Embed Size (px)

Citation preview

Digital BankingInvestor Relations Meeting 8th November 2014

V1

Digital BankingDigitalization seminar, 11th November 2014 Christian Bornfeld, Head of Digital Banking

1. Nordea highlights

2. Customer behaviours & competitive dynamics

3. Digital Banking & the future relationship bank

Nordea highlights

3

Financial results Q314Income holding up despite continued macro headwind, low interest rates and low volatilityCapital gain of EUR 378m related to sale of NetsCost programme delivering according to plan (5% decrease in 2015 vs. 2013 in local currencies on-track)Loan losses are down to 12 bps, below 10 year average Operating profit up 7% YTD (EUR 3,324m)* CET 1 ratio improved 40 bps to 15.6%RoE is up 30 bps YTD to 11.5%*

* Excluding non-recurring items in Q2/14 and Q3/14

Building the future relationship bankChanging customer behaviour and increasing level of operational regulationsIncrease agility, scale and resilienceNew core banking and payment platformsAvg annual increase in IT investments of approx. 30-35% over the coming 4-5 yearsImpairment charge of EUR 344m

1. Nordea highlights

2. Customer behaviours & competitive dynamics

3. Digital Banking & the future relationship bank

Customer behaviours and expectations are changing rapidly

The Internet, smartphones and apps drive customers who are increasingly

connectedknowledgeableempowered& impatient

5 •

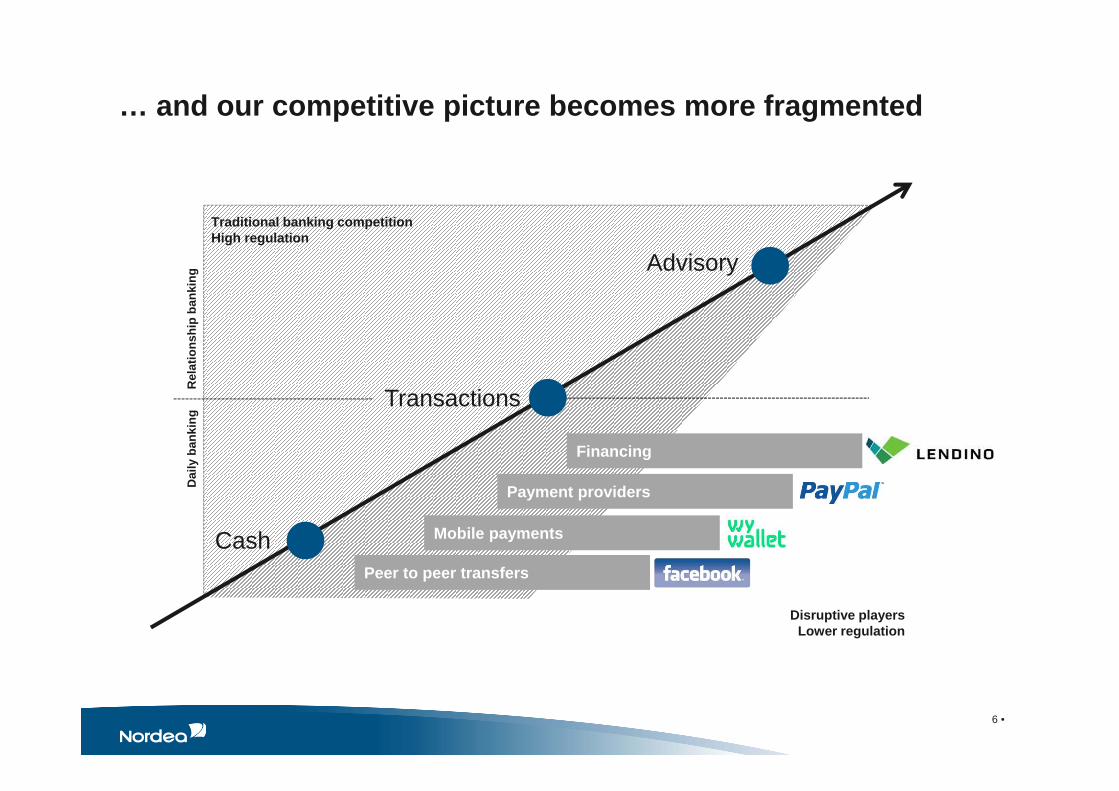

… and our competitive picture becomes more fragmented

Cash

Transactions

Advisory

Traditional banking competitionHigh regulation

Peer to peer transfers

Financing

Mobile payments

Payment providers

Disruptive playersLower regulation

Rel

atio

nshi

p ba

nkin

gD

aily

ban

king

6 •

New behaviours are impacting on all of Nordea’s touch-points

7 •

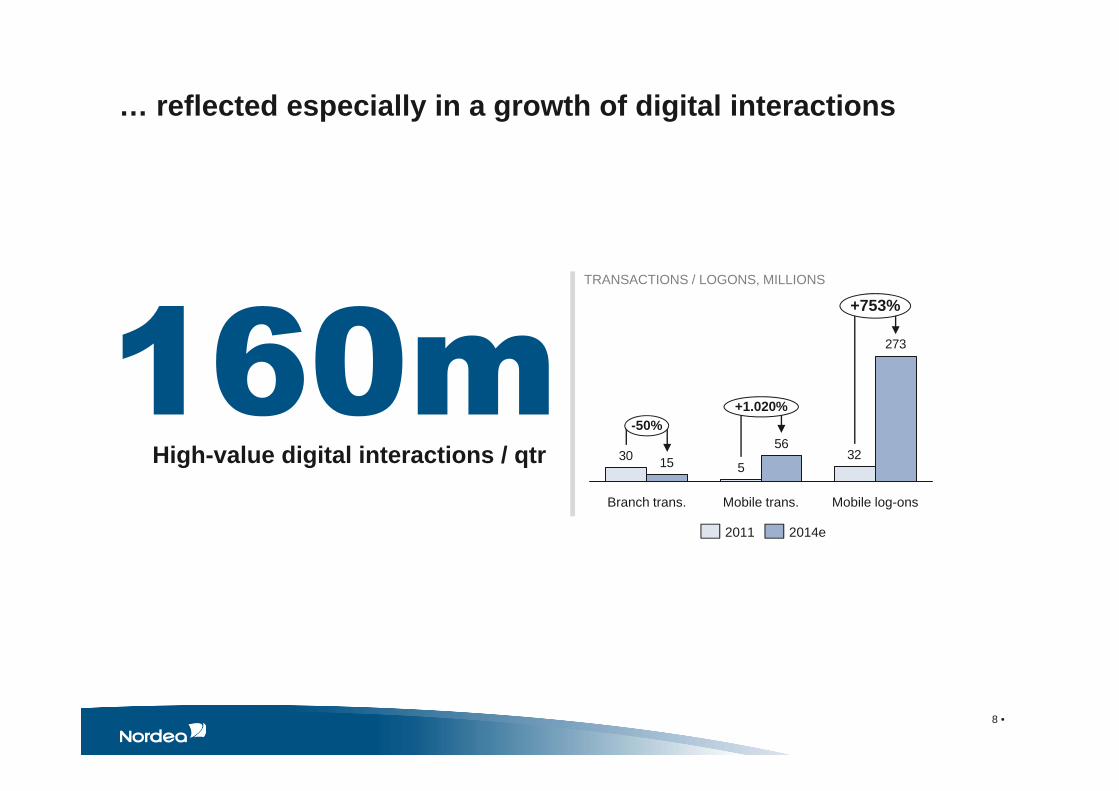

TRANSACTIONS / LOGONS, MILLIONS

8 •

High-value digital interactions / qtr

… reflected especially in a growth of digital interactions

325

30

273

5615

+1.020%-50%

Mobile trans. Mobile log-onsBranch trans.

+753%

2011 2014e

But interactions need to be converted to loyalty and sales

Our business opportunity lies in converting primarily transactionalinteractions, into value creatingdialogues and thereby loyaltyand sales

