Embed Size (px)

Citation preview

July 7th 2015

Digital inside: Get wired to deliver the ultimate luxury experience

Marco Catena Nathalie Remy

With the

McKinsey & Company | 1

McKinsey & Company | 2

Focused on core luxury consumers

Broad geographical scope: 8 countries

Multiple consumer journeys: 4 categories, 3 pricepoints

McKinsey – Altagamma Digital Luxury Experience

2015 edition: A unique

perspective on the

omnichannel global luxury

consumer

McKinsey & Company | 3

Selected insights for luxury players

The paradox of digital luxury

experience

Touchpoints proliferation is

manageable

Digital is a must for luxury

growth

Get wired to deliver the ultimate luxury experience

McKinsey & Company | 4

Selected insights for luxury players

The paradox of digital luxury

experience

Touchpoints proliferation is

manageable

Get wired to deliver the ultimate luxury experience

Digital is a must for luxury

growth

McKinsey & Company | 5

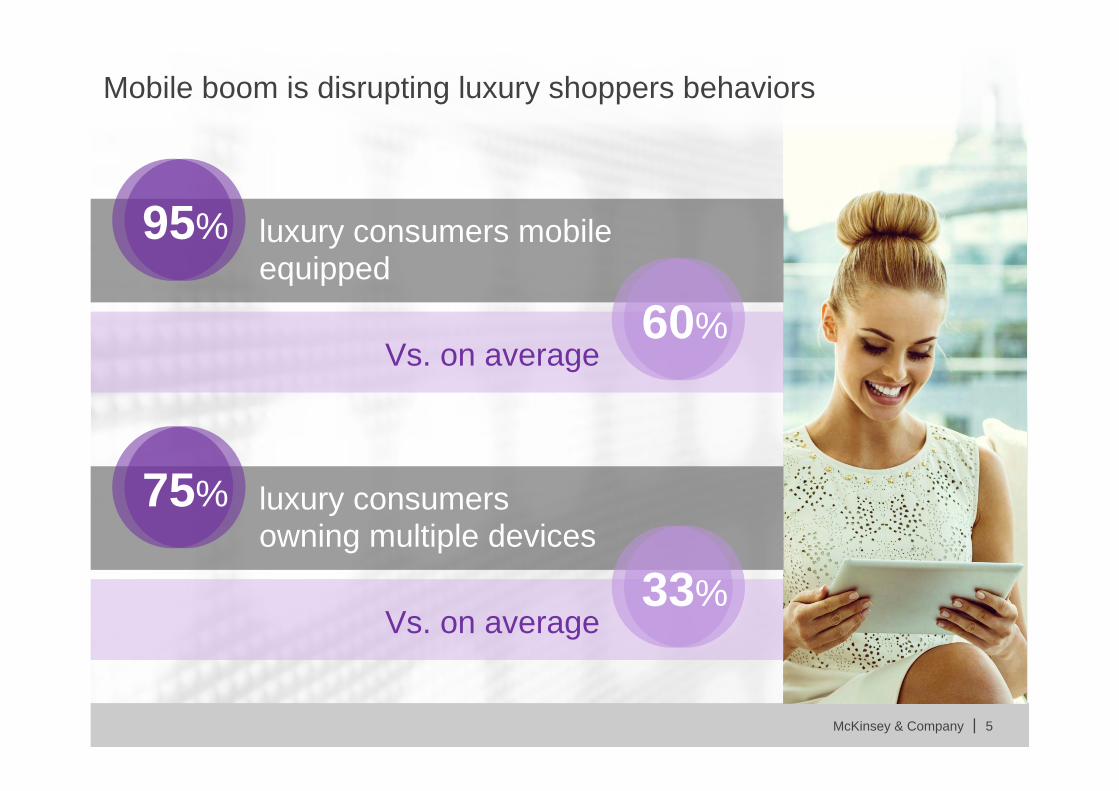

Mobile boom is disrupting luxury shoppers behaviors

luxury consumers mobile equipped

95%

Vs. on average 60%

luxury consumers owning multiple devices

75%

Vs. on average 33%

McKinsey & Company | 6

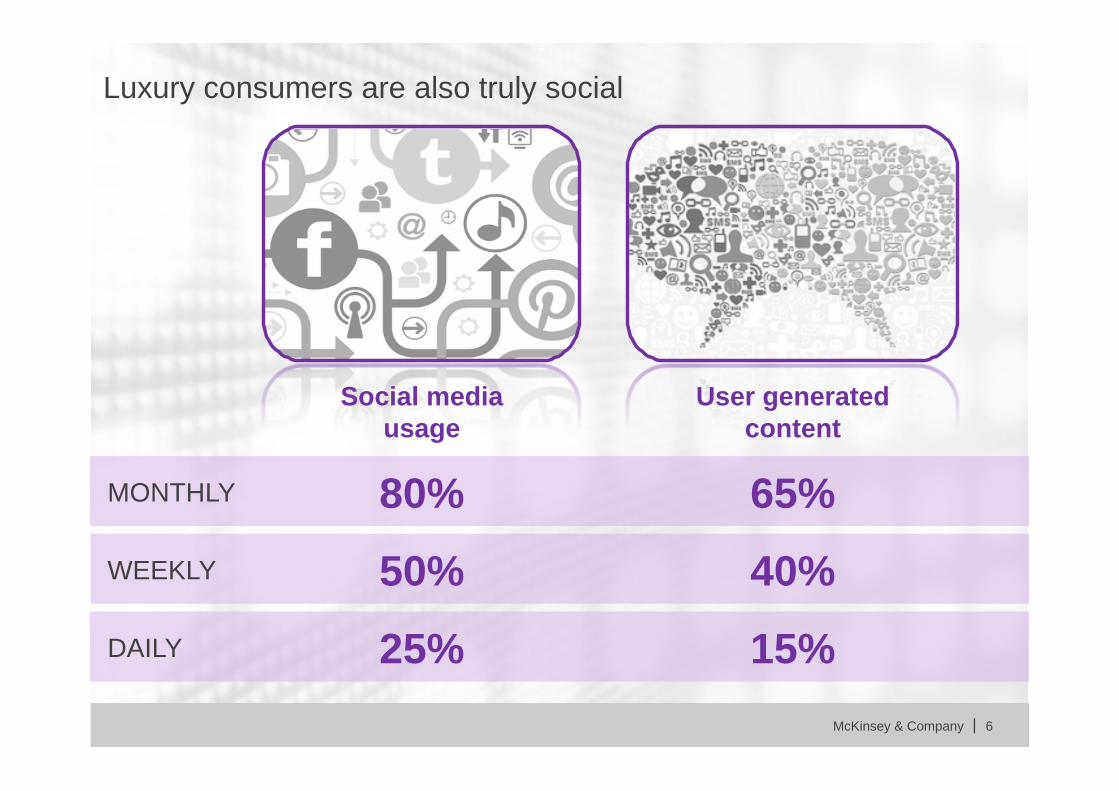

Luxury consumers are also truly social

Social media usage

User generated content

MONTHLY

WEEKLY

DAILY

80%

50%

25%

65%

40%

15%

McKinsey & Company | 7

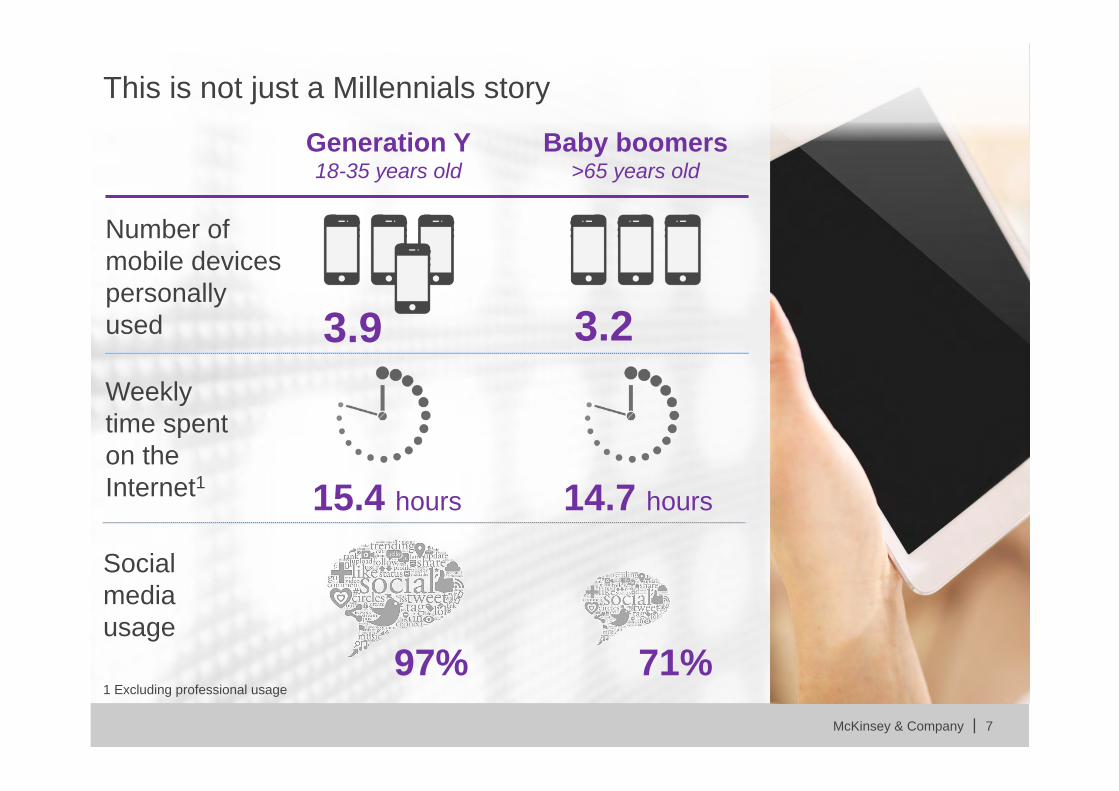

1 Excluding professional usage

Generation Y 18-35 years old

Baby boomers >65 years old

Number of mobile devices personally used

Weekly time spent on the Internet1

3.2 3.9

15.4 hours 14.7 hours

This is not just a Millennials story

Social media usage

97% 71%

McKinsey & Company | 8

The paradox

McKinsey & Company | 9

Selected insights for luxury players

The paradox of digital luxury

