Embed Size (px)

Citation preview

2

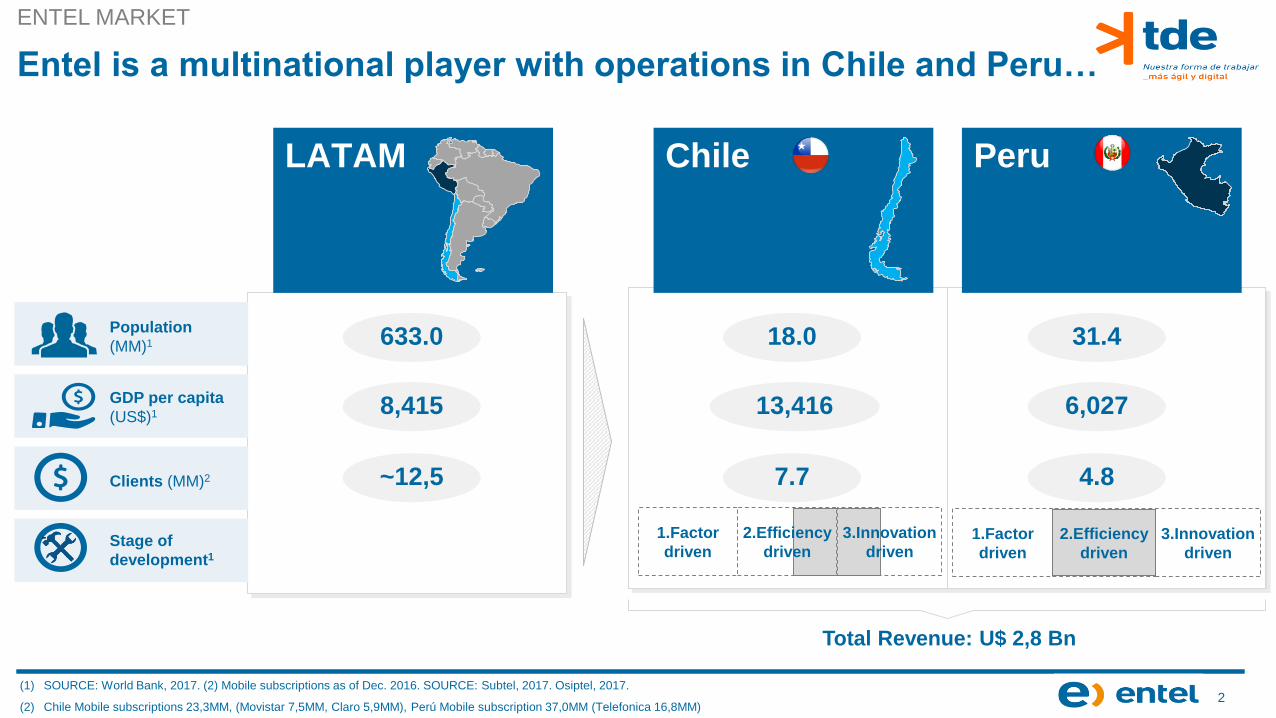

Entel is a multinational player with operations in Chile and Peru…

Population

(MM)1

GDP per capita

(US$)1

Stage of

development1

Clients (MM)2

-

18.0

13,416

31.4

6,027

2.Efficiency

driven

1.Factor

driven

3.Innovation

driven2.Efficiency

driven

1.Factor

driven

3.Innovation

driven

7.7 4.8

Chile Peru

Total Revenue: U$ 2,8 Bn

633.0

8,415

LATAM

ENTEL MARKET

~12,5

(1) SOURCE: World Bank, 2017. (2) Mobile subscriptions as of Dec. 2016. SOURCE: Subtel, 2017. Osiptel, 2017.

(2) Chile Mobile subscriptions 23,3MM, (Movistar 7,5MM, Claro 5,9MM), Perú Mobile subscription 37,0MM (Telefonica 16,8MM)

3SOURCE: Entel activity 2015, 1 TOP 10 - Banco CHILE, Banco ESTADO, Banco SCOTIABANK, Banco BCI, Banco Internacional, Carabineros de Chile, Falabella, Caja los Heroes, PDI, Correos

de Chile

…with a solid position in Chile and high growth in Peru market

ENTEL MARKET

Chile Peru

Segments and

servicesLeadership in Chile High Growth in Peru

Solid position

Solid position

B2C Business to

consumer

B2B Small Medium

Enterprises

B2B Corporations

Fixed Mobile FTTH

Fixed Mobile Data center/ICT1

Fixed Mobile Mobile

Mobile

Call centers

Data center/ICT

4

Why the transformation?

