Embed Size (px)

Citation preview

DEVELOPMENT OF THE REAL ESTATE MARKET IN PRAGUE

Praha, 27 January 2011

David Dušek, Real Estate Appraisal Section

2

Table of Contents

Flat market in Prague

Office market in Prague

3

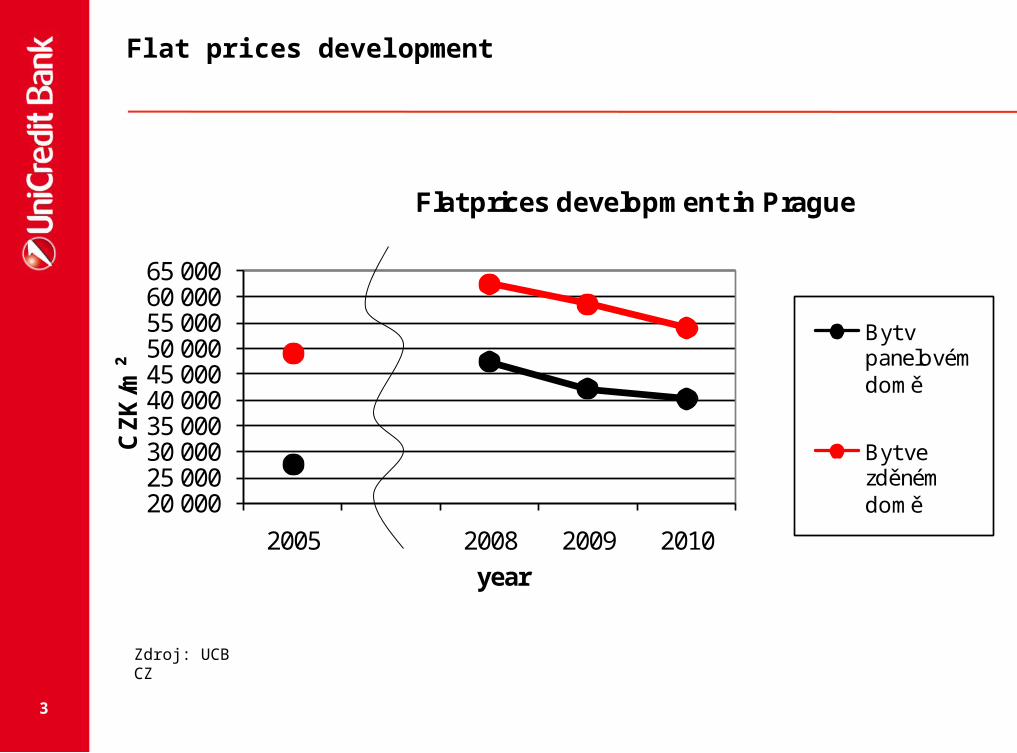

Flat prices development

20 00025 00030 00035 00040 00045 00050 00055 00060 00065 000

2005 2008 2009 2010

CZ

K/m

²

year

Flat prices development in Prague

Byt v panelovém domě

Byt ve zděném domě

Zdroj: UCB CZ

4

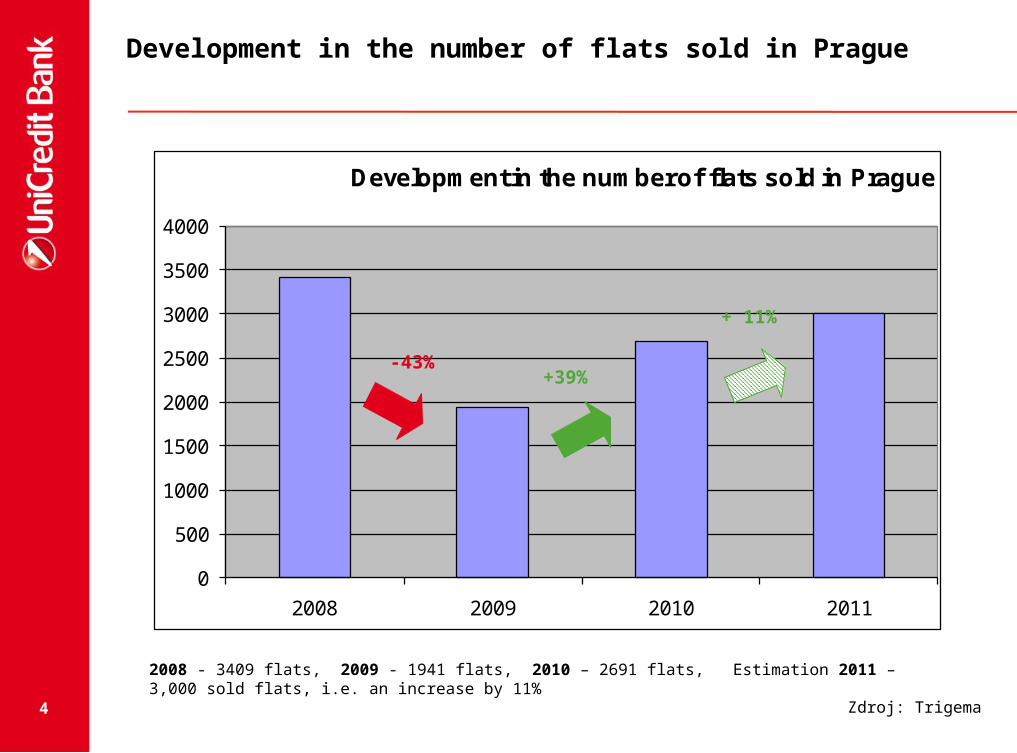

Development in the number of flats sold in Prague

0

500

1000

1500

2000

2500

3000

3500

4000

