Embed Size (px)

Citation preview

Development Impact Fees:Understanding the Current Law

Presented by

Andrew J. McGuire, Esq. Gust Rosenfeld PLC

Alternate Title:

Impact Fee Legislation:The Gift That Keeps On Giving

Recent History – Testing the Waters

2005 – HB 2066 (Striker)

Added annual reporting

Added penalty for not reporting

Recent History – Going for a Home Run

2006 – HB 2381 (Striker) Massive attack on DIFs Sweeping changes “to prevent cities

from doing stupid things like adopting plans for lakes they have no money to build.”

Defined list of public services

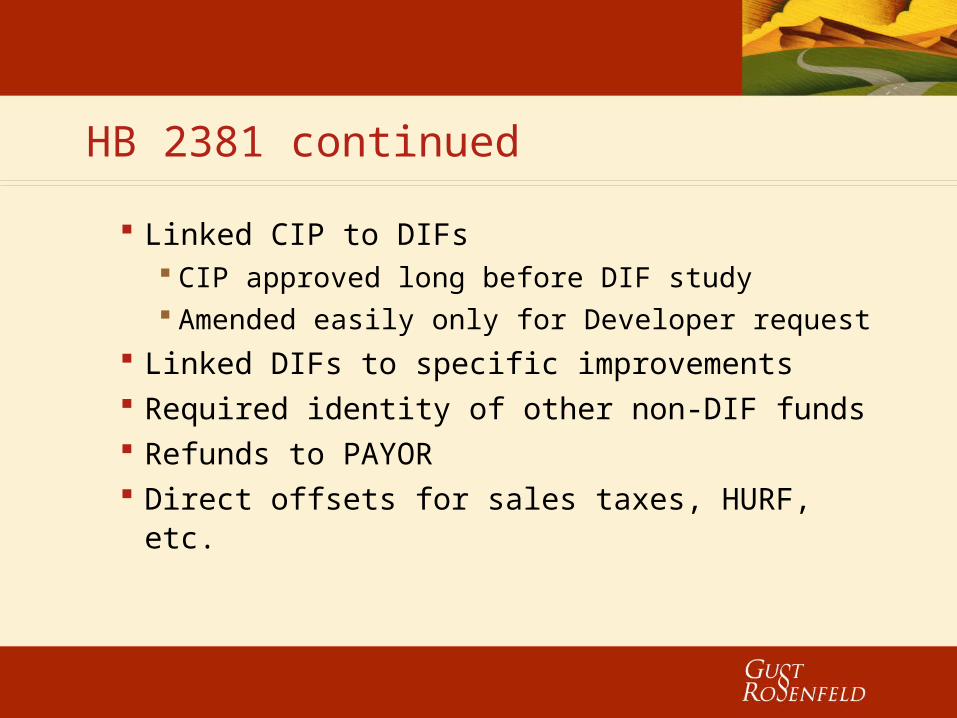

HB 2381 continued

Linked CIP to DIFs CIP approved long before DIF study Amended easily only for Developer request

Linked DIFs to specific improvements Required identity of other non-DIF funds Refunds to PAYOR Direct offsets for sales taxes, HURF, etc.