experience

Touchpoints proliferation is

manageable

Get wired to deliver the ultimate luxury experience

Digital is a must for luxury

growth

McKinsey & Company | 10

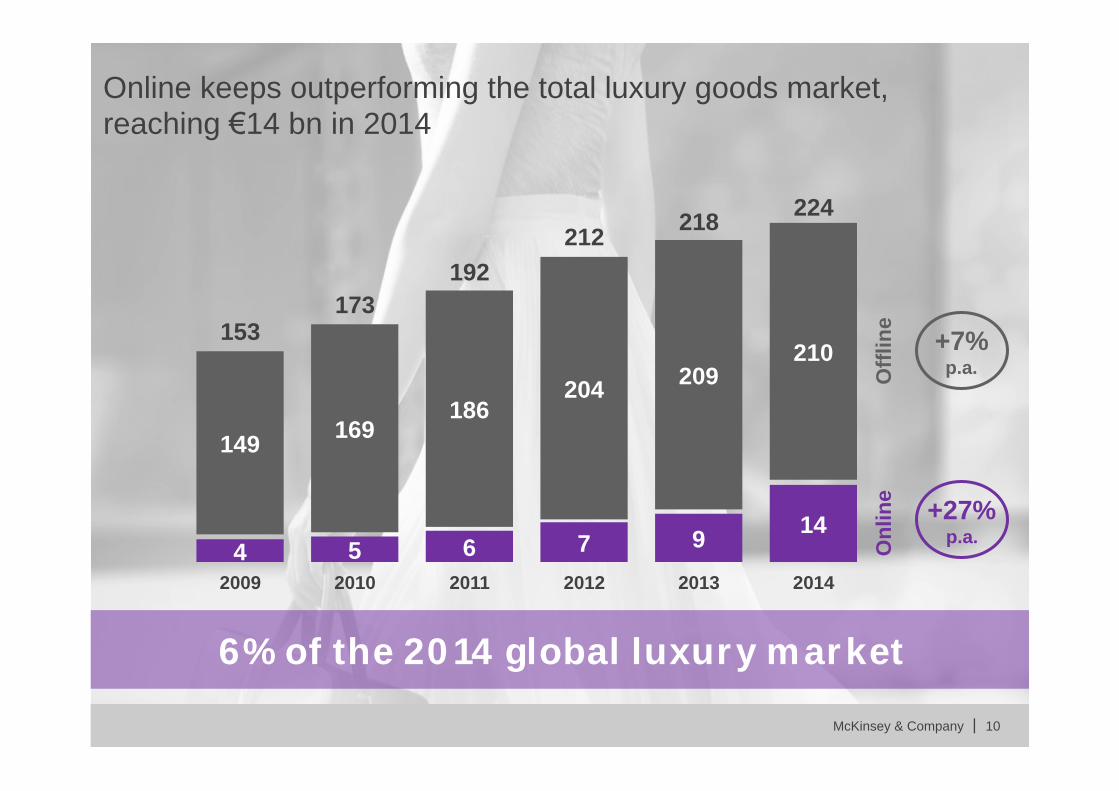

Online keeps outperforming the total luxury goods market, reaching €14 bn in 2014

149

4

153

2009

169

5

173

2010

6

186

192

2011

7

204

212

2012

9

209

218

2013

14

210

224

2014

+7% p.a.

+27% p.a.

Offl

ine

Onl

ine

6% of the 2014 global luxury market

McKinsey & Company | 11

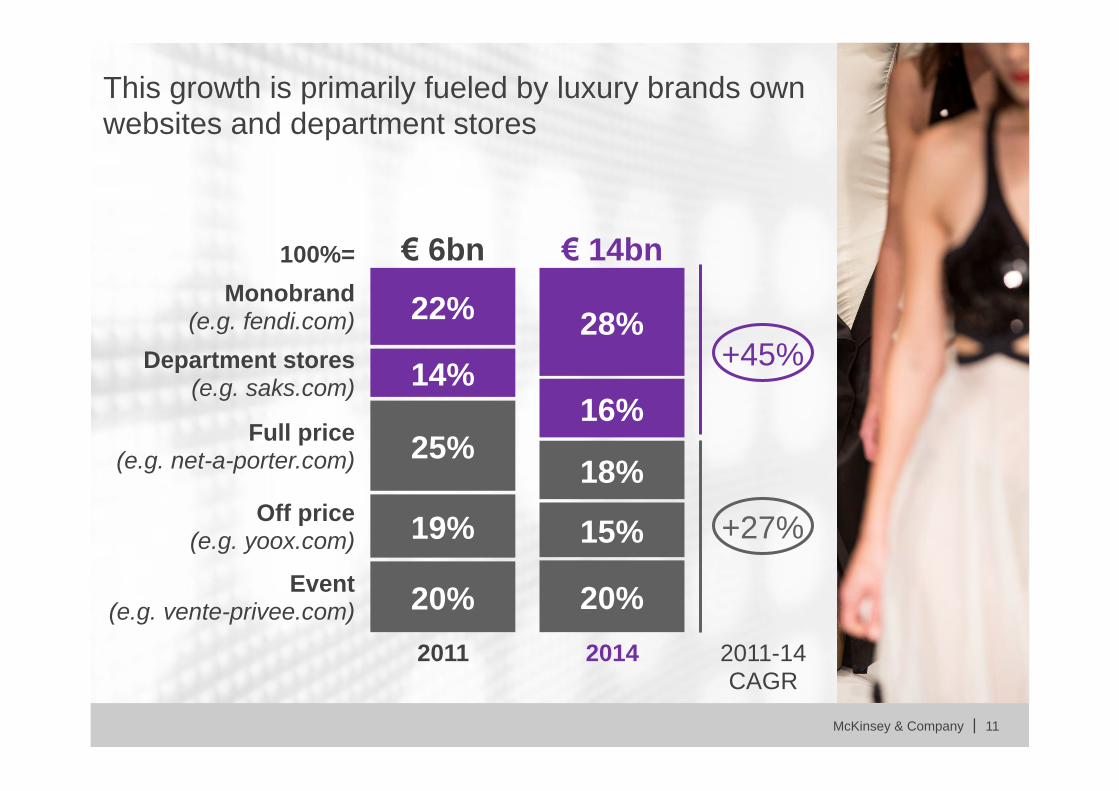

+45%

+27%

Monobrand (e.g. fendi.com)

Department stores (e.g. saks.com)

Full price (e.g. net-a-porter.com)

Off price (e.g. yoox.com)

Event (e.g. vente-privee.com) 20%

19%

25%

14%

22%

20%

15%

18%

16%

28%

2011 2014

€ 6bn € 14bn 100%=

2011-14 CAGR

This growth is primarily fueled by luxury brands own websites and department stores