2008 2009 2010 2011

Development in the number of flats sold in Prague

2008 - 3409 flats, 2009 - 1941 flats, 2010 – 2691 flats, Estimation 2011 – 3,000 sold flats, i.e. an increase by 11%

-43%+39%

+ 11%

Zdroj: Trigema

5

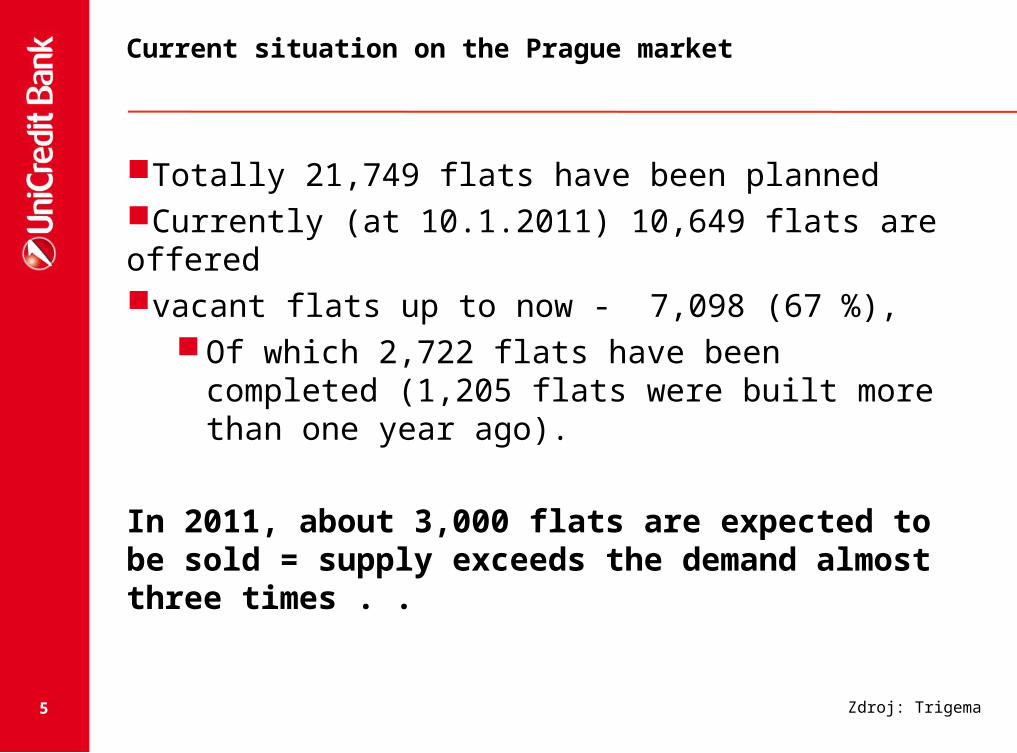

Current situation on the Prague market

Totally 21,749 flats have been planned Currently (at 10.1.2011) 10,649 flats are offeredvacant flats up to now - 7,098 (67 %),

Of which 2,722 flats have been completed (1,205 flats were built more than one year ago).

In 2011, about 3,000 flats are expected to be sold = supply exceeds the demand almost three times . .