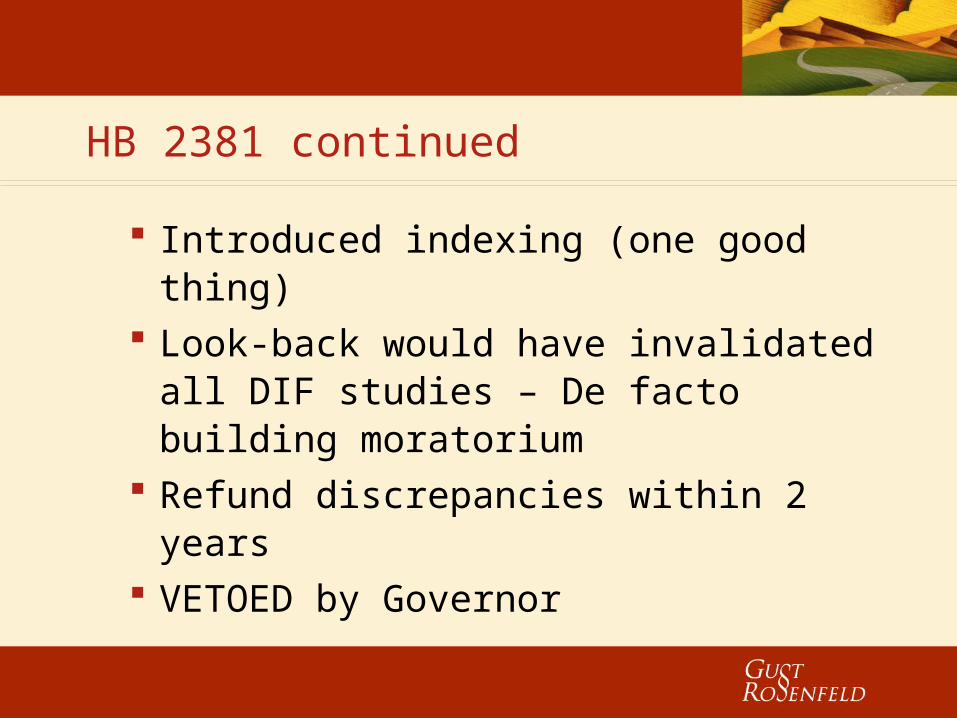

HB 2381 continued

Introduced indexing (one good thing) Look-back would have invalidated all

DIF studies – De facto building moratorium

Refund discrepancies within 2 years VETOED by Governor

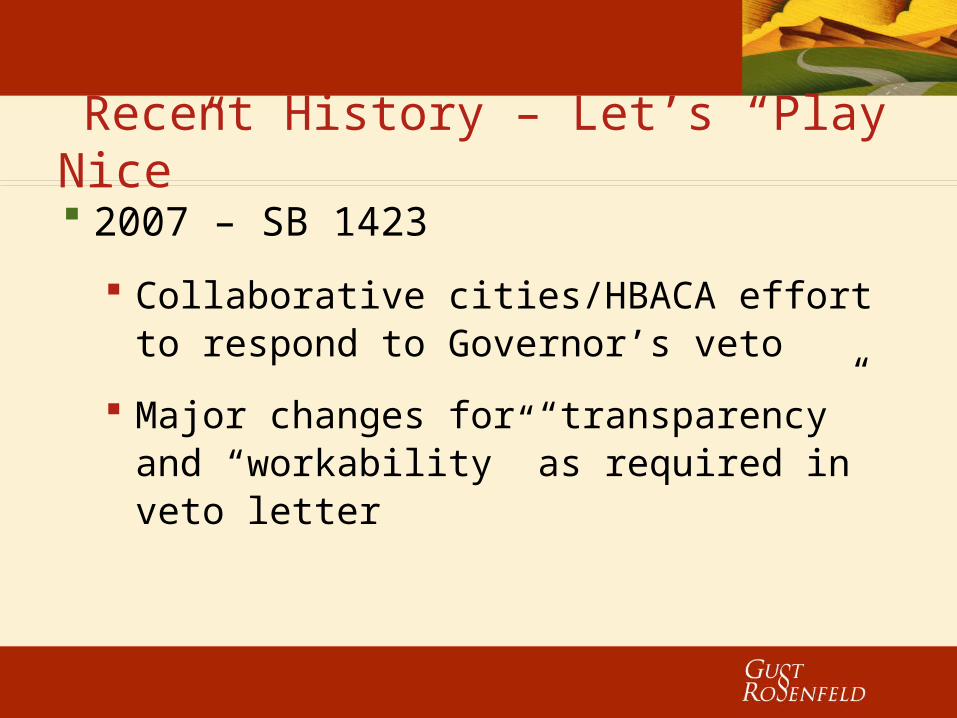

Recent History – Let’s “Play Nice” 2007 – SB 1423

Collaborative cities/HBACA effort to respond to Governor’s veto

Major changes for “transparency” and “workability” as required in veto letter

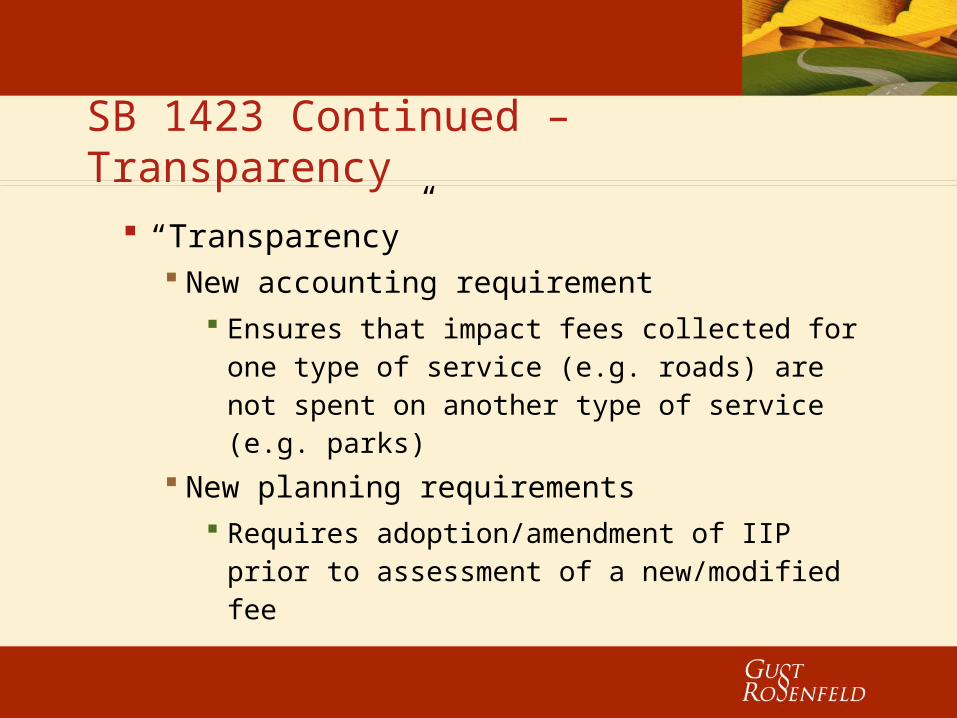

SB 1423 Continued – Transparency

“Transparency” New accounting requirement

Ensures that impact fees collected for one type of service (e.g. roads) are not spent on another type of service (e.g. parks)