Making the relationship digital

9 •

High-value digital interactions / qtr

1. Nordea highlights

2. Customer behaviours & competitive dynamics

3. Digital Banking & the future relationship bank

We will address the well established Relational Banking model

Classic relationship banking

Personal relationship

Knowledge

Responsive

11 •

… and through digitalization, make it scalable for the future

Convenience

Personal

Trust

12 •

Analytics, learning & automation

Digitally enabledrelationship banking

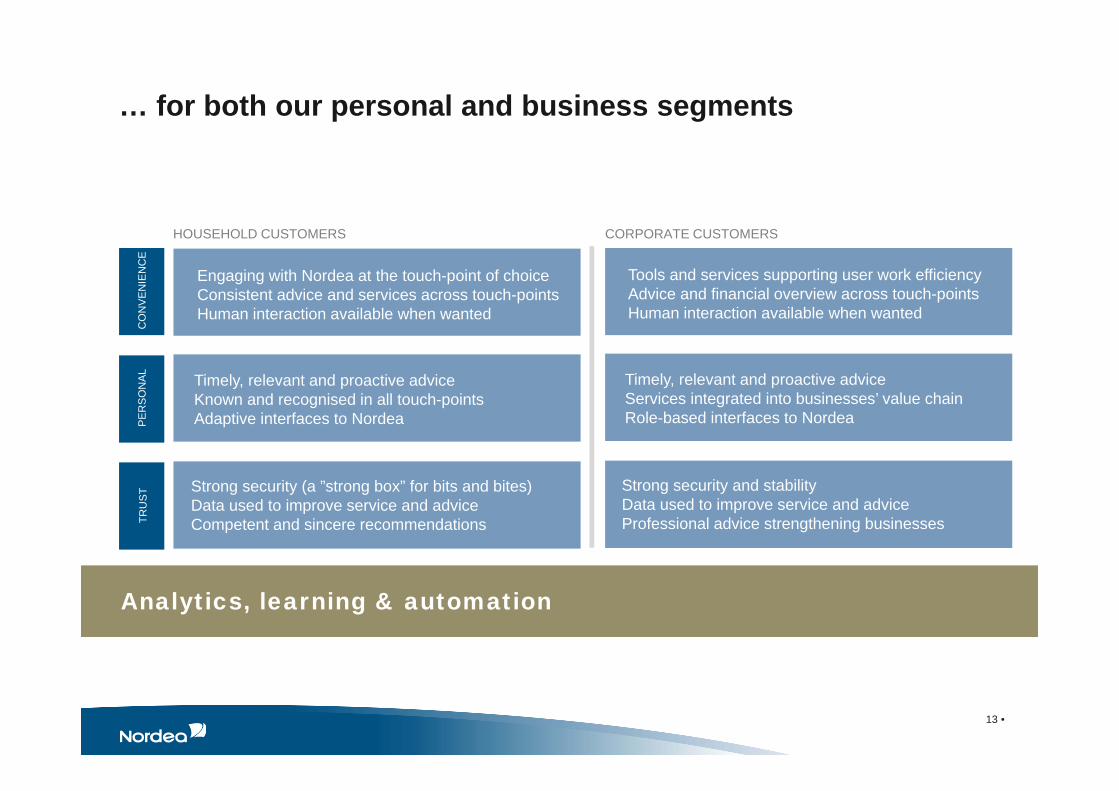

… for both our personal and business segments

13 •

Analytics, learning & automation

Engaging with Nordea at the touch-point of choiceConsistent advice and services across touch-points Human interaction available when wanted

HOUSEHOLD CUSTOMERS CORPORATE CUSTOMERS

Timely, relevant and proactive adviceKnown and recognised in all touch-pointsAdaptive interfaces to Nordea

Strong security (a ”strong box” for bits and bites) Data used to improve service and adviceCompetent and sincere recommendations

CO

NV

EN

IEN

CE

PE

RS

ON

AL

TRU

ST

Tools and services supporting user work efficiencyAdvice and financial overview across touch-points Human interaction available when wanted

Timely, relevant and proactive adviceServices integrated into businesses’ value chainRole-based interfaces to Nordea

Strong security and stability Data used to improve service and adviceProfessional advice strengthening businesses

… allowing us to better serve more customer groups

BUSINESS IMPACT

14 •

Greatly widen target groups for salesIncrease loyaltyLower cost to serveImprove channel mix & productivity

