Embed Size (px)

Citation preview

Copyright © 2013 Farncombe

Digital Switch-Over:

Best Practices for Governments, Regulators and the Industry

June 2013

Confidential and Proprietary 2

An international firm specialised in DSO and digital video delivery

We have advised governments and broadcasters around the World on:

–Strategy for DSO;

–Specifications and Technology Strategy;

– Implementation of Subsidy Schemes.

–Connected TV Platforms/hybrid standards;

We are independent:

–Not owned or related to any vendor, service provider or standards body.

Confidential and Proprietary 3

EXAMPLES OF ASO TIMELINES It takes time to switchover with minimal disruption to users – it is worth learning

from the experience of other countries to avoid the same mistakes

0

1

2

3

4

5

6

7

8

9

10

UK

Be

lgiu

m

Ital

y

Swe

de

n

Lith

uan

ia

Swit

zerl

and

Cze

ch R

ep

ub

lic

Ge

rman

y

Fran

ce

Spai

n

Slo

ven

ia

Esto

nia

Au

stri

a

Ire

lan

d

Po

rtu

gal

Ne

the

rlan

ds

De

nm

ark

No

rway

Source: DVB.org, DigiTAG

# of years

Countries that started later took

less time to switchover, as

technologies were more mature, devices were

cheaper and they could learn from the

experiences of others’

Confidential and Proprietary 4

DSO – KEY RISKS The key challenge is finding a balance between an attractive, future-proof

platform while keeping costs and complexity under control.

Loss of

Quality and Control

Cost and Complexity

Creation of legacy system makes service outdated and require second switchover;

Coverage and line-up worse than analogue;

STB base in the market is too fragmented to create feasible addressable market for new services.

“Overkill” specifications make decoders expensive and slow DTT adoption;

Too complex certification and conformance process inhibit development of manufacturers’ ecosystem;

Lengthy simulcasting period;

Premature or costly set-top-box subsidies and help scheme.

Source: Farncombe

Confidential and Proprietary 5

DSO KEY ACTION LIST FRAMEWORK

3. Develop funding policy

1. Develop DSO policy & Legal framework

3. Manage radio spectrum and coordination matters

2. Implement licensing framework

4. Establish principles for Help Scheme

4. Plan & Deploy DTT network

3. Develop Communications plan

2. Establish DTT branding & Conformance regime

1. Develop Consumer Proposition

5. Establish receiver specifications & costs

1. Decide on Technology & Standards

2. Establish plan for ASO Government

(G)

Regulator(s) (R)

Industry (I)

Source: Plum, Farncombe

In conjunction with Plum Consulting, Farncombe has developed a report with Practical Steps for the DSO to complement the ITU guidelines

Confidential and Proprietary 6

DSO KEY ACTION LIST FRAMEWORK

3. Develop funding policy

1. Develop DSO policy & Legal framework

3. Manage radio spectrum and coordination matters

2. Implement licensing framework

4. Establish principles for Help Scheme

4. Plan & Deploy DTT network

3. Develop Communications plan

2. Establish DTT branding & Conformance regime

1. Develop Consumer Proposition

5. Establish receiver specifications & costs

1. Decide on Technology & Standards

2. Establish plan for ASO Government

(G)

Regulator(s) (R)

Industry (I)

Source: Plum, Farncombe

This presentation will focus on some important aspects of DSO that are often given less priority

Confidential and Proprietary 7

GOVERNMENT: ASO PLAN – DSO TASK FORCE The DSO Task Force must have a clear mandate from the Government to lead the

planning and implementation of the switch-over programme.