Zdroj: Trigema

6

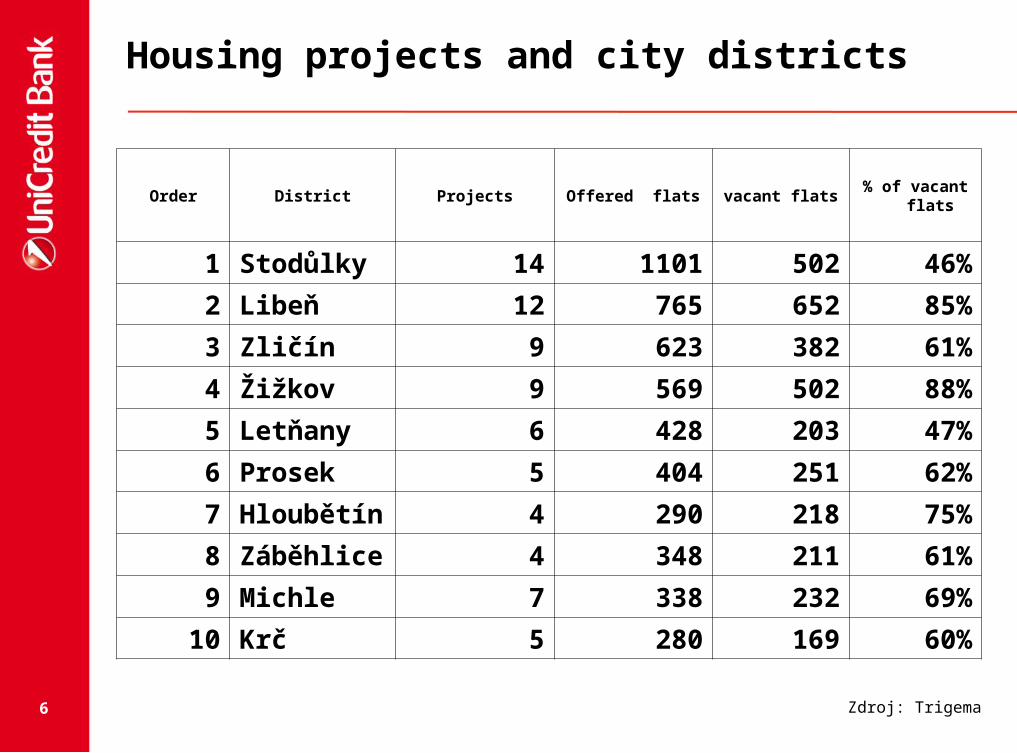

Housing projects and city districts

Order District Projects Offered flats vacant flats% of vacant

flats

1 Stodůlky 14 1101 502 46%

2 Libeň 12 765 652 85%

3 Zličín 9 623 382 61%

4 Žižkov 9 569 502 88%

5 Letňany 6 428 203 47%

6 Prosek 5 404 251 62%

7 Hloubětín 4 290 218 75%

8 Záběhlice 4 348 211 61%

9 Michle 7 338 232 69%

10 Krč 5 280 169 60%

Zdroj: Trigema

7

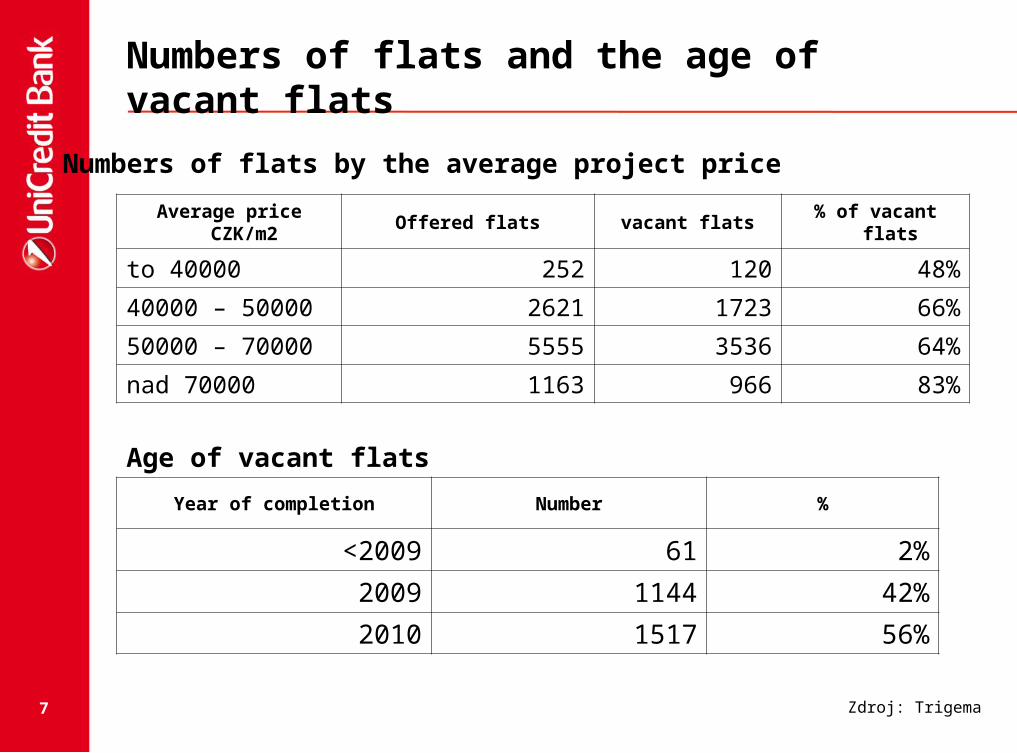

Numbers of flats and the age of vacant flats

Average price CZK/m2 Offered flats vacant flats % of vacant flats

to 40000 252 120 48%