5

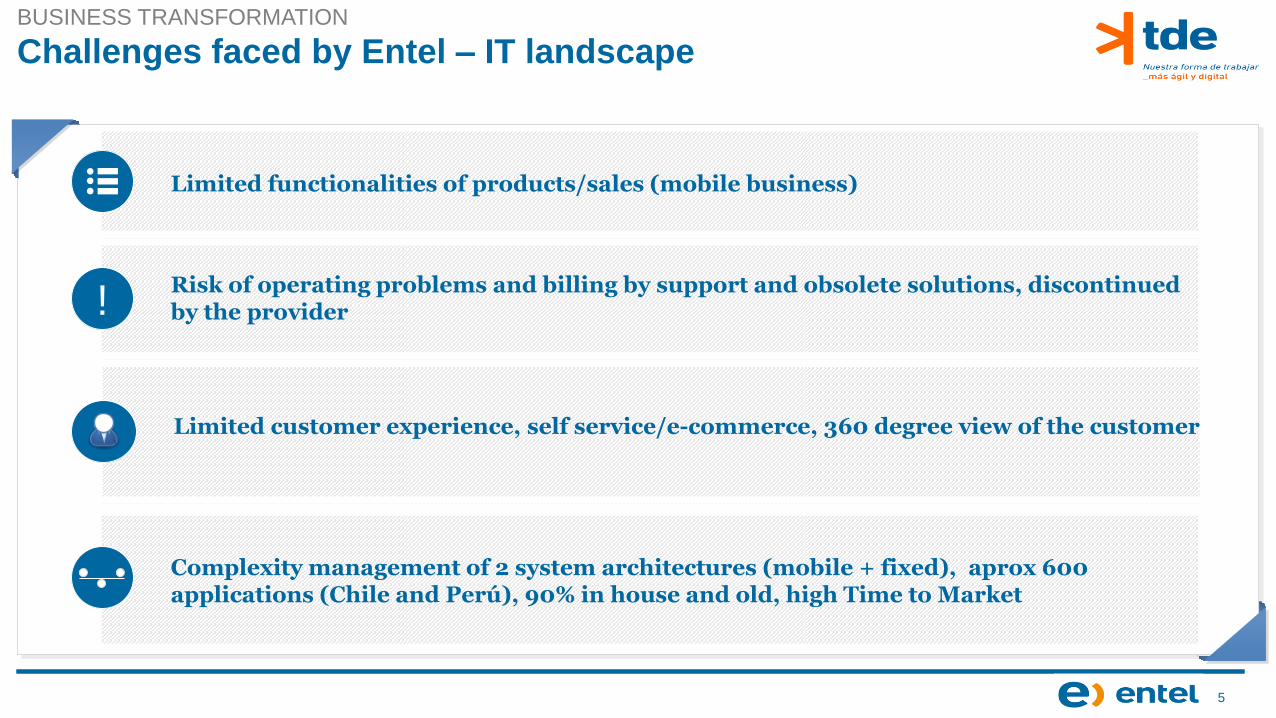

Challenges faced by Entel – IT landscapeBUSINESS TRANSFORMATION

Complexity management of 2 system architectures (mobile + fixed), aprox 600 applications (Chile and Perú), 90% in house and old, high Time to Market

Risk of operating problems and billing by support and obsolete solutions, discontinued by the provider!

Limited functionalities of products/sales (mobile business)

Limited customer experience, self service/e-commerce, 360 degree view of the customer

6

Bajar este video de youtube y dejarlo inserto en la ppt, es pesado para enviarlo por mail

https://www.youtube.com/watch?v=kTns6U8uoXA

71 netizens commonnly known as cybercitizens (network citizens)

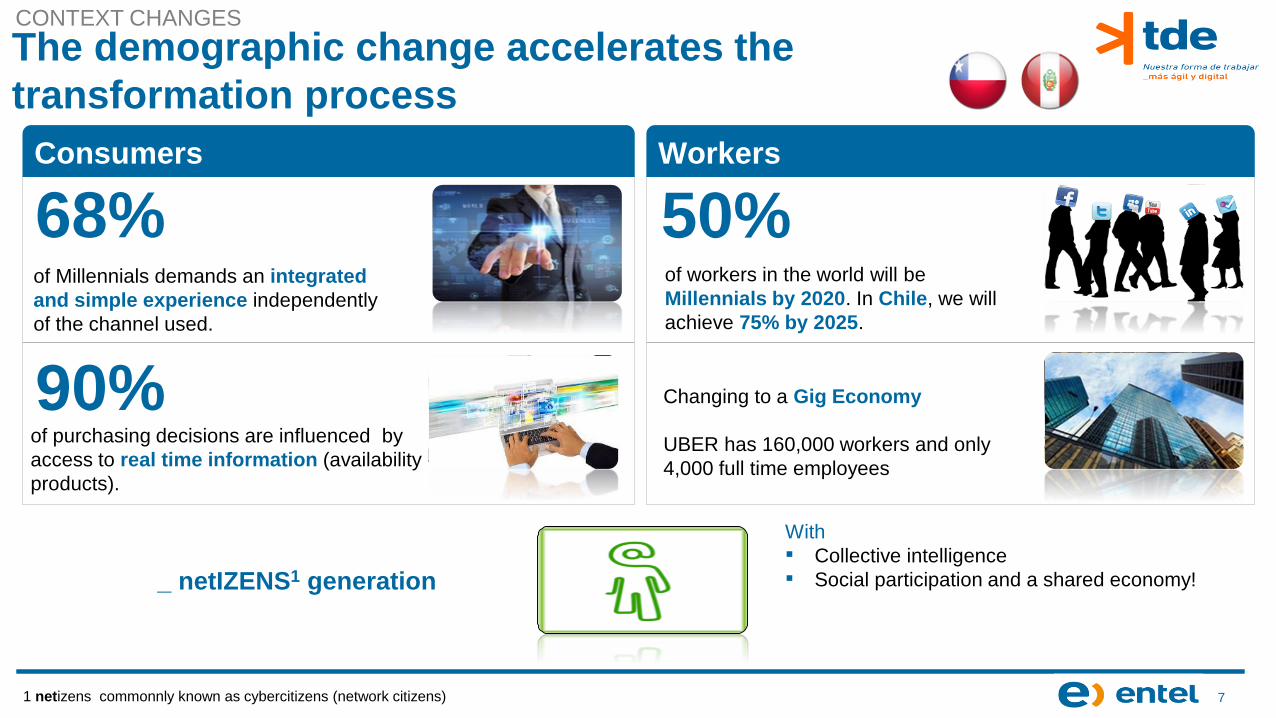

The demographic change accelerates the

transformation process

Consumers Workers

68%of Millennials demands an integrated

and simple experience independently

of the channel used.