Co

mm

un

icat

ion

s

Co

nsu

me

r se

rvic

e

line

Co

nsu

me

r d

evi

ce

Ho

usi

ng

&

Pro

pe

rty

Co

nsu

me

r &

M

arke

t R

ese

arch

Bro

adca

st

infr

astr

uct

ure

He

lp S

che

me

Re

gula

tory

Programme Office

DSO Task Force

Wo

rk-s

trea

ms

Media

Supply chain (OeMs,

retailers, installers)

Government (NRA,

Ministries, etc)

Consumer Groups &

Institutions

Industry (Broadcasters, Trade Bodies & Associations)

Source: Farncombe

Confidential and Proprietary 8

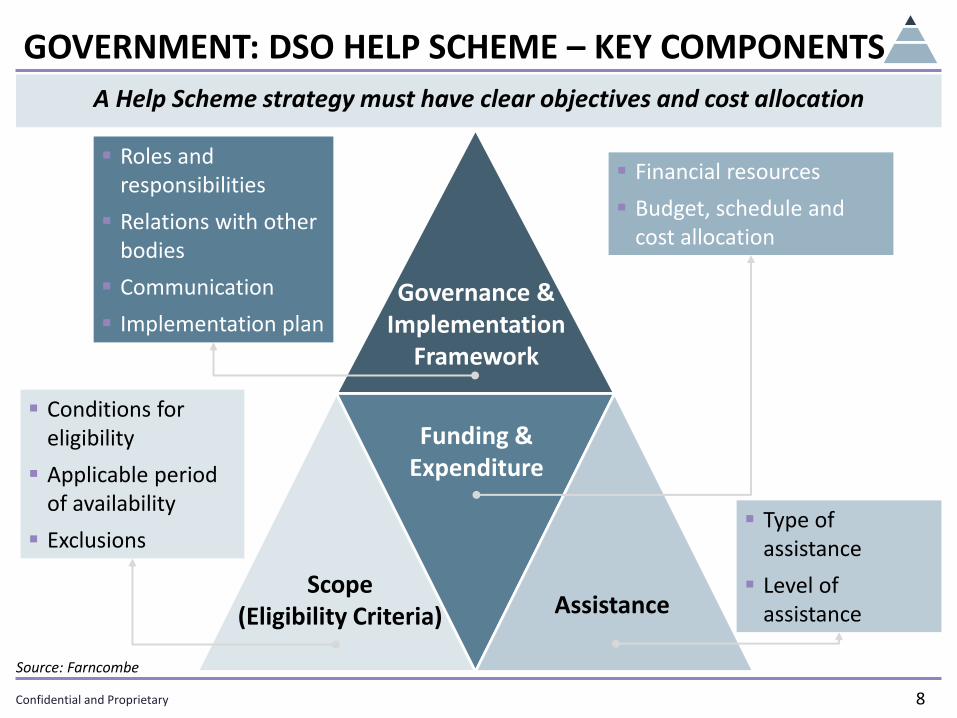

GOVERNMENT: DSO HELP SCHEME – KEY COMPONENTS

A Help Scheme strategy must have clear objectives and cost allocation

Roles and responsibilities

Relations with other bodies

Communication

Implementation plan

Financial resources

Budget, schedule and cost allocation

Type of assistance

Level of assistance

Conditions for eligibility

Applicable period of availability

Exclusions

Governance & Implementation

Framework

Assistance Scope

(Eligibility Criteria)

Funding & Expenditure

Source: Farncombe

Confidential and Proprietary 9

GOVERNMENT: SUBSIDY TIMING IS IMPORTANT Most countries cannot wait for total spontaneous migration, but timing of

introduction of subsidies must be carefully planned

Subsidise STBs 2013

Subsidise STBs 2015

2013 2015 20xx (Analogue Switch off)

Cost savings from delaying

Cost impact for subsidy delay

Source: Farncombe

Waiting until after there is a

established market for

devices can save money as device

costs fall with time and some

people will adopt DTT naturally as they change TVs

or buy STBs

Confidential and Proprietary 10

REGULATORY: MARKET STRUCTURE & LICENSING

Source: Farncombe

It is essential that processes are in place to issue licenses before the DSO starts

Content creator

Broadcaster/TV service provider

MUX owner/ operator

Site owner Network/

Transmission operator

Device manufacturer

Aggregation Multiplexing Distribution Network

Transmission Reception/

Presentation

Content Creation

Confidential and Proprietary 11

REGULATORY: TECHNOLOGY & STANDARDS It is critical to evaluate options and understand the long-term implications of

technology choices

Key implications

Standard STB price;

Risk of creation of legacy device base and “second DSO”.