40000 – 50000 2621 1723 66%

50000 – 70000 5555 3536 64%

nad 70000 1163 966 83%

Age of vacant flats

Year of completion Number %

<2009 61 2%

2009 1144 42%

2010 1517 56%

Numbers of flats by the average project price

Zdroj: Trigema

8

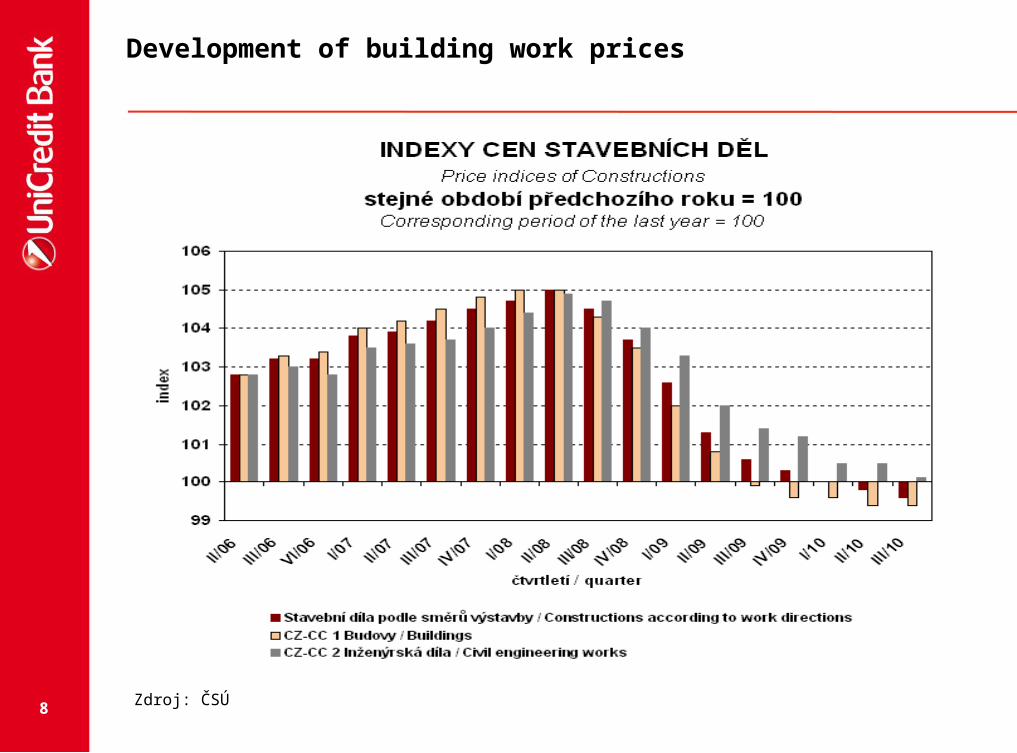

Development of building work prices

Zdroj: ČSÚ

9

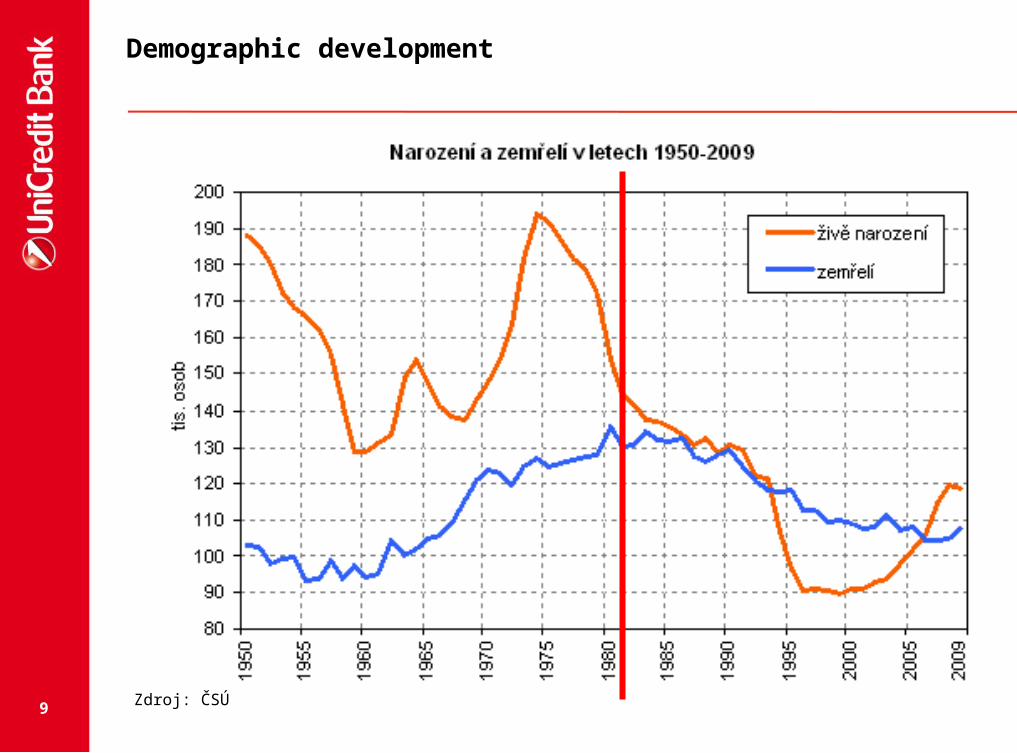

Demographic development

Zdroj: ČSÚ

10

Outlook 2010 - 2012

Work will be halted on a considerable part of large projects being prepared

Speculative developer companies will disappear and the market will be cleaned