Analytics, learning & automation

BREAKING THE 80 / 20 RULE

Broaden engagement across all touch points

Service combining people & technology

Customer knowledge in all touch-points

Customer dialogue

Tailored solutions

Scalable Nordic ideas

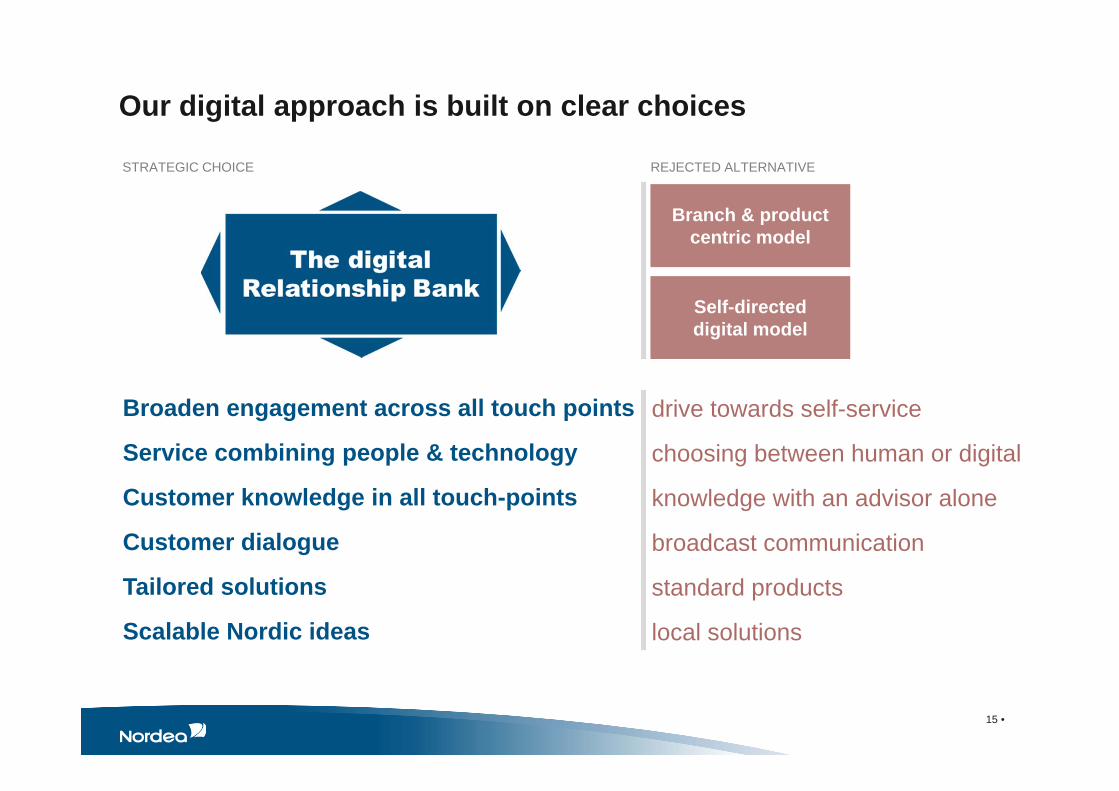

Our digital approach is built on clear choices

Branch & product centric model

Self-directed digital model

drive towards self-service

choosing between human or digital

knowledge with an advisor alone

broadcast communication

standard products

local solutions

REJECTED ALTERNATIVE

15 •

STRATEGIC CHOICE

… and enabled by establishing a dedicated business unit

Responsible for the full value chain

Combining business expertise and creativity with technical knowledge

Change agent to ensure momentum

DIGITAL BANKING SOLUTION PRINCIPLES

Think in end-to-end customer journeys

Leverage analytics and respect data privacy

No physical meetings required

Digital signing / paperless processes

Same front-end for assisted & self-service

Utilize existing public infrastructures

Mobile-first approach to Household

16 •

DIGITAL BANKING

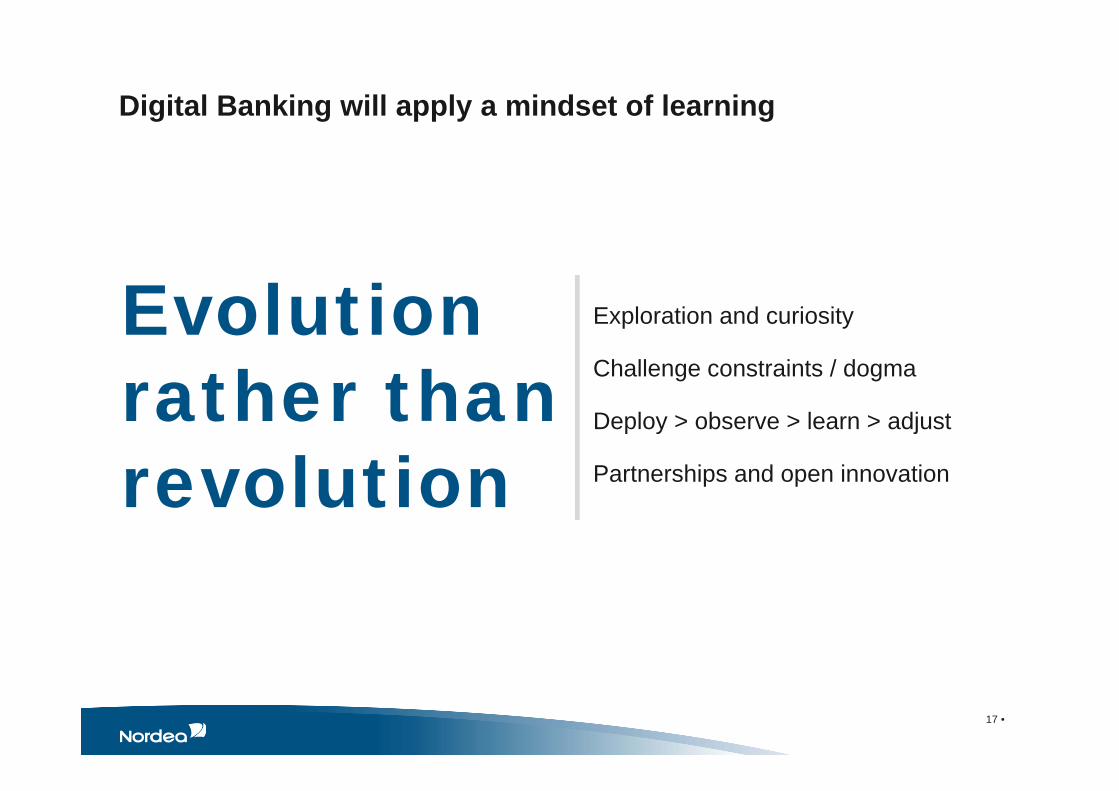

Digital Banking will apply a mindset of learning

Exploration and curiosity

Challenge constraints / dogma

Deploy > observe > learn > adjust

Partnerships and open innovation

Evolution rather than revolution

17 •

…and of collaboration

Evolution rather thanrevolution

18 •

28th – 30th November 2014

The first steps in a longer journey are being implemented

19

Additional investments in online- and mobile – significantly increasing speed of development

Remote meetings rolled out in all countries – improved flexibility for customers in terms of timing and place

Re-mortgaging process automated in Denmark – significantly reducing manual work and drastically decreasing paper send to customers (900,000 letters) and internally (3,500 kg of paper)

Data driven sales pilot in Sweden - targeting mass market customers in Sweden with strong early results

Contact centre improvements in Finland and Norway – chat services, improved identification measures, etc. improving efficiency and customer experience

1

2

3

4

5

…and the priorities for digital transformation are clear

20

Deliver to customers

Build capabilities

Efficiency and agility through simplification

Advanced analytics capabilities feeding all touch-points

New ways of working with customers and partners

Digital marketing/sales competencies & operating model

Simple yet comprehensive 24/7 digital offering for both household and corporate customers

Personalised to reflect customer needs and preferences

Enable key end-to-end customer journeys by combining the strengths of the various touch-points