Security Lower barrier to entry for paid-for DTT services in the future;

Ability to enable addressability and geographical control.

Network Specifications

Overall cost of coverage, availability of services;

Ability to enable mobile TV.

HD vs. SD Number of services available for each broadcaster;

Adoption and attractiveness to consumers .

Interactivity Cost of royalties for manufacturers and developers; required time

for conformance and integration;

Long term structure to enable connected TV services.

Source: Farncombe

Confidential and Proprietary 12

EXAMPLE OF NEW FREE-TO-AIR PLATFORM:TNT 2.0

HbbTV1.5 – based initiative to enable

– Live streaming: video services, live channels, event channels, etc;

– Premium content and pay-TV services on connected TVs;

Mandates specifications for DRM, adaptive streaming, as well as other features

Technical specifications published in July 2011, test suite for OeMs released in July 2012

Standard adopted this year in France, Spain, Belgium, Finland, Netherlands, Russia, Poland

Source: farncombe

Confidential and Proprietary 13

EXAMPLE OF HbbTV APPLICATION: PROGRAM RESTART

France Television launch a Program Restart application on HbbTV in September 2012

– When viewers are switching to the programme after it began, an HbbTV Pop Up is offering to “restart the program”

Confidential and Proprietary 14

EXAMPLE OF HbbTV APPLICATION: CATCH UP TV & VOD

Most channels are already offering Catch UP TV service on the television through IPTV.

HbbTV 1.5 enables these offers to be made available on all compatible Connected TVs

Confidential and Proprietary 15

EXAMPLE OF CONTENT –OWNERS INITIATIVE: YOUVIEW

A “walled garden” to protect advertising

An unified UI and backwards EPG to avoid multiple integration processes

A centralised search engine

Collection of usage statistics and viewing behaviour;

Centralised and managed security

A brand identified with content availability

YouView Shareholders

Confidential and Proprietary 17

Confidential and Proprietary 18

SOME OF THE DECISIONS THAT DID NOT TURN RIGHT

Decision

France chose to launch HD, MPEG-4 using DVB-T

The UK Freeview service was introduced without any means to monetise additional services

The French DTT service did not mandate an EPG ecosystem

Italy mandated (MHP) to ensure its penetration on the base

Multiple Pay DTT operators in Europe launched with proprietary systems and expensive STBs

Impact

Now it is clear that DVB-T2 is a more efficient standard - it will require a second digital switchover to get there

A small specification change would have enabled paid for enhanced services across the whole STB platform

Now it is too late to implement it

MHP implementation did not have a conformance regime – many STBs cannot be used for interactive applications

Many failed– standards can drive down costs and make Pay-DTT feasible.

There are many interlinked and complex decisions that need to be taken into account.

Source: Farncombe research

Confidential and Proprietary 19

INDUSTRY – GROUPS Industry co-ordination is key. Countries with cross-industry support tend to benefit

from shorter transition timescales.

Defining digital standards &

specifications

Managing technical platform

Co-ordinating and selling

digital transition

Supporting vulnerable

groups

“Digital TV Group” “DTT Multiplex Operators Co.” “DSO Task Force” “Help Scheme”

Publishes and maintains the technical specification of the DTT platform

May provide interoperability and certification regime for standards-compliance

Operational oversight of all multiplexes

Manages new channel launches, channel numbering, including EPG requirements, ensuring consistency across different STBs and iDTVs

Independent, platform-neutral, non-profit organization appointed for co-ordinating the implementation of switchover

Works closely with government and regulator(s), industry and supply chain

Tasked with subsidising/assisting vulnerable groups with digital conversion

Option of contracted-out but overseen/ advised by Government

Source: Farncombe

Confidential and Proprietary 20

INDUSTRY – DTT CONSUMER PROPOSITION DTT must be more attractive than analogue services to ensure an easier transition

and take-up by users

The extended channel choice given by DTT has proven to be a key driver of adoption; re-broadcast (+1) services offer flexibility and attract new audiences.