New projects will be rather of an intimate character underlining the locality and/or price + sporadic attempts at the more extensive construction

A lower price level of building work and materials together with the supply and demand interaction will reflect in a lower price of newly offered flats.

Dependence on both the economic and demographic development

11

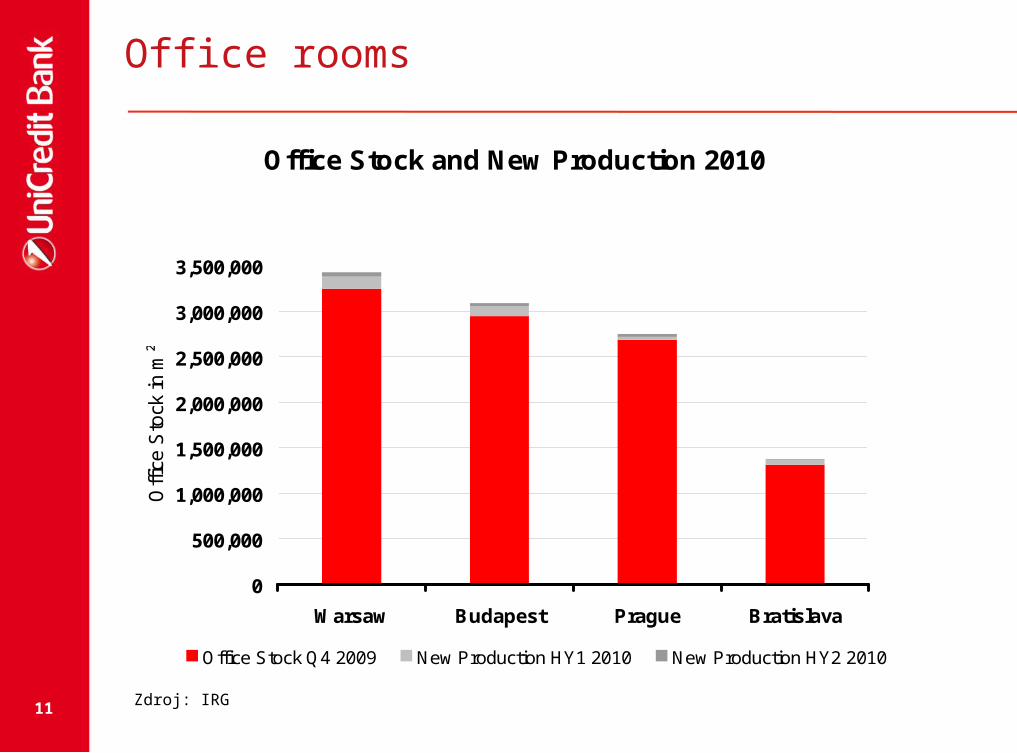

Office rooms

IRG Market Research | Operative Committee Meeting | 17.11.2010IRG Market Research | Operative Committee Meeting | 17.11.2010

Office Stock and New Production 2010

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Warsaw Budapest Prague Bratislava