Changing to a Gig Economy

UBER has 160,000 workers and only

4,000 full time employees

50%of workers in the world will be

Millennials by 2020. In Chile, we will

achieve 75% by 2025.

90%of purchasing decisions are influenced by

access to real time information (availability -

products).

_ netIZENS1 generation

With

▪ Collective intelligence

▪ Social participation and a shared economy!

CONTEXT CHANGES

8

Our Transformation

challenges

9

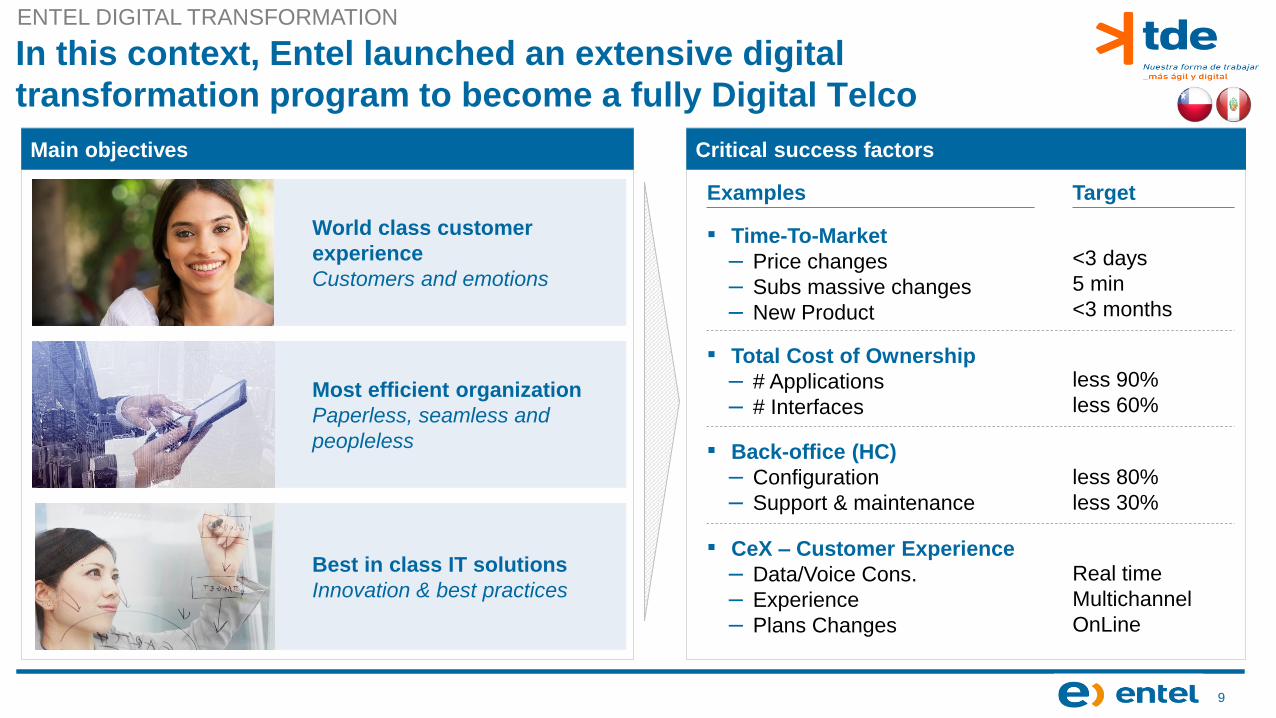

In this context, Entel launched an extensive digital

transformation program to become a fully Digital Telco

Target

▪ Time-To-Market

– Price changes

– Subs massive changes

– New Product

<3 days

5 min

<3 months

▪ Total Cost of Ownership

– # Applications

– # Interfaces

less 90%

less 60%

▪ CeX – Customer Experience

– Data/Voice Cons.

– Experience

– Plans Changes

Real time

Multichannel

OnLine

Examples

▪ Back-office (HC)