New planning requirements Requires adoption/amendment of IIP prior

to assessment of a new/modified fee

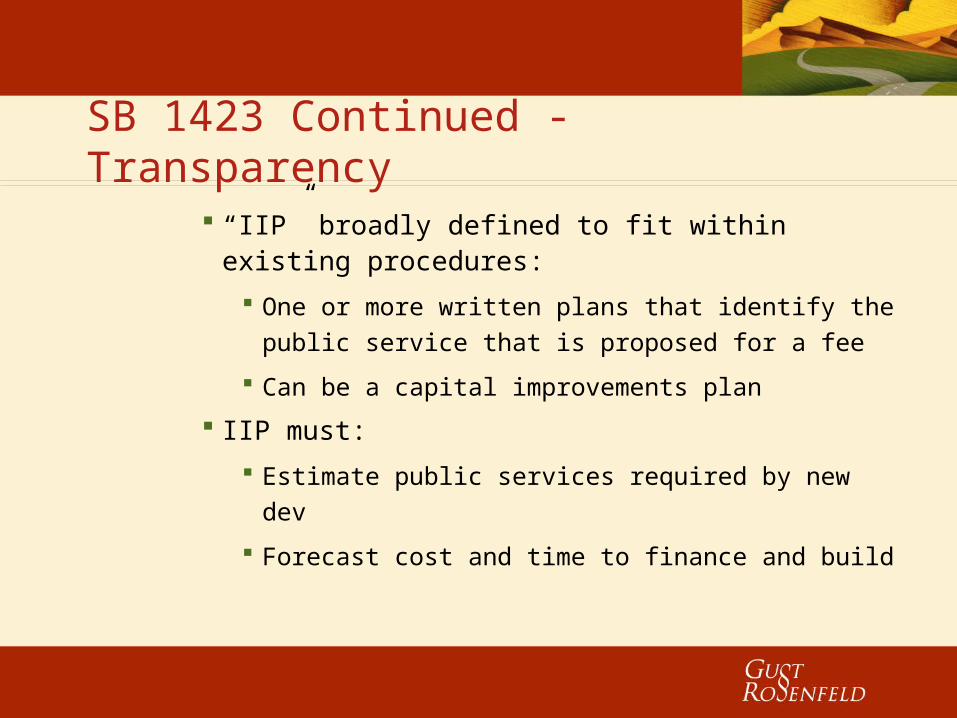

SB 1423 Continued - Transparency

“IIP” broadly defined to fit within existing procedures:

One or more written plans that identify the public service that is proposed for a fee

Can be a capital improvements plan

IIP must:

Estimate public services required by new dev

Forecast cost and time to finance and build

SB 1423 Continued - Transparency

IIP released to public 60 days in advance of hearing

Public hearing on IIP at least 30 days in advance of adoption

Public hearing may address both the IIP and the development fee report concurrently

IIP may be amended w/o hearing to allow shuffling w/n category (only 14-day notice of amendment required)

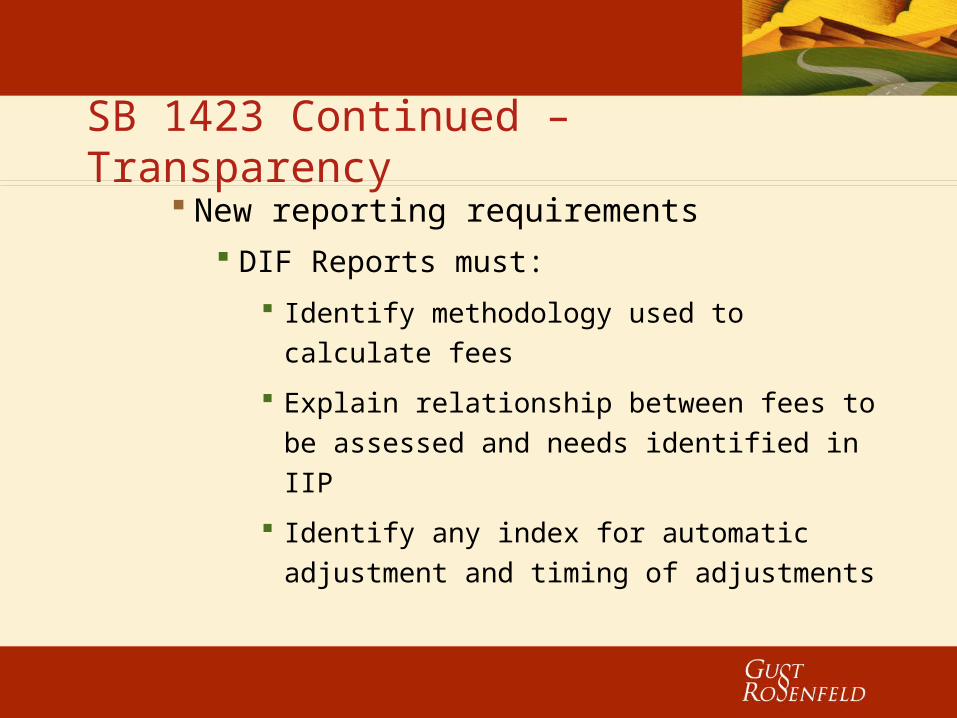

SB 1423 Continued – Transparency New reporting requirements

DIF Reports must:

Identify methodology used to calculate fees

Explain relationship between fees to be assessed and needs identified in IIP

Identify any index for automatic adjustment and timing of adjustments

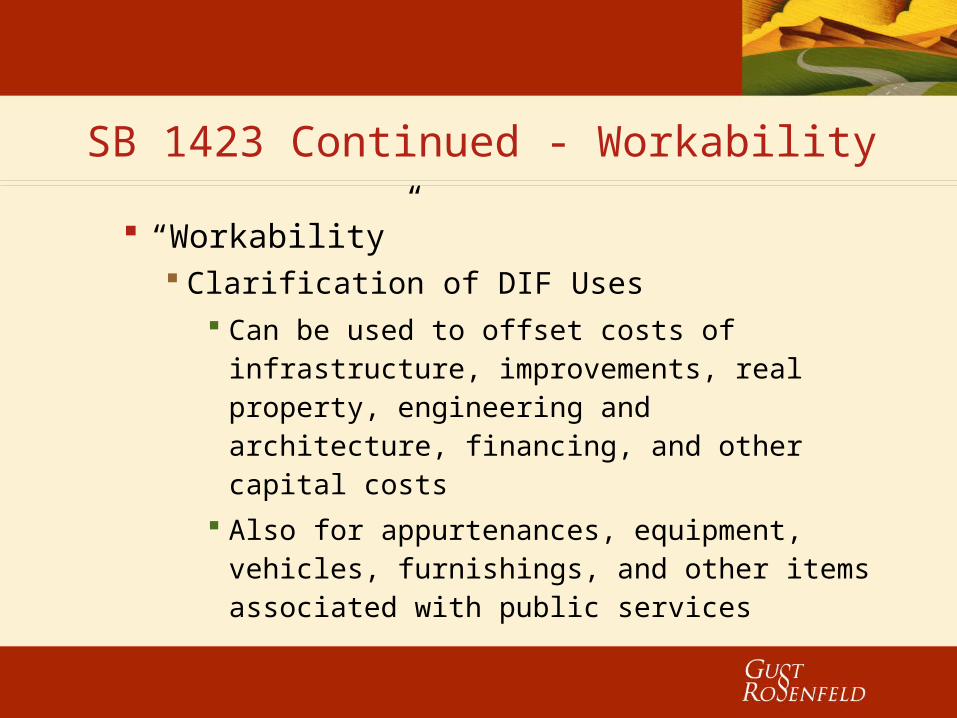

SB 1423 Continued - Workability

“Workability” Clarification of DIF Uses

Can be used to offset costs of infrastructure, improvements, real property, engineering and architecture, financing, and other capital costs

Also for appurtenances, equipment, vehicles, furnishings, and other items associated with public services

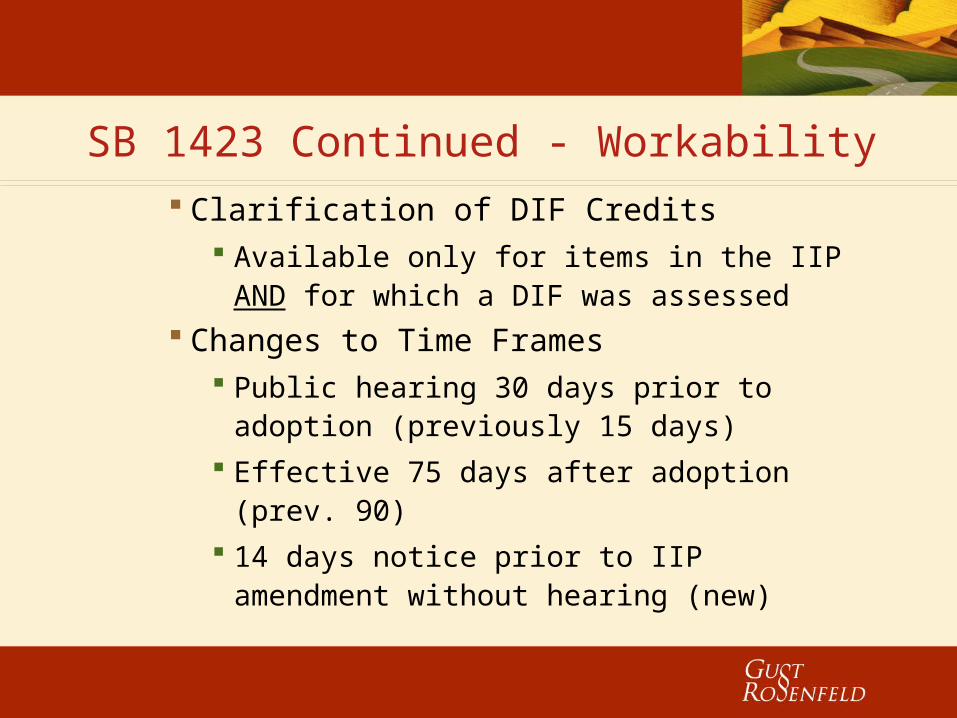

SB 1423 Continued - Workability Clarification of DIF Credits

Available only for items in the IIP AND for which a DIF was assessed

Changes to Time Frames Public hearing 30 days prior to adoption

(previously 15 days) Effective 75 days after adoption (prev.

90) 14 days notice prior to IIP amendment

without hearing (new)