Offi

ce S

tock

in m

²

Office Stock Q4 2009 New Production HY1 2010 New Production HY2 2010

Zdroj: IRG

12

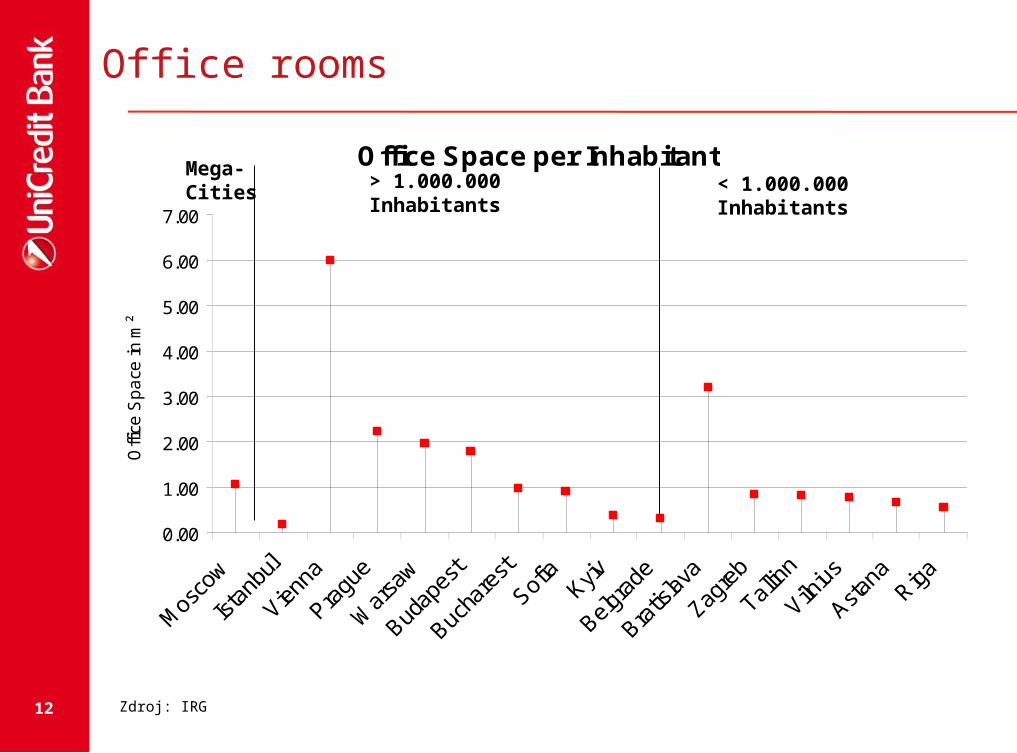

Office Space per Inhabitant

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Offi

ce S

pa

ce in

m²

Zdroj: IRG

Office rooms

IRG Market Research | Operative Committee Meeting | 17.11.2010

Mega-Cities

> 1.000.000 Inhabitants < 1.000.000 Inhabitants

IRG Market Research | Operative Committee Meeting | 17.11.2010

13

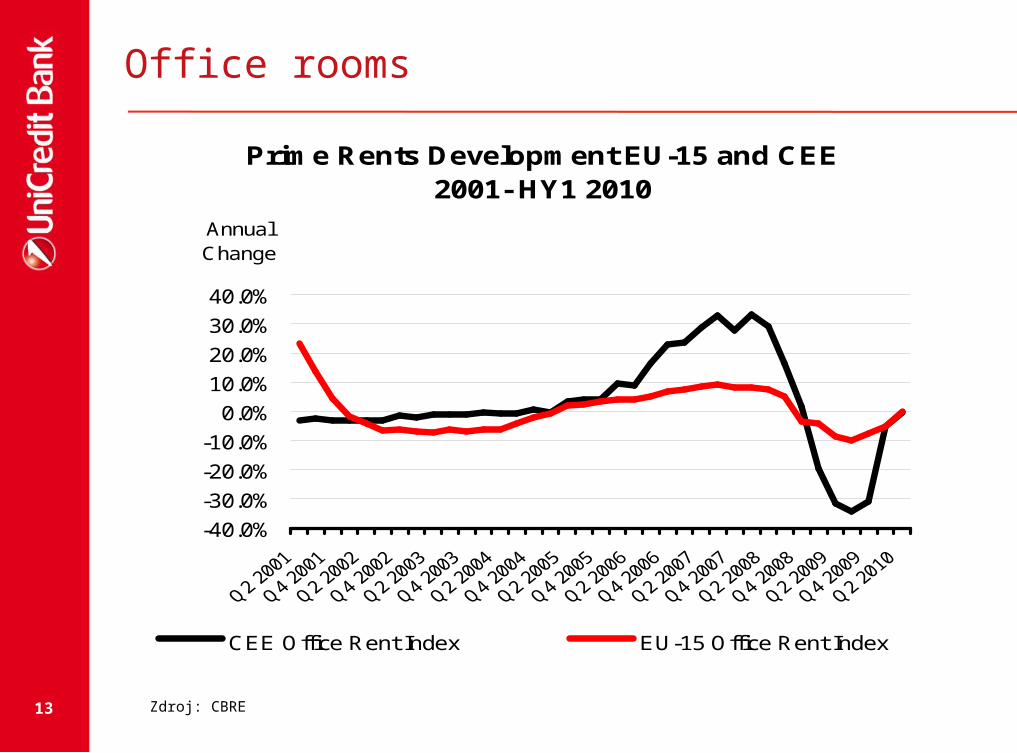

Prime Rents Development EU-15 and CEE2001- HY1 2010

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Annual Change

CEE Office Rent Index EU-15 Office Rent Index

Office rooms

IRG Market Research | Operative Committee Meeting | 17.11.2010Zdroj: CBRE

IRG Market Research | Operative Committee Meeting | 17.11.2010