McKinsey & Company | 12

Most luxury markets are around 6% of online sales

Mainland China

6%

USA

6%

UK

11%

Brazil

2%

Italy

5%

Japan

7%

South Korea

6%

France

6%

McKinsey & Company | 13

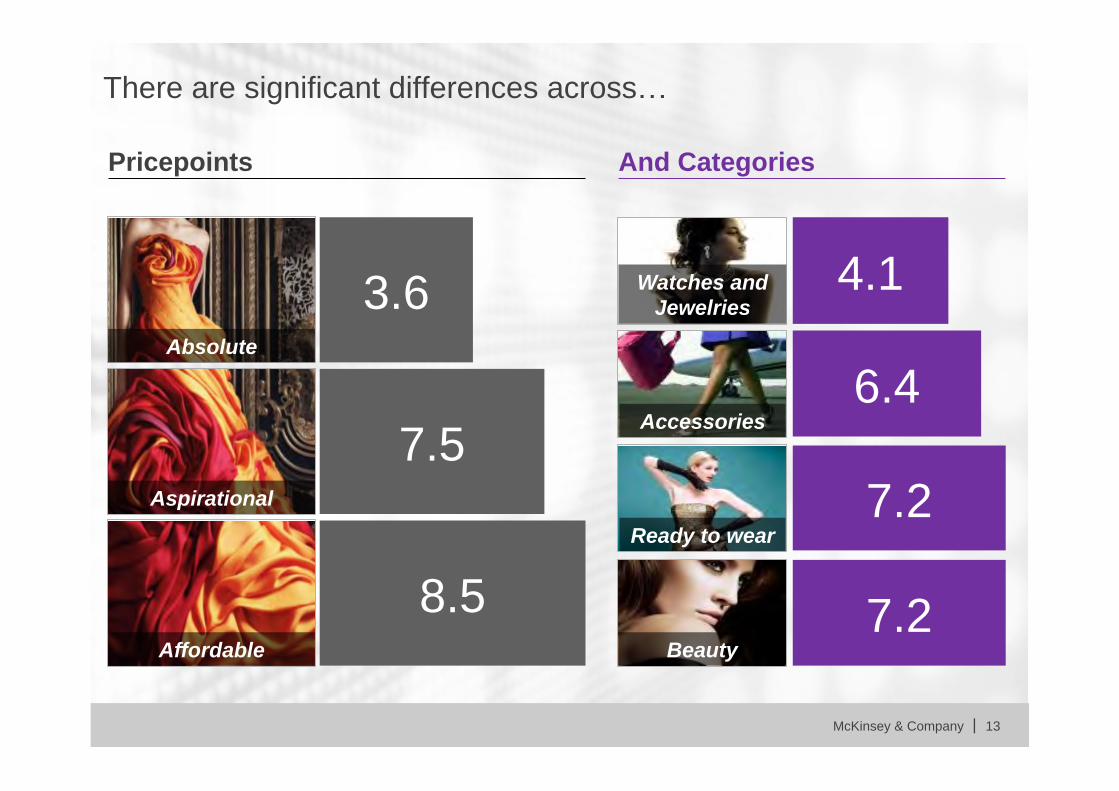

There are significant differences across…

3.6

7.5

8.5

Absolute

Aspirational

Affordable

Ready to wear

Beauty

7.2

7.2

Accessories 6.4

Watches and Jewelries

4.1

Pricepoints And Categories

McKinsey & Company | 14

RAMP-UP

SCALE-UP

PLATEAU

5%

25%

20%

15%

10%

N-4 N N+5 N+7 0%

Online trajectories follow a clear S-curve

Tipping point

McKinsey & Company | 15

With this acceleration, the online luxury share could reach 18% by 2025

Offline

Online

2020F 2009 2014 2% 6%

12% 18%

2025F

€70bn in 2025

McKinsey & Company | 16

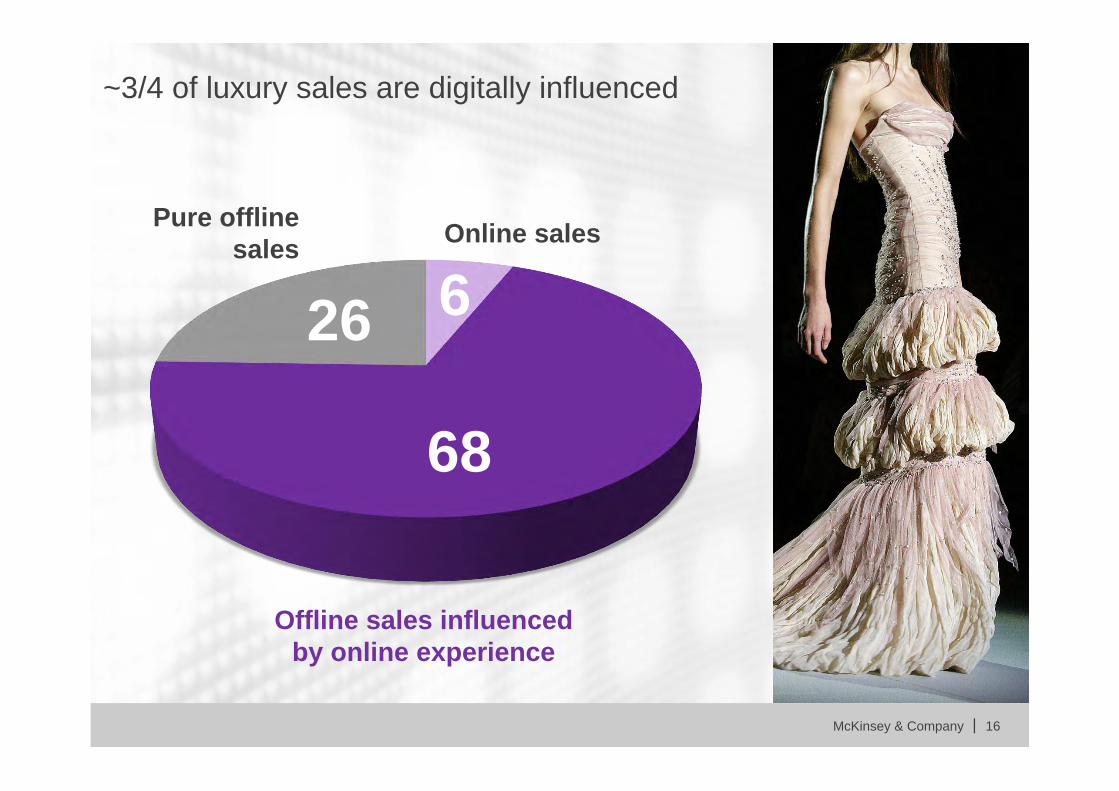

