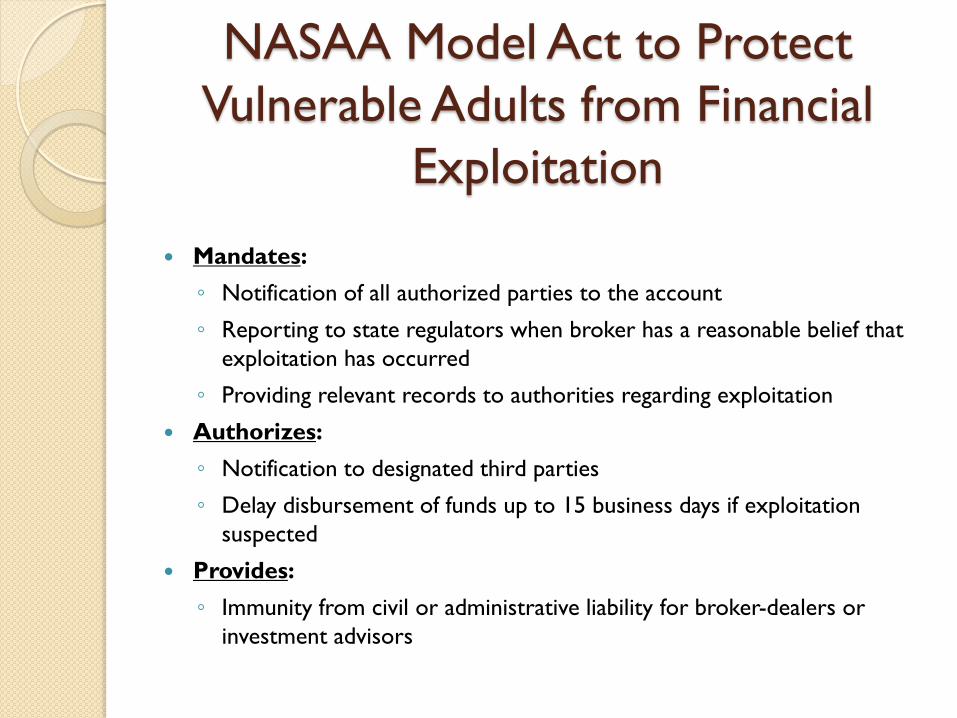

NASAA Model Act to Protect

Vulnerable Adults from Financial

Exploitation

Mandates:

◦ Notification of all authorized parties to the account

◦ Reporting to state regulators when broker has a reasonable belief that

exploitation has occurred

◦ Providing relevant records to authorities regarding exploitation

Authorizes:

◦ Notification to designated third parties

◦ Delay disbursement of funds up to 15 business days if exploitation

suspected

Provides:

◦ Immunity from civil or administrative liability for broker-dealers or

investment advisors

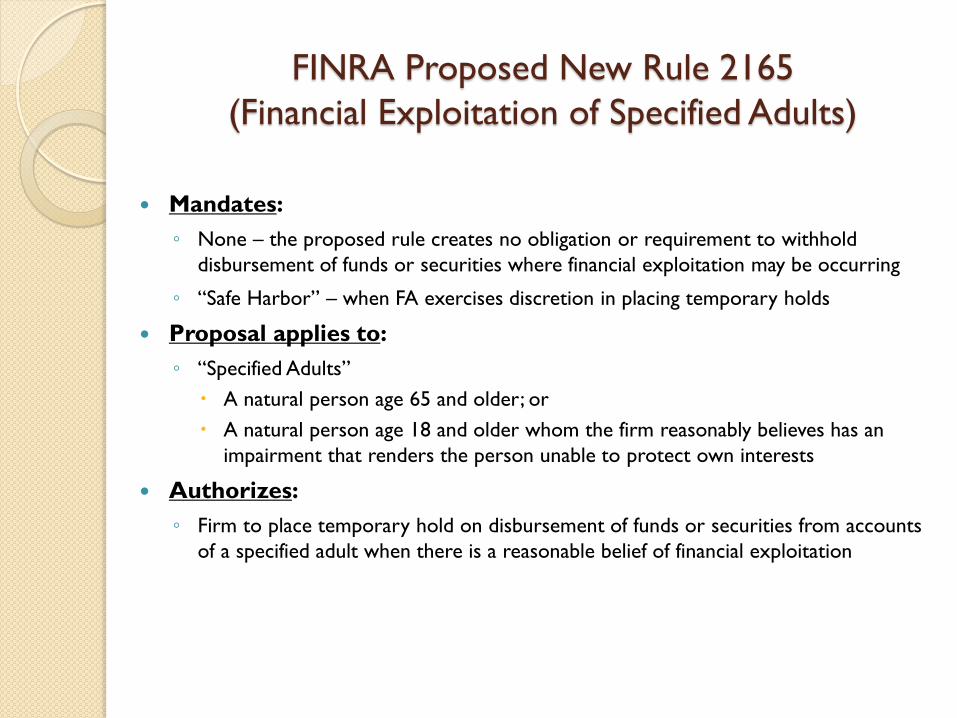

FINRA Proposed New Rule 2165

(Financial Exploitation of Specified Adults)

Mandates:

◦ None – the proposed rule creates no obligation or requirement to withhold

disbursement of funds or securities where financial exploitation may be occurring

◦ “Safe Harbor” – when FA exercises discretion in placing temporary holds

Proposal applies to:

◦ “Specified Adults”

A natural person age 65 and older; or

A natural person age 18 and older whom the firm reasonably believes has an

impairment that renders the person unable to protect own interests

Authorizes:

◦ Firm to place temporary hold on disbursement of funds or securities from accounts

of a specified adult when there is a reasonable belief of financial exploitation

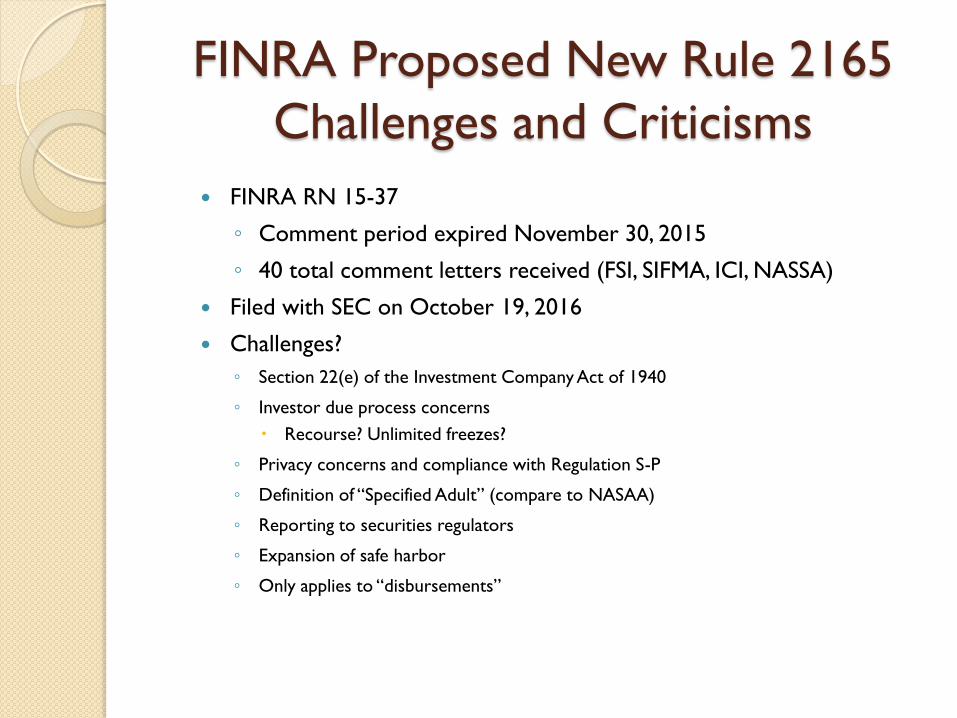

FINRA Proposed New Rule 2165

Challenges and Criticisms

FINRA RN 15-37

◦ Comment period expired November 30, 2015

◦ 40 total comment letters received (FSI, SIFMA, ICI, NASSA)

Filed with SEC on October 19, 2016

Challenges?