– Configuration

– Support & maintenance

less 80%

less 30%

ENTEL DIGITAL TRANSFORMATION

Critical success factorsMain objectives

Best in class IT solutions

Innovation & best practices

Most efficient organization

Paperless, seamless and

peopleless

World class customer

experience

Customers and emotions

10

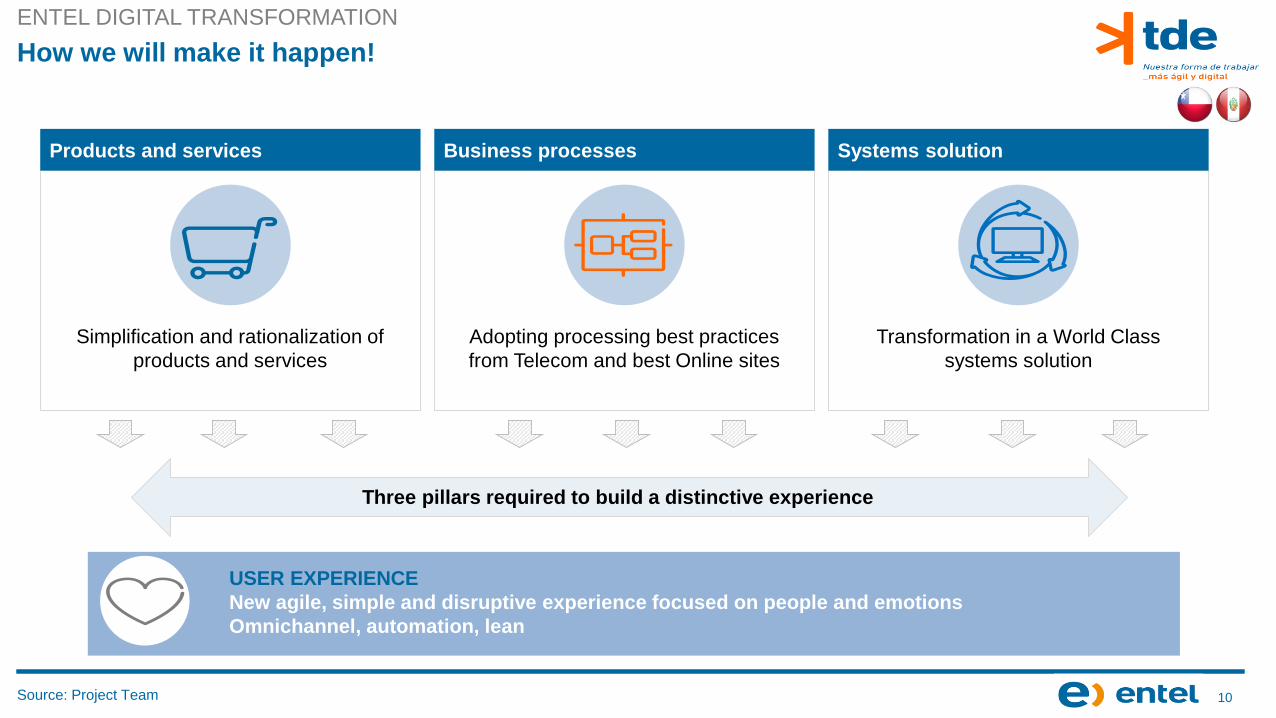

Products and services Business processes Systems solution

Source: Project Team

How we will make it happen!

ENTEL DIGITAL TRANSFORMATION

USER EXPERIENCE

New agile, simple and disruptive experience focused on people and emotions

Omnichannel, automation, lean

Simplification and rationalization of

products and services

Adopting processing best practices

from Telecom and best Online sites

Transformation in a World Class

systems solution

Three pillars required to build a distinctive experience

12SOURCE: Project team

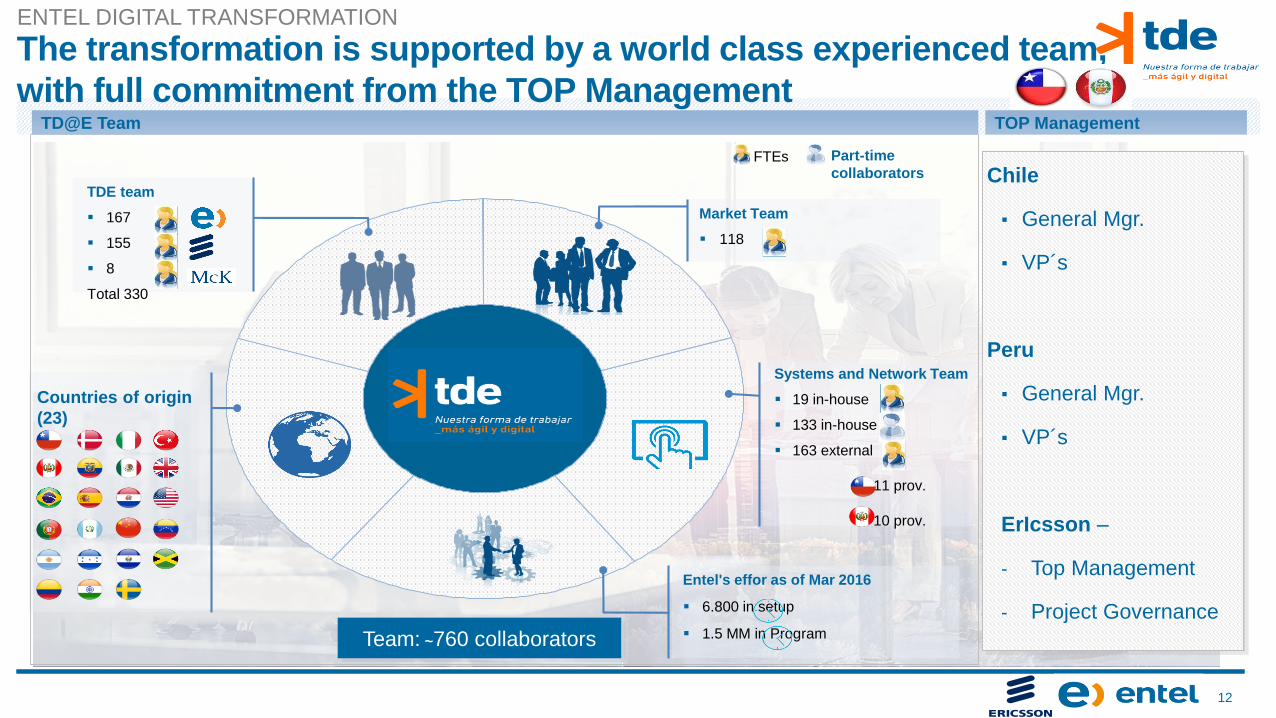

Entel's effor as of Mar 2016

6.800 in setup

1.5 MM in Program

TDE team

167

155

8

Total 330

Systems and Network Team

19 in-house

133 in-house

163 external

- 11 prov.