~3/4 of luxury sales are digitally influenced

Pure offline sales Online sales

Offline sales influenced by online experience

26 6

68

McKinsey & Company | 17

Selected insights for luxury players

The paradox of digital luxury

experience

Get wired to deliver the ultimate luxury experience

Touchpoints proliferation is

manageable

Digital is a must for luxury

growth

McKinsey & Company | 18

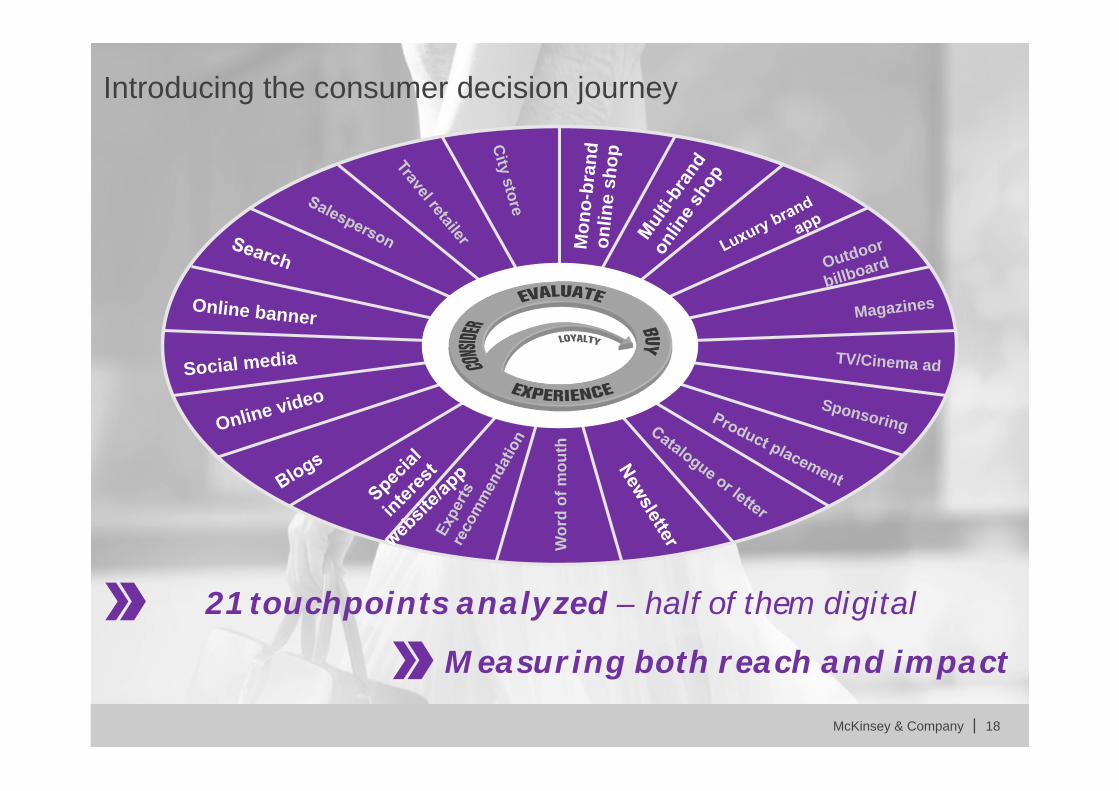

Introducing the consumer decision journey

Mon

o-br

and

on

line

shop

Outdoor

billboard

Magazines

TV/Cinema ad

Sponsoring

Wor

d of

mou

th Online video

Social media

Online banner

City store 21 touchpoints analyzed – half of them digital

Measuring both reach and impact

McKinsey & Company | 19

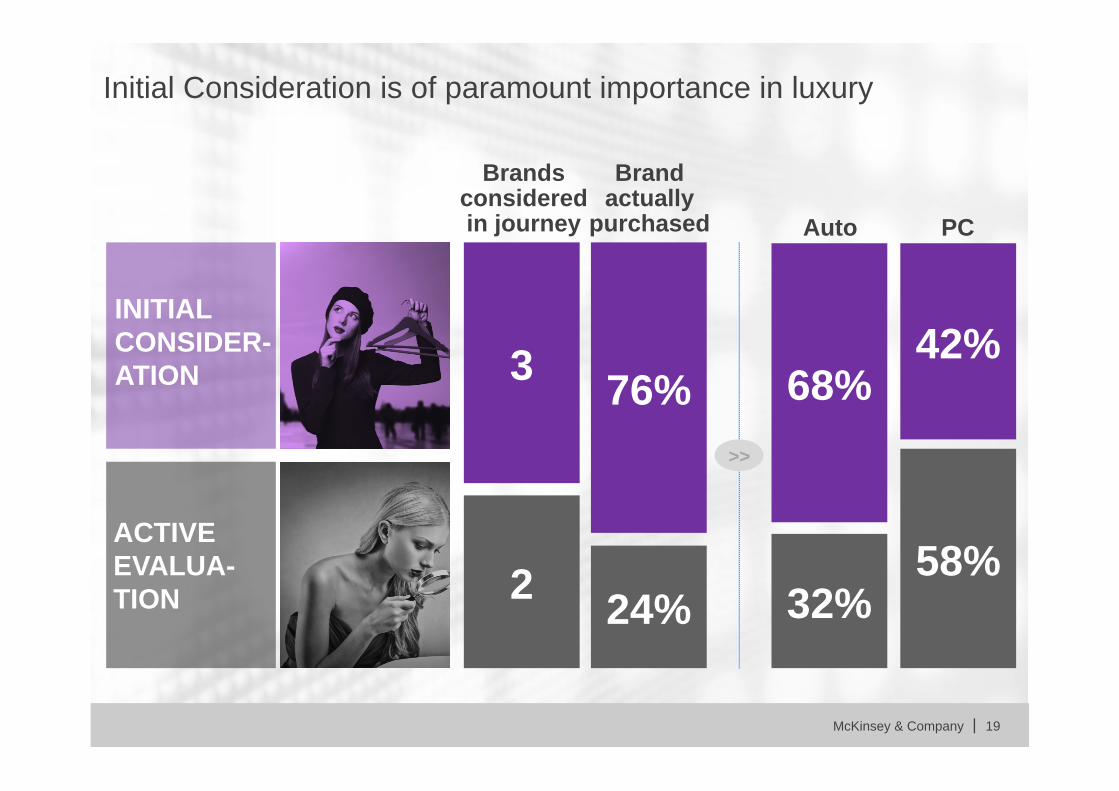

3

