Embed Size (px)

Citation preview

Developing financial part of the Business plan

Lection 11

The main techniques of financial projection fall into three categories:

• Pro forma financial statements.• Pro forma statements are projected financial statements

embodying a set of assumptions about a company’s future performance and funding requirements.

• Cash budgets.• Cash budgets are detailed projections of the specific

incidence of cash moving in and out of the business.

• Operating budgets.• Operating budgets are detailed projections of company-wide

or departmental revenue and/or expense patterns, and they are subsidiary to both pro forma statements and cash flow statements.

Financial plan - Basics

• 5 year time horizon• First two help set cash flow expectations • Last three help define opportunity

• Income Statement

• Balance Sheet

• Cash Flow

• High-level summary of the growth

Financial plan - Basics (cont.)• Reasonable and defendable assumptions

– Highlight key assumptions– Have assumptions on separate tab that drive

the model– Assists in “what if” planning

• Some Key Assumptions– Price– Sales Growth– COGS

Line Items• Rent/employee/month• Equip costs/employee/month• Benefits• Bonuses/Commissions

• Commission plan• What is it versus existing players?

• Payroll Exp/month• Capital raising often results in salary increases• Change in compensation mix with later employees• Less stock heavy more cash intensive

Hints

• Headcount

• Plan slow/run like hell– Slower than expected

• Hiring• Product development• Sales/revenue

– Higher than expected• COSTS

Hints (cont.)• Investment capital is intended to fuel

accelerated growth– Expectations vs. reality– This can kill a business before it hits its stride

• Economies of Scale– Bureaucracies rule – EoS – so old economy

• Magic revenue number?• Market share in year five

Top Ten Mistakes

1. Presenting financials without ability to discuss detail if asked (the model demonstrates that the entrepreneur fully understands the full scope of the business)

2. Plan is overly optimistic. Revenue traction always takes longer. Must understand the sales qualification and challenges

3. Plan is overly pessimistic without clearly identifying upside 4. Revenue plan created solely to match the operational requirements5. Plan does not tie to pipeline, sales cycle, and ability to hire team6. Build plan to try and pump up valuation7. Failure to understand industry comparables and know the gross margins, expense

levels as a % of revenue, and operating margins 8. Failing to account for competition and its affect on prices9. Using the 1% of the market technique to justify opportunity (market size usually off

and most never get 1% of market)10. Entrepreneur does not understand cash implications and subtleties of the timing of

payments and receipts

Top Ten Things You Must Do - Company

1. Develop both a top-down and bottom-up plan2. Ramp-up of new staff must be realistic (including ramp-up and

availability)3. Quality, quantity, and stage of pipeline must be realistic4. Large deals and timeframe to close must be presented realistically5. Judgment needs to be applied to sales management6. In a small start-up, the CEO must know every major account7. Raise the right amount of money (What you need to deliver your

plan with a cushion)8. Working capital requirements must be carefully considered as they

impact CASH9. There are other ways to smooth out cashflow: AR lines, lease

Lines, debt, payables management, etc.10. Establish mentor/advisor relationships

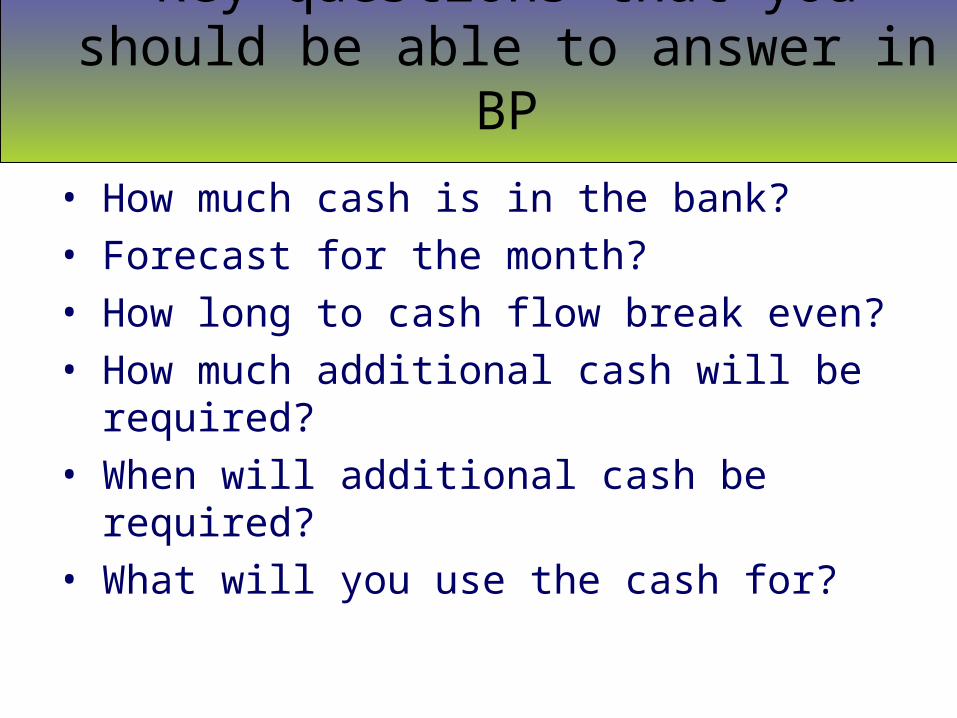

Key questions that you should be able to answer in BP

• How much cash is in the bank?