EPG, subtitling, middleware that enables VoD, e-learning, e-government services, etc, increase the value of the platform.

High-definition improves the overall perception of the service although in most countries it is less of an adoption driver than multichannel.

Portability/ mobility can address new niches (e.g. bus services) and enable multi-screen experience.

Free-to-view is an important driver for adoption – but paid components can make it more attractive. Paid platforms that co-ordinate technical standards are more likely to succeed.

Importance Service Dimension

Additional Channels

Interactivity

HD services

Portable/ Mobile reception

Free or Pay?

Source: Farncombe

Confidential and Proprietary 21

COMMUNICATIONS MODEL Adopting a layered Communication model with emphasis on local activity can

increase the effectiveness of the Communications Plan.

National Advertising

Regional Communications

Local Communications

Community

1-on-1

Third-party support

National Broadcasters; Online outlets; Magazines;

Industry trade publications

Charities and Associations;

Retailer & other POS material

Local TV and Radio; Daily newspapers;

Events

Communications Model

Broadcast messages on mobile phones

Source: Digital UK, Farncombe

Confidential and Proprietary 22

INDUSTRY – DTT CONFORMANCE LOGOS A well-planned conformance regime can ensure that devices in the market are

sound and gives consumers more confidence when buying new devices

Conformance logos can give confidence to

consumers of which services they can receive when they are buying devices, e.g.:

– Basic DTT Channels;

– DTT Channels plus VoD/catch-up functions over e.g. HbbTV;

– DTT Channels including HD channels;

– Pay Channels (e.g. devices with a CA slot).

DigiTiVi

DigiTiVi

Illustrative: DTT platform conformance logos

DigiTiVi+

Source: Farncombe

DigiTiVi

Confidential and Proprietary 23

INDUSTRY – DSO COMMS PLAN INDICATIVE TIMELINES

Source: Farncombe

Confidential and Proprietary 24

SUMMARY: SOME OF THE KEY LESSONS LEARNT

Extended channel choice has been proven to be a key driver of adoption, but other features such as high-definition, mobile reception, EPG and on-demand functionality (catch-up TV integrated with linear TV also help attract viewers.

Product differentiation: DTT must be attractive to users 1

Countries which initially advertised DTT benefits and only later advertised the switch-off deadline have enjoyed easier transitions, especially if tied to a clear receiver conformance regime and DTT brand/logo.

Clear communications 2

Subsidies for DTT devices help speed up the process, but support to installation of antennas, and good co-ordination and logistics are also essential. Specifications for devices must be thought through to enable long-term competition and enable new services.

Well-managed subsidy/ Help scheme 3

Independent of the time taken to plan the switch-off and implement subsidies most people will leave until the last minute to migrate – a gradual transition process helps spreading resources more efficiently and learn from the initial experiences.

Gradual Transition Process 4

Confidential and Proprietary 25

SUMMARY: SOME OF THE KEY LESSONS LEARNT (cont.)

Many of the features that can help make DTT attractive depend on cross-industry co-ordination such as the creation of a EPG, communications, numbering and hybrid TV

Cross-industry co-ordination 5

The DTT plan cannot be imposed to the industry – broadcasters and manufacturers must be in-line with objectives, support trade-offs required. Deadlines must be realistic, otherwise services will not be ready when expected and users will not migrate.

Develop a credible plan with the participation of all key stakeholders 6

Confidential and Proprietary 26

CONTACT INFORMATION

Adriana Menezes Whiteley Head of Strategy Practice [email protected]

+44 203 008 8547