2

Brands considered in journey

76%

24%

Brand actually

purchased

INITIAL CONSIDER-ATION

ACTIVE EVALUA- TION

Initial Consideration is of paramount importance in luxury

Auto

68%

32%

PC

42%

58%

>>

McKinsey & Company | 20

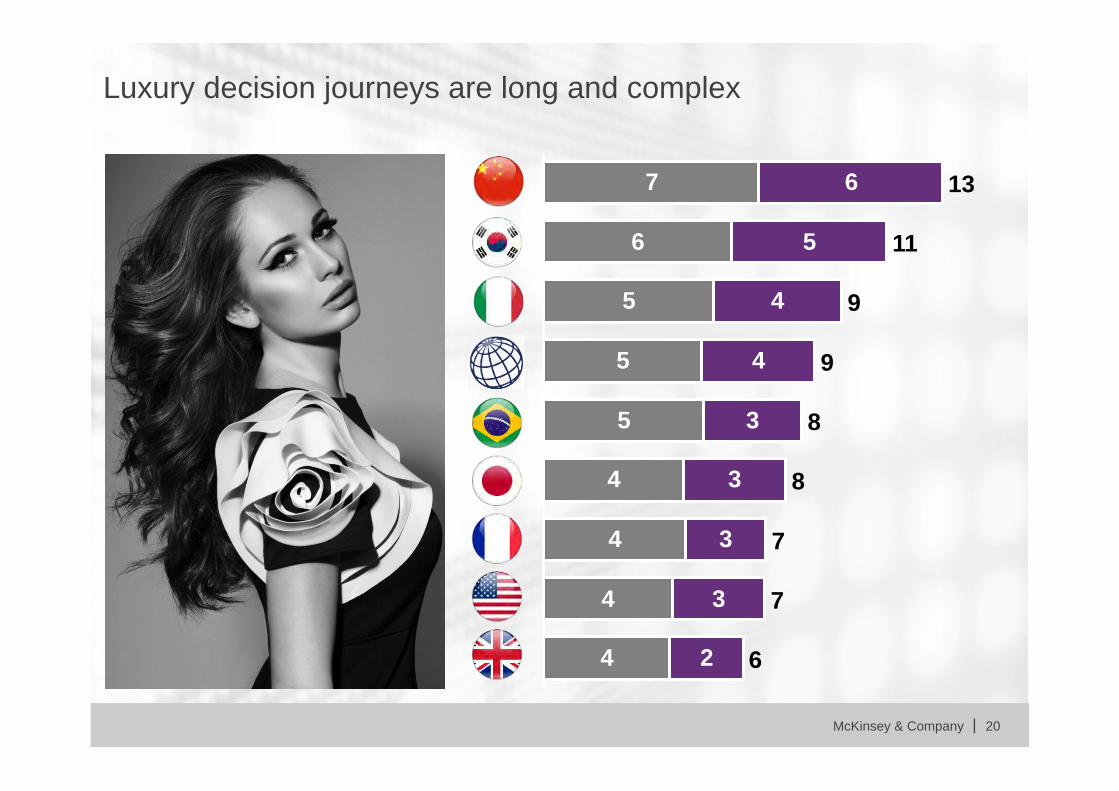

Luxury decision journeys are long and complex

7

6

5

5

4

4

4

6

5

4

3

3

3

3

5

4

4

2 6

7

7

8

8

9

11

13

9

McKinsey & Company | 21

Luxury brands must be everywhere, yet powerful and consistent

80%

66%

50%

43%

36%

19%

Con

sum

ers

expo

sure

City store

Fashion/luxury magazine

Word of mouth

Online community/blog

Social media

Online video service

McKinsey & Company | 22

5 touchpoints are must win battles

City store 1 Word of mouth

Search

Sales person

Brand website

2 3

4 5

McKinsey & Company | 23