◦ Section 22(e) of the Investment Company Act of 1940

◦ Investor due process concerns

Recourse? Unlimited freezes?

◦ Privacy concerns and compliance with Regulation S-P

◦ Definition of “Specified Adult” (compare to NASAA)

◦ Reporting to securities regulators

◦ Expansion of safe harbor

◦ Only applies to “disbursements”

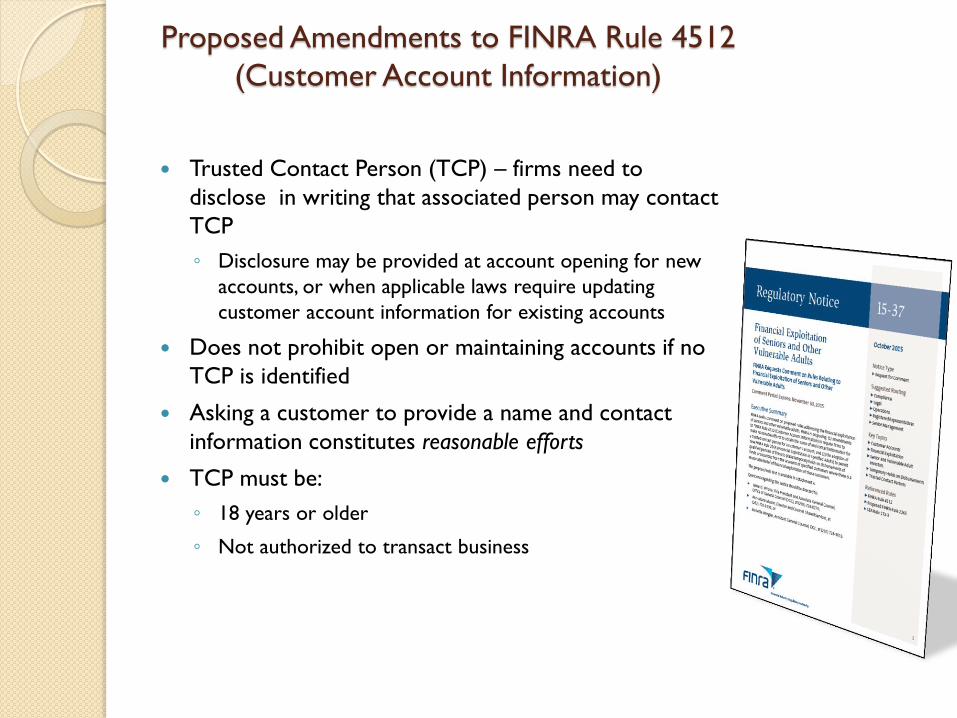

Proposed Amendments to FINRA Rule 4512

(Customer Account Information)

Trusted Contact Person (TCP) – firms need to

disclose in writing that associated person may contact

TCP

◦ Disclosure may be provided at account opening for new

accounts, or when applicable laws require updating

customer account information for existing accounts

Does not prohibit open or maintaining accounts if no

TCP is identified

Asking a customer to provide a name and contact

information constitutes reasonable efforts

TCP must be:

◦ 18 years or older

◦ Not authorized to transact business

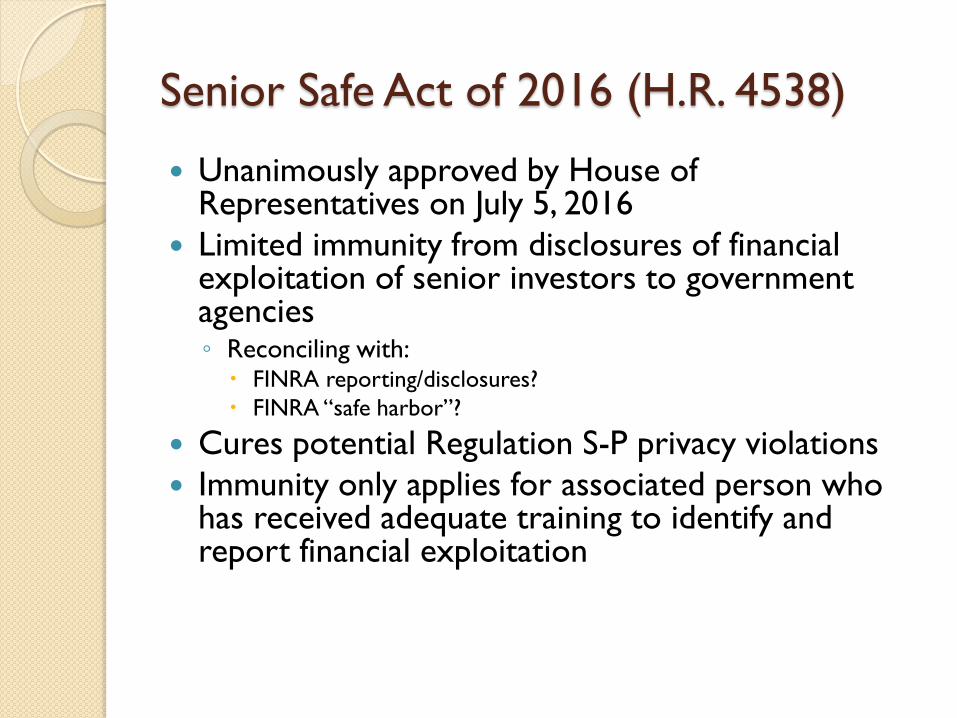

Senior Safe Act of 2016 (H.R. 4538)

Unanimously approved by House of Representatives on July 5, 2016

Limited immunity from disclosures of financial exploitation of senior investors to government agencies ◦ Reconciling with:

FINRA reporting/disclosures?

FINRA “safe harbor”?

Cures potential Regulation S-P privacy violations

Immunity only applies for associated person who has received adequate training to identify and report financial exploitation

Chapter 415 of FL Statutes: Adult Protective Services Act

Mandates:

◦ Reporting any neglect, abuse and exploitation of vulnerable adults

Exploitation means a person who:

◦ Stands in a position of trust with a vulnerable adult; and

◦ Knowingly by deception obtains a vulnerable adult’s assets or property with

◦ Intent to deprive a vulnerable adult of the use or benefit of assets or property

Exploitation may include:

◦ Breaches of fiduciary duty, unauthorized taking of personal assets, misappropriation, and misuse of money belonging to a vulnerable adult

Vulnerable Adult – 18 or older whose ability to perform normal activities is impaired

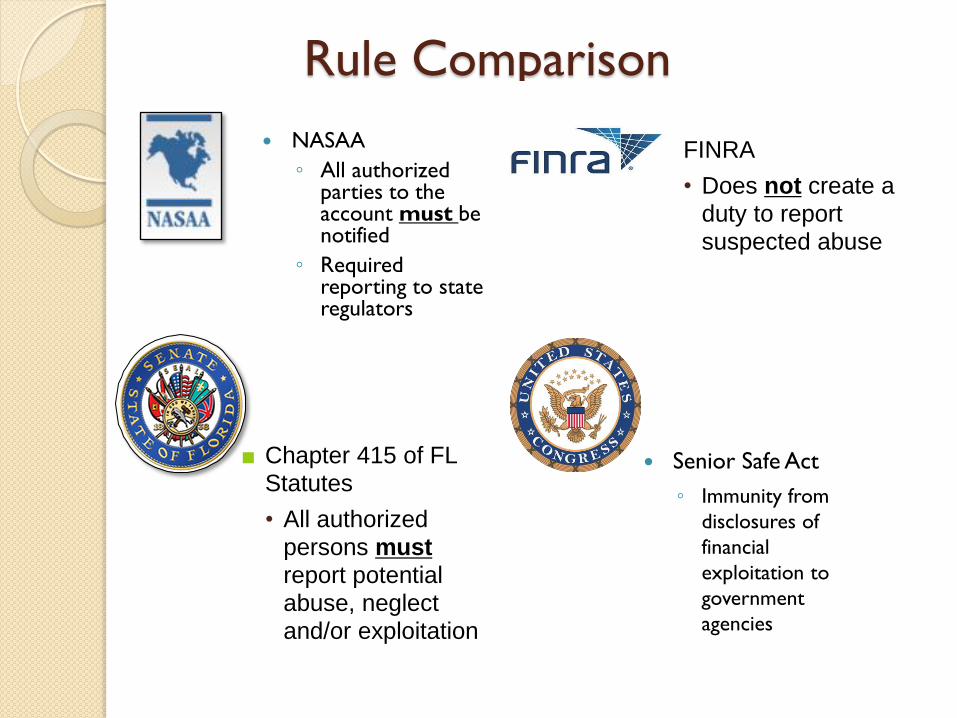

Rule Comparison

NASAA

◦ All authorized parties to the account must be notified

◦ Required reporting to state regulators

■ Chapter 415 of FL Statutes

• All authorized persons must report potential abuse, neglect and/or exploitation