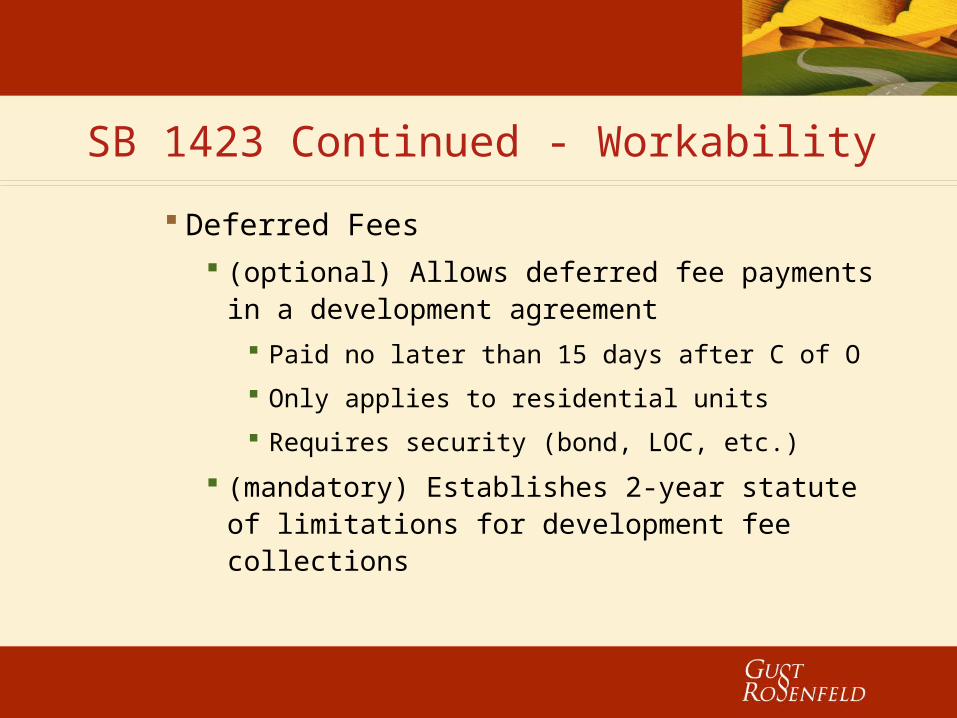

SB 1423 Continued - Workability

Deferred Fees (optional) Allows deferred fee payments in

a development agreement Paid no later than 15 days after C of O

Only applies to residential units

Requires security (bond, LOC, etc.)

(mandatory) Establishes 2-year statute of limitations for development fee collections

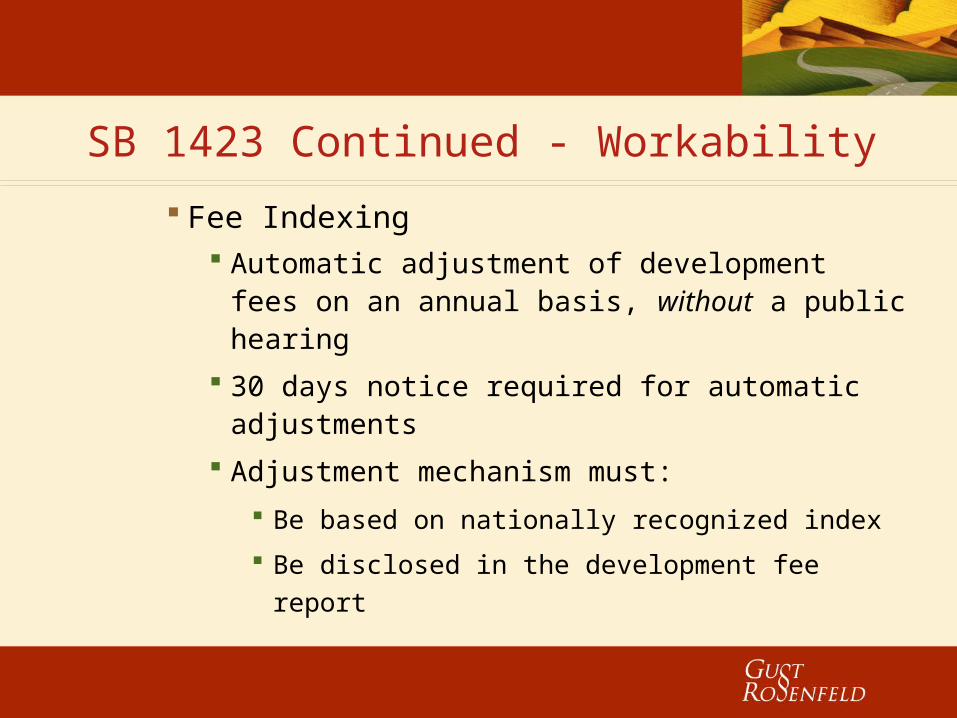

SB 1423 Continued - Workability

Fee Indexing Automatic adjustment of development

fees on an annual basis, without a public hearing

30 days notice required for automatic adjustments

Adjustment mechanism must:

Be based on nationally recognized index

Be disclosed in the development fee report

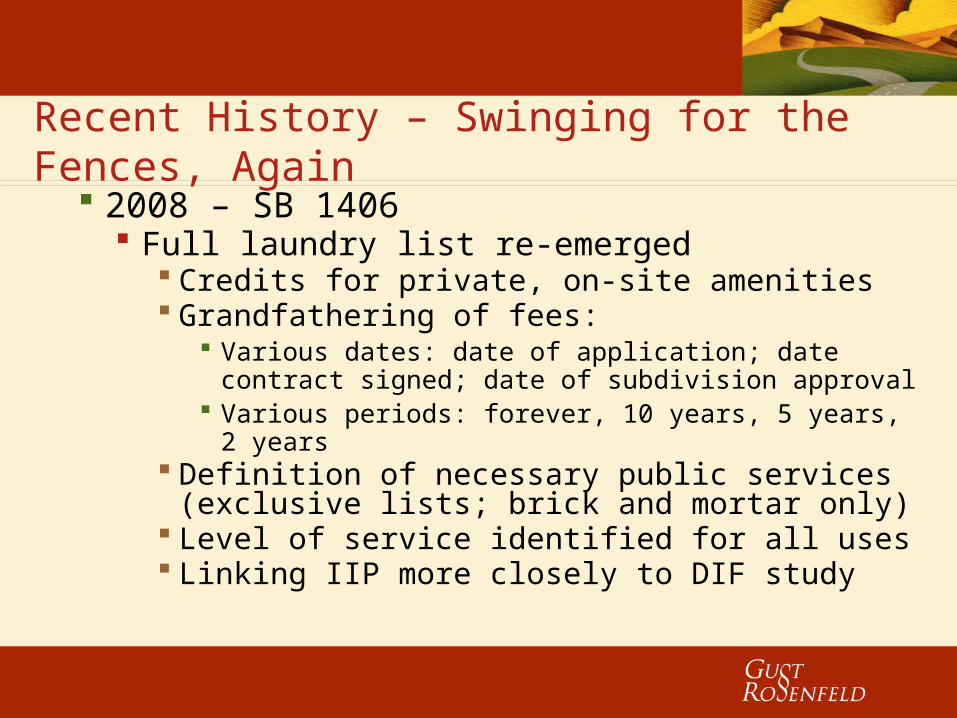

Recent History – Swinging for the Fences, Again

2008 – SB 1406 Full laundry list re-emerged

Credits for private, on-site amenities Grandfathering of fees:

Various dates: date of application; date contract signed; date of subdivision approval

Various periods: forever, 10 years, 5 years, 2 years

Definition of necessary public services (exclusive lists; brick and mortar only)

Level of service identified for all uses Linking IIP more closely to DIF study

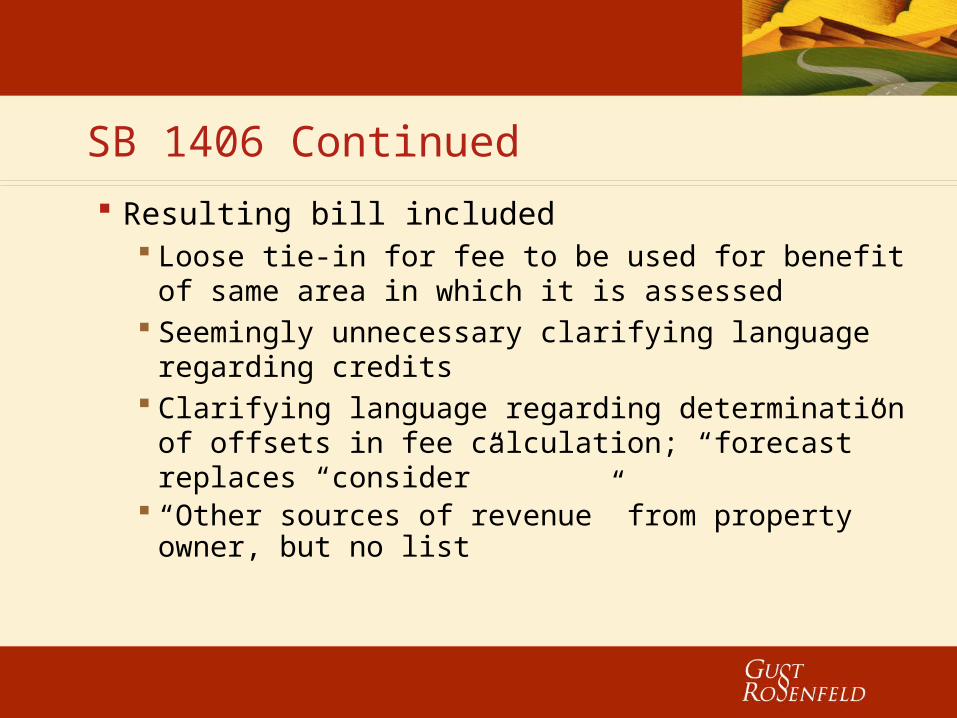

SB 1406 Continued

Resulting bill included Loose tie-in for fee to be used for benefit of

same area in which it is assessed Seemingly unnecessary clarifying language

regarding credits Clarifying language regarding determination

of offsets in fee calculation; “forecast” replaces “consider”

“Other sources of revenue” from property owner, but no list

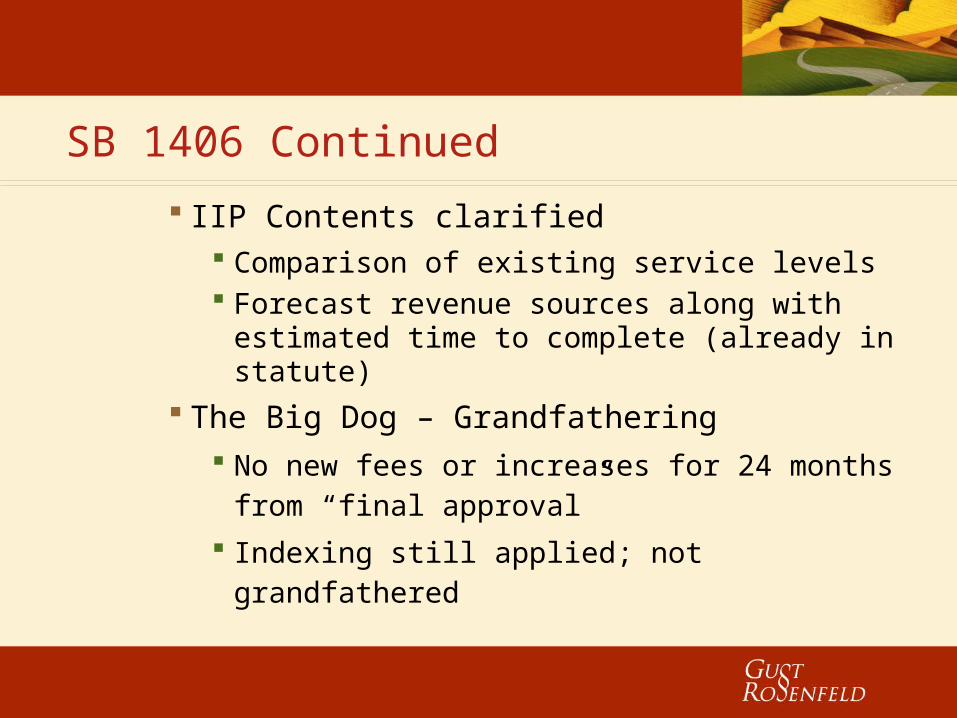

SB 1406 Continued

IIP Contents clarified Comparison of existing service levels Forecast revenue sources along with

estimated time to complete (already in statute)