14IRG Market Research | Operative Committee Meeting | 17.11.2010

Va

ca

nc

y R

ate

/Yie

lds

in %

Re

nts

Eu

ro/m

²/M

on

th

IRG Market Research | Operative Committee Meeting | 17.11.2010

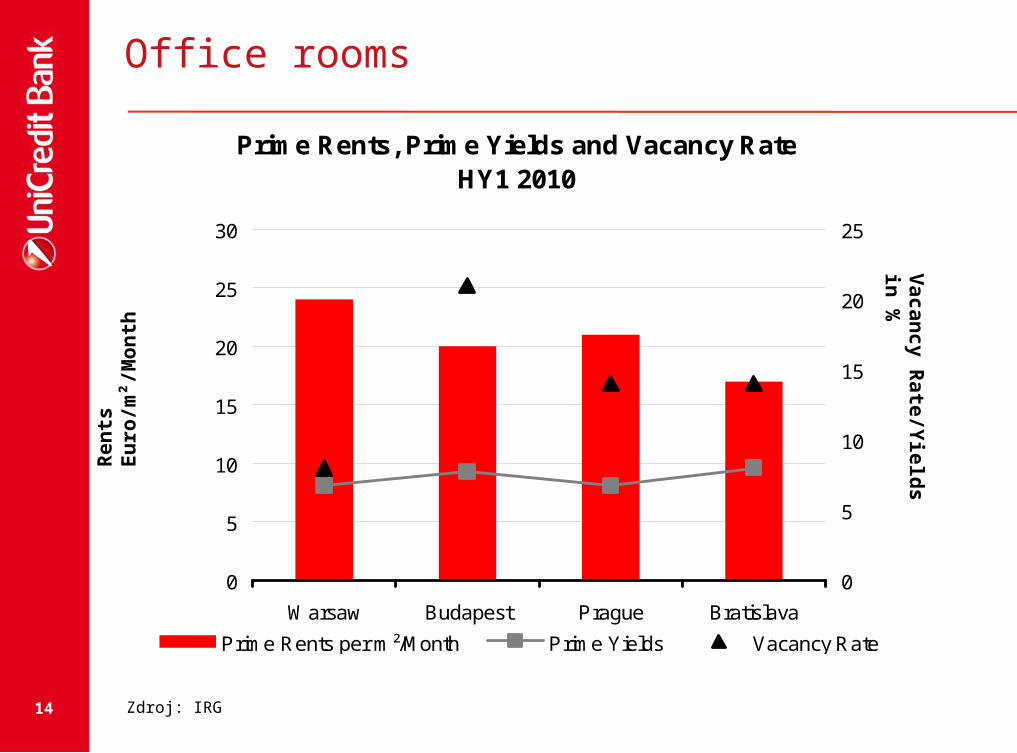

Prime Rents, Prime Yields and Vacancy Rate HY1 2010

0

5

10

15

20

25

30

Warsaw Budapest Prague Bratislava

0

5

10

15

20

25

Prime Rents per m²/Month Prime Yields Vacancy Rate

Office rooms

Zdroj: IRG

15IRG Market Research | Operative Committee Meeting | 17.11.2010

Prime Yields Development2007- HY1 2010

2%

3%

4%

5%

6%

7%

8%

9%

10%

2007 2008 2009 HY1 2010

Pri

me

Re

nts

in

%

Warsaw Budapest Prague Bratislava

Office rooms

Zdroj: IRG

16IRG Market Research | Operative Committee Meeting | 17.11.2010IRG Market Research | Operative Committee Meeting | 17.11.2010