■ FINRA

• Does not create a duty to report suspected abuse

Senior Safe Act

◦ Immunity from

disclosures of

financial

exploitation to

government

agencies

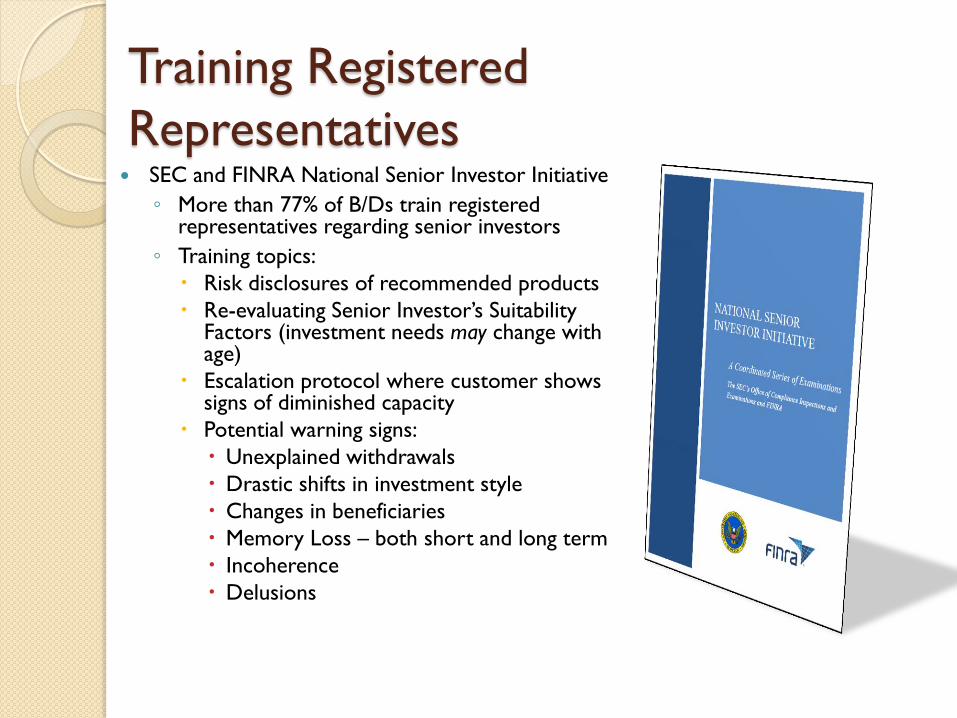

Training Registered

Representatives SEC and FINRA National Senior Investor Initiative

◦ More than 77% of B/Ds train registered representatives regarding senior investors

◦ Training topics:

Risk disclosures of recommended products

Re-evaluating Senior Investor’s Suitability Factors (investment needs may change with age)

Escalation protocol where customer shows signs of diminished capacity

Potential warning signs:

Unexplained withdrawals

Drastic shifts in investment style

Changes in beneficiaries

Memory Loss – both short and long term

Incoherence

Delusions

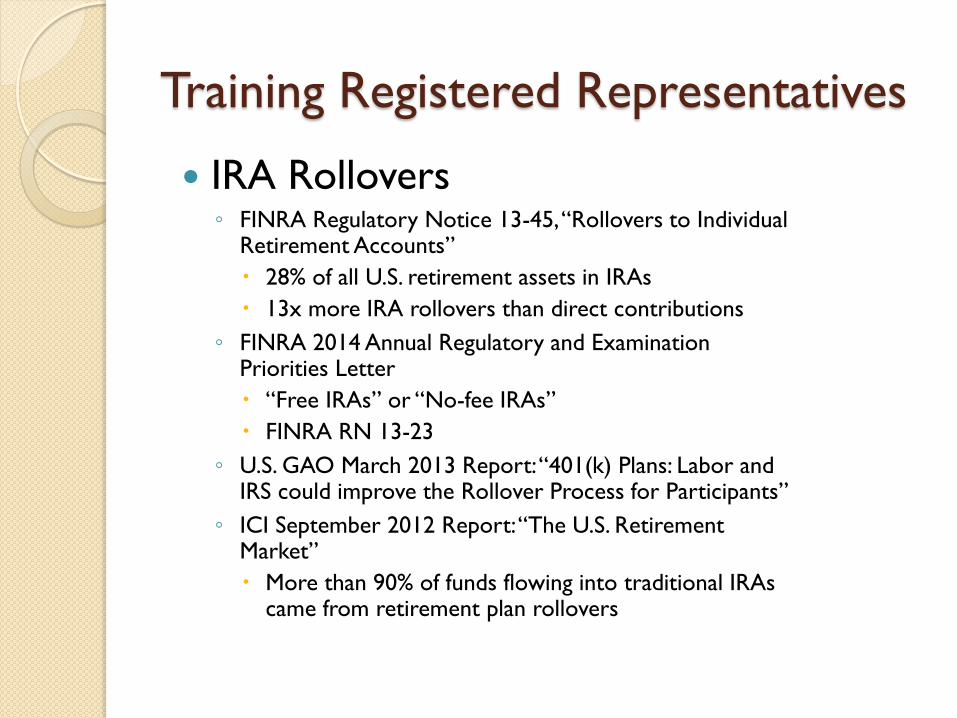

Training Registered Representatives

IRA Rollovers ◦ FINRA Regulatory Notice 13-45, “Rollovers to Individual

Retirement Accounts”

28% of all U.S. retirement assets in IRAs

13x more IRA rollovers than direct contributions

◦ FINRA 2014 Annual Regulatory and Examination Priorities Letter

“Free IRAs” or “No-fee IRAs”

FINRA RN 13-23

◦ U.S. GAO March 2013 Report: “401(k) Plans: Labor and IRS could improve the Rollover Process for Participants”

◦ ICI September 2012 Report: “The U.S. Retirement Market”

More than 90% of funds flowing into traditional IRAs came from retirement plan rollovers

Training Registered Representatives

Training

◦ Investment Options – low cost funds may not offer array of

investments

◦ Fees and Expenses – (i) investment-related expenses and (ii) plan

or account fees

◦ Services – investment advice, planning tools, telephone help lines

and educational materials

◦ Penalty-Free Withdrawals (ages 55 – 59 ½) may be able to take

withdrawals

◦ Protection from creditors and legal judgments

◦ Required minimum distributions

◦ Rolling over employer related stock

Potential Elder Abuse Red Flag

◦ Changes in IRA beneficiaries and/or investment behavior

Firm Policy re: Diminished Capacity

and Elder Abuse Communicate to all employees the firm’s diminished capacity policy

Employees bring to the attention of the CCO any trigger event that

indicates a client is of diminished capacity

Employees document their communications with clients affected by

diminished capacity

Employees provide written follow up of discussions to client and any

designated person

CCO determines if monitoring of transactions is warranted

The firm documents and reviews its Investment Policy Statement annually

with client

Firm Policy re: Diminished Capacity

and Elder Abuse Employees document and report to CCO any suspicious activity that may

indicate elder abuse (multiple withdrawals, new beneficiaries)

CCO reviews the suspicious incident and seeks outside counsel if he/she

feels the client may be a victim of elder financial abuse

Potential Litigation

◦ If you are aggressive or non-responsive, for

example, the plaintiff bar is preparing to sue

you either way.

◦ How do you protect yourself?

Internal controls

Escalation when “red flags” occur

Get help from others and document the process

Protection of Seniors

There are numerous statutes protecting Seniors.

What do you do when a Senior has capacity issues but does not want any

help?

What Happens when the Senior refuses to diversify or make “appropriate”

investment?

Medical laws and privacy issues

Extreme protection of the elderly can have unforeseen (other) adverse

consequences.

Seek help early when there are potential issues or red flags.