The Big Dog – Grandfathering No new fees or increases for 24 months

from “final approval”

Indexing still applied; not grandfathered

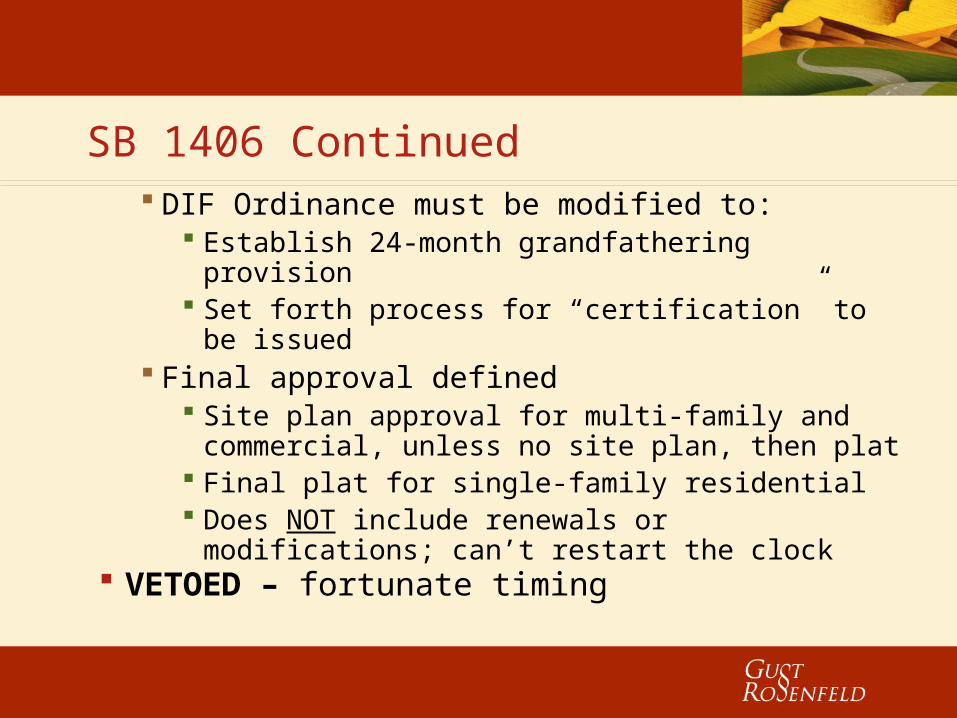

SB 1406 Continued DIF Ordinance must be modified to:

Establish 24-month grandfathering provision Set forth process for “certification” to be

issued Final approval defined

Site plan approval for multi-family and commercial, unless no site plan, then plat

Final plat for single-family residential Does NOT include renewals or modifications;

can’t restart the clock VETOED – fortunate timing

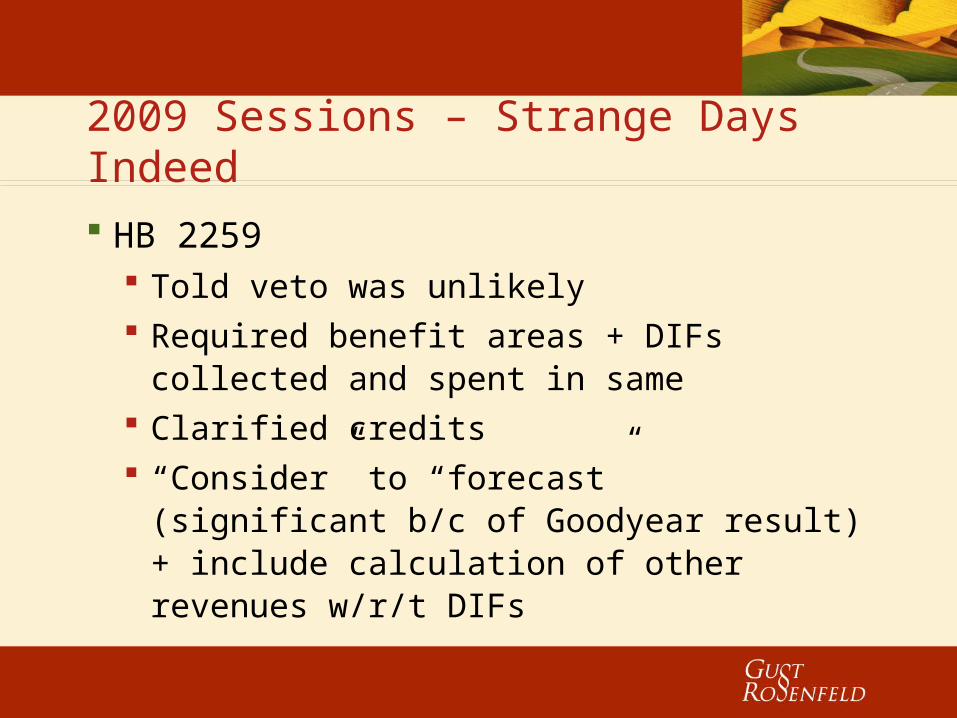

2009 Sessions – Strange Days Indeed

HB 2259 Told veto was unlikely Required benefit areas + DIFs

collected and spent in same Clarified credits “Consider” to “forecast” (significant