- 10 prov.

Countries of origin

(23)

Market Team

118

Part-time

collaboratorsFTEs

Team: ~760 collaborators

Chile

▪ General Mgr.

▪ VP´s

Peru

▪ General Mgr.

▪ VP´s

ErIcsson –

- Top Management

- Project Governance

TD@E Team TOP Management

The transformation is supported by a world class experienced team,

with full commitment from the TOP Management

ENTEL DIGITAL TRANSFORMATION

13

Our solution architecture

14

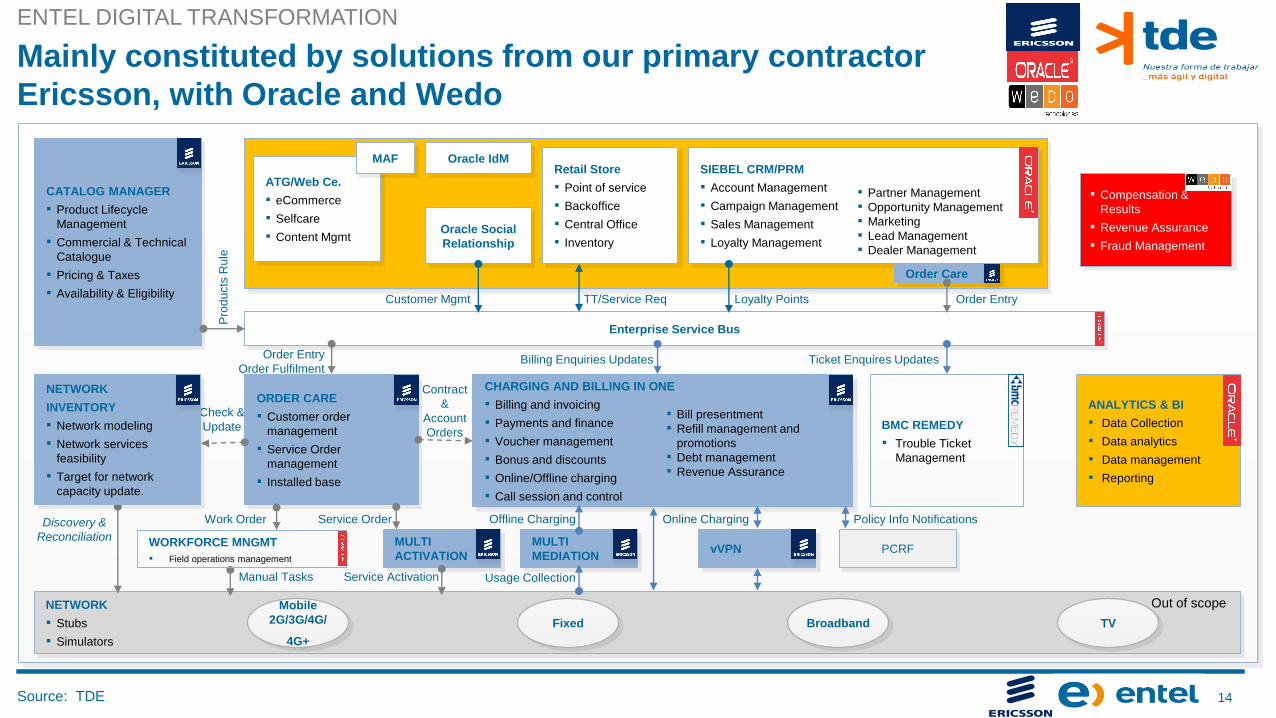

Mainly constituted by solutions from our primary contractor

Ericsson, with Oracle and Wedo

CATALOG MANAGER

▪ Product Lifecycle

Management

▪ Commercial & Technical

Catalogue

▪ Pricing & Taxes

▪ Availability & Eligibility

▪ Compensation &

Results

▪ Revenue Assurance

▪ Fraud Management

Enterprise Service Bus

NETWORK

▪ Stubs

▪ Simulators

ORDER CARE

▪ Customer order

management

▪ Service Order

management

▪ Installed base

ANALYTICS & BI

▪ Data Collection

▪ Data analytics

▪ Data management

▪ Reporting

CHARGING AND BILLING IN ONE

▪ Billing and invoicing

▪ Payments and finance

▪ Voucher management

▪ Bonus and discounts

▪ Online/Offline charging

▪ Call session and control

BMC REMEDY

▪ Trouble Ticket

Management

MULTI

ACTIVATIONPCRFvVPN

MULTI

MEDIATION

ATG/Web Ce.

▪ eCommerce

▪ Selfcare

▪ Content Mgmt

MAF Oracle IdM

Oracle Social

Relationship

Retail Store

▪ Point of service

▪ Backoffice

▪ Central Office

▪ Inventory

SIEBEL CRM/PRM

▪ Account Management

▪ Campaign Management

▪ Sales Management

▪ Loyalty Management

▪ Partner Management

▪ Opportunity Management

▪ Marketing

▪ Lead Management

▪ Dealer Management

Order Care

▪ Bill presentment

▪ Refill management and

promotions

▪ Debt management

▪ Revenue Assurance

Out of scopeMobile

2G/3G/4G/

4G+

Fixed Broadband TV

Work Order

Manual Tasks

Pro

du

cts

Rule

Order Entry

Order Fulfilment

Contract

&

Account

Orders

Service Order

Service Activation

Offline Charging

Usage Collection

Billing Enquiries Updates

Online Charging Policy Info Notifications

Ticket Enquires Updates

Customer Mgmt TT/Service Req Loyalty Points Order Entry

WORKFORCE MNGMT

▪ Field operations management

Discovery &

Reconciliation

Check &

Update

NETWORK

INVENTORY

▪ Network modeling

▪ Network services

feasibility

▪ Target for network

capacity update.