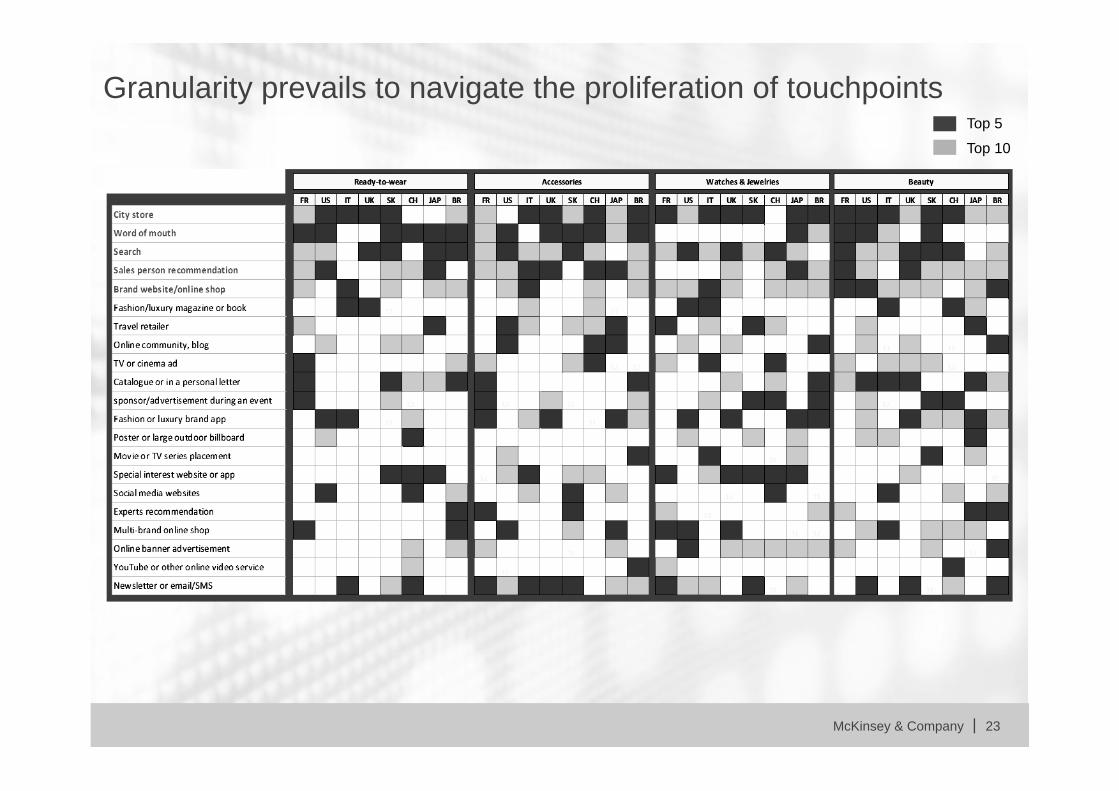

Granularity prevails to navigate the proliferation of touchpoints Top 5

Top 10

McKinsey & Company | 24

Granularity prevails to navigate the proliferation of touchpoints

Ready-to-wear – Italy

Watches&Jewelry – China

Beauty – Japan

Select your local bets

McKinsey & Company | 25

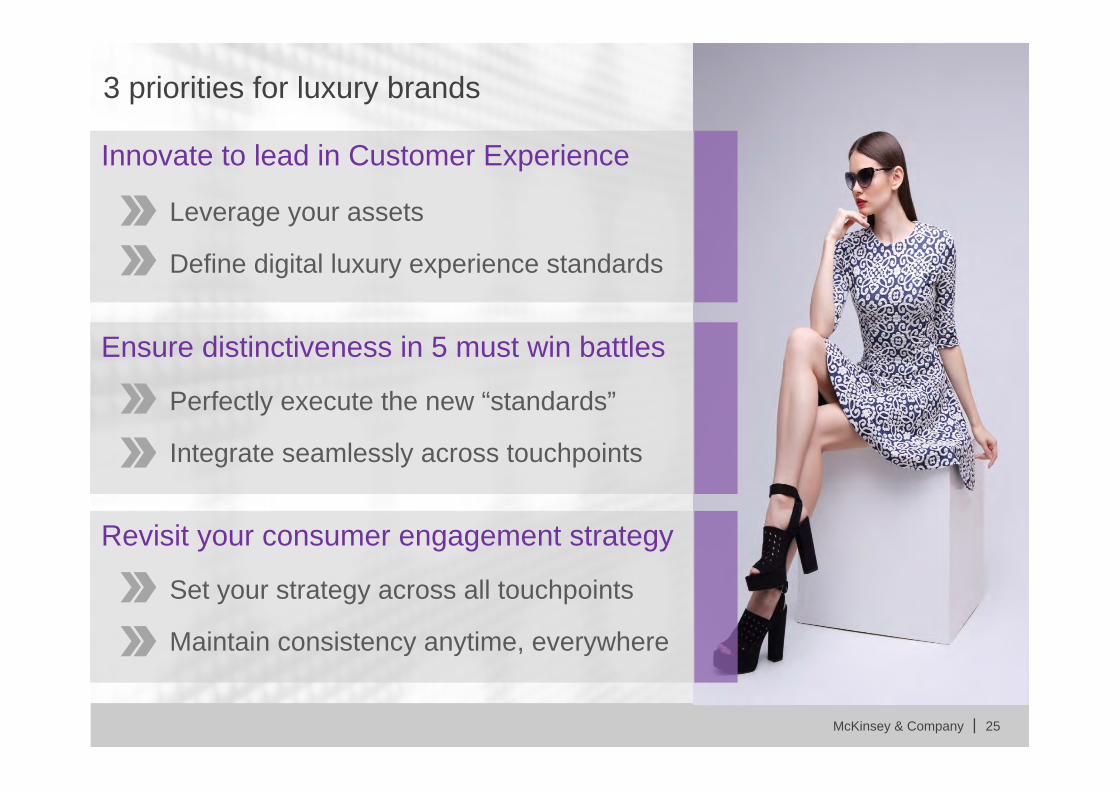

3 priorities for luxury brands

Innovate to lead in Customer Experience

Leverage your assets

Define digital luxury experience standards

Revisit your consumer engagement strategy

Set your strategy across all touchpoints

Maintain consistency anytime, everywhere

Ensure distinctiveness in 5 must win battles

Perfectly execute the new “standards”

Integrate seamlessly across touchpoints

McKinsey & Company | 26

How to make it happen?