• Forecast for the month?

• How long to cash flow break even?

• How much additional cash will be required?

• When will additional cash be required?

• What will you use the cash for?

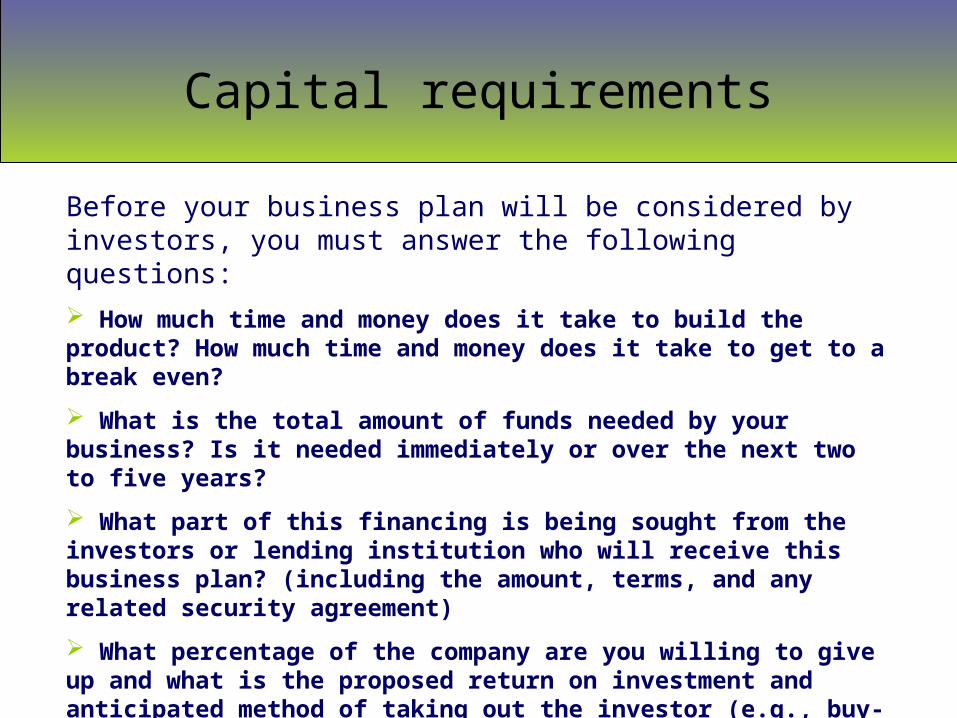

Capital requirements

Before your business plan will be considered by investors, you must answer the following questions: How much time and money does it take to build the product? How much time and money does it take to get to a break even?

What is the total amount of funds needed by your business? Is it needed immediately or over the next two to five years?

What part of this financing is being sought from the investors or lending institution who will receive this business plan? (including the amount, terms, and any related security agreement)

What percentage of the company are you willing to give up and what is the proposed return on investment and anticipated method of taking out the investor (e.g., buy-back, public offering, sale)?

Will the capital markets finance a project of this size and duration?