Source: TDE

ENTEL DIGITAL TRANSFORMATION

15

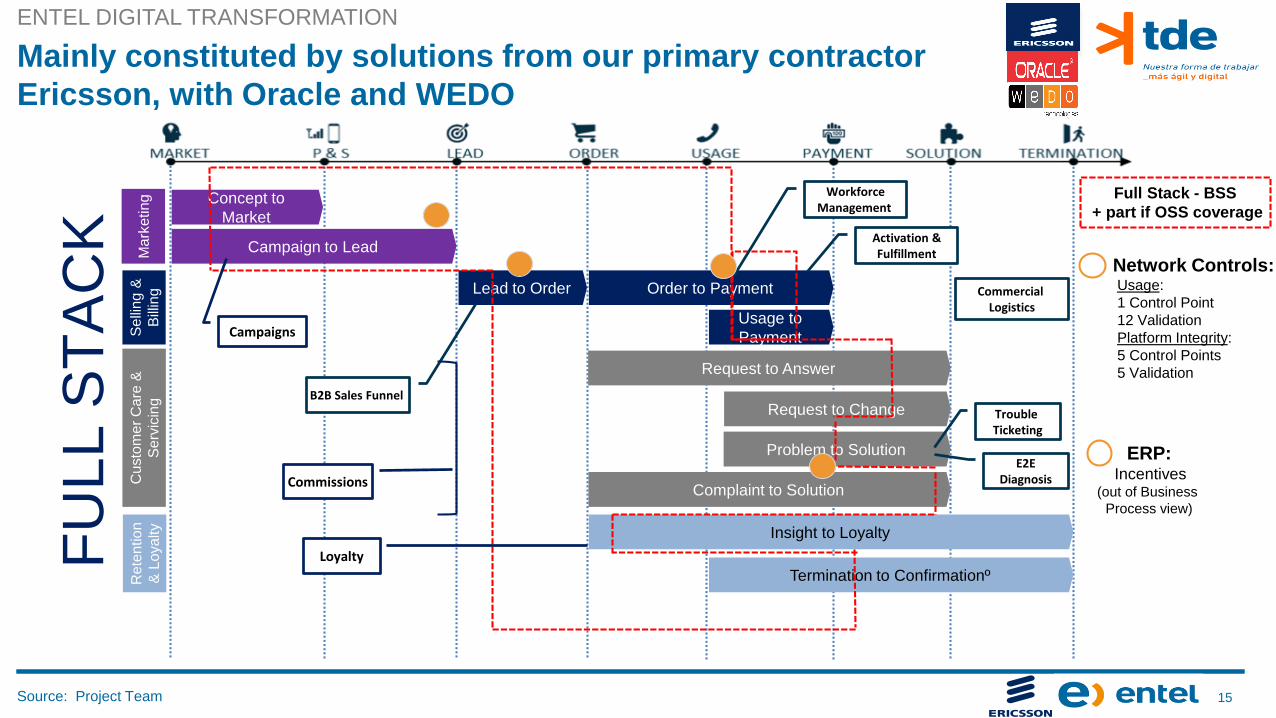

Mainly constituted by solutions from our primary contractor

Ericsson, with Oracle and WEDO

Source: Project Team

ENTEL DIGITAL TRANSFORMATION

Se

llin

g &

Bill

ing

Cu

sto

me

r C

are

&

Se

rvic

ing

Usage to

Payment

Lead to Order

Request to Change

Request to Answer

Complaint to Solution

Problem to Solution

Ma

rke

ting

Campaign to Lead

Concept to

Market

Re

ten

tio

n

& L

oya

lty

Termination to Confirmationº

Insight to Loyalty

Order to Payment

Full Stack - BSS

+ part if OSS coverage

Campaigns

B2B Sales Funnel

Commissions

Loyalty

WorkforceManagement

Activation &Fulfillment

CommercialLogistics

TroubleTicketing

E2EDiagnosis

FU

LL

ST

AC

K

Network Controls:Usage:

1 Control Point

12 Validation

Platform Integrity:

5 Control Points

5 Validation

ERP:Incentives

(out of Business

Process view)