Proactively address the typical roadblocks of digital acceleration

Bring digital inside your operating model and adapt your organization if needed

Design the digital acceleration approach that will fit with your culture

Digital inside: Get wired to deliver the ultimate luxury experience

McKinsey & Company | 28

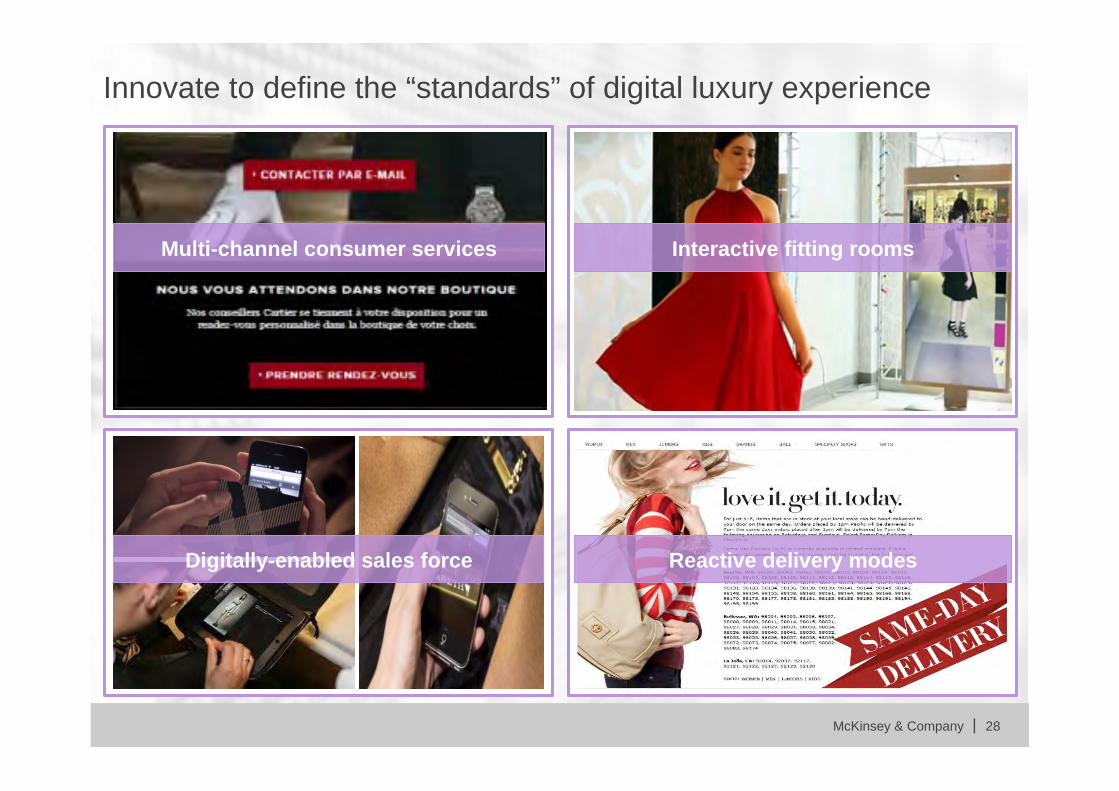

Innovate to define the “standards” of digital luxury experience

Multi-channel consumer services Interactive fitting rooms

Digitally-enabled sales force Reactive delivery modes

McKinsey & Company | 29

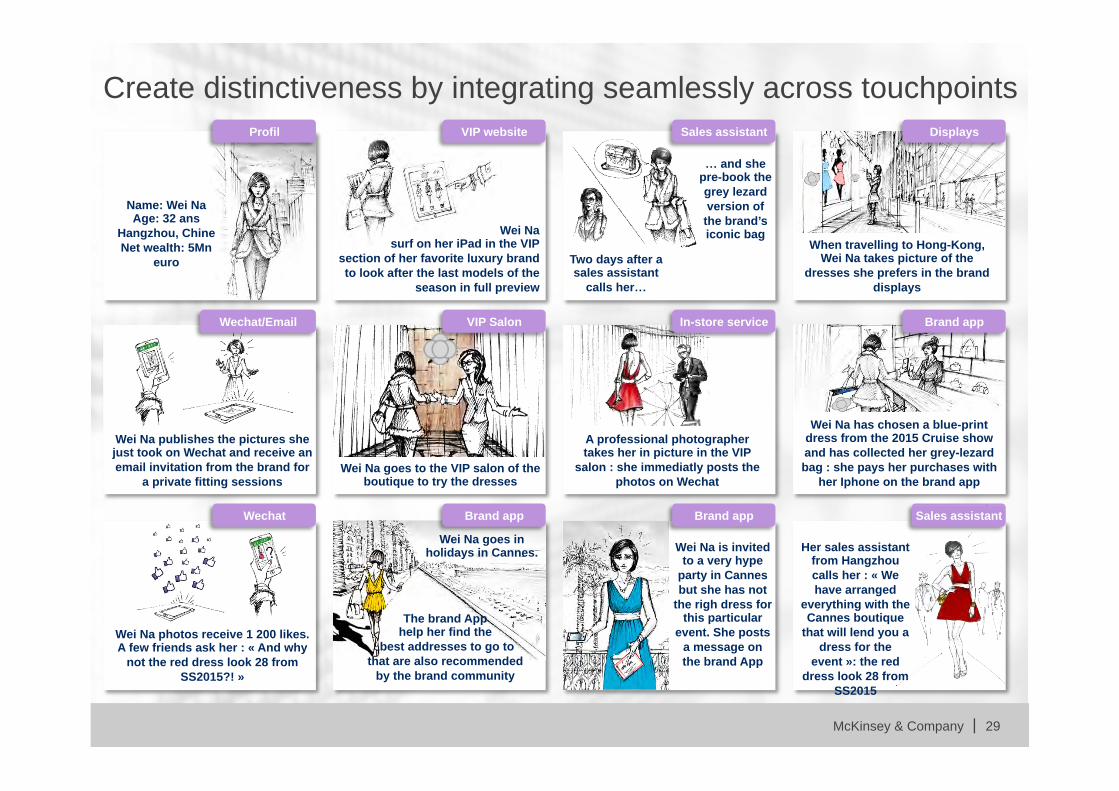

Create distinctiveness by integrating seamlessly across touchpoints

Wei Na surf on her iPad in the VIP

section of her favorite luxury brand to look after the last models of the

season in full preview

VIP website Sales assistant

Two days after a sales assistant

calls her…

… and she pre-book the grey lezard version of

the brand’s iconic bag

Displays

When travelling to Hong-Kong, Wei Na takes picture of the

dresses she prefers in the brand displays

Profil

Name: Wei Na Age: 32 ans

Hangzhou, Chine Net wealth: 5Mn

euro

Wei Na publishes the pictures she just took on Wechat and receive an email invitation from the brand for

a private fitting sessions

Wechat/Email

Wei Na goes to the VIP salon of the boutique to try the dresses

VIP Salon In-store service

A professional photographer takes her in picture in the VIP

salon : she immediatly posts the photos on Wechat

Brand app

Wei Na has chosen a blue-print dress from the 2015 Cruise show and has collected her grey-lezard bag : she pays her purchases with

her Iphone on the brand app

Brand app Brand app Sales assistant

Wei Na photos receive 1 200 likes. A few friends ask her : « And why

not the red dress look 28 from SS2015?! »

The brand App help her find the

best addresses to go to that are also recommended

by the brand community

Wei Na goes in holidays in Cannes. Wei Na is invited

to a very hype party in Cannes but she has not

the righ dress for this particular

event. She posts a message on the brand App

Her sales assistant from Hangzhou calls her : « We have arranged

everything with the Cannes boutique

that will lend you a dress for the

event »: the red dress look 28 from

SS2015

McKinsey & Company | 30

Revisit the way you engage with your consumers

Geo-localized campaigns

Shop directly from social media

Enrich digital content with offline media

Create social buzz and advocacy