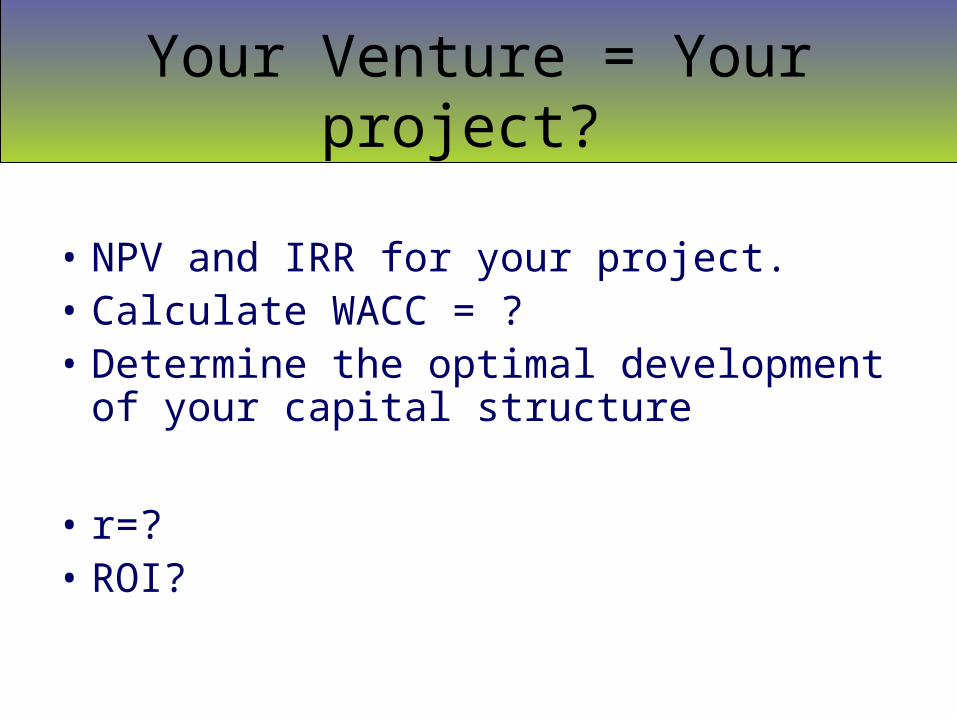

Your Venture = Your project?

• NPV and IRR for your project.• Calculate WACC = ?• Determine the optimal development of

your capital structure

• r=?• ROI?

Explanation of how business will MAKE MONEY

The Purpose of Financial Forecasts

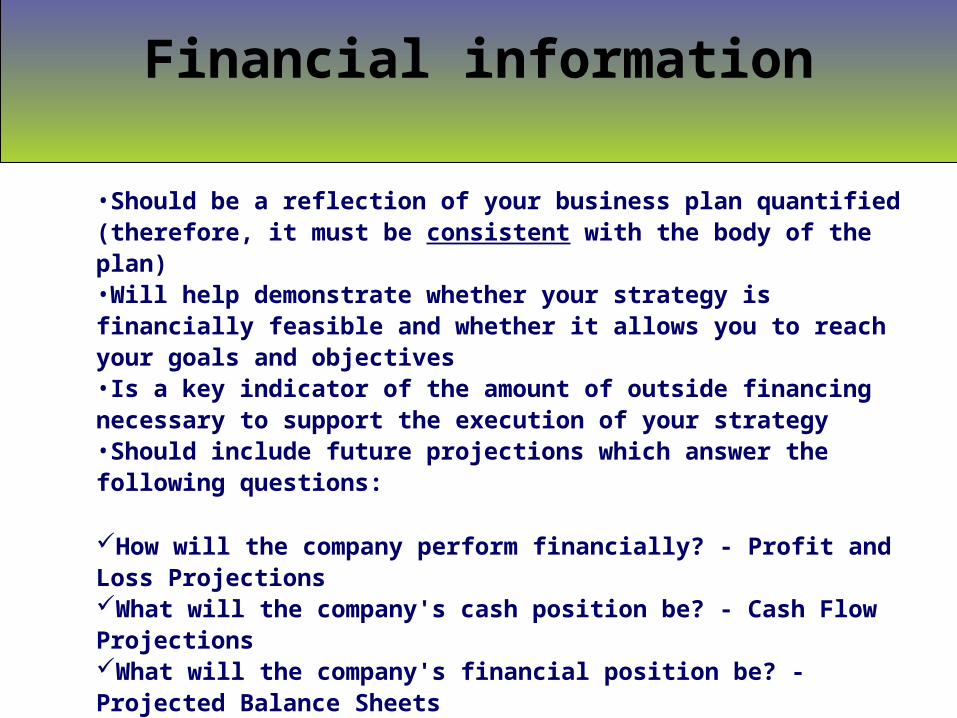

Financial information

•Should be a reflection of your business plan quantified (therefore, it must be consistent with the body of the plan) •Will help demonstrate whether your strategy is financially feasible and whether it allows you to reach your goals and objectives •Is a key indicator of the amount of outside financing necessary to support the execution of your strategy •Should include future projections which answer the following questions:

How will the company perform financially? - Profit and Loss Projections What will the company's cash position be? - Cash Flow Projections What will the company's financial position be? - Projected Balance Sheets

Financial information(cont.)