16

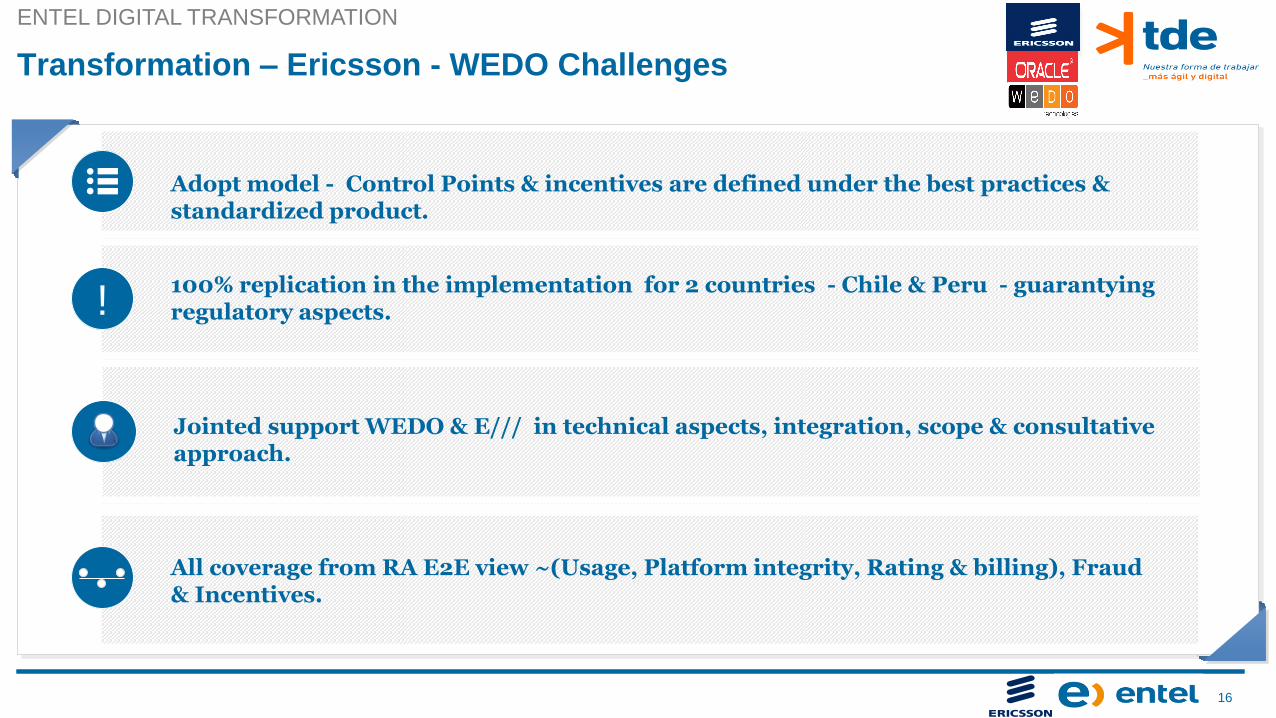

Transformation – Ericsson - WEDO Challenges

ENTEL DIGITAL TRANSFORMATION

All coverage from RA E2E view ~(Usage, Platform integrity, Rating & billing), Fraud & Incentives.

100% replication in the implementation for 2 countries - Chile & Peru - guarantying regulatory aspects.!

Adopt model - Control Points & incentives are defined under the best practices & standardized product.

Jointed support WEDO & E/// in technical aspects, integration, scope & consultative approach.

17

Lessons Learned

Last M

odifie

d 0

3-0

5-2

017 9

:40 P

acific

SA

Sta

ndard

Tim

eP

rinte

d 1

6-1

2-2

016 1

9:3

9 P

acific

SA

Sta

ndard

Tim

e

18

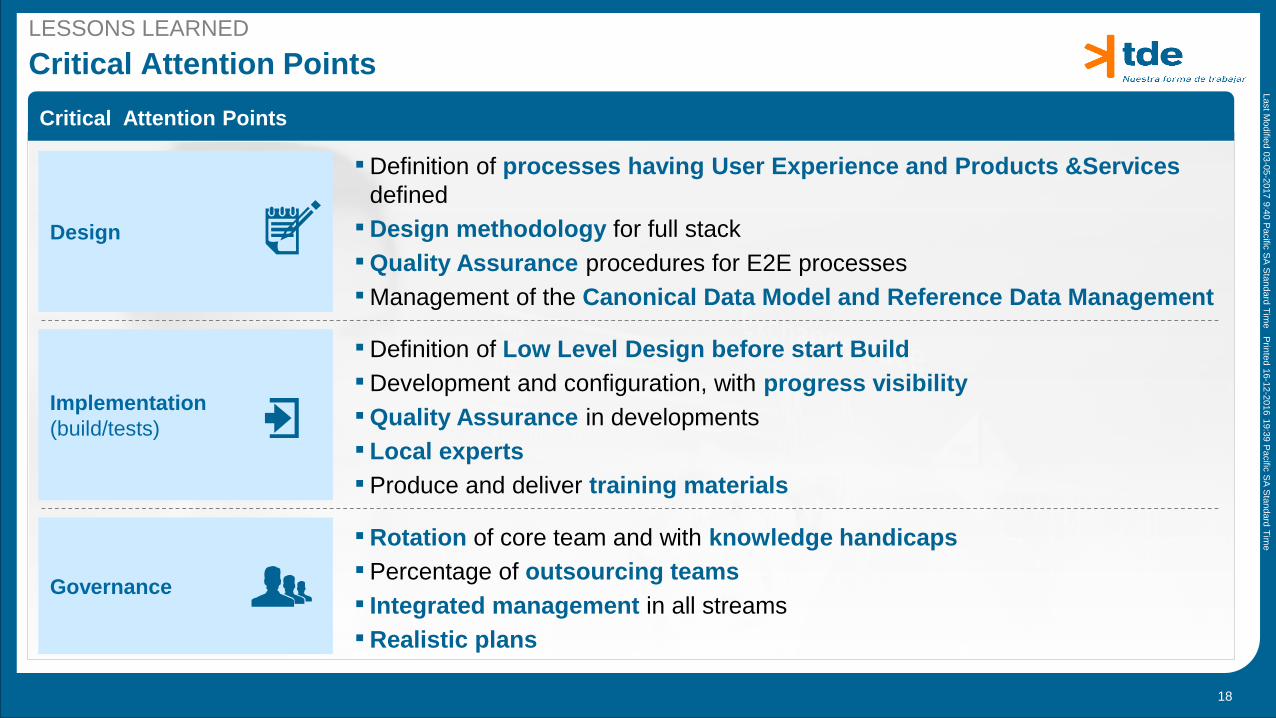

Critical Attention Points

Critical Attention Points

Design

▪Definition of processes having User Experience and Products &Services

defined

▪Design methodology for full stack

▪Quality Assurance procedures for E2E processes

▪Management of the Canonical Data Model and Reference Data Management

Governance

▪Rotation of core team and with knowledge handicaps

▪Percentage of outsourcing teams

▪ Integrated management in all streams

▪Realistic plans

Implementation

(build/tests)