Straight-through fulfilment

Nordic solutions that leverage the scale of Nordea

Prepare for adoption of new banking platforms

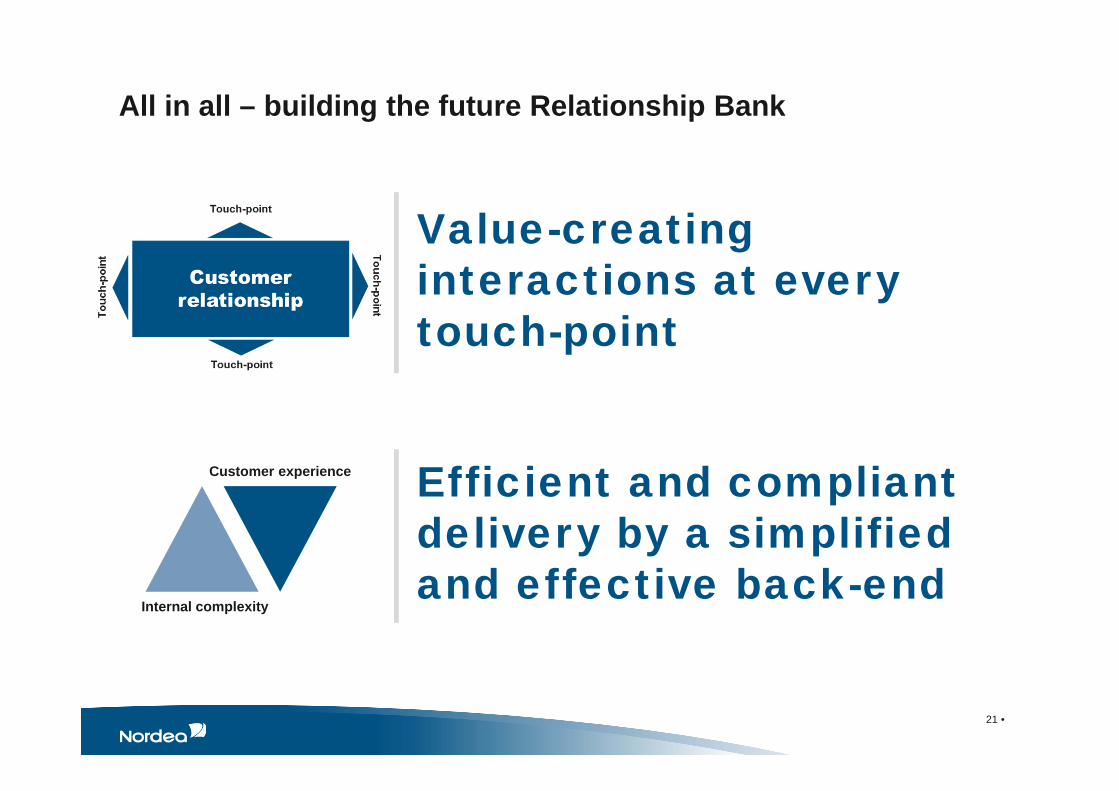

All in all – building the future Relationship Bank

Value-creating interactions at every touch-point

Efficient and compliant delivery by a simplified and effective back-end

21 •

Customer experience

Internal complexity

22 •

Thank you!

Appendix

25

EURm Q3/14 Q2/14 Chg % Q3/14YTD

Q3/13YTD

Chg %

Net interest income 1,396 1,368 2 4,126 4,135 0 3

Net fee & commission income 667 708 -6 2,079 1,939 7 10

Net fair value result 291 356 -18 1,058 1,206 -12 -11

Total income* 2,754 2,456 12 7,711 7,422 4 7

Total income** 2,376 2,456 -3 7,333 7,422 -1 2

Staff costs -728 -907 -20 -2,391 -2,239 7 10

Other expenses -788 -479 65 -1,748 -1,518 15 18

Total expenses -1,516 -1,386 9 -4,139 -3,757 10 13

Total expenses** -1,172 -1,196 -2 -3,605 -3,757 -4 -1

Profit before loan losses** 1,204 1,260 -4 3,728 3,665 2 4

Net loan losses -112 -135 -17 -405 -555 -27 -25

Operating profit 1,126 935 20 3,167 3,110 2 4

Operating profit** 1,093 1,125 -3 3,324 3,110 7 9

Net profit cont. operations 938 716 31 2,494 2,347 6 3

Return on equity (%) 11.2 12.0 -80bps 11.5 11.2 +30bps -

CET1 capital ratio (%) 15.6 15.2 +40bps 15.6 14.4 +120bps -

Cost/income ratio (%) 49 49 unchanged 49 51 -200bps -

* Includes other income**Excluding non-recurring items (Re-structuring charge in Q2, Nets and IT impairment in Q3)

Nordea Financial Results Q314

The leading Nordic retail bank

26

EURm Q3/14 Q2/14 Chg % Q3/14YTD

Q3/13YTD

Chg %

Net interest income 963 952 1 2 854 2 862 0 3

Net fee & commission income 277 264 5 819 770 6 10

Net fair value result 75 95 -21 269 286 -6 -3

Total income 1 323 1 319 0 3 970 4 001 -1 2

Staff costs -329 -336 -2 -1 003 -1 028 -2 0

Total expenses -687 -713 -4 -2 118 -2 210 -4 -1

Profit before loan losses 636 606 5 1 852 1 791 3 7

Net loan losses -86 -119 -28 -329 -333 -1 -1

Operating profit 550 487 13 1 523 1 458 4 8

Retail Banking result Q3/14

Retail Banking contribution*

Operating income Operating profit FTE’s Lending Deposits

54% 45% 59% 67% 60%

* FY 2013

Digital BankingInvestor Relations Meeting 8th November 2014

V1

Digital BankingDigitalization seminar, 11th November 2014 Christian Bornfeld, Head of Digital Banking