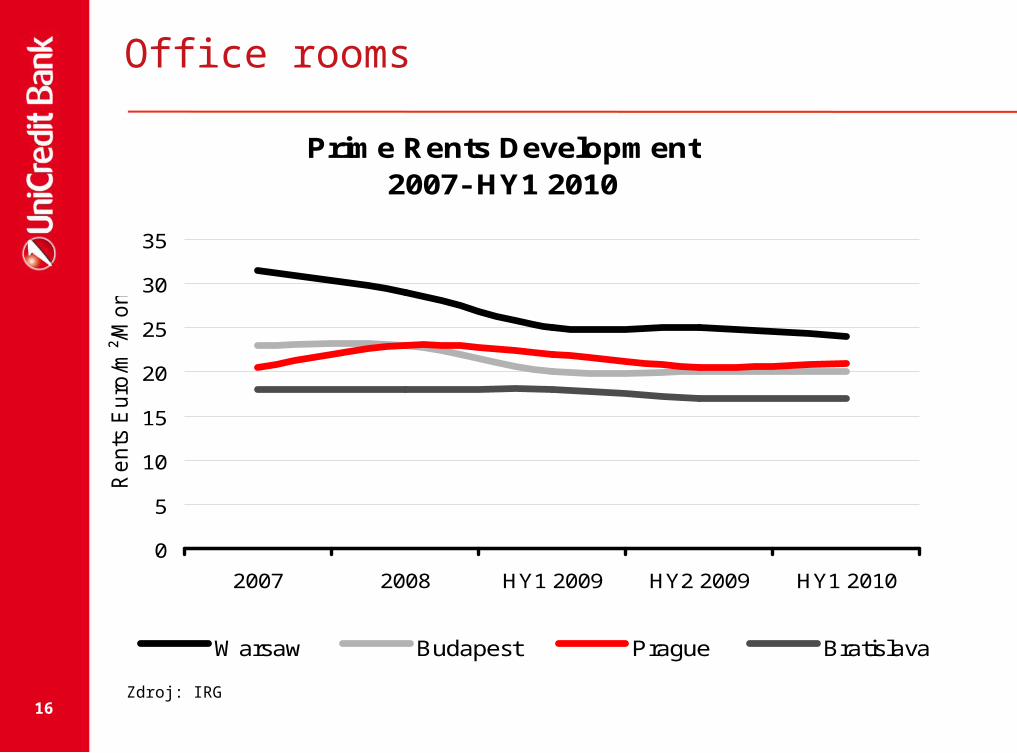

Prime Rents Development2007- HY1 2010

0

5

10

15

20

25

30

35

2007 2008 HY1 2009 HY2 2009 HY1 2010

Re

nts

Eu

ro/m

²/M

on

th

Warsaw Budapest Prague Bratislava

Office rooms

Zdroj: IRG

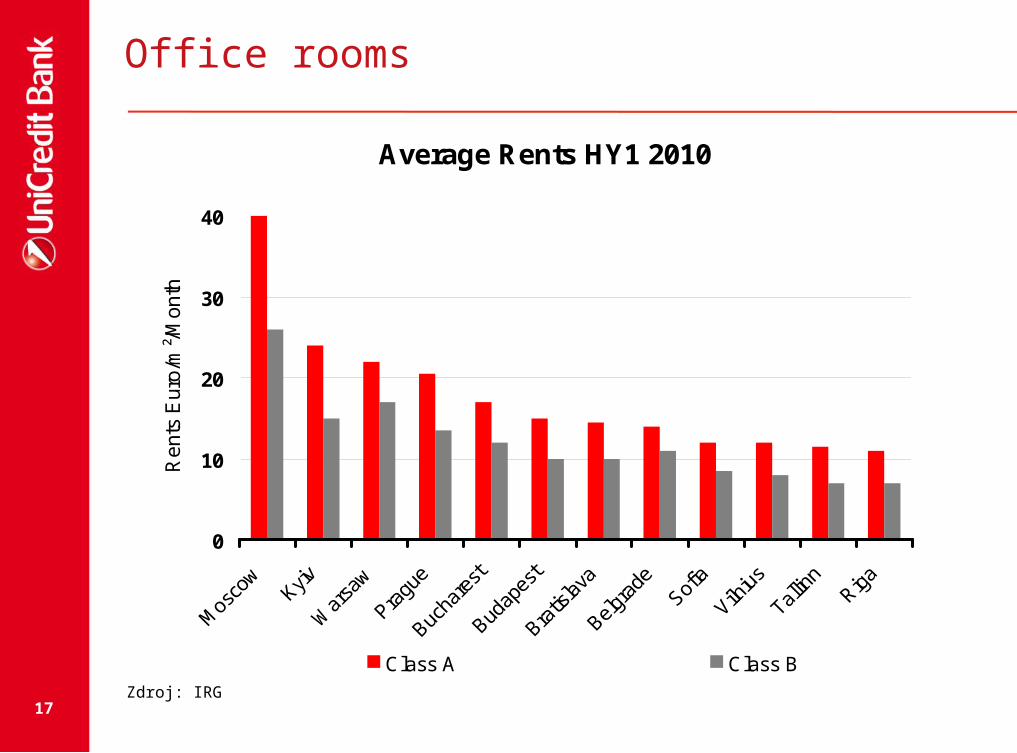

17IRG Market Research | Operative Committee Meeting | 17.11.2010IRG Market Research | Operative Committee Meeting | 17.11.2010

Average Rents HY1 2010

0

10

20

30

40

Rents

Euro

/m²/

Month

Class A Class B

Office rooms

Zdroj: IRG