•Should include a list of significant assumptions used in any individual section or throughout the financial projections that are:

Material to the projected amounts Especially sensitive to variations Deviations from historical trends Especially uncertain

•Should include key financial ratios and should compare to competitors/industry averages. Key ratios include current, debt-to-net worth, return on equity, gross margin, and break-even point (in both sales units and dollars)

Creating Financial Forecasts

Step 1: Products/ServicesDevelopment timelineHow many products? Versions? Upgrades?Prices, discounts, price erosionSales/personCommissionsDistribution channelsCustomer support

Creating Financial Forecasts

Step 2: StaffingHow many departments?How many people to develop product?Timing of marketing and salespeople.Sufficient R&D staff for future products?Competitive salaries, benefits, commissions, recruiting.Administration Department

Creating Financial Forecasts

Step 3: Marketing and AdvertisingTradeshowsPublic relationsAdvertisingConsultantsLead time

Creating Financial Forecasts

Step 4: Other ExpensesCapital equipmentLicensing technologyPatent filingsTelecomRecruiting/RelocationTie as many expenses as possible to headcount

Creating Financial Forecasts

Step 5: Evaluate the ResultsPerform scenario analysisEvaluate your operating ratiosLook at comparable companiesDetermine your cash requirementsConsider a three month cash cushion

Creating Financial Forecasts

Step 6: Financing OptionsEquityLeasesLOC’sLoans

Building YOUR Model – Do’s and

don’ts – Sales

Do Don’t

Typically, the plan should state an average selling price per unit along with the projected number of units to be sold each reporting period. Sales prices should be competitive with similar offerings in the market and should take into consideration the cost to produce and distribute the product.

Assume that you achieve a certain percentage of market share just because it is a small percentage.

Building YOUR Model – Do’s and

don’ts – Cost of Sales

Do Don’t

Accurate unit cost data, taking into consideration the labor, material, and overhead costs to produce each unit. Be sure to have a good grasp on initial product costing so it is protected against price pressure from competitors

Assume a certain percentage for gross margin based on industry average. (while this can be a great sensitivity check…)

Building YOUR Model – Do’s and don’ts – Product Development

Do Don’t

Product development expenses should be closely tied to product introduction timetables elsewhere in the plan. Usually, the headcount should come out directly from the timeline for development.

Assume that you can have a world record in the timing of development and/or a minimal compensation to employees.

Building YOUR Model – Do’s and don’ts – S&M and G&A

Do Don’t

A detailed set of expense assumptions should take into consideration headcount, selling and administrative costs, space, and major promotions. It is useful to compare final expense projections with industry norms. All expense categories should be

considered.

Take industry/certain company ratios

Business plan presentation

Business plan

What Why HowHow much

Venture Capital Fund

Business AngelBANKS Gov, NGOs, FUNDS etc

Financial Plan - Funds Required and Their Uses

A. Current Funding Requirements

1. Amount2. Timing3. Type

a. Equityb. Debtc. Mezzanine

4. Terms

B. Funding Requirements over the Next Five Years

1. Amount2. Timing3. Type4. Terms

C. Use of Funds1. Capital expenditures2. Working capital3. Debt retirement4. Acquisitions

D. Long-Range Financial Strategies (liquidating investors’ positions)

1. Going public2. Leveraged buyout3. Acquisition by another

company4. Debt service levels and timing5. Liquidation of the venture

What Does Mezzanine Financing Mean?

• A hybrid of debt and equity financing that is typically used to finance the expansion of existing companies. Mezzanine financing is basically debt capital that gives the lender the rights to convert to an ownership or equity interest in the company if the loan is not paid back in time and in full. It is generally subordinated to debt provided by senior lenders such as banks and venture capital companies.

Since mezzanine financing is usually provided to the borrower very quickly with little due diligence on the part of the lender and little or no collateral on the part of the borrower, this type of financing is aggressively priced with the lender seeking a return in the 20-30% range.

Financial Data

A. Historical Financial Data (past three to five years)

1. Annual statementsa. Incomeb. Balance sheetc. Cash flows

B. Prospective Financial Data (next 5 year)

1. Next year (by month or quarter)a. Incomeb. Balance sheetc. Cash flowsd. Capital expenditure budget

2. Final four years (by quarter or year)a. Incomeb. Balance sheetc. Cash flowsd. Capital expenditure budget

3. Summary of significant assumptions4. Type of prospective financial dataa. Forecast (management’s best estimate)b. Projection (“what-if ” scenarios)

Financial Data

C. Analysis

1. Historical financial statements

a. Ratio analysis

b. Trend analysis with graphic presentation

2. Prospective financial statements

a. Ratio analysis

b. Trend analysis with graphic presentation

![Eslarner Gemeindebote 2014 (CO-LECTION[TM])](https://img.pdfslide.us/doc/110x75/568ca8ea1a28ab186d9b4b4c/eslarner-gemeindebote-2014-co-lectiontm.jpg)

![CO-LECTION[tm] - 01.2013 - Solarpark Eslarn](https://img.pdfslide.us/doc/110x75/577ce1411a28ab9e78b514e6/co-lectiontm-012013-solarpark-eslarn.jpg)