▪Definition of Low Level Design before start Build

▪Development and configuration, with progress visibility

▪Quality Assurance in developments

▪ Local experts

▪Produce and deliver training materials

LESSONS LEARNED

Last M

odifie

d 0

3-0

5-2

017 9

:40 P

acific

SA

Sta

ndard

Tim

eP

rinte

d 1

6-1

2-2

016 1

9:3

9 P

acific

SA

Sta

ndard

Tim

e

19

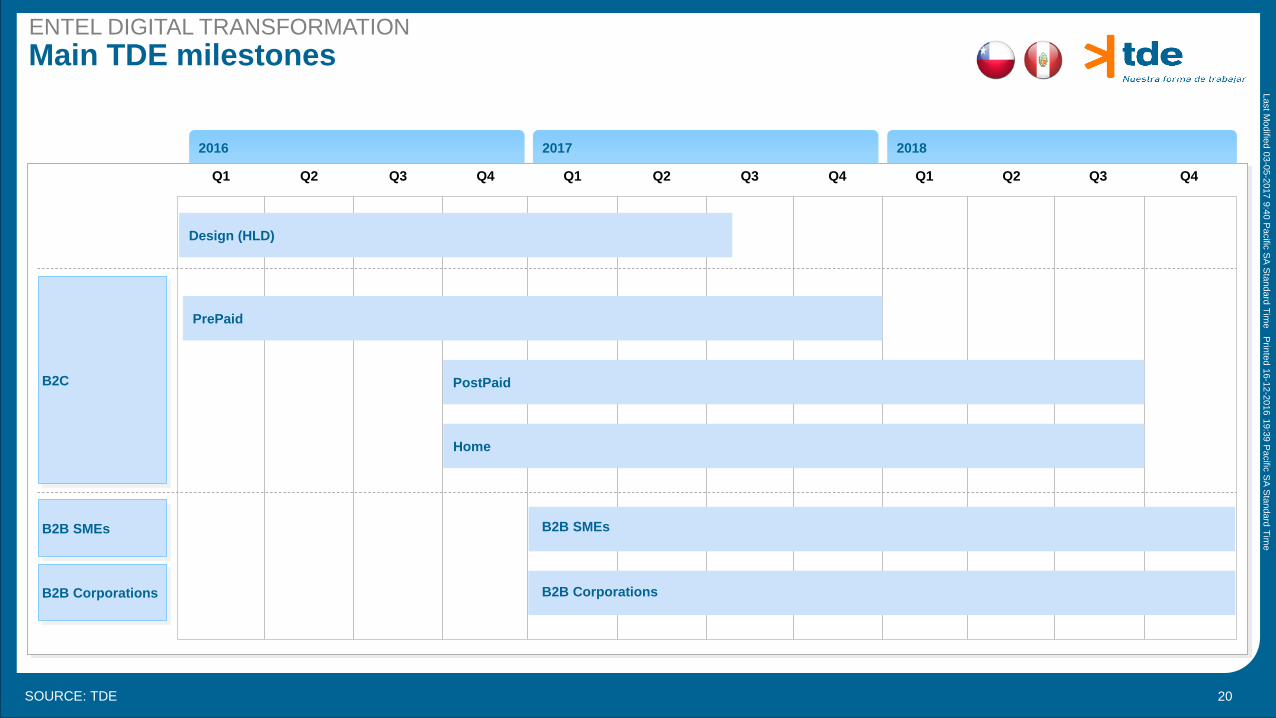

Milestones

Last M

odifie

d 0

3-0

5-2

017 9

:40 P

acific

SA

Sta

ndard

Tim

eP

rinte

d 1

6-1

2-2

016 1

9:3

9 P

acific

SA

Sta

ndard

Tim

e

20

B2C

B2B SMEs

2016 2017 2018

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Design (HLD)

PrePaid

B2B Corporations

Home

PostPaid

B2B SMEs

B2B Corporations

SOURCE: TDE

Main TDE milestonesENTEL DIGITAL TRANSFORMATION

Last M

odifie

d 0

3-0

5-2

017 9

:40 P

acific

SA

Sta

ndard

Tim

eP

rinte

d 1

6-1

2-2

016 1

9:3

9 P

acific

SA

Sta

ndard

Tim

e

21

By the end of the Project

Last M

odifie

d 0

3-0

5-2

017 9

:40 P

acific

SA

Sta

ndard

Tim

eP

rinte

d 1

6-1

2-2

016 1

9:3

9 P

acific

SA

Sta

ndard

Tim

e

22

Main objectives

Best in class IT solutions

Innovation & best practices

Most efficient organization –

Agile

Paperless, seamless and

peopleless

World class customer

experience - Digital

Customers and emotions

2019 ………