b/c of Goodyear result) + include calculation of other revenues w/r/t DIFs

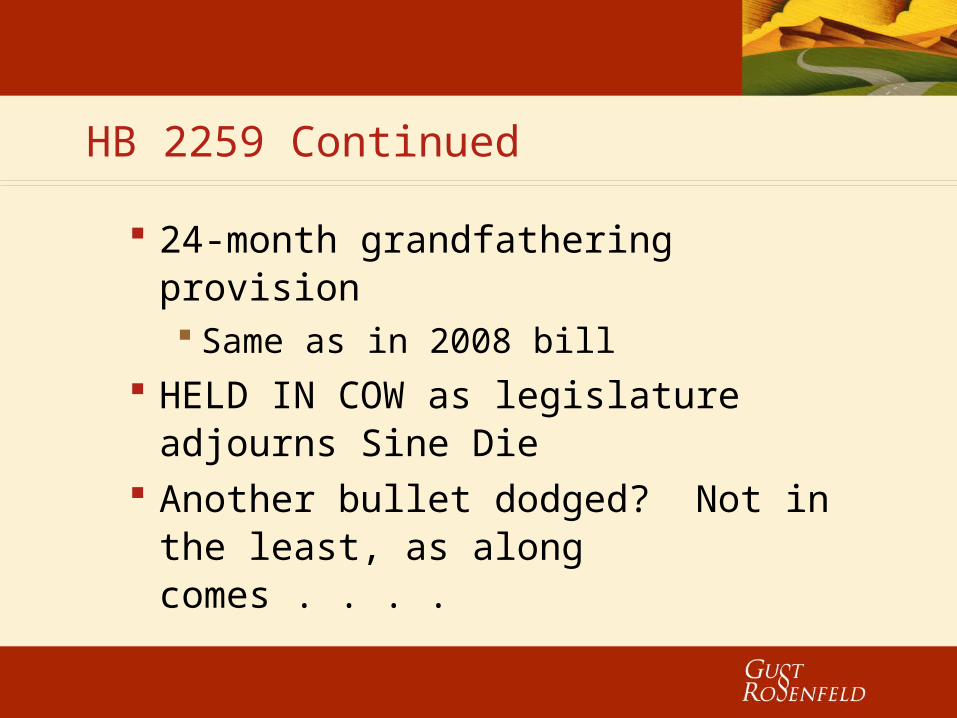

HB 2259 Continued

24-month grandfathering provision Same as in 2008 bill

HELD IN COW as legislature adjourns Sine Die

Another bullet dodged? Not in the least, as along comes . . . .

2009 Sessions Continued – The Nuclear Option

HB 2008 Don’t be fooled by the Constitution,

apparently a budget bill can alter DIFs Included all of the provisions of HB

2259 Benefit areas

Still allows single zone

Likely to spawn many IIP amendments

HB 2008 Continued

“Forecasting” other revenues Still only applicable to extent such

revenues are used for capital in IIP

Unfortunately, lose some benefit of HBACA v. Goodyear decision

Comparison of existing LOS v. new LOS Developers really do believe they are

forced to upgrade other neighborhoods

HB 2008 Continued

Forecast sources of revenue to fund IIP Developers convinced that some projects

in IIP (and for which DIFs are charged) will never be built (i.e. Town Lake)

Grandfathering Increases inapplicable for 24 months

after “final approval” – not extended by renewal

Written schedule upon request

HB 2008 Continued

Moratoria – 6/2009 – 6/2011 for: Building Codes; federal funding

exception Increases to new construction TPT Development fees

Not impose new fees

Not increase existing

Currently law; challenge pending

2010 Session – What was old is new again

Moratorium not enough for HBACA HB 2249 (Rep. Biggs)

Refunds required if facility is not built within 7 years after first DIF collected

Exempts water/sewer

Ignores developer delays

Contains no direction as to how “facility” is determined

HB 2249 Continued

Introduced as refund to payor; amended to current property owner

Dangerous first step toward tying fees to specific projects

Lacks any direction as to how property owner would determine if project built

Fails to account for changes to IIP allowed by statute (i.e. developer request)

Sailed through committee

2010 Session Continued

HB 2259 (Rep. Biggs) Seemingly redundant language

regarding proportionate share LOS limited to existing; if upgraded

along with new development, cost of upgrade apportioned to the city’s costs

Funds from existing residents must be paid prior to DIF funds used

HB 2259 Continued

Detail in IIP required for sources of funds to pay City share of infrastructure

Assigned to one committee; sailed through; ready for caucus

2010 Session Continued

HB 2397 (various sponsors) Essentially repeals all of the changes

over the past five years Repeals moratorium on DIF increases

and building codes Triple assigned in committee (the kiss

of death)

So where are we now?

Apply only indexed increases in fees until 2011 (unless moratorium extended)

DIF studies already underway/anticipated Complete studies to avoid waste of

taxpayer funds; delayed effective date New studies should be timed for end of

moratorium

QUESTIONS?

Andrew J. McGuireGust Rosenfeld PLC

201 East Washington Street, Suite 800Phoenix, Arizona 85004

(602) 257-7664 direct dial602) 340-1538 [email protected]

www.gustlaw.com